Welcome to the SARS Tax Workshop

|

|

|

- Jonah Nash

- 6 years ago

- Views:

Transcription

1 Small Business

2 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible. The information therefore has no binding legal effect and the relevant legislation must be consulted in the event of any doubt as to the meaning or application of any provision.

3 Small Business

4 Points for Discussion Overview Business Types SBC Incentives Example of Income Statement Requirements for VAT Registration Tax clearance process Recordkeeping

5 Overview Why are we paying taxes? Every government is mandated to provide basic services to Basic services include: citizens Education Health Welfare (Child Grants/Old Age Pensions) Policing Every citizen enjoys the benefits of one or other government basic service

6 Overview Why are we paying taxes? Government has a social responsibility towards citizens of this country Social responsibility can only be fulfilled if the necessary taxes have been paid by the people earning taxable income in this country

7 Business Types Individuals: Sole Proprietor Partnership Companies/Close Corporations Trusts

8 Sole Proprietor Single owner Easy to establish Business decision made by owner Owner receives ALL profits Easy to discontinue business

9 Sole Proprietor Limited skill of owner In running business Product knowledge Limited ability to raise capital 2 nd bond on personal property Pension on retirement used as capital Unlimited liability of business debt Private assets at risk

10 Sole Proprietor Business is not seen as a tax entity Business name is not registered with SARS Owner is responsible for tax on profit made

Greater financial strength")

11 Partnership Two or more owners (max 20 partners) Greater financial strength Business decisions are shared based on skills Easy to establish and Easy to discontinue business

12 Partnership Disadvantages Partnership dissolves each time the partners change Not legal entity Lesser degree of business continuity Partners need to be registered individually for tax Each partner is held liable for debt of entire partnership Decision making is shared Business partners are jointly and individually liable for the actions of the other partners Differences of opinion could slow the process down Profit sharing and Tax Partners are responsible for tax on profit made in relation to the profit sharing ratio

13 Partnership Advantages Wider pool of knowledge, skills and contacts Can be cost-effective Benefit from the combination of complimentary skills of two or more people Each partner specializes in certain aspects of their business Raising Capital/funds Two or more partners may be able to contribute more funds because their borrowing capacity may be greater Employee retention Prospective employees may be attracted to the business if given the incentive to become a partner Innovation and support Provide moral support and will allow for more creative brainstorming

14 Company Separate legal entity given juristic personality Exists as a legal entity apart from its members or owners Investors contribute money or other assets to a company Investors hold a share or interest in that company A company s year of assessment is the same as its financial year (not necessarily end Feb)

15 Company Company needs to register as a taxpayer Company responsible to pay tax on profit Directors/mem bers treated as employees for PAYE purposes Company must register for PAYE

16 Company Disadvantages COMPLEX Subject to many legal requirements EXPENSIVE More difficult and expensive to establish and operate

Testamentary (created at")

17 Trusts Trust is a legal entity in its own right and pays tax on profits unless distributed Used for Estate planning Inter Vivos Trust (created during your life) Testamentary (created at death)

18 Tax rates ENTITY Companies and Close Corporations Small Business Corporations TAX RATE 28% flat rate Split rate Trusts: Normal trust 41% flat rate Special trust According to tax tables Natural person According to tax tables

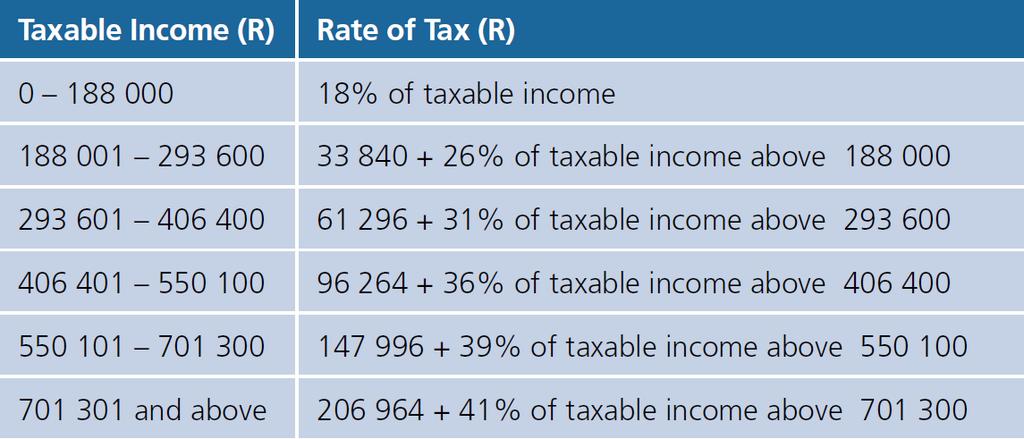

19 Individual tax rates

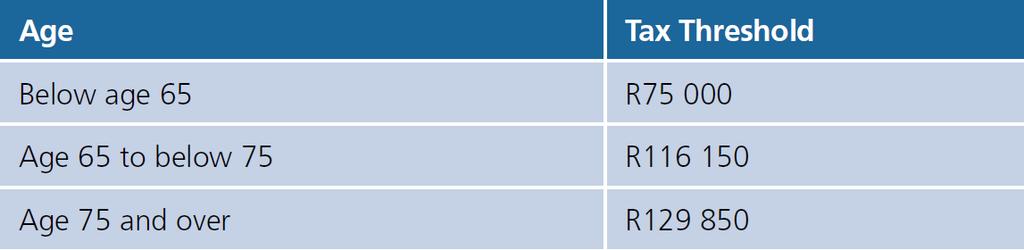

20 Individual tax rebates and thresholds Rebates Thresholds

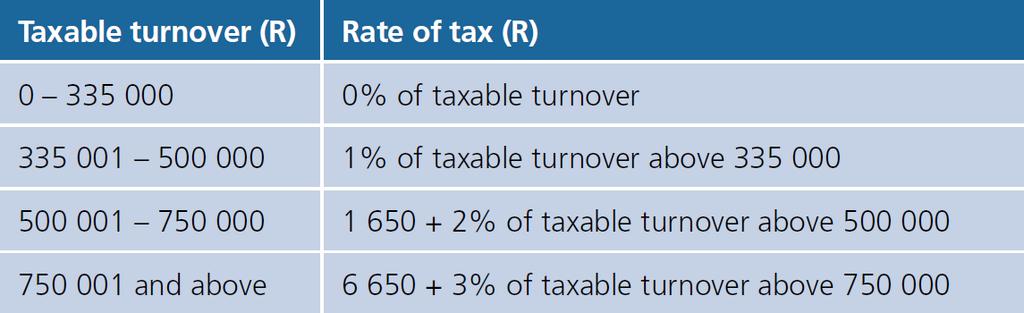

Loss (R 18 000) R 0 (R 48 000) Profit R 45 000 R 0 (R 3000) Profit R 53 000 R 50")

21 Tax Registration NO tax is paid if business makes a loss Business losses are accumulated until a taxable profit is reflected Tax only paid when a profit is made (known as ring fencing) Year 1 Year 2 Year 3 Year 4 Income Taxable Balance Loss (R ) R 0 (R ) Loss (R ) R 0 (R ) Profit R R 0 (R 3000) Profit R R R 0

22 SBC Requirements SBC is not another type of business entity SBC is a type of tax incentive Not more than 20% of revenue may consist of investment income Not more than 20% income from rendering a Personal Service

Shareholding held for the entire year by natural")

23 SBC Requirements Co-Operatives & Private Companies Not applicable to sole proprietors, partnerships, trusts Shareholding held by Natural Persons (Individuals) Shareholding held for the entire year by natural persons Imperative to deregister from other CC s or companies before starting new venture Shareholders to have no interest in other Company Gross Income not exceeding R per year Includes Dormant/ Shelf / Non Trading Companies Excludes listed companies and companies exempt from the payment of Income Tax and some other exceptions Pro Rata amount if trading less than 12 months- Not taxable income, is based on gross income

24 SBC Requirements Dividends Rental from immovable property Interest income Royalties Investment Income

25 SBC Requirements Service is rendered through a CC/ Company Service is performed by Member or Shareholder A person includes a Connected Person Connected person refers to family to the 3 rd degree Personal Service

26 Connected Persons Taxpayer`s grand child Parents =nearest common ancestor Related to parents in the 1 st degree Nephew/niece is related through his father to the taxpayer s father Relative includes the spouse and those related to him/ her to the 3 rd degree Total steps: 1 (parent) + 2 (brother + nephew) = 3 Taxpayer`s Aunt Taxpayer Taxpayer`s child Taxpayer`s Sister Taxpayer`s Great Grand Parents Taxpayer`s Grand Parents Taxpayer`s Parents Taxpayer`s brother Taxpayer`s niece/ nephew

27 SBC Requirements Personal Service is an activity specifically listed in the Act: Accounting Actuarial Science Management Surveying Broadcasting Engineering Sport Auditing Education Law Auctioneering Draftsmanship Journalism Veterinary Services Consulting Information Technology Research Architecture Health Translation Valuation Financial Service Broking Real Estate Broking

28 SBC Requirements Personal Service not applicable if: The CC or Company employs 3 or more permanent staff members throughout the year and the service is not performed by any person who holds an interest in the company Employees cannot be connected to Members / Shareholders If Personal Service not applicable then 20 % rule only applies to Investment Income Employees should be permanent and cannot be connected to Members / Shareholders Minimum of 3 employees should at all times be employed, throughout the year

29 SBC Tax rates Reduced tax rate for Close Corporations No need to apply for SBC status indicate on tax return Apply yearly if requirements are met

30 Turnover Tax rates

31 Benefits of SBC Split rate system of taxation Income Sole Proprietor Turnover Tax Partnership (based on 2 partners) Company SBC

32 Benefits of SBC Sole Proprietor Turnover Tax Partnership Company SBC

33 Benefits of SBC Benefits Immediate write off of all plant machinery used in the process of manufacture An accelerated write-off allowance for depreciable assets (other than manufacturing assets) 50% 1 st year 30% 2 nd year 20% 3 rd year

34 Example of an Income Statement What is it? An income statement is also known as the "Income and Expenditure Statement" or the "Profit and Loss Statement". It is a summary of what income your business has earned, and what expenditure you have made, during the last month or year, or whatever period you want to review. Where the Balance Sheet shows the solvency of your business (are your assets more than your liabilities), and the Cash Flow Statement shows the liquidity of your business (do you have enough cash to pay the bills and salaries), the Income Statement shows you how much profit or loss you are making.

35 Example of an Income Statement INCOME STATEMENT Company's name End Period <PERIOD> Revenue: 0.00 Gross Sales 0.00 Less: Sales Returns and Allowances 0.00 Cost of Goods Sold: 0.00 Materials 0.00 Other direct expenses 0.00 Gross Profit (Loss) 0.00 Other Income: 0.00 Discount received 0.00 Rental income 0.00 Gain (Loss) on Sale of Assets 0.00 Interest received 0.00 Gross Income 0.00 Expenses: Financial expenses 0.00

36 Example of an Income Statement Cont.. Bank Charges and commissions 0.00 Interest 0.00 Personnel expenses 0.00 Wages 0.00 Payroll Taxes 0.00 Other Operational Expenses 0.00 Amortization 0.00 Insurance 0.00 Maintenance & Repairs 0.00 Marketing 0.00 Miscellaneous 0.00 Office Expenses 0.00 Permits and Licenses 0.00 Rent 0.00 Telephone 0.00 Travel 0.00 Utilities 0.00 Vehicle Expenses 0.00 Total Operational Expenses 0.00 Net Income (Loss) 0.00

37 Sources for Income Statements for SBC and SSME`s.. nt/en/56681/income-statement-template ets/pages/theincomestatement.aspx

38 Requirements VAT Registration

39 Tax Administration Act Registration Requirements A person obliged to apply to; or who may voluntarily, register with SARS under a tax Act must do so in terms of the requirements of the TAACT Chapter 3 or, if applicable, the relevant tax Act.

apply for registration for one or more taxes in the prescribed form and manner ; and (c)")

40 Tax Administration Act Registration This person must: Requirements (a) apply for registration within the period provided for in a tax Act or, if no such period is provided for, 21 business days of so becoming obliged or within the further period as SARS may approve in the prescribed form and manner; (b) apply for registration for one or more taxes in the prescribed form and manner ; and (c) provide SARS with the further particulars and any documents as SARS may require for the purpose of registering the person for the tax or taxes.

proper identification of the person; or (b) counteracting identity theft or fraud.")

41 Registration Requirements Tax Administration Act A person registered or applying for registration under a tax Act may be required to submit biometric information in the prescribed form and manner if the information is required to ensure (a) proper identification of the person; or (b) counteracting identity theft or fraud.

42 Registration Requirements Tax Administration Act A person who applies for registration in terms of this Chapter and has not provided all particulars and documents required by SARS, may be regarded not to have applied for registration until all the particulars and documents have been provided to SARS. Where a taxpayer that is obliged to register with SARS under a tax Act fails to do so, SARS may register the taxpayer for one or more tax types as is appropriate under the circumstances.

exceeds the")

43 Requirements for Compulsory registration Who Qualifies? Any person who carries on a business and whose annual turnover (for any 12 month period) exceeds the compulsory threshold of R1 million is liable to register for VAT

44 Requirements for Voluntary registration Who Qualifies? A person carrying on any enterprise whose annual total value of taxable supplies made exceeded R A person carrying on any enterprise whose annual total value of taxable supplies to be made has not exceeded R50 000, but- Who is reasonably expected to exceed R within 12 months from the date of registration Must provide in addition to the information required in terms of Chapter 3 of the Tax Administration Act, the Commissioner with proof that any or more of the following circumstances applies:

45 Requirements for Voluntary registration Who Qualifies? Taxable supplies made for more than two months Proof that the average value of the taxable supplies made in the preceding months prior to the date of application of registration, exceeded R4200 per month For the purposes of determining the average of taxable supplies, use the value of taxable supplies made for a minimum of 2 and a maximum of 11 months immediately preceding the date of application

46 Requirements for Voluntary registration Who Qualifies? Taxable supplies made for one month: In the case where taxable supplies were made for one month preceding the date of application for registration, proof that the total value of taxable supplies made in that month has exceeded R4200

47 Requirements for Voluntary registration Who Qualifies? Written Contracts: In terms of a contractual obligation in writing, required to make taxable supplies in excess of R in the 12 months following the date of registration.

48 Requirements for Voluntary registration Who Qualifies? Finance Agreements: A copy of the relevant agreement where the person has entered into- A financial agreement with a bank registered in terms of the Banks Act A credit agreement with a credit provider as defined in the National Credit Act An agreement with a designated entity, public authority or any other person who continuously or regularly provides finance

49 Requirements for Voluntary registration Who Qualifies? Finance Agreements: A copy of the relevant agreement where the person has entered into- A financial agreement with a person that is not a resident of the republic where it is agreed that: the expenses incurred or to be incurred in the commencement or furtherance of the enterprise the total repayments in terms of the financial, credit or other agreement; will in the 12 months following the date of application for registration exceed R

50 Requirements for Voluntary registration Who Qualifies? Expenditure: Proof of: Expenditure incurred or to be incurred in connection with the commencement or furtherance of the enterprise, as set out in any written agreement entered into Capital goods acquired in connection with the commencement of the enterprise

51 Requirements for Voluntary registration Who Qualifies? Proof of payment or any extended payment agreement entered into in respect of expenditure incurred and capital goods acquired where applicable evidencing that payment in respect of the following items: As at the date of application for registration has exceeded R Will in any consecutive 12 months period commencing before and ending after the date of application for registration exceed R Will in the 12 months following the date of application for registration exceed R50 00

52 Tax Clearance To certify that a taxpayer complies with the rules prescribed in different tax laws All relevant returns should be submitted All payments must have been made or arrangements made for deferred payment via the SARS Collections Department Personal and Enterprise particulars have to be updated with SARS

Manually Verify Successful Yes Capture results on application Print SARS Employee TCC Database")

53 Tax Clearance: Procedure Capture results On application Manual feedback to taxpayer No Receive Application (Hard Copy) Manually Verify Successful Yes Capture results on application Print SARS Employee TCC Database

54 Tax clearance certificates General application valid for 12 months Can be revoked if there is noncompliance. Communication issued Not application specific If successful, cannot reapply within 11 months; can only reapply within two weeks prior to Tax Clearance expiring

55 Tax Clearance for a tender VAT registration may only be applied for in respect of a tender once the tender has been awarded

56 Recordkeeping It is advisable to open a separate bank account so that you do not mix private and business expenses You may choose a system of record keeping that is suited to the purpose and nature of your business Records must clearly reflect your income and expenditure

57 Recordkeeping The records should include: records showing assets, liabilities, various loans register of fixed assets sales slips, invoices, receipts, bank deposit slips records of credit purchases and sales statements of annual stocktaking supporting vouchers All source documents must be available for examination by SARS and must be kept for 5 years

Open: Monday, Tuesday,")

58 Thank you SARS Contact Centre SARS (7277) Visit your nearest SARS branch (to locate a branch visit Open: Monday, Tuesday, Thursday & Friday 08:00 to 16:00; Wednesday 09:00 to 16:00 Find us on Facebook

Individual Income Tax

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

TAX GUIDE FOR MICRO BUSINESSES 2011/12

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

As a small business are you finding it difficult to juggle your taxes?

As a small business are you finding it difficult to juggle your taxes? Introducing Turnover Tax The all-in-one tax that s simple and saves you time and money. Turn over to a new tax! Small businesses have

As a small business are you finding it difficult to juggle your taxes? Introducing Turnover Tax The all-in-one tax that s simple and saves you time and money. Turn over to a new tax! Small businesses have

Capital allowances and Leases

Capital allowances and Leases Content of the session Movable assets Immovable assets Leases 2 Movable assets Section 11(e) Write-off period, straight-line basis Only if no other allowance is available

Capital allowances and Leases Content of the session Movable assets Immovable assets Leases 2 Movable assets Section 11(e) Write-off period, straight-line basis Only if no other allowance is available

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

Budget Highlights 2018

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Tax Guide for Micro Businesses 2010/11. Turnover Tax. for Small Businesses. Tax Guide For Micro Businesses 2010/11 - Page 1

Tax Guide for Micro Businesses 2010/11 Turnover Tax for Small Businesses Tax Guide For Micro Businesses 2010/11 - Page 1 TT Comprehensive Guide.indd 1 TAX GUIDE FOR MICRO BUSINESSES 2010/11 The guide contains

Tax Guide for Micro Businesses 2010/11 Turnover Tax for Small Businesses Tax Guide For Micro Businesses 2010/11 - Page 1 TT Comprehensive Guide.indd 1 TAX GUIDE FOR MICRO BUSINESSES 2010/11 The guide contains

Budget Highlight 2017

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Learnership Allowance

Learnership Allowance Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Learnership Allowance Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

TCS (Tax Clearance Status) November 2018

November 2018") TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

Welcome to the SARS Tax Workshop

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

SARS Tax Guide 2014 / 2015

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2014/15. SARS Tax Guide 2014 / 2015 INCOME TAX: INDIVIDUALS AND TRUSTS

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2014/15. SARS Tax Guide 2014 / 2015 INCOME TAX: INDIVIDUALS AND TRUSTS

Points Of Discussion

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

TAX GUIDE FOR SMALL BUSINESSES 2013/14

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

Income Tax. Tax Guide for Small Businesses 2015/16

Income Tax Tax Guide for Small Businesses 2015/16 Preface Tax Guide for Small Businesses 2015/2016 This guide is a general guide dealing with the taxation of small businesses. This guide is not an official

Income Tax Tax Guide for Small Businesses 2015/16 Preface Tax Guide for Small Businesses 2015/2016 This guide is a general guide dealing with the taxation of small businesses. This guide is not an official

THE EMPLOYER S GUIDE TO PAY AS YOU EARN

THE EMPLOYER S GUIDE TO PAY AS YOU EARN Issued by, Taxpayers Services and Education Department July 2017 EMPLOYER S GUIDE TO P.A.Y.E CONTENTS PART I...1 1.0 PRELIMINARY INTERPRETATION...1 1.1 PURPOSE

THE EMPLOYER S GUIDE TO PAY AS YOU EARN Issued by, Taxpayers Services and Education Department July 2017 EMPLOYER S GUIDE TO P.A.Y.E CONTENTS PART I...1 1.0 PRELIMINARY INTERPRETATION...1 1.1 PURPOSE

Change, the new certainty

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

A person that elected to be registered as above must be registered by the Commissioner with effect from the beginning of that year of assessment.

6.1 WHO QUALIFIES TO REGISTER FOR TURNOVER TAX? A person that qualifies as a micro business may register for TT, if it is a: Natural person (or the deceased or insolvent estate of a natural person is registered

6.1 WHO QUALIFIES TO REGISTER FOR TURNOVER TAX? A person that qualifies as a micro business may register for TT, if it is a: Natural person (or the deceased or insolvent estate of a natural person is registered

Paper F6 (ZAF) Taxation (South Africa) Thursday 8 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (South Africa) Thursday 8 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (South Africa) Thursday 8 December 2016 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are compulsory

Fundamentals Level Skills Module Taxation (South Africa) Thursday 8 December 2016 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are compulsory

INCOME TAX: INDIVIDUALS AND TRUSTS

The SARS Tax Guide: A synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax rates (year of assessment ending 29 February 2016) Individuals

The SARS Tax Guide: A synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax rates (year of assessment ending 29 February 2016) Individuals

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16.

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

companies from 33% to 28%. This booklet is published by FHPKF Publishers (Pty) Ltd for and on behalf of chartered accountants & business advisers

Ltd for and on behalf of chartered accountants & business advisers") BUDGET PROPOSALS 1 Dividends Tax A dividend withholding tax will replace STC from 1 April 2012 at a rate of 15%. 2 Capital Gains Tax As from 1 March 2012, the inclusion rate for individuals and special

BUDGET PROPOSALS 1 Dividends Tax A dividend withholding tax will replace STC from 1 April 2012 at a rate of 15%. 2 Capital Gains Tax As from 1 March 2012, the inclusion rate for individuals and special

INCOME TAX WORKSHOP Taxation of Individuals Presenter: Francis Kamau

INCOME TAX WORKSHOP Taxation of Individuals Friday, 7 th April 2017 Presenter: Francis Kamau Employee taxes Chargeable income For the purposes of section 3(2)(a)(ii), an amount paid to- a person who is,

INCOME TAX WORKSHOP Taxation of Individuals Friday, 7 th April 2017 Presenter: Francis Kamau Employee taxes Chargeable income For the purposes of section 3(2)(a)(ii), an amount paid to- a person who is,

An automated tax clearance system will be implemented this year. 4 Employment Incentive

BUDGET PROPOSALS 1 Retirement Savings Reforms An employer s contribution to retirement funds on behalf of an employee will be treated as a taxable fringe benefit in the hands of the employee. Individuals

BUDGET PROPOSALS 1 Retirement Savings Reforms An employer s contribution to retirement funds on behalf of an employee will be treated as a taxable fringe benefit in the hands of the employee. Individuals

BUDGET 2019 TAX GUIDE

BUDGET 2019 TAX GUIDE 1 This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2019/20. INCOME TAX: INDIVIDUALS AND TRUSTS

BUDGET 2019 TAX GUIDE 1 This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2019/20. INCOME TAX: INDIVIDUALS AND TRUSTS

TAX PROFESSIONAL OCCUPATIONAL CERTIFICATE: Initial Test of Competency RPL Assessment SAQA ID: July Paper 1: Questions 1 and 2 SOLUTIONS

OCCUPATIONAL CERTIFICATE: TAX PROFESSIONAL SAQA ID: 93624 Initial Test of Competency RPL Assessment July 207 Paper : Questions and 2 SOLUTIONS CANDIDATE NUMBER Instructions to Candidates. This competency

OCCUPATIONAL CERTIFICATE: TAX PROFESSIONAL SAQA ID: 93624 Initial Test of Competency RPL Assessment July 207 Paper : Questions and 2 SOLUTIONS CANDIDATE NUMBER Instructions to Candidates. This competency

Paper P6 (ZAF) Advanced Taxation (South Africa) Monday 6 December Professional Level Options Module

Advanced Taxation (South Africa) Monday 6 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Monday 6 December 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section

Professional Level Options Module Advanced Taxation (South Africa) Monday 6 December 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section

Paper P6 (ZAF) Advanced Taxation (South Africa) Thursday 10 December Professional Level Options Module

Advanced Taxation (South Africa) Thursday 10 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Thursday 10 December 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This question paper is divided into two sections:

Professional Level Options Module Advanced Taxation (South Africa) Thursday 10 December 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This question paper is divided into two sections:

Fundamentals Level Skills Module, Paper F6 (CZE)

") Answers Fundamentals Level Skills Module, Paper F6 (CZE) Taxation (Czech) Material, a.s. June 205 Answers and Marking Scheme (a) 204 corporate income tax liability Accounting revenues Sales of goods and

Answers Fundamentals Level Skills Module, Paper F6 (CZE) Taxation (Czech) Material, a.s. June 205 Answers and Marking Scheme (a) 204 corporate income tax liability Accounting revenues Sales of goods and

This booklet is published by PKF Publishers (Pty) Ltd for and on behalf of. chartered accountants & business advisers

Ltd for and on behalf of. chartered accountants & business advisers") BUDGET PROPOSALS 1 Tax-Preferred Savings Accounts Tax-preferred savings accounts, as a measure to encourage household savings, will proceed. These accounts will have an initial annual contribution limit

BUDGET PROPOSALS 1 Tax-Preferred Savings Accounts Tax-preferred savings accounts, as a measure to encourage household savings, will proceed. These accounts will have an initial annual contribution limit

International Tax Lithuania Highlights 2017

International Tax Lithuania Highlights 2017 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements IAS and IFRS, or Business Accounting Standards

International Tax Lithuania Highlights 2017 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements IAS and IFRS, or Business Accounting Standards

Leasing taxation Estonia

2012 KPMG Baltics OÜ, an Estonian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

2012 KPMG Baltics OÜ, an Estonian limited liability company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

South African Income Tax Guide for 2013/2014

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state.

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

Tax Guide For Minnesota Businesses

Tax Guide For Minnesota Businesses 2017-2018 TAX GUIDE FOR MINNESOTA BUSINESSES Olsen Thielen & Co., Ltd. Certified Public Accountants & Consultants 2675 Long Lake Road 300 Prairie Center Drive #300 Roseville,

Tax Guide For Minnesota Businesses 2017-2018 TAX GUIDE FOR MINNESOTA BUSINESSES Olsen Thielen & Co., Ltd. Certified Public Accountants & Consultants 2675 Long Lake Road 300 Prairie Center Drive #300 Roseville,

Points of Discussion

Provisional Tax Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

Provisional Tax Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

TAX GUIDE FOR SMALL BUSINESSES 2009/10

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2009/10 Another helpful guide brought to you by the South African Revenue Service TAX GUIDE FOR SMALL BUSINESSES 2009/10 This document is a

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2009/10 Another helpful guide brought to you by the South African Revenue Service TAX GUIDE FOR SMALL BUSINESSES 2009/10 This document is a

EDUC Mortgages. Sean Couch

EDUC Mortgages Sean Couch Mortgages Just because you have a mortgage This does not mean you will receive a new mortgage, even if it is for the same or less than the current mortgage. New Central Bank Rules

EDUC Mortgages Sean Couch Mortgages Just because you have a mortgage This does not mean you will receive a new mortgage, even if it is for the same or less than the current mortgage. New Central Bank Rules

2017 Tax Issues for Small Businesses Seminar

2017 Tax Issues for Small Businesses Seminar Presented by Piet Nel CA(SA) Piet is the Head of the School of Applied Tax at the Tax Faculty. He formerly lectured in taxation at UNISA and the University

2017 Tax Issues for Small Businesses Seminar Presented by Piet Nel CA(SA) Piet is the Head of the School of Applied Tax at the Tax Faculty. He formerly lectured in taxation at UNISA and the University

TAXFAX 2009/

TAXFAX 2009/2010 www.blickrothenberg.com Table of contents Allowances and Reliefs 2 Individuals - Income Tax Rates 2 National Insurance Contributions 3 Capital Gains Tax 4 Inheritance Tax 5 Trusts - Income

TAXFAX 2009/2010 www.blickrothenberg.com Table of contents Allowances and Reliefs 2 Individuals - Income Tax Rates 2 National Insurance Contributions 3 Capital Gains Tax 4 Inheritance Tax 5 Trusts - Income

VAT 419. Value-Added Tax. Guide for Municipalities /02/25 SP C V

VAT 419 Value-Added Tax Guide for Municipalities www.sars.gov.za 2009/02/25 SP C V2.000 1 VAT 419 Guide for Municipalities Foreword FOREWORD This guide is a general guide concerning the application of

VAT 419 Value-Added Tax Guide for Municipalities www.sars.gov.za 2009/02/25 SP C V2.000 1 VAT 419 Guide for Municipalities Foreword FOREWORD This guide is a general guide concerning the application of

DECEASED ESTATES REGISTRATION & ASSESSMENT

DECEASED ESTATES REGISTRATION & ASSESSMENT Agenda Introduction Position - deaths prior to 1 March 2016 Position - deaths post 1 March 2016 Registration process for Deceased Person Registration process

DECEASED ESTATES REGISTRATION & ASSESSMENT Agenda Introduction Position - deaths prior to 1 March 2016 Position - deaths post 1 March 2016 Registration process for Deceased Person Registration process

Type Jurisdiction Balance Payable Due Return/Form due

Deadlines Corporate Type Jurisdiction Balance Payable Due Return/Form due Income tax Federal return Instalments Federal T4 / T5 information slips NR4 information slips Generally, 2 months after end (i.e.

Deadlines Corporate Type Jurisdiction Balance Payable Due Return/Form due Income tax Federal return Instalments Federal T4 / T5 information slips NR4 information slips Generally, 2 months after end (i.e.

Tax tables 2019/2020 (year of assessment ending 29 February 2020)

") BUDGET SPEECH 2019/2020 ALL YOU NEED TO KNOW Tax tables 2019/2020 (year of assessment ending 29 February 2020) Income tax: Individuals and special trusts Taxable income Rates of tax 0-195 850 18 % of taxable

BUDGET SPEECH 2019/2020 ALL YOU NEED TO KNOW Tax tables 2019/2020 (year of assessment ending 29 February 2020) Income tax: Individuals and special trusts Taxable income Rates of tax 0-195 850 18 % of taxable

Paper F6 (ZAF) Taxation (South Africa) Tuesday 4 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (South Africa) Tuesday 4 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (South Africa) Tuesday 4 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Fundamentals Level Skills Module Taxation (South Africa) Tuesday 4 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Savings Plus Program 457 Deferred Compensation Plan Unforeseeable Emergency Withdrawal Form

Savings Plus Program 457 Deferred Compensation Plan Unforeseeable Emergency Withdrawal Form Please read the instructions and information on pages 3 and 4 before completing this form. SECTION I Participant

Savings Plus Program 457 Deferred Compensation Plan Unforeseeable Emergency Withdrawal Form Please read the instructions and information on pages 3 and 4 before completing this form. SECTION I Participant

Forms of Corporate Structure i

Forms of Corporate Structure i One of the first decisions that you will have to make as a business owner is how the company should be structured. Krishnan Company, P.C., CPA, can help you select the form

Forms of Corporate Structure i One of the first decisions that you will have to make as a business owner is how the company should be structured. Krishnan Company, P.C., CPA, can help you select the form

2017 Basic tax information in Malaysia

2017 Basic tax information in Malaysia INCOME TAX Direct taxation in Malaysia is based on the unitary system and the basis of taxation is territorial in nature. ly income that is accrued or derived from

2017 Basic tax information in Malaysia INCOME TAX Direct taxation in Malaysia is based on the unitary system and the basis of taxation is territorial in nature. ly income that is accrued or derived from

ASQ Basic tax information in Malaysia

ASQ 2016 Basic tax information in Malaysia INCOME TAX Direct taxation in Malaysia is based on the unitary system and the basis of taxation is territorial in nature. Only income that is accrued or derived

ASQ 2016 Basic tax information in Malaysia INCOME TAX Direct taxation in Malaysia is based on the unitary system and the basis of taxation is territorial in nature. Only income that is accrued or derived

Guide to the VAT mini One Stop Shop

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT Brussels, 23 October 2013 Guide to the VAT mini One Stop Shop (REV 1 applicable from 1 January

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT Brussels, 23 October 2013 Guide to the VAT mini One Stop Shop (REV 1 applicable from 1 January

Professional Level Options Module, Paper P6 (ZAF)

") Answers Professional Level Options Module, Paper P6 (ZAF) Advanced Taxation (South Africa) June 2011 Answers Note: The ACCA does not require candidates to quote section numbers or other statutory or case

Answers Professional Level Options Module, Paper P6 (ZAF) Advanced Taxation (South Africa) June 2011 Answers Note: The ACCA does not require candidates to quote section numbers or other statutory or case

INTRODUCTION. Situations should be viewed separately based on specific facts of each scenario.

TAX FACTS 2018 CONTENTS INTRODUCTION... 3 PERSONAL INCOME TAX... 4 CORPORATION TAX... 8 SOCIAL INSURANCE... 12 SPECIAL CONTRIBUTION FOR DEFENCE... 13 INTELLECTUAL PROPERTY... 16 VALUE ADDED TAX... 18 CAPITAL

TAX FACTS 2018 CONTENTS INTRODUCTION... 3 PERSONAL INCOME TAX... 4 CORPORATION TAX... 8 SOCIAL INSURANCE... 12 SPECIAL CONTRIBUTION FOR DEFENCE... 13 INTELLECTUAL PROPERTY... 16 VALUE ADDED TAX... 18 CAPITAL

Business tax highlights

Legislative Update Tax Cuts and Jobs Act Business tax highlights Table of contents Overview...1 C corporation changes... 2 Pass-through entity deduction... 3 Executive compensation... 7 Planning opportunities..

Legislative Update Tax Cuts and Jobs Act Business tax highlights Table of contents Overview...1 C corporation changes... 2 Pass-through entity deduction... 3 Executive compensation... 7 Planning opportunities..

Professional Level Options Module, Paper P6 (ZAF)

") Answers Professional Level Options Module, Paper P6 (ZAF) Advanced Taxation (South Africa) December 2016 Answers Note: ACCA does not require candidates to quote section numbers or other statutory or case

Answers Professional Level Options Module, Paper P6 (ZAF) Advanced Taxation (South Africa) December 2016 Answers Note: ACCA does not require candidates to quote section numbers or other statutory or case

Quick Tax Guide 2013/14 Simplicity from complexity

Quick Tax Guide 2013/14 Simplicity from complexity Income Tax for Individuals Tax rates and rebates Individuals, Estates & Special Trusts 1 (Year ending 28 February 2014) Taxable income as exceeds But

Quick Tax Guide 2013/14 Simplicity from complexity Income Tax for Individuals Tax rates and rebates Individuals, Estates & Special Trusts 1 (Year ending 28 February 2014) Taxable income as exceeds But

Occupational Certificate: Tax Professional

Occupational Certificate: Tax Professional External Integrated Summative Assessment (EISA) Personal Taxation Question EXEMPLAR Part A Aspect of the answer Details of aspects to be included in answer Comp

Occupational Certificate: Tax Professional External Integrated Summative Assessment (EISA) Personal Taxation Question EXEMPLAR Part A Aspect of the answer Details of aspects to be included in answer Comp

CASE STUDIES In draft format must still be made pretty

MCQ s 1. d 2. c 3. b 4. a 5. c 6. d 7. a 8. b 9. d 10. b 11. c 12. d 13. b 14. d 15. c 16. b 17. c 18. d 19. c 20. a 21. b 22. a 23. b 24. b 25. c 26. b 27. a 28. c 29. d 30. c 31. c 32. d 33. c 34. a

MCQ s 1. d 2. c 3. b 4. a 5. c 6. d 7. a 8. b 9. d 10. b 11. c 12. d 13. b 14. d 15. c 16. b 17. c 18. d 19. c 20. a 21. b 22. a 23. b 24. b 25. c 26. b 27. a 28. c 29. d 30. c 31. c 32. d 33. c 34. a

Financial Leadership through Professional Excellence 2017/2018 TAX CARD. Telephone + 27 (0) Facsimile + 27 (0)

Facsimile + 27 (0)") Financial Leadership through Professional Excellence 2017/2018 TAX CAD Telephone + 27 (0) 21 683 4834 Facsimile + 27 (0) 86 541 2872 www.mdacc.co.za mdacc@mdacc.co.za MD House Greenford Office Estate Off

Financial Leadership through Professional Excellence 2017/2018 TAX CAD Telephone + 27 (0) 21 683 4834 Facsimile + 27 (0) 86 541 2872 www.mdacc.co.za mdacc@mdacc.co.za MD House Greenford Office Estate Off

2016/2017 TAX CARD. Financial Leadership through Professional Excellence. Telephone + 27 (0) Facsimile + 27 (0)

Facsimile + 27 (0)") Financial Leadership through Professional Excellence 2016/2017 TAX CAD Telephone + 27 (0) 21 683 4834 Facsimile + 27 (0) 86 541 2872 www.mdacc.co.za mdacc@mdacc.co.za MD House Greenford Office Estate Off

Financial Leadership through Professional Excellence 2016/2017 TAX CAD Telephone + 27 (0) 21 683 4834 Facsimile + 27 (0) 86 541 2872 www.mdacc.co.za mdacc@mdacc.co.za MD House Greenford Office Estate Off

International Tax South Africa Highlights 2018

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

International Tax Indonesia Highlights 2018

International Tax Indonesia Highlights 2018 Investment basics: Currency Indonesian Rupiah (IDR) Foreign exchange control The rupiah is freely convertible. However, approval of Bank Indonesia (the central

International Tax Indonesia Highlights 2018 Investment basics: Currency Indonesian Rupiah (IDR) Foreign exchange control The rupiah is freely convertible. However, approval of Bank Indonesia (the central

IN RESPECT OF FRINGE BENEFITS

GUIDE FOR EMPLOYERS IN RESPECT OF (2016 TAX YEAR) 1 PURPOSE 3 2 SCOPE 3 3 OBLIGATIONS OF THE EMPLOYER 3 4 BENEFITS GRANTED TO RELATIVES OF EMPLOYEES AND OTHERS 4 5 TAXABLE BENEFITS 4 5.1 ACQUISITION OF

GUIDE FOR EMPLOYERS IN RESPECT OF (2016 TAX YEAR) 1 PURPOSE 3 2 SCOPE 3 3 OBLIGATIONS OF THE EMPLOYER 3 4 BENEFITS GRANTED TO RELATIVES OF EMPLOYEES AND OTHERS 4 5 TAXABLE BENEFITS 4 5.1 ACQUISITION OF

Non-Profit Organizations

Non-Profit Organizations and Taxation revenu.gouv.qc.ca This publication is available on our website. This publication is provided for information purposes only. It does not constitute a legal interpretation

Non-Profit Organizations and Taxation revenu.gouv.qc.ca This publication is available on our website. This publication is provided for information purposes only. It does not constitute a legal interpretation

Acc. 433, Chapter Outline for use with Prentice Hall's Federal Taxation Corporations Richard B. Malamud, last updates, in part, November, 2011

Acc. 433, Chapter Outline for use with Prentice Hall's Federal Taxation Corporations Richard B. Malamud, last updates, in part, November, 2011 1) Chapter 1 was not assigned! 2) Formation and Capital Structure

Acc. 433, Chapter Outline for use with Prentice Hall's Federal Taxation Corporations Richard B. Malamud, last updates, in part, November, 2011 1) Chapter 1 was not assigned! 2) Formation and Capital Structure

COLLEGE SAVINGS PLAN (MONTANA)

") COLLEGE SAVINGS PLAN (MONTANA) PLAN DESCRIPTION HANDBOOK The Pacific Life Funds 529 Plan (MT) was created under the Montana Family Education Savings Program (Program).To implement the Program, the state

COLLEGE SAVINGS PLAN (MONTANA) PLAN DESCRIPTION HANDBOOK The Pacific Life Funds 529 Plan (MT) was created under the Montana Family Education Savings Program (Program).To implement the Program, the state

Company Establishment. 1. Forming a Company. Procedures for Establishing a Company. 1. Procedures for Establishing a Company. 1.1 Company Registration

Company Establishment 1. Forming a Company Procedures for Establishing a Company 1. Procedures for Establishing a Company 1.1 Company Registration 1.1.1 Promoters Company promoters are responsible for

Company Establishment 1. Forming a Company Procedures for Establishing a Company 1. Procedures for Establishing a Company 1.1 Company Registration 1.1.1 Promoters Company promoters are responsible for

Paper P6 (ZAF) Advanced Taxation (South Africa) Thursday 7 December Professional Level Options Module

Advanced Taxation (South Africa) Thursday 7 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Thursday 7 December 2017 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

Professional Level Options Module Advanced Taxation (South Africa) Thursday 7 December 2017 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

TAX GUIDE FOR SMALL BUSINESSES 2011/12

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR SMALL BUSINESSES 2011/12 This document

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR SMALL BUSINESSES 2011/12 This document

2. ACCESSIBILITY OF THE PRESENT GENERAL TERMS AND CONDITIONS AND INFORMATION OF THE ORGANIZER

GENERAL TERMS AND CONDITIONS FOR YOUR PARTICIPATION IN THE PROMOTION 1. ORGANIZER OF THE PROMOTION ORGANIZED BY TAVEX EOOD The present Promotion ("Promotion") is organized and conducted by Tavex EOOD,

GENERAL TERMS AND CONDITIONS FOR YOUR PARTICIPATION IN THE PROMOTION 1. ORGANIZER OF THE PROMOTION ORGANIZED BY TAVEX EOOD The present Promotion ("Promotion") is organized and conducted by Tavex EOOD,

ATX ZAF. Advanced Taxation South Africa (ATX ZAF) Strategic Professional Options. Tuesday 4 December 2018

Strategic Professional Options. Tuesday 4 December 2018") Strategic Professional Options Advanced Taxation South Africa (ATX ZAF) Tuesday 4 December 2018 ATX ZAF ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A

Strategic Professional Options Advanced Taxation South Africa (ATX ZAF) Tuesday 4 December 2018 ATX ZAF ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A

Time allowed Tax rates and allowances are on pages 2 5.

Fundamentals Level Skills Module Taxation (Czech) Tuesday 2 June 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates and

Fundamentals Level Skills Module Taxation (Czech) Tuesday 2 June 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates and

PROCLAMATION NO. /2016 TAX ADMINISTRATION PROCLAMATION

PROCLAMATION NO. /2016 TAX ADMINISTRATION PROCLAMATION WHERAS, it is necessary to enact a separate tax administration proclamation governing the administration of domestic taxes with a view to render the

PROCLAMATION NO. /2016 TAX ADMINISTRATION PROCLAMATION WHERAS, it is necessary to enact a separate tax administration proclamation governing the administration of domestic taxes with a view to render the

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

An Act to make provision for the law relating to Value Added Tax. CHAPTER I PRELIMINARY

An Act to make provision for the law relating to Value Added Tax. Enacted by the Parliament of Lesotho Short Title CHAPTER I PRELIMINARY 1. This Act may be cited as the Value Added Tax Act, 2001. Commencement

An Act to make provision for the law relating to Value Added Tax. Enacted by the Parliament of Lesotho Short Title CHAPTER I PRELIMINARY 1. This Act may be cited as the Value Added Tax Act, 2001. Commencement

TAX GUIDE FOR SMALL BUSINESSES 2008/09

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2008/09 Another helpful guide brought to you by the South African Revenue Service TAX GUIDE FOR SMALL BUSINESSES 2008/09 This document is a

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2008/09 Another helpful guide brought to you by the South African Revenue Service TAX GUIDE FOR SMALL BUSINESSES 2008/09 This document is a

Employment Tax Incentive Scheme

Employment Tax Incentive Scheme Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Employment Tax Incentive Scheme Introduction Many young South Africans are excluded from economic activity, and as a result suffer unduly from unemployment, discouragement and economic marginalisation.

Professional Level Options Module, Paper P6 (CYP) 1 Capoda Ltd

1 Capoda Ltd") Answers Professional Level Options Module, Paper P6 (CYP) Advanced Taxation (Cyprus) June 2013 Answers 1 Capoda Ltd (a) To: Laurence, MD Capoda Ltd From: Nicos, Tax Advisor Date: 16 January 2012 Re: Presentation

Answers Professional Level Options Module, Paper P6 (CYP) Advanced Taxation (Cyprus) June 2013 Answers 1 Capoda Ltd (a) To: Laurence, MD Capoda Ltd From: Nicos, Tax Advisor Date: 16 January 2012 Re: Presentation

Mega Cash or Today Show Block Of Cash promotion conducted by the Promoter in the previous 12 months are also ineligible to enter.

TODAY SHOW S MEGA CASH-A-ROO PROMOTION TERMS AND CONDITIONS PARTICIPATION 1. Information on how to enter and the prize(s) form part of these Terms and Conditions. Participation in this promotion is deemed

TODAY SHOW S MEGA CASH-A-ROO PROMOTION TERMS AND CONDITIONS PARTICIPATION 1. Information on how to enter and the prize(s) form part of these Terms and Conditions. Participation in this promotion is deemed

TODAY SHOW S MEGA CASH GIVEAWAY PROMOTION

TODAY SHOW S MEGA CASH GIVEAWAY PROMOTION TERMS AND CONDITIONS PARTICIPATION 1. Information on how to enter and the prize(s) form part of these Terms and Conditions. Participation in this promotion is

TODAY SHOW S MEGA CASH GIVEAWAY PROMOTION TERMS AND CONDITIONS PARTICIPATION 1. Information on how to enter and the prize(s) form part of these Terms and Conditions. Participation in this promotion is

TODAY SHOW S MEGA CASH GIVEAWAY PROMOTION

TODAY SHOW S MEGA CASH GIVEAWAY PROMOTION TERMS AND CONDITIONS PARTICIPATION 1. Information on how to enter and the prize(s) form part of these Terms and Conditions. Participation in this promotion is

TODAY SHOW S MEGA CASH GIVEAWAY PROMOTION TERMS AND CONDITIONS PARTICIPATION 1. Information on how to enter and the prize(s) form part of these Terms and Conditions. Participation in this promotion is

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

OFFSHORE TERMS AND CONDITIONS EFFECTIVE 7 NOVEMBER 2017 VERSION 11

OFFSHORE TERMS AND CONDITIONS EFFECTIVE 7 NOVEMBER 2017 VERSION 11 CONTENTS Definitions 1 Which legal entities are party to this agreement? 2 Which documents form part of the agreement? 2 Who may not invest

OFFSHORE TERMS AND CONDITIONS EFFECTIVE 7 NOVEMBER 2017 VERSION 11 CONTENTS Definitions 1 Which legal entities are party to this agreement? 2 Which documents form part of the agreement? 2 Who may not invest

Source Codes. New Source Codes and Validations

Source Codes New Source Codes and Validations Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make

Source Codes New Source Codes and Validations Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make

Tax Considerations in Choosing the Form of Organization for a New Business

Tax Considerations in Choosing the Form of Organization for a New Business By Charles A. Wry, Jr. mbbp.com @MorseBarnes Boston, MA Cambridge, MA Waltham, MA mbbp.com CityPoint 230 Third Avenue, 4th Floor

Tax Considerations in Choosing the Form of Organization for a New Business By Charles A. Wry, Jr. mbbp.com @MorseBarnes Boston, MA Cambridge, MA Waltham, MA mbbp.com CityPoint 230 Third Avenue, 4th Floor

Mega Cash or Today Show Block Of Cash promotion conducted by the Promoter in the previous 12 months are also ineligible to enter.

TODAY SHOW S MEGA CASH-A-ROO PROMOTION TERMS AND CONDITIONS PARTICIPATION 1. Information on how to enter and the prize(s) form part of these Terms and Conditions. Participation in this promotion is deemed

TODAY SHOW S MEGA CASH-A-ROO PROMOTION TERMS AND CONDITIONS PARTICIPATION 1. Information on how to enter and the prize(s) form part of these Terms and Conditions. Participation in this promotion is deemed

Published on Taxation and customs union (https://ec.europa.eu/taxation_customs/business/vat/telecommunications-broadcasting-electronic-services)

") Published on Taxation and customs union (https://ec.europa.eu/taxation_customs/business/vat/telecommunications-broadcasting-electronic-services) Slovenia-2018-03-28 Groups audience: Slovenia [1] Validity

Published on Taxation and customs union (https://ec.europa.eu/taxation_customs/business/vat/telecommunications-broadcasting-electronic-services) Slovenia-2018-03-28 Groups audience: Slovenia [1] Validity

Global Mobility Services: Taxation of International Assignees - Malawi

www.pwc.com/mw/en Global Mobility Services: Taxation of International Assignees - Malawi Taxation issues & related matters for employers & employees 2017/18 Last Updated: June 2018 This document was not

www.pwc.com/mw/en Global Mobility Services: Taxation of International Assignees - Malawi Taxation issues & related matters for employers & employees 2017/18 Last Updated: June 2018 This document was not

Chapter 23. General Provisions. Article 169. Concept of value added tax. Chapter 24. Taxpayers. Article 170. Taxpayers

DIVISION VII. VALUE-ADDED TAX Chapter 23. General Provisions Article 169. Concept of value added tax The value added tax, hereinafter VAT, is a form of collection to the budget of a portion of the value

DIVISION VII. VALUE-ADDED TAX Chapter 23. General Provisions Article 169. Concept of value added tax The value added tax, hereinafter VAT, is a form of collection to the budget of a portion of the value

Paper P6 (ZAF) Advanced Taxation (South Africa) Monday 7 June Professional Level Options Module

Advanced Taxation (South Africa) Monday 7 June Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Monday 7 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (South Africa) Monday 7 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

ALBANIA TAX CARD 2017

ALBANIA TAX CARD 2017 TAX CARD 2017 ALBANIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Rates 1.1.2 Taxable Income 1.1.3 Exempt Income 1.1.4 Deductible Expenses 1.2 Social Security

ALBANIA TAX CARD 2017 TAX CARD 2017 ALBANIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Rates 1.1.2 Taxable Income 1.1.3 Exempt Income 1.1.4 Deductible Expenses 1.2 Social Security

The Start-up Brief. This FAQ sheet specifically sets out to answer the following questions:

The Start-up Brief Tax Issues This FAQ sheet forms part of a series prepared by postgraduate students from the University of Manchester s School of Law, in conjunction with the Legal Advice Centre. They

The Start-up Brief Tax Issues This FAQ sheet forms part of a series prepared by postgraduate students from the University of Manchester s School of Law, in conjunction with the Legal Advice Centre. They

Disposals of business or farm on "retirement"

Disposals of business or farm on "retirement" Part 19-06-03 This document should be read in conjunction with section 598 of the Taxes Consolidation Act 1997 Document updated May 2018 Table of Contents

Disposals of business or farm on "retirement" Part 19-06-03 This document should be read in conjunction with section 598 of the Taxes Consolidation Act 1997 Document updated May 2018 Table of Contents

Welcome to the SARS Tax Workshop IT14 SD

Welcome to the SARS Tax Workshop IT14 SD The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more

Welcome to the SARS Tax Workshop IT14 SD The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more

Tax Facts BRINGING TAX INTO FOCUS RATES AND ALLOWANCES GUIDE 2018 /

Tax Facts RATES AND ALLOWANCES GUIDE 2018 / 2019 BRINGING TAX INTO FOCUS www.hazlewoods.co.uk CONTENTS PERSONAL TAX Page Income tax rates and allowances 1 Timetable for self-assessment 3 Pensions 3 Capital

Tax Facts RATES AND ALLOWANCES GUIDE 2018 / 2019 BRINGING TAX INTO FOCUS www.hazlewoods.co.uk CONTENTS PERSONAL TAX Page Income tax rates and allowances 1 Timetable for self-assessment 3 Pensions 3 Capital

International Tax Slovenia Highlights 2018

International Tax Slovenia Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Bank accounts may be held and repatriation payments made in any currency. Accounting principles/financial

International Tax Slovenia Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Bank accounts may be held and repatriation payments made in any currency. Accounting principles/financial

No transactions Corporation tax payable (Schedule A) 3,000 6,250 9,250 SDC payable (Schedule D) ,781 5,894 10,633

3,000 6,250 9,250 SDC payable (Schedule D) ,781 5,894 10,633") Answers Professional Level Options Module, Paper P6 (CYP) Advanced Taxation (Cyprus) June 218 Answers 1 (a) MEMORANDUM Alfa Farm Ltd Tax implications of the sale of the existing used tractor and purchase

Answers Professional Level Options Module, Paper P6 (CYP) Advanced Taxation (Cyprus) June 218 Answers 1 (a) MEMORANDUM Alfa Farm Ltd Tax implications of the sale of the existing used tractor and purchase

Paper F6 (HKG) Taxation (Hong Kong) Thursday 9 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Hong Kong) Thursday 9 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Hong Kong) Thursday 9 June 2016 Time allowed Reading and planning: 15 minutes Writing: 3 hours This question paper is divided into two sections: Section A ALL

Fundamentals Level Skills Module Taxation (Hong Kong) Thursday 9 June 2016 Time allowed Reading and planning: 15 minutes Writing: 3 hours This question paper is divided into two sections: Section A ALL

South Africa: VAT essentials

South Africa: VAT essentials Essential information regarding VAT as it applies in South Africa. Scope and Rates Registration VAT grouping Returns VAT recovery International Supplies of Goods and Services

South Africa: VAT essentials Essential information regarding VAT as it applies in South Africa. Scope and Rates Registration VAT grouping Returns VAT recovery International Supplies of Goods and Services

Marius Botha Presenter: Marius Botha CFP Topic: PCE Exam Training February 2018 Session 1

Marius Botha mbotha@iafrica.com Presenter: Marius Botha CFP Topic: PCE Exam Training February 2018 Session 1 Discussion Old Exam Paper Slide 2 Old papers Original dates and question numbers retained but

Marius Botha mbotha@iafrica.com Presenter: Marius Botha CFP Topic: PCE Exam Training February 2018 Session 1 Discussion Old Exam Paper Slide 2 Old papers Original dates and question numbers retained but

Overview of the Tax Structure

Overview of the Tax Structure 2007, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://www.cch.com 1 of 35 3 of 35 Responsibilities of Taxpayers Prepare appropriate tax forms and schedules

Overview of the Tax Structure 2007, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://www.cch.com 1 of 35 3 of 35 Responsibilities of Taxpayers Prepare appropriate tax forms and schedules