Employment Tax Incentive (ETI)

|

|

|

- Christina Wilson

- 6 years ago

- Views:

Transcription

1 ETI 2017

2 Employment Tax Incentive (ETI) The ETI is an incentive aimed at encouraging employers to hire young work seekers. It was implemented with effect from 1 January 2014 The aim of this incentive was to increase the overall employment and the level of job experience for youth. Eligible workers are aged between 18 and 29 and earn above the minimum wages between R2 000 to R6 000 per month. Changes: Ø Continuation of the ETI until 28 February Ø Introduction of an annual cap of R20 million on the claim allowed to each employer.

3 employer Is not in the national, provincial or local sphere of government Who Qualifies The employer is eligible to claim the ETI if the Is not a public entity listed in Schedule 2 or 3 of the Public Finance Management Act Is registered for Employees Tax (PAYE), or must be eligible to register for PAYE Is not a municipal entity Is not disqualified by the Minister of Finance due to the displacement of an employee or by not meeting the conditions as may be prescribed by the Minister by regulation.

4 How do I determine who is a qualifying employee? An individual is a qualifying employee if he or she Has a valid South African ID, Asylum Seeker permit or an ID issued in terms of the Refugee Act Is 18 to 29 years old (please note that the age limit is not applicable if the employee renders services mainly inside a special economic zone (SEZ) to an employer that is operating inside the SEZ, or if the employee is employed by an employer that operates in an industry designated by the Minister of Finance) Is not a domestic worker Is not a connected person to the employer

5 How do I determine who is a qualifying employee? Was employed by the employer or an associated person to the employer on or after 1 October 2013 and Is paid the minimum wage applicable to that employer or if a minimum wage doesn't apply, is paid a wage of at least R2 000 (where the qualifying employee was employed for 160 hours in a month) and not more than R Important: The value of the ETI the employer may claim depends on the value of the monthly remuneration paid to the qualifying employee. If the employee has worked less than 160 hours in the month, the remuneration amount must be grossed up to 160 hours per month to calculate the value of the ETI. The amount can then be calculated and be grossed down in the same ratio.

you pay while leaving the wage received by the employee unaffected Employers will be able to claim the incentive for a 24 month period for")

6 The benefits of the ETI It will reduce the employers cost of hiring young people through a costsharing mechanism with government, by allowing you to reduce the amount of Pay-As-You-Earn (PAYE) you pay while leaving the wage received by the employee unaffected Employers will be able to claim the incentive for a 24 month period for all employees who qualify. The incentive amount differs based on the salary paid to each qualifying employee and whether the qualifying employee was employed during the first 12 months or second 12 months of the ETI programme. This incentive will complement existing government programme with similar objectives e.g. learnership agreements.

7 Example 1 - Employees who earn between R0 - R2 000 Identify all qualifying employees for the month - 3 employees Work out the applicable employment period for each qualifying employee - Within the first 12 months of the ETI programme Then work out each employee s monthly remuneration - R2 000 per month per qualifying employee Calculate the amount of the incentive per qualifying employee according to the calculation. The amount which may be claimed on the EMP201 is: Monthly Remuneration Remuneration ETI per month during the first 12 months of employment of the qualifying employee ETI per month during the next 12 months of employment of the qualifying employee R 0 - R % of Monthly Remuneration 25% of Monthly Remuneration

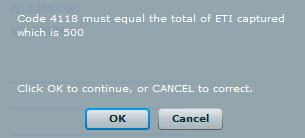

8 Example 1 - Employees who earn between R0 - R2 000 continue The amount which may be claimed on the EMP201 is: From the 13th month of employment, the incentive amount will be calculated as: Monthly Remuneration ETI per month during the next 12 months of employment of the qualifying employee R2 000 per employee 25% of Monthly Remuneration 25% X R2 000 = R500 per employee Amount which may be claimed on the EMP201 R500 per employee X 3 employees who qualify = R1 500 per month

9 Employer Enhancements August 2017 Employer Interim Reconciliation: 15 September and run to 31 October 2017

10 Overview: Last Season Recap Reconciliation Process has not changed Employee database management - Active and Inactive status - Bulk printingof IRP5/IT3(a) certificates Audit Functionality Added - Action centre to manage audit letters

11 Overview: Last Season Recap Audit result not included in certificates Tax paid by employer on behalf of employees efiling Reconciliation process Import a CSV file Inclusion of code 4582 to align with retirement reforms Release notesavailable online Please visit the SARS website for additional documentation and guides.

