Points of Discussion

|

|

|

- Carol Sherman

- 5 years ago

- Views:

Transcription

1 Provisional Tax

2 Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

3 Provisional Tax Overview Provisional tax is not a separate tax. It is a method of paying tax due, to ensure the taxpayer does not pay large amounts on assessment, as the tax liability is spread over the relevant year of assessment. It requires the taxpayers to pay at least two amounts in advance, during the year of assessment, which are based on estimated taxable income. A third payment is optional after the end of the tax year, but before the issuing of the assessment Final liability, however, is worked out upon assessment and the payments will be off-set against the liability for normal tax for the applicable year of assessment. 2

4 Provisional Tax Any Company Any person who receives income other than remuneration or allowance from an Employer who is not registered for Employees Tax A person who is notified by the SARS Commissioner that he/she is a provisional taxpayer Who is Liable 3

5 Specific Exclusions An Approved PBO or recreational clubs in terms of s30 or s30a Body Corporates, share block companies or certain associations of persons Non-resident owners or charterers of ships or aircraft A small business funding entity and a deceased estate Any natural person who does not derive income from the carrying on of any business, if in that relevant year of assessment o Taxable income does not exceed the tax threshold or o The taxable income from interest, dividends, foreign dividends, rental from letting fixed property and remuneration from an employer that is NOT registered for employees tax does not exceed R30 000

6 Estimates of taxable income Individuals & Trusts - During every period submit an estimate of the total taxable income - Taxable portion of the Aggregate capital gain and must be included in both the first and second provisional tax calculations. - The amount of estimate submitted by a provisional taxpayer can not be less than the basic amount applicable to that particular estimate. Companies - May submit a return of an estimate of the total taxable income which will be derived by the company in respect of the year of assessment The basic amount is the taxpayer s taxable income assessed by the Commissioner for the latest preceding year of assessment LESS the amount of any taxable capital gain. 5

7 Basic amount The basic amount is the taxpayers taxable income assessed by the Commissioner for the latest preceding year of assessment, not less than 14 days before the date the taxpayer submits the provisional tax return LESS: I. The amount of any taxable capital gain II. Taxable portion of a retirement fund lump sum benefit or retirement fund lump sum withdrawal benefit or severance benefit (other than any amount included under para (ea) of gross income ) and III. Any amount, including any voluntary award received or accrued contemplated in paragraph (d) of gross income (excluding a severance benefit) The basic amount for all taxpayers must be increased by 8% if the estimate is made more than 18 months after the end of the latest preceding year of assessment. The YOA as shown on the IRP6, will refer to an assessment preceding the year of assessment for which the estimate is made, and for which a notice of assessment relevant to the estimate has been issued by SARS not less than 14 calendar days prior to the due date of such estimate. 6

8 Example 1 Statement for a provisional taxpayer with a YOA ending 28 February 2017: NOA for 2016 YOA was issued on 15 August 2016 IRP6 for 2017 tax year 1 st period is 31 August 2016 NOA for 2015 YOA was issued on 15 July 2015 Solution: 2016 YOA was issued 15 days before the date on which the provisional tax estimate was submitted (between 15 August & 31 August 2016), Due to the 14 day criteria being met, the latest preceding year is the 2016 YOA Estimate is not made more than 18 months (between 28 February 2016 and 31 August 2016) Estimate is not more than 18 months, therefore the basic amount will not increase by 8%. Taxpayers basic amount will be based on the taxable income as assessed in

9 Statement for a provisional taxpayer with a YOA ending on 28 February 2017: NOA for 2016 YOA was issued on 19 Aug 2016 IRP6 for 2017 tax year 1 st period is 31 Aug 2016 NOA for 2015 YOA was issued on 15 July 2015 Solution: Example YOA was issued 11 days before the date on which the provisional tax estimate was submitted. Therefore, the 2016 assessment does not meet the 14 day criteria, the latest preceding YOA is the 2015 tax year of assessment Estimate is not more than 18 months (between 28 Feb and 31 Aug 2016) Basic amount will not be increased by 8% The basic amount will be the amount of taxable income as assessed in

10 Example 3: Statement for a provisional taxpayer with the YOA ending on 28 February 2017: NOA was issued for the 2013 TY on 30 June 2013 Taxable income as assessed in 2013 was R and included a taxable gain of R and severance benefit of R IRP6 for 2017 tax year 1 st period is 31 Aug , 2015, and 2016 tax returns have NOT be submitted Solution: 2013 assessment was issued 14 days more than the date on which the provisional tax estimate was submitted on 31 Aug 2016, as 2014, 2015 and 2016 tax returns have not been submitted Estimate is more than 18 months (between 28 Feb 2013 and 31 Aug 2016) after the end of the last preceding year (2013) Basic amount is as follows: Taxable income assessed in 2013 R Less: Taxable Capital Gain R Less: Severance Benefit R R

11 Example 3 The basic amount (R ) must be increased by 8% for each year from 2013, 2014, 2015, and 2016, therefore [R (R x 8% x 4)] = R R is the basic amount for the 2017 TY In terms of par 19(3), a provisional taxpayer may be asked to justify any estimate made or to furnish full particulars of income, expenditure and / or any other particulars that may be required. i. If SARS is not satisfied with the response, the estimate may be increased to an amount which is considered reasonable. ii. This increase of the estimate by SARS is not subject to objection and appeal. SARS will notify the taxpayer and issue a revised estimate which will be used to calculate your provisional liability. 10

12 First Period - Calculation 11

13 Second Period - Calculation 12

14 Third Period / Top up - Calculation 13

15 First Period - Companies 14

16 Second Period - Companies 15

17 Third Period / Top up - Calculation 16

18 Third Period payments Provisional payment must be paid not later than the effective date Clarifying effect date - YOA ends 28/29 Feb the effective date is seven months after the FYE, 30 September - FYE on a date other than 28/29 Feb, the effective date will be six months after the FYE - Voluntary Payment which any provisional taxpayer can make however, individuals and trusts whose taxable income is more than R or companies with a taxable income of R or more may make a third voluntary payment to avoid interest in terms of section 89quat(2) being levied on any underpayment of tax on assessment. 17

19 Interest on Provisional tax 89bis interest 89quat interest 89quat(2) interest 89quat (4) interest 18

20 Paragraph 20 penalty Levied where it has been determined that the actual taxable income is more than the taxable income estimated on the second provisional tax return Penalty amount depends on whether the actual taxable income is more or less than R1 million The penalty may be levied even if the Commissioner has increased the estimate in terms of par 19(3). The second estimate that has been submitted by the taxpayer is used to determine if the estimate is more or less than R1 million. 19

21 Paragraph 20 penalty Failed to submit the final estimate (2nd IRP6) by the due date, the estimate amount will be deemed to be nil taxable income unless the 2nd IRP6 is submitted four months after the end of the relevant YOA Amounts such as retirement lump sum benefit, retirement lump sum withdrawal benefit or severance benefit payments, are excluded from the calculation of the penalty A penalty levied for the underestimation of taxable income on the second period is reduced by the penalty imposed for the late payment of provisional tax under paragraph 27 Commissioner if satisfied that failure to submit an estimate timeously was not due to intent to evade or postpone payment may remit the penalty wholly or partially. 20

22 Provisional Tax Return on E-filing IRP6 Provisional Tax (IRP6) must be activated on e-filing. In instances where the profile is not activated on efiling the Tax Practitioners must click on: Organisations Organisation Tax Types 21

23 Activating Provisional Tax on efiling Select the tick box for the tax type Provisional Tax (IRP6) Enter the tax reference number Click on the Register button 22

24 Requesting Provisional Tax Return Click on Returns Click on Returns issued Click on Provisional Tax (IRP6) 23

25 Requesting Provisional Tax Return Select the provisional tax period Click on Request Return Provisional tax returns can only be requested for periods that fall within: o The current period o The current period minus two periods o The current period plus one period 24

26 25 Requesting IRP 6 Return

27 26 Completion of IRP 6

28 Demographic Details Company / CC If the taxpayer type is a trust or a company/cc, the following information will be prepopulated on the return: Year of Assessment Period: First (e.g. first period) Taxpayer reference number Registered name Registration number 27

29 Demographic Details Individuals If the taxpayer type is an individual, the following information will be pre-populated on the return: Year of Assessment Taxpayer reference number Initials and Surname Date of birth 28

30 Historical Information The historical information will automatically be displayed if the taxpayer has been assessed within five years from the year of assessment reflected on the provisional tax return. The historical information will be blank if: The last year that the taxpayer was assessed is five years or more prior to the year of assessment reflected on the IRP6 return The taxpayer is a new taxpayer 29

31 Credit Push Payment Payment is performed by the account holder. SARS e-filing will send a payment request to your bank which will indicate, the amount that needs to be paid and gives a payment reference number. The taxpayer then physically authorizes this request on their banking product which acts as an instruction to the bank to make the payment to SARS. Credit Push payments are considered to be irrevocable and can only be made if the account holder has the necessary funds. 30

32 How to set up a credit push on e-filing - Log onto e-filing and click on - Click on bank details Should you need to set up an account, click OR Should you need to update your banking details to a credit push, click Open 31

33 How to set up a credit push on e-filing - Select Credit Push - Scroll down to the bottom, enter the account name and click on the drop down arrow next to Credit Push 32

34 Processing Payment This tab will ONLY appear after filing a return/declaration or got an assessment that shows you must pay - Select Pay Now to proceed 33

35 Processing Payment - Click Ok - Navigate to Additional Payment Create Additional Payment under Returns 34

36 Processing Payment Make payment to proceed with payment or Save Payment to come back at a later stage to complete the payment 35

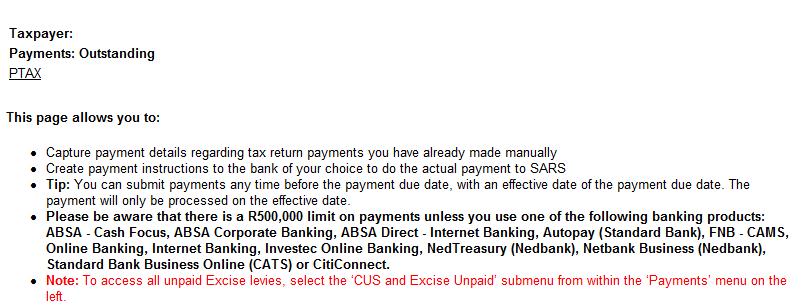

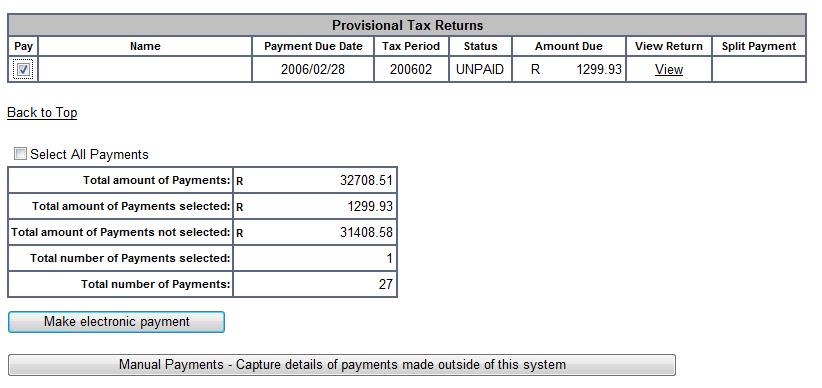

37 Processing Payment Click OK to continue or to save the payment OR Navigate to Payments General Unpaid A list of outstanding payments will appear. 36

38 37 Processing Payment

39 Processing Payment ABSA direct payments may only be made and authorised on the same day. 38

40 39 Processing Payment

41 Processing Payment If payment is successful, the following message will be displayed: 40

42 Payment Confirmation - Click Print Confirmation to print a copy of the transaction details for record purposes 41

43 Click Continue to proceed Payment Confirmation The Payment History page will be displayed. The credit push status will be indicated as "Awaiting Authorisation 42

44 Releasing a Credit Push at my bank Once you have processed your payment on SARS e-filing, you will need to authorise the payment to be released by SARS. Visit to help you with the instructions to follow by selecting your bank name from the website. 43

45 Payment Dates for Provisional Tax Payment dates refer to the 2019 YOA: First provisional tax payment due on: 31 August 2018 Second provisional tax payment due on: 28 February 2019 Third or voluntary payment due on: 30 September 2019 Methods to effect payments to SARS are available: At the Bank Via e-filing Via Electronic Funds Transfer (EFT) NB: Where payments are made electronically, provision must be made for your bank s cut-off times and for a clearance period that could take between two and five days 44

Visit your")

Open: Monday,")

46 Contact Us SARS Contact Centre SARS (7277) Visit your nearest SARS branch (to locate a branch visit Open: Monday, Tuesday, Thursday & Friday 08:00 to 16:00; Wednesday 09:00 to 16:00

47

Points Of Discussion

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

EXTERNAL GUIDE. How to efile your Provisional Tax Return

1. Register For efiling You will need to register as an efiling user before you can file your provisional tax return electronically. To register, go to www.sarsefiling.co.za 1.1. Click on Register 1.2.

1. Register For efiling You will need to register as an efiling user before you can file your provisional tax return electronically. To register, go to www.sarsefiling.co.za 1.1. Click on Register 1.2.

Disclaimer. Copyright notice

Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material) are based on the views and/or opinions of

Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material) are based on the views and/or opinions of

EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling

2013 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling 1 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling DISCLAIMER The information contained in this guide

2013 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling 1 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling DISCLAIMER The information contained in this guide

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

UNPACKING PROVISIONAL TAX PROCESSES 2016

UNPACKING PROVISIONAL TAX PROCESSES 2016 Prepared by Mark Silberman B.Acc C.A.(S.A.) Copyright Accfin Software Page 1 Contents 1. LAWS - THE CHANGING PROVISIONAL TAX PROCESSES... 5 A. Introduction... 5

UNPACKING PROVISIONAL TAX PROCESSES 2016 Prepared by Mark Silberman B.Acc C.A.(S.A.) Copyright Accfin Software Page 1 Contents 1. LAWS - THE CHANGING PROVISIONAL TAX PROCESSES... 5 A. Introduction... 5

Individual Income Tax

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

EXTERNAL GUIDE HOW TO COMPLETE AND SUBMIT YOUR COUNTRY BY COUNTRY INFORMATION

TABLE OF CONTENTS TABLE OF CONTENTS 2 1 PURPOSE 3 2 INTRODUCTION 3 3 THE CBC SUBMISSION 4 3.1 PERSON REQUIRED TO SUBMIT THE CBC 4 3.2 COMPLETE THE CBC REPORT, THE MASTER AND LOCAL FILE 4 3.3 SUBMIT CBC01

TABLE OF CONTENTS TABLE OF CONTENTS 2 1 PURPOSE 3 2 INTRODUCTION 3 3 THE CBC SUBMISSION 4 3.1 PERSON REQUIRED TO SUBMIT THE CBC 4 3.2 COMPLETE THE CBC REPORT, THE MASTER AND LOCAL FILE 4 3.3 SUBMIT CBC01

EXTERNAL GUIDE HOW TO SUBMIT AN OBJECTION OR APPEAL VIA EFILING

TABLE OF CONTENTS 1 PURPOSE 3 2 INTRODUCTION 3 3 LOGON TO THE EFILING WEBSITE 4 3.1 ACCESS THE REQUEST FOR OBJECTION OR APPEAL FORM AND ADMINISTRATIVE PENALTY ASSESSMENT NOTICE 4 3.2 DETAILED PROCEDURES

TABLE OF CONTENTS 1 PURPOSE 3 2 INTRODUCTION 3 3 LOGON TO THE EFILING WEBSITE 4 3.1 ACCESS THE REQUEST FOR OBJECTION OR APPEAL FORM AND ADMINISTRATIVE PENALTY ASSESSMENT NOTICE 4 3.2 DETAILED PROCEDURES

EXTERNAL GUIDE HOW TO COMPLETE THE REGISTRATION, AMENDMENTS AND VERIFICATION FORM (RAV01)

") REGISTRATION, AMENDMENTS TABLE OF CONTENTS 1 2 3 INTRODUCTION 3 INDIVIDUAL 4 REGISTERED REPRESENTATIVE 4 4 TAX PRACTITIONER 4 5 SARS REGISTERED DETAILS 5 6 ACTIVATE REGISTERED USER Tax Practitioner and

REGISTRATION, AMENDMENTS TABLE OF CONTENTS 1 2 3 INTRODUCTION 3 INDIVIDUAL 4 REGISTERED REPRESENTATIVE 4 4 TAX PRACTITIONER 4 5 SARS REGISTERED DETAILS 5 6 ACTIVATE REGISTERED USER Tax Practitioner and

External Guide on how to submit a Request for Remission

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

TCS (Tax Clearance Status) November 2018

November 2018") TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

Welcome to the SARS Tax Workshop

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Budget Highlights 2018

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

EXTERNAL REFERENCE GUIDE SECURITIES TRANSFER TAX. EXTERNAL GUIDE - SECURITIES TRANSFER TAX GEN-PAYM-11-G01 Revision: 3 EFFECTIVE DATE:

2013 EXTERNAL REFERENCE GUIDE SECURITIES EXTERNAL GUIDE - SECURITIES Revision: 3 EFFECTIVE DATE: 2013.11.30 DISCLAIMER The information contained in this guide is intended as guidance only and is not considered

2013 EXTERNAL REFERENCE GUIDE SECURITIES EXTERNAL GUIDE - SECURITIES Revision: 3 EFFECTIVE DATE: 2013.11.30 DISCLAIMER The information contained in this guide is intended as guidance only and is not considered

Source Codes. New Source Codes and Validations

Source Codes New Source Codes and Validations Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make

Source Codes New Source Codes and Validations Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make

GREATSOFT CRM CLIENT RELEASE NOTES

GREATSOFT CRM 2016.1.0 CLIENT RELEASE NOTES CONTENTS INTRODUCTION...1 Prerequisites...1 CRM...2 Tasks...2 Billings...2 Disbursements...2 TAX...2 ITR12 Changes for 2016...2 Other ITR12 Changes... 15 ITR14

GREATSOFT CRM 2016.1.0 CLIENT RELEASE NOTES CONTENTS INTRODUCTION...1 Prerequisites...1 CRM...2 Tasks...2 Billings...2 Disbursements...2 TAX...2 ITR12 Changes for 2016...2 Other ITR12 Changes... 15 ITR14

Introduction. Ayanda Takela (SARS efiling and specialist)

") Introduction Ayanda Takela (SARS efiling and e@syfile specialist) Agenda efiling Profile types Post-Death Registration Scenarios Process to a successful Registration Acquiring a new number Additional Estate

Introduction Ayanda Takela (SARS efiling and e@syfile specialist) Agenda efiling Profile types Post-Death Registration Scenarios Process to a successful Registration Acquiring a new number Additional Estate

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON ACCOMMODATION

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

Budget Highlight 2017

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

Global Mobility Services: Taxation of International Assignees - Swaziland

www.pwc.com/sz/en Global Mobility Services: Taxation of International Assignees - Swaziland People and Organisation Global Mobility Country Guide (Folio) Last Updated: June 2018 This document was not intended

www.pwc.com/sz/en Global Mobility Services: Taxation of International Assignees - Swaziland People and Organisation Global Mobility Country Guide (Folio) Last Updated: June 2018 This document was not intended

EXTERNAL FREQUENTLY ASKED QUESTIONS TAXPAYER CENTRICITY (CLIENT APPROACH. FUNCTIONALITY ON efiling)

") EXTERNAL FREQUENTLY ASKED S TAXPAYER CENTRICITY (CLIENT APPROACH FUNCTIONALITY ON Revision: 0 Page 1 of 6 1 PURPOSE These FAQs provide general information regarding taxpayer centricity, which is a new

EXTERNAL FREQUENTLY ASKED S TAXPAYER CENTRICITY (CLIENT APPROACH FUNCTIONALITY ON Revision: 0 Page 1 of 6 1 PURPOSE These FAQs provide general information regarding taxpayer centricity, which is a new

EXTERNAL GUIDE COMPREHENSIVE GUIDE TO THE ITR12T RETURN FOR TRUSTS

THE ITR12T RETURN FOR TABLE OF CONTENTS 1 INTRODUCTION... 6 2 GENERAL INFORMATION... 6 2.1 WHO MUST COMPLETE AND SUBMIT THE IT12T... 6 2.2 HOW TO OBTAIN A RETURN... 7 2.3 HOW TO SUBMIT A RETURN... 8 2.4

THE ITR12T RETURN FOR TABLE OF CONTENTS 1 INTRODUCTION... 6 2 GENERAL INFORMATION... 6 2.1 WHO MUST COMPLETE AND SUBMIT THE IT12T... 6 2.2 HOW TO OBTAIN A RETURN... 7 2.3 HOW TO SUBMIT A RETURN... 8 2.4

Value-Added Tax Registration Application

Value-Added Tax egistration Application VAT101 Taxpayer Information Nature of Person Partnership / Body of persons Company / CC / Shareblock Public authority / Municipality Association not for gain Estate

Value-Added Tax egistration Application VAT101 Taxpayer Information Nature of Person Partnership / Body of persons Company / CC / Shareblock Public authority / Municipality Association not for gain Estate

A person that elected to be registered as above must be registered by the Commissioner with effect from the beginning of that year of assessment.

6.1 WHO QUALIFIES TO REGISTER FOR TURNOVER TAX? A person that qualifies as a micro business may register for TT, if it is a: Natural person (or the deceased or insolvent estate of a natural person is registered

6.1 WHO QUALIFIES TO REGISTER FOR TURNOVER TAX? A person that qualifies as a micro business may register for TT, if it is a: Natural person (or the deceased or insolvent estate of a natural person is registered

New Tax VDP Applications using efiling. There are two parts to the application process: Tax Practitioner

Application Guide for efiling Tax Voluntary Disclosure Programme 2010 Introduction The South African Revenue Service (SARS) will implement a Voluntary Disclosure Porgramme (VDP) that will be effective

Application Guide for efiling Tax Voluntary Disclosure Programme 2010 Introduction The South African Revenue Service (SARS) will implement a Voluntary Disclosure Porgramme (VDP) that will be effective

Learnership Allowance

Learnership Allowance Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Learnership Allowance Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

efiling Account Management Guide - Payment Allocation

efiling Account Management Guide - Payment Allocation CONTENTS 1. How to obtain a payment listing... 1 2. How to allocate a payment... 3 3. How to re-allocate a payment... 6 4. How to request a payment

efiling Account Management Guide - Payment Allocation CONTENTS 1. How to obtain a payment listing... 1 2. How to allocate a payment... 3 3. How to re-allocate a payment... 6 4. How to request a payment

1. Objective of this manual What is efiling and how does it work in TaxWare? Why use TaxWare?... 3

efiling in TaxWare Index 1. Objective of this manual... 3 2. What is efiling and how does it work in TaxWare?... 3 2.1. Why use TaxWare?... 3 3. Activation of efiling on TaxWare... 3 3.1. Steps to activate

efiling in TaxWare Index 1. Objective of this manual... 3 2. What is efiling and how does it work in TaxWare?... 3 2.1. Why use TaxWare?... 3 3. Activation of efiling on TaxWare... 3 3.1. Steps to activate

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained 1 To Mr. Anil Naidoo

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained To Mr. Anil Naidoo From Tax Manager Subject Tax implications of issues discussed Date 4 December 207 Sub Total Scope We refer to our

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained To Mr. Anil Naidoo From Tax Manager Subject Tax implications of issues discussed Date 4 December 207 Sub Total Scope We refer to our

WHAT TO DO WITH YOUR IRP YEAR OF ASSESSMENT

WHAT TO DO WITH YOUR IRP5 2014 YEAR OF ASSESSMENT Office staff must take into account the undermentioned on receipt of their IRP5 tax certificates for the 2014 tax year ended 28 February 2014. Contact

WHAT TO DO WITH YOUR IRP5 2014 YEAR OF ASSESSMENT Office staff must take into account the undermentioned on receipt of their IRP5 tax certificates for the 2014 tax year ended 28 February 2014. Contact

Introduction. Lerato Mokoena (SARS Support Consultant-eFiling and specialist) Gauteng and Northwest Province

Gauteng and Northwest Province") Introduction Lerato Mokoena (SARS Support Consultant-eFiling and E@syfile specialist) Gauteng and Northwest Province lmokoena2@sars.gov.za Topics to be discussed Tax Compliance status Functionality on

Introduction Lerato Mokoena (SARS Support Consultant-eFiling and E@syfile specialist) Gauteng and Northwest Province lmokoena2@sars.gov.za Topics to be discussed Tax Compliance status Functionality on

Welcome to the SARS Tax Workshop

29 August 2017 Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more

29 August 2017 Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more

DECEASED ESTATES REGISTRATION & ASSESSMENT

DECEASED ESTATES REGISTRATION & ASSESSMENT Agenda Introduction Position - deaths prior to 1 March 2016 Position - deaths post 1 March 2016 Registration process for Deceased Person Registration process

DECEASED ESTATES REGISTRATION & ASSESSMENT Agenda Introduction Position - deaths prior to 1 March 2016 Position - deaths post 1 March 2016 Registration process for Deceased Person Registration process

EXTERNAL GUIDE GUIDE TO THE ITR12 RETURN FOR DECEASED ESTATES. (For persons who die on or after 1 March 2016)

") EXTERNAL GUIDE GUIDE TO THE ITR12 RETURN FOR DECEASED ESTATES (For persons who die on or after 1 March 2016) TABLE OF CONTENTS 1 PURPOSE... 4 2 GENERAL INFORMATION... 4 2.1... 4 2.2 HOW TO SUBMIT A RETURN

EXTERNAL GUIDE GUIDE TO THE ITR12 RETURN FOR DECEASED ESTATES (For persons who die on or after 1 March 2016) TABLE OF CONTENTS 1 PURPOSE... 4 2 GENERAL INFORMATION... 4 2.1... 4 2.2 HOW TO SUBMIT A RETURN

TAXATION IN SOUTH AFRICA 2013/14

SOUTH AFRICAN REVENUE SERVICE TAXATION IN SOUTH AFRICA 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Taxation in South Africa 2013/14 This is a general guide

SOUTH AFRICAN REVENUE SERVICE TAXATION IN SOUTH AFRICA 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Taxation in South Africa 2013/14 This is a general guide

Income Tax. Tax Guide for Small Businesses 2015/16

Income Tax Tax Guide for Small Businesses 2015/16 Preface Tax Guide for Small Businesses 2015/2016 This guide is a general guide dealing with the taxation of small businesses. This guide is not an official

Income Tax Tax Guide for Small Businesses 2015/16 Preface Tax Guide for Small Businesses 2015/2016 This guide is a general guide dealing with the taxation of small businesses. This guide is not an official

Guide for tax rates/duties/levies (Issue 11)

") Guide for tax rates/duties/levies (Issue 11) Guide for tax rates/duties/levies Preface This is a guide provides a current and historical view of the rates for various taxes, duties and levies collected

Guide for tax rates/duties/levies (Issue 11) Guide for tax rates/duties/levies Preface This is a guide provides a current and historical view of the rates for various taxes, duties and levies collected

ACE Centralised Payment Guidance. Training Providers. August 2013

ACE Centralised Payment Guidance Training Providers August 2013 We recommend installing the latest Adobe Acrobat Reader for the best viewing experience: http://get.adobe.com/reader/ Contents 2 Contents

ACE Centralised Payment Guidance Training Providers August 2013 We recommend installing the latest Adobe Acrobat Reader for the best viewing experience: http://get.adobe.com/reader/ Contents 2 Contents

HONORARIA BRANCH RELEASE NOTES

RMS Operations BRANCH HONORARIA BRANCH RELEASE NOTES DATE January 2018 TITLE AUTHOR AUDIENCE Live Branch Honoraria Business Process RMS Operations Branches Amendment Record Amended version Summary of amendments

RMS Operations BRANCH HONORARIA BRANCH RELEASE NOTES DATE January 2018 TITLE AUTHOR AUDIENCE Live Branch Honoraria Business Process RMS Operations Branches Amendment Record Amended version Summary of amendments

NHS Pensions Online Guide 40. Greenbury guide

NHS Pensions Online Guide 40. Greenbury guide 40. Greenbury Guide-20171204-(V12) 1 Table of contents Overview:... 3 1. Allocation of Greenbury screen access... 3 Allocating Greenbury access to an existing

NHS Pensions Online Guide 40. Greenbury guide 40. Greenbury Guide-20171204-(V12) 1 Table of contents Overview:... 3 1. Allocation of Greenbury screen access... 3 Allocating Greenbury access to an existing

True Potential Investor Overdue Payments. Contents

OVERDUE PAYMENTS Contents Overdue Payments 3 Pay Reference Periods 3 Pay Reference Period Start Dates - Examples: 3 Overdue Payments page 4 View Members 5 Upload Contribution 5 The Contributions Template

OVERDUE PAYMENTS Contents Overdue Payments 3 Pay Reference Periods 3 Pay Reference Period Start Dates - Examples: 3 Overdue Payments page 4 View Members 5 Upload Contribution 5 The Contributions Template

As a small business are you finding it difficult to juggle your taxes?

As a small business are you finding it difficult to juggle your taxes? Introducing Turnover Tax The all-in-one tax that s simple and saves you time and money. Turn over to a new tax! Small businesses have

As a small business are you finding it difficult to juggle your taxes? Introducing Turnover Tax The all-in-one tax that s simple and saves you time and money. Turn over to a new tax! Small businesses have

EXTERNAL FREQUENTLY ASKED QUESTIONS SECURITIES TRANSFER TAX

EXTERNAL FREQUENTLY ASKED S SECURITIES TRANSFER TAX Revision: 1 Page 1 of 8 1 PURPOSE This document provides general information regarding Securities Transfer Tax (STT) to all taxpayers. It is not intended

EXTERNAL FREQUENTLY ASKED S SECURITIES TRANSFER TAX Revision: 1 Page 1 of 8 1 PURPOSE This document provides general information regarding Securities Transfer Tax (STT) to all taxpayers. It is not intended

Tax year end processing

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

VALUE ADDED TAX (VAT) RETURNS USER GUIDE

RETURNS USER GUIDE") VALUE ADDED TAX (VAT) RETURNS USER GUIDE February 2018 1 Contents 1. Brief overview of this user guide... 3 2. Important notes about the VAT Return... 3 3. Completing and Submitting the VAT Return Form...

VALUE ADDED TAX (VAT) RETURNS USER GUIDE February 2018 1 Contents 1. Brief overview of this user guide... 3 2. Important notes about the VAT Return... 3 3. Completing and Submitting the VAT Return Form...

EXPLANATORY MEMORANDUM

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 2 EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 Currently, the unemployment

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 2 EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 Currently, the unemployment

STEPS FOR GENERATING ITREG-FILE FOR AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for

sedert 1982 STEPS FOR GENERATING ITREG-FILE FOR e@syfile, AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for e@syfile. 1. Start your reconciliation process by generating the ITREG-file for e@syfile.

sedert 1982 STEPS FOR GENERATING ITREG-FILE FOR e@syfile, AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for e@syfile. 1. Start your reconciliation process by generating the ITREG-file for e@syfile.

MFC AUCTIONS STEP BY STEP ONLINE AUCTION GUIDE. MFC a division of Nedbank

MFC AUCTIONS STEP BY STEP ONLINE AUCTION GUIDE MFC a division of Nedbank MFC AUCTIONS 5 STEPS TO BUYING A VEHICLE ON AUCTION View (Auctions) Browse the Auctions and view the catalogue of available vehicles

MFC AUCTIONS STEP BY STEP ONLINE AUCTION GUIDE MFC a division of Nedbank MFC AUCTIONS 5 STEPS TO BUYING A VEHICLE ON AUCTION View (Auctions) Browse the Auctions and view the catalogue of available vehicles

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

OVERVIEW PAYE 2010 NOVEMBER

OVERVIEW PAYE 2010 NOVEMBER 1 Contents 1. Introduction... 3 2. The aim of the Pay-As-You-Earn (PAYE) reconciliation process... 3 3. What is reconciliation?... 4 4. The Pay-As-You-Earn (PAYE) process...

OVERVIEW PAYE 2010 NOVEMBER 1 Contents 1. Introduction... 3 2. The aim of the Pay-As-You-Earn (PAYE) reconciliation process... 3 3. What is reconciliation?... 4 4. The Pay-As-You-Earn (PAYE) process...

Clubs or societies return guide 2012

IR 9GU March 2012 Clubs or societies return guide 2012 Read this guide to help you fill in your IR 9 return. Complete and send us your IR 9 return by 7 July 2012, unless you have an extension of time to

IR 9GU March 2012 Clubs or societies return guide 2012 Read this guide to help you fill in your IR 9 return. Complete and send us your IR 9 return by 7 July 2012, unless you have an extension of time to

Latest tax developments. May 2016

Latest tax developments May 2016 Introduction Monthly webinar 5 th of 11 webinars Recent developments This one May 2016; Cannot cover all developments in detail; Relevance of developments; Some will roll

Latest tax developments May 2016 Introduction Monthly webinar 5 th of 11 webinars Recent developments This one May 2016; Cannot cover all developments in detail; Relevance of developments; Some will roll

Tax, ETI and UIF Amendments 2018/2019

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

Creating a PO with a Future Date

Creating a PO with a Future Date Core-CT allows you to create a PO with a future date. This functionality can be used when creating a PO that is associated with a contract that is future dated or during

Creating a PO with a Future Date Core-CT allows you to create a PO with a future date. This functionality can be used when creating a PO that is associated with a contract that is future dated or during

HOW TO COMPLETE THE IT14 RETURN

HOW TO COMPLETE THE IT14 RETURN INTRODUCTION This guide is designed to help to accurately complete income tax returns for companies and close corporations (CC). For assistance visit your local SARS branch

HOW TO COMPLETE THE IT14 RETURN INTRODUCTION This guide is designed to help to accurately complete income tax returns for companies and close corporations (CC). For assistance visit your local SARS branch

TAX GUIDE FOR SMALL BUSINESSES 2013/14

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

TRAVEL PORTAL INSTRUCTIONS

TRAVEL PORTAL INSTRUCTIONS Date: June 22, 2018 Version: Version 3.1 Prepared By: Berkley Canada Table of Contents 1 ACCESSING THE PORTAL... 3 1.1 LOGIN & LOGOUT... 3 1.2 RESET YOUR PASSWORD... 3 2 THE

TRAVEL PORTAL INSTRUCTIONS Date: June 22, 2018 Version: Version 3.1 Prepared By: Berkley Canada Table of Contents 1 ACCESSING THE PORTAL... 3 1.1 LOGIN & LOGOUT... 3 1.2 RESET YOUR PASSWORD... 3 2 THE

EXTERNAL FREQUENTLY ASKED QUESTIONS DISPUTE ADMINISTRATION

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

Individual Training Account Making and Managing Claims for ITA Funding on FIPS

Individual Training Account Making and Managing Claims for ITA Funding on FIPS October 2017 V2 Table of Contents Information on Claiming ITA Payments 3 Make a Claim (step by step process) 5 Viewing and

Individual Training Account Making and Managing Claims for ITA Funding on FIPS October 2017 V2 Table of Contents Information on Claiming ITA Payments 3 Make a Claim (step by step process) 5 Viewing and

Striving for Social Justice

Striving for Social Justice The St. Christopher and Nevis Social Security Board St. Christopher and Nevis Social Security Act, 1977 No. 13 of 1977 An Act to repeal the National Provident Fund Act and to

Striving for Social Justice The St. Christopher and Nevis Social Security Board St. Christopher and Nevis Social Security Act, 1977 No. 13 of 1977 An Act to repeal the National Provident Fund Act and to

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS. Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

GOVERNMENT GAZETTE REPUBLIC OF NAMIBIA

GOVERNMENT GAZETTE OF THE REPUBLIC OF NAMIBIA u,~ N$1.00 WINDHOEK 3 December 1999 No. 2240 CONTENTS Page GOVERNMENT NOTICE No. 275 Promulgation of Income Tax Second Amendment Act, 1999 (Act No. 21 of 1999),

GOVERNMENT GAZETTE OF THE REPUBLIC OF NAMIBIA u,~ N$1.00 WINDHOEK 3 December 1999 No. 2240 CONTENTS Page GOVERNMENT NOTICE No. 275 Promulgation of Income Tax Second Amendment Act, 1999 (Act No. 21 of 1999),

Corporate Income Tax. Withholding Tax. Basis of Taxation. Exemptions. Corporate Tax Rebate (Temporary) Residence. Dividends 0 15*

Residence. Dividends 0 15*") SINGAPORE TAX FACTS Corporate Income Tax Basis of Taxation Singapore taxes businesses on a preceding year basis on Singapore-sourced income and on foreign-sourced income remitted into Singapore. Whether

SINGAPORE TAX FACTS Corporate Income Tax Basis of Taxation Singapore taxes businesses on a preceding year basis on Singapore-sourced income and on foreign-sourced income remitted into Singapore. Whether

Government Gazette REPUBLIC OF SOUTH AFRICA

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

The values within the DMS can be held as consolidated totals if required, as any individual items can be extracted from the Service Plan System.

VERSION 3.1.1 The principle idea of the accounting system is to mirror the balance sheet values held within the edynamix Service Plan system with those held on the Dealer Management System (DMS) balance

VERSION 3.1.1 The principle idea of the accounting system is to mirror the balance sheet values held within the edynamix Service Plan system with those held on the Dealer Management System (DMS) balance

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

Example IT14 C C Y Y M M D D Y Y M M D D C C / / / PARTICULARS OF COMPANY / CLOSE CORPORATION PARTICULARS OF PUBLIC OFFICER

Registered ame Trade ame PARTICULARS OF PUBLIC OFFICER Domicilium Citandi Et Executandi (Address for legal purposes) PARTICULARS OF COMPA / CLOSE CORPORATIO Surname Cell no. contact telephone no. I declare

Registered ame Trade ame PARTICULARS OF PUBLIC OFFICER Domicilium Citandi Et Executandi (Address for legal purposes) PARTICULARS OF COMPA / CLOSE CORPORATIO Surname Cell no. contact telephone no. I declare

Exception Report Guide. August 2018

Exception Report Guide August 2018 Quick Payroll Exception Error Guides We understand your day-to-day challenges; this is why we want to try to make your business life easier. We have prepared this guide

Exception Report Guide August 2018 Quick Payroll Exception Error Guides We understand your day-to-day challenges; this is why we want to try to make your business life easier. We have prepared this guide

UNEMPLOYMENT INSURANCE CONTRIBUTIONS ACT NO 4 OF 2002

UNEMPLOYMENT INSURANCE CONTRIBUTIONS ACT NO 4 OF 2002 [ASSENTED TO 27 MARCH 2002 ] [ENGLISH TEXT SIGNED BY PRESIDENT.] AS AMENDED BY TAXATION LAWS AMENDMENT ACT, NO. 30 OF 2002 REVENUE LAWS AMENDMENT ACT,

UNEMPLOYMENT INSURANCE CONTRIBUTIONS ACT NO 4 OF 2002 [ASSENTED TO 27 MARCH 2002 ] [ENGLISH TEXT SIGNED BY PRESIDENT.] AS AMENDED BY TAXATION LAWS AMENDMENT ACT, NO. 30 OF 2002 REVENUE LAWS AMENDMENT ACT,

Tax guide 2018/2019 TAX FACTS

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

Classic Investment Plan

STANLIB Wealth Management Limited Registration number 1996/005412/06 Authorised Administrative FSP in terms of the FAIS Act, 2002 (FSP No. 26/10/590) 17 Melrose Boulevard Melrose Arch 2196 P O Box 202

STANLIB Wealth Management Limited Registration number 1996/005412/06 Authorised Administrative FSP in terms of the FAIS Act, 2002 (FSP No. 26/10/590) 17 Melrose Boulevard Melrose Arch 2196 P O Box 202

Overview of PAYE reconciliation process and 2007/08 policy changes. Another helpful guide brought to you by South African Revenue Service

Overview of PAYE reconciliation process and 2007/08 policy changes Another helpful guide brought to you by South African Revenue Service Overview of PAYE reconciliation process and 2007/08 policy changes

Overview of PAYE reconciliation process and 2007/08 policy changes Another helpful guide brought to you by South African Revenue Service Overview of PAYE reconciliation process and 2007/08 policy changes

This Notice requires you by law to send me

Tax Return for the year ended 5 April 2003 UTR Tax reference Employer reference Issue address Date Inland Revenue office address Area Director SA100 Telephone Please read this page first The green arrows

Tax Return for the year ended 5 April 2003 UTR Tax reference Employer reference Issue address Date Inland Revenue office address Area Director SA100 Telephone Please read this page first The green arrows

Change, the new certainty

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

Global Mobility Services: Taxation of International Assignees - Malawi

www.pwc.com/mw/en Global Mobility Services: Taxation of International Assignees - Malawi Taxation issues & related matters for employers & employees 2017/18 Last Updated: June 2018 This document was not

www.pwc.com/mw/en Global Mobility Services: Taxation of International Assignees - Malawi Taxation issues & related matters for employers & employees 2017/18 Last Updated: June 2018 This document was not

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER 0 Initial Release A Scheepers GM Operational Services

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

Estate Agency Affairs Board. Tax Notes

Estate Agency Affairs Board Tax Notes Contents Page Chapter 1: Tax Administration Act... 1 Part A - Objections... 2 A.1 What assessments and decisions may be objected against?... 2 A.2 SARS s decision

Estate Agency Affairs Board Tax Notes Contents Page Chapter 1: Tax Administration Act... 1 Part A - Objections... 2 A.1 What assessments and decisions may be objected against?... 2 A.2 SARS s decision

D-BIT Payroll. Tax Year End Guide - Preparation And Procedures For Tax Year End D-BIT SYSTEMS (Pty) Ltd D-BIT Systems (Pty) Ltd

Ltd D-BIT Systems (Pty) Ltd") D-BIT SYSTEMS (Pty) Ltd RegNo: 87/0332407 7 Boskruin Business Park Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 2156 South Africa D-BIT Payroll Tax Year End Guide - Preparation And Procedures

D-BIT SYSTEMS (Pty) Ltd RegNo: 87/0332407 7 Boskruin Business Park Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 2156 South Africa D-BIT Payroll Tax Year End Guide - Preparation And Procedures

TAXATION IN SOUTH AFRICA 2016/7

Retirement Fund March 2016 TAXATION IN SOUTH AFRICA 2016/7 Your Retirement - Our Passion Sentinel Retirement Fund Reg No 12/8/1215 Sentinel House 1 Sunnyside Drive Sunnyside Park PARKTOWN 2193 P O Box

Retirement Fund March 2016 TAXATION IN SOUTH AFRICA 2016/7 Your Retirement - Our Passion Sentinel Retirement Fund Reg No 12/8/1215 Sentinel House 1 Sunnyside Drive Sunnyside Park PARKTOWN 2193 P O Box

(Contact us if you need help: Call between 07:30-17:30 (Mon - Fri) or

or") RETIREMENT ANNUITY FUND WITHDRAWAL INSTRUCTION Make an informed decision: BEFORE YOU WITHDRAW ADDITIONAL INFORMATION STEP 1 COMPLETE THE FORM & AGREE TO CONDITIONS OF MEMBERSHIP Please consider the tax

RETIREMENT ANNUITY FUND WITHDRAWAL INSTRUCTION Make an informed decision: BEFORE YOU WITHDRAW ADDITIONAL INFORMATION STEP 1 COMPLETE THE FORM & AGREE TO CONDITIONS OF MEMBERSHIP Please consider the tax

Welcome to the SARS Tax Workshop

Small Business Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Small Business Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

MYOB Advanced. Release Notes

MYOB Advanced Release Notes 2017.1.13 Contents Introduction 1... 1 Installing this Release... 1 New Features 2 Payroll Compliance Updates... 2 Single Touch Payroll... 2 Setting up STP... 2 Submitting Data

MYOB Advanced Release Notes 2017.1.13 Contents Introduction 1... 1 Installing this Release... 1 New Features 2 Payroll Compliance Updates... 2 Single Touch Payroll... 2 Setting up STP... 2 Submitting Data

Unit: Banking Topic: Incoming Payments. Field Name or Data Type. Due Date < Past date >

Solutions Unit: Banking Topic: Incoming Payments 1-1 Incoming Payment (using cash payment means) 1-1-1 Create an A/R Invoice Choose Sales A/R A/R Invoice. Due Date < Past date > Post this invoice to any

Solutions Unit: Banking Topic: Incoming Payments 1-1 Incoming Payment (using cash payment means) 1-1-1 Create an A/R Invoice Choose Sales A/R A/R Invoice. Due Date < Past date > Post this invoice to any

Terms and Conditions Offshore Investment Account

Wealth and Investment Management Terms and Conditions Offshore Investment Account Legal Terms 1. Definitions 1.1 Account means the AIMS Offshore Investment Account; 1.2 BAGL means Barclays Africa Group

Wealth and Investment Management Terms and Conditions Offshore Investment Account Legal Terms 1. Definitions 1.1 Account means the AIMS Offshore Investment Account; 1.2 BAGL means Barclays Africa Group

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

Income Tax. ABC of Capital Gains Tax for Companies (Issue 7) ABC of Capital Gains Tax for Companies (Issue 7) 1

ABC of Capital Gains Tax for Companies (Issue 7) 1") Income Tax ABC of Capital Gains Tax for Companies (Issue 7) ABC of Capital Gains Tax for Companies (Issue 7) 1 Preface ABC of Capital Gains Tax for Companies This guide provides a basic introduction to

Income Tax ABC of Capital Gains Tax for Companies (Issue 7) ABC of Capital Gains Tax for Companies (Issue 7) 1 Preface ABC of Capital Gains Tax for Companies This guide provides a basic introduction to

Taxation Laws Amendment Acts No. 15 of 2016 & 16 of 2016

No. 3 of 2017 February 2017 Taxation Laws Amendment Acts No. 15 of 2016 & 16 of 2016 A. The Taxation Laws Amendment Act No. 15 of 2016 was promulgated in Government Gazette No. 40562 on 19 January 2017.

No. 3 of 2017 February 2017 Taxation Laws Amendment Acts No. 15 of 2016 & 16 of 2016 A. The Taxation Laws Amendment Act No. 15 of 2016 was promulgated in Government Gazette No. 40562 on 19 January 2017.

Quick Start Guide to Payroll Tax Year-End

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

EXTERNAL GUIDE GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017

GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 BACKGROUND 3 3.1 RECONCILIATION PROCESS 3 3.2 INTERIM RECONCILIATION PROCESS 3 3.3 GENERAL

GUIDE FOR VALIDATION RULES APPLICABLE TO RECONCILIATION DECLARATIONS 2017 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 BACKGROUND 3 3.1 RECONCILIATION PROCESS 3 3.2 INTERIM RECONCILIATION PROCESS 3 3.3 GENERAL

TAX GROUP USER GUIDE (REGISTRATION, AMENDMENT AND DE- REGISTRATION) December 2017

December 2017") TAX GROUP USER GUIDE (REGISTRATION, AMENDMENT AND DE- REGISTRATION) December 2017 Contents 1. Brief overview of this user guide... 3 2. Creating and using your e-services account... 4 2.1 Create an e-services

TAX GROUP USER GUIDE (REGISTRATION, AMENDMENT AND DE- REGISTRATION) December 2017 Contents 1. Brief overview of this user guide... 3 2. Creating and using your e-services account... 4 2.1 Create an e-services

Zurich Life Commission Statements & Payments

Zurich Life Commission Statements & Payments Technical Guide For Financial Advisor use only Contents This guide to Zurich Life Commission Statements & Payments includes the following: Introduction... Page

Zurich Life Commission Statements & Payments Technical Guide For Financial Advisor use only Contents This guide to Zurich Life Commission Statements & Payments includes the following: Introduction... Page

INSTITUTIONAL INVESTOR PASSPORT USER GUIDE

INSTITUTIONAL INVESTOR PASSPORT USER GUIDE Welcome to Passport. The enhanced design addresses the specialized needs of the Benefit Payment Administrator to quickly access and effectively analyze your retiree

INSTITUTIONAL INVESTOR PASSPORT USER GUIDE Welcome to Passport. The enhanced design addresses the specialized needs of the Benefit Payment Administrator to quickly access and effectively analyze your retiree

Attaché Payroll 2017/18. End of Year Procedures

Attaché Payroll 2017/18 End of Year Procedures Table of Contents Which Version of Attaché Do I Need to Process End of Year?... 4 Checking that All Operators have Exited Attaché... 5 Blocking Access to

Attaché Payroll 2017/18 End of Year Procedures Table of Contents Which Version of Attaché Do I Need to Process End of Year?... 4 Checking that All Operators have Exited Attaché... 5 Blocking Access to

What s new at SARS? VAT COMPLIANCE

This image cannot currently be displayed. This image cannot currently be displayed. 2015/11/11 What s new at SARS? VAT COMPLIANCE 1 This image cannot currently be displayed. This image cannot currently

This image cannot currently be displayed. This image cannot currently be displayed. 2015/11/11 What s new at SARS? VAT COMPLIANCE 1 This image cannot currently be displayed. This image cannot currently

ICC UAE VAT RETURNS WORKSHOP. 29 th March 2018 Dubai Chamber of Commerce & Industry

ICC UAE VAT RETURNS WORKSHOP 29 th March 2018 Dubai Chamber of Commerce & Industry OVERVIEW OF VAT Direct Tax The person paying the tax to the Government directly bears the incidence of tax It is progressive

ICC UAE VAT RETURNS WORKSHOP 29 th March 2018 Dubai Chamber of Commerce & Industry OVERVIEW OF VAT Direct Tax The person paying the tax to the Government directly bears the incidence of tax It is progressive