Adjusting the Accounts

|

|

|

- Cora Alannah Andrews

- 5 years ago

- Views:

Transcription

1 3-1

2 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain the reasons for adjusting entries. 4. Identify the major types of adjusting entries. 5. Prepare adjusting entries for deferrals. 6. Prepare adjusting entries for accruals. 7. Describe the nature and purpose of an adjusted trial balance. 3-2

3 Preview of Chapter Financial Accounting IFRS Edition, 2e Weygandt Kimmel Kieso

4 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption) Jan. Feb. Mar. Apr. Dec. Generally a month, a quarter, or a year. Also known as the Periodicity Assumption 3-4 LO 1 Explain the time period assumption.

5 Timing Issues Fiscal and Calendar Years Monthly and quarterly time periods are called interim periods. Most large companies must prepare both quarterly and annual financial statements. Fiscal Year = Accounting time period that is one year in length. Calendar Year = January 1 to December LO 1 Explain the time period assumption.

6 Timing Issues Accrual- vs. Cash-Basis Accounting Accrual-Basis Accounting Transactions recorded in the periods in which the events occur. Revenues are recognized when the services are performed, rather than when cash is received. Expenses are recognized when incurred, rather than when paid. 3-6 LO 2 Explain the accrual basis of accounting.

7 Timing Issues Accrual- vs. Cash-Basis Accounting Cash-Basis Accounting Revenues recognized when cash is received. Expenses recognized when cash is paid. Cash-basis accounting is not in accordance with International Financial Reporting Standards (IFRS). 3-7 LO 2 Explain the accrual basis of accounting.

8 Timing Issues Recognizing Revenues and Expenses Revenue Recognition Principle Recognize revenue in the accounting period in which the performance obligation is satisfied. In a service enterprise, revenue is considered to be earned at the time the service is performed. 3-8 LO 2 Explain the accrual basis of accounting.

9 Timing Issues Recognizing Revenues and Expenses Expense Recognition Principle Match expenses with revenues in the period when the company makes efforts to generate those revenues. Let the expenses follow the revenues. 3-9 LO 2 Explain the accrual basis of accounting.

10 Timing Issues Illustration 3-1 IFRS relationships in revenue and expense recognition 3-10 LO 2 Explain the accrual basis of accounting.

11 3-11 LO 2 Explain the accrual basis of accounting.

12 A list of concepts is provided in the left column below, with a description of the concept in the right column below. There are more descriptions provided than concepts. Match the description of the concept to the concept. f e c b 3-12 LO 2

13 The Basics of Adjusting Entries Adjusting Entries Ensure that the revenue recognition and expense recognition principles are followed. Necessary because the trial balance may not contain up-to-date and complete data. Required every time a company prepares financial statements. Will include one income statement account and one statement of financial position account LO 3 Explain the reasons for adjusting entries.

14 The Basics of Adjusting Entries Types of Adjusting Entries Illustration 3-2 Categories of adjusting entries Deferrals 1. Prepaid Expenses. Expenses paid in cash before they are used or consumed. 2. Unearned Revenues. Cash received before services are performed. Accruals 3. Accrued Revenues. Revenues for services performed but not yet received in cash or recorded. 4. Accrued Expenses. Expenses incurred but not yet paid in cash or recorded LO 4 Identify the major types of adjusting entries.

15 The Basics of Adjusting Entries Types of Adjusting Entries Trial Balance Each account is analyzed to determine whether it is complete and up-to-date. Illustration LO 4 Identify the major types of adjusting entries.

16 The Basics of Adjusting Entries Adjusting Entries for Deferrals Deferrals are either: Prepaid expenses OR Unearned revenues LO 5 Prepare adjusting entries for deferrals.

17 The Basics of Adjusting Entries Prepaid Expenses Payment of cash, that is recorded as an asset because service or benefit will be received in the future. Cash Payment BEFORE Expense Recorded Prepayments often occur in regard to: insurance rent supplies equipment advertising buildings 3-17 LO 5 Prepare adjusting entries for deferrals.

to an expense account and Decrease (credit) to an asset account.")

18 The Basics of Adjusting Entries Prepaid Expenses Expire either with the passage of time or through use. Adjusting entry: Increase (debit) to an expense account and Decrease (credit) to an asset account. Illustration LO 5 Prepare adjusting entries for deferrals.

19 The Basics of Adjusting Entries Illustration: Pioneer Advertising Agency purchased supplies costing $2,500 on October 5. Pioneer recorded the payment by increasing (debiting) the asset Supplies. This account shows a balance of $2,500 in the October 31 trial balance. An inventory count at the close of business on October 31 reveals that $1,000 of supplies are still on hand. Oct. 31 Supplies expense 1,500 Supplies 1, LO 5 Prepare adjusting entries for deferrals.

20 The Basics of Adjusting Entries Illustration LO 5

Prepaid Insurance. This account shows a balance of $600 in the Octo")

21 The Basics of Adjusting Entries Illustration: On October 4, Pioneer Advertising paid $600 for a one-year fire insurance policy. Coverage began on October 1. Pioneer recorded the payment by increasing (debiting) Prepaid Insurance. This account shows a balance of $600 in the October 31 trial balance. Insurance of $50 ($600 12) expires each month. Oct. 31 Insurance expense 50 Prepaid insurance LO 5 Prepare adjusting entries for deferrals.

