GLOBAL ECONOMIC OUTLOOK As good as it gets in 2018? Oliver Salmon Lead Economist

|

|

|

- Ernest Kelly

- 5 years ago

- Views:

Transcription

1 GLOBAL ECONOMIC OUTLOOK As good as it gets in 2018? Oliver Salmon Lead Economist March 2018

2 Global synchronized upturn continues 2

3 as trade growth maintains healthy momentum Advanced Econs: Goods trade volumes Index 60 % 6m/6m Global manufacturing PMI (Adv 4 months, LHS) World trade volumes (RHS) Source : Oxford Economics/Haver Analytics -15.0

4 Looser credit conditions are supportive of growth 4

5 Global investment continues to improve G-3: Investment indicators % year, 3mma Standardised indicator 3 Survey-based indicator, advanced 2 3 months (RHS) G-3* investment goods orders indicator (LHS) Source : Oxford Economics/Haver Analytics * US, Germany, Japan -4 5

6 Strongest post-crisis economic growth in

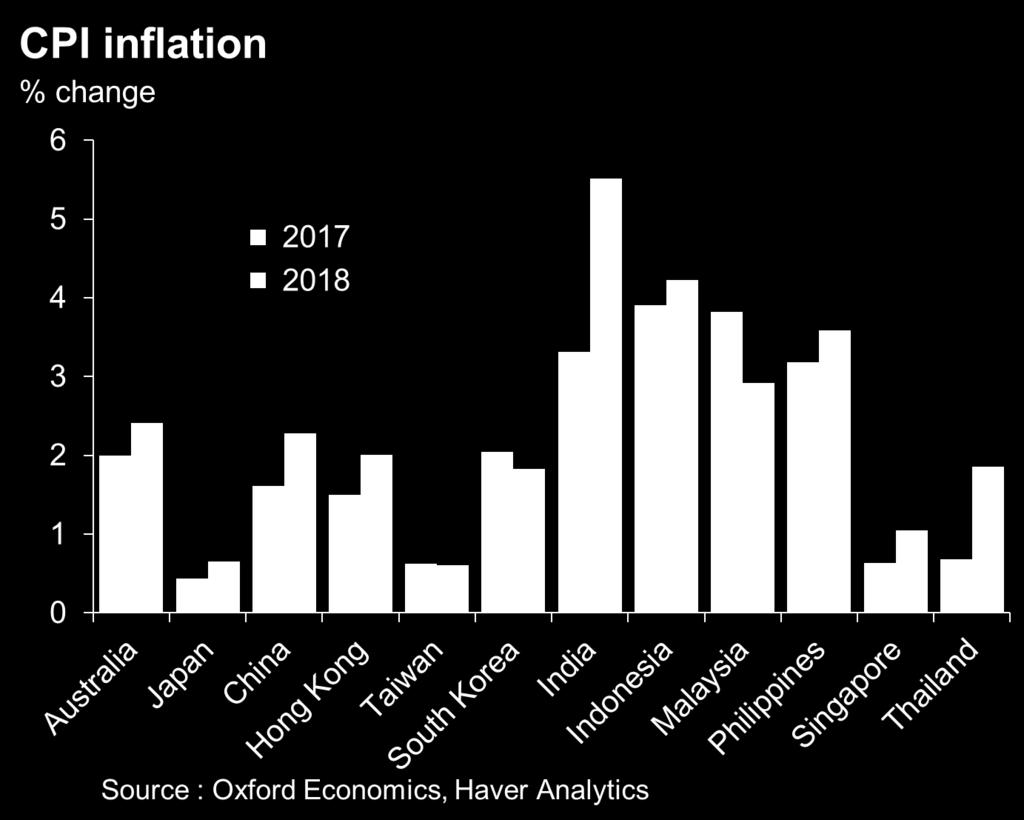

7 while Inflation pressures remain contained 7

8 Global risks remain skewed on the downside 8

9 US policy and market turmoil represent largest concerns 9

10 US: The Great Rotation

11 The triple rotation in the US economy 1. On the macroeconomic front, business investment and exports will be stronger engines of growth, while consumer spending trends will reflect a maturing economy. 2. On the policy front, the Trump administration delivered on its fiscal stimulus promises, with a plan worth $1.5 trillion. Congress meanwhile pushed through a substantial spending bill (worth $300bn on paper, but up to $1.2tn in practice). 3. On the Federal Reserve front, a more hawkish Fed will react to stronger inflation with four rate hikes in

12 Soft data is off the chart at 13-year high 12

13 Consumer spending remains solid around 2.5% 13

14 Investment rebound, partly coming from energy 14

15 but the stronger global backdrop has been key 15

16 In 2018, ongoing rotation to business investment 16

17 Policy mix becoming more pro-growth, risks linger Tax Cuts Government spending Infrastructure Less regulation Political uncertainty Trade protection Immigration 17

