TRANSFER OF FARM ASSETS

|

|

|

- Claud Cummings

- 5 years ago

- Views:

Transcription

1 TRANSFER OF FARM ASSETS

2 Issue 1: Buying and Selling Farmland pp Cost Basis Purchase [IRC 1012] Paid in: cash, debt or other Gift [IRC 1015] Generally donor s basis

3 Issue 1: Buying and Selling Farmland p. 87 Cost Basis Inheritance [IRC 1014] FMV on DOD, or 6 months later May use IRC 2032A, special use valuation on qualifying property to reduce, no more than $1,120,000 in 2017.

4 Issue 1: Buying and Selling Farmland p. 88 Purchase Costs included in basis Real Estate Taxes paid by purchaser owed by seller. If seller reimburses, then RE taxes are deductible

5 Issue 1: Buying and Selling Farmland p. 88 Settlement Costs can be included in basis: Abstract fees Legal fees Recording fees Surveys Title Insurance

6 Issue 1: Buying and Selling Farmland p. 88 Loan Costs are not included in basis, taxpayer can amortize: Points Mortgage Insurance Loan Assumption fees Credit Report costs Fees for appraisal required by lender Fees to refinance a mortgage

7 Issue 1: Buying and Selling Farmland p. 89 Practitioner Notes Growing Crops Gain on unharvested crops sold at the same time as land is 1231 gain Option Payments Gain or loss is capital [Treas. Reg ] Unless asset is subject to 1231

8 Issue 1: Buying and Selling Farmland p. 89 Sale of Land with CRP Contract If the buyer succeeds in interest to the seller s CRP, the new owner takes over. If the buyer does not succeed, then the seller may be required to repay CRP payments received plus interest and any additional costs. USDA Notice CRP-819 provides for early termination: buyer a next gen farmer

9 Issue 2: Disposition of Converted Wetlands pp Wetland mitigation banking uses a market-based approach to restore, create, or enhance wetlands in one place to compensate for unavoidable impacts at another location.

10 Issue 2: Disposition of Converted Wetlands p. 90 Typically, mitigation banking system is administered at the state level. USDA currently recognizes eight wetland mitigation banks See list Operates at zero loss

11 IRC 1257 p. 90 Any gain on the disposition of converted wetlands or highly erodible cropland shall be treated as ordinary income. Any loss recognized (converted wetlands/erodible cropland) shall be treated as a long-term capital loss

12 Converted Wetland p. 91 Any converted wetland as defined in 1201(4) of the Food Security Act of Activities resulting in conversion Held by any other person what used land for farming purposes

13 Example 1 p. 91 Dave owns a farm on the outskirts of Sioux Falls, SD Basis is $1,800 per acre Prime for development 2012 purchases one wetland credit to drain a one acre wetland ($11,000) Cost to tile and drain the acre ($2,000)

14 Example 1 p : Dave sells 10 acres to a developer. The sale includes the one acre of converted wetland. Sale price is $15,000 per acre.

15 Example 1 p. 91 Dave reports the sale of nine acres on Form 4797, Part I. The sales price is $135,000 ($15,000 x 9 acres). His basis deduction is $16,200 ($1,800 x 9 acres).

16 Example 1 p. 91 The sale price for the converted wetland acre is $15,000. Because the gain is from the sale of a converted wetland, the gain is taxed as ordinary income. Dave reports the $200 gain ($15,000 $14,800 basis) on Form 4797.

17 Example 1 p. 91

18 Example 2 p. 92 Same facts as Example 1 except the land was sold for $11,500/Acre. Dave reports the sale of the nine acres on Form 4797, Part I.

19 Example 2 p. 92 One acre is converted wetland with a $14,800 basis. The sale of the wetland acre results in a $3,300 ($11,500 $14,800) long-term capital loss. Dave reports the loss on Form 8949, Sales and Other Dispositions of Capital Assets.

20 Example 2 p.92

21 Example 2 p. 92

22 Issue 3: Form 4797 p. 93 Form 4797 calculates both gains and losses of business property dispositions; gains and losses may come from other forms to be netted on Form 4797

23 Introduction p. 93 Capital and Ordinary transactions are separated; SE tax generally isn t applicable unless recapture of 179 or 280F deductions is required.

24 Figure 1 p. 93 Determine where to report based upon: Type of Property Holding period

25 I.R.C Property p. 93 General rule provides that net gains on business asset dispositions are capital gains, net losses are ordinary losses. The best of both worlds!!

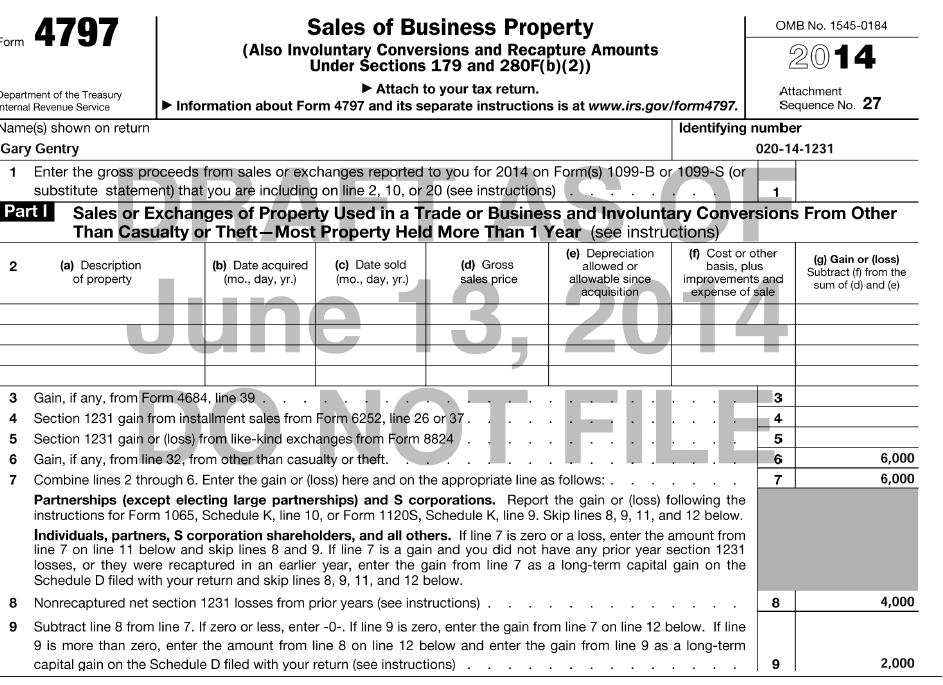

26 I.R.C Transactions p. 94 List of transactions

27 Excluded Property p. 94 List of 4 Taxpayer s Inventory Property held for sale to customers Copyright; compositions; letters U.S. gov t publication

28 Example 1 pp Josephine bought land $65K 11/15/2016 State acquired said land 11/30/2017 for $66K

29 Figure 2.1 p

30 Excluded Gain pp I.R.C gains treated as ordinary income are not included in 1231 gain netting. I.R.C treats 3 relationships as related

31 Nonrecaptured 1231 Losses p. 97 If there is a net 1231 gain in any of the 5 subsequent years following a net 1231 loss, the gain is treated as ordinary income to the extent of the prior nonrecaptured 1231 loss. Surviving spouse doesn t recapture deceased spouse s share.

32 Practitioner Note p. 97 Be aware to look back if your client has not been with you for 5 years, the software may not prompt you.

33 Example 3 p. 97 Gary Gentry facts in Figure 2.2, show gains and losses for

34

35 Depreciation Recapture p. 100 Taxpayers disposing of depreciable property resulting in a taxable transaction for 1245 and 1250 will/may recognize ordinary gains. Cross-reference 1252, 1254 and 1255 recapture

36 I.R.C Property pp I.R.C Property includes Depreciable personal property I.R.C. 167 or 168 Real property depreciated via I.R.C. 167 or 168

37 Recomputed Basis pp RB includes a property s adjusted basis plus any adjustments List of 19 allowed or allowable adjustments

38 Example 4 - Recapture pp Sandy Pitt purchased a loader in 2013 Expensed $10,000 of $120,000 cost in 2013 Used MACRS 5-year Sold for $65,000 in 2017

39 Figure 5 Realized Gain p

40 Sandy s Form 4797 p. 103

41 Practitioner Note p. 103 I.R.C. 197 Intangibles If a taxpayer acquires an intangible while disposing of another intangible at a loss; the loss can t be recognized; must increase basis of retained intangible.

42 I.R.C Recapture p property is defined to be real property that is not and has not ever been 1245 property. E.g. greenhouse is singlepurpose structure and as such is 1245 property.

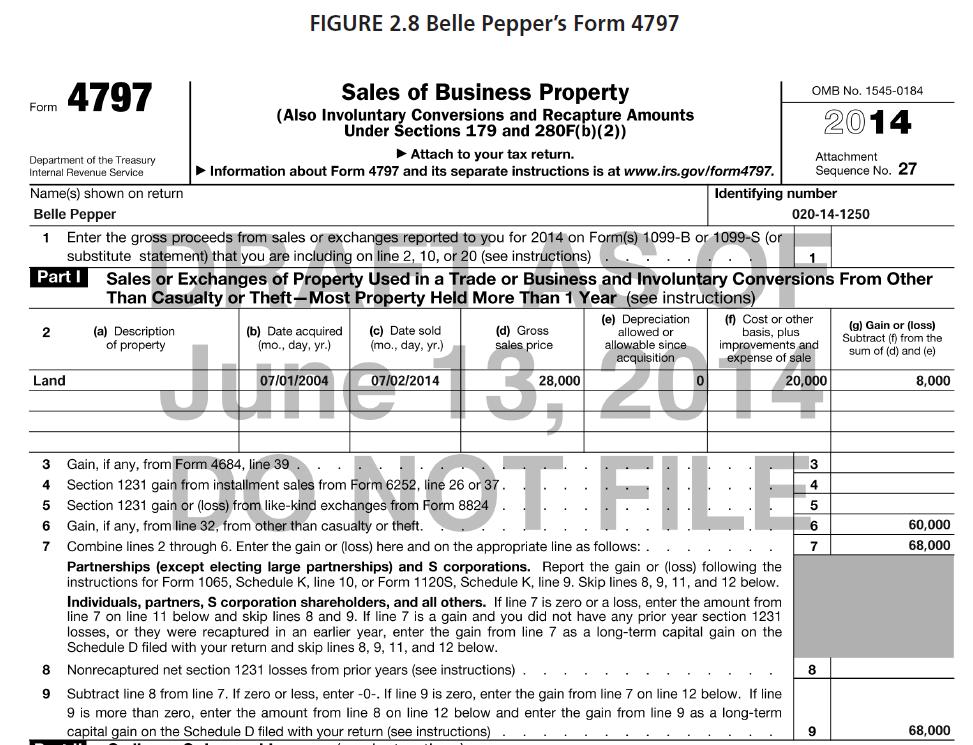

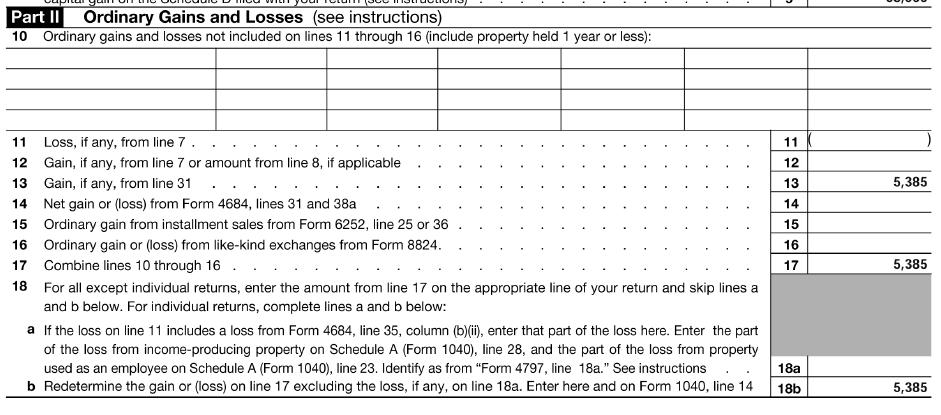

43 1250 recapture p. 104 Gain realized on a 1250 property disposition is recaptured as ordinary income. The portion of the gain which is equivalent to allowable SL depreciation is taxed at a maximum of 25% Excess gain of purchase price is 1231capital gain; taxed at max of 20%

44 Observation p. 104 Most 1250 property is depreciated using SL and is not subject to ordinary income recapture. Unrecaptured rule applies: max tax is 25%

45 Example 5 p. 104 Farm building purchased for $100,000, land $20,000 in 2007 MACRS 150% DB, over 20 year life, half-year convention Sold for $138,000 in 2017: $28K land, $110K for building

46

47

48

49

50 Belle Pepper s 4797 Continued

51 Installment Sales p. 109 When a nondealer sells business property under an installment contract rules apply to the reporting of depreciation recapture and any gain.

52 Installment Reporting p. 109 Taxpayers may use installment reporting if: Not a dealer Sale results in a gain At least one payment deferred to tax year after sale Deferred gain cannot be depreciation recapture

53 Taxable Gain Computation p. 109 Calculate and report installment income on IRS Form 6252 If property is a business asset, sale also reported on Form 4797

54 Taxable Gain Computation p. 109 Other issues Charge interest, report on Schedule B Gain calculated using ordinary and capital gains rules and rates when payment received Holding period ends at time of sale, no change ST to LT

55 Depreciation Recapture p. 109 Only 1231 gains may be reported on the installment method 1245 and 1250 recapture is calculated and recognized in the year of sale, report on Form 4797

56 Example 6 pp Fred Fabricator retired and sells machinery to Bert Builder for $320,000. $100,000 down $44,000 annually plus interest Over next 5 years, begin 2018

57

58 Example 6 (Continued) pp See Forms 4797 and 6252

59 I.R.C. 179 Recapture p. 115 If property, which the taxpayer expensed, falls below 50% business use by the taxpayer, recapture of the excess amount that was expensed over allowable deductions without 179 expensing.

60 Example 7 p. 115 In 2017 Whitney reduced business use of the boat to 40%. She must recapture $4,032. This subject to SE tax

61

62

63 I.R.C. 280F Listed Property Recapture p. 116 Listed property subject to MACRS that is used for more than 50% in qualifying business use is eligible for both accelerated depreciation 179 expense deduction. If use falls below 50%, only SL depreciation is allowed, excess must be recaptured.

64 Example 8 p. 117 Rita bought a computer for $4,000 in 2015 for both personal and business use. Business use was 70% $2,800 business basis $1,000 of that expensed, $1,800 MACRS 5-year prop.

65 Example 8 continued In 2017, Rita s business use drops to 20%. Therefore, she must recapture 179 deduction and recalculate under MACRS SL method.

66

67

68 Issue 4: Livestock Transactions pp Livestock acquisition Livestock sales Casualty gain or loss

69 Livestock acquisition pp Reason for acquiring determines treatment Example 1: Purchased for resale Sale price $13,000 Purchase price - 8,000 Gain $ 5,000

70 Depreciation pp Depreciation begins when first placed in service for intended use Immature livestock IRS says When draft animals can be worked When dairy animals can be milked When breeding animals can bred Taxpayers could argue depreciation begins when dairy animals can be bred

71 Example 2: Placed in Service p. 120

72 Livestock sales pp Purpose for holding livestock determines where a sale is reported. Held for sale: Schedule F (Form 1040) Dairy, breeding, sport, or draft: Form 4797 < 12 (24) months: Form 4797, Part II > 12 (24) months: Depreciated: Form 4797, Part III Not depreciated: Form 4797, Part I

73 Example 3: Dairy livestock pp Calves held for sale $12,150 Raised cows $48,600 Purchased cows $ 6,800 Culled heifers $8,500 Schedule F, line 2: 12,150 Form 4797, line 2: 48,600 Form 4797, line 10: 8,500

74 Form 4797 p. 124 Line 20 6,800 Line 21 15,000 Line 22 15,000 Line 23 0 Line 24 6,800 Line 25a 15,000 Line 25b, 30, 31, 13 6,800

75 Casualty gain or loss pp Dairy, breeding, sport, or draft livestock is treated the same as other trade or business property: Loss is decrease in FMV (limited to basis) Gain is insurance or government payments in excess of basis

76 Example 4: Dairy Livestock pp Cost FMV Insur. Basis 2 raised cows 0 2,200 2,000 0 Purchased cow 2,100 1,100 1,000 0 Purchased cow 2,100 1,100 1,000 1,029

77 Form 4684 p. 125 A B C Line 20 1,029 Line 21 2,000 1,000 1,000 Line 22 2,000 1,000 Line 23 1,100 Line 24 0 Line 25 1,100 Line 26 1,029 Lines 27 & 28 29

78 I.R.C Netting p. 127 Net casualty gains are netted with other I.R.C gains (unless they are deferred) Net casualty losses are ordinary deduction

79 Example 5: Casualty gain deferred pp Insurance proceeds received $3,000 Adjusted tax basis - 0 Gain realized $3,000 Gain deferred - 3,000 Gain recognized $ 0 Cost of replacement property $4,500 Gain deferred - 3,000 Basis of replacement property $1,500

80 Property held for sale pp Generally, no special tax treatment of involuntary conversion Reimbursements reported on Schedule F Usually no gain or loss because items have zero basis

81 Weather-related provisions Two provisions pp Involuntary conversion (applies only to draft, breeding, or dairy animals) 1-year postponement of gain (applies to all livestock)

82 Involuntary Conversion pp Sale must be due to weather conditions (disaster declaration is not required) Replaced within 2 years New livestock used for same purpose (breeding, dairy, or draft) Applies only to sales in excess of normal Must attach a statement to tax return

83 1-year deferral p. 130 Must be disaster declaration Applies only to sales in excess of normal Must attach statement to tax return

84 Livestock deaths due to disease pp Not a casualty because not sudden It is an involuntary conversion Section 1231 property gain or loss is netted with other section 1231 gains and losses Reported on Schedule F or Form 4797

85 Issue 6: Inherited Property pp Basis of inherited property is adjusted to the value on the date of death or alternate valuation date Automatic long-term capital gain holding period Exception: income in respect of a decedent (IRD)

86 Example 1: Growing crops pp

87 Example 2 p. 135 Date-of-death basis adjustment for equipment Does receive a step up in basis Combine not eligible for Section 179

88 Issue 7: Casualty Gains and Losses pp

89 Home p. 138 Form 4684 Line 2 55,000 Line 3 150,000 Line 4 95,000

90 Home p. 141 Form 8949 Line 2-95,000 Schedule D Line 10-95,000 Line 11 95,000 Line 16 0

91 Cropland: Form 4684 p. 139 Line 23 7,000,000 Line 24 6,880,000 Line ,000 Line ,000 Line ,000 Line ,000 Line 38a - 120,000

92 Form 4684 Section B p. 139 Bins Shed Equip. Line 20 15,000 29,250 0 Line 21 50,000 45,000 40,000 Line 22 35,000 15,750 40,000 Lines 29, 30, and 31 15,750

93 Form 4797 p. 140 Line 13 75,000 Line ,250 Line 17-29,750

94 Issue 9: Going Out of Business Case Study p. 143 Tax consequences are dramatically different from one plan to another This issue compares the tax cost of alternatives

95 Business assets p. 144 FMV $1,261,000 Basis - 258,475 Gain $1,002, $ 417, $ 585,250

96 Lump-sum sale pp Income tax $294,810 SE tax 8,554 Total tax $303,364

97 Sale over 2 years pp Income tax $263,352 SE tax 8,554 Total tax $271,906

98 Installment sale of non-deprec. property pp Income tax $278,822 SE tax 8,554 Total tax $287,376

99 Sale of deprec. property over 10 years pp Income tax $257,969 SE tax 8,554 Total tax $266,523

100 Summary p. 152 Total Tax After Tax Inc. Lump-sum sale $303,364 $1,383,463 Sale over 2 years $271,906 $1,390,436 Installment sale $287,376 $1,584,507 Sale over 10 years $266,523 $1,586,627

101

102 Break Time Back to work in 10 minutes

Form 4797 Chapter 3 pp Agricultural Tax Issues

Form 4797 Chapter 3 pp. 85-118 2018 Agricultural Tax Issues Form 4797 Page 85 Reporting of gains and losses on the disposition of business property. The collection point for gains and losses reported elsewhere.

Form 4797 Chapter 3 pp. 85-118 2018 Agricultural Tax Issues Form 4797 Page 85 Reporting of gains and losses on the disposition of business property. The collection point for gains and losses reported elsewhere.

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

Willie and Annette Jump (Example 3.1)

") agreement, check here Part II Explanation of Changes to Income, Deductions, and Credits Enter the line number from the front of the form for each item you are changing and give the reason for each change.

agreement, check here Part II Explanation of Changes to Income, Deductions, and Credits Enter the line number from the front of the form for each item you are changing and give the reason for each change.

Agricultural & Natural Resource Issues Chapter 10 pp National Income Tax Workbook

Agricultural & Natural Resources Tax Issues Chris Bruynis David Marrison Barry Ward Associate Professor Associate Professor Assistant Professor bruynis.1@osu.edu marrison.2@osu.edu ward.8@osu.edu 740-702-3200

Agricultural & Natural Resources Tax Issues Chris Bruynis David Marrison Barry Ward Associate Professor Associate Professor Assistant Professor bruynis.1@osu.edu marrison.2@osu.edu ward.8@osu.edu 740-702-3200

AGRICULTURAL TAX. i n c o m e t a x e s

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

Reporting Installment Sales and Repossessions

Reporting Installment Sales and Repossessions GAIL ABBOTT, EA FOR BLUE RIDGE CHAPTER OF VIRGINIA SOCIETY OF ENROLLED AGENTS OCTOBER 19, 2016 What is an Installment Sale? Sale of Property where you receive

Reporting Installment Sales and Repossessions GAIL ABBOTT, EA FOR BLUE RIDGE CHAPTER OF VIRGINIA SOCIETY OF ENROLLED AGENTS OCTOBER 19, 2016 What is an Installment Sale? Sale of Property where you receive

Q&A: Tax Options for Drought Sales of Livestock

Q&A: Tax Options for Drought Sales of Livestock If a producer is forced to sell livestock, in excess of normal levels, due to shortages of water, feed or other consequences of drought, the income tax on

Q&A: Tax Options for Drought Sales of Livestock If a producer is forced to sell livestock, in excess of normal levels, due to shortages of water, feed or other consequences of drought, the income tax on

Income Tax Management for Farmers in 2011

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

2015 CALT Tax Schools Day 2. Contact Information. Day 2 Topics 12/15/2015. Dave Repp. Paul Neiffer.

2015 CALT Tax Schools Day 2 David Repp and Paul Neiffer Contact Information Dave Repp drepp@dickinsonlaw.com Paul Neiffer Paul.neiffer@claconnect.com 509 823 2920 www.farmcpatoday.com @farmcpa Day 2 Topics

2015 CALT Tax Schools Day 2 David Repp and Paul Neiffer Contact Information Dave Repp drepp@dickinsonlaw.com Paul Neiffer Paul.neiffer@claconnect.com 509 823 2920 www.farmcpatoday.com @farmcpa Day 2 Topics

Tax Considerations of Farm Transfers (Revised 26 February 2009)

") Tax Considerations of Farm Transfers (Revised 26 February 2009) Introduction There are alternative methods of transferring farm assets from one generation to the next. The most common methods are by sale,

Tax Considerations of Farm Transfers (Revised 26 February 2009) Introduction There are alternative methods of transferring farm assets from one generation to the next. The most common methods are by sale,

Weather-Related Sales of Livestock

RTE/2016-10 Revised September 2016 Introduction Weather-Related Sales of Livestock JC Hobbs, Assistant Extension Specialist Department of Agriculture Economics, Oklahoma State University There are two

RTE/2016-10 Revised September 2016 Introduction Weather-Related Sales of Livestock JC Hobbs, Assistant Extension Specialist Department of Agriculture Economics, Oklahoma State University There are two

Instructions for Form 4797

2017 Instructions for Form 4797 Sales of Business Property (Also Involuntary Conversions and Recapture Amounts Under Sections 179 and 280F(b)(2)) Department of the Treasury Internal Revenue Service Section

2017 Instructions for Form 4797 Sales of Business Property (Also Involuntary Conversions and Recapture Amounts Under Sections 179 and 280F(b)(2)) Department of the Treasury Internal Revenue Service Section

DAMAGED, DESTROYED, OR STOLEN PROPERTY

CHAPTER 8 DAMAGED, DESTROYED, OR STOLEN PROPERTY SYNPOSIS (click on section title to go directly there) Introduction... 8.1 General Rules... 8.2 Casualty and Theft Losses... 8.2 Personal-Use Property...

CHAPTER 8 DAMAGED, DESTROYED, OR STOLEN PROPERTY SYNPOSIS (click on section title to go directly there) Introduction... 8.1 General Rules... 8.2 Casualty and Theft Losses... 8.2 Personal-Use Property...

CHAPTER 3 FARM INCOME

MANAGING THE TIMING OF INCOME AND DEDUCTIONS CHAPTER 3 SYNPOSIS (click on section title to go directly there) Introduction... 3.2 Defining Farm and Farming... 3.2 Definition of Farm... 3.2 Definition of

MANAGING THE TIMING OF INCOME AND DEDUCTIONS CHAPTER 3 SYNPOSIS (click on section title to go directly there) Introduction... 3.2 Defining Farm and Farming... 3.2 Definition of Farm... 3.2 Definition of

Weather-Related Sales of Livestock

August 2010 RTE/2010-09 Weather-Related Sales of Livestock Introduction JC Hobbs, Assistant Extension Specialist Department of Agriculture Economics, Oklahoma State University There are two provisions

August 2010 RTE/2010-09 Weather-Related Sales of Livestock Introduction JC Hobbs, Assistant Extension Specialist Department of Agriculture Economics, Oklahoma State University There are two provisions

TABLE OF CONTENTS SECTION I FARM PROBLEMS & EXAMPLES. Installment Contracts and Deferred Grain Contracts

TABLE OF CONTENTS SECTION I FARM PROBLEMS & EXAMPLES Page Installment Contracts and Deferred Grain Contracts... 1-2 Example of Reporting an Installment Sale (Example-Forms)... 3-6 Example of Taxpayer s

TABLE OF CONTENTS SECTION I FARM PROBLEMS & EXAMPLES Page Installment Contracts and Deferred Grain Contracts... 1-2 Example of Reporting an Installment Sale (Example-Forms)... 3-6 Example of Taxpayer s

Installment Sales. Contents. For use in preparing 2012 Returns. Publication 537 Cat. No V. Future Developments. Reminder.

Department of the Treasury Internal Revenue Service Publication 537 Cat. No. 15067V Installment Sales For use in preparing 2012 Returns Contents Future Developments... 1 Reminder... 1 Introduction... 1

Department of the Treasury Internal Revenue Service Publication 537 Cat. No. 15067V Installment Sales For use in preparing 2012 Returns Contents Future Developments... 1 Reminder... 1 Introduction... 1

10/26/2017. Farm Income. Introduction. Defining Farming

Farm Income Kristy Maitre Tax Specialist Materials Complied by Kristine Tidgren Center for Agricultural Law and Taxation October 26, 2017 Introduction Preparing tax returns for farmers and ranchers requires

Farm Income Kristy Maitre Tax Specialist Materials Complied by Kristine Tidgren Center for Agricultural Law and Taxation October 26, 2017 Introduction Preparing tax returns for farmers and ranchers requires

Capital Gains and Losses

Capital Gains and Losses Table of Contents Chapter 1: Basis Of Property... 2 I. Introduction... 2 II. Cost Basis... 2 III. Adjusted Basis... 4 IV. Basis Other Than Cost... 5 Chapter 2: Sale Of Property...

Capital Gains and Losses Table of Contents Chapter 1: Basis Of Property... 2 I. Introduction... 2 II. Cost Basis... 2 III. Adjusted Basis... 4 IV. Basis Other Than Cost... 5 Chapter 2: Sale Of Property...

INCOME TAX MANAGEMENT FOR FARMERS IN George F. Patrick Department of Agricultural Economics Purdue University

INCOME TAX MANAGEMENT FOR FARMERS IN 2007 George F. Patrick Department of Agricultural Economics Purdue University CES Paper No. 364-W December 2007 INCOME TAX MANAGEMENT FOR FARMERS IN 2007 Table of Contents

INCOME TAX MANAGEMENT FOR FARMERS IN 2007 George F. Patrick Department of Agricultural Economics Purdue University CES Paper No. 364-W December 2007 INCOME TAX MANAGEMENT FOR FARMERS IN 2007 Table of Contents

Issue 5: Marijuana and Hemp Taxation p. 40. Hemp uses: Paper Fiber Hemp Oil Hemp Rope Hemp Fabric Marijuana uses: Recreation Medicinal

Issue 5: Marijuana and Hemp Taxation p. 40 Hemp uses: Paper Fiber Hemp Oil Hemp Rope Hemp Fabric Marijuana uses: Recreation Medicinal State Laws p. 40 Many states allow medical and recreational use of

Issue 5: Marijuana and Hemp Taxation p. 40 Hemp uses: Paper Fiber Hemp Oil Hemp Rope Hemp Fabric Marijuana uses: Recreation Medicinal State Laws p. 40 Many states allow medical and recreational use of

INCOME TAX MANAGEMENT FOR FARMERS IN 2011

INCOME TAX MANAGEMENT FOR FARMERS IN 2011 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2011 DRAFT 2011 version has not been peer-reviewed. Comments are welcome.

INCOME TAX MANAGEMENT FOR FARMERS IN 2011 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2011 DRAFT 2011 version has not been peer-reviewed. Comments are welcome.

TAX REPORTING AND PAYMENT

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

2002 Instructions for Schedule F, Profit or Loss From Farming

2002 Instructions for Schedule F, Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1041, 1065, or 1065-B. This activity may subject you

2002 Instructions for Schedule F, Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1041, 1065, or 1065-B. This activity may subject you

2001 Instructions for Schedule D, Capital Gains and Losses

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

1998 Instructions for Schedule D, Capital Gains and Losses

1998 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report: The sale or exchange of a capital asset (defined on this page). Gains from involuntary conversions (other

1998 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report: The sale or exchange of a capital asset (defined on this page). Gains from involuntary conversions (other

U.S. Income Tax Return for an S Corporation

Form Department of the Treasury Internal Revenue Service () Paid Preparer Use Only Caution: Include only trade or business income and expenses on lines 1a through 21. See the instructions for more information.

Form Department of the Treasury Internal Revenue Service () Paid Preparer Use Only Caution: Include only trade or business income and expenses on lines 1a through 21. See the instructions for more information.

2002 Instructions for Schedule D, Capital Gains and Losses

2002 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2002 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

1. Determination of gain or loss. 2. Basis considerations. 3. Definition of a capital asset. 6. Sale or exchange. 7.

Outline 1 Unit09. Property Transactions: Capital Gains and Losses (PAK Chap. 5) This unit examines the tax consequences of property transactions. A property transaction includes sale, exchange, or abandonment

Outline 1 Unit09. Property Transactions: Capital Gains and Losses (PAK Chap. 5) This unit examines the tax consequences of property transactions. A property transaction includes sale, exchange, or abandonment

Basis Rules, Depreciation, and Asset Categorization Chapter 10

Basis Rules, Depreciation, and Asset Categorization Chapter 10 Tax is levied on income, not capital Capital is income that has already been taxed The Tax Toll-Booth 10-2 Gains must be realized before they

Basis Rules, Depreciation, and Asset Categorization Chapter 10 Tax is levied on income, not capital Capital is income that has already been taxed The Tax Toll-Booth 10-2 Gains must be realized before they

Balance Sheets- step one for your 2018 farm analysis

Page 1 of 21 Name Address Phone Email Balance Sheets- step one for your 2018 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and

Page 1 of 21 Name Address Phone Email Balance Sheets- step one for your 2018 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and

Balance Sheets- step one for your 2016 farm analysis

1 of 12 Name Address Phone Email Balance Sheets- step one for your 2016 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and what

1 of 12 Name Address Phone Email Balance Sheets- step one for your 2016 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and what

Farm Tax Update 1/21/2019. Teaching Objectives. Circular 230 Disclosure. Thank You Farmers Tax Guide

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Ag Income Tax Update for Farm Families

Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Extension Educator Gary A. Hachfeld, Extension Educator January 2010 Introduction: For tax years 2009 and 2010, there are a number

Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Extension Educator Gary A. Hachfeld, Extension Educator January 2010 Introduction: For tax years 2009 and 2010, there are a number

Unit10. Property Transactions - Nontaxable Exchanges (PAK Chap. 12)

") 1 Unit10. Property Transactions - Nontaxable Exchanges (PAK Chap. 12) The transactions examined in this chapter overrides the normal rule that provides for the recognition of realized gains and realized

1 Unit10. Property Transactions - Nontaxable Exchanges (PAK Chap. 12) The transactions examined in this chapter overrides the normal rule that provides for the recognition of realized gains and realized

1. Like-Kind Exchanges. 2. Involuntary Conversions. 3. Sale of Principal Residence. 4. Tax Planning Considerations

Outline 1 Unit10. Property Transactions - Nontaxable Exchanges (PAK Chap. 12) The transactions examined in this chapter overrides the normal rule that provides for the recognition of realized gains and

Outline 1 Unit10. Property Transactions - Nontaxable Exchanges (PAK Chap. 12) The transactions examined in this chapter overrides the normal rule that provides for the recognition of realized gains and

SUBMITTED FOR THE HEARING RECORD UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS

SUBMITTED FOR THE HEARING RECORD UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS HOW TAX REFORM WILL GROW OUR ECONOMY AND CREATE JOBS MAY 18, 2017 Submitted By: The American Farm Bureau

SUBMITTED FOR THE HEARING RECORD UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS HOW TAX REFORM WILL GROW OUR ECONOMY AND CREATE JOBS MAY 18, 2017 Submitted By: The American Farm Bureau

TABLE OF CONTENTS. General Rules

T41 1/18 10-1 10 Interest and Taxes TABLE OF CONTENTS KEY ISSUE DESCRIPTION PAGE Introduction... 10-1 10A Investment Interest Expense... 10-2 General Rules... 10-2 Reporting Deductible Investment Interest...

T41 1/18 10-1 10 Interest and Taxes TABLE OF CONTENTS KEY ISSUE DESCRIPTION PAGE Introduction... 10-1 10A Investment Interest Expense... 10-2 General Rules... 10-2 Reporting Deductible Investment Interest...

Knowledge Exchange Report

Farm Credit East October 2012 Knowledge Exchange Report The Federal Estate Tax Effect on the Farming Community Everyone will die at some point. Whether their estate is subject to the Federal Estate Tax

Farm Credit East October 2012 Knowledge Exchange Report The Federal Estate Tax Effect on the Farming Community Everyone will die at some point. Whether their estate is subject to the Federal Estate Tax

Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

OTHER TOOLS TO MANAGE TAX LIABILITY

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

SEGREGATING FERTILITY COSTS BY PHILIP E. HARRIS, ISU VISITING PROFESSOR

SEGREGATING FERTILITY COSTS BY PHILIP E. HARRIS, ISU VISITING PROFESSOR Tax rules require the purchase price of land to be allocated among the land and the various assets that are purchased with the land,

SEGREGATING FERTILITY COSTS BY PHILIP E. HARRIS, ISU VISITING PROFESSOR Tax rules require the purchase price of land to be allocated among the land and the various assets that are purchased with the land,

Farmer and Farmland Owner Income Tax Webinar. Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension

Farmer and Farmland Owner Income Tax Webinar Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension Chris Bruynis Circular 230 Disclosure The information provided in this presentation is for educational

Farmer and Farmland Owner Income Tax Webinar Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension Chris Bruynis Circular 230 Disclosure The information provided in this presentation is for educational

Depreciation i for tax purposes is not the same as depreciation for management decisions or

Depreciation i for tax purposes is not the same as depreciation for management decisions or accounting. Non cash event but still reduces taxable income Flexibility in calculating it Can be used to level

Depreciation i for tax purposes is not the same as depreciation for management decisions or accounting. Non cash event but still reduces taxable income Flexibility in calculating it Can be used to level

Post-Mortem Planning Steve R. Akers

Post-Mortem Planning Steve R. Akers Bessemer Trust Dallas, Texas akers@bessemer.com Copyright 2012 by Bessemer Trust Company, N.A. All rights reserved I. PLANNING ISSUES FOR 2010 DECEDENTS A. Default Rule

Post-Mortem Planning Steve R. Akers Bessemer Trust Dallas, Texas akers@bessemer.com Copyright 2012 by Bessemer Trust Company, N.A. All rights reserved I. PLANNING ISSUES FOR 2010 DECEDENTS A. Default Rule

Specialty Estate Tax Seminar for Farm Families Paul Neiffer, CPA CliftonLarsonAllen, LLP

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP CLAconnect.com Specialty Estate Tax Seminar for Farm Families Paul Neiffer, CPA CliftonLarsonAllen, LLP Speaker Introduction Paul Neiffer, Principal,

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP CLAconnect.com Specialty Estate Tax Seminar for Farm Families Paul Neiffer, CPA CliftonLarsonAllen, LLP Speaker Introduction Paul Neiffer, Principal,

Presented by: Peggy Hall, Legacy Accounting and Software Training Sponsored by: KCAA (Kitsap Community and Agricultural Alliance) WSU Regional Small

WSU Regional Small") Presented by: Peggy Hall, Legacy Accounting and Software Training Sponsored by: KCAA (Kitsap Community and Agricultural Alliance) WSU Regional Small Farms Program Useful Resources Start Up Decisions/Farm

Presented by: Peggy Hall, Legacy Accounting and Software Training Sponsored by: KCAA (Kitsap Community and Agricultural Alliance) WSU Regional Small Farms Program Useful Resources Start Up Decisions/Farm

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University Tax Planning

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

Instructions for Form 4562

2017 Instructions for Form 4562 Department of the Treasury Internal Revenue Service Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue

2017 Instructions for Form 4562 Department of the Treasury Internal Revenue Service Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue

Fertilizer or Nutrients Acquired with Land. By:

Fertilizer or Nutrients Acquired with Land By: Philip E. Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison and University of Wisconsin-Extension and Guido van der

Fertilizer or Nutrients Acquired with Land By: Philip E. Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison and University of Wisconsin-Extension and Guido van der

Tax Planning. and. Management Considerations. for Farmers in George F. Patrick Extension Agricultural Economist Purdue University

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

2017 Farm Income Tax Webinar

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite W Sixth St Media, PA Adjunct Professor - Villanova Law

, CPA Partner - Gibson&Perkins, PC Suite W Sixth St Media, PA Adjunct Professor - Villanova Law") EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite 204-100 W Sixth St Media, PA 19063 Adjunct Professor - Villanova Law School Graduate Tax Program Telephone : 610-565-1708 e-mail

EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite 204-100 W Sixth St Media, PA 19063 Adjunct Professor - Villanova Law School Graduate Tax Program Telephone : 610-565-1708 e-mail

Selling Your Home. Contents. Important Change for Important Reminders. Publication 523 Cat. No W. For use in preparing 1998 Returns

Department of the Treasury Internal Revenue Service Publication 523 Cat. No. 15044W Selling Your Home For use in preparing 1998 Returns Contents Introduction... 2 Chapter 1. Main Home... 2 Chapter 2. Rules

Department of the Treasury Internal Revenue Service Publication 523 Cat. No. 15044W Selling Your Home For use in preparing 1998 Returns Contents Introduction... 2 Chapter 1. Main Home... 2 Chapter 2. Rules

AGROFORESTRY IN ACTION

AGROFORESTRY IN ACTION AF1004-2007 Tax Considerations for the Establishment of Agroforestry Practices by Larry D. Godsey, Economist, University of Missouri Center for Agroforestry Agroforestry is an integrated

AGROFORESTRY IN ACTION AF1004-2007 Tax Considerations for the Establishment of Agroforestry Practices by Larry D. Godsey, Economist, University of Missouri Center for Agroforestry Agroforestry is an integrated

Chapter 4. Cost Considerations

Chapter 4. Cost Considerations In general, forest-related expenditures may be classified for Federal income tax purposes as one of three types: (1) capital costs, which comprise basis these costs include

Chapter 4. Cost Considerations In general, forest-related expenditures may be classified for Federal income tax purposes as one of three types: (1) capital costs, which comprise basis these costs include

AGRICULTURAL FINANCIAL AND TAX PLANNING. Self Employment Tax on Ranch Related Income

AGRICULTURAL FINANCIAL AND TAX PLANNING Self Employment Tax on Ranch Related Income By Thomas J. Bryant, CPA and Ryan Beasley, CPA In last months article we mentioned a February 27, 2017, Internal Revenue

AGRICULTURAL FINANCIAL AND TAX PLANNING Self Employment Tax on Ranch Related Income By Thomas J. Bryant, CPA and Ryan Beasley, CPA In last months article we mentioned a February 27, 2017, Internal Revenue

General Rule Capital Gain or Loss. Sec Example 12-1 Sale. General rule: a sale by a partner generates capital gain or loss.

General Rule Capital Gain or Loss Sec. 741 12-3 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses. Same for: Sale

General Rule Capital Gain or Loss Sec. 741 12-3 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses. Same for: Sale

Conservation-Related Payments and Expenditures

August 2012 RTE/2012-36 Conservation-Related Payments and Expenditures George Patrick, Professor Emeritus Department of Agricultural Economics, Purdue University Introduction Concerns about soil erosion,

August 2012 RTE/2012-36 Conservation-Related Payments and Expenditures George Patrick, Professor Emeritus Department of Agricultural Economics, Purdue University Introduction Concerns about soil erosion,

Tax implications of Hurricane Michael related timber casualty losses

Tax implications of Hurricane Michael related timber casualty losses Yanshu Li, Ph.D. Assistant Professor of Forest Taxation and Economics Yanshu.Li@uga.edu 706-542-2460 Outline Federal income taxes casualty

Tax implications of Hurricane Michael related timber casualty losses Yanshu Li, Ph.D. Assistant Professor of Forest Taxation and Economics Yanshu.Li@uga.edu 706-542-2460 Outline Federal income taxes casualty

INCOME TAX MYTHS, TRUTHS, AND EXAMPLES CONCERNING FARM PROPERTY DISPOSITIONS

Revised October 1996 E.B.96-17 INCOME TAX MYTHS, TRUTHS, AND EXAMPLES CONCERNING FARM PROPERTY DISPOSITIONS by Stuart F. Smith Department of Agricultural, Resource, and Managerial Economics College of

Revised October 1996 E.B.96-17 INCOME TAX MYTHS, TRUTHS, AND EXAMPLES CONCERNING FARM PROPERTY DISPOSITIONS by Stuart F. Smith Department of Agricultural, Resource, and Managerial Economics College of

Tax Implications of Farm Financial Planning Decisions

Tax Implications of Farm Financial Planning Decisions Kevin L. Herbel Kansas Farm Management Association Department of Agricultural Economics Kansas State University Appreciation Expressed to Rob Holcomb,

Tax Implications of Farm Financial Planning Decisions Kevin L. Herbel Kansas Farm Management Association Department of Agricultural Economics Kansas State University Appreciation Expressed to Rob Holcomb,

Financial Resources Available to Beginning Farmers. Peyton Fair Farm Credit Mid-America Les Humpal UT Extension Danny Morris UT Extension

Financial Resources Available to Beginning Farmers Peyton Fair Farm Credit Mid-America Les Humpal UT Extension Danny Morris UT Extension Financial Resources There are several sources of financial resources

Financial Resources Available to Beginning Farmers Peyton Fair Farm Credit Mid-America Les Humpal UT Extension Danny Morris UT Extension Financial Resources There are several sources of financial resources

Davis & associates, p.a. Certified Public Accountants and Consultants

209 FEDERAL TAX RATES Davis & Associates, p.a. Certified Public Accountants and Consultants 97 Washingtonian Boulevard, Suite 550 Gaithersburg, Maryland 20878 Phone: 30.963.6696 Fax: 30.963.6693 www.daviscpas.com

209 FEDERAL TAX RATES Davis & Associates, p.a. Certified Public Accountants and Consultants 97 Washingtonian Boulevard, Suite 550 Gaithersburg, Maryland 20878 Phone: 30.963.6696 Fax: 30.963.6693 www.daviscpas.com

Involuntary Conversion of Business Assets

RTE/2016-03 Revised July 2016 Involuntary Conversion of Business Assets Introduction Guido van der Hoeven, Extension Specialist/Senior Lecturer Department of Agricultural and Resource Economics, NC State

RTE/2016-03 Revised July 2016 Involuntary Conversion of Business Assets Introduction Guido van der Hoeven, Extension Specialist/Senior Lecturer Department of Agricultural and Resource Economics, NC State

CH.15 Non-Donative Property Transfers

CH.15 Non-Donative Property Transfers 1) Intrafamily installment sales 2) Gift-leaseback arrangements 3) Tax-free exchanges with family members 4) Private annuities with family members 5) Grantor retained

CH.15 Non-Donative Property Transfers 1) Intrafamily installment sales 2) Gift-leaseback arrangements 3) Tax-free exchanges with family members 4) Private annuities with family members 5) Grantor retained

Record Keeping 101. Small and Beginning Farmers Workshop Milledgeville, GA February Ag & Applied Economics

Record Keeping 101 Small and Beginning Farmers Workshop Milledgeville, GA February 2014 Overview of Today Why keep records Production records Financial records Five easy steps to record keeping Schedule

Record Keeping 101 Small and Beginning Farmers Workshop Milledgeville, GA February 2014 Overview of Today Why keep records Production records Financial records Five easy steps to record keeping Schedule

PUBLIC INSPECTION COPY

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2011

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2011

Timber Taxation. Why forestry is unique. Dr. Tamara L. Cushing Diboll, TX February 7, 2017

Timber Taxation Dr. Tamara L. Cushing Diboll, TX February 7, 2017 Why forestry is unique O Is it agriculture? O Long-time horizon O Spread-out cash flows O Derived demand O Location dependent 1 What do

Timber Taxation Dr. Tamara L. Cushing Diboll, TX February 7, 2017 Why forestry is unique O Is it agriculture? O Long-time horizon O Spread-out cash flows O Derived demand O Location dependent 1 What do

Disaster Losses and Related Tax Rules

Utah State University DigitalCommons@USU Rural Tax Education Archived USU Extension Publications 9-2017 Disaster Losses and Related Tax Rules JC Hobbs Oklahoma State University Follow this and additional

Utah State University DigitalCommons@USU Rural Tax Education Archived USU Extension Publications 9-2017 Disaster Losses and Related Tax Rules JC Hobbs Oklahoma State University Follow this and additional

CHARITABLE PLANNING. Illinois State Bar Association Trust & Estate Section Estate Planning: Hot Topics. Chicago, Illinois October 10, 2013

CHARITABLE PLANNING Illinois State Bar Association Trust & Estate Section Estate Planning: Hot Topics Chicago, Illinois October 10, 2013 James A. Nepple Nepple Law, PLC 1515 Fifth Avenue, Suite 320 Moline,

CHARITABLE PLANNING Illinois State Bar Association Trust & Estate Section Estate Planning: Hot Topics Chicago, Illinois October 10, 2013 James A. Nepple Nepple Law, PLC 1515 Fifth Avenue, Suite 320 Moline,

CH.15 Non-Donative Property Transfers

CH.15 Non-Donative Property Transfers 1) Intrafamily installment sales 2) Gift-leaseback arrangements 3) Tax-free exchanges with family members 4) Private annuities with family members 5) Grantor retained

CH.15 Non-Donative Property Transfers 1) Intrafamily installment sales 2) Gift-leaseback arrangements 3) Tax-free exchanges with family members 4) Private annuities with family members 5) Grantor retained

Basis Planning The Forgotten Part of Estate Planning Chattanooga Estate Planning Council October 2012

CAVEATS Basis Planning The Forgotten Part of Estate Planning Chattanooga Estate Planning Council October 2012 General Discussion Exceptions Apply Particular Facts can Change the Advice Every Possible Topic

CAVEATS Basis Planning The Forgotten Part of Estate Planning Chattanooga Estate Planning Council October 2012 General Discussion Exceptions Apply Particular Facts can Change the Advice Every Possible Topic

Chapter 12. Property Transactions: Determination of Gain or Loss,Basis Considerations, and Nontaxable Exchanges

Chapter 12 Property Transactions: Determination of Gain or Loss,Basis Considerations, and Nontaxable Exchanges Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004

Chapter 12 Property Transactions: Determination of Gain or Loss,Basis Considerations, and Nontaxable Exchanges Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004

DTN University Pass It On! Farm Family Estate and Succession Planning

DTN University Pass It On! Farm Family Estate and Succession Planning Marcia Zarley Taylor, DTN Executive Editor Andy Biebl, CPA, Tax Partner, CliftonLarsonAllen LLC Nick Houle, CPA, Tax Partner, CliftonLarsonAllen

DTN University Pass It On! Farm Family Estate and Succession Planning Marcia Zarley Taylor, DTN Executive Editor Andy Biebl, CPA, Tax Partner, CliftonLarsonAllen LLC Nick Houle, CPA, Tax Partner, CliftonLarsonAllen

Ag Income Tax Update for Farm Families

Ag Income Tax Update for Farm Families Agricultural Business Management C. Robert Holcomb, EA, Gary A. Hachfeld, Extension Educators Revised 4/2016 Topic Table of Contents Page Depreciation...1 Tangible

Ag Income Tax Update for Farm Families Agricultural Business Management C. Robert Holcomb, EA, Gary A. Hachfeld, Extension Educators Revised 4/2016 Topic Table of Contents Page Depreciation...1 Tangible

BUSINESS BASICS. Personnel Requirements, Tasks to perform, Job Description, Personnel Policy

BUSINESS BASICS 1. Getting Started Forms of Organization Licenses Required Permits Required Insurance 2. Operating Start from Scratch Part Time vs. Full Time Buying 3. Financing Types Costs Sources 4.

BUSINESS BASICS 1. Getting Started Forms of Organization Licenses Required Permits Required Insurance 2. Operating Start from Scratch Part Time vs. Full Time Buying 3. Financing Types Costs Sources 4.

Ag Income Tax Update for Farm Families

Ag Income Tax Update for Farm Families Agricultural Business Management C. Robert Holcomb, EA, Gary A. Hachfeld, Extension Educators 12/2015 Topic Table of Contents Page Depreciation... 1 Tangible Property

Ag Income Tax Update for Farm Families Agricultural Business Management C. Robert Holcomb, EA, Gary A. Hachfeld, Extension Educators 12/2015 Topic Table of Contents Page Depreciation... 1 Tangible Property

Nebraska FSA: Program Opportunities for All Farm Sizes and Types

Nebraska USDA Farm Service Agency Nebraska FSA: Program Opportunities for All Farm Sizes and Types Presenter: Lisa Liska, Farm Loan Manager at Lincoln-Logan- McPherson County FSA Who Is Nebraska FSA? We

Nebraska USDA Farm Service Agency Nebraska FSA: Program Opportunities for All Farm Sizes and Types Presenter: Lisa Liska, Farm Loan Manager at Lincoln-Logan- McPherson County FSA Who Is Nebraska FSA? We

PROBATE INFORMATION SHEET

PROBATE INFORMATION SHEET WHEN YOU HAVE COMPLETED THIS FORM, please bring it to your next scheduled meeting along with a certified copy of the decedent's death certificate. Please be sure to provide information

PROBATE INFORMATION SHEET WHEN YOU HAVE COMPLETED THIS FORM, please bring it to your next scheduled meeting along with a certified copy of the decedent's death certificate. Please be sure to provide information

Federal Tax Rates BURKHART & COMPANY, P.C. 900 S. GAY ST, STE KNOXVILLE, TN PHONE FAX

208 Federal Tax Rates BURKHART & COMPANY, P.C. Certified Public Accountants 900 S. GAY ST, STE. 900 KNOXVILLE, TN 37902 PHONE 865.523.7400 FAX 865.637.7239 WWW.BURKHARTCPA.COM INDIVIDUAL INCOME TAX RATES

208 Federal Tax Rates BURKHART & COMPANY, P.C. Certified Public Accountants 900 S. GAY ST, STE. 900 KNOXVILLE, TN 37902 PHONE 865.523.7400 FAX 865.637.7239 WWW.BURKHARTCPA.COM INDIVIDUAL INCOME TAX RATES

Don t Forget Gifts of Tangible Personal Property

Don t Forget Gifts of Tangible Personal Property PG Calc Feature Article, August 2013 Except for museums that are accustomed to receiving gifts of art and artifacts, charities tend to focus on gifts of

Don t Forget Gifts of Tangible Personal Property PG Calc Feature Article, August 2013 Except for museums that are accustomed to receiving gifts of art and artifacts, charities tend to focus on gifts of

2017 Instructions for Schedule F

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule F Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1040NR,

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule F Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1040NR,

TABLE OF CONTENTS SECTION D ELECTION AND COMPUTATION FORMS

TABLE OF CONTENTS SECTION D ELECTION AND COMPUTATION FORMS The election forms which are included in the Tax Manual have been bolded for reference purposes. The remaining election forms have been updated

TABLE OF CONTENTS SECTION D ELECTION AND COMPUTATION FORMS The election forms which are included in the Tax Manual have been bolded for reference purposes. The remaining election forms have been updated

2017 Instructions for Schedule D

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule D Capital Gains and Losses These instructions explain how to complete Schedule D (Form 1040). Complete Form 8949 before

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule D Capital Gains and Losses These instructions explain how to complete Schedule D (Form 1040). Complete Form 8949 before

Life Events and Taxes

SHIRLEY W. HATCHER, CPA, PA... all things accounting and tax... Life Events and Taxes Life is full of milestones. It s those significant events that we all go through at some point in our lives, like getting

SHIRLEY W. HATCHER, CPA, PA... all things accounting and tax... Life Events and Taxes Life is full of milestones. It s those significant events that we all go through at some point in our lives, like getting

BEGINNING FARMER TAX CREDIT ACT

BEGINNING FARMER TAX CREDIT ACT Revised November, 2001 Administration: The Beginning Farmer Board is created in the Beginning Farmer Tax Credit Act. For administrative and budgetary purposes only the Board

BEGINNING FARMER TAX CREDIT ACT Revised November, 2001 Administration: The Beginning Farmer Board is created in the Beginning Farmer Tax Credit Act. For administrative and budgetary purposes only the Board

Cattle Enterprise Tax and Financial Management

Cattle Enterprise Tax and Financial Management T. Bryant, CPA 1 1 Senior Tax Partner, Beasley, Bryant & Company, CPA s, P.A. Owner/Operator, Overkill Hill Farms, LLC I. Current tax situation for farmers

Cattle Enterprise Tax and Financial Management T. Bryant, CPA 1 1 Senior Tax Partner, Beasley, Bryant & Company, CPA s, P.A. Owner/Operator, Overkill Hill Farms, LLC I. Current tax situation for farmers

AAE 320 Farming Systems Management Problem Set #3

AAE 320 Farming Systems Management Problem Set #3 ANSWER KEY 1) You had a machine shed built and bought a new combine. The machine shed costs $100,000 and the combine costs $200,000. For your internal

AAE 320 Farming Systems Management Problem Set #3 ANSWER KEY 1) You had a machine shed built and bought a new combine. The machine shed costs $100,000 and the combine costs $200,000. For your internal

IRS Issues Notice of proposed ruling on self-employment tax treatment of CRP payments - Suggested outline for comments now available

IRS Issues Notice of proposed ruling on self-employment tax treatment of CRP payments - Suggested outline for comments now available 2321 N. Loop Drive, Ste 200 Ames, Iowa 50010 www.calt.iastate.edu Updated

IRS Issues Notice of proposed ruling on self-employment tax treatment of CRP payments - Suggested outline for comments now available 2321 N. Loop Drive, Ste 200 Ames, Iowa 50010 www.calt.iastate.edu Updated

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

Supplement: Estates. Support.DrakeSoftware.com

Supplement: Estates Support.DrakeSoftware.com 828.524.8020 Drake Tax User s Manual Tax Year 2017 Supplement: Estates (706) support.drakesoftware.com (828) 524-8020 Drake Tax Manual Supplement: Estates

Supplement: Estates Support.DrakeSoftware.com 828.524.8020 Drake Tax User s Manual Tax Year 2017 Supplement: Estates (706) support.drakesoftware.com (828) 524-8020 Drake Tax Manual Supplement: Estates

2014 Income Tax Webinar

2014 Income Tax Webinar Charles Brown ISU Farm Management Specialist 515 240 9214 crbrown@iastate.edu Expired Tax Provisions Above the line deduction for certain expenses of school teachers Above the line

2014 Income Tax Webinar Charles Brown ISU Farm Management Specialist 515 240 9214 crbrown@iastate.edu Expired Tax Provisions Above the line deduction for certain expenses of school teachers Above the line

Economic Recovery Act of 1981: Income Tax Provisions Affecting Farmers and Ranchers

PNW 218 / January 1982 Economic Recovery Act of 1981: Income Tax Provisions Affecting Farmers and Ranchers This circular provides an overview of the major tax law changes made by the Economic Recovery

PNW 218 / January 1982 Economic Recovery Act of 1981: Income Tax Provisions Affecting Farmers and Ranchers This circular provides an overview of the major tax law changes made by the Economic Recovery

Identify property that qualifies for IRC 1031 exchanges Calculate basis of property acquired in a like kind exchange Understand how boot can cause

Pages 40-67 Identify property that qualifies for IRC 1031 exchanges Calculate basis of property acquired in a like kind exchange Understand how boot can cause recognition of gain or loss Advise a client

Pages 40-67 Identify property that qualifies for IRC 1031 exchanges Calculate basis of property acquired in a like kind exchange Understand how boot can cause recognition of gain or loss Advise a client

THE CORPORATE INCOME TAX

3 C H A P T E R THE CORPORATE INCOME TAX LEARNING OBJECTIVES After studying this chapter, you should be able to 1 Apply the requirements for selecting tax years and accounting methods to various types

3 C H A P T E R THE CORPORATE INCOME TAX LEARNING OBJECTIVES After studying this chapter, you should be able to 1 Apply the requirements for selecting tax years and accounting methods to various types

Dairy Grazing Farms in Michigan, Sherrill B. Nott. Staff Paper # October, 2002

Staff Paper Dairy Grazing Farms in Michigan, 2001 by Sherrill B. Nott Staff Paper #2002-30 October, 2002 Copyright: 2002 by Sherrill B. Nott. All rights reserved. Readers may make verbatim copies of this

Staff Paper Dairy Grazing Farms in Michigan, 2001 by Sherrill B. Nott Staff Paper #2002-30 October, 2002 Copyright: 2002 by Sherrill B. Nott. All rights reserved. Readers may make verbatim copies of this

MSSP. Market Segment Specialization Program. Farming -- Specific Income Issues and Farm Cooperatives

MSSP Market Segment Specialization Program Farming -- Specific Income Issues and Farm Cooperatives The taxpayer names and addresses shown in this publication are hypothetical. They were chosen at random

MSSP Market Segment Specialization Program Farming -- Specific Income Issues and Farm Cooperatives The taxpayer names and addresses shown in this publication are hypothetical. They were chosen at random

FILING DEADLINES EXTENDED

IRS Depa r t ment s Tax Relief Provisions for Disaster Losses Shirley Dennis-Escoffier Weather-related casualty losses have been on the increase with Hurricanes Harvey, Irma, and Maria recently leaving

IRS Depa r t ment s Tax Relief Provisions for Disaster Losses Shirley Dennis-Escoffier Weather-related casualty losses have been on the increase with Hurricanes Harvey, Irma, and Maria recently leaving

THE UNEXPECTED CURVE THE ESTATE OF COSTANZA AND ITS IMPACT ON SELF CANCELING INSTALLMENT NOTES

THE UNEXPECTED CURVE THE ESTATE OF COSTANZA AND ITS IMPACT ON SELF CANCELING INSTALLMENT NOTES By: Richard F. Roth I. CREATIVE FINANCING A. The future of estate tax in question. B. The future of gift tax

THE UNEXPECTED CURVE THE ESTATE OF COSTANZA AND ITS IMPACT ON SELF CANCELING INSTALLMENT NOTES By: Richard F. Roth I. CREATIVE FINANCING A. The future of estate tax in question. B. The future of gift tax