Explaining International Business Cycle Synchronization: Recursive Preferences and the Terms of Trade Channel

|

|

|

- Evan Paul

- 5 years ago

- Views:

Transcription

1 1 Explaining International Business Cycle Synchronization: Recursive Preferences and the Terms of Trade Channel Robert Kollmann Université Libre de Bruxelles & CEPR

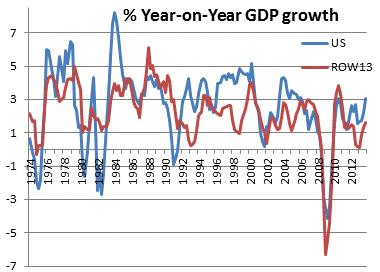

2 World business cycle : High cross-country correlations of GDP, Labor hours, investment 2 Standard macro models cannot explain this! Predict weak (or negative) transmission of country-specific shocks to foreign real activity Predicted cross-country correlations of GDP, I, Labor SMALLER than empirical correlations International correlation puzzle Key challenge for (internat.) macro E.g. Backus, Kehoe & Kydland (1992, 1994)

")

3 3 US & ROW (13 other OECD countries) Correlation: 0.65 Correlation: 0.62 Correlation: 0.62 Correlation: 0.39

4 Not plausible that world business cycle is solely driven by common (world-wide) shocks. Supply shocks: TFP is LESS correlated across countries than GDP Demand shocks: Government purchases are LESS correlated across countries than GDP (YoY: 0.3) Monetary policy shocks explain minor share of GDP Mon.pol. cannot be driver of world business cycle Financial shocks: mattered during global financial crisis, but did NOT matter during rest of post-war history (for ADVANCED countries) INTERNAT. BIZ CYCLE SYNCHRONIZATION MUST PARTLY BE ENDOGENOUS: SYNCHRONIZED DOMESTIC & FOREIGN RESPONSES TO COUNTRY-SPECIFIC SHOCKS Problem: existing models do NOT generate strong endogenous internat. shock transmission 4

5 5 This paper: possible resolution of internat. correlation puzzle Simple DSGE model in which country-specific TFP shocks induce positively correlated responses of domestic & foreign real activity realistic cross-country correlations of real activity Also: volatile real exchange rate

6 THE MODEL Simple two-country (Home, Foreign) structure: 6 2 traded goods Each country produces 1 traded good using domestic capital & labor (immobile) Local spending bias Complete financial markets Exogenous persistent TFP shocks

7 7 Model DIFFERS from standard open econ models: Recursive intertemporal preferences (Nonexpected utility) Epstein, Zin, Weil [EZW] VERY widely used in asset pricing literature; not much used in int l macro Standard int l macro models: time-separable preferences, expected utility

8 Recursive preferences: stochastic discount factor more responsive stronger real exchange rate & terms of trade response to shocks Increase in Home productivity triggers a strong Foreign t.o.t. improvement Foreign labor demand & Foreign investment Will Foreign hours rise? Depends on labor supply response! Foreign t.o.t. improvement Foreign WEALTH With strong negative wealth effect on labor supply: Foreign hours With MUTED labor wealth effect: Foreign L Foreign GDP positive int l comovement 8

9 With RECURSIVE preferences & MUTED LABOR WEALTH EFFECT: model produces sizable cross-country correlations of GDP, Investment, Hours 9 Can reproduce fact that cross-country correlations of Y,I,L are HIGHER than cross-country correlation of TFP Model also generates higher, more realistic real exchange rate volatility than conventional models

10 Muted labor wealth effect Consider two mechanisms Greenwood, Hercowitz & Huffman [GHH] period utility: zero labor wealth effect (compared to King, Plosser & Rebelo [KPR] period utility: negative labor wealth effect) real wage rigidity (in units of aggregate consumption) & demand-determined labor input (workers off labor supply schedule) 10 Finding: real consumption wage rigidity induces especially powerful cross-country transmission, in conjunction with recursive preferences

11 Intuition: Consider persistent rise in Home TFP 11 To explain why Home TFP Foreign GDP have to explain why Home TFP Foreign Labor Terms of trade are key transmission channel: Home TFP Home real exchange rate (RER) depreciates Home terms of trade (t.o.t.) Foreign t.o.t. Positive effect on Foreign Labor DEMAND Positive substitution effect & negative wealth effect on Foreign Labor SUPPLY

12 Foreign L if : STRONG effect on Foreign Labor DEMAND STRONG SUBSTITUTION effect on Foreign Labor SUPPLY WEAK WEALTH effect on Labor SUPPLY 12 Model with WEAK LABOR WEALTH EFFECT can generate STRONG rise in FOREIGN Hours & GDP IF Foreign t.o.t. improve strongly

13 13 Complete markets: Efficient risk sharing / IMRS IMRS appreciation rate of Home RER H F IMRS: intertemporal marginal rate of substitution in consumption Under time-separable preferences: weak RER response to supply shock, as shock has weak effect on IMRS / IMRS H F weak cross-country transmission

14 Recursive preferences: coefficient of risk aversion (CRA) inverse of intertemporal elasticity of substitution (IES) (Under standard preferences: CRA=1/IES) 14 CRUCIAL: When CRA 1/IES: household s Intertemporal Marginal Rate of Substitution (IMRS) depends on (future) life-time utility IMRS is volatile when shocks are persistent [This is why EZW is popular in asset pricing!]

15 Standard assumption: CRA > 1/IES increase in lifetime utility LOWERS IMRS. 15 If Home productivity increase Home life-time utility Home IMRS IMRS / IMRS appreciation rate of Home RER H F Result: under recursive preferences, Home productivity increase triggers STRONGER Foreign RER & terms of trade (t.o.t) deterioration (than with standard time-separable preferences) HOME & FOREIGN GDP, HOURS, INVESTMENT COMOVE POSITIVELY

16 16 What mechanism induces stronger RER depreciation (under recursive preferences)? Under recursive preferences, a rise in Home productivity triggers a large wealth transfer (risk sharing transfer) to Foreign boosts demand for Foreign good lowers demand for Home good amplifies depreciation of Home RER Thus: wealth transfer aligns relative IMRS & RER

17 RECURSIVE PREFERENCES ( STRONG T.O.T. RESPONSE) & MUTED LABOR WEALTH EFFECT (GHH and/or RIGID WAGE) ARE JOINTLY NEEDED FOR CROSS-COUNTRY BUSINESS CYCLE SYNCHRONIZATION With KPR period utility & flexible wage: Assumption of RECURSIVE preferences LOWERS predicted cross-country correlation of Y & L the international correlation puzzle gets worse Intuition: with recursive preferences, Home TFP triggers wealth transfer Home Foreign This DAMPENS rise in Foreign Hours if labor wealth effect is NEGATIVE. 17

18 18 Literature Vast finance literature uses EZW preferences Open economy macro-finance literature is slowly beginning to consider EZW preferences, but mainly considers endowment economies Eg Kollmann (2009, 2015, 2016), Colacito & Croce (2011,2013), Lewis & Liu (2015) Gourio, Siemer & Verdelhan (2013,2015) Etc. These papers show that EZW preferences can explain volatile real exchange rates

19 Contribution of THIS paper: PRODUCTION economy show that recursive (EZW) preferences help to RESOLVE international correlation puzzle. IF assume weak wealth effect on labor (GHH and/or rigid wage) 19 Other papers on production economies with recursive preferences: Benigno, Benigno & Nisticò (2012), Colacito, Croce, Ho & Howard (2014), Mumtaz & Theodoridis (2015), Backus et al. (2016), Tretvoll (2016) Different focus (RER volatility, risk shocks); models do not feature internat. transmission channel due to muted labor wealth effect