18 Tax Cuts & Jobs Act of 2017: $1.5 trillion 18

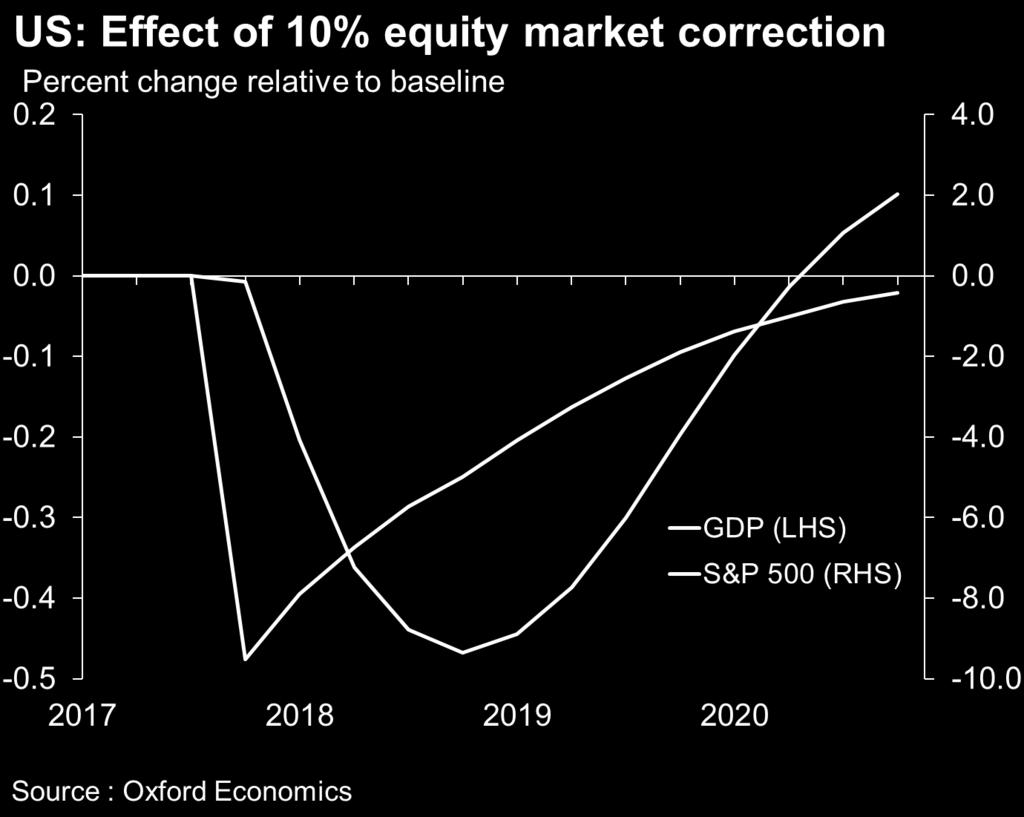

19 Bipartisan Budget Act of 2018: $300bn -> $1.2 trillion? Congress passed a sweeping spending bill this morning that boosts discretionary spending by $300 billion and provides $90 billion in disaster relief. The Bipartisan Budget Act would boost the deficit by $320 billion over the next 10 years, with the budget shortfall breaching the symbolic $1 trillion-mark next year the largest deficit since the Great Recession. Importantly, we believe Congress would not allow for substantial budget cuts in 2020 (as mandated by the sequester caps from the Budget Control Act of 2011), especially in an election year. As such, we estimate the legislation will add $1.2 trillion to the budget deficit over the next decade. 19 Caps on discretionary budget authority, in billions Fiscal 2018 Prior law BBA 2018 Increase Defense $549 $629 $80 Nondefense $516 $579 $63 Total $143 Fiscal 2019 Prior law BBA 2018 Increase Defense $562 $647 $85 Nondefense $529 $597 $68 Total $153 Source: Oxford Economics;

20 Congress spending spree: $2.5tn in 50 days! 20

21 Higher oil prices and weaker dollar push inflation 21

22 Markets expecting more inflation and tighter Fed 22

23 Fed balance sheet normalization: passive & predictable 23

24 Risks to the outlook Financial market stress. Stronger wage growth to accelerate monetary policy normalisation. Savings dip US households spending beyond their means, eroding buffers to insulate against potential future crisis. Trade war potentially self-defeating for US industry. Fiscal profligacy to weigh on future growth. Tighter immigration policy would weigh on growth in labour supply and long term growth potential. 24

25 Household Savings dip 25

26 Financial market stress 26

27 Surging wage growth could spell trouble 27

28 Trade winds intensifying Unilateral US exit from NAFTA is a real possibility. US exit from NAFTA would reduce real GDP growth by 0.5pp in 2019, but the impact would diminish over time. 28

29 Fiscal overdrive and growth exhaustion When the stimulus fades out, higher borrowing cost and reduced fiscal pace will pose a real risk for the US economy.

30 Europe: A sustained period of above-trend growth

31 European PMIs pointing to yet faster growth 31

32 Employment growth strongest since

33 and continuing improvement in investment 33

34 Inflation lagging behind Eurozone: CPI Inflation (Bottom-up f'cast model) % y/y / contribution Core Energy Food alcohol and tobacco Headline Source : Oxford Economics/Haver Analytics Forecast 34

35 underpinned by muted wage growth 35

36 ECB to keep rates unchanged till

37 Risks to the outlook Return of populism? Italian elections deliver hung parliament with populist tilt. New elections still possible. Brexit cliff-edge scenario remains a distinct possibility, no agreement over regulatory alignment the Irish border. Strong Euro sharp rise in Euro could potentially choke off export recovery. ECB tightening rising wages and inflation could prompt a quicker pace of normalization. Trade War Eurozone seems most willing to engage Trump in tit-for-tat tariffs. Weak periphery and slow reform process. 37

38 Return of populism? Italy elections Italian elections delivered a hung parliament with a populist flavor (first major EU country to deliver populist victory). Centre-right alliance has won the most seats (remember Berlusoni!?!), but Five Star Movement emerged as the largest single party and now has right to try and form government. Options include a coalition with the defeated Democratic Party the biggest losers from Sunday s vote or the League. New elections still on the table. Populist agenda likely to be scaled back in coalition government, but so will important fiscal consolidation and structural reform. 38

39 Where are we now on Brexit? Phase one (separation issues) now complete, but only after a fudge on the issue of the Irish border. Next step a transitional deal: UK will remain bound to EU rules during this period. The EU would like the transitional deal to end by December UK will cease to be party to third-party FTA s by March Phase 2 trade talks will begin, though by the end of the Article- 50 period we are only likely to have a heads of agreement. If we proceed down the FTA route it is very unlikely to be ready by the end of the transitional period. 39

