Inherited Traditional IRAs for Non-Spouse Beneficiaries.

|

|

|

- Bennett Short

- 6 years ago

- Views:

Transcription

1 Rev2/15/2018 Inherited Traditional IRAs for Non-Spouse Beneficiaries. We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly. 8:30 am CST or 12:30 pm CST Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may be reproduced in any form and by any means without prior written permission from Collin W. Fritz & Associates, Ltd.

2 Just a Reminder: This is copyrighted material. No audio or video recording is permitted without prior written permission from Collin W. Fritz & Associates, Ltd. Thank you for your compliance. 2

3 The Audio Portion of this presentation is available either by phone or by using the speakers and microphone on your PC. The phone number is provided to you in the confirmation from CWF and again at the time you join the meeting. You will need the access code that was ed to you in the confirmation from CWF. The confirmation code is 9 digits in length e.g You will also need the Audio Pin # which is shown to you at the time you join this meeting. If you need assistance re-connecting please call CWF at Copyright 2011 Collin W. Fritz & Associates, Ltd The Pension Specialists 3

4 Traditional IRAs Purpose(s): An accountholder uses this special savings account to accumulate funds to be primarily used for his or her retirement and to provide for a beneficiary or beneficiaries after his or her death. An IRA is a special tax-preferred revocable trust. 4

5 Overview Once the IRA accountholder dies, his or her IRA becomes an inherited IRA. This happens as a matter of a law. The IRA funds will now be used to benefit the beneficiary(ies) rather than the IRA accountholder. The beneficiary must comply with beneficiary RMD rules. This webinar covers administering a traditional inherited IRA. Similar concepts will apply to inherited Roth IRAs which are addressed in another webinar. Tax Benefit An inherited IRA is a tax preferred savings and investment allowing the beneficiary to continue to receive the benefits of tax deferred income and the compounding of income. 5

6 Overview Special rules apply to an inherited IRA. First, an inherited IRA must make required distributions to the beneficiary(ies). Second, there can be no additional contributions made. If such distributions are not made by the appropriate deadline, a beneficiary is liable to pay a 50% excise tax of the amount required to be withdrawn. Types of Inherited IRAs Traditional SEP-IRA SIMPLE-IRA Roth Traditional IRAs will be discussed first. All of the distribution rules applying to a traditional IRA, also apply to a SEP-IRA and SIMPLE-IRA. Roth IRAs will be discussed second. 6

participant Beneficiaries Original Subsequent In general, the beneficiary will include the")

7 Inherited IRAs for Non-Spouse Distributions Accountholder Before Age 59½ Age 59½ to 70½ and older 7 Contributions Deductible Non-Deductible Custodial or Trust Account Earnings within Account are not Taxed 1. No Annual or Rollover Contribution 2. Transfer-in from decedent s IRA 3. Transfer from inherited IRA to Another Inherited IRA 4. Direct Rollover in from deceased 401(k) participant Beneficiaries Original Subsequent In general, the beneficiary will include the distribution in income and pay tax but will not owe the 10% tax. 7

8 Inherited IRAs for Beneficiaries Traditional IRA Owner has Died Before Decedent s Required Beginning Date On or After Decedent s Required Beginning Date Spouse Beneficiary Who is Sole Beneficiary Non-Spouse or Spouse Who is not Sole Beneficiary Qualified Trust Estate, Non- Qualified Trust, Church or Charity Spouse Beneficiary Who is Sole Beneficiary Non-Spouse or Spouse Who is not Sole Beneficiary Qualified Trust Estate, Non- Qualified Trust, Church or Charity Treat as Own Treat as Own Special Life Distribution Rule 5-Year Rule Standard Life distribution rule 5-Year Rule Standard Life distribution rule using the oldest trust beneficiary 5-Year Rule 5-Year Rule is mandatory Special Life Distribution Rule Standard Life distribution rule Standard Life distribution rule using the oldest trust beneficiary Special Life rule using the decedent s age as of the year he or she died. 8

9 9 CWF # 56I CWF # 56RI 9

10 Possible, Probable Future Law Changes * 1. Reduce the Distribution Period Applying to the Beneficiary a. 30 Years b. 20 Years c. 10 Years d. 5 Years 2. Grandfather current beneficiaries 10

11 Decedent s IRA Inherited IRA for a Non-Spouse Beneficiary Non-Reportable transfer. Any distribution will be a reason code 4 if a Non-Reportable traditional transfer. IRA and Any a Q distribution or T if a Roth will be IRA. a reason code 4 if a traditional IRA and a Q or T if a Roth IRA. 11

Rollover/Conversion Non-Spouse Beneficiary Inherited Roth IRA")

12 Direct Rollovers Yes Rollovers - No Inherited QRP Direct Rollover Non-Spouse Beneficiary Inherited Traditional IRA Inherited QRP (Direct) Rollover/Conversion Non-Spouse Beneficiary Inherited Roth IRA Eligible Retirement Plan to Roth IRA Conversion. Since 2008 other retirement accounts can be converted directly to a Roth IRA. This includes inheriting beneficiary of ERP. Inherited Roth QRP (Direct) Rollover Inherited Roth IRA 12

13 Special Administration 1. Special titling for Form 5498 purposes. As a result of the above special rules, an IRA beneficiary must be able to identify the source of each IRA he or she inherited for purposes of figuring the taxation of a distribution from an IRA. * For example, Jane Doe as beneficiary of John Doe s traditional IRA. 2. No rollover rights 3. No Additional Contributions 4. Special Transfer considerations 5. Special RMD requirements 13

14 General Rule - Annual RMD is made to a Beneficiary Over His or Her Life Expectancy Unless 5 Year Rule Would Apply and Be Elected. Beneficiary Must Take RMD or an Amount larger than the RMD or the 50% tax is owed. 14

15 Special Administration Background: An inherited IRA (or beneficiary IRA) must be administered differently than the IRAs for living accountholders. There are numerous reasons. First, a beneficiary IRA is not allowed to accept additional contributions, and a non-spouse beneficiary is not eligible to roll over a distribution from a beneficiary IRA. Second, the required distribution rules always apply to an inherited IRA. Third, the beneficiary steps into the deceased taxpayer s shoes and assumes the tax rights which the deceased accountholder had in the IRA. With one exception, the IRA distribution will be included in the income of the beneficiary (and not the deceased accountholder), if applicable, and the beneficiary will have to pay the taxes on such distribution at his or her marginal tax rate, if applicable. As a result of the above special rules, an IRA beneficiary must be able to identify the source of each IRA he or she inherited for purposes of figuring the taxation of a distribution from an IRA. For example, Jane Doe as beneficiary of John Doe s traditional IRA. 15

16 Non-Spouse Beneficiary Cannot Elect to treat the Decedent s IRA as own or roll over a distribution from an inherited IRA to another inherited IRA or a regular IRA A non-spouse beneficiary must be very sure that he or she wishes to be paid funds from an inherited IRA, because a rollover is never permissible, including a rollover back into the financial institution which just issued a distribution check. Likely lawsuit if your bank makes a distribution which was not requested. 16

17 IRS Procedures Form 5498 (box 11) - Not Required And Not to be Checked RMD Notices - Not Required, but CWF recommends RMD Calculations - Not Required, but CWF recommends Inherited IRA Plan Agreement - 2 Approaches Tax Court in Bobrow vs. IRS Commissioner Taxpayers rely on IRS Guidance at their own peril. 17

18 Establishing the Inherited IRA for a Beneficiary Created as a matter of law Copy of Decedent s last IRA Plan Agreement New Inherited IRA Plan Agreement - Recommended 18

19 Overview Traditional IRA Beneficiary CWF Inherited IRA Plan Agreement & Disclosure Statement Forms: 40-TI Custodial 41-TI Trust 42 -TI Custodial Self-Directed 19

20 General Procedures Once the IRA custodian/trustee knows of the death of an accountholder, we suggest the following procedure: Identify who is the primary beneficiary or who are the primary beneficiaries. Set up an inherited IRA file for each beneficiary. You will want to put a copy of the deceased accountholder s IRA plan agreement and beneficiary designation in this file along with the other documents discussed herein. Send a letter to each named beneficiary. The letter should inform the beneficiary that you will need to be furnished a certified death certificate (or a similar legal document) as evidence of the accountholder s death. The letter should also inform the beneficiary that certain elections will need to be made as to how and when his or her share is to be paid. A Form #204 or similar form should be enclosed. 20

21 General Procedures (continued): Retain a copy of the death certificate in the file. Retain a copy of the elections and the instruction for a distribution schedule. Determine if some beneficiaries will not be beneficiaries for RMD purposes. Set up procedures to annually monitor these distributions for correctness as to amount and as to timeliness. Document the distribution(s) so that you are preparing the Form 1099-R correctly. Make sure that there is compliance with the withholding rules. Allow each beneficiary to designate his or her own beneficiary(ies) 21

22 Understanding the Policies and Procedures To Pay Out to a Beneficiary As Set Forth in the IRA Plan Agreement The IRA custodian/trustees must understand what its IRA plan agreement states are the policies and procedures applying to required distributions. Set forth below is what CWF s IRA plan agreement states. 1.7 Special Distribution Rules to Ensure Compliance with Required Minimum Distribution Rules by Beneficiaries and Special Provisions for Inherited IRAs. You agree to inform any person who is your beneficiary that he or she is your beneficiary and he or she must inform us of your death. We have the right to require that your beneficiary(ies) furnish us with a certified copy of your death certificate or other documentation as we feel appropriate to verify your death. 22

23 Understanding the Policies and Procedures To Pay Out to a Beneficiary As Set Forth in the IRA Plan Agreement After your death, there are rules which mandate that your IRA funds be distributed to your beneficiary(ies) on or before certain time deadlines. The time deadlines which apply will depend upon whether you died before or on/after your required beginning date and which available option your beneficiary elects. These deadlines are explained in the Disclosure Statement portion of this IRA book. Upon your death, your IRA will be converted into one or more inherited IRAs. The number of inherited IRAs to be created depend upon the number of your primary beneficiaries alive as of the date of your death. There will be an inherited IRA created for each beneficiary. The following rules will govern such inherited IRAs. These rules are in addition to the other rules of this agreement and will govern if there is a conflict. 23

24 Understanding the Policies and Procedures To Pay Out to a Beneficiary As Set Forth in the IRA Plan Agreement You agree that we have the right to establish an inherited IRA account for each beneficiary on our data processing system even before a beneficiary instructs us how he or she will take the withdrawals. We will have the authority to move the funds from your IRA to one of more new inherited IRA accounts. We will have the right, if necessary, because of data processing or administrative requirements to surrender the savings and time deposits which comprised your account and establish new ones for the inherited IRAs. We will transfer an inherited IRA to another IRA custodian or trustee, but only if the requesting beneficiary and the receiving IRA custodian/trustee will furnish us with a special transfer of inherited IRA administrative form so it clearly acknowledged that it is an inherited IRA which is being transferred. Inherited IRAs are not eligible to be rolled over unless the beneficiary is a spouse. He or She need not be the sole beneficiary to receive a distribution from the deceased spouse s IRA. Each beneficiary will be required to instruct us in writing as to how he or she will withdraw funds from his or her inherited IRA so that the required minimum distributions rules will be satisfied. 24

25 Understanding the Policies and Procedures To Pay Out to a Beneficiary As Set Forth in the IRA Plan Agreement A Spouse beneficiary will be deemed to have elected the life-distribution rules unless he or she expressly elects the five-year rule on or before December 31 of the year following the year of your death. A non-spouse beneficiary will also be deemed to have elected the life-distribution rules unless he or she expressly elects the five-year rule on or before December 31 of the year following your death. We have forms available which can be used by your beneficiary to instruct us which option he or she elects and to establish a distribution schedule. Alternatively, the beneficiary may elect to use the alternative certification method. The beneficiary must furnish us a written notice of his or her intent to use the alternative certification method. We will furnish the beneficiary a form which can be used to make this election, upon his or her request. We shall have the authority but not the duty to distribute any required minimum distribution to your beneficiary(ies). Any beneficiary shall be solely responsible to make sure that the required minimum distributions take place on a timely basis. 25

26 Set up the Inherited IRA for Each Inheriting Beneficiary An inherited IRA will be titled, John Doe as the IRA beneficiary of Jane Doe. You will want to put a copy of the decedent s IRA plan agreement and the beneficiary designation into this file. If a deceased accountholder has more than one beneficiary, then there will need to be an inherited IRA set up for each beneficiary. Each beneficiary will individually have to comply with the RMD rules. You may also want the inheriting beneficiary to sign a new inherited IRA plan agreement. This is certainly necessary if the funds are being directly rolled over by a non-spouse beneficiary from a 401(k) plan or similar plan to an inherited IRA. 26

27 Establishing Inherited IRAs/Inherited Plan Agreements CWF has created IRA plan agreements specifically for inheriting beneficiaries. As you know, the rules for beneficiaries differ considerably from those of the original accountholder. A financial institution normally handles a beneficiary situation by merely placing the original plan agreement, or a copy of it, in the beneficiary s file. In an amending situation, it is confusing as to how to amend the plan agreement. Normally amending would still be geared toward only the original accountholder. CWF believes it would simplify things for the financial institution, and the rules would be more clearly understood by the beneficiaries, if the plan agreement detailed the rules as they apply to beneficiaries. 27

28 Establishing Inherited IRAs/Inherited Plan Agreements An inherited IRA plan agreement highlights important beneficiary issues, such as the ability of a beneficiary to, in turn, designate their own beneficiary(ies), the various distribution options and required beginning dates, and the deadline to change from a 5- year rule to the life-distribution rule. These are important issues of which beneficiaries must be made aware to enable them to make informed decisions concerning their inherited account. These issues are not thoroughly explained in the plan agreement which the original accountholder would have signed. We at CWF believe this is a valuable product to aid your financial institution in providing excellent customer service by helping your staff and accountholders understand the special rules which apply to beneficiaries. There are inherited traditional IRAs and inherited Roth IRAs. Sample Inherited IRA Application (See next page) 28

29 Inherited IRAs for Non-Spouse Beneficiaries CWF 40TI Inherited IRA Custodial Account Application Form 5305-A CWF40TI 29

30 Designation of a Beneficiary(ies) by the Inheriting Beneficiary May an inheriting IRA Beneficiary designate a beneficiary or beneficiaries of his or her share? Yes, the 1987 RMD rules generally prevented a beneficiary from designating a beneficiary; the 2002 rules allow such designation. You will want to check to see that your IRA plan agreement has been revised to authorize this. For example, CWF s Form 40-T at section 1.6 provides: Naming Beneficiaries and Methods of Payment. You may name one of more beneficiaries to receive your IRA assets after your death. We require that you use our beneficiary form to designate your beneficiary or beneficiaries and that you sign this form and file it with us during your lifetime. You are deemed to have furnished us with your beneficiary designation if you furnished such a form to an entity with respect to which we are considered to be a successor custodian and we have such designation in our files. You may change your beneficiaries at any time, and the consent of a beneficiary is not required unless you reside in a state with community or marital property laws. When you sign a new beneficiary form, you revoke all prior beneficiary designations. If you don t name a beneficiary, or none of the name beneficiaries are alive on the date of your death, your IRA assets will be paid to your estate. Researching state law. 30

31 Designation of a Beneficiary(ies) by the Inheriting Beneficiary As the beneficial owner of the IRA assets, you can instruct how and when these assets will be paid to the beneficiaries. If you don t instruct, your beneficiaries will have the right to choose how and when the assets will be paid. Any method of payment must satisfy the provisions of Article IV and other governing law. After your death, each primary beneficiary who acquires an interest in your IRA shall have the right to designate his or her own beneficiary(ies) with respect to his or her share. The procedures for designating a beneficiary(ies) which apply to you as the accountholder shall also to your beneficiary. When a beneficiary signs a new or revised beneficiary designation form, your beneficiary revokes all of his or her prior beneficiary designations. If the beneficiary doesn t designate his other beneficiary(ies), or if a designated beneficiary is not alive when the beneficiary dies, then the remaining IRA assets will be paid to such beneficiary s estate. Any method of payment must satisfy the provisions of Article IV and other governing law. 31

32 RMD Calculations - What Rules Apply For the Year the IRA Accountholder Dies? - If the IRA accountholder dies prior to his or her required beginning date. - Prior to 70½ year. No RMD applies for year of death. - If the year of death is the 70½ year, IRS guidance is conflicting. Regulation vs. Publication If the IRA accountholder dies on or after his or her required beginning date - The RMD for the year of death is determined using the Uniform Lifetime Table. 32

33 Distribution, if any, due for year of death. a. If the decedent dies before his or her 70½ year, then there is no required distribution for the beneficiary to take for the year of death. b. If the decedent died during the year he or she attained or would have attained age 70½ or the following year, but before his or her required beginning date and the beneficiary is a spouse beneficiary, then the RMD for such year must be distributed to the surviving spouse beneficiary to the extent not distributed to the decedent prior to his or her death. For a non-spouse beneficiary no distribution is required. c. If the decedent died on or after his or her required beginning date, then his or her RMD for such year must be distributed to the beneficiary to the extent not distributed to the decedent prior to his or her death. 33

34 What Rules Apply When the IRA Accountholder Dies on or after required beginning date? RMD for year of death must be distributed to the beneficiary(ies) to the extent not paid to the decedent by December 31 of such year. If the entire RMD has been paid, then there is no remaining RMD for the year of death needing to be distributed. If the entire RMD had not been paid to the decedent prior to his or her death, then a beneficiary must be paid his or her share of the remaining RMD by December 31 of that year. The non-spouse beneficiary will need to be paid his or her proportionate share of the RMD by December 31, or the 50% tax will apply unless the IRS would waive. 34

35 Determine did the Accountholder die before or after his or her required beginning date? When was the deceased IRA accountholder born? When did the deceased IRA accountholder die? Examples: Jane Doe was born Situation # 1 she died Situation # 2 - she died before her RBD after her RBD Jan 1 Dec 31 Mar 31 Apr 1 Age 70½ Required Beginning Date Dies Before the RBD Dies On or After the RBD 35

36 Determine Which Death Situation Applies 1. Did the IRA Accountholder die before or after RBD? 2. Who or what is the beneficiary? 36

37 Inherited IRAs for Beneficiaries Traditional IRA Owner has Died Before Decedent s Required Beginning Date On or After Decedent s Required Beginning Date Spouse Beneficiary Who is Sole Beneficiary Non-Spouse or Spouse Who is not Sole Beneficiary Qualified Trust Estate, Non- Qualified Trust, Church or Charity Spouse Beneficiary Who is Sole Beneficiary Non-Spouse or Spouse Who is not Sole Beneficiary Qualified Trust Estate, Non- Qualified Trust, Church or Charity Treat as Own Treat as Own Special Life Distribution Rule 5-Year Rule Standard Life distribution rule 5-Year Rule Standard Life distribution rule using the oldest trust beneficiary 5-Year Rule 5-Year Rule is mandatory Special Life Distribution Rule Standard Life distribution rule Standard Life distribution rule using the oldest trust beneficiary Special Life rule using the decedent s age as of the year he or she died. 37

38 1. Life distribution rule 2. 5 Year Rule (Applies only if death occurred before the RBD *) 38

39 Beneficiary Instruction Form: Put a Beneficiary on Notice He or She is Subject to the RMD Rules and Obtain Written Instructions An excellent way to put a beneficiary on notice of the tax rules and the distribution options available is to furnish a beneficiary with a Beneficiary Election of Instruction Form. An IRA custodian may want to use a copy of CWF s Form # 204 or similar form. CWF s Form # 204 is reproduced on the following pages. This form will also be used by the beneficiary to instruct how he or she will comply with the RMD rules. It should be emphasized to the beneficiary that he or she may well wish to consult with their legal and/or financial advisor before completing the form. 39

40 Beneficiary Instruction Form: Put a Beneficiary on Notice He or She is Subject to the RMD Rules and Obtain Written Instructions It is important for the IRA beneficiary to clearly document his or her election, if applicable, and instructions. CWF Form # 204 (Beneficiary s Distribution Notice and Certificates Form and Payment Instructions) can be used for this purpose. Even if the custodian s/trustee s first knowledge of the IRA accountholder s death is the beneficiary requesting the entire balance of the inherited IRA, it is a good idea to have the beneficiary complete a special form. The special distribution instruction will indicate to them that there are more options than a lump sum distribution. 40

41 Inherited IRAs for Non-Spouse Beneficiaries CWF s Form 204 Beneficiary Instruction Form: Put a Beneficiary on Notice He or She is Subject to the RMD Rules and Obtain Written Instructions CWF204 41

42 Inherited IRAs for Non-Spouse Beneficiaries CWF s Form # 204 Beneficiary Instruction Form: Put a Beneficiary on Notice He or She is Subject to the RMD Rules and Obtain Written Instructions CWF204 Withholding Notice 42

43 Inherited IRAs for Non-Spouse Beneficiaries CWF s Form # 57 Distribution Form: Put a Beneficiary on Notice He or She is Subject to the RMD Rules and Obtain Written Instructions CWF57 43

44 What is the 5-Year Rule or option? Applies only if IRA owner dies before his or her required beginning date. The IRA beneficiary must take sufficient distributions to close the inherited IRA by December 31 of the fifth year containing the Anniversary of the accountholder s death. There is no requirement to take out any specific amount in any year. In actuality, the beneficiary is allowed six calendar years to take his or her RMD s. Year of Death Schedule # 1 Schedule # 2 Schedule # 3 Schedule # 4 Schedule # % 0% 0% 100% 0% % 0% 0% 0% 50% % 0% 0% 0% 0% % 33.3% 0% 0% 0% % 33.3% 0% 0% 50% Remainder % Remainder 33.3% Remainder 100% 0% 0% The inherited IRA must have a zero balance by 12/31/2022 if the accountholder dies in

45 Administering the inherited IRA when the beneficiary has elected the 5- year rule or it applies automatically. Tickler System Manual or computer based Why? 50% tax applies if the inherited IRA is not closed by of the year containing the 5 th anniversary of the IRA accountholder s death. Tax penalty owing can be substantial. 45

46 Example of the Adverse Tax Consequences that will result when the 5- year rule automatically applies Jane Doe accumulated $250,000 in her 401(k) plan. At age 57 she retired from ABC corporation with the thought she would find a new job in 3-6 months. On January 10, 2016, she rolled the $250,000 into her traditional IRA at IRA custodian # 1. Jane was married and they had 4 children. She designated her spouse Mark to be her primary beneficiary and to save time as she had another appointment that day she designated her estate to be her contingent beneficiary. Mark died in a car accident on March 13, Jane died in a separate car accident on May 10, Her estate is her IRA beneficiary and the 5-year rule will apply. The distribution of these funds will not be paid over the life expectancy of the children. Tax deferral and income compounding opportunities are lost and more income tax will need to be paid sooner than otherwise would have been the case. 46

47 Situation # 1 Life Distribution Rule for Before RBD Situation 47

48 The Basic Required Distribution Calculation Yearly Beneficiary RMD = FMV as of preceding year Divisor (Life Expectancy of Beneficiary) Divisor: In general, based on age of the beneficiary, determined as of the year following the accountholder s date of death. Single Life Table. 48

49 Single Life Table (Used only by Beneficiaries) Age of Beneficiary Distribution Period (in years) Age of Beneficiary Distribution Period (in years) Age of Beneficiary Distribution Period (in years) 49

50 Single Life Table (Used only by Beneficiaries) Age of Beneficiary Distribution Period (in years) Age of Beneficiary Distribution Period (in years) Age of Beneficiary Distribution Period (in years) 50

51 General Rule RMD calculated using the divisor based on the beneficiary s age determined the year after the IRA Accountholder died. 51

52 Determining the Period/LE Factor (for situation # 1) Example: The IRA Accountholder dies on at the age of 65, before her RBD. Jane Doe is the only primary beneficiary. She is age 40 in 2017 and will be age 41 in The initial factor comes from the single life table and then subsequent factors are determined by subtracting 1.0 for each following year. Beneficiary Factor Year of Death N/A This same schedule is used for subsequent beneficiary(ies) once the original beneficiary dies. 52

53 Determining the Period/LE Factor (for situation # 2) Example: The IRA Accountholder dies on at the age of 75, after her RBD. Jane Doe is the only primary beneficiary. She is age 40 in 2017 and will be age 41 in Beneficiary Factor Year of Death N/A

54 John Doe dies in His beneficiary is his daughter, Betsy. She is age 40 in 2017 and 41 in The balance in the Inherited IRA as of 12/31/2017 is $28,560. Example #1 assumes a 2% interest/earnings rate. Example #2 assumes a 6% interest/earnings rate. Example # 1 at 2% Example #1 Year of Death Subsequent Year Divisor FMV of Preceding Year 2% Interest RMD 2017 N/A $28,000 $560 N/A $28,560 $571 $ $28,462 $569 $ $28,348 $567 $ $28,218 $564 $ $28,071 $561 $725 This same schedule is used for subsequent beneficiary(ies) once the original beneficiary dies. This schedule will exist for 42 years at its maximum. It obviously can be closed prior to

55 Example # 2 at 6% Divisor FMV of Preceding Year 6% Interest Year of Death Subsequent Year 2017 N/A $28,000 $1680 N/A RMD $29,680 $1781 $ $30,766 $1846 $ $31,874 $1912 $ $33,003 $1980 $ $34,152 $2049 $882 Note Inherited IRA balances increase as long as interest or other earnings being added exceed the RMD. 55

56 Situation # 1 Life Distribution Rule for Before RBD Situation Rita Marx is age 53 in She has designated her daughter, Barb Smith age 24 as her sole beneficiary. She dies on 11/8/2017. Remember that any beneficiary including a sole spouse beneficiary, is deemed to have elected the life-distribution rule, unless he or she expressly elects the five-year rule. The first deadline for the life-distribution rule will be 12/31/2018, since Rita died during Barb is entitled to withdraw the RMD amount, or any amount greater than the RMD, including a lump-sum distribution. For 2018, the RMD amount will be based on Barb s single life expectancy. An initial distribution factor will be determined for 2018 and then reduced by one for each subsequent year. Since she will be 25 in 2018, the factor is Rita Marx Dies Factor Age FMV 2% Interest RMD 2018 Age of Beneficiary $30,000 $600 $ $30,025 $602 $ $30,161 $603 $ $30,227 $605 $548 Continues - 56

57 Situation # 1 Life Distribution Rule for Before RBD Situation LE Factor Determination with Multiple Beneficiaries Under the pre-2002 RMD rules, when an IRA accountholder died having named multiple beneficiaries, the RMD calculation for each beneficiary was based on the age of the oldest beneficiary. Under the post-2001 RMD rules, when an IRA accountholder dies having named multiple beneficiaries, the RMD calculation for each based may be based on the age of each applicable beneficiary as long as the separate accounting rules are met. Example: Mary Thoms designated her daughter, Kim (Age 50) and her son Mark (age 43) as her primary beneficiaries, each to receive 50%. Mary died in 2017 at age 69. Separate inherited IRAs are set up for Kim and Mark in the same year as Mary died. The initial LE factor for Kim is 33.3 since she is age 51 in The initial LE factor for Mark is 39.8 since he is age 44 in

58 What are the Separate Accounting Rules? Why are there separate accounting rules? 1. The inherited IRA must be divided into separate accounts and the beneficiaries with respect to one separate account must differ from the beneficiaries for the other separate accounts. Setting up separate inherited IRAs meet this requirement. 2. The separate accounts must be established by December 31 of the year following the IRA accountholder s death 3. The separate RMD calculation starts the later of: (1) date of the accountholder s death or (2) the year following the calendar year the separate accounts were established. 4. The separate accounting must allocate all post-death investment gains and losses for the period prior to the establishment of the separate accounts on a pro rata basis in a reasonable and consistent basis among the separate accounts for the different beneficiaries. The separate accounting must also allocate any post-death distribution to the separate account of the beneficiary receiving that distribution. Sooner the separate inherited IRA accounts are established the better. CWF documents authorize setting up separate inherited IRA accounts. 58

59 Illustration of Separate Beneficiary Accounting Rules Laura Boyer, age 86, died on 11/4/2016. She had been paid her RMD for 2016 prior to her death. She had designated her four children as her IRA beneficiaries Anna (12/9/1947); Maria (10/9/1952); David 12/29/1955): and Miquel (10/4/1961). Each received a 25% share. The IRA had a FMV balance of $32,400 as of 12/31/2016. Separate inherited IRA accounts were set up for the four beneficiaries on March 16, What required minimum distributions must be made for 2017, 2018, 2019, etc.? Laura died after her required beginning date. There will need to be four(4) required distributions made to the four beneficiaries in 2017, and subsequent years, until the share of each has been completely distributed. The standard RMD formula is: 12/31/xx FMV divided by a distribution period. When there are multiple beneficiaries, the general rule is that the oldest beneficiary is used to determine the distribution period. The Single Life Table is used to calculate the distribution period of all inherited IRA situations. 59

60 Illustration of Separate Beneficiary Accounting Rules Anna, Maria, David and Miquel will each need to be paid their share of the 2017 required distribution. Anna is the oldest beneficiary. Her age is 65 in The Single Life Table shows that the distribution period for a person age 65 is 21 years. Each has an RMD amount of $ calculated as follows: $32,400 / 21.0 / 4 = $ Why isn t there a separate accounting made for each beneficiary in 2017? The reason is: Separate accounts are recognized for purposes of calculating the RMDs only after the later of (1) the year the separate accounts are established; or (2) the year of the accountholder s death. Since the separate inherited IRAs were not set up until 2018, the separate calculations will be permissible for 2018, and subsequent years, but not for 2017 purposes. 60

61 Illustration of Separate Beneficiary Accounting Rules The distribution periods for 2017 and subsequent years will be determined as follows: Beneficiary Anna Maria David Miquel Age in Initial Distr, Period for Calculation Purposes Distribution Period Distribution Period Distribution Period Distribution Period Distribution Period

62 Illustration of Separate Beneficiary Accounting Rules Annual Rules: There is a second special separate accounting rule to remember. The second special rule is that the separate accounts must be established by December 31 of the year after the year the accountholder died. This requirement has been met, since the separate inherited accounts were established on March 16, If the separate accounts had not been established until March 16, 2018, then Maria, David and Miquel would not qualify to use the longer distribution periods based on their respective ages. 62

63 Must an IRA Custodian provide for Separate Accounting when there are Multiple Beneficiaries? No. This topic should be covered in the IRA Plan Agreement and explained in the IRA Disclosure Statement The vast majority of IRA custodian/trustees use separate accounting for RMD purposes because they set up separate inherited IRAs. However, some financial institutions do not do so. In this case, an IRA beneficiary may wish to determine what his or her transfer options are. By transferring to an IRA custodian who is willing to apply the separate accounting rules a beneficiary may be able to have smaller RMDs for subsequent years. 63

64 Situation # 2 Life Distribution Rule for After RBD Situation If the beneficiary is a living person other than the spouse, or the spouse is not your sole beneficiary, and the IRA accountholder dies on or after the required beginning date, then applicable distribution period for years after the year of death will be based on the remaining life expectancy of the designated beneficiary. The beneficiary s remaining life expectancy is calculated using the age of the beneficiary in the year following the year of death, reduced by one for each subsequent year. If there are multiple beneficiaries, the age of the oldest is used unless the separate accounting rules apply. Note that the 5-year rule does not apply, (i.e. is unavailable) when the accountholder dies on or after his RBD. Exception: If the beneficiary is older than the deceased IRA accountholder then the applicable distribution for years after the year of death will be based on the age of the deceased IRA accountholder for the year he or she died and then 1.0 will be subtracted for each subsequent year. 64

65 Situation # 2 Life Distribution Rule for After RBD Situation Example: Rita Marx is age 81 in She has designated here daughter, Barb Smith age 44 as her sole beneficiary. The balance in Rita s IRA as of 12/31/2016 was $27,000. Her RMD amount for 2017 is $1, ($27,000 / 17.9). She died on 11/8/2017. There is a non-spouse beneficiary, and the accountholder has died after her required beginning date. Barb is entitled to withdraw the RMD amount or an amount greater than the RMD, including a lump-sum distribution. For 2017, the RMD amount will have been determined using Rita s age and the Uniform Lifetime Table. For subsequent years, the RMD amount will be based on Barb s single life expectancy determined for the year following the death. An initial distribution period will be determined for 2018, based on age 45, and then reduced by one for each subsequent year. The initial factor or divisor is Divisors for subsequent years will be 37.8, 36.8, 35.8, etc Rita Marx Dies Factor Age 2018 Age of Beneficiary continues Continue to reduce by

66 Special Rule When Beneficiary is Older than the IRA Accountholder Example: Jack, age 72 dies in His IRA beneficiary is his sister (i.e. a non-spouse), Marcy, age 74. The required minimum distribution for 2017 is based on the age Jack would have attained had he lived all of 2016, using the Uniform Lifetime Table. Starting in 2017, the year after the death, Marcy s RMD will be calculated using Jack s age and not her own. The worksheet on the next page will illustrate the special calculation needed. 66

67 Special Traditional IRA Beneficiary RMD Calculation - IRA Accountholder Dies ON or AFTER the RBD and IRA Accountholder is younger than the non-spouse beneficiary Example: Decedent Age 72 Beneficiary Age 74 Year Factor Year Factor Year of Death 2016(72) (74) N/A * 2017(75) * * * Applicable Factor Note: Decedent s Life Expectancy Factor is Always used 67

68 Decedent/Beneficiary Life Expectancy Comparison Calculation Exception This exception only applies when the IRA accountholder has died on or after his or her required beginning date. In addition, for this to apply, the deceased IRA accountholder must be younger than the beneficiary. Section 1.401(a)(9)-5 Q&A 5 of the Regulations under the Internal Revenue Code provides that if the IRA owner dies on or after his/her required beginning date, the distribution calendar years after the distribution calendar year containing the IRA owner s date of death is the longer of: 1. The remaining life expectancy of the IRA owner calculated in the year of death and reduced by one for each subsequent year; and 2. The remaining life expectancy of the non-spouse beneficiary calculated in the year AFTER year of death and reduced by one for each subsequent year. 68

69 Situation # 3 No Living Beneficiary for Before RBD date If the IRA accountholder did not designate a living person as a beneficiary and died before the required beginning date, then the estate or other beneficiary will be required to use the 5-year rule. The life-distribution rule does not apply (i.e. cannot be used). Rita Marx is age 53 in She has designated her estate as her sole beneficiary. She dies on 11/8/2017. The life-distribution rule is unavailable. Planning Point Some IRA accountholders will want to have separate or multiple IRA plan agreements. IRA # 1 would designate the children and IRA # 2 would designate his or her church. 69

70 Situation # 3 No Living Beneficiary for Before RBD Situation Rita Marx is age 53 in She has designated her daughter, Barb Smith age 24 as her sole beneficiary. Barb died in Rita has not yet designated another primary beneficiary so her estate is her beneficiary. Rita died on November 16, The estate s only option is the 5 year rule. The life distribution rule is unavailable. The IRA must be closed by December 31, Note: We will see this situation may also exist under a Roth IRA and most everyone will see it as being very undesirable. Who wants a Roth IRA to end in 5 years? The IRS may, most others will not. 70

71 Situation # 4 No Living Beneficiary for After RBD If the IRA accountholder did not designate a living person as a beneficiary and died on or after the required beginning date, then the applicable distribution period (i.e. the original factor) for years after the year of death is based on the age and life expectancy of the decedent as determined as of December 31 of the year of death. For subsequent years, the original factor is reduced by one for each elapsed year. 71

72 Example Inherited IRAs for Non-Spouse Beneficiaries Rita Marx is age 81 in She has designated her estate as her sole beneficiary. The balance in Rita s IRA as 12/31/2016 was $47,000. Her RMD amount for 2017 is $2, ($47,000 / 17.9). She died on 11/08/2017. The beneficiary is not a person (e.g. estate or church), and the accountholder has died after her required beginning date. The estate is required to withdraw the RMD amount or an amount greater than the RMD, including a lump-sum distribution. For 2017, the RMD amount will have been determined using Rita s age and the Uniform Lifetime Table. For subsequent years, the RMD amount will be based on Rita s single life expectancy. An initial distribution factor will be determined for 2017 (but not used for 2017, by referencing the Single Life Table) and then reduced by one for each subsequent year. The initial factor or divisor is 9.7 since was 81. Divisors for subsequent years would be 8.7, 7.7, 6.7, etc Rita s Age Factor Age FMV 2% Interest RMD 17.9 / $47,000 $2, $47,000 $940 $2, $45,314 $906 $5, $41,011 $820 $5, $36,505 $730 $4,448 continues 72 Continue to reduce by

73 Considerations When The Decedent s Estate Is the Inheriting Beneficiary The decedent s estate generally must be assigned a TIN so the IRA custodian/trustee is able to comply with Form 1099-R requirements. Distributions are made to the estate and reported to the IRS using the estate s TIN. The estate is not required to take a lump sum distribution or immediately close the IRA. If the IRA accountholder died before his or her RBD, then the estate beneficiary must use the 5-year rule. The life-distribution rule does not apply. If the IRA accountholder died on or after his or her RBD, the life distribution rule does apply. However, the initial factor is determined using the age of the decedent in the year he or she died and then reduce this factor by one for each subsequent year. 73

74 General Planning Concept Don t have an estate be the IRA beneficiary. Normally the RMD will be much larger when the estate is the inheriting beneficiary. 74

75 Considerations When The Decedent s Estate Is the Inheriting Beneficiary Inherited IRA Sample Pass-Through Language for Legal Opinion Mary Doe has maintained an IRA with ABC institution since She was born on 2/16/1933. She died in July of 2009, at age 76. She had designated her husband as her primary beneficiary. He had died in She had not designated any contingent beneficiary(ies). Her IRA plan agreement indicated her estate was the default beneficiary. Mary s 3 children were each to receive a 1/3 share of her estate. The three children are Nancy, John and Mark. Nancy is the personal representative of the estate. ABC Institution will set up the inherited IRA and title it, The Mary Doe Estate as beneficiary of Mary Doe s IRA. The tax rules do not require the estate to take a lump sum distribution. The life distribution rule applies, but the RMD distribution period will be based on Mary since her estate was her beneficiary. The factor from the Single Life Table is 12.7 since May was age 76 in Nancy will want to check with the attorney assisting her with the estate. It may well be possible under applicable state law for the estate to pass-through to each beneficiary the right to receive these future IRA distributions in such a way that the IRA custodian is able to set up an inherited IRA for each beneficiary. 75

76 Considerations When The Decedent s Estate Is the Inheriting Beneficiary Inherited IRA Sample Pass-Through Language for Legal Opinion We at CWF believe the IRA custodian could set up 3 inherited IRA for the three beneficiary s if an attorney would furnish a legal opinion to the effect: Pursuant to Mary Doe s will, federal law and the laws of State of XX, it is permissible for Mary Doe s estate to pass-through to the estate s three beneficiaries the right to receive the future IRA distributions to which Mary Doe s estate is entitled to receive in distributions over the life expectancy of Mary. That is, the IRA custodian is authorized to establish an inherited IRA for each beneficiary of the estate and close out the estate s inherited IRA. The three inherited IRA accounts would be titled, Nancy as beneficiary of Mary Doe s IRA ; and John as beneficiary of Mary Doe s IRA ; and Mark as beneficiary of Mary Doe s IRA. However, since Mary dies after her required beginning date with her estate as her beneficiary, all three beneficiaries will use an RMD distribution period based on Mary s age. Since Mary attained or would have attained age 76 in 2009, then the divisor for 2010 will be 11.7 ( ). The divisor for 2011 will be 10.7, for 2012 will be 9.7, etc. Each beneficiary, of course, could withdraw in a year any amount larger than the RMD amount. 76

77 Considerations When A Qualified Trust Is the Inheriting Beneficiary There is a special rule for certain trusts. There is no special rule for an estate. The special rule is that the beneficiary(ies) of a qualified trust will be treated as the beneficiary(ies) of the IRA for calculating the applicable distribution period in the RMD calculation, if the following requirements are met: The trust is a valid trust under state law, or would be but for the fact that there is no corpus. The trust is irrevocable or will, by its terms, become irrevocable upon the death of the IRA accountholder. Since the accountholder is deceased, the trust must be irrevocable for this exception to apply to the beneficiary. The beneficiaries of the trust who are beneficiaries with respect to the IRA are identifiable from the trust instrument. The required documentation has been provided to the IRA custodian or trustee. The documentation to be provided depends upon whether the required distributions are occurring before the IRA accountholder has died or after the accountholder has died. The trust must have as its beneficiaries only living persons 77

78 Considerations When A Qualified Trust Is the Inheriting Beneficiary There are also two ways to meet the documentation requirements when an RMD must be paid to a trust beneficiary after the accountholder has died. This requirement must be met by October 31 of the year after the year the accountholder has died. 1. The trustee of the trust provides the IRA custodian/trustee with a copy of the trust instrument for the trust that is the designated IRA beneficiary as of the IRA accountholder s date of birth. 2. The trustee of the trust provides the IRA custodian/trustee with the following: a. A final list of all the beneficiaries of the trust as of September 30 of the year following the year of the accountholder s death. This list must include all contingent and remainder main beneficiaries with a description of the conditions of their entitlement. b. A certification that the list is correct and complete and that the first three trust requirements discussed above have been met: c. An acknowledgment that he or she will provide a copy of the trust instrument when requested by the IRA custodian/trustee 78

79 Considerations When A Qualified Trust Is the Inheriting Beneficiary If the IRA accountholder died before his or her RBD, then the life-distribution rule will be used unless: The trust would elect to use the five-year rule. The oldest beneficiary of the trust will normally be the measuring life. The separate account rules do not apply to the beneficiaries of a trust with respect to the trust s interest in the accountholder s benefit. For each calendar year after the IRA accountholder s death, the applicable distribution period is initially determined from the Single Life Table by using the oldest beneficiary s age in the year after the accountholder s death and then for subsequent years, adjusting such factor by reducing by one for each calendar year that elapses after the accountholder dies. This distribution period will continue and will not be modified by the death of the beneficiary who is the measuring life. Note: The trust is not restricted to a lump sum distribution. 79

80 Considerations When A Qualified Trust Is the Inheriting Beneficiary If the IRA accountholder died on-or-after his or her RMD, then the life distribution rule will be used unless: The oldest beneficiary of the trust will normally be the measuring life. The separate account rules do not apply to the beneficiaries of a trust with respect to the trust s interest in the accountholder s benefit. For each calendar year after the IRA accountholder s death, the applicable distribution period is initially determined from the Single Life Table by using the oldest beneficiary s age in the year after the accountholder s death and then for subsequent years, adjusting such factor by reducing by one for each calendar year that elapses after the accountholder dies. This distribution period will continue and will not be modified by the death of the beneficiary who is the measuring life. Note: The trust is not restricted to a lump sum distribution. 80

81 Consequence if the trust is not a qualified trust If death occurs before RBD, then 5 Year rule is mandatory. If death occurs on or after RMD, then special life distribution rule is used Trust is non-qualified If there is a joint revocable trust and the first spouse dies. If the trust has any non-living beneficiaries such as a church or university designated as a beneficiary. 81

82 Establishing the Inherited IRA for a Beneficiary Data Processing / IRS Reporting Duties Form 5498 RMD Notices Form 1099-R FMV Statements 82

83 Special Administrative Topics What Special Reporting Duties Apply? Final Form 5498 and FMV Statement must be prepared for the deceased IRA Accountholder on a per plan agreement basis Form 5498 and FMV Statement may need to be prepared for each inheriting beneficiary on a per plan agreement basis A final FMV Statement and Form 5498 must be prepared using the IRA accountholder s name and social security number. The IRS has given the IRA custodian/trustee two options. It may either report the fair market value as of the date of death, or it may report a 0 and instruct the executor that he or she may request the value as of the date of death. A final FMV statement and Form 5498 must be prepared for each inheriting beneficiary showing the fair market value of his or her share as of December 31. If the value is 0 because the beneficiary withdrew his or her entire share, then a Form 5498 does not need to be prepared. Report using a beneficiary s name and social security number. 83

84 Special Administrative Topics Special Form 1099-R Reporting for inherited traditional IRAs Form 1099-R Reporting Rule 1 Transfer of funds from decedent s IRA to the inherited IRA of a non-spouse beneficiary is a non-reportable transfer. Form 1099-R Reporting Rule 2 Every distribution made from an inheriting traditional IRA to an inheriting beneficiary must be reported on a Form 1099-R and coded 4 for death. 84

85 Special Administrative Topics IRA Software for Inherited IRAs Approach # 1 IRA Software generally handles the subject of an inherited IRA in one of two ways. Under the first approach, the system is instructed that the IRA accountholder has died. Various subaccounts are automatically set up for the inheriting beneficiary or beneficiaries and the proper amount of money is transferred into each such subaccount. The system will generate the proper information returns for the decedent and the beneficiary(ies). 85

86 Special Administrative Topics IRA Software for Inherited IRAs Approach # 2 Under the second approach, the software is not written as comprehensively. In order to generate governmental reports to each beneficiary, a separate account is et up for each beneficiary on the computer system independent of the account for the original IRA accountholder. The funds are then transferred from the deceased IRA accountholder s account to the inherited IRA of the beneficiary. Such transfers are non-reportable for Form 1099-R and Form 5498 reporting purposes. The account title. John Doe as beneficiary of Jane Doe s IRA should be used. Because so many computer systems use the second approach. CWF has written its contribution and distribution forms to show that funds may be transferred from a decedent s IRA and transferred into the beneficiary s inherited IRA. 86

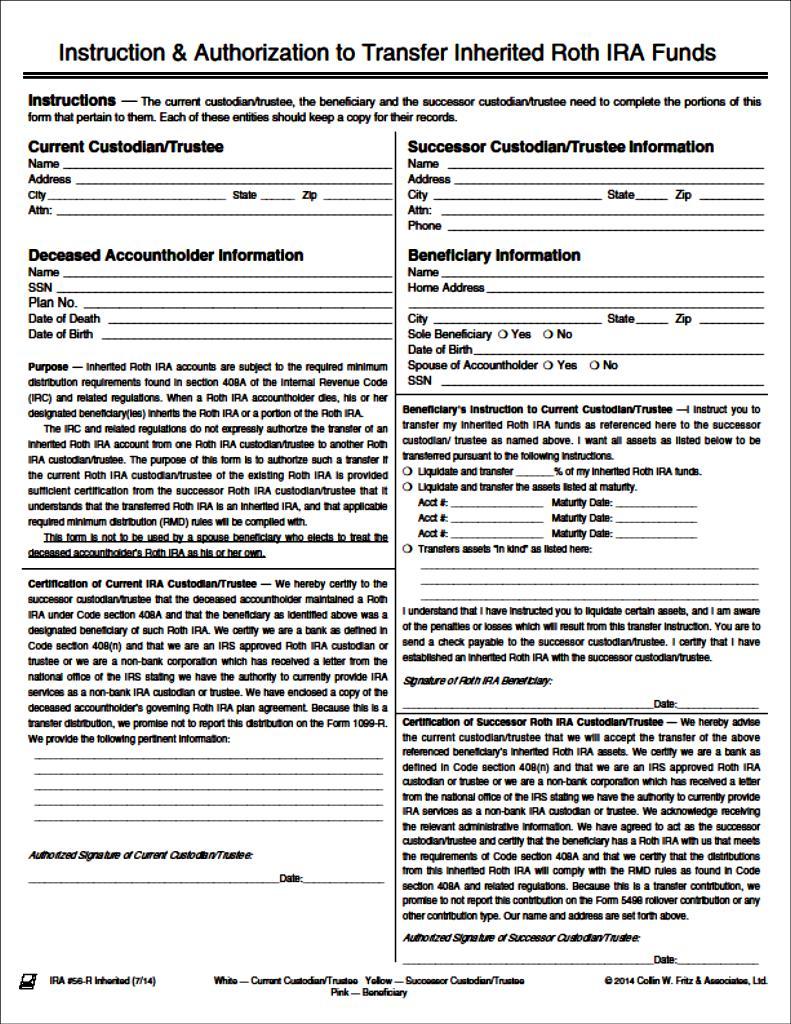

87 Special Administrative Topics For Distribution to a traditional IRA Beneficiary Use Code 4 According to the number of consulting calls we receive on the subject, there seems to be confusion as to when to use code 4 (Death Distribution) in box 7 or the Form 1099-R. For any distribution to an inheriting traditional IRA beneficiary, Code 4 is to be used. It does not matter how many years have passed since the accountholder s death: Code 4 is to be used. Note: Code 4 is not used to inform the IRS that an IRA accountholder has died. 87

88 Inherited IRAs for Non-Spouse Beneficiaries Special Administrative Topics Document the Distribution CWF57 88

89 Special Administrative Topics RMD Notice For Non-Spouse Beneficiaries for 2018 Five-Year Rule CWF

90 Special Administrative Topics RMD Notice For Non-Spouse Beneficiaries for 2018 Life Distribution Rule CWF

91 Special Administrative Topics Missed RMDs 50% Tax is owed unless the IRS would waive Form 5329 completed and filed by the beneficiary Special rule - In some cases, the beneficiary may elect to use the 5-year rule rather than the life distribution rule. Example, IRA owner dies in Beneficiary failed to take RMD distribution for 2016 and 2017 This beneficiary may elect to use 5-year rule rather than the life distribution rule. If so, the 50% tax is not owed for 2016 and Once the beneficiary switches from the life distribution rule to the 5-year, he or she may not switch again. 91

92 Inherited IRAs for Non-Spouse Beneficiaries Special Administrative Topics Alternative Method Applies to Like-Kind Inherited IRAs Multiple Like-Kind Inherited IRAs Be sure to Document CWF # 312 To be Like-Kind the inherited IRA must arise from the same decedent and be the same type of IRA 92

93 Inherited IRAs for Non-Spouse Beneficiaries Inherited IRAs which arise from the same original IRA accountholder are considered to be like-kind IRAs and may be aggregated for purposes of satisfying the RMD requirement. However, you may not aggregate an Inherited IRA from one person with your own personal IRAs, or with an IRA inherited from a different person. 93

94 Special Administrative Topics RMD Alternative Method Multiple Like-Kind Inherited Traditional IRAs Inherited IRAs from the Same Person IRA # 1 IRA # 2 IRA # 3 IRA # 4 RMD $1,000 $1,200 $1,300 $1,400 Could take $4,900 from any one inherited IRA or any combination of IRAs 94

95 Special Administrative Topics: No Rolling Over an Inherited IRA Ever Traditional or Roth IRA by a Non-spouse Beneficiary 95

96 Special Administrative Topics Transferring an Inherited IRA - Special Procedures If you are the receiving institution, the successor custodian/trustee, you will probably want to get a copy of the IRA plan agreement and beneficiary designation of the deceased accountholder. In addition we recommend that you have the beneficiary sign an IRA plan agreement. CWF now has an inherited IRA Plan Agreement for this purpose. Per the IRS, the account must be titled in this manner: ABC Financial Institution as custodian/trustee for John Jones as beneficiary of James Smith s IRA. The transferring custodian/trustee should be certain that the inherited funds will be properly administered by the successor custodian/trustee and that all required minimum distribution rules will be complied with. The CWF Form #56-Inherited was designed for this purpose. This form, or some other appropriate form, should obtain the beneficiary s signature as well as the signature of the representative for the successor custodian/trustee stating that the proper regulations will be followed. 96

97 Special Administrative Topics Transferring an Inherited IRA - Special Procedures CWF56I CWF56RI 97

98 Special Administration Topic Qualified Charitable Distribution Finally Settled 12/18/2015 Now Permanent IRA Beneficiary must be 70½ or older Distribution must be from Inherited Traditional IRA or Roth IRA Cannot be from an active Inherited SEP or an Inherited SIMPLE IRA Counts toward RMD Even Past due RMDs Distributions must be to eligible charity Distributions must be made directly to the charitable organization Individual can deliver/mail personally Special tax calculation rules Inherited Traditional IRA not Prorated Inherited Roth IRA Not in distribution Order 98

99 RMD Distribution Qualified Charitable Distribution Recommended administration IRA Beneficiary responsibility Document distribution No Special custodian/trustee reporting IRA Beneficiary is allowed to deliver check Maximum of $100,000 per year/per person IRA Custodian/Trustee reports as usual IRA Beneficiary reports on Form 1040 Line 15a and 15b QCD in margin 99

100 Inherited IRAs for Non-Spouse Beneficiaries CWF Form # 57-C Certification for Tax-Free Distribution from Traditional/Roth IRA CWF57C 100

101 X Traditional IRA Beneficiary over 70½ 4 X Qualified Charitable Distribution Recommended Administration: IRA Beneficiary responsibility Document distribution No Special custodian/trustee reporting IRA Beneficiary is allowed to deliver check/draft IRA Custodian/Trustee reports as usual 101

102 10,000 0 QCD 102

103 Special Administrative Topics Moving Inherited IRA Funds to an HSA Pursuant to Notice (June 2008), a inherited traditional IRA or Roth IRA beneficiary has the right to make a tax-free transfer of his or her inherited IRA interest to his or her own HSA. It is certainly not clear that the Congress intended to allow a beneficiary to make a tax-free transfer from a decedent s IRA to his or her own HSA, but the IRS has authorized such a transfer in this Notice. And it gets better. When a beneficiary transfers funds from his or her inherited IRA to an HSA, such a transfer will count to satisfy his or her IRA required distribution from the inherited IRA. 103

104 Transfers from IRAs and Inherited IRAs Inherited IRA HSA Example Jane has a inherited traditional IRA with a balance of $30,000. She is HSA eligible for She is age 58. She has a family HDHP. No contributions have yet been made to her HSA for She instructs she wished to do a QFD of $7,900. Inherited IRA HSA $30,000 $7,900 Used to pay qualified medical expense = tax-free 104

105 Transfers from IRAs and Inherited IRAs Inherited IRA HSA Qualified HSA Funding Distribution Must be an Eligible HSA Contribution Must be a trustee-to-trustee transfer (direct rollovers) One per Lifetime Testing Period Inherited IRA HSA Reported as HSA Contribution on 5498-SA Reported as an IRA Distribution on 1099-R. Individual explains on tax return that it is not taxable Cannot be made from an ongoing SEP-IRA or SIMPLE IRA. 105

106 Transfers from IRAs and Inherited IRAs Inherited IRA HSA Must be an Eligible HSA Contribution Must be a trustee-to-trustee transfer (direct rollover) Reported as HSA Contribution on 5498-SA Reported as a Distribution on 1099-R. Special tax explanations. One per Lifetime Exception Changing from Single HDHP to Family HDHP Must be accomplished in same calendar year, for same tax year by Dec 31 Cannot be done between January 1 and April 15 for prior tax year 106

107 CWF HSA # 66 Certification for One Per Lifetime Transfer of IRA Funds To an HSA CWF66 107

108 108

109 New Type of Inherited IRAs Direct Rollover from a 401(k) Plan The law was changed as of January 1, 2007, to allow a non-spouse beneficiary of a pension plan participant to directly roll over the inherited funds into a new type of inherited IRA. The individual/beneficiary is the required to take required distributions from the inherited IRA. This form is used by the individual/beneficiary to instruct how and when distributions will be taken and what method will be used. Normally an individual/beneficiary would directly roll over standard pension funds into an inherited traditional IRA. Inherited IRA Accountholder s Distribution Instruction and Certification to Comply with RMD rules, CWF IRA # 205 Dad s 401(k) Daughters Inherited IRA Daughter s 401(k) Mom s Inherited IRA 109

110 Direct Rollovers of Inherited Funds Inherited QRP Direct Rollover Non-Spouse Beneficiary Inherited Traditional IRA Inherited QRP (Direct) Rollover/Conversion Non-Spouse Beneficiary Inherited Roth IRA Inherited Roth QRP Direct Rollover Inherited Roth IRA 110

111 CWF # 205 Inherited IRA Accountholders Distribution Instructions And Certification to Comply With RMD Rules CWF

112 Special Administrative Beneficiary Disclaimers A Beneficiary Can Decline a Gift Get a copy of the written disclaimer for the file. Get a signed indemnification agreement. This is the most conservative route, but this hold harmless agreement states that the disclaimer takes responsibility for any unforeseen tax consequences. Determine the proper beneficiary(ies). Under the laws of most states, a disclaimed beneficiary is treated as if he or she predeceased the accountholder. It would be best if the IRA Custodian s attorney would make the determination of who are the primary beneficiaries after the disclaimer 112

113 Special Administrative Traditional and Roth IRA Beneficiary Qualified Disclaimer Internal Revenue Code section 2518 Must be irrevocable and unqualified Must be in writing Must be done within the later of 9 months after the date of death, or age 21 (Can be a problem for IRAs) Remember, until the qualified disclaimer is executed, the beneficiary of record is subject to all the usual requirements for RMDs. This includes the custodian/trustee reporting. Cannot direct who is to get his/her share Can disclaim just part of the IRA Recommend using an attorney to cover any applicable state statutes 113

114 Special Administrative What to Do Once the First Inherited IRA Beneficiary Dies The first inheriting beneficiary, presumably, will have designated his or her own beneficiary(ies). The successor beneficiary will have inherited the inherited IRA. The RMD formula which applied to the first inheriting IRA beneficiary will apply to any successor beneficiary. Again, unless there has been some restriction imposed, the successor inheriting beneficiary is able to withdraw more than the required minimum. A successor inheriting beneficiary will wish to designate his or her own beneficiary(ies) and instruct how and when distributions will be taken. CWF has created a special form for a successor inheriting beneficiary to instruct how and when distributions will be taken. It is Form 204-A, Successor Beneficiary s Distribution Notice and Certification Form and Payment Instruction, as set forth at the end of this presentation. Titleing of Form 5498 after the death of the first beneficiary. 114

115 Determining the Period/LE Factor for the Second Inherited Beneficiary Example: The IRA Accountholder (John Doe) dies on at the age of 65, before his RBD. Jane Doe is the only primary beneficiary. She is age 40 in 2015 and will be age 41 in Jane dies in Her beneficiary is her daughter, Mary. The initial factor comes from the single life table and then subsequent factors are determined by subtracting 1.0 for each following year. Beneficiary Factor Year of Death N/A Jane Dies Schedule Continues 115

116 CWF # 204A Successor Beneficiary s Distribution Notice And Certification Form And Payment Instruction CWF204A 116

117 Quiz / Inheriting / Beneficiary IRA Consulting Call of February 3, 2018 Inheriting/Beneficiary IRA Consulting Call of February 3, Alice s mother, Corrine Davis, had her traditional IRA with IRA Custodian #1 for over 25 years. Corrine had died on July 23, 2017 at the age of 83 with a balance of $100,000. Her RMD for 2017 had been calculated to be $6,200. She had not been paid any amount prior to her death. Alice and her three siblings were the primary beneficiaries of Corrine s IRA. Alice and her sister, Mattie were paid $25,000 in September of The other two beneficiaries were Alice s brothers, James and Mark. They were paid no amount in

118 Quiz / Inheriting / Beneficiary IRA Consulting Call of February 3, 2018 Alice Davis, age 47, has just called IRA Custodian # 1 and talks with Dana. Dana handles many tasks in addition to IRA tasks. Alice has called and asked, Wasn t I supposed to be sent a 2017 Form 1099-R showing a distribution of $25,000, the amount I received with respect to my mother s IRA? 118

119 Quiz / Inheriting / Beneficiary IRA Consulting Call of February 3, 2016 Dana informs Alice that she needs to do some research and that she will be calling her back was soon as possible. She discovers that a 2017 Form 1099-R for $100,000 was prepared using the mother s name (Corrine) for, but that no R forms were prepared for Alice and her siblings. Dana asks, What should have been done and what should I do now? How quickly does it need to be done? Goal of Webinar: To discuss this beneficiary situation and others so that attendees will understand how (and why) the IRA Custodian will want to use certain forms and procedures to service an inherited or beneficiary IRA. 119

120 What was Done Incorrectly? 1. No 2017 Form 1099-R for the mother, Corrine 2. Need 2017 Form 1099-R for Alice and Mattie 3. Possibly need to correct the missing RMDs for James and Mark 4. Need to do the proper Reporting and FMV Reporting 120

121 Conclusion. An IRA custodian/trustee needs to perform special administrative duties with respect to the inherited IRAs of non-spouse beneficiaries. This webinar should allow you to perform these duties better and more confidently. Your IRA personnel must determine the situation applying to a particular beneficiary. Then use the proper administrative forms. Any final questions. CWF s consulting number is (800) Thank you for your attendance and participation in this webinar 121

122 Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may be reproduced in any form and by any means without prior written permission from Collin W. Fritz & Associates, Ltd.

A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA

Rev 7/11/2018 A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting

Rev 7/11/2018 A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting

IRAs & Roth IRAs. Beneficiary or Inherited IRAs. Questions & Answers

IRAs & Roth IRAs Beneficiary or Inherited IRAs Questions & Answers Purpose The purpose of this brochure is to provide a person who is a beneficiary of a traditional IRA (including SEPs and SIMPLEs) or

IRAs & Roth IRAs Beneficiary or Inherited IRAs Questions & Answers Purpose The purpose of this brochure is to provide a person who is a beneficiary of a traditional IRA (including SEPs and SIMPLEs) or

Traditional IRAs. Understanding Required Distributions at 70 1 / 2. Questions & Answers

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

Traditional SEP, and SIMPLE IRAs

Traditional SEP, and SIMPLE IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why must I and others age 70 1/2 or older have to take a required distribution? The purpose of an IRA

Traditional SEP, and SIMPLE IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why must I and others age 70 1/2 or older have to take a required distribution? The purpose of an IRA

1. New IRA Contribution Limits for IRA Transfers 3. IRA Rollovers (k) Direct Rollovers 5. Fraudulent contributions

Direct Rollovers 5. Fraudulent contributions") 1. New IRA Contribution Limits for 2013 2. IRA Transfers 3. IRA Rollovers 4. 401(k) Direct Rollovers 5. Fraudulent contributions Rev 12-5-2012 Just a Reminder: This is copyrighted material. No Video or

1. New IRA Contribution Limits for 2013 2. IRA Transfers 3. IRA Rollovers 4. 401(k) Direct Rollovers 5. Fraudulent contributions Rev 12-5-2012 Just a Reminder: This is copyrighted material. No Video or

Are IRA Amendments Required For ?

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

The Webinar will be starting shortly

Rev. 5/2/2018 The Webinar will be starting shortly 8:30 am CST or 12:30 pm CST We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar Copyright 2018 Collin W. Fritz &

Rev. 5/2/2018 The Webinar will be starting shortly 8:30 am CST or 12:30 pm CST We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar Copyright 2018 Collin W. Fritz &

IRA Contribution Limits for 2018 Unchanged at $5,500 and $6,500; 401(k) Limits Do Change

Limits Do Change") Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

Session # 1 Establishing and Contributing

11/15/2018 Session # 1 Establishing and Contributing We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly 8:30 am CST or 12:30

11/15/2018 Session # 1 Establishing and Contributing We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly 8:30 am CST or 12:30

No Form 1099-R Prepared to Report IRA Funds Moving From the Decedent s IRA to an Inherited IRA

Published Since 1984 2015 Tax Filing Deadline is April 18, 2016 ALSO IN THIS ISSUE 2015 Form 5500 Series Returns Should Not Answer the Compliance Questions, Page 2 Inherited IRA Situation - Daughter Dies,

Published Since 1984 2015 Tax Filing Deadline is April 18, 2016 ALSO IN THIS ISSUE 2015 Form 5500 Series Returns Should Not Answer the Compliance Questions, Page 2 Inherited IRA Situation - Daughter Dies,

Three Planning Concepts Why More Individuals Will Want Profit Sharing or One Person 401(k) Plans!

Plans!") Published Since 1984 ALSO IN THIS ISSUE Preparing Two 1099-R Forms is Never Correct When There is Federal Withholding, Page 2 Possible Expansion of the Saver Tax Credit, Page 3 H&H Block Lawsuit Settlement

Published Since 1984 ALSO IN THIS ISSUE Preparing Two 1099-R Forms is Never Correct When There is Federal Withholding, Page 2 Possible Expansion of the Saver Tax Credit, Page 3 H&H Block Lawsuit Settlement

The Webinar will be starting shortly

7/11/2018 The Webinar will be starting shortly 8:45 am CST or 1:00 pm CST Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may

7/11/2018 The Webinar will be starting shortly 8:45 am CST or 1:00 pm CST Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may

RMD Impact When a Surviving Spouse Elects to Treat the Deceased Spouse s IRA as Their Own

Published Since 1984 ALSO IN THIS ISSUE HSA Contribution Limits for Domestic Partners and Other Unmarried Individuals Versus Married Individuals, Page 3 Handling Excess IRA Contributions for 2008 and 2009,

Published Since 1984 ALSO IN THIS ISSUE HSA Contribution Limits for Domestic Partners and Other Unmarried Individuals Versus Married Individuals, Page 3 Handling Excess IRA Contributions for 2008 and 2009,

President Barack Obama Makes SEP/Profit Sharing Plan Contributions for

Published Since 1984 ALSO IN THIS ISSUE President Barack Obama Makes SEP/Profit Sharing Plan Contributions for 2007-2011 Seeking More IRA Contributions From Higher Income Clients and Understanding a Special

Published Since 1984 ALSO IN THIS ISSUE President Barack Obama Makes SEP/Profit Sharing Plan Contributions for 2007-2011 Seeking More IRA Contributions From Higher Income Clients and Understanding a Special

IRA Contribution Limits for 2019 $6,000 and $7,000

Published Since 1984 ALSO IN THIS ISSUE IRA Contributions for 2019 Page 1 IRA Contribution Deductibility Charts for 2018 and 2019 Page 2 Roth IRA Contribution Charts for 2018 and 2019 Page 3 SEP and Simple

Published Since 1984 ALSO IN THIS ISSUE IRA Contributions for 2019 Page 1 IRA Contribution Deductibility Charts for 2018 and 2019 Page 2 Roth IRA Contribution Charts for 2018 and 2019 Page 3 SEP and Simple

Gettechnical Inc. Gettechnical Inc.

Gettechnical Inc. The material used in this text has been drawn from sources believed to be reliable. Every effort has been made to assure the accuracy of the material; however, the accuracy of this information

Gettechnical Inc. The material used in this text has been drawn from sources believed to be reliable. Every effort has been made to assure the accuracy of the material; however, the accuracy of this information

Required Minimum Distributions

Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts What Are Required Minimum Distributions? Required minimum distributions (RMDs)

Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts What Are Required Minimum Distributions? Required minimum distributions (RMDs)

IRS REVISES RULES FOR SUBSTANTIALLY EQUAL PERIODIC PAYMENTS ALSO IN THIS ISSUE. October 2002 Published Since 1984

Published Since 1984 ALSO IN THIS ISSUE IRS Issues Questions & Answers Substantially Equal Periodic Payments Page 2 Analyzing IRA Beneficiary Situations and Options by Examining Various Examples, Page

Published Since 1984 ALSO IN THIS ISSUE IRS Issues Questions & Answers Substantially Equal Periodic Payments Page 2 Analyzing IRA Beneficiary Situations and Options by Examining Various Examples, Page

RECAP FOR COMPLETING THE 2002 FORM 1099-R ALSO IN THIS ISSUE DEADLINE FOR RMD NOTICE REMAINS JANUARY 31, Take note of this...

Published Since 1984 ALSO IN THIS ISSUE RECAP FOR COMPLETING THE 2002 FORM 1099-R QP Communication From the IRS, Page 3 Additional Thoughts on RMD Rules, Page 6 Higher Income Limits for 2003, Page 7 IRS

Published Since 1984 ALSO IN THIS ISSUE RECAP FOR COMPLETING THE 2002 FORM 1099-R QP Communication From the IRS, Page 3 Additional Thoughts on RMD Rules, Page 6 Higher Income Limits for 2003, Page 7 IRS

Arkansas Bankers Trust School IRA Update May 16, 2018

Arkansas Bankers Trust School IRA Update May 16, 2018 Presented by: 1 Patrice Konarik Sunwest Training Corp. Kendalia, TX www.sunwesttraining.com patrice@sunwesttraining.com 830.336.3422 2 Trust School

Arkansas Bankers Trust School IRA Update May 16, 2018 Presented by: 1 Patrice Konarik Sunwest Training Corp. Kendalia, TX www.sunwesttraining.com patrice@sunwesttraining.com 830.336.3422 2 Trust School

What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts

Retirement Planning Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts WHAT ARE REQUIRED MINIMUM DISTRIBUTIONS? Required minimum distributions

Retirement Planning Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts WHAT ARE REQUIRED MINIMUM DISTRIBUTIONS? Required minimum distributions

President Obama Signs the Budget/Tax Bill on December 18, 2015.

Published Since 1984 ALSO IN THIS ISSUE IRA Custodian s Duty to File Corrected Form 1099-Rs Will Change, Page 2 IRA Amendments Being Required For 2015-2016, Page 3 February 1, 2016 Deadline, Page 4 Basic

Published Since 1984 ALSO IN THIS ISSUE IRA Custodian s Duty to File Corrected Form 1099-Rs Will Change, Page 2 IRA Amendments Being Required For 2015-2016, Page 3 February 1, 2016 Deadline, Page 4 Basic

Roth IRAs The Roth IRA

Roth IRAs The Roth IRA 2017 and 2018 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

Roth IRAs The Roth IRA 2017 and 2018 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

ALSO IN THIS ISSUE. The 2004 IRS Form Inherited IRAs and Checkbox 11 (Required Minimum Distribution) on Form 5498

on Form 5498") April 2005 Published Since 1984 ALSO IN THIS ISSUE Completing the 2004 Form 5498-SA, Page 3 Question and Answer, Page 3 Additional Discussion of Automatic Rollover Rules, Page 4 A Planning Technique, Page