20 Open economy models with GHH preferences: No analysis of role of muted labor wealth effect for cross-country correlations of Y,I,L No recursive intertemporal preferences 20 E.g., Devereux et al. (1992), Correia & Rebelo (1995), Jaimovich & Rebelo (2008), Raffo (2010)

21 21 THE MODEL Countries, i=h, F (Home, Foreign) Two traded goods, country i produces good i ω 1 ω with local labor and capital: Yit, = ( Lit, θit,) ( Kit,) i 1 α j α Country i final good: Z ( y /(1 α)) ( y / α), j i, it, it, it, j y it, : input j used by country i; local spending bias: 0< α< 0.5 Final good used for consumption & investment: Zit, = Cit, + Iit,, K =, 1 (1 it δ) K + + it, Iit, 1 α α Country i final good price: P = ( p ) ( p ) it, it, jt, Home terms of trade & RER: q p p /, Ht, H, t Ft, RER P / P = ( q ) Ht, Ht, Ft, Ht, 1 2α Rise in q, RER: Home terms of trade (t.o.t.) improve & Home RER appreciates

22 22 Period utility (, ) 1 [ (, )] 1 it, it, it, 1 σ ψ σ it, it, it, u C L C L = σ > 0, σ 0 Standard period utility: King, Plosser & Rebelo [KPR] (1988) C ζ L it, it, it, = ( ), with ζ '0 < (consistent with balanced growth) Greenwood, Hercowitz & Huffman [GHH] (1988) X ( C, L ) = C + X ν( L ), with ν, ν <0 it, it, it, it, it, it, ( X ) 1 η ( θ ) η, it, it, 1 it, 1 [ it, = with η = X : ensures balanced growth & stationary hours]

23 23 mrs ψ L ψ C ( / )/( / ). it, it, it, it, it, Household intra-temporal optimization: mrs = w it, it, w : wage in consumption units ( consumption wage ) it, KPR: w = C ζ L ζ L it, it, it, it, GHH: w = X ν L,,, '( )/ ( ) '( ) it it it KPR: offer wage is increasing in Consumption a wealth increase REDUCED desired labor supply GHH: labor supply does NOT depend on consumption. Wealth shock does not affect labor supply.

24 24 Recursive EZW intertemporal preferences: = {(1 β) [ ψ ( C, L )] 1 σ + β [ EU 1 γ ] (1 σ)/(1 γ) } 1/(1 σ) it, it, it, it, t it, + 1 σ: 1/IES intertemporal elasticity of substitution (IES) γ : coefficient of risk aversion (CRA) NB When γ = σ : time-separable utility Intertemporal marginal rate of substitution (IMRS) depends on future life-time utility ρ u / C U β it, + 1 it, + 1 it, + 1 it, + 1 u / C ( EU 1 γ ) 1/(1 γ ) it, it, t it, + 1 σ γ Efficient risk sharing ρ ρ / = RER / RER Ht, + 1 Ft, + 1 t+ 1 t

25 25 ρ u / C U β it, + 1 it, + 1 it, + 1 it, /(1 ) uit, / Cit, ( EU γ t it, 1) γ + σ γ ; ρ ρ = RER RER Ht, + 1 Ht, + 1 F, t+ 1 H, t Standard assumption: γ > σ 1/IES (preference for early resolution of uncertainty) Unexpected RISE in future life-time utility LOWERS IMRS: Consumption & life-time utility are substitutes <0 Positive TFP shock in country H: Relative life-time utility of country H RER of country H depreciates strongly Relative price of good H Terms of trade of country H worsen, Terms of trade of country F improve

26 26 Investment decisions: = E ρ t it, 1 {( pit, 1 / Pit, 1 ) MPKit, 11 δ }, MPK, 1 (1 ω it+ ) Yit, + 1 / Kit, + 1 Labor demand: w it, consumption wage ( p / P ) MPL w =, MPL ωy / L,,, it, it, it, it, it it it Flex-wage economy: ( p / P ) MPL = w = mrs,, it, it, i, it it t Sticky-wage economy (predetermined wage): it, it, i, t j, t p / P ( p / p ) α ( p / P ) MPL = w = E mrs it it i, t it,,, t 1 i, t = ; α>0: import share Terms of trade improvement RAISES marginal product of capital & labor, in final good units investment and labor demand

27 27 PARAMETERS Preferences: β=0.99; Frisch labor supply elasticity: 2; Intertemporal elasticity of substitution: IES=1.5; Risk aversion: γ = 1/ IES = 0.66 & γ = 50 Technology: ω= 0.65 [labor share]; α= 0.10 [import share] Productivity: θ it, + 1 it, it, j, t i, t+ 1 ln( θ ) ln( θ ) = κ [ln( θ ) ln( θ )] + ε, κ = Fitted to quarterly US & ROW productivity (hours data), ROW: aggregate of 13 other OECD countries Std( ε θ it, + 1) = 0.78%; Corr( ε θ H, t+ 1, ε θ Ft, + 1 ) = 0.13 Internat. corr. of productivity < internat. corr of GDP SOLUTION METHOD: Third-order approx.

28 28 Historical statistics ( 73q1-13q4) [growth rates/1 st diff.] US ROW Standard deviations (%) GDP Standard deviations relative to GDP Consumption Investment Hours worked Real exchange rate 3.03 n.a. Cross-country correlations GDP 0.45 Consumption 0.35 Investment 0.34 Hours worked 0.43

29 Predicted moments: Flexible wage Role of: KPR/GHH utility; risk aversion (γ) Flexible wage KPR GHH γ=1/ies γ=50 γ=1/ies γ=50 Data (1) (2) (3) (4) (5) Standard deviations (%) GDP Standard deviations relative to GDP C Labor RER ross-country correlations DP abor ansen-jagannathan bound Recursive preferences: RER volatility HJ bound (std(imrs)) KPR utility (negative wealth effect on labor supply): recursive pref. worsen international correlation puzzle GHH utility (zero wealth effect on labor supply): recursive pref. induce higher crosscountry correl. HJ bound=std(imrs)/e(imrs); Sharpe ratio=e(rx)/std(rx); SR HJ. Rx: excess return; historical SR equity:

30 Predicted moments: Flexible wage vs. Rigid wage Role of: KPR/GHH utility; risk aversion (γ) Flexible wage Predeterm. wage KPR GHH KPR GHH γ=1/ies γ=50 γ=1/ies γ=50 γ=50 γ=50 Data (1) (2) (3) (4) (5) (6) (7) Standard deviations (%) GDP Standard deviations relative to GDP C Labor RER ross-country correlations DP abor ansen-jagannathan bound HJ bound=std(imrs)/e(imrs); Sharpe ratio=e(rx)/std(rx); SR HJ. Rx: excess return; historical SR equity:

31 31 Impact responses (%) to 1 std Home TFP innovation Flexible wage Predet. wage KPR GHH GHH γ=1/ies γ=50 γ=1/ies γ=50 γ=50 Y H Y F C H C F Labor H Labor F RER H NX H /Y H

32 32 Conclusion Paper has developed simple DSGE model that solves the international correlation puzzle : Country-specific productivity shocks generate sizable cross-country correlations of GDP, investment, Labor. Real exchange rate is volatile Key ingredients (BOTH are needed!) recursive intertemporal preferences ( volatile RER) weak wealth effect on labor supply ( positive international shock transmission, via t.o.t. channel)

33 THANK YOU! 33

DISCUSSION PAPER SERIES

DISCUSSION PAPER SERIES 2375-1489593584 EXPLAINING INTERNATIONAL BUSINESS CYCLE SYNCHRONIZATION: RECURSIVE PREFERENCES AND THE TERMS OF TRADE CHANNEL Robert Kollmann INTERNATIONAL MACROECONOMICS AND FINANCE