40 Canada-style FTA is the most likely outcome UK: Brexit scenario probabilities Remain in EU 10% EEA 20% No deal, WTO rules & 2019 'cliff edge' 30% FTA 40% 'Softer' 'Harder' Source : Oxford Economics 40

41 China: Policy-induced slowdown to continue

42 China stimulus kickstarted global upturn China housing starts and global commodity prices % yoy Floor space started, 6mma Metals and minerals prices Non-energy prices Source: Oxford Economics, CEIC Data, World Bank 42

43 and benefitted from pick-up in external demand 43

44 but real estate momentum is cooling 44

45 And policy shifting towards less expansionary policy 45

46 In all, we expect the economy to cool in

47 No major change policy stance in coming years No material change on how to balance growth with reform and deleveraging in the coming years. Recent National People s Congress confirmed gradual shift towards greater emphasis on quality over quantity of growth. Commitment to target of doubling GDP between 2010 and 2020 remains growth target of around 6.5%. Focus on reducing financial risks and deleveraging parts of the financial system while aiming for a gradual slowdown of credit growth in the coming two years. Supply-side reform and SOE reform to continue, albeit with Chinese characteristics. 47

48 Asia ex China: Ongoing broad strength despite moderating China

49 Slower Chinese imports matter most to Asia 49

50 but domestic demand remains key Asia-ex India, China & Japan: Growth drivers % year Forecast 15 Domestic demand Exports Source : Oxford Economics/Haver Analytics

51 Fiscal policy to range from neutral to supportive 51

52 Monetary policy rising gradually 52

53 Healthy growth to continue 53

54 Benign inflationary conditions 54

55 No major pressures on Asian FX markets 55

56 India: Growth firing on all cylinders 56

57 Japan: Solid external and domestic conditions in 2018 Japan: Exports and world trade % year World trade F'cast World: Global 10-year government yields % US Japan Germany Forecast -30 Export volumes Source: Oxford Economics Source : Oxford Economics/Haver Analytics 57

58 Risks to the outlook Faster pace of policy tightening in China, impact on trade and commodity prices. Global trade war to hit trade-dependant Asian economies. Rising levels of indebtedness could potentially weigh on growth in the future. Political uncertainty Indonesia, Malaysia, Thailand, India entering election cycle in Geo-political risks in Korea? Faster pace of US tightening leading to capital outflows and rising interest rates. 58

59 Tighter policies to reign in growth 59

60 China sneezes and the world catches a cold! 60

61 Trumps protectionist stance Safeguard tariffs on solar panels and washing machines. 25% tariff on steel and 10% tariff on aluminium imports. National Security threat under Section 232. Renegotiation of NAFTA and KORUS FTA s. Section 301 investigation into alleged Chinese theft of intellectual property. EU drawing up a retaliatory response (tariffs on US imports of 100 products). South Korea already lodged a complaint with the WTO. Trade war good for US : Trump 61

62 US China trade tensions likely to worsen 62

63 Risks of escalated trade war have subsided 63

64 and US protectionism self-defeating 64

65 but global impact still significant 65

66 Asia has been on a credit splurge 66

67 Asia has been on a credit splurge 67

68 THANK YOU! Any questions?

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

California Travel & Tourism Outlook. April 2018

California Travel & Tourism Outlook April 2018 California travel forecast overview Total visitation to California is forecast to grow 2.9% in 2018, following a 2.0% expansion in 2017. The near-term outlook

California Travel & Tourism Outlook April 2018 California travel forecast overview Total visitation to California is forecast to grow 2.9% in 2018, following a 2.0% expansion in 2017. The near-term outlook

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Asia Watch. Trade tensions risk to solid outlook. Group Economics Emerging Markets Research. Group Economics: Enabling smart decisions.

Asia Watch Group Economics Emerging Markets Research 1 March 1 Arjen van Dijkhuizen Senior Economist Tel: +31 5 arjen.van.dijkhuizen@nl.abnamro.com Trade tensions risk to solid outlook Growth EM Asia up

Asia Watch Group Economics Emerging Markets Research 1 March 1 Arjen van Dijkhuizen Senior Economist Tel: +31 5 arjen.van.dijkhuizen@nl.abnamro.com Trade tensions risk to solid outlook Growth EM Asia up

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Risk Outlook May 2016

Global Risk Outlook May 2016 Scott Livermore Managing Director and COO slivermore@oxfordeconomics.com About Oxford Economics Oxford Economics is a world leader in global forecasting and quantitative analysis.

Global Risk Outlook May 2016 Scott Livermore Managing Director and COO slivermore@oxfordeconomics.com About Oxford Economics Oxford Economics is a world leader in global forecasting and quantitative analysis.

EY s Global Economic Outlook Ireland

EY s Global Economic Outlook Ireland January 2018 The global economy is healthy Mark Gregory Chief Economist, UK mgregory@uk.ey.com linkedin.com/in/markgregoryuk Neil Gibson Chief Economist, Ireland neil.gibson1@ie.ey.com

EY s Global Economic Outlook Ireland January 2018 The global economy is healthy Mark Gregory Chief Economist, UK mgregory@uk.ey.com linkedin.com/in/markgregoryuk Neil Gibson Chief Economist, Ireland neil.gibson1@ie.ey.com

Global MT outlook: Will the crisis in emerging markets derail the recovery?

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Mexico Economic Outlook 3Q18. August 2018

Mexico Economic Outlook 3Q18 August 2018 Key messages Global growth continues, but risks are intensifying. The economy grew 2.1% in the first half of the year. Downward bias in our growth forecast for

Mexico Economic Outlook 3Q18 August 2018 Key messages Global growth continues, but risks are intensifying. The economy grew 2.1% in the first half of the year. Downward bias in our growth forecast for

Research Briefing Global

Research Briefing Global Top ten calls for 2017 Trumponomics leads the way Economist Adam Slater Lead Economist +44(0)1865268934 Our top ten calls for 2017 are, not surprisingly, dominated by the impact

Research Briefing Global Top ten calls for 2017 Trumponomics leads the way Economist Adam Slater Lead Economist +44(0)1865268934 Our top ten calls for 2017 are, not surprisingly, dominated by the impact

CONTENTS CONTACT. AUTHORS Gerard Burg Tom Taylor EMBARGOED UNTIL: 11.30AM THURSDAY 15 MARCH 2018 THE FORWARD VIEW GLOBAL. NAB Group Economics

EMBARGOED UNTIL: 11.AM THURSDAY 1 MARCH 1 THE FORWARD VIEW GLOBAL MARCH 1 Summary sabre rattling ahead of a potential trade war? The global economic environment remains the most encouraging it has been

EMBARGOED UNTIL: 11.AM THURSDAY 1 MARCH 1 THE FORWARD VIEW GLOBAL MARCH 1 Summary sabre rattling ahead of a potential trade war? The global economic environment remains the most encouraging it has been

Global economic issues and the impact on Shipping

1st Annual Marine Money Cyprus Forum Global economic issues and the impact on Shipping Andreas Assiotis, PhD 26 April 2017 Table of contents 1 2 3 4 5 Economic Fundamentals and Global Drivers 3 Global

1st Annual Marine Money Cyprus Forum Global economic issues and the impact on Shipping Andreas Assiotis, PhD 26 April 2017 Table of contents 1 2 3 4 5 Economic Fundamentals and Global Drivers 3 Global

ECONOMIC OUTLOOK AND THE US LODGING INDUSTRY. Aran Ryan Director Tourism

ECONOMIC OUTLOOK AND THE US LODGING INDUSTRY Aran Ryan Director aran.ryan@tourismeconomics.com @AranRyan1 March 22, 2017 Some historical perspective Room demand expansion continues Pace of demand growth

ECONOMIC OUTLOOK AND THE US LODGING INDUSTRY Aran Ryan Director aran.ryan@tourismeconomics.com @AranRyan1 March 22, 2017 Some historical perspective Room demand expansion continues Pace of demand growth

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

UNCERTAINTY DIMS EURO AREA GROWTH

EBF Economic Outlook Nr 44 November 2018 2018 AUTUMN OUTLOOK ON THE EURO AREA ECONOMY IN 2018-2019 UNCERTAINTY DIMS EURO AREA GROWTH EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen, Chair of

EBF Economic Outlook Nr 44 November 2018 2018 AUTUMN OUTLOOK ON THE EURO AREA ECONOMY IN 2018-2019 UNCERTAINTY DIMS EURO AREA GROWTH EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen, Chair of

Economic and market snapshot for January 2016

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

Global Economic Outlook - April 2018

Global Economic Outlook - April 2018 April 12, 2018 by Carl Tannenbaum, Ryan James Boyle, Brian Liebovich, Vaibhav Tandon of Northern Trust Entering 2018, our outlook was uniformly upbeat. Fiscal stimulus

Global Economic Outlook - April 2018 April 12, 2018 by Carl Tannenbaum, Ryan James Boyle, Brian Liebovich, Vaibhav Tandon of Northern Trust Entering 2018, our outlook was uniformly upbeat. Fiscal stimulus

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

The Outlook for the World Economy

AIECE General Meeting Brussels, 14/15 November 218 The Outlook for the World Economy Downward risks are rising Klaus-Jürgen Gern Kiel Institute for the World Economy Forecasting Center Global growth has

AIECE General Meeting Brussels, 14/15 November 218 The Outlook for the World Economy Downward risks are rising Klaus-Jürgen Gern Kiel Institute for the World Economy Forecasting Center Global growth has

Teetering on the brink: is the world heading for another financial crisis?

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Eurozone Economic Watch. April 2018

Eurozone Economic Watch April 2018 Eurozone: solid growth and broadly unchanged projections, with protectionist risks BBVA Research - Eurozone Economic Watch / 2 Confidence has weakened in 1Q18 since the

Eurozone Economic Watch April 2018 Eurozone: solid growth and broadly unchanged projections, with protectionist risks BBVA Research - Eurozone Economic Watch / 2 Confidence has weakened in 1Q18 since the

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

Eurozone Economic Watch

BBVA Research Eurozone Economic Watch November 2018 / 1 Eurozone Economic Watch November 2018 Eurozone: Growth to recover in 4Q18, but concerns about the slowdown next year are growing Eurozone GDP growth

BBVA Research Eurozone Economic Watch November 2018 / 1 Eurozone Economic Watch November 2018 Eurozone: Growth to recover in 4Q18, but concerns about the slowdown next year are growing Eurozone GDP growth

LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY

OVERVIEW: The European economy has moved into lower gear amid still robust domestic fundamentals. GDP growth is set to continue at a slower pace. LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY Interrelated

OVERVIEW: The European economy has moved into lower gear amid still robust domestic fundamentals. GDP growth is set to continue at a slower pace. LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY Interrelated

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

HIGH UNCERTAINTY WEIGHING ON GLOBAL GROWTH

HIGH UNCERTAINTY WEIGHING ON GLOBAL GROWTH Summary The expansion may now have peaked. Global growth is projected to settle at 3.7% in 2018 and 2019, marginally below pre-crisis norms, with downside risks

HIGH UNCERTAINTY WEIGHING ON GLOBAL GROWTH Summary The expansion may now have peaked. Global growth is projected to settle at 3.7% in 2018 and 2019, marginally below pre-crisis norms, with downside risks

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR ECONOMIC AND FINANCIAL AFFAIRS. September 2006 Interim forecast

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR ECONOMIC AND FINANCIAL AFFAIRS September 26 Interim forecast Press conference of 6 September 26 European economic growth speeding up, boosted by buoyant domestic

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR ECONOMIC AND FINANCIAL AFFAIRS September 26 Interim forecast Press conference of 6 September 26 European economic growth speeding up, boosted by buoyant domestic

GLOBAL OUTLOOK ECONOMIC WATCH. July 2017

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

An economic update Craig Botham, Economist May 2017

An economic update Craig Botham, Economist May 2017 2016 image of the year Donald and Nigel at Trump towers Source: Splashnews.com. 1 Key issues UK: the election, Brexit and beyond Europe: out of the woods?

An economic update Craig Botham, Economist May 2017 2016 image of the year Donald and Nigel at Trump towers Source: Splashnews.com. 1 Key issues UK: the election, Brexit and beyond Europe: out of the woods?

Global Economics Monthly Review

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

The Deloitte CFO Survey. Defensive and watchful Q Authors. Key contacts

Q2 The Deloitte CFO Survey Defensive and watchful The second quarter survey of Chief Financial Officers reveals growing concerns about Brexit on the part of CFOs and a marked shift towards more defensive

Q2 The Deloitte CFO Survey Defensive and watchful The second quarter survey of Chief Financial Officers reveals growing concerns about Brexit on the part of CFOs and a marked shift towards more defensive

Monthly Economic Insight

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

PMI and economic outlook

PMI and economic outlook Chris Williamson Chief Business Economist, IHS Markit 1 st November 2017 2 PMI coverage Current coverage Expansion pipeline 40+ Countries covered 27,000+ Companies surveyed every

PMI and economic outlook Chris Williamson Chief Business Economist, IHS Markit 1 st November 2017 2 PMI coverage Current coverage Expansion pipeline 40+ Countries covered 27,000+ Companies surveyed every

Global Travel Service

15 Nov 2018 Global Travel Service Global Highlights, November 2018 Economists Adam Sacks President of Tourism Economics asacks@oxfordeconomics. com David Goodger Director of Tourism Economics dgoodger@oxfordeconomi

15 Nov 2018 Global Travel Service Global Highlights, November 2018 Economists Adam Sacks President of Tourism Economics asacks@oxfordeconomics. com David Goodger Director of Tourism Economics dgoodger@oxfordeconomi

U.S. Economic Outlook with Focus on Maine: Shining Amidst Global Gloom

U.S. Economic Outlook with Focus on Maine: Shining Amidst Global Gloom Michael Dolega Senior Economist, TD Economics 15 Annual MEREDA Forecast Conference Portland, Maine January, 15 Key Themes Global economic

U.S. Economic Outlook with Focus on Maine: Shining Amidst Global Gloom Michael Dolega Senior Economist, TD Economics 15 Annual MEREDA Forecast Conference Portland, Maine January, 15 Key Themes Global economic

BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook

7 March 2018 ECONOMIC REVIEW March 2018 BNM MPC BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook Overnight Policy Rate maintained at 3.25%. In line with our expectation, overnight policy rate,

7 March 2018 ECONOMIC REVIEW March 2018 BNM MPC BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook Overnight Policy Rate maintained at 3.25%. In line with our expectation, overnight policy rate,

Fed monetary policy amid a global backdrop of negative interest rates

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

The Prospects Service

The Prospects Service LEADING ECONOMIC ANALYSIS, FORECASTS AND DATA Global Prospects, January 2017 Toplines The world economy remains in a stage of heightened uncertainty, with ongoing Brexit negotiations,

The Prospects Service LEADING ECONOMIC ANALYSIS, FORECASTS AND DATA Global Prospects, January 2017 Toplines The world economy remains in a stage of heightened uncertainty, with ongoing Brexit negotiations,

OUTLOOK FOR THE GLOBAL ECONOMY AND TRAVEL

January 2018 OUTLOOK FOR THE GLOBAL ECONOMY AND TRAVEL Adam Sacks President Tourism Economics @adam_sacks August 2018 Outline The Outlook for the Economy and Travel Views on the global economy Risks Will

January 2018 OUTLOOK FOR THE GLOBAL ECONOMY AND TRAVEL Adam Sacks President Tourism Economics @adam_sacks August 2018 Outline The Outlook for the Economy and Travel Views on the global economy Risks Will

Market volatility to continue

How much more? Renewed speculation that financial institutions may report increased US subprime-related losses has sent equity markets tumbling. How much more bad news can investors expect going forward?

How much more? Renewed speculation that financial institutions may report increased US subprime-related losses has sent equity markets tumbling. How much more bad news can investors expect going forward?

Latin America Outlook 3Q18

BBVA Research - Latin America Outlook 3Q18 / 1 Latin America Outlook 3Q18 July Key messages Global growth remains robust, but risks also increase. Robust growth in the US on the back of fiscal stimulus.

BBVA Research - Latin America Outlook 3Q18 / 1 Latin America Outlook 3Q18 July Key messages Global growth remains robust, but risks also increase. Robust growth in the US on the back of fiscal stimulus.

Global Economic Watch

BBVA Research Global Economic Watch July 2018 / 1 Global Economic Watch July 2018 Steady global growth, but risks intensify Our BBVA-GAIN model projects that global growth could remain slightly above 1%

BBVA Research Global Economic Watch July 2018 / 1 Global Economic Watch July 2018 Steady global growth, but risks intensify Our BBVA-GAIN model projects that global growth could remain slightly above 1%

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

Atradius Country Report. Main Western European Markets - May 2018

Atradius Country Report Main Western European Markets - May 8 Contents Austria Belgium Denmark 7 France 9 Germany Ireland Italy The Netherlands 7 Spain 9 Sweden Switzerland United Kingdom Print all Austria

Atradius Country Report Main Western European Markets - May 8 Contents Austria Belgium Denmark 7 France 9 Germany Ireland Italy The Netherlands 7 Spain 9 Sweden Switzerland United Kingdom Print all Austria

Emerging Markets Weekly Economic Briefing

Emerging Markets Weekly Economic Briefing The risks of renewed capital flight from emerging markets Recent episodes of capital flight from emerging markets have highlighted the vulnerability of a number

Emerging Markets Weekly Economic Briefing The risks of renewed capital flight from emerging markets Recent episodes of capital flight from emerging markets have highlighted the vulnerability of a number

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

The Economic Context for Budget 2019

The Economic Context for Budget 219 1 October 218 Oliver Mangan Chief Economist AIB Steady global growth forecast but GDP (Vol Change) 217 218(f) 219(f) 22(f) World 3.7 3.7 3.7 3.7 Advanced Economies 2.3

The Economic Context for Budget 219 1 October 218 Oliver Mangan Chief Economist AIB Steady global growth forecast but GDP (Vol Change) 217 218(f) 219(f) 22(f) World 3.7 3.7 3.7 3.7 Advanced Economies 2.3

JULY 2018 Summary trade risks to the fore

EMBARGOED UNTIL: 11.3AM THURSDAY 1 JULY 18 THE FORWARD VIEW GLOBAL JULY 18 Summary trade risks to the fore The imposition on July of a % tariff by the on around $3b of imports from China, immediately followed

EMBARGOED UNTIL: 11.3AM THURSDAY 1 JULY 18 THE FORWARD VIEW GLOBAL JULY 18 Summary trade risks to the fore The imposition on July of a % tariff by the on around $3b of imports from China, immediately followed

Leumi. Global Economics Monthly Review. Gil M. Bufman, Chief Economist Arie Tal, Research Economist. March 13, 2018

Global Economics Monthly Review March 13, 2018 Gil M. Bufman, Chief Economist Arie Tal, Research Economist The Finance Division, Economics Department Please note that we will not publish the monthly review

Global Economics Monthly Review March 13, 2018 Gil M. Bufman, Chief Economist Arie Tal, Research Economist The Finance Division, Economics Department Please note that we will not publish the monthly review

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Global Economic Outlook Brittle Strength

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

Global Economic Outlook Brittle Strength RISI North American Conference October 2017 Lasse Sinikallas Director Macroeconomics Agenda 1. Global Snapshot Steady 2. North America Performing 3. China In Transition

Asia Watch. The US giveth, the US taketh away. Group Economics Emerging Markets Research. Group Economics: Enabling smart decisions.

Asia Watch Group Economics Emerging Markets Research 1 June 18 Arjen van Dijkhuizen Senior Economist Tel: +31 68 85 arjen.van.dijkhuizen@nl.abnamro.com The US giveth, the US taketh away Growth momentum

Asia Watch Group Economics Emerging Markets Research 1 June 18 Arjen van Dijkhuizen Senior Economist Tel: +31 68 85 arjen.van.dijkhuizen@nl.abnamro.com The US giveth, the US taketh away Growth momentum

World Economy: Prospects and Risks Masahiro Kawai Graduate School of Public Policy Univ. of Tokyo

World Economy: Prospects and Risks Masahiro Kawai Graduate School of Public Policy Univ. of Tokyo Seoul 13 June 2017 Prospects of the World Economy The world economy is growing in 2017 The US Fed continues

World Economy: Prospects and Risks Masahiro Kawai Graduate School of Public Policy Univ. of Tokyo Seoul 13 June 2017 Prospects of the World Economy The world economy is growing in 2017 The US Fed continues

Outlook for the Economy and Travel Outlook for the Global Economy and Travel

Outlook for the Economy and Travel Outlook for the Global Economy and Travel Adam Sacks President Tourism Economics @adam_sacks Adam Sacks President Tourism Economics @adam_sacks Outline The Outlook for

Outlook for the Economy and Travel Outlook for the Global Economy and Travel Adam Sacks President Tourism Economics @adam_sacks Adam Sacks President Tourism Economics @adam_sacks Outline The Outlook for

Global Economy & the Machine Tool Outlook. Jan 2010 Rhys Herbert

Global Economy & the Machine Tool Outlook Jan 21 Rhys Herbert rherbert@oxfordeconomics.com Which scenario do you favour? Short-term outlook (a) W -shaped cycle Growth initially boosted by inventory rebuild

Global Economy & the Machine Tool Outlook Jan 21 Rhys Herbert rherbert@oxfordeconomics.com Which scenario do you favour? Short-term outlook (a) W -shaped cycle Growth initially boosted by inventory rebuild

Finland falling further behind euro area growth

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

Summary. Economic Update 1 / 7 January 2019

Economic Update Economic Update 1 / 7 Summary 2 Global Global economic growth is expected to have peaked in 2018 at 3.0% and to ease to 2.8% in 2019. Tightening global monetary conditions, fading US fiscal

Economic Update Economic Update 1 / 7 Summary 2 Global Global economic growth is expected to have peaked in 2018 at 3.0% and to ease to 2.8% in 2019. Tightening global monetary conditions, fading US fiscal

OVERVIEW. The EU recovery is firming. Table 1: Overview - the winter 2014 forecast Real GDP. Unemployment rate. Inflation. Winter 2014 Winter 2014

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

OVERVIEW The EU recovery is firming Europe's economic recovery, which began in the second quarter of 2013, is expected to continue spreading across countries and gaining strength while at the same time

ECONOMIC RECOVERY AT CRUISE SPEED

EBF Economic Outlook Nr 43 May 2018 2018 SPRING OUTLOOK ON THE EURO AREA ECONOMIES IN 2018-2019 ECONOMIC RECOVERY AT CRUISE SPEED EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen - Chair of the

EBF Economic Outlook Nr 43 May 2018 2018 SPRING OUTLOOK ON THE EURO AREA ECONOMIES IN 2018-2019 ECONOMIC RECOVERY AT CRUISE SPEED EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen - Chair of the

3 rd Quarter 2018 House View Cautiously Optimistic

3 rd Quarter 2018 House View Cautiously Optimistic Global Backdrop The global economy remains healthy no economic signs of a global slowdown Monetary policy tightening in the US but Fiscal stimulus is

3 rd Quarter 2018 House View Cautiously Optimistic Global Backdrop The global economy remains healthy no economic signs of a global slowdown Monetary policy tightening in the US but Fiscal stimulus is

GETTING STRONGER, BUT TENSIONS ARE RISING

GETTING STRONGER, BUT TENSIONS ARE RISING Summary The world economy will continue to strengthen in 2018 and 2019, with global GDP growth projected to rise to about 4%, from 3.7% in 2017. Stronger investment,

GETTING STRONGER, BUT TENSIONS ARE RISING Summary The world economy will continue to strengthen in 2018 and 2019, with global GDP growth projected to rise to about 4%, from 3.7% in 2017. Stronger investment,

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO)

") Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Global economic outlook: Are we headed for another global recession? Sarah Hunter Head of Americas macro consulting

Global economic outlook: Are we headed for another global recession? Sarah Hunter Head of Americas macro consulting shunter@oxfordeconomics.com 10 th March 2016 Oxford Economics forecast highlights Baseline

Global economic outlook: Are we headed for another global recession? Sarah Hunter Head of Americas macro consulting shunter@oxfordeconomics.com 10 th March 2016 Oxford Economics forecast highlights Baseline

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook February 2015 Stocks to Fully Rebound from Late 2014/Early 2015 Sell-off with ECB Launching Aggressive QE, Rate Cuts by Several

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook February 2015 Stocks to Fully Rebound from Late 2014/Early 2015 Sell-off with ECB Launching Aggressive QE, Rate Cuts by Several

Eurozone. Economic Watch FEBRUARY 2017

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Economic Outlook In the Shoes of an FOMC Member

Economic Outlook In the Shoes of an FOMC Member This material must be read in conjunction with the disclosure statement. 9 April 2018 PRESENTED BY: MARKUS SCHOMER Chief Economist PineBridge Investments

Economic Outlook In the Shoes of an FOMC Member This material must be read in conjunction with the disclosure statement. 9 April 2018 PRESENTED BY: MARKUS SCHOMER Chief Economist PineBridge Investments

Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist

May 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Slower but Still Solid Economic Growth in the First Quarter;

May 218 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Chief Economist Senior Economic Advisor Senior Economist Economist Executive Summary Slower but Still Solid Economic Growth in the First Quarter;

Global Macroeconomic Outlook March LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA FAX

March 208 M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA 02090 78 47 3500 FAX 78 47 34 Global Economic Outlook The IMF continues to forecast a slight pick-up in growth

March 208 M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA 02090 78 47 3500 FAX 78 47 34 Global Economic Outlook The IMF continues to forecast a slight pick-up in growth

AUGUST 2018 Summary growth remains above trend, but risks a concern

EMBARGOED UNTIL: 11.3AM THURSDAY 1 AUGT 1 THE FORWARD VIEW GLOBAL AUGT 1 Summary growth remains above trend, but risks a concern As expected, after hitting a soft patch in Q1, major advanced economy growth

EMBARGOED UNTIL: 11.3AM THURSDAY 1 AUGT 1 THE FORWARD VIEW GLOBAL AUGT 1 Summary growth remains above trend, but risks a concern As expected, after hitting a soft patch in Q1, major advanced economy growth

Fund Management Diary

Fund Management Diary Meeting held on 11 th December 2018 Losing Momentum After a strong start to the year, global growth peaked in the first of 2018 and doesn t look like regaining momentum. Trade tensions

Fund Management Diary Meeting held on 11 th December 2018 Losing Momentum After a strong start to the year, global growth peaked in the first of 2018 and doesn t look like regaining momentum. Trade tensions

GLOBAL INVESTMENT OUTLOOK & STRATEGY

January 2018 John Praveen, PhD Managing Director FOLLOW US ON TWITTER: @prustrategist FOR MORE INFORMATION CONTACT: Kristin Meza Phone: 973-367-4104 Email: kristin.meza@ prudential.com PGIM is the Global

January 2018 John Praveen, PhD Managing Director FOLLOW US ON TWITTER: @prustrategist FOR MORE INFORMATION CONTACT: Kristin Meza Phone: 973-367-4104 Email: kristin.meza@ prudential.com PGIM is the Global

Fund Management Diary

Fund Management Diary Meeting held on 12 th March 2019 Earnings to weigh on emerging market equities A slowdown in both the United States and Chinese economies will weigh heavily on export growth in the

Fund Management Diary Meeting held on 12 th March 2019 Earnings to weigh on emerging market equities A slowdown in both the United States and Chinese economies will weigh heavily on export growth in the

CHINA S ECONOMY AT A GLANCE

CHINA S ECONOMY AT A GLANCE APRIL 218 CONTENTS Key points 2 Gross Domestic Product 3 Industrial Production 4 Investment 5 International trade - trade balance and imports International trade - exports 6

CHINA S ECONOMY AT A GLANCE APRIL 218 CONTENTS Key points 2 Gross Domestic Product 3 Industrial Production 4 Investment 5 International trade - trade balance and imports International trade - exports 6

The Prospects Service

The Prospects Service LEADING ECONOMIC ANALYSIS, FORECASTS AND DATA Global Prospects, September 2017 Toplines The combination of rising consumer confidence, low borrowing costs and declining unemployment

The Prospects Service LEADING ECONOMIC ANALYSIS, FORECASTS AND DATA Global Prospects, September 2017 Toplines The combination of rising consumer confidence, low borrowing costs and declining unemployment

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

Summary. Economic Update 1 / 7 May Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018.

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

The Thai economy is viewed to moderate from last assessment from the intensified impact of the euro area s crisis on merchandise exports, which, in

1 I. Economic and inflation outlook II. Monetary policy stances going forward 2 I. Economic and inflation outlook II. Monetary policy stances going forward 3 The Thai economy is viewed to moderate from

1 I. Economic and inflation outlook II. Monetary policy stances going forward 2 I. Economic and inflation outlook II. Monetary policy stances going forward 3 The Thai economy is viewed to moderate from

Edited Minutes of the Monetary Policy Committee Meeting (No. 8/2018) 19 December 2018, Bank of Thailand Publication Date: 2 January 2019

19 December 2018, Bank of Thailand Publication Date: 2 January 2019") Edited Minutes of the Monetary Policy Committee Meeting (No. 8/2018) 19 December 2018, Bank of Thailand Publication Date: 2 January 2019 Members Present Veerathai Santiprabhob (Chairman), Mathee Supapongse

Edited Minutes of the Monetary Policy Committee Meeting (No. 8/2018) 19 December 2018, Bank of Thailand Publication Date: 2 January 2019 Members Present Veerathai Santiprabhob (Chairman), Mathee Supapongse

Insight. Market View Q Cash

Insight Market View Q 18 This document presents a high level summary of our investment views. As we are making decisions about what to buy and sell in your portfolio, we want to be accountable to you by

Insight Market View Q 18 This document presents a high level summary of our investment views. As we are making decisions about what to buy and sell in your portfolio, we want to be accountable to you by

Growth and Inflation Prospects and Monetary Policy

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016.

PRICE POINT February 2016 Timely intelligence and analysis for our clients. Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016. EXECUTIVE SUMMARY Kenneth Orchard Portfolio

PRICE POINT February 2016 Timely intelligence and analysis for our clients. Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016. EXECUTIVE SUMMARY Kenneth Orchard Portfolio

Summary. Economic Update 1 / 7 December 2017

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

Monetary Policy Report, September 2017

No. 52/2017 Monetary Policy Report, September 2017 Mr. Jaturong Jantarangs, Assistant Governor of the Bank of Thailand (BOT) and Secretary of the Monetary Policy Committee (MPC), released the September

No. 52/2017 Monetary Policy Report, September 2017 Mr. Jaturong Jantarangs, Assistant Governor of the Bank of Thailand (BOT) and Secretary of the Monetary Policy Committee (MPC), released the September

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

FY2016, FY2017 Economic Outlook The global economy will gradually pick up. Will Trump change the world?

Mizuho Economic Outlook & Analysis December 2016 FY2016, FY2017 Economic Outlook The global economy will gradually pick up. Will Trump change the world? The Japanese economy will lift off from the landing

Mizuho Economic Outlook & Analysis December 2016 FY2016, FY2017 Economic Outlook The global economy will gradually pick up. Will Trump change the world? The Japanese economy will lift off from the landing

Forex and Interest Rate Outlook AIB Treasury Economic Research Unit

Forex and Interest Rate Outlook 22nd November 2017 Global economic recovery gathering momentum, but inflation remains very subdued Central banks patient on policy tightening. Rates rise at a slow pace

Forex and Interest Rate Outlook 22nd November 2017 Global economic recovery gathering momentum, but inflation remains very subdued Central banks patient on policy tightening. Rates rise at a slow pace

Key developments and outlook

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

Global Economic Outlook - July 2017

Global Economic Outlook - July 2017 June 28, 2017 by Carl Tannenbaum, Asha Bangalore, Ankit Mital, Brian Liebovich of Northern Trust Global economic activity has generally been good during the first six

Global Economic Outlook - July 2017 June 28, 2017 by Carl Tannenbaum, Asha Bangalore, Ankit Mital, Brian Liebovich of Northern Trust Global economic activity has generally been good during the first six

Global Economic Outlook

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

2018 ECONOMIC OUTLOOK

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.*

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

FUNDAMENTALS. Is 2017 the year of Trumpflation?

December 2016 Trumpflation* Follow us @LGIM #Fundamentals FUNDAMENTALS Is 2017 the year of Trumpflation? Although the cycle is maturing, global growth should hold up well next year. However, increasing

December 2016 Trumpflation* Follow us @LGIM #Fundamentals FUNDAMENTALS Is 2017 the year of Trumpflation? Although the cycle is maturing, global growth should hold up well next year. However, increasing

Global Update. 6 th October, Global Prospects. Contacts: Madan Sabnavis Chief Economist

Global Update Global Prospects 6 th October, 2010 Contacts: Madan Sabnavis Chief Economist 91-022-6754 3489 Samruddha Paradkar Associate Economist 91-022-6754 3407 Krithika Subramanian Associate Economist

Global Update Global Prospects 6 th October, 2010 Contacts: Madan Sabnavis Chief Economist 91-022-6754 3489 Samruddha Paradkar Associate Economist 91-022-6754 3407 Krithika Subramanian Associate Economist

The Economic and Political Outlook. By Roger Bootle

The Economic and Political Outlook By Roger Bootle 1. Agenda The World, China and America. Recovery in the euro-zone. Political worries in Europe. The UK economy. Brexit opportunities and challenges. The

The Economic and Political Outlook By Roger Bootle 1. Agenda The World, China and America. Recovery in the euro-zone. Political worries in Europe. The UK economy. Brexit opportunities and challenges. The

Financial Market Outlook: Stock Rally Continues with Faster & Stronger GDP Rebound, Earnings Recovery & Liquidity

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

November PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone: