Global Risk Outlook May 2016

|

|

|

- Mercy Woods

- 5 years ago

- Views:

Transcription

1 Global Risk Outlook May 2016 Scott Livermore Managing Director and COO

2 About Oxford Economics Oxford Economics is a world leader in global forecasting and quantitative analysis. Our worldwide client base comprises over 1,000 international corporations, financial institutions, government organizations and universities. Founded in 1981 as a joint venture with Oxford University, Oxford Economics is now a leading independent economic consultancy. Headquartered in Oxford, with offices around the world, we employ 250 people, including 150 economists, and a network of 500 contributing researchers. The rigor of our analysis, caliber of staff and links with other leading research groups make us a trusted resource for decision makers.

3 Markets have rebounded. but stress is palpable US: Market volatility CBOE Market Volatility Index, VIX To be updated Source: Haver Analytics 3

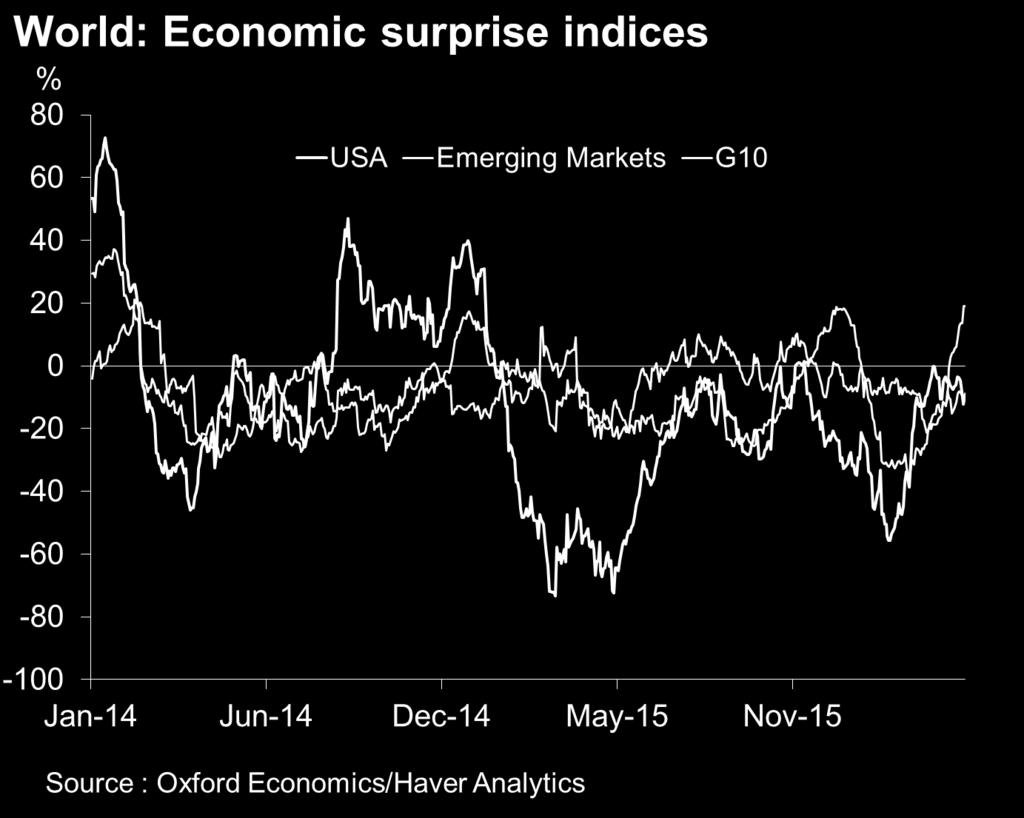

4 Economic news less disappointing 4

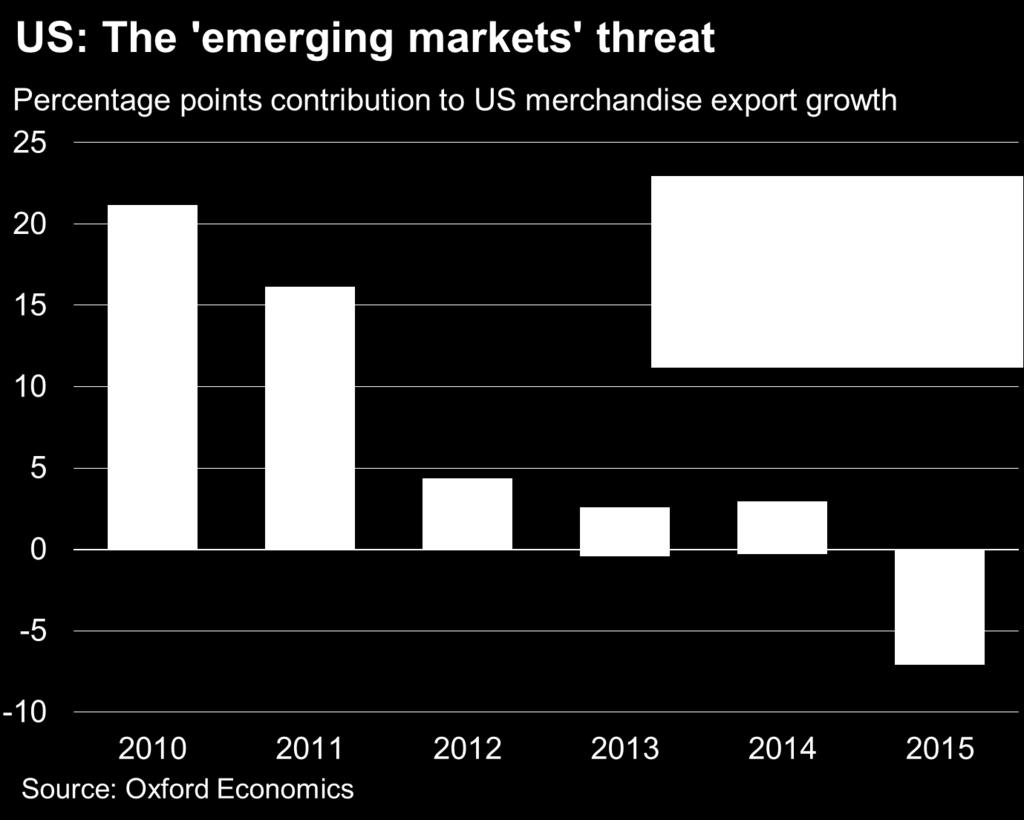

5 Eurozone is fastest growing advanced economy?? Only in Q1s! 5

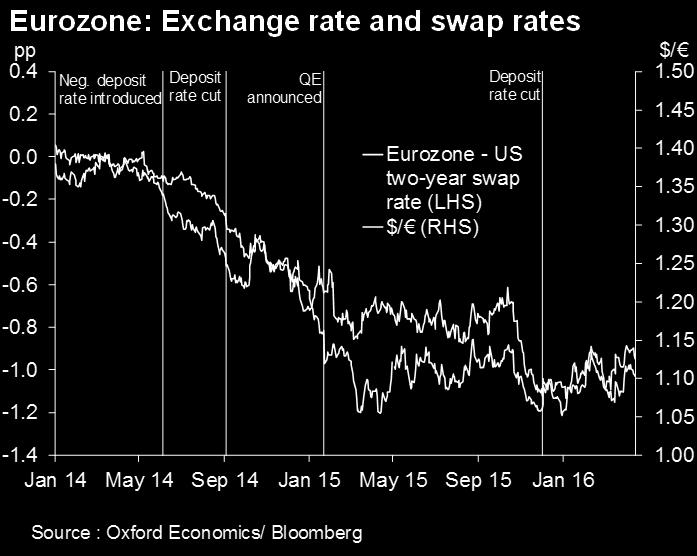

6 Inflation to rebound but ECB closely monitoring 6

7 The end of 2015 slowdown is proving to be sticky March

8 Usual culprits behind slowdown Culprits: Strong US dollar Weak global growth Depressed oil and gas activity + Modest consumer spending 8

9 Employment growth is robust

10 Business investment to remain sluggish in 2016

11 2% growth miss is likely

12 Global headwinds are restraining net exports

13 Leading indicators suggest EM weakness BRICs: Manufacturing Purchasing Managers' Index Index, breakeven level= China Russia India Brazil Source : PMI/Markit/China NBS/Haver Analytics 13

14 Who are the out/underperformers within EMs? Emerging markets: GDP growth (2016) India China Indonesia Peru EMs Turkey Nigeria Colombia Mexico World Chile S. Africa Argentina Russia Brazil % year Source: Oxford Economics 14

15 Risks remain skewed to downside 15

16 China the biggest concern 16

17 Real growth slowed more than NBS data show 17

18 China: Generous monetary and fiscal policy Bank lending and total social financing % yoy Source: Oxford Economics, CEIC Data Bank lending TSF Fiscal policy % GDP, 12mma Revenues Expenditures Balance (RHS) % GDP, 12mma Source: Oxford Economics, CEIC Data

19 Excess supply in real estate significant China: Excess supply in the real estate sector years of supply mn m² Average from Ratio of property under construction to sales (lhs) Average Vacant floor space (rhs) Source : Oxford Economics/Haver Analytics 19

20 and excess capacity in industry still on the rise Production and capacity in industry 2007= Value added in industry Production capacity in industry* Excess capacity (RHS) % Source: Oxford Economics, CEIC Data * From growth accounting 20

21 Our modelling expertise sets us apart Oxford Economics has developed the world s leading globally integrated economic model, relied on by over 150 leading organisations around the world. Our model replicates the world economy by interlinking 46 countries, 6 regional blocs and the Eurozone. It is available with 5, 10 and 25- year forecasting horizon. 29 additional country models being added from May. The global economic model feeds into a series of industry, sub-regional and city models. So, you can quantify the impact of global events on a consistent basis down to your industry and local markets. Our team of 150 economists set underlying global assumptions and ensure that the data, forecasts and formulas in these models are fully up-to-date.

22 Chinese hard landing China: GDP % year 16 Forecast Baseline China hard landing Source : Oxford Economics/Haver Analytics 22

23 Chinese hard landing World: GDP % year 6 Forecast 5 4 Baseline China hard landing Source : Oxford Economics/Haver Analytics 23

24 Chinese hard landing World oil price $/barrel 160 Forecast Baseline China hard landing Source : Oxford Economics/Haver Analytics

25 Chinese hard landing World: Exchange rates vs US$ average % change relative to change in USDCNY * Japan Eurozone UK Singapore Thailand Philippines India Taiwan Indonesia Korea Brazil Chile Argentina Australia Turkey Malaysia S. Africa Mexico Russia * between Aug 10 - Aug 25 and Dec 31 - Jan 8; values above 1 imply a stronger depreciation against US$ than that of the RMB Source : Oxford Economics / Haver Analytics The domestic policy response Chinese authorities embark on a range of actions, including faster policy rate cuts and currency devaluation Global impact and policy actions The slowdown weighs on world trade, commodity prices and other asset prices and global monetary policy adjusts accordingly Global exchange rates adjust sharply in line with recent episodes of stronger RMB weakening 25

26 Asia and commodity producers hit hardest World: GDP in downside scenario % difference in level of GDP versus baseline, 2017 UK USA Poland Eurozone Canada Philippines Thailand Indonesia Turkey Brazil Argentina S.Africa Japan India Malaysia Australia Mexico Korea Chile Taiwan Russia Hong Kong Source : Oxford Economics 26

27 US Treasury yields fall below 2% US: Federal funds rate % 6 Forecast US: 10-year government bond yields %, EOP 6 Forecast China hard landing 4 Baseline 3 Baseline China hard landing Source : Oxford Economics/Haver Analytics Source : Oxford Economics/Haver Analytics 27