DISCUSSION PAPER SERIES 2375-1489593584 EXPLAINING INTERNATIONAL BUSINESS CYCLE SYNCHRONIZATION: RECURSIVE PREFERENCES AND THE TERMS OF TRADE CHANNEL Robert Kollmann INTERNATIONAL MACROECONOMICS AND FINANCE

Forthcoming: Open Economies Review

Forthcoming: Open Economies Review Explaining International Business Cycle Synchronization: Recursive Preferences and the Terms of Trade Channel Robert Kollmann (*) Université Libre de Bruxelles and CEPR

Forthcoming: Open Economies Review Explaining International Business Cycle Synchronization: Recursive Preferences and the Terms of Trade Channel Robert Kollmann (*) Université Libre de Bruxelles and CEPR

Explaining International Business Cycle Synchronization

1 Explaining Inernaional Business Cycle Synchronizaion Rober Kollmann European Cenre for Advanced Research in Economics and Saisics (ECARES), Universié Libre de Bruxelles & CEPR www.roberkollmann.com World

1 Explaining Inernaional Business Cycle Synchronizaion Rober Kollmann European Cenre for Advanced Research in Economics and Saisics (ECARES), Universié Libre de Bruxelles & CEPR www.roberkollmann.com World

Volatility Risk Pass-Through

Volatility Risk Pass-Through Ric Colacito Max Croce Yang Liu Ivan Shaliastovich 1 / 18 Main Question Uncertainty in a one-country setting: Sizeable impact of volatility risks on growth and asset prices

Volatility Risk Pass-Through Ric Colacito Max Croce Yang Liu Ivan Shaliastovich 1 / 18 Main Question Uncertainty in a one-country setting: Sizeable impact of volatility risks on growth and asset prices

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks Giancarlo Corsetti Luca Dedola Sylvain Leduc CREST, May 2008 The International Consumption Correlations Puzzle

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks Giancarlo Corsetti Luca Dedola Sylvain Leduc CREST, May 2008 The International Consumption Correlations Puzzle

Risk Sharing in a World Economy with Uncertainty Shocks *

Federal Reserve Bank of Dallas Globalization and Monetary Policy Institute Working Paper No. 258 http://www.dallasfed.org/assets/documents/institute/wpapers/2015/0258.pdf Risk Sharing in a World Economy

Federal Reserve Bank of Dallas Globalization and Monetary Policy Institute Working Paper No. 258 http://www.dallasfed.org/assets/documents/institute/wpapers/2015/0258.pdf Risk Sharing in a World Economy

Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles

: A Potential Resolution of Asset Pricing Puzzles, JF (2004) Presented by: Esben Hedegaard NYUStern October 12, 2009 Outline 1 Introduction 2 The Long-Run Risk Solving the 3 Data and Calibration Results

: A Potential Resolution of Asset Pricing Puzzles, JF (2004) Presented by: Esben Hedegaard NYUStern October 12, 2009 Outline 1 Introduction 2 The Long-Run Risk Solving the 3 Data and Calibration Results

Oil Price Uncertainty in a Small Open Economy

Yusuf Soner Başkaya Timur Hülagü Hande Küçük 6 April 212 Oil price volatility is high and it varies over time... 15 1 5 1985 199 1995 2 25 21 (a) Mean.4.35.3.25.2.15.1.5 1985 199 1995 2 25 21 (b) Coefficient

Yusuf Soner Başkaya Timur Hülagü Hande Küçük 6 April 212 Oil price volatility is high and it varies over time... 15 1 5 1985 199 1995 2 25 21 (a) Mean.4.35.3.25.2.15.1.5 1985 199 1995 2 25 21 (b) Coefficient

Heterogeneous Firm, Financial Market Integration and International Risk Sharing

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Risks for the Long Run and the Real Exchange Rate

Risks for the Long Run and the Real Exchange Rate Riccardo Colacito - NYU and UNC Kenan-Flagler Mariano M. Croce - NYU Risks for the Long Run and the Real Exchange Rate, UCLA, 2.22.06 p. 1/29 Set the stage

Risks for the Long Run and the Real Exchange Rate Riccardo Colacito - NYU and UNC Kenan-Flagler Mariano M. Croce - NYU Risks for the Long Run and the Real Exchange Rate, UCLA, 2.22.06 p. 1/29 Set the stage

Adaptive Beliefs in RBC models

Adaptive Beliefs in RBC models Sijmen Duineveld May 27, 215 Abstract This paper shows that waves of optimism and pessimism decrease volatility in a standard RBC model, but increase volatility in a RBC

Adaptive Beliefs in RBC models Sijmen Duineveld May 27, 215 Abstract This paper shows that waves of optimism and pessimism decrease volatility in a standard RBC model, but increase volatility in a RBC

Wealth E ects and Countercyclical Net Exports

Wealth E ects and Countercyclical Net Exports Alexandre Dmitriev University of New South Wales Ivan Roberts Reserve Bank of Australia and University of New South Wales February 2, 2011 Abstract Two-country,

Wealth E ects and Countercyclical Net Exports Alexandre Dmitriev University of New South Wales Ivan Roberts Reserve Bank of Australia and University of New South Wales February 2, 2011 Abstract Two-country,

Uncertainty Shocks In A Model Of Effective Demand

Uncertainty Shocks In A Model Of Effective Demand Susanto Basu Boston College NBER Brent Bundick Boston College Preliminary Can Higher Uncertainty Reduce Overall Economic Activity? Many think it is an

Uncertainty Shocks In A Model Of Effective Demand Susanto Basu Boston College NBER Brent Bundick Boston College Preliminary Can Higher Uncertainty Reduce Overall Economic Activity? Many think it is an

Austerity in the Aftermath of the Great Recession

Austerity in the Aftermath of the Great Recession Christopher L. House University of Michigan and NBER. Christian Proebsting EPFL École Polytechnique Fédérale de Lausanne Linda Tesar University of Michigan

Austerity in the Aftermath of the Great Recession Christopher L. House University of Michigan and NBER. Christian Proebsting EPFL École Polytechnique Fédérale de Lausanne Linda Tesar University of Michigan

International Business Cycles and Financial Frictions

International Business Cycles and Financial Frictions Wen Yao Tsinghua University Sept 213 Abstract This paper builds a two-country DSGE model to study the quantitative impact of nancial frictions on business

International Business Cycles and Financial Frictions Wen Yao Tsinghua University Sept 213 Abstract This paper builds a two-country DSGE model to study the quantitative impact of nancial frictions on business

Risky Mortgages in a DSGE Model

1 / 29 Risky Mortgages in a DSGE Model Chiara Forlati 1 Luisa Lambertini 1 1 École Polytechnique Fédérale de Lausanne CMSG November 6, 21 2 / 29 Motivation The global financial crisis started with an increase

1 / 29 Risky Mortgages in a DSGE Model Chiara Forlati 1 Luisa Lambertini 1 1 École Polytechnique Fédérale de Lausanne CMSG November 6, 21 2 / 29 Motivation The global financial crisis started with an increase

The Bond Premium in a DSGE Model with Long-Run Real and Nominal Risks

The Bond Premium in a DSGE Model with Long-Run Real and Nominal Risks Glenn D. Rudebusch Eric T. Swanson Economic Research Federal Reserve Bank of San Francisco Conference on Monetary Policy and Financial

The Bond Premium in a DSGE Model with Long-Run Real and Nominal Risks Glenn D. Rudebusch Eric T. Swanson Economic Research Federal Reserve Bank of San Francisco Conference on Monetary Policy and Financial

International Macroeconomics - Session II

International Macroeconomics - Session II Tobias Broer IIES Stockholm Doctoral Program in Economics Acknowledgement This lecture draws partly on lecture notes by Morten Ravn, EUI Key definitions and concepts

