Presented by: Peggy Hall, Legacy Accounting and Software Training Sponsored by: KCAA (Kitsap Community and Agricultural Alliance) WSU Regional Small

|

|

|

- Margaret Griffin

- 5 years ago

- Views:

Transcription

WSU Regional")

1 Presented by: Peggy Hall, Legacy Accounting and Software Training Sponsored by: KCAA (Kitsap Community and Agricultural Alliance) WSU Regional Small Farms Program

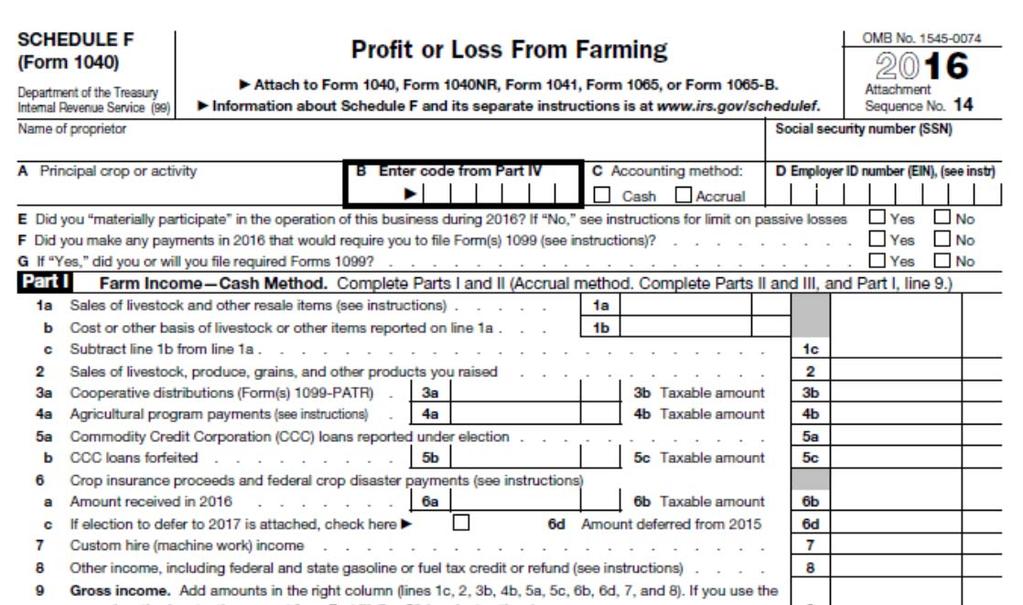

2 Useful Resources Start Up Decisions/Farm or Hobby? General Guidelines Farm Records and Tax Reports Reasons/Tips for Tracking Income and Expenses The Schedule F and Relevant Tax Forms Q&A

3 IRS Publication 225 Farmer s Tax Guide (FTG) 89 pages Examples of tax forms and Tax topic explanations Tax Guide For Owners and Operators of Small and Medium Size Farms 143 pages Penn State Ag Alternatives Understanding Your Federal Farm Income Taxes Ten Things to Know about Farm Income and Deductions - IRS Pub 51 Agricultural Employer s Tax Guide

4 Farm/Farmer IRS Definition Business of farming.cultivate, operate or manage a farm for profit..not timber A farm includes livestock, dairy, poultry, fish fruit, and truck farms, fish farms, plant nursery, orchards, plantations, ranches, greenhouses and bees. Hobby? Hobby 1040 line 21 and expenses on Schedule A - Itemized Deductions, limited to Hobby profit 9 Factors, FTG p26-27 Businesslike manner, time and effort, livelihood, change to improve profits, advisors, make profit in some year

5 Do not use Schedule F (Use Schedule C instead) Agricultural services such as soil preparation Veterinary services Farm labor services Horticulture or management for a fee or contract basis Agritourism Processing (Cheese-making, wine making and other value added processing) Rental of farm house Sale of livestock held for draft, breeding, sport, or dairy is reported on Form 4797 Sale of Business Property

6 Publication 583 Starting a Business and Keeping Records Categorize list of income and expenses (Chart of Accounts) List of Assets bought, sold or traded 1099 informational returns (received and issued) Payroll records Amount products sold Inventory Account receivable Keep records for at least 3 years from the time taxes were filed, but good idea to keep them for 5 years. Employment records should be keep longer.

7 Monitor the progress of your farming business Prepare your financial statements Obtaining and attracting capital (applying for a loan) Identify source of receipts Keep track of deductible expenses. Prepare your tax returns Support items reported on tax returns

8 Keep business and household separate have a dedicated checking account for the farm. Tip: Take a picture of receipts. Keep all farm related receipts develop a system for collecting receipts Use an accounting system paper ledgers, spreadsheets, or accounting program Two methodologies Keep accounts same as Schedule F Do whatever is comfortable for you as long as you can relate back to Schedule F

9 Book_monthly-1nyhir8.xls ($10 Download) - Other free resources

10 QuickBooks Online - $25-$40 per month depending on features - Test Drive QuickBooks Online Plus - Xero - $30-$70 per month depending on features - QuickBooks Desktop - $250 one time investment (one computer)-updates for 3 years Farm dedicated programs EasyFarm - starting at $ FarmWorks Software - $ CenterPoint Accounting for Agriculture by Red Wing - $1195 and up -

11

12 Form 3800 General Business Credits Form 4136 Credit for Federal Tax Paid on Fuel Form 4562 Depreciation and Amortization Form 4684 Casualty & Theft Loss Form 4797 Sale of Business Property Form 4835 Farm Rental Income and Expenses Form Domestic Productions Activities Deduction Form 8824 Like Kind Exchanges Schedule C Profit or Loss from Business (value added processing and agritourism) Schedule D Capital Gains and Losses Schedule SE Self-Employment Taxes Schedule J Income Averaging for Farmers & Fisherman

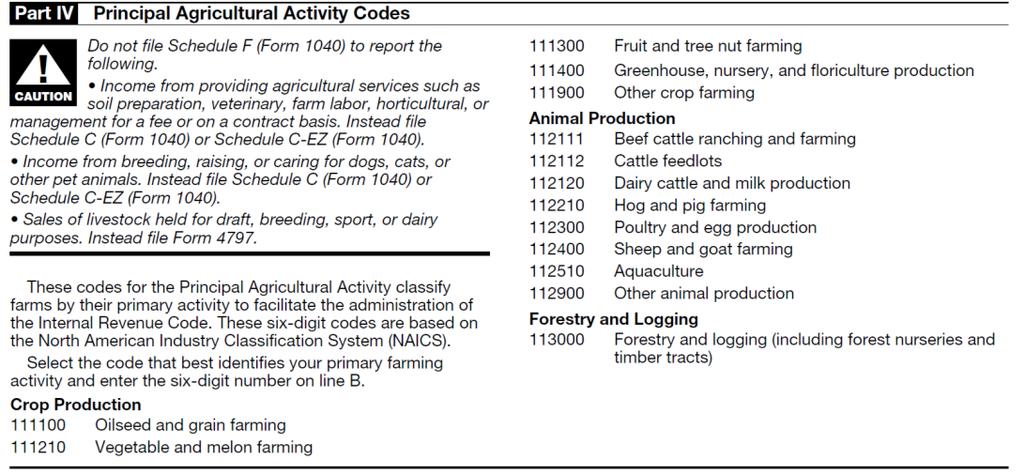

13 Box B: Use appropriate code from Part IV

14 Rent for use of real estate generally not on Schedule F but on Schedule E (Supplemental Income and Loss) Rent received for land in agricultural production is subject to SE tax of the owner materially participates in farm operation, This is reported on Schedule F line 8. Net rental income subject to SE tax is for land use NOT the rent of buildings and equipment. Rental of the buildings and equipment are reported on Schedule C. If the land owner does not materially participate in the farming activity, the tax reporting will depend on the form in which the rental payments are received. Share crop arrangements are reported on Form 4863 Farm Rental Income and Expenses.

15 Test #1 at least three of four of the following Advances, pays or stands goods for at least half of the direct costs of producing commodities Furnishes at least half of the tools, equipment and livestock used Advises and consults with tenant periodically Inspects the production periodically Test #2 - Regularly or frequently makes or takes an important role in management decisions substantially contributing to or affecting the success of the enterprise Test #3 -The land owner works hours 100 or more over a period of 5 weeks or more in activities connected with producing the farm commodities Test #4 - The land owner takes actions that considered in their total effects, show that he or she is materially and significantly involved in the production of the farm, commodities NOTE: Tax planning situation may exists and be beneficial if one spouse owns farming business and the other owns the real estate.

16

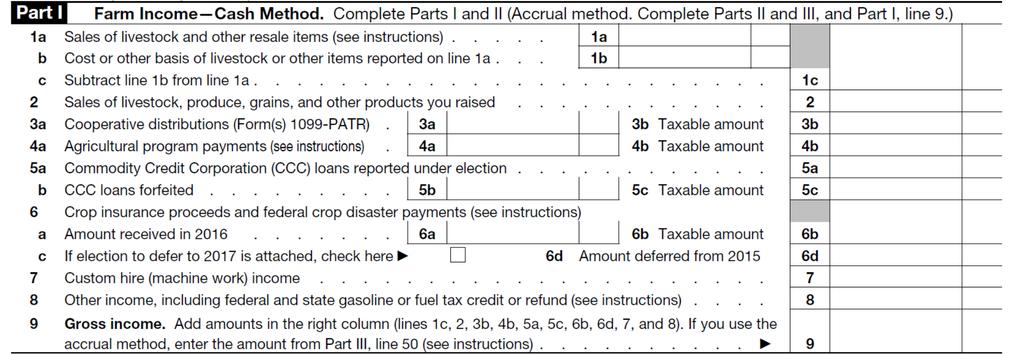

17 Line 1a Report of livestock or other products purchased for resale. 1a Sales of items 1b Basis in items 1c Proceeds from sale after removing basis Line 2 Sales of livestock, produce, grains or other product you raised including barter Line PATR payments received Line 5 CCC Loans generally not counted as income Line 6 - Crop insurance proceeds. Insurance payments from crop damage count as income. They should generally be reported the year they are received. Line 7 Custom Hire (machine work) that you or an employees preform for others or for the use of your property or machines Line 8 Other income can include Credit for Federal excise tax paid on fuels Use Form 4136 to calculate amount. This credit is for fuel for off road use of gasoline, Total *.183 tax credit. Track farm use gallons, mark receipts.

18

19

20 Profit from operating - Selling produce, providing custom hire, etc. Income Expenses = Profit Taxed at Federal and state levels Gain - From the sale of assets, such as tractors, livestock, etc. taxed at a lower rate. Must know the basis in the property. Borrowed capital or return of capital not taxable

21 Part 1 Record assets held MORE than 1 year The gain/loss is taxed at capital gain rates. Part 11 Record assets held for LESS than 1 year. Gain/Loss taxed as ordinary income. Part 111 Record sale of assets used in farming operation. Gain or loss depends on holding period.

22 Assets that you buy price, sales tax, freight, legal fees, and recording fees Assets that you trade - basis left in the traded item, (if applicable) plus the price you paid (boot) Assets given to you - You need to know what the basis was from the person that gave it to you. When, and if, you sell the asset, your basis may be the donor s basis, or the fair market value on the date of the gift. Assets inherited - Your basis is usually the fair market value of the asset on the date of death. This is called a step up in basis. Increases improvements made, usually for land which is not depreciate Decreases depreciation or Section 179 deductions

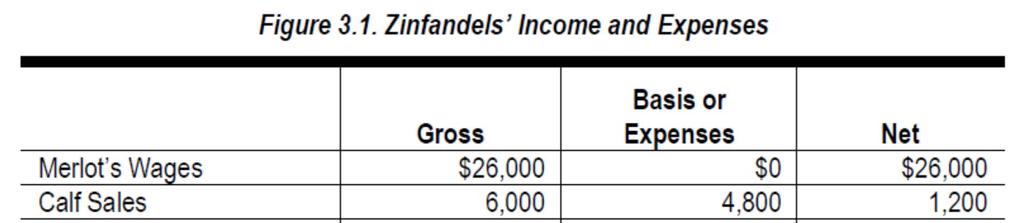

23

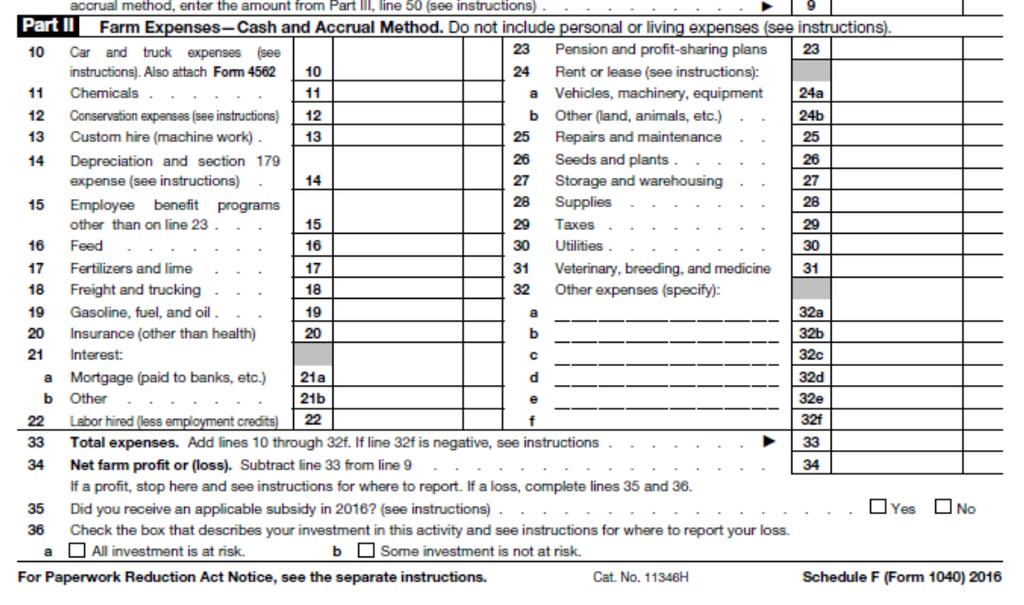

24 Cash method Pre-paid in the year which paid but limited to 50% of all farm related expenses for year. Some exceptions apply. Line 10 Also attach Form 4562 Depreciation regardless of method, See Pub 463 Travel, Entertainment, Gift, and Car Expenses for more information Track mileage (personal and farm) mileage log or GPS system (MileIQ) Standard mileage rate ($.54 per mile in 2016 $.535 in 2017) plus parking and tolls Actual Expenses gas, oil, repairs, insurance, registration, and interest Special Rule for Farms - Pub 225 page 22 - Business use percentage. You can claim 75% of the use of a car or light truck as business use without any records if you used the vehicle during most of the normal business day directly in connection with the business of farming. Lines 11, 13, 15-20, and 31 self explanatory, Line 12 Conservation expenses, NRCS, costs include treatment or movement of earth, diversion channels, ditches. Earthen dams, eradication of brush, planting of windbreaks. Fully deductible Line 14 Depreciation and Section 179 expense use to capitalize assets used in farming Line 21 Mortgage interest Allocate if you are living on the farm, use any reasonable method Chap 4 Line 22 Labor hired = You can deduct reasonable wages you paid to your farm s full and part-time workers. You must withhold Social Security, Medicare and income taxes from your employees wages. Line 29 Taxes Allocate farm property taxes using a reasonable method. Also deduct the Social Security and Medicare taxes you pay to match the amount withheld from wages of farm employees and any federal unemployment tax you pay. Line 30 Utilities Use a reasonable method to allocate farm portion of utilities paid.

25 Pub 946 How To Depreciate Property Form Depreciation and Amortization Depreciation - The using up or wearing out of equipment, breeding animals, livestock facilities, greenhouses, and storage structures. Depreciation is an expense that lowers the basis or your property over time. Useful life charts, by type of asset (3 years-tractors, 5 years-cattle, 7 years- Equipment, 10 years-ag/horticulture structures/fruit and nut trees or vines, 20 years Other Farm Buildings). Section 179 Election to expense assets in the year placed in production and not capitalize. Limit for 2016 $500,000 and can t produce a loss.

26 Schedule SE Self-Employment Taxes Short form, easy to use Tax is posted to Form 1040 Credit for 50% of the tax is posted on page 1, 1040 as adjustment to income

27 IRS Pub 51 (Circular A) - Agricultural Employer s Tax Guide Each employee must Complete Form I-9, Employment Eligibility Verification and W-4 Employee s Withholding Allowance Certificate The $150 Test or the $2,500 Test - All cash wages paid by a farmer-employer must withhold/pay social security, Medicare, state tax and Workers Comp insurance if the farmer paid (1) wages of $2,500 or more during the year to all employees or (2) an individual employee more than $150 in cash wages during the year. If the $2,500 group test isn t met, the $150 test for an employee still applies. Wages paid to children are not subject to FICA if both parents are sole proprietors or partnership in the business.

28 Form 4684 Casualty & Theft Loss Report damage, destruction, or loss of property due to identifiable event that is sudden, unexpected or unusual. Example: car, truck, tractor accident, earthquake, fires, freezing, or storms. Limitation apply. Form 8903 Domestic Production Activities Deduction - W-2 wages paid to non family employees are eligible to deduct 9% of income not to exceed 50% of W-2 wages. Schedule J Income Averaging for Farmers and Fisherman averaged for 3 years. Helpful if wide disparity of income or tax brackets over a 3 year period.

29

30

31 Merlot s wage income is reported on the front of Form The calf sales and the grape sales are both reported on Schedule F (Form 1040). Zoe s sales of grapes to the local winery are also reported on Schedule F (Form 1040), because she has not processed those grapes. Zoe s juice sales are reported on Schedule C (Form 1040), Profit or Loss From Business, because she has processed them beyond the normal stage for preparing grapes for sale from the farm.

32

33 Please consider becoming a member of the KCAA

Prepare, print, and e-file your federal tax return for free!

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com SCHEDULE F (Form 1040) Department of the Treasury Internal Revenue Service (99) Name of proprietor Profit or Loss From Farming

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com SCHEDULE F (Form 1040) Department of the Treasury Internal Revenue Service (99) Name of proprietor Profit or Loss From Farming

2002 Instructions for Schedule F, Profit or Loss From Farming

2002 Instructions for Schedule F, Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1041, 1065, or 1065-B. This activity may subject you

2002 Instructions for Schedule F, Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1041, 1065, or 1065-B. This activity may subject you

TAX ORGANIZER Page 3

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

Farm Taxes. David L. Marrison, Associate Professor

Farm Taxes David L. Marrison, Associate Professor Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax

Farm Taxes David L. Marrison, Associate Professor Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax

2017 Instructions for Schedule F

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule F Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1040NR,

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule F Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1040NR,

CHAPTER 3 FARM INCOME

MANAGING THE TIMING OF INCOME AND DEDUCTIONS CHAPTER 3 SYNPOSIS (click on section title to go directly there) Introduction... 3.2 Defining Farm and Farming... 3.2 Definition of Farm... 3.2 Definition of

MANAGING THE TIMING OF INCOME AND DEDUCTIONS CHAPTER 3 SYNPOSIS (click on section title to go directly there) Introduction... 3.2 Defining Farm and Farming... 3.2 Definition of Farm... 3.2 Definition of

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University Tax Planning

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

Total Tax If you have church employee income, see page 2 of the instructions before you begin.

Form 00-SS U.S. Self-Employment Tax Return (Including the Additional Child Tax Credit for Bona Fide Residents of Puerto Rico) Virgin Islands, Guam, American Samoa, the Commonwealth of the Northern Department

Form 00-SS U.S. Self-Employment Tax Return (Including the Additional Child Tax Credit for Bona Fide Residents of Puerto Rico) Virgin Islands, Guam, American Samoa, the Commonwealth of the Northern Department

Managerial Accounting Using QuickBooks Pro TM

Managerial Accounting Using QuickBooks Pro TM This manual is intended as a reference in furthering knowledge of management accounting for agricultural producers using QuickBooks Pro TM. Historically, agricultural

Managerial Accounting Using QuickBooks Pro TM This manual is intended as a reference in furthering knowledge of management accounting for agricultural producers using QuickBooks Pro TM. Historically, agricultural

2017 Farm Tax Organizer Gurr & Company LLC

2017 Farm Tax Organizer Gurr & Company LLC Here is your tax organizer to assist you in gathering the information necessary information for your Schedule F "Farm" tax return for 2017. The Internal Revenue

2017 Farm Tax Organizer Gurr & Company LLC Here is your tax organizer to assist you in gathering the information necessary information for your Schedule F "Farm" tax return for 2017. The Internal Revenue

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P.

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P. INCOME WORKSHEET SALES/COSTS OF LIVESTOCK PURCHASED FOR RESALE: Sold Proceeds Bought Cost Net Calves/fat cattle $ $ $ Calves/fat cattle

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P. INCOME WORKSHEET SALES/COSTS OF LIVESTOCK PURCHASED FOR RESALE: Sold Proceeds Bought Cost Net Calves/fat cattle $ $ $ Calves/fat cattle

Farmer's Tax Guide. Contents. For use in preparing 2016 Returns. Introduction. Publication 225 Cat. No L

Department of the Treasury Internal Revenue Service Publication 225 Cat. No. 11049L Farmer's Tax Guide For use in preparing 2016 Returns Acknowledgment: The valuable advice and assistance given us each

Department of the Treasury Internal Revenue Service Publication 225 Cat. No. 11049L Farmer's Tax Guide For use in preparing 2016 Returns Acknowledgment: The valuable advice and assistance given us each

Farm/Ranch Accounting and Tax 101

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Farm/Ranch Accounting and Tax 101 Randy Netek, CPA & Brandt Self, CPA May 2018 CLAconnect.com The Agenda Tax Reform Basics of Accounting Documentation

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Farm/Ranch Accounting and Tax 101 Randy Netek, CPA & Brandt Self, CPA May 2018 CLAconnect.com The Agenda Tax Reform Basics of Accounting Documentation

PERSONAL TAX INFORMATION WORKSHEET

PERSONAL TAX INFORMATION WORKSHEET Please check the appropriate box: Date Received: I need my taxes done early for my child s financial aid. Most of the information needed to complete this form can be

PERSONAL TAX INFORMATION WORKSHEET Please check the appropriate box: Date Received: I need my taxes done early for my child s financial aid. Most of the information needed to complete this form can be

2017 TAX PROFORMA/ORGANIZER

2017 TAX PROFORMA/ORGANIZER This Tax Proforma/Organizer package was designed to assist you in collecting the information we need for the preparation of your 2017 income tax return. The following pages

2017 TAX PROFORMA/ORGANIZER This Tax Proforma/Organizer package was designed to assist you in collecting the information we need for the preparation of your 2017 income tax return. The following pages

Cattle Enterprise Tax and Financial Management

Cattle Enterprise Tax and Financial Management T. Bryant, CPA 1 1 Senior Tax Partner, Beasley, Bryant & Company, CPA s, P.A. Owner/Operator, Overkill Hill Farms, LLC I. Current tax situation for farmers

Cattle Enterprise Tax and Financial Management T. Bryant, CPA 1 1 Senior Tax Partner, Beasley, Bryant & Company, CPA s, P.A. Owner/Operator, Overkill Hill Farms, LLC I. Current tax situation for farmers

Tax Return Questionnaire Tax Year

Tax Return Questionnaire - 2018 Tax Year - Page 1 of 18 Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money and help

Tax Return Questionnaire - 2018 Tax Year - Page 1 of 18 Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money and help

Tax Return Questionnaire Tax Year

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

TAX REPORTING AND PAYMENT

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

2017 Farm Income Tax Webinar

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

Balance Sheet and Schedules

Balance Sheet and Schedules CURRENT ASSET SCHEDULE DOLLAR VALUE CASH AND EQUIVALENTS A $ MARKETABLE EQUITIES B $ ACCOUNTS RECEIVABLE C $ MARKET LIVESTOCK $ PRODUCE OR BY-PRODUCTS $ CROP INVENTORY D $ CROP

Balance Sheet and Schedules CURRENT ASSET SCHEDULE DOLLAR VALUE CASH AND EQUIVALENTS A $ MARKETABLE EQUITIES B $ ACCOUNTS RECEIVABLE C $ MARKET LIVESTOCK $ PRODUCE OR BY-PRODUCTS $ CROP INVENTORY D $ CROP

Allen L. Kockler Company 2018 Tax Organizer

Client Information: Returning Client New Client If a new client, please bring a copy of your 2017 tax return 2017 Preparer Allen Kockler Jon Augustus Mark Moore Taxpayer Name Spouse Name Taxpayer DOB Spouse

Client Information: Returning Client New Client If a new client, please bring a copy of your 2017 tax return 2017 Preparer Allen Kockler Jon Augustus Mark Moore Taxpayer Name Spouse Name Taxpayer DOB Spouse

Tax Organizer For 2014 Income Tax Return

Prepared By: Tax Organizer For 2014 Income Tax Return Prepared For: This Tax Organizer can be used to help identify information needed to prepare your 2014 income tax return. Enter your 2014 tax information

Prepared By: Tax Organizer For 2014 Income Tax Return Prepared For: This Tax Organizer can be used to help identify information needed to prepare your 2014 income tax return. Enter your 2014 tax information

Income Tax Organizer

Income Tax Organizer 1200 W. Cherry Lane, Suite 100 Meridian, ID 83642 208-888-6501 office 866-408-1836 fax 1. Personal Information Roberts Hart and Company, CPA's Income Tax Organizer Taxpayer Last Name

Income Tax Organizer 1200 W. Cherry Lane, Suite 100 Meridian, ID 83642 208-888-6501 office 866-408-1836 fax 1. Personal Information Roberts Hart and Company, CPA's Income Tax Organizer Taxpayer Last Name

2017 Conversion Instructions TaxACT to ATX Individual

Updated 08/27/2017 2017 Conversion Instructions TaxACT to ATX Individual TaxACT is a registered trademark of 2nd Story Software, Inc.2nd Story Software, Inc. does not sanction nor participate in this conversion

Updated 08/27/2017 2017 Conversion Instructions TaxACT to ATX Individual TaxACT is a registered trademark of 2nd Story Software, Inc.2nd Story Software, Inc. does not sanction nor participate in this conversion

Please also attach copies of your individual income tax returns for the past two years. About you: Name (First, MI, Last): Taxpayer Social Security #

: Taxpayer Social Security #") JOHN D. GALLO, C.P.A., LLC CERTIFIED PUBLIC ACCOUNTANT 2500 EAST 168TH AVENUE BRIGHTON, COLORADO 80602 (303) 817-7855 www.johngallocpa.com email: john@johngallocpa.com Organizer for individual income tax

JOHN D. GALLO, C.P.A., LLC CERTIFIED PUBLIC ACCOUNTANT 2500 EAST 168TH AVENUE BRIGHTON, COLORADO 80602 (303) 817-7855 www.johngallocpa.com email: john@johngallocpa.com Organizer for individual income tax

OHIO STATE UNIVERSITY EXTENSION. OSU EXTENSION TAXATION PROGRAM January 2014

OHIO STATE UNIVERSITY EXTENSION Tax Bulletin OSU EXTENSION TAXATION PROGRAM January 2014 FUEL TAX CREDITS AND REFUNDS FOR FARMERS INTRODUCTION Farming can be a fuel- intensive business. Both the federal

OHIO STATE UNIVERSITY EXTENSION Tax Bulletin OSU EXTENSION TAXATION PROGRAM January 2014 FUEL TAX CREDITS AND REFUNDS FOR FARMERS INTRODUCTION Farming can be a fuel- intensive business. Both the federal

2017 TAX ORGANIZER F R O M T O

F R O M TAX ORGANIZER T O I (We) have submitted this information for the sole purpose of preparing my (our) tax return(s). Each item can be substantiated by receipts, canceled checks or other documents.

F R O M TAX ORGANIZER T O I (We) have submitted this information for the sole purpose of preparing my (our) tax return(s). Each item can be substantiated by receipts, canceled checks or other documents.

A. Scott Colby, PC Tax Organizer

A. Scott Colby, PC Tax Organizer ***YOU MUST DOWNLOAD THIS ORGANIZER TO YOUR COMPUTER AND OPEN IT IN ADOBE SOFTWARE BEFORE FILLING OUT ANY INFORMATION OR ELSE YOUR INFORMATION WILL NOT BE SAVED.*** ***DO

A. Scott Colby, PC Tax Organizer ***YOU MUST DOWNLOAD THIS ORGANIZER TO YOUR COMPUTER AND OPEN IT IN ADOBE SOFTWARE BEFORE FILLING OUT ANY INFORMATION OR ELSE YOUR INFORMATION WILL NOT BE SAVED.*** ***DO

ROLAND & DIELEMAN 2018 TAX WORKSHEET

ROLAND & DIELEMAN 2018 TAX WORKSHEET FARM 808 4 TH Ave. Grinnell, IA 50112 (641) 236-6558 126 West 3 rd Street Tama, IA 52339 (641) 484-2970 (Grinnell) (641) 484-5622 (Mon./Sat.) 612 4 th St. Sully, IA

ROLAND & DIELEMAN 2018 TAX WORKSHEET FARM 808 4 TH Ave. Grinnell, IA 50112 (641) 236-6558 126 West 3 rd Street Tama, IA 52339 (641) 484-2970 (Grinnell) (641) 484-5622 (Mon./Sat.) 612 4 th St. Sully, IA

2015 ProSystem Tax Line Conversion Chart by Input Form. Individual. January 2015

2015 ProSystem Conversion Chart by Input Form Individual January 2015 The following chart provides Individual tax line conversion data sorted by form and box number. te: CCH ProSystem fx allows tax lines

2015 ProSystem Conversion Chart by Input Form Individual January 2015 The following chart provides Individual tax line conversion data sorted by form and box number. te: CCH ProSystem fx allows tax lines

Record Keeping 101. Small and Beginning Farmers Workshop Milledgeville, GA February Ag & Applied Economics

Record Keeping 101 Small and Beginning Farmers Workshop Milledgeville, GA February 2014 Overview of Today Why keep records Production records Financial records Five easy steps to record keeping Schedule

Record Keeping 101 Small and Beginning Farmers Workshop Milledgeville, GA February 2014 Overview of Today Why keep records Production records Financial records Five easy steps to record keeping Schedule

Tax Organizer For 2017 Income Tax Return

Tax Organizer For 2017 Income Tax Return Prepared For:,,, Prepared By: Strategic Tax & Accounting LLC 3650 Canton Road Marietta, GA 30066 This Tax Organizer can be used to help identify information needed

Tax Organizer For 2017 Income Tax Return Prepared For:,,, Prepared By: Strategic Tax & Accounting LLC 3650 Canton Road Marietta, GA 30066 This Tax Organizer can be used to help identify information needed

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

INCOME TAX CHECKLIST TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE

INCOME TAX CHECKLIST All last names must match the name listed on the Social Security Card. TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE TELEPHONE

INCOME TAX CHECKLIST All last names must match the name listed on the Social Security Card. TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE TELEPHONE

Miscellaneous Information

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

2011 ProSystem Tax Line Conversion Chart by Input Form. Individual. November 2011

2011 ProSystem Conversion Chart by Input Form Individual vember 2011 The following chart provides Individual tax line conversion data sorted by form and box number. te: ProSystem FX allows tax lines to

2011 ProSystem Conversion Chart by Input Form Individual vember 2011 The following chart provides Individual tax line conversion data sorted by form and box number. te: ProSystem FX allows tax lines to

INCOME TAX CHECKLIST TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE

INCOME TAX CHECKLIST All last names must match the name listed on the Social Security Card TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE TELEPHONE

INCOME TAX CHECKLIST All last names must match the name listed on the Social Security Card TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE TELEPHONE

National Society of Accountants Tax Organizer for Tax Year 2012

National Society of Accountants Tax Organizer for Tax Year 2012 Compliments of: Name: Taxpayer SS No. Birthdate/Age Spouse SS No. Birthdate/Age Address: Telephone (Home) ( ) Telephone (Work) ( ) Cell Phone:

National Society of Accountants Tax Organizer for Tax Year 2012 Compliments of: Name: Taxpayer SS No. Birthdate/Age Spouse SS No. Birthdate/Age Address: Telephone (Home) ( ) Telephone (Work) ( ) Cell Phone:

Income Tax Management for Farmers in 2011

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

FARMING AND THE INCOME TAX SYSTEM IS IT A BUSINESS OR A HOBBY? Darlene Eckerman, E.A. D. Eckerman Tax Services, LLC Antigo, Wisconsin, USA

FARMING AND THE INCOME TAX SYSTEM IS IT A BUSINESS OR A HOBBY? Darlene Eckerman, E.A. D. Eckerman Tax Services, LLC Antigo, Wisconsin, USA Summary Which came first, the farm, the sheep or the dream? Do

FARMING AND THE INCOME TAX SYSTEM IS IT A BUSINESS OR A HOBBY? Darlene Eckerman, E.A. D. Eckerman Tax Services, LLC Antigo, Wisconsin, USA Summary Which came first, the farm, the sheep or the dream? Do

Disaster Losses and Related Tax Rules

Utah State University DigitalCommons@USU Rural Tax Education Archived USU Extension Publications 9-2017 Disaster Losses and Related Tax Rules JC Hobbs Oklahoma State University Follow this and additional

Utah State University DigitalCommons@USU Rural Tax Education Archived USU Extension Publications 9-2017 Disaster Losses and Related Tax Rules JC Hobbs Oklahoma State University Follow this and additional

ESTATE AND TRUST INCOME

ESTATE AND TRUST INCOME 2017 (K-1 E/T) Your 2016 K-1 information is shown below. Name of Estate, Trust If any rental real estate, are you an active participant? Name of Estate, Trust If any rental real

ESTATE AND TRUST INCOME 2017 (K-1 E/T) Your 2016 K-1 information is shown below. Name of Estate, Trust If any rental real estate, are you an active participant? Name of Estate, Trust If any rental real

Federal Income Tax on Timber

United States Department of Agriculture Forest Service FS-1007 October 2012 Federal Income Tax on Timber A Quick Guide for Woodland Owners Fourth Edition * 2012 Linda Wang, Ph.D. National Timber Tax Specialist,

United States Department of Agriculture Forest Service FS-1007 October 2012 Federal Income Tax on Timber A Quick Guide for Woodland Owners Fourth Edition * 2012 Linda Wang, Ph.D. National Timber Tax Specialist,

National Society of Accountants Tax Organizer for Tax Year 2018

National Society of Accountants Tax Organizer for Tax Year 2018 Compliments of: Are you Are interested you interested IRS in account IRS monitoring? Yes No Name: Taxpayer SS No. Birthdate/Age Spouse SS

National Society of Accountants Tax Organizer for Tax Year 2018 Compliments of: Are you Are interested you interested IRS in account IRS monitoring? Yes No Name: Taxpayer SS No. Birthdate/Age Spouse SS

Miscellaneous Information

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

2014 Conversion Instructions UltraTax 1040 to TaxWise

2014 Conversion Instructions UltraTax 1040 to TaxWise Important Notice Please Read!!! The data contained in these returns is minimal and contains ONLY the items needed to pass through to the 2014 return.

2014 Conversion Instructions UltraTax 1040 to TaxWise Important Notice Please Read!!! The data contained in these returns is minimal and contains ONLY the items needed to pass through to the 2014 return.

Business Income. Pub 4012 Tab D Pub 4491 Lesson 10

Business Income Pub 4012 Tab D Pub 4491 Lesson 10 Business Determination There are 3 choices 1. A business 2. Income producing, but not a business 3. Not entered into for profit (e.g. hobby) 2 A Business

Business Income Pub 4012 Tab D Pub 4491 Lesson 10 Business Determination There are 3 choices 1. A business 2. Income producing, but not a business 3. Not entered into for profit (e.g. hobby) 2 A Business

Individual Items to Note (1040)

") Individual Items to Note (1040) Items to Note This list provides details about how ProSeries converts the following 1040 calculated carryovers. The 2015 converted client file is not intended to duplicate

Individual Items to Note (1040) Items to Note This list provides details about how ProSeries converts the following 1040 calculated carryovers. The 2015 converted client file is not intended to duplicate

Individual Items to Note (1040)

") Individual Items to Note (1040) Items to Note This list provides details about how ProSeries converts the following 1040 calculated carryovers. The 2013 converted client file is not intended to duplicate

Individual Items to Note (1040) Items to Note This list provides details about how ProSeries converts the following 1040 calculated carryovers. The 2013 converted client file is not intended to duplicate

Agricultural & Natural Resource Issues Chapter 10 pp National Income Tax Workbook

Agricultural & Natural Resources Tax Issues Chris Bruynis David Marrison Barry Ward Associate Professor Associate Professor Assistant Professor bruynis.1@osu.edu marrison.2@osu.edu ward.8@osu.edu 740-702-3200

Agricultural & Natural Resources Tax Issues Chris Bruynis David Marrison Barry Ward Associate Professor Associate Professor Assistant Professor bruynis.1@osu.edu marrison.2@osu.edu ward.8@osu.edu 740-702-3200

OTHER TOOLS TO MANAGE TAX LIABILITY

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

TAX ORGANIZER. If you answer 'Yes' to any of the General Business and Investment questions, please provide detailed information with your answer.

TAX ORGANIZER Enclosed is your Tax Organizer for tax year 2012. Your Organizer contains several sections that include common expenses and deductions that many taxpayers overlook. Please review these sections

TAX ORGANIZER Enclosed is your Tax Organizer for tax year 2012. Your Organizer contains several sections that include common expenses and deductions that many taxpayers overlook. Please review these sections

US Topical Index

2010 1040 US Topical Index Page 1 TOPIC FORM Adoption expenses........................... 37 Alimony paid................................. 24 Alimony received............................. 14.1 Business

2010 1040 US Topical Index Page 1 TOPIC FORM Adoption expenses........................... 37 Alimony paid................................. 24 Alimony received............................. 14.1 Business

Grassfed Beef Ranch QuickBooks Setup Accounts

Grassfed Beef Ranch QuickBooks Setup Accounts The business accounting system first must provide the data for compliance reporting following the expense accounts in the Internal Revenue (IRS) Tax Profit

Grassfed Beef Ranch QuickBooks Setup Accounts The business accounting system first must provide the data for compliance reporting following the expense accounts in the Internal Revenue (IRS) Tax Profit

Farm Tax Update 1/21/2019. Teaching Objectives. Circular 230 Disclosure. Thank You Farmers Tax Guide

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Common Deductions For Business Owners

Common Deductions For Business Owners Within the day-to-day life of your small business, you will incur ordinary and necessary expenses that you can deduct when filing your taxes. So what does that mean?

Common Deductions For Business Owners Within the day-to-day life of your small business, you will incur ordinary and necessary expenses that you can deduct when filing your taxes. So what does that mean?

FARM LIABILITY APPLICATION APPLICANT INFORMATION SECTION

FARM LIABILITY APPLICATION Renewal of # APPLICANT INFORMATION SECTION Date: Producer: : Underwriter: Producer Contact: Producer Phone # Producer FAX # Producer Code Producer Email: Farm or General Liability

FARM LIABILITY APPLICATION Renewal of # APPLICANT INFORMATION SECTION Date: Producer: : Underwriter: Producer Contact: Producer Phone # Producer FAX # Producer Code Producer Email: Farm or General Liability

AGROFORESTRY IN ACTION

AGROFORESTRY IN ACTION AF1004-2007 Tax Considerations for the Establishment of Agroforestry Practices by Larry D. Godsey, Economist, University of Missouri Center for Agroforestry Agroforestry is an integrated

AGROFORESTRY IN ACTION AF1004-2007 Tax Considerations for the Establishment of Agroforestry Practices by Larry D. Godsey, Economist, University of Missouri Center for Agroforestry Agroforestry is an integrated

1040 U.S. Individual Income Tax Return 2011

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 211 m OMB. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 211,

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 211 m OMB. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 211,

STANDARDIZED PERFORMANCE ANALYSIS

STANDARDIZED PERFORMANCE ANALYSIS SPA-6 COW-CALF ENTERPRISE FINANCIAL PERFORMANCE MEASURES WORKSHEET (SPA-FCC) * 6-16-06 SPA is a standardized cow-calf enterprise production and financial performance analysis

STANDARDIZED PERFORMANCE ANALYSIS SPA-6 COW-CALF ENTERPRISE FINANCIAL PERFORMANCE MEASURES WORKSHEET (SPA-FCC) * 6-16-06 SPA is a standardized cow-calf enterprise production and financial performance analysis

National Society of Accountants Tax Organizer for Tax Year 2017

National Society of Accountants Tax Organizer for Tax Year 2017 Compliments of: Berman and Sons, LTD Accountants and Consultants Name: Taxpayer SS No. Birthdate/Age Spouse SS No. Birthdate/Age Address:

National Society of Accountants Tax Organizer for Tax Year 2017 Compliments of: Berman and Sons, LTD Accountants and Consultants Name: Taxpayer SS No. Birthdate/Age Spouse SS No. Birthdate/Age Address:

Timber Taxation. Why forestry is unique. Dr. Tamara L. Cushing Diboll, TX February 7, 2017

Timber Taxation Dr. Tamara L. Cushing Diboll, TX February 7, 2017 Why forestry is unique O Is it agriculture? O Long-time horizon O Spread-out cash flows O Derived demand O Location dependent 1 What do

Timber Taxation Dr. Tamara L. Cushing Diboll, TX February 7, 2017 Why forestry is unique O Is it agriculture? O Long-time horizon O Spread-out cash flows O Derived demand O Location dependent 1 What do

US Client Information 1

2009 1040 US Client Information 1 Page 1 Soukup, Bush & Associates, PC 2032 Caribou Drive, Suite 200 Fort Collins, CO 80525 Telephone number: (970) 223-2727 Fax number: (970) 226-0813 E-mail address: jenny@soukupbush.com

2009 1040 US Client Information 1 Page 1 Soukup, Bush & Associates, PC 2032 Caribou Drive, Suite 200 Fort Collins, CO 80525 Telephone number: (970) 223-2727 Fax number: (970) 226-0813 E-mail address: jenny@soukupbush.com

Tax Tips, Strategies and Opportunities for Progressive Farmers. Franklin H. Famme, CPA, CA

Tax Tips, Strategies and Opportunities for Progressive Farmers Franklin H. Famme, CPA, CA «The only thing raised successfully on this farm last year was taxes!» Topics What is Farming? General Tax Tips

Tax Tips, Strategies and Opportunities for Progressive Farmers Franklin H. Famme, CPA, CA «The only thing raised successfully on this farm last year was taxes!» Topics What is Farming? General Tax Tips

Economic Assistance and Employment Supports Division. Self-Employment Guide A resource for SNAP and Cash Programs

Economic Assistance and Employment Supports Division Self-Employment Guide A resource for SNAP and Cash Programs SE 01.0 Introduction... 3 SE 02.0 Definition of a self-employed person... 3 SE 03.0 Self-employment

Economic Assistance and Employment Supports Division Self-Employment Guide A resource for SNAP and Cash Programs SE 01.0 Introduction... 3 SE 02.0 Definition of a self-employed person... 3 SE 03.0 Self-employment

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

2018 Tax Organizer Personal and Dependent Information

Tax Organizer Personal and Dependent Information Personal Information Name SSN Date of birth Healthcare coverage ALL year Taxpayer Spouse Street address, city, state, and ZIP Occupation Daytime phone Evening

Tax Organizer Personal and Dependent Information Personal Information Name SSN Date of birth Healthcare coverage ALL year Taxpayer Spouse Street address, city, state, and ZIP Occupation Daytime phone Evening

Developing a Cash Flow Plan

Oklahoma Cooperative Extension Service AGEC-751 Developing a Cash Flow Plan Damona G. Doye Extension Economist and Professor A cash flow plan is a recorded projection of the amount and timing of all cash

Oklahoma Cooperative Extension Service AGEC-751 Developing a Cash Flow Plan Damona G. Doye Extension Economist and Professor A cash flow plan is a recorded projection of the amount and timing of all cash

Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

US Client Information 1

1040 US Client Information 1 Page 6 Russell CPAs 5530 Birdcage Street, Suite 105 Citrus Heights, CA 95610 Telephone number: Fax number: E-mail address: (916) 966-9366 (916) 966-8743 Chad@RussellCPAs.com

1040 US Client Information 1 Page 6 Russell CPAs 5530 Birdcage Street, Suite 105 Citrus Heights, CA 95610 Telephone number: Fax number: E-mail address: (916) 966-9366 (916) 966-8743 Chad@RussellCPAs.com

JOYNER, KIRKHAM, KEEL & ROBERTSON, P.C INDIVIDUAL TAX ORGANIZER

Please provide a copy of your 2013 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Your Name SS# Occupation Birth Date Spouse

Please provide a copy of your 2013 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Your Name SS# Occupation Birth Date Spouse

IC Chapter 8. Employment Defined

IC 22-4-8 Chapter 8. Employment Defined IC 22-4-8-1 Definition Sec. 1. (a) "Employment," subject to the other provisions of this section, means service, including service in interstate commerce performed

IC 22-4-8 Chapter 8. Employment Defined IC 22-4-8-1 Definition Sec. 1. (a) "Employment," subject to the other provisions of this section, means service, including service in interstate commerce performed

Session 5: Financial Management

Session 5: Financial Management Session 4: Enterprise Budget Develop enterprise budget Decide on Production System How did they decide on pricing Where will they market Fixed cost Revenue = Price X Quantity

Session 5: Financial Management Session 4: Enterprise Budget Develop enterprise budget Decide on Production System How did they decide on pricing Where will they market Fixed cost Revenue = Price X Quantity

Miscellaneous Information

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Promoting Innovation in Maryland Agricultural and Resource-Based Business. * Now includes financing for tree fruit orchards and hopyards *

Promoting Innovation in Maryland Agricultural and Resource-Based Business Application for the Maryland Vineyard Planting Loan Fund * Now includes financing for tree fruit orchards and hopyards * Program

Promoting Innovation in Maryland Agricultural and Resource-Based Business Application for the Maryland Vineyard Planting Loan Fund * Now includes financing for tree fruit orchards and hopyards * Program

2017 JAMES J. TOWEY, P.C. Information Summarizer for Self Employed

2017 JAMES J. TOWEY, P.C. Information Summarizer for Self Employed 11555 Beamer Road, Ste. 100 Houston, TX 77089 (281)484-5561 (Tel.) (281)481-0987 (Fax) pcjjt76@gmail.com www.jamesjtoweycpa.com CLIENT:

2017 JAMES J. TOWEY, P.C. Information Summarizer for Self Employed 11555 Beamer Road, Ste. 100 Houston, TX 77089 (281)484-5561 (Tel.) (281)481-0987 (Fax) pcjjt76@gmail.com www.jamesjtoweycpa.com CLIENT:

Miscellaneous Information

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

US Topical Index

2010 1040 US Topical Index TOPIC FORM Adoption expenses........................... 37 Alimony paid................................. 24 Alimony received............................. 14.1 Business income

2010 1040 US Topical Index TOPIC FORM Adoption expenses........................... 37 Alimony paid................................. 24 Alimony received............................. 14.1 Business income

Rental Real Estate Deductions

Rental Real Estate Deductions 15 th Edition Stephen Fishman, J.D. Chapter 1 Tax Deduction Basics for Landlords... 1 Learning Objectives... 1 Introduction... 1 How Landlords Are Taxed... 1 Income Taxes

Rental Real Estate Deductions 15 th Edition Stephen Fishman, J.D. Chapter 1 Tax Deduction Basics for Landlords... 1 Learning Objectives... 1 Introduction... 1 How Landlords Are Taxed... 1 Income Taxes

Federal Income Tax on Timber

United States Department of Agriculture Forest Service FS-1007 October 2012 Federal Income Tax on Timber A Quick Guide for Woodland Owners Fourth Edition 2012 United States Department of Agriculture Forest

United States Department of Agriculture Forest Service FS-1007 October 2012 Federal Income Tax on Timber A Quick Guide for Woodland Owners Fourth Edition 2012 United States Department of Agriculture Forest

BYRT CPAs, LLC Tax Organizer

BYRT CPAs, LLC 2017 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

BYRT CPAs, LLC 2017 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

1040 US Tax Organizer

1040 US Tax Organizer Page 1 Please enter all pertinent information. If you have attached a government form for an item, check the box and do not enter a amount. WAGES, SALARIES AND TIPS Employer name:

1040 US Tax Organizer Page 1 Please enter all pertinent information. If you have attached a government form for an item, check the box and do not enter a amount. WAGES, SALARIES AND TIPS Employer name:

Miscellaneous Information

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

TRANSFER OF FARM ASSETS

TRANSFER OF FARM ASSETS Issue 1: Buying and Selling Farmland pp. 87-89 Cost Basis Purchase [IRC 1012] Paid in: cash, debt or other Gift [IRC 1015] Generally donor s basis Issue 1: Buying and Selling Farmland

TRANSFER OF FARM ASSETS Issue 1: Buying and Selling Farmland pp. 87-89 Cost Basis Purchase [IRC 1012] Paid in: cash, debt or other Gift [IRC 1015] Generally donor s basis Issue 1: Buying and Selling Farmland

Miscellaneous Information

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

BYRT CPAs, LLC Tax Organizer

BYRT CPAs, LLC 2016 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

BYRT CPAs, LLC 2016 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

COMPREHENSIVE TAX COURSE

COMPREHENSIVE TAX COURSE Course Topics by Module - LEARNING OBJECTIVES Module 1 Chapter 1: General Material Determine who should file a return. Identify what filing status the taxpayer should use. Determine

COMPREHENSIVE TAX COURSE Course Topics by Module - LEARNING OBJECTIVES Module 1 Chapter 1: General Material Determine who should file a return. Identify what filing status the taxpayer should use. Determine

KEIR EDUCATIONAL RESOURCES

INCOME TAX PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

INCOME TAX PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

Miscellaneous Information

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

Developing a Cash Flow Plan

Developing a Cash Flow Plan Oklahoma Cooperative Extension Service Division of Agricultural Sciences and Natural Resources F-751 Damona G. Doye Extension Economist and Professor Acash flow plan is a recorded

Developing a Cash Flow Plan Oklahoma Cooperative Extension Service Division of Agricultural Sciences and Natural Resources F-751 Damona G. Doye Extension Economist and Professor Acash flow plan is a recorded

AGRICULTURAL TAX. i n c o m e t a x e s

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

1040 US Miscellaneous Questions

1040 US Miscellaneous Questions Page 1 If any of the following items pertain to you or your spouse for, please check the appropriate box and provide additional information if necessary. YES NO PERSONAL

1040 US Miscellaneous Questions Page 1 If any of the following items pertain to you or your spouse for, please check the appropriate box and provide additional information if necessary. YES NO PERSONAL

social security number relationship to you Add numbers on d Total number of exemptions claimed... lines above

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

1040 US Client Information 1

Page 1 1040 US Client Information 1 JONES ACCOUNTING ASSOCIATES 1199 SE DOCK ST OAK HARBOR WA 98277-4067 Telephone number: Fax number: E-mail address: (360) 675-3030 (360) 675-0618 jaoffice@kjonesinc.com

Page 1 1040 US Client Information 1 JONES ACCOUNTING ASSOCIATES 1199 SE DOCK ST OAK HARBOR WA 98277-4067 Telephone number: Fax number: E-mail address: (360) 675-3030 (360) 675-0618 jaoffice@kjonesinc.com

Baldwin CPAs, PLLC 713 West Main Street Richmond, Kentucky

Baldwin CPAs, PLLC 713 West Main Street Richmond, Kentucky 40475 859-626-9040 This Tax Organizer is designed to help you gather the tax information needed to prepare your 2015 personal income tax return.

Baldwin CPAs, PLLC 713 West Main Street Richmond, Kentucky 40475 859-626-9040 This Tax Organizer is designed to help you gather the tax information needed to prepare your 2015 personal income tax return.

AGRICULTURAL FINANCIAL AND TAX PLANNING. Self Employment Tax on Ranch Related Income

AGRICULTURAL FINANCIAL AND TAX PLANNING Self Employment Tax on Ranch Related Income By Thomas J. Bryant, CPA and Ryan Beasley, CPA In last months article we mentioned a February 27, 2017, Internal Revenue

AGRICULTURAL FINANCIAL AND TAX PLANNING Self Employment Tax on Ranch Related Income By Thomas J. Bryant, CPA and Ryan Beasley, CPA In last months article we mentioned a February 27, 2017, Internal Revenue

1040 US Topical Index

1040 US Topical Index Page 1 TOPIC FORM Adoption expenses........................... 37 Alimony paid................................. 24 Alimony received............................. 14.1 Business income

1040 US Topical Index Page 1 TOPIC FORM Adoption expenses........................... 37 Alimony paid................................. 24 Alimony received............................. 14.1 Business income

SELFEMPLOYMENT. Self employment Income/Expense Tracking Worksheet. Tax strategies for the self-employed

ADVANTAXADVANTAXADVANTAX Self employment Income/Expense Tracking Worksheet (Use the worksheet below to track your income and allowable expenses by quarter to assist in deriving your net earnings and estimated

ADVANTAXADVANTAXADVANTAX Self employment Income/Expense Tracking Worksheet (Use the worksheet below to track your income and allowable expenses by quarter to assist in deriving your net earnings and estimated

Income Tax. Individual & Corporate. Revenue Impact of Exemptions

EXHIBIT F-2 Individual & Corporate Income Tax Revenue Impact of Exemptions Arkansas Tax Reform and Relief Legislative Task Force April 26, 2018 Arkansas Department of Finance and Administration Overview

EXHIBIT F-2 Individual & Corporate Income Tax Revenue Impact of Exemptions Arkansas Tax Reform and Relief Legislative Task Force April 26, 2018 Arkansas Department of Finance and Administration Overview