12 Overview: August Enhancements New employer version: Addition of New Fields and Source codes to align with ETI Employee Demographic information Enhancements to the EMP501 Introduction of validation on ETI efiling authentication enhanced

13 set up file can be downloaded from efiling

14 Select Download for Windows Option

15 Always accept updates- Latest version

16 Employee Demographic information

17 Employee Demographic information

18 Employee Demographic information

19 Employee Demographic information

20 Addition of Fields and Source codes

21 ETI screen (Before 2018 YOA)

22 ETI Validations

23 Enhancements to the EMP501

24 Enhancements to the EMP501

25 EMP501 - Offline

26 EMP check

27 EMP 501 SARS/Own data

28 EMP Status

29 EMP 501 Pre-submit

30 EMP 501 Online check

31 efiling authentication enhanced

32 Enhancements to the EMP501

33 General efiling and Questions?

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

Employment Tax Incentive Scheme

Employment Tax Incentive Scheme Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Employment Tax Incentive Scheme Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Employment Tax Incentive Scheme. 2014/12/09 Version

Employment Tax Incentive Scheme 1 Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Employment Tax Incentive Scheme 1 Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Source Codes. New Source Codes and Validations

Source Codes New Source Codes and Validations Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make

Source Codes New Source Codes and Validations Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make

FREQUENTLY ASKED QUESTIONS COMPLETION AND SUBMISSION OF CSV. TM EMPLOYER AND ZIPCENTRALFILE RECONCILIATION DOCUMENTS

FREQUENTLY ASKED QUESTIONS Revision: 1 Page 1 of 8 1 PURPOSE The purpose of this document is to provide answers to frequently asked questions by employers in respect of creating CSV data files and submitting

FREQUENTLY ASKED QUESTIONS Revision: 1 Page 1 of 8 1 PURPOSE The purpose of this document is to provide answers to frequently asked questions by employers in respect of creating CSV data files and submitting

SAPA Conference Spier, Stellenbosch 04 August March

SAPA Conference Spier, Stellenbosch 04 August 2011 17 March INTRODUCTION PAYE processes and forms, over the past few years, have been aggressively modernised so as to ensure better alignment between PAYE

SAPA Conference Spier, Stellenbosch 04 August 2011 17 March INTRODUCTION PAYE processes and forms, over the past few years, have been aggressively modernised so as to ensure better alignment between PAYE

Employer Easy File Q & A

Employer Easy File Q & A Trouble Shooting Solutions Employer installed e@syfile Employer version 6.0.0 and having troubles login: Confirm if employer made a backup in version 5.0.9 If Yes, copy version

Employer Easy File Q & A Trouble Shooting Solutions Employer installed e@syfile Employer version 6.0.0 and having troubles login: Confirm if employer made a backup in version 5.0.9 If Yes, copy version

Omission of source code 4582

Return Submission ETI Omission of source code 4582 With the implementation of the Retirement Reform requirements, information code 4582 and its value were omitted from the submission file created by e@syfile

Return Submission ETI Omission of source code 4582 With the implementation of the Retirement Reform requirements, information code 4582 and its value were omitted from the submission file created by e@syfile

P U BLI C RELEAS E. Document Classification: Official Publication. South African Revenue Service

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

EXTERNAL GUIDE GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017

GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 BACKGROUND 3 3.1 RECONCILIATION PROCESS 3 3.2 INTERIM RECONCILIATION PROCESS 3 3.3 GENERAL

GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 BACKGROUND 3 3.1 RECONCILIATION PROCESS 3 3.2 INTERIM RECONCILIATION PROCESS 3 3.3 GENERAL

P U BLI C RELEAS E. Document Classification: Official Publication. South African Revenue Service

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

P U BLI C RELEAS E This document specifies the requirements for the generation of an import tax file for the yearly as well as the interim submission. The requirements as defined in this version of the

OVERVIEW PAYE 2010 NOVEMBER

OVERVIEW PAYE 2010 NOVEMBER 1 Contents 1. Introduction... 3 2. The aim of the Pay-As-You-Earn (PAYE) reconciliation process... 3 3. What is reconciliation?... 4 4. The Pay-As-You-Earn (PAYE) process...

OVERVIEW PAYE 2010 NOVEMBER 1 Contents 1. Introduction... 3 2. The aim of the Pay-As-You-Earn (PAYE) reconciliation process... 3 3. What is reconciliation?... 4 4. The Pay-As-You-Earn (PAYE) process...

EXPLANATORY MEMORANDUM

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 2 EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 Currently, the unemployment

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 2 EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 Currently, the unemployment

DRAFT GUIDE TO THE EMPLOYMENT TAX INCENTIVE

SOUTH AFRICAN REVENUE SERVICE DRAFT GUIDE TO THE EMPLOYMENT TAX INCENTIVE Another helpful guide brought to you by the South African Revenue Service Preface Draft Guide to the Employment Tax Incentive The

SOUTH AFRICAN REVENUE SERVICE DRAFT GUIDE TO THE EMPLOYMENT TAX INCENTIVE Another helpful guide brought to you by the South African Revenue Service Preface Draft Guide to the Employment Tax Incentive The

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

Ayanda Takela. SARS efiling and Specialist (Gauteng, Free State & Northern Cape Region)

") Ayanda Takela SARS efiling and e@syfile Specialist (Gauteng, Free State & Northern Cape Region) Topics to be discussed General errors experienced on SARS efiling profiles General errors experienced on

Ayanda Takela SARS efiling and e@syfile Specialist (Gauteng, Free State & Northern Cape Region) Topics to be discussed General errors experienced on SARS efiling profiles General errors experienced on

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

External Guide on how to submit a Request for Remission

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

P U BLI C RELEAS E. Document Classification: Official Publication. South African Revenue Service 2014

P U BLI C RELEAS E Document Classification: Official Publication South African Revenue Service 2014 04/2014 Page 1 of 112 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U BLI C RELEAS E Document Classification: Official Publication South African Revenue Service 2014 04/2014 Page 1 of 112 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

Tax and ETI Amendments 2017/2018

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

STEPS FOR GENERATING ITREG-FILE FOR AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for

sedert 1982 STEPS FOR GENERATING ITREG-FILE FOR e@syfile, AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for e@syfile. 1. Start your reconciliation process by generating the ITREG-file for e@syfile.

sedert 1982 STEPS FOR GENERATING ITREG-FILE FOR e@syfile, AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for e@syfile. 1. Start your reconciliation process by generating the ITREG-file for e@syfile.

Exception Report Guide. August 2018

Exception Report Guide August 2018 Quick Payroll Exception Error Guides We understand your day-to-day challenges; this is why we want to try to make your business life easier. We have prepared this guide

Exception Report Guide August 2018 Quick Payroll Exception Error Guides We understand your day-to-day challenges; this is why we want to try to make your business life easier. We have prepared this guide

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

Tax year end processing

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

Overview of PAYE reconciliation process and 2007/08 policy changes. Another helpful guide brought to you by South African Revenue Service

Overview of PAYE reconciliation process and 2007/08 policy changes Another helpful guide brought to you by South African Revenue Service Overview of PAYE reconciliation process and 2007/08 policy changes

Overview of PAYE reconciliation process and 2007/08 policy changes Another helpful guide brought to you by South African Revenue Service Overview of PAYE reconciliation process and 2007/08 policy changes

A guide to understanding the medical scheme fees tax credit

A guide to understanding the medical scheme fees tax credit A guide to understanding the medical scheme fees tax credit 1 TABLE OF CONTENTS 1. INTRODUCTION... 3 2. WHAT ARE THE CHANGES?... 3 3. THE CHANGES

A guide to understanding the medical scheme fees tax credit A guide to understanding the medical scheme fees tax credit 1 TABLE OF CONTENTS 1. INTRODUCTION... 3 2. WHAT ARE THE CHANGES?... 3 3. THE CHANGES

Quick Start Guide to Payroll Tax Year-End

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

D-BIT Payroll. Tax Year End Guide - Preparation And Procedures For Tax Year End D-BIT SYSTEMS (Pty) Ltd D-BIT Systems (Pty) Ltd

Ltd D-BIT Systems (Pty) Ltd") D-BIT SYSTEMS (Pty) Ltd RegNo: 87/0332407 7 Boskruin Business Park Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 2156 South Africa D-BIT Payroll Tax Year End Guide - Preparation And Procedures

D-BIT SYSTEMS (Pty) Ltd RegNo: 87/0332407 7 Boskruin Business Park Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 2156 South Africa D-BIT Payroll Tax Year End Guide - Preparation And Procedures

From IRP5 to tax assessment 15 minutes CPD

From IRP5 to tax assessment 15 minutes CPD By ADV. CARIEN VAN DIJK IRP5s are somewhat like family: they can cause you a lot of headaches but you can t (and probably don t want to) live without them. This

From IRP5 to tax assessment 15 minutes CPD By ADV. CARIEN VAN DIJK IRP5s are somewhat like family: they can cause you a lot of headaches but you can t (and probably don t want to) live without them. This

Mirror Payroll. Guidelines for End-Feb 2016 and March 2016 Retirement Reforms. Version 3.0. February 2016

Mirror Payroll Guidelines for End-Feb 2016 and March 2016 Retirement Reforms. Version 3.0 February 2016 1 Contents Introduction... 2 Legislation up to Feb 2016... 3 Mirror Payroll end-feb procedures...

Mirror Payroll Guidelines for End-Feb 2016 and March 2016 Retirement Reforms. Version 3.0 February 2016 1 Contents Introduction... 2 Legislation up to Feb 2016... 3 Mirror Payroll end-feb procedures...

Learnership Allowance

Learnership Allowance Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Learnership Allowance Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

P U B L I C R E L E A S E

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

PUBLIC RELEASE. Document Classification: Official Publication. South African Revenue Service 2011

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published document SARS

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2011 Page 1 of 52 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published document SARS

P U B L I C R E L E A S E

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2012 Page 1 of 55 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

P U B L I C R E L E A S E Document Classification: Official Publication South African Revenue Service 2012 Page 1 of 55 Revision History Date Version Description Author/s 13 July 2010 V1.0.0 Published

Tax tables 2019/2020 (year of assessment ending 29 February 2020)

") BUDGET SPEECH 2019/2020 ALL YOU NEED TO KNOW Tax tables 2019/2020 (year of assessment ending 29 February 2020) Income tax: Individuals and special trusts Taxable income Rates of tax 0-195 850 18 % of taxable

BUDGET SPEECH 2019/2020 ALL YOU NEED TO KNOW Tax tables 2019/2020 (year of assessment ending 29 February 2020) Income tax: Individuals and special trusts Taxable income Rates of tax 0-195 850 18 % of taxable

