ITA88 PROCESS GUIDE ITA88 PROCESS GUIDE AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS

|

|

|

- Deborah Ferguson

- 5 years ago

- Views:

Transcription

1 AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS SEPTEMBER 2010 _v2.indd 1 1 9/21/10 4:10 PM

2 AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS Introduction ITA88 AGENT APPOINTMENT Who will receive an Agent Appointment? Who might be appointed as agents? How will the employer receive the ITA88 Agent Appointment Notice? What will happen if the employer does not act on the SARS Agent Appointment Notice within the given time period? How long does the employer have to pay over the money, in respect of the Agent Appointment, to SARS? What will happen if the employer pays over the outstanding penalty amount but the taxpayer already made payment in respect thereof? What will the ITA88 Agent Appointment Notice look like? PENALTY PAYMENTS TO SARS Making the administrative penalty payment to SARS Using efiling to make your payment Electronic transfer via Internet banking Over the counter at branches of the relevant banking institutions Debit order Over the counter at a SARS branch e@syfile Employer payments THE AGENT APPOINTMENT RECONCILIATION STATEMENT (ITA88R) How will the employer receive the Agent Appointment Reconciliation Statement? How will the Agent Appointment Reconciliation Statement look? What must the employer do with the Agent Appointment Reconciliation Statement? CONTACT INFORMATION 11 2 AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS

3 AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS Introduction Over the past few years there has been a marked increase in the levels of compliance among taxpayers. These are the taxpayers who are helping our country to grow through their compliance. However, one of the major challenges for SARS remains the large number of taxpayers who consistently do not comply with their tax obligations. The sanctioning of such non-compliance was previously limited to criminal sanctions which did not sufficiently deter non-compliance by these taxpayers. It is only fair on the majority of compliant taxpayers that SARS takes tough action against the non-compliant taxpayers, especially those who have consistently failed to comply with their tax obligations over many years. In October last year SARS announced the introduction of new administrative penalties beginning with monthly penalties for taxpayers who had outstanding returns for multiple years. After allowing non-compliant taxpayers a period in which to submit outstanding returns and avoid these stiff penalties, in January this year SARS issued the first round of penalties to approximately taxpayers who had returns outstanding for multiple years. Where the return remains outstanding, the penalty recurs for each month or part thereof, depending on how long the return remains outstanding. On the Penalty Assessment Notice, the taxpayer was informed to both remedy the non-compliance by submitting the outstanding return and to pay the outstanding amount by the due date reflected on the Penalty Assessment Notice. In addition, the taxpayer was advised to submit a Request for Remission (RFR) where he/she was not in agreement with the penalty amounts imposed. The notice also informed the taxpayer that in the event that he/she did not remedy the non-compliance, did not request a remission and did not pay the penalty, SARS will exercise its right to appoint an agent and withhold the applicable amount(s) from his/her salary in terms of Section 99 of the Income Tax Act No.58 of Since the launch of the administrative penalty system taxpayers have been presented with seven penalty notices to date, as well as various reminders. Notwithstanding these notices and reminders, several taxpayers have not responded to SARS s request to remedy the non-compliance, pay the outstanding penalty amount or request a remission of the penalty. As a result, SARS is now exercising the right to appoint employers, or anyone in control of a taxpayer s money, including salaries and wages, to act as an agent on its behalf. This is done by appointing a third party as an agent through the issuing of a Form ITA88 Notice of Agent Appointment. SARS will issue the Agent Appointment Notice in the following manner: Via the the e@syfile Employer application Via the post using the employer s postal address. On receipt of the ITA88 Agent Appointment Notice, the employer must do the following: Review the list of impacted taxpayers (manage outcomes) Deduct the stipulated amount from the salary or wages of the respective employees, as indicated on the ITA88 Agent Appointment Notice Pay the amounts over to SARS by the due date, as indicated on the ITA88 Agent Appointment Notice. Where the employer is unable to execute the request, the employer must provide feedback on reasons for his/her inability to execute the agent appointment request using one of the following channels: Log on to SARS e@syfile Employer to view the ITA88 Agent Appointment Notice and provide a response to SARS by selecting one of the outcomes from the drop-down list Contact the SARS Contact Centre or visit a SARS branch where an agent will assist the employer with capturing the outcomes in relation to the taxpayers listed on the ITA88 Agent Appointment Notice. SEPTEMBER

4 The following diagram aims to illustrate the process involved when SARS issues an employer with an ITA88 Agent Appointment and the course of action that needs to be followed once the ITA88 has been issued to the employer. 4 AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS

5 ITA88 AGENT APPOINTMENT Who will receive an Agent Appointment? A taxpayer will be due for an Agent Appointment if: A penalty amount is outstanding for two months after the issuing of the original penalty No dispute is in progress regarding the penalty (an ITA88 will be issued only against finalised disputes or if the dispute was disallowed or partially allowed) A valid agent can be identified from the information at SARS s disposal. Who might be appointed as agents? Possible agents who can be appointed for individual taxpayers include: Employers Any debtor who owes the taxpayer money Financial institutions, such as banks Attorneys Medical aid schemes (in case of members of the medical fraternity) Investment managers Insurance companies. These agents will only be appointed if they hold money on behalf of the taxpayer. How will the employer receive the ITA88 Agent Appointment Notice? SARS will issue the Agent Appointment Notice in the following manner: Via the e@syfile Employer application Via the post using the employer s postal address. What will happen if the employer does not act on the SARS Agent Appointment Notice within the given time period? In terms of the Income Tax Act No.58 of 1962, SARS will hold the employer personally liable for the outstanding administrative penalty or penalties, in the event that the employer does indeed hold money on behalf of the taxpayer. How long does the employer have to pay over the money, in respect of the Agent Appointment, to SARS? The payment due date will be reflected on the ITA88 Agent Appointment Notice that will be sent to relevant employers. What will happen if the employer pays over the outstanding penalty amount but the taxpayer already made payment in respect thereof? The overpayment will be refunded to the taxpayer. SEPTEMBER

salary or wages and pay")

6 What will the ITA88 Agent Appointment Notice look like? The PAYE reference number will be used to identify the employer in all engagements related to agent appointments. The content explains the employer s obligation to deduct the money owed to SARS in respect of outstanding administrative penalties, from the specific employee/s (taxpayer/s ) salary or wages and pay it over to SARS. It also explains how the employer can engage with SARS if the employer is unable to fulfil this obligation. The next section of the notice will contain any combination of three separate tables: The ITA88 Agent Appointment Created table shows all the new agent appointments issued against employees of the employer The ITA88 Agent Appointment Cancelled table contains all the cancelled agent appointments as well as the applicable reasons for cancellation The ITA88 Agent Appointment Defaulted table shows all overdue agent appointments and any payments in respect of the employee. 6 AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS _v2.indd 6 9/21/10 4:10 PM