22 The Basics of Adjusting Entries Illustration LO 5

23 The Basics of Adjusting Entries Depreciation Buildings, equipment, and vehicles (assets with long lives) are recorded as assets, rather than an expense, in the year acquired. Depreciation allocates a portion of the asset s cost as an expense during each period of the asset s useful life. Depreciation does not attempt to report the actual change in the value of the asset LO 5 Prepare adjusting entries for deferrals.

24 The Basics of Adjusting Entries Illustration: For Pioneer Advertising, assume that depreciation on the equipment is $480 a year, or $40 per month. Oct. 31 Depreciation expense 40 Accumulated depreciation 40 Accumulated Depreciation is called a contra asset account LO 5 Prepare adjusting entries for deferrals.

25 The Basics of Adjusting Entries Illustration LO 5

on the statement of financial position.")

26 The Basics of Adjusting Entries Statement Presentation Accumulated Depreciation is a contra asset account (credit). Appears just after the account it offsets (Equipment) on the statement of financial position. Book value is the difference between the cost of any depreciable asset and its accumulated depreciation. Illustration LO 5 Prepare adjusting entries for deferrals.

27 The Basics of Adjusting Entries Illustration LO 5 Prepare adjusting entries for deferrals.

28 The Basics of Adjusting Entries Unearned Revenues Receipt of cash that is recorded as a liability because service has not be performed. Cash Receipt BEFORE Revenue Recorded Unearned revenues often occur in regard to: Rent Magazine subscriptions Airline tickets Customer deposits 3-28 LO 5 Prepare adjusting entries for deferrals.

to a liability account and an increase (credit) to a revenue account.")

29 The Basics of Adjusting Entries Unearned Revenues Adjusting entry is made to record the revenue for services performed and to show the liability that remains. Results in a decrease (debit) to a liability account and an increase (credit) to a revenue account. Illustration LO 5 Prepare adjusting entries for deferrals.

30 The Basics of Adjusting Entries Illustration: Pioneer Advertising received $1,200 on October 2 from R. Knox for advertising services expected to be completed by December 31. Unearned Service Revenue shows a balance of $1,200 in the October 31 trial balance. Analysis reveals that the company earned $ 400 of those fees in October. Oct. 31 Unearned service revenue 400 Service revenue LO 5 Prepare adjusting entries for deferrals.

31 The Basics of Adjusting Entries Illustration LO 5

32 The Basics of Adjusting Entries Illustration LO 5 Prepare adjusting entries for deferrals.

33 3-33 LO 5

34 The Basics of Adjusting Entries Adjusting Entries for Accruals Accruals are made to record Revenues for services performed OR Expenses incurred in the current accounting period that have not been recognized through daily entries LO 6 Prepare adjusting entries for accruals.

35 The Basics of Adjusting Entries Accrued Revenues Revenues for services performed but not yet received in cash or recorded. Revenue Recorded BEFORE Cash Receipt Accrued revenues often occur in regard to: Interest Rent Services performed 3-35 LO 6 Prepare adjusting entries for accruals.

36 The Basics of Adjusting Entries Accrued Revenues Adjusting entry shows the receivable that exists and records the revenues for services performed. Adjusting entry: Increases (debits) an asset account and Increases (credits) a revenue account. Illustration LO 6

37 The Basics of Adjusting Entries Illustration: In October Pioneer Advertising Agency recognized $200 for advertising services performed but not recorded. Oct. 31 Accounts receivable 200 Service revenue 200 On November 10, Pioneer receives cash of $ 200 for the services performed. Nov. 10 Cash 200 Accounts receivable LO 6 Prepare adjusting entries for accruals.

38 The Basics of Adjusting Entries Illustration LO 6

39 The Basics of Adjusting Entries Illustration LO 6 Prepare adjusting entries for accruals.

40 The Basics of Adjusting Entries Accrued Expenses Expenses incurred but not yet paid in cash or recorded. Expense Recorded BEFORE Cash Payment Accrued expenses often occur in regard to: Rent Taxes Interest Salaries 3-40 LO 6 Prepare adjusting entries for accruals.

an expense account and Increase (credit) a liability account.")

41 The Basics of Adjusting Entries Accrued Expenses Adjusting entry records the obligation and recognizes the expense. Adjusting entry: Increase (debit) an expense account and Increase (credit) a liability account. Illustration LO 6

42 The Basics of Adjusting Entries Illustration: Pioneer Advertising signed a three-month note payable in the amount of $5,000 on October 1. The note requires Pioneer to pay interest at an annual rate of 12%. Illustration 3-17 Oct. 31 Interest expense 50 Interest payable LO 6 Prepare adjusting entries for accruals.

43 The Basics of Adjusting Entries Illustration LO 6

.")

44 The Basics of Adjusting Entries Illustration: Pioneer Advertising last paid salaries on October 26; the next payment of salaries will not occur until November 9. The employees receive total salaries of $2,000 for a five-day work week, or $400 per day. Thus, accrued salaries at October 31 are $1,200 ($ 400 x 3 days). Illustration LO 6 Prepare adjusting entries for accruals.

