The Great Depression, golden age, and global financial crisis

|

|

|

- Henry O’Brien’

- 5 years ago

- Views:

Transcription

1 The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17

2 CONTEXT Good policies and institutions can promote economic growth and stabilize the economy during a recession. (Units 13-15) Major recessions and slowdowns in growth are due to policy and institutional failures. What caused the economic failures of the last century? What policy-making lessons can we learn from the past?

3 POLICY: AGGREGATE DEMAND SHOCK AD Shock Stabilisation Two sources for aggregate demand shock: change in households consumption or firms investment demand Government has two broad policies that it can use to counter-act a aggregate demand shock and stabilise the economy Policy Instrument Expansionary Contractionary Fiscal Government spending rises falls Tax falls rises Monetary Interest rate falls rises

4 PHILLIPS CURVE Oil price shocks increase inflationary expectations and inflation-stabilising unemployment rate moving the Philips curve up

5 PHILIPS CURVE Philips curve unemployment inflation trade-off in the short run Higher employment may results in inflation in the short run: increase workers bargaining position leads to higher wages leads to higher cost of production leads to inflation The economy can either move along Philips curve as unemployment & inflation change or the Philips curve can shift due to the following reasons: If people expect inflation to be higher in the future, the Philips curve would shift up Unemployment rate which keeps inflation constant is called the inflation-stabilising unemployment rate. If it increases, the Philips curve would shift left.

6 PERIODS IN THE US ECONOMY Names Dates US economy features 1920s Low unemployment, high productivity growth, rising inequality Great Depression High unemployment, deflation, unusually low investment, falling inequality Golden age Low unemployment, high productivity growth & investment, falling inequality Stagflation High unemployment and inflation, low productivity growth, lower profits Great moderation low unemployment & inflation, investment slowing down, sharply rising inequality, rising debt Financial crisis High unemployment, low inflation, rising inequality

7 THE THREE ECONOMIC EPOCHS US: Inequality

8 ECONOMIC EPOCHS: STYLISED FACTS Productivity Unemployment Inequality three low points hits a low point in 1931, 1979 and 2013 High, low, cyclical and high again high during the Great Depression, low till the 1979 and then cyclical with business cycles. Re-emerges again in 2008 with the Financial crisis U-shaped Richest 1% had 20% of income share in 1920s. It declined till 1979 and then started rising to the levels of 1920s

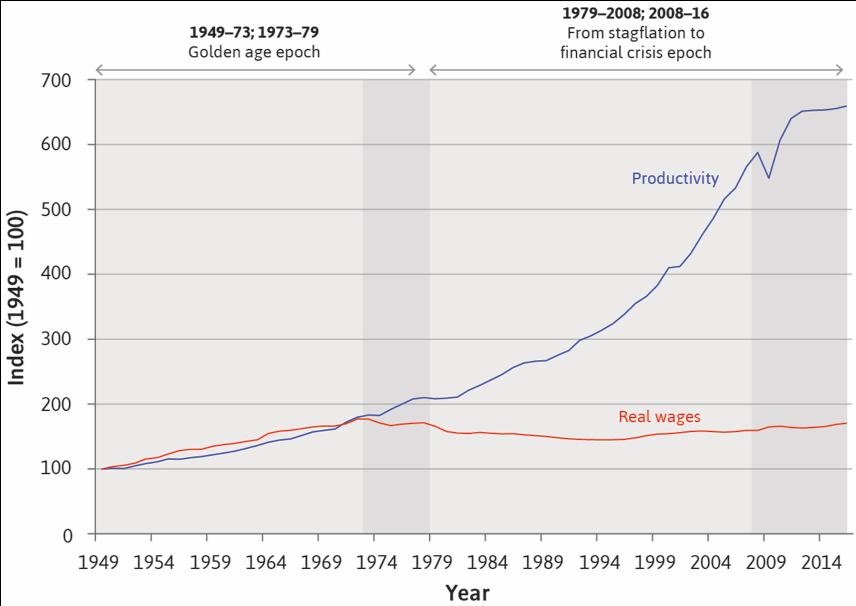

9 THE THREE ECONOMIC EPOCHS US: Unemployment and productivity

10 DIFFERENT EXPERIENCES OF THE THREE EPOCHS Name of Period Differences between US and other rich countries Great Depression US Large, sustained downturn in GDP starting from 1929 UK Avoided a banking crisis, experienced a modest fall in GDP Golden age US Technology leader Outside US Diffusion of technology creates catch-up growth, improving productivity Financial crisis US Housing bubble creates banking crisis Germany, Nordic countries Japan, Canada, Australia Did not experience bubble, largely avoided financial crisis

11 1920S AND THE GREAT DEPRESSION Dates: Conventional wisdom before this epoch Markets are self-correcting, efficient, and ensure the full use of resources. Economic outcomes in the epoch Collapse of aggregate demand, high and persistent unemployment.

12 THE GREAT DEPRESSION Unemployment and productivity growth for the US

13 THE GREAT DEPRESSION: CAUSES Great Depression the period during 1930s in which there was a sharp decline in output and employment in many countries Caused by 3 simultaneous positive feedback mechanisms in the US Pessimism about future Banking system failure Deflation households reacted to the 1929 stock market crash by saving more, further decreasing consumption many banks failed because loans could not be repaid; surviving banks raised interest rates Prices fell due to falling demand

14 THE GREAT DEPRESSION: POLICY Great Depression the period during 1930s in which there was a sharp decline in output and employment in many countries Prolonged by policy Fiscal Monetary contractionary fiscal policy contractionary monetary policy Policy solution New Deal Roosevelt s 1933 reforms

15 THE PROBLEM OF DEFLATION Deflation affects aggregate demand through several routes: the real value of debt increased; debt levels were relatively high. many debtors become insolvent, which also hurt creditors. farmers reacted by producing more to maintain their incomes, but this reduced prices further, leading to deflation. households also postponed the purchase of durables, which further reduced aggregate demand

16 THE GREAT DEPRESSION shocks to AD The downswing was driven by big falls in household and business investment, and in consumption of nondurables

17 THE ROLE OF THE GOLD STANDARD Gold Standard The system of fixed exchange rates by which the value of a currency was defined in terms of gold, for which the currency could be exchanged To prevent gold outflows, the government kept interest rates high This closed off the possibility of using monetary policy to counteract the recession.

