TABLE OF CONTENTS SECTION I FARM PROBLEMS & EXAMPLES. Installment Contracts and Deferred Grain Contracts

|

|

|

- James Pierce

- 5 years ago

- Views:

Transcription

1 TABLE OF CONTENTS SECTION I FARM PROBLEMS & EXAMPLES Page Installment Contracts and Deferred Grain Contracts Example of Reporting an Installment Sale (Example-Forms) Example of Taxpayer s Home On the Farm (Example-Forms) Example of Taxpayer s Home on the Farm/Machine Shed Converted to Personal Use (Example-Forms) Miscellaneous Leasing Issues Environmental clean-up costs Disaster payments & crop insurance, IRC 451(d) year deferral of weather related sale of other livestock, IRC 451(e) year deferral weather related sale of draft, dairy & breeding livestock, IRC 1033(e) Comparison of 1-year and 4-year deferral rules Employment Taxes on Farm Wages Self-Employment Tax Issues Re: Livestock Confinement Bldg Farm Income Averaging (Example-Forms) CCC loans, tax treatment Ag Law Digest (Vol. 21, No. 9) Implications of Death of a Farmer for CCC Loan Purposes CRP payments Patronage Dividends, tax treatment Wetlands Reserve Program Waterway Improvements on Cash Rental Property Qualified Conservation Contributions Hedging vs. Speculation Transaction Guide for Hedging Transactions Disaster Area Designation Iowa (2015) Prepaid Expense Rules Cash Basis Farmers Grouping Farm Activities Single Economic Units Grouping Election - Rental of Farm Real Estate Social Securities Earnings Test/Benefits Corporate Cash Rent Considerations Spousal Farm Rental Arrangements Considerations

2 TABLE OF CONTENTS SECTION I FARM PROBLEMS & EXAMPLES Page Residence Rental to Farm Corporation Tax Planning for the Young And/Or Low-Income Farmer/Non-farmer Agricultural Commodity Tax Planning: Charitable Gifts Gifts to Family Members Made in Kind Ag Law Digest (Vol. 23, No. 2) Depreciating Farm Drainage Tile Depreciation/Amortization (Residual Soil Fertility)- Letter Employment Agreement Form Spousal Employment - Documentation Payment in Kind Schedule Commodity Transfer Agreement IRS Coordinated Issue Papers Discharge of Indebtedness Income Computation/Taxation Discharge of Indebtedness IRC Other Issues Bankruptcy Split Year Election Chapter 7 or Chapter 11 Only Abandonment Entrapment Theory vs. Deflection Theory Ag Law Digest (Vol. 21, No. 12) Electing to Close the Tax Year in Bankruptcy Ag Law Digest (Vol. 21, No. 2) Traps in Abandonment of Property in Bankruptcy Ag Law Digest (Vol. 23, No. 11) The U.S. Supreme Court Settles (for Now) One of the Chapter 12 Bankruptcy Tax Issues... 97

3 INSTALLMENT CONTRACTS & DEFERRED GRAIN CONTRACTS The installment sale method of reporting deferred payments permits cash method farmers to defer the sale of crops or livestock. IRC 453(1)(2)(A) will permit installment sale reporting where deferred payments are received in a later year. The taxpayer may also elect out of installment sale reporting and report the income in the current year. IRC 453(d)(1). Selling grain at harvest with the check to be received January 2, 2016 does not result in alternative minimum tax in This one aspect of the tax law has been simplified. IRC 56(a)(6) was retroactively repealed by TRA of 1997 for tax years beginning after Installment sale reporting can avoid constructive receipt issues by executing a written contract before the taxpayer has a right to payment and not permitting the contract to be used as collateral for a loan. CRITERIA FOR INSTALLMENT CONTRACT REPORTING 1. Use a written contract that, under local law, binds both the seller and the buyer. 2. Add a provision in the contract that under no circumstances will the seller be entitled to any of the sale proceeds prior to the payment date. 3. Execute the contract before the taxpayer has a right to the money, normally prior to delivery. 4. Specify in the written contract that the taxpayer has no right to transfer or assign the contract rights. 5. Add a prohibition against use of the contract as collateral for any loan. 6. Do not permit the buyer of the commodity to credit the seller/farm producer s account and then charge that account for expenses such as seed, fertilizer, etc. 7. The selling farmer s right to the money is evidenced by a contract not a note. 8. The contract may provide for interest. The Tax Court has held that crop share landlords are entitled to use installment reporting to report the sale and income of their crop share rentals under a price later contract in the year following the year of crop production. See Applegate v. Commissioner 980 F.2d 1125 (7 th Cir. 1992) aff g. 94 T.C. 696 (1990). EXAMPLE 1: Kevin Farmer executes a written contract with his local elevator with the following features - non-assignable, non-transferable, cannot be amended with no possibility of prepayment. The written contract requires Kevin to deliver 5,000 bushels of beans on November 19, 2015, with payment of $9.50 per bushel to be made on January 5, Kevin will be treated as receiving income in 2016 for both regular income tax and alternative minimum tax purposes. EXAMPLE 2: Kevin delivers the 5,000 bushels of beans on November 19, 2015 with payment to be received of $9.50 per bushel. Upon delivery, Kevin decides to defer his payment until January 5, Although Kevin is in constructive receipt of the sale proceeds, he should be able to claim installment reporting and defer the income until 2016 for regular income tax and alternative minimum tax purposes.

4 EXAMPLE 3: Kevin delivers 5,000 bushels of beans according to the terms of a price later contract. He has the right to set the price anytime from July 1, 2015 to June 30, The grain buyer agrees to loan back 80% of market value of the beans upon delivery. As a general rule for regular income tax, Kevin Farmer should only report sale proceeds in the year that he has a right to receive payments, in this example, However, due to the receipt of loan proceeds in 2015, the loan proceeds will likely need to be included as income in NOTE YEAR-END TAX PLANNING: Taxpayers may wish to enter into multiple deferred grain contracts prior to year end using multiple bushel quantities. If the taxpayer s income is too low, the taxpayer may elect out of installment sale reporting on certain contracts and bring their income up to their desired amount. The inclusion amount can be determined at the time the return is prepared. NOTE If a cash method farmer dies at year end with deferred grain installment contracts outstanding, the proceeds from the contracts will be treated as income in respect of a decedent (IRD). That is, there will be no step up in basis for the grain to its fair market value at the date of the decedent s death. If the decedent owns stored grain at death, the grain will receive a step up in basis to its fair market value at the date of the decedent s death. PROBLEM: There are worse problems than not deferring income to a future year. If grain or livestock is delivered with title passing to the buyer, the seller is, with limited exceptions, no more than an unsecured creditor. Sellers of livestock can lose their payment assurances under The Packers and Stockyard Act. Deferred contract sellers of grain do not participate in state indemnity funds or elevator bonding. Therefore, if the buyer (i.e. local elevator, etc.) becomes bankrupt or insolvent between the time of sale (delivery) and the time of payment, the seller may receive only a token payment. Third party guarantees or letters of credit may be arranged through the buyer s Bank as additional security although neither may be a realistic option. An escrow account that serves no benefit to the buyer of the commodity will be treated as a payment in the year it is established and funded.

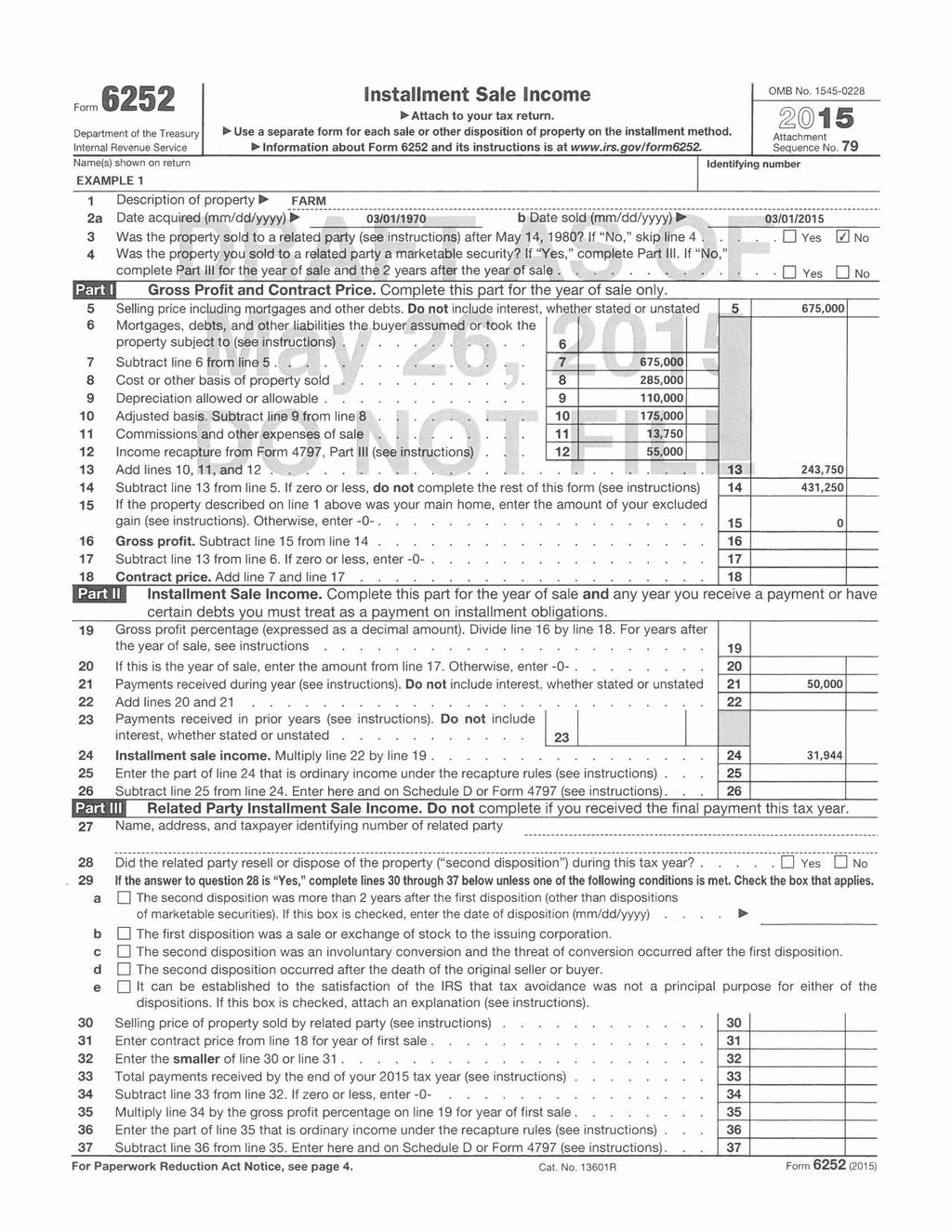

5 EXAMPLE OF REPORTING AN INSTALLMENT SALE Example 1 The Taxpayer sold a farm on contract, with possession on March 1, The following data is pertinent: Acquired March 1, 1970 Sale Price $675,000 Cost 200,000 Improvements 85,000 Depreciation 110,000 Sale Costs 13,750 Received year of sale 50,000 Assume from a total of $110,000 depreciation, $55,000 is attributable to Sec property and the balance is subject to recapture as Section 1250 straight line depreciation on Line 25 of Schedule D. Sec property may include single purpose agricultural facilities, grain storage facilities and machinery sales and the gain is reported as ordinary income on Form 4797 Part III and Part II. The sale would be reported as set forth on the attached Forms 4797, 6252 and Schedule D. Proof of Reporting: Sale price $ 675,000 Cost $200,000 Improvements $ 85,000 Costs of sale 13, ,750 Less depreciation (110,000) Less adjusted cost basis 188,750 Total realized gain $486,250 Reported per this example: A. Ordinary income (due to Sec recapture in 2015) $ 55,000 B. Downpayment ($50,000 x.63889) 31,944 C. Balance of gain to be reported over remainder of contract $625,000 x = $399,306 $486,250 The gains on Lines B & C are fully subject to Section 1250 straight line depreciation recapture and may be taxed at a maximum marginal rate of 25%.

6

7

8

9 TO GET MORE INVOLVED, ASSUME THE TAXPAYER S HOME WAS ON THE FARM: Example 2 ALLOCATION HOME FARM TOTAL Sale Price $60,000 $615,000 $675,000 Initial cost, allocated $25,000 $175,000 $200,000 at time of purchase Additions and $18,000 $ 85,000 $103,000 improvements Depreciation $110,000 $110,000 Costs of sale based on sale price $ 1,250* $ 12,500* $ 13,750 Received in year of $ 4,500* $ 45,000* $ 50,000 sale * 9% of total Assume from a total of $110,000 depreciation, $25,000 is attributable to Sec property and the balance is subject to recapture as Sec straight line depreciation. Also, assume that the taxpayer has owned and lived in the home as the taxpayer s personal residence at least two of the last five years. Proof of Reporting: Sale price of farm $615,000 Cost $175,000 Improvements 85,000 Costs of sale 12, ,500 Less depreciation (110,000) Less adjusted cost basis 162,500 Total realized gain $452,500 Reported as per this example: A. Ordinary income (due to Sec recapture in 2015) 25,000 B. Down payment $45,500 x ,627 C. Balance of gain to be reported over remainder of contract ($569,500 x.6951) $395,873 $452,500 The gains on lines B & C are all subject to Section 1250 straight line depreciation recapture and may be taxed at a maximum marginal rate of 25%. Gain on the sale of the personal residence need not be reported.

10

11

12

13 TO GET MORE INVOLVED, ASSUME THE TAXPAYER S HOME WAS ON THE FARM AND THAT THE MACHINE SHED FORMERLY USED IN THE FARMING OPERATION WAS CONVERTED TO PERSONAL USE MORE THAN TWO YEARS AGO: Example 3 ALLOCATION HOME/MACHINE FARM TOTAL SHED Sale Price $80,000 $595,000 $675,000 Initial cost, allocated $40,000 $160,000 $200,000 at time of purchase Additions and $18,000 $ 85,000 $103,000 improvements Depreciation $15,000 $ 95,000 $110,000 Costs of sale based $ 1,629* $ 12,121* $ 13,750 on sale price Received in year of $ 5,925* $ 44,075* $ 50,000 sale * 11.85% of total ** 88.15% of total Assume from a total of $95,000 depreciation on the farm, $25,000 is attributable to Sec property and the balance is subject to recapture as Sec straight line depreciation. Also, assume that the taxpayer has owned and lived in the home as the taxpayer s personal residence at least two of the last five years and that the machine shed was converted to personal use prior to May 6, Proof of Reporting: Sale price of farm $595,000 Cost $160,000 Improvements 85,000 Costs of sale 12, ,121 Less depreciation ( 95,000) Less adjusted cost basis 162,121 Total realized gain $432,879 Reported as per this example: A. Ordinary income due to Sec recapture in ,000 B. Down payment ($44,075 x.6855) 30,213 C. Balance of gain to be reported over remainder of contract ($550,925 x.6855) $377,666 $432,879 The gains on lines B & C are all subject to Section 1250 recapture and may be taxed at a maximum marginal rate of 25%. Gain on the sale of the personal residence need not be reported. The authors believe that Revenue Ruling is applicable and has not been modified by the final regulations as issued under I.R.C. Sec. 121.

14

15

16

17 MISCELLANEOUS LEASING ISSUES 1. RENTAL INCOME VS. SELF-EMPLOYMENT INCOME. The IRS argues income from all machinery (personal property) leases, regardless of the lessors involvement in the lease, is subject to self-employment tax. Based on the 1989 case of Carl Stevenson, T.C. Memo , the IRS has added a note to Part I of Schedule E If you are in the business of renting personal property, use Schedule C or C-EZ. The IRS has increased its audit activity regarding this issue. I.R.C. Sec defines self-employment income as "net earnings from self-employment derived by an individual from any trade or business carried on by such individual." Specifically excluded from this definition are "rentals from real estate and from personal property leased with the real estate" unless a share rental is involved with material participation. The IRS appears to conclude that if there is no rental of real estate involved, that the rental income is subject to selfemployment tax. Even though I.R.C. Sec requires the individual to be in a trade or business, the IRS is seemingly ignoring the requirement. A given level of activity by the lessor would seem to be necessary to treat lease income as income from a trade or business. The term "trade or business" is held to mean the same as it does under I.R.C. Sec The Courts, in Sec. 162 cases, have always required a certain level of regular, continuous activity to be held to be a trade or business. See Groetzinger v. Commissioner, 87-1 T.C. Par (1987). If only personal property is leased and no trade or business exists, the income is not subject to selfemployment tax and income should be reported on Form 1040, line 21, and expenses on line 36. See also Michael D. Welch, et. al. v. Commissioner, T. C. Memo , where the Taxpayer s tool rental activity was held to be an active trade or business, was properly reported on Schedule C and was not a rental activity within the meaning of the passive activity rules of I.R.C. Sec It also appears in recent audit activity that if a loss were to occur, the IRS is prepared to argue this is a passive loss and limit deductibility. Rental receipts from an activity that does not constitute a business, should be reported as other income. Related expenses are to be reported on the total deduction line with a notation of PPR (Personal Property Rentals) on the dotted line next to the amount. In order to avoid this issue, wherever possible, it may be best to lease the farm machinery with the farm real estate as these rentals are specifically excluded from net income for selfemployment purposes and should be reported on Schedule E. Incorporating or forming an LLC may also reduce the likelihood that rental income would be subject to self-employment tax. 2. LEASE VS. INSTALLMENT SALE. Due to I.R.C. Sec requiring the recapture of all depreciation deductions taken in the year of sale as ordinary income, the installment sale of farm machinery is prohibitive. Leasing, as opposed to an installment sale agreement, may increase the current deductions to the Lessee. With this in mind, one may well desire to lease the property instead of selling it, so the receipts can be reported over a period of years. If the arrangement is a lease, payments are ordinary income to the lessor and are fully deductible by the lessee. (Lessor's rental proceeds are possibly subject to SE tax as described previously). If the arrangement is treated as a sale, a portion of each payment will be treated as imputed interest. The seller will report the Sec recapture in the year of the sale and interest income each year. The buyer (lessee) will have imputed interest expense under I.R.C. Sec. 483 to report and must depreciate the purchase price. Depending upon the participation of the Buyer

