Employment Tax Incentive Scheme. 2014/12/09 Version

|

|

|

- Opal Fletcher

- 5 years ago

- Views:

Transcription

1 Employment Tax Incentive Scheme 1

2 Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation. High youth unemployment means young people are not gaining the skills or experience needed to drive the economy forward. In South Africa s labour market, the current lack of skills and experience as well as perceptions regarding the restrictiveness of labour regulations, make some prospective employers reluctant to hire youth who may lack experience or qualifications. This lack of skills can have long-term adverse effects on the economy. In response to the high rate of youth unemployment, the Government is implementing the incentive mainly aiming at encouraging employers to hire young and less experienced work seekers, as stated in the National Development Plan. The incentive is meant as a temporary programme to stimulate demand for young workers. 2

3 Introduction On 20 September 2013 the Draft Employment Tax Incentive Bill was released for public comment. The bill was signed into law on the 18 December The first phase of the incentive is intended to be simple and easy to implement using existing tax administration platforms. Phase 1 Phase 1 will create the functionality for the employer to submit the declaration (EMP201) with the set off amount for the Employment Tax Incentive (ETI). Phase 2 Phase 2 will create the functionality for the employer to submit his reconciliation (EMP501) with the set off amount for the ETI. This phase, SARS will require the employer to submit the supporting information for all employees qualifying for the incentive. Phase 3 Phase 3 will focus on the implementation of the penalty administration, audits and the refunds process engines Version

4 Points for Discussion 1. The principles and rules pertaining to the Employment Tax incentive Scheme. 2. Calculations on the ETI payments and penalty. 3. The new EMP201 return.

5 Employment Tax Incentive (Legislation) An Employment Tax Incentive will be implemented from the 1 January 2014, however an employer may claim for employees who started work on or after the 1 October Please note (for now), the incentive ceases on 31 December 2016 and any employer with an unused incentive amount on 1 January 2017 will forfeit the amount. The existing learner ship allowance provided for in the Income Tax Act and this employment tax incentive are but two of the initiatives that the government encourages employers to access to increase the levels of employment and skills development. The incentive will be available to all eligible employers that have one or more qualifying employees and is calculated according to Clause 7 of the Employment Tax Incentive Act. Employers will be able to utilise the incentive by reducing the Employees Tax payable in that month by the incentive amount. Employers withhold the amount of tax that is owed by their employees and pay this amount over to SARS. If the employer was to hire a qualifying employee they can deduct the amount of the incentive from the amount of the Employees Tax that is owed to SARS. The amount of tax that is owed by the employees will still be recorded as being paid (there will be no shortfall on assessment) however the employer may retain the cash value of the incentive. 5

6 Employment Tax Incentive (Legislation) The amount of tax that is owed by the employees will still be recorded as being paid (there will be no shortfall on assessment) however the employer may retain the cash value of the incentive. Note that the incentive is not applicable to domestic workers, government employees, employees at parastatals and employees connected or related to the employer. It is aimed at Private Sectors Employers. Public entities are also excluded unless designated by the Minister of Finance by way of notice in the Government Gazette. The Minister of Finance may publish in regulation such conditions as would allow public entities to qualify for designation (in other words, to be allowed to receive the incentive).

7 Qualifying Employee A number of criteria must be met before an employee will be considered to be a qualifying employee (i.e. an employee that generates the incentive). The employee must: 1. Not be less than 18 years old and not more than 29 years old. If the employer is operating in a Special Economic Zone (these zones are still to be determined by the Minister) or designated industry then there is no age limitation for the qualifying employee. 2. Be in possession of a South African ID document or is in possession of an asylum seeker permit. 3. Not be a connected person to the employer (for example they cannot be a relative of the employer (a relative in relation to any person, means the spouse of that person or anybody related to him or her or to his or her spouse within the third degree of consanguinity, or any spouse of anybody so related)), 4. Not be a domestic worker, 5. Be employed by the employer on or after the 1 October 2013 and have commenced working on or after that date. 6. Not earn less than R2000 and not more than R6 000 per month. 7

8 Eligible Employers The employer is eligible to receive the ETI if the employer: is registered for employees tax (PAYE) is not in the national, provincial or local sphere of government; is not a public entity listed in schedule 2 or 3 of the Public Finance Management Act (other than those public entities designated by the Minister of Finance (MOF) by notice in the Gazette); is not a municipal entity is not disqualified by the Minister of Finance due to displacement of an employee or by not meeting such conditions as may be prescribed by Minister of Finance by regulation Note: The employer is not eligible to receive an incentive in respect of that employee only, if the employer pays the employee the amount less than: the regulated wage (an amount payable by a collective agreement; sectoral determination or binding bargaining council agreement) applicable to that employer; or if the regulated wage measure does not apply to that employer, the amount less than R2 000 per month. If the employee works for less than a month, the amount must be grossed up to a full month. 8

9 Disqualification Sector Determination or R2000 The Act describes the minimum wage/remuneration that must be paid by an employer in order for the employer to qualify for the incentive. If an employer is subject to a sector determination or bound by a bargaining counsel agreement, the employer must pay an employee at least the minimum wage as stipulated in the determination in order to qualify for the incentive in respect of that employee. Where an employer is not bound by a determination or an agreement, the employer must pay an employee at least R2 000 in remuneration per month in order to qualify for the incentive in respect of that employee. Where it has been found that they have claimed the incentive despite not being eligible to claim, they will face a penalty of 100% of the total value of the incentive that they have received in respect of each month in respect of that employee that the employer received the incentive. (note it is not on the full ETI but penalty only limited to the employee(s) that did not qualify). In addition, must pay SARS back the ETI incorrectly claimed 9

10 Disqualification Displacement of staff The Act specifically addresses concerns around the displacement of employees by employers intending to benefit from the incentive. An employer MAY cease to qualify for the tax incentive if the resolution of the dispute, whether by agreement, order of court or otherwise, reveals that the dismissal of the employee constitutes an automatically unfair dismissal in terms of section 187(f) of the Labour Relations Act AND, it must be found that the employee was unfairly dismissed in order to hire a new qualifying employee to take advantage of the incentive. Where the employer has been deemed to have displaced an employee, they will have to pay a penalty of R for each employee displaced and MAY also be disqualified from any future participation in the incentive. This disqualification will be taken by the Minister of Finance after taking into account (1) number of employees that have been displaced (2) the effect that the disqualification may directly or indirectly have on the employees 10

11 Calculation of the Incentive The determination of the incentive amount to be deducted from Employees Tax should take place on a monthly basis. The incentive available is calculated as the aggregate of the incentive available for that month together with any roll-over amount from previous periods; i.e. monthly incentive + any roll over. Monthly Incentive In determining the value of the incentive for a particular month, the employer must follow 5 steps: 1. Identify all qualifying employees in respect of that month; 2. Determine the applicable employment period for each qualifying employee (remember that an employee can only qualify for an incentive up to 2 years); 3. Determine each employee s monthly remuneration. The term Monthly Remuneration is defined in the Act as: (a) where an employer employs a qualifying employee for a month, means the amount paid or payable in respect of that month; or (b) where an employer employs a qualifying employee for part of a month, means the amount that would have been payable in respect of that month had that employer employed that employee for the entire month; This means that the remuneration for the month must be grossed up (as if the employee worked the full month) and once the incentive is determined the employer must then gross that incentive amount down to the number of days actually worked. 4. Calculate the amount of the incentive per qualifying employee; and 5. Aggregate the result. 11