International Macroeconomics - Session II Tobias Broer IIES Stockholm Doctoral Program in Economics Acknowledgement This lecture draws partly on lecture notes by Morten Ravn, EUI Key definitions and concepts

Currency Risk Factors in a Recursive Multi-Country Economy

Currency Risk Factors in a Recursive Multi-Country Economy R. Colacito M.M. Croce F. Gavazzoni R. Ready NBER SI - International Asset Pricing Boston July 8, 2015 Motivation The literature has identified

Currency Risk Factors in a Recursive Multi-Country Economy R. Colacito M.M. Croce F. Gavazzoni R. Ready NBER SI - International Asset Pricing Boston July 8, 2015 Motivation The literature has identified

International Asset Pricing and Risk Sharing with Recursive Preferences

p. 1/3 International Asset Pricing and Risk Sharing with Recursive Preferences Riccardo Colacito Prepared for Tom Sargent s PhD class (Part 1) Roadmap p. 2/3 Today International asset pricing (exchange

p. 1/3 International Asset Pricing and Risk Sharing with Recursive Preferences Riccardo Colacito Prepared for Tom Sargent s PhD class (Part 1) Roadmap p. 2/3 Today International asset pricing (exchange

International Debt Deleveraging

International Debt Deleveraging Luca Fornaro London School of Economics ECB-Bank of Canada joint workshop on Exchange Rates Frankfurt, June 213 1 Motivating facts: Household debt/gdp Household debt/gdp

International Debt Deleveraging Luca Fornaro London School of Economics ECB-Bank of Canada joint workshop on Exchange Rates Frankfurt, June 213 1 Motivating facts: Household debt/gdp Household debt/gdp

Behavioral Theories of the Business Cycle

Behavioral Theories of the Business Cycle Nir Jaimovich and Sergio Rebelo September 2006 Abstract We explore the business cycle implications of expectation shocks and of two well-known psychological biases,

Behavioral Theories of the Business Cycle Nir Jaimovich and Sergio Rebelo September 2006 Abstract We explore the business cycle implications of expectation shocks and of two well-known psychological biases,

Capital Controls and Optimal Chinese Monetary Policy 1

Capital Controls and Optimal Chinese Monetary Policy 1 Chun Chang a Zheng Liu b Mark Spiegel b a Shanghai Advanced Institute of Finance b Federal Reserve Bank of San Francisco International Monetary Fund

Capital Controls and Optimal Chinese Monetary Policy 1 Chun Chang a Zheng Liu b Mark Spiegel b a Shanghai Advanced Institute of Finance b Federal Reserve Bank of San Francisco International Monetary Fund

Long run rates and monetary policy

Long run rates and monetary policy 2017 IAAE Conference, Sapporo, Japan, 06/26-30 2017 Gianni Amisano (FRB), Oreste Tristani (ECB) 1 IAAE 2017 Sapporo 6/28/2017 1 Views expressed here are not those of

Long run rates and monetary policy 2017 IAAE Conference, Sapporo, Japan, 06/26-30 2017 Gianni Amisano (FRB), Oreste Tristani (ECB) 1 IAAE 2017 Sapporo 6/28/2017 1 Views expressed here are not those of

Risk-Adjusted Capital Allocation and Misallocation

Risk-Adjusted Capital Allocation and Misallocation Joel M. David Lukas Schmid David Zeke USC Duke & CEPR USC Summer 2018 1 / 18 Introduction In an ideal world, all capital should be deployed to its most

Risk-Adjusted Capital Allocation and Misallocation Joel M. David Lukas Schmid David Zeke USC Duke & CEPR USC Summer 2018 1 / 18 Introduction In an ideal world, all capital should be deployed to its most

Consumption and Portfolio Decisions When Expected Returns A

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory. November 7, 2014

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ali Shourideh Wharton Ariel Zetlin-Jones CMU - Tepper November 7, 2014 Introduction Question: How

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ali Shourideh Wharton Ariel Zetlin-Jones CMU - Tepper November 7, 2014 Introduction Question: How

Government spending shocks, sovereign risk and the exchange rate regime

Government spending shocks, sovereign risk and the exchange rate regime Dennis Bonam Jasper Lukkezen Structure 1. Theoretical predictions 2. Empirical evidence 3. Our model SOE NK DSGE model (Galì and

Government spending shocks, sovereign risk and the exchange rate regime Dennis Bonam Jasper Lukkezen Structure 1. Theoretical predictions 2. Empirical evidence 3. Our model SOE NK DSGE model (Galì and

Skewness in Expected Macro Fundamentals and the Predictability of Equity Returns: Evidence and Theory

Skewness in Expected Macro Fundamentals and the Predictability of Equity Returns: Evidence and Theory Ric Colacito, Eric Ghysels, Jinghan Meng, and Wasin Siwasarit 1 / 26 Introduction Long-Run Risks Model:

Skewness in Expected Macro Fundamentals and the Predictability of Equity Returns: Evidence and Theory Ric Colacito, Eric Ghysels, Jinghan Meng, and Wasin Siwasarit 1 / 26 Introduction Long-Run Risks Model:

Multinational Firms, Trade, and the Trade-Comovement Puzzle

Multinational Firms, Trade, and the Trade-Comovement Puzzle Gautham Udupa CAFRAL December 11, 2018 Motivation Empirical research: More trade between countries associated with increase in business cycle

Multinational Firms, Trade, and the Trade-Comovement Puzzle Gautham Udupa CAFRAL December 11, 2018 Motivation Empirical research: More trade between countries associated with increase in business cycle

Financial Integration and Growth in a Risky World

Financial Integration and Growth in a Risky World Nicolas Coeurdacier (SciencesPo & CEPR) Helene Rey (LBS & NBER & CEPR) Pablo Winant (PSE) Barcelona June 2013 Coeurdacier, Rey, Winant Financial Integration...

Financial Integration and Growth in a Risky World Nicolas Coeurdacier (SciencesPo & CEPR) Helene Rey (LBS & NBER & CEPR) Pablo Winant (PSE) Barcelona June 2013 Coeurdacier, Rey, Winant Financial Integration...

On the Merits of Conventional vs Unconventional Fiscal Policy

On the Merits of Conventional vs Unconventional Fiscal Policy Matthieu Lemoine and Jesper Lindé Banque de France and Sveriges Riksbank The views expressed in this paper do not necessarily reflect those

On the Merits of Conventional vs Unconventional Fiscal Policy Matthieu Lemoine and Jesper Lindé Banque de France and Sveriges Riksbank The views expressed in this paper do not necessarily reflect those

Exchange Rates and Fundamentals: A General Equilibrium Exploration

Exchange Rates and Fundamentals: A General Equilibrium Exploration Takashi Kano Hitotsubashi University @HIAS, IER, AJRC Joint Workshop Frontiers in Macroeconomics and Macroeconometrics November 3-4, 2017

Exchange Rates and Fundamentals: A General Equilibrium Exploration Takashi Kano Hitotsubashi University @HIAS, IER, AJRC Joint Workshop Frontiers in Macroeconomics and Macroeconometrics November 3-4, 2017

Booms and Busts in Asset Prices. May 2010

Booms and Busts in Asset Prices Klaus Adam Mannheim University & CEPR Albert Marcet London School of Economics & CEPR May 2010 Adam & Marcet ( Mannheim Booms University and Busts & CEPR London School of

Booms and Busts in Asset Prices Klaus Adam Mannheim University & CEPR Albert Marcet London School of Economics & CEPR May 2010 Adam & Marcet ( Mannheim Booms University and Busts & CEPR London School of

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ariel Zetlin-Jones and Ali Shourideh

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ariel Zetlin-Jones and Ali Shourideh Discussion by Gaston Navarro March 3, 2015 1 / 25 Motivation

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ariel Zetlin-Jones and Ali Shourideh Discussion by Gaston Navarro March 3, 2015 1 / 25 Motivation

Appendix: Net Exports, Consumption Volatility and International Business Cycle Models.

