A Guide for Employers Date: August 2016

|

|

|

- Rose Preston

- 6 years ago

- Views:

Transcription

1 Direct Earnings Attachment A Guide for Employers Date: August 2016 v3.0 December 2017

2 What this Guide is about This guide explains what you, as an employer, need to do if Debt Management, as part of the Department for Communities (DfC) asks you to implement a Direct Earnings Attachment (DEA). Where you receive a notice to operate a DEA we ask you to read the information contained in this guide. It provides information on: what a DEA is how a DEA operates how to calculate a DEA your responsibilities how to make payments to the DfC Debt Management. This guide is intended to help you understand the main points about a DEA. It is not a full description or statement of the law. Further guidance which includes worked examples can be found in the Frequently Asked Questions section. 2 v3.0

3 Contents No. Title Page Frequently asked questions, answers and examples 4 1 Introduction to Direct Earnings Attachments (DEAs) How does a DEA arise? What legal responsibilities and duties does a DEA place on an employer? 6 2 Protected and Net Earnings Protected Earnings Net Earnings What counts as earnings What does not count as earnings 8 3 How is a DEA calculated? (includes deductions rates table) Making deductions Fixed rate deductions Other Orders and Priorities First DEA deduction (pay day) Administrative costs 12 4 Responsibilities Employer DfC Debt Management 13 5 Making Payments to DfC Debt Management Methods of Payment - process map BACS - DfC preferred method of payment Cheque Card (Debit/Credit) DEA payment schedule Where to send a payment schedule Where can I get more information? 20 6 Comments about our service 20 Appendix 1 DEN 2 Letter 21 Appendix 2 DEA Payment schedule 23 Appendix 3 Payment examples by BACS 25 3 v3.0

4 Frequently asked questions, answers and examples Page 1 What if my employee does not earn enough for me to make the deduction or to 27 allow the full deduction? 2 What happens if I make a payment of salary after an employee has left my 27 employment? 3 Under what circumstances do I need to send a supporting payment schedule to 27 DfC Debt Management 4 I have been applying a fixed rate amount as requested by DfC Debt 28 Management but the employee s earnings have now changed. What do I do? 5 How do I inform the employee of the amount of deductions? 28 6 What if the employee thinks the amount they owe is wrong? 28 7 Is there a protected earnings limit? 28 8 What happens if there are other orders in place? 29 9 I have reduced the DEA deduction from January s pay period because other 29 orders in place would reduce the employee s net earnings to below 60% if the full deduction was applied. Do I need to make up the difference in the February pay period? 10 I send payments to other departments, for example Child Maintenance Service. 29 Can I use either of their accounts to send DEA deduction payments? 11 I have received a letter from the DfC Debt Management to apply a fixed rate 29 amount for each pay period. What is this? 12 How would I apply a rounding of the net wage? How do I calculate deductions when the employee receives holiday pay in 31 advance? 14 What happens if the pay includes an amount in respect of any arrears due? What happens if an employee receives a bonus? Do I have to send a schedule each time I send DfC Debt Management a 33 payment? 17 How do I calculate deductions when the employee has two jobs? What happens if I fail to make a deduction when it is due, or deduct an 34 incorrect amount? 19 How are loans treated? What happens if I do not pay my employee weekly or calendar monthly? What happens if the employee receives both regular and irregular payments? 36 4 v3.0

5 1. Introduction to a Direct Earnings Attachment The Welfare Reform (Northern Ireland) Order 2015, which became law on 9 December 2015, allows Debt Management, part of Department for Communities (DfC) to ask you as an employer, to make deductions directly from your employee s earnings. We (DfC Debt Management) do this by asking you to operate a Direct Earnings Attachment (DEA). We do not have to go through the civil courts to do this, unlike for example the Attachment of Earnings Order (AOE) process. Within the Welfare Reform (Northern Ireland) Order 2015, the legislation covering DEAs, part of the Social Security (Overpayments and Recovery) Regulations (NI) 2016, came into force on 20 June 2016 and these regulations are available on the internet. A DEA has its own regulations and operates differently from other orders such as a Deduction from Earnings Order (DEO) or AEO. A DEA does not replace any of these other orders and in some circumstances employers may receive requests to implement deductions for multiple orders for the same employee. The Northern Ireland Housing Executive (NIHE), who can recover monies resulting from Housing Benefit overpayments, also has the power to issue a Direct Earnings Attachment under this legislation. Please note, however, that this guidance reflects only DEAs operated by the DfC Debt Management. A DEN2 letter will be issued to an employer as a formal notice to set up a Direct Earnings Attachment. see Appendix How does a DEA arise? Where we have been unable to recover monies owed to the DfC from debtors not in receipt of a benefit, and who have not voluntarily agreed to repay, those monies may be recovered by deduction from the debtor s earnings. We will send you a formal notice for each qualifying employee asking you to implement a DEA, including basic instructions on how to do this. We will include the National Insurance number of the employee on all Departmental letters sent to you. It is important that you quote this reference number: on any correspondence you send to us in the payment / payee reference field if you make an online Bankers Automated Clearing Services (BACS) payment for an individual employee on the back of a cheque if you make a cheque payment for an individual employee if you are making a card (debit/credit) payment for one employee 5 v3.0

6 1.2 What legal responsibilities and duties does a DEA place on an employer? You have a legal obligation to: calculate a deduction based on the net earnings (page 7) for each pay date (see page 8 How is a DEA calculated? ) or apply a fixed amount calculated by us if we ask you to do so (see page 10) pay the amounts deducted (other than your administrative costs) to us by the 19th day of the month following the month in which the deduction is made ensure payments to DfC Debt Management carry the required reference, DfC Debt Management use the employee s National Insurance number, that allows us to allocate to the debtors accounts keep a record of each employee from whom a DEA deduction has been made, together with the amount of each deduction notify DfC Debt Management of any periods in which there is a nil deduction If you fail to comply, you may be subject, upon conviction, to a fine of up to 1,000 per notice. You have a duty to notify DfC Debt Management in writing or by phone within 10 days of the date of the DEA notice: when someone we have asked you to implement a DEA for never worked for you or has ceased employment when, and the date from which, an employee ceases to be in your employment If either of the above applies you will need to notify us in writing at the address shown at the top of the DEA notice letter, or by phone. You have a duty to your employee: to notify your employee in writing of: o the amount of the deduction taken, including any amount taken for administrative costs (see section on Administrative Costs, page 12) o how the deduction amount was calculated The above information may be provided on the payslip for the pay period to which the deduction relates. Ensure you advise your employee that deductions will be made from their wages/salary and paid over to DfC Debt Management well in advance of the payday when the first deduction will be made. If you have any problems or queries relating to the DEA, please ring our dedicated employer helpline number on v3.0

7 2. Protected and Net Earnings 2.1 Protected Earnings Where we ask you to operate a DEA you must consider what is known as the Protected Earnings Amount which is an amount equal to 60% of an employee's net earnings. This means that for each pay period where a DEA calculation is applicable, you must additionally ensure (after adding the amount of the DEA to the total amount of other orders that may be already in place) that your employee is left with at least 60% of their net wage. In cases where the addition of the DEA would increase the overall amount of deductions to more than 40% of the net wage, the DEA deduction must be adjusted to an amount that will leave the employee with 60% of their net earnings. This applies even where we have asked you to apply a fixed rate deduction (see page 10). Therefore, in the circumstance where (before the consideration of a DEA deduction) other orders are already in place and the employee s net wage is already equal to or less than 60% of their overall and initial net wage (some other orders do not apply the protected earnings consideration), you should not deduct any DEA amount calculated for that pay period. However, you must still check if a deduction applies for the next and every subsequent pay period, and additionally ensure that a schedule is sent to us in respect of this pay period (including 0.00/nil payments), as we will have been expecting to receive a payment. 2.2 Net Earnings For the purposes of calculating a DEA deduction, net earnings means earnings after the deduction of: Income Tax Class 1 National Insurance and Superannuation contributions What counts as earnings? Wages Salary Fees Bonuses Commission Overtime pay Occupational pensions, if paid with wages or salary 1 The definition of superannuation should be that as applied within the application of other orders (and so will, therefore, exclude stakeholder pension contributions and Free Standing Additional Voluntary Contributions (AVCs) 7 v3.0

8 Compensation payments Statutory sick pay Payment in lieu of notice Most other payments on top of wages 2.4 What does not count as earnings? Statutory maternity pay Statutory adoption pay Ordinary statutory paternity pay Statutory Shared Parental Pay Any pension, benefit, allowance or credit paid by DfC, NIHE or HM Revenue & Customs (HMRC) A guaranteed minimum pension under the Pensions Scheme (Northern Ireland) Act 1993 (a) Amounts paid by a public department of the Government of the United Kingdom or anywhere outside the United Kingdom Sums paid to reimburse expenses wholly and necessarily incurred in the course of the employment Pay or allowances as a member of Her Majesty s forces, other than pay or allowances payable to them by you as a special member of a reserve force Statutory Redundancy Payments You must continue to calculate a DEA deduction every pay day until either: we advise you to stop the employee leaves your employment the employee dies and the salary is paid after the date of the employee s death the amount to recover is no longer outstanding or we ask you to apply a fixed rate deduction (see page 10). 3. How is a DEA calculated? There are two deduction percentage rates for calculation Standard Rate and Higher Rate. DfC Debt Management will let you know which of these rates we want you to apply, when we contact you about setting up the DEA. The rate we ask you to apply may change throughout the life of the DEA, from Standard to Higher and vice versa, and you will be notified of this by letter. After considering an employee s protected earnings requirements calculate the employee s net earnings for the pay period find the correct deduction percentage rate based on: 8 v3.0

9 a. the frequency of their pay (apply frequency rate from Table for Standard Rate or for Higher Rate) b. the net earnings figure multiply the net earnings figure by the percentage rate Standard or Higher - to calculate the DEA amount Note - if you are calculating a DEA based on a daily rate, you must also multiply the daily rate figure by the number of days in the pay period. If payments are made every two or four weeks, calculate weekly pay and deduct the percentage in the table. Deduction from Earnings Percentage Rates Table Daily Earnings Weekly Earnings Monthly Earnings Deduction from Earnings Rate (Standard) Deduction from Earnings Rate (Higher) Rate to Apply (Percentage of net earnings) Rate to Apply (Percentage of net earnings) Up to 15 Up to 100 Up to 430 NIL 5% Between and 23 Between and 32 Between and 39 Between and 54 Between and 75 Between and 160 Between and 220 Between and 270 Between and 375 Between and or more or more Between and 690 Between and 950 Between and 1,160 Between 1, and 1,615 Between, and 2,240 2, or more 3% 6% 5% 10% 7% 14% 11% 22% 15% 30% 20% 40% If you need to confirm with us that you are deducting at the correct rate, you can do this by phoning v3.0

10 3.1 Making deductions The DEA should be implemented from the next pay day which falls on or after 22 days from the date of the DEN 2. The period of 22 days has been put in place to allow the employer time to set up the DEA. The payment to DfC Debt Management should be received, at the latest, by the 19th of the month following the month in which you make your first deduction. Example DEN 2 (notice to employer to implement a DEA) issued on 2 September 201X. Employee is paid monthly paid on the last working day of the month. The Employer must implement the DEA from the first payday on or after 24 September 201X. The first payment should therefore be taken from the wage paid on 30 September 201X and must be received by the DfC Debt Management by 19 October 201X at the latest. Example DEN 2 issued on 2 September 201X. Employee is paid weekly Friday pay day The Employer must implement the DEA from the first payday on or after 24 September 201X. The first payment should therefore be taken from the wage paid on 27 September 201X and must be received by the DfC Debt Management on 19th October 201X at the latest. Each time you make a deduction you: may deduct 1.00 from your employee s earnings towards your administrative costs for operating the order, even if this reduces your employee s income below the protected earnings limit (see FAQ 7) and must inform your employee in writing about each deduction (including the amount you can deduct towards your costs) on the pay day on which it is made or, where impractical, not later than the following payday (see FAQ 5). Please ensure that you advise your employee that deductions will be made from their wages/salary and paid over to DfC Debt Management, well in advance of the pay day when the first deduction will be made. 3.2 Fixed Rate Deductions In exceptional circumstances we may write to you to apply a fixed rate deduction amount for an employee. This revised amount should be applied from the next (and each subsequent) pay date following the date you receive the notice. However, if the earnings for any pay date are below the threshold (See: Table above) then no DEA deduction can be applied. You must always ensure that the Protected Earnings Rate is taken into account, including when we have asked you to apply a fixed rate deduction. 10 v3.0

11 3.3 Other Orders and Priorities After calculating the DEA amount, you must consider: other priority orders in place and the protected earnings amount (see page 7) The DEA can be imposed without a court order, but if your employee has any other deduction orders against them there are rules that tell you which you should take first. If your employee has one or more of the following in place, or they are received after a DEA notice has been received, these will take priority over a DEA (and are known as priority orders): Northern Ireland Deduction from Earnings Order (DEO) from Child Maintenance Service Student Loans A student loan is not an order but if it is being recovered, it is treated in exactly the same way as a priority order. Once these priority orders have been taken into account in your calculation a DEA will then take priority over any other orders, known as non-priority orders or notices. The order of non-priority orders will be decided by the date of the notice. If you have any further enquiries on orders or priorities, please contact us using the telephone number First DEA deduction (payday) The DEA notice issued to you has effect from the next pay day which falls on or after 22 days after the date on the notice letter. As an example, if a notice is issued on 28 November 2016; the first pay date would be on or after the 20 December Payments to DfC Debt Management need to be made in line with your payroll and at least on a monthly basis. If your employee is paid monthly or four weekly, payments must match this cycle. If your employee is paid weekly, payments may be made either weekly as the deduction is taken or on a per month basis. Regardless of the payment cycle, remittance to DfC Debt Management must be made by the 19th day of the month following the date the deduction was made. Please ensure that you advise your employee that deductions will be made from their wages/salary and paid over to DfC Debt Management, well in advance of the pay day when the first deduction will be made. 11 v3.0

12 3.5 Administrative costs For each pay period where a calculation results in a DEA deduction, you may take up to 1 from your employee s earnings towards your administrative costs. This charge is to cover your costs so do not send this administration cost deduction to DfC Debt Management. You can take this charge even if it reduces the employee's income below the 60% protected earnings amount. Please note that the administration charge of 1.00 is only applied when a DEA deduction is actually made, and cannot be deducted for any pay period when no DEA deduction is made. The maximum charge is 1.00 per deduction, therefore, if a deduction was for a number of weeks added together, for example holiday pay paid in advance, the administration charge would still be a maximum of Responsibilities 4.1 Employer It is your responsibility to ensure you calculate the deduction correctly from your employee s net earnings each pay period and pay that amount to us. When you calculate the DEA deduction amount, you must: Ensure that your employee has enough net earnings in the pay period for you to calculate a deduction (see Table, page 9). check that the correct percentage rate (Standard or Higher) has been applied against those net earnings Check that the total of all deductions does not exceed 40% and therefore leave the employee with less than the protected earnings amount which is 60% of their total net earnings during the calculating period to which the deduction relates (see page 9). DfC Debt Management has a legal requirement to issue a DEN 2 (letter to employer to implement DEA) to the employer address provided by HMRC. Even though you may have contracted a payroll provider to undertake your payroll activities associated with DEA, it is your responsibility to ensure the DEN 2 is forwarded to the payroll provider. Do not ask DfC Debt Management to amend your employer address as provided by HMRC in order to direct the DEN 2 to your payroll provider. 12 v3.0

13 4.2 DfC Debt Management It is Debt Management s responsibility to contact you if you fail to make a payment to us when it is due contact you to verify payment information, if applicable refund monies directly to an employee when the balance of the debt has been reduced to zero but a further payment has been received from an employer return monies to an employer where, under the regulations, no DEA payment should have been made, for example: o a payment made to us in error as the earnings for that pay period were under the earnings threshold, and no DEA deduction should therefore have been made o a payment made to us in error because other deductions were already 40% or greater of net earnings for that pay period, and therefore no DEA deduction should have been made In both these cases you should contact us on the employer helpline number ( ) for information on how these monies can be returned to you. DfC Debt Management is not able to: return monies to an employer where a DEA payment was applicable, but was calculated at an incorrect rate, for example: o where we have received a payment greater than the one which should have been calculated for a specific pay period In this case, and from the following pay period(s), you should reduce the amount to be deducted by the excess previously taken. For example, an employer sends a payment for 100 when only 80 was due. At the next pay period the amount of the DEA to be deducted should be reduced by 20. trace and return monies to an employer, where: o the employer has sent a payment meant for us to another department or account In this case you should still make a payment to us but additionally make contact with the other department in order to recover the money you incorrectly paid. 13 v3.0

14 5 Making payments to DfC Debt Management You are required to pay the amount you have calculated and deducted from your employee s net wages to DfC Debt Management as soon as possible. Ideally this will be at the same time as you make the deduction(s) from your employee s salary. However, you must send us the payment no later than the 19 th day of the month following the month in which you have taken it (For example, if you take the money on 30 September, you must send it to us before 19 October; if you take the money on 1 October, you must send it to us before 19 November). DfC Debt Management offer several Method of Payment options to employers. These are summarised within the process map on page 15. These options are explained in detail on pages to ensure that payments sent to DfC Debt Management contain the relevant information to allow them to be allocated correctly to the employee s account. Note Under no circumstances should you send us a cash payment. 14 v3.0

15 5.1 Methods of payment process map DEA Employer Method of Payment Options Are you making one payment for one employee or a consolidated payment for many employees? Are you making one payment for one employee? Options available to make payment to DfC Are you making one consolidated payment for many employees? Options available to make payment to DfC BACS Cheque Card BACS Cheque Actions Enter DfC Debt Management bank account and sort code details (shown below) Enter Employee s National Insurance number in the Payment / Payee reference field Do not send a schedule* Actions Make cheque payable to DfC Debt Management Write employee s National Insurance number on the reverse of the cheque Send cheque to PO Box 2180 (full address below) A supporting payment schedule must be sent** Actions Ring to pay by debit/credit card Give card details and employee s National Insurance number Do not send a schedule* Actions Enter DfC Debt Management bank account and sort code details (shown below) Enter Employer name in the Payment / Payee reference field A supporting payment schedule must be sent** Actions Make cheque payable to DfC Debt Management Write Employer name on reverse of cheque Send cheque to PO Box 2180 (full address below) A supporting payment schedule must be sent** *When your payroll makes one BACS payment to DfC Debt Management for one DEA deduction from an employee s salary and the payment carries their National Insurance number as the Payment / Payee Reference, no schedule needs to be sent. ** Supporting payment schedule can be forwarded via or post, details of how to do this can be found in the Where to send a payment schedule section on page 18 of this guide. DfC Account Number: DfC Sort Code: PO Box Address: Direct Earnings Attachment Department for Communities PO Box 2180 Belfast BT1 9XT v3.0 15

16 5.2 BACS - DfC preferred method of payment DfC Debt Management bank details are: Account Number: Sort code: Payment / Payee Reference: It is critical that you enter one of the two references illustrated below, as applicable. Please use either 1. National Insurance number where you are making a single BACS payment in respect of an individual employee, or a series of single BACS payments in respect of each of a number of individual employees In both these cases as each individual payment will be allocated to a National Insurance number it is not necessary for you to forward a supporting payment schedule. 2. Employer Name as the payment reference where you are making a single consolidated BACS payment for more than one employee In this instance, a supporting payment schedule is required to allow DfC Debt Management to correctly allocate payments to individual s accounts. Further information on the content of the schedule and how to forward it to DfC Debt Management is contained in the DEA payment Schedules section on page 18. It is critical that a supporting payment schedule is completed and sent to DfC Debt Management for each consolidated BACS payment. Failure to do this will result in unnecessary contact to you from DfC Debt Management. Appendix 3 shows two examples of how the Payment / Payee Reference fields should be completed for a BACS payment, for an individual employee and for more than one employee. The account screen you use for making BACS (online) payments may look different to those shown in the examples in Appendix 3. v3.0 16

17 5.3 Cheque You can also pay by cheque. The cheque should be made payable to: DfC Debt Management and sent to: Direct Earnings Attachment Department for Communities PO Box 2180 Belfast BT1 9XT It is critical that you write on the reverse of the cheque one of the two references illustrated below, as applicable; Please use either: 1. National Insurance number for a payment for an individual employee only or 2. Employer Name as the payment reference for a payment for more than one employee. It is also critical that a supporting payment schedule is completed and sent to us for each cheque payment you make, and that the total amount on the schedule and the cheque match. Failure to do so will mean that DfC Debt Management will not be able to allocate payments to the correct accounts and will result in unnecessary contact to you from DfC. Further information on the content of the schedule and how to forward it to DfC Debt Management is contained in the DEA payment Schedules section on page Card (Debit/Credit) A card payment can only be made for one individual employee and you must quote the National Insurance number when you telephone. If you have more than one employee, you must make a separate payment for each employee. If you wish to make a payment by debit or credit card use the telephone number Please have your card details and the employee s National Insurance number to hand along with your letter when you ring. You do not need to complete a supporting payment schedule when paying by card. Note Under no circumstances should you send us a cash payment. v3.0 17

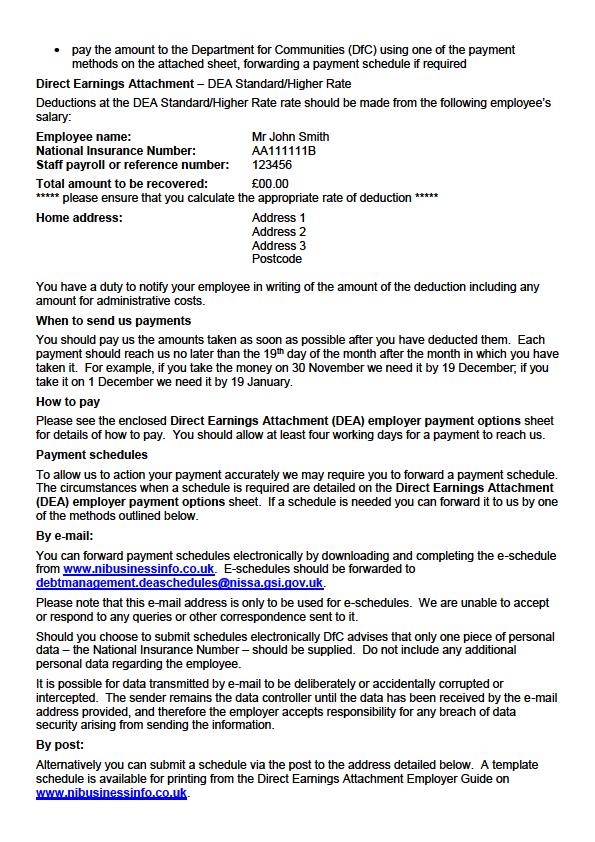

18 5.5 DEA Payment Schedule The DfC requires that a supporting payment schedule be completed and issued in order to ensure that the correct payment is allocated to the correct debtor account and prevents any unnecessary contact to you from DfC Debt Management. However, if you are making either a single BACS payment for one employee or a series of single BACS payments for a number of individual employees, or a card payment for one employee (you can make a series of single card payments if more than one employee has a DEA) You do not need to complete and issue a schedule provided that the employee s National Insurance number is given as a reference in the 3 scenarios detailed above. In all other circumstances i.e. a BACS payment that consolidates a number of individual DEA deductions into one payment a cheque payment where a 0.00/Nil deduction is being made* a schedule must be completed and issued to DfC Debt Management. Where a number of individual DEA deductions have been consolidated into one payment (either by BACS or cheque), all the individual deduction details can be entered onto one schedule provided that the total adds up to the payment made. 5.6 Where to send a payment schedule DfC Debt Management has introduced an route to receive payment schedules from employers, this is the preferred way for payment schedules to be sent. By employers providing the data via , the process of allocating payments to our customer records on our DfC Debt Management systems is more efficient and results in fewer queries. You can forward payment schedules electronically by downloading and completing the template from v3.0 18

19 For the payment schedule, the following information is to be supplied for each employee: Date of payment Amount National Insurance Number Initials of Employee (max of 5 initials) Identify whether payment is by BACS or cheque Reason for any nil deductions Completed e-schedules should be forwarded to debtmanagement.deaschedules@nissa.gov.uk, the total value of the schedule should match the payment made to DfC Debt Management. Please note that this address is only to be used for e-schedules, we are unable to accept or respond to any queries or other correspondence sent to it. For data security reasons the data required for the payment schedule is slightly different to that on the paper schedule. By restricting the data recorded on the payment schedule DfC Debt Management will still have enough information to correctly allocate payments to our customer records, whilst minimising the risk of personal data being fraudulently used should the fall into the hands of a third party. Schedules do not need to be encrypted before ing. It is possible for data transmitted by to be deliberately or accidently corrupted or intercepted. The sender remains the data controller until the data has been received at the address provided, and therefore the employer accepts responsibility for any breach of data security arising from sending the information. The postal route for sending payment schedules remains in place and a schedule template for use when forwarding schedules is available at Appendix 2 of this guide. Should you have any queries regarding the new process please contact us on Schedules can be posted to: Direct Earnings Attachment Department for Communities PO Box 2180 Belfast BT1 9XT v3.0 19

20 5.7 Where can I get more information? If your question is not included in the Frequently Asked Questions section, and you need more information about, or help to operate a Direct Earnings Attachment, please ring our dedicated employer helpline on The employer helpline will be open from 9.00 am to 5.00 pm Monday to Friday. 6 Comments about our service We hope that the information in this leaflet is helpful, and that when contacting the helpline, the service received is informative, courteous and professional. We welcome your feedback regarding our service. If you have any comments, please contact us on or write to us at the address at the top of the DEA letter. v3.0 20

v3.")

21 Appendix 1 DEN 2 Letter Formal notice from DfC Debt Management to set up a DEA (example) v3.0 21

22 v3.0 22

23 Direct Earnings Attachment Payments Schedule Appendix 2 To: DfC DM Direct Earnings Attachment, Department for Communities PO Box 2180, Belfast BT1 9XT From: Employer Name: Address: Telephone No: Item Amount Week/ Mth No Employee s Surname followed by Forename Staff / Reference Number Employee s National Insurance Reason for nil deduction if applicable To be completed by Employer For DfC use only This sheet total Cheque No Completed By Name Paid By BACS Deductions from Earnings Attachment (Tick payments if applicable) schedule Phone Number Date Date Checked By: v3.0 23

24 The schedule overleaf must be completed: when making a single consolidated BACS payment in respect of more than one employee when making any cheque payment when a 0.00 (nil) DEA deduction is due for an employee This schedule must be returned to us at the address below, this is also the address if you are paying by cheque. Do not include or send any correspondence to this address. Direct Earnings Attachment Department for Communities PO Box 2180 Belfast BT1 9XT If you are paying by Cheque ensure it is payable to DfC Debt Management and that it is referenced on the reverse with either a National Insurance number if the payment is for a single employee, or reference DEA if the payment is for more than one employee. If you are paying by BACS complete the transaction using the bank details below DfC Debt Management bank details Sort Code: Account Number: Payee Reference: If the payment is for a single employee the reference must be the employee s National Insurance number but if the payment is for more than one employee, the reference must be the Employer s Name If you are paying by card please ring the number at the top of the letter you received. Important The amount of the cheque or online payment must be the same as the total amount of the deductions shown on the Direct Earnings Attachment payments schedule overleaf. Do not send cash through the post. Do not use this schedule to recover or deduct previous overpayment. v3.0 24

25 Payment by BACS payment for one employee Appendix 3 Payment is for one employee, or is a series of individual payments in respect of each of a number of individual employees - the Payment / Payee reference must be the employee s National Insurance number If you do not enter the employee s National Insurance number, or use a different Payment / Payee reference, or you input the National Insurance number incorrectly, this will mean the payment you send will not be received correctly and will not automatically allocate it to their account. If this happens we may need to take the following action: contacting you as we will not be aware that the payment has been sent manual intervention to trace the debtor to match against the right employer manually allocating the payment to the employee s account This creates delays in payment allocation and unnecessary contact to you from the DfC Debt Management. v3.0 25

26 Payment by BACS - payment for more than one employee Payment is a single consolidated BACS payment in respect of more than one employee - the Payment / Payee reference must be the Employer s Name. The Payment / Payee reference should be the Employer Name this will be used to match the payment against the Employer Name on the associated Payments Schedule Please ensure you also complete the DEA schedule which should contain details for each employee that the payment represents and send the schedule to us as soon as you have made the payment. Failure to send in a schedule will mean that the DfC Debt Management will not be able to allocate payments to the correct accounts and will result in unnecessary contact to you from the DfC Debt Management. v3.0 26

27 Frequently asked Questions & Answers 1. What if my employee does not earn enough for me to make the deduction or to allow the full deduction? If the weekly or monthly earnings are below the threshold (see Table, page 9) you cannot make a DEA deduction or you should not make a deduction if the net earnings are below the relevant payment period deductions threshold as show in the Table But you must either send us a schedule or contact us via the employers helpline to inform us of this. You must continue to check if a DEA deduction is applicable each pay period until;- we tell you to stop or the amount to recover is no longer outstanding or The employee leaves your employment. 2. What happens if I make a payment of salary after an employee has left my employment? You must notify us within 10 days of your employee leaving, but should continue to apply the deduction until full and final payments of their salary have been made. 3. Under what circumstances do I need to send a supporting payment schedule to DfC Debt Management? Payment Method Schedule Required? Reason When making a single BACS payment for an individual employee When making a series of single BACS payments in respect of each of a number of individual employees When making a single consolidated BACS payment for more than one employee When making any cheque payment NO NO YES YES As each individual payment will be referenced using the employee s National Insurance number account As each individual payment will be referenced using the employee s National Insurance number account DfC will need to be able to attribute the right payment to the right account. The BACS reference should be the Employer Name DfC will need this to be able to attribute the right payment to the right account v3.0 27

28 Payment Method When making any card payment When your monthly payroll run has identified that no DEA payment ( 0.00 deduction) is due for an employee Schedule Required? NO YES Or contact us via the employers helpline to inform us Reason Each individual payment will be automatically allocated to a National Insurance number account If you have more than one employee, you must make a separate payment for each employee As this will notify DfC, who will have been expecting to receive a payment 4. I have been applying a fixed rate amount as requested by DfC Debt Management but the employee s earnings have now changed. What do I do? If you receive a notice informing you to apply a fixed rate amount, it should be applied from the next available pay day and continue to apply this rate for future pay periods until DfC contact you to either apply a different rate or advise you to stop deductions altogether. However, no DEA deduction can be made (calculated or fixed rate) from earnings which are below the threshold (see Table, page 9). The protected earnings rules still apply to a fixed rate deduction. 5. How do I inform the employee of the amount of deductions? The regulations state that the employer must inform the employee of the amount of the deduction, including any administration costs, and how that amount is calculated. This information can be included on the payslip, by showing the amount with the explanation DEA table or DEA fixed. 6. What if the employee thinks the amount they owe is wrong? If your employee thinks that the amount of money they owe is wrong, you should advise them to contact us on the telephone number at the top of the letter they received about the Direct Earnings Attachment. Please do not provide your employee with the employer helpline number, as use of this number by an employee will cause a hand-off delay when they contact DfC Debt Management to resolve their query. 7. Is there a protected earnings limit? An employee must be left with 60% of their net earnings after the DEA deduction and deductions from any other orders have been made. If the full DEA deduction, after other orders, reduces net earnings to less than 60%, a partial DEA deduction can be made up to the protected earnings level. The protected earnings rule applies even when we ask you to apply a fixed DEA deduction rate. v3.0 28

29 8. What happens if there are other orders in place? The current priority of orders and other deductions such as Student Loans remains unchanged with the introduction of DEAs. A DEA is a non-priority order and as such will always give way to any other orders that might already have been served on the employee. If other deductions already being taken from the employee s net wage leave the employee with net earnings below 60% of the net wage before a DEA is considered, then a DEA deduction cannot be taken. If a DEA deduction can be taken, the result of this deduction must not leave the employee with less than 60% of their net earnings. If the full DEA deduction, after other orders, reduces net earnings to less than 60%, a partial deduction can be made up to the protected earnings level. The difference should not be carried forward. A deduction should only be carried forward where a shortfall occurs due to an incorrect lesser amount being deducted in error, or when one or more deductions have been missed. The maximum amount which can be deducted for a Direct Earnings Attachment is 20% of the net earnings if deductions are being taken at the Standard rate, as illustrated in the Table or 40% if deductions are being taken at the Higher rate, as illustrated in the Table. 9. I have reduced the DEA deduction from January s pay period because other orders in place would reduce the employee s net earnings to below 60% if the full deduction was applied. Do I need to make up the difference in the February pay period? No, this should not be carried forward. A deduction should only be carried forward where a shortfall occurs due to an incorrect lesser amount being deducted in error, or when one or more deductions have been missed. 10. I send payments to other departments, for example the Child Maintenance Service. Can I use either of their accounts to send DEA deduction payments? No. Only use the account details provided in this guide or as shown on the DEA schedule when you make a DEA payment to us. The departments work separately and collect the payments for different reasons. Please note that if you send a payment to another department in error, it will be your responsibility to contact the other department and to recover the money. 11. I have received a letter from the DfC Debt Management to apply a fixed rate amount for each pay period. What is this? In exceptional circumstances, the DfC Debt Management may agree an alternative fixed amount with your employee, which is usually a lower amount than the DEA deduction calculated by you. If we decide a fixed rate is applicable, we will write to you to apply a fixed rate amount to be deducted each pay day. You should continue to apply this rate for future pay periods until either;- the amount to recover is no longer outstanding; or the employee leaves your employment; or v3.0 29

30 DfC contact you to either apply a different rate; or advise you to stop deductions altogether. However, if for any pay period the earnings are below the relevant threshold within the Table, no DEA deduction can be applied as the protected earnings rules still applies to a fixed rate deduction. This fixed amount applies even where the employee receives an advance of pay, such as holiday pay paid in advance. For example, the employee receives their normal weekly wage plus two weeks holiday pay. The fixed amount of x per week would apply to both the current pay week and each weeks in advance of pay. Therefore the DEA deduction would be x x How would I apply any rounding of the net wage? All calculations for the purpose of a DEA which result in a fraction of a penny are rounded to the nearest whole penny, with the exact half a penny being rounded down to the nearest whole penny, as follows for a net wage of: per week x 5% = o The weekly deduction would be per week x 7% = o The weekly deduction to apply would be per week x 7% = o The weekly deduction to apply would be , per month. 1, x 11% = o The monthly deduction to apply would be Example: DEA calculation for a monthly paid employee: You receive a DEA notice from the DfC Debt Management dated 25 July 201X asking you to set up deductions from your employee s salary according to Table. Your employee is paid monthly, on the last working day of each month. the employer has to implement the DEA from the first payday on or after 16 August 201X (the day following 22 days from DEN 2), which in this case is 30 August 201X. Calculate the employee s gross earnings comprising their monthly wages (including bonuses, overtime, commission but excluding SMP etc.). In this case, the gross wage is 1,200 deduct tax, NICs (National Insurance contributions) and superannuation contributions which, in this case, is 240 That leaves net earnings of 960 look up the appropriate percentage applicable for that monthly net wage figure within Table in this example 960 would attract a deduction of 7% at Standard rate and 14% at Higher rate which when calculated is (Standard rate) or (Higher rate) check if, following the deduction (and deductions for any other orders in place) it still leaves the employee with 60% of net earnings (see 7.2) v3.0 30

31 send the deduction of or to the DfC. The payment must reach the DfC Debt Management by 19 September 201X at the latest. deduct 1.00 if you wish for your administrative costs pay your employee (being 1,200 less 240 less less 1.00) or (being 1,200 less 240 less less 1.00) and itemise the deduction on their payslip 13. How do I calculate deductions when the employee receives holiday pay in advance? Where the amount to be paid to the employee on any pay-day includes an advance in respect of future pay, the total amount to deduct is determined by dividing the whole amount of net earnings by the number of pay periods, calculate a single deduction amount and then calculate the total deduction amount by multiplying that single deduction by the number of pay periods. Example: for employee s paid holiday pay in advance You are operating a DEA for an employee who you pay weekly, and you pay them a weekly wage which includes an advance of holiday pay for two weeks. the net wage, after tax, NICs and superannuation contributions is , which is one week s wage of , and two weeks holiday pay at per week totalling calculate your employee s total net earnings = divide this by the number of pay periods the payment is for / 3 (weeks) = Identify from Table the correct percentage deduction rate for weekly earnings of (e.g to 375 = 11% or 22%) calculate the weekly deduction x 11% = ( 36.58) or x 22% = ( 73.16). multiply this weekly deduction by the number of weeks the payment is for in total - 3 x = or 3 x = pay DfC or deduct a further 1.00 if you wish for your administrative costs 14. What happens if the pay includes an amount in respect of any arrears due? You should apply the appropriate rate from Table the total net payment in the period it is received. So, for example, if an employee was usually paid 500 net per month but in a given month was paid 750 (to include a net payment of arrears of 250), then you should apply the deduction applicable from Table the monthly net earnings payment of 750. In this example, a deduction of 5% or 10% would be applied. v3.0 31

32 15. What happens if my employee receives a bonus? A bonus is to be added to the income for the week or month it was paid in, if both payments were made on the same day. If a bonus is paid within the same tax period, but separate from the monthly wage, two separate calculations are made, as illustrated in the second example below. If a bonus is paid outside the pay period, the bonus will be added to the payment made on the following pay day. Example: Bonus paid with a normal wage Your employee is monthly paid, and gets paid on the last working day of the month. Their net wage on 30 August 201X was 1,625.73, and, in addition, they received a bonus of 550. add the net wage and the bonus together. 1, = 2, identify from Table the correct percentage deduction rate for their monthly earnings = 15% or 30% calculate the deduction - 2, x 15% = or 2, x 30% = pay DfC or deduct a further 1.00 if you wish for your administrative costs Example: Bonus paid separately from a normal wage Your employee is monthly paid, and gets paid on the 25th of the month On 25 September 201X he received a month s wage of 1, On 30 September 201X he received a bonus of 550. Calculate the DEA deduction for 25 September 201X. calculate your employees net earnings for the month which in this case is 1, , x 15% = or 1, x 30% = pay DfC or deduct a further 1.00 of you wish for administrative costs Add the bonus paid on 30 September 201X and the net wage paid on 25 September together. 1, = 2, calculate the total deduction - 2, x 15% = or 2, x 30% = subtract the amount already deducted = or = 165 pay DfC or 165 deduct a further 1.00 if you wish for your administrative costs v3.0 32

33 16. Do I have to send a schedule each time I send DfC Debt Management a payment? The table on the following page illustrates the circumstances when you do not need to send in a schedule and the circumstances when a schedule is necessary. 17. How do I calculate deductions when the employee has two jobs? If you have an employee with two or more jobs with you, and they are paid for different pay periods (e.g. one is weekly paid and one is monthly paid), you should treat this as two separate calculations. This will mean that you should apply correct payment period from Table to each of these payments, calculate the deductions separately and make a payment to DfC Debt Management of a total of the two separate amounts. However, if the employee has two or more jobs with you, but they are all paid on the same day for the same period, the wages can be added together and calculated as one deduction. Example: An employee with two jobs You receive a DEA notice dated 1 August 201X. Your employee is paid weekly for one job and monthly for another. The weekly pay is paid on a Friday and the monthly pay is paid on the last week day of the month. The first deductions for each job are as follows. the employer has to implement the DEA from the first pay day on or after 22 August 201X (22 days from DEN 2) which in this case is 23 August 201X for the weekly pay, and 30 August 201X for the monthly pay. calculate your employees net earnings for the weekly wage paid on 23 August 201X (which in this case is ) identify from Table the correct weekly percentage deduction rate i.e to 160 = 3% or 6% calculate the deduction x 3% = 4.48 or x 6% = 8.97 calculate your employees net earnings for the weekly wage paid on 30 August 201X = identify from Table the correct percentage deduction rate i.e to 160 = 3% or 6% calculate the deduction x 3% = 4.48 or x 6% = 8.97 calculate your employee s net earnings for the first month following the 22 day period, paid on 30 August 201X, which in this case is identify from Table the correct monthly percentage deduction rate i.e to 690 = 3% or 6% calculate the deduction x 3% = or x 6% = for each weekly calculation you may deduct 1.00 if you wish for your administration costs for each monthly calculation you may deduct 1.00 if you wish for your administration costs v3.0 33

Direct Earnings Attachment. A Guide for employers

Direct Earnings Attachment A Guide for employers February 2017 What this Guide is about This guide explains what you, as an employer, need to do if Debt Management, as part of the Department for Communities

Direct Earnings Attachment A Guide for employers February 2017 What this Guide is about This guide explains what you, as an employer, need to do if Debt Management, as part of the Department for Communities

Direct Earnings Attachment. A Guide for employers

Direct Earnings Attachment A Guide for employers August 2016 Direct Earnings Attachment A Guide for Employers Publication Date: August 2016 1 What this Guide is about This guide explains what you, as an

Direct Earnings Attachment A Guide for employers August 2016 Direct Earnings Attachment A Guide for Employers Publication Date: August 2016 1 What this Guide is about This guide explains what you, as an

Direct Earnings Attachment

Direct Earnings Attachment A more detailed guide This detailed guidance has been developed to complement the publication Direct Earnings Attachment - A Guide for Employers. It is intended to provide employers

Direct Earnings Attachment A more detailed guide This detailed guidance has been developed to complement the publication Direct Earnings Attachment - A Guide for Employers. It is intended to provide employers

A guide to the Local Government Pension Scheme (LGPS) for employees in England and Wales

for employees in England and Wales") Kent Pension Fund A guide to the Local Government Pension Scheme (LGPS) for employees in England and Wales www.kentpensionfund.co.uk Index 1. About this Booklet 2. About the Local Government Pension Scheme

Kent Pension Fund A guide to the Local Government Pension Scheme (LGPS) for employees in England and Wales www.kentpensionfund.co.uk Index 1. About this Booklet 2. About the Local Government Pension Scheme

classic plus retirement benefits A brief guide to the benefits available

classic plus retirement benefits A brief guide to the benefits available This booklet provides a guide to pension benefits for anyone leaving and taking their classic plus pension. It gives practical information

classic plus retirement benefits A brief guide to the benefits available This booklet provides a guide to pension benefits for anyone leaving and taking their classic plus pension. It gives practical information

18/02/2014. IRIS PAYE-Master. Release Notes

18/02/2014 IRIS PAYE-Master Release Notes 16/02/2015 Dear Customer, Welcome to your IRIS PAYE-Master software update for 2014/2015. This update of the software includes some new features and enhancements.

18/02/2014 IRIS PAYE-Master Release Notes 16/02/2015 Dear Customer, Welcome to your IRIS PAYE-Master software update for 2014/2015. This update of the software includes some new features and enhancements.

A Guide to the Local Government Pension Scheme for Employees in England and Wales

A Guide to the Local Government Pension Scheme for Employees in England and Wales Employees in England and Wales April 2017 V1 Produced by Orbis Pension Services April 2017 1 INDEX 1 About this booklet

A Guide to the Local Government Pension Scheme for Employees in England and Wales Employees in England and Wales April 2017 V1 Produced by Orbis Pension Services April 2017 1 INDEX 1 About this booklet

A Guide to the Local Government Pension Scheme for Employees in England and Wales

West Midlands Pension Fund A Guide to the Local Government Pension Scheme for Employees in England and Wales Employees in England and Wales: April 2016 Version 1.9 Contents About This Book About the Local

West Midlands Pension Fund A Guide to the Local Government Pension Scheme for Employees in England and Wales Employees in England and Wales: April 2016 Version 1.9 Contents About This Book About the Local

Cash ISA. Customer Guide and Application Form

Cash ISA Customer Guide and Application Form Introducing the Wesleyan Bank Cash ISA Before you take out an ISA This document describes the important features of a Wesleyan Bank Cash Individual Savings

Cash ISA Customer Guide and Application Form Introducing the Wesleyan Bank Cash ISA Before you take out an ISA This document describes the important features of a Wesleyan Bank Cash Individual Savings

CASH ISA CUSTOMER GUIDE AND APPLICATION FORM

CASH ISA CUSTOMER GUIDE AND APPLICATION FORM 02 Cash Individual Savings Account (ISA) CASH INDIVIDUAL SAVINGS ACCOUNT (CASH ISA) This document gives the main points about the Wesleyan Bank Cash Individual

CASH ISA CUSTOMER GUIDE AND APPLICATION FORM 02 Cash Individual Savings Account (ISA) CASH INDIVIDUAL SAVINGS ACCOUNT (CASH ISA) This document gives the main points about the Wesleyan Bank Cash Individual

Frequently Asked Questions

Frequently Asked Questions October 2018 Welcome As you are now a pensioner of the ICI Pension Fund, we are sending you this Frequently Asked Questions leaflet which will hopefully answer any questions

Frequently Asked Questions October 2018 Welcome As you are now a pensioner of the ICI Pension Fund, we are sending you this Frequently Asked Questions leaflet which will hopefully answer any questions

A Guide to the Local Government Pension Scheme for Employees in Scotland (from 1 April 2015)

") A Guide to the Local Government Pension Scheme for Employees in Scotland (from 1 April 2015) Employees in Scotland issued April 2018 V1.6 Index 1. About this Booklet pg 5 2. About the Local Government

A Guide to the Local Government Pension Scheme for Employees in Scotland (from 1 April 2015) Employees in Scotland issued April 2018 V1.6 Index 1. About this Booklet pg 5 2. About the Local Government

A Guide to the Local Government Pension Scheme for Employees in England and Wales

A Guide to the Local Government Pension Scheme for Employees in England and Wales Employees in England and Wales April 2017 V3.0 1 Index 1. About this Booklet pg 5 2. About the Local Government Pension

A Guide to the Local Government Pension Scheme for Employees in England and Wales Employees in England and Wales April 2017 V3.0 1 Index 1. About this Booklet pg 5 2. About the Local Government Pension

Postgraduate Loan guide to terms and conditions

Postgraduate Loan guide to terms and conditions 2016/17 www.gov.uk/postgraduateloan /SF_England /SFEFILM Contents 1 What this guide s about 02 2 Your loan contract 02 3 Who does what 03 4 Your responsibilities

Postgraduate Loan guide to terms and conditions 2016/17 www.gov.uk/postgraduateloan /SF_England /SFEFILM Contents 1 What this guide s about 02 2 Your loan contract 02 3 Who does what 03 4 Your responsibilities

Retirement Guide to the Local Government Pension Scheme (Northern Ireland)

") Retirement Guide to the Local Government Pension Scheme (Northern Ireland) 2 Northern Ireland Local Government Officers Superannuation Committee (NILGOSC) Contents Introduction Introduction.... 5 Retiring

Retirement Guide to the Local Government Pension Scheme (Northern Ireland) 2 Northern Ireland Local Government Officers Superannuation Committee (NILGOSC) Contents Introduction Introduction.... 5 Retiring

Current Account Conditions and AccounT Information.

Current Account Conditions and AccounT Information. If you open an account with us it will be with Yorkshire Building Society (trading as Norwich & Peterborough Building Society, Norwich & Peterborough

Current Account Conditions and AccounT Information. If you open an account with us it will be with Yorkshire Building Society (trading as Norwich & Peterborough Building Society, Norwich & Peterborough

A guide to the Local Government Pension Scheme (LGPS) England and Wales June 2018 v5

England and Wales June 2018 v5") A guide to the Local Government Pension Scheme (LGPS) England and Wales June 2018 v5 Contents Section 1 - About this Booklet Page 5 Section 2 - About the Local Government Pension Scheme (LGPS) Page 6 Who

A guide to the Local Government Pension Scheme (LGPS) England and Wales June 2018 v5 Contents Section 1 - About this Booklet Page 5 Section 2 - About the Local Government Pension Scheme (LGPS) Page 6 Who

Welcome to our Newsletter which contains important information. CONTENTS CONTENTS. Paying Tax in Retirement 1 P60 2. Changes to your Pension Scheme 3

Pensioner Newsletter Welcome to our Newsletter which contains important information. CONTENTS CONTENTS Paying Tax in Retirement 1 P60 2 Changes to your Pension Scheme 3 Pensioners Living Abroad 4 Payment

Pensioner Newsletter Welcome to our Newsletter which contains important information. CONTENTS CONTENTS Paying Tax in Retirement 1 P60 2 Changes to your Pension Scheme 3 Pensioners Living Abroad 4 Payment

pension benefits for new employees

July 2016 pension benefits for new employees University of Newcastle upon Tyne Retirement Benefits Plan (RBP) Saving for your future with help from the University At Newcastle University, we are committed

July 2016 pension benefits for new employees University of Newcastle upon Tyne Retirement Benefits Plan (RBP) Saving for your future with help from the University At Newcastle University, we are committed

Personal Lending Products

Personal Lending Products Terms and conditions Applies from 15th July 2017 Introduction The details of your credit facilities are set out in the agreement which comes with this booklet. The agreement

Personal Lending Products Terms and conditions Applies from 15th July 2017 Introduction The details of your credit facilities are set out in the agreement which comes with this booklet. The agreement

Collection of Student Loans

Employer Helpbook E17(2013) Collection of Student Loans An employer s guide to the collection of Student Loans Use from 6 April 2013 Updated from 1 May 2013 Help and guidance Help and guidance is available

Employer Helpbook E17(2013) Collection of Student Loans An employer s guide to the collection of Student Loans Use from 6 April 2013 Updated from 1 May 2013 Help and guidance Help and guidance is available

Attachment Orders A guide for employers

Attachment Orders A guide for employers Her Majesty s Courts Service in association with Court Service Northern Ireland Scottish Government Department for Work and Pensions Department for Communities and

Attachment Orders A guide for employers Her Majesty s Courts Service in association with Court Service Northern Ireland Scottish Government Department for Work and Pensions Department for Communities and

Contributions: Guide for employers

Contributions: Guide for employers no. 20 This leaflet is a guide for employers and includes information on the schedule return. States of Guernsey Social Security 1 If, after reading this leaflet, you

Contributions: Guide for employers no. 20 This leaflet is a guide for employers and includes information on the schedule return. States of Guernsey Social Security 1 If, after reading this leaflet, you

Salary Exchange for your pension. Our Post Office, your rewards

Salary Exchange for your pension Our Post Office, your rewards 1 This booklet contains important information for Post Office colleagues who are being automatically included in Salary Exchange for pension

Salary Exchange for your pension Our Post Office, your rewards 1 This booklet contains important information for Post Office colleagues who are being automatically included in Salary Exchange for pension

/19 TERMS & CONDITIONS Student loans - a guide to terms and conditions

www.studentfinanceni.co.uk 2018 /19 TERMS & CONDITIONS Student loans - a guide to terms and conditions Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities

www.studentfinanceni.co.uk 2018 /19 TERMS & CONDITIONS Student loans - a guide to terms and conditions Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities

A Guide to the Local Government Pension Scheme for Employees in Scotland (from 1 April 2015)

") A Guide to the Local Government Pension Scheme for Employees in Scotland (from 1 April 2015) Employees in Scotland issued April 2016 V1.4 Page 1 Index 1. About this Booklet pg 5 2. About the Local Government

A Guide to the Local Government Pension Scheme for Employees in Scotland (from 1 April 2015) Employees in Scotland issued April 2016 V1.4 Page 1 Index 1. About this Booklet pg 5 2. About the Local Government

WESLEYAN BANK LTD GENERAL TERMS AND CONDITIONS

WESLEYAN BANK LTD GENERAL TERMS AND CONDITIONS 02 Wesleyan Bank Ltd General Terms and Conditions Introduction These Terms and Conditions explain our obligations to you and your obligations to us; and apply

WESLEYAN BANK LTD GENERAL TERMS AND CONDITIONS 02 Wesleyan Bank Ltd General Terms and Conditions Introduction These Terms and Conditions explain our obligations to you and your obligations to us; and apply

UNIVERSITY OF BRISTOL PENSION SALARY EXCHANGE UBPAS

UNIVERSITY OF BRISTOL PENSION SALARY EXCHANGE UBPAS PENSION SALARY EXCHANGE FOR UBPAS The University of Bristol operates a Pension Salary Exchange scheme ( Salary Exchange ) for members of the University

UNIVERSITY OF BRISTOL PENSION SALARY EXCHANGE UBPAS PENSION SALARY EXCHANGE FOR UBPAS The University of Bristol operates a Pension Salary Exchange scheme ( Salary Exchange ) for members of the University

Student loans a guide to terms and conditions

2018/19 Student loans a guide to terms and conditions /SFWales /SF_Wales /SFWFILM 1 What s this guide about? 3 2 Your loan contract 3 3 Who does what? 4 4 Your responsibilities 5 5 Your repayment plan

2018/19 Student loans a guide to terms and conditions /SFWales /SF_Wales /SFWFILM 1 What s this guide about? 3 2 Your loan contract 3 3 Who does what? 4 4 Your responsibilities 5 5 Your repayment plan

Salary Sacrifice Scheme

Salary Sacrifice Scheme EMPLOYEE GUIDE TO NORTHUMBRIA UNIVERSITY SPORT MEMBERSHIP OF NORTHUMBRIA UNIVERSITY SPORT THROUGH SALARY SACRIFICE What is Sport Central? Sport Central is the University s new purpose

Salary Sacrifice Scheme EMPLOYEE GUIDE TO NORTHUMBRIA UNIVERSITY SPORT MEMBERSHIP OF NORTHUMBRIA UNIVERSITY SPORT THROUGH SALARY SACRIFICE What is Sport Central? Sport Central is the University s new purpose

This Notice requires you by law to send me

Tax Return for the year ended 5 April 2003 UTR Tax reference Employer reference Issue address Date Inland Revenue office address Area Director SA100 Telephone Please read this page first The green arrows

Tax Return for the year ended 5 April 2003 UTR Tax reference Employer reference Issue address Date Inland Revenue office address Area Director SA100 Telephone Please read this page first The green arrows

Student Loan Deduction Tables

Tables SL3 Tables Use from 6 April 2005 HMRC 03/06 When to use these tables Tables Use these tables for employees for whom you have received a Notice to Start s form SL1, or for new employees who have

Tables SL3 Tables Use from 6 April 2005 HMRC 03/06 When to use these tables Tables Use these tables for employees for whom you have received a Notice to Start s form SL1, or for new employees who have

All users: Using Basic PAYE Tools Includes how to correct submissions in the current tax year.

Basic PAYE Tools User Guide All users: Using Basic PAYE Tools Includes how to correct submissions in the current tax year. You can use this guide from 6 April 2015 Updated: 10 June 2015 1 Contents Introduction....

Basic PAYE Tools User Guide All users: Using Basic PAYE Tools Includes how to correct submissions in the current tax year. You can use this guide from 6 April 2015 Updated: 10 June 2015 1 Contents Introduction....

Increasing Your Retirement Benefits

Increasing Your Retirement Benefits This guide describes how you can increase your retirement benefits and applies to individuals who were contributing members of the Scheme on 1 April 2015 or who have

Increasing Your Retirement Benefits This guide describes how you can increase your retirement benefits and applies to individuals who were contributing members of the Scheme on 1 April 2015 or who have

A Guide to the Local Government Pension Scheme for Employees in England and Wales

A Guide to the Local Government Pension Scheme for Employees in England and Wales Employees in England and Wales April 2014 V1.3 1 Index 1. About this Booklet 2. About the Local Government Pension Scheme

A Guide to the Local Government Pension Scheme for Employees in England and Wales Employees in England and Wales April 2014 V1.3 1 Index 1. About this Booklet 2. About the Local Government Pension Scheme

Student loans - a guide to terms and conditions 2018/19.

Student loans - a guide to terms and conditions www.gov.uk/studentfinance 2018/19 Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities 4 5 Which Repayment

Student loans - a guide to terms and conditions www.gov.uk/studentfinance 2018/19 Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities 4 5 Which Repayment

Your guide to Royal Mail pension salary exchange

Your guide to Royal Mail pension salary exchange Contents 04 07 08 Introduction to PSE What do I need to know? PSE - a step-bystep guide 10 14 17 Payslip examples: before and after PSE launches Your take-home

Your guide to Royal Mail pension salary exchange Contents 04 07 08 Introduction to PSE What do I need to know? PSE - a step-bystep guide 10 14 17 Payslip examples: before and after PSE launches Your take-home

Modern Merchant Banking

Modern Merchant Banking Business Notice Account (BNA) Issue 6 Summary Box This application form cover sheet provides you with two product summary boxes for the terms currently available on this product.

Modern Merchant Banking Business Notice Account (BNA) Issue 6 Summary Box This application form cover sheet provides you with two product summary boxes for the terms currently available on this product.

PENALTIES FOR LATE PAYMENT OF PAYE

PENALTIES FOR LATE PAYMENT OF PAYE OVERVIEW For return periods starting on or after 6 April 2010, HMRC may charge penalties where PAYE is not paid in full and in time. Under the new penalty regime, the

PENALTIES FOR LATE PAYMENT OF PAYE OVERVIEW For return periods starting on or after 6 April 2010, HMRC may charge penalties where PAYE is not paid in full and in time. Under the new penalty regime, the

A Guide to the Local Government Pension Scheme for Employees in Scotland (from 1 April 2015)

") A Guide to the Local Government Pension Scheme for Employees in Scotland (from 1 April 2015) Employees in Scotland issued March 2015 V1.0 1 Index 1. About this Booklet pg 5 2. About the Local Government

A Guide to the Local Government Pension Scheme for Employees in Scotland (from 1 April 2015) Employees in Scotland issued March 2015 V1.0 1 Index 1. About this Booklet pg 5 2. About the Local Government

Employers Guide to Operating the Pension Scheme

Employers Guide to Operating the Pension Scheme PLUMBING & MECHANICAL SERVICES (UK) INDUSTRY PENSION SCHEME GUIDE TO OPERATING THE PENSION SCHEME Contents Page 1. Accounting for Pension Scheme 1 2. Additional

Employers Guide to Operating the Pension Scheme PLUMBING & MECHANICAL SERVICES (UK) INDUSTRY PENSION SCHEME GUIDE TO OPERATING THE PENSION SCHEME Contents Page 1. Accounting for Pension Scheme 1 2. Additional

2017/ 18. Student loansa guide to terms and conditions.

2017/ 18 Student loansa guide to terms and conditions www.studentfinanceni.co.uk Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities 4 5 Your repayment

2017/ 18 Student loansa guide to terms and conditions www.studentfinanceni.co.uk Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities 4 5 Your repayment

April 2018 South Tyneside Council Providing pension services for Tyne and Wear Pension Fund and Northumberland County Council Pension Fund

Mr A B Sample 2 Sample Road Anywhere Any Town Any County AB1 1BA April 2018 South Tyneside Council Providing pension services for Tyne and Wear Pension Fund and Northumberland County Council Pension Fund

Mr A B Sample 2 Sample Road Anywhere Any Town Any County AB1 1BA April 2018 South Tyneside Council Providing pension services for Tyne and Wear Pension Fund and Northumberland County Council Pension Fund

Student Loans Company. Repaying your student loan

Student Loans Company Repaying your student loan Contents Page Introduction 3 How much do I repay? 4 Do I pay interest on my loan? 6 How do I repay? 7 When will I get a statement? 11 Coming to the end

Student Loans Company Repaying your student loan Contents Page Introduction 3 How much do I repay? 4 Do I pay interest on my loan? 6 How do I repay? 7 When will I get a statement? 11 Coming to the end

A Summary of the Universities Superannuation Scheme (June 2013)

") A Summary of the Universities Superannuation Scheme (June 2013) 1. Purpose The purpose of this guide is to provide a basic understanding of the benefits available from the Universities Superannuation Scheme

A Summary of the Universities Superannuation Scheme (June 2013) 1. Purpose The purpose of this guide is to provide a basic understanding of the benefits available from the Universities Superannuation Scheme

Pension. Pension Same benefit, less tax. Your guide to

Your guide to Pension Welcome to Pension, a new way of paying pension contributions into your UPM UK Pension Scheme that will save money for both you and the Company. Simply put, it will reduce National

Your guide to Pension Welcome to Pension, a new way of paying pension contributions into your UPM UK Pension Scheme that will save money for both you and the Company. Simply put, it will reduce National

Improving the operation of Pay As You Earn (PAYE) Publication date: 27 th July 2010 Closing date for comments: 23 rd September 2010

Publication date: 27 th July 2010 Closing date for comments: 23 rd September 2010") Improving the operation of Pay As You Earn (PAYE) Publication date: 27 th July 2010 Closing date for comments: 23 rd September 2010 Subject of this document: Scope of this document: Who should read this:

Improving the operation of Pay As You Earn (PAYE) Publication date: 27 th July 2010 Closing date for comments: 23 rd September 2010 Subject of this document: Scope of this document: Who should read this:

Royal Mail Share Incentive Plan

Royal Mail Share Incentive Plan Invitation to join the Partnership & Matching Plan contents> 2Introduction 4How does Partnership & Matching work? 5Who is eligible? 6How could I benefit and what factors

Royal Mail Share Incentive Plan Invitation to join the Partnership & Matching Plan contents> 2Introduction 4How does Partnership & Matching work? 5Who is eligible? 6How could I benefit and what factors

Provided by Scottish Widows Bank SUMMARY BOX SUMMARY BOX. The interest rate is variable. The current rate is shown in the table below.

E-CASH ISA 3 Provided by Scottish Widows Bank SUMMARY BOX PLEASE READ THIS SUMMARY BOX BEFORE YOU COMPLETE THE APPLICATION AND THEN KEEP IT FOR YOUR RECORDS. DON T RETURN IT WITH THE APPLICATION. This

E-CASH ISA 3 Provided by Scottish Widows Bank SUMMARY BOX PLEASE READ THIS SUMMARY BOX BEFORE YOU COMPLETE THE APPLICATION AND THEN KEEP IT FOR YOUR RECORDS. DON T RETURN IT WITH THE APPLICATION. This

Student loans - a guide to terms and conditions

Student loans - a guide to terms and conditions www.gov.uk/studentfinance 2017/18 /SF_England /SFEFILM Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities

Student loans - a guide to terms and conditions www.gov.uk/studentfinance 2017/18 /SF_England /SFEFILM Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities

Local Government Pension Scheme

LGPS Contributions Local Government Pension Scheme A Guide for Scheme Employers Issue 4 : March 2016 http://portal.norfolkpensionfund.org Page 2 of 15 Contents Introduction This guide aims to answer any

LGPS Contributions Local Government Pension Scheme A Guide for Scheme Employers Issue 4 : March 2016 http://portal.norfolkpensionfund.org Page 2 of 15 Contents Introduction This guide aims to answer any

General Terms & Conditions for Savings Accounts

General Terms & Conditions for Savings Accounts April 2018 How are we regulated? The Society is authorised by the Prudential Regulation Authority (PRA) and regulated by both the Financial Conduct Authority

General Terms & Conditions for Savings Accounts April 2018 How are we regulated? The Society is authorised by the Prudential Regulation Authority (PRA) and regulated by both the Financial Conduct Authority

NHS Pensions - Claim for payment of children's pension (AW158)

") NHS Pensions - Claim for payment of children's pension (AW158) This form only applies to member's whose Scheme membership ended before 1 April 2008. Member's surname Other names Membership number SD /

NHS Pensions - Claim for payment of children's pension (AW158) This form only applies to member's whose Scheme membership ended before 1 April 2008. Member's surname Other names Membership number SD /

Webinar: How NEST can help you support clients with auto enrolment

Webinar: How NEST can help you support clients with auto enrolment Questions and answers February 2016 Choosing to use NEST 1. Is a NEST pension scheme always a qualifying scheme for auto enrolment? Yes,

Webinar: How NEST can help you support clients with auto enrolment Questions and answers February 2016 Choosing to use NEST 1. Is a NEST pension scheme always a qualifying scheme for auto enrolment? Yes,

SMART Pensions. A smarter way to pay your pension contributions

SMART Pensions A smarter way to pay your pension contributions SMART Pensions A smarter way to pay your pension contributions Contents Introduction Glossary of Terms Understanding how SMART Pensions works

SMART Pensions A smarter way to pay your pension contributions SMART Pensions A smarter way to pay your pension contributions Contents Introduction Glossary of Terms Understanding how SMART Pensions works

THE LOCAL GOVERNMENT PENSION SCHEME. Full Guide for New Members

THE LOCAL GOVERNMENT PENSION SCHEME Full Guide for New Members THE LOCAL GOVERNMENT PENSION SCHEME (LGPS) SCOTLAND [Scottish version, April 2018] 1 Contents Welcome to the Scheme 3 What is the Local Government

THE LOCAL GOVERNMENT PENSION SCHEME Full Guide for New Members THE LOCAL GOVERNMENT PENSION SCHEME (LGPS) SCOTLAND [Scottish version, April 2018] 1 Contents Welcome to the Scheme 3 What is the Local Government

UNIVERSITY OF BRISTOL PENSION SALARY EXCHANGE USS

UNIVERSITY OF BRISTOL PENSION SALARY EXCHANGE USS April 2015 PENSION SALARY EXCHANGE FOR USS The University of Bristol operates a Pension Salary Exchange scheme ( Salary Exchange ) for members of the Universities

UNIVERSITY OF BRISTOL PENSION SALARY EXCHANGE USS April 2015 PENSION SALARY EXCHANGE FOR USS The University of Bristol operates a Pension Salary Exchange scheme ( Salary Exchange ) for members of the Universities

A Guide to the Local Government Pension Scheme for Employees in England and Wales

A Guide to the Local Government Pension Scheme for Employees in England and Wales Employees in England and Wales July 2016 1 Index 1. About this Booklet pg 5 2. About the Local Government Pension Scheme

A Guide to the Local Government Pension Scheme for Employees in England and Wales Employees in England and Wales July 2016 1 Index 1. About this Booklet pg 5 2. About the Local Government Pension Scheme

Investment Funds Plan and Investment Funds Individual Savings Account (ISA)

") Investment Funds Plan and Investment Funds Individual Savings Account (ISA) Terms and Conditions Effective Date 3 January 2018 How to contact us If you have any questions or need to contact us at any time,

Investment Funds Plan and Investment Funds Individual Savings Account (ISA) Terms and Conditions Effective Date 3 January 2018 How to contact us If you have any questions or need to contact us at any time,

Switching Your Account to us

Switching Your Account to us Help for what matters A guide to the Current Account Switch Service 2 Introduction Now you are switching to us, we will handle everything for you in 7 working days from the

Switching Your Account to us Help for what matters A guide to the Current Account Switch Service 2 Introduction Now you are switching to us, we will handle everything for you in 7 working days from the

If you Joined the LGPS Before 1 April 2014