Tax Implications of Farm Financial Planning Decisions

|

|

|

- Edmund Woods

- 5 years ago

- Views:

Transcription

1 Tax Implications of Farm Financial Planning Decisions Kevin L. Herbel Kansas Farm Management Association Department of Agricultural Economics Kansas State University Appreciation Expressed to Rob Holcomb, EA Extension Educator, Ag. Business Management University of Minnesota FINPACK Face to Face Training American Ag Credit Salina October 2 3, 2017 Tax Implications of Farm Financial Planning Decisions Income Tax Basics Liquidation Issues Deferred Tax Issues Cancellation of Debt Bankruptcy Tax Implications of Farm Financial Planning Decisions There ARE income tax implications when financial planning with a farm family Payment of income tax is part of a profitable business over the long term it is also often part of steps taken in difficult financial situations Debt is paid off with after tax dollars Include tax advisor in the planning process Tax Implications of Farm Financial Planning Decisions Income Tax Aspects and Consequences of Financial Distress Transactions by Bryan Manny and Mark Wood business planning/financialmanagement/income tax aspects and consequences financial Risk and Profit Conference Proceedings and profitconference/previous conference proceedings/2016 risk and profitconference 1

2 Taxable income is generally one of two categories ordinary income and capital gain Ordinary Income Any income received that does not qualify as a capital gain Ordinary Farm Income Income derived from the sale of commodities, livestock, and/or custom services provided as part of the farming operation (reported on Schedule F) Tax Basis The amount of investment a taxpayer has in an asset With some items the full basis is deducted (expensed) in the year of purchase fertilizer, feed, seed, etc Used for computing gain or loss if an asset is sold Usually equals an asset s purchase price (original cost basis) less any accumulated depreciation that has been, or could have been, taken (remaining, or adjusted, tax basis) Capital Assets Anything purchased that must be depreciated (machinery, breeding livestock, buildings) Assets held until disposition but that are not depreciable (i.e. land you do not get a tax deduction when you purchase land) Assets produced on the farm and held for a sufficient time to receive capital asset treatment (i.e. raised breeding livestock) Remaining Tax Basis Portion that is not taxable when as asset is sold Depreciable assets may have: Capital Gain (amount over original cost basis) Depreciation Recapture (amount of original cost that has been depreciated is taxed as ordinary income Remaining Basis not taxed If an asset has been depreciated out, any proceeds from the sale of the asset are fully taxable Expensing (utilizing Sec 179 Expense Deduction) or bonus depreciation in year of purchase will use up basis quickly 2

3 Remaining Tax Basis With non depreciable assets (i.e. land) will usually be equal to the original cost basis of the asset May have some adjustments due to additional investment to improve the asset, partial sale, other activity Inherited capital assets have initial basis equal to the value at date of inheritance in most instances ( stepped up tax basis) Gifted capital assets have initial basis equal to that of the giver at the time of the gift Sale of Capital Assets Sale of Capital Assets are generally reported as Depreciation Recapture or Capital Gain (Reported on 4797 and Schedule D) Remaining Tax Basis Raised breeding stock have no tax basis since the cost of production have already been deducted Generally ordinary gain if held less than 24 months (cattle and horses 12 months all other livestock) If held 24 months or more (cattle and horses 12 months all other livestock), all proceeds from the sale of raised breeding stock receive capital gain treatment Depreciation Qualifying capital assets (machinery, breeding livestock, buildings, land improvements such as drainage tile) cannot be deducted as an ordinary farm expense the year that they are purchased the expense must be spread over a period of years 3

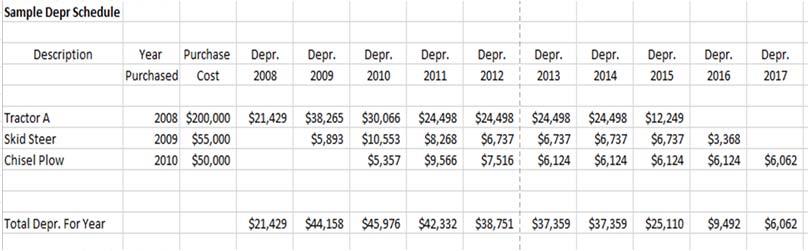

4 Depreciation Depreciation Depreciation 4

5 Wages, business income, investment income on federal tax return Rate depends upon filing status and type of entity Rates run from 10% to 39.6% currently For Kansas income taxes, rates have changed in 2017 and business income is again taxable Rental/Investment Income (Passive) Taxed at the current bracket rate Generally not subject to SE Tax Wage Income Taxed at the current bracket rate FICA and Medicare withholding on W 2 Income subject to self employment tax Farm business and Non farm business income is taxed at the current bracket rate (regular tax) Self employment tax is 15.3% (12.5 % OASDI & 2.8% Medicare) OASDI cap is $127,200 for 2017 (up from $118,500 in 2016) Long term capital gain If gain fits in the 10% or 15% = 0% If gain fits in the 25%, 28%, 33% or 35% = 15% If gain fits in the 39.6% = 20% Un recaptured 1250 gain (Buildings) Difference between accelerated and SL depr. = 25% 5

6 Installment sale of capital gain property Gain is taxable as dollars are received Land, Raised Breeding Stock Installment sale of property where there is depreciation recapture involved Immediate recognition depreciation recapture in year of sale regardless of dollars received Machinery, purchased breeding stock Income Averaging Available for Farmers and Fishermen Performed on Schedule J Federal Form 1040 Is a blending of the tax rates rather than averaging income Alternative Minimum Tax (AMT) AMT is a completely separate tax calculation Taxpayer owes the higher of the regular tax or the AMT tax Taxpayer can qualify for a credit in future years when AMT is not owed Caused by high income, large capital gains and large itemized deductions Deferred Tax Liability Deferred tax liability on a balance sheet becomes very important in a situation that may involve liquidation Many tax planning activities do not remove tax liability they just defer the liability Pre paid farm expenses and deferred sales are reconciled during a farm liquidation 6

