OVERVIEW PAYE 2010 NOVEMBER

|

|

|

- Kelley Baldwin

- 5 years ago

- Views:

Transcription

1 OVERVIEW PAYE 2010 NOVEMBER 1

2 Contents 1. Introduction The aim of the Pay-As-You-Earn (PAYE) reconciliation process What is reconciliation? The Pay-As-You-Earn (PAYE) process Completing and submitting your Monthly Employer Declaration (EMP201) The Statement of Account (EMPSA) Preparing your Reconciliation (EMP501), including Interim (Biannual) Reconciliation and Annual Reconciliation If you use a payroll system Completing and submitting your reconciliation (EMP501) Forms required to complete the reconciliation Using a payroll system Completing your declaration manually Submitting your declaration to SARS Issuing employee tax certificates to employees [IRP5s/IT3(a)s] What will SARS do once I have submitted my declaration? Common reconciliation issues My tax certificates do not match what I have paid SARS. This could be as a result of: Where there is a difference between the Monthly Employer Declarations (EMP201s) submitted and the EMP Common payment problems and how to resolve them Unallocated payments Underpayment due to interest and penalties Outstanding returns Resolving account inaccuracies relating to unallocated and incorrectly allocated payments Registering employees SARS communication Glossary of terms

3 1. Introduction Over the past three years, SARS has been modernising and simplifying tax processes in line with international best practice. Each year we work towards improving service standards, incorporating the latest technology and developments in tax standards. Our aim is to provide a straightforward, user-friendly process and solution. As part of this, SARS has made further changes to fine-tune the Paye-As-You-Earn (PAYE) process. We have introduced entirely new elements, including new fields. These changes are a vital part of SARS s long-term vision to have a more accurate reconciliation process. More information means a less cumbersome process, as returns are increasingly pre-populated. It also means a more efficient tax service, with faster turnaround times. This brochure will give the employer some insight into the PAYE process and your responsibility as an employer. Other detailed guides for the various steps of the PAYE process are available for download on For further information, please visit a SARS branch, call the SARS Contact Centre on SARS (7277) or visit 2. The aim of the Pay-As-You-Earn (PAYE) reconciliation process PAYE RECONCILIATION AIMS TO ANSWER TWO QUESTIONS WHY DO THESE QUESTIONS MATTER? 1 Have I matched my actual PAYE liabilities as declared on the EMP501 with all the IRP5s for the tax year? Have I accurately reflected the PAYE liabilities on the IRP5s? Have I made adjustments for all errors? 2 Is the employee data correct for accurate pre-population of tax returns? Have I accurately matched the liabilities to employee records? This will help you exclude liabilities or payments related to certificates issued in prior years. Identify and resolve any differences between liabilities declared on your EMP201s and actual liabilities based on IRP5s. Determine what is due to/by SARS for the tax year. Help you reconcile your IRP5s with the taxes withheld. Issue accurate IRP5s to your employees for tax year. Note: You will not be allowed to issue IRP5s to your employees if you are not reconciled for tax year. 3

4 3. What is reconciliation? RECONCILIATION IS WHICH MEANS A process to match taxes declared on monthly EMP201s with the actual liabilities based on the final IRP5s to be issued for the relevant year of assessment. You need to start by knowing what you have declared and what, with hindsight, you should have declared for the year of assessment. Ability to understand the difference (if any) between actual tax liabilities and payments made to SARS. You need to be able to match what you owe to the payments you have actually made. A process to match back your actual liabilities to funds withheld from your employees. You need to be able to work out how the total you have paid matches individual employee liabilities for their IRP5s. AND WHAT IS NOT RECONCILIATION? RECONCILIATION IS NOT WHICH MEANS Just a reflection of the payments and liabilities declared on your monthly EMP201 forms. A reconciliation can be correct even if the balance identifies that you owe money or have a credit for the tax year. Note: It is possible you may have overpaid for the year, but submitting a refund may require careful documentation for this and prior years. 4. The Pay-As-You-Earn (PAYE) process EMPLOYER S RESPONSIBILITY TIMEFRAMES WHAT YOU NEED TO DO The Monthly Employer Declaration (EMP201) Completing and submitting your Monthly Employer Declaration (EMP201) Each month s declaration must be submitted and paid on or before the 7th of each month. Should the 7th fall on a weekend or public holiday, the payment must be made on the last business day preceding the 7th of the month. Declare the total payment made for PAYE, SDL and UIF SARS now provides employers with a detailed Statement of Account (EMPSA) containing all Monthly Employer Declaration (EMP201) and PAYE (Employer Reconciliation Declaration [EMP501]) transactions The EMPSA is automatically issued for tax periods which fall in the current transaction year (March 2010 to February 2011 for this year). For a detailed explanation please read the corresponding section 4

5 EMPLOYER S RESPONSIBILITY TIMEFRAMES WHAT YOU NEED TO DO Completing and submitting the interim (biannual) PAYE reconciliation Preparing for the interim (biannual) PAYE reconciliation Completing and submitting your interim (biannual) reconciliation Issuing Employee Income Tax Certifi cates [IRP5/IT3(a)s] to employees 1 June to interim (biannual) submission period The interim (biannual) reconciliation is for the six month period from 1 March to 31 August. Collate employees demographic information as per the IRP5/IT3(a) requirements for that particular year Capture this information into your payroll system (where applicable) Gather all other information required, i.e. EMP201s, and payments in respect of the EMP201s, for the period March to August. For a detailed explanation please read the corresponding section 1 September to 29 October Ensure that you have the latest version of e@syfile Employer, which can be downloaded from Complete your Employer Reconciliation Declaration (including EMP501, IRP5/IT3(a) and EMP601) along with all employee tax certificates for the relevant transaction year and submit to SARS Copies of your submitted documents must be kept for five years. For a detailed explanation please read the corresponding section Only provide certificates to employees whose employment was terminated up to the closing of the biannual period (either due to resignation, death, immigration or an employer ceasing to be an employer) according to the current process and legislation. Completing and submitting the annual PAYE reconciliation (during Employers Tax Season) Preparing for the annual reconciliation (Employers Tax Season) March The annual reconciliation is for the twelve month period from 1 March of the current tax year to the end of February the following year Collate employees demographic information as per the IRP5/IT3(a) requirements for that particular year Capture this information into your payroll system (where applicable) Gather all other information required, i.e. EMP201s, and payments in respect of the EMP201s, for the period March to February the following year. For a detailed explanation please read the corresponding section Completing and submitting your Employer Reconciliation Declaration Issuing Employee Income Tax Certifi cates [IRP5/IT3(a)s] to employees 1 April to 31 May Ensure that you have the latest version of e@syfile Employer, which can be downloaded from Complete your Employer Reconciliation Declaration (including EMP501, IRP5/IT3(a) and EMP601) along with all employee tax certificates for the relevant transaction year and submit to SARS Copies of your submitted documents must be kept for five years. For a detailed explanation please read the corresponding section June or immediately after reconciling Issue employee tax certificates [IRP5s and IT3(a)s] to all employees For a detailed explanation please read the corresponding section 5

allocations. This is done by completing a Monthly Employer Declaration (EMP201), and submitting it to SARS together with the payment on or before the 7th of each month.")

SARS will provide employers with a detailed Statement of Account (EMPSA) containing all Monthly Employer Declaration (EMP201) and PAYE (Employer Reconciliation")

![Declaration [EMP501]) transactions. The EMPSA will be automatically issued for tax periods which fall in the current transaction year (March 2010 to February 2011) and onwards.](/docs-images/89/98892122/images/6-6.jpg "The EMPSA will contain a summary of all financial transactions for PAYE, SDL and UIF for the specific tax period(s).")

6 5. Completing and submitting your Monthly Employer Declaration (EMP201) Each month employers have to declare their total Pay-As-You-Earn (PAYE), Skills Development Levy (SDL) and Unemployment Insurance Fund (UIF) allocations. This is done by completing a Monthly Employer Declaration (EMP201), and submitting it to SARS together with the payment on or before the 7th of each month. Should the 7th fall on a weekend or public holiday, payment must be made on the last business day preceding the 7th of the month. A new EMP201 was introduced earlier this year, and must be used. If an old EMP201 form is used, it will be rejected. The new EMP201 is easily distinguishable: - It is a landscape format Adobe (PDF) form - A unique payment reference number (PRN) is pre-populated onto each form, and must be used when making payments to ensure that your payment is correctly allocated - There are two fields for employers to indicate any penalties and/or interest to be paid for the relevant period Specimen 1 Enter your reference number/s 2 Enter the declarant s particulars 3 Enter the payment allocation Employers have a legal obligation to submit their EMP201s and make the corresponding payment. In terms of the Income Tax Act 58 of 1962, employers are required to: - Deduct the correct amount of tax from employees - Pay those amounts to SARS, and - Declare such amounts paid to SARS on a Monthly Employer Declaration form (EMP201) 6. The Statement of Account (EMPSA) SARS will provide employers with a detailed Statement of Account (EMPSA) containing all Monthly Employer Declaration (EMP201) and PAYE (Employer Reconciliation Declaration [EMP501]) transactions. The EMPSA will be automatically issued for tax periods which fall in the current transaction year (March 2010 to February 2011) and onwards. The EMPSA will contain a summary of all financial transactions for PAYE, SDL and UIF for the specific tax period(s). The EMPSA will empower the employer by giving him/her the tools needed to ensure that his/her SARS account is in good standing, and will ensure transparency. Where previously employers received three separate statements, the EMPSA will combine these statements to give employers a broader view of their PAYE, SDL and UIF transactions. Transaction discrepancies will also be highlighted to enable employers to manage their accounts effectively. 6

7 Employers registered on efiling and Employer will receive an EMPSA monthly whilst employers who file their EMP201 and PAYE returns manually will receive an EMPSA by post quarterly. For the 2008 and onward transaction years, the employer must request an EMPSA using efiling, Employer or by calling the SARS Contact Centre on SARS (7277). Requests pertaining to any transaction year/s must be made at a SARS branch. 7. Preparing your Reconciliation (EMP501), including Interim (Biannual) Reconciliation and Annual Reconciliation Employers are now required to submit interim (biannual) reconciliation declarations, a critical new element in setting the foundation for increasingly efficient processing of PAYE submissions. The interim (biannual) submission is a reconciliation for the six month period from 1 March to 31 August. The annual reconciliation is a reconciliation for the full twelve month period from 1 March to the end of February. These declarations must be submitted to SARS by the date the Commissioner for SARS, prescribes by notice in the Government Gazette. The interim (biannual) reconciliation process is exactly the same as the annual reconciliation declaration except that the declaration and employee Income Tax certificates are in respect of six months only. The submission can be made either electronically or manually. While SARS relaxed the requirement for employers to complete the new fields during the April/May 2010 PAYE reconciliation, employers are now required to complete these additional mandatory fields and validate the data files submitted to SARS. You will need all your EMP201s in order to: Declare and correct your liability (the amounts owing to SARS for PAYE, SDL and UIF) for each month Calculate the actual payments made in respect of your tax liabilities for each month Separate any liabilities, payments and/or employer tax certificates which do not relate to this reconciliation. Reconciliation involves matching all tax due (liabilities) with all tax paid and checking these against the total value of all tax certificates created. The reconciliation process only relates to tax paid and not additional tax, not penalties and not interest. Reconcile the sum of your monthly declarations against the sum of the taxable portion on your employee tax certificates by adding the totals of each monthly declaration, and also adding the total tax of each employee tax certificate. Compare both these amounts with the actual tax paid. These three amounts should all be equal. If they are not, the employer will be able to rectify the amounts, update the amounts so that they balance or make payment for the shortfall. Note: The EMP201 information for the interim biannual reconciliation will be for the six month period March to August. The annual reconciliation will be for the twelve month period March to February. 7.1 If you use a payroll system Ensure that all the necessary information as per the prescribed format has been captured in your payroll system. Your payroll system will generate a CSV file containing all the IRP5/IT3(a) information. Note: SARS will no longer accept CSV files generated using a payroll system employers must import their CSV file into e@syfile Employer for submission to SARS. 7.2 Completing and submitting your reconciliation (EMP501) Reconciliation documents [EMP501, IRP5/IT3(a), EMP601 and EMP701] are available from all SARS branches. A major development in the reconciliation process over the past three years was the introduction of a free software application, e@syfile Employer, to reduce turnaround times and errors. e@syfile Employer ultimately provides a simpler, more convenient process for both employers and SARS, and also offers all the reconciliation documents in one convenient software package. The latest version of e@syfile Employer can be downloaded from at any time. Note: Please ensure that you have the latest version of e@syfile Employer everytime you want to make a submission to SARS. Any submission done using previous versions of e@syfile Employer will not be accepted. 7

Specimen Specimen")

")

")

8 7.2.1 Forms required to complete the reconciliation Employee Tax Certificate (IRP5/IT3a) Specimen Specimen Employers must complete and submit Income Tax certificates to SARS. For the interim (biannual) reconciliation the tax certificates must not be issued to employees as they are for SARS s administrative purposes only. However, the relevant certificate must be provided to employees whose employment was terminated prior to the closing of the biannual period (either due to resignation, death, immigration or an employer ceasing to be an employer) according to the current process and legislation. For the annual reconciliation the final tax certificates for the full tax year must be given to employees. 8

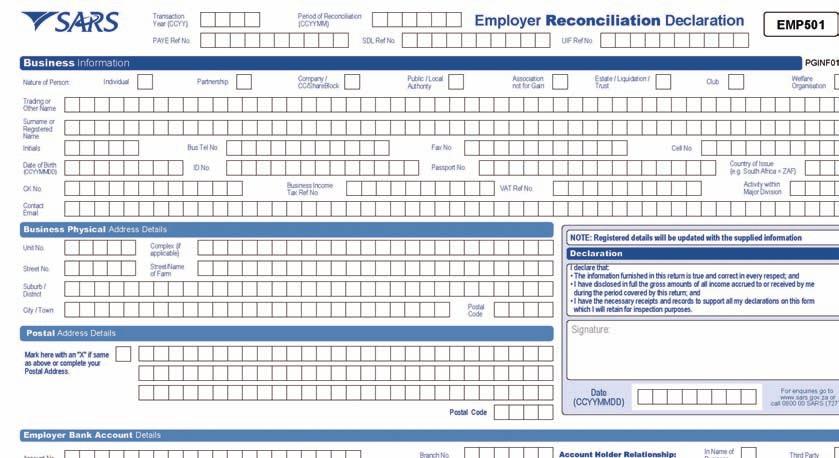

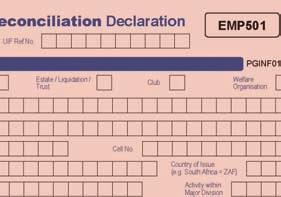

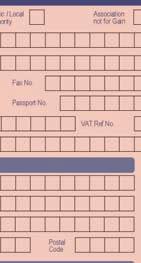

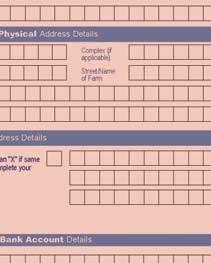

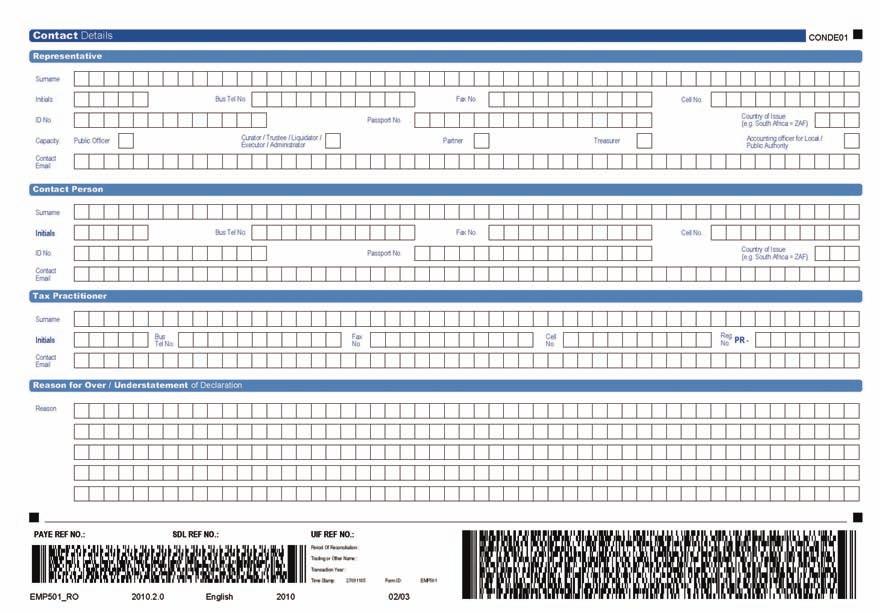

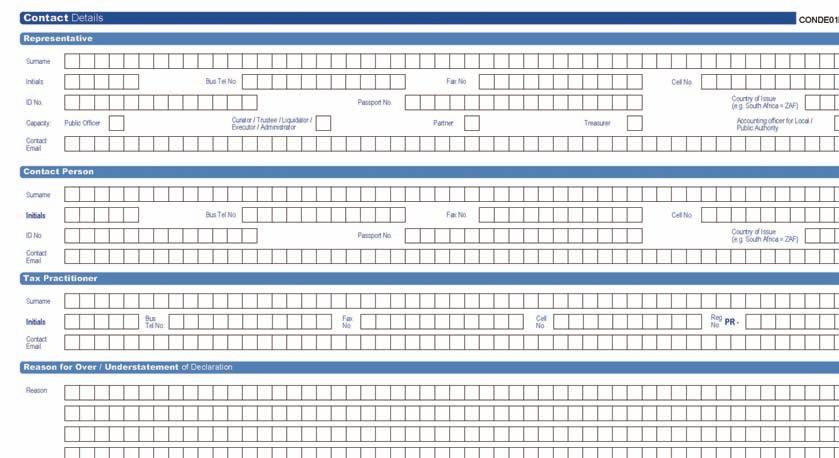

9 The Employer Reconciliation Declaration (EMP501) Specimen 1 Enter business information 8 Sign and submit the declaration Specimen 2 Enter all relevant contact detail information 3 Enter a reason in the case of over/ understatement of declaration 9

")

reconciliations to declare: The actual monthly")

Total SDL and UIF liability (if registered/liable for these tax types) The actual employees tax,")

value of the IRP5 tax certificates The amount due by/to the employer.")

10 4 Enter your revised monthly liability 5 Enter the revised amounts (excluding payments in respect of other years of assessment, penalties and interest Specimen 6 Calculate the actual IRP5 tax liability for the transaction year: Import payroll fi les Enter manual certifi cates 7 Calculate amount due to/by SARS. This does not have to equal to zero The EMP501 is an integral part of the annual and interim (biannual) reconciliation. The employer uses the form for annual and interim (biannual) reconciliations to declare: The actual monthly liabilities Total employees tax liability The actual monthly SDL and UIF liabilities (if registered/liable for these tax types) Total SDL and UIF liability (if registered/liable for these tax types) The actual employees tax, SDL and UIF payments made to SARS (excluding any penalties or interest payments) The total employees tax (SITE and PAYE) value of the IRP5 tax certificates The amount due by/to the employer. Once the employer has completed the declaration, he/she must sign it and submit it to SARS together with the other reconciliation documents. If e@syfile Employer is used and the user opts to submit electronically no manual documentation is submitted to SARS. Remember to complete the now mandatory employer demographic information on your EMP501 and the demographic and financial information related to your IRP5/IT3(a)s. 10

s that have already")

")

11 The Tax Certificate Cancellation Declaration (EMP601) Specimen The EMP601 must be completed if the employer needs to cancel any IRP5/IT3(a)s that have already been submitted to SARS. The Reconciliation Declaration Adjustment (EMP701) Specimen Complete an EMP701 if you need to make adjustments to PAYE declarations and payments in respect of an annual reconciliation declaration for a prior transaction year. The EMP701 is only used for the annual reconciliation change required. This form is not used for the interim (biannual) reconciliation. You will also need to submit the respective IRP5/IT3(a) certificates which you wish to amend or add, and an EMP601 if you wish to delete a certificate for the change to this particular reconciliation submission. 11

s] which is generated using your payroll system.")

12 7.2.2 Using a payroll system Import your PAYE CSV files into e@syfile Employer. A PAYE CSV file is electronic data of your employee tax certificates [IRP5/IT3(a)s] which is generated using your payroll system. Reconcile your liabilities against employee tax certificates for the year. You will need your employer monthly declarations (EMP201s) to calculate the actual payments made in respect of the liabilities. For the interim biannual reconciliation the information is required for the six month period March to August. For the annual reconciliation the information is required for the twelve month period March to February. Note: SARS will no longer accept CSV files generated using a payroll system employers must import their CSV file into e@syfile Employer for submission to SARS Completing your declaration manually Follow the steps above using the manual documents which are available at all SARS branches. The manual certificates with the signed EMP501/EMP701, and where applicable an EMP601, must be submitted to SARS. The EMP701 can only be used to change an annual reconciliation declaration of a prior year. Note: Employers making use of manual certificates may only issue these to employees once SARS is satisfied that the reconciliation has been completed correctly for the annual reconciliation. For the interim (biannual) reconciliation the tax certificates must not be issued to employees as they are for SARS s administrative purposes only. However, the relevant certificate must be provided to employees whose employment was terminated prior to the closing of the biannual period (either due to resignation, death, immigration or an employer ceasing to be an employer) according to the current process and legislation Submitting your declaration to SARS You have the following submission methods available to you: For e@syfile Employer submissions (ZIP file format): Making electronic-only submissions: Using e@syfile Employer, you can make your submission electronically via efiling Completing your submission electronically and submitting it manually: if you are submitting your reconciliation on disk to a SARS branch, you must include signed hardcopies of the EMP501, and, if applicable, an EMP601 and EMP701. For manual submissions: Submitting manual documents only: You will need to submit signed hardcopies of all your reconciliation documents to your nearest SARS branch. Note: Don t leave your submission to the last minute. If there are any problems you will need time to sort them out Issuing employee tax certificates to employees [IRP5s/IT3(a)s] Interim (biannual) tax certificates must not be issued to employees as they are for SARS s administrative purposes only. However, the relevant certificate must be provided to employees whose employment was terminated prior to the closing of the biannual period. This must be done within 14 days of such termination. Tax certificates submitted for the interim (biannual) reconciliation will differ from the certificates submitted annually in the following ways: Interim (biannual) tax certificates will only be issued to SARS and must not be issued to employees Interim (biannual) tax certificates will reflect information on income and deductions for a maximum period of six months Employees tax may be reflected against code 4102 (PAYE). The total amount does not have to be split into SITE(4101) and PAYE (4102) 12

13 For employees whose employment was terminated up to the closing of the interim (biannual) period for instance due to resignation, death, immigration or where the employer ceased to be an employer: The tax certificate must reflect financial information for the period actually employed Where there were deductions in respect of employees tax, it must be split and reflected against code 4101(SITE) and 4102 (PAYE). The calendar month in the tax certifi cate number (code 3010) must be specified as 02 to indicate that this is a final tax certificate. The same certificate should be submitted to SARS at the end of the tax year as part of the final submission. For the annual reconciliation e@syfile Employer automatically generates an Adobe PDF version of all Tax certificates. After the annual reconciliation for the full tax year, employers must issue the final Income Tax certificates to employees. When creating their submission, employers have the option of storing the PDF certificates created as part of their reconciliation. 8. What will SARS do once I have submitted my declaration? If you do submit, SARS will check for discrepancies in your declaration, such as: o Whether or not there is a significant difference in the liability you declared and the actual liability you owe o If the funds declared were not actually paid to SARS If you owe SARS you will need to settle the amount If there are no discrepancies in the submission, SARS will accept it and employees will begin receiving (upon request) pre-populated tax returns (after the annual reconciliation and in time for Personal Income Tax Season) If you do not submit your declarations, your employees will not receive a pre-populated tax return for Personal Income Tax Season. 9. Common reconciliation issues 9.1. My tax certificates do not match my total liabilities. This could be as a result of: Not all IRP5s are included with reconciliation IRP5 s are included of which liability is declared in a previous year Liabilities are not accurately reflected Prior year liabilities are declared in a month of the current transaction year Rounding errors You have not recovered employee taxes from your employees Where there is a difference between the Monthly Employer Declarations (EMP201s) submitted and the EMP501 The fi ling of your Monthly Employer Declarations (EMP201s) is a critical element in the reconciliation. The EMP201s are like tiny building blocks underlying the reconciliation. If there are any errors in your EMP201s, it will affect the reconciliation. See section 10 Common payment problems and how to resolve them for more information. Note: This is not an exhaustive list, just a summary of the most common items. 13

14 10. Common payment problems and how to resolve them 10.1 Unallocated payments An unallocated payment is any payment (or portion thereof) that could not be assigned to a specific Monthly Employer Declaration (EMP201). This would occur in instances where the employer paid more than the value of the EMP201, did not file their return, or did not specify the correct payment reference number (PRN) when making payment. These payments will not be taken into consideration when calculating penalties and interest, and when performing the annual (Employer Reconciliation Declaration [EMP501] reconciliation. This could result in compliance actions being initiated against the employer. It is therefore critical that these payments are followed up and correctly assigned by employers Underpayment due to interest and penalties Where interest and penalties are charged due to a late payment the payment will first be offset against these charges before being assigned to any tax declared on the Monthly Employer Declaration (EMP201). Most employers do not increase their payments to take account of this and as a result an underpayment occurs for the particular tax period which will continue to accrue interest until it is settled. If these additional charges have been correctly imposed, the employer is required to make an additional payment using the EMP201 payment reference number (PRN) to ensure that the payment is correctly allocated. The employer could face penalties and interest if the payment is not made Outstanding returns If no Monthly Employer Declaration (EMP201) is filed the accompanying payment cannot be allocated. Ensure that the correct EMP201 is submitted and the relevant payment using the correct Payment Reference Number is made timeously Resolving account inaccuracies relating to unallocated and incorrectly allocated payments An online function has been provided on e@syfile Employer and efiling for employers to rectify unallocated payments. This function will also provide employers with a means to request SARS to change allocations that have been incorrectly performed. Employers not registered for e@syfile Employer or efiling may visit the nearest SARS branch for assistance. For a detailed guide, please visit Employers may either allocate a payment themselves by indicating the specific Monthly Employer Declaration (EMP201) to which the payment should be assigned (by specifying the appropriate PRN) or by requesting that SARS allocates the payment to any outstanding balances reflected on the EMPSA (see section 3.1 The Statement of Account (EMPSA) above). This is referred to as a payment on account and is specified by using as the last eight digits on the payment reference (PRN). SARS will allocate the payment according to SARS payment allocation rules. Note: This is not an exhaustive list, just a summary of the most common items. For more information regarding SARS payment rules please go to and select I want to make a payment to view the SARS payment rules. 11. Registering employees Employers can now use e@syfile Employer or efiling to register new employees for Income Tax. Please refer to the e@syfile Employer User Guide for more information on the ITREG specifications. Once an employee s demographic information has been validated, and the employer has submitted the reconciliation, the employee will be registered for Income Tax. Both the employer and employee will be informed of the Income Tax number. Where the application is unsuccessful, the reason for failure of the registration will be communicated to the employer. 12. SARS communication All communication SARS issues for the employer s attention on efiling is also issued through the e@syfile Employer channel, helping employers keep abreast of any changes or matters of interest which affect them. SARS also communicates regularly with employers by post, through advertising and the media. 14

15 13. Glossary of terms Term CSV file EMP201 EMP301 EMP501 EMP601 EMP701 EMPSA IRP5/IT3a ITREG certificate PAYE SDL SITE Tax liability UIF Description Electronic data of your employee tax certificates [IRP5/IT3(a)s] which is generated using your payroll system The Monthly Employer Declaration Underpayment on Account letter Employer Reconciliation Declaration Tax Certificate Cancellation Declaration Reconciliation Declaration Adjustment Statement of Account Employee Tax Certificate Income Tax Registration certificate Pay-As-You-Earn Skills-Development-Levy Standard Income Tax on Employees Amount of tax withheld from the employees, which is owed to SARS Unemployment Insurance Fund 15

16 16 Lehae la SARS 299 Bronkhorst Street Nieuw Muckleneuk Pretoria 0181 Private Bag X923 Pretoria 0001 Tel: Fax: Contact Centre: SARS (7277)

Overview of PAYE reconciliation process and 2007/08 policy changes. Another helpful guide brought to you by South African Revenue Service

Overview of PAYE reconciliation process and 2007/08 policy changes Another helpful guide brought to you by South African Revenue Service Overview of PAYE reconciliation process and 2007/08 policy changes

Overview of PAYE reconciliation process and 2007/08 policy changes Another helpful guide brought to you by South African Revenue Service Overview of PAYE reconciliation process and 2007/08 policy changes

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

FREQUENTLY ASKED QUESTIONS COMPLETION AND SUBMISSION OF CSV. TM EMPLOYER AND ZIPCENTRALFILE RECONCILIATION DOCUMENTS

FREQUENTLY ASKED QUESTIONS Revision: 1 Page 1 of 8 1 PURPOSE The purpose of this document is to provide answers to frequently asked questions by employers in respect of creating CSV data files and submitting

FREQUENTLY ASKED QUESTIONS Revision: 1 Page 1 of 8 1 PURPOSE The purpose of this document is to provide answers to frequently asked questions by employers in respect of creating CSV data files and submitting

A STEP-BY-STEP GUIDE TO THE EMPLOYER RECONCILIATION PROCESS

EF NO. Trading or Other Name: Transaction Year: Time Stamp: 21159840 A STEP-BY-STEP GUIDE TO THE EMPLOYE ECONCILIATION POCESS Transaction Year (CCYY) Period of econciliation (CCYYMM) Business Information

EF NO. Trading or Other Name: Transaction Year: Time Stamp: 21159840 A STEP-BY-STEP GUIDE TO THE EMPLOYE ECONCILIATION POCESS Transaction Year (CCYY) Period of econciliation (CCYYMM) Business Information

EXTERNAL GUIDE GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017

GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 BACKGROUND 3 3.1 RECONCILIATION PROCESS 3 3.2 INTERIM RECONCILIATION PROCESS 3 3.3 GENERAL

GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 BACKGROUND 3 3.1 RECONCILIATION PROCESS 3 3.2 INTERIM RECONCILIATION PROCESS 3 3.3 GENERAL

ITA88 PROCESS GUIDE ITA88 PROCESS GUIDE AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS

AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS SEPTEMBER 2010 _v2.indd 1 1 9/21/10 4:10 PM AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS Introduction ITA88 AGENT APPOINTMENT Who

AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS SEPTEMBER 2010 _v2.indd 1 1 9/21/10 4:10 PM AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS Introduction ITA88 AGENT APPOINTMENT Who

SAPA Conference Spier, Stellenbosch 04 August March

SAPA Conference Spier, Stellenbosch 04 August 2011 17 March INTRODUCTION PAYE processes and forms, over the past few years, have been aggressively modernised so as to ensure better alignment between PAYE

SAPA Conference Spier, Stellenbosch 04 August 2011 17 March INTRODUCTION PAYE processes and forms, over the past few years, have been aggressively modernised so as to ensure better alignment between PAYE

P U B L I C R E L E A S E

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

PUBLIC RELEASE. Document Classification: Official Publication. South African Revenue Service 2011

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published document SARS

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published document SARS

P U B L I C R E L E A S E

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2012 Page 1 of 55 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2012 Page 1 of 55 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

Quick Start Guide to Payroll Tax Year-End

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

efiling Account Management Guide - Payment Allocation

efiling Account Management Guide - Payment Allocation CONTENTS 1. How to obtain a payment listing... 1 2. How to allocate a payment... 3 3. How to re-allocate a payment... 6 4. How to request a payment

efiling Account Management Guide - Payment Allocation CONTENTS 1. How to obtain a payment listing... 1 2. How to allocate a payment... 3 3. How to re-allocate a payment... 6 4. How to request a payment

P U BLI C RELEAS E. Document Classification: Official Publication. South African Revenue Service

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

Employer Easy File Q & A

Employer Easy File Q & A Trouble Shooting Solutions Employer installed e@syfile Employer version 6.0.0 and having troubles login: Confirm if employer made a backup in version 5.0.9 If Yes, copy version

Employer Easy File Q & A Trouble Shooting Solutions Employer installed e@syfile Employer version 6.0.0 and having troubles login: Confirm if employer made a backup in version 5.0.9 If Yes, copy version

External Guide on how to submit a Request for Remission

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

PUBLIC RELEASE. Document Classification: Official Publication. South African Revenue Service 2009

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

P U BLI C RELEAS E. Document Classification: Official Publication. South African Revenue Service 2014

P U BLI C RELEAS E Document Classification: Official Publication South African Revenue Service 2014 04/2014 Page 1 of 112 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U BLI C RELEAS E Document Classification: Official Publication South African Revenue Service 2014 04/2014 Page 1 of 112 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

Tax year end processing

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

STEPS FOR GENERATING ITREG-FILE FOR AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for

sedert 1982 STEPS FOR GENERATING ITREG-FILE FOR e@syfile, AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for e@syfile. 1. Start your reconciliation process by generating the ITREG-file for e@syfile.

sedert 1982 STEPS FOR GENERATING ITREG-FILE FOR e@syfile, AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for e@syfile. 1. Start your reconciliation process by generating the ITREG-file for e@syfile.

Welcome to the SARS Tax Workshop

29 August 2017 Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more

29 August 2017 Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more

P U BLI C RELEAS E. Document Classification: Official Publication. South African Revenue Service

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

Welcome to the SARS Tax Workshop

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

From IRP5 to tax assessment 15 minutes CPD

From IRP5 to tax assessment 15 minutes CPD By ADV. CARIEN VAN DIJK IRP5s are somewhat like family: they can cause you a lot of headaches but you can t (and probably don t want to) live without them. This

From IRP5 to tax assessment 15 minutes CPD By ADV. CARIEN VAN DIJK IRP5s are somewhat like family: they can cause you a lot of headaches but you can t (and probably don t want to) live without them. This

Omission of source code 4582

Return Submission ETI Omission of source code 4582 With the implementation of the Retirement Reform requirements, information code 4582 and its value were omitted from the submission file created by e@syfile

Return Submission ETI Omission of source code 4582 With the implementation of the Retirement Reform requirements, information code 4582 and its value were omitted from the submission file created by e@syfile

Employment Tax Incentive (ETI)

") ETI 2017 Employment Tax Incentive (ETI) The ETI is an incentive aimed at encouraging employers to hire young work seekers. It was implemented with effect from 1 January 2014 The aim of this incentive was

ETI 2017 Employment Tax Incentive (ETI) The ETI is an incentive aimed at encouraging employers to hire young work seekers. It was implemented with effect from 1 January 2014 The aim of this incentive was

Source Codes. New Source Codes and Validations

Source Codes New Source Codes and Validations Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make

Source Codes New Source Codes and Validations Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make

Employment Tax Incentive Scheme

Employment Tax Incentive Scheme Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Employment Tax Incentive Scheme Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Ayanda Takela. SARS efiling and Specialist (Gauteng, Free State & Northern Cape Region)

") Ayanda Takela SARS efiling and e@syfile Specialist (Gauteng, Free State & Northern Cape Region) Topics to be discussed General errors experienced on SARS efiling profiles General errors experienced on

Ayanda Takela SARS efiling and e@syfile Specialist (Gauteng, Free State & Northern Cape Region) Topics to be discussed General errors experienced on SARS efiling profiles General errors experienced on

Employment Tax Incentive Scheme. 2014/12/09 Version

Employment Tax Incentive Scheme 1 Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Employment Tax Incentive Scheme 1 Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

A QUICK GUIDE TO DIVIDENDS TAX

A QUICK GUIDE TO DIVIDENDS TAX i A QUICK GUIDE TO DIVIDENDS TAX 1. INTRODUCTION TO DIVIDENDS TAX In 2007, the Minister of Finance announced that Secondary Tax on Companies (STC) would be replaced by Dividends

A QUICK GUIDE TO DIVIDENDS TAX i A QUICK GUIDE TO DIVIDENDS TAX 1. INTRODUCTION TO DIVIDENDS TAX In 2007, the Minister of Finance announced that Secondary Tax on Companies (STC) would be replaced by Dividends

EXTERNAL GUIDE. How to efile your Provisional Tax Return

1. Register For efiling You will need to register as an efiling user before you can file your provisional tax return electronically. To register, go to www.sarsefiling.co.za 1.1. Click on Register 1.2.

1. Register For efiling You will need to register as an efiling user before you can file your provisional tax return electronically. To register, go to www.sarsefiling.co.za 1.1. Click on Register 1.2.

Exception Report Guide. August 2018

Exception Report Guide August 2018 Quick Payroll Exception Error Guides We understand your day-to-day challenges; this is why we want to try to make your business life easier. We have prepared this guide

Exception Report Guide August 2018 Quick Payroll Exception Error Guides We understand your day-to-day challenges; this is why we want to try to make your business life easier. We have prepared this guide

SECTION 4: STATEMENT OF WORK EXPERIENCE

SECTION 4: STATEMENT OF WORK EXPERIENCE Curriculum Number: 331303001 Curriculum Title: Tax Technician Learner Details Name: ID Number: Employer Details Company Name: Address: Supervisor Name: Work Telephone:

SECTION 4: STATEMENT OF WORK EXPERIENCE Curriculum Number: 331303001 Curriculum Title: Tax Technician Learner Details Name: ID Number: Employer Details Company Name: Address: Supervisor Name: Work Telephone:

EXTERNAL GUIDE HOW TO SUBMIT AN OBJECTION OR APPEAL VIA EFILING

TABLE OF CONTENTS 1 PURPOSE 3 2 INTRODUCTION 3 3 LOGON TO THE EFILING WEBSITE 4 3.1 ACCESS THE REQUEST FOR OBJECTION OR APPEAL FORM AND ADMINISTRATIVE PENALTY ASSESSMENT NOTICE 4 3.2 DETAILED PROCEDURES

TABLE OF CONTENTS 1 PURPOSE 3 2 INTRODUCTION 3 3 LOGON TO THE EFILING WEBSITE 4 3.1 ACCESS THE REQUEST FOR OBJECTION OR APPEAL FORM AND ADMINISTRATIVE PENALTY ASSESSMENT NOTICE 4 3.2 DETAILED PROCEDURES

D-BIT Payroll. Tax Year End Guide - Preparation And Procedures For Tax Year End D-BIT SYSTEMS (Pty) Ltd D-BIT Systems (Pty) Ltd

Ltd D-BIT Systems (Pty) Ltd") D-BIT SYSTEMS (Pty) Ltd RegNo: 87/0332407 7 Boskruin Business Park Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 2156 South Africa D-BIT Payroll Tax Year End Guide - Preparation And Procedures

D-BIT SYSTEMS (Pty) Ltd RegNo: 87/0332407 7 Boskruin Business Park Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 2156 South Africa D-BIT Payroll Tax Year End Guide - Preparation And Procedures

Tax Guide for Micro Businesses 2010/11. Turnover Tax. for Small Businesses. Tax Guide For Micro Businesses 2010/11 - Page 1

Tax Guide for Micro Businesses 2010/11 Turnover Tax for Small Businesses Tax Guide For Micro Businesses 2010/11 - Page 1 TT Comprehensive Guide.indd 1 TAX GUIDE FOR MICRO BUSINESSES 2010/11 The guide contains

Tax Guide for Micro Businesses 2010/11 Turnover Tax for Small Businesses Tax Guide For Micro Businesses 2010/11 - Page 1 TT Comprehensive Guide.indd 1 TAX GUIDE FOR MICRO BUSINESSES 2010/11 The guide contains

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

GREATSOFT CRM CLIENT RELEASE NOTES

GREATSOFT CRM 2016.1.0 CLIENT RELEASE NOTES CONTENTS INTRODUCTION...1 Prerequisites...1 CRM...2 Tasks...2 Billings...2 Disbursements...2 TAX...2 ITR12 Changes for 2016...2 Other ITR12 Changes... 15 ITR14

GREATSOFT CRM 2016.1.0 CLIENT RELEASE NOTES CONTENTS INTRODUCTION...1 Prerequisites...1 CRM...2 Tasks...2 Billings...2 Disbursements...2 TAX...2 ITR12 Changes for 2016...2 Other ITR12 Changes... 15 ITR14

Points of Discussion

Provisional Tax Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

Provisional Tax Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

Individual Income Tax

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

WHAT TO DO WITH YOUR IRP YEAR OF ASSESSMENT

WHAT TO DO WITH YOUR IRP5 2014 YEAR OF ASSESSMENT Office staff must take into account the undermentioned on receipt of their IRP5 tax certificates for the 2014 tax year ended 28 February 2014. Contact

WHAT TO DO WITH YOUR IRP5 2014 YEAR OF ASSESSMENT Office staff must take into account the undermentioned on receipt of their IRP5 tax certificates for the 2014 tax year ended 28 February 2014. Contact

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON ACCOMMODATION

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY Foreword This document is a general guide dealing with the PAYE responsibility

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY Foreword This document is a general guide dealing with the PAYE responsibility

EXTERNAL FREQUENTLY ASKED QUESTIONS DISPUTE ADMINISTRATION

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained 1 To Mr. Anil Naidoo

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained To Mr. Anil Naidoo From Tax Manager Subject Tax implications of issues discussed Date 4 December 207 Sub Total Scope We refer to our

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained To Mr. Anil Naidoo From Tax Manager Subject Tax implications of issues discussed Date 4 December 207 Sub Total Scope We refer to our

MINUTES OF THE STATEMENT OF ACCOUNTS DISCUSSION WITH THE OFFICE OF THE TAX OMBUD HELD ON 6 NOVEMBER 2017 AT 87 FRIKKIE DE BEER STREET, MENLYN.

MINUTES OF THE STATEMENT OF ACCOUNTS DISCUSSION WITH THE OFFICE OF THE TAX OMBUD HELD ON 6 NOVEMBER 2017 AT 87 FRIKKIE DE BEER STREET, MENLYN. ATTENDEES: Eric Mkhawane Gert van Heerden Talitha Maude Sibusiso

MINUTES OF THE STATEMENT OF ACCOUNTS DISCUSSION WITH THE OFFICE OF THE TAX OMBUD HELD ON 6 NOVEMBER 2017 AT 87 FRIKKIE DE BEER STREET, MENLYN. ATTENDEES: Eric Mkhawane Gert van Heerden Talitha Maude Sibusiso

Points Of Discussion

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

The Easy2Understand Tax Guidebook for SMEs

The Easy2Understand Tax Guidebook for SMEs TABLE of contents Introduction OnE: Types of Tax as they relate to SMEs What is VAT? What is PAYE, UIF, SDL? What is Dividends Tax? What is Customs and Excise?

The Easy2Understand Tax Guidebook for SMEs TABLE of contents Introduction OnE: Types of Tax as they relate to SMEs What is VAT? What is PAYE, UIF, SDL? What is Dividends Tax? What is Customs and Excise?

The Use of Advanced Analytics in Tax Administrations Dublin, Ireland

The Use of Advanced Analytics in Tax Administrations Dublin, Ireland SARS Modernization Program: Improved Organizational Performance and Value Delivery Randall Carolissen (PhD) Group Executive Revenue

The Use of Advanced Analytics in Tax Administrations Dublin, Ireland SARS Modernization Program: Improved Organizational Performance and Value Delivery Randall Carolissen (PhD) Group Executive Revenue

REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER 0 Initial Release A Scheepers GM Operational Services

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

Tax and ETI Amendments 2017/2018

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Nombasa Langeni (Nombasa.Langeni@treasury.gov.za)

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Nombasa Langeni (Nombasa.Langeni@treasury.gov.za)

Tax, ETI and UIF Amendments 2018/2019

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

TAX GUIDE FOR MICRO BUSINESSES 2011/12

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

A person that elected to be registered as above must be registered by the Commissioner with effect from the beginning of that year of assessment.

6.1 WHO QUALIFIES TO REGISTER FOR TURNOVER TAX? A person that qualifies as a micro business may register for TT, if it is a: Natural person (or the deceased or insolvent estate of a natural person is registered

6.1 WHO QUALIFIES TO REGISTER FOR TURNOVER TAX? A person that qualifies as a micro business may register for TT, if it is a: Natural person (or the deceased or insolvent estate of a natural person is registered

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

Individual Tax Module. July 2015 Release Notes

Individual Tax Module July 2015 Release Notes What s new in the Individual Tax Module? July 2015 release 2014/2015 tax year What s new in this release? The Individual Tax Module (ITM) has been updated

Individual Tax Module July 2015 Release Notes What s new in the Individual Tax Module? July 2015 release 2014/2015 tax year What s new in this release? The Individual Tax Module (ITM) has been updated

FAQs: Increase in the VAT rate from 1 April 2018 Value-Added Tax

Value-Added Tax Frequently Asked Questions: Increase in the VAT rate 1 In the Minister s Budget speech on 21 February 2018, an increase in the standard rate of VAT was announced. The rate increase applies

Value-Added Tax Frequently Asked Questions: Increase in the VAT rate 1 In the Minister s Budget speech on 21 February 2018, an increase in the standard rate of VAT was announced. The rate increase applies

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

What s new at SARS? VAT COMPLIANCE

This image cannot currently be displayed. This image cannot currently be displayed. 2015/11/11 What s new at SARS? VAT COMPLIANCE 1 This image cannot currently be displayed. This image cannot currently

This image cannot currently be displayed. This image cannot currently be displayed. 2015/11/11 What s new at SARS? VAT COMPLIANCE 1 This image cannot currently be displayed. This image cannot currently

EXTERNAL REFERENCE GUIDE SECURITIES TRANSFER TAX. EXTERNAL GUIDE - SECURITIES TRANSFER TAX GEN-PAYM-11-G01 Revision: 3 EFFECTIVE DATE:

2013 EXTERNAL REFERENCE GUIDE SECURITIES EXTERNAL GUIDE - SECURITIES Revision: 3 EFFECTIVE DATE: 2013.11.30 DISCLAIMER The information contained in this guide is intended as guidance only and is not considered

2013 EXTERNAL REFERENCE GUIDE SECURITIES EXTERNAL GUIDE - SECURITIES Revision: 3 EFFECTIVE DATE: 2013.11.30 DISCLAIMER The information contained in this guide is intended as guidance only and is not considered

FAQs: Increase in the VAT rate from 1 April Value-Added Tax. Frequently Asked Questions Increase in the VAT rate

Value-Added Tax Frequently Asked Questions Increase in the VAT rate 1 In the Minister s Budget speech on 21 February 2018, an increase in the standard rate of VAT was announced. The rate increase applies

Value-Added Tax Frequently Asked Questions Increase in the VAT rate 1 In the Minister s Budget speech on 21 February 2018, an increase in the standard rate of VAT was announced. The rate increase applies

TCS (Tax Clearance Status) November 2018

November 2018") TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

EXTERNAL GUIDE HOW TO COMPLETE THE REGISTRATION, AMENDMENTS AND VERIFICATION FORM (RAV01)

") REGISTRATION, AMENDMENTS TABLE OF CONTENTS 1 2 3 INTRODUCTION 3 INDIVIDUAL 4 REGISTERED REPRESENTATIVE 4 4 TAX PRACTITIONER 4 5 SARS REGISTERED DETAILS 5 6 ACTIVATE REGISTERED USER Tax Practitioner and

REGISTRATION, AMENDMENTS TABLE OF CONTENTS 1 2 3 INTRODUCTION 3 INDIVIDUAL 4 REGISTERED REPRESENTATIVE 4 4 TAX PRACTITIONER 4 5 SARS REGISTERED DETAILS 5 6 ACTIVATE REGISTERED USER Tax Practitioner and

Mirror Payroll. Guidelines for End-Feb 2016 and March 2016 Retirement Reforms. Version 3.0. February 2016

Mirror Payroll Guidelines for End-Feb 2016 and March 2016 Retirement Reforms. Version 3.0 February 2016 1 Contents Introduction... 2 Legislation up to Feb 2016... 3 Mirror Payroll end-feb procedures...

Mirror Payroll Guidelines for End-Feb 2016 and March 2016 Retirement Reforms. Version 3.0 February 2016 1 Contents Introduction... 2 Legislation up to Feb 2016... 3 Mirror Payroll end-feb procedures...

LMC Express (Pty) Ltd

Ltd") LMC Express (Pty) Ltd (Registration number: 1997/012971/07) Manual in terms of section 51 of the Promotion of Access to Information Act, 2 of 2000 Promotion of Access to Information Act, 2 of 2000 (The

LMC Express (Pty) Ltd (Registration number: 1997/012971/07) Manual in terms of section 51 of the Promotion of Access to Information Act, 2 of 2000 Promotion of Access to Information Act, 2 of 2000 (The

2017 Ohio IT 1040ES, Voucher 1 Due April 18, Electronic Payment Available

2017 Ohio IT 1040ES, Voucher 1 Due April 18, 2017 Electronic Available Cut on the dotted lines. DO NOT USE PENCIL to complete this form. (Voucher 1) Due April 18, 2017 0 0 2017 Ohio IT 1040ES, Voucher

2017 Ohio IT 1040ES, Voucher 1 Due April 18, 2017 Electronic Available Cut on the dotted lines. DO NOT USE PENCIL to complete this form. (Voucher 1) Due April 18, 2017 0 0 2017 Ohio IT 1040ES, Voucher

PAYE Reporting Released November 2016

PYE Reporting Released November 2016 Introduction The Government is modernising New Zealand s tax system to make it simpler and more certain for New Zealanders. Improving the administration of PYE is an

PYE Reporting Released November 2016 Introduction The Government is modernising New Zealand s tax system to make it simpler and more certain for New Zealanders. Improving the administration of PYE is an

The ABC. of Capital Gains Tax for Companies

The ABC of Capital Gains Tax for Companies The ABC of Capital Gains Tax for Companies FOREWORD This guide deals with some of the basic principles of Capital Gains Tax (CGT) in order to contribute to a

The ABC of Capital Gains Tax for Companies The ABC of Capital Gains Tax for Companies FOREWORD This guide deals with some of the basic principles of Capital Gains Tax (CGT) in order to contribute to a

Global Mobility Services: Taxation of International Assignees - Swaziland

www.pwc.com/sz/en Global Mobility Services: Taxation of International Assignees - Swaziland People and Organisation Global Mobility Country Guide (Folio) Last Updated: June 2018 This document was not intended

www.pwc.com/sz/en Global Mobility Services: Taxation of International Assignees - Swaziland People and Organisation Global Mobility Country Guide (Folio) Last Updated: June 2018 This document was not intended

VDP applications. August 2015

VDP applications August 2015 Overview for this webinar VDP Relief offered under the VDP; Overview of the VDP process; When VDP is not available: Pending or current audit/investigation Requirements for

VDP applications August 2015 Overview for this webinar VDP Relief offered under the VDP; Overview of the VDP process; When VDP is not available: Pending or current audit/investigation Requirements for

TAX GUIDE FOR SMALL BUSINESSES 2013/14

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

SARS approach to Government institutions

SARS approach to Government institutions 1. SARS focusses on the Tax Compliance of Government Institutions at a National, Provincial and Local Level. 2. SARS Risks that we focus are: Correct Registration,

SARS approach to Government institutions 1. SARS focusses on the Tax Compliance of Government Institutions at a National, Provincial and Local Level. 2. SARS Risks that we focus are: Correct Registration,

2016/17 GUIDE TO... Self Assessment. Chartered Accountants Registered Auditors FOR ELECTRONIC USE ONLY

2016/17 GUIDE TO... Self Assessment Chartered Accountants Registered Auditors 020 8731 0777 www.cohenarnold.com FOR ELECTRONIC USE ONLY YOUR GUIDE TO Self Assessment It is a fundamental part of the self

2016/17 GUIDE TO... Self Assessment Chartered Accountants Registered Auditors 020 8731 0777 www.cohenarnold.com FOR ELECTRONIC USE ONLY YOUR GUIDE TO Self Assessment It is a fundamental part of the self

7.1 Introduction Web services (pspp.pensionsbc.ca) Payroll reporting Preparing your payroll report Non-payroll reports 22

Payroll reporting Preparing your payroll report Non-payroll reports 22") Section Contents 7 Reporting 7.1 Introduction 3 7.2 Web services (pspp.pensionsbc.ca) 3 7.2.1 Resources available on the Employer Reporting home page 4 7.3 Payroll reporting 6 7.3.1 Pensionable salary

Section Contents 7 Reporting 7.1 Introduction 3 7.2 Web services (pspp.pensionsbc.ca) 3 7.2.1 Resources available on the Employer Reporting home page 4 7.3 Payroll reporting 6 7.3.1 Pensionable salary

Disclaimer. Copyright notice

Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material) are based on the views and/or opinions of

Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material) are based on the views and/or opinions of

EXTERNAL GUIDE COMPREHENSIVE GUIDE TO THE ITR12T RETURN FOR TRUSTS

THE ITR12T RETURN FOR TABLE OF CONTENTS 1 INTRODUCTION... 6 2 GENERAL INFORMATION... 6 2.1 WHO MUST COMPLETE AND SUBMIT THE IT12T... 6 2.2 HOW TO OBTAIN A RETURN... 7 2.3 HOW TO SUBMIT A RETURN... 8 2.4

THE ITR12T RETURN FOR TABLE OF CONTENTS 1 INTRODUCTION... 6 2 GENERAL INFORMATION... 6 2.1 WHO MUST COMPLETE AND SUBMIT THE IT12T... 6 2.2 HOW TO OBTAIN A RETURN... 7 2.3 HOW TO SUBMIT A RETURN... 8 2.4

Global Mobility Services: Taxation of International Assignees - Malawi

www.pwc.com/mw/en Global Mobility Services: Taxation of International Assignees - Malawi Taxation issues & related matters for employers & employees 2017/18 Last Updated: June 2018 This document was not

www.pwc.com/mw/en Global Mobility Services: Taxation of International Assignees - Malawi Taxation issues & related matters for employers & employees 2017/18 Last Updated: June 2018 This document was not

Services, Duties and Responsibilities

Table of Contents Accounting... 3 Powerprop... 3 Bank Account... 3 Levies... 3 Payables... 3 Reporting... 4 Budgets... 4 Audit... 4 Insufficient Funds... 4 Credit Control and Arrears... 5 Employees of

