New Tax Rules. For You and Your Business Owners

|

|

|

- Ella Watts

- 5 years ago

- Views:

Transcription

1 New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented by Laura Stees, CPA Partner & Business Strategist Stees, Walker & Company, LLP Keith Troutman, CPA Partner, Tax Department Squar Milner

2 The New Postcard-size Pages

3 The New Postcard-size Pages

4 Plus 6 Schedules Schedule 1 Additional Income and Adjustments To Income Schedule 2 Tax Schedule 3 Nonrefundable Credits Schedule 4 Other Taxes Schedule 5 Other Payments and Refundable Credits Schedule 6 Foreign Address and Third Party Designee

5 Entities - Change! Pass-throughs: Sec 199A 20% reduction (taken on the Individual return) Meals & Entertainment The New Rules QSBS Depreciation (bonus 179) Examples by Entity Good to Know: Corporate Tax Rate Reduction Modified NOL s Interest deduction limitation Qualified Opportunity Zones Individual Comparisons and Examples State and Local Non-Conformity

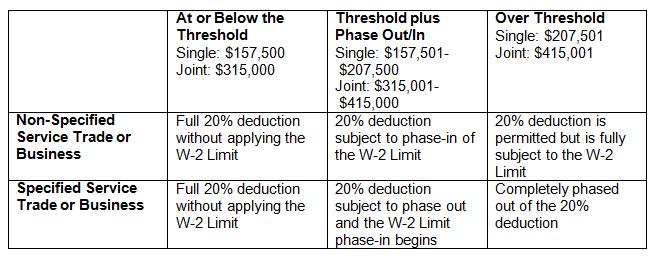

6 199A - 20% Deduction of Certain Pass-through Income (taken on the individual return) For tax years after 12/31/17, subject to a sunset at the end of 2025, the law generally allows an individual taxpayer (including a trust or estate) a deduction for 20% of the individual s domestic qualified business income from a partnership, S corporation, or sole proprietorship.

7 199A Beware of the Cliff When taxable income is greater than $207,500 (single) or $415,000 (married) you need wages and/or property to qualify for any 199A benefit, assuming you are an in favor business. Computation rules before the taxable income limitation lesser of: 1. 20% of qualified business income, or 2. Greater of: 50% of W-2 wages 25% of W-2 wages + 2.5% of unadjusted basis of qualified property

8 199A Qualified Property The term qualified property is generally defined to mean any qualified trade or business, tangible property of a character subject to depreciation that is: i. held by and available for use in the qualified trade or business at the close of the taxable year ii. iii. which is used at any point during the taxable year in the production of QBI, and the depreciable period for which has not ended before the close of the taxable year

9 199A Income That Does Not Qualify QBI includes the net domestic business taxable income, gain, deduction, and loss with respect to any qualified trade or business. QBI specifically excludes the following items of income, gain, deduction, or loss: 1) Investment-type income such as dividends, investment interest income, short-term & long-term capital gains, commodities gains, foreign currency gains, and similar items 2) Wages and guaranteed payments 3) Qualified REIT dividends, qualified cooperative dividends, or qualified PTP income.

10 199A Out of Favor Businesses Specified service trade or businesses are not included in qualified businesses Involves the performance of services in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services Any trade or business of which the principal asset is the reputation or skill of one or more of its owners or employees (limited to product endorsements, use of a personal likeness, appearance fees)

11 199A Out of Favor Businesses (cont.) Any business that involves the performance of services that consist investment and investment managing trading or dealing in securities, partnership interest, or commodities. The deduction may apply to income from a specified service trade or business if the taxpayer s taxable income does not exceed $315,000 (for married individuals filing jointly or $157,500 for other individuals). Under the conference agreement, this benefit would be phased out over the next $100,000 of taxable income for married individuals filing jointly ($50,000 for other individuals).

12 199A Phase-out Graph

13 199A Flowchart

14 199A S VS C CORPORATION Tax rate comparison, including the double taxation effect S-Corp C-Corp C Corp Rate on 1120 Cap Gains on % Gains Effective % 79% of 3.8% NIIT Tax 10% 21% 21% 0% 12% 21% 21% 0% 22% 32.85% 21% 15% 11.85% 24% 35.85% 21% 15% 11.85% 3.002% 34% 35.85% 21% 15% 11.85% 3.002% 35% 35.85% 21% 15% 11.85% 3.002% 37% 39.8% 21% 20% 15.5% 3.002% Note: The breakpoints above are not exact, because the 2018 capital gains rates do not apply by brackets as they did in C-Corporations: Earnings are taxed at 21% + capital gains tax on dividends at a 79% effective rate (earnings less 21%) + NIIT tax

15 199A Example Not Specified Service Business QBI $ 500,000 W-2 Wages $ 215,000 Qualified Property $ 600,000 Taxable Income $ 650,000 Married Filing Joint Conclusion: Over the cliff 20% of QBI $ 100,000 50% of Wages $ 107,500 20% of QBI is less than 50% of Wages Full 20% deduction allowed Deduction $ 100,000

16 199A Example (cont.) Not Specified Service Business QBI $ 300,000 W-2 Wages $ 80,000 Qualified Property $ 600,000 Taxable Income $ 380,000 Married Filing Joint Conclusion: Phase in Range from $315,000 to $415,000 % into the phase in Range: $380,000 - $315,000 $ 65,000 20% of QBI $ 60,000 50% of Wages $ 40,000 65% 50% of wages are less than 20% of QBI Partial Deduction allowed Deduction $ 47,000 $60,000 - ($60,000-$40,000 x 65%)

17 199A Example (cont.) Specified Service Business QBI $ 300,000 W-2 Wages $ 150,000 Qualified Property $ - Taxable Income $ 380,000 Married Filing Joint Conclusion: Phase in Range from $315,000 to $415,000 % into the phase in Range: $380,000 - $315,000 $ 65,000 65% 20% of QBI $ 60,000 50% of Wages $ 75, % of Qualified Property $ - Wage limitation is higher than QBI Partial Deduction allowed Deduction $ 21,000 $60,000 X 35%

18 199A Example: Real Estate Not Specified Service Business -Real Estate QBI $ 400,000 W-2 Wages $ - Qualified Property $ 3,000,000 Taxable Income $ 450,000 Married Filing Joint Conclusion: 20% of QBI $ 80,000 50% of Wages $ - 2.5% of Qualified Property $ 75,000 Property limitation is lower than QBI Deduction $ 75,000

19 199A Planning Opportunities The Deduction sunsets Wage compensation planning issues Deduction planning for professional/service businesses Deduction planning with partnership guaranteed payments

20 199A Strategies to Increase QBI Deduction Reduce income especially at the phase-out levels Transform income from specified service business into non-specified service business Think about entity choice, compensation, and asset depreciation

21 199A Strategies to Reduce Income Possibly file separate returns if spouse earns enough income (non community property states or income) Increase retirement plan contributions Consider passing on bonus depreciation to extend benefit over multiple years

22 199A Entity Choice Example It is important to also consider the permanent nature of the C Corp tax rate decrease vs. the temporary nature of the 20% QBI deduction for pass-throughs in determining entity choice.

23 199A Advantage to S. Corp Assume sole owner of S Corp and 99% owner of partnership No outside employees Ignore basis in qualified property

24 199A Advantage to S. Corp Assume sole owner of S Corp and 99% owner of partnership Outside employees paid $200,000 in W-2 wages Ignore basis in qualified property

25 Meals & Entertainment (cont.)

26 Meals & Entertainment (cont.)

27 QSBS-Qualified Small Business Stock A qualified small business stock (QSBS) is the stock, or share, of a qualified small business (QSB), as defined by the Internal Revenue Code (IRC). A qualified small business is a domestic and active C-corporation whose gross assets, valued at original cost, do not exceed $50 million on and immediately after its stock issuance.

28 QSBS-Qualified Small Business Stock (cont.) The investor must not be a corporation Qualified small business stock (QSBS) is any stock acquired from a qualified small business (QSB) after 8/10/1993. To claim the tax benefits of a share being qualified, the following must apply: Must have acquired the stock at its original issue and not from the secondary market Purchase the stock with cash or property, or as payment for a service The investor must hold the stock for at least five years to reap the tax benefits of a QSBS. At least 80% of the issuing corporation's assets must be used in the operations of one or more of its qualified trades or businesses

29 QSBS - Qualified Small Business Stock (cont.) The Internal Revenue Code (IRC) Section 1202 defines a qualified small business (QSB). These QSBs do not operate in the hospitality industry, financial sector, farming business, or any business heavily dependent on the skill of one or more of its employees such as healthcare, law, accounting, engineering, consulting, architecture, and others. Businesses that qualify for QSB status include companies in the technology, retail, wholesale, and manufacturing fields. Qualified startups and qualified businesses looking to expand their operations may raise initial or additional capital through a QSBS offering. These companies may also use qualified small business stock (QSBS) as a form of an in-kind payment. In-kind payments are frequently utilized to compensate employees for services rendered when cash flow is minimal. QSBS can also be used to retain employees and as an incentive to help the company grow and succeed.

30 QSBS - Qualified Small Business Stock (cont.) Tax treatment for a QSB stock depends on when the stock was acquired and the length of its holding. The Protecting Americans from Tax Hikes Act (PATH Act), allows investors to exclude 100% of capital gains on qualified small business stock (QSBS) if the stock qualifies under Section 1202 of the IRC. The exclusion has a cap of $10 million, or 10 times the adjusted basis of the stock, whichever is greater.

31 QSBS - Qualified Small Business Stock (cont.) Additionally, there are holding requirements for the full exclusion of alternative minimum tax (AMT) and net investment income (NII) tax. The AMT is typically imposed on individuals or investors who have tax exemptions that allow them to decrease their income tax due 100% capital gains exclusion for QSBS acquired after 9/27/2010. A 100% exclusion on capital gain applies, which also includes exclusions from the AMT and NII tax 75% capital gains exclusion for QSBS acquired between 2/18/2009, and 9/27/2010. However, 7% of the gain is subject to AMT 50% capital gains exclusion for QSBS acquired between 8/11/1993, and 2/17/2009. However, 7% of the gain is subject to AMT

32 QSBS - Qualified Small Business Stock (cont.) Example of QSBS Capital Gains Taxation If you invested $1.5 million in a tech startup on 10/1/2010, and held that investment for five years, you can sell the QSBS for up to (10 x $1.5 million, which was the original investment) + $1.5 million = $16.5 million. Once you deduct your initial investment, you have a $15 million capital gain. You will pay zero federal tax on the $15 million capital gain. This case applies, of course, if the startup appreciates in value. Likewise, an investor who seeded $500,000 in the same tech startup will be able to sell up to $10 million + $500,000 = $10.5 million without tax being applied to the capital gain of $10 million.

33 QSBS - Qualified Small Business Stock (cont.) Example of QSBS Capital Gains Taxation (cont.) In the case of the investor above, if his total proceeds from the sale totaled $20 million, a 23.8% capital gains tax would be applied to the $5 million gain ($20 million - $15 million) If the stockholder wants to sell the stock but has not held it for the minimum 5-year holding period, Section 1045 of the IRC allows the investor to defer the gain by reinvesting the proceeds from the sale of the qualified small business stock (QSBS) into another QSBS within 60 days. This defers the tax due on any capital gain made on the original QSBS Landmine: DOES NOT WORK IN CALIFORNIA

34 Depreciation: 179 Expensing New law: Section 179 expensing election is modified to increase the maximum amount that can be deducted to $1 million (up from $500,000 under present law). The dollar limit is reduced dollar-for-dollar to the extent the total cost of section 179 property placed in service during the tax year exceeds $2.5 million (up from $2 million under present law). These limits are adjusted annually for inflation. The changes are effective for property placed in service in tax years beginning after 2017.

35 Depreciation: 179 Expensing (cont.) New law: Expands the availability of the expensing election to depreciable tangible personal property used in connection with furnishing lodging e.g., beds and other furniture for use in hotels and apartment buildings. The 179 election is further expanded to include, at the taxpayer s election, roofs, HVAC property, fire protection and alarm systems, and security systems, so long as these improvements are made to nonresidential real property and placed in service after the date the realty was first placed in service.

36 Bonus Depreciation Bonus depreciation percentage increased from 50% to 100% for property acquired and placed in service after 9/27/17, and before 2023 Phase down of the bonus depreciation percentage beginning in % deduction for property placed in service in % deduction for property placed in service in % deduction for property placed in service in % deduction for property placed in service in 2026 Property that is acquired prior to 9/28/17, but placed in service after 9/27/17, would remain subject to the bonus depreciation percentages available under prior law i.e., 50% for property placed in service in 2017, 40% for property placed in service in 2018, and 30% for property placed in service in 2019

New law: Changes the definition of qualified property (i.e., property")

37 Bonus Depreciation (cont.) New law: Changes the definition of qualified property (i.e., property eligible for bonus depreciation) to include used property acquired by purchase so long as the acquiring taxpayer had not previously used the acquired property and so long as the property is not acquired from a related party

for qualified improvement property, defined as certain interior improvements to nonresidential real property that are placed")

38 Qualified Improvement Property Eliminates the special 15-year recovery period for qualified leasehold improvement property, qualified restaurant property, and qualified retail improvement property Instead, it provides a single 15-year recovery period (20 years for ADS) for qualified improvement property, defined as certain interior improvements to nonresidential real property that are placed in service after the initial placed-in-service date of the realty

39 Qualified Improvement Property (cont.) A large portion of restaurant building and building improvement property will be required to be depreciated as non-residential real property over a 39-year recovery period due to the change in the definition of qualified restaurant property Only the qualified restaurant property that meets the qualified improvement property definition will be 15-year property and thus eligible for bonus depreciation NOTE: Waiting on a technical correction. As currently written, all QIP is 39 year property

40 ADS Recovery Period The ADS recovery period for residential rental property is shortened from 40 years to 30 years Any real property trade or business that elects out of the interest deduction limitation (explained next slide) is required to depreciate building property under ADS. QIP 20 year straight-line under ADS* Residential Rental 30 years under ADS Non-Residential Real 40 years under ADS

41 Business Interest Expense Limitation Section 163(j) is amended to disallow a deduction for net business interest expense of any taxpayer in excess of 30% of a business s adjusted taxable income plus floor plan financing interest. Adjusted taxable income generally would be a business s taxable income computed without regard to: (1) any item of interest, gain, deduction, or loss that is not properly allocable to a trade or business; (2) business interest or business interest income; (3) the amount of any net operating loss deduction; (4) the 20% deduction for certain pass-through income, and (5) in the case of tax years beginning before 1/1/2022, any deduction allowable for depreciation, amortization, or depletion.

42 Business Interest Expense Limitation (cont.) Section 163(j) is amended to disallow a deduction for net business interest expense of any taxpayer in excess of 30% of a business s adjusted taxable income plus floor plan financing interest. Adjusted taxable income generally would be a business s taxable income computed without regard to: (1) Any item of interest, gain, deduction, or loss that is not properly allocable to a trade or business; (2) Business interest or business interest income; (3) The amount of any net operating loss deduction; (4) The 20% deduction for certain pass-through income, and (5) In the case of tax years beginning before 1/1/2022, any deduction allowable for depreciation, amortization, or depletion.

Business interest is defined as any interest paid or accrued on indebtedness properly allocable to a trade")

43 Business Interest Expense Limitation (cont.) Business interest is defined as any interest paid or accrued on indebtedness properly allocable to a trade or business. This does not include investment interest expense, which is subject to its own limitations. An exception to the limitation applies to taxpayers with average annual gross receipts for the threetaxable-year period ending with the prior tax year that do not exceed $25 million.

44 Good to Know Corporate Tax Rate Reduction Modified NOL s Interest deduction limitation Qualified Opportunity Zones Individual Comparisons and Examples State and Local Non-Conformity

45 Corporate Tax Rate Reduction Old law: Progressive structure up to 35% New law: Flat tax rate of 21% 80% dividends received deduction lowered to 65% 70% dividends received deduction lowered to 50%, effective for tax years 2017 and beyond

46 Corporate Tax Rate Reduction (cont.) The corporate rate reduction will greatly affect choice-of-entity decisions for some business entities. Aggregate U.S. Federal Income Tax Rate on Domestic Business Income (incl. 3.8% Medicare Tax) Pre-Tax Reform Post-Tax Reform C Corporation 50.5% 39.8% Flow-Through Entity 43.4% 33.4% %

47 Corporate AMT Repeal of the corporate AMT effective 12/31/17 AMT credit carryovers can be used to the extent of the taxpayer s regular tax liability For 2018, 2019, and 2020, to the extent that AMT credit carryovers exceed regular tax liability, 50% of the excess AMT credit carryovers would be refundable Any remaining AMT credit would be fully refundable in 2021

48 Modified NOL Deduction New law: Limits the NOL deduction to 80% of taxable income, effective with respect to losses arising in tax years beginning after 12/31/17. Will require separate tracking of NOLs before and after this date Current law: Generally provides a 2-yr carryback and 20-yr carryforward for NOLs New law: Provides indefinite carryforward of NOLs arising in tax years ending after 12/31/17

Due to language in the law, losses arising in fiscal years that begin before 12/31/17 and end after 12/31/17 are subject to the new carryback and carry forward")

49 Modified NOL Deduction (cont.) Due to language in the law, losses arising in fiscal years that begin before 12/31/17 and end after 12/31/17 are subject to the new carryback and carry forward rules but not the 80% limitation Deferred purchases to 2019 could be advantageous because the 80% NOL limitation would create an NOL in 2018

50 Election Out of Interest Expense Limitation Certain taxpayers can elect for the interest expense limitation not to apply Businesses making this election would be required to use the alternative depreciation system (ADS) to depreciate certain property For an electing real estate business, ADS would be used to depreciate nonresidential real property (40yr SL), residential rental property (30yr SL), and qualified improvement property (20yr SL)

51 Example of Business Interest Expense Calc. ABC partnership generates $200 of noninterest income. Its only expenses are $80 of business interest and $30 of depreciation (taxable income before limitation = $90) Under the law, the deduction for business interest is limited to 30% of adjusted taxable income, that is, 30% x $200 = $60 ABC deducts $60 of business interest and allocates the $20 of excess business interest to the partners (additional K-1 reporting)

52 Investors: K-1 s from partnerships/s-corps The new 20% deduction and limitation on interest deduction require flow-through entities to provide additional information to partners for use on individual returns 20% deduction income, w-2 wages, property basis, REIT dividends, PTP income Limitation on interest deduction - excess taxable income, excess business interest income

53 Qualified Opportunity Zones The Tax Cuts and Jobs Act of 2018 contains provisions for reduction of capital gains where qualifying funds are invested for long term in qualifying investments in qualifying areas Definition of qualifying investment funds is generous Definition of qualifying investments is broad Definition of qualifying areas is diverse across the U.S. Opportunity for gain deferral and potential exclusion from future taxation

54 Qualified Opportunity Zones (cont.) Taxpayer must reinvest capital gain into qualified opportunity zone fund Must generally reinvest within 180 days of the capital gain event Provides for gain deferral up until 12/31/2026 on reinvested capital gain If investment is held for more than 10 years, then potential exclusion available on appreciation of investment Can be a closely-held fund or a syndicated investment vehicle Complex legislation with many potential traps, so consultation with tax advisors before investment is important

55 Qualified Opportunity Zones Example Investor sells stock for $2M ($1M of long term capital gain) on 7/1/2018 Investor invests $1M in an interest in a QOZ Fund on 11/1/2018 Does not need to invest the entire $2M 12/31/2026: Investor s tax basis in the QOZ Fund was increased by $150K (15% of $1M) $50K on 11/1/2023, and $100K on 11/1/2025 Investor has to pay tax on $850K long-term capital gain 11/2/2028: Investment in the QOZ Fund has appreciated from $1M to $5M ($4M in potential gain). If the investment in the QOZ Fund is sold, then there is no taxable gain on the $4M of appreciation * Results/outcomes may vary

56 Individuals - Change! Most changes effective after 12/31/17 Most individual changes are temporary Many taxpayers will no longer be itemizers MFJ: $24k standard deduction Many taxpayers will no longer owe AMT Some taxpayers will pay more, others will pay less

57 Key Individual Comparisons Item 2018 Pre-Tax Reform Tax Reform Tax brackets 7 rates: 10, 15, 25, 28, 33, 35, 39.6% 7 rates: 10, 12, 22, 24, 32, 35, 37% Taxable Income Family provisions Many deductions Personal and dependency exemptions. $1,000 child credit if under age 17; phaseout starts $110K for MFJ Fewer deductions (state tax, property tax), new one for certain business owners( 199A). $2,000 Child credit if under age 17 ($1,400 refundable); need valid SSN + $500 non-child dependent credit (not refundable); phaseout starts at $200K ($400K if MFJ). Itemized vs standard deduction 33% of individuals itemize deductions Increase in standard deduction; reduction in itemized deductions. Far fewer individuals will itemize. Inflation adjustment CPI-U Chained Consumer Price Index Capital gains / qualified dividends Basically unchanged MFJ: 0% rate up to $77,200; 15% rate up to $479,000; 20% over $479,000 AMT Several preferences and adj; exemptions adj for inflation Retained; higher exemptions; adjustments modified due to regular tax changes

58 Key Individual Comparisons - MFJ Income range 2018 Rate Pre-Tax Reform Tax Reform Rate $ Difference $1 to $19,050 10% 10% 0 $19,051 to $77,400 15% 12% 1,750 $77,401 to $156,150 25% 22% 2,362 $156,151 to $165,000 28% 22% 531 $165,001 to $237,950 28% 24% 2,918 $237,951 to $315,000 33% 24% 6,934 $315,001 to $400,000 33% 32% 850 $400,001 to $424,950 33% 35% -499 $424,951 to $480,050 35% 35% 0 $480,051 to $600, % 35% 5,517 Over $600, % 37% Depends on income

59 Key Individual Comparisons Itemized Deduction Medical Mortgage interest on principal and 2nd homes Investment interest expense State taxes Charitable contribution deduction Casualty/theft loss Misc itemized ded subject to 2% AGI threshold Overall limitation on itemized deductions Tax Reform Rate Retain; 7.5% threshold for 2017 & 2018 (also for AMT) Debt up to $750K (remains $1 million for debt that exists on or before 12/15/17) Retain Maximum $10K ($5K if MFS) Cash contribution limit increased to 60% of AGI Repeal, except for federally-declared disasters Repealed Repealed

60 State and Local Taxes 2018 through 2025 Total deduction is $10,000 ($5K if MFS) May deduct combination of: Income or sales tax State and local property taxes (no foreign real property taxes) Exceptions Taxes imposed at entity level or in carrying on a trade or business Property taxes for residential rental property or business property Property taxes on investment land (likely still allowed on Sch A) CA Excellence Fund

61 Interest Expense 2018 through 2025 Only interest on Acquisition Indebtedness (AI) up to $750K Unless debt existed at 12/15/17 (then still $1 million AI limit) Binding contract exception if entered into before 12/15/17, to close on purchase before 2018 and if purchase before 4/1/18 If refinance treat as incurred on date of original debt to extent doesn t exceed the refinanced debt. No deduction for interest on home equity debt Effective for 2018 tax year no grandfather rule

62 Loss Limitation (Other than C Corps) New law: Contains a significant change to non-passive losses of taxpayers other than C corporations. Excess business loss of such a taxpayer will not be allowed for the tax year. An excess business loss for the tax year would be $500,000 for married individuals filing jointly or $250,000 for other individuals. Because the rule doesn t affect a taxpayer s ability to offset income and losses from separate businesses, it provides incentive for taxpayers to classify their activities as trades or businesses to the extent possible. Any excess business loss of the taxpayer would be treated as part of the taxpayer s net operating loss (NOL) and carried forward to subsequent tax years.

63 A Few Examples Typical family of four earning median family income of $73k 2018 Pre-Tax Reform Tax Reform W-2 Earnings $73,000 $73,000 Standard Deduction -13,000-24,000 Personal Exemptions -16, Taxable Income $43,400 $49,000 Tax $5,558 $5,499 Child Tax Credit -2,000-4,000 Net Tax Liability $3,558 $1,499 Tax reduction under Tax Reform $2,059 Tax reduction under REFORM if children were not under age 17 but otherwise met the definition of a dependent (no child credit under current law and only $500 x 2 under Tax reform) $1,059

64 Effect Depends on Details of Each Situation Family of 4, wages $100K, state taxes $8K, mtg int $10.5K, charitable $500 Family of 4, wages $250K, mtg int $40K, State tax $35K, charitable $5K, misc. $3K Pre-Tax Reform Tax Reform Pre-Tax Reform Tax Reform Taxable income $64,400 $76,000 $150,400 $195,000 Tax $8,708 $8,739 $28,908 $35,379 Child credit $2,000 $4,000 $0 $4,000 AMT $0 $0 $3,372 $0 Net tax $6,708 $4,739 $32,280 $31,379 Savings (add l tax) $1,969 $901 Tax if kids 17 or older $8,708 $7,739 $32,280 $34,379 Savings (add l tax) $969 ($2,099)

65 Married Couple, No Children, Rents, Salary $150, Pre-Tax Reform Tax Reform W-2 Earnings $150,000 $150,000 Standard Deduction -13,000-24,000 Personal Exemptions -8, Taxable Income $128,700 $126,000 Tax $23,483 $19,599 Tax Reduction w/ Reform $3,884 Marginal Tax Rate 25% 22%

66 Example of High Income CA Couple Family of 4, wages $1,500,000, mtg int $40K, State taxes $160K, charitable $15K, miscellaneous $5K 2018 Pre-Tax Reform Tax Reform Taxable Income $1,280,000 $1,435,000 Tax $451,024 $470,329 Child Credit $0 $0 AMT $0 $0 Net Tax $451,024 $470,329 Additional Tax w/reform $19,305 Marginal Tax Rate 39.6% 37% Average Tax Rate 35.2% 32.8%

67 Example of High Income CA Couple (cont.) Family of 4, flow through income $1,500,000, mtg int $40K, State taxes $160K, charitable $15K, miscellaneous $5K 2018 pre-tax reform Tax Reform Taxable Income $1,280,000 $1,135,000 Tax $451,024 $359,329 Child Credit $0 $0 AMT $0 $0 Net Tax $451,024 $359,329 Additional Tax (Savings) w/reform $(91,695) Marginal Tax Rate 39.6% 37% Average Tax Rate 35.2% 31.7%

5/29/ TAX CUTS AND JOBS ACT OVERVIEW. Individual Tax. Introduction-Individual Provisions. Dauphin County Bar Association May 30, 2018

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

Tax cuts and jobs act

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

How Tax Reforms Impacts Your Vineyard February 8, Presented by: Kathy Freshwater, CPA Craig Anderson, CPA

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

How Does Tax Reform Affect Real Estate Developers & Investors?

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

Tax Cuts and Jobs Act Real Estate Industry Impact. April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD

Tax Cuts and Jobs Act Real Estate Industry Impact April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD Topics for Today Rate Changes Business Interest Limitation Net Operating Losses Excess

Tax Cuts and Jobs Act Real Estate Industry Impact April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD Topics for Today Rate Changes Business Interest Limitation Net Operating Losses Excess

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018 WHAT WE WILL COVER TODAY 1 2 Business & individual provisions of the Tax Cuts and Jobs

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018 WHAT WE WILL COVER TODAY 1 2 Business & individual provisions of the Tax Cuts and Jobs

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 Important Highlights for Individuals and Small Businesses On December 15, 2017, Congress released the 2017 Tax Cut and Jobs Act ( the Act ) that has now passed both the House

Tax Cuts and Jobs Act of 2017 Important Highlights for Individuals and Small Businesses On December 15, 2017, Congress released the 2017 Tax Cut and Jobs Act ( the Act ) that has now passed both the House

Adam Williams. Anthony Licavoli. Principal Tax Manager

1 2 Adam Williams Principal 734.302.4179 adam.williams@rehmann.com Anthony Licavoli Tax Manager 248.463.4598 anthony.licavoli@rehmann.com 3 4 5 What is your impression about the speed at which Congress

1 2 Adam Williams Principal 734.302.4179 adam.williams@rehmann.com Anthony Licavoli Tax Manager 248.463.4598 anthony.licavoli@rehmann.com 3 4 5 What is your impression about the speed at which Congress

Tax Reform: What You Need To Know

Tax Reform: What You Need To Know January 24, 2018 Presented by: Blake Harrison, CPA/PFS Senior Tax Manager LBMC Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on

Tax Reform: What You Need To Know January 24, 2018 Presented by: Blake Harrison, CPA/PFS Senior Tax Manager LBMC Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS. February 8, 2018 Bruce I. Booken Rose K. Wilson

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS February 8, 2018 Bruce I. Booken Rose K. Wilson The 2017 Tax Act Signed into law on December 22, 2017 Provisions apply NOW to taxable years beginning after

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS February 8, 2018 Bruce I. Booken Rose K. Wilson The 2017 Tax Act Signed into law on December 22, 2017 Provisions apply NOW to taxable years beginning after

New Tax Law: Issues for Partnerships, S corporations, and Their Owners

New Tax Law: Issues for Partnerships, S corporations, and Their Owners January 18, 2018 1 Introduction H.R. 1, originally known as the Tax Cuts and Jobs Act, was signed into law on December 22, 2017. The

New Tax Law: Issues for Partnerships, S corporations, and Their Owners January 18, 2018 1 Introduction H.R. 1, originally known as the Tax Cuts and Jobs Act, was signed into law on December 22, 2017. The

TAX CUTS AND JOBS ACT

TAX CUTS AND JOBS ACT Businesses Corporate tax rate will now be a flat 21% beginning January 1, 2018. Corporate alternative minimum tax has been repealed. Effective for tax years beginning after December

TAX CUTS AND JOBS ACT Businesses Corporate tax rate will now be a flat 21% beginning January 1, 2018. Corporate alternative minimum tax has been repealed. Effective for tax years beginning after December

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA)

") Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

TAX REFORM INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

The following chart sets forth some of the provisions affecting individuals in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

Comparison of House and Senate Tax Reform Bills

Comparison of House and Senate Tax Reform Bills Provision Individual Rates (Single) 12% $0 - $44,999 25% $45,000 - $199,999 35% $200,000 - $499,999 39.6% $500,000 + Senate Version of H.R. 1, the 10% $0

Comparison of House and Senate Tax Reform Bills Provision Individual Rates (Single) 12% $0 - $44,999 25% $45,000 - $199,999 35% $200,000 - $499,999 39.6% $500,000 + Senate Version of H.R. 1, the 10% $0

Integrity Accounting

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Tax Planning for Real Estate Under the TCJA

By now, you have been bombarded with summaries and articles on the 507-page tax bill, formerly known as the Tax Cuts and Jobs Act of 2017, and signed into law by President Trump on Dec. 22, 2017 (the Act).

By now, you have been bombarded with summaries and articles on the 507-page tax bill, formerly known as the Tax Cuts and Jobs Act of 2017, and signed into law by President Trump on Dec. 22, 2017 (the Act).

SPECIAL REPORT. Tax Law Essentials. Brought to you by Mercer Advisors

SPECIAL REPORT Tax Law Essentials Brought to you by Mercer Advisors Game-changing tax package The recently enacted Tax Cuts and Jobs Act (TCJA) is a sweeping, game-changing tax package. Here s a look at

SPECIAL REPORT Tax Law Essentials Brought to you by Mercer Advisors Game-changing tax package The recently enacted Tax Cuts and Jobs Act (TCJA) is a sweeping, game-changing tax package. Here s a look at

Tax Cuts & Jobs Act (TCJA)

") Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

2017 TAX CUTS AND JOBS ACT

2017 TAX CUTS AND JOBS ACT The Tax Cuts and Jobs Act was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and impacts most taxpayers; especially individuals

2017 TAX CUTS AND JOBS ACT The Tax Cuts and Jobs Act was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and impacts most taxpayers; especially individuals

TAX REFORM INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

The following chart sets forth some of the provisions affecting individuals in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

Tax Cuts and Jobs Act. Issues Impacting the Real Estate Industry

Tax Cuts and Jobs Act Issues Impacting the Real Estate Industry Tax Cuts and Jobs Act Issues Impacting the Real Estate Industry On December 22, 2017, President Trump signed the Tax Cuts and Jobs Act (the

Tax Cuts and Jobs Act Issues Impacting the Real Estate Industry Tax Cuts and Jobs Act Issues Impacting the Real Estate Industry On December 22, 2017, President Trump signed the Tax Cuts and Jobs Act (the

AAO Board of Trustees and Council on Government Affairs. Analysis of New Tax Reform Law

Memorandum To: From: AAO Board of Trustees and Council on Government Affairs Arnold & Porter Kaye Scholer Date: December 22, 2017 Re: Analysis of New Tax Reform Law This memo is intended for use by the

Memorandum To: From: AAO Board of Trustees and Council on Government Affairs Arnold & Porter Kaye Scholer Date: December 22, 2017 Re: Analysis of New Tax Reform Law This memo is intended for use by the

Tax Reform Update for Businesses and Individuals BOSTON NEWPORT PROVIDENCE SHANGHAI WALTHAM KAHNLITWIN.COM

Tax Reform Update for Businesses and Individuals BOSTON NEWPORT PROVIDENCE SHANGHAI WALTHAM KAHNLITWIN.COM Presented by LAURA H. YALANIS, CPA/MST SHAREHOLDER I work closely with clients to help them achieve

Tax Reform Update for Businesses and Individuals BOSTON NEWPORT PROVIDENCE SHANGHAI WALTHAM KAHNLITWIN.COM Presented by LAURA H. YALANIS, CPA/MST SHAREHOLDER I work closely with clients to help them achieve

TAX CUTS & JOBS ACT DEVELOPMENTS

TAX CUTS & JOBS ACT DEVELOPMENTS P L A N N I N G F O R B U S I N E S S E S A N D I N D I V I D U A L S D E C E M B E R 1 2, 2 0 1 8 THE TAX CUTS & JOBS ACT AT A GLANCE BUSINESS PROVISIONS Reduced Tax Rates

TAX CUTS & JOBS ACT DEVELOPMENTS P L A N N I N G F O R B U S I N E S S E S A N D I N D I V I D U A L S D E C E M B E R 1 2, 2 0 1 8 THE TAX CUTS & JOBS ACT AT A GLANCE BUSINESS PROVISIONS Reduced Tax Rates

Business Changes in the Tax Cuts and Jobs Act. Alan D. Sobel, CPA December 27,

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

TAX CUTS AND JOB ACT OF 2017 Highlights

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

Tax Cuts and Jobs Act February 8, 2018

Tax Cuts and Jobs Act 2017 February 8, 2018 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any specific taxpayer

Tax Cuts and Jobs Act 2017 February 8, 2018 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any specific taxpayer

Tax Cuts and Jobs Act Construction Industry Impact

Tax Cuts and Jobs Act Construction Industry Impact Presented By: Sean M. Auger, Partner 1 Introduction Most but not all provisions effective for tax periods beginning after December 31, 2017 2 General

Tax Cuts and Jobs Act Construction Industry Impact Presented By: Sean M. Auger, Partner 1 Introduction Most but not all provisions effective for tax periods beginning after December 31, 2017 2 General

TAX UPDATE TAX CUTS & JOBS ACT (2018) Add l Elderly & Blind Joint & Surviving Spouse: $1,300

Add l Elderly & Blind Joint & Surviving Spouse: $1,300") TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

Tax Cuts and Jobs Act. Durham Chamber of Commerce Public Policy Meeting January 9, 2018

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

TAX CUTS AND JOBS ACT OF 2017

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

HFMA Annual AccounTing and AudiTing UpdaTe. Tax UpdaTe

HFMA Annual AccounTing and AudiTing UpdaTe Tax UpdaTe Presented by: Jeffrey J. Petrell, JD, CPA, CGMA Partner Health Care Tax Services Kelly A. Brocious, CPA Senior Manager Health Care Tax Services 97

HFMA Annual AccounTing and AudiTing UpdaTe Tax UpdaTe Presented by: Jeffrey J. Petrell, JD, CPA, CGMA Partner Health Care Tax Services Kelly A. Brocious, CPA Senior Manager Health Care Tax Services 97

Tax Cuts and Jobs Act Changes Impacting Real Estate. Presented by: Sefi Silverstein, CPA Len Nitti, CPA, MST

Tax Cuts and Jobs Act Changes Impacting Real Estate Presented by: Sefi Silverstein, CPA Len Nitti, CPA, MST Our Speakers Sefi Silverstein, CPA Len Nitti, CPA, MST 2 Housekeeping To submit questions use

Tax Cuts and Jobs Act Changes Impacting Real Estate Presented by: Sefi Silverstein, CPA Len Nitti, CPA, MST Our Speakers Sefi Silverstein, CPA Len Nitti, CPA, MST 2 Housekeeping To submit questions use

Tax Reform: What Dealers Need to Know

Tax Reform: What Dealers Need to Know 1 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication is not intended or written

Tax Reform: What Dealers Need to Know 1 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication is not intended or written

Corporate and Business Provision House Bill (HR 1) Senate Bill Final Bill

Senate Bill Final Bill") Selected provisions of the House and Senate tax reform bills as passed by both houses of Congress which resulted in the final bill in the far right column. Introduction: This summary contains what ZLQ

Selected provisions of the House and Senate tax reform bills as passed by both houses of Congress which resulted in the final bill in the far right column. Introduction: This summary contains what ZLQ

What the Tax Cuts and Jobs Act Means for the Real Estate Industry

What the Tax Cuts and Jobs Act Means for the Real Estate Industry PRESENTED BY: ADAM HILL, CPA, PARTNER JON WILLIAMSON, CPA, MT, TAX MANAGER KIM PALMER, CPA, MT, PARTNER February 1, 2018 Welcome & Introductions

What the Tax Cuts and Jobs Act Means for the Real Estate Industry PRESENTED BY: ADAM HILL, CPA, PARTNER JON WILLIAMSON, CPA, MT, TAX MANAGER KIM PALMER, CPA, MT, PARTNER February 1, 2018 Welcome & Introductions

The Tax Cuts and Jobs Act of 2017

The Tax Cuts and Jobs Act of 2017 is the most comprehensive revision to the Internal Revenue Code Since 1986. This new Tax Act reduces tax rates for individuals and corporations, repeals exemptions, eliminates

The Tax Cuts and Jobs Act of 2017 is the most comprehensive revision to the Internal Revenue Code Since 1986. This new Tax Act reduces tax rates for individuals and corporations, repeals exemptions, eliminates

Business Tax. Pass-Through Entities. New 20% Deduction

Business Tax Pass-Through Entities New 20% Deduction For tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026, taxpayers who have domestic qualified business income (QBI) from a partnership,

Business Tax Pass-Through Entities New 20% Deduction For tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026, taxpayers who have domestic qualified business income (QBI) from a partnership,

Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F

Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F 2 0 1 7 OUR GOAL FOR TODAY Develop an awareness of the recent law changes that will affect healthcare organizations OUR GOAL FOR TODAY

Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F 2 0 1 7 OUR GOAL FOR TODAY Develop an awareness of the recent law changes that will affect healthcare organizations OUR GOAL FOR TODAY

IRC 199A Deduction for Qualified Business Income

IRC 199A Deduction for Qualified Business Income What is it? 20% deduction against qualified business income Designed to provide a tax break to owners of pass through entities, in light of substantial

IRC 199A Deduction for Qualified Business Income What is it? 20% deduction against qualified business income Designed to provide a tax break to owners of pass through entities, in light of substantial

Tax Cuts and Jobs Act

Tax Cuts and Jobs Act Presenters: Timothy M. Tikalsky, CPA Date: February 6, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs Act (TCJA) Name given by House in H.R.

Tax Cuts and Jobs Act Presenters: Timothy M. Tikalsky, CPA Date: February 6, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs Act (TCJA) Name given by House in H.R.

Tax Cuts and Jobs Act 2017 HR 1

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

Tax Reform Webinar January 4, 2018

Tax Reform Webinar January 4, 2018 Speakers: Jerry Frumm Vice Chairman & Chief Investment Officer, Senior Lifestyle Jeanne McGlynn Delgado, Vice President Government Affairs, ASHA Randy Hardock Partner,

Tax Reform Webinar January 4, 2018 Speakers: Jerry Frumm Vice Chairman & Chief Investment Officer, Senior Lifestyle Jeanne McGlynn Delgado, Vice President Government Affairs, ASHA Randy Hardock Partner,

2018 Spring Professional Advisor Seminar Presentation: Mike Martin

2018 Spring Professional Advisor Seminar Presentation: Mike Martin Today s Agenda not necessarily in this order Review of many (not all) important aspects of the: 2018 Tax Cut and Jobs Act (TCJA) What

2018 Spring Professional Advisor Seminar Presentation: Mike Martin Today s Agenda not necessarily in this order Review of many (not all) important aspects of the: 2018 Tax Cut and Jobs Act (TCJA) What

2018 TAX SEMINAR OPPORTUNITIES & IMPACTS. Tax Cuts and Jobs Acts Enacted December 22, Most changes go into effect January 1, 2018

2018 TAX SEMINAR OPPORTUNITIES & IMPACTS Tax Cuts and Jobs Acts Enacted December 22, 2017 Most changes go into effect January 1, 2018 S e m i n a r s p o n s o re d b y A n n L a u f m a n o f A L A F

2018 TAX SEMINAR OPPORTUNITIES & IMPACTS Tax Cuts and Jobs Acts Enacted December 22, 2017 Most changes go into effect January 1, 2018 S e m i n a r s p o n s o re d b y A n n L a u f m a n o f A L A F

HOW THE TAX CUTS AND JOBS ACT AFFECTS YOU

HOW THE TAX CUTS AND JOBS ACT AFFECTS YOU I. New Opportunities for Estate Planning and Gifting The doubling of the estate, gift, and GST tax exemptions to $11.18 million per person ($22.36 million per

HOW THE TAX CUTS AND JOBS ACT AFFECTS YOU I. New Opportunities for Estate Planning and Gifting The doubling of the estate, gift, and GST tax exemptions to $11.18 million per person ($22.36 million per

ESTIMATED KANSAS IMPACT OF THE FEDERAL TAX CUTS AND JOBS ACT

ESTIMATED KANSAS IMPACT OF THE FEDERAL TAX CUTS AND JOBS ACT KANSAS DEPARTMENT OF REVENUE FEBRUARY 14, 2018 Summary... 2 Individual Tax Reform... 8 Tax Rate Reform... 8 Deduction for Qualified Business

ESTIMATED KANSAS IMPACT OF THE FEDERAL TAX CUTS AND JOBS ACT KANSAS DEPARTMENT OF REVENUE FEBRUARY 14, 2018 Summary... 2 Individual Tax Reform... 8 Tax Rate Reform... 8 Deduction for Qualified Business

Tax Reform Highlights

etax Alert Tax Reform Highlights Final Business/Corporate/Partnership Provisions in Tax Cuts and Jobs Act of 2017 Here is a chart that briefly summarizes the major provisions affecting our business clients,

etax Alert Tax Reform Highlights Final Business/Corporate/Partnership Provisions in Tax Cuts and Jobs Act of 2017 Here is a chart that briefly summarizes the major provisions affecting our business clients,

Highlights. Tax Cuts and Jobs Act of 2017

Highlights Tax Cuts and Jobs Act of 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $9,525 $9,525 to $38,700 $9,525 to $38,700 12% $38,700 to $93,700 25% $38,700 to $82,500 22% $93,700

Highlights Tax Cuts and Jobs Act of 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $9,525 $9,525 to $38,700 $9,525 to $38,700 12% $38,700 to $93,700 25% $38,700 to $82,500 22% $93,700

Tax Cuts and Jobs Act of 2017 (TCJA) Key General Business Tax Provisions

Key General Business Tax Provisions") Item IRC Expensing and Depreciating Section 179 Limits 179(b) For property service in For property service in The maximum Section 179 deduction and phaseout threshold are increased to $1 million and $2.5

Item IRC Expensing and Depreciating Section 179 Limits 179(b) For property service in For property service in The maximum Section 179 deduction and phaseout threshold are increased to $1 million and $2.5

Tax Cuts and Jobs Act Passed by Congress

Tax Cuts and Jobs Act Passed by Congress On December 19 and 20, 2017, the House and Senate approved a final version of H.R. 1, the Tax Cuts and Jobs Act, renamed An Act to provide for reconcilation purusant

Tax Cuts and Jobs Act Passed by Congress On December 19 and 20, 2017, the House and Senate approved a final version of H.R. 1, the Tax Cuts and Jobs Act, renamed An Act to provide for reconcilation purusant

DissoMaster Version

DissoMaster Version 2017-2 DissoMaster 2017-2 incorporates tax updates from the Tax Cuts and Jobs Act (TCJA). Most TCJA personal income tax changes sunset after 2025; changes re spousal support deductibility

DissoMaster Version 2017-2 DissoMaster 2017-2 incorporates tax updates from the Tax Cuts and Jobs Act (TCJA). Most TCJA personal income tax changes sunset after 2025; changes re spousal support deductibility

KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017

OF 2017") KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017 New tax laws resulting from the TCJA represent the most significant changes in our tax structure in more than 30 years. Most provisions for individuals

KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017 New tax laws resulting from the TCJA represent the most significant changes in our tax structure in more than 30 years. Most provisions for individuals

Tax Planning for Real Estate

Tax Planning for Real Estate Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Pass-thru Deduction Deduction equal to 20% of domestic qualified business income (QBI) from a passthrough entity

Tax Planning for Real Estate Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Pass-thru Deduction Deduction equal to 20% of domestic qualified business income (QBI) from a passthrough entity

Breaking Down the Tax Cuts & Jobs Act of COPYRIGHT 2018 Bowles Rice LLP

Breaking Down the Tax Cuts & Jobs Act of 2017 COPYRIGHT 2018 Bowles Rice LLP Tax Avoidance is Good Anyone may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose

Breaking Down the Tax Cuts & Jobs Act of 2017 COPYRIGHT 2018 Bowles Rice LLP Tax Avoidance is Good Anyone may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose

Tax Cuts & Jobs Act of 2017

Tax Cuts & Jobs Act of 2017 WHAT BUSINESSES & S NEED TO KNOW DECEMBER 19, 2017 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in

Tax Cuts & Jobs Act of 2017 WHAT BUSINESSES & S NEED TO KNOW DECEMBER 19, 2017 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in

To help organizations navigate the key provisions affecting businesses, we have summarized top provisions below.

HOW TAX REFORM IMPACTS BUSINESSES Summary On December 22, 2017, the President signed the Tax Cuts and Jobs Act (the "Act"). Signing the Act marked the largest change to U.S. tax policy in decades. Most

HOW TAX REFORM IMPACTS BUSINESSES Summary On December 22, 2017, the President signed the Tax Cuts and Jobs Act (the "Act"). Signing the Act marked the largest change to U.S. tax policy in decades. Most

Tax Cuts and Jobs Act Questions and Answers for Small Businesses

Tax Cuts and Jobs Act Questions and Answers for Small Businesses February, 2018 This is a summary of items that are subject to variations and exceptions. It is not to be relied upon as tax advice. For

Tax Cuts and Jobs Act Questions and Answers for Small Businesses February, 2018 This is a summary of items that are subject to variations and exceptions. It is not to be relied upon as tax advice. For

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business August 10, 2018 Sarah Armstrong, Esq. Marjorie A. Rogers, Esq. Ed Street, CPA/ABV/CFF, CVA, ASA The information provided

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business August 10, 2018 Sarah Armstrong, Esq. Marjorie A. Rogers, Esq. Ed Street, CPA/ABV/CFF, CVA, ASA The information provided

TAX CUTS AND JOBS ACT EXECUTIVE SUMMARY

TAX CUTS AND JOBS ACT EXECUTIVE SUMMARY Mariner Retirement Advisors INDIVIDUAL INCOME TAX CHANGES Individual Income Tax Rates Single - 10%, 15%, 25%, 28%, 33%, 35%, 39.6%. Top rate begins at income over

TAX CUTS AND JOBS ACT EXECUTIVE SUMMARY Mariner Retirement Advisors INDIVIDUAL INCOME TAX CHANGES Individual Income Tax Rates Single - 10%, 15%, 25%, 28%, 33%, 35%, 39.6%. Top rate begins at income over

Government Affairs. The White Papers TAX REFORM.

Government Affairs The White Papers TAX REFORM www.independentagent.com January 3, 2018 Below is a summary of the provisions of the new tax reform law that are most likely to impact Big I members. This

Government Affairs The White Papers TAX REFORM www.independentagent.com January 3, 2018 Below is a summary of the provisions of the new tax reform law that are most likely to impact Big I members. This

2017 Tax Reform What you need to Know

Oil & Natural Gas Accounting & Tax 2018 2017 Tax Reform What you need to Know November 8, 2018 J. Marlin Witt, CPA, CFP, CGMA What Makes Us Different, Makes You Better Overview of Reform Product of budget

Oil & Natural Gas Accounting & Tax 2018 2017 Tax Reform What you need to Know November 8, 2018 J. Marlin Witt, CPA, CFP, CGMA What Makes Us Different, Makes You Better Overview of Reform Product of budget

The Tax Cuts and Jobs Act1 (TCJA) made

made") Significant Provisions of the Tax Cuts and Jobs Act Affecting Closely Held Businesses and Their Owners by Gerald A. Shanker The Tax Cuts and Jobs Act1 (TCJA) made significant changes to the Internal Revenue

Significant Provisions of the Tax Cuts and Jobs Act Affecting Closely Held Businesses and Their Owners by Gerald A. Shanker The Tax Cuts and Jobs Act1 (TCJA) made significant changes to the Internal Revenue

Tax Cuts and Jobs Act of 2017

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

Head of Household $0 - $9,525 $13,600 $9,525 - $38,700 $13,600 - $51,800 $38,700 - $82,500 $51,800 - $82,500 $82,500 - $157,500 $157,500

TAX REFORM - IMPACT TO INDIVIDUALS Summary On Friday, December 22, 2017, the President signed the Tax Cuts and Jobs Act (the Act ). The Act provides the most comprehensive update to the tax code since

TAX REFORM - IMPACT TO INDIVIDUALS Summary On Friday, December 22, 2017, the President signed the Tax Cuts and Jobs Act (the Act ). The Act provides the most comprehensive update to the tax code since

Tax Reform The Tax Cuts and Jobs Act March 2, 2018

FPA of Greater Indiana Tax Reform The Tax Cuts and Jobs Act March 2, 2018 Presented by: William R. Owen, Jr. CPA, CFP BGBC Partners, LLP 300 N. Meridian Street Indianapolis, IN 46204 (317) 860-1092 FPA

FPA of Greater Indiana Tax Reform The Tax Cuts and Jobs Act March 2, 2018 Presented by: William R. Owen, Jr. CPA, CFP BGBC Partners, LLP 300 N. Meridian Street Indianapolis, IN 46204 (317) 860-1092 FPA

Tax Cut and Jobs Act. (updated 12/17/17) assurance - consulting - tax - technology - pncpa.com

assurance - consulting - tax - technology - pncpa.com") Tax Cut and Jobs Act (updated 12/17/17) assurance - consulting - tax - technology - pncpa.com Postlethwaite & Netterville, A Professional Accounting Corporation Overview Individual Tax Tax Reform Individual

Tax Cut and Jobs Act (updated 12/17/17) assurance - consulting - tax - technology - pncpa.com Postlethwaite & Netterville, A Professional Accounting Corporation Overview Individual Tax Tax Reform Individual

May 8, 2018 Watkins Glen, New York

May 8, 2018 Watkins Glen, New York This presentation is intended for general educational and/or informational purposes only and does not replace specific, independent professional advice. This presentation

May 8, 2018 Watkins Glen, New York This presentation is intended for general educational and/or informational purposes only and does not replace specific, independent professional advice. This presentation

Tax Cuts and Jobs Act Key Implications for Individuals

Tax Cuts and Jobs Act Key Implications for Individuals Overview The 2017 Tax Reform legislation, the most significant federal tax law reform in over 30 years, was passed by both the House of Representatives

Tax Cuts and Jobs Act Key Implications for Individuals Overview The 2017 Tax Reform legislation, the most significant federal tax law reform in over 30 years, was passed by both the House of Representatives

Tax Bill Comparison. December 2017

Tax Bill Comparison December 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $45,000 $0 to $9,525 $9,525 to $38,700 $45,000 to $200,000 $9,325 to $38,700 $38,700 to $93,700 $200,000

Tax Bill Comparison December 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $45,000 $0 to $9,525 $9,525 to $38,700 $45,000 to $200,000 $9,325 to $38,700 $38,700 to $93,700 $200,000

Tax Update Focusing on the Tax Cuts and Jobs Act of John F. Ermer, CPA Israel O. Perez, CPA

Tax Update Focusing on the Tax Cuts and Jobs Act of 2017 John F. Ermer, CPA Israel O. Perez, CPA Contact Information John F. Ermer, CPA E-mail: jermer@bhcbcpa.com Telephone: 203) 787-6527 Israel O. Perez,

Tax Update Focusing on the Tax Cuts and Jobs Act of 2017 John F. Ermer, CPA Israel O. Perez, CPA Contact Information John F. Ermer, CPA E-mail: jermer@bhcbcpa.com Telephone: 203) 787-6527 Israel O. Perez,

(615)

") Welcome Brian B. McCuller is the Tax Practice Leader for LBMC. Brian is an attorney and a CPA with over twenty years of experience in the state and local tax field. He specializes in multi-state tax planning

Welcome Brian B. McCuller is the Tax Practice Leader for LBMC. Brian is an attorney and a CPA with over twenty years of experience in the state and local tax field. He specializes in multi-state tax planning

2018 Corporate/Business Tax Law Review

BUSINESS CONCEPTS MARCH 2018 2018 Corporate/Business Tax Law Review In our last tax article, we discussed how the 2017 Tax Cuts and Jobs Act (TCJA) brought many changes to individual income tax filers.

BUSINESS CONCEPTS MARCH 2018 2018 Corporate/Business Tax Law Review In our last tax article, we discussed how the 2017 Tax Cuts and Jobs Act (TCJA) brought many changes to individual income tax filers.

Biggest tax bill in 30+ years redefines tax landscape

NBC Tower - Suite 1500 455 North Cityfront Plaza Drive Chicago, IL 60611 312.670.7444 www.orba.com Biggest tax bill in 30+ years redefines tax landscape On December 22, 2017, the most sweeping tax legislation

NBC Tower - Suite 1500 455 North Cityfront Plaza Drive Chicago, IL 60611 312.670.7444 www.orba.com Biggest tax bill in 30+ years redefines tax landscape On December 22, 2017, the most sweeping tax legislation

The Tax Cuts and Jobs Act Impact on C Corps, S Corps and Individuals

The Tax Cuts and Jobs Act Impact on C Corps, S Corps and Individuals Charles J. Garrison, CPA Joseph M. Press, CPA Community Bankers Association of Oklahoma 2018 Annual Convention September 13, 2018 Corporation

The Tax Cuts and Jobs Act Impact on C Corps, S Corps and Individuals Charles J. Garrison, CPA Joseph M. Press, CPA Community Bankers Association of Oklahoma 2018 Annual Convention September 13, 2018 Corporation

Tax Update for 2018 and 2019

Tax Update for 2018 and 2019 Individual Tax Changes Business Tax Changes Depreciation Changes Inflation Adjustments IRS Mileage Rates Affordable Care Act Partnership Audit Rules The following is a summary

Tax Update for 2018 and 2019 Individual Tax Changes Business Tax Changes Depreciation Changes Inflation Adjustments IRS Mileage Rates Affordable Care Act Partnership Audit Rules The following is a summary

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE. Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP MOST SWEEPING TAX REFORM SINCE 1986 Tax Cuts and Jobs Act signed December 22, 2017 Generally

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP MOST SWEEPING TAX REFORM SINCE 1986 Tax Cuts and Jobs Act signed December 22, 2017 Generally

Business Tax Provisions

On December 22, 2017, President Trump signed the Tax Jobs and Cuts Act of 2017 (the Act). This will be the biggest tax overhaul in 30 years. The provisions below affect all entities from individuals to

On December 22, 2017, President Trump signed the Tax Jobs and Cuts Act of 2017 (the Act). This will be the biggest tax overhaul in 30 years. The provisions below affect all entities from individuals to

Individual Taxes. TAX CUTS & JOBS ACT OF Tax Brackets: 7 Tax Brackets: 7 Tax Brackets: 4 Tax Brackets:

COMPARISON OF CURRENT TAX LAW VS. TAX CUTS AND JOBS ACT Individual Taxes Ordinary Income Tax Brackets (Single Tax Brackets Shown) 10%: $0 - $9,325 15%: $9,326 - $37,950 25%: $37,951 - $91,900 28%: $91,901

COMPARISON OF CURRENT TAX LAW VS. TAX CUTS AND JOBS ACT Individual Taxes Ordinary Income Tax Brackets (Single Tax Brackets Shown) 10%: $0 - $9,325 15%: $9,326 - $37,950 25%: $37,951 - $91,900 28%: $91,901

The Impact of Tax Reform on Businesses and Individuals BOSTON NEWPORT PROVIDENCE SHANGHAI WALTHAM KAHNLITWIN.COM

The Impact of Tax Reform on Businesses and Individuals BOSTON NEWPORT PROVIDENCE SHANGHAI WALTHAM KAHNLITWIN.COM Presented by LAURA H. YALANIS, CPA/MST SHAREHOLDER I work closely with clients to help them

The Impact of Tax Reform on Businesses and Individuals BOSTON NEWPORT PROVIDENCE SHANGHAI WALTHAM KAHNLITWIN.COM Presented by LAURA H. YALANIS, CPA/MST SHAREHOLDER I work closely with clients to help them

HIGHLIGHTS OF TAX CUTS AND JOBS ACT OF 2017

HIGHLIGHTS OF TAX CUTS AND JOBS ACT OF 2017 SELECTED CHANGES PRIMARILY IMPACTING INDIVIDUALS INDIVIDUAL INCOME TAX RATES (Effective for tax years beginning after 2017 and before 2026) Single Individuals

HIGHLIGHTS OF TAX CUTS AND JOBS ACT OF 2017 SELECTED CHANGES PRIMARILY IMPACTING INDIVIDUALS INDIVIDUAL INCOME TAX RATES (Effective for tax years beginning after 2017 and before 2026) Single Individuals

N/A. Kiddie Tax Various bracket thresholds Ordinary and capital gains rates applicable to trusts and estates

We have prepared a summary of the House and the Senate versions of the proposed tax reform bill. Once they reach an agreement on a final bill, we will update the summary as needed. House Bill (H. R. 1)

We have prepared a summary of the House and the Senate versions of the proposed tax reform bill. Once they reach an agreement on a final bill, we will update the summary as needed. House Bill (H. R. 1)

12/19/2018 THOUGHTWARE. Financial Services THOUGHTWARE. Tax Reform Update. Income Tax Update for Financial Institutions

THOUGHTWARE Financial Services THOUGHTWARE Financial Services Tax Reform Update Income Tax Update for Financial Institutions December 20, 2018 1 To Receive CPE Credit Individuals Participate in entire

THOUGHTWARE Financial Services THOUGHTWARE Financial Services Tax Reform Update Income Tax Update for Financial Institutions December 20, 2018 1 To Receive CPE Credit Individuals Participate in entire

SENATE TAX REFORM PROPOSAL INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only

The following chart sets forth some of the provisions affecting individuals in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only

Tax Reform Update Highlights as of March Reg Baker CPA LLC (808)

") Tax Reform Update Highlights as of March 2018 Reg Baker CPA LLC (808) 753-6026 reg@regbaker.com www.regbaker.com 1 DISCLAIMER The material appearing in this presentation is for informational purposes only

Tax Reform Update Highlights as of March 2018 Reg Baker CPA LLC (808) 753-6026 reg@regbaker.com www.regbaker.com 1 DISCLAIMER The material appearing in this presentation is for informational purposes only

Michael J. Reilly, CPA/ABV, CVA, CFF, CDA Nicholas L. Shires, CPA

Michael J. Reilly, CPA/ABV, CVA, CFF, CDA Nicholas L. Shires, CPA Key Tax Provisions in the Tax Cut and Jobs Act Michael J. Reilly, CPA/ABV, CVA, CFF, CDA - Tax Partner Nicholas L. Shires, CPA - Tax Partner

Michael J. Reilly, CPA/ABV, CVA, CFF, CDA Nicholas L. Shires, CPA Key Tax Provisions in the Tax Cut and Jobs Act Michael J. Reilly, CPA/ABV, CVA, CFF, CDA - Tax Partner Nicholas L. Shires, CPA - Tax Partner

TAX CUTS AND JOBS ACT SUMMARY

TAX CUTS AND JOBS ACT SUMMARY Mariner Retirement Advisors The Tax Cuts and Jobs Act ( TCJA ) was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and

TAX CUTS AND JOBS ACT SUMMARY Mariner Retirement Advisors The Tax Cuts and Jobs Act ( TCJA ) was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and

WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES

Tax Reform: WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES Presented By: JOHN HELLER, CPA Manager Tax Services Group Agenda We will cover: Review Corporate Tax Changes Business Deduction Changes

Tax Reform: WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES Presented By: JOHN HELLER, CPA Manager Tax Services Group Agenda We will cover: Review Corporate Tax Changes Business Deduction Changes

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU THE TAX CUTS & JOBS ACT OF 2017 (HR 1) Preliminary Summary Analysis Presented by: A. Mac Stevens, CPA Member of the Eide Bailly LLP National Tax Office Ron

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU THE TAX CUTS & JOBS ACT OF 2017 (HR 1) Preliminary Summary Analysis Presented by: A. Mac Stevens, CPA Member of the Eide Bailly LLP National Tax Office Ron

2017 Tax Cuts and Jobs Act: Impact on U.S. Real Estate Businesses

CLIENT MEMORANDUM 2017 Tax Cuts and Jobs Act: Impact on U.S. Real Estate Businesses January 30, 2018 The new tax act signed into law on December 22, 2017, popularly known as the Tax Cuts and Jobs Act (

CLIENT MEMORANDUM 2017 Tax Cuts and Jobs Act: Impact on U.S. Real Estate Businesses January 30, 2018 The new tax act signed into law on December 22, 2017, popularly known as the Tax Cuts and Jobs Act (

Impact of Tax Reform on Farmers. Tax and Accounting Department Fall 2018

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Today s Outline. Tax Cuts and Jobs Act of 2017

Today s Outline Tax Cuts and Jobs Act of 2017 I. Introduction and Background II. Individual Income Tax III. Business Tax IV. Employment, Compensation and Retirement V. Tax-Exempt Organization VI. Estate

Today s Outline Tax Cuts and Jobs Act of 2017 I. Introduction and Background II. Individual Income Tax III. Business Tax IV. Employment, Compensation and Retirement V. Tax-Exempt Organization VI. Estate

Implications of the 2017 Tax Act: Choice of Entity

Implications of the 2017 Tax Act: Choice of Entity January 25, 2018: Bruce Booken, Buchanan Ingersoll & Rooney Lisa Starczewski, Buchanan Ingersoll & Rooney Samuel Starr, Bloomberg BNA 1 The 2017 Tax Act

Implications of the 2017 Tax Act: Choice of Entity January 25, 2018: Bruce Booken, Buchanan Ingersoll & Rooney Lisa Starczewski, Buchanan Ingersoll & Rooney Samuel Starr, Bloomberg BNA 1 The 2017 Tax Act

Law Offices of Bradley J. Frigon 6500 S. Quebec St. Suite 330 Englewood, CO

2018 National Conference on Special Needs Planning and Special Needs Trusts Tax Reform and Year End Tax Planning for Self Settled and Third Party Trusts Bradley J. Frigon October 18, 2018 Law Offices of

2018 National Conference on Special Needs Planning and Special Needs Trusts Tax Reform and Year End Tax Planning for Self Settled and Third Party Trusts Bradley J. Frigon October 18, 2018 Law Offices of