International financial crises

|

|

|

- Morris Cameron

- 5 years ago

- Views:

Transcription

1 International Macroeconomics Master in International Economic Policy International financial crises Lectures Nicolas Coeurdacier

2 Lectures 11 and 12 International financial crises 1. Financial crises and balance sheet effects 2. Sovereign Debt Crises 3. Asset bubbles

3 Lectures 11 and 12 International financial crises 1. Financial crises and balance sheet effects 2. Sovereign Debt Crises 3. Asset bubbles

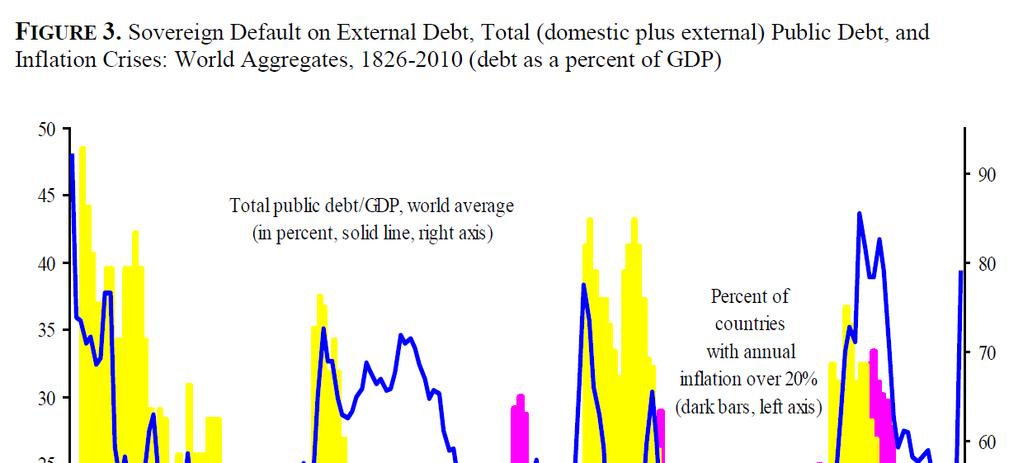

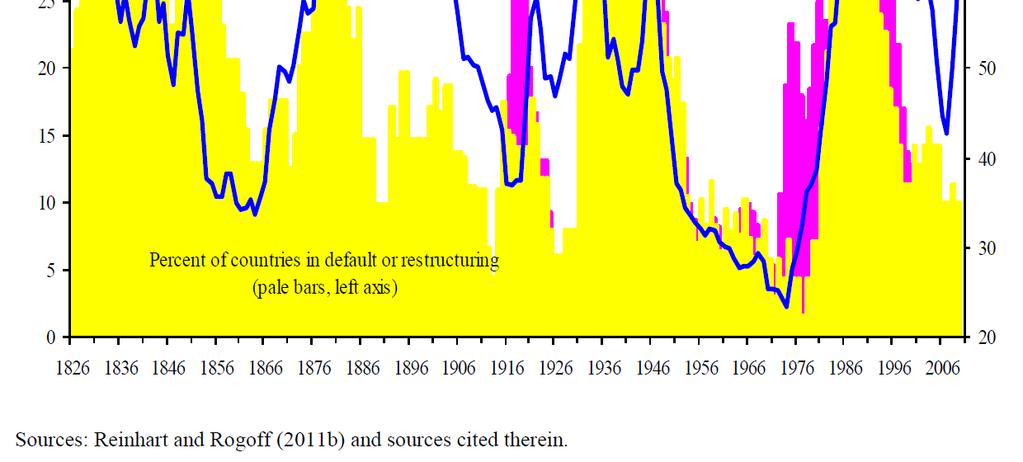

4 Sovereign debt crisis Sovereign - no international enforcement of debt contracts (difficult for creditors to seize assets, no collateral, no bankruptcy court) What is default? Missing any contractual payment: - outright complete default(rare) - repudiation or moratorium - restructuring: renegotiation (with terms less favorable to the lender: haircut) Serial default(long history): a widespread phenomenon

5

Debt,")

6 Greece: Central Government (domestic plus external) Debt, Default, Hyperinflation, and Banking Crises, (debt as a percent of GDP) Restructuring external debt (yellow) Reinhardt and Rogoff, 2010

7 What is the cost of sovereign default? Gain (wealth transfer) against reputation cost Greece default (1826): no access to international capital markets for 53 years More recently: Uruguay (2003) restructured its debt (stretching maturity dates 5 years). Returned to capital markets a month later. The haircut, or loss to bondholders, was small (13.3%, in net present value) orderly sovereign workouts are possible (not the case of Argentina)

8 Broader macroeconomic costs Triggers or worsen banking crisis Triggers currency crisis Both together generate large output losses Trade disruption (Rose, 2005): countries in default face very high risk premia to finance simple trade activities; disruption of trade credit

9 Understanding defaults: some basic theory

10 Understanding defaults: some basic theory

11 Understanding defaults: some basic theory

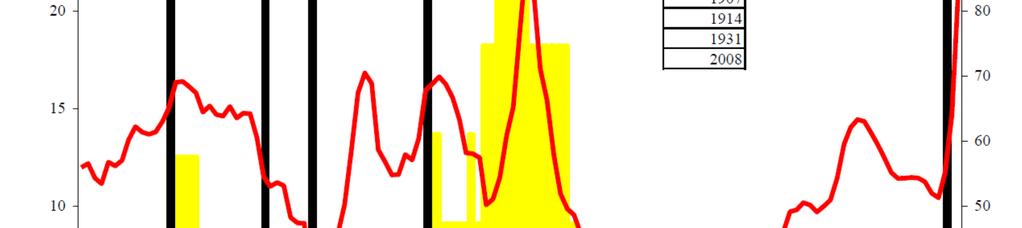

12 From financial crisis to sovereign default Typical stages of financial crises (Reinhart and Rogoff, 2009) 1) private debt surges (domestic banking credit growth + external borrowing) 2) banking crises often precede sovereign debt crises (bail outs + collapsing revenues: government debts rise by about 86% in the 3 years after financial crisis): See Ireland (bail out of banks: public debt increased by 20 % point of GDP) 3)public borrowing accelerates ahead of a sovereign debt crisis ; government often has hidden debts (Greece) 4) On eve of banking and debt crises composition of debt shifts toward short-term maturities