Appendix: Net Exports, Consumption Volatility and International Business Cycle Models. Andrea Raffo Federal Reserve Bank of Kansas City February 2007 Abstract This Appendix studies the implications of

Appendix: Net Exports, Consumption Volatility and International Business Cycle Models. Andrea Raffo Federal Reserve Bank of Kansas City February 2007 Abstract This Appendix studies the implications of

Welfare Costs of Long-Run Temperature Shifts

Welfare Costs of Long-Run Temperature Shifts Ravi Bansal Fuqua School of Business Duke University & NBER Durham, NC 27708 Marcelo Ochoa Department of Economics Duke University Durham, NC 27708 October

Welfare Costs of Long-Run Temperature Shifts Ravi Bansal Fuqua School of Business Duke University & NBER Durham, NC 27708 Marcelo Ochoa Department of Economics Duke University Durham, NC 27708 October

News Shocks and Asset Price Volatility in a DSGE Model

News Shocks and Asset Price Volatility in a DSGE Model Akito Matsumoto 1 Pietro Cova 2 Massimiliano Pisani 2 Alessandro Rebucci 3 1 International Monetary Fund 2 Bank of Italy 3 Inter-American Development

News Shocks and Asset Price Volatility in a DSGE Model Akito Matsumoto 1 Pietro Cova 2 Massimiliano Pisani 2 Alessandro Rebucci 3 1 International Monetary Fund 2 Bank of Italy 3 Inter-American Development

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Convergence, capital accumulation and the nominal exchange rate

Convergence, capital accumulation and the nominal exchange rate Péter Benczúr and István Kónya Magyar Nemzeti Bank and Central European University September 2 Disclaimer The views expressed are those of

Convergence, capital accumulation and the nominal exchange rate Péter Benczúr and István Kónya Magyar Nemzeti Bank and Central European University September 2 Disclaimer The views expressed are those of

Fiscal Multipliers in Recessions. M. Canzoneri, F. Collard, H. Dellas and B. Diba

1 / 52 Fiscal Multipliers in Recessions M. Canzoneri, F. Collard, H. Dellas and B. Diba 2 / 52 Policy Practice Motivation Standard policy practice: Fiscal expansions during recessions as a means of stimulating

1 / 52 Fiscal Multipliers in Recessions M. Canzoneri, F. Collard, H. Dellas and B. Diba 2 / 52 Policy Practice Motivation Standard policy practice: Fiscal expansions during recessions as a means of stimulating

Endogenous Trade Participation with Incomplete Exchange Rate Pass-Through

Endogenous Trade Participation with Incomplete Exchange Rate Pass-Through Yuko Imura Bank of Canada June 28, 23 Disclaimer The views expressed in this presentation, or in my remarks, are my own, and do

Endogenous Trade Participation with Incomplete Exchange Rate Pass-Through Yuko Imura Bank of Canada June 28, 23 Disclaimer The views expressed in this presentation, or in my remarks, are my own, and do

Risks For The Long Run And The Real Exchange Rate

Riccardo Colacito, Mariano M. Croce Overview International Equity Premium Puzzle Model with long-run risks Calibration Exercises Estimation Attempts & Proposed Extensions Discussion International Equity

Riccardo Colacito, Mariano M. Croce Overview International Equity Premium Puzzle Model with long-run risks Calibration Exercises Estimation Attempts & Proposed Extensions Discussion International Equity

Habit Formation in State-Dependent Pricing Models: Implications for the Dynamics of Output and Prices

Habit Formation in State-Dependent Pricing Models: Implications for the Dynamics of Output and Prices Phuong V. Ngo,a a Department of Economics, Cleveland State University, 22 Euclid Avenue, Cleveland,

Habit Formation in State-Dependent Pricing Models: Implications for the Dynamics of Output and Prices Phuong V. Ngo,a a Department of Economics, Cleveland State University, 22 Euclid Avenue, Cleveland,

TFP Persistence and Monetary Policy. NBS, April 27, / 44

TFP Persistence and Monetary Policy Roberto Pancrazi Toulouse School of Economics Marija Vukotić Banque de France NBS, April 27, 2012 NBS, April 27, 2012 1 / 44 Motivation 1 Well Known Facts about the

TFP Persistence and Monetary Policy Roberto Pancrazi Toulouse School of Economics Marija Vukotić Banque de France NBS, April 27, 2012 NBS, April 27, 2012 1 / 44 Motivation 1 Well Known Facts about the

WORKING PAPER SERIES. No 36 / Investment-Specific Shocks, Business Cycles, and Asset Prices

BANK OF LITHUANIA. WORKING PAPER SERIES No 1 / 28 SHORT-TERM FORECASTING OF GDP USING LARGE MONTHLY DATASETS: A PSEUDO REAL-TIME FORECAST EVALUATION EXERCISE 1 WORKING PAPER SERIES Investment-Specific

BANK OF LITHUANIA. WORKING PAPER SERIES No 1 / 28 SHORT-TERM FORECASTING OF GDP USING LARGE MONTHLY DATASETS: A PSEUDO REAL-TIME FORECAST EVALUATION EXERCISE 1 WORKING PAPER SERIES Investment-Specific

Household Debt, Financial Intermediation, and Monetary Policy

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Gernot Müller (University of Bonn, CEPR, and Ifo)

") Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

Consumption Baskets and Currency Choice in International Borrowing

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Policy Research Working Paper 587 Consumption Baskets and Currency Choice in International

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Policy Research Working Paper 587 Consumption Baskets and Currency Choice in International

Discussion of Capital Flows and the Adjustment to Common Shocks in a Two-Country Business Cycle Model Ivan Jaccard & Frank Smets

Discussion of Capital Flows and the Adjustment to Common Shocks in a Two-Country Business Cycle Model Ivan Jaccard & Frank Smets Robert Kollmann, ULB and CEPR Bank of France, December 13, 2013 1 IMPORTANT

Discussion of Capital Flows and the Adjustment to Common Shocks in a Two-Country Business Cycle Model Ivan Jaccard & Frank Smets Robert Kollmann, ULB and CEPR Bank of France, December 13, 2013 1 IMPORTANT

News and Business Cycles in Open Economies

NIR JAIMOVICH SERGIO REBELO News and Business Cycles in Open Economies We study the effects of news about future total factor productivity (TFP) in a small open economy. We show that an open-economy version

NIR JAIMOVICH SERGIO REBELO News and Business Cycles in Open Economies We study the effects of news about future total factor productivity (TFP) in a small open economy. We show that an open-economy version

The Transmission of Monetary Policy through Redistributions and Durable Purchases

The Transmission of Monetary Policy through Redistributions and Durable Purchases Vincent Sterk and Silvana Tenreyro UCL, LSE September 2015 Sterk and Tenreyro (UCL, LSE) OMO September 2015 1 / 28 The

The Transmission of Monetary Policy through Redistributions and Durable Purchases Vincent Sterk and Silvana Tenreyro UCL, LSE September 2015 Sterk and Tenreyro (UCL, LSE) OMO September 2015 1 / 28 The

Entry, Trade Costs and International Business Cycles

Entry, Trade Costs and International Business Cycles Roberto Fattal and Jose Lopez UCLA SED Meetings July 10th 2010 Entry, Trade Costs and International Business Cycles SED Meetings July 10th 2010 1 /

Entry, Trade Costs and International Business Cycles Roberto Fattal and Jose Lopez UCLA SED Meetings July 10th 2010 Entry, Trade Costs and International Business Cycles SED Meetings July 10th 2010 1 /

Macroeconomics Sequence, Block I. Introduction to Consumption Asset Pricing

Macroeconomics Sequence, Block I Introduction to Consumption Asset Pricing Nicola Pavoni October 21, 2016 The Lucas Tree Model This is a general equilibrium model where instead of deriving properties of

Macroeconomics Sequence, Block I Introduction to Consumption Asset Pricing Nicola Pavoni October 21, 2016 The Lucas Tree Model This is a general equilibrium model where instead of deriving properties of

What drives the German current account? And how does it affect the other Euro Area member states?

What drives the German current account? And how does it affect the other Euro Area member states? Robert Kollmann (ECARES, Université Libre de Bruxelles & CEPR) Marco Ratto (JRC, European Commission) Werner

What drives the German current account? And how does it affect the other Euro Area member states? Robert Kollmann (ECARES, Université Libre de Bruxelles & CEPR) Marco Ratto (JRC, European Commission) Werner

Adjustment Costs, Agency Costs and Terms of Trade Disturbances in a Small Open Economy

Adjustment Costs, Agency Costs and Terms of Trade Disturbances in a Small Open Economy This version: April 2004 Benoît Carmichæl Lucie Samson Département d économique Université Laval, Ste-Foy, Québec

Adjustment Costs, Agency Costs and Terms of Trade Disturbances in a Small Open Economy This version: April 2004 Benoît Carmichæl Lucie Samson Département d économique Université Laval, Ste-Foy, Québec

Unemployment (Fears), Precautionary Savings, and Aggregate Demand

, Precautionary Savings, and Aggregate Demand") Unemployment (Fears), Precautionary Savings, and Aggregate Demand Wouter J. Den Haan (LSE & CEPR), Pontus Rendahl (University of Cambridge & CEPR), and Markus Riegler (LSE) January 27, 2014 Overview Heterogeneous

Unemployment (Fears), Precautionary Savings, and Aggregate Demand Wouter J. Den Haan (LSE & CEPR), Pontus Rendahl (University of Cambridge & CEPR), and Markus Riegler (LSE) January 27, 2014 Overview Heterogeneous

Balance Sheet Recessions

Balance Sheet Recessions Zhen Huo and José-Víctor Ríos-Rull University of Minnesota Federal Reserve Bank of Minneapolis CAERP CEPR NBER Conference on Money Credit and Financial Frictions Huo & Ríos-Rull

Balance Sheet Recessions Zhen Huo and José-Víctor Ríos-Rull University of Minnesota Federal Reserve Bank of Minneapolis CAERP CEPR NBER Conference on Money Credit and Financial Frictions Huo & Ríos-Rull

Risk and Ambiguity in Models of Business Cycles by David Backus, Axelle Ferriere and Stanley Zin

Discussion Risk and Ambiguity in Models of Business Cycles by David Backus, Axelle Ferriere and Stanley Zin 1 Introduction This is a very interesting, topical and useful paper. The motivation for this

Discussion Risk and Ambiguity in Models of Business Cycles by David Backus, Axelle Ferriere and Stanley Zin 1 Introduction This is a very interesting, topical and useful paper. The motivation for this

The Tail that Wags the Economy: Belief-driven Business Cycles and Persistent Stagnation

The Tail that Wags the Economy: Belief-driven Business Cycles and Persistent Stagnation Julian Kozlowski Laura Veldkamp Venky Venkateswaran NYU NYU Stern NYU Stern June 215 1 / 27 Introduction The Great

The Tail that Wags the Economy: Belief-driven Business Cycles and Persistent Stagnation Julian Kozlowski Laura Veldkamp Venky Venkateswaran NYU NYU Stern NYU Stern June 215 1 / 27 Introduction The Great

Disaster Risk and Asset Returns: An International. Perspective 1

Disaster Risk and Asset Returns: An International Perspective 1 Karen K. Lewis 2 Edith X. Liu 3 February 2017 1 For useful comments and suggestions, we thank Charles Engel, Mick Devereux, Jessica Wachter,

Disaster Risk and Asset Returns: An International Perspective 1 Karen K. Lewis 2 Edith X. Liu 3 February 2017 1 For useful comments and suggestions, we thank Charles Engel, Mick Devereux, Jessica Wachter,

AGGREGATE FLUCTUATIONS WITH NATIONAL AND INTERNATIONAL RETURNS TO SCALE. Department of Economics, Queen s University, Canada

INTERNATIONAL ECONOMIC REVIEW Vol. 43, No. 4, November 2002 AGGREGATE FLUCTUATIONS WITH NATIONAL AND INTERNATIONAL RETURNS TO SCALE BY ALLEN C. HEAD 1 Department of Economics, Queen s University, Canada

INTERNATIONAL ECONOMIC REVIEW Vol. 43, No. 4, November 2002 AGGREGATE FLUCTUATIONS WITH NATIONAL AND INTERNATIONAL RETURNS TO SCALE BY ALLEN C. HEAD 1 Department of Economics, Queen s University, Canada

Examining the Bond Premium Puzzle in a DSGE Model

Examining the Bond Premium Puzzle in a DSGE Model Glenn D. Rudebusch Eric T. Swanson Economic Research Federal Reserve Bank of San Francisco John Taylor s Contributions to Monetary Theory and Policy Federal

Examining the Bond Premium Puzzle in a DSGE Model Glenn D. Rudebusch Eric T. Swanson Economic Research Federal Reserve Bank of San Francisco John Taylor s Contributions to Monetary Theory and Policy Federal

Not All Oil Price Shocks Are Alike: A Neoclassical Perspective

Not All Oil Price Shocks Are Alike: A Neoclassical Perspective Vipin Arora Pedro Gomis-Porqueras Junsang Lee U.S. EIA Deakin Univ. SKKU December 16, 2013 GRIPS Junsang Lee (SKKU) Oil Price Dynamics in

Not All Oil Price Shocks Are Alike: A Neoclassical Perspective Vipin Arora Pedro Gomis-Porqueras Junsang Lee U.S. EIA Deakin Univ. SKKU December 16, 2013 GRIPS Junsang Lee (SKKU) Oil Price Dynamics in

International Transmission of Credit Shocks in an Equilibrium Model with Production Heterogeneity

International Transmission of Credit Shocks in an Equilibrium Model with Production Heterogeneity Yuko Imura Bank of Canada Julia K. Thomas Ohio State University April 22, 2015 ABSTRACT Many policymakers

International Transmission of Credit Shocks in an Equilibrium Model with Production Heterogeneity Yuko Imura Bank of Canada Julia K. Thomas Ohio State University April 22, 2015 ABSTRACT Many policymakers

The Transmission of Monetary Policy Operations through Redistributions and Durable Purchases

The Transmission of Monetary Policy Operations through Redistributions and Durable Purchases Vincent Sterk and Silvana Tenreyro UCL, LSE June 2014 Sterk and Tenreyro (UCL, LSE) OMO June 2014 1 / 52 The

The Transmission of Monetary Policy Operations through Redistributions and Durable Purchases Vincent Sterk and Silvana Tenreyro UCL, LSE June 2014 Sterk and Tenreyro (UCL, LSE) OMO June 2014 1 / 52 The

WORKING PAPER NO NONTRADED GOODS, MARKET SEGMENTATION, AND EXCHANGE RATES. Michael Dotsey Federal Reserve Bank of Philadelphia.

WORKING PAPER NO. 06-9 NONTRADED GOODS, MARKET SEGMENTATION, AND EXCHANGE RATES Michael Dotsey Federal Reserve Bank of Philadelphia and Margarida Duarte Federal Reserve Bank of Richmond May 2006 Nontraded

WORKING PAPER NO. 06-9 NONTRADED GOODS, MARKET SEGMENTATION, AND EXCHANGE RATES Michael Dotsey Federal Reserve Bank of Philadelphia and Margarida Duarte Federal Reserve Bank of Richmond May 2006 Nontraded

One-Factor Asset Pricing

One-Factor Asset Pricing with Stefanos Delikouras (University of Miami) Alex Kostakis Manchester June 2017, WFA (Whistler) Alex Kostakis (Manchester) One-Factor Asset Pricing June 2017, WFA (Whistler)

One-Factor Asset Pricing with Stefanos Delikouras (University of Miami) Alex Kostakis Manchester June 2017, WFA (Whistler) Alex Kostakis (Manchester) One-Factor Asset Pricing June 2017, WFA (Whistler)

Lorant Kaszab (MNB) Roman Horvath (IES)

Roman Horvath (IES)") Aleš Maršál (NBS) Lorant Kaszab (MNB) Roman Horvath (IES) Modern Tools for Financial Analysis and ing - Matlab 4.6.2015 Outline Calibration output stabilization spending reversals Table : Impact of QE

Aleš Maršál (NBS) Lorant Kaszab (MNB) Roman Horvath (IES) Modern Tools for Financial Analysis and ing - Matlab 4.6.2015 Outline Calibration output stabilization spending reversals Table : Impact of QE

Real Exchange Rate Dynamics With Endogenous Distribution Services (Preliminary and Incomplete)

") Real Exchange Rate Dynamics With Endogenous Distribution Services (Preliminary and Incomplete) Millan L. B. Mulraine First Version: December 25 Current Version: December 25 Abstract This paper demonstrates

Real Exchange Rate Dynamics With Endogenous Distribution Services (Preliminary and Incomplete) Millan L. B. Mulraine First Version: December 25 Current Version: December 25 Abstract This paper demonstrates

Household finance in Europe 1

IFC-National Bank of Belgium Workshop on "Data needs and Statistics compilation for macroprudential analysis" Brussels, Belgium, 18-19 May 2017 Household finance in Europe 1 Miguel Ampudia, European Central

IFC-National Bank of Belgium Workshop on "Data needs and Statistics compilation for macroprudential analysis" Brussels, Belgium, 18-19 May 2017 Household finance in Europe 1 Miguel Ampudia, European Central

The Extensive Margin of Trade and Monetary Policy

The Extensive Margin of Trade and Monetary Policy Yuko Imura Bank of Canada Malik Shukayev University of Alberta June 2, 216 The views expressed in this presentation are our own, and do not represent those

The Extensive Margin of Trade and Monetary Policy Yuko Imura Bank of Canada Malik Shukayev University of Alberta June 2, 216 The views expressed in this presentation are our own, and do not represent those

International Business Cycle Transmissions and News Shocks

International Business Cycle Transmissions and News Shocks Yingtong Xie Macalester College Abstract This paper examines how news shocks affect the business cycle comovements across countries. In the context

International Business Cycle Transmissions and News Shocks Yingtong Xie Macalester College Abstract This paper examines how news shocks affect the business cycle comovements across countries. In the context

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg *

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg * Eric Sims University of Notre Dame & NBER Jonathan Wolff Miami University May 31, 2017 Abstract This paper studies the properties of the fiscal

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg * Eric Sims University of Notre Dame & NBER Jonathan Wolff Miami University May 31, 2017 Abstract This paper studies the properties of the fiscal

ECON 4325 Monetary Policy and Business Fluctuations

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

International Asset Pricing with Recursive Preferences

International Asset Pricing with Recursive Preferences Riccardo Colacito Mariano M. Croce Abstract Focusing on US and UK, we document that both the Backus and Smith (1993) finding, concerning the low correlation

International Asset Pricing with Recursive Preferences Riccardo Colacito Mariano M. Croce Abstract Focusing on US and UK, we document that both the Backus and Smith (1993) finding, concerning the low correlation

Trade in Capital Goods and International Co-movements of Macroeconomic Variables

Open Econ Rev (2009) 20:113 122 DOI 10.1007/s11079-007-9053-5 Trade in Capital Goods and International Co-movements of Macroeconomic Variables Koichi Yoshimine Thomas P. Barbiero Published online: 23 May

Open Econ Rev (2009) 20:113 122 DOI 10.1007/s11079-007-9053-5 Trade in Capital Goods and International Co-movements of Macroeconomic Variables Koichi Yoshimine Thomas P. Barbiero Published online: 23 May

Evaluating International Consumption Risk Sharing. Gains: An Asset Return View

Evaluating International Consumption Risk Sharing Gains: An Asset Return View KAREN K. LEWIS EDITH X. LIU October, 2012 Abstract Multi-country consumption risk sharing studies that match the equity premium

Evaluating International Consumption Risk Sharing Gains: An Asset Return View KAREN K. LEWIS EDITH X. LIU October, 2012 Abstract Multi-country consumption risk sharing studies that match the equity premium

Risk Aversion Sensitive Real Business Cycles

Risk Aversion Sensitive Real Business Cycles Zhanhui Chen NTU Ilan Cooper BI Paul Ehling BI Costas Xiouros BI Current Draft: November 2016 Abstract We study endogenous state-contingent technology choice

Risk Aversion Sensitive Real Business Cycles Zhanhui Chen NTU Ilan Cooper BI Paul Ehling BI Costas Xiouros BI Current Draft: November 2016 Abstract We study endogenous state-contingent technology choice

Euro Area and U.S. External Adjustment: The Role of Commodity Prices and Emerging Market Shocks

Euro Area and U.S. External Adjustment: The Role of Commodity Prices and Emerging Market Shocks Massimo Giovannini (European Commission, Joint Research Centre) Robert Kollmann (ECARES, Université Libre

Euro Area and U.S. External Adjustment: The Role of Commodity Prices and Emerging Market Shocks Massimo Giovannini (European Commission, Joint Research Centre) Robert Kollmann (ECARES, Université Libre

Noise Traders, Exchange Rate Disconnect Puzzle, and the Tobin Tax

Noise Traders, Exchange Rate Disconnect Puzzle, and the Tobin Tax September 2008 Abstract This paper proposes a framework to explain why the nominal and real exchange rates are highly volatile and seem

Noise Traders, Exchange Rate Disconnect Puzzle, and the Tobin Tax September 2008 Abstract This paper proposes a framework to explain why the nominal and real exchange rates are highly volatile and seem

Household income risk, nominal frictions, and incomplete markets 1

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Disaster risk and its implications for asset pricing Online appendix

Disaster risk and its implications for asset pricing Online appendix Jerry Tsai University of Oxford Jessica A. Wachter University of Pennsylvania December 12, 2014 and NBER A The iid model This section

Disaster risk and its implications for asset pricing Online appendix Jerry Tsai University of Oxford Jessica A. Wachter University of Pennsylvania December 12, 2014 and NBER A The iid model This section

Long-Run Risks, the Macroeconomy, and Asset Prices

Long-Run Risks, the Macroeconomy, and Asset Prices By RAVI BANSAL, DANA KIKU AND AMIR YARON Ravi Bansal and Amir Yaron (2004) developed the Long-Run Risk (LRR) model which emphasizes the role of long-run

Long-Run Risks, the Macroeconomy, and Asset Prices By RAVI BANSAL, DANA KIKU AND AMIR YARON Ravi Bansal and Amir Yaron (2004) developed the Long-Run Risk (LRR) model which emphasizes the role of long-run

Housing Prices and Growth

Housing Prices and Growth James A. Kahn June 2007 Motivation Housing market boom-bust has prompted talk of bubbles. But what are fundamentals? What is the right benchmark? Motivation Housing market boom-bust

Housing Prices and Growth James A. Kahn June 2007 Motivation Housing market boom-bust has prompted talk of bubbles. But what are fundamentals? What is the right benchmark? Motivation Housing market boom-bust

Equilibrium Yield Curve, Phillips Correlation, and Monetary Policy

Equilibrium Yield Curve, Phillips Correlation, and Monetary Policy Mitsuru Katagiri International Monetary Fund October 24, 2017 @Keio University 1 / 42 Disclaimer The views expressed here are those of

Equilibrium Yield Curve, Phillips Correlation, and Monetary Policy Mitsuru Katagiri International Monetary Fund October 24, 2017 @Keio University 1 / 42 Disclaimer The views expressed here are those of

What Do International Asset Returns Imply About Consumption Risk-Sharing?

What Do International Asset Returns Imply About Consumption Risk-Sharing? (Preliminary and Incomplete) KAREN K. LEWIS EDITH X. LIU June 10, 2009 Abstract An extensive literature has examined the potential

What Do International Asset Returns Imply About Consumption Risk-Sharing? (Preliminary and Incomplete) KAREN K. LEWIS EDITH X. LIU June 10, 2009 Abstract An extensive literature has examined the potential

Term Premium Dynamics and the Taylor Rule. Bank of Canada Conference on Fixed Income Markets

Term Premium Dynamics and the Taylor Rule Michael Gallmeyer (Texas A&M) Francisco Palomino (Michigan) Burton Hollifield (Carnegie Mellon) Stanley Zin (Carnegie Mellon) Bank of Canada Conference on Fixed

Term Premium Dynamics and the Taylor Rule Michael Gallmeyer (Texas A&M) Francisco Palomino (Michigan) Burton Hollifield (Carnegie Mellon) Stanley Zin (Carnegie Mellon) Bank of Canada Conference on Fixed

Terms of Trade Shocks and Investment in Commodity-Exporting Economies 1

Terms of Trade Shocks and Investment in Commodity-Exporting Economies Jorge Fornero Markus Kirchner Andrés Yany Research Division Central Bank of Chile XXXII Economist Meeting of the Central Bank of Peru

Terms of Trade Shocks and Investment in Commodity-Exporting Economies Jorge Fornero Markus Kirchner Andrés Yany Research Division Central Bank of Chile XXXII Economist Meeting of the Central Bank of Peru

Unemployment (Fears), Precautionary Savings, and Aggregate Demand

, Precautionary Savings, and Aggregate Demand") Unemployment (Fears), Precautionary Savings, and Aggregate Demand Wouter J. Den Haan (LSE & CEPR), Pontus Rendahl (University of Cambridge & CEPR), and Markus Riegler (LSE) June 28, 2013 Overview 1 Model

Unemployment (Fears), Precautionary Savings, and Aggregate Demand Wouter J. Den Haan (LSE & CEPR), Pontus Rendahl (University of Cambridge & CEPR), and Markus Riegler (LSE) June 28, 2013 Overview 1 Model

Revisiting real exchange rate volatility: Non-traded goods and cointegrated TFP shocks

Col.lecció d Economia E18/375 Revisiting real exchange rate volatility: Non-traded goods and cointegrated TFP shocks Aydan Dogan Timo Bettendorf UB Economics Working Papers 2018/375 Revisiting real exchange

Col.lecció d Economia E18/375 Revisiting real exchange rate volatility: Non-traded goods and cointegrated TFP shocks Aydan Dogan Timo Bettendorf UB Economics Working Papers 2018/375 Revisiting real exchange

Credit Decomposition and Business Cycles

Credit Decomposition and Business Cycles Berrak Bahadir University of Georgia Inci Gumus Sabanci University September 3, 211 Abstract Recent empirical evidence suggests that household and business credit

Credit Decomposition and Business Cycles Berrak Bahadir University of Georgia Inci Gumus Sabanci University September 3, 211 Abstract Recent empirical evidence suggests that household and business credit

Frequency of Price Adjustment and Pass-through

Frequency of Price Adjustment and Pass-through Gita Gopinath Harvard and NBER Oleg Itskhoki Harvard CEFIR/NES March 11, 2009 1 / 39 Motivation Micro-level studies document significant heterogeneity in

Frequency of Price Adjustment and Pass-through Gita Gopinath Harvard and NBER Oleg Itskhoki Harvard CEFIR/NES March 11, 2009 1 / 39 Motivation Micro-level studies document significant heterogeneity in

Topic 2: International Comovement Part1: International Business cycle Facts: Quantities

Topic 2: International Comovement Part1: International Business cycle Facts: Quantities Issue: We now expand our study beyond consumption and the current account, to study a wider range of macroeconomic

Topic 2: International Comovement Part1: International Business cycle Facts: Quantities Issue: We now expand our study beyond consumption and the current account, to study a wider range of macroeconomic

One-Factor Asset Pricing

One-Factor Asset Pricing with Stefanos Delikouras (University of Miami) Alex Kostakis MBS 12 January 217, WBS Alex Kostakis (MBS) One-Factor Asset Pricing 12 January 217, WBS 1 / 32 Presentation Outline

One-Factor Asset Pricing with Stefanos Delikouras (University of Miami) Alex Kostakis MBS 12 January 217, WBS Alex Kostakis (MBS) One-Factor Asset Pricing 12 January 217, WBS 1 / 32 Presentation Outline

International Macroeconomics and Finance Session 4-6

International Macroeconomics and Finance Session 4-6 Nicolas Coeurdacier - nicolas.coeurdacier@sciences-po.fr Master EPP - Fall 2012 International real business cycles - Workhorse models of international

International Macroeconomics and Finance Session 4-6 Nicolas Coeurdacier - nicolas.coeurdacier@sciences-po.fr Master EPP - Fall 2012 International real business cycles - Workhorse models of international

Topic 7: Asset Pricing and the Macroeconomy

Topic 7: Asset Pricing and the Macroeconomy Yulei Luo SEF of HKU November 15, 2013 Luo, Y. (SEF of HKU) Macro Theory November 15, 2013 1 / 56 Consumption-based Asset Pricing Even if we cannot easily solve

Topic 7: Asset Pricing and the Macroeconomy Yulei Luo SEF of HKU November 15, 2013 Luo, Y. (SEF of HKU) Macro Theory November 15, 2013 1 / 56 Consumption-based Asset Pricing Even if we cannot easily solve

Inter-sectoral Labor Immobility, Sectoral Co-movement, and. News Shocks

Inter-sectoral Labor Immobility, Sectoral Co-movement, and News Shocks Munechika Katayama Kyoto University katayama@econ.kyoto-u.ac.jp Kwang Hwan Kim Yonsei University kimkh@yonsei.ac.kr June 3, 24 Abstract

Inter-sectoral Labor Immobility, Sectoral Co-movement, and News Shocks Munechika Katayama Kyoto University katayama@econ.kyoto-u.ac.jp Kwang Hwan Kim Yonsei University kimkh@yonsei.ac.kr June 3, 24 Abstract

Government Spending, Distortionary Taxation and the International Transmission of Business Cycles

Journal of Economic Integration 25(2), June 2010; 403-426 Government Spending, Distortionary Taxation and the International Transmission of Business Cycles María Pía Olivero Drexel University Abstract

Journal of Economic Integration 25(2), June 2010; 403-426 Government Spending, Distortionary Taxation and the International Transmission of Business Cycles María Pía Olivero Drexel University Abstract

Asset Pricing with Endogenously Uninsurable Tail Risks. University of Minnesota

Asset Pricing with Endogenously Uninsurable Tail Risks Hengjie Ai Anmol Bhandari University of Minnesota asset pricing with uninsurable idiosyncratic risks Challenges for asset pricing models generate

Asset Pricing with Endogenously Uninsurable Tail Risks Hengjie Ai Anmol Bhandari University of Minnesota asset pricing with uninsurable idiosyncratic risks Challenges for asset pricing models generate