Concrete Pavement Workshop

|

|

|

- Asher Nelson

- 6 years ago

- Views:

Transcription

1 Fundamentals of Life Cycle Cost Analysis Concrete Pavement Workshop Madison Marriott West Middleton, Wisconsin February 11, 2016 Leif G. Wathne, P.E. American Concrete Pavement Association

2 Fundamentals of Life Cycle Cost Analysis A Tool for Better Pavement Investment and Engineering Decisions Content based on information in ACPA Engineering Bulletin (EB011)

3 Life-Cycle Cost Analysis Introduction

4 What is Life-Cycle Cost Analysis? Life-cycle cost analysis (LCCA): An analysis technique used to evaluate the overall long-term economic efficiency between competing alternate investment options (e.g., pavements). Based on well-founded economic principles. Identifies the strategy that will yield the best value by providing the expected performance at the lowest cost over the analysis period. Is not an engineering tool for determining how long a pavement design or rehabilitation alternative will last or how well it will perform.

5 Why Bother with an LCCA? Pavement types perform differently over time. Equivalent designs are not always achievable. LCCA compares the total discounted cost of each design over a specific analysis period to minimize the financial burden of the roadway on taxpayers.

6 Why Bother with an LCCA? Failure to account for costs over the life of the pavement may lead to a larger budget burden or deficit in the future. Consider these initial and LCCA cost trends developed by the Louisiana DOT in 2003:

7 We Must Consider Life Cycle Costs! Economic principles tell us that if we want to minimize the cost of a durable good that requires repair, maintenance and replacement over time, we must minimize present value of those costs, not minimize initial costs. If the myopic strategy is adopted to accept the lower up-front price despite higher [present value], the buyers are actually made worse off. - Dr. William Holahan Chair and Professor Department of Economics University of Wisconsin - Milwaukee

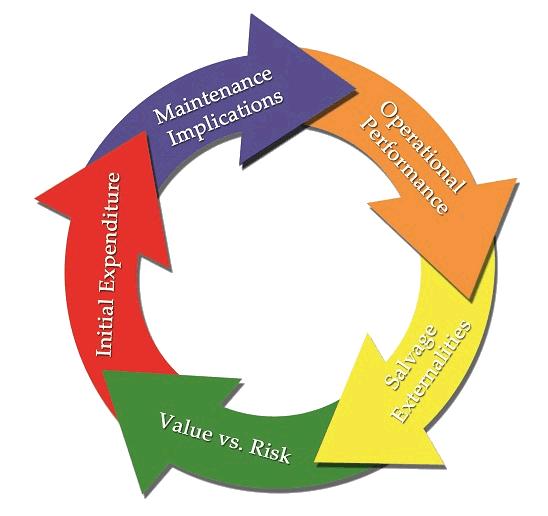

8 Life-Cycle Cost Analysis Basic Steps in a Single Project LCCA

9 Life-Cycle Cost Analysis Step 1 Select the Analysis Period

10 LCCA Analysis Period The analysis period is the timeframe over which the alternative strategies/treatments are compared. Must encompass the initial performance period and at least one major follow-up preservation/ rehabilitation activity for each strategy. FHWA recommends an analysis period of at least 35 years for all pavement projects. ACPA recommends an analysis period of years because common practice in many states is to design the concrete pavement alternate for 30+ years.

11 Agency Practices: Analysis Period 2012 ACPA LCCA EB (28) December 2013 ACPA Survey (38) Analysis Period (yrs) Percent of Responding Agencies Analysis Period (yrs) Percent of Responding Agencies Agency < 30 4% 30 11% 35 18% < 30 3% AL 30 8% NC, TN, WY 35 16% AK, AR, ID, MT, NV, OH 40 39% 40 37% AZ, BC, CO, FL, GA, IN, IA, KS, KY, LA, MD, MS, SD, WV 45 7% 45 5% IL, MO % % MB, PA, QC, SC, MN, NE, NY, VA, WA, WI Varies 5% HI, MI

12 Life-Cycle Cost Analysis Step 2 Select a Discount Rate

13 LCCA Discount Rate The real discount rate (also known as the real interest rate) is used in pavement LCCAs. Accounts for fluctuations in both investment interest rates and the rate of inflation. Today s costs can be used as proxies for future costs. d = 1 + ii iiiiii 1 + ii iiiiii 1 d = the real discount rate, % i int = the interest rate, % i inf = the inflation rate, %

, and/or 3.")

14 Selecting an Interest Rate Funds for paving projects are obtained by: 1. Levying taxes, 2. Borrowing money (i.e., selling bonds), and/or 3. Charging users for services (e.g., toll revenue). The interest rate assumed for the LCCA of a project should reflect the type of entity raising the money and the method(s) used to raise it.

15 Selecting an Inflation Rate The inflation rate may be: 1. A single value if it is assumed that all components of future costs inflate at a uniform rate OR 2. Several different values for various cost components when there are significant differences in inflation among the cost components. Several general inflation indices are compiled regularly by the Bureau of Labor Statistics (BLS) in the U.S. Department of Labor.

16 Various Inflation Rates

recommends using the United")

17 Determining the Real Discount Rate If local interest and inflation rates are not readily available to develop a local real discount rate, FHWA (and ACPA) recommends using the United State s Office of Management and Budget (OMB) real discount rate. If there is concern with the variability in the OMB real discount rate, a moving average of the value should be considered.

18 Determining the Real Discount Rate OMB Circular A-94 Appendix C Published annually November 2015 Current OMB Rate 1.5%

19 Agency Practices: Discount Rate December 2013 ACPA Survey (43) Real Discount Rate (%) Percent of Responding Agencies Agency < 3 23% CO*, KS, MI*, MN*, MO*, NV*, OH*, PA*, SC*, WV* 3 14% GA, IL, IA, MD, MT, NY 3 to 4 9% AR, FL, NE, SD 4 42% 4 to 5 0% - AL, AK, AZ, CA, CT, DE, ID, IN, LA, MS, NJ, NM, NC, TN, UT, VA, WA, WY 5 or more 12% BC, KY, MB, QC, WI OMB Circular A-94, App. C % % % % 5-yr avg 1.6% * Denotes a state whose real discount rate is based either on the OMB or a moving average of the OMB.

20 Impact of discount rate? How does the discount rate impact the analysis?

")

21 Life-Cycle Cost Analysis Step 3 Estimate Initial Agency Costs (A)

22 Initial Agency Costs Only those initial agency costs that are different among the various alternatives need to be considered for reasonably similar alternates. Pavement costs include items such as subgrade preparation, bases, and surface material; associated labor and equipment, etc. When historical bid prices are used as estimates, consider the impact of material price escalators, payment practices (sy v. tons), bidding practices (shifting), job size, etc..

23 Initial Agency Costs Important to get as correct as possible! Influences results more than anything else in analysis Do not use average bid values blindly Easiest or Toughest to get??? Use quality local information WCPA can help with realistic estimates!

24 Life-Cycle Cost Analysis Step 4 Estimate User Costs (B)

25 User Costs Costs that are incurred by users of the roadway over the analysis period, mainly... Work zone costs: Incurred during lane closures and other periods of construction, preservation/rehabilitation, and maintenance work. Vehicle operating costs: Incurred during the normal use of the roadway (roughness and rigdity) Accidents: Damage to the user s/other s vehicle and/or public or private property; injury costs.

26 Agency Practices: User Costs 2012 ACPA LCCA EB (40) December 2013 ACPA Survey (42) User Costs Considered Percent of Responding Agencies User Costs Considered Percent of Responding Agencies Agency Yes 42% Yes 43% AK, CA, CO, CT, DE, GA, KS, KY, LA, MD, MI, NV, NM, QC, SC, VT, VA, WA No 58% No 55% AL, AZ, AR, FL, ID, IL, IN, IA, MN, MO, MS, MT, NE, NJ, NY, NC, OH, SD, TN, UT, WV, WI, WY Sometimes 2% PA

27 Life-Cycle Cost Analysis Step 5 Estimate Future Agency Costs (C)

28 Future Agency Costs All cost components must be considered because the present value of costs associated with engineering, administrative, and traffic control are impacted by the time value of money (timing, discount rate). Future activities are dependent on the initial pavement design. Must consider both maintenance/operation and preservation/rehabilitation costs and timing.

29 Maintenance and Operation Costs Daily costs associated with keeping the pavement at a given level of service. Several billion dollars are spent each year on pavement maintenance by highway agencies in the U.S. Short-term solutions typically have significantly larger maintenance requirements than long-life solutions, regardless of the size of the project.

