Additional Information

|

|

|

- Merry Fields

- 5 years ago

- Views:

Transcription

1 Charles Brown 2015 Farm Income Tax Webinar Field Specialist - Farm Management crbrown@iastate.edu Additional Information Tax Summary Social Security Wage Base Entity Comparison Chart Deferring Crop Insurance Depreciation Recovery Periods Employee or Contract Labor Succession Planning With Sub S Corp Medicare Tax Increase 1

2 Additional Information Oral Lease Agreement Iowa Anti-Corporate Farming Laws Mid-2015 Tax Policy Update Syngenta Claims Case Pension Contribution Limits Retirement Plan Comparison Chart Tax Calendar Additional Information Iowa Capital Gain Deduction Health Reimbursement Plans Marginal Tax Bracket Workers Compensation & Exemptions 2

3 Federal Depreciation 2015 Section 179 Expense election $25,000 maximum New & used equipment Tax years beginning in 2015 Only on cash boot paid 15 yr. property or less Only business assets(>50%), not rental Offsets business income & Section 1231 gain Can t be used on inherited assets or related party assets except between siblings Federal Depreciation 2015 Section 179 Expense election Phaseout starts at $200,000 of qualifying assets - $1 for $1 $500,000 extended for 2015(?) 3

4 Federal Depreciation % bonus depreciation Gone for 2015 unless Congress changes law Only available on new assets placed in service by 12/31/15 20 yr. life property or less Includes shops, machine sheds, pole barns Available for business and rental assets Cash boot and traded basis qualifies Can depreciate 50% of cash paid plus traded basis in first year Must elect out by class if not used Federal Depreciation % bonus depreciation Not available for business assets purchased from related parties Not available for qualified leasehold assets to related parties if 80% ownership test is met New grain bins or machine sheds leased to a related party would qualify Can create net operating loss (NOL) 4

5 Iowa Coupling 2015 In previous years Iowa Coupled with Federal Sec. 179 Did not couple with Federal bonus depreciation Tax Implications of Leasing Operating Lease Immediate deduction of lease payments What is not an Operating Lease Lease payment is applied to equity position A portion of the lease payment is designated as interest or equivalent of interest Lessee acquires ownership, or title of the equipment upon specified number of lease payments 5

6 Tax Implications of Leasing What is not an Operating Lease Over a short time the equipment is used, the total amount a lessee pays is an exceedingly large portion of the total sum required to buy the equipment outright Equipment payments exceed the current fair rental value At the time any purchase option may be excerised, the title to the equipment can be acquired for an exceedingly small purchase option price in relation to the actual value of the equipment. Tax Implications of Leasing Unanticipated Consequences Operating Lease Equipment traded and trade-in value applied to lease Trade-in value considered same as sold Gain is taxable Trade-in value must be amortized over length of lease No immediate deduction as a lease payment 6

7 Deferring Crop Insurance Proceeds Can only defer income related to yield loss Must normally sell more than 50% of crop the year following harvest Revenue insurance is calculated on both price and yield Must allocate income between yield loss and price Crop Insurance Allocation Deferral Table If Harvest Price Is: Lower Than Base Price If Actual Yield Is: Lower Than Guaranteed Yield How much can be deferred? Partial Lower Than Base Price Greater Than Guaranteed Yield None Greater Than Base Price Greater Than Base Price Greater Than Guaranteed Yield Lower Than Guaranteed Yield None-There is no crop insurance claim in this situation All 7

Requires a minimum of a 2-year lease term Additional tax credit if the beginning farmer is a veteran. www.")

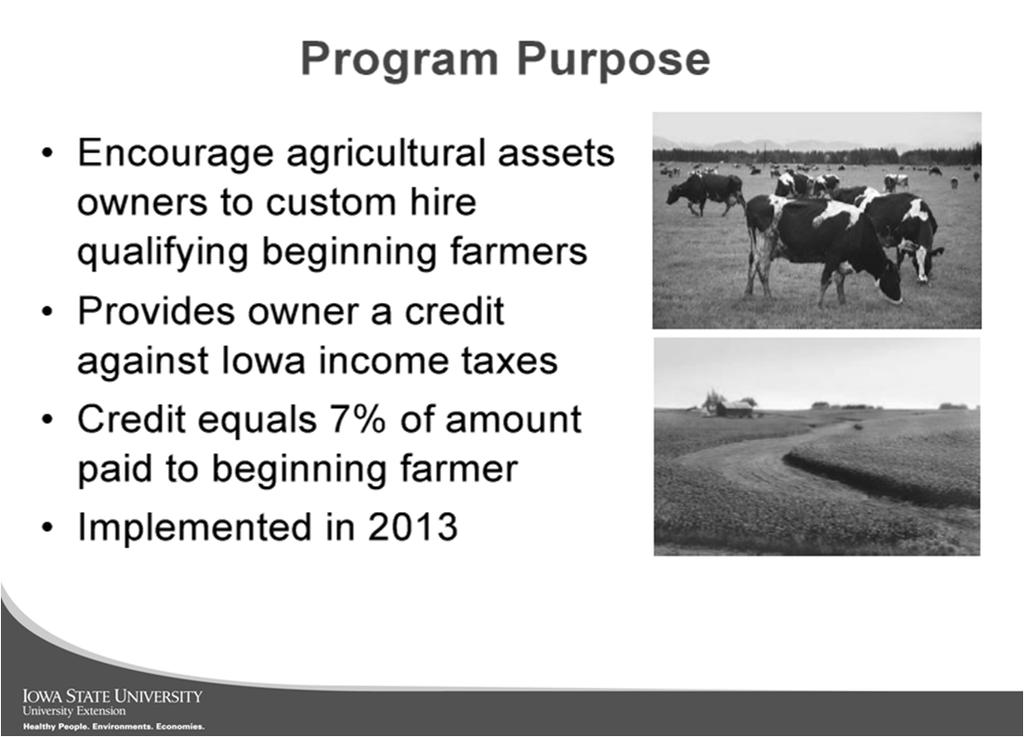

8 Crop Insurance Allocation Beginning Farmer Tax Credit Programs Provides Iowa income tax credits to landowners Landowner can receive an annual state tax credit for leasing land or custom hiring a beginning farmer 7% of gross income for a cash rent lease cannot include the bonus portion of Flexible Cash Lease 17% of gross income for crop share lease 7% of custom hire labor (less than 12 months) Requires a minimum of a 2-year lease term Additional tax credit if the beginning farmer is a veteran. 8

9 Beginning Farmer Tax Credit Procedures Application/Approval 4-page application (due October 1) IowaFinanceAuthority.gov/IADD Signed by landowner and beginning farmer Beginning farmer s financial statement Less than 30 days old when submitted to IADD Completed by lender with witness signature Net worth less than $703,844 Beginning farmer s background letter Submit application and appropriate fee $250 application fee plus: $50 service fee for each year of cash lease $100 service fee for each year of crop share lease. 9

10 Example Crop Share 160 Acres allocated ½ to corn, ½ to soybeans 80 acres corn at 167 bu x 50% x $3.83 x 17% = $4, Total corn crop = 13,360 bu. Owner s share = 6,680 bu. 80 acres soybeans at 48 bu x 50% x $8.91 x 17% = $ Total soybean crop = 3,840 bu. Owner s share = 1,920 bu. Total share lease tax credit = $

11 11

12 12

13 Unemployment Tax FUTA & SUTA Non-Agriculture Employees Paid wages of $1,500 or more in any calendar quarter or had one or more employees for some portion of at least one day during each of 20 different weeks. Agriculture Employees Cash wages of $20,000 or more paid in any calendar quarter or had 10 or more ag employees during some portion of a day (need not be at same time) at least 1 day during any 20 different weeks. Paying with Commodities Saves SE tax Doesn t count as wages for FUTA Report as income and wage expense on Schedule F Issue W2 Employee reports wage income and additional gain or loss from sale of commodity Employee must have control and dominion over commodity before it is sold Follow the rules! 13

14 Wages Paid In Kind Documentation on employment relationship, compensation practices and transfer of commodities. Marketing of commodity must be done by employee, not employer. Employee must stand the risk of gain of loss Use quantity, or % of production Spouse must have separate checking acct. Wages Paid In Kind Employee holding period must be as long as possible Cost of ownership must be born by employee Identify noncash payment, use documents to show quantity, quality, grade, etc. 14

15 Wages Paid in Kind Cash advances will be counted as cash wages Immediate conversion will be counted as cash wages Sole source of income will add to the question of immediate conversion. A farmer receiving PIK and then selling the commodity could generate earned income on the additional income earned. Divergent Incomes for 2015 Low to no taxable income for 2015 Use up government deductions if at all possible Standard deduction MFJ = $12,600 Personal exemption = $4,000 Married family of 4 $28,600 of Federal tax free income That is about 8,000 bu. of corn or 3,500 bu. of soybeans If net operating loss (NOL) is unavoidable Can elect to carry it back either 2 or 5 years or carry forward 15

16 Divergent Incomes for 2015 High income year Lock in grain price, but use deferred payment contract Prepay expenses Can prepay rent, up to 12 months Not between related parties Pay up accrued interest Sec. 179 Expense Election $25,000, maybe more? Bonus depreciation, 50%? Double up on itemized deductions Fund retirement plans Deferred Payment Contracts Have multiple contracts Cash basis taxpayers can use for tax planning Can elect to pull back a contract into current year Has to be full contract 16

17 Charitable Remainder Trusts Two types Annuity trust Unitrust Both allow tax-free sale of assets, with income stream back to the donor during his/her lifetime and the remainder of trusts assets paid to named charity upon trust termination Charitable deduction limited to 30% of AGI Unused deduction can only be carried ahead 5 yrs. Charitable remainder value must equal at least 10% of the net fair market value of the property as of the date of contribution Charitable Remainder Trusts Annuity trust Payment each year back to the donor as either a fixed amount, or a percentage of the initial value of the trust Life of donor/beneficiary or term certain that can not exceed 20 yrs. Can not add additional assets at later time Can distribute principle back to donor 17

18 Charitable Remainder Trusts Unitrust Payment back to donor is computed as percentage of an annual revaluation of the market value of the trust assets May accept additional contributions of assets Can only distribute earned interest and dividends back to donor Capital gains will added to trust assets unless specified otherwise in trust document Charitable Remainder Trusts Sequences and tax results of CRT 1. Donor creates irrevocable CRT, terms of trust require an annual income stream back to donor with the remainder passing to a charitable organization at the death of the donor or after specified term of years 2. Donor transfers appreciated long-term capital gain asset to trust, claims a charitable deduction for market value of asset, but reduced by retained income interest. Zero basis assets give no charitable deduction 18

19 Charitable Remainder Trusts Sequences and tax results of CRT 3. After trust receives asset, asset in normally sold, but reports no taxable gain due to its charitable status 4. The CRT invests the sale proceeds to provide source of income to allow specified payment to donor 5. At the death of the donor, the property within the trust passes to the charity, the trust property is not part of the taxable estate of the donor Charitable Remainder Trusts Example 1 Market value of farm land is $331,500 Percentage payback to donor is 9.79% Term selected is 13 yrs. Donor will receive a charitable deduction of approximately $50,000 Donor will receive income stream of approximately $32,500 per year Income stream is taxable income to donor based on capital gain rates 19

20 Charitable Remainder Trusts Example 2 Grain worth $200,000 transferred to CRT Trust sells grain, pays no tax $0 basis in grain, no charitable deduction Trust specifies 6% income stream to donor $12,000/yr. income stream to donor Ordinary income tax paid by donor on income stream, no social security tax paid Thank you! 20

2014 Income Tax Webinar

2014 Income Tax Webinar Charles Brown ISU Farm Management Specialist 515 240 9214 crbrown@iastate.edu Expired Tax Provisions Above the line deduction for certain expenses of school teachers Above the line

2014 Income Tax Webinar Charles Brown ISU Farm Management Specialist 515 240 9214 crbrown@iastate.edu Expired Tax Provisions Above the line deduction for certain expenses of school teachers Above the line

2017 Farm Income Tax Webinar

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

Tax Potholes and Pitfalls

Tax Potholes And Pitfalls January 31, 2013 Paul Neiffer, CPA 1 1 Agenda Background on CLA and other items. Update on the New Tax Laws Tax Potholes and Pitfalls Crop Insurance Tax Planning for 2012/13.

Tax Potholes And Pitfalls January 31, 2013 Paul Neiffer, CPA 1 1 Agenda Background on CLA and other items. Update on the New Tax Laws Tax Potholes and Pitfalls Crop Insurance Tax Planning for 2012/13.

Income Tax Management for Farmers in 2011

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

DTN University Pass It On! Farm Family Estate and Succession Planning

DTN University Pass It On! Farm Family Estate and Succession Planning Marcia Zarley Taylor, DTN Executive Editor Andy Biebl, CPA, Tax Partner, CliftonLarsonAllen LLC Nick Houle, CPA, Tax Partner, CliftonLarsonAllen

DTN University Pass It On! Farm Family Estate and Succession Planning Marcia Zarley Taylor, DTN Executive Editor Andy Biebl, CPA, Tax Partner, CliftonLarsonAllen LLC Nick Houle, CPA, Tax Partner, CliftonLarsonAllen

Updates to 2015 edition of Conservation Options: A Landowner s Guide to Conserving Your Land for Future Generations

Updates to 2015 edition of Conservation Options: A Landowner s Guide to Conserving Your Land for Future Generations In a great victory for landowners interested in conservation, Congress and the president

Updates to 2015 edition of Conservation Options: A Landowner s Guide to Conserving Your Land for Future Generations In a great victory for landowners interested in conservation, Congress and the president

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

Tax Planning Considerations for 2015

Tax Planning Considerations for 2015 Most strategies that could have an impact on your taxes need to be made by December 31 if you want them reflected on your 2015 tax return. Executive summary As the

Tax Planning Considerations for 2015 Most strategies that could have an impact on your taxes need to be made by December 31 if you want them reflected on your 2015 tax return. Executive summary As the

Agribusiness Farm Tax Seminar

Agribusiness Farm Tax Seminar Specialty Estate Tax Seminar for Farm Families Nicholas Houle, CPA, MBT Christopher Hesse, CPA December 17, 2013 CLAconnect.com Disclaimers To ensure compliance imposed by

Agribusiness Farm Tax Seminar Specialty Estate Tax Seminar for Farm Families Nicholas Houle, CPA, MBT Christopher Hesse, CPA December 17, 2013 CLAconnect.com Disclaimers To ensure compliance imposed by

2016 Tax Preparation Checklist. Documentation for Itemized Deductions

Essentials for Taxpayers For 2016 Federal Returns Due in April 2017 2016 Tax Preparation Checklist n Copy of 2015 tax return n Social Security number(s) taxpayers and dependents n W-2 forms from all employers

Essentials for Taxpayers For 2016 Federal Returns Due in April 2017 2016 Tax Preparation Checklist n Copy of 2015 tax return n Social Security number(s) taxpayers and dependents n W-2 forms from all employers

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University Tax Planning

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

Farm Taxes. David L. Marrison, Associate Professor

Farm Taxes David L. Marrison, Associate Professor Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax

Farm Taxes David L. Marrison, Associate Professor Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax

Batten Down the Hatches and Protect the Hen House Keeping the Government Foxes (IRS) at Bay

at Bay") Batten Down the Hatches and Protect the Hen House Keeping the Government Foxes (IRS) at Bay Orman R. Wilson, CPA October 20, 2016 Birmingham, Selma & Tuscaloosa, Alabama USA Today s Outline You are a timber

Batten Down the Hatches and Protect the Hen House Keeping the Government Foxes (IRS) at Bay Orman R. Wilson, CPA October 20, 2016 Birmingham, Selma & Tuscaloosa, Alabama USA Today s Outline You are a timber

AGRICULTURAL TAX. i n c o m e t a x e s

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014)

") THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014) Presented to: CENTENNIAL ESTATE PLANNING COUNCIL November

THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014) Presented to: CENTENNIAL ESTATE PLANNING COUNCIL November

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018 The TCJA s Impact on Farmers and Ranchers Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018 The TCJA s Impact on Farmers and Ranchers Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation

Specialty Estate Tax Seminar for Farm Families Paul Neiffer, CPA CliftonLarsonAllen, LLP

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP CLAconnect.com Specialty Estate Tax Seminar for Farm Families Paul Neiffer, CPA CliftonLarsonAllen, LLP Speaker Introduction Paul Neiffer, Principal,

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP CLAconnect.com Specialty Estate Tax Seminar for Farm Families Paul Neiffer, CPA CliftonLarsonAllen, LLP Speaker Introduction Paul Neiffer, Principal,

Comprehensive Charitable Planning

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

Tax Planning. and. Management Considerations. for Farmers in George F. Patrick Extension Agricultural Economist Purdue University

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

Four Tier Accounting for Charitable Remainder Trust. Richard C. Capasso, CPA, CFP, PFS

Four Tier Accounting for Charitable Remainder Trust Richard C. Capasso, CPA, CFP, PFS Charitable Remainder Trust Provide an option for dealing with appreciated property to philanthropic donors Trust is

Four Tier Accounting for Charitable Remainder Trust Richard C. Capasso, CPA, CFP, PFS Charitable Remainder Trust Provide an option for dealing with appreciated property to philanthropic donors Trust is

2018 Year-End Tax Planning for Individuals

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

Who Blinked? The American Taxpayer Relief Act of Winter 2013 A 45,000 foot view of Recent Tax Law Changes affecting Agriculture

Who Blinked? The American Taxpayer Relief Act of 2012 Winter 2013 A 45,000 foot view of Recent Tax Law Changes affecting Agriculture Federal Income Tax Changes Affecting Agriculture Individual Income Tax

Who Blinked? The American Taxpayer Relief Act of 2012 Winter 2013 A 45,000 foot view of Recent Tax Law Changes affecting Agriculture Federal Income Tax Changes Affecting Agriculture Individual Income Tax

Tax Planning with Qualified Charitable Distributions

Tax Planning with Qualified Charitable Distributions Understand how to benefit from this tax-saving tool GIVING WITH GREATER BENEFITS Are you age 70 1/2 or higher and subject to required minimum distributions

Tax Planning with Qualified Charitable Distributions Understand how to benefit from this tax-saving tool GIVING WITH GREATER BENEFITS Are you age 70 1/2 or higher and subject to required minimum distributions

2018 Options and Opportunities: Charitable Giving and the New Tax Rules

2018 Options and Opportunities: Charitable Giving and the New Tax Rules Page 1 Single filers (2018 2025): Joint filers (2018 2025): Page 2 In 2017, the standard deduction combined with the personal exemption

2018 Options and Opportunities: Charitable Giving and the New Tax Rules Page 1 Single filers (2018 2025): Joint filers (2018 2025): Page 2 In 2017, the standard deduction combined with the personal exemption

Ag Income Tax Update for Farm Families

2006-07 Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Regional Extension Educator Gary A. Hachfeld, Regional Extension Educators Updated 6/2007 Introduction: For the 2006 and

2006-07 Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Regional Extension Educator Gary A. Hachfeld, Regional Extension Educators Updated 6/2007 Introduction: For the 2006 and

Life Income Gifts 4/19/2016. How a Life Income Gift Works. Rebecca E. Dupras, Esq. Vice President of Development Silicon Valley Community Foundation

Life Income Gifts Rebecca E. Dupras, Esq. Vice President of Development Silicon Valley Community Foundation How a Life Income Gift Works Gift Donor Life Income Gift Remainder to Charity Income tax deduction

Life Income Gifts Rebecca E. Dupras, Esq. Vice President of Development Silicon Valley Community Foundation How a Life Income Gift Works Gift Donor Life Income Gift Remainder to Charity Income tax deduction

INCOME TAX MANAGEMENT FOR FARMERS IN 2011

INCOME TAX MANAGEMENT FOR FARMERS IN 2011 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2011 DRAFT 2011 version has not been peer-reviewed. Comments are welcome.

INCOME TAX MANAGEMENT FOR FARMERS IN 2011 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2011 DRAFT 2011 version has not been peer-reviewed. Comments are welcome.

charitable contributions

charitable contributions Your ability to control when and how you make charitable contributions can lower your income tax bill, effectively reducing the actual cost of any gift you make, while fulfilling

charitable contributions Your ability to control when and how you make charitable contributions can lower your income tax bill, effectively reducing the actual cost of any gift you make, while fulfilling

Estate Tax Overview Disinherit the IRS with planning and Philanthropy

52 N. Broadway Peru, IN 46970 P: (765)470-7090 F: (765)470-7091 www.dobbslegal.com Estate Tax Overview Disinherit the IRS with planning and Philanthropy Polly J. Dobbs, Esq. LET S TALK TAXES Upon death,

52 N. Broadway Peru, IN 46970 P: (765)470-7090 F: (765)470-7091 www.dobbslegal.com Estate Tax Overview Disinherit the IRS with planning and Philanthropy Polly J. Dobbs, Esq. LET S TALK TAXES Upon death,

Individual Tax Planning 2015 & Beyond

Individual Tax Planning 2015 & Beyond Tax Bracket Comparison 2015 & 2012 2015 MARRIED FILING JOINT 2012 MARRIED FILING JOINT 10% - up to $18,450 10% - up to $17,400 15% - $18,451 - $74,900 15% - $17,401

Individual Tax Planning 2015 & Beyond Tax Bracket Comparison 2015 & 2012 2015 MARRIED FILING JOINT 2012 MARRIED FILING JOINT 10% - up to $18,450 10% - up to $17,400 15% - $18,451 - $74,900 15% - $17,401

TMS Wealth Management Conference. Southwest Mississippi Community College. Presented by: Benny Jeansonne, CPA/ABV, CVA Peyton Cavin, CPA

TMS Wealth Management Conference September 26, 2014 Southwest Mississippi Community College Presented by: Benny Jeansonne, CPA/ABV, CVA Peyton Cavin, CPA Potential Taxes I. Income Taxes Potential Taxes

TMS Wealth Management Conference September 26, 2014 Southwest Mississippi Community College Presented by: Benny Jeansonne, CPA/ABV, CVA Peyton Cavin, CPA Potential Taxes I. Income Taxes Potential Taxes

Dear Client: Basic Numbers You Need to Know

Dear Client: As 2013 draws to a close, there is still time to reduce your 2013 tax bill and plan ahead for 2014. This letter highlights several potential tax-saving opportunities for you to consider. I

Dear Client: As 2013 draws to a close, there is still time to reduce your 2013 tax bill and plan ahead for 2014. This letter highlights several potential tax-saving opportunities for you to consider. I

Tax Cuts and Jobs Act of 2017 (TCJA) Key Individual Tax Provisions

Key Individual Tax Provisions") Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

YEAR-END TAX PLANNING LETTER

YEAR-END TAX PLANNING LETTER SUBMITTED BY Huntsville I Pensacola www.anglincpa.com Dear Clients and Friends, As 2018 draws to a close, there is still time to reduce your 2018 tax bill and plan ahead for

YEAR-END TAX PLANNING LETTER SUBMITTED BY Huntsville I Pensacola www.anglincpa.com Dear Clients and Friends, As 2018 draws to a close, there is still time to reduce your 2018 tax bill and plan ahead for

Year-End Tax Planning Summary December 2015

Year-End Tax Planning Summary December 2015 Overview Thanks to the continued political gridlock in Washington, 2015 did not see comprehensive tax reform. However, on December 18th, Congress passed the

Year-End Tax Planning Summary December 2015 Overview Thanks to the continued political gridlock in Washington, 2015 did not see comprehensive tax reform. However, on December 18th, Congress passed the

President Obama's 2016 Federal Budget Proposal

President Obama's 2016 Federal Budget Proposal March 10, 2015 by Tim Steffen On the heels of his first State of the Union address to the nation after the mid-term elections, President Obama released his

President Obama's 2016 Federal Budget Proposal March 10, 2015 by Tim Steffen On the heels of his first State of the Union address to the nation after the mid-term elections, President Obama released his

Charitable Remainder Trusts

Charitable Remainder Trusts Calculations and Examples Charitable Remainder Trust Summary of Benefits 2 Actuarial Calculations 3 Text Description 4 CRUT/Sell/Keep Comparison Summary of Benefits 5 Cash Flow

Charitable Remainder Trusts Calculations and Examples Charitable Remainder Trust Summary of Benefits 2 Actuarial Calculations 3 Text Description 4 CRUT/Sell/Keep Comparison Summary of Benefits 5 Cash Flow

New Tax Rules. For You and Your Business Owners

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

Taxes for Working Forests and Tree Farms. Mark Megalos, & Rick Hamilton, NC RF Extension Forester, Retired

Taxes for Working Forests and Tree Farms Mark Megalos, & Rick Hamilton, NC RF Extension Forester, Retired Income Tax Implications 1. Timber Sales and Basis 2. Cost-Share Payments 3. Reforestation Tax Incentive

Taxes for Working Forests and Tree Farms Mark Megalos, & Rick Hamilton, NC RF Extension Forester, Retired Income Tax Implications 1. Timber Sales and Basis 2. Cost-Share Payments 3. Reforestation Tax Incentive

Issues AND. Tax-Powered Philanthropy: Doing well by doing good

Issues AND INSIGHTS February 2015 Tax-Powered Philanthropy: Doing well by doing good IN THIS ARTICLE Higher tax rates offer greater potential savings from charitable giving Strategies such as outright

Issues AND INSIGHTS February 2015 Tax-Powered Philanthropy: Doing well by doing good IN THIS ARTICLE Higher tax rates offer greater potential savings from charitable giving Strategies such as outright

Top Producer Seminar A New Tax Bill: What You Need To Know Now. Paul Neiffer, CPA January 25, 2018 Chicago, Illinois

Top Producer Seminar A New Tax Bill: What You Need To Know Now Paul Neiffer, CPA January 25, 2018 Chicago, Illinois Speaker Introduction Paul Neiffer, Principal, CliftonLarsonAllen Frequent national speaker

Top Producer Seminar A New Tax Bill: What You Need To Know Now Paul Neiffer, CPA January 25, 2018 Chicago, Illinois Speaker Introduction Paul Neiffer, Principal, CliftonLarsonAllen Frequent national speaker

Through the Crystal Ball Farm Business Structure After Tax Reform. Paul Neiffer, CPA January 26, 2017 Chicago, Illinois

Through the Crystal Ball Farm Business Structure After Tax Reform Paul Neiffer, CPA January 26, 2017 Chicago, Illinois Speaker Introduction Paul Neiffer, Principal, CliftonLarsonAllen Frequent national

Through the Crystal Ball Farm Business Structure After Tax Reform Paul Neiffer, CPA January 26, 2017 Chicago, Illinois Speaker Introduction Paul Neiffer, Principal, CliftonLarsonAllen Frequent national

Agricultural and Natural Resource Issues Chapter 9 pp National Income Tax Workbook

Agricultural and Natural Resource Issues Chapter 9 pp. 287-327 2018 National Income Tax Workbook Agricultural and Natural Resources Issues Barry Ward, Davis Marrison, and Chris Bruynis Ag Economy Update

Agricultural and Natural Resource Issues Chapter 9 pp. 287-327 2018 National Income Tax Workbook Agricultural and Natural Resources Issues Barry Ward, Davis Marrison, and Chris Bruynis Ag Economy Update

Planned Giving 201. Presented by Christy Eckoff, JD, LL.M. Director of Gift Planning

Planned Giving 201 Presented by Christy Eckoff, JD, LL.M. Director of Gift Planning The Community Foundation for Greater Atlanta Bullet Mission information here To be the most trusted resource for growing

Planned Giving 201 Presented by Christy Eckoff, JD, LL.M. Director of Gift Planning The Community Foundation for Greater Atlanta Bullet Mission information here To be the most trusted resource for growing

How Does Tax Reform Affect Real Estate Developers & Investors?

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

SELECTED 2016 TAXATION ISSUES

SELECTED 2016 TAXATION ISSUES FOR IOWA FARMERS By Kristine A. Tidgren i November 2016 It has been estimated that the Internal Revenue Code and its accompanying regulations comprise more than 10 million

SELECTED 2016 TAXATION ISSUES FOR IOWA FARMERS By Kristine A. Tidgren i November 2016 It has been estimated that the Internal Revenue Code and its accompanying regulations comprise more than 10 million

TAX REPORTING AND PAYMENT

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

TAX ORGANIZER Page 3

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

Charitable Planned Giving Strategies

Charitable Planned Giving Strategies Courtesy of: Yellowstone Boys & Girls Ranch Foundation, Inc. This presentation was prepared for educational purposes only. It must not be used as a basis for tax or

Charitable Planned Giving Strategies Courtesy of: Yellowstone Boys & Girls Ranch Foundation, Inc. This presentation was prepared for educational purposes only. It must not be used as a basis for tax or

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

Volume 9, Issue Broadway Woodmere, NY (516)

") How to Avoid a Basis Management Disaster Many of us in the legal, financial and accounting worlds discover our new clients well-intentioned, yet disastrous, plans after the fact. The widow has already

How to Avoid a Basis Management Disaster Many of us in the legal, financial and accounting worlds discover our new clients well-intentioned, yet disastrous, plans after the fact. The widow has already

Charitable Remainder Unitrust. Planned Charitable Giving Using a Split-Interest Trust

Charitable Remainder Unitrust Planned Charitable Giving Using a Split-Interest Trust CRUT Overview Lifetime transfer of cash or property in trust in exchange for unitrust interest payable over (a) Fixed

Charitable Remainder Unitrust Planned Charitable Giving Using a Split-Interest Trust CRUT Overview Lifetime transfer of cash or property in trust in exchange for unitrust interest payable over (a) Fixed

Impact of Tax Reform on Farmers. Tax and Accounting Department Fall 2018

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Time is running out to make important planning moves before the year s end, so don t delay.

2015 Year-end tax planning Time is running out to make important planning moves before the year s end, so don t delay. The changes in various tax provisions brought about with the 2012 Tax Act continue

2015 Year-end tax planning Time is running out to make important planning moves before the year s end, so don t delay. The changes in various tax provisions brought about with the 2012 Tax Act continue

Advanced marketing concepts. Brought to you by the Advanced Consulting Group of Nationwide

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

The top federal income tax rate has increased from 35% to 39.6%. All other federal income tax rates are the same as they were in 2012.

Gift Planning and the New Tax Law PG Calc Featured Article, February 2013 http://www.pgcalc.com/about/featured-article-february-2013.htm The American Taxpayer Relief Act (ATRA) passed by Congress on January

Gift Planning and the New Tax Law PG Calc Featured Article, February 2013 http://www.pgcalc.com/about/featured-article-february-2013.htm The American Taxpayer Relief Act (ATRA) passed by Congress on January

Year End Tax Planning for Individuals

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

2013 TAX AND FINANCIAL PLANNING TABLES. An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning.

2013 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning. WHAT YOU WILL SEE IN THIS BROCHURE 2013 Income Tax Changes Tax Rates

2013 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning. WHAT YOU WILL SEE IN THIS BROCHURE 2013 Income Tax Changes Tax Rates

KEIR EDUCATIONAL RESOURCES

INCOME TAX PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

INCOME TAX PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

Understanding CRTs. A Summary of Charitable Remainder Trusts (CRTs) VLC

VLC") Understanding CRTs A Summary of Charitable Remainder Trusts (CRTs) VLC0439-0917 GET READY FOR RETIREMENT If your retirement planning objectives include lifetime income planning, estate tax reduction, 1

Understanding CRTs A Summary of Charitable Remainder Trusts (CRTs) VLC0439-0917 GET READY FOR RETIREMENT If your retirement planning objectives include lifetime income planning, estate tax reduction, 1

The Tax Cuts & Jobs Act

The Tax Cuts & Jobs Act Ten Key Changes that May Impact You August 2, 2018 Contact Information Kristine Tidgren, ktidgren@iastate.edu www.calt.iastate.edu @CALT_IowaState 2 1. MANY CHANGES ARE HERE TODAY,

The Tax Cuts & Jobs Act Ten Key Changes that May Impact You August 2, 2018 Contact Information Kristine Tidgren, ktidgren@iastate.edu www.calt.iastate.edu @CALT_IowaState 2 1. MANY CHANGES ARE HERE TODAY,

(married filing jointly) indexed for inflation in future years.

indexed for inflation in future years.") 2 AMERICAN TAXPAYER RELIEF ACT OF 2012 excess of the applicable threshold. These thresholds will be indexed for inflation in future years. Because the tax rates are permanent, for 2013 you can employ the

2 AMERICAN TAXPAYER RELIEF ACT OF 2012 excess of the applicable threshold. These thresholds will be indexed for inflation in future years. Because the tax rates are permanent, for 2013 you can employ the

e-pocket TAX TABLES 2017 and 2018 Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates

e-pocket TAX TABLES 2017 and 2018 Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

e-pocket TAX TABLES 2017 and 2018 Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

How Tax Reforms Impacts Your Vineyard February 8, Presented by: Kathy Freshwater, CPA Craig Anderson, CPA

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

Planning Under the New Tax Rules

Planning Under the New Tax Rules PLANNING UNDER THE NEW TAX RULES Businesses, both large and small, as well as individuals, face a markedly different tax landscape following passage of the Tax Cuts and

Planning Under the New Tax Rules PLANNING UNDER THE NEW TAX RULES Businesses, both large and small, as well as individuals, face a markedly different tax landscape following passage of the Tax Cuts and

Tax cuts and jobs act

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

2017 INCOME AND PAYROLL TAX RATES

2017-2018 Tax Tables A quick reference for income, estate and gift tax information QUICK LINKS: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum

2017-2018 Tax Tables A quick reference for income, estate and gift tax information QUICK LINKS: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum

Family Wealth Services 2013 year-end tax planning considerations for high-net-worth individuals and families

Family Wealth Services 2013 year-end tax planning considerations for high-net-worth individuals and families Dec. 3, 2013 Today s presenters Randy Abeles Family Wealth Services National Practice and Great

Family Wealth Services 2013 year-end tax planning considerations for high-net-worth individuals and families Dec. 3, 2013 Today s presenters Randy Abeles Family Wealth Services National Practice and Great

Net Operating Losses. Presented by: Keith Altobelli, EA

Presented by: Keith Altobelli, EA Net Operating Losses Objectives In this webinar the student will learn to: Calculate an NOL Determine whether to carry an NOL back or forward To claim an NOL deduction

Presented by: Keith Altobelli, EA Net Operating Losses Objectives In this webinar the student will learn to: Calculate an NOL Determine whether to carry an NOL back or forward To claim an NOL deduction

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

Charitable Giving Techniques

Charitable Giving Techniques Helping achieve your charitable and estate-planning goals Trust Tip A trust can be thought of as having two parts an income interest and a remainder interest. The income interest

Charitable Giving Techniques Helping achieve your charitable and estate-planning goals Trust Tip A trust can be thought of as having two parts an income interest and a remainder interest. The income interest

Your Comprehensive Guide to 2013 Year-End Tax Planning

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

Using Your Assets to Promote your Values. Lawrence M. Lehmann, JD, AEP, CAP Lehmann Norman & Marcus LC

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

NAR Frequently Asked Questions Health Insurance Reform

NEW MEDICARE TAX ON UNEARNED NET INVESTMENT INCOME Q-1: Who will be subject to the new taxes imposed in the health legislation? A: A new 3.8% tax will apply to the unearned income of High Income taxpayers.

NEW MEDICARE TAX ON UNEARNED NET INVESTMENT INCOME Q-1: Who will be subject to the new taxes imposed in the health legislation? A: A new 3.8% tax will apply to the unearned income of High Income taxpayers.

WILLMS, S.C. MEMORANDUM

WILLMS, S.C. LAW FIRM MEMORANDUM TO: FROM: Clients and Friends of Willms, S.C. Maureen L. O Leary DATE: January 6, 2011 RE: Income Tax Provisions of the 2010 Tax Act In addition to the important estate

WILLMS, S.C. LAW FIRM MEMORANDUM TO: FROM: Clients and Friends of Willms, S.C. Maureen L. O Leary DATE: January 6, 2011 RE: Income Tax Provisions of the 2010 Tax Act In addition to the important estate

Multigenerational Retirement Distribution Planning. Maximizing the Family Wealth Planning Benefits of Qualified Plans and IRAs

Multigenerational Retirement Distribution Planning Maximizing the Family Wealth Planning Benefits of Qualified Plans and IRAs Overview Qualified plans, IRAs and other tax-deferred plans often constitute

Multigenerational Retirement Distribution Planning Maximizing the Family Wealth Planning Benefits of Qualified Plans and IRAs Overview Qualified plans, IRAs and other tax-deferred plans often constitute

Highlights. Tax Cuts and Jobs Act of 2017

Highlights Tax Cuts and Jobs Act of 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $9,525 $9,525 to $38,700 $9,525 to $38,700 12% $38,700 to $93,700 25% $38,700 to $82,500 22% $93,700

Highlights Tax Cuts and Jobs Act of 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $9,525 $9,525 to $38,700 $9,525 to $38,700 12% $38,700 to $93,700 25% $38,700 to $82,500 22% $93,700

Tax Bill Comparison. December 2017

Tax Bill Comparison December 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $45,000 $0 to $9,525 $9,525 to $38,700 $45,000 to $200,000 $9,325 to $38,700 $38,700 to $93,700 $200,000

Tax Bill Comparison December 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $45,000 $0 to $9,525 $9,525 to $38,700 $45,000 to $200,000 $9,325 to $38,700 $38,700 to $93,700 $200,000

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS Nicholas J. Houle CPA/PFS CFP 2010 Ag Summit Principal December, 2010 LarsonAllen Financial LLC Chicago, IL Minneapolis, MN 612-376-4760 nhoule@larsonallen.com

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS Nicholas J. Houle CPA/PFS CFP 2010 Ag Summit Principal December, 2010 LarsonAllen Financial LLC Chicago, IL Minneapolis, MN 612-376-4760 nhoule@larsonallen.com

THE NEW CONSERVATION TAX INCENTIVES. Stephen J. Small, Esq. (10/14/08)

") THE NEW CONSERVATION TAX INCENTIVES By Stephen J. Small, Esq. (10/14/08) On August 17, 2006, the President signed into law the Pension Protection Act of 2006. That law included the first major new income

THE NEW CONSERVATION TAX INCENTIVES By Stephen J. Small, Esq. (10/14/08) On August 17, 2006, the President signed into law the Pension Protection Act of 2006. That law included the first major new income

Frequently Asked Questions ENDOWMENT FUNDS

Frequently Asked Questions ENDOWMENT FUNDS 1. Do I Need a Will? Most likely. Without a will, the laws of the state will determine who will receive your assets and who will manage your estate. As a result,

Frequently Asked Questions ENDOWMENT FUNDS 1. Do I Need a Will? Most likely. Without a will, the laws of the state will determine who will receive your assets and who will manage your estate. As a result,

numer cal anal ysi shown, esul nei her guar ant ees nor ect ons, and act ual esul may gni cant Any assumpt ons est es, on, her val ues hypot het cal

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Charitable Giving Techniques

Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving, although appropriate for some,

Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving, although appropriate for some,

Comprehensive Charitable Planning

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

line of Sight Tax Transitions Navigating the Continuing Complexities of a Changing Landscape Suzanne Shier Tax Strategist

line of Sight 2012 2013 Tax Transitions Navigating the Continuing Complexities of a Changing Landscape Suzanne Shier Tax Strategist We hope you enjoy the latest presentation from Northern Trust s Line

line of Sight 2012 2013 Tax Transitions Navigating the Continuing Complexities of a Changing Landscape Suzanne Shier Tax Strategist We hope you enjoy the latest presentation from Northern Trust s Line

Charitable Planning CLIENT GUIDE

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Thursday, March WRM# TOPIC: The New Playing Field A Review of the Net Investment Income Tax and Final Regulations.

Thursday, March 27 2014 WRM# 14-12 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms. The

Thursday, March 27 2014 WRM# 14-12 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms. The

A Comparison of the 2016 Presidential Candidates Tax Proposals

A Comparison of the 2016 Presidential Candidates Tax Proposals Caveat: The plans outlined in this summary are based on each candidate s tax policy proposal. Tax positions on a candidate s website are aspirational,

A Comparison of the 2016 Presidential Candidates Tax Proposals Caveat: The plans outlined in this summary are based on each candidate s tax policy proposal. Tax positions on a candidate s website are aspirational,

e-pocket TAX TABLES 2014 and 2015 Quick Links:

e-pocket TAX TABLES 2014 and 2015 Quick Links: 2014 Income and Payroll Tax Rates 2015 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

e-pocket TAX TABLES 2014 and 2015 Quick Links: 2014 Income and Payroll Tax Rates 2015 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

Tuesday, June 20, 2017 Probate Track Rooms: Income Tax Considerations In Estate Planning 10:30 a.m. 11:00 a.m. Presented by Jessica Doro 2007

Tuesday, June 20, 2017 Probate Track Rooms: 318-320 Income Tax Considerations In Estate Planning 10:30 a.m. 11:00 a.m. Presented by Jessica Doro 2007 First Avenue SE PO Box 2804 Cedar Rapids, Iowa 52406

Tuesday, June 20, 2017 Probate Track Rooms: 318-320 Income Tax Considerations In Estate Planning 10:30 a.m. 11:00 a.m. Presented by Jessica Doro 2007 First Avenue SE PO Box 2804 Cedar Rapids, Iowa 52406

2018 Tax Planning & Reference Guide

2018 Tax Planning & Reference Guide The 2018 Tax Planning & Reference Guide is designed to be a reference only and is not intended to provide tax advice. Please consult your professional tax advisor prior

2018 Tax Planning & Reference Guide The 2018 Tax Planning & Reference Guide is designed to be a reference only and is not intended to provide tax advice. Please consult your professional tax advisor prior

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

2016 Year-End Tax-Planning Letter

Dear Clients and Friends: With a new administration taking shape in our nation s capital after the elections, you can expect that significant tax reforms will be debated, and perhaps enacted, in the near

Dear Clients and Friends: With a new administration taking shape in our nation s capital after the elections, you can expect that significant tax reforms will be debated, and perhaps enacted, in the near

TAX TIPS FOR SENIORS AND THEIR FAMILY. Presented by: Andrew H. Hook, CELA, CFP, AEP Jessica A. Hayes, Esq./ Elizabeth Q. Boehmcke, Esq.

TAX TIPS FOR SENIORS AND THEIR FAMILY Presented by: Andrew H. Hook, CELA, CFP, AEP Jessica A. Hayes, Esq./ Elizabeth Q. Boehmcke, Esq. ESTATE TAXES 2015 Estate Tax Exemption Amount: $5,430,000 per person.

TAX TIPS FOR SENIORS AND THEIR FAMILY Presented by: Andrew H. Hook, CELA, CFP, AEP Jessica A. Hayes, Esq./ Elizabeth Q. Boehmcke, Esq. ESTATE TAXES 2015 Estate Tax Exemption Amount: $5,430,000 per person.

Tax Considerations of Farm Transfers (Revised 26 February 2009)

") Tax Considerations of Farm Transfers (Revised 26 February 2009) Introduction There are alternative methods of transferring farm assets from one generation to the next. The most common methods are by sale,

Tax Considerations of Farm Transfers (Revised 26 February 2009) Introduction There are alternative methods of transferring farm assets from one generation to the next. The most common methods are by sale,

Year-End Tax Planning Letter

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F

Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F 2 0 1 7 OUR GOAL FOR TODAY Develop an awareness of the recent law changes that will affect healthcare organizations OUR GOAL FOR TODAY

Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F 2 0 1 7 OUR GOAL FOR TODAY Develop an awareness of the recent law changes that will affect healthcare organizations OUR GOAL FOR TODAY

2016 Charitable Giving Review

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

Life Estates: Planning Considerations Gifts of Homes and Farms with Retained Use

Life Estates: Planning Considerations Gifts of Homes and Farms with Retained Use We sometimes hear from friends that they intend to leave their residences, or perhaps farm property, to The First Church

Life Estates: Planning Considerations Gifts of Homes and Farms with Retained Use We sometimes hear from friends that they intend to leave their residences, or perhaps farm property, to The First Church