18 INITIAL POLICY ISSUES Government policy both amplified and prolonged the shock: Contractionary fiscal policy austerity to maintain balanced budget Contractionary monetary policy real interest rate increased

19 POLICY REFORM Roosevelt s reforms Roosevelt s reforms in 1933 changed expectations, which started economy recovery The New Deal Fiscal Policy government spending on public works and relief programmes to increase aggregate demand and counter-act shock New Deal resulted in a budget deficit Gold Standard Monetary Policy Banking System US left the gold standard Nominal interest rate close to zero reforms initiated to avoid bank runs

and increased consumption")

20 POLICY REFORM Households cut consumption to restore target wealth during depression ( ) and increased consumption from 1933

21 1920S AND THE GREAT DEPRESSION Dates: Conventional wisdom before this epoch Markets are self-correcting, efficient, and ensure the full use of resources. Economic outcomes in the epoch Collapse of aggregate demand, high and persistent unemployment. Lessons learnt from the epoch Instability is an intrinsic feature of the aggregate economy and aggregate demand can be stabilised by government policy. Best framework to understand the epoch Keynes

22 GOLDEN AGE OF CAPITALISM AND ITS DEMISE Dates: Conventional wisdom before this epoch Government policy can implement an employment target by picking a point on the Phillips curve. Economic outcomes in the epoch Late-60s decline in profits, investment, and productivity growth. Stable Phillips curve trade-off disappears.

23 THE GOLDEN AGE: period with high productivity growth, high employment and stable inflation Living standards were doubling every 20 years.

24 CATCH-UP GROWTH Poor economies grew faster than richer economics to catch up.

25 GOLDEN AGE: CAUSES Changes in economic policy making and regulation Government s reassurance that a policy for supporting aggregate demand would be use when necessary Size of governments increased continuously Bretton Woods System was established, which was a more flexible alternative to the Gold Standard Bretton Woods a post-war monetary system that maintained a system of fixed but adjustable exchange rates Postwar agreement between employers and workers Sharing the gains of technological progress between workers and employers provided incentives for firms to innovate

26 WORKERS AND EMPLOYERS A virtuous circle of low unemployment, high profits and high investment: High after-tax profits in many advanced economies Expectations of high profits led to high levels of investment High investment and technological progress created more jobs, keeping unemployment low Fair-shares bargaining: Trade unions gave workers high bargaining power, which allowed wages to increase Technology adoption: The union voice effect encouraged cooperation between workers and firms in the face of technology adoption

27 USING THE LABOUR MARKET MODEL Technological progress shifted the price-setting curve up wage-setting curve shifted up due to increased worker bargaining power (informal agreement between employees and employers to share the gains to technological progress)

28 USING THE LABOUR MARKET MODEL

29 POSTWAR ACCORD ACROSS COUNTRIES Wage restraint achieved by a single centralized union, or coordinated among unions (e.g. West Germany) Government s centralised wage policy set wages directly in state-owned firms, creating wage guidance (e.g. France) Strong but fragmented unions resulted in weak coordination and opposition to technological progress, and the country s performance in the golden age was worse than elsewhere (e.g. Britain).

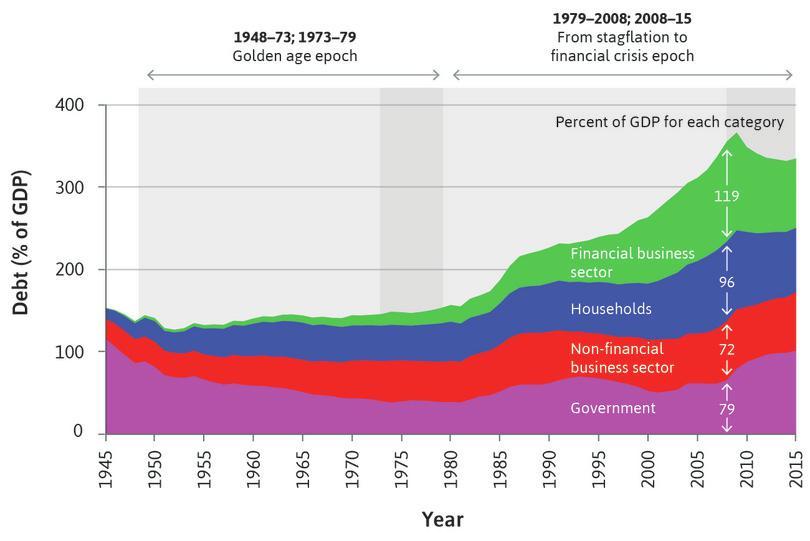

30 COLLAPSE OF THE POSTWAR ACCORD Price-setting curve eventually shifted down Workers demanded higher wages Economy-wide productivity slowdown Oil price shocks in the 1970s Workers increasingly strong bargaining position implied that Employers bore the costs of the oil price shocks Lower investment and productivity growth Rising inflation and high unemployment

31 COLLAPSE OF THE POSTWAR ACCORD

32 STAGFLATION Stagflation Persistent high inflation combined with high unemployment. Result of an upward shift of Phillips curve.

33 TYPES OF CRISES Great Depression Golden Age Stagflation caused by shocks and amplification mechanism of the aggregate demand active management of demand side by the government, while problems were creeping up on the supply side caused by shocks and amplification mechanism on both the demand and supply side Stagflation Problems on the supply side of the economy depressed the rates of profit, investment, and productivity growth. Demand-side policies that would have been part of the solution during the Great Depression had not become part of the amplification mechanism in the economy

34 GOLDEN AGE OF CAPITALISM AND ITS DEMISE Dates: Conventional wisdom before this epoch Government policy can implement an employment target by picking a point on the Phillips curve. Economic outcomes in the epoch Late-60s decline in profits, investment, and productivity growth. Stable Phillips curve trade-off disappears. Lessons learnt from the epoch The need to maintain profits, investment, and productivity growth. The ability of a government to implement sustainable low unemployment using aggregate demand policies limited. Best framework to understand the epoch Friedman

35 FROM STAGNATION TO THE FINANCIAL CRISIS Dates: Conventional wisdom before this epoch Instability has been purged from capitalist dynamics; minimally regulated financial markets work well. Economic outcomes in the epoch Financial and housing market crash of 2008.

36 SUPPLY-SIDE REFORMS Stagflation leads to policies centred on shifting the balance of power between employers and workers: Restrictive monetary and fiscal policy governments tolerated high unemployment rates to lower inflation and reduce workers bargaining power Shifting the wage-setting curve down through cuts in unemployment benefits and legislation that reduced trade union power Results in The Great Moderation Productivity growth no longer shared with workers Low and stable inflation, falling unemployment Investment did not match the growth in profits

37 GREAT MODERATION

38 PROBLEMS WITH THE GREAT MODERATION Rising inequality Financial deregulation results in higher debts as households improve their consumption via borrowing Rising debt Increasing house prices Rising inequality due to end of fairshares bargaining

39 GREAT MODERATION

40 HOUSING BOOM AND THE FINANCIAL ACCELERATOR Buying a house: mortgage requires a secured (collateralised) loan Financial accelerator: when house prices go up, so does the value of collateral, and households can borrow more. This pushes up house prices further and sustains the bubble.

41 SUBPRIME BORROWERS Poor households usually require collateral to borrow. Home loans risk falls when house prices are expected to rise Lenders ask for lower deposits, or even no deposit at all.

42 FINANCIAL DEREGULATION Great moderation, rising house prices, and the development of fancy new financial assets (CDOs and MBSs) made it profitable for banks to significantly increase lending recklessly.

43 HOUSING MARKET High debt-to-income ratio lead to the house prices becoming unsustainable and collapsing in 2008 (Financial Accelerator)

44 THE FINANCIAL CRISIS Great Moderation ended by the global financial crisis, triggered by fall in US house prices Despite bank bailouts and stabilisation policies, there followed a sustained global fall in aggregate output.

45 THE FINANCIAL CRISIS Initial fall in housing prices started a range of feedback processes: Non-residential investment and consumption fell (due to wealth targeting), especially among poorer households with subprime mortgages Spillover effects to the financial sector through the subprime mortgages Bank s borrower could not pay back due to negative home equity Investment also fell, which increased unemployment

46 FINANCIAL CRISIS rising house prices increased consumption through debt Household net worth shrank with rising unemployment Household cut consumption as wealth below target

47

48 LESSONS LEARNT

49 LESSONS LEARNT

50 FROM STAGNATION TO THE FINANCIAL CRISIS Dates: Conventional wisdom before this epoch Instability has been purged from capitalist dynamics; minimally regulated financial markets work well. Economic outcomes in the epoch Financial and housing market crash of Lessons learnt from the epoch Debt-fuelled financial and housing bubbles can co-exist with low and stable inflation, and will destabilise an economy in the absence of appropriate regulations. Best framework to understand the epoch Minsky

51 SUMMARY Epochs Great Depression Golden Age and Stagflation Great moderation and Financial Crisis Economists have learned from the successes and the failures of the three epochs. Successful policies in each epoch did not prevent positive feedback processes that contributed to subsequent crises No school of thought has policy advice that would have been good in every epoch

Lecture 7. Unemployment and Fiscal Policy

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

Lecture 7 Unemployment and Fiscal Policy The Multiplier Model As we ve seen spending on investment projects tends to cluster. What are the two reasons for this? 1. Firms may adopt a new technology at

OCR Economics A-level

OCR Economics A-level Macroeconomics Topic 3: Application of Policy Instruments 3.5 Approaches to policy and macroeconomic context Notes Explain why approaches to macroeconomic policy change in accordance

OCR Economics A-level Macroeconomics Topic 3: Application of Policy Instruments 3.5 Approaches to policy and macroeconomic context Notes Explain why approaches to macroeconomic policy change in accordance

Chapter 10. The Great Recession: A First Look. (1) Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices

Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices") Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Aggregate Demand and Aggregate Supply

Aggregate Demand and Aggregate Supply Aggregate Demand and Aggregate Supply The Learning Objectives in this presentation are covered in Chapter 20: Aggregate Demand and Aggregate Supply LEARNING OBJECTIVES

Aggregate Demand and Aggregate Supply Aggregate Demand and Aggregate Supply The Learning Objectives in this presentation are covered in Chapter 20: Aggregate Demand and Aggregate Supply LEARNING OBJECTIVES

Problem Set Suggested Answers. These answers were thought out as a guide of what a correct answer could have been. Do not consider them exhaustive.

Department of Economics Economics 115 University of California The 20 th Century World Economy Berkeley, CA 94720 Spring 2009 Problem Set Suggested Answers These answers were thought out as a guide of

Department of Economics Economics 115 University of California The 20 th Century World Economy Berkeley, CA 94720 Spring 2009 Problem Set Suggested Answers These answers were thought out as a guide of

What is Monetary Policy?

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

Economic state of the union, EuroMemo Engelbert Stockhammer Kingston University

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Number 2: The UK Spending Deficit What is it and must it be eliminated now?

Economics: the plain truth A series of plain briefings for Reps and Activists Number 2: The UK Spending Deficit What is it and must it be eliminated now? By squeezing families and businesses too hard,

Economics: the plain truth A series of plain briefings for Reps and Activists Number 2: The UK Spending Deficit What is it and must it be eliminated now? By squeezing families and businesses too hard,

Suggested Answers Problem Set # 5 Economics 501 Daniel

1. Use graphs of IS-LM-FE and AS-AD models to explain why RBC models with productivity shocks and money-supply shocks fail to explain the pro-cyclicality of money growth and inflation. Inflation falls

1. Use graphs of IS-LM-FE and AS-AD models to explain why RBC models with productivity shocks and money-supply shocks fail to explain the pro-cyclicality of money growth and inflation. Inflation falls

ECO 209Y MACROECONOMIC THEORY AND POLICY

Department of Economics Prof. Gustavo Indart University of Toronto March 14, 2007 ECO 209Y MACROECONOMIC THEORY AND POLICY SOLUTION Term Test #3 LAST NAME FIRST NAME STUDENT NUMBER Circle the section of

Department of Economics Prof. Gustavo Indart University of Toronto March 14, 2007 ECO 209Y MACROECONOMIC THEORY AND POLICY SOLUTION Term Test #3 LAST NAME FIRST NAME STUDENT NUMBER Circle the section of

LECTURE 18. AS/AD in demand-deficient Ireland: Unemployment and Deflation

LECTURE 18 AS/AD in demand-deficient Ireland: Unemployment and Deflation THE AGGREGATE SUPPLY CURVE Aggregate supply curve Each possible price level Quantity of goods & services All nation s businesses

LECTURE 18 AS/AD in demand-deficient Ireland: Unemployment and Deflation THE AGGREGATE SUPPLY CURVE Aggregate supply curve Each possible price level Quantity of goods & services All nation s businesses

AQA Economics A-level

AQA Economics A-level Macroeconomics Topic 3: Economic Performance 3.1 Economic growth and economic cycle Notes The difference between short run and long run growth Short run growth is the percentage increase

AQA Economics A-level Macroeconomics Topic 3: Economic Performance 3.1 Economic growth and economic cycle Notes The difference between short run and long run growth Short run growth is the percentage increase

Economic Policy in the Crisis. Lars Calmfors Jönköping International Business School, 2 November 2009

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Lecture 10: The Hitchhiker s Guide to Economic Policy Debates

Lecture 10: The Hitchhiker s Guide to Economic Policy Debates Ming-sen Wang Department of Economics University of Arizona June 20, 2013 Overview The ideas of economists and political philosophers, both

Lecture 10: The Hitchhiker s Guide to Economic Policy Debates Ming-sen Wang Department of Economics University of Arizona June 20, 2013 Overview The ideas of economists and political philosophers, both

Maynard s Revenge: Keynesianism and the Crisis. Lance Taylor New School for Social Research

Maynard s Revenge: Keynesianism and the Crisis Lance Taylor New School for Social Research Maynard s Macroeconomics I Fundamental uncertainty Prices of assets vs. prices of goods and services Output =

Maynard s Revenge: Keynesianism and the Crisis Lance Taylor New School for Social Research Maynard s Macroeconomics I Fundamental uncertainty Prices of assets vs. prices of goods and services Output =

Module 19 Equilibrium in the Aggregate Demand Aggregate Supply Model

What you will learn in this Module: The difference between short-run and long-run macroeconomic equilibrium The causes and effects of demand shocks and supply shocks How to determine if an economy is experiencing

What you will learn in this Module: The difference between short-run and long-run macroeconomic equilibrium The causes and effects of demand shocks and supply shocks How to determine if an economy is experiencing

Notes on Hyman Minsky s Financial Instability Hypothesis

FINANCIAL INSTABILITY Prof. Pavlina R. Tcherneva Econ 331/WS 2006 Notes on Hyman Minsky s Financial Instability Hypothesis Summary Prior to WWII, economies were described by frequent and severe depressions

FINANCIAL INSTABILITY Prof. Pavlina R. Tcherneva Econ 331/WS 2006 Notes on Hyman Minsky s Financial Instability Hypothesis Summary Prior to WWII, economies were described by frequent and severe depressions

3/9/2010. Topics PP542. Macroeconomic Goals (cont.) Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History

Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History") Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

Chapter 19 (8) International Monetary Systems: An Historical Overview

International Monetary Systems: An Historical Overview") Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Session 16. Review Session

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

In January 2017 UK Public sector net debt is 1,682.8 billion equivalent to 85.3% of GDP

UK National Debt Budget deficit annual borrowing... 2 UK net borrowing... 3 UK net borrowing as % of GDP... 3 Deficit down but debt up?... 4 Debt as % of GDP... 4 Recent history of UK National Debt...

UK National Debt Budget deficit annual borrowing... 2 UK net borrowing... 3 UK net borrowing as % of GDP... 3 Deficit down but debt up?... 4 Debt as % of GDP... 4 Recent history of UK National Debt...

MACROECONOMICS. Section I Time 70 minutes 60 Questions

MACROECONOMICS Section I Time 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

MACROECONOMICS Section I Time 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

Session 12. The New Normal. Deflation and Zero Lower Bound.

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Session 12. The New Normal. Deflation and Zero Lower Bound. Deflation and Interest Rates The Zero Lower Bound trap The Great Depression The Great Recession Deflation and the Zero Lower Bound Trap Deflation

Chapter 16. MODERN PRINCIPLES OF ECONOMICS Third Edition

Chapter 16 MODERN PRINCIPLES OF ECONOMICS Third Edition Monetary Policy Outline Monetary Policy: The Best Case The Negative Real Shock Dilemma When the Fed Does Too Much 2 Introduction In this chapter,

Chapter 16 MODERN PRINCIPLES OF ECONOMICS Third Edition Monetary Policy Outline Monetary Policy: The Best Case The Negative Real Shock Dilemma When the Fed Does Too Much 2 Introduction In this chapter,

Chapter 7 Introduction to Economic Growth and Instability

Chapter 7 Introduction to Economic Growth and Instability Chapter Overview This chapter previews economic growth, the business cycle, unemployment, and inflation. It sets the stage for the analytical presentation

Chapter 7 Introduction to Economic Growth and Instability Chapter Overview This chapter previews economic growth, the business cycle, unemployment, and inflation. It sets the stage for the analytical presentation

Perspectives on the U.S. Economy

Perspectives on the U.S. Economy Presentation for Irish Institute Seminar, April 14, 2008 Bob Murphy Department of Economics Boston College Three Perspectives 1. Historical Overview of U.S. Economic Performance

Perspectives on the U.S. Economy Presentation for Irish Institute Seminar, April 14, 2008 Bob Murphy Department of Economics Boston College Three Perspectives 1. Historical Overview of U.S. Economic Performance

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction

Chapter 1 Introduction") Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Understanding the World Economy Final Exam Indicative answers

Nicolas Coeurdacier Master Economics & Business Spring 2017 Understanding the World Economy Final Exam Indicative answers I. Multiple choice [50 points = 2 per question] It is a multiple choice questionnaire.

Nicolas Coeurdacier Master Economics & Business Spring 2017 Understanding the World Economy Final Exam Indicative answers I. Multiple choice [50 points = 2 per question] It is a multiple choice questionnaire.

Archimedean Upper Conservatory Economics, November 2016 Quiz, Unit VI, Stabilization Policies

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The federal budget tends to move toward _ as the economy. A. deficit; contracts B. deficit; expands C.

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The federal budget tends to move toward _ as the economy. A. deficit; contracts B. deficit; expands C.

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System

Chapter 18 The International Financial System") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

Business Cycle Theory

Business Cycle Theory Changes in Business Activity Economics, Unit: 06 Lesson: 01 Objectives 1.Describe phases of business cycle 2.Identify and explain the factors that cause business cycles 3.Analyze

Business Cycle Theory Changes in Business Activity Economics, Unit: 06 Lesson: 01 Objectives 1.Describe phases of business cycle 2.Identify and explain the factors that cause business cycles 3.Analyze

Finland falling further behind euro area growth

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

II. Underlying domestic macroeconomic imbalances fuelled current account deficits

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

II. Underlying domestic macroeconomic imbalances fuelled current account deficits Macroeconomic imbalances, including housing and credit bubbles, contributed to significant current account deficits in

Archimedean Upper Conservatory Economics, October 2016

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The marginal propensity to consume is equal to: A. the proportion of consumer spending as a function of

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The marginal propensity to consume is equal to: A. the proportion of consumer spending as a function of

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS. Economics 134 Spring 2018 Professor David Romer LECTURE 19

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS Economics 134 Spring 2018 Professor David Romer LECTURE 19 INCOME INEQUALITY AND MACROECONOMIC BEHAVIOR APRIL 4, 2018 I. OVERVIEW A. Changes in inequality

UNIVERSITY OF CALIFORNIA DEPARTMENT OF ECONOMICS Economics 134 Spring 2018 Professor David Romer LECTURE 19 INCOME INEQUALITY AND MACROECONOMIC BEHAVIOR APRIL 4, 2018 I. OVERVIEW A. Changes in inequality

1 of 24. Modern Macroeconomics: From the Short Run to the Long Run. 2 of 24. They could not have differed more sharply on economic theory and policy.

1 of 24 2 of 24 the Long Run They could not have differed more sharply on economic theory and policy. P R E P A R E D B Y FERNANDO QUIJANO, YVONN QUIJANO, AND XIAO XUAN XU 3 of 24 1 A P P L Y I N G T H

1 of 24 2 of 24 the Long Run They could not have differed more sharply on economic theory and policy. P R E P A R E D B Y FERNANDO QUIJANO, YVONN QUIJANO, AND XIAO XUAN XU 3 of 24 1 A P P L Y I N G T H

Econ 323 Economic History of the U.S. Prof. Eschker Fall 2018

Econ 323 Economic History of the U.S. Prof. Eschker Fall 2018 Today s Topics Business Cycles Causes of The Depression Keynesian Monetarist Business Cycles The expansions and contractions in real GDP Business

Econ 323 Economic History of the U.S. Prof. Eschker Fall 2018 Today s Topics Business Cycles Causes of The Depression Keynesian Monetarist Business Cycles The expansions and contractions in real GDP Business

The Outlook for the European and the German Economy

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

The Outlook for the European and the German Economy Annual Economic Forum of the German American Chamber of Commerce Chicago January 26, 2012 Joachim Scheide, Kiel Institute for the World Economy Once

Maneuvering Past Stagflation: Prospects for the U.S. Economy In

Maneuvering Past Stagflation: Prospects for the U.S. Economy In 2007-2008 By Michael Mussa Senior Fellow The Peter G. Peterson Institute for International Economics Washington, DC Presented at the annual

Maneuvering Past Stagflation: Prospects for the U.S. Economy In 2007-2008 By Michael Mussa Senior Fellow The Peter G. Peterson Institute for International Economics Washington, DC Presented at the annual

ECON Drexel University Summer 2008 Assignment 2. Due date: July 29, 2008

ECON 202-001 Drexel University Summer 2008 Assignment 2 Due date: July 29, 2008 Instructor: Yuan Yuan Name This homework has up to 10 points bonus. Question 1 (40 points, 2 points each): MULTIPLE CHOICE.

ECON 202-001 Drexel University Summer 2008 Assignment 2 Due date: July 29, 2008 Instructor: Yuan Yuan Name This homework has up to 10 points bonus. Question 1 (40 points, 2 points each): MULTIPLE CHOICE.

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Ch 26: Aggregate Demand and Aggregate Supply Aggregate Supply Purpose of aggregate supply: aggregate demand model is to explain

Disclaimer: This resource package is for studying purposes only EDUCATION Ch 26: Aggregate Demand and Aggregate Supply Aggregate Supply Purpose of aggregate supply: aggregate demand model is to explain

Objectives of Macroeconomics ECO403

Objectives of Macroeconomics ECO403 http//vustudents.ning.com Actual budget The amount spent by the Federal government (to purchase goods and services and for transfer payments) less the amount of tax

Objectives of Macroeconomics ECO403 http//vustudents.ning.com Actual budget The amount spent by the Federal government (to purchase goods and services and for transfer payments) less the amount of tax

CHAPTER 15 Long-Run Macroeconomic Adjustments

PART 5: THE LONG RUN AND CURRENT ISSUES IN MACRO THEORY AND POLICY CHAPTER 15 Long-Run Macroeconomic Adjustments Slides prepared by Bruno Fullone, George Brown College 2010 McGraw-Hill Ryerson Limited

PART 5: THE LONG RUN AND CURRENT ISSUES IN MACRO THEORY AND POLICY CHAPTER 15 Long-Run Macroeconomic Adjustments Slides prepared by Bruno Fullone, George Brown College 2010 McGraw-Hill Ryerson Limited

Yves Mersch: Monetary policy and economic inequality

Yves Mersch: Monetary policy and economic inequality Keynote speech by Mr Yves Mersch, Member of the Executive Board of the European Central Bank, at the Corporate Credit Conference, hosted by Muzinich,

Yves Mersch: Monetary policy and economic inequality Keynote speech by Mr Yves Mersch, Member of the Executive Board of the European Central Bank, at the Corporate Credit Conference, hosted by Muzinich,

PSE 2011 Using the top income database: inequality and financial crises

PSE 2011 Using the top income database: inequality and financial crises A B Atkinson, Nuffield College, Oxford (based on joint work with Salvatore Morelli, University of Oxford) 1 1. Introduction: Inequality

PSE 2011 Using the top income database: inequality and financial crises A B Atkinson, Nuffield College, Oxford (based on joint work with Salvatore Morelli, University of Oxford) 1 1. Introduction: Inequality

Chapter 18. The International Financial System Intervention in the Foreign Exchange Market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

1 of 15 12/1/2013 1:28 PM

1 of 15 12/1/2013 1:28 PM Policy tools include Population growth, spending behavior, and invention. Wars, natural disasters, and trade disruptions. Tax policy, government spending, and the availability

1 of 15 12/1/2013 1:28 PM Policy tools include Population growth, spending behavior, and invention. Wars, natural disasters, and trade disruptions. Tax policy, government spending, and the availability

THE FINANCIAL CRISIS AND THE GREAT RECESSION

Chapter 15 THE FINANCIAL CRISIS AND THE GREAT RECESSION Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter reviews the origins and development of the financial crisis of 2007-8 and

Chapter 15 THE FINANCIAL CRISIS AND THE GREAT RECESSION Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter reviews the origins and development of the financial crisis of 2007-8 and

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

A. What is the value of the tax increase multiplier if the MPC is.80? B. Consumption changes by 400 and disposable income by 100. What is the MPC?

KOFA HIGH SCHOOL SOCIAL SCIENCES DEPARTMENT AP ECONOMICS EXAM PREP WORKSHOP # 3 > AGGREGATE DEMAND AND SUPY NAME : DATE : 1. Figure out the following multiplier questions : A. What is the value of the

KOFA HIGH SCHOOL SOCIAL SCIENCES DEPARTMENT AP ECONOMICS EXAM PREP WORKSHOP # 3 > AGGREGATE DEMAND AND SUPY NAME : DATE : 1. Figure out the following multiplier questions : A. What is the value of the

Expansionary Fiscal Policy 2. If the economy is experiencing a recession what type of fiscal policy would be in order?

Stabilization Policies Reading Guide Chapters 12, 16, and 18 Chapter 12: Fiscal Policy 1. Assess the effect of fiscal policy on real output, price level, and the level of employment in the long run and

Stabilization Policies Reading Guide Chapters 12, 16, and 18 Chapter 12: Fiscal Policy 1. Assess the effect of fiscal policy on real output, price level, and the level of employment in the long run and

Lecture 13: The Great Depression

Lecture 13: The Great Depression November 1, 2016 Prof. Wyatt Brooks Finishing the Equity Premium Equity Premium: How much higher is the average return on stocks than on safe assets (US Treasury bonds)

Lecture 13: The Great Depression November 1, 2016 Prof. Wyatt Brooks Finishing the Equity Premium Equity Premium: How much higher is the average return on stocks than on safe assets (US Treasury bonds)

Structural Changes in the Maltese Economy

Structural Changes in the Maltese Economy Dr. Aaron George Grech Modelling and Research Department, Central Bank of Malta, Castille Place, Valletta, Malta Email: grechga@centralbankmalta.org Doi:10.5901/mjss.2015.v6n5p423

Structural Changes in the Maltese Economy Dr. Aaron George Grech Modelling and Research Department, Central Bank of Malta, Castille Place, Valletta, Malta Email: grechga@centralbankmalta.org Doi:10.5901/mjss.2015.v6n5p423

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Lecture 12: Economic Fluctuations. Rob Godby University of Wyoming

Lecture 12: Economic Fluctuations Rob Godby University of Wyoming Short-Run Economic Fluctuations Economic activity fluctuates from year to year. In some years, the production of goods and services rises.

Lecture 12: Economic Fluctuations Rob Godby University of Wyoming Short-Run Economic Fluctuations Economic activity fluctuates from year to year. In some years, the production of goods and services rises.

I. Learning Objectives II. The Income-Consumption and Income-Saving Relationships

I. Learning Objectives In this chapter students will learn: A. How changes in income affect consumption (and saving). B. About factors other than income that can affect consumption. C. How changes in real

I. Learning Objectives In this chapter students will learn: A. How changes in income affect consumption (and saving). B. About factors other than income that can affect consumption. C. How changes in real

Fluctuations of Investment Durability Irregularity of Innovation Variability of Profits Variability of Expectations

Shifts in the Invest Demand Curve Acquisition, Maintenance and Operating Costs Business Taxes Technological Change Stock of Capital Goods on Hand Expectations Fluctuations of Investment Durability Irregularity

Shifts in the Invest Demand Curve Acquisition, Maintenance and Operating Costs Business Taxes Technological Change Stock of Capital Goods on Hand Expectations Fluctuations of Investment Durability Irregularity

Structural changes in the Maltese economy

Structural changes in the Maltese economy Article published in the Annual Report 2014, pp. 72-76 BOX 4: STRUCTURAL CHANGES IN THE MALTESE ECONOMY 1 Since the global recession that took hold around the

Structural changes in the Maltese economy Article published in the Annual Report 2014, pp. 72-76 BOX 4: STRUCTURAL CHANGES IN THE MALTESE ECONOMY 1 Since the global recession that took hold around the

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

22/03/2012. Inflation Cycles. The 1920s were years of unprecedented prosperity.

The 1920s were years of unprecedented prosperity. Then, in October 1929, the stock market crashed. Overnight, stock prices fell by 30 percent. The Great Depression began and by 1933, real GDP had fallen

The 1920s were years of unprecedented prosperity. Then, in October 1929, the stock market crashed. Overnight, stock prices fell by 30 percent. The Great Depression began and by 1933, real GDP had fallen

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 8

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 8 REVIEW OF OPEN-ECONOMY IS-MP AND THE AD-IA FRAMEWORK FEBRUARY 12, 2018 I. OVERVIEW II. OPEN-ECONOMY

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 8 REVIEW OF OPEN-ECONOMY IS-MP AND THE AD-IA FRAMEWORK FEBRUARY 12, 2018 I. OVERVIEW II. OPEN-ECONOMY

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?

Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Chapter 19 International Monetary Systems: An Historical Overview

Chapter 19 International Monetary Systems: An Historical Overview Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Goals of macroeconomic policies internal and external balance Gold

Chapter 19 International Monetary Systems: An Historical Overview Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Goals of macroeconomic policies internal and external balance Gold

remain the same until the end of 2018.

We predict that the European interest rate will remain the same until the end of 2018. Throughout the past three years the interest rate has remained low. In 2017 and 2016 it has been 0.00% and in 2015

We predict that the European interest rate will remain the same until the end of 2018. Throughout the past three years the interest rate has remained low. In 2017 and 2016 it has been 0.00% and in 2015

Inflation and Unemployment: The Phillips Curve

Printed Page 331 [Notes/Highlighting] Inflation and Unemployment: The Phillips Curve What the Phillips curve is and the nature of the short-run trade-off between inflation and unemployment Why there is

Printed Page 331 [Notes/Highlighting] Inflation and Unemployment: The Phillips Curve What the Phillips curve is and the nature of the short-run trade-off between inflation and unemployment Why there is

A Note on the Economic Recovery in the 1930s. 1

K.G. Persson: A Note on the Economic Recovery in the 1930s. 1 Europe The Great Depression was not only an unprecedented economic shock to output, employment and prices, it also shattered the economic doctrines

K.G. Persson: A Note on the Economic Recovery in the 1930s. 1 Europe The Great Depression was not only an unprecedented economic shock to output, employment and prices, it also shattered the economic doctrines

Postponed recovery. The advanced economies posted a sluggish growth in CONJONCTURE IN FRANCE OCTOBER 2014 INSEE CONJONCTURE

INSEE CONJONCTURE CONJONCTURE IN FRANCE OCTOBER 2014 Postponed recovery The advanced economies posted a sluggish growth in Q2. While GDP rebounded in the United States and remained dynamic in the United

INSEE CONJONCTURE CONJONCTURE IN FRANCE OCTOBER 2014 Postponed recovery The advanced economies posted a sluggish growth in Q2. While GDP rebounded in the United States and remained dynamic in the United

The Model at Work. (Reference Slides I may or may not talk about all of this depending on time and how the conversation in class evolves)

") TOPIC 7 The Model at Work (Reference Slides I may or may not talk about all of this depending on time and how the conversation in class evolves) Note: In terms of the details of the models for changing

TOPIC 7 The Model at Work (Reference Slides I may or may not talk about all of this depending on time and how the conversation in class evolves) Note: In terms of the details of the models for changing

Session 9. The Interactions Between Cyclical and Long-term Dynamics: The Role of Inflation

Session 9. The Interactions Between Cyclical and Long-term Dynamics: The Role of Inflation Potential Output and Inflation Inflation as a Mechanism of Adjustment The Role of Expectations and the Phillips

Session 9. The Interactions Between Cyclical and Long-term Dynamics: The Role of Inflation Potential Output and Inflation Inflation as a Mechanism of Adjustment The Role of Expectations and the Phillips

ISSUES RAISED AT THE ECB WORKSHOP ON ASSET PRICES AND MONETARY POLICY

ISSUES RAISED AT THE ECB WORKSHOP ON ASSET PRICES AND MONETARY POLICY C. Detken, K. Masuch and F. Smets 1 On 11-12 December 2003, the Directorate Monetary Policy of the Directorate General Economics in

ISSUES RAISED AT THE ECB WORKSHOP ON ASSET PRICES AND MONETARY POLICY C. Detken, K. Masuch and F. Smets 1 On 11-12 December 2003, the Directorate Monetary Policy of the Directorate General Economics in

Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017

ISSN 1718-836 Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017 Re: Québec Excerpts from The Quebec Economic Plan November 2017 Update, Québec Public Accounts 2016-2017

ISSN 1718-836 Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017 Re: Québec Excerpts from The Quebec Economic Plan November 2017 Update, Québec Public Accounts 2016-2017

Please choose the most correct answer. You can choose only ONE answer for every question.

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The global economy: so far so good? 1

Presentation at the Belgian Financial Forum, Brussels, 8 July 5 The global economy: so far so good? Malcolm D Knight, General Manager Bank for International Settlements 4 was one of the best years for

Presentation at the Belgian Financial Forum, Brussels, 8 July 5 The global economy: so far so good? Malcolm D Knight, General Manager Bank for International Settlements 4 was one of the best years for

Post War Policy Errors that have Damaged the UK Economy R T H O N J O H N R E D W O O D M P

Post War Policy Errors that have Damaged the UK Economy R T H O N J O H N R E D W O O D M P The last sixty years of UK economic policy making have seen a number of bad reccessions which were the result

Post War Policy Errors that have Damaged the UK Economy R T H O N J O H N R E D W O O D M P The last sixty years of UK economic policy making have seen a number of bad reccessions which were the result

The Current Economic Crisis in the U.S.: A Crisis of Over-Investment

The Current Economic Crisis in the U.S.: A Crisis of Over-Investment David M. Kotz University of Massachusetts Amherst and Shanghai University of Finance and Economics dmkotz@econs.umass.edu January, 2013

The Current Economic Crisis in the U.S.: A Crisis of Over-Investment David M. Kotz University of Massachusetts Amherst and Shanghai University of Finance and Economics dmkotz@econs.umass.edu January, 2013

Unemployment and Inflation

Unemployment and Inflation By A. V. Vedpuriswar October 15, 2016 Inflation This refers to the phenomenon by which the price level rises and money loses value. There are two kinds of inflation: Demand pull

Unemployment and Inflation By A. V. Vedpuriswar October 15, 2016 Inflation This refers to the phenomenon by which the price level rises and money loses value. There are two kinds of inflation: Demand pull

CIE Economics AS-level

CIE Economics AS-level Topic 4: The Macroeconomy a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis Notes Determinants of AD: Aggregate demand is the total demand in the economy. It measures spending

CIE Economics AS-level Topic 4: The Macroeconomy a) Aggregate Demand (AD) and Aggregate Supply (AS) analysis Notes Determinants of AD: Aggregate demand is the total demand in the economy. It measures spending

Implications of Fiscal Austerity for U.S. Monetary Policy

Implications of Fiscal Austerity for U.S. Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston The Global Interdependence Center Central Banking Conference

Implications of Fiscal Austerity for U.S. Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston The Global Interdependence Center Central Banking Conference

10.2 Recent Shocks to the Macroeconomy Introduction. Housing Prices. Chapter 10 The Great Recession: A First Look

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Shanghai Livingston American School Quarterly / Trimester Plan 3 AP Macro

Shanghai Livingston American School Quarterly / Trimester Plan 3 AP Macro Concept / Topic To Teach: Unit 4 MODULE 22: SAVING, INVESTMENT, AND THE FINANCIAL Specific Objectives: ELD Standards SYSTEM Week

Shanghai Livingston American School Quarterly / Trimester Plan 3 AP Macro Concept / Topic To Teach: Unit 4 MODULE 22: SAVING, INVESTMENT, AND THE FINANCIAL Specific Objectives: ELD Standards SYSTEM Week

Antonio Fazio: Overview of global economic and financial developments in first half 2004

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

East Asia Crisis of Econ October 8, Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo

East Asia Crisis of 1997 Econ 7920 October 8, 2008 Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo The East Asian currency crisis of 1997 caused severe distress for the countries of East Asia

East Asia Crisis of 1997 Econ 7920 October 8, 2008 Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo The East Asian currency crisis of 1997 caused severe distress for the countries of East Asia

Fair Value Lending. Regulating against a Property Bubble. Reform Alliance

Fair Value Lending Regulating against a Property Bubble Reform Alliance A. Fair Value Lending The same economists and estate agents who talked about soft landings back in 2007 are back on the airwaves

Fair Value Lending Regulating against a Property Bubble Reform Alliance A. Fair Value Lending The same economists and estate agents who talked about soft landings back in 2007 are back on the airwaves

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno eparker@unr.edu DJIA / CPI 15,000 10,000 5,000 0 1949 1951 1953 A Look at the DJIA Adjusting

IMPLICATIONS OF THE GLOBAL FINANCIAL CRISIS Elliott Parker, Ph.D. Professor of Economics University of Nevada, Reno eparker@unr.edu DJIA / CPI 15,000 10,000 5,000 0 1949 1951 1953 A Look at the DJIA Adjusting

ECON Intermediate Macroeconomic Theory

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

The Great Depression. Economic Forces in American History

The Great Depression Economic Forces in American History The Great Depression: Outline Contours of the Decline Explaining the Downturn Explaining the Severity Some old explanations Some recent explanations

The Great Depression Economic Forces in American History The Great Depression: Outline Contours of the Decline Explaining the Downturn Explaining the Severity Some old explanations Some recent explanations

Lessons from the Great Depression

Used with permission from Cengage Lessons from the Great Depression Textbook authors: James Gwartney, Richard Stroup, Russell Sobel, & David Macpherson Slides authored and animated by: James Gwartney &

Used with permission from Cengage Lessons from the Great Depression Textbook authors: James Gwartney, Richard Stroup, Russell Sobel, & David Macpherson Slides authored and animated by: James Gwartney &

ophillips Curve Multiple Choice Identify the choice that best completes the statement or answers the question.

ophillips Curve Multiple Choice Identify the choice that best completes the statement or answers the question. 1. If the natural rate of unemployment is 5%, and the actual rate of unemployment is 4%: A.

ophillips Curve Multiple Choice Identify the choice that best completes the statement or answers the question. 1. If the natural rate of unemployment is 5%, and the actual rate of unemployment is 4%: A.

Knowledge Series : Inflation. February 2009

Knowledge Series : Inflation February 2009 Price Shocks? Fiscal measures? Declining output? Excess money supply? Inflation Monetary tightening? 2 3 Introduction to Inflation - Inflation

Knowledge Series : Inflation February 2009 Price Shocks? Fiscal measures? Declining output? Excess money supply? Inflation Monetary tightening? 2 3 Introduction to Inflation - Inflation

CHAPTER 13: Monetary Policy

CHAPTER 13: Monetary Policy 1a. FIGURE 13A 1 An Expansionary Monetary Policy Nominal Interest Rate (%) Price level (GDP deflator, 2002= 100) Quantity of Money ($ billions) Real GDP (2002 $billions) An

CHAPTER 13: Monetary Policy 1a. FIGURE 13A 1 An Expansionary Monetary Policy Nominal Interest Rate (%) Price level (GDP deflator, 2002= 100) Quantity of Money ($ billions) Real GDP (2002 $billions) An

Eurozone Ernst & Young Eurozone Forecast June 2013

Eurozone Ernst & Young Eurozone Forecast June 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Ernst & Young

Eurozone Ernst & Young Eurozone Forecast June 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Ernst & Young

Stagnation and Institutional Structures

Stagnation and Institutional Structures David M. Kotz University of Massachusetts Amherst Shanghai University of Finance and Economics Deepankar Basu University of Massachusetts Amherst September, 2017

Stagnation and Institutional Structures David M. Kotz University of Massachusetts Amherst Shanghai University of Finance and Economics Deepankar Basu University of Massachusetts Amherst September, 2017

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

Econ 102 Exam 2 Name ID Section Number

Econ 102 Exam 2 Name ID Section Number 1. In a closed economy government spending was $30 billion, consumption was $70 billion, taxes were $20 billion, and GDP was $110 billion this year. Investment spending

Econ 102 Exam 2 Name ID Section Number 1. In a closed economy government spending was $30 billion, consumption was $70 billion, taxes were $20 billion, and GDP was $110 billion this year. Investment spending

Macroeconomic Issues and Policy. Stabilization Policy. Time Lags Regarding Monetary and Fiscal Policy

C H A P T E R 15 Macroeconomic Issues and Policy Prepared by: Fernando Quijano and Yvonn Quijano Stabilization Policy Stabilization policy describes both monetary and fiscal policy, the goals of which

C H A P T E R 15 Macroeconomic Issues and Policy Prepared by: Fernando Quijano and Yvonn Quijano Stabilization Policy Stabilization policy describes both monetary and fiscal policy, the goals of which

Fiscal Policy What is Fiscal Policy? Classical View vs. Keynesian View: 1. Classical View: Keynesian View:

Fiscal Policy What is Fiscal Policy? Fiscal policy is the process of shaping government taxation and government spending so as to achieve certain objectives. According to Prof. Samuelson, by a positive

Fiscal Policy What is Fiscal Policy? Fiscal policy is the process of shaping government taxation and government spending so as to achieve certain objectives. According to Prof. Samuelson, by a positive