12 Calculation of the Incentive There are effectively 6 different calculations depending on the applicable employment period and the monthly remuneration of the qualifying employee; pursuant to the table below. Monthly Remuneration Employment Tax Incentive per month during the first 12 months of employment of the qualifying employee Employment Tax Incentive per month during the next 12 months of employment of the qualifying employee R 0 - R % of Monthly Remuneration 25% of Monthly Remuneration R R4 000 R1 000 R500 R R6 000 Formula: X = A (B x (C D)) R1 000 (0.5 x (Monthly Remuneration R4 000)) Formula: X = A (B x (C D)) R500 (0.25 x (Monthly Remuneration R4 000)) The incentive will be available for a maximum 24-month period per qualifying employee, broken up into a first 12 months and a next 12 months. In calculating whether the 24-month period has expired, and if not, whether the qualifying employee falls within the first or next 12-month period, the total number of months that the qualifying employee was employed by the eligible employer, as well as by any associated institution in respect of that employer must be taken into account. In determining the first or the second 12 month period, only the months in which the employee was a qualifying employee are taken into account. For example, the employee may be a qualifying employee in the first three months but not a qualifying employee in the fourth and the fifth months. If the employee is a qualifying employee in the sixth month, the sixth month is month number four as far as the 12 month period is concerned. 12

13 Calculation of the Incentive Example 1 (basic calculation) In May 2014, Eligible Employer employs 2 qualifying employees, Mr A and Ms B (Step 1). Their monthly remuneration is R1 800 (industry standard minimum wage) and R5 200, respectively (step 2). Mr A is in the 4th month of employment with Eligible Employer and Ms B is in the 14th month (step 3). Calculation (step 4) Mr A - Because Mr A earns below R a month during the first 12-month period, the incentive amount available to Eligible Employer is 50% of R1 800 = R900 a month. Ms B - Because Ms B earns between R4 000 and R6 000 during the second 12- month period, the incentive amount available to Eligible Employer is calculated according to the following formula: R500 (0.25 x (R5 200 R4 000)) = R200 a month. Aggregation (step 5): The available incentive for May is R1 100 (R900 + R200). 13

14 Calculation of the Incentive Example 2 Tony spares shop hire 4 employees: 1. Steven (24) (month 14) Salary R Dorothy (34) Salary R Celeste (28) Celeste is Tony s daughter Salary R3 300 and 4. Kevin (19) (month 9) Salary R2 500 Total Employees Tax to be deducted is R Calculate his employment tax incentive; Only Steven and Kevin Qualify, Dorothy is over the age limit and Celeste is a connected person. Steven: R500 - (0.25 x (R4 300 R4000)) = R500 - R75 = R425 14

15 Calculation of the Incentive Kevin: He earns between R2 000 and R4 000, therefore the incentive applicable to his salary is R1 000 (he is in year 1) The total incentive = R1 425 for the month Therefore the employer pays employees tax of R R1 425 = R

16 Calculation of the Incentive Example 3 (effect of part-month employment) Halfway through August 2014, Eligible Employer appoints a qualifying employee, Ms E (step 1). According to her employment contract, Ms E is entitled to an amount of R4 200 per month. However, as Ms E only starts in the third quarter of the month, she only receives R1 050 in respect of August. Therefore, Ms E s monthly remuneration is R4 200 (step 2). {Remember when determining the incentive we must use the full months remuneration and not the actual remuneration.} Ms C is in her 1st month with Eligible Employer (step 3).The month of August has 20 working days, of which Ms E worked 5. Calculation (step 4) Ms E - Ms E s monthly remuneration is R Because Ms E earns between R4 000 and R6 000 during the first 12-month period, the incentive amount must be calculated as follows: Formula: R1 000 (0.5 x (R4 200 R4 000)) = R900 Apportionment according to clause 7(5): 5/20 x R900 = R225 Aggregation (step 5): The incentive for August is R

17 Calculation of the Incentive Example 4 (Part of a month) Sandra is a qualifying employee and she earned R1 980 for the month. She started work during the month and only worked 14 days of this 21 working day month. Calculate the incentive applicable to her Remuneration. Answer R x 21 = R2 969 Therefore the incentive is: R x 14 = R666 17

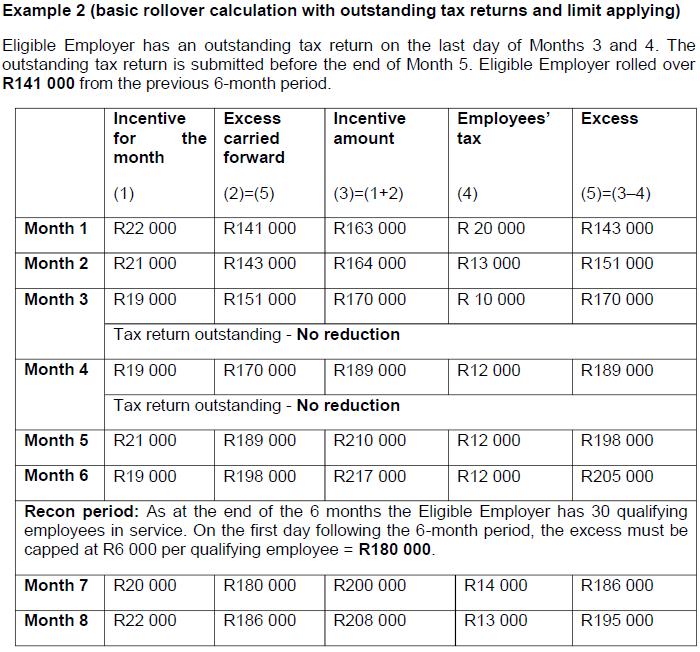

18 Roll Over Amounts There are three instances where an incentive amount available may be rolled over. Firstly, if the incentive amount available exceeds Employees Tax otherwise due in a month, the excess may be carried forward to the next month within certain limits. Secondly, where the incentive amount is available, however the employer does not reduce employee s tax by this incentive amount (be it for whatever reason, say wage clerk forgot to deduct) Thirdly, if the employer was not allowed to reduce the Employees' Tax payable due to tax returns outstanding or SARS debt incurred, the incentive amount may be carried forward for future use. Ordinarily, the monthly incentive will consist of the incentive pertaining to that month as well as any excess that the employer has carried forward from previous months. However, there is a periodic limit on the excess that may be carried forward: On the first day of the month following the end of each Employees Tax reconciliation period (currently 6 monthly), the amount of the excess that will be available for reducing the Employees' Tax in that month may not exceed R6 000 in respect of each qualifying employee employed by the employer as on that date. 18

19 Roll Over Amounts 19

20 20

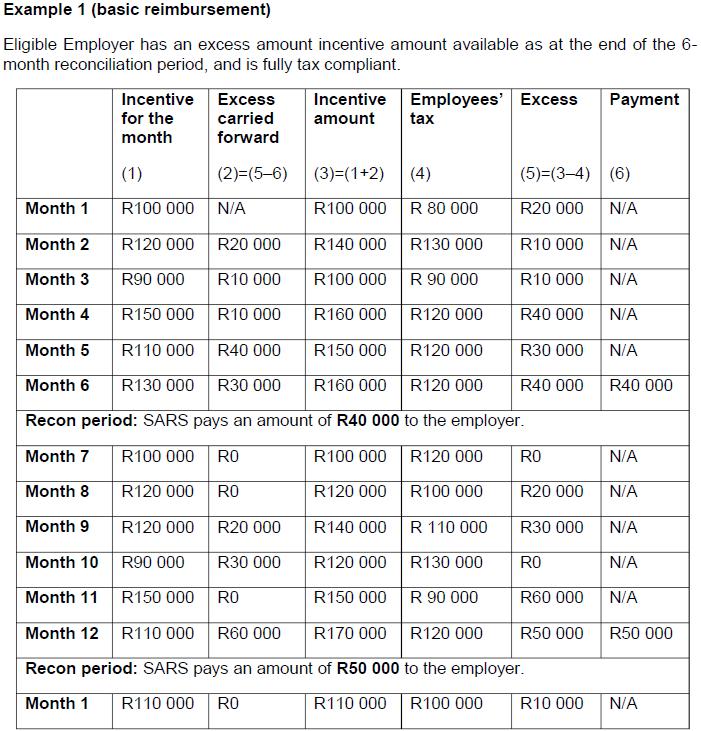

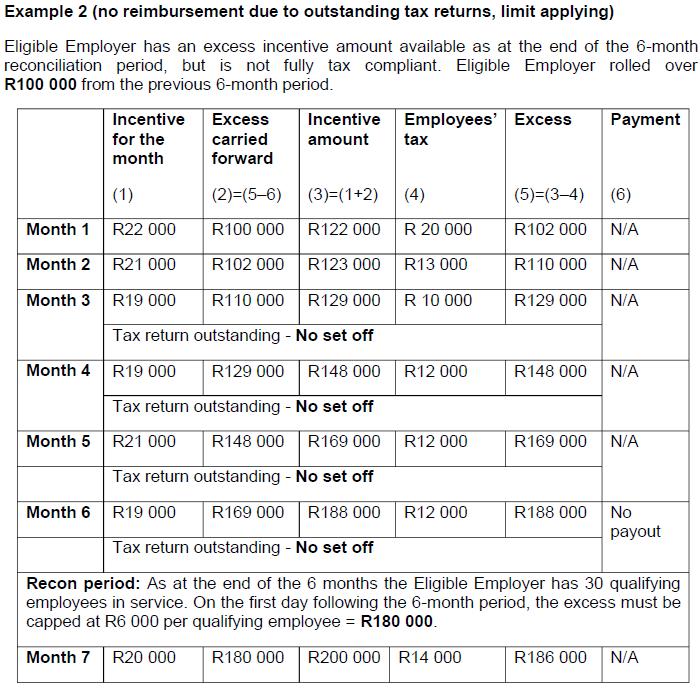

21 Reimbursements Reimbursements cannot currently be processed. However, from a date to be announced by the Minister of Finance through notice in the Government Gazette (Tday), employers will become entitled to reimbursements in respect of the incentive available. As from the effective date, an employer will be entitled to a reimbursement of the entire incentive amount available as at the end of each Employees Tax reconciliation period. Further, if the employer is entitled to a reimbursement, the excess incentive amount will revert to a nil balance for the following month. However, if the employer is not tax compliant as at the end of the 6-month reconciliation period, the excess amount payable to the employer may not be paid out. 21

22 Reimbursements 22

23 23

24 Monthly Submissions The monthly submissions and the reconciliation submissions (annual and interim) will be aligned to enable the submission of the monthly ETI information. The following forms/declarations will be enhanced to enable submission of the monthly ETI data: Monthly Employer Declaration (EMP201) Employer Reconciliation Declaration (EMP501) Legal Entity Registration form (REG01) Employee Tax Certificate [IRP5/IT3(a)] The implementation of this legislation has been phased, with phase 1 ensuring that the employers can submit their EMP201 declarations on the 7 of February SARS will change the reconciliation forms during February. The EMP201 can still be requested from the Call Centre, or through Branch Office and e-filing. 24

25 25

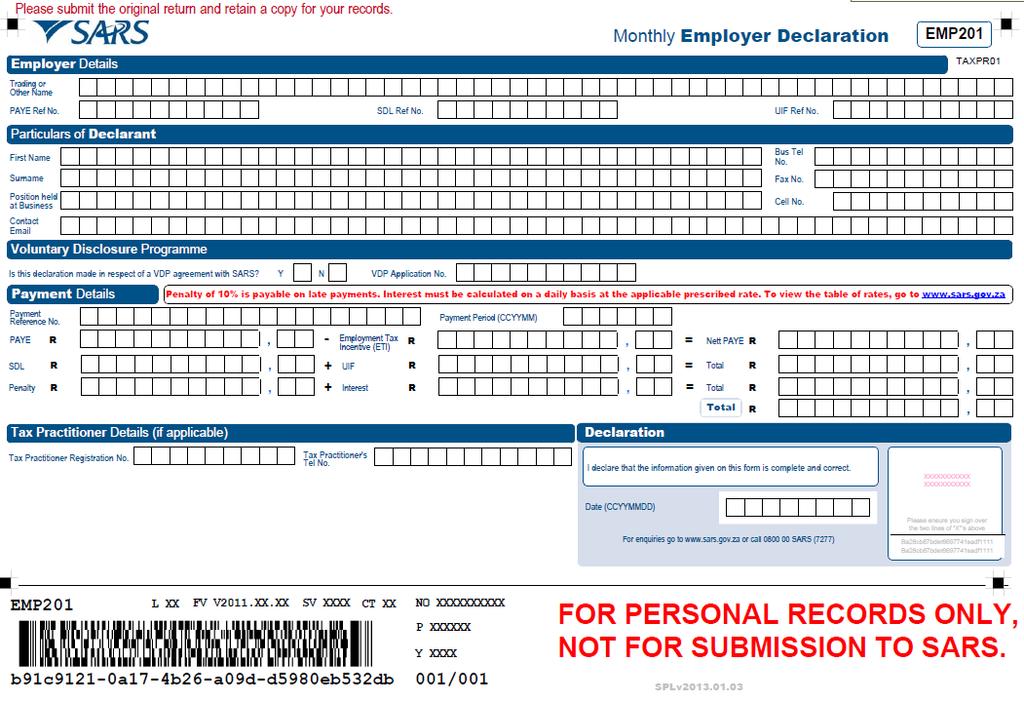

26 Completion of the EMP201 The employer will enter their normal Employees Tax withheld in the PAYE field They will then enter their Employment tax incentive in the applicable field. 4 The Nett PAYE field will be automatically calculated for the employer. If the ETI amount is greater than the PAYE amount then the NETT PAYE will default to 0. A negative amount is not allowed. SDL and UIF is completed as per normal. The totals of these two fields will be automatically calculated for the employer. Nett PAYE + Totals (SDL & UIF) + Totals (Pen & Int) = Total payable for the period. ( = 4) This is a self assessed return, therefore the employer must keep a record of how many employees qualified for each month the incentive is claimed. 26

27 Completion of the EMP201 The employer must keep a monthly record of the following: Start Date of the employee, Salary amount of the employee, Amount of the Employment Tax Incentive calculated per employee, Employees ID number, Employees Income tax number, Special Economic Zone Details of where the employee works. 27

28 Contact SARS National Call Centre: SARS E-filing: For free SARS Tax workshops: Taxes/Pages/default.aspx Version

Employment Tax Incentive Scheme

Employment Tax Incentive Scheme Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Employment Tax Incentive Scheme Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

Employment Tax Incentive (ETI)

") ETI 2017 Employment Tax Incentive (ETI) The ETI is an incentive aimed at encouraging employers to hire young work seekers. It was implemented with effect from 1 January 2014 The aim of this incentive was

ETI 2017 Employment Tax Incentive (ETI) The ETI is an incentive aimed at encouraging employers to hire young work seekers. It was implemented with effect from 1 January 2014 The aim of this incentive was

DRAFT GUIDE TO THE EMPLOYMENT TAX INCENTIVE

SOUTH AFRICAN REVENUE SERVICE DRAFT GUIDE TO THE EMPLOYMENT TAX INCENTIVE Another helpful guide brought to you by the South African Revenue Service Preface Draft Guide to the Employment Tax Incentive The

SOUTH AFRICAN REVENUE SERVICE DRAFT GUIDE TO THE EMPLOYMENT TAX INCENTIVE Another helpful guide brought to you by the South African Revenue Service Preface Draft Guide to the Employment Tax Incentive The

Tax and ETI Amendments 2017/2018

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

Overview of PAYE reconciliation process and 2007/08 policy changes. Another helpful guide brought to you by South African Revenue Service

Overview of PAYE reconciliation process and 2007/08 policy changes Another helpful guide brought to you by South African Revenue Service Overview of PAYE reconciliation process and 2007/08 policy changes

Overview of PAYE reconciliation process and 2007/08 policy changes Another helpful guide brought to you by South African Revenue Service Overview of PAYE reconciliation process and 2007/08 policy changes

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

Tax, ETI and UIF Amendments 2018/2019

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY Foreword This document is a general guide dealing with the PAYE responsibility

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY Foreword This document is a general guide dealing with the PAYE responsibility

OVERVIEW PAYE 2010 NOVEMBER

OVERVIEW PAYE 2010 NOVEMBER 1 Contents 1. Introduction... 3 2. The aim of the Pay-As-You-Earn (PAYE) reconciliation process... 3 3. What is reconciliation?... 4 4. The Pay-As-You-Earn (PAYE) process...

OVERVIEW PAYE 2010 NOVEMBER 1 Contents 1. Introduction... 3 2. The aim of the Pay-As-You-Earn (PAYE) reconciliation process... 3 3. What is reconciliation?... 4 4. The Pay-As-You-Earn (PAYE) process...

FREQUENTLY ASKED QUESTIONS COMPLETION AND SUBMISSION OF CSV. TM EMPLOYER AND ZIPCENTRALFILE RECONCILIATION DOCUMENTS

FREQUENTLY ASKED QUESTIONS Revision: 1 Page 1 of 8 1 PURPOSE The purpose of this document is to provide answers to frequently asked questions by employers in respect of creating CSV data files and submitting

FREQUENTLY ASKED QUESTIONS Revision: 1 Page 1 of 8 1 PURPOSE The purpose of this document is to provide answers to frequently asked questions by employers in respect of creating CSV data files and submitting

REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER 0 Initial Release A Scheepers GM Operational Services

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

EXPLANATORY MEMORANDUM

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 2 EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 Currently, the unemployment

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 2 EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 Currently, the unemployment

PAYE must be deducted by an employer from remuneration paid to an employee when the income accrues or is paid to the employee.

PAYE must be deducted by an employer from remuneration paid to an employee when the income accrues or is paid to the employee. Q How can PAYE be deducted from an accrual? Income that accrues in one tax

PAYE must be deducted by an employer from remuneration paid to an employee when the income accrues or is paid to the employee. Q How can PAYE be deducted from an accrual? Income that accrues in one tax

External Guide on how to submit a Request for Remission

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

TAX GUIDE FOR MICRO BUSINESSES 2011/12

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

Quick Start Guide to Payroll Tax Year-End

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

Tax tables 2019/2020 (year of assessment ending 29 February 2020)

") BUDGET SPEECH 2019/2020 ALL YOU NEED TO KNOW Tax tables 2019/2020 (year of assessment ending 29 February 2020) Income tax: Individuals and special trusts Taxable income Rates of tax 0-195 850 18 % of taxable

BUDGET SPEECH 2019/2020 ALL YOU NEED TO KNOW Tax tables 2019/2020 (year of assessment ending 29 February 2020) Income tax: Individuals and special trusts Taxable income Rates of tax 0-195 850 18 % of taxable

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON ACCOMMODATION

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Nombasa Langeni (Nombasa.Langeni@treasury.gov.za)

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Nombasa Langeni (Nombasa.Langeni@treasury.gov.za)

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

Economic Landscape of South Africa

Economic Landscape of South Africa INTRODUCTION One of the leading economies in Africa, with a well-developed infrastructure and established trade links with the rest of the continent, South Africa is

Economic Landscape of South Africa INTRODUCTION One of the leading economies in Africa, with a well-developed infrastructure and established trade links with the rest of the continent, South Africa is

Tax year end processing

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

REPUBLIC OF SOUTH AFRICA. No. 63 of 2001: Unemployment Insurance Act as amended by Unemployment Insurance Amendment Act, No 32 of 2003

REPUBLIC OF SOUTH AFRICA No. 63 of 2001: Unemployment Insurance Act as amended by Unemployment Insurance Amendment Act, No 32 of 2003 ACT To establish the Unemployment Insurance Fund; to provide for the

REPUBLIC OF SOUTH AFRICA No. 63 of 2001: Unemployment Insurance Act as amended by Unemployment Insurance Amendment Act, No 32 of 2003 ACT To establish the Unemployment Insurance Fund; to provide for the

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

Briefing on the Youth Wage Subsidy: Specific Questions:

19 May 2012 Tim Harris MP Briefing on the Youth Wage Subsidy: The DA fully supports the implementation of the Youth Wage Subsidy outlined in National Treasury s document Confronting youth unemployment:

19 May 2012 Tim Harris MP Briefing on the Youth Wage Subsidy: The DA fully supports the implementation of the Youth Wage Subsidy outlined in National Treasury s document Confronting youth unemployment:

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

UNEMPLOYMENT INSURANCE ACT

UNEMPLOYMENT INSURANCE ACT as amended by Unemployment Insurance Amendment Act, No 32 of 2003 To establish the Unemployment Insurance Fund; to provide for the payment from the Fund of unemployment benefits

UNEMPLOYMENT INSURANCE ACT as amended by Unemployment Insurance Amendment Act, No 32 of 2003 To establish the Unemployment Insurance Fund; to provide for the payment from the Fund of unemployment benefits

EXTERNAL GUIDE GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017

GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 BACKGROUND 3 3.1 RECONCILIATION PROCESS 3 3.2 INTERIM RECONCILIATION PROCESS 3 3.3 GENERAL

GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 BACKGROUND 3 3.1 RECONCILIATION PROCESS 3 3.2 INTERIM RECONCILIATION PROCESS 3 3.3 GENERAL

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

Standing Committee on Finance (SCOF): Report-Back Hearings 22 October DRAFT Employment Tax Incentive Bill

: Report-Back Hearings 22 October DRAFT Employment Tax Incentive Bill") Standing Committee on Finance (SCOF): Report-Back Hearings 22 October 2013 DRAFT Employment Tax Incentive Bill Response Document from National Treasury as presented to SCOF 1. Introduction Many South Africans

Standing Committee on Finance (SCOF): Report-Back Hearings 22 October 2013 DRAFT Employment Tax Incentive Bill Response Document from National Treasury as presented to SCOF 1. Introduction Many South Africans

SARS approach to Government institutions

SARS approach to Government institutions 1. SARS focusses on the Tax Compliance of Government Institutions at a National, Provincial and Local Level. 2. SARS Risks that we focus are: Correct Registration,

SARS approach to Government institutions 1. SARS focusses on the Tax Compliance of Government Institutions at a National, Provincial and Local Level. 2. SARS Risks that we focus are: Correct Registration,

Cape Town Johannesburg Durban

APPOINTMENT AS ACCOUNTANTS TO: SIR / MADAM We hereby wish to confirm our appointment as accountants and financial advisors to the above business and its owners / members / directors. The terms and conditions

APPOINTMENT AS ACCOUNTANTS TO: SIR / MADAM We hereby wish to confirm our appointment as accountants and financial advisors to the above business and its owners / members / directors. The terms and conditions

The new KiwiSaver legislation

21 December 2007 Special report from the Policy Advice Division of Inland Revenue The new KiwiSaver legislation This report will form the basis of an article to appear in the Tax Information Bulletin.

21 December 2007 Special report from the Policy Advice Division of Inland Revenue The new KiwiSaver legislation This report will form the basis of an article to appear in the Tax Information Bulletin.

P U BLI C RELEAS E. Document Classification: Official Publication. South African Revenue Service

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

Employer Easy File Q & A

Employer Easy File Q & A Trouble Shooting Solutions Employer installed e@syfile Employer version 6.0.0 and having troubles login: Confirm if employer made a backup in version 5.0.9 If Yes, copy version

Employer Easy File Q & A Trouble Shooting Solutions Employer installed e@syfile Employer version 6.0.0 and having troubles login: Confirm if employer made a backup in version 5.0.9 If Yes, copy version

Individual Income Tax

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

P U BLI C RELEAS E. Document Classification: Official Publication. South African Revenue Service

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

SAPA Conference Spier, Stellenbosch 04 August March

SAPA Conference Spier, Stellenbosch 04 August 2011 17 March INTRODUCTION PAYE processes and forms, over the past few years, have been aggressively modernised so as to ensure better alignment between PAYE

SAPA Conference Spier, Stellenbosch 04 August 2011 17 March INTRODUCTION PAYE processes and forms, over the past few years, have been aggressively modernised so as to ensure better alignment between PAYE

PUBLIC RELEASE. Document Classification: Official Publication. South African Revenue Service 2011

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published document SARS

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published document SARS

IN THE LABOUR COURT OF SOUTH AFRICA SITTING IN DURBAN REPORTABLE CASE NO D849/02. Date heard: 2003/04/17. Date delivered: 2003/04/23

IN THE LABOUR COURT OF SOUTH AFRICA SITTING IN DURBAN Date delivered: 2003/04/23 REPORTABLE CASE NO D849/02 Date heard: 2003/04/17 In the matter between: STEVEN CHRISTOPHER JARDINE APPLICANT and TONGAAT

IN THE LABOUR COURT OF SOUTH AFRICA SITTING IN DURBAN Date delivered: 2003/04/23 REPORTABLE CASE NO D849/02 Date heard: 2003/04/17 In the matter between: STEVEN CHRISTOPHER JARDINE APPLICANT and TONGAAT

P U B L I C R E L E A S E

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

SECTION 4: STATEMENT OF WORK EXPERIENCE

SECTION 4: STATEMENT OF WORK EXPERIENCE Curriculum Number: 331303001 Curriculum Title: Tax Technician Learner Details Name: ID Number: Employer Details Company Name: Address: Supervisor Name: Work Telephone:

SECTION 4: STATEMENT OF WORK EXPERIENCE Curriculum Number: 331303001 Curriculum Title: Tax Technician Learner Details Name: ID Number: Employer Details Company Name: Address: Supervisor Name: Work Telephone:

P U BLI C RELEAS E. Document Classification: Official Publication. South African Revenue Service 2014

P U BLI C RELEAS E Document Classification: Official Publication South African Revenue Service 2014 04/2014 Page 1 of 112 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U BLI C RELEAS E Document Classification: Official Publication South African Revenue Service 2014 04/2014 Page 1 of 112 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

UNEMPLOYMENT INSURANCE CONTRIBUTIONS ACT NO 4 OF 2002

UNEMPLOYMENT INSURANCE CONTRIBUTIONS ACT NO 4 OF 2002 [ASSENTED TO 27 MARCH 2002 ] [ENGLISH TEXT SIGNED BY PRESIDENT.] AS AMENDED BY TAXATION LAWS AMENDMENT ACT, NO. 30 OF 2002 REVENUE LAWS AMENDMENT ACT,

UNEMPLOYMENT INSURANCE CONTRIBUTIONS ACT NO 4 OF 2002 [ASSENTED TO 27 MARCH 2002 ] [ENGLISH TEXT SIGNED BY PRESIDENT.] AS AMENDED BY TAXATION LAWS AMENDMENT ACT, NO. 30 OF 2002 REVENUE LAWS AMENDMENT ACT,

PAYROLL TAX POCKET GUIDE. A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa.

PAYROLL TAX POCKET GUIDE 2019 2020 A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside

PAYROLL TAX POCKET GUIDE 2019 2020 A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside

D-BIT Payroll. Employees Remuneration for UIF, SDL, PAYE. D-BIT SYSTEMS (Pty) Ltd D-BIT Systems (Pty) Ltd) 2/24/2012, 3:18 PM

Ltd D-BIT Systems (Pty) Ltd) 2/24/2012, 3:18 PM") D-BIT SYSTEMS (Pty) Ltd RegNo: 87/033407 D-Bit Building 18 Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 156 South Africa D-BIT Payroll Employees for UIF, SDL, PAYE 01... D-BIT Systems (Pty)

D-BIT SYSTEMS (Pty) Ltd RegNo: 87/033407 D-Bit Building 18 Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 156 South Africa D-BIT Payroll Employees for UIF, SDL, PAYE 01... D-BIT Systems (Pty)

P U B L I C R E L E A S E

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2012 Page 1 of 55 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2012 Page 1 of 55 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

An Act to ensure the continuity of the provision of legal services within the Government and certain public bodies

FIRST SESSION THIRTY-NINTH LEGISLATURE Bill 135 (2011, chapter 2) An Act to ensure the continuity of the provision of legal services within the Government and certain public bodies Introduced 21 February

FIRST SESSION THIRTY-NINTH LEGISLATURE Bill 135 (2011, chapter 2) An Act to ensure the continuity of the provision of legal services within the Government and certain public bodies Introduced 21 February

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained 1 To Mr. Anil Naidoo

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained To Mr. Anil Naidoo From Tax Manager Subject Tax implications of issues discussed Date 4 December 207 Sub Total Scope We refer to our

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained To Mr. Anil Naidoo From Tax Manager Subject Tax implications of issues discussed Date 4 December 207 Sub Total Scope We refer to our

PUBLIC RELEASE. Document Classification: Official Publication. South African Revenue Service 2009

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

International Tax South Africa Highlights 2018

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

COIDA : COMPENSATION FOR OCCUPATIONAL INJURIES AND DISEASES ACT,1993. AMENDED IN 1997

COIDA : COMPENSATION FOR OCCUPATIONAL INJURIES AND DISEASES ACT,1993. AMENDED IN 1997 1 OUR MISSION TO COMPENSATE EMPLOYEES FOR DISABLEMENT CAUSED BY OCCUPATIONAL INJURIES SUSTAINED AND OR DISEASES CONTRACTED

COIDA : COMPENSATION FOR OCCUPATIONAL INJURIES AND DISEASES ACT,1993. AMENDED IN 1997 1 OUR MISSION TO COMPENSATE EMPLOYEES FOR DISABLEMENT CAUSED BY OCCUPATIONAL INJURIES SUSTAINED AND OR DISEASES CONTRACTED

ALL MAN LABOUR SERVICES CC JUDGMENT: [1] Appellant approached the court a quo for an order to compel respondent to pay

![ALL MAN LABOUR SERVICES CC JUDGMENT: [1] Appellant approached the court a quo for an order to compel respondent to pay](/thumbs/87/96656620.jpg "ALL MAN LABOUR SERVICES CC JUDGMENT: [1] Appellant approached the court a quo for an order to compel respondent to pay") IN THE LABOUR APPEAL COURT OF SOUTH AFRICA (HELD AT JOHANNESBURG) Case No.: JA 12/2007 ALL MAN LABOUR SERVICES CC Appellant and THE SERVICES SECTOR EDUCATION & TRAINING AUTHORITY Respondent JUDGMENT: DAVIS

IN THE LABOUR APPEAL COURT OF SOUTH AFRICA (HELD AT JOHANNESBURG) Case No.: JA 12/2007 ALL MAN LABOUR SERVICES CC Appellant and THE SERVICES SECTOR EDUCATION & TRAINING AUTHORITY Respondent JUDGMENT: DAVIS

AGRICULTURE FINANCIAL SERVICES ACT

Province of Alberta AGRICULTURE FINANCIAL SERVICES ACT Revised Statutes of Alberta 2000 Chapter A-12 Current as of December 15, 2017 Office Consolidation Published by Alberta Queen s Printer Alberta Queen

Province of Alberta AGRICULTURE FINANCIAL SERVICES ACT Revised Statutes of Alberta 2000 Chapter A-12 Current as of December 15, 2017 Office Consolidation Published by Alberta Queen s Printer Alberta Queen

The Director-General National Treasury Private Bag X115 PRETORIA 0001

STAATSKOERANT, 14 AUGUSTUS 2009 No.32489 3 GENERAL NOTICE NOTICE 1103 OF 2009 NATIONAL TREASURY PREFERENTIAL PROCUREMENT POLICY FRAMEWORK ACT, 2000, (ACT NO.5 OF 2000): DRAFT PREFERENTIAL PROCUREMENT REGULATIONS,

STAATSKOERANT, 14 AUGUSTUS 2009 No.32489 3 GENERAL NOTICE NOTICE 1103 OF 2009 NATIONAL TREASURY PREFERENTIAL PROCUREMENT POLICY FRAMEWORK ACT, 2000, (ACT NO.5 OF 2000): DRAFT PREFERENTIAL PROCUREMENT REGULATIONS,

A QUICK GUIDE TO DIVIDENDS TAX

A QUICK GUIDE TO DIVIDENDS TAX i A QUICK GUIDE TO DIVIDENDS TAX 1. INTRODUCTION TO DIVIDENDS TAX In 2007, the Minister of Finance announced that Secondary Tax on Companies (STC) would be replaced by Dividends

A QUICK GUIDE TO DIVIDENDS TAX i A QUICK GUIDE TO DIVIDENDS TAX 1. INTRODUCTION TO DIVIDENDS TAX In 2007, the Minister of Finance announced that Secondary Tax on Companies (STC) would be replaced by Dividends

Office: Mobile: Fax: Maternity Benefits Agreement Form

Maternity Benefits Agreement Form Before you sign this agreement, please check the following: Are you sure you are contributing monthly to UIF? (YES/NO) If UIF is not deducted from your salary you cannot

Maternity Benefits Agreement Form Before you sign this agreement, please check the following: Are you sure you are contributing monthly to UIF? (YES/NO) If UIF is not deducted from your salary you cannot

GROUP FIVE BEE TRANSACTION - SUMMARY OF SALIENT TERMS OF BLACK PROFESSIONALS STAFF TRUST DEED AND IZAKHIWO IMFUNDO TRUST DEED

5513383_1 18/10/2012 GROUP FIVE BEE TRANSACTION - SUMMARY OF SALIENT TERMS OF BLACK PROFESSIONALS STAFF TRUST DEED AND IZAKHIWO IMFUNDO TRUST DEED (Note: terms defined in the circular bear the same meanings

5513383_1 18/10/2012 GROUP FIVE BEE TRANSACTION - SUMMARY OF SALIENT TERMS OF BLACK PROFESSIONALS STAFF TRUST DEED AND IZAKHIWO IMFUNDO TRUST DEED (Note: terms defined in the circular bear the same meanings

ITA88 PROCESS GUIDE ITA88 PROCESS GUIDE AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS

AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS SEPTEMBER 2010 _v2.indd 1 1 9/21/10 4:10 PM AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS Introduction ITA88 AGENT APPOINTMENT Who

AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS SEPTEMBER 2010 _v2.indd 1 1 9/21/10 4:10 PM AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS Introduction ITA88 AGENT APPOINTMENT Who

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

VDP applications. August 2015

VDP applications August 2015 Overview for this webinar VDP Relief offered under the VDP; Overview of the VDP process; When VDP is not available: Pending or current audit/investigation Requirements for

VDP applications August 2015 Overview for this webinar VDP Relief offered under the VDP; Overview of the VDP process; When VDP is not available: Pending or current audit/investigation Requirements for

Change, the new certainty

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

Tax Guide for Micro Businesses 2010/11. Turnover Tax. for Small Businesses. Tax Guide For Micro Businesses 2010/11 - Page 1

Tax Guide for Micro Businesses 2010/11 Turnover Tax for Small Businesses Tax Guide For Micro Businesses 2010/11 - Page 1 TT Comprehensive Guide.indd 1 TAX GUIDE FOR MICRO BUSINESSES 2010/11 The guide contains

Tax Guide for Micro Businesses 2010/11 Turnover Tax for Small Businesses Tax Guide For Micro Businesses 2010/11 - Page 1 TT Comprehensive Guide.indd 1 TAX GUIDE FOR MICRO BUSINESSES 2010/11 The guide contains

TAX GUIDE FOR SMALL BUSINESSES 2013/14

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

Omission of source code 4582

Return Submission ETI Omission of source code 4582 With the implementation of the Retirement Reform requirements, information code 4582 and its value were omitted from the submission file created by e@syfile

Return Submission ETI Omission of source code 4582 With the implementation of the Retirement Reform requirements, information code 4582 and its value were omitted from the submission file created by e@syfile

SKILLS DEVELOPMENT ACT 97 OF 1998

SKILLS DEVELOPMENT ACT 97 OF 1998 [ASSENTED TO 20 OCTOBER 1998] [DATE OF COMMENCEMENT: 10 SEPTEMBER 1999] (Unless otherwise indicated) (English text signed by the President) as amended by Skills Development

SKILLS DEVELOPMENT ACT 97 OF 1998 [ASSENTED TO 20 OCTOBER 1998] [DATE OF COMMENCEMENT: 10 SEPTEMBER 1999] (Unless otherwise indicated) (English text signed by the President) as amended by Skills Development

Payroll Pocket Guide. as at March A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa

Payroll Pocket Guide as at March 2013 A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa Quick Reference Subsistence Allowance Travel inside RSA

Payroll Pocket Guide as at March 2013 A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa Quick Reference Subsistence Allowance Travel inside RSA

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE EMPLOYEE BENEFITS (GRAP 25)

") ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE EMPLOYEE BENEFITS (GRAP 25) Issued by the Accounting Standards Board November 2009 Acknowledgment This Standard of Generally

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE EMPLOYEE BENEFITS (GRAP 25) Issued by the Accounting Standards Board November 2009 Acknowledgment This Standard of Generally

PRESENTATION TO SABOA CONFERENCE

PRESENTATION TO SABOA CONFERENCE THE DEVELOPMENT OF PERFORMANCE BASED GROSS NEGOTIATED MODEL CONTRACT DOCUMENT FOR THE ROLL-OUT OF IPTNs 23 FEBRUARY 2012 1 CONTENTS PURPOSE OF THE PRESENTATION CURRENT

PRESENTATION TO SABOA CONFERENCE THE DEVELOPMENT OF PERFORMANCE BASED GROSS NEGOTIATED MODEL CONTRACT DOCUMENT FOR THE ROLL-OUT OF IPTNs 23 FEBRUARY 2012 1 CONTENTS PURPOSE OF THE PRESENTATION CURRENT

PAYROLL COMPLIANCE by Ron Warren, CA(SA)

") PAYROLL COMPLIANCE by Ron Warren, CA(SA) When considering the great range of topics that fall under the heading of Payroll compliance and the fact that I have just over an hour in which to cover them,

PAYROLL COMPLIANCE by Ron Warren, CA(SA) When considering the great range of topics that fall under the heading of Payroll compliance and the fact that I have just over an hour in which to cover them,

Government Gazette REPUBLIC OF SOUTH AFRICA. Vol. 550 CapeTown 28 April 2011 No

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

SAPA - ANNUAL PAYE UPDATE BREAKFAST, Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014

SAPA - ANNUAL PAYE UPDATE BREAKFAST, 2014 Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014 Content Chapter 4 Annexure C Davis Tax Review Committee Miscellaneous 1 Content: Chapter

SAPA - ANNUAL PAYE UPDATE BREAKFAST, 2014 Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014 Content Chapter 4 Annexure C Davis Tax Review Committee Miscellaneous 1 Content: Chapter

Québec Budget Summary

March 17, 2016 HIGHLIGHTS Retroactive decrease in the daycare contribution for a second child Changes in the criteria for the SBD Changes to the transfer tax on immovables ( Land transfer tax") Support

March 17, 2016 HIGHLIGHTS Retroactive decrease in the daycare contribution for a second child Changes in the criteria for the SBD Changes to the transfer tax on immovables ( Land transfer tax") Support

FNB Credit Card & ebucks Shop Appliances Campaign. Terms and Conditions. Date these rules were first published: 12 October 2018

FNB Credit Card & ebucks Shop - Appliances Campaign Terms and Conditions Date these rules were first published: 12 October 2018 Date these rules were last changed: N/A Read these campaign rules carefully.

FNB Credit Card & ebucks Shop - Appliances Campaign Terms and Conditions Date these rules were first published: 12 October 2018 Date these rules were last changed: N/A Read these campaign rules carefully.

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Nombasa Langeni (Nombasa.Langeni@treasury.gov.za)

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Nombasa Langeni (Nombasa.Langeni@treasury.gov.za)

Office: Mobile: Fax:

Mediclinic Baby Maternity Benefits Agreement Form Before you sign this agreement, please check the following: Are you sure you are contributing monthly to UIF? (YES/NO) If UIF is not deducted from your

Mediclinic Baby Maternity Benefits Agreement Form Before you sign this agreement, please check the following: Are you sure you are contributing monthly to UIF? (YES/NO) If UIF is not deducted from your

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS. Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

Brand New Superannuation Fund

Superannuation Trust Deed for a Self- Managed Fund for Brand New Superannuation Fund CLEARDOCS PTY 1 Albert St Hawthorn VIC 3000 Tel: 03 98869123 Fax: 03 98869123 it@cleardocs.com http://www.cleardocs.com

Superannuation Trust Deed for a Self- Managed Fund for Brand New Superannuation Fund CLEARDOCS PTY 1 Albert St Hawthorn VIC 3000 Tel: 03 98869123 Fax: 03 98869123 it@cleardocs.com http://www.cleardocs.com

OID Detail 2018 Tax Year End

OID Detail 2018 Tax Year End Occupational Injuries and Diseases (OID) Extracts from the Occupational Injuries and Diseases Act 1.1 Definitions "employee" means a person who has entered into or works under

OID Detail 2018 Tax Year End Occupational Injuries and Diseases (OID) Extracts from the Occupational Injuries and Diseases Act 1.1 Definitions "employee" means a person who has entered into or works under

1.1 Beneficiary is the person who actually receives a TrustEd Bursary.

SCHOOL-DAYS PRODUCT TERMS & CONDITIONS OF USE These terms and conditions form part of our agreement which governs the receipt and use of the School-Days member card and your relationship with Trusted Bursaries

SCHOOL-DAYS PRODUCT TERMS & CONDITIONS OF USE These terms and conditions form part of our agreement which governs the receipt and use of the School-Days member card and your relationship with Trusted Bursaries

Payroll Tax Pocket Guide 2017/18

Payroll Tax Pocket Guide 2017/18 A complete reference guide covering legislative matters that affect the HR & payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside RSA

Payroll Tax Pocket Guide 2017/18 A complete reference guide covering legislative matters that affect the HR & payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside RSA

A guide to understanding the medical scheme fees tax credit

A guide to understanding the medical scheme fees tax credit A guide to understanding the medical scheme fees tax credit 1 TABLE OF CONTENTS 1. INTRODUCTION... 3 2. WHAT ARE THE CHANGES?... 3 3. THE CHANGES

A guide to understanding the medical scheme fees tax credit A guide to understanding the medical scheme fees tax credit 1 TABLE OF CONTENTS 1. INTRODUCTION... 3 2. WHAT ARE THE CHANGES?... 3 3. THE CHANGES

Bill 75 (2016, chapter 13)

") FIRST SESSION FORTY-FIRST LEGISLATURE Bill 75 (2016, chapter 13) An Act respecting the restructuring of university-sector defined benefit pension plans and amending various legislative provisions Introduced

FIRST SESSION FORTY-FIRST LEGISLATURE Bill 75 (2016, chapter 13) An Act respecting the restructuring of university-sector defined benefit pension plans and amending various legislative provisions Introduced

IN THE LABOUR COURT OF SOUTH AFRICA HELD AT CAPE TOWN SOUTH AFRICAN BREWERIES LIMITED. DAVID WOOLFREY First Respondent

IN THE LABOUR COURT OF SOUTH AFRICA HELD AT CAPE TOWN Case no: C 407/98 In the matter between: SOUTH AFRICAN BREWERIES LIMITED Applicant BEER DIVISION AND DAVID WOOLFREY First Respondent FOOD AND ALLIED

IN THE LABOUR COURT OF SOUTH AFRICA HELD AT CAPE TOWN Case no: C 407/98 In the matter between: SOUTH AFRICAN BREWERIES LIMITED Applicant BEER DIVISION AND DAVID WOOLFREY First Respondent FOOD AND ALLIED

APPOINTMENT AS TAX CONSULTANTS TO:

APPOINTMENT AS TAX CONSULTANTS TO: Name: Identity Number: Tax Number: SIR / MADAM We hereby wish to confirm our appointment by you, as tax consultants and financial advisors. The terms and conditions of

APPOINTMENT AS TAX CONSULTANTS TO: Name: Identity Number: Tax Number: SIR / MADAM We hereby wish to confirm our appointment by you, as tax consultants and financial advisors. The terms and conditions of

Government Gazette REPUBLIC OF SOUTH AFRICA. AIDS HELPLINE: Prevention is the cure

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

24 November 2016 The National Treasury 240 Vermeulen Street PRETORIA 0001

24 November 2016 The National Treasury 240 Vermeulen Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Mmule Majola (mmule.majola@treasury.gov.za)

24 November 2016 The National Treasury 240 Vermeulen Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Mmule Majola (mmule.majola@treasury.gov.za)

Welcome to the SARS Tax Workshop

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Release Notes 5.0b. Classic and Premier. May 2018

Release Notes 5.0b Classic and Premier May 2018 Table of Contents 1.0 Important Notice (Classic/Premier) 3 1.1 RSA Companies 3 1.2 Swaziland Companies 4 2.0 Auto Renewals 5 3.0 Licence Agreement 6 4.0

Release Notes 5.0b Classic and Premier May 2018 Table of Contents 1.0 Important Notice (Classic/Premier) 3 1.1 RSA Companies 3 1.2 Swaziland Companies 4 2.0 Auto Renewals 5 3.0 Licence Agreement 6 4.0

Next >> Quick Tax Guide 2019/20 South Africa. Making an impact that matters

Next >> Quick Tax Guide 2019/20 South Africa Making an impact that matters Contents... 1...1...1...2...3...4 Severance and Retirement Fund Lump Sum...4... 5...5...6...7...7...7...7... 8...8...8...9...9...9...9...10...10...10...10...10...11...

Next >> Quick Tax Guide 2019/20 South Africa Making an impact that matters Contents... 1...1...1...2...3...4 Severance and Retirement Fund Lump Sum...4... 5...5...6...7...7...7...7... 8...8...8...9...9...9...9...10...10...10...10...10...11...

GOVERNMENT GAZETTE OF THE REPUBLIC OF NAMIBIA. N$4.40 WINDHOEK - 27 January 2014 No. 5395

GOVERNMENT GAZETTE OF THE REPUBLIC OF NAMIBIA N$4.40 WINDHOEK - 27 January 2014 No. 5395 CONTENTS Page GOVERNMENT NOTICES No. 5 No. 6 Regulations relating to use of vocational and training levies for funding

GOVERNMENT GAZETTE OF THE REPUBLIC OF NAMIBIA N$4.40 WINDHOEK - 27 January 2014 No. 5395 CONTENTS Page GOVERNMENT NOTICES No. 5 No. 6 Regulations relating to use of vocational and training levies for funding

Tax guide 2018/2019 TAX FACTS

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

GUIDE TO THE URBAN DEVELOPMENT ZONE TAX INCENTIVE

GUIDE TO THE URBAN DEVELOPMENT ZONE TAX INCENTIVE Foreword This guide is a general guide with regard to the urban development zone tax incentive. It is not meant to delve into the precise technical and

GUIDE TO THE URBAN DEVELOPMENT ZONE TAX INCENTIVE Foreword This guide is a general guide with regard to the urban development zone tax incentive. It is not meant to delve into the precise technical and

CO-OPERATIVE BANKS ACT

REPUBLIC OF SOUTH AFRICA CO-OPERATIVE BANKS ACT IRIPHABLIKI YOMZANTSI AFRIKA UMTHETHO WEEBHANKI ZENTSEBENZISWANO No, 07 ACT To promote and advance the social and economic welfare of all South Africans

REPUBLIC OF SOUTH AFRICA CO-OPERATIVE BANKS ACT IRIPHABLIKI YOMZANTSI AFRIKA UMTHETHO WEEBHANKI ZENTSEBENZISWANO No, 07 ACT To promote and advance the social and economic welfare of all South Africans

TAX GUIDE FOR SMALL BUSINESSES 2011/12

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR SMALL BUSINESSES 2011/12 This document

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR SMALL BUSINESSES 2011/12 This document

Increased Personal Income Tax Rates

flash Alert A Publication for Global Mobility and Tax Professionals by KPMG s Global Mobility Services Practice South Africa Personal Tax Rate, Fringe Benefit Changes in Budget 2015 by KPMG, South Africa

flash Alert A Publication for Global Mobility and Tax Professionals by KPMG s Global Mobility Services Practice South Africa Personal Tax Rate, Fringe Benefit Changes in Budget 2015 by KPMG, South Africa

STANDARD INTERPRETATION GUIDELINE

STANDARD INTERPRETATION GUIDELINE 2019-05 INCOME TAX ACT 2015 INCOME TAX (EMPLOYMENT INCENTIVES) REGULATIONS 2016 EMPLOYMENT INCENTIVES This Standard Interpretation Guideline (SIG) sets out Fiji Revenue

STANDARD INTERPRETATION GUIDELINE 2019-05 INCOME TAX ACT 2015 INCOME TAX (EMPLOYMENT INCENTIVES) REGULATIONS 2016 EMPLOYMENT INCENTIVES This Standard Interpretation Guideline (SIG) sets out Fiji Revenue