PUBLIC RELEASE. Document Classification: Official Publication. South African Revenue Service 2009

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

ITA88 PROCESS GUIDE ITA88 PROCESS GUIDE AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS

AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS SEPTEMBER 2010 _v2.indd 1 1 9/21/10 4:10 PM AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS Introduction ITA88 AGENT APPOINTMENT Who

AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS SEPTEMBER 2010 _v2.indd 1 1 9/21/10 4:10 PM AN EMPLOYERS GUIDE TO THE ITA88 AGENT APPOINTMENT PROCESS Introduction ITA88 AGENT APPOINTMENT Who

A STEP-BY-STEP GUIDE TO THE EMPLOYER RECONCILIATION PROCESS

EF NO. Trading or Other Name: Transaction Year: Time Stamp: 21159840 A STEP-BY-STEP GUIDE TO THE EMPLOYE ECONCILIATION POCESS Transaction Year (CCYY) Period of econciliation (CCYYMM) Business Information

EF NO. Trading or Other Name: Transaction Year: Time Stamp: 21159840 A STEP-BY-STEP GUIDE TO THE EMPLOYE ECONCILIATION POCESS Transaction Year (CCYY) Period of econciliation (CCYYMM) Business Information

Welcome to the SARS Tax Workshop

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

A person that elected to be registered as above must be registered by the Commissioner with effect from the beginning of that year of assessment.

6.1 WHO QUALIFIES TO REGISTER FOR TURNOVER TAX? A person that qualifies as a micro business may register for TT, if it is a: Natural person (or the deceased or insolvent estate of a natural person is registered

6.1 WHO QUALIFIES TO REGISTER FOR TURNOVER TAX? A person that qualifies as a micro business may register for TT, if it is a: Natural person (or the deceased or insolvent estate of a natural person is registered

New Tax VDP Applications using efiling. There are two parts to the application process: Tax Practitioner

Application Guide for efiling Tax Voluntary Disclosure Programme 2010 Introduction The South African Revenue Service (SARS) will implement a Voluntary Disclosure Porgramme (VDP) that will be effective

Application Guide for efiling Tax Voluntary Disclosure Programme 2010 Introduction The South African Revenue Service (SARS) will implement a Voluntary Disclosure Porgramme (VDP) that will be effective

Standing Committee on Finance (SCOF): Report-Back Hearings 22 October DRAFT Employment Tax Incentive Bill

: Report-Back Hearings 22 October DRAFT Employment Tax Incentive Bill") Standing Committee on Finance (SCOF): Report-Back Hearings 22 October 2013 DRAFT Employment Tax Incentive Bill Response Document from National Treasury as presented to SCOF 1. Introduction Many South Africans

Standing Committee on Finance (SCOF): Report-Back Hearings 22 October 2013 DRAFT Employment Tax Incentive Bill Response Document from National Treasury as presented to SCOF 1. Introduction Many South Africans

COIDA : COMPENSATION FOR OCCUPATIONAL INJURIES AND DISEASES ACT,1993. AMENDED IN 1997

COIDA : COMPENSATION FOR OCCUPATIONAL INJURIES AND DISEASES ACT,1993. AMENDED IN 1997 1 OUR MISSION TO COMPENSATE EMPLOYEES FOR DISABLEMENT CAUSED BY OCCUPATIONAL INJURIES SUSTAINED AND OR DISEASES CONTRACTED

COIDA : COMPENSATION FOR OCCUPATIONAL INJURIES AND DISEASES ACT,1993. AMENDED IN 1997 1 OUR MISSION TO COMPENSATE EMPLOYEES FOR DISABLEMENT CAUSED BY OCCUPATIONAL INJURIES SUSTAINED AND OR DISEASES CONTRACTED

SARS approach to Government institutions

SARS approach to Government institutions 1. SARS focusses on the Tax Compliance of Government Institutions at a National, Provincial and Local Level. 2. SARS Risks that we focus are: Correct Registration,

SARS approach to Government institutions 1. SARS focusses on the Tax Compliance of Government Institutions at a National, Provincial and Local Level. 2. SARS Risks that we focus are: Correct Registration,

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON ACCOMMODATION

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

EXTERNAL REFERENCE GUIDE SECURITIES TRANSFER TAX. EXTERNAL GUIDE - SECURITIES TRANSFER TAX GEN-PAYM-11-G01 Revision: 3 EFFECTIVE DATE:

2013 EXTERNAL REFERENCE GUIDE SECURITIES EXTERNAL GUIDE - SECURITIES Revision: 3 EFFECTIVE DATE: 2013.11.30 DISCLAIMER The information contained in this guide is intended as guidance only and is not considered

2013 EXTERNAL REFERENCE GUIDE SECURITIES EXTERNAL GUIDE - SECURITIES Revision: 3 EFFECTIVE DATE: 2013.11.30 DISCLAIMER The information contained in this guide is intended as guidance only and is not considered

A QUICK GUIDE TO DIVIDENDS TAX

A QUICK GUIDE TO DIVIDENDS TAX i A QUICK GUIDE TO DIVIDENDS TAX 1. INTRODUCTION TO DIVIDENDS TAX In 2007, the Minister of Finance announced that Secondary Tax on Companies (STC) would be replaced by Dividends

A QUICK GUIDE TO DIVIDENDS TAX i A QUICK GUIDE TO DIVIDENDS TAX 1. INTRODUCTION TO DIVIDENDS TAX In 2007, the Minister of Finance announced that Secondary Tax on Companies (STC) would be replaced by Dividends

EXTERNAL GUIDE HOW TO COMPLETE THE REGISTRATION, AMENDMENTS AND VERIFICATION FORM (RAV01)

") REGISTRATION, AMENDMENTS TABLE OF CONTENTS 1 2 3 INTRODUCTION 3 INDIVIDUAL 4 REGISTERED REPRESENTATIVE 4 4 TAX PRACTITIONER 4 5 SARS REGISTERED DETAILS 5 6 ACTIVATE REGISTERED USER Tax Practitioner and

REGISTRATION, AMENDMENTS TABLE OF CONTENTS 1 2 3 INTRODUCTION 3 INDIVIDUAL 4 REGISTERED REPRESENTATIVE 4 4 TAX PRACTITIONER 4 5 SARS REGISTERED DETAILS 5 6 ACTIVATE REGISTERED USER Tax Practitioner and

Special Voluntary Disclosure Programme. GUIDE: SPECIAL VOLUNTARY DISCLOSURE PROGRAMME (v1.2)

") GUIDE: SPECIAL VOLUNTARY DISCLOSURE PROGRAMME (v1.2) This is a preliminary guide, which is subject to Parliamentary legislative processes. This version is based on the proposals to Parliament following

GUIDE: SPECIAL VOLUNTARY DISCLOSURE PROGRAMME (v1.2) This is a preliminary guide, which is subject to Parliamentary legislative processes. This version is based on the proposals to Parliament following

efiling Account Management Guide - Payment Allocation

efiling Account Management Guide - Payment Allocation CONTENTS 1. How to obtain a payment listing... 1 2. How to allocate a payment... 3 3. How to re-allocate a payment... 6 4. How to request a payment

efiling Account Management Guide - Payment Allocation CONTENTS 1. How to obtain a payment listing... 1 2. How to allocate a payment... 3 3. How to re-allocate a payment... 6 4. How to request a payment

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY Foreword This document is a general guide dealing with the PAYE responsibility

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY Foreword This document is a general guide dealing with the PAYE responsibility

Economic Landscape of South Africa

Economic Landscape of South Africa INTRODUCTION One of the leading economies in Africa, with a well-developed infrastructure and established trade links with the rest of the continent, South Africa is

Economic Landscape of South Africa INTRODUCTION One of the leading economies in Africa, with a well-developed infrastructure and established trade links with the rest of the continent, South Africa is

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

Individual Income Tax

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

The Use of Advanced Analytics in Tax Administrations Dublin, Ireland

The Use of Advanced Analytics in Tax Administrations Dublin, Ireland SARS Modernization Program: Improved Organizational Performance and Value Delivery Randall Carolissen (PhD) Group Executive Revenue

The Use of Advanced Analytics in Tax Administrations Dublin, Ireland SARS Modernization Program: Improved Organizational Performance and Value Delivery Randall Carolissen (PhD) Group Executive Revenue

REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER 0 Initial Release A Scheepers GM Operational Services

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

Budget Highlights 2018

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Points of Discussion

Provisional Tax Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

Provisional Tax Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

The use of tax administrative data in research: a South African experience. Public Economics for Development, Maputo, July 2017

The use of tax administrative data in research: a South African experience Public Economics for Development, Maputo, July 2017 0 OUTLINE Introduction why tax administration data? Behind the scenes: setting

The use of tax administrative data in research: a South African experience Public Economics for Development, Maputo, July 2017 0 OUTLINE Introduction why tax administration data? Behind the scenes: setting

Points Of Discussion

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

Tax, ETI and UIF Amendments 2018/2019

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling

2013 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling 1 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling DISCLAIMER The information contained in this guide

2013 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling 1 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling DISCLAIMER The information contained in this guide

Only bidders who satisfy the following criteria are eligible to submit an offer: (This is a requirement on submission).

.") 2. Bidders Obligations: 2.1 Eligibility Criteria Only bidders who satisfy the following criteria are eligible to submit an offer: (This is a requirement on submission). 2.1.1 Technical Specification Sheet

2. Bidders Obligations: 2.1 Eligibility Criteria Only bidders who satisfy the following criteria are eligible to submit an offer: (This is a requirement on submission). 2.1.1 Technical Specification Sheet

Introduction. Lerato Mokoena (SARS Support Consultant-eFiling and specialist) Gauteng and Northwest Province

Gauteng and Northwest Province") Introduction Lerato Mokoena (SARS Support Consultant-eFiling and E@syfile specialist) Gauteng and Northwest Province lmokoena2@sars.gov.za Topics to be discussed Tax Compliance status Functionality on

Introduction Lerato Mokoena (SARS Support Consultant-eFiling and E@syfile specialist) Gauteng and Northwest Province lmokoena2@sars.gov.za Topics to be discussed Tax Compliance status Functionality on

Key Summary of the E-Filing Process Step 1. Sign Up / Sign In Sign Up : Sign In :... 6

Table of Contents Key Summary of the E-Filing Process... 3 Step 1. Sign Up / Sign In... 5 1.1 Sign Up :... 5 1.2 Sign In :... 6 Step 2. Download Spreadsheet CT & ixbrl A/c / Co. House / VAT... 7 Step 3.

Table of Contents Key Summary of the E-Filing Process... 3 Step 1. Sign Up / Sign In... 5 1.1 Sign Up :... 5 1.2 Sign In :... 6 Step 2. Download Spreadsheet CT & ixbrl A/c / Co. House / VAT... 7 Step 3.

SAPA - ANNUAL PAYE UPDATE BREAKFAST, Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014

SAPA - ANNUAL PAYE UPDATE BREAKFAST, 2014 Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014 Content Chapter 4 Annexure C Davis Tax Review Committee Miscellaneous 1 Content: Chapter

SAPA - ANNUAL PAYE UPDATE BREAKFAST, 2014 Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014 Content Chapter 4 Annexure C Davis Tax Review Committee Miscellaneous 1 Content: Chapter

Release Notes 5.1a. Premier and Classic. September 2018

Release Notes 5.1a Premier and Classic September 2018 Table of Contents 1.0 Important Notice: Licence Agreement (Classic/Premier) 3 2.0 RSA: PAYE Interim Reconciliation Submissions (Classic/Premier) 4

Release Notes 5.1a Premier and Classic September 2018 Table of Contents 1.0 Important Notice: Licence Agreement (Classic/Premier) 3 2.0 RSA: PAYE Interim Reconciliation Submissions (Classic/Premier) 4

UNEMPLOYMENT INSURANCE CONTRIBUTIONS ACT NO 4 OF 2002

UNEMPLOYMENT INSURANCE CONTRIBUTIONS ACT NO 4 OF 2002 [ASSENTED TO 27 MARCH 2002 ] [ENGLISH TEXT SIGNED BY PRESIDENT.] AS AMENDED BY TAXATION LAWS AMENDMENT ACT, NO. 30 OF 2002 REVENUE LAWS AMENDMENT ACT,

UNEMPLOYMENT INSURANCE CONTRIBUTIONS ACT NO 4 OF 2002 [ASSENTED TO 27 MARCH 2002 ] [ENGLISH TEXT SIGNED BY PRESIDENT.] AS AMENDED BY TAXATION LAWS AMENDMENT ACT, NO. 30 OF 2002 REVENUE LAWS AMENDMENT ACT,

Assisting the disadvantaged groups Statements and Comments. Introduction. 1. Context and background ESTONIA

Assisting the disadvantaged groups Statements and Comments Kaia Philips University of Tartu, Institute of Economics Introduction In 2004, the Estonian Ministry of Social Affairs, in cooperation with various

Assisting the disadvantaged groups Statements and Comments Kaia Philips University of Tartu, Institute of Economics Introduction In 2004, the Estonian Ministry of Social Affairs, in cooperation with various

Accrual Profile Effective Dates

Accrual Profile Effective Dates Starting on Monday, July 11, 2011, Accrual Profile Effective dates will be tracked in TIM. An employee who has an accrual profile of SPA Non-Exempt for example, and changes

Accrual Profile Effective Dates Starting on Monday, July 11, 2011, Accrual Profile Effective dates will be tracked in TIM. An employee who has an accrual profile of SPA Non-Exempt for example, and changes

EXTERNAL FREQUENTLY ASKED QUESTIONS

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 0 Page 1 of 5 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of Power of Attorney for all tax types. This document should

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 0 Page 1 of 5 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of Power of Attorney for all tax types. This document should

Key Summary of the E-Filing Process Step 1. Sign Up / Sign In... 5

Table of Contents Key Summary of the E-Filing Process... 3 1 Step 1. Sign Up / Sign In... 5 1.1 Sign Up :... 5 1.2 How to Appoint Additional Users :... 7 1.3 Sign In :... 8 2 Step 2. Download Spreadsheet

Table of Contents Key Summary of the E-Filing Process... 3 1 Step 1. Sign Up / Sign In... 5 1.1 Sign Up :... 5 1.2 How to Appoint Additional Users :... 7 1.3 Sign In :... 8 2 Step 2. Download Spreadsheet

South Africa Foreign Services Exemption Amended

South Africa Foreign Services Exemption Amended South Africa s Taxation Laws Amendment Act, No. 17 of 2017, promulgated on 18 December 2017, contained the amendment, capping the private-sector foreign

South Africa Foreign Services Exemption Amended South Africa s Taxation Laws Amendment Act, No. 17 of 2017, promulgated on 18 December 2017, contained the amendment, capping the private-sector foreign

TAX GUIDE FOR MICRO BUSINESSES 2011/12

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

Budget Highlight 2017

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

FINANCIAL INFORMATION REGULATION

Deposited November 4, 1993 O.C. 1505/93 Financial Information Act [includes amendments up to B.C. Reg. 249/2002] Contents 1 Definition 2 Application 3 Prescribed form 4 Prescribed amount and classification

Deposited November 4, 1993 O.C. 1505/93 Financial Information Act [includes amendments up to B.C. Reg. 249/2002] Contents 1 Definition 2 Application 3 Prescribed form 4 Prescribed amount and classification

DECEASED ESTATES REGISTRATION & ASSESSMENT

DECEASED ESTATES REGISTRATION & ASSESSMENT Agenda Introduction Position - deaths prior to 1 March 2016 Position - deaths post 1 March 2016 Registration process for Deceased Person Registration process

DECEASED ESTATES REGISTRATION & ASSESSMENT Agenda Introduction Position - deaths prior to 1 March 2016 Position - deaths post 1 March 2016 Registration process for Deceased Person Registration process

Government Gazette REPUBLIC OF SOUTH AFRICA. AIDS HELPLINE: Prevention is the cure

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

EXTERNAL GUIDE. How to efile your Provisional Tax Return

1. Register For efiling You will need to register as an efiling user before you can file your provisional tax return electronically. To register, go to www.sarsefiling.co.za 1.1. Click on Register 1.2.

1. Register For efiling You will need to register as an efiling user before you can file your provisional tax return electronically. To register, go to www.sarsefiling.co.za 1.1. Click on Register 1.2.

Please note that this process must be completed within 2 months from date of signing the Budget Breakdown to certification

B1/1 BROAD-BASED BEE INFORMATION GATHERING WORKBOOK QSE This workbook specifies all the documentation that we require to complete your audit. In terms of the SAB&T BEE SERVICES AUDIT PROCESS, we need to

B1/1 BROAD-BASED BEE INFORMATION GATHERING WORKBOOK QSE This workbook specifies all the documentation that we require to complete your audit. In terms of the SAB&T BEE SERVICES AUDIT PROCESS, we need to

Government Gazette REPUBLIC OF SOUTH AFRICA. Vol. 441 Cape Town 28 March 2002 No

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 441 Cape Town 28 March 2002 No. 23289 THE PRESIDENCY No. 406 28 March 2002 It is hereby notified that the President has assented to the following Act, which

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 441 Cape Town 28 March 2002 No. 23289 THE PRESIDENCY No. 406 28 March 2002 It is hereby notified that the President has assented to the following Act, which

TAX GUIDE FOR SMALL BUSINESSES 2013/14

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

SKILLS DEVELOPMENT ACT 97 OF 1998

SKILLS DEVELOPMENT ACT 97 OF 1998 [ASSENTED TO 20 OCTOBER 1998] [DATE OF COMMENCEMENT: 10 SEPTEMBER 1999] (Unless otherwise indicated) (English text signed by the President) as amended by Skills Development

SKILLS DEVELOPMENT ACT 97 OF 1998 [ASSENTED TO 20 OCTOBER 1998] [DATE OF COMMENCEMENT: 10 SEPTEMBER 1999] (Unless otherwise indicated) (English text signed by the President) as amended by Skills Development

Payroll Processing Previous Tax Year Payslip Adjustments

Payroll Processing Previous Tax Year Payslip Adjustments Capturing of Adjustments for February in the Previous Tax Year In order to capture adjustments for previous Tax Years it is necessary to process

Payroll Processing Previous Tax Year Payslip Adjustments Capturing of Adjustments for February in the Previous Tax Year In order to capture adjustments for previous Tax Years it is necessary to process

Toronto Employment and Social Services

OPERATING PROGRAM SUMMARY Contents Overview & Recommendations I: 2015 2017 Service Overview and Plan 5 II: Council Budget III: Issues for Discussion 27 Toronto Employment and Social Services 2015 OPERATING

OPERATING PROGRAM SUMMARY Contents Overview & Recommendations I: 2015 2017 Service Overview and Plan 5 II: Council Budget III: Issues for Discussion 27 Toronto Employment and Social Services 2015 OPERATING

Basic PAYE Tools Using Basic PAYE Tools for the Employer Payment Summary (EPS) only

only") Basic PAYE Tools Using Basic PAYE Tools for the Employer Payment Summary (EPS) only You can use this guide from 6 April 2013 Updated: 9 April 2013 www.hmrc.gov.uk/payerti 1 Contents Introduction 3 Getting

Basic PAYE Tools Using Basic PAYE Tools for the Employer Payment Summary (EPS) only You can use this guide from 6 April 2013 Updated: 9 April 2013 www.hmrc.gov.uk/payerti 1 Contents Introduction 3 Getting

Briefing on the Youth Wage Subsidy: Specific Questions:

19 May 2012 Tim Harris MP Briefing on the Youth Wage Subsidy: The DA fully supports the implementation of the Youth Wage Subsidy outlined in National Treasury s document Confronting youth unemployment:

19 May 2012 Tim Harris MP Briefing on the Youth Wage Subsidy: The DA fully supports the implementation of the Youth Wage Subsidy outlined in National Treasury s document Confronting youth unemployment:

Inform Practice Note #19

Inform Practice Note #19 June 2009 (Version 1 - June 2009) Streamlining Payment Processes cidb s Inform Practice notes provide guidance and clarity in achieving client objectives in construction procurement

Inform Practice Note #19 June 2009 (Version 1 - June 2009) Streamlining Payment Processes cidb s Inform Practice notes provide guidance and clarity in achieving client objectives in construction procurement

Service Charter. South African Revenue Service Service Charter

Service Charter South African Revenue Service Service Charter 1 South African Revenue Service Your Rights Obligations and Service timelines 2 Service Charter WHAT WE DO IN SOUTH AFRICA We, the South African

Service Charter South African Revenue Service Service Charter 1 South African Revenue Service Your Rights Obligations and Service timelines 2 Service Charter WHAT WE DO IN SOUTH AFRICA We, the South African

2013/ /18 STRATEGIC PLAN & 2013/14 ANNUAL PERFORMANCE PLAN. Presentation to the Standing Committee on Finance 14 May 2013

2013/14-2017/18 STRATEGIC PLAN & 2013/14 ANNUAL PERFORMANCE PLAN Presentation to the Standing Committee on Finance 14 May 2013 Executive Leadership team 2 Oupa Magashula, Commissioner Ivan Pillay, Deputy

2013/14-2017/18 STRATEGIC PLAN & 2013/14 ANNUAL PERFORMANCE PLAN Presentation to the Standing Committee on Finance 14 May 2013 Executive Leadership team 2 Oupa Magashula, Commissioner Ivan Pillay, Deputy

TAX GUIDE FOR SMALL BUSINESSES 2011/12

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR SMALL BUSINESSES 2011/12 This document

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR SMALL BUSINESSES 2011/12 This document

Release Notes 5.1a. Sage 200c. September 2018

Release Notes 5.1a Sage 200c September 2018 Table of Contents 1.0 Important Notice: Licence Agreement 3 2.0 RSA: PAYE Interim Reconciliation Submissions 4 2.1 Changes to IRP5 Certificates 4 2.2 Explanation

Release Notes 5.1a Sage 200c September 2018 Table of Contents 1.0 Important Notice: Licence Agreement 3 2.0 RSA: PAYE Interim Reconciliation Submissions 4 2.1 Changes to IRP5 Certificates 4 2.2 Explanation

City of Johannesburg Supply Chain Management Unit

City of Johannesburg Supply Chain Management Unit SUPPLIER NAME: REQUEST FOR QUOTATION FOR GOODS AND SERVICES FOR THE CITY OF JOHANNESBURG Procurement Less than R 200 000 (Including Vat) (For publication

City of Johannesburg Supply Chain Management Unit SUPPLIER NAME: REQUEST FOR QUOTATION FOR GOODS AND SERVICES FOR THE CITY OF JOHANNESBURG Procurement Less than R 200 000 (Including Vat) (For publication

DIRECTIVE 6 TRANSITIONAL PROVISIONS FOR REVENUE COLLECTED BY THE SOUTH AFRICAN REVENUE SERVICE (SARS)

") DIRECTIVE 6 TRANSITIONAL PROVISIONS FOR REVENUE COLLECTED BY THE SOUTH AFRICAN REVENUE SERVICE (SARS) Issued by the Accounting Standards Board July 2009 Directive 6 Copyright 2009 by the Accounting Standards

DIRECTIVE 6 TRANSITIONAL PROVISIONS FOR REVENUE COLLECTED BY THE SOUTH AFRICAN REVENUE SERVICE (SARS) Issued by the Accounting Standards Board July 2009 Directive 6 Copyright 2009 by the Accounting Standards

MINISTRY OF THE SOLICITOR GENERAL

THE ESTIMATES, 2001-02 1 SUMMARY The Mandate of the Ministry of the Solicitor General is to enhance public safety in Ontario in ways that reflect community needs and advance social justice. The Ministry

THE ESTIMATES, 2001-02 1 SUMMARY The Mandate of the Ministry of the Solicitor General is to enhance public safety in Ontario in ways that reflect community needs and advance social justice. The Ministry

TCS (Tax Clearance Status) November 2018

November 2018") TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

Branch Stakeholder Meeting Minutes

Branch Stakeholder Meeting Minutes Minutes of the meeting held: Date: 27 March 2014 Time: 09:00am Venue: Umhlanga Ridge office Present: SARS: Vikash Ganpath Laven Moodley Xolani Hlongwane Ramcharan Himla

Branch Stakeholder Meeting Minutes Minutes of the meeting held: Date: 27 March 2014 Time: 09:00am Venue: Umhlanga Ridge office Present: SARS: Vikash Ganpath Laven Moodley Xolani Hlongwane Ramcharan Himla

Sage 50 US Edition Payroll year-end checklist

Sage 50 US Edition Payroll year-end checklist Helpful articles on https://support.na.sage.com: How to install tax formulas and tax form updates Article ID 10193 How do I print reports? Article ID 35183

Sage 50 US Edition Payroll year-end checklist Helpful articles on https://support.na.sage.com: How to install tax formulas and tax form updates Article ID 10193 How do I print reports? Article ID 35183