Identify property that qualifies for IRC 1031 exchanges Calculate basis of property acquired in a like kind exchange Understand how boot can cause

|

|

|

- Ethan Hunter

- 5 years ago

- Views:

Transcription

1 Pages 40-67

2 Identify property that qualifies for IRC 1031 exchanges Calculate basis of property acquired in a like kind exchange Understand how boot can cause recognition of gain or loss Advise a client about the mechanics of a deferred or reversed exchange Understand the special rules that apply with related parties Personal residence and like-kind exchange

3 Identify other real property interests that may qualify for a like-kind exchange Report a like-kind exchange Structure a transaction to not qualify as a like kind exchange

4 (a)nonrecognition OF GAIN OR LOSS FROM EXCHANGES SOLELY IN KIND (1)IN GENERAL No gain or loss shall be recognized on the exchange of property held for productive use in a trade or business or for investment if such property is exchanged solely for property of like kind which is to be held either for productive use in a trade or business or for investment

5 Both relinquished and acquired property must be Investment property or Protective use in a trade or business Not Property primarily held for sale Securities, certificates of trust, beneficial interest Partnership interests, evidences of indebtedness or Personal use assets

6 Real Property Any real estate for any other real estate (used in a trade or business or held for investment)

7 Like kind or Like class Depreciable Tangible Property Like class Same general asset class or same product class Product class- NAICS (North America Industry Classification System)

8 Defined by Treasury Regs (a)2(b)(2) and Rev. Proc C.B Office furniture, fixtures, and equipment 2. Information systems (computers and peripheral equipment) 3. Data handling equipment, except computers 4. Airplanes (airframes and engines), except those used in commercial or contract carrying of passengers or freight, and all helicopters (airframes and engines) 5. Automobiles and taxis 6. Buses

9 7. Light general-purpose trucks 8. Heavy general-purpose trucks 9. Railroad cars and locomotives, except those owned by railroad transportation companies 10. Tractor units for use over-the-road 11. Trailers and trailer-mounted containers 12. Vessels, barges, tugs, and similar water transportation equipment, except those used in marine construction

10 Depreciable Tangible Personal Property NAICS same 6 digit class = Like Kind /naics for a copy of the NAICS manual The North American Industry Classification System (NAICS) is the standard used by Federal statistical agencies in classifying business establishments for the purpose of collecting, analyzing, and publishing statistical data related to the U.S. business economy

11

12

13

14 Bob Builder transfers a grader to Frank Farmer in exchange for a scraper. Neither property is within any of the general asset classes. However, both properties are within the same product class (NAICS code ). The grader and scraper are of a like class and are like-kind for purposes of section 1031

15 Qualify for IRC 1031 like kind property Exchanged properties must be like kind No like class exchanges qualify Intangible Personable Property Nature or Character of the rights exchanged Nature or Character of the underlying property exchanged

16 Basis of the replacement property = Basis of the relinquished property: Increased by any costs incurred Increased by any additional consideration paid (Boot) Basis of acquired property = Carryover basis Increased by any gain recognized Decrease by any Boot received Decreased by any loss recognized

17 Basis of Replacement property = Basis of Relinquished property + any fees Carryover basis + any transaction fees + gain recognized Adjusted basis of Aaron s truck $2,500 Less Boot (cash) received Add Gain recognized Basis of Aaron s acquired truck $2,400

18 I have one truck that I use for my Beekeeping business and my family uses for recreational use Can I still exchange my truck in a like-kind transaction and postpone any gain on the transaction? If so, how?

19 July 15, 2017, Merrill traded in a pickup truck he basis of $28,000 Placed in service on June 30, 2015 He used the pickup 75% of the time in his beekeeping business 25% for personal use

20 Year Depreciation Calculation Depreciation Allowable 100% Business Use 75% Business Use 2015 $28, % = $ 4,200 $3, $28, % = $ 7,140 5, $28, % ½ = 2,499 1,874 Total $13,839 $ 10,379

21 Cost of relinquished pickup $28,000 Accumulated depreciation using 100% business use (13,839) Exchange basis $14,161 Cash boot paid (10,000) Adjusted basis of new pickup for depreciation $24,161 Cost of relinquished pickup $28,000 Accumulated depreciation for business use (10,379) Exchange basis $17,621 Cash boot paid 10,000 Adjusted basis of new pickup for gain or loss $27,621

22 Rather than trade in his truck Merrill gifts it to his son Truck FMV $20,000 Carryover basis 17,621 If son trades gifted truck in for new truck (plus $10K cash) Son s basis in new truck is $27,621 Any IRC 1245 recapture in old truck carries over to new truck

23 Boot is generally cash but may be any other non like-kind asset Could be a transfer of liabilities (net) Could result in a gain If not like kind boot is transferred could result in a loss How does boot effects basis?

24 Two possible effects on the basis of property received Increases basis by the amount of gain recognized.or Decreases basis by total FMV of boot received If the FMV of boot is = or less than gain no adjustment to basis

+ $800 cash Pick-up truck (FMV of $4,200) Both vehicles used 100% business Both are like class per (#7 page 41) light general purpose truck What")

25 W.W exchanges delivery van (FMV $3K & adj. basis $5K) + $800 cash Pick-up truck (FMV of $4,200) Both vehicles used 100% business Both are like class per (#7 page 41) light general purpose truck What is W.W. s gain on the transaction Received $4,200 + $800 = $5,000 Relinquished (basis) $3,000 Gain realized $2,000

26 W.W. receives pick-up truck (FMV $2,800 & $2,200 cash) $5,000 Relinquishes van ($3,000 basis) Gain realized 2,000 Gain recognized 2,000 Basis in truck $3,000 (basis in van) + 2,000 gain recognized - 2,200 boot received = $2,800 new basis & no deferred gain

27 Dan apartment building $400K basis, $800 FMV, $320K mortgage Elene apartment building $700 basis, $1M FMV, $660 mortgage Dan relinquishes his apartment + $160K cash Does Dan have a gain and if so how much?

28

29 Dan Elene Adjusted basis of property transferred $400,000 $700,000 Cash paid 0 160,000 Liability on property received 600, ,000 Cash received (160,000) 0 Liability on property transferred (320,000) (600,000) Gain recognized $160,000 $120,000

30 Dan Elene Adjusted basis of property transferred $400,000 $700,000 Cash paid 0 160,000 Cash received (160,000) -0- Net debt transferred 280, ,000 Gain recognized 160, ,000 Basis in property acquired $680,000 $700,000

31 Dan sells property for $880,000 Pays off mortgage of 320,000 Net proceeds 560,000 Proceeds held in escrow by a qualified intermediary Dan purchases Elene s property for $ 1,000,000 Finances 440,000 Realized gain 480,000 Recognized gain $ - 0 -

32 Taxpayer may have to report ordinary income If the taxpayer receives boot Limited to lesser of The recomputed basis of the property or The excess of the amount realized on the disposition over the adjusted basis of the property

33 Like-kind personal property is section 1245 property in most cases, which means that the relinquished property and the replacement property are subject to the same recapture rules. In some cases, section 1245 real property and property that is not section 1245 real property are like-kind even though subject to differing recapture provisions. In those cases, the section 1245 recapture rules can cause gain to be recognized as ordinary income at the time of the like-kind exchange even though the gain would not have to be recognized under the section 1031 like-kind exchange rules for qualifying real property.

34 Vickie purchased a new machine - cash $3,400 + old machine - dealer allowance 1,360 Original cost of $5,000 Depreciation 3,950 Adj. basis $1,050 Realized gain 310 Recognized gain $ -0- Why?

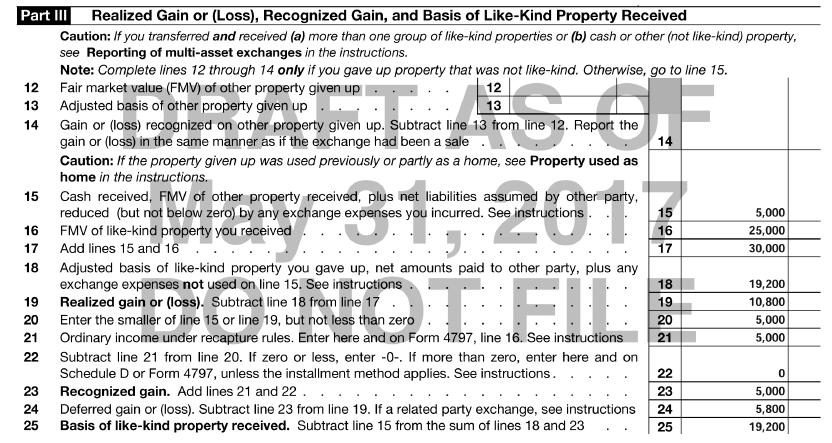

35 2017 Mike traded tractor #1 FMV $30,000 For tractor #2 FMV 25,000 Received cash 5,000 #1 cost $50,000 Depreciation 30,800 Adj. basis $19,200 Realized IRC 1245 gain 10,800 Gain realized boot 5,000 Deferred IRC 1245 recapture $5,800

36

37 Penelope exchange a warehouse for land & dep. real property FMV - warehouse $112,000 Depreciation 20,000 Basis 92,000 Land FMV 95,000 Other depreciable real property 15,000 Recognized gain $5,000 Greater of: $2,000 (112, ,000) $5,000 (20,000 addt. depreciation - $15,000)

38 Seller disposes of property first Hope to find replacement property later Potential drawback no replacement property available Timing constraints within Treas. Regs. Requires a qualified intermediary to hold funds Property for property No constructive receipt of funds

39 In a deferred exchange, the replacement property must be 1. Identified within 45 days after the taxpayer relinquishes the exchanged property, and 2. Received by the earlier of 180 days after the date the taxpayer relinquishes the exchanged property or the due date of the taxpayer s return for the tax year in which the relinquishment occurs

40 Exchange one for two

41 A Qualified Intermediary ( QI ) is a person who: Is not the taxpayer or a disqualified person; Enters into a written agreement with the taxpayer (the exchange agreement) under which the qualified intermediary: Acquires the relinquished property from the taxpayer; Transfers the relinquished property to the buyer; Acquires the replacement property from the seller; Transfers the replacement property to the taxpayer. The exchange agreement must expressly limit the taxpayer s rights to receive, pledge, borrow, or otherwise obtain benefits of money or other property held by the qualified intermediary

42 Taxpayer s agent Employee Accountant Attorney Banker Broker Real estate agent (within a 2 year period of the transfer) Related party IRC 267(b) or 707(b)

Two corporations which are members of the same controlled group (4)A grantor and a fiduciary of any trust;")

43 (b)relationships The persons referred to in subsection (a) are:(1)members of a family, as defined in subsection (c)(4); (2)An individual and a corporation more than 50 percent in value of the outstanding stock of which is owned, directly or indirectly, by or for such individual; (3)Two corporations which are members of the same controlled group (4)A grantor and a fiduciary of any trust; (5)A fiduciary of a trust and a fiduciary of another trust, if the same person is a grantor of both trusts; (6)A fiduciary of a trust and a beneficiary of such trust; (7)A fiduciary of a trust and a beneficiary of another trust, if the same person is a grantor of both trusts; (8)A fiduciary of a trust and a corporation more than 50 percent in value of the outstanding stock of which is owned, directly or indirectly (9)A person and an organization to which section 501

44 Fred Wants out of farming - Farm $800,000 FMV George Wants to build mansion on Fred s property George Has no property to exchange with Fred Fred hires a qualified intermediary facilitates sale to George Fred finds a beach house ($800,000) rental property within 45 days Fred recognizes no gain on the exchange as long as the transaction is completed within the earlier of 180 days or due date of return

45 Can we do this backwards? First - Purchase the replacement property Than - Dispose of the existing property Rev. Proc , provide a Safe Harbor Property must be held in a QEAA Qualified Exchange Accommodation Arrangement Six additional requirements need to be met

46 1. Title to the property is held by an exchange accommodation titleholder who is not the taxpayer or a disqualified person and who is subject to federal income tax for the entire period from the date the titleholder acquires the property until it is transferred again to complete the exchange. 2. At the time the ownership of the property is transferred to the titleholder, the taxpayer has a bona fide intent that the property held by the titleholder represents either replacement property or relinquished property in an exchange that qualifies for nonrecognition of gain under section 1031.

47 3. No later than 5 business days after the title is transferred, the taxpayer and the titleholder enter into a written agreement that the property is being held to facilitate a section 1031 exchange, and that the taxpayer and the titleholder agree to report the acquisition, holding, and disposition of the property as specified in Rev. Proc No later than 45 days after the taxpayer transfers the replacement property to the titleholder, the taxpayer identifies the relinquished property (the taxpayer can identify alternative and multiple properties under the rules previously discussed).

48 5. No later than 180 days after the title is transferred to the titleholder, the property is transferred as either replacement or relinquished property. 6. The combined time period that the relinquished property and the replacement property are held in the QEAA does not exceed 180 days.

49 Lana owns parcel A and wants parcel B before it gets sold Lana would like to postpone the gain on the sale of parcel Lana has not yet found a buyer for parcel A, but believes it will sell Can she purchase parcel B purchased first and still postpone the gain under IRC 1031 and if so how?

50 Lana can utilize the services of a QEAA The QEAA can acquire the property on the TP s behalf Title actually will be in the name of the TP It would be difficult to get financing otherwise Lina would need to either get a bridge loan or self-finance The QEAA than disposes of parcel A

51 Related parties can exchange property and defer gain under IRC 1031 A subsequent disposition within two years can cause the recognition of that gain Who are related parties? Once again defined by IRC 267(b) & 707(b)(1) Additional requirement Filing Form 8824 for the year of sale and for the following two years

52 July 2016, Emily exchanges properties with her son Arthur Both properties were help for investment Emily property has a FMV of $100,000 and basis of $60,000 Arthur s property has a FMV of $100,000 and basis of $80,000 The exchange qualified as a like-kind exchange April 2017, Arthur sells property to an unrelated party for $102,000

53 Arthur must recognize a gain on the sale of: Adjusted basis $80,000 Sales price 102,000 Gain $22,000 Emily as a result of the subsequent sale also must report her deferred gain of: Adjusted basis $100,000 ($60,000 + $40,000 deferred gain) Basis 60,000 Gain $40,000

54 If the disposition was a nonrecognition transaction The related parties derived no tax advantage from shifting basis between the exchanged properties, or An exchange of undivided interests in different properties resulted in each related party holding either the entire interest in a single property or a larger undivided interest in any of the properties.

55 Generally not allowed for like-kind exchange If you sold your home for a loss could you deduct it? Courts have held that the hope that your residences increases in value does not make it an investment property There is a Safe Harbor difficult standard to meet Same rules under IRC 280 personal use test Includes the 14 day or 10% personal use test

56 TP can relinquish/exchange investment property (land and or building) Receive rental property or land Convert the rental or build a residence TP must hold (as a residence) for 5 years to qualify for IRC 121

57 Ownership in a trust (very limited circumstances) Easements (not personal property) Timberland only timberland for raw land Leasehold interests Must be 30 year or more for other real estate Fractional interest Must be tenants in common not for a share of a stock or partnership interest recent court case

58 Tenants in common - are co-owners who each own a separate and undivided interest in the same real property and have an equal right to the possession and use of the property. They each have an Undivided Fractional Interest. Not a partnership Joint ownership Two friends get together and purchase rental property One can exchange his/her interest for another rental property

59 Rev. Proc spells out conditions that must be met Requires IRS Letter Ruling 15 required conditions that must be met

60 Form 8824 Like-Kind exchange Form 6252 Installment sale (like-kind exchange) Several examples in the book

61 Carl owns a 500 unit apartment & a JD tractor used on the property Carl wants a larger tractor- cost of $20,000 Current tractor FMV $5,000 & $-0- basis Option 1- Sell tractor for $5,000 and recognize $5,000 ord. income Option 2 trade-in old tractor + $15,000 cash (gain is deferred) Basis in new tractor: Option 1 = $20,000 Basis in new tractor: Option 2 = $15,000

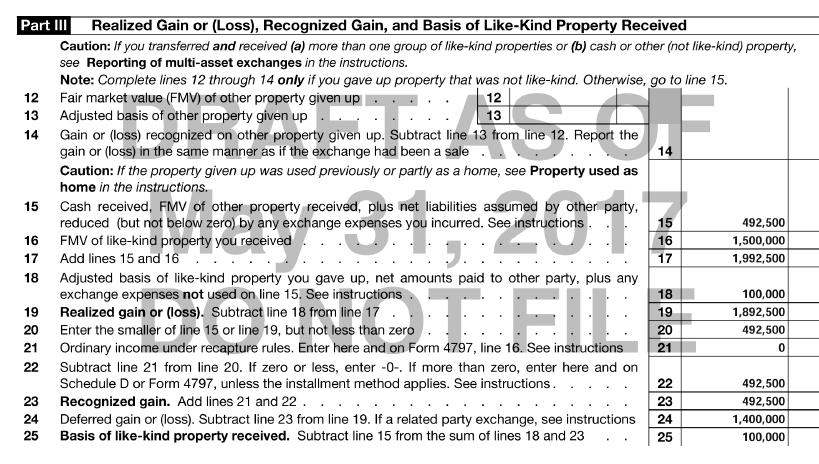

62 Ima wants to sell her 1000 acre farm in Iowa (no structures) FMV is $2,000,000 Basis in farm - $100,000 Wants to avoid paying tax on the sale/gain Finds a motel in Alabama FMV $1,500,000 Both parties agree to the exchange + $500,000 cash to Ima Additional transfer tax of $7,500 due (from Ima) Ima has a gain equal to the boot less the addt. cost = $492,500 Files Form 8824 Like-kind exchange Form 4797 Sale of business property and Schedule D (Form 1040)

63

64 What would happen if (in the prior example) the motel owner did not have the $500,000 cash (Boot) to balance the transaction? Another option could be a like-kind exchange with an installment sale agreement This would also have the effect of spreading out Ima s gain over multi years Interest would be charged on the installment balance and Ima would have a source of yearly cash to keep her bad business decision going Ima files Form 8824 & Form 6252

65 I want to pay the tax now Why???? I have a NOL carry forward I am in a low tax bracket (now & it s going up) I have other capital losses to offset Higher basis in new property (IRC 179, bonus depreciation spread the cost over a period of time) Reduce SE tax (additional depreciation) I like paying taxes ( or I never did it before)

66 Sell the currently owned asset Receive the payment directly from the buyer Purchas the new asset Keep the transactions separated Difficult to do with a dealer (car, equipment,) IRS may challenge and re-characterize as a like-kind exchange

67 If basis of old property exceeds FMV in a like-kind exchange losses are postponed Better off selling property and recognizing loss, unless you don t need the loss now Have an NOL Have carryover capital losses In a low tax bracket

68 Any Questions??????????????

1031 Like-Kind Exchanges Advanced Topics, Updates, and Industry News

1031 Like-Kind Exchanges Advanced Topics, Updates, and Industry News Ken Shore, Vice President 1031 Exchange Specialist May, 2015 1 Like Kind Exchange History Legislative Rationale Continuity of Investment

1031 Like-Kind Exchanges Advanced Topics, Updates, and Industry News Ken Shore, Vice President 1031 Exchange Specialist May, 2015 1 Like Kind Exchange History Legislative Rationale Continuity of Investment

Internal Revenue Service

Internal Revenue Service Number: 201408019 Release Date: 2/21/2014 Index Number: 1031.00-00, 1031.05-00 ------------------------- ------------------------------------------------------------ -------------------------------

Internal Revenue Service Number: 201408019 Release Date: 2/21/2014 Index Number: 1031.00-00, 1031.05-00 ------------------------- ------------------------------------------------------------ -------------------------------

U.S. INTERNAL REVENUE CODE SECTION 1031 TAX DEFERRED LIKE KIND EXCHANGES. This outline has been modified to reflect the recent changes in the tax law.

U.S. INTERNAL REVENUE CODE SECTION 1031 TAX DEFERRED LIKE KIND EXCHANGES This outline has been modified to reflect the recent changes in the tax law. I. SECTION 1031 LIKE KIND EXCHANGE A. What is a 1031

U.S. INTERNAL REVENUE CODE SECTION 1031 TAX DEFERRED LIKE KIND EXCHANGES This outline has been modified to reflect the recent changes in the tax law. I. SECTION 1031 LIKE KIND EXCHANGE A. What is a 1031

5/4/2016. Common Terms. Disadvantages of Exchanging. Advantages of Exchanging. Impact of Recent Tax Legislation Like-Kind Exchanges

Advanced 1031 Like-Kind Exchange Issues Presented by: Michael A. Fritton, CPA Somerset CPAs, P.C. Common Terms 1031 Exchange Like-Kind Exchange Property Swap Starker Transaction Advantages of Exchanging

Advanced 1031 Like-Kind Exchange Issues Presented by: Michael A. Fritton, CPA Somerset CPAs, P.C. Common Terms 1031 Exchange Like-Kind Exchange Property Swap Starker Transaction Advantages of Exchanging

Internal Revenue Service

Internal Revenue Service Number: 200329021 Release Date: 7/18/2003 Index: 1031.00-00 Department of the Treasury P.O. Box 7604 Ben Franklin Station Washington, DC 20044 Person to Contact: Telephone Number:

Internal Revenue Service Number: 200329021 Release Date: 7/18/2003 Index: 1031.00-00 Department of the Treasury P.O. Box 7604 Ben Franklin Station Washington, DC 20044 Person to Contact: Telephone Number:

EVERYTHING YOU EVER WANTED TO KNOW ABOUT 1031 EXCHANGES AND THE TAX-SAVING OPPORTUNITIES

EVERYTHING YOU EVER WANTED TO KNOW ABOUT 1031 EXCHANGES AND THE TAX-SAVING OPPORTUNITIES (Updated November 10, 2017) 1707 North Main Street Longmont, CO 80501 (888) 367-1031 www.efirstbank1031.com 1707

EVERYTHING YOU EVER WANTED TO KNOW ABOUT 1031 EXCHANGES AND THE TAX-SAVING OPPORTUNITIES (Updated November 10, 2017) 1707 North Main Street Longmont, CO 80501 (888) 367-1031 www.efirstbank1031.com 1707

ABOUT CASCADE EXCHANGE SERVICES, INC. (CES):

:") ABOUT CASCADE EXCHANGE SERVICES, INC. (CES): CES, a qualified tax deferred exchange intermediary performing accommodation services since 1990, offers nationwide exchange capabilities to our clients. We

ABOUT CASCADE EXCHANGE SERVICES, INC. (CES): CES, a qualified tax deferred exchange intermediary performing accommodation services since 1990, offers nationwide exchange capabilities to our clients. We

1031 Tax Deferred Real Estate Transactions & Reverse 1031 Transactions

1031 Tax Deferred Real Estate Transactions & Reverse 1031 Transactions Continuing Real Estate Education Seminar Pierre E. Debbas, Esq. Romer Debbas, LLP 183 Madison Avenue Suite 904 New York, NY 10016

1031 Tax Deferred Real Estate Transactions & Reverse 1031 Transactions Continuing Real Estate Education Seminar Pierre E. Debbas, Esq. Romer Debbas, LLP 183 Madison Avenue Suite 904 New York, NY 10016

Date: November 20, Refer Reply To: CC:IT&A:5 - PLR In Re: * * *

Citations: LTR 200712013 Date: Nov. 20, 2006 No Recognition of Gain Realized on Reverse Like-Kind Exchange The Service has ruled that section 1031(f) will not apply to trigger recognition of any gain realized

Citations: LTR 200712013 Date: Nov. 20, 2006 No Recognition of Gain Realized on Reverse Like-Kind Exchange The Service has ruled that section 1031(f) will not apply to trigger recognition of any gain realized

1031 Exchange Topics. Reference Guide to 1031 Exchanges Exchange Solutions Nationwide. Investment Property Exchange Services, Inc.

1031 Exchange Topics Reference Guide to 1031 Exchanges 1031 Exchange Solutions Nationwide Investment Property Exchange Services, Inc. a Fidelity National Financial Company FORTUNE 500 1031 Exchange Topics

1031 Exchange Topics Reference Guide to 1031 Exchanges 1031 Exchange Solutions Nationwide Investment Property Exchange Services, Inc. a Fidelity National Financial Company FORTUNE 500 1031 Exchange Topics

James R. Browne Dallas TX Real Estate Sales and Exchanges

James R. Browne Dallas TX 72505 Real Estate Sales and Exchanges Speaker Strasburger & Price, LLP 901 Main Street, Suite 4400 Dallas, Texas 75202.3794 Tel: 214.651.4420 Fax: 214.659.4019 jim.browne@strasburger.com

James R. Browne Dallas TX 72505 Real Estate Sales and Exchanges Speaker Strasburger & Price, LLP 901 Main Street, Suite 4400 Dallas, Texas 75202.3794 Tel: 214.651.4420 Fax: 214.659.4019 jim.browne@strasburger.com

Installment Sales. Contents. For use in preparing 2012 Returns. Publication 537 Cat. No V. Future Developments. Reminder.

Department of the Treasury Internal Revenue Service Publication 537 Cat. No. 15067V Installment Sales For use in preparing 2012 Returns Contents Future Developments... 1 Reminder... 1 Introduction... 1

Department of the Treasury Internal Revenue Service Publication 537 Cat. No. 15067V Installment Sales For use in preparing 2012 Returns Contents Future Developments... 1 Reminder... 1 Introduction... 1

STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE

New York State Department of Taxation and Finance Office of Counsel STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. M150511A The Department of Taxation and Finance

New York State Department of Taxation and Finance Office of Counsel STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. M150511A The Department of Taxation and Finance

Section 1031 Tax Deferred Exchanges. A Guide to the Best Strategy for Real Estate Investment

Section 1031 Tax Deferred Exchanges A Guide to the Best Strategy for Real Estate Investment Jon Fisher 303-850-4197 Vice President Land Title Exchange Corporation Cell: 303-981-8866 Fax: 303-393-4849

Section 1031 Tax Deferred Exchanges A Guide to the Best Strategy for Real Estate Investment Jon Fisher 303-850-4197 Vice President Land Title Exchange Corporation Cell: 303-981-8866 Fax: 303-393-4849

William J. Gessner, Esq.

Exchange Solutions Group, LLC William J. Gessner, Esq. Senior 1031 Exchange Counsel Tax Deferred Exchanges Nationwide A Presentation for: Maryland Association of CPAs September 22, 2011 William J. Gessner,

Exchange Solutions Group, LLC William J. Gessner, Esq. Senior 1031 Exchange Counsel Tax Deferred Exchanges Nationwide A Presentation for: Maryland Association of CPAs September 22, 2011 William J. Gessner,

TAX MEMORANDUM. CPAs, Clients & Associates. David L. Silverman, Esq. Shirlee Aminoff, Esq. DATE: April 2, Attorney-Client Privilege

LAW OFFICES DAVID L. SILVERMAN, J.D., LL.M. 2001 MARCUS AVENUE LAKE SUCCESS, NEW YORK 11042 (516) 466-5900 SILVERMAN, DAVID L. TELECOPIER (516) 437-7292 NYTAXATTY@AOL.COM AMINOFF, SHIRLEE AMINOFFS@GMAIL.COM

LAW OFFICES DAVID L. SILVERMAN, J.D., LL.M. 2001 MARCUS AVENUE LAKE SUCCESS, NEW YORK 11042 (516) 466-5900 SILVERMAN, DAVID L. TELECOPIER (516) 437-7292 NYTAXATTY@AOL.COM AMINOFF, SHIRLEE AMINOFFS@GMAIL.COM

Like-Kind Exchanges Under Section 1031

Like-Kind Exchanges Under Section 1031 Member FEDERATION OF EXCHANGE ACCOMMODATORS Copyright 2007 Banker Exchange, LLC THE BASICS OF SECTION 1031 LIKE-KIND EXCHANGES INTRODUCTION In April 1992, Banker

Like-Kind Exchanges Under Section 1031 Member FEDERATION OF EXCHANGE ACCOMMODATORS Copyright 2007 Banker Exchange, LLC THE BASICS OF SECTION 1031 LIKE-KIND EXCHANGES INTRODUCTION In April 1992, Banker

Conducting Aircraft Tax Free Exchanges

Conducting Aircraft Tax Free Exchanges Webinar Presentation - June 16th, 2010 Presenter: Keith G. Swirsky, President Tel: (202) 342-5251 Fax: (202) 965-5725 kswirsky@gkglaw.com Disclaimers This presentation

Conducting Aircraft Tax Free Exchanges Webinar Presentation - June 16th, 2010 Presenter: Keith G. Swirsky, President Tel: (202) 342-5251 Fax: (202) 965-5725 kswirsky@gkglaw.com Disclaimers This presentation

TULSA ESTATE PLANNING FORUM

TULSA ESTATE PLANNING FORUM APRIL 9, 2018 IRC 1031 EXCHANGES Brief Overview Presentation By Richard W. Riddle, Esq. RIDDLE & WIMBISH, P.C. 5314 South Yale, Suite 200 Tulsa, Oklahoma 74135 (918) 494-3770

TULSA ESTATE PLANNING FORUM APRIL 9, 2018 IRC 1031 EXCHANGES Brief Overview Presentation By Richard W. Riddle, Esq. RIDDLE & WIMBISH, P.C. 5314 South Yale, Suite 200 Tulsa, Oklahoma 74135 (918) 494-3770

Tax-Free Exchanges of Aircraft Under Section 1031

Tax-Free Exchanges of Aircraft Under Section 1031 Keith G. Swirsky, Esquire Galland, Kharasch, Greenberg, Fellman & Swirsky, P.C. 1054 Thirty-first Street, N.W., Suite 200 Washington, D.C. 20007 Telephone:

Tax-Free Exchanges of Aircraft Under Section 1031 Keith G. Swirsky, Esquire Galland, Kharasch, Greenberg, Fellman & Swirsky, P.C. 1054 Thirty-first Street, N.W., Suite 200 Washington, D.C. 20007 Telephone:

Parent = Subsidiary = Taxpayer = QI = Bank = Administrator = A = B = Lease Program 1 = Lease Program 2 =

This Private Letter Ruling is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page.,qwhuqdo5hyhqxh6huylfh Number: 200240049 Release Date: 10/4/2002 Index No.: 1031.05-00

This Private Letter Ruling is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page.,qwhuqdo5hyhqxh6huylfh Number: 200240049 Release Date: 10/4/2002 Index No.: 1031.05-00

Property Transactions - Nontaxable Exchanges

Discussion Questions Chapter I12 Property Transactions - Nontaxable Exchanges I12-1 The statement is not correct. For nontaxable exchanges, taxpayers maintain a continuing investment in comparable property.

Discussion Questions Chapter I12 Property Transactions - Nontaxable Exchanges I12-1 The statement is not correct. For nontaxable exchanges, taxpayers maintain a continuing investment in comparable property.

1031 Exchanges. Seminar Topic: This material provides an in-depth examination. The Basics and Pitfalls

1031 Exchanges The Basics and Pitfalls Seminar Topic: This material provides an in-depth examination of the process and procedure in a 1031 Exchange including structuring the transaction as an exchange

1031 Exchanges The Basics and Pitfalls Seminar Topic: This material provides an in-depth examination of the process and procedure in a 1031 Exchange including structuring the transaction as an exchange

Tax-Free Exchanges Under IRC 1031

May 17, 2011 Tax-Free Exchanges Under IRC 1031 GKG Law, P.C. Webinar Series Presenter: Keith G. Swirsky President Phone: (202) 342-5251 kswirsky@gkglaw.com www.gkglaw.com Disclaimers This presentation

May 17, 2011 Tax-Free Exchanges Under IRC 1031 GKG Law, P.C. Webinar Series Presenter: Keith G. Swirsky President Phone: (202) 342-5251 kswirsky@gkglaw.com www.gkglaw.com Disclaimers This presentation

Internal Revenue Service

Internal Revenue Service Number: 200327039 Release Date: 7/3/2003 Index No.: 1031.00-00 Department of the Treasury P.O. Box 7604 Ben Franklin Station Washington, DC 20044 Person to Contact: Telephone Number:

Internal Revenue Service Number: 200327039 Release Date: 7/3/2003 Index No.: 1031.00-00 Department of the Treasury P.O. Box 7604 Ben Franklin Station Washington, DC 20044 Person to Contact: Telephone Number:

Private Letter Ruling , 07/13/2007, IRC Sec(s). 1031

. 1031") Checkpoint Contents Federal Library Federal Source Materials IRS Rulings & Releases Private Letter Rulings & TAMs, FSAs, SCAs, CCAs, GCMs, AODs & Other FOIA Documents Private Letter Rulings & Technical

Checkpoint Contents Federal Library Federal Source Materials IRS Rulings & Releases Private Letter Rulings & TAMs, FSAs, SCAs, CCAs, GCMs, AODs & Other FOIA Documents Private Letter Rulings & Technical

PENNSYLVANIA DEPARTMENT OF REVENUE

PENNSYLVANIA DEPARTMENT OF REVENUE ISSUED: OCTOBER 20, 2006 PIT Bulletin 2006 07 RTT Bulletin 2006 01 SUT Bulletin 2006 01 PENNSYLVANIA TAX TREATMENT OF IRC 1031 LIKE-KIND EXCHANGES IRC 1031 Like-Kind

PENNSYLVANIA DEPARTMENT OF REVENUE ISSUED: OCTOBER 20, 2006 PIT Bulletin 2006 07 RTT Bulletin 2006 01 SUT Bulletin 2006 01 PENNSYLVANIA TAX TREATMENT OF IRC 1031 LIKE-KIND EXCHANGES IRC 1031 Like-Kind

Chapter C:2. Corporate Formations and Capital Structure

Discussion Questions Chapter C:2 Corporate Formations and Capital Structure C:2-1 Various. A new business can be conducted as a sole proprietorship, partnership, C corporation, S corporation, LLC, or LLP.

Discussion Questions Chapter C:2 Corporate Formations and Capital Structure C:2-1 Various. A new business can be conducted as a sole proprietorship, partnership, C corporation, S corporation, LLC, or LLP.

1031 Exchanges: What Realtors Need to Know. Student Handouts

1031 Exchanges: What Realtors Need to Know Student Handouts I. Benefits A. Benefits to Investors 1. Defer capital gains tax 2. Leverage for wealth building 3. Diversification 4. Consolidation 5. Cash flow

1031 Exchanges: What Realtors Need to Know Student Handouts I. Benefits A. Benefits to Investors 1. Defer capital gains tax 2. Leverage for wealth building 3. Diversification 4. Consolidation 5. Cash flow

Section 1031 Exchanges under the United States Internal Revenue Code (26 U.S.C. 1031)

") Section 1031 Exchanges under the United States Internal Revenue Code (26 U.S.C. 1031) Presented by: A. Jay Kenlan, Esq. Kenlan, Schwiebert, Facey & Goss, PC 1 Section 1031 Exchanges under United States

Section 1031 Exchanges under the United States Internal Revenue Code (26 U.S.C. 1031) Presented by: A. Jay Kenlan, Esq. Kenlan, Schwiebert, Facey & Goss, PC 1 Section 1031 Exchanges under United States

Like-Kind Exchanges In The Energy Industry. Todd D. Keator Thompson & Knight LLP

Like-Kind Exchanges In The Energy Industry Todd D. Keator Thompson & Knight LLP 214-969-1797 Todd.Keator@tklaw.com February 2, 2015 Introduction Background Operation of 1031 Forward Exchanges Reverse Exchange

Like-Kind Exchanges In The Energy Industry Todd D. Keator Thompson & Knight LLP 214-969-1797 Todd.Keator@tklaw.com February 2, 2015 Introduction Background Operation of 1031 Forward Exchanges Reverse Exchange

1031 EXCHANGE TOPICS

1031 EXCHANGE TOPICS Answers to Popular 1031 Exchange Questions Marie Flavin, Esq. Senior Vice President Regional Manager (877) 230-1031 Toll Free (888) 310-1868 Toll Free Fax marie.flavin@ipx1031.com

1031 EXCHANGE TOPICS Answers to Popular 1031 Exchange Questions Marie Flavin, Esq. Senior Vice President Regional Manager (877) 230-1031 Toll Free (888) 310-1868 Toll Free Fax marie.flavin@ipx1031.com

Tax-Free Aircraft Exchanges Under IRC 1031 and Bonus Depreciation Update and Basics

Aviation Tax Law Webinar December 8, 2015 Tax-Free Aircraft Exchanges Under IRC 1031 and Bonus Depreciation Update and Basics Presented by: Keith G. Swirsky Christopher B. Younger GKG Law, P.C. 1055 Thomas

Aviation Tax Law Webinar December 8, 2015 Tax-Free Aircraft Exchanges Under IRC 1031 and Bonus Depreciation Update and Basics Presented by: Keith G. Swirsky Christopher B. Younger GKG Law, P.C. 1055 Thomas

1031 Exchange Reporting Guide

2014 1031 Exchange Reporting Guide Helping to Simplify the Reporting of your 1031 Exchange 1.800.828.1031.1031 www.1031 1031CORP CORP.com Introduction In our on-going commitment to provide our valued clients

2014 1031 Exchange Reporting Guide Helping to Simplify the Reporting of your 1031 Exchange 1.800.828.1031.1031 www.1031 1031CORP CORP.com Introduction In our on-going commitment to provide our valued clients

IRC 1031 Tax Deferred Exchange Exchanges. Whitney Brennan Vice President Southeast Region, IPX

IRC 1031 Tax Deferred Exchange 1031 Exchanges Whitney Brennan Vice President Southeast Region, IPX1031 1 Course Objectives Today s program is designed to help you better understand: Objective 1 Objective

IRC 1031 Tax Deferred Exchange 1031 Exchanges Whitney Brennan Vice President Southeast Region, IPX1031 1 Course Objectives Today s program is designed to help you better understand: Objective 1 Objective

1031 EXCHANGE TOPICS. Answers to Popular 1031 Exchange Questions Exchange Solutions Nationwide

1031 EXCHANGE TOPICS Answers to Popular 1031 Exchange Questions 1031 Exchange Solutions Nationwide 1031 EXCHANGE TOPICS Offices Nationwide (888) 771-1031 www.ipx1031.com Copyright 2014 Investment Property

1031 EXCHANGE TOPICS Answers to Popular 1031 Exchange Questions 1031 Exchange Solutions Nationwide 1031 EXCHANGE TOPICS Offices Nationwide (888) 771-1031 www.ipx1031.com Copyright 2014 Investment Property

1031 Exchanges. by G. Scott Haislet

1031 Exchanges by G. Scott Haislet 2004-2014 G. Scott Haislet, CPA Attorney at Law Certified Specialist Taxation California State Bar, Board of Legal Specialization 1031 exchange qualified intermediary

1031 Exchanges by G. Scott Haislet 2004-2014 G. Scott Haislet, CPA Attorney at Law Certified Specialist Taxation California State Bar, Board of Legal Specialization 1031 exchange qualified intermediary

A Like Kind 1031 Exchange How to Guide for CPAs

A Like Kind 1031 Exchange How to Guide for CPAs Certified Public Accountants (CPAs) often advise their clients on whether they would benefit from tax deferral strategies such as Internal Revenue Code (IRC)

A Like Kind 1031 Exchange How to Guide for CPAs Certified Public Accountants (CPAs) often advise their clients on whether they would benefit from tax deferral strategies such as Internal Revenue Code (IRC)

Capital Gains and Losses

Capital Gains and Losses Table of Contents Chapter 1: Basis Of Property... 2 I. Introduction... 2 II. Cost Basis... 2 III. Adjusted Basis... 4 IV. Basis Other Than Cost... 5 Chapter 2: Sale Of Property...

Capital Gains and Losses Table of Contents Chapter 1: Basis Of Property... 2 I. Introduction... 2 II. Cost Basis... 2 III. Adjusted Basis... 4 IV. Basis Other Than Cost... 5 Chapter 2: Sale Of Property...

Chapter C:2. Corporate Formations and Capital Structure

Discussion Questions Chapter C:2 Corporate Formations and Capital Structure C:2-1 Various. A new business can be conducted as a sole proprietorship, partnership, C corporation, S corporation, LLC, or LLP.

Discussion Questions Chapter C:2 Corporate Formations and Capital Structure C:2-1 Various. A new business can be conducted as a sole proprietorship, partnership, C corporation, S corporation, LLC, or LLP.

Building for the Future

Building for the Future FEA 2018 Annual Conference Scott Saunders Asset Preservation, Inc. Creative and Non-Real Estate Exchanges September 12 14, 2018 Marriott Country Club Plaza Kansas City, Missouri

Building for the Future FEA 2018 Annual Conference Scott Saunders Asset Preservation, Inc. Creative and Non-Real Estate Exchanges September 12 14, 2018 Marriott Country Club Plaza Kansas City, Missouri

OTHER TOOLS TO MANAGE TAX LIABILITY

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

CHICAGO TITLE INSURANCE COMPANY

CHICAGO TITLE INSURANCE COMPANY TOPIC: 1031 Exchanges -- Traps and Trip Wires By: Jeffrey I. Hrdlicka Senior State Underwriting Counsel, Chicago Title Insurance Company I. The Basics A. Internal Revenue

CHICAGO TITLE INSURANCE COMPANY TOPIC: 1031 Exchanges -- Traps and Trip Wires By: Jeffrey I. Hrdlicka Senior State Underwriting Counsel, Chicago Title Insurance Company I. The Basics A. Internal Revenue

Instructions for Company Income Tax Return (Form S128-C) For Year Ended 31 March 2018 (or Other Approved Year)

For Year Ended 31 March 2018 (or Other Approved Year)") Instructions for Company Income Tax Return (Form S128-C) For Year Ended 31 March 2018 (or Other Approved Year) General Instructions Which Companies Must File an Income Tax Return What is a company? A company

Instructions for Company Income Tax Return (Form S128-C) For Year Ended 31 March 2018 (or Other Approved Year) General Instructions Which Companies Must File an Income Tax Return What is a company? A company

ABA: Safe Harbor Parking Like-Kind Exchanges

ABA: Safe Harbor Parking Like-Kind Exchanges Robert D. Schachat and Glenn Johnson Ernst & Young LLP January 22, 2011 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst

ABA: Safe Harbor Parking Like-Kind Exchanges Robert D. Schachat and Glenn Johnson Ernst & Young LLP January 22, 2011 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst

1031 Exchange Principles

1031 Exchange Principles 250 W Old Wilson Bridge Road Suite 320 Worthington OH 43085 (614) 471-2211 www.bishofffinancial.com Securities Offered ThroughCambridge Investment Research, Inc. A Broker-Dealer,

1031 Exchange Principles 250 W Old Wilson Bridge Road Suite 320 Worthington OH 43085 (614) 471-2211 www.bishofffinancial.com Securities Offered ThroughCambridge Investment Research, Inc. A Broker-Dealer,

Unit10. Property Transactions - Nontaxable Exchanges (PAK Chap. 12)

") 1 Unit10. Property Transactions - Nontaxable Exchanges (PAK Chap. 12) The transactions examined in this chapter overrides the normal rule that provides for the recognition of realized gains and realized

1 Unit10. Property Transactions - Nontaxable Exchanges (PAK Chap. 12) The transactions examined in this chapter overrides the normal rule that provides for the recognition of realized gains and realized

1. Like-Kind Exchanges. 2. Involuntary Conversions. 3. Sale of Principal Residence. 4. Tax Planning Considerations

Outline 1 Unit10. Property Transactions - Nontaxable Exchanges (PAK Chap. 12) The transactions examined in this chapter overrides the normal rule that provides for the recognition of realized gains and

Outline 1 Unit10. Property Transactions - Nontaxable Exchanges (PAK Chap. 12) The transactions examined in this chapter overrides the normal rule that provides for the recognition of realized gains and

1031 Exchanges: Benefits to Timberland and Forest Landowners

1031 Exchanges: Benefits to Timberland and Forest Landowners Smart timberland and forest land owners maintain a relentless focus on improving performance of their holdings through portfolio adjustments,

1031 Exchanges: Benefits to Timberland and Forest Landowners Smart timberland and forest land owners maintain a relentless focus on improving performance of their holdings through portfolio adjustments,

Section 1031 for Professionals

Section 1031 for Professionals Real Estate Law Day November 14, 2014 John D. Hamrick, VP Edmund & Wheeler, Inc. 603-336-3190 john@section1031.com Shhhhhhhh.. Don t Tell anyone. Your clients are eligible

Section 1031 for Professionals Real Estate Law Day November 14, 2014 John D. Hamrick, VP Edmund & Wheeler, Inc. 603-336-3190 john@section1031.com Shhhhhhhh.. Don t Tell anyone. Your clients are eligible

Instructions for Form 4562

2002 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury

2002 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury

Who is Asset Preservation, Inc.? Capital Gain, Estate & Other Tax Issues in 2012/ Exchange Trends in 2012/2013 Overview of Delayed Exchanges

Hosted by: Presented by: Scott R. Saunders Sr. Vice President Who is Asset Preservation, Inc.? Capital Gain, Estate & Other Tax Issues in 2012/2013 1031 Exchange Trends in 2012/2013 Overview of Delayed

Hosted by: Presented by: Scott R. Saunders Sr. Vice President Who is Asset Preservation, Inc.? Capital Gain, Estate & Other Tax Issues in 2012/2013 1031 Exchange Trends in 2012/2013 Overview of Delayed

Tax Traps in Oil and Gas Like-Kind Exchange Transactions. Todd Way Vinson & Elkins LLP Dallas, Texas. Julia Pashin Vinson & Elkins LLP Dallas, Texas

Tax Traps in Oil and Gas Like-Kind Exchange Transactions Todd Way Vinson & Elkins LLP Dallas, Texas Julia Pashin Vinson & Elkins LLP Dallas, Texas 14.01 Oil and Gas Like-Kind Exchange Transactions after

Tax Traps in Oil and Gas Like-Kind Exchange Transactions Todd Way Vinson & Elkins LLP Dallas, Texas Julia Pashin Vinson & Elkins LLP Dallas, Texas 14.01 Oil and Gas Like-Kind Exchange Transactions after

Internal Revenue Service

Internal Revenue Service Number: 201216007 Release Date: 4/20/2012 Index Number: 1031.02-00 ---------------------------------------------------------- --------------------------------------- ----------------------------------------------------

Internal Revenue Service Number: 201216007 Release Date: 4/20/2012 Index Number: 1031.02-00 ---------------------------------------------------------- --------------------------------------- ----------------------------------------------------

Welcome! Section 1031 Exchanges. Innovative Strategies and Issues. Presented by Don Munford Smith Anderson

Welcome! Section 1031 Exchanges Innovative Strategies and Issues Presented by Don Munford 2015 Smith Anderson Section 1031 Exchanges Innovative Strategies and Issues Reminder Today s PowerPoint presentation

Welcome! Section 1031 Exchanges Innovative Strategies and Issues Presented by Don Munford 2015 Smith Anderson Section 1031 Exchanges Innovative Strategies and Issues Reminder Today s PowerPoint presentation

1031 Exchanges: Benefits for Farmers and Ranchers

1031 Exchanges: Benefits for Farmers and Ranchers Smart farmers and ranchers can upgrade or replace land holdings with another property by using a tax deferment tool called 1031 tax deferred exchanges.

1031 Exchanges: Benefits for Farmers and Ranchers Smart farmers and ranchers can upgrade or replace land holdings with another property by using a tax deferment tool called 1031 tax deferred exchanges.

1031 Tax Deferred Exchanges Brown Bag on October 18, 2013

1031 Tax Deferred Exchanges Brown Bag on October 18, 2013 Are you ready for an in-depth discussion of the 1031 Exchange processes, requirements and how to utilize 1031 Exchanges to help build and preserve

1031 Tax Deferred Exchanges Brown Bag on October 18, 2013 Are you ready for an in-depth discussion of the 1031 Exchange processes, requirements and how to utilize 1031 Exchanges to help build and preserve

2003 ELA Lease Accountants Conference

2003 ELA Lease Accountants Conference Basics of Tax Leasing (1) September 9, 2003 Speakers: Suresh Makam CitiCapital Bankers Leasing Roger Idnani Boeing Capital Corporation Single Investor Lease Lessor

2003 ELA Lease Accountants Conference Basics of Tax Leasing (1) September 9, 2003 Speakers: Suresh Makam CitiCapital Bankers Leasing Roger Idnani Boeing Capital Corporation Single Investor Lease Lessor

Form 4797 Chapter 3 pp Agricultural Tax Issues

Form 4797 Chapter 3 pp. 85-118 2018 Agricultural Tax Issues Form 4797 Page 85 Reporting of gains and losses on the disposition of business property. The collection point for gains and losses reported elsewhere.

Form 4797 Chapter 3 pp. 85-118 2018 Agricultural Tax Issues Form 4797 Page 85 Reporting of gains and losses on the disposition of business property. The collection point for gains and losses reported elsewhere.

Internal Revenue Service Number: Release Date: 3/2/2007 Index Number:

Internal Revenue Service Number: 200709036 Release Date: 3/2/2007 Index Number: 1031.06-00 ---------------- ------------------------------------------------------- -------------------------------------------------

Internal Revenue Service Number: 200709036 Release Date: 3/2/2007 Index Number: 1031.06-00 ---------------- ------------------------------------------------------- -------------------------------------------------

The Future of Lease Taxation & Planning

The Future of Lease Taxation & Planning October 24, 2006 Strategies and Reporting Introductions Mr. David Fowler Tax Partner PricewaterhouseCoopers LLP Ph: 614.225.8736 E-mail: david.fowler@us.pwc.com

The Future of Lease Taxation & Planning October 24, 2006 Strategies and Reporting Introductions Mr. David Fowler Tax Partner PricewaterhouseCoopers LLP Ph: 614.225.8736 E-mail: david.fowler@us.pwc.com

Income Tax I Fall 2017 Suggested Solutions to Practice Problems

Income Tax I Fall 2017 Suggested Solutions to Practice Problems A. Gain, Loss, and Basis 1. Although Jay receives new stock with a total fair market value of $600 (1,000 shares times $0.60), he realizes

Income Tax I Fall 2017 Suggested Solutions to Practice Problems A. Gain, Loss, and Basis 1. Although Jay receives new stock with a total fair market value of $600 (1,000 shares times $0.60), he realizes

Like-Kind Exchange Mechanics 2018

Like-Kind Exchange Mechanics 2018 Mark A. Vogel Tax Education Services Denver, Colorado mvogel.tax@gmail.com mvogel@du.edu (Handouts - 158 pages.) 1. Questions for the Instructor: Administrative Matters

Like-Kind Exchange Mechanics 2018 Mark A. Vogel Tax Education Services Denver, Colorado mvogel.tax@gmail.com mvogel@du.edu (Handouts - 158 pages.) 1. Questions for the Instructor: Administrative Matters

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

Instructions for Form 4562 Depreciation and Amortization (Section references are to the Internal Revenue Code, unless otherwise noted.

Department of the Treasury Internal Revenue Service Instructions for Form 4562 Depreciation and Amortization (Section references are to the Internal Revenue Code, unless otherwise noted.) General Instructions

Department of the Treasury Internal Revenue Service Instructions for Form 4562 Depreciation and Amortization (Section references are to the Internal Revenue Code, unless otherwise noted.) General Instructions

University of Akron MTax Direct Melanie McCoskey, Ph.D., CPA Module 1 Corporate Formation

University of Akron MTax Direct Melanie McCoskey, Ph.D., CPA mmccoskey@uakron.edu 330.972.6930 Module 1 Corporate Formation May 4, 2015 2 Overview of Chapter Corporate Formation Effect on corp» Gain/loss

University of Akron MTax Direct Melanie McCoskey, Ph.D., CPA mmccoskey@uakron.edu 330.972.6930 Module 1 Corporate Formation May 4, 2015 2 Overview of Chapter Corporate Formation Effect on corp» Gain/loss

FIDUCIARY INCOME TAXES

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

1031 Exchange Topics. Reference Guide to 1031 Exchanges Exchange Solutions Nationwide. Investment Property Exchange Services, Inc.

1031 Exchange Topics Reference Guide to 1031 Exchanges 1031 Exchange Solutions Nationwide Investment Property Exchange Services, Inc. a Fidelity National Financial Company FORTUNE 500 1031 Exchange Topics

1031 Exchange Topics Reference Guide to 1031 Exchanges 1031 Exchange Solutions Nationwide Investment Property Exchange Services, Inc. a Fidelity National Financial Company FORTUNE 500 1031 Exchange Topics

2018 Schedule LK, Like-Kind Exchanges

2018 Schedule LK, Like-Kind Exchanges Used in combination with Schedules M1NC, M2NC, M2SBNC, M4NC, KFNC, KSNC, KPCNC, and KPINC. *187031* Name Social Security Number/Minnesota Tax ID Number/FEIN Before

2018 Schedule LK, Like-Kind Exchanges Used in combination with Schedules M1NC, M2NC, M2SBNC, M4NC, KFNC, KSNC, KPCNC, and KPINC. *187031* Name Social Security Number/Minnesota Tax ID Number/FEIN Before

MSCPA FEDERAL TAX COMMITTEE FEDERAL TAX FORUMS TAX ACCOUNTING BY LORRAINE A. TRAVERS

IRS explains E&P adjustment following switch in depreciation recovery period--plr 201410029 A business that begins depreciating assets using a short recovery period and/or a rapid recovery method may later

IRS explains E&P adjustment following switch in depreciation recovery period--plr 201410029 A business that begins depreciating assets using a short recovery period and/or a rapid recovery method may later

Chapter Money Education 13-1

Chapter 13 Nontaxable transaction Realized gain/loss not currently recognized Recognition is postponed to a future date Basis, potential depreciation recapture, and holding period carry over Tax-free transaction

Chapter 13 Nontaxable transaction Realized gain/loss not currently recognized Recognition is postponed to a future date Basis, potential depreciation recapture, and holding period carry over Tax-free transaction

Highlights from the 199A Proposed Regulations

Highlights from the 199A Proposed Regulations August 13, 2018 Kristine A. Tidgren Treasury and the IRS released IRC 199A proposed regulations, REG-107892-18, on August 8, 2018. The regulations will not

Highlights from the 199A Proposed Regulations August 13, 2018 Kristine A. Tidgren Treasury and the IRS released IRC 199A proposed regulations, REG-107892-18, on August 8, 2018. The regulations will not

Oil and Gas Tax Issues. Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP

Oil and Gas Tax Issues Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP Arnett Carbis Toothman llp 2018 Depletion and Ways to Compute What is depletion and what is its

Oil and Gas Tax Issues Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP Arnett Carbis Toothman llp 2018 Depletion and Ways to Compute What is depletion and what is its

1031 Tax Deferred Exchanges & International Investors

IRC 1031 Tax Deferred Exchange 1031 Tax Deferred Exchanges & International Investors Diane O. Rivera, CES Vice President IPX1031 Diane.Rivera@ipx1031.com - 1 - Introduction U.S. Internal Revenue Code Section

IRC 1031 Tax Deferred Exchange 1031 Tax Deferred Exchanges & International Investors Diane O. Rivera, CES Vice President IPX1031 Diane.Rivera@ipx1031.com - 1 - Introduction U.S. Internal Revenue Code Section

Section 1031 Exchanges: A Legitimate Tax Shelter for Business

MAY 2004 Section 1031 Exchanges: A Legitimate Tax Shelter for Business By Christian M. McBurney Engaging in a like-kind exchange under IRC section 1031 is one of the few legitimate tax shelters available

MAY 2004 Section 1031 Exchanges: A Legitimate Tax Shelter for Business By Christian M. McBurney Engaging in a like-kind exchange under IRC section 1031 is one of the few legitimate tax shelters available

Realty Exchange Corporation

Realty Exchange Corporation The attached information will help explain the steps to create a successful taxdeferred exchange to: Save Thousands of Dollars in Taxes! Realty Exchange Corporation is one of

Realty Exchange Corporation The attached information will help explain the steps to create a successful taxdeferred exchange to: Save Thousands of Dollars in Taxes! Realty Exchange Corporation is one of

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. Twenty third Edition (August 2015)

") LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Managers Staff File Twenty third Edition (August 2015) Highlights of this Edition The following are some of the important update

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Managers Staff File Twenty third Edition (August 2015) Highlights of this Edition The following are some of the important update

Instructions for Income Tax Return for Trusts and Estates (Form S128-TE) For Year Ended 31 March 2018

For Year Ended 31 March 2018") Instructions for Income Tax Return for Trusts and Estates (Form S128-TE) For Year Ended 31 March 2018 General Instructions Which Trusts and Estates Must File an Income Tax Return A trust is a legal arrangement

Instructions for Income Tax Return for Trusts and Estates (Form S128-TE) For Year Ended 31 March 2018 General Instructions Which Trusts and Estates Must File an Income Tax Return A trust is a legal arrangement

IRC Section 1031 Exchange: A Powerful Financial Tool For The Agricultural Family

IRC Section 1031 Exchange: A Powerful Financial Tool For The Agricultural Family An Educational Resource From Solid Rock Wealth Management By Christopher Nolt, LUTCF Introduction The IRC Section 1031 Exchange

IRC Section 1031 Exchange: A Powerful Financial Tool For The Agricultural Family An Educational Resource From Solid Rock Wealth Management By Christopher Nolt, LUTCF Introduction The IRC Section 1031 Exchange

Federal Income Taxation Chapter 5 Capital Appreciation

Presentation: Federal Income Taxation Chapter 5 Capital Appreciation Professors Wells September 12, 2017 CH 2-4 Capital Appreciation Tax Basis Recovery p.225 61(a)(3) gross income includes gains derived

Presentation: Federal Income Taxation Chapter 5 Capital Appreciation Professors Wells September 12, 2017 CH 2-4 Capital Appreciation Tax Basis Recovery p.225 61(a)(3) gross income includes gains derived

Teresa Person, CES Course No Provider No. 0001

Teresa Person, CES tperson@1031exchangecorp.com Historical Perspective Original Tax Law Defers or Eliminates Tax on Capital Gains Gain or loss is not recognized when property held for use in trade or

Teresa Person, CES tperson@1031exchangecorp.com Historical Perspective Original Tax Law Defers or Eliminates Tax on Capital Gains Gain or loss is not recognized when property held for use in trade or

Inland Private Capital Corporation Exchange Solutions & Investing in Private Placements A Presentation for Certified Public Accountants

Inland Private Capital Corporation 1031 Exchange Solutions & Investing in Private Placements A Presentation for Certified Public Accountants Disclaimers Investments are suitable for accredited investors

Inland Private Capital Corporation 1031 Exchange Solutions & Investing in Private Placements A Presentation for Certified Public Accountants Disclaimers Investments are suitable for accredited investors

Charitable Gifts. Carolyn M. Osteen

Charitable Gifts Carolyn M. Osteen A. Income Tax Deduction For Charitable Gifts 1. The percentage limitations for income tax deductions for charitable contributions by individuals. a. Basic limit: 50 percent

Charitable Gifts Carolyn M. Osteen A. Income Tax Deduction For Charitable Gifts 1. The percentage limitations for income tax deductions for charitable contributions by individuals. a. Basic limit: 50 percent

Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Exchanges - Concepts and Tax Implications

Exchanges - Concepts and Tax Implications Course Description While tax reform visions have changed the tax on profits realized from the disposition of real estate, investors still seek escape hatches from

Exchanges - Concepts and Tax Implications Course Description While tax reform visions have changed the tax on profits realized from the disposition of real estate, investors still seek escape hatches from

2017 National Conference on Special Needs Planning. Trust Income, Trust Expenses and Calculating Distributable Net Income Bradley J.

2017 National Conference on Special Needs Planning and Special Needs Trusts Trust Income, Trust Expenses and Calculating Distributable Net Income Bradley J. Frigon Law Offices of Bradley J. Frigon 6500

2017 National Conference on Special Needs Planning and Special Needs Trusts Trust Income, Trust Expenses and Calculating Distributable Net Income Bradley J. Frigon Law Offices of Bradley J. Frigon 6500

MEMORANDUM. Ronald Frump ( Frump ) is the CEO of Frump International, Inc. ( Frump Inc. ). Frump

is the CEO of Frump International, Inc. ( Frump Inc. ). Frump") MEMORANDUM TO: Senior Partner FROM: J.D. Team Number 22 DATE: November 12, 2007 SUBJECT: 2007 Law Student Tax Challenge Problem I. Introduction Ronald Frump ( Frump ) is the CEO of Frump International,

MEMORANDUM TO: Senior Partner FROM: J.D. Team Number 22 DATE: November 12, 2007 SUBJECT: 2007 Law Student Tax Challenge Problem I. Introduction Ronald Frump ( Frump ) is the CEO of Frump International,

Instructions for Form 4562

2016 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

2016 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Depreciation, Cost Recovery, Amortization, and Depletion

C H A P T E R 8 Depreciation, Cost Recovery, Amortization, and Depletion L E A R N I N G O B J E C T I V E S : After completing Chapter 8, you should be able to: LO.1 LO.2 LO.3 LO.4 State the rationale

C H A P T E R 8 Depreciation, Cost Recovery, Amortization, and Depletion L E A R N I N G O B J E C T I V E S : After completing Chapter 8, you should be able to: LO.1 LO.2 LO.3 LO.4 State the rationale

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

Tax Deferred 1031 Real Property Exchanges

Realtors Land Institute presents Tax Deferred 1031 Real Property Exchanges A Land University Course Facilitator Guide Copyright 2004 by the, an affiliate of the National Association of REALTORS. All rights

Realtors Land Institute presents Tax Deferred 1031 Real Property Exchanges A Land University Course Facilitator Guide Copyright 2004 by the, an affiliate of the National Association of REALTORS. All rights

Chapter Two - Formation of a Corporation

Chapter Two - Formation of a Corporation Fundamental income tax elements: 1) Transferor: 351(a) - nonrecognition treatment applicable to the asset transferor (if certain conditions are met); otherwise:

Chapter Two - Formation of a Corporation Fundamental income tax elements: 1) Transferor: 351(a) - nonrecognition treatment applicable to the asset transferor (if certain conditions are met); otherwise:

Instructions for Form 4562

2000 Department Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue Code unless otherwise noted. of the Treasury

2000 Department Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue Code unless otherwise noted. of the Treasury

Paper F6 (LSO) Taxation (Lesotho) Tuesday 12 June Fundamentals Level Skills Module. Time allowed

Taxation (Lesotho) Tuesday 12 June Fundamentals Level Skills Module. Time allowed") Fundamentals Level Skills Module Taxation (Lesotho) Tuesday 12 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

Fundamentals Level Skills Module Taxation (Lesotho) Tuesday 12 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

Chapter 2 Property Acquisition and Cost Recovery SOLUTIONS MANUAL

Chapter 2 Property Acquisition and Cost Recovery SOLUTIONS MANUAL Discussion Questions 1. [LO 1] Explain why the tax laws require the cost of certain assets to be capitalized and recovered over time rather

Chapter 2 Property Acquisition and Cost Recovery SOLUTIONS MANUAL Discussion Questions 1. [LO 1] Explain why the tax laws require the cost of certain assets to be capitalized and recovered over time rather

UPSTREAM OIL AND GAS LIKE-KIND EXCHANGE TRANSACTIONS AFTER TAX REFORM

FEBRUARY 27, 2018 UPSTREAM OIL AND GAS LIKE-KIND EXCHANGE TRANSACTIONS AFTER TAX REFORM Tax Executives Institute Houston Chapter Presented by Julia Pashin and Megan James BIOGRAPHY JULIA PASHIN Summary

FEBRUARY 27, 2018 UPSTREAM OIL AND GAS LIKE-KIND EXCHANGE TRANSACTIONS AFTER TAX REFORM Tax Executives Institute Houston Chapter Presented by Julia Pashin and Megan James BIOGRAPHY JULIA PASHIN Summary

How To Depreciate Property

Department of the Treasury Internal Revenue Service Publication 946 Contents Future Developments 2 What's New for 2015 2 Cat No 1081F What's New for 2016 2 How To Depreciate Property Reminders 2 Section

Department of the Treasury Internal Revenue Service Publication 946 Contents Future Developments 2 What's New for 2015 2 Cat No 1081F What's New for 2016 2 How To Depreciate Property Reminders 2 Section

THE TAX CUTS AND JOBS ACT & AGRICULTURAL PRODUCERS. KRISTINE TIDGREN, Ames, Iowa Center for Agricultural Law & Taxation, Iowa State University

THE TAX CUTS AND JOBS ACT & AGRICULTURAL PRODUCERS KRISTINE TIDGREN, Ames, Iowa Center for Agricultural Law & Taxation, Iowa State University October 2018 0 1 TABLE OF CONTENTS I. INTRODUCTION...3 II.

THE TAX CUTS AND JOBS ACT & AGRICULTURAL PRODUCERS KRISTINE TIDGREN, Ames, Iowa Center for Agricultural Law & Taxation, Iowa State University October 2018 0 1 TABLE OF CONTENTS I. INTRODUCTION...3 II.

Instructions for Form 4562

2017 Instructions for Form 4562 Department of the Treasury Internal Revenue Service Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue

2017 Instructions for Form 4562 Department of the Treasury Internal Revenue Service Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue

"This document may not be used or cited as precedent. Section 6110(j)(3) of the Internal Revenue Code,"

(3) of the Internal Revenue Code,") PRIVATE RULING 200440002; 2004 PRL LEXIS 762, * PRIVATE RULING 200440002 "This document may not be used or cited as precedent. Section 6110(j)(3) of the Internal Revenue Code," Section 1031 -- Like-Kind

PRIVATE RULING 200440002; 2004 PRL LEXIS 762, * PRIVATE RULING 200440002 "This document may not be used or cited as precedent. Section 6110(j)(3) of the Internal Revenue Code," Section 1031 -- Like-Kind