45 The Basics of Adjusting Entries Illustration LO 6

46 The Basics of Adjusting Entries Illustration LO 6 Prepare adjusting entries for accruals.

47 3-47 LO 6 Prepare adjusting entries for accruals.

48 Micro Computer Services Inc. began operations on August 1, At the end of August 2014, management attempted to prepare monthly financial statements. The following information relates to August. Prepare the adjusting journal entries needed at August 31, (Amounts are in Chinese yuan.) 1. At August 31, the company owed its employees 8,000 in salaries and wages that will be paid on September 1. Salaries and wages expense 8,000 Salaries and wages payable 8, LO 6

49 Micro Computer Services Inc. began operations on August 1, At the end of August 2014, management attempted to prepare monthly financial statements. The following information relates to August. Prepare the adjusting journal entries needed at August 31, (Amounts are in Chinese yuan.) 2. At August 1, the company borrowed 300,000 from a local bank on a 15-year mortgage. The annual interest rate is 10%. Interest expense ( 300,000 x 10% x 1/12) 2,500 Interest payable 2, LO 6

50 Micro Computer Services Inc. began operations on August 1, At the end of August 2014, management attempted to prepare monthly financial statements. The following information relates to August. Prepare the adjusting journal entries needed at August 31, (Amounts are in Chinese yuan.) 3. Revenue for services performed but unrecorded for August totaled 11,000. Accounts receivable 11,000 Service revenue 11, LO 6

51 The Basics of Adjusting Entries Summary of Basic Relationships Illustration LO 6 Prepare adjusting entries for accruals.

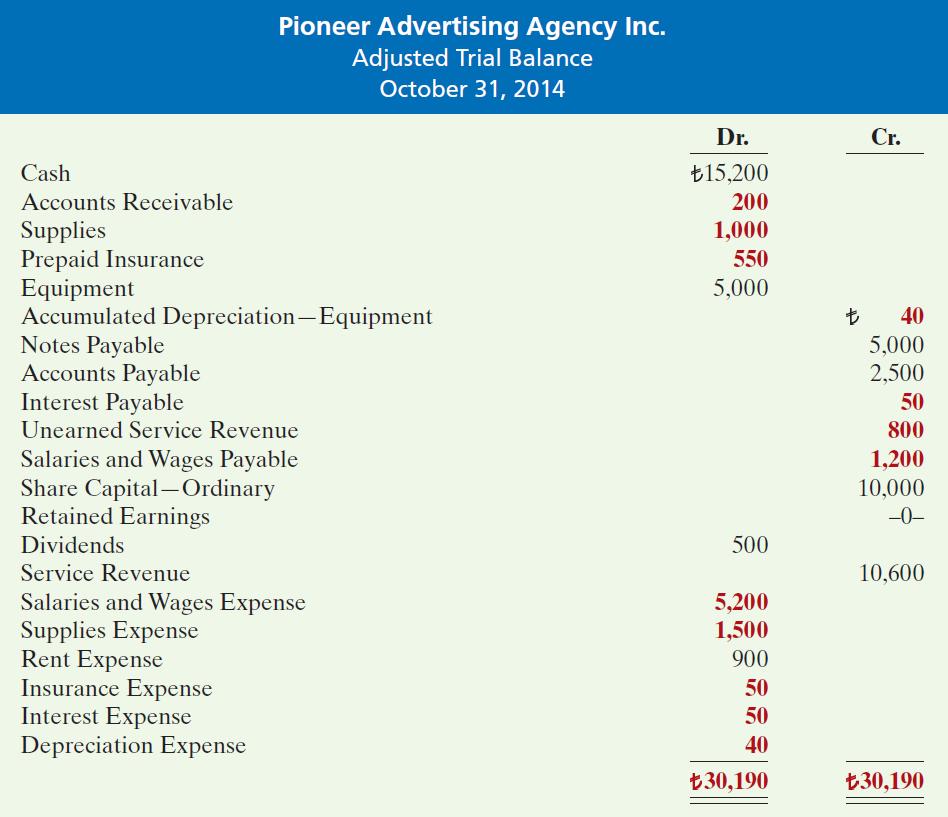

52 The Adjusted Trial Balance Adjusted Trial Balance Prepared after all adjusting entries are journalized and posted. Purpose is to prove the equality of debit balances and credit balances in the ledger. Is the primary basis for the preparation of financial statements LO 7 Describe the nature and purpose of an adjusted trial balance.

53 3-53 Illustration 3-25

54 Preparing Financial Statements Financial Statements are prepared directly from the Adjusted Trial Balance. Income Statement Retained Earnings Statement Statement of Financial Position 3-54 LO 7 Describe the nature and purpose of an adjusted trial balance.

55 Illustration LO 7

56 Illustration LO 7

57 APPENDIX 3A Alternative Treatment of Prepaid Expenses and Unearned Revenues When a company prepays an expense, it debits that amount to an expense account. When a company receives payment for future services, it credits the amount to a revenue account LO 8 Prepare adjusting entries for the alternative treatment of deferrals.

58 APPENDIX 3A Prepaid Expenses Company may choose to debit (increase) an expense account rather than an asset account. This alternative treatment is simply more convenient. Illustration 3A LO 8 Prepare adjusting entries for the alternative treatment of deferrals.

59 APPENDIX 3A Unearned Revenues Company may credit (increase) a revenue account when they receive cash for future services. Illustration 3A LO 8 Prepare adjusting entries for the alternative treatment of deferrals.

60 APPENDIX 3A Summary of Additional Adjustment Relationships Illustration 3A LO 8 Prepare adjusting entries for the alternative treatment of deferrals.

61 APPENDIX 3B CONCEPTS IN ACTION Qualities of Useful Information Illustration 3B LO 9 Discuss financial reporting concepts.

62 APPENDIX 3B CONCEPTS IN ACTION Enhancing Qualities Comparability Consistency Verifiability Timeliness Understandability 3-62 LO 9 Discuss financial reporting concepts.

63 APPENDIX 3B CONCEPTS IN ACTION Assumptions in Financial Reporting Illustration 3B LO 9

64 APPENDIX 3B CONCEPTS IN ACTION Assumptions in Financial Reporting Illustration 3B LO 9

65 APPENDIX 3B CONCEPTS IN ACTION Principles of Financial Reporting Measurement Principles Historical Cost Principle Fair Value Principle Revenue Recognition Principle Expense Recognition Principle Full Disclosure Principle 3-65 LO 9 Discuss financial reporting concepts.

66 APPENDIX 3B CONCEPTS IN ACTION Principles of Financial Reporting Constraints in Financial Reporting Accounting standard-setters weigh the cost that companies will incur to provide the information against the benefit that financial statement users will gain from having the information available LO 9

67 Another Perspective Key Points 3-67 Like IFRS, companies applying GAAP use accrual-basis accounting to ensure that they record transactions that change a company s financial statements in the period in which events occur. Similar to IFRS, cash-basis accounting is not in accordance with GAAP. GAAP also divides the economic life of companies into artificial time periods. Under both GAAP and IFRS, this is referred to as the time period assumption. GAAP has more than 100 rules dealing with revenue recognition. Many of these rules are industry specific. Revenue recognition under IFRS is determined primarily by a single standard, IAS 18. Despite this large disparity in the detailed guidance devoted to revenue recognition, the general revenue recognition principles required by IFRS that are used in this textbook are similar to those under GAAP.

68 Another Perspective Key Points Internal controls are a system of checks and balances designed to detect and prevent fraud and errors. The Sarbanes-Oxley Act requires U.S. companies to enhance their systems of internal control. However, many foreign companies do not have this requirement. Under IFRS, revaluation to fair value of items such as land and buildings is permitted. This is not permitted under GAAP. The form and content of financial statements are very similar under GAAP and IFRS. Any significant differences will be discussed in those chapters that address specific financial statements. Revenue recognition fraud is a major issue in U.S. financial reporting. The same situation exists for most other countries as well. 3-68

69 Another Perspective Key Points As indicated above, both the IASB and FASB are working together on a common conceptual framework. Some of the major issues that are being addressed are: 3-69 What are the qualitative characteristics that make accounting information useful? What is the primary objective of financial reporting? What basis should be used to measure and report, that is, should a historical cost or fair value approach be used? What criteria should be used to determine when revenue should be recognized and when expenses have been incurred? What guidelines should be established for disclosing financial information?

70 Another Perspective Key Points Income includes both revenues, which arise during the normal course of operating activities, and gains, which arise from activities outside of the normal sales of goods and services. The term income is not used this way under GAAP. Instead, under GAAP income refers to the net difference between revenues and expenses. Expenses under IFRS include both those costs incurred in the normal course of operations, as well as losses that are not part of normal operations. This is in contrast to GAAP, which defines each separately. 3-70

71 Another Perspective Looking to the Future As this textbook is being written, the IASB and FASB are close to completing a joint project on revenue recognition. The purpose of this project is to develop comprehensive guidance on when to recognize revenue. This approach focuses on changes in assets and liabilities as the basis for revenue recognition. It is hoped that this approach will lead to more consistent accounting in this area. For more on this topic, see

72 Copyright Copyright 2013 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein. 3-72

Adjusting The Accounts

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

CHAPTER3 Adjusting the Accounts

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Chapter 3 Adjusting the Accounts 高立翰

Chapter 3 Adjusting the Accounts 高立翰 Study Objectives 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. ( 不考 ) 3. Explain the reasons for adjusting entries. 4. Identify

Chapter 3 Adjusting the Accounts 高立翰 Study Objectives 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. ( 不考 ) 3. Explain the reasons for adjusting entries. 4. Identify

The Recording Process

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

CHAPTER 3 Adjusting the Accounts

Solutions Manual Financial and Managerial Accounting, 2nd Edition Weygandt Kimmel Kieso Completed Instant download SOLUTIONS MANUAL for Financial and Managerial Accounting, 2nd Edition by Jerry J. Weygandt,

Solutions Manual Financial and Managerial Accounting, 2nd Edition Weygandt Kimmel Kieso Completed Instant download SOLUTIONS MANUAL for Financial and Managerial Accounting, 2nd Edition by Jerry J. Weygandt,

The Recording Process

2-1 Chapter 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and

2-1 Chapter 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and

CHAPTER 3. Adjusting the Accounts 6, 7 1 8, 9, 10, 11, 12, 13, 18, 19, , 18 6A 12, 13 14, 15

CHAPTER 3 Adjusting the Accounts ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Explain the time period assumption. *2. Explain

CHAPTER 3 Adjusting the Accounts ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Explain the time period assumption. *2. Explain

Investments. 1. Discuss why corporations invest in debt and share securities.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

Liabilities. Chapter 10. Learning Objectives. After studying this chapter, you should be able to:

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

PREVIEW OF CHAPTER 5-2

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

CHAPTER3. Adjusting the Accounts. Apago PDF Enhancer. Study Objectives. Feature Story WHAT WAS YOUR PROFIT?

CHAPTER3 Study Objectives After studying this chapter, you should be able to: [1] Explain the time period assumption. [2] Explain the accrual basis of accounting. [3] Explain the reasons for adjusting

CHAPTER3 Study Objectives After studying this chapter, you should be able to: [1] Explain the time period assumption. [2] Explain the accrual basis of accounting. [3] Explain the reasons for adjusting

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

THE ACCOUNTING INFORMATION SYSTEM

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 5-1 5-2 PREVIEW OF CHAPTER 5 5-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 5-1 5-2 PREVIEW OF CHAPTER 5 5-3

Financial Statement Analysis

14-1 Chapter 14 Financial Statement Analysis 14-2 Learning Objectives After studying this chapter, you should be able to: 1. Discuss the need for comparative analysis. 2. Identify the tools of financial

14-1 Chapter 14 Financial Statement Analysis 14-2 Learning Objectives After studying this chapter, you should be able to: 1. Discuss the need for comparative analysis. 2. Identify the tools of financial

Accounting in Action. Chapter 1. Learning Objectives. After studying this chapter, you should be able to:

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

Chapter 17 Accounting for Accruals and Deferrals

Chapter 17 Accounting for Accruals and Deferrals o Understand Accrual and Deferrals o Accrued Expense o Accrued Revenue o Deferred Expense o Deferred Revenue 1 Accruals and Deferrals Accruals Expenses

Chapter 17 Accounting for Accruals and Deferrals o Understand Accrual and Deferrals o Accrued Expense o Accrued Revenue o Deferred Expense o Deferred Revenue 1 Accruals and Deferrals Accruals Expenses

PREVIEW OF CHAPTER 20-2

20-1 PREVIEW OF CHAPTER 20 20-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 20 Accounting for Pensions and Postretirement Benefits LEARNING OBJECTIVES After studying this chapter,

20-1 PREVIEW OF CHAPTER 20 20-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 20 Accounting for Pensions and Postretirement Benefits LEARNING OBJECTIVES After studying this chapter,

Accounting for Receivables

8-1 Chapter 8 Accounting for Receivables 8-2 Learning Objectives After studying this chapter, you should be able to: 1. Identify the different types of receivables. 2. Explain how companies recognize accounts

8-1 Chapter 8 Accounting for Receivables 8-2 Learning Objectives After studying this chapter, you should be able to: 1. Identify the different types of receivables. 2. Explain how companies recognize accounts

Section A: Multiple-Choice Questions (2 marks each; Total 30 marks)

") Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Chapter 4 Question Review 1

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

PREVIEW OF CHAPTER 2-2

2-1 PREVIEW OF CHAPTER 2 2-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 2 for Financial Reporting Conceptual Framework LEARNING OBJECTIVES After studying this chapter, you should

2-1 PREVIEW OF CHAPTER 2 2-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 2 for Financial Reporting Conceptual Framework LEARNING OBJECTIVES After studying this chapter, you should

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 22-1 22-2 PREVIEW OF CHAPTER 22 22-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 22-1 22-2 PREVIEW OF CHAPTER 22 22-3

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

1-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS. Balance Sheet and Statement of of Cash Flows. Usefulness of the Balance Sheet

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 5-1 5-2 Balance Sheet and Statement of of Cash Flows Balance Sheet Balance Sheet

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 5-1 5-2 Balance Sheet and Statement of of Cash Flows Balance Sheet Balance Sheet

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

The Accounting Cycle. End of the Period C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

Chapter 11. Corporations: Organization, Share Transactions, Dividends, and Retained Earnings. Learning Objectives

11-1 Chapter 11 Corporations: Organization, Share Transactions, Dividends, and Retained Earnings Learning Objectives After studying this chapter, you should be able to: 1. Identify the major characteristics

11-1 Chapter 11 Corporations: Organization, Share Transactions, Dividends, and Retained Earnings Learning Objectives After studying this chapter, you should be able to: 1. Identify the major characteristics

Chapter 3: The Measurement Fundamentals of Financial Accounting

1 Chapter 3: The Measurement Fundamentals of Financial Accounting 2 Basic Assumptions Basic assumptions are foundations of financial accounting measurements The basic assumptions are Economic entity Fiscal

1 Chapter 3: The Measurement Fundamentals of Financial Accounting 2 Basic Assumptions Basic assumptions are foundations of financial accounting measurements The basic assumptions are Economic entity Fiscal

Accounting for Receivables

9 Accounting for Receivables Learning Objectives 1 2 3 4 Explain how companies recognize accounts receivable. Describe how companies value accounts receivable and record their disposition. Explain how

9 Accounting for Receivables Learning Objectives 1 2 3 4 Explain how companies recognize accounts receivable. Describe how companies value accounts receivable and record their disposition. Explain how

PREVIEW OF CHAPTER Slide 4-2

4-1 PREVIEW OF CHAPTER 4 4-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 4 Related Information Income Statement and LEARNING OBJECTIVES After studying this chapter, you should

4-1 PREVIEW OF CHAPTER 4 4-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 4 Related Information Income Statement and LEARNING OBJECTIVES After studying this chapter, you should

Chapter 6 Accounting Adjustments and Working papers

Chapter 6 Accounting Adjustments and Working papers Topics 1. Cash basis vs. Accrual Basis 2. Accrued Income 3. Accrued Expenses 4. Prepaid Expenses 5. Unearned Income 6. Depreciation 7. Supply Expenses

Chapter 6 Accounting Adjustments and Working papers Topics 1. Cash basis vs. Accrual Basis 2. Accrued Income 3. Accrued Expenses 4. Prepaid Expenses 5. Unearned Income 6. Depreciation 7. Supply Expenses

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 20-1 20-2 PREVIEW OF CHAPTER 20 20-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 20-1 20-2 PREVIEW OF CHAPTER 20 20-3

Accounting 1A Class Notes Chapter 3 The Adjusting Process

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

PREVIEW OF CHAPTER 14-2

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

Adjusting the Accounts

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

THE ACCOUNTING INFORMATION SYSTEM

2 THE ACCOUNTING INFORMATION SYSTEM DISCUSSION QUESTIONS 1. The conceptual framework of accounting is the collection of general concepts that logically flow from the objective of financial reporting to

2 THE ACCOUNTING INFORMATION SYSTEM DISCUSSION QUESTIONS 1. The conceptual framework of accounting is the collection of general concepts that logically flow from the objective of financial reporting to

PREVIEW OF CHAPTER 24

24-1 PREVIEW OF CHAPTER 24 24-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield Presentation and 24 Disclosure in Financial Reporting LEARNING OBJECTIVES After studying this chapter,

24-1 PREVIEW OF CHAPTER 24 24-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield Presentation and 24 Disclosure in Financial Reporting LEARNING OBJECTIVES After studying this chapter,

Chapter. Chapter. Accounting and the Time Value of Money. Time Value of Money. Basic Time Value Concepts. Basic Time Value Concepts

Accounting and the Time Value Money 6 6-1 Prepared by Coby Harmon, University California, Santa Barbara Basic Time Value Concepts Time Value Money In accounting (and finance), the term indicates that a

Accounting and the Time Value Money 6 6-1 Prepared by Coby Harmon, University California, Santa Barbara Basic Time Value Concepts Time Value Money In accounting (and finance), the term indicates that a

CHAPTER 3 Selected Solutions. The Accounting Information System. Brief Topics Questions Exercises Exercises Problems

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

Chapter 3 The Adjusting Process

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2

7-1 C H A P T E R 7 CASH AND RECEIVABLES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2 Learning Objectives 1. Identify items considered cash. 2. Indicate how to report cash and

7-1 C H A P T E R 7 CASH AND RECEIVABLES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2 Learning Objectives 1. Identify items considered cash. 2. Indicate how to report cash and

PREVIEW OF CHAPTER 17-2

17-1 PREVIEW OF CHAPTER 17 17-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 17 Investments LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Describe

17-1 PREVIEW OF CHAPTER 17 17-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 17 Investments LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Describe

Statement of Cash Flows

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

TH E ACCO U NTI NG LEARNING OBJECTIVES. Needed: A Reliable Information System. After studying this chapter, you should be able to:

2760T_c03_066-129.qxd 11/4/08 9:31 PM Page 66 C H A P T E R 3 TH E ACCO U NTI NG I N F O R M ATI O N SYSTE M LEARNING OBJECTIVES After studying this chapter, you should be able to: 1 Understand basic accounting

2760T_c03_066-129.qxd 11/4/08 9:31 PM Page 66 C H A P T E R 3 TH E ACCO U NTI NG I N F O R M ATI O N SYSTE M LEARNING OBJECTIVES After studying this chapter, you should be able to: 1 Understand basic accounting

C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE

16-1 C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 16-2 Dilutive Securities and Earnings Per Share Dilutive Securities and

16-1 C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 16-2 Dilutive Securities and Earnings Per Share Dilutive Securities and

Chapter 14. Statement of Cash Flows

1 Chapter 14 Statement of Cash Flows 2 Figure 14-1 3 Definition of Cash Cash consists of coin, currency, and available funds on deposit at the bank. Negotiable instruments such as money orders, certified

1 Chapter 14 Statement of Cash Flows 2 Figure 14-1 3 Definition of Cash Cash consists of coin, currency, and available funds on deposit at the bank. Negotiable instruments such as money orders, certified

Do you subscribe to any magazines? Most of us subscribe

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Review of a Company s Accounting System

CHAPTER 3 O BJECTIVES After reading this chapter, you will be able to: 1 Understand the components of an accounting system. 2 Know the major steps in the accounting cycle. 3 Prepare journal entries in

CHAPTER 3 O BJECTIVES After reading this chapter, you will be able to: 1 Understand the components of an accounting system. 2 Know the major steps in the accounting cycle. 3 Prepare journal entries in

Learning Objectives. LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet.

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

GAAP AND REVISION. DEFINITION OF ELEMENTS OF FINANCIAL STATEMENTS Revision concepts

GAAP AND REVISION INTRODUCE THE GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP) Accounting standards The Conceptual Framework Accounting concepts & principles CONCEPTUAL FRAMEWORK Describes objective of

GAAP AND REVISION INTRODUCE THE GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP) Accounting standards The Conceptual Framework Accounting concepts & principles CONCEPTUAL FRAMEWORK Describes objective of

Introduction to Fund Accounting

Classification of of Nonbusiness Organizations Introduction to Accounting for nonbusiness organizations. Five Major Classifications 1. Governmental units. 2. Hospitals and other health care providers.

Classification of of Nonbusiness Organizations Introduction to Accounting for nonbusiness organizations. Five Major Classifications 1. Governmental units. 2. Hospitals and other health care providers.

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

A. II. B. I. III. A. B.

II. A. B. I. III. A. B. Adjusting the Accounts Chapters 3 and 4 "Cash" Basis vs. "Accrual" Basis: Cash Accrual Revenue Expenses Generally Accepted Accounting Principles (GAAP) require using the basis.

II. A. B. I. III. A. B. Adjusting the Accounts Chapters 3 and 4 "Cash" Basis vs. "Accrual" Basis: Cash Accrual Revenue Expenses Generally Accepted Accounting Principles (GAAP) require using the basis.

T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts:

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

Solution to Problem 31 Adjusting entries. Solution to Problem 32 Closing entries.

Solution to Problem 31 Adjusting entries. 1. Utilities expense 27,000 Accounts payable 27,000 2. Rent revenue 4,000 Unearned revenue 4,000 3. Supplies 2,000 Supplies expense 2,000 4. Interest receivable

Solution to Problem 31 Adjusting entries. 1. Utilities expense 27,000 Accounts payable 27,000 2. Rent revenue 4,000 Unearned revenue 4,000 3. Supplies 2,000 Supplies expense 2,000 4. Interest receivable

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1 The accounting cycle is accounting process that extends from the very start of an accounting period to the absolute

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1 The accounting cycle is accounting process that extends from the very start of an accounting period to the absolute

Important Terminology

Important Terminology Recognition When we "recognize" a revenue or expense, it means that we record the amount in our general ledger and the amount is included in our income statement. Deferral When we

Important Terminology Recognition When we "recognize" a revenue or expense, it means that we record the amount in our general ledger and the amount is included in our income statement. Deferral When we

Chapter 3 the Adjusting Process. Learning Objective 1 Describe the nature of the adjusting process.

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

Text. Stay focused and keep doing what you believe in Melody Kulp (second from left; David Reinstein is on the far left)

") Stay focused and keep doing what you believe in Melody Kulp (second from left; David Reinstein is on the far left) 3 Adjusting Accounts and A Look Back Chapter 2 explained the analysis and recording of

Stay focused and keep doing what you believe in Melody Kulp (second from left; David Reinstein is on the far left) 3 Adjusting Accounts and A Look Back Chapter 2 explained the analysis and recording of

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

Professor Authored Problems Intermediate Accounting I Acct 341/541. Accounting Cycle

Professor Authored Problems Intermediate Accounting I Acct 341/541 Accounting Cycle Problem 17 Accounting cycle definitions. Please provide (1) complete, clear, accurate definitions, and (2) a good example.

Professor Authored Problems Intermediate Accounting I Acct 341/541 Accounting Cycle Problem 17 Accounting cycle definitions. Please provide (1) complete, clear, accurate definitions, and (2) a good example.

Adjustments, Financial Statements and the Quality of Earnings

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Fundamentals of Accounting Resources

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? Probable future sacrifice of economic benefits arising from present

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? Probable future sacrifice of economic benefits arising from present

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

Chapter 16: Dilutive Securities and Earnings per Share

Intermediate Accounting, 11th ed. Kieso, Weygandt, and Warfield Chapter 16: Dilutive Securities and Earnings per Share Prepared by Jep Robertson and Renae Clark New Mexico State University Chapter 16:

Intermediate Accounting, 11th ed. Kieso, Weygandt, and Warfield Chapter 16: Dilutive Securities and Earnings per Share Prepared by Jep Robertson and Renae Clark New Mexico State University Chapter 16:

After completing Chapter 2, your students should be able to answer these questions:

Solution Manual for Financial Accounting A Business Process Approach 3rd Edition by Reimers Link full download solution manual: http://testbankcollection.com/download/solution-manual-for-financial-accountinga-business-process-approach-3rd-edition-by-reimers/

Solution Manual for Financial Accounting A Business Process Approach 3rd Edition by Reimers Link full download solution manual: http://testbankcollection.com/download/solution-manual-for-financial-accountinga-business-process-approach-3rd-edition-by-reimers/

Accounting consists of three basic activities it

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

PREVIEW OF CHAPTER 1-2

1-1 PREVIEW OF CHAPTER 1 1-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 1 Accounting Standards Financial Reporting and LEARNING OBJECTIVES After studying this chapter, you should

1-1 PREVIEW OF CHAPTER 1 1-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 1 Accounting Standards Financial Reporting and LEARNING OBJECTIVES After studying this chapter, you should

Accounting I Class Schedule

Accounting I Class Schedule Accounting I Instructor: Dr. Ben Mahdavian Time: Tuesday 1:00 3:30 PM Thurs. 1:00 3:30 PM Room: BJ 106 02/09/2016 through 06/02/2016 Office Hours: Thursday 12:30-1:00 P.M in

Accounting I Class Schedule Accounting I Instructor: Dr. Ben Mahdavian Time: Tuesday 1:00 3:30 PM Thurs. 1:00 3:30 PM Room: BJ 106 02/09/2016 through 06/02/2016 Office Hours: Thursday 12:30-1:00 P.M in

Commecs College Macro Plan ( )

") Commecs College Macro Plan (-) Subject: Accounting Class: XI Sections: AZIZ TABBA, BUKHARI Unit No. Start Date 1 Aug 01, End Date Aug 03, Number Of Periods Topic/Chapter Contents Objectives By the end

Commecs College Macro Plan (-) Subject: Accounting Class: XI Sections: AZIZ TABBA, BUKHARI Unit No. Start Date 1 Aug 01, End Date Aug 03, Number Of Periods Topic/Chapter Contents Objectives By the end

CHAPTER1. Accounting in Action. PreviewofCHAPTER1. What is Accounting?

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

Financial Accounting s Conceptual Foundations

Economics /Management 4 Financial Accounting Financial Accounting s Conceptual Foundations L-2 A highly-stylized Information System Basic Functions (all info systems): 1. Collection of transactions data

Economics /Management 4 Financial Accounting Financial Accounting s Conceptual Foundations L-2 A highly-stylized Information System Basic Functions (all info systems): 1. Collection of transactions data

Chapter 2 Review of the Accounting Process

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

CHAPTER 8. Accounting for Receivables 1, 2 1 3, 4, 5, 6, 7 4, 5, 6, 7, 8 12, 13, 14, 15, 16

CHAPTER 8 Accounting for Receivables ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Identify the different types of receivables.

CHAPTER 8 Accounting for Receivables ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Identify the different types of receivables.

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

The Accounting Cycle Accruals and Deferrals

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

Visit Free Slides and Ebooks : CHAPTER 23. Statement of Cash Flows

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

The Accounting Cycle: Accruals and Deferrals

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Investing and Financing Decisions and the Balance Sheet Irwin/McGraw-Hill

Chapter 2 Investing and Financing Decisions and the Balance Sheet Business Background To understand amounts appearing on a company s balance sheet we need to answer these questions: What business activities

Chapter 2 Investing and Financing Decisions and the Balance Sheet Business Background To understand amounts appearing on a company s balance sheet we need to answer these questions: What business activities

PROFESSOR S CLASS NOTES COB 241 Sections 13, 14, 15 Class on September 17, 2018

PROFESSOR S CLASS NOTES COB 241 Sections 13, 14, 15 Class on September 17, 2018 Administrative Items Re-do Seating Chart for Sections 14 and 15 Reminder of correct usage of Self-Assessments Reminder of

PROFESSOR S CLASS NOTES COB 241 Sections 13, 14, 15 Class on September 17, 2018 Administrative Items Re-do Seating Chart for Sections 14 and 15 Reminder of correct usage of Self-Assessments Reminder of

2/10/2009. The accounting ACCOUNTING TRANSACTIONS AND EVENTS. Analysing transactions. Chapter 2

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

Chapter 5: Using Financial Statement Information

1 Chapter 5: Using Financial Statement Information 2 Control and Prediction Financial accounting numbers are useful in two fundamental ways: They help investors and creditors influence and monitor the

1 Chapter 5: Using Financial Statement Information 2 Control and Prediction Financial accounting numbers are useful in two fundamental ways: They help investors and creditors influence and monitor the

Chapter 5 Accrual Adjustments and Financial Statement Preparation. Revenue recognition Matching expenses to revenues Expenses related to periods

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

PROBLEM 3-2B. (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...

J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...") PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry.

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry. A. Accumulated Depreciation yes B. Albert Stucky, Drawings No C. Office equipment

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry. A. Accumulated Depreciation yes B. Albert Stucky, Drawings No C. Office equipment

Chapter 11. Notes, Bonds, and Leases

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

Chapter 5 Accrual Adjustments and Financial Statement Preparation. Revenue recognition Matching expenses to revenues Expenses related to periods

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting