Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F

|

|

|

- Godwin Perkins

- 5 years ago

- Views:

Transcription

1 Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F

2 OUR GOAL FOR TODAY Develop an awareness of the recent law changes that will affect healthcare organizations

3 OUR GOAL FOR TODAY The Good News The Bad News & More

4 What Didn t Make the Cut The Good News!

5 WHAT DIDN T MAKE THE CUT? Clarification of unrelated business income tax treatment of entities exempt from tax under section 501(a) (House) Exclusion of research income from unrelated business taxable income limited to publicly available research (House) Simplification of excise tax on private foundation investment income (House)

6 WHAT DIDN T MAKE THE CUT? Private operating foundation requirements relating to operation of an art museum (House) Exception to the private foundation excess business holdings rules for philanthropic business holdings (House) Section 501(c)(3) organizations permitted to make statements relating to political campaign in ordinary course of activities in carrying out exempt purpose (House)

7 Additional reporting requirements for donor advised fund sponsoring organizations (House) WHAT DIDN T MAKE THE CUT? Name & logo treated as unrelated business income (Senate) Repeal of tax-exempt status for professional sports leagues (Senate)

8 Modification of taxes on excess benefit transactions (intermediate sanctions) (Senate) WHAT DIDN T MAKE THE CUT? Reduction in minimum age for allowable in-service distributions (House) Termination of private activity bond (House) No tax-exempt bonds for professional stadiums (House)

9 Modification of rules governing hardship distributions (House) WHAT DIDN T MAKE THE CUT? Modification of rules related to hardship withdrawals from cash or deferred arrangements (Senate) Modification of nondiscrimination rules for certain plans providing benefits or contributions to older, longer service participants (House)

10 Limitation on exclusion for employer-provided housing (House) WHAT DIDN T MAKE THE CUT? Repeal of exclusion for employee achievement awards (House) Sunset of exclusion for dependent care assistance programs (House)

11 Repeal of exclusion for educational assistance programs (House) WHAT DIDN T MAKE THE CUT? Repeal of exclusion for qualified tuition reductions (House) Repeal of exclusion for adoption assistance programs (House)

12 Repeal of deduction for student loan interest (House) WHAT DIDN T MAKE THE CUT? Repeal of deduction for qualified tuition & related expenses (House) Repeal of deduction for student loan interest (House)

13 WHAT DIDN T MAKE THE CUT? Repeal of exclusion for interest on U.S. savings bonds used for higher education expenses (House) Termination of New Markets Tax Credit (House)

14 What Made the Cut The Bad News for Exempt Healthcare!

15 Excise Tax on Compensation in Excess of $1M EXCISE TAX ON EXECUTIVE COMPENSATION Follows corporate rate (21%) Five highest-paid employees Taxable compensation Includes nonqualified deferred compensation from ineligible deferred compensation includible when there is not substantial risk of forfeiture (457(f))

16 Excise Tax Parachute payments 3x greater than the five-year salary average (excluding retirement benefits) Exempts not highly compensated employees from the definition of parachute payments Exempts professional medical services COMPENSATION & EMPLOYEE BENEFITS

17 COMPENSATION & EMPLOYEE BENEFITS Exclusion for qualified moving expense reimbursement repealed Exception for active duty members of the Armed Forces

18 UNRELATED BUSINESS INCOME FOR CORPS Corporate Tax Rates Taxable Income Income Tax All Income 21%

19 UNRELATED BUSINESS INCOME FOR TRUSTS Trust Tax Rates Taxable Income Income Tax Not over $2,550 10% $2,551 $9,150 $ % of the excess over $2,550 $9,151 $12,500 $1, % of the excess over $9,150 > $12,500 $3, % of the excess over $12,500

20 UNRELATED BUSINESS INCOME Silo Income/Loss by Activity Loss from one activity cannot offset income from another Activity Definition PTP Investment K-1 Investment Royalties Rents Other? Effective years beginning after December 31, 2017

21 UNRELATED BUSINESS INCOME UBI Increased by Certain Fringe Benefits Qualified transportation, and Qualified parking Guidance needed to determine what is included? Out of pocket payments to third party vendors Cost or FMV of owned property Effective beginning December 31, 2017

22 Corporate alternative minimum tax repealed Bonus depreciation 100% through 2022, then scaled back through 2026 UNRELATED BUSINESS INCOME Business Provisions that might impact your organization Section 179 expensing $1M

Net interest expense limitation No entertainment deductions UNRELATED BUSINESS INCOME Business")

23 NOL deduction 80% taxable income (generated after ) Net interest expense limitation No entertainment deductions UNRELATED BUSINESS INCOME Business Provisions that might impact your organization

24 TAX-EXEMPT BONDS Repeals the exclusion from gross income for interest on advance refunding bonds

25 PRIVATE ACTIVITY BONDS Repeal of Tax Credit Bonds Clean renewable energy bonds Qualified energy conservation bonds Qualified zone academy bonds Qualified school construction bonds Direct-pay bonds

26 Increase limitation to 60% Standard mileage rate, not adjusted for inflation No deduction for payments made in exchange for college athletic seating rights CHARITABLE CONTRIBUTIONS

27 Increased standard deductions ITEMIZED DEDUCTIONS $10,000 limit on state & local tax deduction Medical expense deduction Impact on charitable giving?

28 ESTATE TAX Increase exclusion to $10M Inflation adjustment $11.2M 2018 Regulations for differences between the basic exclusion amount in effect At the time of decedent's death At the time of any gifts made by the descendent Effective for estates of decedents dying & gifts made after December 31, 2017

29 Decline in Charitable Giving? HOW WILL THIS IMPACT MY ORGANIZATION? Itemized Deductions: Sales Tax $ 2, $ - $ - Real Estate Taxes $ 15, $ 10, $ 10, Home Mortgage Interest $ - $ - $ - Charity $ 7, $ 7, $ - Increased Standard Deduction $ - $ 7, $ 14, Total Itemized Deductions $ 24, $ 24, $ 24,000.00

30 DONOR STRATEGIES? Bunching of itemized deductions Donor advised funds Qualified charitable distributions (QCDs)

31 BUNCHING ILLUSTRATION BUNCHING Itemized Deductions: State income tax $ 10, $ 10, $ 10, $ 10, Real Estate Taxes $ - $ - $ - $ - Home Mortgage Interest $ 8, $ 7, $ 8, $ 7, Charity $ 20, $ - $ 20, $ - Increased Standard Deduction $ - $ 6, $ - $ 6, Total Itemized Deductions $ 38, $ 24, $ 38, $ 24, $ 125, WITHOUT BUNCHING Itemized Deductions: State income tax $ 10, $ 10, $ 10, $ 10, Real Estate Taxes $ - $ - $ - $ - Home Mortgage Interest $ 8, $ 8, $ 8, $ 8, Charity $ 10, $ 10, $ 10, $ 10, Increased Standard Deduction $ - $ - $ - $ - Total Itemized Deductions $ 28, $ 28, $ 28, $ 28, $ 112,000.00

32 DONOR ADVISED FUND ILLUSTRATION Even Charitable Over 5 Years Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 State Tax Deduction 10,000 10,000 10,000 10,000 10,000 Interest Expense Charitable 20,000 20,000 20,000 20,000 20,000 Total 30,000 30,000 30,000 30,000 30, ,000 Fund DAF in Year 1 Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 State Tax Deduction 10,000 10,000 10,000 10,000 10,000 Interest Expense Charitable 100, Additional standard deduction 14,000 14,000 14,000 14,000 Total 110,000 24,000 24,000 24,000 24, ,000

33 W/O QCD W/ QCD RMD Income 12,000 0 Itemized Deductions: State income tax 10,000 10,000 Real Estate Taxes 0 0 Home Mortgage Interest 0 0 Charity 12,000 0 Increased Standard Deduction 2,000 14,000 Total Itemized Deductions 24,000 24,000 QCD ILLUSTRATION

34 What Made the Cut The Good News for Taxable Healthcare!

35 21% Flat Tax Rate

36 Bonus Depreciation DEPRECIATION PROVISIONS Cost recovery 100 percent through 2022 for qualified property placed in service after September 27, , 60, 40 & 20 percent for property placed in service in , respectively Definition of qualified property expanded by removing requirement that original use begin with taxpayer Specified property included & excluded (Previously 40, 30 & 20 percent bonus depreciation for qualified property in , respectively; property must be new to qualify)

37 Section 179 Expensing DEPRECIATION PROVISIONS Cost recovery Up to $1 million Phaseout beginning at $2.5 million of assets placed in service Definition of qualified property expanded to include certain improvements to nonresidential real property, including roofs, HVAC systems, fire protection & alarm systems & security systems (Previously up to $520,000; phaseout beginning at $2,070,000 of assets placed in service)

38 Deduction generally limited to sum of Business interest income BUSINESS INTEREST EXPENSE DEDUCTION Floor plan financing interest 30 percent of adjusted taxable income Taxable income +/- Items of income, gain, deduction or loss not properly allocable to trade/business + Business interest expense - Business interest income + Net operating loss + Pass-through business deduction + Depletion, depreciation & amortization (taxable years beginning before January 1, 2022, only)

Following businesses may elect not to be subject to limitation provided they use ADS method for depreciation Real property businesses Farming")

39 Excess carried forward indefinitely BUSINESS INTEREST EXPENSE DEDUCTION Limit does not apply to Businesses with average annual gross receipts $25 million (affiliated group basis) Regulated public utility business (including electric cooperatives) Following businesses may elect not to be subject to limitation provided they use ADS method for depreciation Real property businesses Farming businesses (including agricultural & horticultural cooperatives)

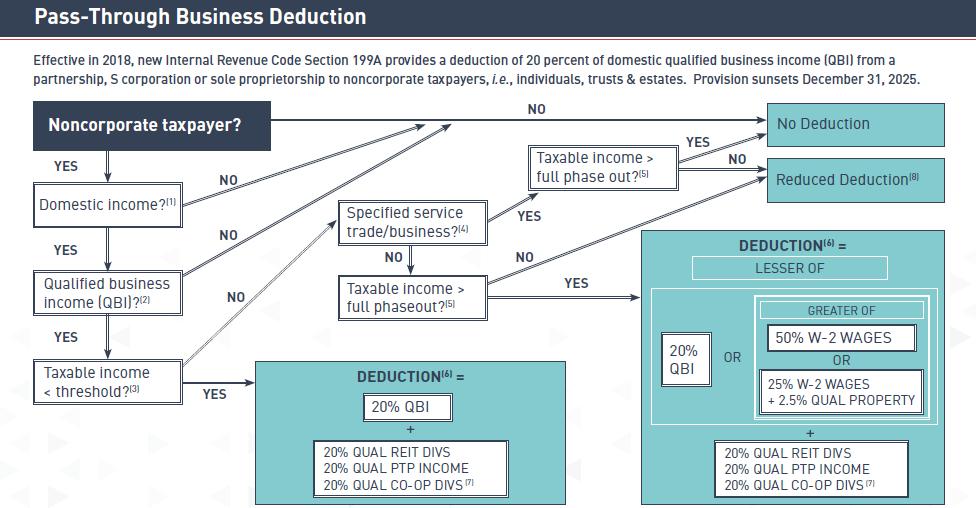

40 Pass-Through Business Deduction QUALIFIED BUSINESS INCOME DEDUCTION Sunsets 12/31/2025 Deduction = 20 percent of Domestic qualified business income from partnership, S corporation or sole proprietorship Qualified REIT dividends Qualified cooperative dividends Qualified PTP income Available to individuals, trusts & estates Aimed at maintaining tax rate benefit of flowthrough structure Sunsets December 31, 2025 Limitations apply

41 Domestic: effectively connected with conduct of trade/business within U.S. & Puerto Rico QUALIFIED BUSINESS INCOME DEDUCTION Sunsets 12/31/2025 Qualified business income: net amount of items of income, gain, deduction & loss with respect to any qualified trade or business, except Reasonable compensation Guaranteed payments Investment income Short-term & long-term capital gain/loss Dividend income Interest income (Note overall loss treated as loss for purposes of calculation in subsequent year)

42 QUALIFIED BUSINESS INCOME DEDUCTION Sunsets 12/31/2025 Limitations: Apply when taxable income exceeds $157,500 single ($315,000 MFJ) & phase out over next $50,000 ($100,000) of taxable income 1) Wage limitation: Greater of 50 percent of W-2 wages paid with respect to business OR 25 percent of W-2 wages paid plus 2.5 percent of unadjusted basis (immediately after acquisition) of all qualified property 2) Not allowed for specified service trade or businesses once income exceeds threshold amounts

43 Specified service business: Any trade or business involving performance of services in fields of QUALIFIED BUSINESS INCOME DEDUCTION Sunsets 12/31/2025 Health Law Accounting Actuarial science Performance arts Investing & investment management, trading or dealing in securities, partnership interests or commodities Consulting Athletics Financial services Brokerage service Principal asset is reputation or skill of one or more of its employees or owners

44 Need further guidance in several areas QUALIFIED BUSINESS INCOME DEDUCTION Sunsets 12/31/2025 Definition qualified trade or business Application of grouping elections Clarification on how definition of specified service trade or business applies Whether wages paid by an affiliated management company count for purposes of wage limitation

45

46

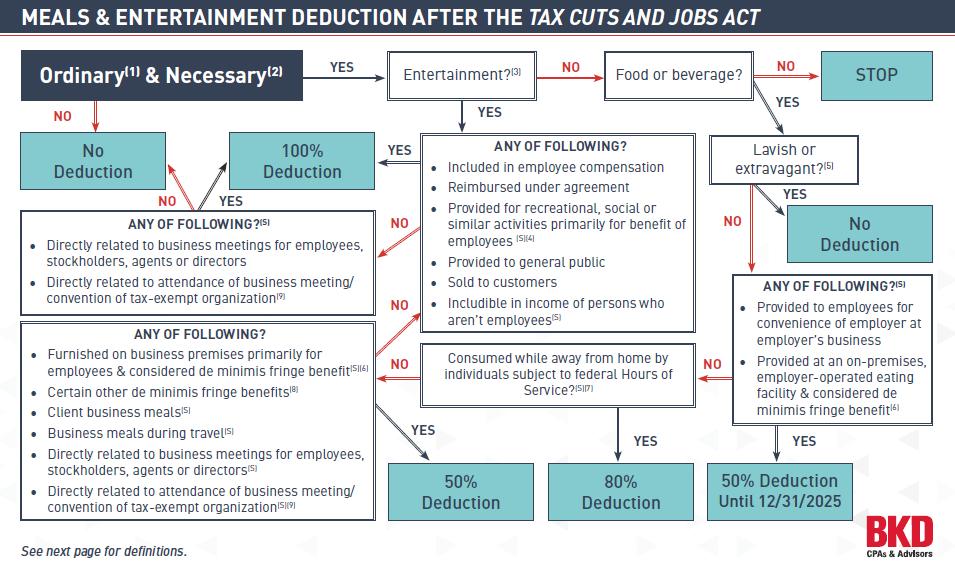

47 Entertainment Expense Entertainment expenses no longer deductible Meals Expenditures Business meals remain 50% deductible Convenience meals now subject to 50% limit; previously fully deductible OTHER CONSIDERATIONS FOR TAXABLE ENTITIES

48

49

50 Carried Interest Partnership profits interest in connection with performance of services Long-term capital gain rate after three-year holding period with respect to any applicable partnership interest Like-Kind Exchange Deferral of gain limited to real property not held primarily for sale Cash Method of Accounting Allowed for C Corporations with <$25mil in gross receipts (Previously <$5mil) OTHER CONSIDERATIONS FOR TAXABLE ENTITIES

51 Pass-through vs C Corp ENTITY STRUCTURE COMPARISON Pass-through entity 37% top rate with no QBI deduction 29.6% top rate with full QBI deduction No deduction for state income tax C corporation 39.8% top rate if all profits are distributed (blended rate: 21% corp rate; 23.8% max dividend rate) Full deduction for state income tax

52 Pass-through vs C Corp ENTITY STRUCTURE COMPARISON Long-term distribution plans Pass-through favors high distribution rate C corp favors low distribution rate Long-term succession plans Buyers want assets, not C corp shares Customized modeling essential

53 PLANNING STRATEGIES FOR BUSINESSES Consider strategies to accelerate deductions & defer income for permanent tax savings Capital repair expensing & partial dispositions Accounting method changes R&D credit studies Cost segregation studies

54 Keep Up with What s Next BKD Contacts alewman@bkd.com pgerich@bkd.com BKD Tax Reform Resource Center bkd.com/taxreform Simply Tax Podcast bkd.com/simplytax BKD Year-End Advisor bkd.com/advisor

55 Questions?

56 Thank You!

Tax Cuts & Jobs Act of 2017

Tax Cuts & Jobs Act of 2017 What Exempt Organizations Need to Know BIG CHANGES AHEAD FOR EXEMPT ORGANIZATIONS DECEMBER 20, 2017 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

Tax Cuts & Jobs Act of 2017 What Exempt Organizations Need to Know BIG CHANGES AHEAD FOR EXEMPT ORGANIZATIONS DECEMBER 20, 2017 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018 WHAT WE WILL COVER TODAY 1 2 Business & individual provisions of the Tax Cuts and Jobs

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018 WHAT WE WILL COVER TODAY 1 2 Business & individual provisions of the Tax Cuts and Jobs

How Does Tax Reform Affect Real Estate Developers & Investors?

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

Tax Reform s Effect on the Banking Industry

Tax Reform s Effect on the Banking Industry FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete

Tax Reform s Effect on the Banking Industry FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete

TAX CUTS AND JOBS ACT

TAX CUTS AND JOBS ACT Businesses Corporate tax rate will now be a flat 21% beginning January 1, 2018. Corporate alternative minimum tax has been repealed. Effective for tax years beginning after December

TAX CUTS AND JOBS ACT Businesses Corporate tax rate will now be a flat 21% beginning January 1, 2018. Corporate alternative minimum tax has been repealed. Effective for tax years beginning after December

2017 Tax Reform What you need to Know

Oil & Natural Gas Accounting & Tax 2018 2017 Tax Reform What you need to Know November 8, 2018 J. Marlin Witt, CPA, CFP, CGMA What Makes Us Different, Makes You Better Overview of Reform Product of budget

Oil & Natural Gas Accounting & Tax 2018 2017 Tax Reform What you need to Know November 8, 2018 J. Marlin Witt, CPA, CFP, CGMA What Makes Us Different, Makes You Better Overview of Reform Product of budget

Adam Williams. Anthony Licavoli. Principal Tax Manager

1 2 Adam Williams Principal 734.302.4179 adam.williams@rehmann.com Anthony Licavoli Tax Manager 248.463.4598 anthony.licavoli@rehmann.com 3 4 5 What is your impression about the speed at which Congress

1 2 Adam Williams Principal 734.302.4179 adam.williams@rehmann.com Anthony Licavoli Tax Manager 248.463.4598 anthony.licavoli@rehmann.com 3 4 5 What is your impression about the speed at which Congress

Tax-Exempt Highlights Comparison. Tax Cuts and Jobs Act of 2017

Tax-Exempt Highlights Comparison Tax Cuts and Jobs Act of 2017 On December 22, President Trump signed into law the (P.L. 115-97), a sweeping tax reform law that will entirely change the tax landscape.

Tax-Exempt Highlights Comparison Tax Cuts and Jobs Act of 2017 On December 22, President Trump signed into law the (P.L. 115-97), a sweeping tax reform law that will entirely change the tax landscape.

Tax cuts and jobs act

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

Corporate and Business Provision House Bill (HR 1) Senate Bill Final Bill

Senate Bill Final Bill") Selected provisions of the House and Senate tax reform bills as passed by both houses of Congress which resulted in the final bill in the far right column. Introduction: This summary contains what ZLQ

Selected provisions of the House and Senate tax reform bills as passed by both houses of Congress which resulted in the final bill in the far right column. Introduction: This summary contains what ZLQ

How Tax Reforms Impacts Your Vineyard February 8, Presented by: Kathy Freshwater, CPA Craig Anderson, CPA

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

HFMA Annual AccounTing and AudiTing UpdaTe. Tax UpdaTe

HFMA Annual AccounTing and AudiTing UpdaTe Tax UpdaTe Presented by: Jeffrey J. Petrell, JD, CPA, CGMA Partner Health Care Tax Services Kelly A. Brocious, CPA Senior Manager Health Care Tax Services 97

HFMA Annual AccounTing and AudiTing UpdaTe Tax UpdaTe Presented by: Jeffrey J. Petrell, JD, CPA, CGMA Partner Health Care Tax Services Kelly A. Brocious, CPA Senior Manager Health Care Tax Services 97

Tax Cuts & Jobs Act of 2017

Tax Cuts & Jobs Act of 2017 WHAT BUSINESSES & S NEED TO KNOW DECEMBER 19, 2017 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in

Tax Cuts & Jobs Act of 2017 WHAT BUSINESSES & S NEED TO KNOW DECEMBER 19, 2017 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in

Pass-Through Considerations of Tax Reform

Pass-Through Considerations of Tax Reform JANUARY 23, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group

Pass-Through Considerations of Tax Reform JANUARY 23, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

Tax Cuts and Jobs Act. Durham Chamber of Commerce Public Policy Meeting January 9, 2018

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

Tax reform for tax-exempt organizations and donors

Tax reform for tax-exempt organizations and donors Congress has passed the conference agreement for tax reform. Background On Friday, December 15, the conference committee approved the report of its agreement

Tax reform for tax-exempt organizations and donors Congress has passed the conference agreement for tax reform. Background On Friday, December 15, the conference committee approved the report of its agreement

New Tax Rules. For You and Your Business Owners

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

TAX CUTS & JOBS ACT DEVELOPMENTS

TAX CUTS & JOBS ACT DEVELOPMENTS P L A N N I N G F O R B U S I N E S S E S A N D I N D I V I D U A L S D E C E M B E R 1 2, 2 0 1 8 THE TAX CUTS & JOBS ACT AT A GLANCE BUSINESS PROVISIONS Reduced Tax Rates

TAX CUTS & JOBS ACT DEVELOPMENTS P L A N N I N G F O R B U S I N E S S E S A N D I N D I V I D U A L S D E C E M B E R 1 2, 2 0 1 8 THE TAX CUTS & JOBS ACT AT A GLANCE BUSINESS PROVISIONS Reduced Tax Rates

Tax Reform Highlights

etax Alert Tax Reform Highlights Final Business/Corporate/Partnership Provisions in Tax Cuts and Jobs Act of 2017 Here is a chart that briefly summarizes the major provisions affecting our business clients,

etax Alert Tax Reform Highlights Final Business/Corporate/Partnership Provisions in Tax Cuts and Jobs Act of 2017 Here is a chart that briefly summarizes the major provisions affecting our business clients,

KPMG report: Tax reform for taxexempt organizations and donors

KPMG report: Tax reform for taxexempt organizations and donors December 6, 2017 Tax reform for tax-exempt organizations and donors A number of provisions in both the House and Senate tax reform proposals

KPMG report: Tax reform for taxexempt organizations and donors December 6, 2017 Tax reform for tax-exempt organizations and donors A number of provisions in both the House and Senate tax reform proposals

The Qualified Business Income Deduction Under the Tax Cuts and Jobs Act

The Qualified Business Income Deduction Under the Tax Cuts and Jobs Act By Julia Dengel, jdengel@bkd.com The Tax Cuts and Jobs Act (TCJA) made significant changes to corporate and individual taxation,

The Qualified Business Income Deduction Under the Tax Cuts and Jobs Act By Julia Dengel, jdengel@bkd.com The Tax Cuts and Jobs Act (TCJA) made significant changes to corporate and individual taxation,

AAO Board of Trustees and Council on Government Affairs. Analysis of New Tax Reform Law

Memorandum To: From: AAO Board of Trustees and Council on Government Affairs Arnold & Porter Kaye Scholer Date: December 22, 2017 Re: Analysis of New Tax Reform Law This memo is intended for use by the

Memorandum To: From: AAO Board of Trustees and Council on Government Affairs Arnold & Porter Kaye Scholer Date: December 22, 2017 Re: Analysis of New Tax Reform Law This memo is intended for use by the

2017 Tax Reform Bill. Education Provisions Impacting Schools, Colleges, Universities and Employers

2017 Tax Reform Bill Education Provisions Impacting Schools, Colleges, Universities and Employers Topic Bill s IRC s American Opportunity Tax Credit 1201 25A Combines the Hope and Lifetime Learning credits

2017 Tax Reform Bill Education Provisions Impacting Schools, Colleges, Universities and Employers Topic Bill s IRC s American Opportunity Tax Credit 1201 25A Combines the Hope and Lifetime Learning credits

TAX CUTS AND JOB ACT OF 2017 Highlights

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS. February 8, 2018 Bruce I. Booken Rose K. Wilson

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS February 8, 2018 Bruce I. Booken Rose K. Wilson The 2017 Tax Act Signed into law on December 22, 2017 Provisions apply NOW to taxable years beginning after

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS February 8, 2018 Bruce I. Booken Rose K. Wilson The 2017 Tax Act Signed into law on December 22, 2017 Provisions apply NOW to taxable years beginning after

COMPARISON OF THE HOUSE- AND SENATE-PASSED VERSIONS OF THE TAX CUTS AND JOBS ACT

COMPARISON OF THE HOUSE- AND SENATE-PASSED VERSIONS OF THE TAX CUTS AND JOBS ACT Prepared by the Staff of the JOINT COMMITTEE ON TAXATION December 7, 2017 JCX-64-17 INTRODUCTION This document, 1 prepared

COMPARISON OF THE HOUSE- AND SENATE-PASSED VERSIONS OF THE TAX CUTS AND JOBS ACT Prepared by the Staff of the JOINT COMMITTEE ON TAXATION December 7, 2017 JCX-64-17 INTRODUCTION This document, 1 prepared

The Impact of the Tax Cuts and Jobs Act of 2017 on Tax Exempt Organizations. Presented by: Eugene J. Logan, CPA Ellen A.

The Impact of the Tax Cuts and Jobs Act of 2017 on Tax Exempt Organizations Presented by: Eugene J. Logan, CPA Ellen A. Martin, CPA CPE Reminders To receive continuing education credit, you must answer

The Impact of the Tax Cuts and Jobs Act of 2017 on Tax Exempt Organizations Presented by: Eugene J. Logan, CPA Ellen A. Martin, CPA CPE Reminders To receive continuing education credit, you must answer

Today s Outline. Tax Cuts and Jobs Act of 2017

Today s Outline Tax Cuts and Jobs Act of 2017 I. Introduction and Background II. Individual Income Tax III. Business Tax IV. Employment, Compensation and Retirement V. Tax-Exempt Organization VI. Estate

Today s Outline Tax Cuts and Jobs Act of 2017 I. Introduction and Background II. Individual Income Tax III. Business Tax IV. Employment, Compensation and Retirement V. Tax-Exempt Organization VI. Estate

ESTIMATED KANSAS IMPACT OF THE FEDERAL TAX CUTS AND JOBS ACT

ESTIMATED KANSAS IMPACT OF THE FEDERAL TAX CUTS AND JOBS ACT KANSAS DEPARTMENT OF REVENUE FEBRUARY 14, 2018 Summary... 2 Individual Tax Reform... 8 Tax Rate Reform... 8 Deduction for Qualified Business

ESTIMATED KANSAS IMPACT OF THE FEDERAL TAX CUTS AND JOBS ACT KANSAS DEPARTMENT OF REVENUE FEBRUARY 14, 2018 Summary... 2 Individual Tax Reform... 8 Tax Rate Reform... 8 Deduction for Qualified Business

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

Tax Reform: What You Need To Know

Tax Reform: What You Need To Know January 24, 2018 Presented by: Blake Harrison, CPA/PFS Senior Tax Manager LBMC Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on

Tax Reform: What You Need To Know January 24, 2018 Presented by: Blake Harrison, CPA/PFS Senior Tax Manager LBMC Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on

Tax Cuts and Jobs Act Passed by Congress

Tax Cuts and Jobs Act Passed by Congress On December 19 and 20, 2017, the House and Senate approved a final version of H.R. 1, the Tax Cuts and Jobs Act, renamed An Act to provide for reconcilation purusant

Tax Cuts and Jobs Act Passed by Congress On December 19 and 20, 2017, the House and Senate approved a final version of H.R. 1, the Tax Cuts and Jobs Act, renamed An Act to provide for reconcilation purusant

New Tax Law: Issues for Partnerships, S corporations, and Their Owners

New Tax Law: Issues for Partnerships, S corporations, and Their Owners January 18, 2018 1 Introduction H.R. 1, originally known as the Tax Cuts and Jobs Act, was signed into law on December 22, 2017. The

New Tax Law: Issues for Partnerships, S corporations, and Their Owners January 18, 2018 1 Introduction H.R. 1, originally known as the Tax Cuts and Jobs Act, was signed into law on December 22, 2017. The

2017 TAX CUTS AND JOBS ACT

2017 TAX CUTS AND JOBS ACT The Tax Cuts and Jobs Act was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and impacts most taxpayers; especially individuals

2017 TAX CUTS AND JOBS ACT The Tax Cuts and Jobs Act was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and impacts most taxpayers; especially individuals

What the Tax Cuts and Jobs Act Means for the Real Estate Industry

What the Tax Cuts and Jobs Act Means for the Real Estate Industry PRESENTED BY: ADAM HILL, CPA, PARTNER JON WILLIAMSON, CPA, MT, TAX MANAGER KIM PALMER, CPA, MT, PARTNER February 1, 2018 Welcome & Introductions

What the Tax Cuts and Jobs Act Means for the Real Estate Industry PRESENTED BY: ADAM HILL, CPA, PARTNER JON WILLIAMSON, CPA, MT, TAX MANAGER KIM PALMER, CPA, MT, PARTNER February 1, 2018 Welcome & Introductions

Jim Nitsche. Billy Hopkins. Sherry Porter

Billy Hopkins bhopkins@wyattfirm.com Jim Nitsche jnitsche@wyattfirm.com Sherry Porter spporter@wyattfirm.com Business Income Tax Changes 1. Corporate income tax rate reduced to 21% for tax years beginning

Billy Hopkins bhopkins@wyattfirm.com Jim Nitsche jnitsche@wyattfirm.com Sherry Porter spporter@wyattfirm.com Business Income Tax Changes 1. Corporate income tax rate reduced to 21% for tax years beginning

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal The Tax Act of 2017: H.R. 1 The Tax Cuts and Jobs Act short title was stricken An Act to provide for reconciliation

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal The Tax Act of 2017: H.R. 1 The Tax Cuts and Jobs Act short title was stricken An Act to provide for reconciliation

The Tax Cuts and Jobs Act Impact on C Corps, S Corps and Individuals

The Tax Cuts and Jobs Act Impact on C Corps, S Corps and Individuals Charles J. Garrison, CPA Joseph M. Press, CPA Community Bankers Association of Oklahoma 2018 Annual Convention September 13, 2018 Corporation

The Tax Cuts and Jobs Act Impact on C Corps, S Corps and Individuals Charles J. Garrison, CPA Joseph M. Press, CPA Community Bankers Association of Oklahoma 2018 Annual Convention September 13, 2018 Corporation

Tax Reform Implications for Higher Education

Tax Reform Implications for Higher Education Karen A. Gries, CPA, Principal Chastity Wilson, JD, LLM, CPA, Principal Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors,

Tax Reform Implications for Higher Education Karen A. Gries, CPA, Principal Chastity Wilson, JD, LLM, CPA, Principal Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors,

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU THE TAX CUTS & JOBS ACT OF 2017 (HR 1) Preliminary Summary Analysis Presented by: A. Mac Stevens, CPA Member of the Eide Bailly LLP National Tax Office Ron

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU THE TAX CUTS & JOBS ACT OF 2017 (HR 1) Preliminary Summary Analysis Presented by: A. Mac Stevens, CPA Member of the Eide Bailly LLP National Tax Office Ron

The Tax Cuts and Jobs Act of 2017

The Tax Cuts and Jobs Act of 2017 is the most comprehensive revision to the Internal Revenue Code Since 1986. This new Tax Act reduces tax rates for individuals and corporations, repeals exemptions, eliminates

The Tax Cuts and Jobs Act of 2017 is the most comprehensive revision to the Internal Revenue Code Since 1986. This new Tax Act reduces tax rates for individuals and corporations, repeals exemptions, eliminates

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 Important Highlights for Individuals and Small Businesses On December 15, 2017, Congress released the 2017 Tax Cut and Jobs Act ( the Act ) that has now passed both the House

Tax Cuts and Jobs Act of 2017 Important Highlights for Individuals and Small Businesses On December 15, 2017, Congress released the 2017 Tax Cut and Jobs Act ( the Act ) that has now passed both the House

Tax Cut and Jobs Act. (updated 12/17/17) assurance - consulting - tax - technology - pncpa.com

assurance - consulting - tax - technology - pncpa.com") Tax Cut and Jobs Act (updated 12/17/17) assurance - consulting - tax - technology - pncpa.com Postlethwaite & Netterville, A Professional Accounting Corporation Overview Individual Tax Tax Reform Individual

Tax Cut and Jobs Act (updated 12/17/17) assurance - consulting - tax - technology - pncpa.com Postlethwaite & Netterville, A Professional Accounting Corporation Overview Individual Tax Tax Reform Individual

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business August 10, 2018 Sarah Armstrong, Esq. Marjorie A. Rogers, Esq. Ed Street, CPA/ABV/CFF, CVA, ASA The information provided

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business August 10, 2018 Sarah Armstrong, Esq. Marjorie A. Rogers, Esq. Ed Street, CPA/ABV/CFF, CVA, ASA The information provided

Tax Cuts and Jobs Act 2017 HR 1

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

Tax Cuts and Jobs Act of 2017 (TCJA) Key Individual Tax Provisions

Key Individual Tax Provisions") Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

TAX REFORM INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

The following chart sets forth some of the provisions affecting individuals in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

H. R. 1. To provide for reconciliation pursuant to title II of the concurrent resolution on the budget for fiscal year 2018.

115TH CONGRESS 1ST SESSION H. R. 1... (Original Signature of Member) To provide for reconciliation pursuant to title II of the concurrent resolution on the budget for fiscal year 018. IN THE HOUSE OF REPRESENTATIVES

115TH CONGRESS 1ST SESSION H. R. 1... (Original Signature of Member) To provide for reconciliation pursuant to title II of the concurrent resolution on the budget for fiscal year 018. IN THE HOUSE OF REPRESENTATIVES

Tax Reform Act of 2014

Provisions Affecting Exempt Organizations On February 26, 2014, House Ways and Means Committee Chairman Dave Camp (R-MI-4) released his comprehensive tax reform proposal. Intended as a discussion draft

Provisions Affecting Exempt Organizations On February 26, 2014, House Ways and Means Committee Chairman Dave Camp (R-MI-4) released his comprehensive tax reform proposal. Intended as a discussion draft

Integrity Accounting

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

2018 TAX SEMINAR OPPORTUNITIES & IMPACTS. Tax Cuts and Jobs Acts Enacted December 22, Most changes go into effect January 1, 2018

2018 TAX SEMINAR OPPORTUNITIES & IMPACTS Tax Cuts and Jobs Acts Enacted December 22, 2017 Most changes go into effect January 1, 2018 S e m i n a r s p o n s o re d b y A n n L a u f m a n o f A L A F

2018 TAX SEMINAR OPPORTUNITIES & IMPACTS Tax Cuts and Jobs Acts Enacted December 22, 2017 Most changes go into effect January 1, 2018 S e m i n a r s p o n s o re d b y A n n L a u f m a n o f A L A F

Business Tax. Pass-Through Entities. New 20% Deduction

Business Tax Pass-Through Entities New 20% Deduction For tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026, taxpayers who have domestic qualified business income (QBI) from a partnership,

Business Tax Pass-Through Entities New 20% Deduction For tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026, taxpayers who have domestic qualified business income (QBI) from a partnership,

TAX REFORM INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

The following chart sets forth some of the provisions affecting individuals in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

Tax Reform: What Dealers Need to Know

Tax Reform: What Dealers Need to Know 1 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication is not intended or written

Tax Reform: What Dealers Need to Know 1 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication is not intended or written

TAX CUTS & JOBS ACT OF 2017

TAX CUTS & JOBS ACT OF 2017 Summary of Impact on Higher Education Institutions November 9, 2017 Joyce Dulworth, CPA Partner Nick Wallace, CPA Director 1 OVERVIEW On November 2, the House Ways & Means Committee

TAX CUTS & JOBS ACT OF 2017 Summary of Impact on Higher Education Institutions November 9, 2017 Joyce Dulworth, CPA Partner Nick Wallace, CPA Director 1 OVERVIEW On November 2, the House Ways & Means Committee

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU DISCLAIMER These materials, and the accompanying oral presentation, are for educational purposes only and are not intended to be written advice concerning

TAX REFORM: WHAT IT DOES, WHAT IT MEANS TO YOU DISCLAIMER These materials, and the accompanying oral presentation, are for educational purposes only and are not intended to be written advice concerning

Tax Cuts and Jobs Act February 8, 2018

Tax Cuts and Jobs Act 2017 February 8, 2018 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any specific taxpayer

Tax Cuts and Jobs Act 2017 February 8, 2018 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any specific taxpayer

Individual Taxes. TAX CUTS & JOBS ACT OF Tax Brackets: 7 Tax Brackets: 7 Tax Brackets: 4 Tax Brackets:

COMPARISON OF CURRENT TAX LAW VS. TAX CUTS AND JOBS ACT Individual Taxes Ordinary Income Tax Brackets (Single Tax Brackets Shown) 10%: $0 - $9,325 15%: $9,326 - $37,950 25%: $37,951 - $91,900 28%: $91,901

COMPARISON OF CURRENT TAX LAW VS. TAX CUTS AND JOBS ACT Individual Taxes Ordinary Income Tax Brackets (Single Tax Brackets Shown) 10%: $0 - $9,325 15%: $9,326 - $37,950 25%: $37,951 - $91,900 28%: $91,901

The Tax Cuts and Jobs Act1 (TCJA) made

made") Significant Provisions of the Tax Cuts and Jobs Act Affecting Closely Held Businesses and Their Owners by Gerald A. Shanker The Tax Cuts and Jobs Act1 (TCJA) made significant changes to the Internal Revenue

Significant Provisions of the Tax Cuts and Jobs Act Affecting Closely Held Businesses and Their Owners by Gerald A. Shanker The Tax Cuts and Jobs Act1 (TCJA) made significant changes to the Internal Revenue

IMPACT OF THE NEW TAX LAW ON NONPROFIT HOSPITALS AND HEALTH SYSTEMS OVERVIEW

Catherine E. Livingston Gerald Griffith Amy Bibby, CPA clivingston@jonesday.com ggriffith@jonesday.com amy.bibby@dhgllp.com 202-879-3756 312-269-1507 828-236-5797 313.230.7907 IMPACT OF THE NEW TAX LAW

Catherine E. Livingston Gerald Griffith Amy Bibby, CPA clivingston@jonesday.com ggriffith@jonesday.com amy.bibby@dhgllp.com 202-879-3756 312-269-1507 828-236-5797 313.230.7907 IMPACT OF THE NEW TAX LAW

Tax Developments Affecting Exempt Organizations Where We Are Today With Tax Reform. Presented by: Gene J. Logan & Robin S. Murphy

Tax Developments Affecting Exempt Organizations Where We Are Today With Tax Reform Presented by: Gene J. Logan & Robin S. Murphy Agenda Where we are today in the process Thoughts and Observations on the

Tax Developments Affecting Exempt Organizations Where We Are Today With Tax Reform Presented by: Gene J. Logan & Robin S. Murphy Agenda Where we are today in the process Thoughts and Observations on the

TAX REFORM CORPORATE & BUSINESS

The following chart sets forth some of the provisions affecting businesses in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

The following chart sets forth some of the provisions affecting businesses in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

Tax Cuts and Jobs Act Construction Industry Impact

Tax Cuts and Jobs Act Construction Industry Impact Presented By: Sean M. Auger, Partner 1 Introduction Most but not all provisions effective for tax periods beginning after December 31, 2017 2 General

Tax Cuts and Jobs Act Construction Industry Impact Presented By: Sean M. Auger, Partner 1 Introduction Most but not all provisions effective for tax periods beginning after December 31, 2017 2 General

5/29/ TAX CUTS AND JOBS ACT OVERVIEW. Individual Tax. Introduction-Individual Provisions. Dauphin County Bar Association May 30, 2018

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA)

") Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

THE TAX CUTS AND JOBS ACT

THE TAX CUTS AND JOBS ACT INDIVIDUALS The Tax Cuts and Jobs Act contains numerous provisions that will have a significant impact on the tax liability reported by individuals and families. Some of the more

THE TAX CUTS AND JOBS ACT INDIVIDUALS The Tax Cuts and Jobs Act contains numerous provisions that will have a significant impact on the tax liability reported by individuals and families. Some of the more

TAX REFORM CORPORATE & BUSINESS

The following chart sets forth some of the provisions affecting businesses in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

The following chart sets forth some of the provisions affecting businesses in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

May 8, 2018 Watkins Glen, New York

May 8, 2018 Watkins Glen, New York This presentation is intended for general educational and/or informational purposes only and does not replace specific, independent professional advice. This presentation

May 8, 2018 Watkins Glen, New York This presentation is intended for general educational and/or informational purposes only and does not replace specific, independent professional advice. This presentation

Don t Let 2018 Be Taxing:

Don t Let 2018 Be Taxing: How Changes to the Tax Laws Change How We Counsel Businesses March 15, 2018 Agenda Introduction C corporation overview Pass-through overview Comparison 2 Introduction Types of

Don t Let 2018 Be Taxing: How Changes to the Tax Laws Change How We Counsel Businesses March 15, 2018 Agenda Introduction C corporation overview Pass-through overview Comparison 2 Introduction Types of

Senate Version - "The Tax Cuts and Jobs Act"

Senate Version - "The Tax Cuts and Jobs Act" Joint Committee on Taxation, Description of the Chairman's Mark of the Tax Cuts and Jobs Act (JCX-51-17), Nov. 9, 2017. Late in the evening on November 9, Senate

Senate Version - "The Tax Cuts and Jobs Act" Joint Committee on Taxation, Description of the Chairman's Mark of the Tax Cuts and Jobs Act (JCX-51-17), Nov. 9, 2017. Late in the evening on November 9, Senate

12/19/2018 THOUGHTWARE. Financial Services THOUGHTWARE. Tax Reform Update. Income Tax Update for Financial Institutions

THOUGHTWARE Financial Services THOUGHTWARE Financial Services Tax Reform Update Income Tax Update for Financial Institutions December 20, 2018 1 To Receive CPE Credit Individuals Participate in entire

THOUGHTWARE Financial Services THOUGHTWARE Financial Services Tax Reform Update Income Tax Update for Financial Institutions December 20, 2018 1 To Receive CPE Credit Individuals Participate in entire

20% maximum corporate tax rate. 25% maximum rate for personal service corporations.

H.R. 1, THE TAX CUTS AND JOBS ACT, PASSED BY HOUSE OF REPRESENTATIVES ON NOVEMBER 16, 2017 ( HOUSE BILL ) THE TAX CUTS AND JOBS ACT, AS PASSED BY THE SENATE ON DECEMBER 2, 2017 ( ) Except as noted, legislation

H.R. 1, THE TAX CUTS AND JOBS ACT, PASSED BY HOUSE OF REPRESENTATIVES ON NOVEMBER 16, 2017 ( HOUSE BILL ) THE TAX CUTS AND JOBS ACT, AS PASSED BY THE SENATE ON DECEMBER 2, 2017 ( ) Except as noted, legislation

Business Changes in the Tax Cuts and Jobs Act. Alan D. Sobel, CPA December 27,

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

LAST UPDATED JANUARY 5, 2018 WITH FINAL CONFERENCE AGREEMENT

PROVISIONS OF H.R. 1, THE TAX CUTS AND JOBS ACT AND PROVISIONS OF THE SENATE TAX CUTS AND JOBS ACT IMPACTING HIGHER EDUCATION (NOTE: ALL PROVISIONS WOULD BECOME EFFECTIVE JANUARY 1, 2018 UNLESS OTHERWISE

PROVISIONS OF H.R. 1, THE TAX CUTS AND JOBS ACT AND PROVISIONS OF THE SENATE TAX CUTS AND JOBS ACT IMPACTING HIGHER EDUCATION (NOTE: ALL PROVISIONS WOULD BECOME EFFECTIVE JANUARY 1, 2018 UNLESS OTHERWISE

Taxpayers may recharacterize contributions to one type of IRA (traditional or Roth) as a contribution to the other type of IRA.

as a contribution to the other type of IRA.") BENEFITS Affordable Care Act Individual Mandate Under the Affordable Care Act, individuals must have minimum essential The individual responsibility payment is reduced to $0 effective for months beginning

BENEFITS Affordable Care Act Individual Mandate Under the Affordable Care Act, individuals must have minimum essential The individual responsibility payment is reduced to $0 effective for months beginning

N/A. Kiddie Tax Various bracket thresholds Ordinary and capital gains rates applicable to trusts and estates

We have prepared a summary of the House and the Senate versions of the proposed tax reform bill. Once they reach an agreement on a final bill, we will update the summary as needed. House Bill (H. R. 1)

We have prepared a summary of the House and the Senate versions of the proposed tax reform bill. Once they reach an agreement on a final bill, we will update the summary as needed. House Bill (H. R. 1)

TAX REFORM. Overview. Congressional Republican Timeline. Senate Finance Links. The U.S. House of Representatives. Joint Committee on Taxation

TAX REFORM Overview On November 2, House Republicans released their tax reform bill titled, Tax Cuts and Jobs Act. Michael Best Strategies (MBS) tax policy experts, Denise Bode and Anne Canfield continue

TAX REFORM Overview On November 2, House Republicans released their tax reform bill titled, Tax Cuts and Jobs Act. Michael Best Strategies (MBS) tax policy experts, Denise Bode and Anne Canfield continue

KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017

OF 2017") KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017 New tax laws resulting from the TCJA represent the most significant changes in our tax structure in more than 30 years. Most provisions for individuals

KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017 New tax laws resulting from the TCJA represent the most significant changes in our tax structure in more than 30 years. Most provisions for individuals

How Did Nonprofits Fare In Tax Reform?

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com How Did Nonprofits Fare In Tax Reform? By

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com How Did Nonprofits Fare In Tax Reform? By

Highlights of the Senate Tax Cuts and Jobs Act

WEALTH SOLUTIONS GROUP Highlights of the Senate Tax Cuts and Jobs Act The Senate passed a bill with the same name as the House, but with plenty of other differences The Senate version of a tax reform proposal

WEALTH SOLUTIONS GROUP Highlights of the Senate Tax Cuts and Jobs Act The Senate passed a bill with the same name as the House, but with plenty of other differences The Senate version of a tax reform proposal

Businesses. Provision Corporate income Eight brackets with a 35% top rate. 21% flat rate

Businesses 21% flat rate Corporate income Eight brackets with a 35% top rate Personal service corporations taxed No special rate for personal service at a 35% flat rate corporations Passthrough income

Businesses 21% flat rate Corporate income Eight brackets with a 35% top rate Personal service corporations taxed No special rate for personal service at a 35% flat rate corporations Passthrough income

SENATE TABLE OF CONTENTS

Tax Cuts and Jobs Act -- s in Nov. 9 Chair s Mark (Black) and Nov. 14 Senate Chair s Modifications (Green) compared to the JCT Description of the House Proposals Nov. 15 (Blue) Chair s Amendments (Purple).

Tax Cuts and Jobs Act -- s in Nov. 9 Chair s Mark (Black) and Nov. 14 Senate Chair s Modifications (Green) compared to the JCT Description of the House Proposals Nov. 15 (Blue) Chair s Amendments (Purple).

Tax Cuts & Jobs Act (TCJA)

") Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

Business Provisions Under the Tax Cuts and Jobs Act Compared to Previous Tax Law

Tax Rates Corporate tax rate Top rate of 35 percent Flat rate of 21 percent (effective 1/1/2018) Alternative minimum tax (AMT) 20 percent Repealed; AMT credits refundable from 2018 through 2021 (1) Personal

Tax Rates Corporate tax rate Top rate of 35 percent Flat rate of 21 percent (effective 1/1/2018) Alternative minimum tax (AMT) 20 percent Repealed; AMT credits refundable from 2018 through 2021 (1) Personal

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

Individual Provisions page 2. New Deduction for Pass-through Income page 5. Corporate (and Other Business) Provisions page 6

Provisions page 6") Table of Contents Individual Provisions page 2 New Deduction for Pass-through Income page 5 Corporate (and Other Business) Provisions page 6 Partnership (and Other Pass-through Business) Provisions page

Table of Contents Individual Provisions page 2 New Deduction for Pass-through Income page 5 Corporate (and Other Business) Provisions page 6 Partnership (and Other Pass-through Business) Provisions page

Impact of Tax Reform on Farmers. Tax and Accounting Department Fall 2018

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

TAX UPDATE TAX CUTS & JOBS ACT (2018) Add l Elderly & Blind Joint & Surviving Spouse: $1,300

Add l Elderly & Blind Joint & Surviving Spouse: $1,300") TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

Tax Reform Overview. Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP

Tax Reform Overview Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Notable Individual Changes Individual Rates Standard Deduction Personal Exemptions Child/Family Credit Senate Overall

Tax Reform Overview Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Notable Individual Changes Individual Rates Standard Deduction Personal Exemptions Child/Family Credit Senate Overall

EXEMPT ORGANIZATIONS & THE NEW TAX BILL Changes and implications you should understand

CLICK TO EDIT MASTER TEXT STYLES EXEMPT ORGANIZATIONS & THE NEW TAX BILL Changes and implications you should understand BARB MCGUAN Principal April 23, 2018 CLICK TO EDIT MASTER TEXT AGENDA STYLES FEDERAL

CLICK TO EDIT MASTER TEXT STYLES EXEMPT ORGANIZATIONS & THE NEW TAX BILL Changes and implications you should understand BARB MCGUAN Principal April 23, 2018 CLICK TO EDIT MASTER TEXT AGENDA STYLES FEDERAL

To help organizations navigate the key provisions affecting businesses, we have summarized top provisions below.

HOW TAX REFORM IMPACTS BUSINESSES Summary On December 22, 2017, the President signed the Tax Cuts and Jobs Act (the "Act"). Signing the Act marked the largest change to U.S. tax policy in decades. Most

HOW TAX REFORM IMPACTS BUSINESSES Summary On December 22, 2017, the President signed the Tax Cuts and Jobs Act (the "Act"). Signing the Act marked the largest change to U.S. tax policy in decades. Most

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER #1 Corporate Tax Rates New Corporate Flat Tax Rate of 21% replaces old graduated brackets

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER #1 Corporate Tax Rates New Corporate Flat Tax Rate of 21% replaces old graduated brackets

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE. Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP MOST SWEEPING TAX REFORM SINCE 1986 Tax Cuts and Jobs Act signed December 22, 2017 Generally

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP MOST SWEEPING TAX REFORM SINCE 1986 Tax Cuts and Jobs Act signed December 22, 2017 Generally

Roadmap to Key Provisions of the Tax Cuts and Jobs Act (H.R. 1)

") After months of speculation over what would be included in Trump-era tax reform, legislative language is finally here, with the release of the. The 429-page document would reshuffle the existing scheme

After months of speculation over what would be included in Trump-era tax reform, legislative language is finally here, with the release of the. The 429-page document would reshuffle the existing scheme

TAX CUTS AND JOBS ACT OF 2017

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

The impact of Tax Reform on the Not-For- Profit and Higher Education sectors

The impact of Tax Reform on the Not-For- Profit and Higher Education sectors Please disable pop-up blocking software before viewing this webcast January 4, 2018 CPE Reminders To receive CPE, you must be

The impact of Tax Reform on the Not-For- Profit and Higher Education sectors Please disable pop-up blocking software before viewing this webcast January 4, 2018 CPE Reminders To receive CPE, you must be

The Tax Cuts and Jobs Act

Advanced Planning The Tax Cuts and Jobs Act Congress has passed the Tax Cuts and Jobs Act, the most sweeping tax reform since 1986. In today s world, pursuing your life s goals is being challenged in new

Advanced Planning The Tax Cuts and Jobs Act Congress has passed the Tax Cuts and Jobs Act, the most sweeping tax reform since 1986. In today s world, pursuing your life s goals is being challenged in new