7 Farm Liquidation Tax consequences are dramatically different from one plan to another Planning is important to understand the tax consequences of alternatives If you are working with a situation that will involve liquidation of farm property, make sure to have a tax advisor involved An estimate of the approximate tax due can be entered as an override entry in FINPACK Bankruptcy A last resort? pursue other options first The purpose of the federal bankruptcy laws enacted by congress is to provide a financial fresh start in certain circumstances through discharge of debts Generally four types Chapter 7, 11, 12 and 13 Cancellation of Debt When debt is cancelled or forgiven, the amount forgiven may be includable in taxable income. Exceptions and exclusions include: Debt is forgiven as a gift Sale is seller financed and the price is reduced which requires basis adjustment If debt is deductible (i.e. an account payable that is for a deductible item) and taxpayer uses cash method for tax filing Bankruptcy Chapter 7 Chapter 7: Liquidation Primarily will be a farmer not planning to farm in the future Debtor may be an individual, partnership, corporation or other business entity A trustee is appointed to liquidate all nonexempt assets and distribute the proceeds to creditors Bankruptcy court oversees sale of assets as well as any cancelled debt 7

8 Bankruptcy Chapter 12 Chapter 12: Reorganization Designed specifically for the reorganization of family farms (started in 1986; amended in 2005) Only available to persons who meet the definition of family farmer set forth in the statute A family farmer may be an individual, corporation or partnership Involves a reorganization plan that usually lasts 3 5 years If plan is followed, court will discharge debt agreed to in the plan Bankruptcy Chapter 11 Chapter 11: Reorganization Allows debtor to enter into an agreement with creditors under which debts are restructured to allow the debtor to continue all or part of the business operation May provide an option for those farms that are too large for Chapter 12 In general, any partnership, corporation or limited liability company except a governmental unit may be a debtor in a Chapter 11 case Bankruptcy Chapter 12 Chapter 12: Reorganization In a Chapter 12 Bankruptcy farm debt cannot exceed $4,153,150 (tied to inflation since 2005) At least 50% of the debt (excluding primary residence) must be related to the farming operation More than 50% of the gross income of an individual, or husband and wife, must have been from farming in the preceding three tax years See United States Courts website ( for further information Questions or More Information Kansas Farm Management Association (KFMA) Extension Agricultural Economics Kevin L. Herbel Waters Hall kherbel@ksu.edu Manhattan, KS

Balance Sheet-A Financial Management Tool

Balance Sheet-A Financial Management Tool Robin Reid (robinreid@ksu.edu) and Kevin Herbel (kherbel@ksu.edu) Revision of MF-291 by Dr. Michael Langemeier Kansas State University Department of Agricultural

Balance Sheet-A Financial Management Tool Robin Reid (robinreid@ksu.edu) and Kevin Herbel (kherbel@ksu.edu) Revision of MF-291 by Dr. Michael Langemeier Kansas State University Department of Agricultural

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University Tax Planning

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

Bankruptcy Questions Answered!

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

Depreciation i for tax purposes is not the same as depreciation for management decisions or

Depreciation i for tax purposes is not the same as depreciation for management decisions or accounting. Non cash event but still reduces taxable income Flexibility in calculating it Can be used to level

Depreciation i for tax purposes is not the same as depreciation for management decisions or accounting. Non cash event but still reduces taxable income Flexibility in calculating it Can be used to level

DTN University Pass It On! Farm Family Estate and Succession Planning

DTN University Pass It On! Farm Family Estate and Succession Planning Marcia Zarley Taylor, DTN Executive Editor Andy Biebl, CPA, Tax Partner, CliftonLarsonAllen LLC Nick Houle, CPA, Tax Partner, CliftonLarsonAllen

DTN University Pass It On! Farm Family Estate and Succession Planning Marcia Zarley Taylor, DTN Executive Editor Andy Biebl, CPA, Tax Partner, CliftonLarsonAllen LLC Nick Houle, CPA, Tax Partner, CliftonLarsonAllen

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS Nicholas J. Houle CPA/PFS CFP 2010 Ag Summit Principal December, 2010 LarsonAllen Financial LLC Chicago, IL Minneapolis, MN 612-376-4760 nhoule@larsonallen.com

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS Nicholas J. Houle CPA/PFS CFP 2010 Ag Summit Principal December, 2010 LarsonAllen Financial LLC Chicago, IL Minneapolis, MN 612-376-4760 nhoule@larsonallen.com

Form 4797 Chapter 3 pp Agricultural Tax Issues

Form 4797 Chapter 3 pp. 85-118 2018 Agricultural Tax Issues Form 4797 Page 85 Reporting of gains and losses on the disposition of business property. The collection point for gains and losses reported elsewhere.

Form 4797 Chapter 3 pp. 85-118 2018 Agricultural Tax Issues Form 4797 Page 85 Reporting of gains and losses on the disposition of business property. The collection point for gains and losses reported elsewhere.

Farm/Ranch Accounting and Tax 101

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Farm/Ranch Accounting and Tax 101 Randy Netek, CPA & Brandt Self, CPA May 2018 CLAconnect.com The Agenda Tax Reform Basics of Accounting Documentation

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Farm/Ranch Accounting and Tax 101 Randy Netek, CPA & Brandt Self, CPA May 2018 CLAconnect.com The Agenda Tax Reform Basics of Accounting Documentation

Income Statement-A Financial Management Tool

Income Statement-A Financial Management Tool Robin Reid (robinreid@ksu.edu) and Kevin Herbel (kherbel@ksu.edu) Revision of MF-294 by Dr. Michael Langemeier Kansas State University Department of Agricultural

Income Statement-A Financial Management Tool Robin Reid (robinreid@ksu.edu) and Kevin Herbel (kherbel@ksu.edu) Revision of MF-294 by Dr. Michael Langemeier Kansas State University Department of Agricultural

Specialty Estate Tax Seminar for Farm Families Paul Neiffer, CPA CliftonLarsonAllen, LLP

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP CLAconnect.com Specialty Estate Tax Seminar for Farm Families Paul Neiffer, CPA CliftonLarsonAllen, LLP Speaker Introduction Paul Neiffer, Principal,

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP CLAconnect.com Specialty Estate Tax Seminar for Farm Families Paul Neiffer, CPA CliftonLarsonAllen, LLP Speaker Introduction Paul Neiffer, Principal,

CORRECTED OMB No For DEBTOR S name. 3 Interest if included in box 2 4

Attention! This form is provided for informational purposes and should not be reproduced on personal computer printers by individual taxpayers for filing. The printed version of this form is a "machine

Attention! This form is provided for informational purposes and should not be reproduced on personal computer printers by individual taxpayers for filing. The printed version of this form is a "machine

Income Tax Management for Farmers in 2011

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

Questions and Answers About Farm Debt

Revised October 2003 Agdex 817-14 Questions and Answers About Farm Debt This factsheet addresses some of the common, and some not-so-common, questions asked by farmers about the legal implications of debt.

Revised October 2003 Agdex 817-14 Questions and Answers About Farm Debt This factsheet addresses some of the common, and some not-so-common, questions asked by farmers about the legal implications of debt.

TAX REPORTING AND PAYMENT

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

Agribusiness Farm Tax Seminar

Agribusiness Farm Tax Seminar Specialty Estate Tax Seminar for Farm Families Nicholas Houle, CPA, MBT Christopher Hesse, CPA December 17, 2013 CLAconnect.com Disclaimers To ensure compliance imposed by

Agribusiness Farm Tax Seminar Specialty Estate Tax Seminar for Farm Families Nicholas Houle, CPA, MBT Christopher Hesse, CPA December 17, 2013 CLAconnect.com Disclaimers To ensure compliance imposed by

Through the Crystal Ball Farm Business Structure After Tax Reform. Paul Neiffer, CPA January 26, 2017 Chicago, Illinois

Through the Crystal Ball Farm Business Structure After Tax Reform Paul Neiffer, CPA January 26, 2017 Chicago, Illinois Speaker Introduction Paul Neiffer, Principal, CliftonLarsonAllen Frequent national

Through the Crystal Ball Farm Business Structure After Tax Reform Paul Neiffer, CPA January 26, 2017 Chicago, Illinois Speaker Introduction Paul Neiffer, Principal, CliftonLarsonAllen Frequent national

OTHER TOOLS TO MANAGE TAX LIABILITY

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

Tax Planning. and. Management Considerations. for Farmers in George F. Patrick Extension Agricultural Economist Purdue University

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

Executive Compensation

Executive Compensation Bulletin IRS Issues Two Final Rules With Implications for High-Income Taxpayers Russ Hall and Steve Seelig, Towers Watson January 13, 2014 Recently, the Internal Revenue Service

Executive Compensation Bulletin IRS Issues Two Final Rules With Implications for High-Income Taxpayers Russ Hall and Steve Seelig, Towers Watson January 13, 2014 Recently, the Internal Revenue Service

Utica Shale: Federal Income Taxation for Landowners. Cleveland-Marshall College of Law September 14, 2012

Utica Shale: Federal Income Taxation for Landowners Cleveland-Marshall College of Law September 14, 2012 Presented by: James M. Rosa, CPA, PFS Lease v Sale Determining whether the transfer of an interest

Utica Shale: Federal Income Taxation for Landowners Cleveland-Marshall College of Law September 14, 2012 Presented by: James M. Rosa, CPA, PFS Lease v Sale Determining whether the transfer of an interest

The Agricultural Extension Service maintains a county farm agent in each of North Carolina s 100 counties and a home agent in 94 counties. They are as

4 meal JAN UARY, 1943 WAR SERIES EXTENSION BULLETIN, \/ HE - FARMER S INCOME TAX 1- NORTH CAROLINA STATE COLLEGE OF AGRICULTURE AND ENGINEERING OF THE UNIVERSITY OF NORTH CAROLINA AND U. 5. DEPARTMENT

4 meal JAN UARY, 1943 WAR SERIES EXTENSION BULLETIN, \/ HE - FARMER S INCOME TAX 1- NORTH CAROLINA STATE COLLEGE OF AGRICULTURE AND ENGINEERING OF THE UNIVERSITY OF NORTH CAROLINA AND U. 5. DEPARTMENT

Farm Taxes. David L. Marrison, Associate Professor

Farm Taxes David L. Marrison, Associate Professor Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax

Farm Taxes David L. Marrison, Associate Professor Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax

Understanding employer-granted stock options

Understanding employer-granted stock options Important information for option holders Employee stock options can be one of the most valuable benefits companies provide as part of a benefits package. However,

Understanding employer-granted stock options Important information for option holders Employee stock options can be one of the most valuable benefits companies provide as part of a benefits package. However,

Time is running out to make important planning moves before the year s end, so don t delay.

2015 Year-end tax planning Time is running out to make important planning moves before the year s end, so don t delay. The changes in various tax provisions brought about with the 2012 Tax Act continue

2015 Year-end tax planning Time is running out to make important planning moves before the year s end, so don t delay. The changes in various tax provisions brought about with the 2012 Tax Act continue

SUBMITTED FOR THE HEARING RECORD UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS

SUBMITTED FOR THE HEARING RECORD UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS HOW TAX REFORM WILL GROW OUR ECONOMY AND CREATE JOBS MAY 18, 2017 Submitted By: The American Farm Bureau

SUBMITTED FOR THE HEARING RECORD UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS HOW TAX REFORM WILL GROW OUR ECONOMY AND CREATE JOBS MAY 18, 2017 Submitted By: The American Farm Bureau

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

Tax Potholes and Pitfalls

Tax Potholes And Pitfalls January 31, 2013 Paul Neiffer, CPA 1 1 Agenda Background on CLA and other items. Update on the New Tax Laws Tax Potholes and Pitfalls Crop Insurance Tax Planning for 2012/13.

Tax Potholes And Pitfalls January 31, 2013 Paul Neiffer, CPA 1 1 Agenda Background on CLA and other items. Update on the New Tax Laws Tax Potholes and Pitfalls Crop Insurance Tax Planning for 2012/13.

Agricultural Business Management

Agricultural Business Management Farm Legal Series Phillip L. Kunkel, Jeffrey A. Peterson, P. Jason Thibodeaux, Dorraine Larison, Matthew Webster, Betsy Whitlatch, S. Scott Wick, Kathi J. Wright Attorneys,

Agricultural Business Management Farm Legal Series Phillip L. Kunkel, Jeffrey A. Peterson, P. Jason Thibodeaux, Dorraine Larison, Matthew Webster, Betsy Whitlatch, S. Scott Wick, Kathi J. Wright Attorneys,

Ag Income Tax Update for Farm Families

Ag Income Tax Update for Farm Families Agricultural Business Management C. Robert Holcomb, EA, Gary A. Hachfeld, Extension Educators Revised 4/2016 Topic Table of Contents Page Depreciation...1 Tangible

Ag Income Tax Update for Farm Families Agricultural Business Management C. Robert Holcomb, EA, Gary A. Hachfeld, Extension Educators Revised 4/2016 Topic Table of Contents Page Depreciation...1 Tangible

Ag Income Tax Update for Farm Families

Ag Income Tax Update for Farm Families Agricultural Business Management C. Robert Holcomb, EA, Gary A. Hachfeld, Extension Educators 12/2015 Topic Table of Contents Page Depreciation... 1 Tangible Property

Ag Income Tax Update for Farm Families Agricultural Business Management C. Robert Holcomb, EA, Gary A. Hachfeld, Extension Educators 12/2015 Topic Table of Contents Page Depreciation... 1 Tangible Property

Corporate Taxes. Standard Deduction: Estate & Trust Tax Rates

WEALTH ADVISORY OUTSOURCING AUDIT, TAX, AND CONSULTING Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor How Tax Reform Affects

WEALTH ADVISORY OUTSOURCING AUDIT, TAX, AND CONSULTING Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor How Tax Reform Affects

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

Updates to 2015 edition of Conservation Options: A Landowner s Guide to Conserving Your Land for Future Generations

Updates to 2015 edition of Conservation Options: A Landowner s Guide to Conserving Your Land for Future Generations In a great victory for landowners interested in conservation, Congress and the president

Updates to 2015 edition of Conservation Options: A Landowner s Guide to Conserving Your Land for Future Generations In a great victory for landowners interested in conservation, Congress and the president

Willie and Annette Jump (Example 3.1)

") agreement, check here Part II Explanation of Changes to Income, Deductions, and Credits Enter the line number from the front of the form for each item you are changing and give the reason for each change.

agreement, check here Part II Explanation of Changes to Income, Deductions, and Credits Enter the line number from the front of the form for each item you are changing and give the reason for each change.

TAX ORGANIZER Page 3

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

Estate Planning What Do We Need to Know Now? Stacy Hambelton Agriculture Business Specialist Gainesville, MO

Estate Planning What Do We Need to Know Now? Stacy Hambelton Agriculture Business Specialist Gainesville, MO Retirement and Estate Planning Issues Men (farmers in particular) don t plan for their retirement

Estate Planning What Do We Need to Know Now? Stacy Hambelton Agriculture Business Specialist Gainesville, MO Retirement and Estate Planning Issues Men (farmers in particular) don t plan for their retirement

3:45 p.m. - 4:30 p.m.

2016 Commercial & Bankruptcy Law Seminar Pending Doom: Another Ag Crisis 3:45 p.m. - 4:30 p.m. Presented by Larry Eide Pappajohn Shriver, Eide & Nielsen, PC 103 E State St. Ste. 800 Mason City, IA 50402

2016 Commercial & Bankruptcy Law Seminar Pending Doom: Another Ag Crisis 3:45 p.m. - 4:30 p.m. Presented by Larry Eide Pappajohn Shriver, Eide & Nielsen, PC 103 E State St. Ste. 800 Mason City, IA 50402

TRANSFER OF FARM ASSETS

TRANSFER OF FARM ASSETS Issue 1: Buying and Selling Farmland pp. 87-89 Cost Basis Purchase [IRC 1012] Paid in: cash, debt or other Gift [IRC 1015] Generally donor s basis Issue 1: Buying and Selling Farmland

TRANSFER OF FARM ASSETS Issue 1: Buying and Selling Farmland pp. 87-89 Cost Basis Purchase [IRC 1012] Paid in: cash, debt or other Gift [IRC 1015] Generally donor s basis Issue 1: Buying and Selling Farmland

Ag Income Tax Update for Farm Families

2006-07 Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Regional Extension Educator Gary A. Hachfeld, Regional Extension Educators Updated 6/2007 Introduction: For the 2006 and

2006-07 Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Regional Extension Educator Gary A. Hachfeld, Regional Extension Educators Updated 6/2007 Introduction: For the 2006 and

2012 Risk and Profit Conference Breakout Session Presenters. 4. The Economic, Legal, and Tax Implications of An Oil Lease

2012 Risk and Profit Conference Breakout Session Presenters 4. The Economic, Legal, and Tax Implications of An Oil Lease Kent Miller Kent Miller serves as an extension agricultural

2012 Risk and Profit Conference Breakout Session Presenters 4. The Economic, Legal, and Tax Implications of An Oil Lease Kent Miller Kent Miller serves as an extension agricultural

Farm Tax and Farm Sales Affected by New Fiscal Cliff Legislation

Farm Tax and Farm Sales Affected by New Fiscal Cliff Legislation Marc Lovell Tax School and Department of Agricultural and Consumer Economics University of Illinois February 7, 2013 farmdoc daily (3):23

Farm Tax and Farm Sales Affected by New Fiscal Cliff Legislation Marc Lovell Tax School and Department of Agricultural and Consumer Economics University of Illinois February 7, 2013 farmdoc daily (3):23

CHOICE OF BUSINESS ENTITY: PRESENT LAW AND DATA RELATING TO C CORPORATIONS, PARTNERSHIPS, AND S CORPORATIONS

CHOICE OF BUSINESS ENTITY: PRESENT LAW AND DATA RELATING TO C CORPORATIONS, PARTNERSHIPS, AND S CORPORATIONS Prepared by the Staff of the JOINT COMMITTEE ON TAXATION April 10, 2015 JCX-71-15 CONTENTS INTRODUCTION...

CHOICE OF BUSINESS ENTITY: PRESENT LAW AND DATA RELATING TO C CORPORATIONS, PARTNERSHIPS, AND S CORPORATIONS Prepared by the Staff of the JOINT COMMITTEE ON TAXATION April 10, 2015 JCX-71-15 CONTENTS INTRODUCTION...

2018 Year-End Tax Planning

2018 Year-End Tax Planning October 2018 1101 Wootton Parkway Suite 400 Rockville, Maryland 20852 Phone: 301.924.2160 Fax: 202.204.6322 2 Year-End Tax Planning - Overview As year end approaches, it's a

2018 Year-End Tax Planning October 2018 1101 Wootton Parkway Suite 400 Rockville, Maryland 20852 Phone: 301.924.2160 Fax: 202.204.6322 2 Year-End Tax Planning - Overview As year end approaches, it's a

Farm Tax Update 1/21/2019. Teaching Objectives. Circular 230 Disclosure. Thank You Farmers Tax Guide

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Ag Income Tax Update for Farm Families

Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Extension Educator Gary A. Hachfeld, Extension Educator January 2010 Introduction: For tax years 2009 and 2010, there are a number

Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Extension Educator Gary A. Hachfeld, Extension Educator January 2010 Introduction: For tax years 2009 and 2010, there are a number

Timber Taxation. Why forestry is unique. Dr. Tamara L. Cushing Diboll, TX February 7, 2017

Timber Taxation Dr. Tamara L. Cushing Diboll, TX February 7, 2017 Why forestry is unique O Is it agriculture? O Long-time horizon O Spread-out cash flows O Derived demand O Location dependent 1 What do

Timber Taxation Dr. Tamara L. Cushing Diboll, TX February 7, 2017 Why forestry is unique O Is it agriculture? O Long-time horizon O Spread-out cash flows O Derived demand O Location dependent 1 What do

Top Producer Seminar

Top Producer Seminar Are You Ready for A Wild Tax Ride? Paul Neiffer, CPA CliftonLarsonAllen, LLP January 30, 2014 CLAconnect.com Are You ready for a Wild Tax Ride? Topics The Deceptively High 2013 Tax

Top Producer Seminar Are You Ready for A Wild Tax Ride? Paul Neiffer, CPA CliftonLarsonAllen, LLP January 30, 2014 CLAconnect.com Are You ready for a Wild Tax Ride? Topics The Deceptively High 2013 Tax

2002 Instructions for Schedule F, Profit or Loss From Farming

2002 Instructions for Schedule F, Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1041, 1065, or 1065-B. This activity may subject you

2002 Instructions for Schedule F, Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1041, 1065, or 1065-B. This activity may subject you

Gary A. Hachfeld, David B. Bau, & C. Robert Holcomb, Extension Educators

Balance Sheet Agricultural Business Management Gary A. Hachfeld, David B. Bau, & C. Robert Holcomb, Extension Educators Financial Management Series #1 6/2017 A complete set of financial statements for

Balance Sheet Agricultural Business Management Gary A. Hachfeld, David B. Bau, & C. Robert Holcomb, Extension Educators Financial Management Series #1 6/2017 A complete set of financial statements for

NEWARK-FREMONT LEGAL CENTER BANKRUPTCY WORKSHEET

NEWARK-FREMONT LEGAL CENTER BANKRUPTCY WORKSHEET Complete the form below and then call our office for an appointment. 794-LAWS Please Print Clearly! DEBTOR JOINT DEBTOR Full Name Street Address Mailing

NEWARK-FREMONT LEGAL CENTER BANKRUPTCY WORKSHEET Complete the form below and then call our office for an appointment. 794-LAWS Please Print Clearly! DEBTOR JOINT DEBTOR Full Name Street Address Mailing

2017 Farm Income Tax Webinar

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018 The TCJA s Impact on Farmers and Ranchers Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation

Kansas Farm Bureau Young Farmers and Leaders Conference Manhattan, KS January 26, 2018 The TCJA s Impact on Farmers and Ranchers Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation

Year-End Tax Tips for Individuals

Year-End Tax Tips for Individuals New tax legislation has brought greater certainty to year-end planning, but also created new challenges. There is still time to set up an appointment for year-end planning.

Year-End Tax Tips for Individuals New tax legislation has brought greater certainty to year-end planning, but also created new challenges. There is still time to set up an appointment for year-end planning.

Farmer and Farmland Owner Income Tax Webinar. Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension

Farmer and Farmland Owner Income Tax Webinar Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension Chris Bruynis Circular 230 Disclosure The information provided in this presentation is for educational

Farmer and Farmland Owner Income Tax Webinar Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension Chris Bruynis Circular 230 Disclosure The information provided in this presentation is for educational

Year End Tax Planning for Individuals

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

Instructions for Completing Wisconsin Schedule I 2017

Caution: The revised version of the 2017 Schedule I instructions was placed on the Internet on February 2, 2018. The instructions have been revised to include changes to federal law that were made by Public

Caution: The revised version of the 2017 Schedule I instructions was placed on the Internet on February 2, 2018. The instructions have been revised to include changes to federal law that were made by Public

Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Be sure to put your name at the bottom of each page. The assets and debts pages also require you to number the pages.

Bankruptcy Questionnaire Instructions Complete & Return to: Law Offices of Olivier Denier Long 10500 Sager Avenue, Suite "B" Fairfax, VA 22030-2414 703-591-1600 Bankruptcy is a time honored practice that

Bankruptcy Questionnaire Instructions Complete & Return to: Law Offices of Olivier Denier Long 10500 Sager Avenue, Suite "B" Fairfax, VA 22030-2414 703-591-1600 Bankruptcy is a time honored practice that

CHAPTER 3 FARM INCOME

MANAGING THE TIMING OF INCOME AND DEDUCTIONS CHAPTER 3 SYNPOSIS (click on section title to go directly there) Introduction... 3.2 Defining Farm and Farming... 3.2 Definition of Farm... 3.2 Definition of

MANAGING THE TIMING OF INCOME AND DEDUCTIONS CHAPTER 3 SYNPOSIS (click on section title to go directly there) Introduction... 3.2 Defining Farm and Farming... 3.2 Definition of Farm... 3.2 Definition of

Managerial Accounting Using QuickBooks Pro TM

Managerial Accounting Using QuickBooks Pro TM This manual is intended as a reference in furthering knowledge of management accounting for agricultural producers using QuickBooks Pro TM. Historically, agricultural

Managerial Accounting Using QuickBooks Pro TM This manual is intended as a reference in furthering knowledge of management accounting for agricultural producers using QuickBooks Pro TM. Historically, agricultural

2015 CALT Tax Schools Day 2. Contact Information. Day 2 Topics 12/15/2015. Dave Repp. Paul Neiffer.

2015 CALT Tax Schools Day 2 David Repp and Paul Neiffer Contact Information Dave Repp drepp@dickinsonlaw.com Paul Neiffer Paul.neiffer@claconnect.com 509 823 2920 www.farmcpatoday.com @farmcpa Day 2 Topics

2015 CALT Tax Schools Day 2 David Repp and Paul Neiffer Contact Information Dave Repp drepp@dickinsonlaw.com Paul Neiffer Paul.neiffer@claconnect.com 509 823 2920 www.farmcpatoday.com @farmcpa Day 2 Topics

CORRECTED OMB No For DEBTOR S name. 3 Interest if included in box 2 4

Attention: Do not download, print, and file Copy A with the IRS. Copy A appears in red, similar to the official IRS form, but is for informational purposes only. A penalty of 50 per information return

Attention: Do not download, print, and file Copy A with the IRS. Copy A appears in red, similar to the official IRS form, but is for informational purposes only. A penalty of 50 per information return

Farm Financial Risk Management: Introduction to Farm Financial Statements for New and Beginning Farmers

Farm Financial Risk Management: Introduction to Farm Financial Statements for New and Beginning Farmers Kim Morgan, Assistant Professor, Agricultural and Applied Economics, Virginia Tech; Peter Callan,

Farm Financial Risk Management: Introduction to Farm Financial Statements for New and Beginning Farmers Kim Morgan, Assistant Professor, Agricultural and Applied Economics, Virginia Tech; Peter Callan,

In the most far-reaching revision

A Business Newsletter for Agriculture Vol. 9, No. 11 www.extension.iastate.edu/agdm October 2005 Major developments in Chapter 12 bankruptcy* Neil Harl, Charles F. Curtiss Distinguished Professor in Agriculture

A Business Newsletter for Agriculture Vol. 9, No. 11 www.extension.iastate.edu/agdm October 2005 Major developments in Chapter 12 bankruptcy* Neil Harl, Charles F. Curtiss Distinguished Professor in Agriculture

Tax Genius. limiting total contribution deductions to 50% of AGI was increased to 60%, allowing a slightly larger deduction in some cases.

Tax Genius 2018 Pocket Tax Guide Online Edition It has been a busy time for tax-related news and upcoming changes. We have compiled many of the tax changes, deductions and tax rates for easy reference

Tax Genius 2018 Pocket Tax Guide Online Edition It has been a busy time for tax-related news and upcoming changes. We have compiled many of the tax changes, deductions and tax rates for easy reference

Ag Income Tax Update for Farm Families

Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Extension Educator Gary A. Hachfeld, Extension Educator April 2009 Introduction: For tax years 2008 and 2009, there are a number

Ag Income Tax Update for Farm Families Prepared by: C. Robert Holcomb, EA, Extension Educator Gary A. Hachfeld, Extension Educator April 2009 Introduction: For tax years 2008 and 2009, there are a number

REAL ESTATE PROPERTY FORECLOSURE and CANCELLATION OF DEBT AUDIT TECHNIQUE GUIDE

REAL ESTATE PROPERTY FORECLOSURE and CANCELLATION OF DEBT AUDIT TECHNIQUE GUIDE NOTE: This document is not an official pronouncement of the law or the position of the Service and cannot be used, cited,

REAL ESTATE PROPERTY FORECLOSURE and CANCELLATION OF DEBT AUDIT TECHNIQUE GUIDE NOTE: This document is not an official pronouncement of the law or the position of the Service and cannot be used, cited,

TAX FACTS AND TABLES at a glance

TAX FACTS AND TABLES 2013 at a glance Are you making smart investment decisions that can help Reduce your taxes The first step in reducing the amount of tax you pay on your investments is to get the facts.

TAX FACTS AND TABLES 2013 at a glance Are you making smart investment decisions that can help Reduce your taxes The first step in reducing the amount of tax you pay on your investments is to get the facts.

CHAPTER 10 COMPARATIVE FORMS OF DOING BUSINESS LECTURE NOTES

CHAPTER 10 COMPARATIVE FORMS OF DOING BUSINESS 10.1 FORMS OF DOING BUSINESS LECTURE NOTES 1. Legal Forms. Business entities can be organized into the following principal legal forms. Sole proprietorship.

CHAPTER 10 COMPARATIVE FORMS OF DOING BUSINESS 10.1 FORMS OF DOING BUSINESS LECTURE NOTES 1. Legal Forms. Business entities can be organized into the following principal legal forms. Sole proprietorship.

Tax Update for the N.E. ACA Conference. Jeff Solomon, Managing Partner, KN+S

Tax Update for the N.E. ACA Conference Jeff Solomon, Managing Partner, KN+S Katz Nannis + Solomon, PC Boutique, regional CPA firm focused on entrepreneurial companies with an emphasis on technology Much

Tax Update for the N.E. ACA Conference Jeff Solomon, Managing Partner, KN+S Katz Nannis + Solomon, PC Boutique, regional CPA firm focused on entrepreneurial companies with an emphasis on technology Much

Reporting Capital Gains And Losses for Wisconsin By Individuals Estates Trusts

State of Wisconsin Department of Revenue Reporting Capital Gains And Losses for Wisconsin By Individuals Estates Trusts For Use in Preparing 1999 Returns Publication 103 (11/99) Printed on Recycled Paper

State of Wisconsin Department of Revenue Reporting Capital Gains And Losses for Wisconsin By Individuals Estates Trusts For Use in Preparing 1999 Returns Publication 103 (11/99) Printed on Recycled Paper

Year-End Tax Planning Summary December 2015

Year-End Tax Planning Summary December 2015 Overview Thanks to the continued political gridlock in Washington, 2015 did not see comprehensive tax reform. However, on December 18th, Congress passed the

Year-End Tax Planning Summary December 2015 Overview Thanks to the continued political gridlock in Washington, 2015 did not see comprehensive tax reform. However, on December 18th, Congress passed the

Calculating Depreciation Recapture Under IRC 1245 and 1250: Minimizing Tax Through Transaction Planning

FOR LIVE PROGRAM ONLY Calculating Depreciation Recapture Under IRC 1245 and 1250: Minimizing Tax Through Transaction Planning TUESDAY, AUGUST 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Calculating Depreciation Recapture Under IRC 1245 and 1250: Minimizing Tax Through Transaction Planning TUESDAY, AUGUST 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

11/3/2011. Debt & Taxes

Debt & Taxes Elizabeth A. Maresca Clinical Associate Professor Fordham Law School, New York, NY Tax & Consumer Litigation Clinic I. General Rules: Income from discharge of indebtedness, exemptions and

Debt & Taxes Elizabeth A. Maresca Clinical Associate Professor Fordham Law School, New York, NY Tax & Consumer Litigation Clinic I. General Rules: Income from discharge of indebtedness, exemptions and

Mark A Wood. Tracy Ellingson. Kent,

Tracy Ellingson From: Sent: To: Subject: Attachments: Mark Wood Saturday, May 27, 2017 9:01 AM Kent Vickre 5-6 Mark Wood, K-State Farm Management Class Guest lecture Materials 2016 KSU

Tracy Ellingson From: Sent: To: Subject: Attachments: Mark Wood Saturday, May 27, 2017 9:01 AM Kent Vickre 5-6 Mark Wood, K-State Farm Management Class Guest lecture Materials 2016 KSU

TAX INFORMATION 2013

6JAN201217025633 TAX INFORMATION 2013 This booklet contains tax information relevant to ownership of Units of Cross Timbers Royalty Trust and should be retained. (This page intentionally left blank.) Cross

6JAN201217025633 TAX INFORMATION 2013 This booklet contains tax information relevant to ownership of Units of Cross Timbers Royalty Trust and should be retained. (This page intentionally left blank.) Cross

2011 Tax Guide. What You Need to Know About the New Rules

2011 Tax Guide What You Need to Know About the New Rules Tax Guide 2011 This guide is not intended to be tax advice and should not be treated as such. Each individual s tax situation is different. You

2011 Tax Guide What You Need to Know About the New Rules Tax Guide 2011 This guide is not intended to be tax advice and should not be treated as such. Each individual s tax situation is different. You

Balance Sheet and Schedules

Balance Sheet and Schedules CURRENT ASSET SCHEDULE DOLLAR VALUE CASH AND EQUIVALENTS A $ MARKETABLE EQUITIES B $ ACCOUNTS RECEIVABLE C $ MARKET LIVESTOCK $ PRODUCE OR BY-PRODUCTS $ CROP INVENTORY D $ CROP

Balance Sheet and Schedules CURRENT ASSET SCHEDULE DOLLAR VALUE CASH AND EQUIVALENTS A $ MARKETABLE EQUITIES B $ ACCOUNTS RECEIVABLE C $ MARKET LIVESTOCK $ PRODUCE OR BY-PRODUCTS $ CROP INVENTORY D $ CROP

INCOME TAX MANAGEMENT FOR FARMERS IN George F. Patrick Department of Agricultural Economics Purdue University

INCOME TAX MANAGEMENT FOR FARMERS IN 2007 George F. Patrick Department of Agricultural Economics Purdue University CES Paper No. 364-W December 2007 INCOME TAX MANAGEMENT FOR FARMERS IN 2007 Table of Contents

INCOME TAX MANAGEMENT FOR FARMERS IN 2007 George F. Patrick Department of Agricultural Economics Purdue University CES Paper No. 364-W December 2007 INCOME TAX MANAGEMENT FOR FARMERS IN 2007 Table of Contents

AGRICULTURAL FINANCIAL AND TAX PLANNING. Self Employment Tax on Ranch Related Income

AGRICULTURAL FINANCIAL AND TAX PLANNING Self Employment Tax on Ranch Related Income By Thomas J. Bryant, CPA and Ryan Beasley, CPA In last months article we mentioned a February 27, 2017, Internal Revenue

AGRICULTURAL FINANCIAL AND TAX PLANNING Self Employment Tax on Ranch Related Income By Thomas J. Bryant, CPA and Ryan Beasley, CPA In last months article we mentioned a February 27, 2017, Internal Revenue

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

Tax. 2nd Edition. Management Strategies for Farmers. Merle Good Alberta Agriculture and Rural Development

Tax Management Strategies for Farmers 2nd Edition Merle Good Alberta Agriculture and Rural Development Dean Gallimore and Colin Miller Chartered Accountants Lethbridge Published by Alberta Agriculture

Tax Management Strategies for Farmers 2nd Edition Merle Good Alberta Agriculture and Rural Development Dean Gallimore and Colin Miller Chartered Accountants Lethbridge Published by Alberta Agriculture

MESA OFFSHORE TRUST 2000 FEDERAL INCOME TAX INFORMATION

MESA OFFSHORE TRUST 2000 FEDERAL INCOME TAX INFORMATION (The Trust ) 2000 FEDERAL INCOME TAX INFORMATION Instructions for Schedules A, B, C & D Schedule A For Unit Holders who file income tax returns on

MESA OFFSHORE TRUST 2000 FEDERAL INCOME TAX INFORMATION (The Trust ) 2000 FEDERAL INCOME TAX INFORMATION Instructions for Schedules A, B, C & D Schedule A For Unit Holders who file income tax returns on

Tax Facts Quick Reference

Tax Facts Quick Reference 2015 Income Investment Estate Retirement Social Security NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Income Ordinary Income Tax Rates and Brackets Tax Rate Married, Filing

Tax Facts Quick Reference 2015 Income Investment Estate Retirement Social Security NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Income Ordinary Income Tax Rates and Brackets Tax Rate Married, Filing

Congress Passes Fiscal Cliff Act

Congress Passes Fiscal Cliff Act Pulling back from the fiscal cliff at the 13th hour, Congress preserved most of the George W. Bush-era tax cuts and extended many other lapsed tax provisions. The Senate

Congress Passes Fiscal Cliff Act Pulling back from the fiscal cliff at the 13th hour, Congress preserved most of the George W. Bush-era tax cuts and extended many other lapsed tax provisions. The Senate

Davis & associates, p.a. Certified Public Accountants and Consultants

209 FEDERAL TAX RATES Davis & Associates, p.a. Certified Public Accountants and Consultants 97 Washingtonian Boulevard, Suite 550 Gaithersburg, Maryland 20878 Phone: 30.963.6696 Fax: 30.963.6693 www.daviscpas.com

209 FEDERAL TAX RATES Davis & Associates, p.a. Certified Public Accountants and Consultants 97 Washingtonian Boulevard, Suite 550 Gaithersburg, Maryland 20878 Phone: 30.963.6696 Fax: 30.963.6693 www.daviscpas.com

Record Keeping in Farm Management

South Dakota State University Open PRAIRIE: Open Public Research Access Institutional Repository and Information Exchange Extension Extra SDSU Extension 5-1-2004 Record Keeping in Farm Management Agustin

South Dakota State University Open PRAIRIE: Open Public Research Access Institutional Repository and Information Exchange Extension Extra SDSU Extension 5-1-2004 Record Keeping in Farm Management Agustin

2017 Year-End Income Tax Planning for Individuals December 2017

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

INCOME TAX MANAGEMENT FOR FARMERS IN 2011

INCOME TAX MANAGEMENT FOR FARMERS IN 2011 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2011 DRAFT 2011 version has not been peer-reviewed. Comments are welcome.

INCOME TAX MANAGEMENT FOR FARMERS IN 2011 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2011 DRAFT 2011 version has not been peer-reviewed. Comments are welcome.

Evaluating the Financial Viability of the Business

Evaluating the Financial Viability of the Business Just as it is important to construct a new building on a strong foundation, it is important to build the economic future of your business on a sound financial

Evaluating the Financial Viability of the Business Just as it is important to construct a new building on a strong foundation, it is important to build the economic future of your business on a sound financial

President Obama's 2016 Federal Budget Proposal

President Obama's 2016 Federal Budget Proposal March 10, 2015 by Tim Steffen On the heels of his first State of the Union address to the nation after the mid-term elections, President Obama released his

President Obama's 2016 Federal Budget Proposal March 10, 2015 by Tim Steffen On the heels of his first State of the Union address to the nation after the mid-term elections, President Obama released his

(This page has been left blank intentionally.)

") 2016 9FEB2017150852 (This page has been left blank intentionally.) Permian Basin Royalty Trust 2911 Turtle Creek Boulevard Suite 850 Dallas, Texas 75219 Telephone Toll-Free 1-855-588-7839 February 17,

2016 9FEB2017150852 (This page has been left blank intentionally.) Permian Basin Royalty Trust 2911 Turtle Creek Boulevard Suite 850 Dallas, Texas 75219 Telephone Toll-Free 1-855-588-7839 February 17,

2017 Year-End Tax Planning

2017 Year-End Tax Planning If you've been following the news out of Washington, you probably know that for the first time in decades, tax reform is a real possibility. Given that both the House and the

2017 Year-End Tax Planning If you've been following the news out of Washington, you probably know that for the first time in decades, tax reform is a real possibility. Given that both the House and the

TAX INFORMATION 2014

6JAN201217025633 TAX INFORMATION 2014 This booklet contains tax information relevant to ownership of Units of Cross Timbers Royalty Trust and should be retained. (This page intentionally left blank.) Cross

6JAN201217025633 TAX INFORMATION 2014 This booklet contains tax information relevant to ownership of Units of Cross Timbers Royalty Trust and should be retained. (This page intentionally left blank.) Cross

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2016 www.cordascocpa.com INTRODUCTION 2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS It s that time of year again.

2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2016 www.cordascocpa.com INTRODUCTION 2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS It s that time of year again.

FEB

2018 16FEB2019081321 (This page has been left blank intentionally.) Permian Basin Royalty Trust 2911 Turtle Creek Boulevard Suite 850 Dallas, Texas 75219 Telephone Toll-Free 1-855-588-7839 February 28,

2018 16FEB2019081321 (This page has been left blank intentionally.) Permian Basin Royalty Trust 2911 Turtle Creek Boulevard Suite 850 Dallas, Texas 75219 Telephone Toll-Free 1-855-588-7839 February 28,

Case BLS Doc Filed 09/22/15 Page 1 of 6 EXHIBIT 3 ANALYSIS OF CERTAIN U.S. FEDERAL INCOME TAX CONSEQUENCES OF THE PLAN

Case 15-10541-BLS Doc 1087-3 Filed 09/22/15 Page 1 of 6 EXHIBIT 3 ANALYSIS OF CERTAIN U.S. FEDERAL INCOME TAX CONSEQUENCES OF THE PLAN Case 15-10541-BLS Doc 1087-3 Filed 09/22/15 Page 2 of 6 ANALYSIS OF

Case 15-10541-BLS Doc 1087-3 Filed 09/22/15 Page 1 of 6 EXHIBIT 3 ANALYSIS OF CERTAIN U.S. FEDERAL INCOME TAX CONSEQUENCES OF THE PLAN Case 15-10541-BLS Doc 1087-3 Filed 09/22/15 Page 2 of 6 ANALYSIS OF

GMS SURGENT 2014 YEAR-END TAX SAVING TIPS

GMS SURGENT 2014 YEAR-END TAX SAVING TIPS As the days on the calendar grow short and the holiday season gets into full swing, we at GMS Surgent would like to provide you with some valuable ideas to reduce

GMS SURGENT 2014 YEAR-END TAX SAVING TIPS As the days on the calendar grow short and the holiday season gets into full swing, we at GMS Surgent would like to provide you with some valuable ideas to reduce

Financial Ratios Used in Financial Management

Financial Ratios Used in Financial Management Robin Reid (robinreid@ksu.edu) and Kevin Herbel (kherbel@ksu.edu) Revision of MF-270 by Dr. Michael Langemeier Kansas State University Department of Agricultural

Financial Ratios Used in Financial Management Robin Reid (robinreid@ksu.edu) and Kevin Herbel (kherbel@ksu.edu) Revision of MF-270 by Dr. Michael Langemeier Kansas State University Department of Agricultural

Closely Held Corporations

Closely Held Corporations Tax Planning Course Description This course examines and explains the practical aspects of using the closely held corporation to maximize after-tax return on business operations.

Closely Held Corporations Tax Planning Course Description This course examines and explains the practical aspects of using the closely held corporation to maximize after-tax return on business operations.