7 The ITA88 Agent Appointment Created table contains a listing of all employees in respect of which the employer has been appointed as an agent. Each employees name, tax reference, and ID number has been supplied for ease of identification. The ITA88 Transaction number is the unique reference number which, together with the employer s PAYE tax reference number, should be quoted when resolving any queries with SARS The monthly instalments ( ITA88 Monthly Deduction ) and total amount ( ITA88 amount due by Taxpayer at issue date ) are reflected. The employer is responsible for paying the monthly instalment by the due date stipulated. In instances of affordability (ie taxpayer not able to afford the total amount as one salary deduction), the total value will be broken into instalments, indicated by: the ITA88 Start Date and ITA88 End Date will be different. The start date is the date by which the first instalment should be paid whereas the end date is the date by which the last instalment must be paid, and, the instalment value will be less than the total amount. The ITA88 amount due by Taxpayer at issue date divided by the ITA88 Monthly Deduction indicates the number of instalments Each ITA88 appointment contains the 19-digit Payment Reference Number that must be used when making payment. It is essential the this number is correctly quoted so that the payment is correctly reflected and allocated to the taxpayer s account. The ITA88 Agent Appointment Cancelled table contains a listing of all employees where the ITA88 appointment previously issued, has been cancelled The ITA88 Transaction number can be used to trace the cancellation back to the original appointment, reflected in the table, ITA88 Agent Appointment Created The amount and date the agent appointment was cancelled A cancellation reason is recorded against each transaction. Typically it would reflect the reason or outcome as communicated to SARS by the employer (for example, taxpayer no longer employed; taxpayer can t afford deductions, etc). SEPTEMBER

8 The ITA88 Agent Appointment Defaulted table contains a listing of all employees where the ITA88 instalment is 30 days overduethe employee s information Each default transaction contains unique ITA88 transaction number to which the default refers, original amount at the issue date of the ITA88 Agent Appointment Notice, payments received to date, and, the default amount still outstanding The 19-digit Payment Reference Number that must be used when making payment is also provided. This reference must be used to ensure that the payment is correctly reflected and allocated to the taxpayer s account. On receipt of the ITA88 Agent Appointment Notice, the employer must do the following: Review the list of impacted employees Deduct the stipulated amount from the salary or wages of the respective employees, as indicated on the ITA88 Agent Appointment Notice Pay the amounts over to SARS by the due date, as indicated on the ITA88 Agent Appointment Notice. Where the employer is unable to execute the request to withhold the stipulated amount against the salaries and wages of the employee as requested by SARS, the employer must provide feedback on reasons for his/her inability to execute the agent appointment request via one of the following channels: Employer to log on to SARS e@syfile Employer to view the ITA88 Agent Appointment Notice and provide a response to SARS by selecting one of the outcomes from the drop-down list Contact the SARS Contact Centre or visit a SARS branch where an agent will assist the employer with capturing of the responses in relation to the employees listed on the ITA88 Agent Appointment Notice Important note on affordability Because the employer has more information about the employee s financial situation, the employer is advised to use its discretion when determining whether or not the employee is able to afford the once-off lump sum deduction from his/her salary or wages or if monthly instalments over a period of time determined by SARS would be a better alternative. 8 AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS

9 PENALTY PAYMENTS TO SARS Making the administrative penalty payment to SARS The following channels are available to employers for the payment of administrative penalty amounts to SARS: efiling Electronic transfer via Internet banking Over the counter at branches of the relevant banking institutions Debit order Over the counter at a SARS branch e@syfile Employer application. Using efiling to make your payment efiling is the free, secure electronic tax return and payment submission service offered by SARS to eliminate the risks and hassles associated with the submission of manual tax returns and payments. SARS efiling provides far more convenient, reliable and accurate electronic payment facilities. efiling is supported by the following banking institutions, namely ABSA, FNB, Investec, Nedbank and Standard Bank. To access efiling, visit Electronic transfer via Internet banking Payments can be made directly to SARS using the internet banking services offered by ABSA, FNB, Investec, Nedbank and Standard Bank. It is imperative that the correct payment reference information is provided in all instances to ensure that tax payments are easily identified and correctly allocated by SARS. The following items are essential to ensure that payments are processed correctly: 1. SARS beneficiary account ID 2. A 19-digit bank payment reference number. This tells SARS exactly who the client is and enables the allocation of such payment to a specific tax/duty and period. For the payment of administrative penalty amounts, the employer needs to use the unique 19-digit PRN as it appears on the relevant payment form. The beneficiary ID that is applicable to ABSA, FNB, Nedbank and Standard Bank payments in respect of administrative penalties is SARS-ITA. Over the counter at branches of the relevant banking institutions Any payment can be made at any ABSA, FNB, Nedbank or Standard Bank branch. These payments must comply with the same payment referencing requirements used for internet payments. Banks require the following information in order to accept and process SARS payments: SARS tax form/payment advice containing the 19-digit payment reference number and the tax type that the employer intends paying (administrative penalty) The amount due. In order for SARS to process the clients payment in a timely and accurate manner, it is imperative that the correct information is supplied to the banke when making over the counter payments. The bank will reject all payments which do not conform to the payment reference criteria listed above. Please note that the SARS tax form/payment advice stipulates the information needed to initiate the deposit. Cheque payments must be made out to South African Revenue Service (no abbreviation allowed), in any of the official languages. SEPTEMBER

Once the employer has made the required payment for those confirmed employees, SARS will issue the employer with")

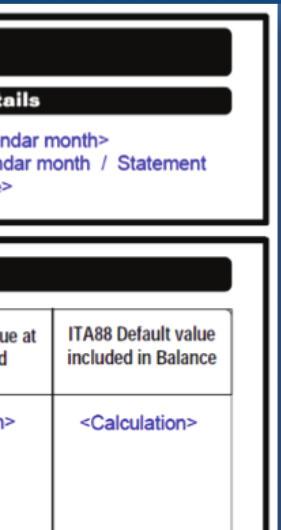

10 Debit order Debit orders made at SARS will not be activated in respect of efiling. Once registered for efiling, any debit order made with SARS will automatically be cancelled. The client must then initiate a new debit order arrangement with efiling. Over the counter at a SARS branch Payment can be made during Cash Hall office hours at any SARS branch. For ease of processing, employers should ensure that the tax form/payment advice indicating the taxpayer reference number, tax type and tax period is attached to all payments. e@syfile Employer payments For payments using e@syfile Employer, kindly refer to the e@syfile Employer User Guide available on the SARS website THE AGENT APPOINTMENT RECONCILIATION STATEMENT (ITA88R) Once the employer has made the required payment for those confirmed employees, SARS will issue the employer with an Agent Appointment Reconciliation Statement ITA88R at the end of every month. How will the employer receive the Agent Appointment Reconciliation Statement? SARS will issue the Agent Appointment Reconciliation Statement in the following manner: Via the e@syfile Employer application Via the post using the employer s postal address. How will the Agent Appointment Reconciliation Statement look? The Agent Appointment Reconciliation Statement ITA88R cover page contains similar information to that of the ITA88 Agent Appointment Notice. The statement contains the agent appointment movements for the employer during the previous calendar month. The Statement From Date and Statement To Date states the calendar month for which the statement was generated The statement contains the employee s or employees information 10 AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS

11 The opening balance at the beginning of the month is stated New agent appointments created, agent appointments cancelled and payments received are indicated The closing balance at the end of the month is indicated Any amount in default is indicated. What must the employer do with the Agent Appointment Reconciliation statement? Once the employer has received the ITA88R and is satisfied with the correctness of its content, SARS advises that the ITA88R be filed in the event that a dispute arises in the future. CONTACT INFORMATION If you need information on your agent appointment you can contact the SARS Contact Centre on SARS (7277). A list of Frequently Asked Questions (FAQs) has also been compiled to assist employers in understanding the process please go to SEPTEMBER

12 Lehae la SARS 299 Bronkhorst Street Nieuw Muckleneuk 0181 Private Bag X923 Pretoria AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

OVERVIEW PAYE 2010 NOVEMBER

OVERVIEW PAYE 2010 NOVEMBER 1 Contents 1. Introduction... 3 2. The aim of the Pay-As-You-Earn (PAYE) reconciliation process... 3 3. What is reconciliation?... 4 4. The Pay-As-You-Earn (PAYE) process...

OVERVIEW PAYE 2010 NOVEMBER 1 Contents 1. Introduction... 3 2. The aim of the Pay-As-You-Earn (PAYE) reconciliation process... 3 3. What is reconciliation?... 4 4. The Pay-As-You-Earn (PAYE) process...

Overview of PAYE reconciliation process and 2007/08 policy changes. Another helpful guide brought to you by South African Revenue Service

Overview of PAYE reconciliation process and 2007/08 policy changes Another helpful guide brought to you by South African Revenue Service Overview of PAYE reconciliation process and 2007/08 policy changes

Overview of PAYE reconciliation process and 2007/08 policy changes Another helpful guide brought to you by South African Revenue Service Overview of PAYE reconciliation process and 2007/08 policy changes

External Guide on how to submit a Request for Remission

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

EXTERNAL GUIDE HOW TO SUBMIT AN OBJECTION OR APPEAL VIA EFILING

TABLE OF CONTENTS 1 PURPOSE 3 2 INTRODUCTION 3 3 LOGON TO THE EFILING WEBSITE 4 3.1 ACCESS THE REQUEST FOR OBJECTION OR APPEAL FORM AND ADMINISTRATIVE PENALTY ASSESSMENT NOTICE 4 3.2 DETAILED PROCEDURES

TABLE OF CONTENTS 1 PURPOSE 3 2 INTRODUCTION 3 3 LOGON TO THE EFILING WEBSITE 4 3.1 ACCESS THE REQUEST FOR OBJECTION OR APPEAL FORM AND ADMINISTRATIVE PENALTY ASSESSMENT NOTICE 4 3.2 DETAILED PROCEDURES

EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling

2013 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling 1 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling DISCLAIMER The information contained in this guide

2013 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling 1 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling DISCLAIMER The information contained in this guide

SAPA Conference Spier, Stellenbosch 04 August March

SAPA Conference Spier, Stellenbosch 04 August 2011 17 March INTRODUCTION PAYE processes and forms, over the past few years, have been aggressively modernised so as to ensure better alignment between PAYE

SAPA Conference Spier, Stellenbosch 04 August 2011 17 March INTRODUCTION PAYE processes and forms, over the past few years, have been aggressively modernised so as to ensure better alignment between PAYE

REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER 0 Initial Release A Scheepers GM Operational Services

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

EXTERNAL FREQUENTLY ASKED QUESTIONS DISPUTE ADMINISTRATION

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

Welcome to the SARS Tax Workshop

29 August 2017 Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more

29 August 2017 Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more

efiling Account Management Guide - Payment Allocation

efiling Account Management Guide - Payment Allocation CONTENTS 1. How to obtain a payment listing... 1 2. How to allocate a payment... 3 3. How to re-allocate a payment... 6 4. How to request a payment

efiling Account Management Guide - Payment Allocation CONTENTS 1. How to obtain a payment listing... 1 2. How to allocate a payment... 3 3. How to re-allocate a payment... 6 4. How to request a payment

Tough New Penalties for outstanding income tax returns

Tough New Penalties for outstanding income tax returns New penalties System to be implemented as from 23 November 2009 Penalties 1 INTRODUCTION Individual taxpayers have a window of opportunity until 20

Tough New Penalties for outstanding income tax returns New penalties System to be implemented as from 23 November 2009 Penalties 1 INTRODUCTION Individual taxpayers have a window of opportunity until 20

Service Charter. South African Revenue Service Service Charter

Service Charter South African Revenue Service Service Charter 1 South African Revenue Service Your Rights Obligations and Service timelines 2 Service Charter WHAT WE DO IN SOUTH AFRICA We, the South African

Service Charter South African Revenue Service Service Charter 1 South African Revenue Service Your Rights Obligations and Service timelines 2 Service Charter WHAT WE DO IN SOUTH AFRICA We, the South African

Introduction. Lerato Mokoena (SARS Support Consultant-eFiling and specialist) Gauteng and Northwest Province

Gauteng and Northwest Province") Introduction Lerato Mokoena (SARS Support Consultant-eFiling and E@syfile specialist) Gauteng and Northwest Province lmokoena2@sars.gov.za Topics to be discussed Tax Compliance status Functionality on

Introduction Lerato Mokoena (SARS Support Consultant-eFiling and E@syfile specialist) Gauteng and Northwest Province lmokoena2@sars.gov.za Topics to be discussed Tax Compliance status Functionality on

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

EXTERNAL REFERENCE GUIDE SECURITIES TRANSFER TAX. EXTERNAL GUIDE - SECURITIES TRANSFER TAX GEN-PAYM-11-G01 Revision: 3 EFFECTIVE DATE:

2013 EXTERNAL REFERENCE GUIDE SECURITIES EXTERNAL GUIDE - SECURITIES Revision: 3 EFFECTIVE DATE: 2013.11.30 DISCLAIMER The information contained in this guide is intended as guidance only and is not considered

2013 EXTERNAL REFERENCE GUIDE SECURITIES EXTERNAL GUIDE - SECURITIES Revision: 3 EFFECTIVE DATE: 2013.11.30 DISCLAIMER The information contained in this guide is intended as guidance only and is not considered

A QUICK GUIDE TO DIVIDENDS TAX

A QUICK GUIDE TO DIVIDENDS TAX i A QUICK GUIDE TO DIVIDENDS TAX 1. INTRODUCTION TO DIVIDENDS TAX In 2007, the Minister of Finance announced that Secondary Tax on Companies (STC) would be replaced by Dividends

A QUICK GUIDE TO DIVIDENDS TAX i A QUICK GUIDE TO DIVIDENDS TAX 1. INTRODUCTION TO DIVIDENDS TAX In 2007, the Minister of Finance announced that Secondary Tax on Companies (STC) would be replaced by Dividends

Dot not submit your application if you do not agree to or thoroughly understand our Terms and Conditions.

TERMS AND CONDITIONS The following websites are divisions of The Finance Turtle Group a registered company in the Republic of South Africa with Registration number: 2009/171156/23; www.loans4africa.co.za

TERMS AND CONDITIONS The following websites are divisions of The Finance Turtle Group a registered company in the Republic of South Africa with Registration number: 2009/171156/23; www.loans4africa.co.za

WHAT TO DO WITH YOUR IRP YEAR OF ASSESSMENT

WHAT TO DO WITH YOUR IRP5 2014 YEAR OF ASSESSMENT Office staff must take into account the undermentioned on receipt of their IRP5 tax certificates for the 2014 tax year ended 28 February 2014. Contact

WHAT TO DO WITH YOUR IRP5 2014 YEAR OF ASSESSMENT Office staff must take into account the undermentioned on receipt of their IRP5 tax certificates for the 2014 tax year ended 28 February 2014. Contact

Welcome to the SARS Tax Workshop

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Make your money work for you. Not your bank.

Make your money work for you. Not your bank. beyond a bank Transactional TRANSACTIONAL BANKING Sasfin Transactional Banking accounts make your money work for you, not your bank. Our Business Banking account

Make your money work for you. Not your bank. beyond a bank Transactional TRANSACTIONAL BANKING Sasfin Transactional Banking accounts make your money work for you, not your bank. Our Business Banking account

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

NPM PRIVACY NOTICE Personal Data and Full Process:

Company Name National Parking Management Limited Company Number 08237818 Registered in England and Wales Registered Address 20 Francis Street Northampton NN1 2NZ Data Protection Officer Contact Details

Company Name National Parking Management Limited Company Number 08237818 Registered in England and Wales Registered Address 20 Francis Street Northampton NN1 2NZ Data Protection Officer Contact Details

Quick Start Guide to Payroll Tax Year-End

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

EXTERNAL GUIDE GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017

GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 BACKGROUND 3 3.1 RECONCILIATION PROCESS 3 3.2 INTERIM RECONCILIATION PROCESS 3 3.3 GENERAL

GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 BACKGROUND 3 3.1 RECONCILIATION PROCESS 3 3.2 INTERIM RECONCILIATION PROCESS 3 3.3 GENERAL

Engagement Letter. 27 May Taxation Secretarial Accounting Statutory Services. P O Box Kyalami Midrand South Africa

Engagement Letter 27 May 2014 ENGAGEMENT LETTER FOR SERVICES Individuals Company Close Corporation Trust Partnership Other Date: Dear Sirs/Madams, We are pleased to confirm the arrangements for Technical

Engagement Letter 27 May 2014 ENGAGEMENT LETTER FOR SERVICES Individuals Company Close Corporation Trust Partnership Other Date: Dear Sirs/Madams, We are pleased to confirm the arrangements for Technical

Clubs or societies return guide 2012

IR 9GU March 2012 Clubs or societies return guide 2012 Read this guide to help you fill in your IR 9 return. Complete and send us your IR 9 return by 7 July 2012, unless you have an extension of time to

IR 9GU March 2012 Clubs or societies return guide 2012 Read this guide to help you fill in your IR 9 return. Complete and send us your IR 9 return by 7 July 2012, unless you have an extension of time to

Please address all correspondences to the Director: Finance, and always quote your student number. Private Bag X5050 THOHOYANDOU 0950

STUDENT FEES 2018 CORRESPONDENCES Please address all correspondences to the Director: Finance, and always quote your student number. Postal Address: CALENDARS University of Venda Private Bag X5050 THOHOYANDOU

STUDENT FEES 2018 CORRESPONDENCES Please address all correspondences to the Director: Finance, and always quote your student number. Postal Address: CALENDARS University of Venda Private Bag X5050 THOHOYANDOU

What s new at SARS? VAT COMPLIANCE

This image cannot currently be displayed. This image cannot currently be displayed. 2015/11/11 What s new at SARS? VAT COMPLIANCE 1 This image cannot currently be displayed. This image cannot currently

This image cannot currently be displayed. This image cannot currently be displayed. 2015/11/11 What s new at SARS? VAT COMPLIANCE 1 This image cannot currently be displayed. This image cannot currently

City of Johannesburg - Accounts

EVERY month, the City sends out about 900 000 accounts for rates and services via the post. But it s also possible to get these monthly bills via email. All you have to do is register with the City's e-services.

EVERY month, the City sends out about 900 000 accounts for rates and services via the post. But it s also possible to get these monthly bills via email. All you have to do is register with the City's e-services.

Employer Easy File Q & A

Employer Easy File Q & A Trouble Shooting Solutions Employer installed e@syfile Employer version 6.0.0 and having troubles login: Confirm if employer made a backup in version 5.0.9 If Yes, copy version

Employer Easy File Q & A Trouble Shooting Solutions Employer installed e@syfile Employer version 6.0.0 and having troubles login: Confirm if employer made a backup in version 5.0.9 If Yes, copy version

FREQUENTLY ASKED QUESTIONS COMPLETION AND SUBMISSION OF CSV. TM EMPLOYER AND ZIPCENTRALFILE RECONCILIATION DOCUMENTS

FREQUENTLY ASKED QUESTIONS Revision: 1 Page 1 of 8 1 PURPOSE The purpose of this document is to provide answers to frequently asked questions by employers in respect of creating CSV data files and submitting

FREQUENTLY ASKED QUESTIONS Revision: 1 Page 1 of 8 1 PURPOSE The purpose of this document is to provide answers to frequently asked questions by employers in respect of creating CSV data files and submitting

Points Of Discussion

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

MFC AUCTIONS STEP BY STEP ONLINE AUCTION GUIDE. MFC a division of Nedbank

MFC AUCTIONS STEP BY STEP ONLINE AUCTION GUIDE MFC a division of Nedbank MFC AUCTIONS 5 STEPS TO BUYING A VEHICLE ON AUCTION View (Auctions) Browse the Auctions and view the catalogue of available vehicles

MFC AUCTIONS STEP BY STEP ONLINE AUCTION GUIDE MFC a division of Nedbank MFC AUCTIONS 5 STEPS TO BUYING A VEHICLE ON AUCTION View (Auctions) Browse the Auctions and view the catalogue of available vehicles

TCS (Tax Clearance Status) November 2018

November 2018") TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

Omission of source code 4582

Return Submission ETI Omission of source code 4582 With the implementation of the Retirement Reform requirements, information code 4582 and its value were omitted from the submission file created by e@syfile

Return Submission ETI Omission of source code 4582 With the implementation of the Retirement Reform requirements, information code 4582 and its value were omitted from the submission file created by e@syfile

Clubs or societies return guide 2018

IR9G March 2018 Clubs or societies return guide 2018 Read this guide to help you fill in your IR9 return. Complete and send us your IR9 return by 7 July 2018, unless you have an extension of time to file

IR9G March 2018 Clubs or societies return guide 2018 Read this guide to help you fill in your IR9 return. Complete and send us your IR9 return by 7 July 2018, unless you have an extension of time to file

RETIREMENT ANNUITY FUND Application Form

RETIREMENT ANNUITY FUND Application Form IMPORTANT INFORMATION Before investing, read the Terms and Conditions of the Fund carefully to decide if the product meets your financial needs. Consider getting

RETIREMENT ANNUITY FUND Application Form IMPORTANT INFORMATION Before investing, read the Terms and Conditions of the Fund carefully to decide if the product meets your financial needs. Consider getting

ENDOWMENT APPLICATION

ENDOWMENT APPLICATION Instructions 1. This application and supporting documentation must be emailed to instruct@ashburtoninvest.co.za. 2. Please complete all relevant sections of this application in order

ENDOWMENT APPLICATION Instructions 1. This application and supporting documentation must be emailed to instruct@ashburtoninvest.co.za. 2. Please complete all relevant sections of this application in order

Discretionary Investment Application

Discretionary Investment Application Wealthport (Pty) Ltd (2012/025878/07) Wealthport (Pty) Ltd ( Wealthport ) is an Authorised Financial Services Provider (FSP No. 44158) Ballyoaks Office Park, 35 Ballyclare

Discretionary Investment Application Wealthport (Pty) Ltd (2012/025878/07) Wealthport (Pty) Ltd ( Wealthport ) is an Authorised Financial Services Provider (FSP No. 44158) Ballyoaks Office Park, 35 Ballyclare

EXTERNAL GUIDE. How to efile your Provisional Tax Return

1. Register For efiling You will need to register as an efiling user before you can file your provisional tax return electronically. To register, go to www.sarsefiling.co.za 1.1. Click on Register 1.2.

1. Register For efiling You will need to register as an efiling user before you can file your provisional tax return electronically. To register, go to www.sarsefiling.co.za 1.1. Click on Register 1.2.

FAQs: Increase in the VAT rate from 1 April 2018 Value-Added Tax

Value-Added Tax Frequently Asked Questions: Increase in the VAT rate 1 In the Minister s Budget speech on 21 February 2018, an increase in the standard rate of VAT was announced. The rate increase applies

Value-Added Tax Frequently Asked Questions: Increase in the VAT rate 1 In the Minister s Budget speech on 21 February 2018, an increase in the standard rate of VAT was announced. The rate increase applies

FNB Investments Tax Free Savings Account Application

FNB Investments Tax Free Savings Account Application Instructions 1. This application and supporting documentation must be emailed to or fax it to 0860 762 468. 2. Please complete all relevant sections

FNB Investments Tax Free Savings Account Application Instructions 1. This application and supporting documentation must be emailed to or fax it to 0860 762 468. 2. Please complete all relevant sections

Direct Earnings Attachment. A Guide for employers

Direct Earnings Attachment A Guide for employers February 2017 What this Guide is about This guide explains what you, as an employer, need to do if Debt Management, as part of the Department for Communities

Direct Earnings Attachment A Guide for employers February 2017 What this Guide is about This guide explains what you, as an employer, need to do if Debt Management, as part of the Department for Communities

A Guide for Employers Date: August 2016

Direct Earnings Attachment A Guide for Employers Date: August 2016 v3.0 December 2017 What this Guide is about This guide explains what you, as an employer, need to do if Debt Management, as part of the

Direct Earnings Attachment A Guide for Employers Date: August 2016 v3.0 December 2017 What this Guide is about This guide explains what you, as an employer, need to do if Debt Management, as part of the

P U B L I C R E L E A S E

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

Ayanda Takela. SARS efiling and Specialist (Gauteng, Free State & Northern Cape Region)

") Ayanda Takela SARS efiling and e@syfile Specialist (Gauteng, Free State & Northern Cape Region) Topics to be discussed General errors experienced on SARS efiling profiles General errors experienced on

Ayanda Takela SARS efiling and e@syfile Specialist (Gauteng, Free State & Northern Cape Region) Topics to be discussed General errors experienced on SARS efiling profiles General errors experienced on

PUBLIC RELEASE. Document Classification: Official Publication. South African Revenue Service 2011

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published document SARS

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published document SARS

EXTERNAL FREQUENTLY ASKED QUESTIONS TAXPAYER CENTRICITY (CLIENT APPROACH. FUNCTIONALITY ON efiling)

") EXTERNAL FREQUENTLY ASKED S TAXPAYER CENTRICITY (CLIENT APPROACH FUNCTIONALITY ON Revision: 0 Page 1 of 6 1 PURPOSE These FAQs provide general information regarding taxpayer centricity, which is a new

EXTERNAL FREQUENTLY ASKED S TAXPAYER CENTRICITY (CLIENT APPROACH FUNCTIONALITY ON Revision: 0 Page 1 of 6 1 PURPOSE These FAQs provide general information regarding taxpayer centricity, which is a new

P U B L I C R E L E A S E

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2012 Page 1 of 55 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2012 Page 1 of 55 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

ENDOWMENT TAX-FREE SAVINGS ACCOUNT Application Form

ENDOWMENT TAX-FREE SAVINGS ACCOUNT Application Form IMPORTANT INFORMATION Before investing, read the Terms and Conditions of the Policy carefully to decide if the product meets your financial needs. Consider

ENDOWMENT TAX-FREE SAVINGS ACCOUNT Application Form IMPORTANT INFORMATION Before investing, read the Terms and Conditions of the Policy carefully to decide if the product meets your financial needs. Consider

Direct Earnings Attachment. A Guide for employers

Direct Earnings Attachment A Guide for employers August 2016 Direct Earnings Attachment A Guide for Employers Publication Date: August 2016 1 What this Guide is about This guide explains what you, as an

Direct Earnings Attachment A Guide for employers August 2016 Direct Earnings Attachment A Guide for Employers Publication Date: August 2016 1 What this Guide is about This guide explains what you, as an

From IRP5 to tax assessment 15 minutes CPD

From IRP5 to tax assessment 15 minutes CPD By ADV. CARIEN VAN DIJK IRP5s are somewhat like family: they can cause you a lot of headaches but you can t (and probably don t want to) live without them. This

From IRP5 to tax assessment 15 minutes CPD By ADV. CARIEN VAN DIJK IRP5s are somewhat like family: they can cause you a lot of headaches but you can t (and probably don t want to) live without them. This