28 Remain enjoy a narrow lead in the polls

29 Option prices imply 15% depreciation post-brexit

30 Investor & corporate confidence would be hit

31 GDP impact: noticeable but not catastrophic

32 Risks remain skewed to downside 32

33 with significant real economy implications 33

34 China the biggest concern 34

35 Trump: trade protectionism Estimated negative impact from Trumps' proposed trade tariffs (% change in levels vs our base case of no new tariffs) Consumer Year GDP Employment Spending Inflation * Source: Oxford Economics * Inflation rate under scenario (base case 2.3%) The risk of a global trade war would unfold, which would yield much more negative implications than our scenario illustrates. 35

36 Trump: tax 36

37 37 Financial market contagion

38 Financial market contagion 38

39 Financial market contagion 39

40 40 Commodity demand weakness

41 Weak commodity demand causes financial strains 41

42 Weak commodity demand causes financial strains 42

43 Weak commodity demand causes financial strains 43

44 Weak commodity demand causes financial strains 44

45 45 Geopolitical tensions

46 Geopolitical tensions scenario 46

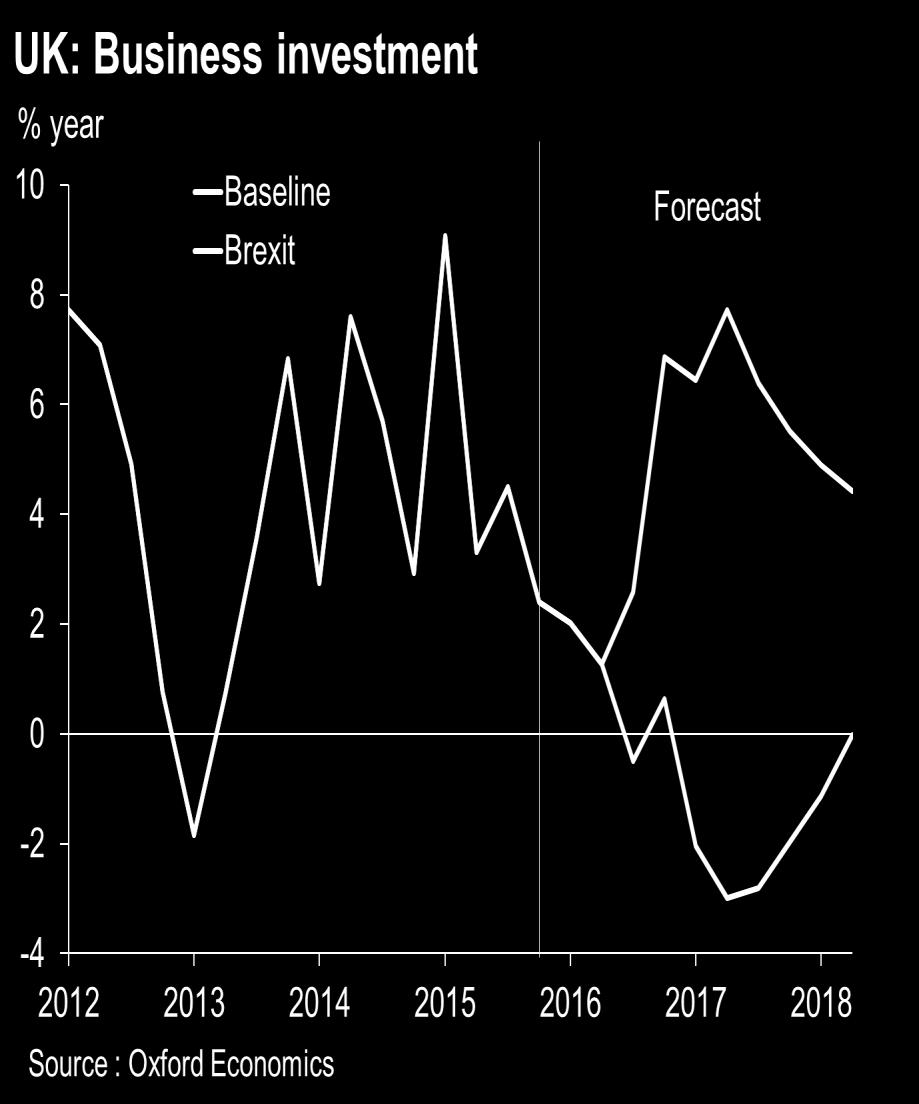

47 Geopolitical tensions scenario 47

48 48 Global upturn

49 Global upturn 49

50 Global Risk Outlook May 2016 Scott Livermore

51 EUROPE: BREXIT economic impacts

52 Markets reacted badly to the referendum

53 We would expect gilt yields to move lower Would gilt yields rise? Modest increase in borrowing Ratings agencies likely to put UK on negative watch Short-term interest rates lower Any risk premia would soon fade if MPC demonstrated it was in control UK would remain a safe haven

54 Uncertainty could dampen activity in short-term

55 A weaker would drive up inflation but exporters in price-sensitive sectors would benefit

56 Brexit would pose a dilemma for policymakers Monetary policy Inflation moves above target by early-2017 But MPC have been happy to look through temporary, sterling-generated, overshoots before Recent dovishness suggests rate cut is the most likely response given growth concerns Fiscal policy OBR would judge government in breach of fiscal mandate & growth not weak enough to trigger escape clause Chancellor likely to plead extenuating circumstances

57 with significant implications for financial markets 57

58 and significant implications for commodities 58

59 and significant implications for policy 59

60 and significant implications for policy 60

61 and significant implications for policy 61

62 and significant implications for policy 62

63 and significant implications for policy 63

64 and significant implications for policy 64

65 Global economy: Feeble, Fickle & Fragmented World GDP growth for 2016: 2.3% slowest pace of global growth since Forecast for 2017 cut further to 2.7%. EMs economies expected to remain subpar. Strains in financial markets have abated but conditions still tighter conditions than end-2015, and global risks are still skewed to the downside. Slowdown in US is proving to be sticky, but fundamentals remain strong. Central banks increased use of unconventional policy tools lends support to near-term growth (Japan, EZ), but there are questions about marginal benefits. Key risk: financial market strains: confidence, wealth and credit shock China & EMs Ammunition? 65 Geopolitical?

66 Housing recovery remains very gradual Drivers: Income growth Low interest rates Modest home price inflation Pent-up demand 66

67 Labor market supporting domestic demand Eurozone: consumption and real income % y/y 4 Consumption % y/y RPDI % y/y Source : Oxford Economics/Haver Analytics 67

68 ISM manufacturing has rebounded The spread has narrowed between the manufacturing and non-manufacturing sectors 68

69 Today s Global Economic Model Oxford s Global Economic Model is the world s leading globally integrated macro model, used by over 140 clients around the world, including finance ministries, leading banks, and blue-chip companies. With a 30-year track record, the model provides a rigorous and consistent structure for forecasting, scenario analysis, stress testing and impact analysis. The model covers 46 countries in detail, plus the Eurozone, and provides headline forecasts for another 30 countries. Remaining countries are covered in trading blocs. Data and forecasts in the model are updated each month. The model is available with 5, 10 and 25- year forecast horizons. Oxford Economics provides telephone and support, and runs regular training workshops.

Fed monetary policy amid a global backdrop of negative interest rates

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Global economic outlook: Are we headed for another global recession? Sarah Hunter Head of Americas macro consulting

Global economic outlook: Are we headed for another global recession? Sarah Hunter Head of Americas macro consulting shunter@oxfordeconomics.com 10 th March 2016 Oxford Economics forecast highlights Baseline

Global economic outlook: Are we headed for another global recession? Sarah Hunter Head of Americas macro consulting shunter@oxfordeconomics.com 10 th March 2016 Oxford Economics forecast highlights Baseline

Teetering on the brink: is the world heading for another financial crisis?

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Economic Outlook. Macro Research Itaú Unibanco

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

What is driving US Treasury yields higher?

What is driving Treasury yields higher? " our programme for reducing our [Fed's] balance sheet, which began in October, is proceeding smoothly. Barring a very significant and unexpected weakening in the

What is driving Treasury yields higher? " our programme for reducing our [Fed's] balance sheet, which began in October, is proceeding smoothly. Barring a very significant and unexpected weakening in the

Emerging Markets Weekly Economic Briefing

Emerging Markets Weekly Economic Briefing The risks of renewed capital flight from emerging markets Recent episodes of capital flight from emerging markets have highlighted the vulnerability of a number

Emerging Markets Weekly Economic Briefing The risks of renewed capital flight from emerging markets Recent episodes of capital flight from emerging markets have highlighted the vulnerability of a number

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

GLOBAL MARKET OUTLOOK

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

GLOBAL OUTLOOK ECONOMIC WATCH. July 2017

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

GLOBAL OUTLOOK ECONOMIC WATCH July 2017 Positive global outlook, with projections revised across areas The global outlook remains positive. Our BBVA-GAIN model estimates global GDP growth at 1% QoQ in,

Global Economy & the Machine Tool Outlook. Jan 2010 Rhys Herbert

Global Economy & the Machine Tool Outlook Jan 21 Rhys Herbert rherbert@oxfordeconomics.com Which scenario do you favour? Short-term outlook (a) W -shaped cycle Growth initially boosted by inventory rebuild

Global Economy & the Machine Tool Outlook Jan 21 Rhys Herbert rherbert@oxfordeconomics.com Which scenario do you favour? Short-term outlook (a) W -shaped cycle Growth initially boosted by inventory rebuild

Oxford Economics: Macromodelling. contagion & downside risks. Keith Church Director of Macroeconomic Modelling.

Oxford Economics: Macromodelling - capturing contagion & downside risks Keith Church Director of Macroeconomic Modelling kchurch@oxfordeconomics.com December 2015 Introduction How should macro models be

Oxford Economics: Macromodelling - capturing contagion & downside risks Keith Church Director of Macroeconomic Modelling kchurch@oxfordeconomics.com December 2015 Introduction How should macro models be

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

All the BRICs dampening world trade in 2015

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Global MT outlook: Will the crisis in emerging markets derail the recovery?

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Key Economic Challenges in Japan and Asia. Changyong Rhee IMF Asia and Pacific Department February

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES. Bank of Russia.

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES Bank of Russia July 218 < -1% -1-9% -9-8% -8-7% -7-6% -6-5% -5-4% -4-3% -3-2% -2-1% -1 % 1% 1 2% 2 3% 3 4% 4 5% 5 6% 6 7% 7 8% 8 9% 9 1% 1 11% 11

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY CHALLENGES Bank of Russia July 218 < -1% -1-9% -9-8% -8-7% -7-6% -6-5% -5-4% -4-3% -3-2% -2-1% -1 % 1% 1 2% 2 3% 3 4% 4 5% 5 6% 6 7% 7 8% 8 9% 9 1% 1 11% 11

The Outlook for the World Economy

AIECE General Meeting Brussels, 14/15 November 218 The Outlook for the World Economy Downward risks are rising Klaus-Jürgen Gern Kiel Institute for the World Economy Forecasting Center Global growth has

AIECE General Meeting Brussels, 14/15 November 218 The Outlook for the World Economy Downward risks are rising Klaus-Jürgen Gern Kiel Institute for the World Economy Forecasting Center Global growth has

Emerging Markets Weekly Economic Briefing

Emerging Markets Weekly Economic Briefing Global scenarios Slower growth in emerging markets is a key risk to our central forecast for the global economy. While more positive signs have recently appeared

Emerging Markets Weekly Economic Briefing Global scenarios Slower growth in emerging markets is a key risk to our central forecast for the global economy. While more positive signs have recently appeared

Growth and Inflation Prospects and Monetary Policy

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Growth and Inflation Prospects and Monetary Policy 1. Growth and Inflation Prospects and Monetary Policy The Thai economy expanded by slightly less than the previous projection due to weaker-than-anticipated

Economic Outlook January, 2012

Economic Outlook January, 2012 Summary Global economy Low global growth scenario, tail risks have become smaller. Risks (Debt Ceiling, elections in Italy, growth in Europe). Brazil Activity shows signs

Economic Outlook January, 2012 Summary Global economy Low global growth scenario, tail risks have become smaller. Risks (Debt Ceiling, elections in Italy, growth in Europe). Brazil Activity shows signs

AUGUST 2018 Summary growth remains above trend, but risks a concern

EMBARGOED UNTIL: 11.3AM THURSDAY 1 AUGT 1 THE FORWARD VIEW GLOBAL AUGT 1 Summary growth remains above trend, but risks a concern As expected, after hitting a soft patch in Q1, major advanced economy growth

EMBARGOED UNTIL: 11.3AM THURSDAY 1 AUGT 1 THE FORWARD VIEW GLOBAL AUGT 1 Summary growth remains above trend, but risks a concern As expected, after hitting a soft patch in Q1, major advanced economy growth

Asia Watch. Trade tensions risk to solid outlook. Group Economics Emerging Markets Research. Group Economics: Enabling smart decisions.

Asia Watch Group Economics Emerging Markets Research 1 March 1 Arjen van Dijkhuizen Senior Economist Tel: +31 5 arjen.van.dijkhuizen@nl.abnamro.com Trade tensions risk to solid outlook Growth EM Asia up

Asia Watch Group Economics Emerging Markets Research 1 March 1 Arjen van Dijkhuizen Senior Economist Tel: +31 5 arjen.van.dijkhuizen@nl.abnamro.com Trade tensions risk to solid outlook Growth EM Asia up

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016 Page 1 Themes Oil s Not Well A world of cheap petroleum Eastern Anxiety China attempts a difficult transition Growing Prospects Central

Rebalancing Economic Themes and Emerging Risks for the Balance of 2016 Page 1 Themes Oil s Not Well A world of cheap petroleum Eastern Anxiety China attempts a difficult transition Growing Prospects Central

Asian Insights What to watch closely in Asia in 2016

Asian Insights What to watch closely in Asia in 2016 Q1 2016 The past year turned out to be a year where one of the oldest investment adages came true: Sell in May and go away, don t come back until St.

Asian Insights What to watch closely in Asia in 2016 Q1 2016 The past year turned out to be a year where one of the oldest investment adages came true: Sell in May and go away, don t come back until St.

Indonesia Economic Outlook and Policy Challenges

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Global Economic Outlook

Global Economic Outlook The Institute of Strategic and International Studies Kuala Lumpur, November 2012 Mangal Goswami Mangal Goswami Deputy Director IMF Singapore Regional Training Institute Action Needed

Global Economic Outlook The Institute of Strategic and International Studies Kuala Lumpur, November 2012 Mangal Goswami Mangal Goswami Deputy Director IMF Singapore Regional Training Institute Action Needed

eregionaloutlooksincharts

eregionaloutlooksincharts (clickonregion) EastAsiaandPaci c EuropeandCentralAsia LatinAmericaandtheCaribbean MiddleEastandNorthAfrica SouthAsia Sub-SaharanAfrica The Economic Outlook for East Asia and

eregionaloutlooksincharts (clickonregion) EastAsiaandPaci c EuropeandCentralAsia LatinAmericaandtheCaribbean MiddleEastandNorthAfrica SouthAsia Sub-SaharanAfrica The Economic Outlook for East Asia and

Monetary Policy under Fed Normalization and Other Challenges

Javier Guzmán Calafell, Deputy Governor, Banco de México* Santander Latin America Day London, June 28 th, 2018 */ The opinions and views expressed in this document are the sole responsibility of the author

Javier Guzmán Calafell, Deputy Governor, Banco de México* Santander Latin America Day London, June 28 th, 2018 */ The opinions and views expressed in this document are the sole responsibility of the author

GLOBAL ECONOMIC OUTLOOK As good as it gets in 2018? Oliver Salmon Lead Economist

GLOBAL ECONOMIC OUTLOOK As good as it gets in 2018? Oliver Salmon Lead Economist osalmon@oxfordeconomics.com March 2018 Global synchronized upturn continues 2 as trade growth maintains healthy momentum

GLOBAL ECONOMIC OUTLOOK As good as it gets in 2018? Oliver Salmon Lead Economist osalmon@oxfordeconomics.com March 2018 Global synchronized upturn continues 2 as trade growth maintains healthy momentum

HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES

Key Points HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES Global growth has moderated, and it is expected to slow from 3 percent in 18 to.9 percent in. International trade and manufacturing

Key Points HIGHLIGHTS from CHAPTER 1: GLOBAL OUTLOOK DARKENING SKIES Global growth has moderated, and it is expected to slow from 3 percent in 18 to.9 percent in. International trade and manufacturing

Global investment event Winners and losers from the recent oil price rally

For client use only Global investment event Winners and losers from the recent oil price rally Since mid-2017, oil prices have been on an upward trend. Strong oil demand growth, OPECled production cuts,

For client use only Global investment event Winners and losers from the recent oil price rally Since mid-2017, oil prices have been on an upward trend. Strong oil demand growth, OPECled production cuts,

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

Global Economics Monthly Review

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

China: Beyond the headlines. Bill Maldonado HSBC Global Asset Management

China: Beyond the headlines Bill Maldonado HSBC Global Asset Management Are you a China Bull or a Bear? Source: Various news publications 2 Bear myth #1: Hard landing? GDP: Growth is slowing, but it s

China: Beyond the headlines Bill Maldonado HSBC Global Asset Management Are you a China Bull or a Bear? Source: Various news publications 2 Bear myth #1: Hard landing? GDP: Growth is slowing, but it s

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Mexico: Dealing with international financial uncertainty. Manuel Sánchez

Manuel Sánchez United States Mexico Chamber of Commerce, Chicago, IL, August 6, 2015 Contents 1 Moderate economic growth 2 Waiting for the liftoff 3 Taming inflation 2 Since 2014, Mexico s economic recovery

Manuel Sánchez United States Mexico Chamber of Commerce, Chicago, IL, August 6, 2015 Contents 1 Moderate economic growth 2 Waiting for the liftoff 3 Taming inflation 2 Since 2014, Mexico s economic recovery

Latin America: the shadow of China

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Global Investment Outlook

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook April 2014 Stocks to Rebound & Post Further Gains as Global Growth Strengthens after Q1 Soft Patch, Earnings Rebound, Low Interest

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook April 2014 Stocks to Rebound & Post Further Gains as Global Growth Strengthens after Q1 Soft Patch, Earnings Rebound, Low Interest

WTO lowers forecast after sub-par trade growth in first half of 2014

PRESS RELEASE PRESS/722 26 September 214 (-) WTO lowers forecast after sub-par trade growth in first half of 214 TRADE STATISTICS WTO economists have reduced their forecast for world trade growth in 214

PRESS RELEASE PRESS/722 26 September 214 (-) WTO lowers forecast after sub-par trade growth in first half of 214 TRADE STATISTICS WTO economists have reduced their forecast for world trade growth in 214

World Economic Outlook. Recovery Strengthens, Remains Uneven April

World Economic Outlook Recovery Strengthens, Remains Uneven April 214 1 April 214 WEO: Key Messages Global growth strengthened in 213H2, will accelerate further in 214-1 Advanced economies are providing

World Economic Outlook Recovery Strengthens, Remains Uneven April 214 1 April 214 WEO: Key Messages Global growth strengthened in 213H2, will accelerate further in 214-1 Advanced economies are providing

The Global Economy. RISI Asian Forest Products Summit 22 June, David Katsnelson Director, Macroeconomics

The Global Economy Heightened drisks RISI Asian Forest Products Summit 22 June, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. China Slowing, Not Crashing

The Global Economy Heightened drisks RISI Asian Forest Products Summit 22 June, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. China Slowing, Not Crashing

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 2009

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Mexico: 2016 IMF ARTICLE IV CONSULTATION

Mexico: 2016 IMF ARTICLE IV CONSULTATION Wilson Center, January 9, 2017 Western Hemisphere Department International Monetary Fund BACKGROUND Growth in Economic Activity and Employment Have Remained Stable

Mexico: 2016 IMF ARTICLE IV CONSULTATION Wilson Center, January 9, 2017 Western Hemisphere Department International Monetary Fund BACKGROUND Growth in Economic Activity and Employment Have Remained Stable

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute November 2018 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute November 2018 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Emerging Markets Weekly Economic Briefing

21 Emerging Markets Emerging Markets Weekly Economic Briefing Recession looms for some emerging economies Several major emerging economies struggling with domestically-induced problems are now in, or flirting

21 Emerging Markets Emerging Markets Weekly Economic Briefing Recession looms for some emerging economies Several major emerging economies struggling with domestically-induced problems are now in, or flirting

Emerging Markets Weekly Economic Briefing

Emerging Markets Weekly Economic Briefing Divergence in emergers monetary policy This year economic activity across the emergers has been subdued but inflation has generally remained moderate, allowing

Emerging Markets Weekly Economic Briefing Divergence in emergers monetary policy This year economic activity across the emergers has been subdued but inflation has generally remained moderate, allowing

EY s Global Economic Outlook Ireland

EY s Global Economic Outlook Ireland January 2018 The global economy is healthy Mark Gregory Chief Economist, UK mgregory@uk.ey.com linkedin.com/in/markgregoryuk Neil Gibson Chief Economist, Ireland neil.gibson1@ie.ey.com

EY s Global Economic Outlook Ireland January 2018 The global economy is healthy Mark Gregory Chief Economist, UK mgregory@uk.ey.com linkedin.com/in/markgregoryuk Neil Gibson Chief Economist, Ireland neil.gibson1@ie.ey.com

Global Economic Prospects: A Fragile Recovery. June M. Ayhan Kose Four Questions

//7 Global Economic Prospects: A Fragile Recovery June 7 M. Ayhan Kose akose@worldbank.org Four Questions How is the health of the global economy? Recovery underway, broadly as expected How important is

//7 Global Economic Prospects: A Fragile Recovery June 7 M. Ayhan Kose akose@worldbank.org Four Questions How is the health of the global economy? Recovery underway, broadly as expected How important is

Quarterly market summary

Quarterly market summary 3rd Quarter 2017 Economic overview Economic data released during the quarter seemed to signal a continuation of synchronised global recovery in almost all regions. This is being

Quarterly market summary 3rd Quarter 2017 Economic overview Economic data released during the quarter seemed to signal a continuation of synchronised global recovery in almost all regions. This is being

Economic and market snapshot for January 2016

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

International Monetary Fund

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

Global Sovereign Conference Singapore 6 September

Global Sovereign Conference Singapore September 1 --- --- Politics, Populism and the Global Economy Brian Coulton Chief Economist --- --- Key Messages World economy muddling along but global macro risks

Global Sovereign Conference Singapore September 1 --- --- Politics, Populism and the Global Economy Brian Coulton Chief Economist --- --- Key Messages World economy muddling along but global macro risks

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO)

") Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Global/Regional Economic and Financial Outlook. Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June

Global/Regional Economic and Financial Outlook Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June 11-12 2015 2015/SFOM13/002 Session: 1 Global/Regional Economic and Financial

Global/Regional Economic and Financial Outlook Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June 11-12 2015 2015/SFOM13/002 Session: 1 Global/Regional Economic and Financial

What could debt restructuring imply for the Eurozone? Adrian Cooper

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

OUTLOOK FOR THE GLOBAL ECONOMY AND TRAVEL

January 2018 OUTLOOK FOR THE GLOBAL ECONOMY AND TRAVEL Adam Sacks President Tourism Economics @adam_sacks August 2018 Outline The Outlook for the Economy and Travel Views on the global economy Risks Will

January 2018 OUTLOOK FOR THE GLOBAL ECONOMY AND TRAVEL Adam Sacks President Tourism Economics @adam_sacks August 2018 Outline The Outlook for the Economy and Travel Views on the global economy Risks Will

Moderate but continued growth expected for global steel demand

PRESS RELEASE Moderate but continued growth expected for global steel demand worldsteel Short Range Outlook October 2017 Brussels, 16 October 2017 - The World Steel Association (worldsteel) today released

PRESS RELEASE Moderate but continued growth expected for global steel demand worldsteel Short Range Outlook October 2017 Brussels, 16 October 2017 - The World Steel Association (worldsteel) today released

LATIN AMERICA OUTLOOK 4Q2016 OUTLOOK LATIN AMERICA. 4th QUARTER 2016

LATIN AMERICA OUTLOOK 4Q OUTLOOK LATIN AMERICA 4th QUARTER LATIN AMERICA OUTLOOK 4Q Main messages The global economy is heading for a slow recovery. Global GDP growth will improve slightly from the second

LATIN AMERICA OUTLOOK 4Q OUTLOOK LATIN AMERICA 4th QUARTER LATIN AMERICA OUTLOOK 4Q Main messages The global economy is heading for a slow recovery. Global GDP growth will improve slightly from the second

Key developments and outlook

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile. 4-6 October 2017

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

IMF forecasts India s GDP growth to improve from 6.7% in FY2018 to 7.4% in FY2019 : World Economic Outlook

All Members, IMF forecasts India s GDP growth to improve from 6.7% in FY2018 to 7.4% in FY2019 : World Economic Outlook International monetary fund (IMF) in its latest update on World Economic Outlook

All Members, IMF forecasts India s GDP growth to improve from 6.7% in FY2018 to 7.4% in FY2019 : World Economic Outlook International monetary fund (IMF) in its latest update on World Economic Outlook

Global Economic Watch

BBVA Research Global Economic Watch July 2018 / 1 Global Economic Watch July 2018 Steady global growth, but risks intensify Our BBVA-GAIN model projects that global growth could remain slightly above 1%

BBVA Research Global Economic Watch July 2018 / 1 Global Economic Watch July 2018 Steady global growth, but risks intensify Our BBVA-GAIN model projects that global growth could remain slightly above 1%

2016 External Sector Report

216 External Sector Report Global Imbalances and Policy Challenges September, 216 o Evolution of Global Current Accounts and Exchange Rates Widening and reconfiguration of imbalances in 215 Drivers: Asymmetric

216 External Sector Report Global Imbalances and Policy Challenges September, 216 o Evolution of Global Current Accounts and Exchange Rates Widening and reconfiguration of imbalances in 215 Drivers: Asymmetric

Sovereign Risks and Financial Spillovers

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Quarterly market summary 4th Quarter 2018

POOLED PENSIONS Quarterly market summary 4th Quarter 2018 Economic overview As the quarter progressed, investors became increasingly concerned about the outlook for the world economy. The perception was

POOLED PENSIONS Quarterly market summary 4th Quarter 2018 Economic overview As the quarter progressed, investors became increasingly concerned about the outlook for the world economy. The perception was

Global Macroeconomic Outlook March 2016

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

Prepared by Meketa Investment Group Global Economic Outlook Projections for global growth continue to be lowered, as the economic recovery in many countries remains weak. The IMF reduced their 206 global

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

Market Insight Economy and Asset Classes December Oil Prices Downtrending: The Real Global Economic Stimulus

Market Insight Economy and Asset Classes December 2014 Oil Prices Downtrending: The Real Global Economic Stimulus 2 Equities Markets Feature In Citi analysts view, the expansion phase the US are enjoying

Market Insight Economy and Asset Classes December 2014 Oil Prices Downtrending: The Real Global Economic Stimulus 2 Equities Markets Feature In Citi analysts view, the expansion phase the US are enjoying

MASTER INVESTOR SHOW APRIL

MASTER INVESTOR SHOW APRIL 2016 TWITTER @USTEWART WWW.7IM.CO.UK BREXIT - GREXIT - OR FIRE EXIT? APRIL 2016 TWITTER @USTEWART WWW.7IM.CO.UK GREAT START TO A NEW YEAR! A TOUGH START TO 2016 US -10.5% Europe

MASTER INVESTOR SHOW APRIL 2016 TWITTER @USTEWART WWW.7IM.CO.UK BREXIT - GREXIT - OR FIRE EXIT? APRIL 2016 TWITTER @USTEWART WWW.7IM.CO.UK GREAT START TO A NEW YEAR! A TOUGH START TO 2016 US -10.5% Europe

NOVEMBER 2018 Summary global growth is above average but slowing

EMBARGOED UNTIL: 11.AM THURSDAY 1 NOVEMBER 1 THE FORWARD VIEW GLOBAL NOVEMBER 1 Summary global growth is above average but slowing While global growth remains above average, available GDP data for Q point

EMBARGOED UNTIL: 11.AM THURSDAY 1 NOVEMBER 1 THE FORWARD VIEW GLOBAL NOVEMBER 1 Summary global growth is above average but slowing While global growth remains above average, available GDP data for Q point

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Monetary Policy Stance amid the Risk of Uneven Global Growth and External Imbalance

Monetary Policy Stance amid the Risk of Uneven Global Growth and External Imbalance Agus D.W. Martowardojo Governor Bank Indonesia Prepared for Mandiri Investment Forum, January 27, 2015 2 1 Global Economic

Monetary Policy Stance amid the Risk of Uneven Global Growth and External Imbalance Agus D.W. Martowardojo Governor Bank Indonesia Prepared for Mandiri Investment Forum, January 27, 2015 2 1 Global Economic

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Summary. Economic Update 1 / 7 December 2017

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

SEPTEMBER Overview

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

OXFORD ECONOMICS. Stress testing and risk management services

OXFORD ECONOMICS Stress testing and risk management services September 2014 The rising need for rigorous stress testing Stress testing has become a critical component of the risk identification and risk

OXFORD ECONOMICS Stress testing and risk management services September 2014 The rising need for rigorous stress testing Stress testing has become a critical component of the risk identification and risk

Latin America Outlook 2Q18

BBVA Research - Latin America Outlook 2Q18 / 1 Latin America Outlook 2Q18 April Key messages Global growth remains robust., although uncertainty is increasing. US fiscal stimulus may underpin progress

BBVA Research - Latin America Outlook 2Q18 / 1 Latin America Outlook 2Q18 April Key messages Global growth remains robust., although uncertainty is increasing. US fiscal stimulus may underpin progress

Global Investment Strategy. Scenario Analysis Winter 2012/13

Global Investment Strategy Scenario Analysis Winter 2012/13 Introduction Our central scenario is for a reacceleration in global growth in 2013 and 2014, which should be help risk assets outperform during

Global Investment Strategy Scenario Analysis Winter 2012/13 Introduction Our central scenario is for a reacceleration in global growth in 2013 and 2014, which should be help risk assets outperform during

3rd Research Conference Towards Recovery and Sustainable Growth in the Altered Global Environment

3rd Research Conference Towards Recovery and Sustainable Growth in the Altered Global Environment Erdem Başçı Governor 28-29 April 214, Skopje Overview: Inflation and Monetary Policy Retail loan growth

3rd Research Conference Towards Recovery and Sustainable Growth in the Altered Global Environment Erdem Başçı Governor 28-29 April 214, Skopje Overview: Inflation and Monetary Policy Retail loan growth

Global Economic Outlook

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

GLOBAL EQUITY MARKET OUTLOOK

LPL RESEARCH WEEKLY MARKET COMMENTARY KEY TAKEAWAYS 2017 was an excellent year for international equities, particularly EM. We favor the United States and EM equities for tactical global asset allocations

LPL RESEARCH WEEKLY MARKET COMMENTARY KEY TAKEAWAYS 2017 was an excellent year for international equities, particularly EM. We favor the United States and EM equities for tactical global asset allocations

Emerging Markets Weekly Economic Briefing

1 Emerging Markets Emerging Markets Weekly Economic Briefing Forecasts eased down again as trade remains sluggish We have cut our forecast for China again following weak growth in Q1. We now expect the

1 Emerging Markets Emerging Markets Weekly Economic Briefing Forecasts eased down again as trade remains sluggish We have cut our forecast for China again following weak growth in Q1. We now expect the

The Economic and Political Outlook. By Roger Bootle

The Economic and Political Outlook By Roger Bootle 1. Agenda The World, China and America. Recovery in the euro-zone. Political worries in Europe. The UK economy. Brexit opportunities and challenges. The

The Economic and Political Outlook By Roger Bootle 1. Agenda The World, China and America. Recovery in the euro-zone. Political worries in Europe. The UK economy. Brexit opportunities and challenges. The

New in 2013: Greater emphasis on capital flows Refinements to EBA methodology Individual country assessments

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

2017 Asia and Pacific Regional Economic Outlook:

217 Asia and Pacific Regional Economic Outlook: Preparing for Choppy Seas Ranil Salgado International Monetary Fund Asia and Pacific Department May 12, 217 OAP Seminar Key messages and roadmap The near-term

217 Asia and Pacific Regional Economic Outlook: Preparing for Choppy Seas Ranil Salgado International Monetary Fund Asia and Pacific Department May 12, 217 OAP Seminar Key messages and roadmap The near-term

Indonesia: Building on Resilience and Prospering Amid Global Economic Uncertainty

Indonesia: Building on Resilience and Prospering Amid Global Economic Uncertainty 2016 Article IV Consultation Report on Indonesia John G. Nelmes IMF Senior Resident Representative for Indonesia Academic

Indonesia: Building on Resilience and Prospering Amid Global Economic Uncertainty 2016 Article IV Consultation Report on Indonesia John G. Nelmes IMF Senior Resident Representative for Indonesia Academic

The Asia Pacific Fund, Inc.

Baring Asset Management (Asia) Limited 19th Floor Edinburgh Tower 15 Queen s Road Central Hong Kong Tel: (852) 2841 1411 Fax: (852) 2868 411 The Asia Pacific Fund, Inc. Investment Outlook & Strategy www.asiapacificfund.com

Baring Asset Management (Asia) Limited 19th Floor Edinburgh Tower 15 Queen s Road Central Hong Kong Tel: (852) 2841 1411 Fax: (852) 2868 411 The Asia Pacific Fund, Inc. Investment Outlook & Strategy www.asiapacificfund.com

Discussion of Bacchetta & Benhima paper The Demand for Liquid Assets and International Capital Flows

Discussion of Bacchetta & Benhima paper The Demand for Liquid Assets and International Capital Flows Marcel Fratzscher European Central Bank Conference Financial Globalization: Shifting Balances Banco

Discussion of Bacchetta & Benhima paper The Demand for Liquid Assets and International Capital Flows Marcel Fratzscher European Central Bank Conference Financial Globalization: Shifting Balances Banco

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009 December 17, 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact:

Prudential International Investments Advisers, LLC. Global Investment Strategy & Outlook For 2009 December 17, 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact:

Weekly Market Commentary

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Latin America Outlook 3Q18

BBVA Research - Latin America Outlook 3Q18 / 1 Latin America Outlook 3Q18 July Key messages Global growth remains robust, but risks also increase. Robust growth in the US on the back of fiscal stimulus.

BBVA Research - Latin America Outlook 3Q18 / 1 Latin America Outlook 3Q18 July Key messages Global growth remains robust, but risks also increase. Robust growth in the US on the back of fiscal stimulus.

Latin America Equities

Latin America Equities March 2013 Stephen Burrows, Senior Investment Manager Emerging Markets - Pictet Asset Management Dec-10 Feb-11 Apr-11 Jun-11 Aug-11 Oct-11 Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12

Latin America Equities March 2013 Stephen Burrows, Senior Investment Manager Emerging Markets - Pictet Asset Management Dec-10 Feb-11 Apr-11 Jun-11 Aug-11 Oct-11 Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12

Recent Recent Developments 0

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)