30 Agency Practices: Maint. Costs 2012 ACPA LCCA EB (31) December 2013 ACPA Survey (40) Maint. Costs Considered Percent of Responding Agencies Maint. Costs Considered Percent of Responding Agencies Agency Yes 77% Yes 78% AK, AZ, AR, BC, CA, CO, DE, GA, ID, IL, IN, LA, MB, MI, MN, MT, NE, NV, NM, NY, NC, PA, QC, SD, TN, UT, VT, VA, WV, WI, WY No 23% No 22% AL, IA, KS, MD, MO, OH, SC, WA

31 Preservation and Rehab. Costs Large future agency costs associated with improving the condition of the pavement or extending its service life. Preservation and rehabilitation activities and their timing should be based on the distresses that are predicted to develop in the pavement. Best to develop pavement performance predictions based on local performance history data; otherwise, AASHTOWare Pavement ME can be used.

32 Agency Practices: Rehab. Costs 2012 ACPA LCCA EB (31) December 2013 ACPA Survey (41) Rehab. Costs Considered Percent of Responding Agencies Rehab. Costs Considered Percent of Responding Agencies Agency Yes 97% Yes 98% AL, AK, AZ, AR, BC, CA, CO, DE, FL, GA, HI, ID, IL, IN, IA, KS, LA, MB, MD, MN, MO, MS, MT, NE, NV, NM, NY, NC, OH, PA, QC, PA, SC, SD, TN, UT, VA, WA, WV, WI, WY No 3% No 2% MI

33 Life-Cycle Cost Analysis Step 6 Estimate Residual or Salvage Value

34 Residual or Salvage Value Defined in one of three ways: The net value that the pavement would have in the marketplace if it is recycled at the end of its life, The value of the remaining service life (RSL) at the end of the analysis, OR The value of the existing pavement as a support layer for an overlay at the end of the analysis period. Residual or salvage value must be defined the same way for all alternatives. Always in final year, so Δ$ is what is important.

35 Agency Practices: Residual Value 2012 ACPA LCCA EB (35) December 2013 ACPA Survey (40) Residual Value Considered Percent of Responding Agencies Residual Value Considered Percent of Responding Agencies Agency Yes 51% Yes 55% AK, AZ, AR, CA, CT, GA, HI, ID, IN, KS, MB, MD, MN, MT, NE, NV, NY, PA, QC, VA, WA, WI No 49% No 45% AL, CO, FL, IL, IA, KY, LA, MI, MO, MS, NC, OH, SC, SD, TN, UT, WV, WY

the initial construction cost Source:")

36 Beware NAPA/NCAT False Definition This approach results in a salvage value near (or even higher than) the initial construction cost Source: Life Cycle Cost Analysis for Pavements NCAT/NAPA Webinar 6/4/14 Actual value is EITHER from continued use OR from sale of scrap material as it is recycled

37 Think about Your Last Car Value at the end of your ownership was EITHER Trade in or private party sale value because it will be continued to be used OR Scrap value because it is not drivable due to age or accident and NOT the sum of these.

38 Pavement Management Plan from City of Leawood, Kansas Life-Cycle Cost Analysis Step 7 Compare Alternatives

39 Compare Alternatives Alternatives considered must be compared using a common measure of economic worth. Investment alternatives such as pavement strategies are most commonly compared on the basis of: Present worth (also called net present value [NPV]) Annual worth (also called equivalent uniform annual cost [EUAC]) NPV and EUAC provide the same ranking

40 Agency Practices: Calc. Method 2012 ACPA LCCA EB (29) December 2013 ACPA Survey (31) Calculation Method Used Percent of Responding Agencies Calc. Method Used Percent of Responding Agencies Agency Net Present Value (NPV) Only 66% NPV 65% AL, AR, CA, CO, KS, LA, MD, MN, MO, MN, NV, NM, OH, PA, SC, UT, VT, WA, WV, WY Equivalent Uniform Annual Cost (EUAC) Only 17% EUAC 19% DE, IL, MI, NC, SD, WI Both NPV and EUAC 17% NPV + EUAC 16% AZ, GA, ID, IN, TN

41 Net Present Value (NPV) NPV analyses are directly applicable only to mutually exclusive alternates each with the same analysis period. The formula for the present value or worth ($P) of a one-time future cost or benefit ($F) is: $PP = $FF 1 (1 + d) t d = the real discount rate, % t = the year in which the one-time future cost or benefit occurs

42 Analysis Methods Deterministic approach a single defined value is assumed and used for each activity. Probabilistic approach variability of each input is accounted for and used to generate a probability distribution for the calculated life-cycle cost.

43 Agency Practices: Analysis Method 2012 ACPA LCCA EB (29) December 2013 ACPA Survey (32) Analysis Method Used Percent of Responding Agencies Analysis Method Used Percent of Responding Agencies Agency Deterministic 80% Deterministic 78% AL, AR, CA, GA, ID, IL, KS, LA, MI, MN, MO, MT, NV, NM, NY, NC, OH, PA, SD, TN, UT, VT, WV, WI, WY Probabilistic 10% Probabilistic 13% AZ, CO, IN, MD Both Det. and Prob. 10% Both 9% DE, SC, WA

44 Analysis Tools Most modern spreadsheet software include standard functions for calculating the present worth and annual worth. Proprietary software to compute LCCAs include: AASHTOWare Pavement ME (deterministic) FHWA s RealCost (deterministic and probabilistic) ACPA s StreetPave & WinPAS (both deterministic) CAC s CANPave (deterministic) Asphalt Pavement Alliance s (APA s) LCCA Original and LCCA Express (both deterministic)

45 Agency Practices: Analysis Tools 2012 ACPA LCCA EB (29) December 2013 ACPA Survey (31) LCCA Tool Used Percent of Responding Agencies LCCA Tool Used Percent of Responding Agencies Agency State- Developed Tool 62% State- Developed Tool 65% AR, GA, ID, IL, KS, MI, MN, MO, MT, NV, NM, NY, NC, OH, PA, SC, SD, TN, UT, WI RealCost 41% RealCost 39% AZ, CA, CO, DE, IN, LA, MD, SC, TN, UT, VT, WA DARWinME TM 17% Pavement ME 16% AL, CO, TN, VT, WV

46 Compare Results Because different components of the LCCA indicate different things about the alternates, the components typically are viewed separately and together to aid in interpretation/evaluation. When two alternatives have very similar net present values over the analysis period, it is advisable to choose the less risky alternative (i.e., the one with the higher proportion of the net present value attributable to initial costs).

47 Existing 80-yr old concrete pavement Existing 34-yr old asphalt pavement Life-Cycle Cost Analysis Example of Single-Project LCCA in Whitefish Bay, WI

48 Local Road Example Agency/Owner: Village of Whitefish Bay, WI Location: Diversey Boulevard Street Year of LCCA: 2008 Roadway Classification: Residential Project Scope: Reconstruction of approximately 10,000 SY (8,360 m 2 ) of pavement. Other Project Details: Existing 80-yr old concrete pavement is still in good condition with no scheduled maintenance, rehabilitation or reconstruction planned. Existing 34-yr old asphalt pavement has significant structural and material durability distresses.

of concrete atop 4 in. (100 mm) of granular subbase.")

of granular base with a 2-in.")

49 Local Road Example Concrete Alternate: 7 in. (175 mm) of concrete atop 4 in. (100 mm) of granular subbase. Asphalt Alternate: 3 in. (75 mm) of asphalt atop 10 in. (250 mm) of granular base with a 2-in. (50-mm) asphalt overlay one year after initial construction.

50 Local Road Example Step 1 Select Analysis Period: 90 years Step 2 Select Real Discount Rate: 3% Step 3 Estimate Initial Agency Costs: Concrete Alternate: $373,940 Asphalt Alternate: $318,068 Step 4 Estimate User Costs: User costs were not considered. As bid, user costs for the staged asphalt construction would have been significantly more than those of concrete or an asphalt pavement placed in a single construction phase. Based on activity timings in the next step, future user costs likely also are more for the asphalt alternate.

51 Local Road Example Step 5 Estimate Future Agency Costs: Concrete Alternate: Year Type of Work Description of Work Quantity Unit Price Total Cost 15 Maintenance Joint Sealing (15%) 2,250 LF $0.50/LF $1, Maintenance Joint Sealing (30%) 4,500 LF $0.50/LF $2, Preservation Full Depth Repair (2% 6 ft Repair) 40 CY $180/CY $7, Preservation Partial Depth Repair (3% Joint Repaired) 180 LF $15.00/LF $2, Maintenance Joint Sealing (30%) 4,500 LF $0.50/LF $2, Maintenance Joint Sealing (30%) 4,500 LF $0.50/LF $2, Preservation Full Depth Repair (4% 6 ft Repair) 80 CY $180/CY $14, Preservation Partial Depth Repair (6% Joint Repaired) 360 LF $15.00/LF $5, Maintenance Joint Sealing (30%) 4,500 LF $0.50/LF $2,250

52 Local Road Example Step 5 Estimate Future Agency Costs: Concrete Alternate:

53 Local Road Example Step 5 Estimate Future Agency Costs: Asphalt Alternate: Year Type of Work Description of Work Quantity Unit Price Total Cost 3 Maintenance Crack Sealing 3,000 LF $0.50/LF $1,500 7 Maintenance Crack Sealing 4,000 LF $0.50/LF $2, Preservation Seal Coat 10,000 SY $1.75/SY $17, Maintenance Crack Sealing 5,000 LF $0.50/LF $2, Maintenance Crack Sealing 6,000 LF $0.50/LF $3, Reconstruct Remove Pavement 10,000 SY $2.00/SY $20, Reconstruct Pavement Replacement 1 LS $318,068/LS $318, Maintenance Crack Sealing 3,000 LF $0.50/LF $1, Maintenance Crack Sealing 4,000 LF $0.50/LF $2, Preservation Seal Coat 10,000 SY $1.75/SY $17, Maintenance Crack Sealing 5,000 LF $0.50/LF $2, Maintenance Crack Sealing 6,000 LF $0.50/LF $3, Reconstruct Remove Pavement 10,000 SY $2.00/SY $20, Reconstruct Pavement Replacement 1 LS $318,068/LS $318, Maintenance Crack Sealing 3,000 LF $0.50/LF $1, Maintenance Crack Sealing 4,000 LF $0.50/LF $2, Preservation Seal Coat 10,000 SY $1.75/SY $17, Maintenance Crack Sealing 5,000 LF $0.50/LF $2, Maintenance Crack Sealing 6,000 LF $0.50/LF $3,000

54 Local Road Example Step 5 Estimate Future Agency Costs: Asphalt Alternate:

55 Local Road Example Step 6 Estimate Residual Value: Residual value is assumed similar for both alternates; thus it s excluded. Even if residual values were considered, any remaining value for either alternate likely would not have significant present worth due to the length of the analysis period. 3% Discount Rate

56 Local Road Example Step 7 Compare Alternatives: ASPHALT CONCRETE

57 Local Road Example Step 7 Compare Alternatives: Concrete Alternate: Year Type of Work Total Cost Present Worth 0 Initial Construction $373,940 $ 373, Maintenance $1,125 $ Maintenance/Preservation $12,150 $ 5, Maintenance $2,250 $ Maintenance/Preservation $22,050 $ 3, Maintenance $2,250 $ 245 TOTAL NET PRESENT VALUE: $ 384,250 Present Worth Future Cost $PP = $FF 1 (1 + d) t Time of Expenditure Discount Rate = 3%

58 Local Road Example Step 7 Compare Alternatives: Asphalt Alternate: Year Type of Work Total Cost Present Worth 0 Initial Construction $318,068 $ 318,068 3 Maintenance $1,500 $ 1,373 7 Maintenance $2,000 $ 1, Maintenance/Preservation $20,000 $ 12, Maintenance $3,000 $ 1, Reconstruction $338,068 $ 139, Maintenance $1,500 $ Maintenance $2,000 $ Maintenance/Preservation $20,000 $ 5, Maintenance $3,000 $ Reconstruction $338,068 $ 57, Maintenance $1,500 $ Maintenance $2,000 $ Maintenance/Preservation $20,000 $ 2, Maintenance $3,000 $ 266 TOTAL NET PRESENT VALUE: $ 542,254

59 Local Road Example Step 7 Compare Alternatives: Concrete Alternative Initial Cost: $373,940 NPV: $384,250 Asphalt Alternative Initial Cost: $318,068 NPV: $542,254 Initial agency cost for the asphalt alternate is 15% less than that of the concrete alternate. The concrete alternate will cost 29% less (in constant dollars) than the asphalt alternate over the analysis period investigated. 97% of Conc Alt is initial cost, whereas only 59% of Asphalt Alt is initial cost Conc Alt has a much lower risk of higher-than-expected costs

60 Thank You! apps.acpa.org ACPA Application Library local.acpa.org ACPA-affiliated Chapter/States resources.acpa.org Resource Center wikipave.org ACPA s paving wiki

61 Impact of Analysis Period What if analysis period was 30 years or less?

62 Impact of Time Value of Money These were both $338k

63 Impact of Real Discount Rate

64 Impact of Material Inflation Using MIT escalation factors applied to 40% of the reconstruction (e.g., the pavement portion of the reconstruction cost) of the asphalt alternative at years 30 and 60 The asphalt alternative NPV increases by 9.7% to $594,659, up from the NPV of $542,254 without the material inflation accounting.

65 Total Cost of Ownership Using a 0% interest rate in real discount rate calc. This results in a negative real discount rate Provides a real feel for outlays over analysis period Concrete Alternative: Year Type of Work Total Cost Present Worth 0 Initial Construction $373,940 $ 373, Maintenance $1,125 $ 2, Maintenance/Preservation $12,150 $ 39, Maintenance $2,250 $ 13, Maintenance/Preservation $22,050 $ 231, Maintenance $2,250 $ 42,627 TOTAL OWNERSHIP COST: $ 703,101

66 Total Cost of Ownership Asphalt Alternative: Year Type of Work Total Cost Present Worth 0 Initial Construction $318,068 $ 318,068 3 Maintenance $1,500 $ 1,687 7 Maintenance $2,000 $ 2, Maintenance/Preservation $20,000 $ 36, Maintenance $3,000 $ % Reconstruction Non-asphalt $209,763 $ 680, % Reconst. -5.2% $128,306 $ 639, Maintenance $1,500 $ 5, Maintenance $2,000 $ 8, Maintenance/Preservation $20,000 $ 116, Maintenance $3,000 $ 23, % Reconstruction Non-asphalt $209,763 $ 2,206, % Reconst. -5.2% $128,306 $ 3,187, Maintenance $1,500 $ 17, Maintenance $2,000 $ 27, Maintenance/Preservation $20,000 $ 378, Maintenance $3,000 $ 74,795 TOTAL NET PRESENT VALUE: $ 7,732,216

67 Impact of Activity Timing Estimate 1% 3% 5%

68 Life-Cycle Cost Analysis What Else is in ACPA s LCCA Engineering Bulletin?

69 LCCA Examples Document also contains: Highway and Airport examples Probabilistic analysis results

70 Applications/Extensions and Appendices Network-Level Service Life and Economic Analyses Sustainability in the Context of a Life-Cycle Cost Analysis The Role of LCCA in Pavement Type Selection Total Cost of Ownership Example Mississippi Network of 36 Pavements The Potential Impact of Material Quantity Specifications on LCCA Results Present Worth Calculations and Deterministic Analysis Worksheet Historic Oil Price Trends and Volatility Federal Policy on Pavement Type Selection

Comparative Revenues and Revenue Forecasts Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas

Comparative Revenues and Revenue Forecasts 2010-2014 Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas Comparative Revenues and Revenue Forecasts This data shows tax

Comparative Revenues and Revenue Forecasts 2010-2014 Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas Comparative Revenues and Revenue Forecasts This data shows tax

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017 This document provides a summary of the annuity training requirements that agents are required to complete for each

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017 This document provides a summary of the annuity training requirements that agents are required to complete for each

Older consumers and student loan debt by state

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

2016 Workers compensation premium index rates

2016 Workers compensation premium index rates NH WA OR NV CA AK ID AZ UT MT WY CO NM MI VT ND MN SD WI NY NE IA PA IL IN OH WV VA KS MO KY NC TN OK AR SC MS AL GA TX LA FL ME MA RI CT NJ DE MD DC = Under

2016 Workers compensation premium index rates NH WA OR NV CA AK ID AZ UT MT WY CO NM MI VT ND MN SD WI NY NE IA PA IL IN OH WV VA KS MO KY NC TN OK AR SC MS AL GA TX LA FL ME MA RI CT NJ DE MD DC = Under

Property Tax Relief in New England

Property Tax Relief in New England January 23, 2015 Adam H. Langley Senior Research Analyst Lincoln Institute of Land Policy www.lincolninst.edu Property Tax as a % of Personal Income OK AL IN UT SD MS

Property Tax Relief in New England January 23, 2015 Adam H. Langley Senior Research Analyst Lincoln Institute of Land Policy www.lincolninst.edu Property Tax as a % of Personal Income OK AL IN UT SD MS

TCJA and the States Responding to SALT Limits

TCJA and the States Responding to SALT Limits Kim S. Rueben Tuesday, January 29, 2019 1 What does this mean for Individuals under TCJA About two-thirds of taxpayers will receive a tax cut with the largest

TCJA and the States Responding to SALT Limits Kim S. Rueben Tuesday, January 29, 2019 1 What does this mean for Individuals under TCJA About two-thirds of taxpayers will receive a tax cut with the largest

RhodeWorks: achieving a state of good repair through asset management

1 RhodeWorks: achieving a state of good repair through asset management Shoshana Lew Chief Operating Officer, RI Department of Transportation July 12, 2017 NV UT HI FL TX GA MD AR WI AL TN OR CO MN VA

1 RhodeWorks: achieving a state of good repair through asset management Shoshana Lew Chief Operating Officer, RI Department of Transportation July 12, 2017 NV UT HI FL TX GA MD AR WI AL TN OR CO MN VA

State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks

State-By-State Tax Breaks for Seniors, 2016 State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks AL Payments from defined benefit private plans are

State-By-State Tax Breaks for Seniors, 2016 State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks AL Payments from defined benefit private plans are

Charts with Analysis: Tax Tax Type: Sales and Use Tax Topic: Cash for Clunkers Payments

Effective July 1, 2009, until November 1, 2009, the federal government has enacted the Consumer Assistance to Recycle and Save (CARS) Program, Title XIII of PL 111-32 (2009), 123 Stat. 1859. The program,

Effective July 1, 2009, until November 1, 2009, the federal government has enacted the Consumer Assistance to Recycle and Save (CARS) Program, Title XIII of PL 111-32 (2009), 123 Stat. 1859. The program,

SIGNIFICANT PROVISIONS OF STATE UNEMPLOYMENT INSURANCE LAWS JANUARY 2008

U.S. DEPARTMENT OF LABOR EMPLOYMENT AND TRAINING ADMINISTRATION Office Workforce Security SIGNIFICANT PROVISIONS OF STATE UNEMPLOYMENT INSURANCE LAWS JANUARY 2008 AL AK AZ AR CA CO CT DE DC FL GA HI /

U.S. DEPARTMENT OF LABOR EMPLOYMENT AND TRAINING ADMINISTRATION Office Workforce Security SIGNIFICANT PROVISIONS OF STATE UNEMPLOYMENT INSURANCE LAWS JANUARY 2008 AL AK AZ AR CA CO CT DE DC FL GA HI /

Florida 1/1/2016 Workers Compensation Rate Filing

Florida 1/1/2016 Workers Compensation Rate Filing Kirt Dooley, FCAS, MAAA October 21, 2015 1 $ Billions 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 Florida s Workers Compensation Premium Volume 2.368 0.765 0.034

Florida 1/1/2016 Workers Compensation Rate Filing Kirt Dooley, FCAS, MAAA October 21, 2015 1 $ Billions 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 Florida s Workers Compensation Premium Volume 2.368 0.765 0.034

Tax Breaks for Elderly Taxpayers in the States in 2016

AL Payments from defined benefit private plans are exempt; most public systems are exempt; military and US Civil service are exempt Special Homestead ion for 65+ +25.2% +2.4% AK No PIT Homestead ion for

AL Payments from defined benefit private plans are exempt; most public systems are exempt; military and US Civil service are exempt Special Homestead ion for 65+ +25.2% +2.4% AK No PIT Homestead ion for

Tax Freedom Day 2018 is April 19th

Apr. 2018 Tax Freedom Day 2018 is April 19th Erica York Analyst Key Findings Tax Freedom Day is a significant date for taxpayers and lawmakers because it represents how long Americans as a whole have to

Apr. 2018 Tax Freedom Day 2018 is April 19th Erica York Analyst Key Findings Tax Freedom Day is a significant date for taxpayers and lawmakers because it represents how long Americans as a whole have to

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis Report Authors: John Holahan, Matthew Buettgens, Caitlin Carroll, and Stan Dorn Urban Institute November

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis Report Authors: John Holahan, Matthew Buettgens, Caitlin Carroll, and Stan Dorn Urban Institute November

Local Anesthesia Administration by Dental Hygienists State Chart

Education or AK 1981 General Both Specific Yes WREB 16 hrs didactic; 6 hrs ; 8 hrs lab AZ 1976 General Both Accredited Yes WREB 36 hrs; 9 types of AR 1995 Direct Both Accredited/ Board Approved No 16 hrs

Education or AK 1981 General Both Specific Yes WREB 16 hrs didactic; 6 hrs ; 8 hrs lab AZ 1976 General Both Accredited Yes WREB 36 hrs; 9 types of AR 1995 Direct Both Accredited/ Board Approved No 16 hrs

2018 National Electric Rate Study

2018 National Electric Rate Study Ranking of Typical Residential, Commercial and Industrial Electric Bills LES Administrative Board June 15, 2018 Emily N. Koenig Director of Finance & Rates 1 Why is the

2018 National Electric Rate Study Ranking of Typical Residential, Commercial and Industrial Electric Bills LES Administrative Board June 15, 2018 Emily N. Koenig Director of Finance & Rates 1 Why is the

Tax Freedom Day 2019 is April 16th

Apr. 2019 Tax Freedom Day 2019 is April 16th Erica York Economist Madison Mauro Research Assistant Emma Wei Research Assistant Key Findings This year, Tax Freedom Day falls on April 16, or 105 days into

Apr. 2019 Tax Freedom Day 2019 is April 16th Erica York Economist Madison Mauro Research Assistant Emma Wei Research Assistant Key Findings This year, Tax Freedom Day falls on April 16, or 105 days into

Taxing Investment Income in the States New Hampshire Fiscal Policy Institute 2 nd Annual Budget and Policy Conference Concord, NH January 23, 2015

Taxing Investment Income in the States New Hampshire Fiscal Policy Institute 2 nd Annual Budget and Policy Conference Concord, NH January 23, 2015 Norton Francis State and Local Finance Initiative Urban-Brookings

Taxing Investment Income in the States New Hampshire Fiscal Policy Institute 2 nd Annual Budget and Policy Conference Concord, NH January 23, 2015 Norton Francis State and Local Finance Initiative Urban-Brookings

State Trust Fund Solvency

Unemployment Insurance State Trust Fund Solvency National Employment Law Project Conference - Washington DC December 7, 2009 Robert Pavosevich pavosevich.robert@dol.gov Unemployment Insurance Program

Unemployment Insurance State Trust Fund Solvency National Employment Law Project Conference - Washington DC December 7, 2009 Robert Pavosevich pavosevich.robert@dol.gov Unemployment Insurance Program

The Acquisition of Regions Insurance Group. April 6, 2018

The Acquisition of Regions Insurance Group April 6, 2018 Forward-Looking Statements This presentation contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform

The Acquisition of Regions Insurance Group April 6, 2018 Forward-Looking Statements This presentation contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform

Charles Gullickson (Penn Treaty/ANIC Task Force Chair), Richard Klipstein (NOLHGA)

, Richard Klipstein (NOLHGA)") MEMO DATE: TO: Charles Gullickson (Penn Treaty/ANIC Task Force Chair), Richard Klipstein (NOLHGA) FROM: Vincent L. Bodnar, ASA, MAAA RE: Penn Treaty Network American Insurance Company and American Network

MEMO DATE: TO: Charles Gullickson (Penn Treaty/ANIC Task Force Chair), Richard Klipstein (NOLHGA) FROM: Vincent L. Bodnar, ASA, MAAA RE: Penn Treaty Network American Insurance Company and American Network

MEMORANDUM. SUBJECT: Benchmarks for the Second Half of 2008 & 12 Months Ending 12/31/08

MEMORANDUM TO: FROM: HR Investment Center Members Matt Cinque, Managing Director DATE: March 12, 2009 SUBJECT: Benchmarks for the Second Half of 2008 & 12 Months Ending 12/31/08 Please find enclosed the

MEMORANDUM TO: FROM: HR Investment Center Members Matt Cinque, Managing Director DATE: March 12, 2009 SUBJECT: Benchmarks for the Second Half of 2008 & 12 Months Ending 12/31/08 Please find enclosed the

The Lincoln National Life Insurance Company Term Portfolio

The Lincoln National Life Insurance Company Term Portfolio State Availability as of 7/16/2018 PRODUCTS AL AK AZ AR CA CO CT DE DC FL GA GU HI ID IL IN IA KS KY LA ME MP MD MA MI MN MS MO MT NE NV NH NJ

The Lincoln National Life Insurance Company Term Portfolio State Availability as of 7/16/2018 PRODUCTS AL AK AZ AR CA CO CT DE DC FL GA GU HI ID IL IN IA KS KY LA ME MP MD MA MI MN MS MO MT NE NV NH NJ

Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average

Issue Brief March 6, 2012 Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average The money we pay in fees and taxes helps create jobs, build a strong economy, and preserve Oregon

Issue Brief March 6, 2012 Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average The money we pay in fees and taxes helps create jobs, build a strong economy, and preserve Oregon

Age of Insured Discount

A discount may apply based on the age of the insured. The age of each insured shall be calculated as the policyholder s age as of the last day of the calendar year. The age of the named insured in the

A discount may apply based on the age of the insured. The age of each insured shall be calculated as the policyholder s age as of the last day of the calendar year. The age of the named insured in the

SCHIP: Let the Discussions Begin

Figure 0 SCHIP: Let the Discussions Begin Diane Rowland, Sc.D. Executive Vice President, Henry J. Kaiser Family Foundation and Executive Director, Kaiser Commission on for Alliance for Health Reform February

Figure 0 SCHIP: Let the Discussions Begin Diane Rowland, Sc.D. Executive Vice President, Henry J. Kaiser Family Foundation and Executive Director, Kaiser Commission on for Alliance for Health Reform February

Massachusetts Budget and Policy Center

Progressive Massachusetts 2013 Policy Conference March 24, 2013 Lasell College Newton, MA Presentation by Massachusetts Budget and Policy Center Our State Budget: Building a Better Future Together Massachusetts

Progressive Massachusetts 2013 Policy Conference March 24, 2013 Lasell College Newton, MA Presentation by Massachusetts Budget and Policy Center Our State Budget: Building a Better Future Together Massachusetts

Long-Term Care Education Requirements Prior to Selling

for Training AK All Health 8 hrs 4 hrs 24 months AL All Accident & Health 8 hrs 4 hrs Renewal deadline is the date the license expires. s are renewed biennially based on agent's birth month and year. AR

for Training AK All Health 8 hrs 4 hrs 24 months AL All Accident & Health 8 hrs 4 hrs Renewal deadline is the date the license expires. s are renewed biennially based on agent's birth month and year. AR

36 Million Without Health Insurance in 2014; Decreases in Uninsurance Between 2013 and 2014 Varied by State

36 Million Without Health Insurance in 2014; Decreases in Uninsurance Between 2013 and 2014 Varied by State An estimated 36 million people in the United States had no health insurance in 2014, approximately

36 Million Without Health Insurance in 2014; Decreases in Uninsurance Between 2013 and 2014 Varied by State An estimated 36 million people in the United States had no health insurance in 2014, approximately

Who s Above the Social Security Payroll Tax Cap? BY NICOLE WOO, JANELLE JONES, AND JOHN SCHMITT*

Issue Brief September 2011 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax: 202-588-1356 www.cepr.net Who s Above the Social Security

Issue Brief September 2011 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax: 202-588-1356 www.cepr.net Who s Above the Social Security

2016 GEHA. dental. FEDVIP Plans. let life happen. gehadental.com

2016 GEHA dental FEDVIP Plans let life happen gehadental.com Smile, you re covered, with great benefits and a large national network. High maximum benefits $25,000 for High Option Growing network of dentists

2016 GEHA dental FEDVIP Plans let life happen gehadental.com Smile, you re covered, with great benefits and a large national network. High maximum benefits $25,000 for High Option Growing network of dentists

Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston

The Growing Instability of Revenues over the Business Cycle: Putting the New England States in Perspective Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston Lincoln Institute

The Growing Instability of Revenues over the Business Cycle: Putting the New England States in Perspective Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston Lincoln Institute

ehealth, Inc Fall Cost Report for Individual and Family Policyholders

ehealth, Inc. 2010 Fall Cost Report for and Family Policyholders Table of Contents Page Methodology.................................................................. 2 ehealth, Inc. 2010 Fall Cost Report

ehealth, Inc. 2010 Fall Cost Report for and Family Policyholders Table of Contents Page Methodology.................................................................. 2 ehealth, Inc. 2010 Fall Cost Report

Long-Term Care Education Requirements Prior to Selling

for AK All Health 8 hrs 4 hrs 24 months AL All Accident & Health 8 hrs 4 hrs Renewal deadline is the date the license expires. s are renewed biennially based on agent's birth month and year. AR All Accident,

for AK All Health 8 hrs 4 hrs 24 months AL All Accident & Health 8 hrs 4 hrs Renewal deadline is the date the license expires. s are renewed biennially based on agent's birth month and year. AR All Accident,

Alaska Transportation Finance Study Alaska Municipal League

Alaska Transportation Finance Study Alaska Municipal League presented to Alaska House Transportation Committee presented by Christopher Wornum Cambridge Systematics, Inc. February 12, 2009 Transportation

Alaska Transportation Finance Study Alaska Municipal League presented to Alaska House Transportation Committee presented by Christopher Wornum Cambridge Systematics, Inc. February 12, 2009 Transportation

Federal Tax Reform Impact on 2019 Legislative Sessions: GILTI

Federal Tax Reform Impact on 2019 Legislative Sessions: GILTI Executive Committee Task Force on State and Local Taxation Scottsdale, Arizona November 17, 2018 Karl Frieden, COST Deborah Bierbaum, AT&T

Federal Tax Reform Impact on 2019 Legislative Sessions: GILTI Executive Committee Task Force on State and Local Taxation Scottsdale, Arizona November 17, 2018 Karl Frieden, COST Deborah Bierbaum, AT&T

Eye on the South Carolina Housing Market presented at 2008 HBA of South Carolina State Convention August 1, 2008

Eye on the South Carolina Housing Market presented at 28 HBA of South Carolina State Convention August 1, 28 Robert Denk Assistant Staff Vice President, Forecasting & Analysis 2, US Single Family Housing

Eye on the South Carolina Housing Market presented at 28 HBA of South Carolina State Convention August 1, 28 Robert Denk Assistant Staff Vice President, Forecasting & Analysis 2, US Single Family Housing

RLI TRANSPORTATION A Division of RLI Insurance Company 2970 Clairmont Road, Suite 1000 Atlanta, GA Phone: Fax:

RLI TRANSPORTATION A Division of RLI Insurance Company 2970 Clairmont Road, Suite 1000 Atlanta, GA 30329 Phone: 404-315-9515 Fax: 404-315-6558 AGENCY/BROKER PROFILE Please type your answers. Use a separate

RLI TRANSPORTATION A Division of RLI Insurance Company 2970 Clairmont Road, Suite 1000 Atlanta, GA 30329 Phone: 404-315-9515 Fax: 404-315-6558 AGENCY/BROKER PROFILE Please type your answers. Use a separate

Corporate Income Tax and Policy Considerations

Corporate Income Tax and Policy Considerations Presentation by Richard Anklam, Executive Director, New Mexico Tax Research Institute To The Interim Revenue Stabilization and Tax Policy Committee September

Corporate Income Tax and Policy Considerations Presentation by Richard Anklam, Executive Director, New Mexico Tax Research Institute To The Interim Revenue Stabilization and Tax Policy Committee September

Just The Facts: On The Ground SIF Utilization

Just The Facts: On The Ground SIF Utilization The Access 4 Learning Community (A4L), previously the SIF Association, has changed its brand name due to the fact that the majority of its 3,000 members represent

Just The Facts: On The Ground SIF Utilization The Access 4 Learning Community (A4L), previously the SIF Association, has changed its brand name due to the fact that the majority of its 3,000 members represent

State of the Automotive Finance Market

State of the Automotive Finance Market A look at loans and leases in Q4 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

State of the Automotive Finance Market A look at loans and leases in Q4 2017 Presented by: Melinda Zabritski Sr. Director, Financial Solutions www.experian.com/automotive 2018 Experian Information Solutions,

State and Local Sales Tax Revenue Losses from E-Commerce: Estimates as of July 2004

State and Local Sales Tax Revenue Losses from E-Commerce: Estimates as of July 2004 by Dr. Donald Bruce, Research Assistant Professor dbruce@utk.edu and Dr. William F. Fox, Professor and Director billfox@utk.edu

State and Local Sales Tax Revenue Losses from E-Commerce: Estimates as of July 2004 by Dr. Donald Bruce, Research Assistant Professor dbruce@utk.edu and Dr. William F. Fox, Professor and Director billfox@utk.edu

Fiduciary Tax Returns

Functions and Procedures Index Books On Line Main Directory Overview... 2 How does it work?... 3 What Information is transmitted to the Tax Service?... 4 How do I initiate this service?... 8 Do I have

Functions and Procedures Index Books On Line Main Directory Overview... 2 How does it work?... 3 What Information is transmitted to the Tax Service?... 4 How do I initiate this service?... 8 Do I have

Frequently Asked Questions on Durable Medical Equipment, Prosthetics, Orthotics, and Supplies (DMEPOS) 2015 Medicare Payment Final Rules (CMS-1614-F)

2015 Medicare Payment Final Rules (CMS-1614-F)") Frequently Asked Questions on Durable Medical Equipment, Prosthetics, Orthotics, and Supplies (DMEPOS) 2015 Medicare Payment Final Rules (CMS-1614-F) Adjusting DMEPOS Payment Amounts Using Competitive

Frequently Asked Questions on Durable Medical Equipment, Prosthetics, Orthotics, and Supplies (DMEPOS) 2015 Medicare Payment Final Rules (CMS-1614-F) Adjusting DMEPOS Payment Amounts Using Competitive

Unemployment Insurance Benefit Adequacy: How many? How much? How Long?

Unemployment Insurance Benefit Adequacy: How many? How much? How Long? Joel Sacks, Deputy Commissioner Washington State Employment Security Department March 1, 2012 1 Outline How many get unemployment

Unemployment Insurance Benefit Adequacy: How many? How much? How Long? Joel Sacks, Deputy Commissioner Washington State Employment Security Department March 1, 2012 1 Outline How many get unemployment

2018 ADDENDUM INSTRUCTIONS

2018 ADDENDUM INSTRUCTIONS FEBRUARY 22, 2019 UPDATE: 2018 MUNICIPAL REFERENCE BOOK 1. DELAWARE funds are listed on page 15. You may note on page 15 to see the addendum for additional Delaware funds. The

2018 ADDENDUM INSTRUCTIONS FEBRUARY 22, 2019 UPDATE: 2018 MUNICIPAL REFERENCE BOOK 1. DELAWARE funds are listed on page 15. You may note on page 15 to see the addendum for additional Delaware funds. The

Section 4(f) That was then this is now. Recent developments in Section 4(f) compliance

That was then this is now. Recent developments in Section 4(f) compliance") Section 4(f) That was then this is now Recent developments in Section 4(f) compliance Section 4(f) of the 1966 DOT Act The Secretary may approve a transportation program or project requiring the use of

Section 4(f) That was then this is now Recent developments in Section 4(f) compliance Section 4(f) of the 1966 DOT Act The Secretary may approve a transportation program or project requiring the use of

Medicare Alert: Temporary Member Access

Medicare Alert: Temporary Member Access Plan Sponsor: Coventry/Aetna Medicare Part D Effective Date: Jan. 12, 2015 Geographic Area: National If your pharmacy is a Non Participating provider in the Aetna/Coventry

Medicare Alert: Temporary Member Access Plan Sponsor: Coventry/Aetna Medicare Part D Effective Date: Jan. 12, 2015 Geographic Area: National If your pharmacy is a Non Participating provider in the Aetna/Coventry

Percent of Employees Waiving Coverage 27.0% 30.6% 29.1% 23.4% 24.9%

Number of Health Plans Reported 18,186 3,561 681 2,803 3,088 Offer HRA or HSA 34.0% 42.7% 47.0% 39.7% 35.0% Annual Employer Contribution $1,353 $1,415 $1,037 $1,272 $1,403 Percent of Employees Waiving

Number of Health Plans Reported 18,186 3,561 681 2,803 3,088 Offer HRA or HSA 34.0% 42.7% 47.0% 39.7% 35.0% Annual Employer Contribution $1,353 $1,415 $1,037 $1,272 $1,403 Percent of Employees Waiving

COMPARISON OF ABA MODEL RULE FOR REGISTRATION OF IN-HOUSE COUNSEL WITH STATE VERSIONS

As of September 7, 2016 2016 American Bar Association COMPARISON OF ABA MODEL RULE FOR REGISTRATION OF IN-HOUSE COUNSEL WITH STATE VERSIONS AMERICAN BAR ASSOCIATION CENTER FOR PROFESSIONAL RESPONSIBILITY

As of September 7, 2016 2016 American Bar Association COMPARISON OF ABA MODEL RULE FOR REGISTRATION OF IN-HOUSE COUNSEL WITH STATE VERSIONS AMERICAN BAR ASSOCIATION CENTER FOR PROFESSIONAL RESPONSIBILITY

PLAN TODAY AND HELP SECURE YOUR FUTURE.

PLAN TODAY AND HELP SECURE YOUR FUTURE. GROUP LONG TERM CARE INSURANCE Underwritten by Genworth Life Insurance Company 38682CV 01/28/07 38682CV_SCPMG 03/01/14 This brochure contains educational information

PLAN TODAY AND HELP SECURE YOUR FUTURE. GROUP LONG TERM CARE INSURANCE Underwritten by Genworth Life Insurance Company 38682CV 01/28/07 38682CV_SCPMG 03/01/14 This brochure contains educational information

2017 Supplemental Tax Information

2017 Supplemental Tax Information We have compiled the following information to help you prepare your 2017 federal and state tax returns: - Percentage of income from U.S. government obligations - Federal

2017 Supplemental Tax Information We have compiled the following information to help you prepare your 2017 federal and state tax returns: - Percentage of income from U.S. government obligations - Federal

Report to Congressional Defense Committees

Report to Congressional Defense Committees The Department of Defense Comprehensive Autism Care Demonstration December 2016 Quarterly Report to Congress In Response to: Senate Report 114-255, page 205,

Report to Congressional Defense Committees The Department of Defense Comprehensive Autism Care Demonstration December 2016 Quarterly Report to Congress In Response to: Senate Report 114-255, page 205,

LCCA Design and Maintenance

LCCA Design and Maintenance John Cunningham Iowa Concrete Paving Association ASCE Conference November 6, 2013 www.iowaconcretepaving.org Life Cycle Cost Analysis Life cycle cost analysis (LCCA) is an economic

LCCA Design and Maintenance John Cunningham Iowa Concrete Paving Association ASCE Conference November 6, 2013 www.iowaconcretepaving.org Life Cycle Cost Analysis Life cycle cost analysis (LCCA) is an economic

The Economics of Homelessness

15 The Economics of Homelessness Despite frequent characterization as a psychosocial problem, the problem of homelessness is largely economic. People who become homeless have insufficient financial resources

15 The Economics of Homelessness Despite frequent characterization as a psychosocial problem, the problem of homelessness is largely economic. People who become homeless have insufficient financial resources

ACORD Forms Updated in AMS R1

ACORD Forms Updated in AMS360 2017 R1 The following forms will use the ACORD form viewer, also new in this release. Forms with an indicate they were added because of requests in the Product Enhancement

ACORD Forms Updated in AMS360 2017 R1 The following forms will use the ACORD form viewer, also new in this release. Forms with an indicate they were added because of requests in the Product Enhancement

< Executive Summary > Ready Mixed Concrete Industry Data Report Edition

Ready Mixed Concrete Industry Data Report A benchmarking tool for planning, evaluating and directing the financial activities of your organization. 2012 Edition (2011 data) < Executive Summary > Prepared

Ready Mixed Concrete Industry Data Report A benchmarking tool for planning, evaluating and directing the financial activities of your organization. 2012 Edition (2011 data) < Executive Summary > Prepared

Getting Better Value for the Healthcare Dollar. National Conference of State Legislators Fall Forum November 30, 2011.

Getting Better Value for the Healthcare Dollar National Conference of State Legislators Fall Forum November 30, 2011 NCQA History NCQA a non-profit that for 21 years has worked with federal, state, consumer

Getting Better Value for the Healthcare Dollar National Conference of State Legislators Fall Forum November 30, 2011 NCQA History NCQA a non-profit that for 21 years has worked with federal, state, consumer

Indexed Universal Life Caps

Indexed Universal Life Caps Effective March 15, 2013, the caps on FG Life-Elite II will be changing as follows: Cap Illustrative Rate 100% Participation Annual Point-to-Point 14.75% 8.32% 140% Participation

Indexed Universal Life Caps Effective March 15, 2013, the caps on FG Life-Elite II will be changing as follows: Cap Illustrative Rate 100% Participation Annual Point-to-Point 14.75% 8.32% 140% Participation

PLEASE NOTE: Required American Equity specific Product Training must be completed PRIOR to soliciting an Application to A

PLEASE NOTE: Required American Equity specific Product Training must be completed IOR to soliciting an Application to A Signed in as: JOSEPH E GOSS LTD 3/12/2014 1:18:30 PM Home Announcements Information

PLEASE NOTE: Required American Equity specific Product Training must be completed IOR to soliciting an Application to A Signed in as: JOSEPH E GOSS LTD 3/12/2014 1:18:30 PM Home Announcements Information

Application Trade Credit Insurance Multi Buyer

Chubb Global Markets Political Risk & Credit 1133 Avenue of the Americas New York, NY 10036 (212) 835-3138 (NY) (312) 612-8827 (Chicago) (213) 612-5512 (Los Angeles) Application Trade Credit Insurance

Chubb Global Markets Political Risk & Credit 1133 Avenue of the Americas New York, NY 10036 (212) 835-3138 (NY) (312) 612-8827 (Chicago) (213) 612-5512 (Los Angeles) Application Trade Credit Insurance

CONTINGENT COVERAGES AVAILABLE FOR AUTO LESSORS

CONTINGENT COVERAGES AVAILABLE FOR AUTO LESSORS LESSORS CONTINGENT LIABILITY $100,000 per person, $300,000 per occurrence, Bodily Injury; and $50,000 per occurrence, Property Damage ($100/300/50). As the

CONTINGENT COVERAGES AVAILABLE FOR AUTO LESSORS LESSORS CONTINGENT LIABILITY $100,000 per person, $300,000 per occurrence, Bodily Injury; and $50,000 per occurrence, Property Damage ($100/300/50). As the

Supreme Court Ruling on the Affordable Care Act (ACA): Overview & Implications

: Overview & Implications") Supreme Court Ruling on the Affordable Care Act (ACA): Overview & Implications June 28, 2012 Avalere Health LLC Avalere Health LLC The intersection of business strategy and public policy In a 5-4 Decision,

Supreme Court Ruling on the Affordable Care Act (ACA): Overview & Implications June 28, 2012 Avalere Health LLC Avalere Health LLC The intersection of business strategy and public policy In a 5-4 Decision,

Introduction to the Individual LTC Standards of the Interstate Insurance Product Regulation Commission (IIPRC) March 2011

March 2011") Introduction to the Individual LTC Standards of the Interstate Insurance Product Regulation Commission (IIPRC) March 2011 Karen Schutter, Executive Director, IIPRC Marie Roche, Assistant Vice President,

Introduction to the Individual LTC Standards of the Interstate Insurance Product Regulation Commission (IIPRC) March 2011 Karen Schutter, Executive Director, IIPRC Marie Roche, Assistant Vice President,

The Affordable Care Act (ACA)

") The Affordable Care Act (ACA) An Overview by the Kaiser Family Foundation NBC News Editorial Roundtable June 26, 2013 1. The Basics of the Affordable Care Act (ACA) Expanded Medicaid Coverage Starting

The Affordable Care Act (ACA) An Overview by the Kaiser Family Foundation NBC News Editorial Roundtable June 26, 2013 1. The Basics of the Affordable Care Act (ACA) Expanded Medicaid Coverage Starting

INTERIM SUMMARY REPORT ON RISK ADJUSTMENT FOR THE 2016 BENEFIT YEAR

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Center for Consumer Information and Insurance Oversight 200 Independence Avenue SW Washington, DC 20201 INTERIM SUMMARY REPORT

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Center for Consumer Information and Insurance Oversight 200 Independence Avenue SW Washington, DC 20201 INTERIM SUMMARY REPORT

Medicaid in an Era of Change: Findings from the Annual Kaiser 50 State Medicaid Budget Survey

Medicaid in an Era of Change: Findings from the Annual Kaiser 50 State Medicaid Budget Survey Robin Rudowitz Associate Director, Kaiser Commission on Medicaid and the Uninsured The Henry J. Kaiser Family

Medicaid in an Era of Change: Findings from the Annual Kaiser 50 State Medicaid Budget Survey Robin Rudowitz Associate Director, Kaiser Commission on Medicaid and the Uninsured The Henry J. Kaiser Family

Please print using blue or black ink. Please keep a copy for your records and send completed form to the following address.

20 Disbursement for Beneficiary/QDRO Account IBEW Local Union No. 716 Retirement Plan Instructions About You Please print using blue or black ink. Please keep a copy for your records and send completed

20 Disbursement for Beneficiary/QDRO Account IBEW Local Union No. 716 Retirement Plan Instructions About You Please print using blue or black ink. Please keep a copy for your records and send completed

The State Tax Implications of Federal Tax Reform Legislation

The State Tax Implications of Federal Tax Reform Legislation Executive Committee Task Force on State and Local Taxation Phoenix, Arizona January 14, 2017 Joe Crosby, Multistate Associates Karl Frieden,

The State Tax Implications of Federal Tax Reform Legislation Executive Committee Task Force on State and Local Taxation Phoenix, Arizona January 14, 2017 Joe Crosby, Multistate Associates Karl Frieden,

Comments and Thoughts on Senate Tax Legislation Senate Hearing March 4, 2015

Comments and Thoughts on Senate Tax Legislation Senate Hearing March 4, 2015 Dale Craymer Texas Taxpayers and Research Association 400 West 15 th Street Austin, Texas 78701 www.ttara.org Page 2 TTARA For:

Comments and Thoughts on Senate Tax Legislation Senate Hearing March 4, 2015 Dale Craymer Texas Taxpayers and Research Association 400 West 15 th Street Austin, Texas 78701 www.ttara.org Page 2 TTARA For:

STATE MOTOR FUEL TAX INCREASES:

STATE MOTOR FUEL TAX INCREASES: 2013-2018 Since 2013, 27 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-four of those states increased their

STATE MOTOR FUEL TAX INCREASES: 2013-2018 Since 2013, 27 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-four of those states increased their

PRODUCTS CURRENTLY AVAILABLE FOR SALE. Marquis SP

INTEREST RATES - April 16, 2017 to May 15, 2017 Notices 1. Before soliciting or taking any annuity applications, it is required that you have completed Lafayette Life's Annuity Training and any Continuing

INTEREST RATES - April 16, 2017 to May 15, 2017 Notices 1. Before soliciting or taking any annuity applications, it is required that you have completed Lafayette Life's Annuity Training and any Continuing

Taxing Food for Home Consumption

Taxing Food for Home Consumption Taxing the Poor: Road Map Regional differences in income poverty & poverty related outcomes Historical patterns of property tax Emergence of supermajority rules Growth

Taxing Food for Home Consumption Taxing the Poor: Road Map Regional differences in income poverty & poverty related outcomes Historical patterns of property tax Emergence of supermajority rules Growth

The Entry, Performance, and Viability of De Novo Banks

The Entry, Performance, and Viability of De Novo Banks Yan Lee and Chiwon Yom* FEDERAL DEPOSIT INSURANCE CORPORATION *The views expressed here are solely of the authors and do not necessarily reflect the

The Entry, Performance, and Viability of De Novo Banks Yan Lee and Chiwon Yom* FEDERAL DEPOSIT INSURANCE CORPORATION *The views expressed here are solely of the authors and do not necessarily reflect the

States and Medicaid Provider Taxes or Fees

March 2016 Fact Sheet States and Medicaid Provider Taxes or Fees Medicaid is jointly financed by states and the federal government. Provider taxes are an integral source of Medicaid financing governed

March 2016 Fact Sheet States and Medicaid Provider Taxes or Fees Medicaid is jointly financed by states and the federal government. Provider taxes are an integral source of Medicaid financing governed

What in the World is IRP?

2014 IFTA / IRP Managers & Law Enforcement Workshop Kansas City, MO What in the World is IRP? Presented by: Deb Hill CA Renée Kyser - AL Long, long ago Early 1900s How do we Finance? Structured Taxes 1

2014 IFTA / IRP Managers & Law Enforcement Workshop Kansas City, MO What in the World is IRP? Presented by: Deb Hill CA Renée Kyser - AL Long, long ago Early 1900s How do we Finance? Structured Taxes 1

Cover Crops Green Lands Blue Waters Conference November 03, 2015

Cover Crops 2015 Green Lands Blue Waters Conference November 03, 2015 Disclaimer For Illustration Purposes Only This material does not change the content or the meaning of current policy provisions, filed

Cover Crops 2015 Green Lands Blue Waters Conference November 03, 2015 Disclaimer For Illustration Purposes Only This material does not change the content or the meaning of current policy provisions, filed

Zions Bank Economic Overview

Zions Bank Economic Overview Utah League of Cities and Towns June 18, 2018 Utah Economic Conditions CA 0.6% OR 1.4% WA 1.7% NV 2.0% Utah Population 3 rd Fastest Growing in U.S. ID 2.2% UT 1.9% AZ 1.6%

Zions Bank Economic Overview Utah League of Cities and Towns June 18, 2018 Utah Economic Conditions CA 0.6% OR 1.4% WA 1.7% NV 2.0% Utah Population 3 rd Fastest Growing in U.S. ID 2.2% UT 1.9% AZ 1.6%

AUTO LEASE Insurance Program

P.O. Box 701 Valley Forge, PA 19482 Tel 800-722-3229 Fax 610-933-4993 www.gmi-insurance.com AUTO LEASE Insurance Program CONTINGENT COVERAGES AVAILABLE FOR AUTO LESSORS LESSORS CONTINGENT LIABILITY $100,000

P.O. Box 701 Valley Forge, PA 19482 Tel 800-722-3229 Fax 610-933-4993 www.gmi-insurance.com AUTO LEASE Insurance Program CONTINGENT COVERAGES AVAILABLE FOR AUTO LESSORS LESSORS CONTINGENT LIABILITY $100,000

Experts Predict Sharp Decline in Competition across the ACA Exchanges

Percent of August 19, 2016 Experts Predict Sharp Decline in Competition across the ACA Exchanges Avalere experts predict that one-third of the country will have no exchange plan competition in 2017, leaving

Percent of August 19, 2016 Experts Predict Sharp Decline in Competition across the ACA Exchanges Avalere experts predict that one-third of the country will have no exchange plan competition in 2017, leaving

Insured Deposit Program. Updated 03/31/2017

Insured Deposit Program Welcome to the FDIC Insured Deposit Program. Under this program, available cash balances (from security transactions, dividend and interest payments and other activities) in your

Insured Deposit Program Welcome to the FDIC Insured Deposit Program. Under this program, available cash balances (from security transactions, dividend and interest payments and other activities) in your

Domestic violence funding reduced from $1,253,000 to $1,000,000. $53,000 to fund elder law hotline eliminated.

Court Fees and Fines and State Appropriations by State* 2009-10 Amounts, Major Changes from 2009 Legislative Sessions Noted Revised 3/8/10 (**See note below related to court fees and fines) State Court

Court Fees and Fines and State Appropriations by State* 2009-10 Amounts, Major Changes from 2009 Legislative Sessions Noted Revised 3/8/10 (**See note below related to court fees and fines) State Court

IMPROVING COLLEGE ACCESS

IMPROVING COLLEGE ACCESS Grants and Resources for Education Leaders West Virginia Leaders of Education Conference December 3, 2018 THE EDUCATION ALLIANCE Statewide non-profit organization W E brings B

IMPROVING COLLEGE ACCESS Grants and Resources for Education Leaders West Virginia Leaders of Education Conference December 3, 2018 THE EDUCATION ALLIANCE Statewide non-profit organization W E brings B

Uniform Consent to Service of Process

Applicant Company Name: NAIC No. FEIN: Uniform Consent to Service of Process Original Designation Amended Designation (must be submitted directly to states) Applicant Company Name: Previous Name (if applicable):

Applicant Company Name: NAIC No. FEIN: Uniform Consent to Service of Process Original Designation Amended Designation (must be submitted directly to states) Applicant Company Name: Previous Name (if applicable):

Property Tax Deferral: A Proposal to Help Massachusetts Seniors

Property Tax Deferral: A Proposal to Help Massachusetts Seniors Alicia H. Munnell and Abigail N. Walters Center for Retirement Research at Boston College Economic Perspectives on State and Local Taxes

Property Tax Deferral: A Proposal to Help Massachusetts Seniors Alicia H. Munnell and Abigail N. Walters Center for Retirement Research at Boston College Economic Perspectives on State and Local Taxes

Presented by: Matt Turkstra

Presented by: Matt Turkstra 1 » What s happening in Ohio?» How is health insurance changing? Individual and Group Health Insurance» Important employer terms» Impact small businesses that do not offer insurance?

Presented by: Matt Turkstra 1 » What s happening in Ohio?» How is health insurance changing? Individual and Group Health Insurance» Important employer terms» Impact small businesses that do not offer insurance?

Obamacare in Pictures

Obamacare in Pictures VISUALIZING THE EFFECTS OF THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Spring 2014 If you like your health care plan, can you really keep it? At least 4.7 million health care plans

Obamacare in Pictures VISUALIZING THE EFFECTS OF THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Spring 2014 If you like your health care plan, can you really keep it? At least 4.7 million health care plans

Obamacare in Pictures. Visualizing the Effects of the Patient Protection and Affordable Care Act

Visualizing the Effects of the Patient Protection and Affordable Care Act Fall 2012 expands dependence on government health care dumps millions into Medicaid and creates new federal subsidies for government-approved

Visualizing the Effects of the Patient Protection and Affordable Care Act Fall 2012 expands dependence on government health care dumps millions into Medicaid and creates new federal subsidies for government-approved

Current Trends in the Medicaid RFP Procurement Landscape

Current Trends in the Medicaid RFP Procurement Landscape This is a Presentation Subtitle PRESENTED BY: Michael Lutz Avalere Health October 31, 2017 About Us Michael Lutz Vice President mlutz@avalere.com

Current Trends in the Medicaid RFP Procurement Landscape This is a Presentation Subtitle PRESENTED BY: Michael Lutz Avalere Health October 31, 2017 About Us Michael Lutz Vice President mlutz@avalere.com

Black Knight Mortgage Monitor

Black Knight Mortgage Monitor Mortgage Market Performance Observations Data as of May, 2014 Month-end Black Knight First Look May 2014 Total U.S. loan delinquency rate (loans 30 or more days past due,

Black Knight Mortgage Monitor Mortgage Market Performance Observations Data as of May, 2014 Month-end Black Knight First Look May 2014 Total U.S. loan delinquency rate (loans 30 or more days past due,

NCSL Midwest States Fiscal Leaders Forum. March 10, 2017

NCSL Midwest States Fiscal Leaders Forum March 10, 2017 Public Pensions: 50-State Overview David Draine, Senior Officer Public Sector Retirement Systems Project The Pew Charitable Trusts More than 40 active,

NCSL Midwest States Fiscal Leaders Forum March 10, 2017 Public Pensions: 50-State Overview David Draine, Senior Officer Public Sector Retirement Systems Project The Pew Charitable Trusts More than 40 active,

STATE TAX WITHHOLDING GUIDELINES

STATE TAX WITHHOLDING GUIDELINES ( Guardian Insurance & Annuity Company, Inc. and Guardian Life Insurance Company of America (hereafter collectively referred to as Company )) (Last Updated 11/2/215) state

STATE TAX WITHHOLDING GUIDELINES ( Guardian Insurance & Annuity Company, Inc. and Guardian Life Insurance Company of America (hereafter collectively referred to as Company )) (Last Updated 11/2/215) state

STATE MOTOR FUEL TAX INCREASES:

Since 2013, 26 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-three of those states increased their state gas tax, while three states Kentucky,

Since 2013, 26 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-three of those states increased their state gas tax, while three states Kentucky,

Administrative handbook Aetna Funding Advantage SM

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Administrative handbook Aetna Funding Advantage SM For self-insured groups with less than 100 eligible employees

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Administrative handbook Aetna Funding Advantage SM For self-insured groups with less than 100 eligible employees

Texas Economic Outlook: Cruising in Third Gear

Texas Economic Outlook: Cruising in Third Gear Keith Phillips Assistant Vice President and Senior Economist 1/19/17 The views expressed in this presentation are strictly those of the presenter and do not

Texas Economic Outlook: Cruising in Third Gear Keith Phillips Assistant Vice President and Senior Economist 1/19/17 The views expressed in this presentation are strictly those of the presenter and do not

Strategic Partner(s) - Private Corporate Debt RFP #I Response to Inquiries

- Private Corporate Debt RFP #I Response to Inquiries") Strategic Partner(s) - Private Corporate Debt RFP #I-2017-4 Response to Inquiries 1. We would like to complete the IPERS RFP #I-2017-4 but have a few questions that require clarification: a. Please define

Strategic Partner(s) - Private Corporate Debt RFP #I-2017-4 Response to Inquiries 1. We would like to complete the IPERS RFP #I-2017-4 but have a few questions that require clarification: a. Please define

Executive Summary. Introduction

Date: Regarding: 2014-2017 United States Animal Loss Claims (External Dissemination) Prepared by: David Fennig, Strategic Analyst Executive Summary The purpose of this ForeCAST SM is to analyze claims

Date: Regarding: 2014-2017 United States Animal Loss Claims (External Dissemination) Prepared by: David Fennig, Strategic Analyst Executive Summary The purpose of this ForeCAST SM is to analyze claims

Arturo Pérez National Conference of State Legislatures

STATE BUDGET UPDATE Presentation at the Fiscal Leaders Seminar & Fall Forum Washington, D.C. Arturo Pérez National Conference of State Legislatures OVERVIEW Better state fiscal conditions Few budget gaps

STATE BUDGET UPDATE Presentation at the Fiscal Leaders Seminar & Fall Forum Washington, D.C. Arturo Pérez National Conference of State Legislatures OVERVIEW Better state fiscal conditions Few budget gaps

State, Local and Net Tuition Revenue Supporting General Operating Expenses of Higher Education, U.S., Fiscal Year 2010, Current (unadjusted) Dollars

Dollars") State, Local and Net Tuition Revenue Supporting General Operating Expenses of Higher Education, U.S., Fiscal Year 2010, Current (unadjusted) Dollars Net Tuition $51.3 Billion 37% All State Support $73.7

State, Local and Net Tuition Revenue Supporting General Operating Expenses of Higher Education, U.S., Fiscal Year 2010, Current (unadjusted) Dollars Net Tuition $51.3 Billion 37% All State Support $73.7

Premium Savings Program Broker Training

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Premium Savings Program Broker Training April 2013 We are responding to ACA changes Pricing volatility Rate shock

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Premium Savings Program Broker Training April 2013 We are responding to ACA changes Pricing volatility Rate shock