")

13 (Source Reinhart and Rogoff)

14

15 Cumulative increase in public debt after the financial crisis (selected countries) Source Reinhart and Rogoff

16 Debt Sustainability? Every period the government runs a deficit its debt increases How can we assess the sustainability of the path of government debt? Hard question but can examine the conditions under which the government can stabilise the debt burden. A useful tool to calculate the size of fiscal adjustment needed to stabilise debt at a current level Or a useful tool to calculate the eventual level of debt that will occur if current deficit is maintained

17 Sustainable Debt Debt is sustainable if Debt/GDP not changing: (1) Ratio rises because of interest payments r x (Debt/GDP) (2) Ratio falls because of output growth g x (Debt/GDP) (3) Debt increases because of primary deficit (G-T) Putting (1), (2) and (3) together: Change Debt/GDP = (r-g) Debt/GDP + Primary Deficit/GDP Debt sustainability (Change Debt/GDP = 0), implies: (r-g) Debt = Primary Surplus In other words the government needs to run a primary surplus to cover the excess of interest payments over GDP growth.

18 Sustainable Debt To keep debt levels constant fiscal policy needs to generate primary surplus/gdp = (r-g) Debt/GDP If r>g government has to run a primary surplus in order to control the Debt/GDP ratio If r<g then government can run a deficit (of a certain size) without seeing Debt/GDP ratio increase Shifts in interest rates and growth rates have big impact on government debt dynamics If r increases with Debt/GDP and higher r leads to lower g then countries can rapidly find their public finances deteriorating

19 2010 Debt Sustainability in the G7 Primary Balance 2010 r-g Debt GDP Canada France Germany Italy Japan United Kingdom United States Table shows primary surpluses needed (for different values r-g) to stabilise G7 s debt level at 2010 value.

20 Sovereign debt crisis in Argentina ( ) Context: The Convertibility Plan , President Carlos Menem takes office. Monthly inflation > 200%. Output plummeting April 1991, Finance Minister Domingo Cavallo implements the Convertibility Plan, including the policy of a Currency Board: Fixed Exchange Rate of 1 Peso / $1 People free to buy and sell Dollars. Implication: Central Bank no longer controls monetary policy. gradual loss of competitiveness as no longer possible to depreciate the currency and inflation still high

21 (HYPER)INFLATION Argentinean Inflation (% )

22 In 2000 Argentina does not stand out as hopeless

23 Indicators of Fiscal Sustainability Argentina s crisis caused not by high debt (around 50% GDP) buthighrandfallingg! (source: Perry & Serven, WB03)

24 Sustainable Debt - Argentina To stabilize the debt to GDP ratio, one needs: (r-g)d/y=pdf/y. D(dec 2001) = 140 bn. Pesos Y(2001) = 269 bn Pesos g( ) = -2.9 % (2001: -4.4%; 2000: -0.8, 1999: -3.5) r = 8.7 % (high but including risk premium) Required primary surplus = (140/269)*(11.6) = 6%! (actual primary surplus in 2000 = 0.3%) If negative growth is seen as persistent, this is unsustainable. Unless fiscal policy is adjusted, debt will rise continuously.

25 Sustainable Debt - Argentina Simple calculations but firm implications: (a) Although debt was not extraordinarily high, the low growth quickly makes the debt burden unsustainable (b) If growth prospects turn around, no major problems, but that requires reforms (c) Default is only a temporary relief, unless growth picks up and fiscal policy changes Problem partly due to sovereign debt -the non-existence of a chapter 11 for sovereign nations -who decides when and if a country is bankrupt?

26 Currency Mismatch and Balance Sheets Effects

27 The Unravelling recession exacerbated government s fiscal position investor fears that currency board would be abandoned fear of devaluation pushed up yield spreads dramatically increasing fiscal burden from interest payments, banking system increasingly based around dollars peso devaluation even more expensive with election focused on economic policy, capital inflows dried up. In December 2000, IMF offered $40bn subject to fiscal conditions Very costly debt exchange in mid-2001, then Argentina convinced US to get IMF to offer a further $8bn But by December 2001, the conditions had not been met, IMF pulled the plug, and government introduced outright default on public debt and exchange controls, abandoned peg, let currency float. Forced pesificationof dollar bank deposits at 1.40 Peso to $, dollar loans converted at 1-1, banks foreign exchange reserves confiscated huge balance sheet blow to the banks

28 Run on Banks and Capital Outflows $US billion $US billion IVQ 2000 IQ 2001 IIQ 2001 IIIQ 2001 IVQ IVQ 2000 IQ 2001 IIQ 2001 IIIQ 2001 IVQ 2001 Bank Deposits Balance of Payments-Non Financial Private Sector Capital Account Source: Argentine Central Bank and Ministry of Economy

1995:1 1996:1 1997:1 1998:1 1999:1 2000:1")

29 2002:1 2003:1 2004:1 2001: Exchange Rate: Peso / $ (inverted scale) 1995:1 1996:1 1997:1 1998:1 1999:1 2000:1 1994:1 1993:1 1992:1 1991:1

30 The Hair Cut March4,2005NYTimes It took more than three years of stop-and-go negotiations, threats, political maneuvers and court battles, but the largest government debt default in history ended here Thursday, as the Argentine government announced that 76 percent of its creditors had accepted a proposal that will pay them at most 30 cents. This was the biggest haircut or loss on principal, for investors of any sovereign bond restructuring in modern times.

31 Debt sustainability in Greece r-g Primary Balance 2010 Debt GDP Greece Source: OECD Economic Outlook, 2010 Table shows primary surpluses needed (for different values r-g) to stabilise Greece s debt level at 2010 value. Note, today s Greek debt is 139% of GDP 10 year interest rate Greek T-Bill (securities issued) Source: ecb

32 Greece Fiscal Adjustment

33 Balance sheet effects and the euro crisis? Greece out? Danger of self-fulfilling expectations on euro crisis? expect euro zone to break-up existng euro debt seen as foreign currency debt debt/gdp rato explodes (debt legally in euro ; GDP in «drachma» that depreciates) country becomes (even more) insolvent because of change in expectations (same with interest rate and risk premium)

34 Portugal - In 2010, another Greece? -Public Debt expected to be roughly 80% of GDP. -Fiscal deficit was 9.4% of GDP in 2009, 7.3% in Austerity plan: In 2011, we are going to reduce the deficit to 4.6 percent (Prime Minister Socrates) -Growth slowdown quite pronounced but not as bad as Ireland (-1% in 2009, 1% in 2010 and 1% in 2011) Interest rates on Portuguese 10-year T Bonds (securities issued). Source: ecb -ECB actions and fiscal adjustment have calmed down market expectations.

35 Ireland In 2010, circular causality with self-fulfilling expectations? Expect Ireland to default risk premium on Irish public debt cost of refinancing debt Irish public debt could become unsustainable Interest rates on debt issued Irish, 10-year T Bonds In 2010, more fundamentals based view of crisis was also put forward: even with low interest rate public debt burdened with banks debt would not be sustainable?

36 Ten years interest rates in big 4 Debt issued. Source: ecb

37 Key distinction, key current debate Liquidity crisis: Circular causality with self-fulfilling expectatons remedy: European Financial Stability Facility (EFSF) = financial safety net : objective break the expectations Solvency crisis: some countries will not be able to repay (whatever markets reactons) remedy: restructure sovereign debt. When? How much?

38 Run on public debt and multiple equilibria -Back to financial crisis with self fulfilling expectations crises and multiple equilibria -an investor has choice between German Treasury bond (zero probability of default) and I. Treasury bond (probability p of default); (10 year bonds ) Return on German T. bond: 1+r G Return on I. T bond : but probability pof default with hthe haircut (% of present value of debt not reimbursed) Expected return: (1-p) (1+r I ) + p(1-h) if no default if default If I. bonds are held must be that : 1+r G = (1-p) (1+r I ) + p(1-h) So (1+r I ) = 1+r G -p(1-h) note if p = 0; r G = r I no spread (1-p) More generally r I and spread increase with p and h: I. must compensate for risk and size of default

39 Run on public debt and multiple equilibria -A numerical example (too simple): 1+r G = 1.02 ; h= 0.5 (50% haircut) ; p = 10% (1+r I ) = 1+r G -p(1-h) = 1.08 or 8% interest rate (spread 600 basis points with G) (1-p) First relation (rr) : r I increases withp -How does p (the probability of default) change with r I? D t D t-1 = r D t-1 + T G For given primary balance: an increase in r increases future D t increases p Second relation (pp): p increases withr I

40 r I The case of low level of debt D 1 equilibrium no crisis pp almost vertical: p does not increase with r and is low No crisis : p close to 0, r I close to r G rr : r increases with p r G 1 0 p (proba of default)

41 r I The case of higher level of debt 3 equilibrium crisis, low interest rate and low probability of crisis versus high interest rates and high probability of crisis (the stable one with infinite interest rates and p=1) pp: p increases a lot with r and is high rr : r increases with p r G 0 1 p (proba of default)

Understanding the World Economy Master in Economics and Business. Financial crisis. Nicolas Coeurdacier

Understanding the World Economy Master in Economics and Business Financial crisis Lecture 12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 12 : Financial crisis 1. Currency crisis: first

Understanding the World Economy Master in Economics and Business Financial crisis Lecture 12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 12 : Financial crisis 1. Currency crisis: first

Fixed Exchange Rates and Currency Unions

Trade and International Finance SciencesPo Second Year Fall 2018 Fixed Exchange Rates and Currency Unions Lecture 8 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Fixed exchange rates and currency

Trade and International Finance SciencesPo Second Year Fall 2018 Fixed Exchange Rates and Currency Unions Lecture 8 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Fixed exchange rates and currency

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Can the Euro Survive?

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

Can the Euro Survive? AED/IS 4540 International Commerce and the World Economy Professor Sheldon sheldon.1@osu.edu Sovereign Debt Crisis Market participants tend to focus on yield spread between country

Greece, November 2011, in light of Argentinean Experience exactly ten years ago.