Table of Contents Accounting... 3 Powerprop... 3 Bank Account... 3 Levies... 3 Payables... 3 Reporting... 4 Budgets... 4 Audit... 4 Insufficient Funds... 4 Credit Control and Arrears... 5 Employees of

UNPACKING PROVISIONAL TAX PROCESSES 2016

UNPACKING PROVISIONAL TAX PROCESSES 2016 Prepared by Mark Silberman B.Acc C.A.(S.A.) Copyright Accfin Software Page 1 Contents 1. LAWS - THE CHANGING PROVISIONAL TAX PROCESSES... 5 A. Introduction... 5

UNPACKING PROVISIONAL TAX PROCESSES 2016 Prepared by Mark Silberman B.Acc C.A.(S.A.) Copyright Accfin Software Page 1 Contents 1. LAWS - THE CHANGING PROVISIONAL TAX PROCESSES... 5 A. Introduction... 5

February Dividends Tax Information Guide

February 2012 Dividends Tax Information Guide Contents 1. Purpose of this Information Guide ---------------------------------------------------------- 4 2. Background --------------------------------------------------------------------------------------

February 2012 Dividends Tax Information Guide Contents 1. Purpose of this Information Guide ---------------------------------------------------------- 4 2. Background --------------------------------------------------------------------------------------

Welcome to the SARS Tax Workshop IT14 SD

Welcome to the SARS Tax Workshop IT14 SD The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more

Welcome to the SARS Tax Workshop IT14 SD The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more

Paid Parental Leave scheme Employer Toolkit

Paid Parental Leave scheme Employer Toolkit humanservices.gov.au Contents 1. What we mean by table of terms and definitions 3 2. The Paid Parental Leave scheme in summary 4 2.1 What it is 4 2.2 Why we

Paid Parental Leave scheme Employer Toolkit humanservices.gov.au Contents 1. What we mean by table of terms and definitions 3 2. The Paid Parental Leave scheme in summary 4 2.1 What it is 4 2.2 Why we

INTERCODE PAYROLL V5.0.0 RELEASE NOTES

INTERCODE PAYROLL V5.0.0 RELEASE NOTES BEFORE INSTALLING THE UPDATE It is recommended that you make backup copies of all your existing employer files before you install any updates to Intercode Payroll.

INTERCODE PAYROLL V5.0.0 RELEASE NOTES BEFORE INSTALLING THE UPDATE It is recommended that you make backup copies of all your existing employer files before you install any updates to Intercode Payroll.

PAYE error correction and adjustment anonymised summary of feedback

PAYE error correction and adjustment anonymised summary of feedback Introduction A Government discussion document Making Tax Simpler Better administration of PAYE and GST was released in late 2015. It

PAYE error correction and adjustment anonymised summary of feedback Introduction A Government discussion document Making Tax Simpler Better administration of PAYE and GST was released in late 2015. It

Impact Summary: Modernising the correction of errors in PAYE information

Impact Summary: Modernising the correction of errors in PAYE information Section 1: General information Purpose Inland Revenue is solely responsible for the analysis and advice set out in this Impact Summary,

Impact Summary: Modernising the correction of errors in PAYE information Section 1: General information Purpose Inland Revenue is solely responsible for the analysis and advice set out in this Impact Summary,

Paid Parental Leave scheme Employer Toolkit

Paid Parental Leave scheme Employer Toolkit humanservices.gov.au Contents 1. What we mean by table of terms and definitions 3 2. The Paid Parental Leave scheme in summary 4 2.1 What it is 4 2.2 Why we

Paid Parental Leave scheme Employer Toolkit humanservices.gov.au Contents 1. What we mean by table of terms and definitions 3 2. The Paid Parental Leave scheme in summary 4 2.1 What it is 4 2.2 Why we

Self Assessment GUIDE TO... HAZLEMS FENTON LLP.

GUIDE TO... Self Assessment HAZLEMS FENTON LLP www.hazlemsfenton.com YOUR GUIDE TO Self Assessment It is a fundamental part of the self assessment system that responsibility lies with you, the taxpayer,

GUIDE TO... Self Assessment HAZLEMS FENTON LLP www.hazlemsfenton.com YOUR GUIDE TO Self Assessment It is a fundamental part of the self assessment system that responsibility lies with you, the taxpayer,

EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling

2013 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling 1 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling DISCLAIMER The information contained in this guide

2013 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling 1 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling DISCLAIMER The information contained in this guide

KURLAND ACCOUNTING SERVICES

KURLAND ACCOUNTING SERVICES COMPANY PROFILE Paperworks Suite 354 Private Bag X043 Benoni, 1501 Tel: 011 849 7478 Cell: 082 458 6908 Fax: 086 671 1669 Email: info@kurlandaccounting.co.za Website: www.kurlandaccounting.co.za

KURLAND ACCOUNTING SERVICES COMPANY PROFILE Paperworks Suite 354 Private Bag X043 Benoni, 1501 Tel: 011 849 7478 Cell: 082 458 6908 Fax: 086 671 1669 Email: info@kurlandaccounting.co.za Website: www.kurlandaccounting.co.za

Guide on Valuation of Assets for Capital Gains Tax Purposes

Guide on Valuation of Assets for Capital Gains Tax Purposes Guide on Valuation of Assets for Capital Gains Tax Purposes FOREWORD This guide provides general guidelines regarding valuation of assets as

Guide on Valuation of Assets for Capital Gains Tax Purposes Guide on Valuation of Assets for Capital Gains Tax Purposes FOREWORD This guide provides general guidelines regarding valuation of assets as

Income Tax. Tax Guide for Small Businesses 2015/16

Income Tax Tax Guide for Small Businesses 2015/16 Preface Tax Guide for Small Businesses 2015/2016 This guide is a general guide dealing with the taxation of small businesses. This guide is not an official

Income Tax Tax Guide for Small Businesses 2015/16 Preface Tax Guide for Small Businesses 2015/2016 This guide is a general guide dealing with the taxation of small businesses. This guide is not an official

E-Remittance How-to EMPLOYER REPORTING INSTRUCTIONS

When remitting your contributions electronically (E-Remit), you will be asked to complete several steps to make sure the information submitted meets pension plan standards. Before you begin, it might be

When remitting your contributions electronically (E-Remit), you will be asked to complete several steps to make sure the information submitted meets pension plan standards. Before you begin, it might be

Making it easier for borrowers to repay their student loans

Making it easier for borrowers to repay their student loans A government discussion document Hon Peter Dunne Minister of Revenue First published in June 2009 by the Policy Advice Division of Inland Revenue,

Making it easier for borrowers to repay their student loans A government discussion document Hon Peter Dunne Minister of Revenue First published in June 2009 by the Policy Advice Division of Inland Revenue,

New Tax VDP Applications using efiling. There are two parts to the application process: Tax Practitioner

Application Guide for efiling Tax Voluntary Disclosure Programme 2010 Introduction The South African Revenue Service (SARS) will implement a Voluntary Disclosure Porgramme (VDP) that will be effective

Application Guide for efiling Tax Voluntary Disclosure Programme 2010 Introduction The South African Revenue Service (SARS) will implement a Voluntary Disclosure Porgramme (VDP) that will be effective

TAKAFUL INDUSTRY S CUSTOMER SERVICE CHARTER

TAKAFUL INDUSTRY S CUSTOMER SERVICE CHARTER r 1 P a g e 1. PILLAR 1: TAKAFUL MADE ACCESSIBLE Description Offer an active engagement model wherein a customer is aware of: Multi-channel options & accessibility

TAKAFUL INDUSTRY S CUSTOMER SERVICE CHARTER r 1 P a g e 1. PILLAR 1: TAKAFUL MADE ACCESSIBLE Description Offer an active engagement model wherein a customer is aware of: Multi-channel options & accessibility