PUBLIC RELEASE. Document Classification: Official Publication. South African Revenue Service 2009

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

Applying to join the Discovery Health Medical Scheme as part of an employer group in 2018

Applying to join the Discovery Health Medical Scheme as part of an employer group in 2018 Contact us Tel (Members): 0860 99 88 77, Tel (Health partners): 0860 44 55 66, PO Box 784262, Sandton, 2146, www.discovery.co.za

Applying to join the Discovery Health Medical Scheme as part of an employer group in 2018 Contact us Tel (Members): 0860 99 88 77, Tel (Health partners): 0860 44 55 66, PO Box 784262, Sandton, 2146, www.discovery.co.za

Disputing an assessment

IR776 June 2018 Disputing an assessment What to do if you dispute an assessment 2 DISPUTING AN ASSESSMENT Introduction While we make every effort to apply the tax laws fairly and correctly, there may be

IR776 June 2018 Disputing an assessment What to do if you dispute an assessment 2 DISPUTING AN ASSESSMENT Introduction While we make every effort to apply the tax laws fairly and correctly, there may be

CUSTOMS EXTERNAL POLICY PAYMENTS

CUSTOMS EXTERNAL POLICY PAYMENTS Revision: 3 Page 1 of 11 TABLE OF CONTENTS 1 SCOPE 3 2 POLICY 3 2.1 Date of payment 3 2.2 Proof of payment 3 2.3 Acceptable payment methods 3 2.3.1 Electronic payments

CUSTOMS EXTERNAL POLICY PAYMENTS Revision: 3 Page 1 of 11 TABLE OF CONTENTS 1 SCOPE 3 2 POLICY 3 2.1 Date of payment 3 2.2 Proof of payment 3 2.3 Acceptable payment methods 3 2.3.1 Electronic payments

AMERICAN EXPRESS CHARGE CARDS TERMS & CONDITIONS

AMERICAN EXPRESS CHARGE CARDS TERMS & CONDITIONS American Express Charge Cards THE PARTIES TO THE AGREEMENT The parties to this Cardmember Agreement (the "Agreement") are AMEX (Middle East) B.S.C. (c)

AMERICAN EXPRESS CHARGE CARDS TERMS & CONDITIONS American Express Charge Cards THE PARTIES TO THE AGREEMENT The parties to this Cardmember Agreement (the "Agreement") are AMEX (Middle East) B.S.C. (c)

A STEP-BY-STEP GUIDE TO THE EMPLOYER RECONCILIATION PROCESS

EF NO. Trading or Other Name: Transaction Year: Time Stamp: 21159840 A STEP-BY-STEP GUIDE TO THE EMPLOYE ECONCILIATION POCESS Transaction Year (CCYY) Period of econciliation (CCYYMM) Business Information

EF NO. Trading or Other Name: Transaction Year: Time Stamp: 21159840 A STEP-BY-STEP GUIDE TO THE EMPLOYE ECONCILIATION POCESS Transaction Year (CCYY) Period of econciliation (CCYYMM) Business Information

Individual Income Tax

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

BULBANK ONLINE ELECTRONIC BANKING SERVICE GENERAL TERMS AND CONDITIONS

BULBANK ONLINE ELECTRONIC BANKING SERVICE GENERAL TERMS AND CONDITIONS I. SUBJECT OF THE SERVICE 1. Through the BULBANK ONLINE electronic banking service, UNICREDIT BULBANK AD (hereinafter referred to

BULBANK ONLINE ELECTRONIC BANKING SERVICE GENERAL TERMS AND CONDITIONS I. SUBJECT OF THE SERVICE 1. Through the BULBANK ONLINE electronic banking service, UNICREDIT BULBANK AD (hereinafter referred to

EXTERNAL GUIDE HOW TO COMPLETE AND SUBMIT YOUR COUNTRY BY COUNTRY INFORMATION

TABLE OF CONTENTS TABLE OF CONTENTS 2 1 PURPOSE 3 2 INTRODUCTION 3 3 THE CBC SUBMISSION 4 3.1 PERSON REQUIRED TO SUBMIT THE CBC 4 3.2 COMPLETE THE CBC REPORT, THE MASTER AND LOCAL FILE 4 3.3 SUBMIT CBC01

TABLE OF CONTENTS TABLE OF CONTENTS 2 1 PURPOSE 3 2 INTRODUCTION 3 3 THE CBC SUBMISSION 4 3.1 PERSON REQUIRED TO SUBMIT THE CBC 4 3.2 COMPLETE THE CBC REPORT, THE MASTER AND LOCAL FILE 4 3.3 SUBMIT CBC01

ANZ CREDIT CARDS CONDITIONS OF USE CONSUMER CREDIT CARDS

ANZ CREDIT CARDS CONDITIONS OF USE 10.2017 CONSUMER CREDIT CARDS Containing terms and conditions for: ANZ Consumer Credit Cards ANZ Internet Banking ANZ Phone Banking ANZ Mobile Banking BPAY ANZ Contacts

ANZ CREDIT CARDS CONDITIONS OF USE 10.2017 CONSUMER CREDIT CARDS Containing terms and conditions for: ANZ Consumer Credit Cards ANZ Internet Banking ANZ Phone Banking ANZ Mobile Banking BPAY ANZ Contacts

Tax year end processing

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

ANZ ASSURED & PERSONAL OVERDRAFT

ANZ ASSURED & PERSONAL OVERDRAFT TERMS AND CONDITIONS 12.2017 Introduction If you are thinking about obtaining a personal credit facility from ANZ or have any questions about your existing facility, simply

ANZ ASSURED & PERSONAL OVERDRAFT TERMS AND CONDITIONS 12.2017 Introduction If you are thinking about obtaining a personal credit facility from ANZ or have any questions about your existing facility, simply

Unit Trusts Application Form Non - Individual Investors (new investors only)

") Unit Trusts Application Form Non - Individual Investors (new investors only) To view the full list of funds and the Minimum Disclosure Documents (MDD's) with applicable fund minimums and fees, refer to

Unit Trusts Application Form Non - Individual Investors (new investors only) To view the full list of funds and the Minimum Disclosure Documents (MDD's) with applicable fund minimums and fees, refer to

2.2 Calendar Year means from 1 January until 31 December of each year;

Subscription Terms for Purchase of Document Packs and Updates 1. Introduction 1.1 This document sets out the terms and conditions ( the Terms ) pertaining to the subscription of various Document Packs

Subscription Terms for Purchase of Document Packs and Updates 1. Introduction 1.1 This document sets out the terms and conditions ( the Terms ) pertaining to the subscription of various Document Packs

General Terms and Conditions for the Opening and Use of Deposit Accounts

General Terms and Conditions for the Opening and Use of Deposit Accounts Landsbankinn hf. No. 1529-01 September 2017 These Terms and Conditions apply to all deposit accounts established with Landsbankinn

General Terms and Conditions for the Opening and Use of Deposit Accounts Landsbankinn hf. No. 1529-01 September 2017 These Terms and Conditions apply to all deposit accounts established with Landsbankinn

ENDOWMENT POLICY Application Form for Individual Investors

ENDOWMENT POLICY Application Form for Individual Investors IMPORTANT INFORMATION Before investing, read the Terms and Conditions of the Policy carefully to decide if the product meets your financial needs.

ENDOWMENT POLICY Application Form for Individual Investors IMPORTANT INFORMATION Before investing, read the Terms and Conditions of the Policy carefully to decide if the product meets your financial needs.

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

Impact Summary: Modernising the correction of errors in PAYE information

Impact Summary: Modernising the correction of errors in PAYE information Section 1: General information Purpose Inland Revenue is solely responsible for the analysis and advice set out in this Impact Summary,

Impact Summary: Modernising the correction of errors in PAYE information Section 1: General information Purpose Inland Revenue is solely responsible for the analysis and advice set out in this Impact Summary,

Māori authorities tax return/annual Māori authority credit account return guide 2013

IR 8G November 2012 Māori authorities tax return/annual Māori authority credit account return guide 2013 Complete and send us your IR 8 and IR 8J return by 7 July 2013, unless you have an extension of

IR 8G November 2012 Māori authorities tax return/annual Māori authority credit account return guide 2013 Complete and send us your IR 8 and IR 8J return by 7 July 2013, unless you have an extension of

SARS approach to Government institutions

SARS approach to Government institutions 1. SARS focusses on the Tax Compliance of Government Institutions at a National, Provincial and Local Level. 2. SARS Risks that we focus are: Correct Registration,

SARS approach to Government institutions 1. SARS focusses on the Tax Compliance of Government Institutions at a National, Provincial and Local Level. 2. SARS Risks that we focus are: Correct Registration,

Al. Jerozolimskie 123A; Warszawa, Poland

Agreement version: 1.0. Applicable as of: 31.05.2017 In force as of: 31.05.2017 LOAN AGREEMENT NO. Riga 2018-06-13 This Loan Agreement is concluded by and between: LENDER: First name, Last name /Company

Agreement version: 1.0. Applicable as of: 31.05.2017 In force as of: 31.05.2017 LOAN AGREEMENT NO. Riga 2018-06-13 This Loan Agreement is concluded by and between: LENDER: First name, Last name /Company

American Express Corporate Card Cardmember Agreement Joint & Several Liability

American Express Corporate Card Cardmember Agreement Joint & Several Liability American Express Corporate Card THE PARTIES TO THE AGREEMENT The parties to this Cardmember Agreement (the "Agreement") are

American Express Corporate Card Cardmember Agreement Joint & Several Liability American Express Corporate Card THE PARTIES TO THE AGREEMENT The parties to this Cardmember Agreement (the "Agreement") are

Simplifying taxpayer requirements. A Government discussion paper on proposals for change

Simplifying taxpayer requirements A Government discussion paper on proposals for change First published in December 1997 by the Inland Revenue Department, PO Box 2198, Wellington, New Zealand. Simplifying

Simplifying taxpayer requirements A Government discussion paper on proposals for change First published in December 1997 by the Inland Revenue Department, PO Box 2198, Wellington, New Zealand. Simplifying

Māori authority tax rules

IR1202 December 2017 Māori authority tax rules This design is an interpretation of the Mangopare pattern and represents partnership Contents Who is this guide for? 3 The Māori authority credit system 3

IR1202 December 2017 Māori authority tax rules This design is an interpretation of the Mangopare pattern and represents partnership Contents Who is this guide for? 3 The Māori authority credit system 3

Absa Retirement Annuity and Preservation Fund

Wealth and Investment Management Unrestricted Absa Retirement Annuity and Preservation Fund Terms and Conditions Absa Investment Management Services Proprietary Limited Reg No 1980/002425/07 Authorised

Wealth and Investment Management Unrestricted Absa Retirement Annuity and Preservation Fund Terms and Conditions Absa Investment Management Services Proprietary Limited Reg No 1980/002425/07 Authorised

PRESERVATION FUND Application Form

PRESERVATION FUND Application Form IMPORTANT INFORMATION Before investing, read the Terms and Conditions of the Fund carefully to decide if the product meets your financial needs. Consider getting financial

PRESERVATION FUND Application Form IMPORTANT INFORMATION Before investing, read the Terms and Conditions of the Fund carefully to decide if the product meets your financial needs. Consider getting financial

Tax-free Savings Application

Tax-free Savings Application Wealthport (Pty) Ltd (2012/025878/07) Wealthport (Pty) Ltd ( Wealthport ) is an Authorised Financial Services Provider (FSP No. 44158) Ballyoaks Office Park, 35 Ballyclare

Tax-free Savings Application Wealthport (Pty) Ltd (2012/025878/07) Wealthport (Pty) Ltd ( Wealthport ) is an Authorised Financial Services Provider (FSP No. 44158) Ballyoaks Office Park, 35 Ballyclare

Registered superannuation funds return guide 2018

IR44G March 2018 Registered superannuation funds return guide 2018 Complete and send us your IR44 return by 7 July 2018, unless you have an extension of time to file - see page 4 of the guide. 2 REGISTERED

IR44G March 2018 Registered superannuation funds return guide 2018 Complete and send us your IR44 return by 7 July 2018, unless you have an extension of time to file - see page 4 of the guide. 2 REGISTERED

Non-resident income tax return guide 2011

IR 3NRG February 2011 Non-resident income tax return guide 2011 Please read page 5 of this guide to see if you have to complete an IR 3NR. This guide is based on New Zealand tax laws at the time of printing

IR 3NRG February 2011 Non-resident income tax return guide 2011 Please read page 5 of this guide to see if you have to complete an IR 3NR. This guide is based on New Zealand tax laws at the time of printing

Exception Report Guide. August 2018

Exception Report Guide August 2018 Quick Payroll Exception Error Guides We understand your day-to-day challenges; this is why we want to try to make your business life easier. We have prepared this guide

Exception Report Guide August 2018 Quick Payroll Exception Error Guides We understand your day-to-day challenges; this is why we want to try to make your business life easier. We have prepared this guide

ANZ V2+Broking For advisers and their clients FREQUENTLY ASKED QUESTIONS

ANZ V2+Broking For advisers and their clients FREQUENTLY ASKED QUESTIONS Adviser FAQs New clients Is the ANZ Cash Investment Account still available? Yes, you still have the option to open either an ANZ

ANZ V2+Broking For advisers and their clients FREQUENTLY ASKED QUESTIONS Adviser FAQs New clients Is the ANZ Cash Investment Account still available? Yes, you still have the option to open either an ANZ

Service Level Agreement Administration of Revenue Recapture

Service Level Agreement Administration of Revenue Recapture Date State of Minnesota Minnesota Department of Revenue And Agency Name Revenue Recapture ID Revised May 9, 2017 1 8 Table of Contents Page Introduction

Service Level Agreement Administration of Revenue Recapture Date State of Minnesota Minnesota Department of Revenue And Agency Name Revenue Recapture ID Revised May 9, 2017 1 8 Table of Contents Page Introduction

Terms of settlement. Contents. Valid as of

Valid as of 01.12.2016 Contents Definitions 2 General provisions 2 Applicable conditions 2 Identification of account and bank 2 Submitting data 3 Commission fee 3 Rights and obligations of SEB 3 Term of

Valid as of 01.12.2016 Contents Definitions 2 General provisions 2 Applicable conditions 2 Identification of account and bank 2 Submitting data 3 Commission fee 3 Rights and obligations of SEB 3 Term of

Please read the Pre-Agreement Statement below. You ll need to refer to it if your loan is approved.

Pre-Agreement Statement Please read the Pre-Agreement Statement below. You ll need to refer to it if your loan is approved. Babereki Personal Loan Pre Agreement Statement in terms of Section 92 of the

Pre-Agreement Statement Please read the Pre-Agreement Statement below. You ll need to refer to it if your loan is approved. Babereki Personal Loan Pre Agreement Statement in terms of Section 92 of the

AT-CALL SAVINGS ACCOUNTS

AT-CALL SAVINGS ACCOUNTS PART 1 - AT-CALL SAVINGS ACCOUNTS PRODUCT DISCLOSURE STATEMENT (Corporations Act (Cth) 2001) Comprises of the following documents Part 1 - Product Disclosure Statement for all

AT-CALL SAVINGS ACCOUNTS PART 1 - AT-CALL SAVINGS ACCOUNTS PRODUCT DISCLOSURE STATEMENT (Corporations Act (Cth) 2001) Comprises of the following documents Part 1 - Product Disclosure Statement for all

EXTERNAL POLICY CHANGE OF BANKING DETAILS FOR INDIVIDUALS

EXTERNAL POLICY CHANGE OF BANKING DETAILS FOR INDIVIDUALS Revision: 3 Page 1 of 7 1 SCOPE This policy applies to a request by an individual taxpayer to change bank account details at the SARS office. This

EXTERNAL POLICY CHANGE OF BANKING DETAILS FOR INDIVIDUALS Revision: 3 Page 1 of 7 1 SCOPE This policy applies to a request by an individual taxpayer to change bank account details at the SARS office. This

Switching Terms for current accounts

Switching Terms for current accounts 234000211.indd 1 09/11/2017 05:23 Contents There are two ways you can move your account from your old bank to a new one with us. They work in different ways, so read

Switching Terms for current accounts 234000211.indd 1 09/11/2017 05:23 Contents There are two ways you can move your account from your old bank to a new one with us. They work in different ways, so read

1. General terms and conditions for payment transfer services

General terms and 1 (16) Corporate and institutional customers Effective as of 4 April 2016 and until 12 January 2018. The General Terms and consist of the Common Section of the General Terms and Conditions

General terms and 1 (16) Corporate and institutional customers Effective as of 4 April 2016 and until 12 January 2018. The General Terms and consist of the Common Section of the General Terms and Conditions

The authorised user will have a right to access information about the account, unless otherwise agreed.

An account in the name of a deceased person can only be used if a certificate of probate from a district court or similar documentation issued by a foreign qualified authority is presented. 6. Third parties'

An account in the name of a deceased person can only be used if a certificate of probate from a district court or similar documentation issued by a foreign qualified authority is presented. 6. Third parties'

This schedule should be read in conjunction with the engagement letter and the standard terms & conditions.

APPENDIX B1 PERSONAL TAX INDIVIDUALS, SOLE TRADERS & COUPLES SCHEDULE OF SERVICES This schedule should be read in conjunction with the engagement letter and the standard terms & conditions. Recurring compliance

APPENDIX B1 PERSONAL TAX INDIVIDUALS, SOLE TRADERS & COUPLES SCHEDULE OF SERVICES This schedule should be read in conjunction with the engagement letter and the standard terms & conditions. Recurring compliance

AIA MPF Contribution Guide

PENSION - MPF AIA MPF Contribution Guide mpf.aia.com.hk To help you easily fulfil your contribution obligations, AIA offers various tools to ease your administrative burden. Contribution Guide Three simple

PENSION - MPF AIA MPF Contribution Guide mpf.aia.com.hk To help you easily fulfil your contribution obligations, AIA offers various tools to ease your administrative burden. Contribution Guide Three simple

VERSION 1.0 ENDOWMENT POLICY TERMS AND CONDITIONS

VERSION 1.0 ENDOWMENT POLICY TERMS AND CONDITIONS The Policy is underwritten by Prescient Life (RF) Limited. This document contains the terms and conditions applicable to your investment and sets out the

VERSION 1.0 ENDOWMENT POLICY TERMS AND CONDITIONS The Policy is underwritten by Prescient Life (RF) Limited. This document contains the terms and conditions applicable to your investment and sets out the

Loan Agreement Pre-Agreement Statement and General Terms & Conditions in terms of section 92 of the National Credit Act No 34 of 2005

Definitions Loan Agreement Pre-Agreement Statement and General Terms & Conditions in terms of section 92 of the National Credit Act No 34 of 2005 In this Agreement the following words have the meanings

Definitions Loan Agreement Pre-Agreement Statement and General Terms & Conditions in terms of section 92 of the National Credit Act No 34 of 2005 In this Agreement the following words have the meanings

Term Deposits. Terms and Conditions and General Information.

Term Deposits. Terms and Conditions and General Information. Effective Date: 12 November 2016 This booklet sets out the terms and conditions for BankSA Term Deposit Accounts, along with general information

Term Deposits. Terms and Conditions and General Information. Effective Date: 12 November 2016 This booklet sets out the terms and conditions for BankSA Term Deposit Accounts, along with general information

for employers Quick Reference Guide for Plan Administrators of Personal Funding Accounts inside:

for employers Quick Reference Guide for Plan Administrators of Personal Funding Accounts inside: Welcome... 2 Implementation of Personal Funding Accounts... 4 Steps for Employers... 4 Steps for Employees...

for employers Quick Reference Guide for Plan Administrators of Personal Funding Accounts inside: Welcome... 2 Implementation of Personal Funding Accounts... 4 Steps for Employers... 4 Steps for Employees...

Credit Card Important Information

Credit Card Important Information Representative Example: Representative 11.1% APR (variable) based on an assumed Credit Limit of 1,200. Standard interest rate for purchases: 6.9% p.a. (variable). Annual

Credit Card Important Information Representative Example: Representative 11.1% APR (variable) based on an assumed Credit Limit of 1,200. Standard interest rate for purchases: 6.9% p.a. (variable). Annual