1 Greece, November 2011, in light of Argentinean Experience exactly ten years ago. Keynote speech by Domingo Cavallo at the CEO Summit, Doing More on Less, Athens, November 22, 2011 Let me be very sincere

1 Greece, November 2011, in light of Argentinean Experience exactly ten years ago. Keynote speech by Domingo Cavallo at the CEO Summit, Doing More on Less, Athens, November 22, 2011 Let me be very sincere

What could debt restructuring imply for the Eurozone? Adrian Cooper

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico 1 Current situation Eurozone (im)balances: a Small World Rising imbalances since the creation of the euro Eurozone current

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico 1 Current situation Eurozone (im)balances: a Small World Rising imbalances since the creation of the euro Eurozone current

Economic and Financial Affairs Committee. The EMU: challenges and the way forward

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

Economic and Financial Affairs Committee The EMU: challenges and the way forward May 2013 1 1 Background (1) 2007-2008 U.S. sub-prime crisis: excessive risk-taking including opaque securitization & housing

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

cepr Briefing Paper Paying the Bills in Brazil: Does the IMF s Math Add Up? CENTER FOR ECONOMIC AND POLICY RESEARCH By Mark Weisbrot and Dean Baker 1

cepr CENTER FOR ECONOMIC AND POLICY RESEARCH Briefing Paper Paying the Bills in Brazil: Does the IMF s Math Add Up? By Mark Weisbrot and Dean Baker 1 September 25, 2002 CENTER FOR ECONOMIC AND POLICY RESEARCH

cepr CENTER FOR ECONOMIC AND POLICY RESEARCH Briefing Paper Paying the Bills in Brazil: Does the IMF s Math Add Up? By Mark Weisbrot and Dean Baker 1 September 25, 2002 CENTER FOR ECONOMIC AND POLICY RESEARCH

Lecture 3: Country Risk

Lecture 3: Country Risk 1. The portfolio-balance model with default risk. 2. Default. 3. What determines sovereign spreads? 4. Debt Sustainability Analysis (DSA). 1. The portfolio balance model applied

Lecture 3: Country Risk 1. The portfolio-balance model with default risk. 2. Default. 3. What determines sovereign spreads? 4. Debt Sustainability Analysis (DSA). 1. The portfolio balance model applied

Transcript of interview with ESM Managing Director Klaus Regling. The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016

Transcript of interview with ESM Managing Director Klaus Regling Published in Yomiuri Shimbun (Japan), 1 February 2016 The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016 Yomiuri

Transcript of interview with ESM Managing Director Klaus Regling Published in Yomiuri Shimbun (Japan), 1 February 2016 The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016 Yomiuri

LEARNING OBJECTIVES 4. Debt and

LEARNING OBJECTIVES 4. Debt and Default Describe how sovereign debt is a contingent claim in context of financial mar rket penalties and broader macroeconomic costs. Determine the probability of default

LEARNING OBJECTIVES 4. Debt and Default Describe how sovereign debt is a contingent claim in context of financial mar rket penalties and broader macroeconomic costs. Determine the probability of default

What Governance for the Eurozone? Paul De Grauwe London School of Economics

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

What Governance for the Eurozone? Paul De Grauwe London School of Economics Outline of presentation Diagnosis od the Eurocrisis Design failures of Eurozone Redesigning the Eurozone: o Role of central bank

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Greece should restructure its debt but stay in the Euro

Greece should restructure its debt but stay in the Euro By Domingo Cavallo Sep 23, 2011 Greece should restructure its debt and reorganize its economy, but stay in the Euro and accept its monetary discipline.

Greece should restructure its debt but stay in the Euro By Domingo Cavallo Sep 23, 2011 Greece should restructure its debt and reorganize its economy, but stay in the Euro and accept its monetary discipline.

Economic state of the union, EuroMemo Engelbert Stockhammer Kingston University

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Policy Reforms after the Crisis

367 Policy Reforms after the Crisis Norman Chan The title of this session is supposed to be policy reforms after the 28 9 financial crisis. I think there s a big question about the title because I m not

367 Policy Reforms after the Crisis Norman Chan The title of this session is supposed to be policy reforms after the 28 9 financial crisis. I think there s a big question about the title because I m not

Lecture 6: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Understanding the World Economy. Fiscal policy. Nicolas Coeurdacier Lecture 9

Understanding the World Economy Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3. Debt and deficits 4. Fiscal policy

Understanding the World Economy Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3. Debt and deficits 4. Fiscal policy

Global Financial Systems Chapter 19 Sovereign Debt Crises

Global Financial Systems Chapter 19 Sovereign Debt Crises Jon Danielsson London School of Economics 2018 To accompany Global Financial Systems: Stability and Risk http://www.globalfinancialsystems.org/

Global Financial Systems Chapter 19 Sovereign Debt Crises Jon Danielsson London School of Economics 2018 To accompany Global Financial Systems: Stability and Risk http://www.globalfinancialsystems.org/

Recent developments and challenges for the Portuguese economy

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

The Euro Area Crisis and Ireland. Philip R. Lane! April 6th 2011! Policy Institute!

The Euro Area Crisis and Ireland Philip R. Lane! April 6th 2011! Policy Institute! Outline! Review/Analysis of Irish boom-bust-recovery cycle! European-level developments! Outstanding issues! Relative

The Euro Area Crisis and Ireland Philip R. Lane! April 6th 2011! Policy Institute! Outline! Review/Analysis of Irish boom-bust-recovery cycle! European-level developments! Outstanding issues! Relative

Managing the Fragility of the Eurozone. Paul De Grauwe London School of Economics

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

Managing the Fragility of the Eurozone Paul De Grauwe London School of Economics The causes of the crisis in the Eurozone Fragility of the system Asymmetric shocks that have led to imbalances Interaction

IS A DEBT TARGET FOR THE EMU FEASIBLE?

IS A DEBT TARGET FOR THE EMU FEASIBLE? Paolo Canofari, Piero Esposito SEP Policy Brief No. 12 26 February 2014 Introduction The newly elected government led by Alexis Tsipras is challenging the European

IS A DEBT TARGET FOR THE EMU FEASIBLE? Paolo Canofari, Piero Esposito SEP Policy Brief No. 12 26 February 2014 Introduction The newly elected government led by Alexis Tsipras is challenging the European

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003 Performance in the nineties: Better than most up to 1998, worse than most afterwards Real GDP Growth Rate (Percentages) 1981-90

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003 Performance in the nineties: Better than most up to 1998, worse than most afterwards Real GDP Growth Rate (Percentages) 1981-90

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

Econ 340. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

Discussion of Marcel Fratzscher s book Die Deutschland-Illusion Klaus Regling, ESM Managing Director Brussels, 30 September 2014 (Please check this statement against delivery) The euro area suffers from

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS. Economics 134 Spring 2018 Professor David Romer

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS LECTURE 17 THE LONG-RUN BUDGET OUTLOOK MARCH 21, 2018 I. FEASIBLE AND INFEASIBLE BUDGET POLICIES A. The distinction between the debt and the deficit B.

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS LECTURE 17 THE LONG-RUN BUDGET OUTLOOK MARCH 21, 2018 I. FEASIBLE AND INFEASIBLE BUDGET POLICIES A. The distinction between the debt and the deficit B.

Final exam Non-detailed correction 3 hours. This are indicative directions on how structure the essay questions and what was expected.

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

Interview with Klaus Regling, Managing Director, ESM. Published in Hospodárske noviny (Slovakia) on 16 September Interviewer: Tomáš Púchly

on 16 September Interviewer: Tomáš Púchly") Interview with Klaus Regling, Managing Director, ESM Published in Hospodárske noviny (Slovakia) on 16 September 2016 Interviewer: Tomáš Púchly WEB VERSION Hospodárske noviny: When Mario Draghi pledged

Interview with Klaus Regling, Managing Director, ESM Published in Hospodárske noviny (Slovakia) on 16 September 2016 Interviewer: Tomáš Púchly WEB VERSION Hospodárske noviny: When Mario Draghi pledged

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Understanding the World Economy Master in Economics and Business. Fiscal policy. Nicolas Coeurdacier

Understanding the World Economy Master in Economics and Business Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3.

Understanding the World Economy Master in Economics and Business Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3.

A Two-Handed Economist s Presentation on The Treaty. Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012

A Two-Handed Economist s Presentation on The Treaty Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012 The Fiscal Compact Treaty: Two Angles, Four Questions A

A Two-Handed Economist s Presentation on The Treaty Professor Karl Whelan University College Dublin Presentation for Labour Party April 28, 2012 The Fiscal Compact Treaty: Two Angles, Four Questions A

In search of symmetry in the eurozone

In search of symmetry in the eurozone Paul De Grauwe 2 May 2012 One of the major problems of the eurozone is the divergence of the competitive positions that have built up since the early 2000s. This divergence

In search of symmetry in the eurozone Paul De Grauwe 2 May 2012 One of the major problems of the eurozone is the divergence of the competitive positions that have built up since the early 2000s. This divergence

The Greek and EU crisis Athens, KEPE, June 27, 2012

The Greek and EU crisis Athens, KEPE, June 27, 2012 Nicholas Economides Stern School of Business, New York University http://www.stern.nyu.edu/networks/ NET Institute http://www.netinst.org/ mailto:economides@stern.nyu.edu

The Greek and EU crisis Athens, KEPE, June 27, 2012 Nicholas Economides Stern School of Business, New York University http://www.stern.nyu.edu/networks/ NET Institute http://www.netinst.org/ mailto:economides@stern.nyu.edu

Understanding the World Economy Final Exam Indicative answers

Nicolas Coeurdacier Master Economics & Business Spring 2017 Understanding the World Economy Final Exam Indicative answers I. Multiple choice [50 points = 2 per question] It is a multiple choice questionnaire.

Nicolas Coeurdacier Master Economics & Business Spring 2017 Understanding the World Economy Final Exam Indicative answers I. Multiple choice [50 points = 2 per question] It is a multiple choice questionnaire.

Supply and Demand over the Business Cycle

Session 9. The Model at Work. v Business Cycles v The Economy in the Long Run: Recession and recovery Monetary expansion The everyday business of the central bank v Summing up: The IS/LM Model in Closed

Session 9. The Model at Work. v Business Cycles v The Economy in the Long Run: Recession and recovery Monetary expansion The everyday business of the central bank v Summing up: The IS/LM Model in Closed

Financial Crises. Benjamin Graham. Videos in this lecture are from Kahn Academy

Financial Crises Videos in this lecture are from Kahn Academy Today s Plan An updated syllabus is posted Today s topics: Kahn Academy Videos on foreign currency reserves and speculative attacks The Asian

Financial Crises Videos in this lecture are from Kahn Academy Today s Plan An updated syllabus is posted Today s topics: Kahn Academy Videos on foreign currency reserves and speculative attacks The Asian

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

LESSONS OF THE EUROPEAN CRISIS FOR REGIONAL MONETARY AND FINANCIAL INTEGRATION IN EAST ASIA

LESSONS OF THE EUROPEAN CRISIS FOR REGIONAL MONETARY AND FINANCIAL INTEGRATION IN EAST ASIA Ulrich Volz, German Development Institute 8 August 2012, United Nations Economic and Social Commission for Asia

LESSONS OF THE EUROPEAN CRISIS FOR REGIONAL MONETARY AND FINANCIAL INTEGRATION IN EAST ASIA Ulrich Volz, German Development Institute 8 August 2012, United Nations Economic and Social Commission for Asia

The future of the euro zone

http://www.oklein.fr/politique-economique/the-future-of-the-euro-zone/ The future of the euro zone By Olivier Klein Some background to begin with. The European Monetary System (EMS) was put in place to

http://www.oklein.fr/politique-economique/the-future-of-the-euro-zone/ The future of the euro zone By Olivier Klein Some background to begin with. The European Monetary System (EMS) was put in place to

Presentation at the 2011 Philadelphia Fed Policy Forum December 2, University of Maryland & NBER

Presentation at the 2011 Philadelphia Fed Policy Forum December 2, 2011 Enrique G. Mendoza Enrique G. Mendoza University of Maryland & NBER 1. Short: May/Dec. 2010 Greece, Ireland plans 2. Tall: July 2011

Presentation at the 2011 Philadelphia Fed Policy Forum December 2, 2011 Enrique G. Mendoza Enrique G. Mendoza University of Maryland & NBER 1. Short: May/Dec. 2010 Greece, Ireland plans 2. Tall: July 2011

The fiscal adjustment after the crisis in Argentina

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

Periphery research: Greece Signs of improvement compared to the recovery in Latvia

Investment Research General Market Conditions 15 August 2014 Periphery research: Greece Signs of improvement compared to the recovery in Latvia Latvia s economy went into free fall in H2 07 but due to

Investment Research General Market Conditions 15 August 2014 Periphery research: Greece Signs of improvement compared to the recovery in Latvia Latvia s economy went into free fall in H2 07 but due to

Developing Countries Chapter 22

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas After being asked a number of questions about the bank and the Eurozone, we have decided to publish the answers

Euro, sovereign debt, liquidity and other issues: questions and answers from BNP Paribas After being asked a number of questions about the bank and the Eurozone, we have decided to publish the answers

Interview with Klaus Regling, Managing Director, ESM Published in Politis (Cyprus), 8 November 2015

, 8 November 2015") Interview with Klaus Regling, Managing Director, ESM Published in Politis (Cyprus), 8 November 2015 Politis: The main goal of the programme is to restore confidence in Cyprus. Is this mission complete?

Interview with Klaus Regling, Managing Director, ESM Published in Politis (Cyprus), 8 November 2015 Politis: The main goal of the programme is to restore confidence in Cyprus. Is this mission complete?

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

Lecture #8: How Scary is the US Trade Deficit?

Parsons, 2007 Lecture #8: How Scary is the US Trade Deficit? First, the facts: How big IS the US deficit? Well, if we look at the current account, whose largest component is the trade deficit, it was about

Parsons, 2007 Lecture #8: How Scary is the US Trade Deficit? First, the facts: How big IS the US deficit? Well, if we look at the current account, whose largest component is the trade deficit, it was about

ABSTRACT. This paper shows that the Russian 1998 crisis had a big impact on capital flows to Emerging Market

Sudden Stop, Financial Factors and Economic Collapse in Latin America: Learning from Argentina and Chile Guillermo A. Calvo and Ernesto Talvi NBER Working Paper No. 11153 February 2005 JEL No. F31, F32,

Sudden Stop, Financial Factors and Economic Collapse in Latin America: Learning from Argentina and Chile Guillermo A. Calvo and Ernesto Talvi NBER Working Paper No. 11153 February 2005 JEL No. F31, F32,

How Europe is Overcoming the Euro Crisis?

How Europe is Overcoming the Euro Crisis? Klaus Regling, Managing Director, ESM University of Latvia, Riga 3 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did not fully accept

How Europe is Overcoming the Euro Crisis? Klaus Regling, Managing Director, ESM University of Latvia, Riga 3 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did not fully accept

The EU is running out of choices to tame the crisis

PABLO DE OLAVIDE UNIVERSITY, Sevilla, SPAIN Conference: «Addressing the Sovereign Debt Crisis in Euro Area» Wednesday, 18 May 2011 The EU is running out of choices to tame the crisis Panayotis GLAVINIS

PABLO DE OLAVIDE UNIVERSITY, Sevilla, SPAIN Conference: «Addressing the Sovereign Debt Crisis in Euro Area» Wednesday, 18 May 2011 The EU is running out of choices to tame the crisis Panayotis GLAVINIS

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016 THIS TRAINING MATERIAL IS THE PROPERTY OF THE JOINT VIENNA INSTITUTE (JVI)

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016 THIS TRAINING MATERIAL IS THE PROPERTY OF THE JOINT VIENNA INSTITUTE (JVI)

The Financial Crisis of ? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

Greece and the Eurozone: Background, Context, and Prospects

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas (UC Irvine) Center for Social Theory and Comparative History UCLA March 9, 2015 Agenda Background on Greece Context: Eurozone

Greece and the Eurozone: Background, Context, and Prospects Stergios Skaperdas (UC Irvine) Center for Social Theory and Comparative History UCLA March 9, 2015 Agenda Background on Greece Context: Eurozone

Teetering on the brink: is the world heading for another financial crisis?

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Study Questions (with Answers) Lecture 15 International Macroeconomics

Lecture 15 International Macroeconomics") Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Ranking Country Page. Category 1: Countries with positive CEP Default Index and positive NTE. 1 Estonia 1. 2 Luxembourg 2.

Overview: Single Results of Euro Countries Ranking Country Page Category 1: Countries with positive CEP Default Index and positive NTE 1 Estonia 1 2 Luxembourg 2 3 Germany 3 4 Netherlands 4 5 Austria 5

Overview: Single Results of Euro Countries Ranking Country Page Category 1: Countries with positive CEP Default Index and positive NTE 1 Estonia 1 2 Luxembourg 2 3 Germany 3 4 Netherlands 4 5 Austria 5

The International Monetary System

INTERNATIONAL FINANCIAL MANAGEMENT Fourth Edition EUN / RESNICK The International Monetary System 2 Chapter Two INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter serves to introduce the

INTERNATIONAL FINANCIAL MANAGEMENT Fourth Edition EUN / RESNICK The International Monetary System 2 Chapter Two INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter serves to introduce the

GUESSING THE TRIGGER POINT FOR A U.S. DEBT CRISIS

No. 10-45 August 2010 working paper GUESSING THE TRIGGER POINT FOR A U.S. DEBT CRISIS By Arnold Kling The ideas presented in this research are the author s and do not represent official positions of the

No. 10-45 August 2010 working paper GUESSING THE TRIGGER POINT FOR A U.S. DEBT CRISIS By Arnold Kling The ideas presented in this research are the author s and do not represent official positions of the

Regling: Greece has to repay that loan in full. That is our expectation, nothing has changed in that regard.

Handelsblatt, 6 March 2015 Greece needs to repay its loan in full Handelsblatt: Mr. Regling, the euro rescue fund EFSF has lent around 142 billion to Greece and is thus by far Greece s largest creditor.

Handelsblatt, 6 March 2015 Greece needs to repay its loan in full Handelsblatt: Mr. Regling, the euro rescue fund EFSF has lent around 142 billion to Greece and is thus by far Greece s largest creditor.

How to avoid a double-dip recession in the eurozone

How to avoid a double-dip recession in the eurozone Paul De Grauwe 15 November 2012 1. Introduction: A double-dip recession? The risk of a double-dip recession in the eurozone has been increasing during

How to avoid a double-dip recession in the eurozone Paul De Grauwe 15 November 2012 1. Introduction: A double-dip recession? The risk of a double-dip recession in the eurozone has been increasing during

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking Institutional Money Kongress Frankfurt, 21 February 2017 300 Park Avenue South - 5

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking Institutional Money Kongress Frankfurt, 21 February 2017 300 Park Avenue South - 5

Eurozone Focus The Ongoing Saga Of Sovereign Debt

14 The Ongoing Saga Of Sovereign Debt Sovereign debt will continue to be the headline issue for the Eurozone. Whilst the discordant debate over Greece has certainly overshadowed concerns over Portugal,

14 The Ongoing Saga Of Sovereign Debt Sovereign debt will continue to be the headline issue for the Eurozone. Whilst the discordant debate over Greece has certainly overshadowed concerns over Portugal,

Greece Should Default and Abandon the Euro

Greece Should Default and Abandon the Euro By Nouriel Roubini Sep 16, 2011 1:00:00 AM Last Updated Greece is insolvent, uncompetitive and stuck in an ever-deepening depression, exacerbated by harsh and

Greece Should Default and Abandon the Euro By Nouriel Roubini Sep 16, 2011 1:00:00 AM Last Updated Greece is insolvent, uncompetitive and stuck in an ever-deepening depression, exacerbated by harsh and

Understanding the World Economy Master in Economics and Business. Fiscal policy. Nicolas Coeurdacier

Understanding the World Economy Master in Economics and Business Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3.

Understanding the World Economy Master in Economics and Business Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3.

Portugal: economic adjustment and challenges ahead

Portugal: economic adjustment and challenges ahead Carlos da Silva Costa Governor Madrid, November 10 th 2015 Forum Europa Outline I. Adjustment of the Portuguese II. Lessons to be drawn III. Challenges

Portugal: economic adjustment and challenges ahead Carlos da Silva Costa Governor Madrid, November 10 th 2015 Forum Europa Outline I. Adjustment of the Portuguese II. Lessons to be drawn III. Challenges

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies?

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies? Presented by: Howard Archer Chief European & U.K. Economist IHS Global Insight European Fiscal Stimulus Limited? Europeans

Will Fiscal Stimulus Packages Be Effective in Turning Around the European Economies? Presented by: Howard Archer Chief European & U.K. Economist IHS Global Insight European Fiscal Stimulus Limited? Europeans

Study Questions. Lecture 15 International Macroeconomics

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

Suggested answers to Problem Set 5

DEPARTMENT OF ECONOMICS SPRING 2006 UNIVERSITY OF CALIFORNIA, BERKELEY ECONOMICS 182 Suggested answers to Problem Set 5 Question 1 The United States begins at a point like 0 after 1985, where it is in

DEPARTMENT OF ECONOMICS SPRING 2006 UNIVERSITY OF CALIFORNIA, BERKELEY ECONOMICS 182 Suggested answers to Problem Set 5 Question 1 The United States begins at a point like 0 after 1985, where it is in

Session 11. Fiscal Policy

Session 11. Fiscal Policy Government size Budget balances Fiscal Policy over the business cycle Debt and sustainability Understanding Fiscal Policy: Government size Government size varies across countries.

Session 11. Fiscal Policy Government size Budget balances Fiscal Policy over the business cycle Debt and sustainability Understanding Fiscal Policy: Government size Government size varies across countries.

Modelling the sovereign debt crisis in Europe

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

Modelling the sovereign debt crisis in Europe National Institute Global Econometric Model Dawn Holland October 211 Project LINK Meeting on the World Economy National Institute of Economic and Social Research

Debt Sustainability. JURAJ SIPKO City University, VŠM, Bratislava

Debt Sustainability JURAJ SIPKO City University, VŠM, Bratislava Introduction The outbreak of the mortgage crisis in the USA caused the global financial and economic crisis. Both crises have had to cope

Debt Sustainability JURAJ SIPKO City University, VŠM, Bratislava Introduction The outbreak of the mortgage crisis in the USA caused the global financial and economic crisis. Both crises have had to cope

Economic Policy in the Crisis. Lars Calmfors Jönköping International Business School, 2 November 2009

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM Institute of International and European Affairs, Dublin 17 January 2014 Europe reacts to the euro crisis at national and EU level A comprehensive

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM Institute of International and European Affairs, Dublin 17 January 2014 Europe reacts to the euro crisis at national and EU level A comprehensive

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform

Developing Countries: Growth, Crisis, and Reform") Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

Banks and sovereign debt in Europe

Banks and sovereign debt in Europe University of Lisbon Lars Nyberg, 19 January 2012 Sovereign debt and banking problems in Europe. Sweden s experiences in the 1990 s anything to learn? CDS premiums for

Banks and sovereign debt in Europe University of Lisbon Lars Nyberg, 19 January 2012 Sovereign debt and banking problems in Europe. Sweden s experiences in the 1990 s anything to learn? CDS premiums for

Member of

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

Making Europe Safer Prof. Stijn Van Nieuwerburgh Member of www.euro-nomics.com New York University Stern School of Business National Bank of Belgium, December 22, 2011 Agenda Diagnosis of design issues

The sharp accumulation in government debt can t go on forever

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

The sharp accumulation in government debt can t go on forever Summary: Sovereign debts have increased sharply since the eighties; Global monetary stimulus has created a low interest rate environment but

The Economics of the European Union

Fletcher School, Tufts University The Economics of the European Union Prof. George Alogoskoufis Lecture 21: The Eurozone Crisis, Why it Happened and Lessons for the Future Two Important Recent Reports

Fletcher School, Tufts University The Economics of the European Union Prof. George Alogoskoufis Lecture 21: The Eurozone Crisis, Why it Happened and Lessons for the Future Two Important Recent Reports

The Outlook for the European and the German Economy

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

Impact of Greece Debt Crisis on World Economy

Impact of Greece Debt Crisis on World Economy Kovid Kumar Gupta 1 kovid.gupta@gmail.com Abstract This study aims at exploring the reasons behind the Greece debt crisis that emerged in the 21 st century

Impact of Greece Debt Crisis on World Economy Kovid Kumar Gupta 1 kovid.gupta@gmail.com Abstract This study aims at exploring the reasons behind the Greece debt crisis that emerged in the 21 st century

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 5,

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 5, 2014 http://ijecm.co.uk/ ISSN 2348 0386 Α FINANCIAL ANALYSIS OF PUBLIC FINANCES IN GREECE Markou, Angelos Technological

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 5, 2014 http://ijecm.co.uk/ ISSN 2348 0386 Α FINANCIAL ANALYSIS OF PUBLIC FINANCES IN GREECE Markou, Angelos Technological

WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM?

WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM? Jean-Pierre Aubry, Associate Fellow, CIRANO Annual conference of the Canadian Economic Association HEC, Montréal, May 30th

WHAT INVESTMENT RETURNS CAN WE EXPECT THE ECONOMY TO SUPPORT IN THE LONG-TERM? Jean-Pierre Aubry, Associate Fellow, CIRANO Annual conference of the Canadian Economic Association HEC, Montréal, May 30th

Global Debt Crisis & Impact on India. October 2011

Global Debt Crisis & Impact on India October 2011 1 Disclaimer The information contained herein is proprietary and the property of Venator Search Partners and Piper Serica Advisors Pvt. Ltd.. This Presentation

Global Debt Crisis & Impact on India October 2011 1 Disclaimer The information contained herein is proprietary and the property of Venator Search Partners and Piper Serica Advisors Pvt. Ltd.. This Presentation

Design failures of the euro area 1

1 Paul De Grauwe London School of Economics Economists were early critics of the design of the euro area, though many of their warnings went unheeded. This column discusses some fundamental design flaws,

1 Paul De Grauwe London School of Economics Economists were early critics of the design of the euro area, though many of their warnings went unheeded. This column discusses some fundamental design flaws,

Eurozone crisis and its impact on Belarus

Eurozone crisis and its impact on Belarus Seminar at the Ministry of Economy of the Republic of Belarus Robert Kirchner Minsk, 8 October 2012 The Euro crisis = An ugly combination of public debt, banking

Eurozone crisis and its impact on Belarus Seminar at the Ministry of Economy of the Republic of Belarus Robert Kirchner Minsk, 8 October 2012 The Euro crisis = An ugly combination of public debt, banking

The Great Depression, golden age, and global financial crisis

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

FINANCE & DEVELOPMENT

CLIMBI OUT OF DEBT 6 FINANCE & DEVELOPMENT March 2018 NG A new study offers more evidence that cutting spending is less harmful to growth than raising taxes Alberto Alesina, Carlo A. Favero, and Francesco

CLIMBI OUT OF DEBT 6 FINANCE & DEVELOPMENT March 2018 NG A new study offers more evidence that cutting spending is less harmful to growth than raising taxes Alberto Alesina, Carlo A. Favero, and Francesco

Final exam Non-detailed correction 3 hours

International Finance Master PEI Spring 2013 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours Documents not allowed. Basic calculator allowed. For the Multiple Choice Questions, use the answer

International Finance Master PEI Spring 2013 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours Documents not allowed. Basic calculator allowed. For the Multiple Choice Questions, use the answer

MANAGING GREEK INDEBTEDNESS: How Greece can regain fiscal credibility and avoid the recessionary debt-trap

MANAGING GREEK INDEBTEDNESS: How Greece can regain fiscal credibility and avoid the recessionary debt-trap Nicos Christodoulakis Athens University of Economics and Business Public Financial Management

MANAGING GREEK INDEBTEDNESS: How Greece can regain fiscal credibility and avoid the recessionary debt-trap Nicos Christodoulakis Athens University of Economics and Business Public Financial Management

Emerging from the Crisis

Emerging from the Crisis i Franklin Allen University of Pennsylvania Elena Carletti European University Institute Louvain-La-Neuve May 6, 2010 What caused the crisis? The conventional wisdom used to be

Emerging from the Crisis i Franklin Allen University of Pennsylvania Elena Carletti European University Institute Louvain-La-Neuve May 6, 2010 What caused the crisis? The conventional wisdom used to be

Themes in bond investing June 2009

For professional investors only Not for public distribution January 2011 Themes in bond investing June 2009 Introduction Eurozone sovereign risk concerns are back in the spotlight following the Irish bailout.

For professional investors only Not for public distribution January 2011 Themes in bond investing June 2009 Introduction Eurozone sovereign risk concerns are back in the spotlight following the Irish bailout.

3/9/2010. Topics PP542. Macroeconomic Goals (cont.) Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History

Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History") Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system