18 (Lessee) and the assets purchased (leased), the Buyer (Lessee) may also take 179 expense and depreciation. The Farmers Tax Guide, Publication 225, provides that the intent or the parties determines whether an agreement is a lease or an installment sale. Publication 225 further provides in absence of other persuasive factors, an agreement will be treated as a sale rather than a lease if any of the following is true: 1. The agreement applies part of each payment toward an equity interest you will receive. 2. The lessee receives title to the property after paying a stated amount of required payments. 3. The lessee must, over a short period of time, pay an amount that represents an unusually large part of the price you would pay to buy the property. 4. The lessee pays rent that is much more than the current fair rental value of the property. 5. The lessee has an option to buy the property at a small price compared to the value of the property at the time the lessee can exercise the option. Determining the value at the time of entering into the original agreement also indicates a sale. 6. The lessee having an option to buy the property at a small price, compared to the total amount paid under the lease. 7. The lease designates some part of the payments as interest, or part of the payments are easy to recognize as interest. Important factors to be considered in determining whether the agreement is a lease or a sale are the parties' intention, the fact that the owner/lessor pays insurance and taxes and if the lease runs over the estimated life of the machinery. An appraisal would also be important. Interest should not be charged if a lease is intended. If an option to purchase should be involved at any time, the option to purchase should be at FAIR MARKET VALUE at the time of purchase. Automatically receiving title at the end of the lease period smacks of a sale and should be avoided. The lease payment should be comparable to what used property would lease for, the problem here being that there are no guidelines for the leasing of used equipment. See Tillman v. Comm., 71 T.C.M (1996) where the "rental agreement" passed title to the Lessee upon execution of the lease, required the Lessee to be responsible for insurance, maintenance and bear the risk of loss was held to be a conditional sales contract. The principle issue is the business reality and economic substance of the transaction. EXAMPLE (1): Able Farmer rents his farm machinery to his daughter, Beth Farmer, under a written lease which requires Beth to pay fair rental value, to repair the machinery, and to provide and pay for insurance on the machinery. Beth may purchase one or more items leased at its fair market value during or upon completion of the lease term. Able Farmer should report the income on Schedule E if the equipment is rented with other land and he is not involved in a trade or business. If land is not rented with the machinery and Able is not involved in a trade or business, the income should be reported on Other Income Line 21 of the Form 1040 and expense on Total Adjustments Line 36 of the Form 1040 and should be identified as P.P.R. Able should report the income on Schedule C if he is involved in a trade or business. It would appear in this set of facts that there is no personal involvement by Able Farmer and that the payments are properly reported on Schedule E or Form 1040, line 21 and line 36, although IRS may argue otherwise. Beth Farmer may take lease payments as an expense on her Schedule F. EXAMPLE (2): Assume Beth Farmer owns a tractor purchased in 2001 at a cost of $22,500. In 2014 she leases a new tractor under a true lease for the sum of $12,500 per year and transfers her tractor to the Lessor for the first payment. Beth Farmer must report the trade-in as a sale, has

19 ordinary income as a result of I.R.C. Sec recapture in the amount of $12,500 and a lease expense on her Schedule F in the amount of $12,500. EXAMPLE (3): Kevin Farmer needs a machine shed for his equipment. Kevin Farmer signs a lease containing the following terms: 1. The $30,000 cost of the machine shed is paid by a leasing company. 2. The lease term is for six years, began in 2009 and is payable as follows: Date payment due Amount of payment Date payment due Amount of payment $7, $6, , , , ,000 Kevin Farmer is responsible for paying all real estate taxes, insurance, utilities, and repairs on the machine shed during the lease period and at the end of the lease period, Kevin Farmer may purchase the building from the leasing company for $1,000. If this purchase option is not exercised, the leasing company reserves the right to remove the building. This lease is merely a financing arrangement, and should be treated as a purchase. Kevin Farmer has all the responsibilities of ownership of the machine shed and the "buyout" amount of $1,000 does not approximate the fair market value of the shed. Kevin Farmer should depreciate the cost of the shed over 20 years and deduct the imputed interest. EXAMPLE (4): Assume Kevin Farmer executes a lease granting the Lessor a right of access to his real estate, pays $4, per year for seven years as rental payments, pays all real estate taxes, insurance and repairs. The lease may be renewed at the end of seven years at fair market value. The building may be purchased at fair market value at the end of the lease or the lease may be terminated. This lease should be treated as a true lease, as the Lessor provided all of the original equity and no bargain purchase was included. 3. LEASING OF A VEHICLE. The question of leasing a vehicle vs. purchasing must be decided on a case by case basis. Although one generally looks at the least cost approach, other tax and non-tax considerations may be involved. The leasing of an automobile or pickup with a gross vehicle weight of less than 6,000 pounds, that is used in a trade or business, may result in the inclusion of an amount in the taxpayer's income. Likewise, this type of vehicle would be subject to MACRS rules and I.R.C. Sec. 280(f) depreciation limits. If a vehicle was purchased, the owner would be entitled to depreciation and interest expense deductions. If a vehicle is leased, the owner is entitled to deduct the business portion of the lease and nonrefundable security deposit subject to the lease value inclusion amounts. If the fair market value of such a vehicle is greater than $16,000 for automobiles and $17,350 for trucks and vans leases beginning in 2015, the inclusion amount must be computed under Rev. Proc The inclusion amount is to be prorated based on the number of days leased during the year and the percentage of business and investment use. The income is reported on the same schedule where the leasing expense is deducted.

20 ENVIRONMENTAL CLEAN-UP COSTS Priv. Ltr. Rul points out that it is not only painful but expensive to be confronted with environmental clean-up. In that ruling, capitalization was required for the following expenditures: 1. Testing for soil contamination. 2. Testing for groundwater contamination. 3. Excavating and transporting contaminated soil. 4. Legal fees to defend EPA and state agency charges and claims of third parties. 5. Cost of oversight of clean-up activities. 6. Environmental audits. Deduction of costs as current expenses was denied, capitalization of the expenses was required and the expenses were termed incidental, with such costs not adding to the value of the property nor materially prolonging its life. As to legal fees, the same reasoning and result will occur since the fees take on the character of the suit on which the costs were expended. Where there is rehabilitation or restoration that will benefit the property for the remainder of its useful life, the cost must be capitalized. Assessment of the problem, removal of the contamination and replacement of new soil would be a capital item and the legal costs associated therewith would be treated in the same way. Rev. Rul , C.B. 35 addresses the question in a somewhat more favorable light. In this case, the taxpayer bought five acres of land in rural Texas. The land was located near an exit of an Interstate. It was used for grazing and was not contaminated by hazardous waste when purchased. A truck stop was built on the land, and over the years the same became contaminated. The EPA investigated and ordered remedial action consisting of excavation of land at a cost of $45, The Ruling takes the very reasonable position that the expenditure is an expense that is fully deductible as an ordinary and necessary business expense. The expenditure did not result in an improvement that increased the value of the property, and instead, was simply restored to the condition existing prior to the contamination. A manufacturer who replaced underground storage tanks was able to deduct costs incurred in their removal, cleaning and disposal as ordinary business expenses. See Rev. Rul , I.R.B Taxpayer was allowed to currently deduct environmental clean-up costs for contamination occurring during its ownership period, but had to capitalize the environmental clean-up costs for contamination occurring prior to its ownership. Priv. Ltr. Rul For property purchased that was already contaminated, (i.e. property that had housed a dry cleaning business and remedial action including the removal of dry cleaning equipment and replacement of contaminated soil), the expenditures would be a capital expenditure not currently deductible. Priv. Ltr. Rul See also United Dairy Farmers, Inc. v. U.S., 107 F. Supp. 2d 937 (S.D. Ohio 2000) where the Court held a Corporation could not deduct environmental clean up costs.

21 New proposed and temporary IRS regulations issued regarding the capitalization vs. the current deduction of repairs gives further authority for the treatment of previously contaminated properties. FACTS: X purchases a store located on land that, unbeknownst to her, contained underground gasoline storage tanks left by a prior owner. The tanks had leaked, causing soil contamination X was not aware of the contamination at the time of purchase. X incurs costs to remediate the soil RESULT: X is required to capitalize the remediation costs because of the betterment to the land The fact of having acquired the asset with a defect, whether known or unknown, is not relevant to the determination. SOURCE: Reg (a)-3T(h)(4), Example (1). The Court held that environmental remediation costs could be currently deducted if the taxpayer could prove they had caused the contamination during the taxpayer s ownership period. Kerr-McGee Corp. v. U.S U.S. Tax Cases (CCH) Paragraph (Fed. Cls. 2007). The IRS in Rev. Rul , C.B. 509 has determined expenditures incurred to remediate contamination from a manufacturing plant must be capitalized as part of inventory costs under IRC Section 263A. The Ruling also provides that the IRS will not challenge current deductions for remediation costs in any prior taxable year ending on or before February 6, The IRS in Rev. Rul , C.B. 67 has provided additional clarification of issues raised in Rev. Rul , in a variety of manufacturing examples. I.R.C. Sec. 198 provided that qualified clean up costs paid or incurred after August 5, 1997, and paid and incurred before January 1, 2001, would be currently deducted if the taxpayer so elects. This provision has now been extended by the 2010 Tax Relief, Unemployment Insurance Reauthorization and Jobs Creation Act to include expenditures paid or incurred before January 1, Section 198(h) of the Internal Revenue Code states this section shall not apply to expenditures after Deccember 31, These sections apply to hazardous substances referred to as brownfields which include the abatement or control of hazardous substances at a qualified contaminated site. A qualified contaminated site is property that is held for use in a trade or business, for the production of income or as stock in trade or inventory and on which there has been a release of a hazardous substance. The taxpayer must obtain a statement from the states environmental agency as to the release of the hazardous substance. The requirement of the site being located in a targeted area was removed effective December 21, The elimination of the targeted area requirement expands eligible sites to those containing a hazardous substance as certified by a state environmental agency. If the property is later sold, the clean up costs will be treated as being subject to I.R.C. Sec depreciation recapture. Although this election is attractive, the effect will be limited as it

22 must be in connection with the abatement and/or control of hazardous waste on a qualified containment site. The IRS apparently will accept private ruling requests regarding the subject of environmental clean up costs deductibility due to the possible elective deduction under I.R.C. Sec. 198, the possible deduction as ordinary and necessary business expenses under I.R.C. Sec. 162 or as losses under I.R.C. Sec. 165 or the necessity to capitalize these expenses under I.R.C. Section 263. Rev. Proc , C.B The IRS has also provided guidance for taxpayers electing to deduct qualified environmental remediation expenditures under I.R.C. Sec Rev. Proc , C.B The election is made by claiming the costs as a current deduction on the appropriate business schedule being filed and describing them as Section 198 Election. The election must be made on a timely filed return including extensions in the year the expenditures were incurred.

23 DISASTER PAYMENTS & CROP INSURANCE IRC 451(d) GENERAL RULE: Crop loss proceeds from crop insurance and USDA disaster payments are included as income in the year of receipt. However, the cash basis taxpayer may elect to include the proceeds as income in the year following receipt, if the crop loss proceeds are as a result of crop insurance or federal disaster payments received as a result of hail, fire loss, flood, drought or other natural disaster and the income would have normally been reported in the later year under the taxpayer s normal business practice. The provision covers payments made because of damage to crops or the inability to plant crops. IRC 451(d) and Rev. Rul , C.B The exception applies to crop insurance proceeds and disaster payments received under the Agricultural Act of 1949, as amended, and Title II of the Disaster Assistance Act of Agreements with insurance companies that make payments without regard to actual losses do not qualify. IRS Notice 89-55, C.B ELECTION: To defer reporting until the year following receipt, the following information that must be included in a separate, signed election form attached to either an original or amended tax return: 1. Name and address of the taxpayer. 2. A declaration that the taxpayer is making an election under IRC 451(d) & IRC Identify the specific crop or crops destroyed or damaged. 4. A declaration that under normal practice the income that was lost from the crops that were destroyed or damaged would have been included in income for the year following the year of destruction or damage. 5. The cause of the damage and dates the damage occurred. 6. If crop insurance was involved, the amount received from the insurance carriers itemized with respect to each crop and the date received. 7. Name of the insurance carrier. As to disaster payments, it does not appear that there must be a declaration that the area is a disaster area. However, one must still meet the factual test of the disaster, such as drought or flood. NOTE: Rev. Rul provides that where an election was made to defer receipt of taxable income to the year following, such election applied not only to crop insurance receipts but also to disaster payments. Crop insurance proceeds and disaster payments must be combined and reported consistently. The taxpayer cannot pick and choose. The election covers all crops, as well as all crop insurance proceeds. If crop insurance proceeds are received for two crops and the election is made, the proceeds from both are reported in the following year. An election counts for only the tax year that it is made in. An issue arises if the taxpayer receives disaster and/or crop insurance payments for two different crops and the crops are normally marketed in two different years. See, Rev. Rul , C.B. 113, where the taxpayer was required to sell over 50% of all crops in year following harvest to defer all insurance payments. Proceeds from a disaster payment or crop insurance for a crop normally sold at harvest would seem not to be deferrable. NOTE: The Tax Court held in Nelson v. Comm. 130 T.C. 570 (2008) that taxpayers were not eligible to defer federal crop insurance proceeds to the following year, where only 35% of the current crop proceeds were reported in the following year.

24 The Tax Court held that 35% of the crop was less than substantial and not sufficient to support deferral to the following tax year. The Eighth Circuit (Nelson v. Comm., 568 F.3d 662(8 th Cir. 2009), upheld the Tax Court s ruling. The Eighth Circuit used Rev. Rul , C.B.113 as authority that the election to defer was available only to a taxpayer who deferred greater than 50% of income from such crop to the following year. Gross crop insurance proceeds must be deferred. If the farmer has deferred the payment of crop insurance premium to the fall and the insurance carrier reduces the crop insurance proceeds by the premium owed, the gross amount of insurance proceeds without the offset for the insurance premium must be deferred. The crop insurance premium should then be deducted as a current expense. EXAMPLE: Kevin Farmer is entitled to $42,000 crop insurance proceeds, but owes $6,000 of premium and therefore only receives $36,000. Kevin may defer $42,000 of insurance proceeds to the following year and deduct $6,000 crop insurance expense in the current year. The taxpayer may not elect to report payments in the year of loss if the proceeds are received in the year following the year of loss. FSA disaster payments received in the year following the year of loss are not deferrable. CROP REVENUE COVERAGE (CRC) INSURANCE PAYMENTS: CRC insurances are privately developed policies which are broader in scope than the traditional multi peril crop insurance policy. CRC insurance covers any revenue losses whether caused by a casualty (i.e. flood, hail), low prices or low yields. Actual historic production is utilized to set the coverage which ranges from 50% to 85% of production. The commodity base price sets a minimum guarantee, but there is a second price test at harvest which may increase the guarantee. As noted above, the IRS has previously taken the position that crop insurance that provides for payments without regard to actual losses do not qualify for deferral. IRS Notice If a crop insurance payment is based on both crop loss and price loss from a revenue-based insurance policy, only the portion intended to reimburse the farmer for crop loss is deferrable. The portion payable because of a decline in market price is not deferrable and is income in the year the payment is received. Documentation from the insurance carrier may be needed to determine the amount of any loss payment eligible for deferral. Consider the following examples from Roger McEowen s CALT materials Tax and Legal Issues Associated With the 2012 Drought, July 20, 2012 (updated August 6, 2012): EXAMPLE: Al Beback took out an insurance policy (RP) on his corn crop. Under the terms of the policy the approved corn yield was set at 170 bushels/acre, and the base price for corn was set at $4.15/bushel. At harvest, the price of corn was $3.25/bushel. Al s insurance coverage level was set at 75 percent, and his yield was 100 bushels/acre. Al s final revenue guarantee under the policy is 170 bushels x $4.15 x.75 = $529.13/acre. Al s calculated revenue is his actual yield (100 bushels/acre) multiplied by the harvest price ($3.25/bushel) which equals $325/acre. Al s insurance proceeds is the guaranteed amount ($529.13/acre) less the calculated revenue ($325/acre), or $204.12/acre. His physical loss is the 170 bushel/acre approved yield less his actual yield of 100 bushels/acre, or 70 bushels/acre. Multiplied by the harvest price of $3.25/bushel, the result is a physical loss of $227.50/acre. Al s price loss is computed by taking the base price of $4.15/bushel less the harvest price of $3.25/bushel, or $.90/bushel. When multiplied by the approved yield of 170 bushels/acre, the result is $153.00/acre.

25 So, to summarize, Al has the following: Total loss: (1) anticipated income/acre [170 $4.15/ bushel = $705.50/acre] less (2) actual result [100 $3.25/acre = $325.00] for a result of $380.50/acre. Physical loss: 70 bushels/acre x $3.25/bushel harvest price = $227.50/acre Price loss: 170 bushels/acre x $.90/bushel = $ Physical loss as percentage of total loss: $227.50/ =.5979 Insurance payment: $204.12/acre Insurance payment attributable to physical loss (which is deferrable): $ x.5979 = $122.04/acre Portion of insurance payment that is not deferrable: $ $ = $82.08/acre If harvest price exceeds the base price, consider the following example: EXAMPLE: The facts are the same as in the previous example, except that the harvest price of corn was $4.50/bushel. Al s final revenue guarantee under the policy is 170 bushels/acre x $4.15 x.75 = $529.13/acre. Al s calculated revenue is his actual yield (100 bushels/acre) multiplied by the harvest price ($4.50/bushel) which equals $450.00/acre. Al s insurance proceeds are the guaranteed amount ($529.13/acre) less the calculated revenue ($450.00), or $79.13/acre. His yield loss is the 70 bushels/acre which is then multiplied by the harvest price of $4.50/bushel, for a physical loss of $315/acre. Al s price loss is zero because the harvest price exceeded the base price. So, to summarize, Al has the following: Total loss (per acre): $ (physical loss) + $0.00 (price loss) Physical loss as percentage of total loss: $315/315 = 1.00 Insurance payment: $79.13/acre Insurance payment attributable to physical loss (which is deferrable): $79.13 x 1.00 = $79.13/acre Portion of insurance payment that is not deferrable: $ = $0.00 OBSERVATION: Normally, if the price of crop at the time of harvest exceeds the base price, the physical loss will constitute 100 percent of the total loss, and the entire insurance payment will be deferrable. However, if insurance proceeds for physical loss to crops are collected before the harvest price is determined and the harvest price ultimately exceeds the base price, any additional payment attributable to the price difference could be deemed by IRS to be attributable to revenue loss that would not be eligible for deferral. NOTE: For policies not based on physical loss (such as a Group Revenue Protection (GRP) policy, payments received are not deferrable. The same holds true for an Average Crop Revenue Election (ACRE) payment because it is received after the end of the marketing year and in a year after the year the crop at issue is produced. Due to the drop in crop prices during 2013, many farmers may receive revenue loss payments, which will be nondeferrable.

26 WEATHER RELATED SALE OF LIVESTOCK ONE-YEAR DEFERRAL (DISASTER AREA) IRC 451(e) ELECTION: Cash method farmers (principal trade or business is farming) who sell livestock due to weather related sales (i.e. drought, flood, etc.) may elect a one-year deferral for the reporting of gain over and above normal tax year sales. The area of the taxpayer s trade or business must be in or near an area declared to be a disaster area eligible for federal assistance in order for the taxpayer to be eligible for this one-year deferral. Livestock need not have been raised or sold in the actual disaster area; however, sale must have occurred solely on account of the drought or other condition and its impact on water, grazing or other requirements of the animals within the area. IRC (c) and IRS Notice The deferral election applies to all livestock held for sale (raised or feeders), as well as, livestock used for draft, breeding, dairy or sporting purposes, and livestock held for < 2 yrs. (cattle & horses) and other livestock held for < 1 yr. NOTE: Before 1997, only sales of livestock due to drought were eligible for deferral. Sales related to other weather-related conditions (tornadoes, floods, etc.) were added for tax years beginning in 1997 and thereafter. ELECTION FORMAT: A separate election form is to be attached to the return, is to be filed on or before the due date of the return, including extensions, and must contain the following: 1. Declare that you are making an election under IRC 451(e) & IRC Regs Show evidence of the weather related conditions that forced the early sale, including the date (if known) the area was designated as eligible for federal assistance as a disaster area. The sale of livestock may occur before the designation is made. 3. Explanation showing the relationship between the weather related conditions and reason for sale. 4. Document the total number of animals sold in each of the three preceding years. 5. Document the total number of animals that would have been sold under normal conditions. 6. Document total number of animals sold that particular year and the number sold because of the weather related conditions. 7. Compute the amount to be deferred to the following year. TAX PLANNING NOTE - EXTENSION OF DEFERRAL ELECTION PERIOD: For sales of draft, breeding or diary livestock, taxpayers can elect to take advantage of the one (1) year deferral provisions of IRC 451(e) during any of the four (4) years after the close of the first taxable year in which any part of the gain or conversion from livestock sales are realized. IRC 451(e)(3) & 1033(e)(2). This provision is effective for tax returns whose due date (without extensions) is after 12/31/02.

27 WEATHER RELATED SALE OF DRAFT, DAIRY & BREEDING LIVESTOCK FOUR-YEAR REINVESTMENT IRC 1033(e) IRC 1033 allows taxpayers who are forced to involuntarily sell livestock to defer gain into replacement property provided qualified replacement property is timely purchased. For example, livestock destroyed by disease may be replaced in a tax deferred manner under IRC 1033(d) (not discussed herein). Livestock held for draft, dairy or breeding purposes sold in excess of normal yearly sales due to drought, flood or other weather related conditions may similarly be replaced under IRC 1033(e). The applicable replacement period is four years after the close of the first taxable year in which any part of the gain on conversion is realized. NOTE: The American Jobs Creation Act of 2004 increased the prior 2-year replacement period to a 4-year period, for tax years with a return due date, excluding extensions, after Sales of draft, dairy or breeding livestock will qualify for involuntary conversion treatment regardless of how long they have been held by the taxpayer. There is no required 12- or 24-month holding period. There is also no requirement that a weather damaged area be declared a drought or disaster area if livestock is replaced within two (2) years. However, if livestock is to be replaced under the 4-year replacement provision authorized in IRC 1033(e)(2), then a disaster/drought declaration must have been made for the area of the taxpayer s trade or business. REPLACEMENT PROPERTY: Replacement livestock must be similar or related in service or use. Thus, dairy cows should be replaced by dairy cows. IRC Regs (e)-1(d). However, breeding cattle may replace buffalo of the same sex. PLR The American Jobs Creation Act of 2004 also expanded IRC 1033 to permit taxpayers to replace livestock with other tangible farm property, if it was not feasible to replace livestock with similar livestock. EXAMPLE: A farmer that sells livestock early in a federally designated drought disaster area and is unable to buy back livestock due to the drought, may reinvest in farm equipment and machinery. However, if replacement property is not like-kind, a 2-year replacement period applies. IRC 1033(e), 1033(f) and 1033(a)(2)(B)(i). If due to soil or other environmental contamination, it is not feasible to reinvest in similar livestock, the taxpayer may invest the proceeds from involuntarily converted livestock into other tangible or real property used for farming purposes. REQUIRED STATEMENT FORMAT (YEAR OF SALE) IRC REGS (e)(1) & (a)(2): 1. Taxpayers must attach a statement to their return for the year in which livestock was sold and provide evidence of existence of the weather related conditions that forced the sale. 2. Compute the gain realized on the sale or exchange. 3. Document the number and kind of livestock sold or exchanged. 4. Document the number of livestock of each kind that would have been sold under the usual business practice in the absence of the weather related conditions.

28 NOTE: The actual election to defer gain can be made at any time within the normal statute of limitations for the period in which the gain was realized, assuming it is before the expiration of the period within which the converted property must be replaced. IRC Regs (a)-2(c)(2). The replacement of the livestock should be reported on the following years tax returns. In the event there is not full reinvestment, the return for the year of the weather related sales must be amended to report additional income in an amount equal to the sum not reinvested. TAX PLANNING NOTE: A taxpayer with raised breeding or dairy animals may prefer to recognize gain as a capital gain in the year of sale, if the income can be reported at the 0% or 15% capital gain rates. This would likely occur with a sole proprietor farmer where regular depreciation or IRC 179 expensing from purchased replacement livestock will offset ordinary SE taxed income in higher tax rate brackets. IRS NOTIFICATION OF EXTENDED DROUGHT LOCATIONS: Due to the intense, prolonged drought in parts of the United States, IRS issued Notice which provides additional time to replace livestock that was initially sold as a result of drought. Notice explains how a taxpayer can determine whether additional time is available. EXAMPLE: The 4-year replacement period scheduled to end on , is extended for one additional year if, for any weekly period included in the 12-month period ending on , severe, extreme or exceptional drought conditions were reported for any location in the county that experienced the drought that forced the sale of the livestock or for any location in a neighboring county. The replacement period may be further extended if the drought conditions persist after To assist taxpayers in determining whether their replacement period has been extended, IRS publishes a yearly list of counties that experienced exceptional, extreme or severe drought for the 12-month period ending each August 31st. This list was complied after consultation with the National Drought Mitigation Center. See Notice for the list of counties for which the replacement period has been extended for the 12-month period ending

29 ONE YEAR (IRC 451(e)) VS. FOUR YEAR (IRC 1033(e)) NOTE: PLR s , and provide that a taxpayer may revoke an election for 1-year deferral under IRC 451(e) and may apply to the District Director for a determination on whether the taxpayer may, in the alternative, defer income under IRC 1033(e) if eligible livestock is replaced within 4 years. A Private Letter Ruling or a Determination Letter will be necessary to request the change. However, this alternative tax reporting/deferral should be possible as all required information would have been filed with the taxpayer s return when the IRC 451(e) election was made; and, there is no requirement to file an IRC 1033(e) election by the due date of the return. NOTE: IRC Regs (a)-2(c)(2) requires an informational statement containing similar information to IRC 451(e) to be included with the return for the tax year or years in which the gain is realized but does not require a per se election. NOTE: It is not possible to first elect under IRC 1033(e), revoke the election, and then make an IRC 451(e) election, as the one-year deferral election needs to be made by the due date of the return, including extensions. ******************************************************** COMPARISON OF ONE-YEAR (IRC 451(e)) / FOUR-YEAR RULES (IRC 1033(e)) Issue Sec. 451(e) - One Yr. Sec. 1033(e) - Four Yr. Period to make election Rule covers Rule allows Due date of return, including extensions (If 1033 livestock four years from due date of return, including extensions) Sales of all livestock in excess of normal business practice Postponement of income to following year Within 4 years of the end of the sale year Sales of draft, breeding and dairy livestock in excess of normal business practice Postpone gain by replacement of livestock Cause of sale Weather related sale Weather related sale, disease Disaster declared Yes No, unless beyond two years, then federal designation is necessary to replace livestock in years 3 and 4 Repurchase required No Yes Carryover basis N/A Basis decreased by gain deferred Replacement period N/A Within 4 years of the end of sale year unless extended by the IRS Qualifying Livestock All livestock Draft, Breeding or Dairy Livestock

30 EMPLOYMENT TAXES ON FARM WAGES Farmers who pay cash wages to an employee of $ or more in a year or exceed a total of $2, of total payroll for the year are subject to social security and medicare taxes on all wages paid. For 2014 farmers must withhold 7.65% of the employee's wages and pay 7.65% as the employer's share. If wages exceed $200, for any one employee, the employer must withhold 0.9% additional medicare tax from the employee s share. Farmers should have each employee sign an I-9 and a W-4 and withhold federal and state income taxes from the wages. Farmers are required to deposit social security and medicare taxes as well as income taxes withheld during the year, unless the tax liability is less than $2, If less than $2, of liability, the taxes may be paid in full with a timely filed quarterly or annual return. Quarterly deposits of state withholding are required if withholding is less than $150 per month. If your state withholding is more than $ , a monthly deposit is required. The minimum threshold for FUTA deposits is $ Farmers are liable for FUTA taxes and SUTA taxes only if they pay wages in excess of $20, in any calendar quarter in the previous two years or employ 10 or more employees a day for at least 20 different weeks during the previous two years. The first $7, of wages are subject to FUTA taxes at a rate of 6.0% less a credit of 5.4% or a rate of.6% for 1/1/13 to 12/31/13. If the farmer pays the employee s share of social security and medicare taxes without deducting it from the employee s wage, this payment amount is treated as additional income to the employee and must be included in Box 1 of the employee s W-2. The payment amount does not increase the employee s social security and medicare wages nor does it get added to total wages for FUTA purposes. Farm wages to a child or spouse of the taxpayer are generally subject to employment taxes including social security and medicare, state and federal income tax withholding and FUTA taxes. Farm wages paid to a child who is under the age of 18 are exempt from social security and medicare taxes. Wages paid to a child who is under the age of 21 for domestic services in the parents home are exempt from social security and medicare taxes. Farm wages or domestic wages paid to a child who is under age 21 are exempt from FUTA tax. Farm wages paid to a spouse are subject to social security and medicare taxes, but are exempt from FUTA tax. Domestic wages paid to a spouse are exempt from social security and medicare tax as well as FUTA tax. In Ross v. Comm., T.C. Summary Opinion , Ms. Ross did consulting and tax preparation and employed her children, ages 8, 11, and 15. The children performed various services including shredding, filing, trash removal, etc. Although Ms. Ross kept time records, no payroll checks were issued and payments were made directly to third parties as directed by her children. The court concluded these wages were not properly deductible. The court discussed general factors that would not support a deduction. Review Dumond v. Comm., T.C. Summary Opinion , (January 31, 2005) where wages to children (ages 10 and 5) were disallowed when received in a lump sum at year end, checks were not cashed until the following year and proceeds went back into the parent s account. Also see Denman v. Comm., 48 T.C. 439 (1967) where only 10% of claimed wages to 10 year old and 7 year old children were allowed. A tax planning opportunity arises for parents to pay their children a wage (must provide a W-2) for work in the home or trade/business to provide the earned income basis upon which to

31 contribute up to $5,500 per year into a Roth IRA. Under the basis recovery rules for Roth IRA distributions, the contributions would be available for distribution for college expenses without income taxation and without incurring the 10% early withdrawal penalty. Also, under current law, the funds held in a Roth IRA account would not be considered a resource for college financial aid purposes. This appears to be a better investment for college-bound children than educational IRAs, if one must choose between the two. However, a Roth IRA contribution will not preclude a contribution to an educational IRA in the same year. The issue also arises whether part-time day laborers are employees or independent contractors. In a farm setting it would seem difficult to find that these laborers are anything other than employees, as the employer is in control of hours, and the laborers do not bring any equipment to the job site. In order to protect the employer in the event of their injury, the employees need to be covered under a workman s compensation insurance policy. In September of 2011, the Service announced a Voluntary Worker Classification Settlement Program. (VCSP) (IRS Announcement, ; IR ). In December of 2012, the VCSP was modified in IRS Announcement ; I.R.B The VCSP permits a taxpayer under IRS audit, other than an employment tax audit, to be eligible to participate. The current eligibility requirements are clarified to provide (a) that a taxpayer who is a member of an affiliated group within the meaning of section 1504(a) is not eligible to participate in the VCSP, if any member of the affiliated group is under employment tax audit, b) that a taxpayer is not eligible to participate if the taxpayer is contesting in court the classification of the class or classes of workers from a previous audit by the IRS or Department of Labor, and c) eliminates the requirement that a taxpayer agree to extend the period of limitations on assessment of employment taxes as part of the VCSP closing agreement with IRS.

32 SELF-EMPLOYMENT TAX ISSUES REGARDING LIVESTOCK CONFINEMENT BUILDINGS If a sole proprietor constructs a confinement building, places their own livestock in the building, provides all management and labor, and pays all expenses, certainly the farmer is materially participating and any net profit will be subject to self-employment tax. The self-employment tax issues become blurred when farm owners construct agricultural production facilities which are subject to a contractual production agreement with a third party tenant/producer. Whether self-employment tax is incurred or not will likely be determined by the extent of involvement the owner retains with regard to the livestock and facilities. In Gill v. Comm. T.C. Memo , the Tax Court determined that self-employment tax liability applied to all payments received by two taxpayers who constructed a poultry facility that was supplied with poultry from a third party. The taxpayers received a monthly payment from the supplier of the poultry flock and were required to perform certain maintenance items, inspections and general flock management responsibilities. The Court held that rental income which was not subject to selfemployment tax, included only payments for use of space and only such services that are required to maintain the property. Further, any exemption from self-employment tax should be narrowly construed. A similar holding resulted where amounts received under a contract to grow sugar beets were subjected to self-employment tax. Schmidt v. Comm., T.C. Memo Under many contractual arrangements regarding livestock confinements, virtually all operating expenses, inventory, and overhead associated with the building are the responsibility of the tenant/producer, rather than the building owner. To avoid having the income being subjected to self-employment tax, the building owner must not participate to a significant degree or bear a substantial risk of loss. One option may be to split the contractual arrangement into two separate agreements. One agreement would be strictly for the rental of the building and a 1099 would be issued showing that this would be rental income exempt from self-employment tax. Given that the capital costs for such buildings are so large, a return on capital shown as rent should not be unreasonable. A second agreement would be entered into providing for herd/flock management. A separate 1099 for nonemployee compensation or a W-2 would be issued for any payments made under this second agreement and said payments would be subject to self-employment tax or FICA tax. If this payment is to a third party and not the owner of the facility, certainly no self-employment tax would be due as the activity of another could not be imputed to the facility owner. However, taxpayers attempting to split payments from shipping companies between lease payments and wages for driving the trucks were found to not actually lease the trucks and all income was to be treated as wage income. Escobar de Paz v. Comm., T.C. Memo , (May 26, 2000). Also see Delno v. Celebrezze, 347 F2.d 159 (9 th Cir. 1965) where the Court held income to be subject to self-employment tax where owner performed services of a substantial nature. In Tax Court Memo Decision, the Court held that rent paid by the taxpayers controlled corporation to the taxpayers, individually, at a rate of $21 per pig run through the building, was held to be subject to self-employment tax. Solvie v. Comm., T.C. Memo , (March 9, 2004). The rent paid on the new building was double the rent paid to the taxpayers on their other buildings and the rent calculation was based on the number of hogs run through the building, not strictly the number of pig spaces. The Solvies wages did not increase even though the number of hogs had increased. With high depreciation and large interest expense payments in early years creating a loss, treatment as a rental activity may not be the best from an income tax perspective. The taxpayer may prefer to offset the loss against self-employment income. QUERY: Can the taxpayer change horses in mid-stream when the building is paid for and depreciation deductions are significantly lower? For example, decrease rent (use a triple net lease) and have tenant furnish labor, management and pay for repairs?

33 FARMERS & FISHERMEN INCOME AVERAGING If you are an individual engaged in a farm business or are a fisherman (brought to us by the American Jobs Creation Act of 2004 [AJCA 04]), you are allowed to elect to average your current farm income over three prior base years to obtain the benefit of applying lower income tax rates from those prior years. Farm income averaging, although originally scheduled to be available to farmers for only 1998, 1999 and 2000, has become a permanent feature of the tax law. A farm business, for income averaging purposes, is defined by a cross-reference to IRC Sec. 263A(e)(4), as the trade or business of farming involving the cultivation of land or the raising or harvesting of any agricultural commodity and includes operating a nursery or sod farm or the raising or harvesting of trees bearing fruit, nuts or other crops or ornamental trees. The instructions for Schedule J provide that a farm business does not include contract harvesting of a commodity. Effective for tax years beginning after 7/22/08, income averaging is available for those catching, taking or harvesting (not processing) fish, mollusks, crustaceans, etc. If a taxpayer farms and fishes, the taxpayer must combine both incomes for averaging purposes. Crewmen who are paid a percentage of the catch may also average income. Taxpayers who have farm income during the tax year as a sole proprietor, a partner in a partnership or a shareholder in an S corporation may use income averaging without regard to whether the individual was engaged in a farming business in any prior year. Prop. Reg. Sec (b). Elected farm income, (EFI) which is averaged over the prior three years, is the amount of taxable income attributable to any farming business which is specifically elected by the taxpayer as subject to income averaging. Any portion of taxable income attributable to farming may be designated as elected farm income for averaging purposes, but may not exceed the taxpayers taxable income. Elected farm income may not exceed taxable income for the taxpayer and net capital gain attributable to a farming business may not exceed total net capital gain for the taxpayer. Elected farm income includes net Schedule F income, gain from the sale or disposition of property (other than land or timber) regularly used by a farmer for a substantial period in a farming business and the taxpayers share of net farm income from a partnership, LLC or Sub S Corporation. Final regulations provide that wages to a Shareholder in a Sub S Corporation engaged in farming and the landlord s share of a crop share lease may be included in elected farm income. It does not matter whether the landlord materially participates in the production of the crop. After 2003 there must be a written lease to prove the crop-share lease. The final regulations specify that elected farm income includes all income and gains less deductions and losses (including loss carryovers and carrybacks and including non-farm losses) attributable to an individual s farming business. The regulations state, however, that income, gain or loss from the sale of development rights, grazing rights and other similar rights are not treated as attributable to a farming business. A significant question has been whether elected farm income for the election year can be negative. IRS Publication 225 for the year 2015 provides in part: If your taxable income for any base year was zero because your deductions were more than income, you may have negative taxable income for that year to combine with your EFI on Schedule J.

34 The final regulations provide all allowable deductions including any NOL, are used to determine taxable income even if the result is negative. However, any negative amount that provided a benefit in another taxable year must be added back to the base year taxable amount. Therefore, NOL carried to other years and providing a benefit may not be used. [Reg (d)(2)] The regulations provide a safe harbor for the disposition of property after the cessation of farming. They state if a gain or loss (from the disposition of property) is realized after cessation of a farming business, such gain or loss is treated as attributable to a farming business if the property is sold within a reasonable time after cessation of the farming business. A sale or other disposition within one year of cessation of a farming business is presumed to be within a reasonable time. Whether a sale or other disposition that occurs more than one year after cessation of the farming business is within a reasonable time depends on all the facts and circumstances. [Reg (e)(1)(ii)(B)]. The regulations make it clear that income averaging affects only federal income tax, and has no application to employment taxes (FICA, FUTA, SECA or income tax withholding). Previously, the regulations stated that income averaging does not apply for purposes of figuring alternative minimum tax. However, Section 314(a) of the AJCA-04 provides that in calculating alternative minimum tax, regular tax liability will be determined without regard to farm income averaging. Therefore, taxpayers using income averaging will receive the full benefit of said lower tax rates. Income tax is to be determined by allocating elected farm income to the base years only after all other adjustments and determinations have been made. The regulations allow taxpayers with both ordinary income and capital gain income that are eligible for income averaging to select how much of the elected farm income is made up of capital gain or ordinary income. [Reg (e)(2)(i)]. If the elected farm income includes both ordinary income and capital gain income, the regulations provide such income must be allocated in equal portions among the tax brackets of the three prior years. Capital gains that are included in the tax bracket of a prior year do not offset capital losses from that year. They are taxed at the lesser of the capital gains rate or the ordinary income tax rates for the prior year. [Reg (d)(1)]. Net capital losses first offset net capital gains, both farm and nonfarm, before reducing ordinary income. [Reg (e)(ii), Ex. 3,4]. The rule that capital losses can only offset up to $3,000 or ordinary income per year still applies for purposes of elected farm income calculations, also. [Reg. Sec (e)(ii) Ex. 5]. Thus a taxpayer can elect to carryback only ordinary income or any combination after making these adjustments. The final regulations permit a taxpayer to make changes or revoke the election on an amended return if the statute has not expired. EXAMPLE 1: Kevin and Jane are married with no dependent children, and use the standard deduction. Kevin s Schedule F income for the year is $130,000 and their taxable income is $113,600. In the past, Kevin and Jane have been reporting taxable income in the 10%/15% bracket. Assume taxable incomes for tax years 2012, 2013 and 2014 are $16,000, $17,000 and $18,000 respectively. Each of 2012, 2013 and 2014 would need approximately $58,000 of additional taxable income to reach the top of the 10%/15% tax bracket. Kevin and Jane could elect to average all of their current farm income or gains, up to their 2015 taxable income, and keep the elected farm income in the 15% bracket. We will assume for this example that only $96,600 is averaged with approximately $38,700 being removed from the 25% bracket. This would reduce their current tax liability by approximately $38,700 of income x 10% or approximately $3,870. See Example 1 on Schedule J following, which shows actual savings totaling $3, [$19, regular tax less $16,070 Schedule J tax].

35 EXAMPLE 2: Assume Kevin and Jane had the following income for the three base years and 2015: 2012 ($50,000) (includes $30,000 NOL) 2014 $ 1, , $150,000 Also assume electable farm income for 2015 is $93,000. Kevin and Jane must eliminate the NOL from the base year 2012, therefore, base year income becomes ($20,000). Base years plus elected farm income 2012 ($20,000) + 31,000 = 11, $15, ,000 = 46, , ,000 = 32,500 Tax computations are as follows: Base year Share of Income after Income tax Income tax Add l. tax Base Income elected share of elected with farm without farm due to Year as adjusted farm income farm income income avg. income avg. EFI 2012 ($20,000) $31,000 $11,000 x 10% $1, $ 0 $1, ,000 31,000 46,000 x 10/15% $6, $1,500 4, ,500 31,000 32,500 x 10/15% $3, , Taxable Less elected Income farm income Taxable Income ,000 (93,000) 57,000 x 10/15% 7, INCOME TAX WITH INCOME AVERAGING $17, INCOME TAX WITHOUT INCOME AVERAGING 10% $ 1,845 15% 8, % 18, ,000 $29, INCOME TAX SAVINGS $29, $17, = $12,035 EXAMPLE 3: Kevin and Jane are eligible for income averaging, elect to apply Schedule J to $45,000 of income in 2013, to $60,000 of income in 2014 and $66,000 for the year Their base income for averaging must reflect the additions which occur from their prior income averaging. For example: Base Income $10,000 $10,000 $10,000 $45,000 $60,000 $66,000 EFI 13 15,000 15,000 15,000-45,000 25,000 25,000 25,000 0 EFI 14 20,000 20,000 20,000-60,000 45,000 45,000 20,000 0 EFI 15 22,000 22,000 22,000-66,000 67,000 42,000 22,000 0

36 SCHEDULE J (Form 1040) Department of the Treasury Internal Revenue Service (99) Income Averaging for Farmers and Fishermen Attach to Form 1040 or Form 1040NR. Information about Schedule J and its separate instructions is at DRAFT AS OF May 21, 2015 DO NOT FILE OMB No Attachment Sequence No. 20 Name(s) shown on return Social security number (SSN) EXAMPLE 1 1 Enter the taxable income from your 2015 Form 1040, line 43, or Form 1040NR, line ,600 2a Enter your elected farm income (see instructions). Do not enter more than the amount on line 1 2a Capital gain included on line 2a: b Excess, if any, of net long-term capital gain over net short-term capital loss b c Unrecaptured section 1250 gain c 3 Subtract line 2a from line Figure the tax on the amount on line 3 using the 2015 tax rates (see instructions) } 5 If you used Schedule J to figure your tax for: 2014, enter the amount from your 2014 Schedule J, line but not 2014, enter the amount from your 2013 Schedule J, line but not 2013 or 2014, enter the amount from your ,000 Schedule J, line 3. Otherwise, enter the taxable income from your 2012 Form 1040, line 43; Form 1040A, line 27; Form 1040EZ, line 6; Form 1040NR, line 41; or Form 1040NR-EZ, line 14. If zero or less, see instructions. 96,600 17,000 1,700 6 Divide the amount on line 2a by ,200 7 Combine lines 5 and 6. If zero or less, enter ,200 8 Figure the tax on the amount on line 7 using the 2012 tax rates (see instructions) } 9 If you used Schedule J to figure your tax for: 2014, enter the amount from your 2014 Schedule J, line but not 2014, enter the amount from your 2013 Schedule J, line ,000 Otherwise, enter the taxable income from your 2013 Form 1040, line 43; Form 1040A, line 27; Form 1040EZ, line 6; Form 1040NR, line 41; or Form 1040NR-EZ, line 14. If zero or less, see instructions. 6, Enter the amount from line , Combine lines 9 and 10. If less than zero, enter as a negative amount 11 49, Figure the tax on the amount on line 11 using the 2013 tax rates (see instructions) , If you used Schedule J to figure your tax for 2014, enter the amount from your 2014 Schedule J, line 3. Otherwise, enter the taxable income from your 2014 Form 1040, line 43; Form 1040A, line 27; Form 1040EZ, line 6; Form 1040NR, line 41; or Form 1040NR-EZ, line 14. If zero or less, see instructions , Enter the amount from line , Combine lines 13 and 14. If less than zero, enter as a negative amount 15 50, Figure the tax on the amount on line 15 using the 2014 tax rates (see instructions) , Add lines 4, 8, 12, and For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No Y Schedule J (Form 1040) ,170 Schedule J (Form 1040) 2015 Page 2 18 Amount from line , If you used Schedule J to figure your tax for: 2014, enter the amount from your 2014 Schedule J, line but not 2014, enter the amount from your 2013 Schedule J, line but not 2013 or 2014, enter the amount from your ,600 Schedule J, line 4. Otherwise, enter the tax from your 2012 Form 1040, line 44;* Form 1040A, line 28;* Form 1040EZ, line 10; Form 1040NR, line 42;* or Form 1040NR-EZ, line ,700 DRAFT AS OF May 21, } 2015 DO NOT FILE 20 If you used Schedule J to figure your tax for: 2014, enter the amount from your 2014 Schedule J, line but not 2014, enter the amount from your 2013 Schedule J, line 4. Otherwise, enter the tax from your 2013 Form 1040, line 44;* Form 1040A, line 28;* Form 1040EZ, line 10; Form 1040NR, line 42;* or Form 1040NR-EZ, line If you used Schedule J to figure your tax for 2014, enter the amount from your 2014 Schedule J, line 4. Otherwise, enter the tax from your 2014 Form 1040, line 44;* Form 1040A, line 28;* Form 1040EZ, line 10; Form 1040NR, line 42;* or Form 1040NR-EZ, line } 1,800 *Only include tax reported on this line that is imposed by section 1 of the Internal Revenue Code (see instructions). Do not include alternative minimum tax from Form 1040A. 22 Add lines 19 through , Tax. Subtract line 22 from line 18. Also include this amount on Form 1040, line 44; or Form 1040NR, line ,070 Caution: Your tax may be less if you figure it using the 2015 Tax Table, Tax Computation Worksheet, Qualified Dividends and Capital Gain Tax Worksheet, or Schedule D Tax Worksheet. Attach Schedule J only if you are using it to figure your tax. Schedule J (Form 1040) 2015

37 SCHEDULE J (Form 1040) Department of the Treasury Internal Revenue Service (99) Income Averaging for Farmers and Fishermen Attach to Form 1040 or Form 1040NR. Information about Schedule J and its separate instructions is at DRAFT AS OF May 21, 2015 DO NOT FILE OMB No Attachment Sequence No. 20 Name(s) shown on return Social security number (SSN) EXAMPLE 2 1 Enter the taxable income from your 2015 Form 1040, line 43, or Form 1040NR, line ,000 2a Enter your elected farm income (see instructions). Do not enter more than the amount on line 1 2a Capital gain included on line 2a: b Excess, if any, of net long-term capital gain over net short-term capital loss b c Unrecaptured section 1250 gain c 3 Subtract line 2a from line Figure the tax on the amount on line 3 using the 2015 tax rates (see instructions) } 5 If you used Schedule J to figure your tax for: 2014, enter the amount from your 2014 Schedule J, line but not 2014, enter the amount from your 2013 Schedule J, line but not 2013 or 2014, enter the amount from your ,000 Schedule J, line 3. Otherwise, enter the taxable income from your 2012 Form 1040, line 43; Form 1040A, line 27; Form 1040EZ, line 6; Form 1040NR, line 41; or Form 1040NR-EZ, line 14. If zero or less, see instructions. 93,000 57,000 7, Divide the amount on line 2a by ,000 7 Combine lines 5 and 6. If zero or less, enter ,000 8 Figure the tax on the amount on line 7 using the 2012 tax rates (see instructions) } 9 If you used Schedule J to figure your tax for: 2014, enter the amount from your 2014 Schedule J, line but not 2014, enter the amount from your 2013 Schedule J, line ,000 Otherwise, enter the taxable income from your 2013 Form 1040, line 43; Form 1040A, line 27; Form 1040EZ, line 6; Form 1040NR, line 41; or Form 1040NR-EZ, line 14. If zero or less, see instructions. 1, Enter the amount from line , Combine lines 9 and 10. If less than zero, enter as a negative amount 11 46, Figure the tax on the amount on line 11 using the 2013 tax rates (see instructions) , If you used Schedule J to figure your tax for 2014, enter the amount from your 2014 Schedule J, line 3. Otherwise, enter the taxable income from your 2014 Form 1040, line 43; Form 1040A, line 27; Form 1040EZ, line 6; Form 1040NR, line 41; or Form 1040NR-EZ, line 14. If zero or less, see instructions , Enter the amount from line , Combine lines 13 and 14. If less than zero, enter as a negative amount 15 32, Figure the tax on the amount on line 15 using the 2014 tax rates (see instructions) , Add lines 4, 8, 12, and , For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No Y Schedule J (Form 1040) 2015 Schedule J (Form 1040) 2015 Page 2 18 Amount from line , If you used Schedule J to figure your tax for: 2014, enter the amount from your 2014 Schedule J, line but not 2014, enter the amount from your 2013 Schedule J, line but not 2013 or 2014, enter the amount from your Schedule J, line 4. Otherwise, enter the tax from your 2012 Form 1040, line 44;* Form 1040A, line 28;* Form 1040EZ, line 10; Form 1040NR, line 42;* or Form 1040NR-EZ, line ,500 DRAFT AS OF May 21, } 2015 DO NOT FILE 20 If you used Schedule J to figure your tax for: 2014, enter the amount from your 2014 Schedule J, line but not 2014, enter the amount from your 2013 Schedule J, line 4. Otherwise, enter the tax from your 2013 Form 1040, line 44;* Form 1040A, line 28;* Form 1040EZ, line 10; Form 1040NR, line 42;* or Form 1040NR-EZ, line If you used Schedule J to figure your tax for 2014, enter the amount from your 2014 Schedule J, line 4. Otherwise, enter the tax from your 2014 Form 1040, line 44;* Form 1040A, line 28;* Form 1040EZ, line 10; Form 1040NR, line 42;* or Form 1040NR-EZ, line } 150 *Only include tax reported on this line that is imposed by section 1 of the Internal Revenue Code (see instructions). Do not include alternative minimum tax from Form 1040A. 22 Add lines 19 through , Tax. Subtract line 22 from line 18. Also include this amount on Form 1040, line 44; or Form 1040NR, line , Caution: Your tax may be less if you figure it using the 2015 Tax Table, Tax Computation Worksheet, Qualified Dividends and Capital Gain Tax Worksheet, or Schedule D Tax Worksheet. Attach Schedule J only if you are using it to figure your tax. Schedule J (Form 1040) 2015

38 EXAMPLE OF INCOME TAX TREATMENT OF CCC LOANS Consider the following example: Assume CCC loan received October 15, 2015 $10,000 Price of corn when resold 45,000 Activity I.R.C. Sec. 77 Election Made Loan Reported as Income Upon receipt of loan Report Income in 2015 of $10, Paid cash in the amount of Basis remains the same in corn $10,000 to redeem corn from CCC Corn sold in 2016 after Income of $45,000-$10,000 or redeeming corn $35,000. I.R.C. Sec. 77 Election Made Loan Not Reported as Income No entry (loan) Basis remains the same in corn Income of $35,000 TOTAL INCOME $45,000 $35,000 Due to the current grain prices and low county posted rates, no taxable gain on redemption of grain will occur. If there is a taxable gain on redemption of the grain due to the loan reduction, this will be reported on CCC 1099-G and will need to be reported on Schedule F line 6(a) and on 6(b). Other commentators may have a different opinion on handling these loans and repayments. An argument can be made that when an election has been made under I.R.C. Sec. 77 to report the loan as income, and loan is repaid, the basis of the commodity is reduced and no gain on the repayment of the loan would be recognized. See Rev. Rul , C.B. 41 and I.R.C. Sec. 1016(a)(8). When the commodity is sold the gain would be recognized by having a lower cost basis in the commodity. This difference of opinion does not change the total amount of income to be reported, but may result in a timing difference as to when it will be reported. Please review the instructions and examples as set forth in Publication 225, Farmer s Tax Guide. These instructions and examples clearly set forth authority to defer recognition of the market gain until the commodity is sold, when you have made an I.R.C. Sec. 77 election. The authors believe, however, that this reduction in the loan amount is a planned payment of the marketing assistance loan program and should be recognized at the time the loan is repaid. The sealing of the commodity and redeeming the loan for less than face value are two distinct transactions. WHEN REPORTING THE LOAN AS INCOME (ELECTION UNDER I.R.C. SEC. 77), THE FOLLOWING APPLY: 1. When the loan is received you have, in effect, sold the grain. Taxwise, it is the same as if grain was sold to the elevator. 2. If the grain is redeemed and the loan repaid, you are in effect using a planned program payment to reduce the amount of the loan and the difference should be recognized as income. 3. If the grain is redeemed and the loan is repaid, the cost basis of the grain would remain the same.