Agricultural and Natural Resource Issues Chapter 9 pp National Income Tax Workbook

|

|

|

- Marylou Waters

- 5 years ago

- Views:

Transcription

1 Agricultural and Natural Resource Issues Chapter 9 pp National Income Tax Workbook

2 Agricultural and Natural Resources Issues Chris Bruynis, David Marrison, and Barry Ward

3 Ag Economy Update NIB 1. Farm Bill Payments Lower in 2018 (or zero). 2. Trade War with China - (Soybeans). 3. Market Facilitation Program. 4. Farm Economy is Still VERY Tight. 5. New Farm Bill Discussions on Horizon.

4 Current Farm Bill Payments Agriculture Risk Coverage (ARC) and Price Loss Coverage (PLC) programs were authorized by the 2014 Farm Bill. Payment levels down for payments being received for 2017 now.

5

6

7

8 Market Facilitation Program (MFP) Soybeans $1.65 per bushel. Corn 1 cent per bushel. Dairy 12 cents per hundred weight. Pork $8 per head. Wheat 14 cents per bushel.

9 It does not matter how slowly you go as long as you do not stop. Confucious

10

11 MAJOR STRESS FOR FARMERS!

12 TJCA What is the definition of the creators of tax reform?

13 Someone who solves a problem you didn t know you had in a way you don t understand.

14 Chapter 9: Agricultural and Natural Resources Issues Issue 1: Issue 2: Issue 3: Issue 4: Issue 5: Farm Loss Deduction Limits Depreciation of Farm Assets Farm and Ranch Tax Elections Farm Lease Income and the QBI Deduction Section 199A and Agricultural and Horticultural Cooperatives

15 Issue 1: Farm Loss Deduction Limits Pages

16 Farm Loss Limit prior to TCJA pp Rule applied only if receiving applicable subsidy. Threshold was the greater of: $150,000 ($300,000 MFJ) or The excess of aggregate net farm income of 5 preceding years. (See Example 9.1). If farmer had non-business income exceeding the threshold then the excess loss was carried over as Schedule F deduction loss over non-business income was a NOL.

17 New Rules under TCJA pp Loss limit applies to all noncorporate businesses Applies to S corp shareholders too! No subsidy received requirement. Revised threshold amount $250,000 ($500,000 MFJ) No 5 year net income lookback option Anything over this threshold is a NOL.

18 Ex. 9.2 David Stump p. 290 Single taxpayer Sch. C loss $248,000, Sch. F loss $22,000 Aggregate business loss $270,000 Loss deduction limited to $250,000 Excess loss ($20,000) is part of NOL (Ex. 9.3) Self Employment Tax unaffected by NOL

19 Ex. 9.4 Flow-through Loss Limitation p. 290 Applies at owner level. Owner combines flow-through items with other individual items (Ex. 9.4). David Stump Sole proprietor Sch C loss (248,000) Sole proprietor Sch F loss (22,000) Saw-You-Coming K-1 gain 9,000 Overall Loss (261,000) Loss Limitation 250,000 Carryover as part of NOL 11,000

20 At-Risk and PAL Limits pp Rules unchanged by TCJA. Applied to each of the taxpayer s losses before applying the TCJA overall loss limitation. First, At-risk Then, Passive Activity Loss Disallowed losses carryover.

21 Farm Net Operating Losses under TCJA 5-year carryback for farm losses eliminated. 2-year carryback for nonfarm losses eliminated. Farms still have this option. Carryover loss deduction limited to 80%. Unlimited carryover. Farmers may elect out of 2-year carry back. pp

22 Ex. 9.6 Surprise for Denise p. 292 $382,000 farm loss limited by TCJA Pay tax on the $166k $132,000 NOL carryover (or back?) ($382K - $250K)

23 What do accountants suffer from that ordinary people don t? Pages

24 Issue 2: Depreciation Pages

25 Issue 2: Depreciation of Farm Assets pp year MACRS for new farm equipment and machinery. Used farm equipment remains as 7-year. Farm use is defined by IRC 263A. Incidental processing okay Not custom operator Not reseller ADS life continues at 10 years for all equipment (new/used). Grain bins and fences continue as 7-year MACRS.

26 TCJA Depreciation Changes p % DB for farm assets in the 3, 5, 7 and 10-Year MACRS classes. Trees and vines are 10 year property previously SL, now 150 DB. 15 and 20 year property continue at 150% DB.

2018- $86,000 depreciation ($430,000/5 x.")

27 Ex. 9.9 Difference a Year Makes p. 294 $430,000 new combine purchase w/out bonus or sec $46,071 depreciation ($430,000/7 x.5 x 150%) $86,000 depreciation ($430,000/5 x.5 x 200%) $39,929 more

28 Planning Pointer Excess p. 294 This increase in the rate of depreciation for many farm assets, combined with the shorter MACRS recovery class for new farm equipment and machinery, may generate more depreciation than is needed by some taxpayers.

29 Interest Expense Limitation and Required Use of ADS Taxpayers with 3-year average gross receipts over $25 million are subject to interest deduction limits: Limited to 30% of adjusted taxable income Can elect out, but must then use ADS on property in 10- year or greater MACRS life. Details in New Legislation Business Chapter. p. 294

30 Vehicle Depreciation pp IRC 280F limits apply to passenger vehicles Definitions unchanged by TCJA Limits increased - $10,000 in Year 1

31 No Like Kind Exchange for Personal Property pp only applies to real property under the TCJA. Equipment trade-ins are now taxable events. Most likely result will be taxable gain. Offset is increased basis for depreciation.

32 Ex Farm Tractor Trade-in pp List price of new tractor - $397,000 Trade-in allowance - $112,000 Cash price - $285,000 ATB of trade $61,262 (250, ,738) Reportable ordinary gain $50,738 (112,000-61,262) See Fig. 9.8

33 Ex Tax Planning p. 300 Recognized gain could likely be offset by depreciation. Amos can Sec. 179 because he s under the $2.5 million investment limit. Bonus is class by class (too much?). Depreciation reduces SE tax. Equipment gain is not SE income.

34 Single Purpose Livestock and Horticultural Facilty Any general use is excluded. 10-year property rather than: 20-year general purpose farm building 27.5-year residential rental property 39-year nonfarm building Work space is restricted. p. 300

35 Qualifying Structure? p. 301 Ex equipment incidental to livestock OK Ex same building but equipment is used for crops NOT OK Don must use 20-year MACRS

36 Additional Single Purpose Benefits p. 301 Included in Sec definition and therefore eligible for Sec year life eligible for bonus

37 Ex Sec. 179 and Bonus p. 301 Dan Dairyman spent a total of $2.8 million on depreciable assets. State does not accept SDA. Dan exceeds Sec. 179 investment limit by $300,000 (2,800,000-2,500,000). Max. 179 is $700,000. (1,000, ,000) Balance could be bonus depreciation.

38 Fig. 9.9 Sec. 179 or Bonus p. 302 Numerous limits on Sec Bonus is class by class. Bonus unavailable to some taxpayers based on other tax elections. Bonus automatically applies (v. 179 election).

39 Issue 3: Farm/Ranch Tax Elections Pages

40 Issue 3: Farm/Ranch Tax Elections p. 305 General Rules for Making Election: Some made by default Some have to elect on return Some are separate election See Figure 9.10 for guidance (pp )

41 Issue 4: Farm Lease Income & QBI Pages

42 Farm Leases & the QBI Deduction Qualified Business Income (QBI) is the net amount of qualified items of income, gain, deduction, and loss with respect to any qualified trade or business of the taxpayer. Trade or Business- taxpayer must be involved in the activity with continuity and regularity and the taxpayer s primary purpose for engaging in the activity must be for income or profit. See: I.R.C & Commissioner v. Groetzinger

43 So What Does this Mean for Farm Lease Income?

44 Farm Leases & QBI Deduction pp A farm rental activity is a trade or business that qualifies for the QBI deduction if it is conducted regularly and with a profit motive, regardless of the type of the lease and the type of services that the landlord provides. Special rules apply to self-rentals. Although farm rental income may be eligible for the QBI deduction, it may not be subject to selfemployment (SE) tax, and it may be a passive activity. See: I.R.C & Commissioner v. Groetzinger

45 Let s Look Closer

46 Cash Lease p. 317 Cash lease tenant pays cash for acreage. Usually no material participation and not subject to SE tax. (see requirements for participation). Is this eligible for QBI Deduction?

47 Material Participation p. 317 Cash lease subject to SE tax if landlord materially participates. Material participation if: Advises/consults with tenant & inspects Landlord furnishes most tools/equipment Landlord advances $ or has financial responsibility

48 Material Participation Tests p Pay half costs, furnish half tools, advise or consult, inspect. 2. Regular/frequent management decisions. 3. Landlord works 100 hours or more over period that is 5 weeks or more. 4. Activities that show material and significant involvement.

49 What Do You Think? Landowner who completely turns over management of the land to an agent, such as a professional farm management company, and does not otherwise materially participate in the farming operation, does not have SE income from renting land for agricultural use but can still claim the QBI deduction if the purpose of the rental is income or profit. A triple net lease arrangement, where the tenant pays the taxes, insurance, and maintenance, may not give rise to material participation, and it may not qualify for the QBI deduction.

50 Self-Rental QBI Deduction p. 318 For QBI deduction, rental of farm land to a related trade or business is treated as a trade or business if the rental and the other trade or business are commonly controlled. Rental to partnership or S corporation in which Taxpayer materially participates is subject to SE tax. Martin v. Commissioner no obligation to participate, no SE tax.

51 Crop Share p. 319 Rent in exchange for share of crop. Conduct activities regularly and for income/profit, eligible for QBI deduction.

. 8 th Circuit not SE income.")

52 Conservation Reserve Program Payments CRP payments quality for QBI if is a regular activity and for profit. Subject to SE tax if actively engaged (unless receiving social security). 8 th Circuit not SE income. So Outside 8 th Yes QBI, Inside 8 th No QBI? pp

53 New IRC Section 199A Deduction for Qualified Business Income (QBI) Landlords: Crop share landlords filing a Schedule F are eligible. Cash rent landlords filing a Schedule E likely won t be eligible pending final regs (although there is some disagreement). Crop share landlords filing Form 4835 may qualify (if they are materially participating they likely will). Landlords will likely have to pass as a trade or business according to IRC Section 162

54 New IRC Section 199A Deduction for Qualified Business Income (QBI) Farms with Multiple Entities: Proposed regulations indicate that common ownership of business entities allows the farmer to combine the rent income with the farm income an advantage Section 1231 Capital Gain Income: Will not qualify as QBI if the gain is treated as a capital gain likely not good for dairy producers

55 Issue 5: 199A and Ag. & Horticultural Cooperatives Pages

56 Issue 5: 199A and Ag. & Horticultural Cooperatives TCJA repealed 199 (Domestic Production Activities Deduction). TCJA provides Specified Ag. or Hort. Cooperatives with a deduction that was 20% of gross. Sales to non-cooperatives were 20% of net. Known as the Grain Glitch. Consolidated Appropriations Act (CCA) modifies deduction under 199A(g) to rather provide a deduction similar to DPAD. p. 319

57 More Paper Work Sales to Cooperative vs General Business

58 Calculate the Deduction p. 323 QBI deduction for patron is 20% reduced by lesser of: 9% of QBI from Trade or Business allocable to qualified coop payments, or 50% of allocated W-2 wages.

59 Ex QBI Deduction Coop Patron p. 324 No Wages Paid Pat sold grain through coop $230K PURPIM, $20K dividend $200K expenses no wages $50K QBI Deduction is $10K (20%) reduced by lesser of $4,500 or $0

60 Ex QBI Deduction Coop Patron p. 324 with Wages Paid Pat paid $25,000 W-2 wages. Tentative QBI is $10,000. Reduced by lessor: $4,500 (9% of $50,000) $12,500 (50% of $25,000) QBI deduction is $5,500 ($10K reduced by lesser of $4,500 or $12,500).

61 Ex QBI Deduction Coop Patron p. 324 with additional Pass-Through Deduction Pat also got $2,500 deduction from Cooperative. QBI deduction is $12,500 ($10,000 + $2,500)

62 You have been given the task of transporting 3,000 apples 1,000 miles from Appleland to Bananaville. Your truck can carry 1,000 apples at a time. Every time you travel a mile towards Bananaville you must pay a tax of 1 apple but you pay nothing when going in the other direction (towards Appleland). What is highest number of apples you can get to Bananaville?

63 David L. Marrison, Extension Educator Thank You

64 Step one: First you want to make 3 trips of 1,000 apples 333 miles. You will be left with 2,001 apples and 667 miles to go. Step two: Next you want to take 2 trips of 1,000 apples 500 miles. You will be left with 1,000 apples and 167 miles to go (you have to leave an apple behind). Step three: Finally, you travel the last 167 miles with one load of 1,000 apples and are left with 833 apples in Bananaville.

Agricultural and Natural Resource Issues Chapter 9 pp National Income Tax Workbook

Agricultural and Natural Resource Issues Chapter 9 pp. 287-327 2018 National Income Tax Workbook Agricultural and Natural Resources Issues Barry Ward, Davis Marrison, and Chris Bruynis Ag Economy Update

Agricultural and Natural Resource Issues Chapter 9 pp. 287-327 2018 National Income Tax Workbook Agricultural and Natural Resources Issues Barry Ward, Davis Marrison, and Chris Bruynis Ag Economy Update

Farm Tax Update 1/21/2019. Teaching Objectives. Circular 230 Disclosure. Thank You Farmers Tax Guide

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Farmer and Farmland Owner Income Tax Webinar. Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension

Farmer and Farmland Owner Income Tax Webinar Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension Chris Bruynis Circular 230 Disclosure The information provided in this presentation is for educational

Farmer and Farmland Owner Income Tax Webinar Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension Chris Bruynis Circular 230 Disclosure The information provided in this presentation is for educational

Agricultural & Natural Resource Issues Chapter 10 pp National Income Tax Workbook

Agricultural & Natural Resources Tax Issues Chris Bruynis David Marrison Barry Ward Associate Professor Associate Professor Assistant Professor bruynis.1@osu.edu marrison.2@osu.edu ward.8@osu.edu 740-702-3200

Agricultural & Natural Resources Tax Issues Chris Bruynis David Marrison Barry Ward Associate Professor Associate Professor Assistant Professor bruynis.1@osu.edu marrison.2@osu.edu ward.8@osu.edu 740-702-3200

AGRICULTURAL TAX. i n c o m e t a x e s

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

The Tax Cuts & Jobs Act

The Tax Cuts & Jobs Act Ten Key Changes that May Impact You August 2, 2018 Contact Information Kristine Tidgren, ktidgren@iastate.edu www.calt.iastate.edu @CALT_IowaState 2 1. MANY CHANGES ARE HERE TODAY,

The Tax Cuts & Jobs Act Ten Key Changes that May Impact You August 2, 2018 Contact Information Kristine Tidgren, ktidgren@iastate.edu www.calt.iastate.edu @CALT_IowaState 2 1. MANY CHANGES ARE HERE TODAY,

Corporate Taxes. Standard Deduction: Estate & Trust Tax Rates

WEALTH ADVISORY OUTSOURCING AUDIT, TAX, AND CONSULTING Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor How Tax Reform Affects

WEALTH ADVISORY OUTSOURCING AUDIT, TAX, AND CONSULTING Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor How Tax Reform Affects

HIGHLIGHTS OF THE TAX CUTS AND JOBS ACT FOR AGRICULTURAL PRODUCERS

HIGHLIGHTS OF THE TAX CUTS AND JOBS ACT FOR AGRICULTURAL PRODUCERS by Kristine Tidgren I. INTRODUCTION The Tax Cuts and Jobs Act (TCJA) ushered in the most significant changes to our tax code in more than

HIGHLIGHTS OF THE TAX CUTS AND JOBS ACT FOR AGRICULTURAL PRODUCERS by Kristine Tidgren I. INTRODUCTION The Tax Cuts and Jobs Act (TCJA) ushered in the most significant changes to our tax code in more than

Farm/Ranch Accounting and Tax 101

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Farm/Ranch Accounting and Tax 101 Randy Netek, CPA & Brandt Self, CPA May 2018 CLAconnect.com The Agenda Tax Reform Basics of Accounting Documentation

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Farm/Ranch Accounting and Tax 101 Randy Netek, CPA & Brandt Self, CPA May 2018 CLAconnect.com The Agenda Tax Reform Basics of Accounting Documentation

THE TAX CUTS AND JOBS ACT & AGRICULTURAL PRODUCERS. KRISTINE TIDGREN, Ames, Iowa Center for Agricultural Law & Taxation, Iowa State University

THE TAX CUTS AND JOBS ACT & AGRICULTURAL PRODUCERS KRISTINE TIDGREN, Ames, Iowa Center for Agricultural Law & Taxation, Iowa State University October 2018 0 1 TABLE OF CONTENTS I. INTRODUCTION...3 II.

THE TAX CUTS AND JOBS ACT & AGRICULTURAL PRODUCERS KRISTINE TIDGREN, Ames, Iowa Center for Agricultural Law & Taxation, Iowa State University October 2018 0 1 TABLE OF CONTENTS I. INTRODUCTION...3 II.

Top Producer Seminar A New Tax Bill: What You Need To Know Now. Paul Neiffer, CPA January 25, 2018 Chicago, Illinois

Top Producer Seminar A New Tax Bill: What You Need To Know Now Paul Neiffer, CPA January 25, 2018 Chicago, Illinois Speaker Introduction Paul Neiffer, Principal, CliftonLarsonAllen Frequent national speaker

Top Producer Seminar A New Tax Bill: What You Need To Know Now Paul Neiffer, CPA January 25, 2018 Chicago, Illinois Speaker Introduction Paul Neiffer, Principal, CliftonLarsonAllen Frequent national speaker

Farm Taxes. David L. Marrison, Associate Professor

Farm Taxes David L. Marrison, Associate Professor Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax

Farm Taxes David L. Marrison, Associate Professor Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

HOW THE TCJA APPLIES TO YOUR FARMING (AND OTHER) BUSINESS LATTAHARRIS, LLP CLIENT SEMINARS JUNE 12-15, 2018

BUSINESS LATTAHARRIS, LLP CLIENT SEMINARS JUNE 12-15, 2018") HOW THE TCJA APPLIES TO YOUR FARMING (AND OTHER) BUSINESS LATTAHARRIS, LLP CLIENT SEMINARS JUNE 12-15, 2018 Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation Washburn University

HOW THE TCJA APPLIES TO YOUR FARMING (AND OTHER) BUSINESS LATTAHARRIS, LLP CLIENT SEMINARS JUNE 12-15, 2018 Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation Washburn University

Impact of Tax Reform on Farmers. Tax and Accounting Department Fall 2018

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018 The TCJA s Impact on Farmers and Ranchers Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018 The TCJA s Impact on Farmers and Ranchers Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation

2017 Farm Income Tax Webinar

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

Center for Agricultural Law & Taxation. Tax Cuts & Jobs Act. Key Provisions Impacting Agricultural Producers and Small Businesses June 12, 2018

Tax Cuts & Jobs Act Key Provisions Impacting Agricultural Producers and Small Businesses June 12, 2018 Contact Information Kristine Tidgren, ktidgren@iastate.edu www.calt.iastate.edu @CALT_IowaState 2

Tax Cuts & Jobs Act Key Provisions Impacting Agricultural Producers and Small Businesses June 12, 2018 Contact Information Kristine Tidgren, ktidgren@iastate.edu www.calt.iastate.edu @CALT_IowaState 2

Tax Cuts and Jobs Act - Cost Recovery Provisions, Expensing, and Like-kind Exchanges last updated

Tax Cuts and Jobs Act - Cost Recovery Provisions, Expensing, and Like-kind Exchanges last updated 12.27.2017 The Tax Cuts and Jobs Act was signed into law by the President on Friday, December 22, 2017.

Tax Cuts and Jobs Act - Cost Recovery Provisions, Expensing, and Like-kind Exchanges last updated 12.27.2017 The Tax Cuts and Jobs Act was signed into law by the President on Friday, December 22, 2017.

Form 4797 Chapter 3 pp Agricultural Tax Issues

Form 4797 Chapter 3 pp. 85-118 2018 Agricultural Tax Issues Form 4797 Page 85 Reporting of gains and losses on the disposition of business property. The collection point for gains and losses reported elsewhere.

Form 4797 Chapter 3 pp. 85-118 2018 Agricultural Tax Issues Form 4797 Page 85 Reporting of gains and losses on the disposition of business property. The collection point for gains and losses reported elsewhere.

Tax Cuts and Jobs Act of 2017 (TCJA) Key General Business Tax Provisions

Key General Business Tax Provisions") Item IRC Expensing and Depreciating Section 179 Limits 179(b) For property service in For property service in The maximum Section 179 deduction and phaseout threshold are increased to $1 million and $2.5

Item IRC Expensing and Depreciating Section 179 Limits 179(b) For property service in For property service in The maximum Section 179 deduction and phaseout threshold are increased to $1 million and $2.5

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER #1 Corporate Tax Rates New Corporate Flat Tax Rate of 21% replaces old graduated brackets

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER #1 Corporate Tax Rates New Corporate Flat Tax Rate of 21% replaces old graduated brackets

2017 TAX CUTS AND JOBS ACT

2017 TAX CUTS AND JOBS ACT A Taxation Focus Austin Duerfeldt Agricultural Economist Email: aduerfeldt2@unl.edu Phone: (402) 873-3166 Facebook: SE NE Ag Economist Twitter: SENE_AgEcon Things to note before

2017 TAX CUTS AND JOBS ACT A Taxation Focus Austin Duerfeldt Agricultural Economist Email: aduerfeldt2@unl.edu Phone: (402) 873-3166 Facebook: SE NE Ag Economist Twitter: SENE_AgEcon Things to note before

Before you sell Understanding the tax impact of sales to cooperatives

The Advanced Consulting Group White paper Before you sell Understanding the tax impact of sales to cooperatives Ryan Patton, MBA Consultant, Advanced Consulting Group Key highlights Qualified buisiness

The Advanced Consulting Group White paper Before you sell Understanding the tax impact of sales to cooperatives Ryan Patton, MBA Consultant, Advanced Consulting Group Key highlights Qualified buisiness

Chapter 3 TCJA: Depreciation, Bonus Dep., 179, NOLs, and 461(L) Depreciation

Depreciation") Chapter 3 TCJA: Depreciation, Bonus Dep., 179, NOLs, and 461(L) Depreciation ADS Recovery Period for Residential Property is Shortened (Section 168(g)(2)(C)) ADS recovery period for residential rental

Chapter 3 TCJA: Depreciation, Bonus Dep., 179, NOLs, and 461(L) Depreciation ADS Recovery Period for Residential Property is Shortened (Section 168(g)(2)(C)) ADS recovery period for residential rental

Income Tax Management for Farmers in 2011

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

2/8/2019. Agenda for Today. Technical Corrections 2019 TAX FILING SEASON UPDATE KEY ISSUES AND DEVELOPMENTS FEBRUARY 8, 2019

2019 TAX FILING SEASON UPDATE KEY ISSUES AND DEVELOPMENTS FEBRUARY 8, 2019 Roger A. McEowen roger.mceowen@washburn.edu www.washburnlaw.edu/waltr @WashburnWaltr Agenda for Today Technical Corrections and

2019 TAX FILING SEASON UPDATE KEY ISSUES AND DEVELOPMENTS FEBRUARY 8, 2019 Roger A. McEowen roger.mceowen@washburn.edu www.washburnlaw.edu/waltr @WashburnWaltr Agenda for Today Technical Corrections and

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

In-depth Look at 199A & the Case for Non-Qualified Patronage After Tax Reform

In-depth Look at 199A & the Case for Non-Qualified Patronage After Tax Reform Presented by: Eric Krienert, Tax Director Moss Adams eric.krienert@mossadams.com 209-955-6118 What We Will Cover Today The

In-depth Look at 199A & the Case for Non-Qualified Patronage After Tax Reform Presented by: Eric Krienert, Tax Director Moss Adams eric.krienert@mossadams.com 209-955-6118 What We Will Cover Today The

2018 Federal Income Tax Update Business

2018 Federal Income Tax Update Business FTU- Business IRC 199A ISSUES 2 Business Tax Changes Under the Tax Cuts and Jobs Act The Tax Cuts and Jobs Act of 2017 (the Act ) contains significant legislation

2018 Federal Income Tax Update Business FTU- Business IRC 199A ISSUES 2 Business Tax Changes Under the Tax Cuts and Jobs Act The Tax Cuts and Jobs Act of 2017 (the Act ) contains significant legislation

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University Tax Planning

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

Tax Update for 2018 and 2019

Tax Update for 2018 and 2019 Individual Tax Changes Business Tax Changes Depreciation Changes Inflation Adjustments IRS Mileage Rates Affordable Care Act Partnership Audit Rules The following is a summary

Tax Update for 2018 and 2019 Individual Tax Changes Business Tax Changes Depreciation Changes Inflation Adjustments IRS Mileage Rates Affordable Care Act Partnership Audit Rules The following is a summary

I TAX REFORM FOR INDIVIDUALS

I TAX REFORM FOR INDIVIDUALS A. Simplification and Reform of Rates, Standard Deductions, and Exemptions 1. Reduction and simplification of individual income tax rates and modification of inflation adjustment

I TAX REFORM FOR INDIVIDUALS A. Simplification and Reform of Rates, Standard Deductions, and Exemptions 1. Reduction and simplification of individual income tax rates and modification of inflation adjustment

AGRICULTURAL FINANCIAL AND TAX PLANNING. Self Employment Tax on Ranch Related Income

AGRICULTURAL FINANCIAL AND TAX PLANNING Self Employment Tax on Ranch Related Income By Thomas J. Bryant, CPA and Ryan Beasley, CPA In last months article we mentioned a February 27, 2017, Internal Revenue

AGRICULTURAL FINANCIAL AND TAX PLANNING Self Employment Tax on Ranch Related Income By Thomas J. Bryant, CPA and Ryan Beasley, CPA In last months article we mentioned a February 27, 2017, Internal Revenue

TAX in the News. Qualified Business Income Deduction. Part 2 (August 29, 2018): Specified Service Trade or Business (SSTB)

: Specified Service Trade or Business (SSTB)") Tax Information for Tax Practitioners Part 1 (August 22, 2018): Overview Part 2 (August 29, 2018): Specified Service Trade or Business (SSTB) Part 3 (September 19, 2018): QBI Vocabulary Part 4 (September

Tax Information for Tax Practitioners Part 1 (August 22, 2018): Overview Part 2 (August 29, 2018): Specified Service Trade or Business (SSTB) Part 3 (September 19, 2018): QBI Vocabulary Part 4 (September

The Tax Cuts and New Jobs Act (TCJA)

") The Tax Cuts and New Jobs Act (TCJA) October 2, 2018 October 2, 2018 Format for today: 45 minute presentation 30 minutes for question and answer How to: Housekeeping Items Expand slides to full screen

The Tax Cuts and New Jobs Act (TCJA) October 2, 2018 October 2, 2018 Format for today: 45 minute presentation 30 minutes for question and answer How to: Housekeeping Items Expand slides to full screen

NEW LEGISLATION BUSINESS

NEW LEGISLATION BUSINESS 2 Land Grant University Tax Education Foundation Corporate Tax Rate... 24 Employer Credit for Paid Family and Medical Leave.... 25 Credit for Prior-Year Minimum Tax Liability of

NEW LEGISLATION BUSINESS 2 Land Grant University Tax Education Foundation Corporate Tax Rate... 24 Employer Credit for Paid Family and Medical Leave.... 25 Credit for Prior-Year Minimum Tax Liability of

THE PRESENT TAX LANDSCAPE: IMPLICATIONS FOR INDIVIDUALS, BUSINESSES, INVESTORS, AND OTHERS. Roger A. McEowen and Lori A. McMillan

THE PRESENT TAX LANDSCAPE: IMPLICATIONS FOR INDIVIDUALS, BUSINESSES, INVESTORS, AND OTHERS Roger A. McEowen and Lori A. McMillan CONTACT INFORMATION Roger A. McEowen Kansas Farm Bureau Professor of Agricultural

THE PRESENT TAX LANDSCAPE: IMPLICATIONS FOR INDIVIDUALS, BUSINESSES, INVESTORS, AND OTHERS Roger A. McEowen and Lori A. McMillan CONTACT INFORMATION Roger A. McEowen Kansas Farm Bureau Professor of Agricultural

New Legislation - Business. Chapter 2 pp National Income TAX Workbook

New Legislation - Business Chapter 2 pp. 23-58 2018 National Income TAX Workbook QBI Stuff Allowable Years Property shall be treated as If such property has a class life in years of Years property may

New Legislation - Business Chapter 2 pp. 23-58 2018 National Income TAX Workbook QBI Stuff Allowable Years Property shall be treated as If such property has a class life in years of Years property may

2018 Corporate/Business Tax Law Review

BUSINESS CONCEPTS MARCH 2018 2018 Corporate/Business Tax Law Review In our last tax article, we discussed how the 2017 Tax Cuts and Jobs Act (TCJA) brought many changes to individual income tax filers.

BUSINESS CONCEPTS MARCH 2018 2018 Corporate/Business Tax Law Review In our last tax article, we discussed how the 2017 Tax Cuts and Jobs Act (TCJA) brought many changes to individual income tax filers.

Michael J. Reilly, CPA/ABV, CVA, CFF, CDA

Michael J. Reilly, CPA/ABV, CVA, CFF, CDA Key Tax Provisions in the Tax Cut and Jobs Act Michael J. Reilly, CPA/ABV, CVA, CFF, CDA - Tax Partner mreilly@dmcpas.com Tax Reform Seminar Embassy Suites by

Michael J. Reilly, CPA/ABV, CVA, CFF, CDA Key Tax Provisions in the Tax Cut and Jobs Act Michael J. Reilly, CPA/ABV, CVA, CFF, CDA - Tax Partner mreilly@dmcpas.com Tax Reform Seminar Embassy Suites by

Aviation Tax Issues From The New Tax Changes: Opportunities, Challenges & Questions Sue Folkringa, CPA

Aviation Tax Issues From The New Tax Changes: Opportunities, Challenges & Questions Sue Folkringa, CPA 2018 NBAA Regional Forum San Jose, CA September 6, 2018 Wolcott & Associates, P.A. - What We Do We

Aviation Tax Issues From The New Tax Changes: Opportunities, Challenges & Questions Sue Folkringa, CPA 2018 NBAA Regional Forum San Jose, CA September 6, 2018 Wolcott & Associates, P.A. - What We Do We

Office of Chief Counsel Internal Revenue Service memorandum

Office of Chief Counsel Internal Revenue Service memorandum Number: 200325002 Release Date: 6/20/2003 UILC: 1401.00-00 CC:TEGE:EOEG:ET1 SCA-147742-01 date: May 29, 2003 to: from: VIRGINIA E. COCHRAN DEPUTY

Office of Chief Counsel Internal Revenue Service memorandum Number: 200325002 Release Date: 6/20/2003 UILC: 1401.00-00 CC:TEGE:EOEG:ET1 SCA-147742-01 date: May 29, 2003 to: from: VIRGINIA E. COCHRAN DEPUTY

October Don Nitchie Tonya Knorr Garen Paulson Allen Deutz. Inside this Newsletter:

Don Nitchie Tonya Knorr Garen Paulson Allen Deutz Inside this Newsletter: What is a Fair Farm Rental Agreement? SWMFBMA Board Meeting December Prepare for your Tax Planning Appointment The New Qualified

Don Nitchie Tonya Knorr Garen Paulson Allen Deutz Inside this Newsletter: What is a Fair Farm Rental Agreement? SWMFBMA Board Meeting December Prepare for your Tax Planning Appointment The New Qualified

US TAX SYSTEM. # Important to Account for Impact of Taxes on Income. R we are concerned with after-tax cash flows (ATCF)

") US TAX SYSTEM # Important to Account for Impact of Taxes on Income R we are concerned with after-tax cash flows (ATCF) # Internal Revenue Service (IRS) R responsible for collecting taxes R regulations

US TAX SYSTEM # Important to Account for Impact of Taxes on Income R we are concerned with after-tax cash flows (ATCF) # Internal Revenue Service (IRS) R responsible for collecting taxes R regulations

How Does Tax Reform Affect Real Estate Developers & Investors?

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

New Law Part 1. Other Sec. 199A Issues

New Law Part 1 Other Sec. 199A Issues 2 Three STEPS (Non-SSBs) 1) Potential QBI Deduction: 20% x QBI 2) W2+UB Limit Phases-in based upon TI: (% W-2 Wages + Unadjusted Basis) 3) TI-NCG Limit: Taxable income

New Law Part 1 Other Sec. 199A Issues 2 Three STEPS (Non-SSBs) 1) Potential QBI Deduction: 20% x QBI 2) W2+UB Limit Phases-in based upon TI: (% W-2 Wages + Unadjusted Basis) 3) TI-NCG Limit: Taxable income

INCOME TAX MANAGEMENT FOR FARMERS IN 2011

INCOME TAX MANAGEMENT FOR FARMERS IN 2011 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2011 DRAFT 2011 version has not been peer-reviewed. Comments are welcome.

INCOME TAX MANAGEMENT FOR FARMERS IN 2011 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2011 DRAFT 2011 version has not been peer-reviewed. Comments are welcome.

Business Changes in the Tax Cuts and Jobs Act. Alan D. Sobel, CPA December 27,

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

Things to note before starting

A Taxation Focus Austin Duerfeldt Agricultural Economist Email: aduerfeldt2@unl.edu Phone: (402) 873-3166 Facebook: SE NE Ag Economist Twitter: SENE_AgEcon 2017 TAX CUTS AND JOBS ACT Things to note before

A Taxation Focus Austin Duerfeldt Agricultural Economist Email: aduerfeldt2@unl.edu Phone: (402) 873-3166 Facebook: SE NE Ag Economist Twitter: SENE_AgEcon 2017 TAX CUTS AND JOBS ACT Things to note before

Oil and Gas Tax Issues. Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP

Oil and Gas Tax Issues Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP Arnett Carbis Toothman llp 2018 Depletion and Ways to Compute What is depletion and what is its

Oil and Gas Tax Issues Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP Arnett Carbis Toothman llp 2018 Depletion and Ways to Compute What is depletion and what is its

INCOME TAX MANAGEMENT FOR FARMERS IN 2010

INCOME TAX MANAGEMENT FOR FARMERS IN 2010 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2010 DRAFT INCOME TAX MANAGEMENT FOR FARMERS IN 2010 Table of Contents

INCOME TAX MANAGEMENT FOR FARMERS IN 2010 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2010 DRAFT INCOME TAX MANAGEMENT FOR FARMERS IN 2010 Table of Contents

Presented by: Cyndi G. Warren, CPA Warren Averett Farming and Taxes 101

Presented by: Cyndi G. Warren, CPA Warren Averett www.warrenaverett.com Farming and Taxes 101 AGENDA TAX REFORM High Level Overview Choice of Entity Considerations Q & A HOW DID WE GET HERE? HOUSE OF REPRESENTATIVES

Presented by: Cyndi G. Warren, CPA Warren Averett www.warrenaverett.com Farming and Taxes 101 AGENDA TAX REFORM High Level Overview Choice of Entity Considerations Q & A HOW DID WE GET HERE? HOUSE OF REPRESENTATIVES

How Tax Reforms Impacts Your Vineyard February 8, Presented by: Kathy Freshwater, CPA Craig Anderson, CPA

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

Tax Cuts and Jobs Act Update

Tax Cuts and Jobs Act Update INSIGHTS FOR BUSINESSES & INDIVIDUALS JUNE 14, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Tax Cuts and Jobs Act Update INSIGHTS FOR BUSINESSES & INDIVIDUALS JUNE 14, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Depreciation i for tax purposes is not the same as depreciation for management decisions or

Depreciation i for tax purposes is not the same as depreciation for management decisions or accounting. Non cash event but still reduces taxable income Flexibility in calculating it Can be used to level

Depreciation i for tax purposes is not the same as depreciation for management decisions or accounting. Non cash event but still reduces taxable income Flexibility in calculating it Can be used to level

QBI, QBIA, and QBID. New 199A: Qualified Business Income Deduction or Amount

IRC Sec. 199A QBID QBI, QBIA, and QBID New 199A: Qualified Business Income Deduction or Amount 2 The first part of this presentation refers to the Section 199A deduction as QBID (Qualified Business Income

IRC Sec. 199A QBID QBI, QBIA, and QBID New 199A: Qualified Business Income Deduction or Amount 2 The first part of this presentation refers to the Section 199A deduction as QBID (Qualified Business Income

Tax Reform Highlights

etax Alert Tax Reform Highlights Final Business/Corporate/Partnership Provisions in Tax Cuts and Jobs Act of 2017 Here is a chart that briefly summarizes the major provisions affecting our business clients,

etax Alert Tax Reform Highlights Final Business/Corporate/Partnership Provisions in Tax Cuts and Jobs Act of 2017 Here is a chart that briefly summarizes the major provisions affecting our business clients,

*187171* Before you complete this schedule, read the instructions which are on a separate sheet.

*187171* 2018 Schedule M2SBNC, Federal Adjustments Minnesota has not adopted the federal law changes enacted after December 16, 2016 that affect federal taxable income for tax year 2018. Tax year beginning,

*187171* 2018 Schedule M2SBNC, Federal Adjustments Minnesota has not adopted the federal law changes enacted after December 16, 2016 that affect federal taxable income for tax year 2018. Tax year beginning,

Who Blinked? The American Taxpayer Relief Act of Winter 2013 A 45,000 foot view of Recent Tax Law Changes affecting Agriculture

Who Blinked? The American Taxpayer Relief Act of 2012 Winter 2013 A 45,000 foot view of Recent Tax Law Changes affecting Agriculture Federal Income Tax Changes Affecting Agriculture Individual Income Tax

Who Blinked? The American Taxpayer Relief Act of 2012 Winter 2013 A 45,000 foot view of Recent Tax Law Changes affecting Agriculture Federal Income Tax Changes Affecting Agriculture Individual Income Tax

Channel Islands Chapter of the California Society of Enrolled Agents

Channel Islands Chapter of the California Society of Enrolled Agents IRS Regulations Clarify Business Pass-Through Deduction Article Highlights: Trade or Business Definition Qualified Business Income Limitation

Channel Islands Chapter of the California Society of Enrolled Agents IRS Regulations Clarify Business Pass-Through Deduction Article Highlights: Trade or Business Definition Qualified Business Income Limitation

Michael J. Reilly, CPA/ABV, CVA, CFF, CDA Nicholas L. Shires, CPA

Michael J. Reilly, CPA/ABV, CVA, CFF, CDA Nicholas L. Shires, CPA Key Tax Provisions in the Tax Cut and Jobs Act Michael J. Reilly, CPA/ABV, CVA, CFF, CDA - Tax Partner Nicholas L. Shires, CPA - Tax Partner

Michael J. Reilly, CPA/ABV, CVA, CFF, CDA Nicholas L. Shires, CPA Key Tax Provisions in the Tax Cut and Jobs Act Michael J. Reilly, CPA/ABV, CVA, CFF, CDA - Tax Partner Nicholas L. Shires, CPA - Tax Partner

Tax Cuts & Jobs Act (TCJA)

") Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

New Legislation - Business. Chapter 2 pp National Income TAX Workbook

New Legislation - Business Chapter 2 pp. 23-58 2018 National Income TAX Workbook Corporate Tax Changes p. 24 Tax years beginning after 12/31/2017 Flat 21% tax rate Limit on accumulated earnings credit

New Legislation - Business Chapter 2 pp. 23-58 2018 National Income TAX Workbook Corporate Tax Changes p. 24 Tax years beginning after 12/31/2017 Flat 21% tax rate Limit on accumulated earnings credit

TAX REPORTING AND PAYMENT

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s 1120 Deskbook. 28th Edition (October 2018)

") T20 10/18 Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1120 Deskbook 28th Edition (October 2018) Highlights of this Edition Important new feature of the 2018 Edition

T20 10/18 Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1120 Deskbook 28th Edition (October 2018) Highlights of this Edition Important new feature of the 2018 Edition

Tax reform potpourri. cooperatives. Overview of key provisions affecting. Presented By:

Tax reform potpourri Overview of key provisions affecting cooperatives Presented By: David Antoni, KPMG LLP National Society of Accountants for Cooperatives 2018 Tax, Finance & Accounting Conference for

Tax reform potpourri Overview of key provisions affecting cooperatives Presented By: David Antoni, KPMG LLP National Society of Accountants for Cooperatives 2018 Tax, Finance & Accounting Conference for

Net Worth Statement Instructions & Forms Dan Childs NF-AE-01-02

Net Worth Statement Instructions & Forms Dan Childs NF-AE-01-02 NF Net Worth Statement Instructions The Samuel Roberts Noble Foundation Introduction: Good financial management is very important to being

Net Worth Statement Instructions & Forms Dan Childs NF-AE-01-02 NF Net Worth Statement Instructions The Samuel Roberts Noble Foundation Introduction: Good financial management is very important to being

Nonpassive Business Loss Limit (Sec. 461(l))

)") Nonpassive Business Loss Limit (Sec. 461(l)) Excess Nonpassive Business Loss Not Deductible in Current Year Applies to all taxpayers other than C corporations. Excess Business Loss = The excess of the

Nonpassive Business Loss Limit (Sec. 461(l)) Excess Nonpassive Business Loss Not Deductible in Current Year Applies to all taxpayers other than C corporations. Excess Business Loss = The excess of the

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018 WHAT WE WILL COVER TODAY 1 2 Business & individual provisions of the Tax Cuts and Jobs

Tax Cuts & Jobs Act W H AT B U S I N E S S E S & I N D I V I D U A L S N E E D T O K N O W D E C E M B E R 1 2, 2018 WHAT WE WILL COVER TODAY 1 2 Business & individual provisions of the Tax Cuts and Jobs

Ag Income Tax Update for Farm Families

Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Extension Educator Gary A. Hachfeld, Extension Educator January 2010 Introduction: For tax years 2009 and 2010, there are a number

Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Extension Educator Gary A. Hachfeld, Extension Educator January 2010 Introduction: For tax years 2009 and 2010, there are a number

Tax Planning. and. Management Considerations. for Farmers in George F. Patrick Extension Agricultural Economist Purdue University

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

Tax-Saving Tips. The Advisory Firm s. IRS Issues Final Section 199A Regulations and Defines QBI. Rental Property QBI

The Advisory Firm s February 2019 IRS Issues Final Section 199A Regulations and Defines QBI Example. You have $120,000 of net income on Schedule C. You deducted $10,000 for self-employed health insurance,

The Advisory Firm s February 2019 IRS Issues Final Section 199A Regulations and Defines QBI Example. You have $120,000 of net income on Schedule C. You deducted $10,000 for self-employed health insurance,

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Specialized Industry Tax Guide

ITG 8/18 Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s Specialized Industry Tax Guide 20 th Edition (August 2018) Highlights of this Edition The following are some

ITG 8/18 Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s Specialized Industry Tax Guide 20 th Edition (August 2018) Highlights of this Edition The following are some

Business Provisions Under the Tax Cuts and Jobs Act Compared to Previous Tax Law

Tax Rates Corporate tax rate Top rate of 35 percent Flat rate of 21 percent (effective 1/1/2018) Alternative minimum tax (AMT) 20 percent Repealed; AMT credits refundable from 2018 through 2021 (1) Personal

Tax Rates Corporate tax rate Top rate of 35 percent Flat rate of 21 percent (effective 1/1/2018) Alternative minimum tax (AMT) 20 percent Repealed; AMT credits refundable from 2018 through 2021 (1) Personal

Asset Management Conference

National Housing & Rehabilitation Association Asset Management Conference June 11 12, 2018 Bethesda, MD Sponsors: OVERVIEW LIHTC itself emerged from the Tax Cuts and Jobs Act largely unchanged Other main

National Housing & Rehabilitation Association Asset Management Conference June 11 12, 2018 Bethesda, MD Sponsors: OVERVIEW LIHTC itself emerged from the Tax Cuts and Jobs Act largely unchanged Other main

2014 Income Tax Webinar

2014 Income Tax Webinar Charles Brown ISU Farm Management Specialist 515 240 9214 crbrown@iastate.edu Expired Tax Provisions Above the line deduction for certain expenses of school teachers Above the line

2014 Income Tax Webinar Charles Brown ISU Farm Management Specialist 515 240 9214 crbrown@iastate.edu Expired Tax Provisions Above the line deduction for certain expenses of school teachers Above the line

2017 Tax Reform: Checkpoint Special Study on Business Tax Changes in the "Tax Cuts and Jobs Act"

2017 Tax Reform: Checkpoint Special Study on Business Tax Changes in the "Tax Cuts and Jobs Act" On December 15, the Conference Committee-having reconciled and merged the differing House and Senate provisions

2017 Tax Reform: Checkpoint Special Study on Business Tax Changes in the "Tax Cuts and Jobs Act" On December 15, the Conference Committee-having reconciled and merged the differing House and Senate provisions

2017 Tax Reform: Checkpoint Special Study on Business Tax Changes in the. "Tax Cuts and Jobs Act"

2017 Tax Reform: Checkpoint Special Study on Business Tax Changes in the "Tax Cuts and Jobs Act" Text of the "Tax Cuts and Jobs Act." Joint Explanatory Statement of the Committee of Conference. On December

2017 Tax Reform: Checkpoint Special Study on Business Tax Changes in the "Tax Cuts and Jobs Act" Text of the "Tax Cuts and Jobs Act." Joint Explanatory Statement of the Committee of Conference. On December

Exempt Organization Business Income Tax Return

Form For calendar year 2013 or other tax year beginning, and ending. 34 Unrelated business taxable income. Subtract line 33 from line 32. If line 33 is greater than line 32, enter the smaller of zero or

Form For calendar year 2013 or other tax year beginning, and ending. 34 Unrelated business taxable income. Subtract line 33 from line 32. If line 33 is greater than line 32, enter the smaller of zero or

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

Additional Information

Charles Brown 2015 Farm Income Tax Webinar Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Summary Social Security Wage Base Entity Comparison

Charles Brown 2015 Farm Income Tax Webinar Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Summary Social Security Wage Base Entity Comparison

TABLE OF CONTENTS SECTION I FARM PROBLEMS & EXAMPLES. Installment Contracts and Deferred Grain Contracts

TABLE OF CONTENTS SECTION I FARM PROBLEMS & EXAMPLES Page Installment Contracts and Deferred Grain Contracts... 1-2 Example of Reporting an Installment Sale (Example-Forms)... 3-6 Example of Taxpayer s

TABLE OF CONTENTS SECTION I FARM PROBLEMS & EXAMPLES Page Installment Contracts and Deferred Grain Contracts... 1-2 Example of Reporting an Installment Sale (Example-Forms)... 3-6 Example of Taxpayer s

IRS Issues Notice of proposed ruling on self-employment tax treatment of CRP payments - Suggested outline for comments now available

IRS Issues Notice of proposed ruling on self-employment tax treatment of CRP payments - Suggested outline for comments now available 2321 N. Loop Drive, Ste 200 Ames, Iowa 50010 www.calt.iastate.edu Updated

IRS Issues Notice of proposed ruling on self-employment tax treatment of CRP payments - Suggested outline for comments now available 2321 N. Loop Drive, Ste 200 Ames, Iowa 50010 www.calt.iastate.edu Updated

REAL ESTATE REVIEW WINTER 2019

REAL ESTATE REVIEW WINTER 2019 BONUS DEPRECIATION TAX REFORM CHANGES MAKE COST SEGREGATION STUDIES ESSENTIAL TAX REFORM AND PARTNERSHIPS: WHAT YOU NEED TO KNOW THE POTENTIAL IMPACTS OF TAX REFORM TO REAL

REAL ESTATE REVIEW WINTER 2019 BONUS DEPRECIATION TAX REFORM CHANGES MAKE COST SEGREGATION STUDIES ESSENTIAL TAX REFORM AND PARTNERSHIPS: WHAT YOU NEED TO KNOW THE POTENTIAL IMPACTS OF TAX REFORM TO REAL

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA)

") Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE. Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP MOST SWEEPING TAX REFORM SINCE 1986 Tax Cuts and Jobs Act signed December 22, 2017 Generally

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP MOST SWEEPING TAX REFORM SINCE 1986 Tax Cuts and Jobs Act signed December 22, 2017 Generally

New Tax Rules. For You and Your Business Owners

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

10/24/2017. Farm Expenses. 26 CFR Expenses of Farmers. Ordinary and Necessary

Farm Expenses Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 24, 2017 26 CFR 1.162 12 Expenses of Farmers Farms engaged in for profit activities A farmer who operates a farm

Farm Expenses Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 24, 2017 26 CFR 1.162 12 Expenses of Farmers Farms engaged in for profit activities A farmer who operates a farm

Understanding Section 199A

Understanding Section 199A PRESENTERS: PHOTO PHOTO Dan Fales Shareholder Tony Schweier Shareholder Definition of key terms Agenda Who gets the deduction Aggregation election Limitation on the deduction

Understanding Section 199A PRESENTERS: PHOTO PHOTO Dan Fales Shareholder Tony Schweier Shareholder Definition of key terms Agenda Who gets the deduction Aggregation election Limitation on the deduction

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 INDIVIDUALS Standard Deduction Personal exemption State income tax/sales tax itemized deduction Mortgage interest Property taxes itemized deduction Tax brackets Alternative

Tax Cuts and Jobs Act of 2017 INDIVIDUALS Standard Deduction Personal exemption State income tax/sales tax itemized deduction Mortgage interest Property taxes itemized deduction Tax brackets Alternative

News. Tax Cuts and Jobs Act

News Release Date: 12/26/17 Cross References H.R. 1 Tax Cuts and Jobs Act On December 22, 2017 the President signed into law H.R. 1 (officially titled An Act to Provide for Reconciliation Pursuant to Titles

News Release Date: 12/26/17 Cross References H.R. 1 Tax Cuts and Jobs Act On December 22, 2017 the President signed into law H.R. 1 (officially titled An Act to Provide for Reconciliation Pursuant to Titles

WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES

Tax Reform: WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES Presented By: JOHN HELLER, CPA Manager Tax Services Group Agenda We will cover: Review Corporate Tax Changes Business Deduction Changes

Tax Reform: WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES Presented By: JOHN HELLER, CPA Manager Tax Services Group Agenda We will cover: Review Corporate Tax Changes Business Deduction Changes

BUSINESS DEDUCTIONS 510 Limitation on Deduction of Business Interest

BUSINESS DEDUCTIONS 510 Limitation on Deduction of Business Interest NEW LAW EXPLAINED Limitation on deduction of business interest for all taxpayers. The deduction of interest paid or accrued on a debt

BUSINESS DEDUCTIONS 510 Limitation on Deduction of Business Interest NEW LAW EXPLAINED Limitation on deduction of business interest for all taxpayers. The deduction of interest paid or accrued on a debt

total fair market value in 2003 is $550. The fair market *In addition to the 80% nonbusiness part of the expense.

Expense Amount Schedule A amount of the section deduction ($) for a total Deductible mortgage interest $,500 Line or * business income of $7,7. This amount goes on line Real estate taxes $,000 Line * since

Expense Amount Schedule A amount of the section deduction ($) for a total Deductible mortgage interest $,500 Line or * business income of $7,7. This amount goes on line Real estate taxes $,000 Line * since

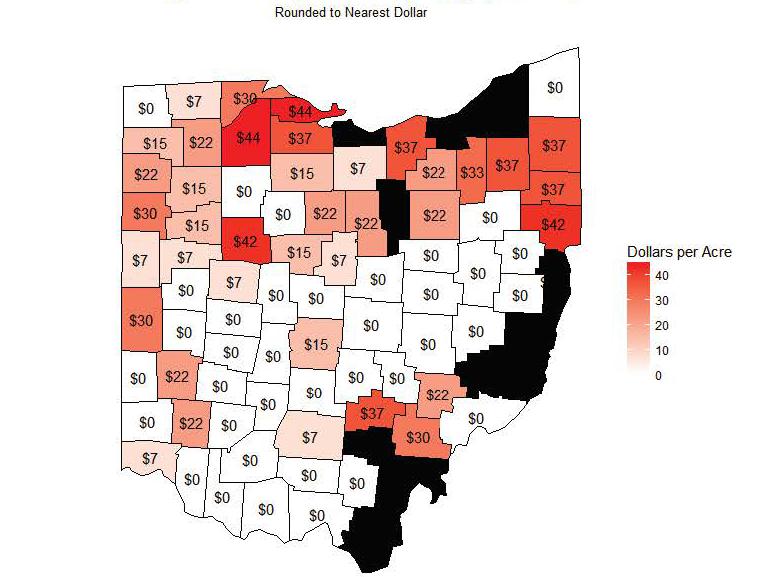

National marketing year average price less than the $3.70 Reference Price. Suppose a farmer is eligible what triggers a corn County ARC Payment?

AAE 320 Fall 2014 Final Exam Name: KEY 1) (20 pts. total, 2 pts. each) True or False? Mark your answer. a) T F_X_ Wisconsin s cranberry industry maybe important in the U.S., but production in Canada far

AAE 320 Fall 2014 Final Exam Name: KEY 1) (20 pts. total, 2 pts. each) True or False? Mark your answer. a) T F_X_ Wisconsin s cranberry industry maybe important in the U.S., but production in Canada far

Ag Income Tax Update for Farm Families

2006-07 Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Regional Extension Educator Gary A. Hachfeld, Regional Extension Educators Updated 6/2007 Introduction: For the 2006 and

2006-07 Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Regional Extension Educator Gary A. Hachfeld, Regional Extension Educators Updated 6/2007 Introduction: For the 2006 and

Instructions for Form 4562

2017 Instructions for Form 4562 Department of the Treasury Internal Revenue Service Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue

2017 Instructions for Form 4562 Department of the Treasury Internal Revenue Service Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue

THE VALUE OF ACCELERATED DEPRECIATION USE BY FARMERS: EVIDENCE FROM MICHIGAN. Leonard Lloyd Polzin

THE VALUE OF ACCELERATED DEPRECIATION USE BY FARMERS: EVIDENCE FROM MICHIGAN By Leonard Lloyd Polzin A THESIS Submitted to Michigan State University in partial fulfilment of the requirement for the degree

THE VALUE OF ACCELERATED DEPRECIATION USE BY FARMERS: EVIDENCE FROM MICHIGAN By Leonard Lloyd Polzin A THESIS Submitted to Michigan State University in partial fulfilment of the requirement for the degree