Farmer and Farmland Owner Income Tax Webinar. Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension

|

|

|

- Anissa Wade

- 5 years ago

- Views:

Transcription

1 Farmer and Farmland Owner Income Tax Webinar Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension

2 Chris Bruynis

3 Circular 230 Disclosure The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and authoritative information concerning the subject matter covered, but it is communicated with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional services. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.

4 Teaching Objectives Discuss Key Provisions of Tax Cuts & Job Act of 2017 Which May Impact Farm Operations. General Tax Provisions Schedule A Deductions Federal Estate Tax Depreciation Changes Like-Kind Exchanges Net Operating Loss Qualified Business Deduction 199A and Ag. & Horticultural Cooperatives

5 2018 Farmers Tax Guide Get a copy of the Farmer s Tax Guide at your local County Extension office or access it on-line at:

6 New Tax Brackets The new tax brackets are effective for years after December 31, 2017 and expire after December 31, The income tax brackets will be adjusted for inflation after December 31, 2018 and rounded up to the next lowest multiple of $100 in future years.

7 Head of Household The tax act retains the head-of-household filing status that originally was to be eliminated under the House legislation. However, the new tax act requires the Treasury department to issue due diligence requirements that pertain to paid preparers in determining whether or not an individual qualifies to file as head of household. A penalty of $500 per instance is to be assessed against paid preparers who fail to meet the requirements for determining the correct status.

8 Individual

9 Married Filing Jointly 2017 Tax Brackets 2018 tax brackets Rate Income Bracket Rate Income Bracket 10% $0 - $18,649 10% $ 0 - $19,049 15% $18,650 - $75,899 12% $19,050 - $77,399 25% $75,900 - $153,099 22% $77, ,999 28% $153,100 - $233,349 24% $165,000 - $314,999 33% $233,350 - $416,699 32% $315,000 - $399,999 35% $416,700 - $470,699 35% $400,000 - $599, % $470, % $600,000+

10 Long-Term Capital Gains Rate 2017 Tax Brackets 2018 Tax Brackets Tax Bracket Capital Gains Rate Income Bracket Capital Gains Rate 10% 0% S $0 $38,600 0% 15% 0% MFJ $0 $77,200 0% 25% 15% S $38,601 $425,800 15% 28% 15% MFJ $77,201 $479,000 15% 33% 15% S $425, % 35% 15% MFJ $479, % 39.60% 20%

11 Standard Deductions & Exemptions Filing Status Deduction Deduction Single $6,350 $12,000 Married Filing Jointly $12,700 $24,000 Head of Household $9,350 $12,000 Personal Exemption $4,050 none

12 Standard Deduction The additional standard deduction for the elderly and blind are retained and, thus, not changed. For years after 2018, the standard deduction will be indexed for inflation using the chained consumer price index for urban consumers.

13 Schedule A Deductions 1. State/Local/Property Tax (SALT) 2. Medical and Dental Expense Deduction 3. Home Mortgage Interest Deduction 4. Personal Casualty & Theft Loss Deduction 5. Charitable Contribution Deductions 6. Misc. Itemized Deductions Subject to 2% Floor

14 State and Local Taxes (SALT) Deductions Under the new plan, taxpayers who itemize will be able to deduct their state individual income, sales and property taxes up to a limit of $10,000 in total starting in 2018 ($5,000 for individual filers). Previously, the deduction was unlimited. deduct either individual income taxes or sales taxes. property taxes previously were also entirely deductible.

15 SALT Deduction - Business Please note that this provision DOES NOT pertain to the taxes accrued or paid in carrying on a trade or business.

16 Medical and Dental Expenses Medical and dental expenses remain in place but are tweaked. Before tax reform excess above 10% of your adjusted gross income (AGI). AGI $40,000; medical expenses $5,000 $5,000 - (10% x $40,000 = $4,000) = $1,000. After tax reform - 7.5% is in place for two years retroactive to January 1, AGI $40,000; medical expenses $5,000 $5,000 - (7.5% x $40,000 = $3,000) = $2,000.

17 Home Mortgage Interest Interest on up to $750,000 in mortgage debt can be deducted This cap affects home purchases made after December 14, A mortgage from December 14 or earlier Deduct interest on up to $1 million in debt (the old cap) Prior to the new law, interest on up to $100,000 in home equity debt was also deductible meaning interest on $1.1 million could be claimed. The new legislation wiped out the deduction for home equity debt, including on existing loans, beginning in 2018 unless used to substantially improve home.

18 Casualty and Theft Losses Casualty losses were eligible prior to 2018 as itemized deductions to the extent that they exceeded $100 plus 10% of your adjusted gross income. Events included natural disasters, fires, robberies, and other qualifying occurrences. The new law now preserves the deduction only for disasters for which a presidential disaster area declaration was made. Property used in trade or business still qualifies

19 Charitable Contribution Deductions Itemized charitable deduction remained unchanged. However with the higher standardized deduction, this may be a moot point. Filers who plan their charitable gifts may be able to get themselves over the new standard deduction and itemize if they use a strategy called "bunching."

20 Schedule A Deductions Miscellaneous deductions which exceed 2% of your AGI will be eliminated for the tax years 2018 through This includes deductions for unreimbursed employee expenses and tax preparation expenses. It includes expenses that you incur in your job that are not reimbursed, like tools and supplies; required uniforms not suitable for ordinary wear; dues and subscriptions; and job search expenses. These expenses also include unreimbursed travel and mileage, as well as the home office deduction.

21 Schedule A Deductions Please note that the elimination of unreimbursed employee expenses only affects taxpayers who claim an employee-related deduction on Schedule A. As a business owner filing a Schedule C or Schedule F, your business-related deductions are not affected by the elimination of Schedule A deductions.

22 Hobby Farm Example Hobby farm expenses can be entered to offset hobby farm income on Schedule A under other income. With the larger standardized deduction, these may be lost under the new rules. Before, if you claimed the income and deducted the itemized deduction it cancelled each other out. Now if you claim the income and cannot itemize (standard deduction is larger) your hobby farm may increase your net tax liability

23 Timber Considerations Ownership Issues Owned as a business schedule C Timber expenses are fully deductible including state and local taxes Owned as an investment Schedule A Timber expenses are no longer deductible Option to elect state and local property taxes as part of the timber costs (capitalize the expenses) and deduct upon sale of timber. Schedule A deductions limited to $10,000

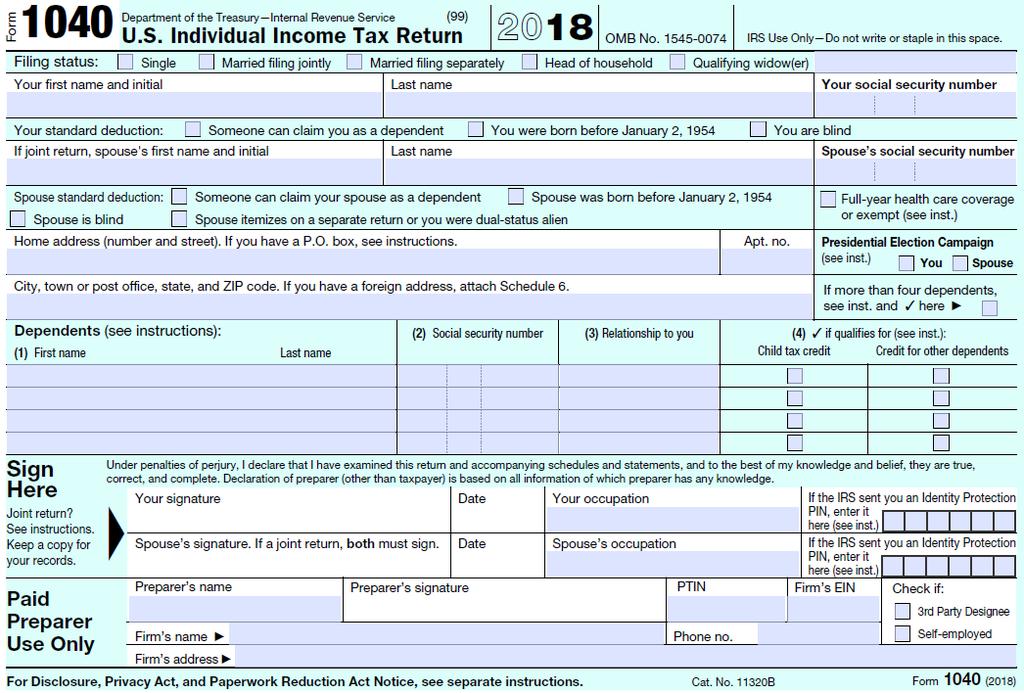

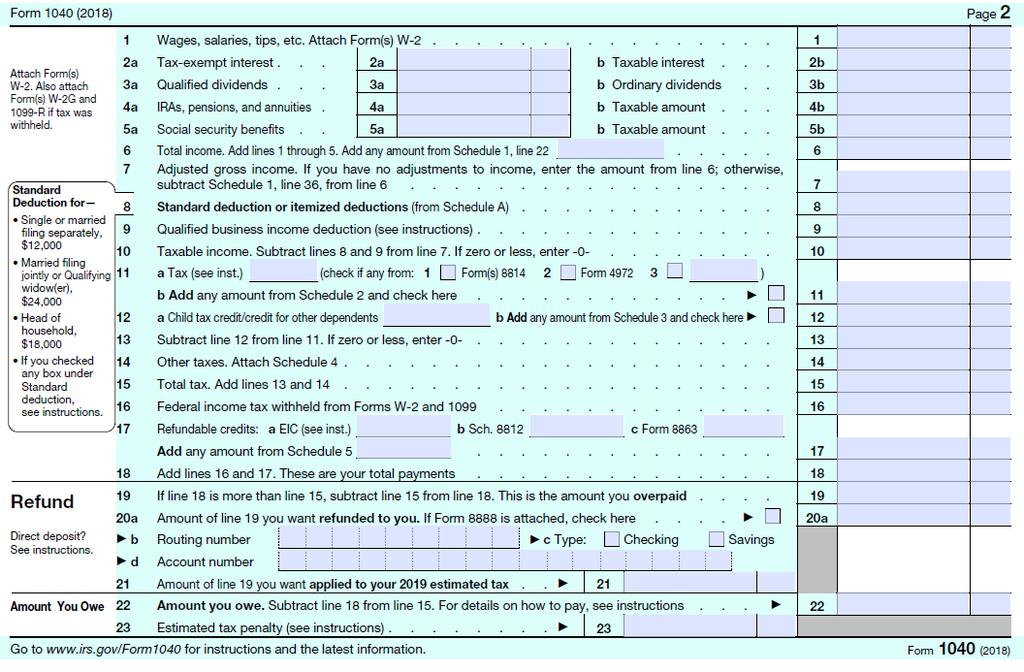

24 New 1040

25 New 1040

26 David Marrison

27 Topics 1. Estate & Gift Tax Update 2. Farm Equipment Depreciation 3. First Year Depreciation 4. Section 179 Expensing 5. Like Kind Exchanges 6. Net Operating Loss 7. Cash Accounting

28 Federal Estate Tax

29 Federal Estate Tax Federal Exemption was $5,490,000 for Tax Reform increased limit- $11,180,000 for Excess taxed at maximum of 40%. Annual gift exclusion is $15,000. Step up in basis has been continued. In 2026, will revert back 2017 levels.

30 Ohio Estate Tax As of January 1, 2013, the Ohio Estate Tax has been repealed.

31 Don t Let Sleeping Dogs Lie

32 Equipment Depreciation

33 Class Life of Assets Prior to New Tax All assets are placed into an asset class (regardless of the practical or real useful life of the asset. MACRS Classes: 3, 5, 7, 10, 15, 20, 27.5, & 39 3 year: breeding hogs, non-race horses over 12 years old. 5 year: breeding livestock, goats, dairy cattle, sheep, trailers, computers/calculators, logging equipment, solar property, & farm truck 7 year: farm equipment & machinery, grain bins, fences, office equipment, horses, younger than 12 years old, anaerobic digesters 10 year: greenhouse, single purpose structures, orchards, & vineyards. 15 year drainage tile & paved lots 20 year: farm buildings & storage (apples, onion, potato)

34 Modified Accelerated Cost Recovery System (MACRS) General Depreciation System 150% Declining Balance- used for farm equipment* 200% Declining Balance Straight line Alternative Depreciation System Straight line

35 A Comparison of Depreciation Schedules Year MACRS 150% MACRS 200% Straight-Line 2018 (1/2 Year) $5,357 $7,143 $3, $9,566 $12,245 $7, $7,516 $8,746 $7, $6,124 $6,247 $7, $6,124 $4,462 $7, $6,124 $4,462 $7, $6,124 $4,462 $7, (1/2 Year) $3,062 $2,231 $3,571 For Used Tractor: Purchase Price of $50,000

36 Changes for Farm & Machinery Depreciation Cost recovery period is now 5 years (not 7) for new farm machinery and equipment. Grain bins, fences, and used equipment stay as 7 year assets. 200% declining balance is to be used on 3, 5, 7 and 10 year property. 150% declining balance on 15 and 20 year property. Trees and vines are 10 year property previously SL, now 150 DB.

2018- $86,000 depreciation ($430,000/5 x.")

37 What a Difference a Year Makes $430,000 new combine purchase with out Bonus or Section 179 Depreciation $46,071 depreciation ($430,000/7 x.5 x 150%) $86,000 depreciation ($430,000/5 x.5 x 200%) $39,929 more

38 Accelerated Depreciation Bonus Depreciation Section 179

39 A Look Back at Previous Bonus Depreciation Rules Bonus Depreciation Requirements: Recovery period of 20 years or less Original use commenced with Taxpayer. Property required to be depreciated through Alternative Depreciation System (ADS) is not eligible for this deduction. Placed in service before1/1/2020.

40 Old Phase Out Bonus Depreciation Rules 50% deduction allowed through % for % for % for 2020 and later

41 NEW Bonus Depreciation Rules Expands to 100% for next five years. For property placed in service after 9/27/2017. Recovery period still 20 year or less. Removes requirement that usage must begin with taxpayer. Both new and used equipment is eligible. Family sale restrictions.

42 New Phase Out Bonus Depreciation Rules 100% through % for % for % for % for % for 2027 and beyond

43 Section 179-Equipment Expensing Can expense new or used equipment in year of purchase. Cannot exceed the taxable income derived from the business. Cannot create a loss.

44 Section 179-Equipment Expensing I.R.C. 179 deduction was $510,000 with $2,030,000 phase-out limit ($1 for $1) in For 2018, has expanded to $1 million with a $2.5 million dollar phase-out limit ($1 for $1). Will be indexed for inflation for future years. Provisions are not set to expire.

45 Interest Expense Limitation Taxpayers with 3-year average gross receipts over $25 million are subject to interest deduction limits: Limited to 30% of adjusted taxable income Can elect out, but must then use ADS on property in 10- year or greater MACRS life.

46 Excessive Depreciation Concerns This increase in the rate of depreciation for many farm assets, combined with the shorter MACRS recovery class for new farm equipment and machinery, may generate more depreciation than is needed by some taxpayers. The taxpayer can elect to use the SL method of depreciation and now may also elect to use the 150% method. Both elections are made on a class-by-class basis each year. To further reduce the amount of depreciation, the taxpayer may elect to use the alternative depreciation system (ADS), which calculates depreciation using the SL method and lengthens the recovery period.

47 Like Kind Exchanges

48 No Like Kind Exchange for Personal Property 1031 now only applies to real property (land) under the TCJA. Farm equipment and breeding heifers not eligible. Equipment trade-ins are now immediate (in the year) taxable events. Most likely result will be taxable gain. Offset is increased basis for depreciation.

49 Amos Buys Tractor Under Old Rules 2017 New Tractor Cost- $397,000 Tractor for Trade In- $112,000 Reduced Cash Amount- $285,000 Old Tractor Basis- $61,262 So Basis for depreciation Is- $346,262 No gain was recognized on disposition of tractor.

50 Amos Buys Tractor Under New Rules 2018 Tractor for Trade In- $112,000 Old Tractor Basis- $61,262 Taxable Gain $50,738 (Part III, Form 4797) New Tractor Cost- $397,000 New Basis for depreciation Is- $397,000

51 So what does Amos Do? Simply think of it as a sale of the used piece of equipment and the purchase of the new piece of equipment. Elect to take offset the taxable gain of $50,738 by using I.R.C. 179 (provided he is under investment limit of $2,500,000.) or use bonus depreciation.

52 Cautions/Observations Some taxpayers may not always be able to immediately offset the gain recognized by taxable exchanges. May already have used the maximum $1,000,000 section 179 deduction or may have exceeded the $2,500,000 investment limit on qualifying purchases. May not want to use bonus depreciation because it applies to the entire recovery class basis. This may create more than the optimal amount of depreciation expense.

53 Farm Loss Deduction Limits

54 Farm Net Operating Losses under TCJA 5-year carryback for farm losses eliminated. 2-year carryback for nonfarm losses eliminated. Farms still have this option. Carryover loss deduction limited to 80%. Unlimited carryover. Farmers may elect out of 2-year carry back.

55 Cash Accounting

56 Cash Accounting Expands who may use cash accounting. Can now use cash accounting if < $25 million in gross receipts. Was <$5 million Impacts C Corps

57 David L. Marrison, Extension Educator Coshocton County Extension 724 South 7th Street, Room 110 Coshocton, Ohio Thank You!

58 Barry Ward

59 Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018 (AtPfRPtTIIaVotCRotBfFY2018) Also known as the: Tax Cuts and Jobs Act (TCJA) Signed into law on December 22nd, 2017

60 New Tax Rate C-Corporations One of the cornerstones of the Tax Cuts and Jobs Act (TCJA) was to reduce tax rate for C-Corporations. Was permanently reduced to a flat 21%.

61 Corporate Tax Pre TCJA C-corporation Rate through December 31, 2017

62 New Tax Rate C-Corporations Medium to larger C-Corps benefit Smaller C-Corps don t benefit A C-Corp with net income less than $96,500 was better off with the old C-Corp rates (in terms of rates only!) Corporate AMT is repealed for tax years beginning after Dec 31, 2017.

63 New IRC Section 199A Deduction for Qualified Business Income A deduction in the amount of 20% is allowed for pass through entities - sole proprietorships, partnerships, and S corporations (LLCs are included) from Qualified Business Income from what is termed a Qualified Trade or Business This deduction allows for continued tax neutrality between business entity types

64 New IRC Section 199A Deduction Determine Qualified Business Income (QBI). Includes Schedule C, F, E, Form 4797 recapture, Form 4835 There are a number of definitions, thresholds, and limitations that apply to this deduction. Generally the 199A deduction for QBI is the lesser of: 20% of combined QBI or 20% of taxable income minus net capital gain-qualified cooperative dividends.

65 New IRC Section 199A Deduction for Qualified Business Income Also known as (AKA): 199A Deduction for Pass Through Entities 199A Deduction Business Deduction Pass-through Entity Deduction Pass-through Business Deduction QBI Deduction

66 Definitions for QBI Deduction Qualified Business Income (QBI) - is the net amount of qualified items of income, gain, deduction, and loss with respect to any qualified trade or business of the taxpayer. Trade or Business- taxpayer must be involved in the activity with continuity and regularity and the taxpayer s primary purpose for engaging in the activity must be for income or profit. See: I.R.C & Commissioner v. Groetzinger

67 QBI Deduction The QBI Deduction is claimed on the individual s tax returns whether an individual itemize deductions (Sch A) or does not itemize. This deduction reduces taxable income and is 20% of qualifying business income (or 20% of taxable ordinary income).

68 QBI Deduction Example: You make $100,000 in a pass-through business but with the new standard deduction ($24,000) your taxable income is $76,000 (assume all income is ordinary) Your deduction is the lesser of: 20% of $100,000 = $20,000 20% of $76,000 = $15,200 Deduction is $15,200

69 QBI Deduction Married Filing Jointly No Dependents - No Wage Income FACTS FROM 1040 & Sch. 1 BACK PAGE 1040 W-2 WAGES $0 SCH F $100K SCH D (THIS ALWAYS GETS DEDUCTED!!!) SCH C SCH E (Front & Back Page) AGI $100K STD DED/ITEMIZE $24K NET TAXABLE INC $76K QBI DEDUCTION $15,200 TAXABLE INCOME $60, S NET, 1065 NET, GUARANTEED PAYMENTS, 1041 AGI $100K QBI Deduction: $100K X 20% = $20,000 QBI Deduction: $76K X 20% = $15,200 QBI = LESSER OF: $15,200

70 QBI Deduction Married Filing Jointly No Dependents - Wage Income FACTS FROM 1040 & Sch. 1 BACK PAGE 1040 W-2 WAGES $24K SCH F $100K SCH D (THIS ALWAYS GETS DEDUCTED!!!) SCH C SCH E (Front & Back Page) AGI $124K STD DED/ITEMIZE $24K NET TAXABLE INC $100K QBI DEDUCTION $20,000 TAXABLE INCOME $80, S NET, 1065 NET, GUARANTEED PAYMENTS, 1041 AGI $124K QBI Deduction: $100K X 20% = $20,000 QBI Deduction: $100K X 20% = $20,000 QBI = LESSER OF: $20,000

71 QBI Deduction Limitations Specified Service Trade or Business Specified Service Trade or Business (SSTB): A specified service trade or business such as one that performs services in the health, law, consulting, athletics, financial services, brokerage services, accounting, or any trade or business where the principal asset is the reputation or skill of one or more of its employees or owners. Full 20% QBI Deduction if these businesses are under the bottom of the limitation phase-in range $157,500 Single or $315,000 MFJ No deduction if these business have Qualified Business Income greater than $207,000 Single or $415,000 MFJ (top of the phase-in range) Limited deductions in the phase-in ranges $ K Single $ K MFJ

72 QBI Deduction Limitations For individuals with taxable income of less than $157,500 for single filers and $315,000 for joint filers. The deductible amount for EACH qualified trade or business is 20% of the taxpayers qualified business income (QBI) Taxable income above these amounts results in limitation phase-ins

73 QBI Deduction - Limitations High Income Taxpayers Need Wages and/or Property to qualify For individuals with taxable income of more than $157,500 for single filers and $315,000 for joint filers. Limitation Phase-in amounts: $50,000 for single filers and $100,000 for joint filers Limitation Phase-in range for single filers: $157,000 - $207,000 Limitation Phase-in range for joint filers: $315,000 - $415,000

74 QBI Deduction Limitations Full 20% Deduction Wage Limitation Phase-in Range Full Wage Limitation Applies $0 $157,500 $315,000 $157,500 $315,000 $207,500 $415,000 $207,500 $415,000

75 QBI Deduction Limitations - SSTBs Full 20% Deduction Wage Limitation Phase-in Range No QBI Deduction Allowed $0 $157,500 $315,00 $157,500 $315,000 $207,500 $415,000 $207,500 $415,000

76 QBI - Limitations Once filers reach the top of the limitation phase-in range ($207,500 for single filers and $415,000 for joint filers) the calculations are simple (relatively): The deduction is the greater of: 50% of the W-2 wages paid by the business or The sum of 25% of the W-2 wages paid plus 2.5% of the depreciable property.

77 QBI Depreciable Property What is the depreciable property and how to calculate: Tangible property, subject to depreciation (meaning inventory doesn't count), which is held by the business at the end of the year and is used -- at ANY point in the year -- in the production of QBI. The depreciable period starts on the date the property is placed in service and ends on the LATER OF: 10 years OR the last day of the last full year in the asset's "regular" (not ADS) depreciation period.

78 QBI - Depreciable Property To illustrate, assume Ohio Farm purchases a piece of machinery on November 18, 2018 for 100,000. The machinery is used in the business, and is depreciated over 5 years. Even though the depreciable life of the asset is only 5 years, the owners of Ohio Farm will be able to take the unadjusted basis of $100,000 into consideration for purposes of this second limitation for ten full years, from , because the qualifying period runs for the LONGER of the useful life (5 years) OR 10 years.

79 QBI - Depreciable Property The basis taken into consideration is "unadjusted basis," meaning it is NOT reduced by any depreciation deductions. In fact, Section 199A(b)(2)(B)(ii) requires that you take into consideration the basis of the property "immediately after acquisition." Any asset that was fully depreciated prior to 2018, unless it was placed in service after 2008, will not count towards basis. Just as with W-2 wages, a shareholder or partner may only take into consideration for purposes of applying the limitation 2.5% his or her allocable share of the basis of the property. So if the total basis of S corporation property is $1,000,000 and you are a 20% shareholder, your basis limitation is $1,000,000 * 20% * 2.5% = $5,000.

80 QBI Limitation Calculation For example: You have $1,000,000 of qualified business income and you re potentially entitled to a $200,000 deduction but you exceed the threshold. Your business s wages equal $300,000 and you hold $1 million in depreciable property: Your deduction is the greater of: Wage: $300,000 x 50% = $150,000 Wage/Property Combo:$300,000 x 25% + $1mil x 2.5% = $100,000

are carried over to subsequent years to offset")

81 Qualified Business Losses & QBI Worksheet Qualified Business Losses (QBL) are carried over to subsequent years to offset QBI

82 Domestic Production Activities Deduction (DPAD) Repealed The deduction under IRC Section 199 known as the Domestic Production Activities Deduction (DPAD) is repealed effective January 1, This deduction was beneficial for Cooperatives and farms with employees earning W-2 wages.

83 Grain Glitch Fixed (Cooperative Glitch) Consolidated Appropriations Act 2018 signed on March 23, 2018 The 20-percent deduction calculated based upon their gross sales was eliminated and replaced with a hybrid Section 199A deduction Grain sales made prior to March 23 to Coops do not qualify under the temporary provision

84 Sales to Cooperatives Step 1: First, patrons calculate the 20 percent 199A QBI deduction that would apply if they had sold the commodity to a non-cooperative. But they don t stop there. Step 2: The patron must then subtract from that initial 199A deduction amount whichever of the following is smaller: 9 percent of net income attributable to cooperative sale(s) OR 50 percent of W-2 wages they paid to earn that income from the cooperative Step 3: Add back in cooperative's qualified production activities income (QPAI) attributable to that patron's sales.

85 Allocating the Deduction to Patrons Allocate the coop s deduction to patrons based on value of business w/ coop Sales to coops may result in a net QBI Deduction: Greater than 20% if the farmer taxpayer pays no W2 wages and coop passes through all or a large portion of the allocable QBI Equal to 20% if farmer taxpayer pays enough W2 wages to fully limit their coop sales QBI deduction to 11% and the coop passes through all allocable QBI Less than 20% if farmer taxpayer pays enough W2 wages to fully limit their coop sales QBI to 11% and the coop passes through less than the allocable QBI

86 QBI Deduction Coop Patron No Wages Paid Pat sold grain through coop $230K PURPIM, $20K patronage dividend $200K expenses no wages $50K QBI QBI Deduction is $10K (20%) reduced by lesser of ($50K x 9% = $4,500 or $0 x 50% = $0).so $10K

87 QBI Deduction Coop Patron with additional Pass-Through Deduction Same fact pattern as previous except Pat also got $2,500 deduction from coop QBI deduction is $12,500 ($10,000 + $2,500)

88 QBI Deduction Coop Patron with Wages Paid Same fact pattern as first example except. Pat paid $25,000 W-2 wages QBI deduction is $5,500 ($10K reduced by lesser of $4,500 or $12,500)

89 Sales to Both- Need to Segregate Income/Expenses Sales to Non- Cooperatives Sales to Cooperatives

90 Tracking and Calculating Coop Sales and Expenses Track expenses (including labor, machinery expenses, etc.) per field and allocate to those bushels sold to cooperatives Prorate total expenses from Schedule F on a per bushel/per cwt basis There may be incentive to increase NFI on coop sales vs non-coop sales depending on W-2 wages paid and the portion of QBI passes to patrons

91 Farm Lease Income and QBI Deduction Farm lease/rental income qualifies for the QBI deduction if conducted: For income/profit With continuity and regularity May be QBI even if: Not subject to SE tax Passive activity

92 Farm Lease Income and QBI Deduction Crop share landlords filing a Schedule F are eligible Crop share landlords filing Form 4835 may qualify (if they are materially participating they likely will) Landlords will likely have to pass as a trade or business according to IRC Section 162 Cash rent landlords filing a Schedule E may or may not qualify pending final regs Landlords will likely have to pass as a trade or business according to IRC Section 162

93 What Do You Think? Landowner who completely turns over management of the land to an agent, such as a professional farm management company, and does not otherwise materially participate in the farming operation, does not have SE income from renting land for agricultural use? A triple net lease arrangement, where the tenant pays the taxes, insurance, and maintenance, may not give rise to material participation, and it may not qualify for the QBI deduction. What minimum activity will qualify a cash rent income as QBI?

94 Farm Lease Income and QBI Deduction Farms with Multiple Entities: Proposed regulations indicate that common ownership of business entities allows the farmer to combine the rent income with the farm income an advantage Section 1231 Capital Gain Income: Will not qualify as QBI if the gain is treated as a capital gain likely not good for dairy producers

8 th Circuit not SE income So Outside 8 th Yes QBI, Inside 8 th No QBI? pp.")

95 Conservation Reserve Program Payments CRP payments quality for QBI if is a regular activity and for profit Subject to SE tax if actively engaged (unless receiving social security) 8 th Circuit not SE income So Outside 8 th Yes QBI, Inside 8 th No QBI? pp

96 QBI Deduction The QBI deduction will offset income tax liability and AMT however It will not reduce self-employment income or net investment income

97 QBI Deduction Things to remember if nothing else. The very large majority of farmers will be eligible for the entire 20% deduction! Qualified Business Income from sales to cooperatives will need to be tracked separately Cash rent income to cash rent landlords may or may not qualify

98 QBI Deduction Ohio Tax Ramifiactions Ohio bases individual tax calculations on adjusted gross income. This deduction is taken after the adjusted gross income calculation and therefore can not be claimed for Ohio taxable income calculations. Ohio does have a separate Business Income Tax Deduction

99 Business Meals Deduction The TCJA reduces the deduction for meals provided for the convenience of the employer to 50 percent through 2025 (was 100%) After 2025, the deduction is eliminated fully

100 Farmer Tax Strategy Entity Choice Which is best: Sole-proprietor, partnership, S-corp, C-corp Multiple entities Plan for some income to take advantage of QBID Zeroing out income may not be a planning goal Avoid NOLs if possible Conversion out of a C-Corp - lower penalty Avoid hobby farm filing Gross sales cost of goods sold Avoid investment ownership of timber

101 Farmer Tax Strategy Some W-2 wage income will allow farmer to maximize the QBI Deduction Charitable giving One possible method for farmers to contribute charitably is to gift commodities to the charitable organization escapes tax and avoids the limits due to new higher standard deductions Bunching personal deductions

102 Chris Bruynis: David Marrison: Barry Ward:

Farm Tax Update 1/21/2019. Teaching Objectives. Circular 230 Disclosure. Thank You Farmers Tax Guide

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Agricultural and Natural Resource Issues Chapter 9 pp National Income Tax Workbook

Agricultural and Natural Resource Issues Chapter 9 pp. 287-327 2018 National Income Tax Workbook Agricultural and Natural Resources Issues Barry Ward, Davis Marrison, and Chris Bruynis Ag Economy Update

Agricultural and Natural Resource Issues Chapter 9 pp. 287-327 2018 National Income Tax Workbook Agricultural and Natural Resources Issues Barry Ward, Davis Marrison, and Chris Bruynis Ag Economy Update

Agricultural and Natural Resource Issues Chapter 9 pp National Income Tax Workbook

Agricultural and Natural Resource Issues Chapter 9 pp. 287-327 2018 National Income Tax Workbook Agricultural and Natural Resources Issues Chris Bruynis, David Marrison, and Barry Ward Ag Economy Update

Agricultural and Natural Resource Issues Chapter 9 pp. 287-327 2018 National Income Tax Workbook Agricultural and Natural Resources Issues Chris Bruynis, David Marrison, and Barry Ward Ag Economy Update

The Tax Cuts & Jobs Act

The Tax Cuts & Jobs Act Ten Key Changes that May Impact You August 2, 2018 Contact Information Kristine Tidgren, ktidgren@iastate.edu www.calt.iastate.edu @CALT_IowaState 2 1. MANY CHANGES ARE HERE TODAY,

The Tax Cuts & Jobs Act Ten Key Changes that May Impact You August 2, 2018 Contact Information Kristine Tidgren, ktidgren@iastate.edu www.calt.iastate.edu @CALT_IowaState 2 1. MANY CHANGES ARE HERE TODAY,

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University Tax Planning

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

Impact of Tax Reform on Farmers. Tax and Accounting Department Fall 2018

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

Corporate Taxes. Standard Deduction: Estate & Trust Tax Rates

WEALTH ADVISORY OUTSOURCING AUDIT, TAX, AND CONSULTING Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor How Tax Reform Affects

WEALTH ADVISORY OUTSOURCING AUDIT, TAX, AND CONSULTING Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor How Tax Reform Affects

Agricultural & Natural Resource Issues Chapter 10 pp National Income Tax Workbook

Agricultural & Natural Resources Tax Issues Chris Bruynis David Marrison Barry Ward Associate Professor Associate Professor Assistant Professor bruynis.1@osu.edu marrison.2@osu.edu ward.8@osu.edu 740-702-3200

Agricultural & Natural Resources Tax Issues Chris Bruynis David Marrison Barry Ward Associate Professor Associate Professor Assistant Professor bruynis.1@osu.edu marrison.2@osu.edu ward.8@osu.edu 740-702-3200

AGRICULTURAL TAX. i n c o m e t a x e s

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

THE TAX CUTS AND JOBS ACT & AGRICULTURAL PRODUCERS. KRISTINE TIDGREN, Ames, Iowa Center for Agricultural Law & Taxation, Iowa State University

THE TAX CUTS AND JOBS ACT & AGRICULTURAL PRODUCERS KRISTINE TIDGREN, Ames, Iowa Center for Agricultural Law & Taxation, Iowa State University October 2018 0 1 TABLE OF CONTENTS I. INTRODUCTION...3 II.

THE TAX CUTS AND JOBS ACT & AGRICULTURAL PRODUCERS KRISTINE TIDGREN, Ames, Iowa Center for Agricultural Law & Taxation, Iowa State University October 2018 0 1 TABLE OF CONTENTS I. INTRODUCTION...3 II.

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA)

") Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

HIGHLIGHTS OF THE TAX CUTS AND JOBS ACT FOR AGRICULTURAL PRODUCERS

HIGHLIGHTS OF THE TAX CUTS AND JOBS ACT FOR AGRICULTURAL PRODUCERS by Kristine Tidgren I. INTRODUCTION The Tax Cuts and Jobs Act (TCJA) ushered in the most significant changes to our tax code in more than

HIGHLIGHTS OF THE TAX CUTS AND JOBS ACT FOR AGRICULTURAL PRODUCERS by Kristine Tidgren I. INTRODUCTION The Tax Cuts and Jobs Act (TCJA) ushered in the most significant changes to our tax code in more than

Farm Taxes. David L. Marrison, Associate Professor

Farm Taxes David L. Marrison, Associate Professor Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax

Farm Taxes David L. Marrison, Associate Professor Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax

Top Producer Seminar A New Tax Bill: What You Need To Know Now. Paul Neiffer, CPA January 25, 2018 Chicago, Illinois

Top Producer Seminar A New Tax Bill: What You Need To Know Now Paul Neiffer, CPA January 25, 2018 Chicago, Illinois Speaker Introduction Paul Neiffer, Principal, CliftonLarsonAllen Frequent national speaker

Top Producer Seminar A New Tax Bill: What You Need To Know Now Paul Neiffer, CPA January 25, 2018 Chicago, Illinois Speaker Introduction Paul Neiffer, Principal, CliftonLarsonAllen Frequent national speaker

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018 The TCJA s Impact on Farmers and Ranchers Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018 The TCJA s Impact on Farmers and Ranchers Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation

TAX REFORM INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

The following chart sets forth some of the provisions affecting individuals in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

Things to note before starting

A Taxation Focus Austin Duerfeldt Agricultural Economist Email: aduerfeldt2@unl.edu Phone: (402) 873-3166 Facebook: SE NE Ag Economist Twitter: SENE_AgEcon 2017 TAX CUTS AND JOBS ACT Things to note before

A Taxation Focus Austin Duerfeldt Agricultural Economist Email: aduerfeldt2@unl.edu Phone: (402) 873-3166 Facebook: SE NE Ag Economist Twitter: SENE_AgEcon 2017 TAX CUTS AND JOBS ACT Things to note before

HOW THE TCJA APPLIES TO YOUR FARMING (AND OTHER) BUSINESS LATTAHARRIS, LLP CLIENT SEMINARS JUNE 12-15, 2018

BUSINESS LATTAHARRIS, LLP CLIENT SEMINARS JUNE 12-15, 2018") HOW THE TCJA APPLIES TO YOUR FARMING (AND OTHER) BUSINESS LATTAHARRIS, LLP CLIENT SEMINARS JUNE 12-15, 2018 Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation Washburn University

HOW THE TCJA APPLIES TO YOUR FARMING (AND OTHER) BUSINESS LATTAHARRIS, LLP CLIENT SEMINARS JUNE 12-15, 2018 Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation Washburn University

In-depth Look at 199A & the Case for Non-Qualified Patronage After Tax Reform

In-depth Look at 199A & the Case for Non-Qualified Patronage After Tax Reform Presented by: Eric Krienert, Tax Director Moss Adams eric.krienert@mossadams.com 209-955-6118 What We Will Cover Today The

In-depth Look at 199A & the Case for Non-Qualified Patronage After Tax Reform Presented by: Eric Krienert, Tax Director Moss Adams eric.krienert@mossadams.com 209-955-6118 What We Will Cover Today The

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018 WHAT WE WILL COVER TODAY 1 2 Business & individual provisions of the Tax Cuts and Jobs

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018 WHAT WE WILL COVER TODAY 1 2 Business & individual provisions of the Tax Cuts and Jobs

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 Important Highlights for Individuals and Small Businesses On December 15, 2017, Congress released the 2017 Tax Cut and Jobs Act ( the Act ) that has now passed both the House

Tax Cuts and Jobs Act of 2017 Important Highlights for Individuals and Small Businesses On December 15, 2017, Congress released the 2017 Tax Cut and Jobs Act ( the Act ) that has now passed both the House

SPECIAL REPORT. Tax Law Essentials. Brought to you by Mercer Advisors

SPECIAL REPORT Tax Law Essentials Brought to you by Mercer Advisors Game-changing tax package The recently enacted Tax Cuts and Jobs Act (TCJA) is a sweeping, game-changing tax package. Here s a look at

SPECIAL REPORT Tax Law Essentials Brought to you by Mercer Advisors Game-changing tax package The recently enacted Tax Cuts and Jobs Act (TCJA) is a sweeping, game-changing tax package. Here s a look at

How Tax Reforms Impacts Your Vineyard February 8, Presented by: Kathy Freshwater, CPA Craig Anderson, CPA

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

Today s Outline. Tax Cuts and Jobs Act of 2017

Today s Outline Tax Cuts and Jobs Act of 2017 I. Introduction and Background II. Individual Income Tax III. Business Tax IV. Employment, Compensation and Retirement V. Tax-Exempt Organization VI. Estate

Today s Outline Tax Cuts and Jobs Act of 2017 I. Introduction and Background II. Individual Income Tax III. Business Tax IV. Employment, Compensation and Retirement V. Tax-Exempt Organization VI. Estate

Center for Agricultural Law & Taxation. Tax Cuts & Jobs Act. Key Provisions Impacting Agricultural Producers and Small Businesses June 12, 2018

Tax Cuts & Jobs Act Key Provisions Impacting Agricultural Producers and Small Businesses June 12, 2018 Contact Information Kristine Tidgren, ktidgren@iastate.edu www.calt.iastate.edu @CALT_IowaState 2

Tax Cuts & Jobs Act Key Provisions Impacting Agricultural Producers and Small Businesses June 12, 2018 Contact Information Kristine Tidgren, ktidgren@iastate.edu www.calt.iastate.edu @CALT_IowaState 2

TAX CUTS AND JOB ACT OF 2017 Highlights

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

TAX REFORM INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

The following chart sets forth some of the provisions affecting individuals in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

2018 TAX SEMINAR OPPORTUNITIES & IMPACTS. Tax Cuts and Jobs Acts Enacted December 22, Most changes go into effect January 1, 2018

2018 TAX SEMINAR OPPORTUNITIES & IMPACTS Tax Cuts and Jobs Acts Enacted December 22, 2017 Most changes go into effect January 1, 2018 S e m i n a r s p o n s o re d b y A n n L a u f m a n o f A L A F

2018 TAX SEMINAR OPPORTUNITIES & IMPACTS Tax Cuts and Jobs Acts Enacted December 22, 2017 Most changes go into effect January 1, 2018 S e m i n a r s p o n s o re d b y A n n L a u f m a n o f A L A F

2018 Spring Professional Advisor Seminar Presentation: Mike Martin

2018 Spring Professional Advisor Seminar Presentation: Mike Martin Today s Agenda not necessarily in this order Review of many (not all) important aspects of the: 2018 Tax Cut and Jobs Act (TCJA) What

2018 Spring Professional Advisor Seminar Presentation: Mike Martin Today s Agenda not necessarily in this order Review of many (not all) important aspects of the: 2018 Tax Cut and Jobs Act (TCJA) What

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

Farm/Ranch Accounting and Tax 101

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Farm/Ranch Accounting and Tax 101 Randy Netek, CPA & Brandt Self, CPA May 2018 CLAconnect.com The Agenda Tax Reform Basics of Accounting Documentation

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Farm/Ranch Accounting and Tax 101 Randy Netek, CPA & Brandt Self, CPA May 2018 CLAconnect.com The Agenda Tax Reform Basics of Accounting Documentation

I TAX REFORM FOR INDIVIDUALS

I TAX REFORM FOR INDIVIDUALS A. Simplification and Reform of Rates, Standard Deductions, and Exemptions 1. Reduction and simplification of individual income tax rates and modification of inflation adjustment

I TAX REFORM FOR INDIVIDUALS A. Simplification and Reform of Rates, Standard Deductions, and Exemptions 1. Reduction and simplification of individual income tax rates and modification of inflation adjustment

Business Tax. Pass-Through Entities. New 20% Deduction

Business Tax Pass-Through Entities New 20% Deduction For tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026, taxpayers who have domestic qualified business income (QBI) from a partnership,

Business Tax Pass-Through Entities New 20% Deduction For tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026, taxpayers who have domestic qualified business income (QBI) from a partnership,

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 INDIVIDUALS Standard Deduction Personal exemption State income tax/sales tax itemized deduction Mortgage interest Property taxes itemized deduction Tax brackets Alternative

Tax Cuts and Jobs Act of 2017 INDIVIDUALS Standard Deduction Personal exemption State income tax/sales tax itemized deduction Mortgage interest Property taxes itemized deduction Tax brackets Alternative

Tax Update Focusing on the Tax Cuts and Jobs Act of John F. Ermer, CPA Israel O. Perez, CPA

Tax Update Focusing on the Tax Cuts and Jobs Act of 2017 John F. Ermer, CPA Israel O. Perez, CPA Contact Information John F. Ermer, CPA E-mail: jermer@bhcbcpa.com Telephone: 203) 787-6527 Israel O. Perez,

Tax Update Focusing on the Tax Cuts and Jobs Act of 2017 John F. Ermer, CPA Israel O. Perez, CPA Contact Information John F. Ermer, CPA E-mail: jermer@bhcbcpa.com Telephone: 203) 787-6527 Israel O. Perez,

WHAT TAX REFORM MEANS FOR SMALL BUSINESSES & PASS-THROUGH ENTITIES. Julie Peters, Attorney Polston Tax Resolution & Accounting

WHAT TAX REFORM MEANS FOR SMALL BUSINESSES & PASS-THROUGH ENTITIES Julie Peters, Attorney Polston Tax Resolution & Accounting TAX CUT AND JOBS ACT The new tax law, called the Tax Cut and Jobs Act (TCJA),

WHAT TAX REFORM MEANS FOR SMALL BUSINESSES & PASS-THROUGH ENTITIES Julie Peters, Attorney Polston Tax Resolution & Accounting TAX CUT AND JOBS ACT The new tax law, called the Tax Cut and Jobs Act (TCJA),

Tax Cuts and Jobs Act of 2017

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

Breaking Down the Tax Cuts & Jobs Act of COPYRIGHT 2018 Bowles Rice LLP

Breaking Down the Tax Cuts & Jobs Act of 2017 COPYRIGHT 2018 Bowles Rice LLP Tax Avoidance is Good Anyone may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose

Breaking Down the Tax Cuts & Jobs Act of 2017 COPYRIGHT 2018 Bowles Rice LLP Tax Avoidance is Good Anyone may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER #1 Corporate Tax Rates New Corporate Flat Tax Rate of 21% replaces old graduated brackets

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER #1 Corporate Tax Rates New Corporate Flat Tax Rate of 21% replaces old graduated brackets

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

Business Tax Provisions

On December 22, 2017, President Trump signed the Tax Jobs and Cuts Act of 2017 (the Act). This will be the biggest tax overhaul in 30 years. The provisions below affect all entities from individuals to

On December 22, 2017, President Trump signed the Tax Jobs and Cuts Act of 2017 (the Act). This will be the biggest tax overhaul in 30 years. The provisions below affect all entities from individuals to

Tax Planning. and. Management Considerations. for Farmers in George F. Patrick Extension Agricultural Economist Purdue University

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

Tax cuts and jobs act

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

ESTIMATED KANSAS IMPACT OF THE FEDERAL TAX CUTS AND JOBS ACT

ESTIMATED KANSAS IMPACT OF THE FEDERAL TAX CUTS AND JOBS ACT KANSAS DEPARTMENT OF REVENUE FEBRUARY 14, 2018 Summary... 2 Individual Tax Reform... 8 Tax Rate Reform... 8 Deduction for Qualified Business

ESTIMATED KANSAS IMPACT OF THE FEDERAL TAX CUTS AND JOBS ACT KANSAS DEPARTMENT OF REVENUE FEBRUARY 14, 2018 Summary... 2 Individual Tax Reform... 8 Tax Rate Reform... 8 Deduction for Qualified Business

New Tax Rules. For You and Your Business Owners

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

The Tax Cuts and Jobs Act of 2017

The Tax Cuts and Jobs Act of 2017 is the most comprehensive revision to the Internal Revenue Code Since 1986. This new Tax Act reduces tax rates for individuals and corporations, repeals exemptions, eliminates

The Tax Cuts and Jobs Act of 2017 is the most comprehensive revision to the Internal Revenue Code Since 1986. This new Tax Act reduces tax rates for individuals and corporations, repeals exemptions, eliminates

Tax Reform: What You Need To Know

Tax Reform: What You Need To Know January 24, 2018 Presented by: Blake Harrison, CPA/PFS Senior Tax Manager LBMC Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on

Tax Reform: What You Need To Know January 24, 2018 Presented by: Blake Harrison, CPA/PFS Senior Tax Manager LBMC Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on

Government Affairs. The White Papers TAX REFORM.

Government Affairs The White Papers TAX REFORM www.independentagent.com January 3, 2018 Below is a summary of the provisions of the new tax reform law that are most likely to impact Big I members. This

Government Affairs The White Papers TAX REFORM www.independentagent.com January 3, 2018 Below is a summary of the provisions of the new tax reform law that are most likely to impact Big I members. This

Tax Cuts and Jobs Act 2017 HR 1

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

Adam Williams. Anthony Licavoli. Principal Tax Manager

1 2 Adam Williams Principal 734.302.4179 adam.williams@rehmann.com Anthony Licavoli Tax Manager 248.463.4598 anthony.licavoli@rehmann.com 3 4 5 What is your impression about the speed at which Congress

1 2 Adam Williams Principal 734.302.4179 adam.williams@rehmann.com Anthony Licavoli Tax Manager 248.463.4598 anthony.licavoli@rehmann.com 3 4 5 What is your impression about the speed at which Congress

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS. February 8, 2018 Bruce I. Booken Rose K. Wilson

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS February 8, 2018 Bruce I. Booken Rose K. Wilson The 2017 Tax Act Signed into law on December 22, 2017 Provisions apply NOW to taxable years beginning after

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS February 8, 2018 Bruce I. Booken Rose K. Wilson The 2017 Tax Act Signed into law on December 22, 2017 Provisions apply NOW to taxable years beginning after

Tax Update for 2018 and 2019

Tax Update for 2018 and 2019 Individual Tax Changes Business Tax Changes Depreciation Changes Inflation Adjustments IRS Mileage Rates Affordable Care Act Partnership Audit Rules The following is a summary

Tax Update for 2018 and 2019 Individual Tax Changes Business Tax Changes Depreciation Changes Inflation Adjustments IRS Mileage Rates Affordable Care Act Partnership Audit Rules The following is a summary

Tax Cuts and Jobs Act. Durham Chamber of Commerce Public Policy Meeting January 9, 2018

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

US TAX SYSTEM. # Important to Account for Impact of Taxes on Income. R we are concerned with after-tax cash flows (ATCF)

") US TAX SYSTEM # Important to Account for Impact of Taxes on Income R we are concerned with after-tax cash flows (ATCF) # Internal Revenue Service (IRS) R responsible for collecting taxes R regulations

US TAX SYSTEM # Important to Account for Impact of Taxes on Income R we are concerned with after-tax cash flows (ATCF) # Internal Revenue Service (IRS) R responsible for collecting taxes R regulations

Biggest tax bill in 30+ years redefines tax landscape

NBC Tower - Suite 1500 455 North Cityfront Plaza Drive Chicago, IL 60611 312.670.7444 www.orba.com Biggest tax bill in 30+ years redefines tax landscape On December 22, 2017, the most sweeping tax legislation

NBC Tower - Suite 1500 455 North Cityfront Plaza Drive Chicago, IL 60611 312.670.7444 www.orba.com Biggest tax bill in 30+ years redefines tax landscape On December 22, 2017, the most sweeping tax legislation

Tax Cuts and Jobs Act Real Estate Industry Impact. April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD

Tax Cuts and Jobs Act Real Estate Industry Impact April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD Topics for Today Rate Changes Business Interest Limitation Net Operating Losses Excess

Tax Cuts and Jobs Act Real Estate Industry Impact April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD Topics for Today Rate Changes Business Interest Limitation Net Operating Losses Excess

SENATE TAX REFORM PROPOSAL INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Senate Finance Committee s version of the Tax Cuts and Jobs Act bill, as approved by the Senate Finance Committee on November

The following chart sets forth some of the provisions affecting individuals in the Senate Finance Committee s version of the Tax Cuts and Jobs Act bill, as approved by the Senate Finance Committee on November

KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017

OF 2017") KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017 New tax laws resulting from the TCJA represent the most significant changes in our tax structure in more than 30 years. Most provisions for individuals

KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017 New tax laws resulting from the TCJA represent the most significant changes in our tax structure in more than 30 years. Most provisions for individuals

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU DISCLAIMER These materials, and the accompanying oral presentation, are for educational purposes only and are not intended to be written advice concerning

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU DISCLAIMER These materials, and the accompanying oral presentation, are for educational purposes only and are not intended to be written advice concerning

Income Tax Management for Farmers in 2011

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

TAX ORGANIZER Page 3

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

Tax Cuts & Jobs Act: What You Need to Know

TRI Tax Resolution Institute where your tax debt is your power! Tax Cuts & Jobs Act: What You Need to Know Presented by: Peter Y. Stephan, CPA February 20, 2018 Crossing the River... 2 Meet our speaker

TRI Tax Resolution Institute where your tax debt is your power! Tax Cuts & Jobs Act: What You Need to Know Presented by: Peter Y. Stephan, CPA February 20, 2018 Crossing the River... 2 Meet our speaker

TAX CUTS AND JOBS ACT SUMMARY

TAX CUTS AND JOBS ACT SUMMARY Mariner Retirement Advisors The Tax Cuts and Jobs Act ( TCJA ) was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and

TAX CUTS AND JOBS ACT SUMMARY Mariner Retirement Advisors The Tax Cuts and Jobs Act ( TCJA ) was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and

2018 Corporate/Business Tax Law Review

BUSINESS CONCEPTS MARCH 2018 2018 Corporate/Business Tax Law Review In our last tax article, we discussed how the 2017 Tax Cuts and Jobs Act (TCJA) brought many changes to individual income tax filers.

BUSINESS CONCEPTS MARCH 2018 2018 Corporate/Business Tax Law Review In our last tax article, we discussed how the 2017 Tax Cuts and Jobs Act (TCJA) brought many changes to individual income tax filers.

Aviation Tax Issues From The New Tax Changes: Opportunities, Challenges & Questions Sue Folkringa, CPA

Aviation Tax Issues From The New Tax Changes: Opportunities, Challenges & Questions Sue Folkringa, CPA 2018 NBAA Regional Forum San Jose, CA September 6, 2018 Wolcott & Associates, P.A. - What We Do We

Aviation Tax Issues From The New Tax Changes: Opportunities, Challenges & Questions Sue Folkringa, CPA 2018 NBAA Regional Forum San Jose, CA September 6, 2018 Wolcott & Associates, P.A. - What We Do We

Tax Cuts & Jobs Act (TCJA)

") Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

Corporate and Business Provision House Bill (HR 1) Senate Bill Final Bill

Senate Bill Final Bill") Selected provisions of the House and Senate tax reform bills as passed by both houses of Congress which resulted in the final bill in the far right column. Introduction: This summary contains what ZLQ

Selected provisions of the House and Senate tax reform bills as passed by both houses of Congress which resulted in the final bill in the far right column. Introduction: This summary contains what ZLQ

Tax Cuts and Jobs Act February 8, 2018

Tax Cuts and Jobs Act 2017 February 8, 2018 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any specific taxpayer

Tax Cuts and Jobs Act 2017 February 8, 2018 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any specific taxpayer

10/8/2018. First major tax reform since Signed into law by President Donald Trump on December 22, 2017.

First major tax reform since 1986. Signed into law by President Donald Trump on December 22, 2017. 1 Introduction n Changes n Personal side: set to expire 12/31/2025 n Business side: mostly permanent n

First major tax reform since 1986. Signed into law by President Donald Trump on December 22, 2017. 1 Introduction n Changes n Personal side: set to expire 12/31/2025 n Business side: mostly permanent n

KEIR EDUCATIONAL RESOURCES

INCOME TAX PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

INCOME TAX PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

NOACSC Tax Hot Topics. September 21, 2018 Christopher E. Axene, CPA

NOACSC Tax Hot Topics September 21, 2018 Christopher E. Axene, CPA Fringe Benefits - The Good (?) First rule of thumb cash (or its equivalent) paid to employees is always taxable unless it is a reimbursement

NOACSC Tax Hot Topics September 21, 2018 Christopher E. Axene, CPA Fringe Benefits - The Good (?) First rule of thumb cash (or its equivalent) paid to employees is always taxable unless it is a reimbursement

Tax Cuts and Jobs Act Passed by Congress

Tax Cuts and Jobs Act Passed by Congress On December 19 and 20, 2017, the House and Senate approved a final version of H.R. 1, the Tax Cuts and Jobs Act, renamed An Act to provide for reconcilation purusant

Tax Cuts and Jobs Act Passed by Congress On December 19 and 20, 2017, the House and Senate approved a final version of H.R. 1, the Tax Cuts and Jobs Act, renamed An Act to provide for reconcilation purusant

5/29/ TAX CUTS AND JOBS ACT OVERVIEW. Individual Tax. Introduction-Individual Provisions. Dauphin County Bar Association May 30, 2018

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

Channel Islands Chapter of the California Society of Enrolled Agents

Channel Islands Chapter of the California Society of Enrolled Agents IRS Regulations Clarify Business Pass-Through Deduction Article Highlights: Trade or Business Definition Qualified Business Income Limitation

Channel Islands Chapter of the California Society of Enrolled Agents IRS Regulations Clarify Business Pass-Through Deduction Article Highlights: Trade or Business Definition Qualified Business Income Limitation

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU THE TAX CUTS & JOBS ACT OF 2017 (HR 1) Preliminary Summary Analysis Presented by: A. Mac Stevens, CPA Member of the Eide Bailly LLP National Tax Office Ron

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU THE TAX CUTS & JOBS ACT OF 2017 (HR 1) Preliminary Summary Analysis Presented by: A. Mac Stevens, CPA Member of the Eide Bailly LLP National Tax Office Ron

Comparison of House and Senate Tax Reform Bills

Comparison of House and Senate Tax Reform Bills Provision Individual Rates (Single) 12% $0 - $44,999 25% $45,000 - $199,999 35% $200,000 - $499,999 39.6% $500,000 + Senate Version of H.R. 1, the 10% $0

Comparison of House and Senate Tax Reform Bills Provision Individual Rates (Single) 12% $0 - $44,999 25% $45,000 - $199,999 35% $200,000 - $499,999 39.6% $500,000 + Senate Version of H.R. 1, the 10% $0

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business August 10, 2018 Sarah Armstrong, Esq. Marjorie A. Rogers, Esq. Ed Street, CPA/ABV/CFF, CVA, ASA The information provided

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business August 10, 2018 Sarah Armstrong, Esq. Marjorie A. Rogers, Esq. Ed Street, CPA/ABV/CFF, CVA, ASA The information provided

Tax Reform Highlights

etax Alert Tax Reform Highlights Final Business/Corporate/Partnership Provisions in Tax Cuts and Jobs Act of 2017 Here is a chart that briefly summarizes the major provisions affecting our business clients,

etax Alert Tax Reform Highlights Final Business/Corporate/Partnership Provisions in Tax Cuts and Jobs Act of 2017 Here is a chart that briefly summarizes the major provisions affecting our business clients,

Tax Cuts and Jobs Act Construction Industry Impact

Tax Cuts and Jobs Act Construction Industry Impact Presented By: Sean M. Auger, Partner 1 Introduction Most but not all provisions effective for tax periods beginning after December 31, 2017 2 General

Tax Cuts and Jobs Act Construction Industry Impact Presented By: Sean M. Auger, Partner 1 Introduction Most but not all provisions effective for tax periods beginning after December 31, 2017 2 General

SENATE TAX REFORM PROPOSAL INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only

The following chart sets forth some of the provisions affecting individuals in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only

Business Changes in the Tax Cuts and Jobs Act. Alan D. Sobel, CPA December 27,

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

Davis & associates, p.a. Certified Public Accountants and Consultants

209 FEDERAL TAX RATES Davis & Associates, p.a. Certified Public Accountants and Consultants 97 Washingtonian Boulevard, Suite 550 Gaithersburg, Maryland 20878 Phone: 30.963.6696 Fax: 30.963.6693 www.daviscpas.com

209 FEDERAL TAX RATES Davis & Associates, p.a. Certified Public Accountants and Consultants 97 Washingtonian Boulevard, Suite 550 Gaithersburg, Maryland 20878 Phone: 30.963.6696 Fax: 30.963.6693 www.daviscpas.com

2017 TAX CUTS AND JOBS ACT

2017 TAX CUTS AND JOBS ACT A Taxation Focus Austin Duerfeldt Agricultural Economist Email: aduerfeldt2@unl.edu Phone: (402) 873-3166 Facebook: SE NE Ag Economist Twitter: SENE_AgEcon Things to note before

2017 TAX CUTS AND JOBS ACT A Taxation Focus Austin Duerfeldt Agricultural Economist Email: aduerfeldt2@unl.edu Phone: (402) 873-3166 Facebook: SE NE Ag Economist Twitter: SENE_AgEcon Things to note before

Tax Reform Webinar January 4, 2018

Tax Reform Webinar January 4, 2018 Speakers: Jerry Frumm Vice Chairman & Chief Investment Officer, Senior Lifestyle Jeanne McGlynn Delgado, Vice President Government Affairs, ASHA Randy Hardock Partner,

Tax Reform Webinar January 4, 2018 Speakers: Jerry Frumm Vice Chairman & Chief Investment Officer, Senior Lifestyle Jeanne McGlynn Delgado, Vice President Government Affairs, ASHA Randy Hardock Partner,

Tax Reform: What Dealers Need to Know

Tax Reform: What Dealers Need to Know 1 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication is not intended or written

Tax Reform: What Dealers Need to Know 1 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication is not intended or written

Integrity Accounting

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Understanding the Tax Reform Bill

Understanding the Tax Reform Bill JANUARY 23, 2018 Miguel G. Farra, CPA, JD Tax Chairman Emilio Escandon, CPA Managing Principal, NY Gary DuBoff, CPA, CFP Principal 1 Agenda I. Individuals II. Qualified

Understanding the Tax Reform Bill JANUARY 23, 2018 Miguel G. Farra, CPA, JD Tax Chairman Emilio Escandon, CPA Managing Principal, NY Gary DuBoff, CPA, CFP Principal 1 Agenda I. Individuals II. Qualified

Before you sell Understanding the tax impact of sales to cooperatives

The Advanced Consulting Group White paper Before you sell Understanding the tax impact of sales to cooperatives Ryan Patton, MBA Consultant, Advanced Consulting Group Key highlights Qualified buisiness

The Advanced Consulting Group White paper Before you sell Understanding the tax impact of sales to cooperatives Ryan Patton, MBA Consultant, Advanced Consulting Group Key highlights Qualified buisiness

AAO Board of Trustees and Council on Government Affairs. Analysis of New Tax Reform Law

Memorandum To: From: AAO Board of Trustees and Council on Government Affairs Arnold & Porter Kaye Scholer Date: December 22, 2017 Re: Analysis of New Tax Reform Law This memo is intended for use by the

Memorandum To: From: AAO Board of Trustees and Council on Government Affairs Arnold & Porter Kaye Scholer Date: December 22, 2017 Re: Analysis of New Tax Reform Law This memo is intended for use by the

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

Tax Cuts & Jobs Act of 2017

Tax Cuts & Jobs Act of 2017 WHAT BUSINESSES & S NEED TO KNOW DECEMBER 19, 2017 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in

Tax Cuts & Jobs Act of 2017 WHAT BUSINESSES & S NEED TO KNOW DECEMBER 19, 2017 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in

HOW THE TAX CUTS AND JOBS ACT AFFECTS YOU

HOW THE TAX CUTS AND JOBS ACT AFFECTS YOU I. New Opportunities for Estate Planning and Gifting The doubling of the estate, gift, and GST tax exemptions to $11.18 million per person ($22.36 million per

HOW THE TAX CUTS AND JOBS ACT AFFECTS YOU I. New Opportunities for Estate Planning and Gifting The doubling of the estate, gift, and GST tax exemptions to $11.18 million per person ($22.36 million per

2018 Federal Income Tax Update Business

2018 Federal Income Tax Update Business FTU- Business IRC 199A ISSUES 2 Business Tax Changes Under the Tax Cuts and Jobs Act The Tax Cuts and Jobs Act of 2017 (the Act ) contains significant legislation

2018 Federal Income Tax Update Business FTU- Business IRC 199A ISSUES 2 Business Tax Changes Under the Tax Cuts and Jobs Act The Tax Cuts and Jobs Act of 2017 (the Act ) contains significant legislation

Tax Cuts and Jobs Act of 2017 (TCJA) Key Individual Tax Provisions

Key Individual Tax Provisions") Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

Tax Reform Update Highlights as of March Reg Baker CPA LLC (808)

") Tax Reform Update Highlights as of March 2018 Reg Baker CPA LLC (808) 753-6026 reg@regbaker.com www.regbaker.com 1 DISCLAIMER The material appearing in this presentation is for informational purposes only

Tax Reform Update Highlights as of March 2018 Reg Baker CPA LLC (808) 753-6026 reg@regbaker.com www.regbaker.com 1 DISCLAIMER The material appearing in this presentation is for informational purposes only

Brackets (seven) - Taxable Income Single Filers. Between $9,525 and $38,700. Between $2,550 and $9,150. Between $157,500 and $200,000

- Taxable Income Single Filers. Between $9,525 and $38,700. Between $2,550 and $9,150. Between $157,500 and $200,000") Individual Taxes (Which Would Expire After 2025) Brackets (seven) - Taxable Income Single Filers Up to $9,525 Between $9,525 and $38,700 Between $38,700 and $82,500 Between $200,000 and $500,000 Above

Individual Taxes (Which Would Expire After 2025) Brackets (seven) - Taxable Income Single Filers Up to $9,525 Between $9,525 and $38,700 Between $38,700 and $82,500 Between $200,000 and $500,000 Above

How Does Tax Reform Affect Real Estate Developers & Investors?

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar