Session # 1 Establishing and Contributing

|

|

|

- Everett Hunter

- 5 years ago

- Views:

Transcription

1 11/15/2018 Session # 1 Establishing and Contributing We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly 8:30 am CST or 12:30 pm CST Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may be reproduced in any form and by any means without prior written permission from Collin W. Fritz & Associates, Ltd.

2 2

3 The Audio Portion of this presentation is available either by phone or by using the speakers and microphone on your PC. The phone number is provided to you in the confirmation from CWF and again at the time you join the meeting. You will need the access code that was ed to you in the confirmation from CWF. The confirmation code is 9 digits in length e.g You will also need the Audio Pin # which is shown to you at the time you join this meeting If you need assistance re-connecting please call CWF at

4 Types of IRAs Traditional IRAs An individual IRA SEP IRAs An employer plan IRA, including a one person business SIMPLE IRAs An employer plan IRA, including a one person business. Roth IRAs An individual IRA 4

5 The Roth IRA Life Span Years or more Distributions Income earned will be taxfree or taxable Accountholder Before Age 59½ Contributions Non-Deductible Custodial or Trust Account Earnings within Account are not Taxed Age 59½ to 70½ and older Beneficiaries Original Subsequent Conversions Rollovers Transfers Recharacterizations Other Specials Postponed Recontributions Separate Tax Entity In general, the accountholder or beneficiary will not include the distribution in income and pay tax. 5

6 Purposes of Types of IRAs Established by Congress to encourage people to save for retirement Supplement to Social Security and any Private or Governmental pension plan Main differences of Roth IRA versus Traditional IRA No 70½ rule for contributions contributions may be made at age 71, 72, 73, etc. No RMDs for Roth IRAs (except Inherited accounts). Tax free income versus taxable income 6

7 Overview of Roth IRAs IRA is a one person Pension plan Why do they exist? Save for retirement Transfer wealth to beneficiary(ies) First Year for Roth IRA Contributions Roth IRA (Senator Roth Del.) 7

8 Business Goals of the Roth IRA Custodian A deposit source and investment source Long Term New customer/client relationship Strengthening existing relationships Fees: Early withdrawal interest fees Annual administration Termination Transfer Investment fees and commissions 8

9 Personal Goals for Roth IRAs Save/Transfer Wealth: Retirement permissive, not mandatory Wealth accumulation and transfer to beneficiary(ies). Tax Reasons: Earn tax-free income 9

10 Establishing Roth IRAs Must be established with Financial Institution. Authorized to Act as a Custodian or Trustee. Banks Savings & Loans Credit Unions Certain Trust Companies & Brokerage Firms IRA Annuities are issued by an insurance company. 10

11 Purpose of Roth IRAs Purpose(s): An accountholder uses this special savings account (i.e. a tax preferred revocable trust) to accumulate funds which may be used for his or her retirement but they are not required to be so used and also to provide for beneficiaries after his or her death. Since the RMD rules do not apply to a Roth accountholder, the Roth IRA may be used to accumulate funds for potential tax-free distribution to beneficiaries. 11

12 Definition of Roth IRAs Special trust or custodial account For the exclusive benefit of the individual and the individual s beneficiary(ies). Special rules are explained in a written document called the Plan Agreement. Rules govern opening, contribution to, and withdrawing money from a Roth IRA. The rules must be contained in the plan agreement and followed in order to have a valid Roth IRA. Rules found in the Internal Revenue Code (IRC) and related U.S. Treasury Regulations (REG) Financial institutions that maintain Roth IRAs are either the trustee or custodian of the account. 12

13 Tax Benefits of a Roth IRA Compounding Growth is faster since no current taxation of earnings and possible earnings will not be taxed. No tax deduction for the contribution. Tax credit (in some cases). Tax Free Qualified distributions (if certain rules met). Example: Commencing in 2015, Jane Doe contributes $5,000 per year for 10 years. These contributions are made when she is age She never takes a distribution. She dies at age 80. The Roth IRA had a balance of $130,000. The $80,000 of earnings when distributed from her Roth IRA (i.e. an inherited Roth IRA) are never taxed nor will any of the earnings realized by her beneficiary(ies) after her death be taxed. Her beneficiary must take required distributions over his or her life expectancy. Commencing with the year after the Roth IRA owner dies. Special rules for a Spouse Beneficiary. 13

14 Roth IRA Plan Agreement 14

15 Tax Benefits of a Roth IRA Maximizing Contributions To a Roth IRA A person wants to maximize the amount he or she contributes to a Roth IRA. The tax rules permit eight different types of contributions to a Roth IRA. In some years the person might be eligible to make just one of the types of Roth IRA Contributions. In other years he or she might be eligible to make all eight types or might be ineligible to make any Roth IRA contribution. The Eight types of Roth IRA contributions are: 1. An annual contribution; 2. A conversion contribution from a traditional IRA; 3. A conversion contribution from a SEP-IRA; 4. A conversion contributions from a SIMPLE-IRA; 5. A direct rollover (i.e. a conversion) of non-roth funds; 6. A direct rollover or rollover of Designated Roth funds; 7. A direct rollover or rollover of a deceased spouse s Designated Roth funds; and 8. A direct rollover (i.e. a conversion) of non-roth funds from a deceased spouse s 401(k) plan; 15

16 Establishing Roth IRAs Certain documentation must be completed and provided to the accountholder when an IRA is established, in order to comply with IRS requirements. Written Plan Agreement Custodial - IRS Form 5305-RA Trust - IRS Form 5305-R Custodial Self-Directed - IRS Form 5305-RA Annuity - IRS From 5305-RB Written Disclosure Statement Plain English Explanation Revocation Rules Financial Projections, when Applicable Financial Disclosure 16

17 Roth IRAs CWF Form # 40-R Roth IRA Custodial Account Application Make sure the agreement is valid and up-to-date. Contract between accountholder and the financial institution. A plan agreement establishes a new Roth IRA which is reported separately from other IRAs. Invalid Roth IRA Expected Tax Benefits Unrealized 17

18 Completing the Plan Agreement Depositor Information All verified to your financial institution s satisfaction. May request/demand more information to complete your customer profile. 18

19 Completing the Plan Agreement Roth IRA Revocation Disclosure 7-Day Revocation Right No fees, penalties, or change in value are allowed to be assessed. The Roth IRA/Custodian must give specific revocation instructions and must follow the disclosed procedure. CWF s application page calls for an express revocation disclosure. 19

20 Traditional and Roth IRAs Designation of Beneficiaries Accountholders have the right to name a beneficiary. The beneficiary(ies) of the Roth IRA will be the owners of the Roth IRA proceeds upon death of the accountholder. Accountholders are not required to name beneficiaries to have a valid Roth IRA. 20

21 Designation of Beneficiaries Primary Beneficiaries Contingent Beneficiaries Primary Beneficiaries vs. Contingent Beneficiaries: Name, Address, Social Security Number or TIN, Date of Birth, Relationship to IRA Owner, Share % 21

22 Designation of Beneficiaries Who can be named as a beneficiary? Any living individual Estate (To avoid for Roth IRAs) since the 5-year rule will apply and Roth IRA must be closed. Undesirable. Trust Church Charity Foundation Etc. 22

23 Trust as Beneficiary Allows the accountholder ability to exercise greater control over how the Roth IRA assets will be distributed after his or her death. Useful tool, especially when assets go to minor children. Used in estate planning. If a trust is the named beneficiary of a Roth IRA, the financial institution should obtain a copy of the trust document. A Roth IRA cannot be put into the trust for a living accountholder. General Planning Rule. Designate individuals directly as the IRA beneficiary(ies) rather than designating a trust which has the individuals as the trust beneficiaries. 23

24 Designation of Beneficiaries Right to Name or Change Beneficiaries based on Terms of Roth IRA Plan Agreement. Effect of Differing Will, Trust, Divorce Decree or Legal Separation on Roth IRA Beneficiary Documentation. Generally, the individual designated on the Roth IRA beneficiary form receives the funds. Some states have a statute or case law that gives a different result. Legal advice should be consulted, and document advice in writing. 24

25 No Named Beneficiary If no named beneficiary, generally assets go to the accountholder s estate. Distributed according to state law. Funds will go to the state if no family members found in a specified period of time. Caveat: The Estate must not be the sole primary beneficiary since the Roth IRA must be closed under the 5 year rule. 25

26 Beneficiary Dying Before the Roth IRA Owner Pro Rata Per Stirpes Option of Either Customized Beneficiary Forms 26

pro rata basis X per stirpes")

27 Designation of Beneficiaries CWF Application - Pro Rata vs. Per Stirpes (Select one) pro rata basis X per stirpes 27

28 Designation of Beneficiaries Pro Rata Example Roth IRA Owner Situation 1 Three primary beneficiaries sharing equally: 1. 1/3 share 2. 1/3 share 3. 1/3 share Upon death of the IRA Owner, each beneficiary gets 1/3 of the Roth IRA. 28

29 Designation of Beneficiaries Pro Rata Example Roth IRA Owner Situation 2 Three primary beneficiaries sharing equally 1. 1/3 share 2. 1/3 share Beneficiary # 2 predeceases Roth IRA Owner 3. 1/3 share Upon death of the Roth IRA Owner, each SURVIVING beneficiary gets ½ of the Roth IRA. Note: Nothing goes to the estate or family of the deceased primary beneficiary. 29

30 Designation of Beneficiaries Per Stirpes Example Roth IRA Owner Situation 1 Three primary beneficiaries sharing equally: 1. 1/3 share 2. 1/3 share 3. 1/3 share Upon death of the Roth IRA Owner, each beneficiary gets 1/3 of the Roth IRA. (Same as under Pro Rata). 30

31 Designation of Beneficiaries Per Stirpes Example Roth IRA Owner Situation 2 Three primary beneficiaries sharing equally 1. 1/3 share 2. 1/3 share Beneficiary # 2 predeceases Roth IRA Owner 3. 1/3 share Upon death of the IRA Owner, each SURVIVING beneficiary gets 1/3 of the Roth IRA. Note: The 1/3 share of the Roth IRA belonging to the deceased primary beneficiary goes to the deceased primary beneficiary s heirs and issues as determined by the Roth IRA plan agreement. 31

32 Eligibility & Contribution Type 32

33 Signatures & Revocation Right 33

34 Designation of Beneficiaries Spousal Consent of the Other Spouse s Beneficiary Designation State with community or marital property laws 34

35 Designation of Beneficiaries Spousal Consent of the Other Spouse s Beneficiary Designation Federal Law State Law Non-Community property or marital property law states Community or marital property law states Community Property States: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington Marital Property States: Wisconsin and Alaska If the IRA accountholder names someone other than or in addition to his or her spouse as primary beneficiary(ies), and community or marital property laws apply, the spouse must sign the Application consenting to the other beneficiary(ies) or the designation of the other beneficiaries will be invalid. 35

36 The Disclosure Statement 1. Revocation Right 2. Plain English Explanation Tax Rules Contractual Provisions Non-Tax topics 3. Financial Disclosures (and Fees) 36

37 Financial Disclosure Type of disclosure depends on the initial Roth IRA investment. Investments where growth can be easily estimated: Ex. CD or Savings accounts Numerical projection of growth is required. Investments where growth cannot be reasonably estimated: Ex. Stocks, Bonds, Real Estate No numerical projection is necessary A disclosure of all fees or charges is always required and must be included in any projection. Disclosure is conservative estimate of the growth in value of the Roth IRA. Must show effect of continued contributions, early withdrawal penalties, and fees will have on the Roth IRA s value. 37

38 Financial Projection Preprinted Interest rate no greater Compounding terms no greater All Fees and penalties must be disclosed and projected Read your financial projection carefully to determine how fees and penalties are treated. Most preprinted financial projections do not include fees and penalties Indicate the correction attachment on the application 38

39 Financial Projection Special Attachment/Custom Financial Projection If any of the above conditions/terms are different than the terms of the preprinted projection, a financial projection is still required, it just must be done differently. Indicate correct attachment on the application 39

40 Completing the Financial Projection Financial Projection Example: A Roth IRA is established for a Roth IRA accountholder age 52 at the end of year, making an annual contribution of $5,000. The investment pays.1%, compounds quarterly, and has a 3-month penalty for early withdrawal. No fees are disclosed. Since a regular, annual contribution is being made, you must choose from the tables labeled Annual Contribution. The Rollover Contribution tables are used if the Roth IRA is established with a rollover of transfer contribution. 40

41 Completing the Financial Projection Financial Projection Example: A Roth IRA is established for a Roth IRA accountholder age 52 at the end of year, making an annual contribution of $5,000. The investment pays.1%, compounds quarterly, and has a 3-month penalty for early withdrawal. No fees are disclosed. The annual Contribution tables calculate $1,000 per year from January 1 of each year. The Rollover (Transfer) Calculation tables calculate $1,000, once only, from January 1. 41

42 Establishing a Roth IRA Customer Identification Program (CIP) Rules Apply Truth-In-Savings Act (TISA) Rules Apply FDIC and NCUA Insurance - $250,000. All Roth IRAs, traditional IRAs, SEP and SIMPLEs are aggregated. IRAs are a separate insured category Security Exchange Commission (SEC) Other Investment Disclosures 42

43 Establishing a Roth IRA Double check to make sure the customer wants a Roth IRA and that a Roth IRA Application was completed.. Provide signed and dated copy of the Roth IRA application. Provide a copy of an up-to-date and current Plan Agreement, including additional contractual term. Provide copy of an up-to-date and complete Disclosure Statement. Provide a copy of CIP and TISA Disclosures 43

44 Types of Roth IRA Contributions Annual or Regular Spousal Conversions Rollovers Transfers Recharacterizations Re-contributions 44

45 Which type of Roth IRA vs. Traditional IRA contribution is best? Depends on the individual person s situation. May change from year to year. Deductions may be greater for contributions to one type of IRA than another. Eligibility plays a factor. For instance, a person may not be eligible for a Roth IRA. A person may be ineligible to claim a deduction for a traditional IRA contribution. Can have both Traditional and Roth IRAs. 45

46 Which type of IRA/ IRA contribution is best? Factors to consider: His or her tax bracket at the time of contribution His or her tax bracket at the time of anticipated distributions Whether or not he or she will need the funds during retirement The investment return one may realize How long the funds will be within the Roth IRA. 46

47 IRA Contributions Deadline When Can Contributions Be Made? Contributions to a Roth IRA for a given year can be made at any time during the year as long as by the due date of the individuals federal income tax return, not including extensions. Deadline many times is modified due to Emancipation Day holiday. For 2016 Deadline was April 18, 2017 For 2017 Deadline was April 17, 2018 For 2018 Deadline is April 15,

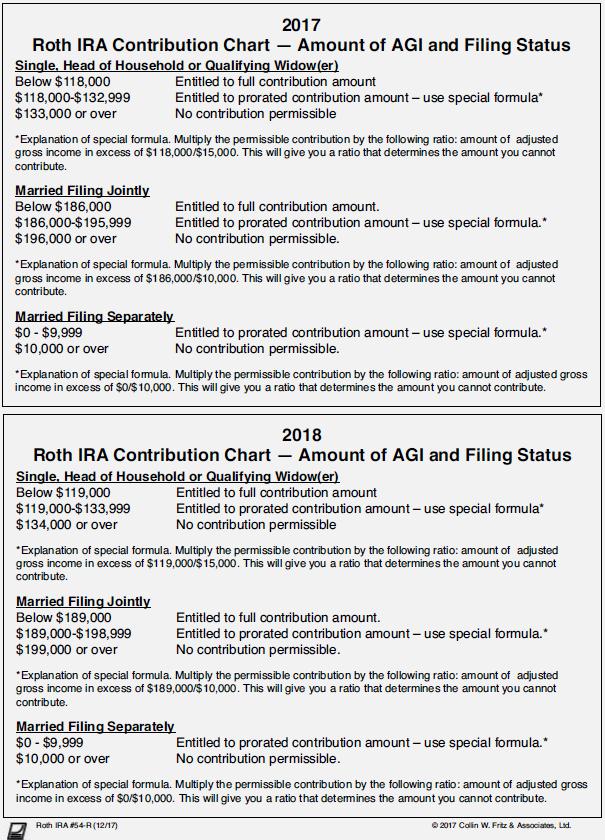

48 IRA Contributions Traditional and Roth IRA Contribution Deadlines: Due date of Federal Tax Return without extensions: Effect of Emancipation Day on Filing Deadlines: For 2011 tax year: April 17, 2012 For 2012 tax year: April 15, 2013 No effect For 2013 tax year: April 15, 2014 No effect For 2014 tax year: April 15, 2015 No effect For 2015 tax year: April 18, 2016 For 2016 tax year: April 18, 2017 For 2017 tax year: April 17, 2018 For 2018 tax year: April 15, 2019 No effect 48

49 Contribution Deadline Due date of Individual s Federal Income Tax Return without regard to extensions March 1 early filing date for Commercial Farmers and Fisherman. Discuss estimated tax payment rules. Mailed contributions postmark date control Making early contributions is not allowed. Example: In December of 2016, a person could not make a contribution for In December of 2017, a person cannot make a contribution for In December of 2018, a person cannot make a contribution for

50 When does a Person have to establish the Roth IRA? Same as Traditional IRAs. A person has until the due date (without extensions) for filing his or her federal income tax return, normally April 15, to establish and fund his or her traditional IRA for the previous tax year. April 15, 2019 is the deadline for 2018 contributions. When is a person eligible to contribute to a Roth IRA? A person is eligible for a regular contribution if he or she has modified adjusted gross income below a certain limit for the calendar year for which he or she wishes to make the contribution, and he or she has compensation (income earned from performing material personal services). He or she may also qualify for a rollover to a transfer contribution or certain contributions. What is compensation? What is not compensation? 50

51 Roth IRAs: Contribution Eligibility and Contribution Limits Earned and Taxable Income Safe Harbor - W-2 Box 1 (Wages, tips, other compensation) less Box 11(Nonqualified plans) Does NOT include interest, dividends, rents, retirement income, capital gains, or other investment income Exceptions Taxable Alimony or Taxable Separate Maintenance Non-Taxable Combat Pay Tax-Year 2004 and 2005 closed May 29, 2009 Tax-Year 2006 closed October 15,

52 Contribution Eligibility and Contribution Limits Age Limit: Traditional IRA: Age 70 ½ Roth: No Age Limit As long as a person has compensation and complies with the MAGI restrictions, he or she can make a Roth IRA contribution regardless of how old or young he or she is. 52

53 Roth Contribution Limits How much is a person eligible to contribute to a Roth IRA for the current tax year if he or she will NOT be at least 50 as of December 31? A person is eligible to contribute the lesser of 100% of his or her compensation, or $5,000 for as reduced by any amount he or she contributed to a traditional IRA. For , the annual contribution limit is $5,500. For 2019 the annual contribution limit is $6,000. A person age 50 or older as of December is authorized to make catch-up contributions up to $1,000. The $6000 is adjusted by a cost of living formula. Once the change is $500, the $6000 will change to be $6000. How much is a person eligible to contribute to a Roth IRA for the current tax year if he or she will be at least age 50 as of December 31? A person is eligible to contribute the lesser of 100% of his or her compensation, or $6,000, for as reduced by the amount he or she contributed to a traditional IRA for the same tax year. For , the annual contribution is $6,500. For 2019 the annual contribution limit is $7,

54 Traditional and Roth Contributions May a person contribute to a traditional IRA and also a Roth IRA for the same year? Yes, but the person s aggregate traditional IRA and Roth IRA contributions are subject to the applicable contribution limit for such year. For example, if a contribution limit is $5,500, then the sum of the person s traditional IRA contributions and his or her Roth IRA contributions must be $5,500 or less. Traditional and Roth $5,500 or $6,500 Multiple IRAs traditional and/or Roth 54

55 CWF Form 54-R 55

56 Roth IRA Contribution Eligibility and Limits Cannot have too much MAGI Generally, a person can contribute to a Roth IRA only if he or she has taxable compensation (defined later) and the modified AGI (defined later) is less than: $199,000 for married filing jointly or qualifying widow(er), $135,000 for single, head of household, or married filing separately and the person did not live with his or her spouse at any time during the year, and $10,000 for married filing separately and the person lived with his or her spouse at the time during the year. 56

57 Roth IRA Contribution Eligibility and Limits Cannot have too much MAGI Generally, a person can contribute to a Roth IRA only if he or she has taxable compensation (defined later) and the modified AGI (defined later) is less than: $203,000 for married filing jointly or qualifying widow(er), $137,000 for single, head of household, or married filing separately and the person did not live with his or her spouse at any time during the year, and $10,000 for married filing separately and the person lived with his or her spouse at the time during the year. 57

58 Contribution Eligibility and Contribution Limits Compensation Limits: Traditional IRA: None, does not apply. Roth: Requirements for Annual Contributions: Requirement # 1 - Must have compensation, earned and taxable income Requirement # 2 - Must not have too much compensation or MAGI Married, Joint Return or Qualifying Widow(er) Single, Head of Household Married, Filing Separately MAGI Effect on Roth IRA Contributions % Less than $183,000 $184,000 $186,000 $189,000 $193, % Between Prorated % More than $193,000 $194,000 $196,000 $ $203,000 0% Less than $116,000 $117,000 $118,000 $120,000 $122, % Between Prorated % More than $131,000 $132,000 $133,000 $135,000 $137,000 0% Less than 100% Between Prorated % More than $10,000 $10,000 $10,000 $10,000 $10,000 0% 58

59 Roth IRA Contribution Eligibility and Limits A person s permissible Roth contribution limit is gradually reduced if his or her MAGI exceeds certain amounts. Married, Joint Return or Qualifying Widow(er) Single, Head of Household Married, Filing Separately MAGI Effect on Roth IRA Contributions % Less than $183,000 $184,000 $186,000 $189,000 $193, % Between Prorated % More than $193,000 $194,000 $196,000 $ $203,000 0% Less than $116,000 $117,000 $118,000 $120,000 $122, % Between Prorated % More than $131,000 $132,000 $133,000 $135,000 $137,000 0% Less than 100% Between Prorated % More than $10,000 $10,000 $10,000 $10,000 $10,000 0% 59

60 Roth IRA Contribution Eligibility and Limits Contribution Limit Reduced - Example Example: Jane Doe is a 45-year old, single individual with a taxable compensation of $113,000. She wants to make the maximum allowable contribution to her Roth IRA for Her modified AGI for 2018 is $125,000. She has not contributed to any traditional IRA, so the maximum contribution limit before the modified AGI reduction is $5,500. Using the steps described earlier figure her reduced Roth IRA contribution of $3,670 as show below. Ineligible Contribution = $5,500 x MAGI Phaseout amount $10,000 or $15,000 $5,500 x $5,000 ($125,000 - $120,000) / $15,000 = $1, Round Down = $1, Permissible Roth IRA = $3,670 (after being rounded up) Contribution $5,500-$1,830 = $3,670 60

61 Spousal IRA Limit For if a person files a joint return and his or her taxable compensation is less than that of his or her spouse, the most that can be contributed for the year to the IRA is the smaller of the following two amounts: 1. $5,500 ($6,500 if her or she is age 50 or older), or 2. The total compensation includible in the gross income of both spouses for the year, reduced by the following two amounts. a. The individual spouse s IRA contribution for the year to a traditional IRA b. Any contributions for the year to a Roth IRA on behalf of the individual s spouse. This means that the total combined contributions that can be made for the person s IRA and his or her IRA can be as much as $11,000 ($12,000 if only one spouse is age 50 or older or $13,000 if both are age 50 or older). For the combined limits are $11,000, $12,000 and $13,000! 61

62 Contribution Eligibility and Contribution Limits Spousal Contribution Exception Married Joint Tax Return Joint Earned Income Spouse with Lesser Income uses Joint Earned Income to determine eligibility 62

63 Contribution Eligibility and Contribution Limits Spousal Contribution Exception Example: Mary age 68, and John, age 63, are married. Mary has 2016 compensation of $28,000. John has $3,000 in compensation. They are eligible to each contribute $6,500 to their respective Roth IRA. John Mary Roth IRA $6,500 $6,500 John is allowed to use Mary s compensation to make his own contribution of $6,500 or Mary may make a contribution to John s Roth IRA 63

64 Contribution Eligibility and Contribution Limits Example: Mary age 68, and John, age 73, are married. Mary has 2016 compensation of $7,500. John has $3,000 in compensation, for a total of $10,500. They are eligible for the following contributions. John Mary Traditional IRA -0- $6,000 Traditional IRA Roth IRA $4,500 $6,000 Traditional IRA Roth IRA $4,500 $6,000 Roth IRA Roth IRA $6,000 $4,500 Roth IRA 64

65 Annual Contribution Documentation Use Correct Form for Contribution Type of Contribution Tax Year Date of contribution Accountholder signature Amount 65

66 CWF Form 54-R 66

67 Savers Tax Credit Special/Additional Tax Benefit for Individuals with low or moderate incomes. Tax Credit = Roth IRA Contributions x Applicable Percentage (either 0%, 10%, 20% or 50%) (Limited to $2,000) Sara is single. Her MAGI is $18,000. Her applicable percentage is 50%. She contributes $500 to her Roth IRA. Her tax credit is $250 ($500 x 50%) David and Mary are married. Their MAGI is $61,000. Their applicable percentage is 10%. Both contribute $1,000 to their Roth IRAs. Their tax credit is = $1,000 x 10% or $100 x 2 = $

68 To what extent is a person entitled to a tax credit for an Roth IRA contribution? A formula is used to calculate the credit. Allowed credit = contribution (no more than $2,000) x applicable percentage. The credit may vary from $1 to $1,000, depending on the amount the person contributes to the IRA, his or her filing status and his or her modified adjusted gross income. If the following requirements are met for a given tax year, then this person will qualify for this credit. 1. Be at least 18 years of age as of December 31 of such year 2. Not a dependent on someone else s tax return 3. Not a student as defined in Internal Revenue Code section 25B(c) 4. Have adjusted gross income under certain limits, which are based on your filing status: Joint Filers $61, $61, $62, $63, $64, Head of Household $45, $46, $46, $47, $48, All other filers $30, $30, $31, $31, $32, Must not have received certain distributions which disqualify the person from claiming the credit, or certain distributions which were made to his or her spouse. Because of the complexity of this credit, a person will want to review IRS Publication 590 for a complete explanation. 68

69 Tax Credit for Roth IRA Contributions Adjusted Gross Income 2018 Head of Household Over Not Over $0 $28,500 $30,750 $47,250 Joint Return Over Not Over Adjusted Gross Income 2019 Head of Household Over Not Over All Others Over Not Over Credit % 0-38 $0 $38,000 $0 $28,875 $0 $19,250 50% $38,500 $41,000 $28,875 $31,125 $19,250 $20,750 20% $41,500 $64,000 $31,125 $48,000 $20,750 $32,000 10% 63 $64,000 $48,000 $32,000 0% 69

70 To what extent is a person entitled to a tax credit for an Roth IRA contribution? A formula is used to calculate the credit. Allowed credit = contribution (no more than $2,000) x applicable percentage. The credit may vary from $1 to $1,000, depending on the amount the person contributes to the IRA, his or her filing status and his or her modified adjusted gross income. If the above requirements are met for a given tax year, then this person will qualify for this credit. 70

71 Savers Tax Credit Illustration # 1 Total Income $28,000 $28,000 <IRA Deduction> 0 0 Adjusted Gross Income $28,000 $28,000 Std. Deductions & Exemptions $9,500 $9,500 Taxable Income $18,000 $18,000 Tax $2354 $2,354 IRA Credit 0 $200 Net Tax $2354 $2154 Other Taxes 0 0 Total Tax $2354 $2154 Less Withholding $ Owe/Refund $46 (Refund) $246 (Refund) Example: Paul contributes $2,000 to a new Roth IRA. His credit percentage is 10% since his filing status is single and his modified adjusted gross income is $28,

72 IRA Reports Forms or Reports Prepared by the IRA Custodian Fair Market Statement - January 31 Form 1099-R - January 31 RMD Notices - January 31 (Does not apply to Roth) Form May 31 RMD Notices for Beneficiaries are NOT Required by the IRS, but CWF strongly recommends they be furnished for liability reasons Auditing and Tax Compliance Purposes 72

73 1/1/ /31/2017 CWF Sample of Fair Market Statement Roth IRA Account For 2016 For /1/

74 IRS Tax Forms Forms Prepared by the IRA Custodian 5498: Contributions and Fair Market Value 1099-R: Distributions Forms Prepared by the IRA Accountholder 1040 and others: Used to claim a tax credit or a tax deduction plus used to report a distribution and pay tax on it. 5329: Used to report one or more IRA taxes- 6%, 10% or 50% Used to explain certain distributions from traditional and Roth IRAs. 74

75 Reporting Forms Form

76 Reporting Forms Form

77 Reporting Forms Form 1099-R 77

78 Reporting Forms: 2015 Form 1040 Reporting Forms: Form

79 Reporting Forms: 2015 Form 1040 Reporting Forms: Form

80 Reporting Forms: 2015 Form 1040 Reporting Forms: Form

81 Reporting Forms: 2015 Form 1040 Reporting Forms: Form

82 Reporting Forms: 2015 Form 1040 Reporting Forms: Form

83 Reporting Forms: 2015 Form 1040 Reporting Forms: Form

84 Methods to Convert a Traditional IRA to a Roth IRA 84

85 Methods to Convert a Traditional IRA to a Roth IRA 1. Will increase as the economy improved 2. Converting traditional IRA funds when Funds are All Taxable 3. Converting traditional IRA funds when a portion is taxable and a portion is not 4. Converting traditional IRA funds when none of the funds are taxable. The Goal. 85

86 Methods to Convert a Traditional IRA to a Roth IRA Conversions A person can convert traditional IRA funds to a Roth IRA. The conversion is treated as a rollover, regardless of the conversion method used. Most of the rules for rollovers apply to these rollovers. However, the 1- year waiting period does not apply. Tax Purpose Moving the funds into the Roth IRA will allow the earnings to not be taxed whereas the earnings of a traditional IRA are always taxed. 86

87 Roth Conversions Roth Conversions 1. Will increase as the economy improved 2. Converting traditional IRA funds when Funds are All Taxable 3. Converting traditional IRA funds when a portion is taxable and a portion is not 4. Converting traditional IRA funds when none of the funds are taxable. The Goal. 87

88 Roth Conversions Conversions A person can convert traditional IRA funds to a Roth IRA. The conversion is treated as a rollover, regardless of the conversion method used. Most of the rules for rollovers apply to these rollovers. However, the 1- year waiting period does not apply. Tax Purpose Moving the funds into the Roth IRA will allow the earnings to not be taxed whereas the earnings of a traditional IRA are always taxed. 88

89 Roth Conversions Conversion methods. You can convert amounts from a traditional IRA to a Roth IRA in any of the following three ways. Rollover. He or She can receive a distribution from a traditional IRA and roll it over (contribute it) to a Roth IRA within 60 days after the distribution. Trustee-to-trustee transfer. He or she can direct the trustee of the traditional IRA to the trustee of the Roth IRA. Same trustee transfer. If the trustee of the traditional IRA also maintains the Roth IRA, he or she can direct the trustee to transfer an amount from the traditional IRA to the Roth IRA. The conversion is treated as a rollover, regardless of the conversion method used. Most of the rules for rollovers apply to these rollovers. However, the 1-year waiting period does not apply. 89

90 Roth Conversions A person can convert traditional IRA, SEP-IRA and SIMPLE IRA funds to a Roth IRA. The conversion is treated as a rollover, regardless of the conversion method used. Most of the rules for rollover apply to these rollovers. However, the 1-year waiting period does not apply. Conversion = Pay Tax Now to Have Right to earn Tax-Free Income later. In 2017 Anita has a traditional IRA with a balance of $25,000. Anita is age 35. It is assumed this $25,000 will grow to be $350,000 in 2047 when she is age 65. Should Anita convert her $25,000 traditional IRA? If Anita never converts her traditional IRA, she and her beneficiaries will be required to pay tax on their withdrawal amounts at whatever marginal tax rate applies to the recipient. If the tax rate is assumed to be 20%, then $70,000 of taxes will be paid. If Anita does a conversion in 2017 by paying $5,000 to the IRS, none of the $350,000 when distributed in the future will be taxable. 90

91 Roth Conversions Rules and Procedures 60-Day Rule applies to conversion by rollover method Does not count for the one-per-year rule Reportable distribution from traditional IRA on Form 1099-R on calendar year basis IRS Code 2 (Under 59½) or 7 in Box 7, Distribution code(s) Reportable Roth contribution on Form 5498 on calendar year basis Box 3, Roth IRA conversion amount Conversion amount has same five-year period for qualified distribution purposes Conversion has separate five-year period for penalty tax purposes 91

92 Tax Free Income - Illustration David opened his Roth IRA on January 2, 2008, by making a conversion contribution of $19,000. David was born on January 15, He designates his daughter, Amy, as his beneficiary. Amy was born on February 14, David died on February 2, He was 59. Amy elects to use the life distribution rule. She will need to take her first distribution by December 31, A distribution is not required for It is assumed the balance in the Roth IRA will be $22,500 as of December 31, It is also assumed she will only take out the required amount each year and no more. The schedule will apply to her: Observations 1. David is age 59 when he dies in Amy is age The distributions to Amy in 2011 and 2012 will be non-qualified since the five-year rule has not been met. Even so, these distributions are being returned to Amy. 3. All distributions after 2012 will be qualified and will be tax-free. 4. David s conversion of $19,000 in 2008 will produce $122,288 of tax-free income over a 49 year period if the earnings rate is 6%. 92

93 Tax Free Income - Illustration Year Balance as of Jan. 1 Inherited Roth IRA RMD Schedule for Amy RMD Divisor Earnings 6% Distributions (Q)ualified (NQ)ualified Bal. as of Year-End 2011 $22, $1,350 $455 NQ-T $23, $23, $1,404 $483 NQ-T $24, $25, $1,459 $513 Q $25, $25, $1,516 $544 Q $26, $30, $1,822 $733 Q $31, $38, $2,300 $1,114 Q $39, $46, $2,791 $1,698 Q $47, $52, $3,178 $2,597 Q $53, $53, $3,217 $4,001 Q $52, $31, $1,909 $7,230 Q $26, $26, $1,590 $7,792 Q $20, $20, $1,212 $8,454 Q $13, $13, $783 $9,324 Q $4, $4, $271 $4,784 Q 0 Total Earnings & Distributions $118,787 $141,288 93

94 Roth Conversions Rules for 2010 Conversions Acceleration of income rules for later withdrawals Death of Roth IRA Accountholder Rules for Conversion Standard Tax Rule for Conversions occurring in 2011 and later NO longer any requirement to establish a separate Roth IRA, for a conversion contribution Partial Conversions are permissible Conversions in 2018 is irrevocable 94

95 Roth IRA Conversion Contributions Rules and Procedures 60-Day Rule applies to conversion by rollover method Does not count for the one-per-year rule Reportable distribution from traditional IRA on Form 1099-R on calendar year basis IRS Code 2 (Under 59½) or 7 in Box 7, Distribution code(s) Reportable Roth contribution on Form 5498 on calendar year basis Box 3, Roth IRA conversion amount Conversion amount has same five-year period for qualified distribution purposes Conversion has separate five-year period for penalty tax purposes 95

96 Roth IRA Conversion Contributions Eligibility Requirements Required Minimums cannot be converted IRA RMDs must be satisfied first Separate Roth IRA Plan Agreement is not required SEP IRAs can be converted to a Roth IRA SIMPLE IRAs can be converted to a Roth IRA after its 2-year holding period Other retirement accounts can not be converted directly to a Roth IRA before January 1, 2008 Inheriting beneficiary cannot convert an inherited traditional IRA directly to Roth IRA Sole spouse beneficiary can elect to treat it as his/her own or any spouse beneficiary can rollover the inherited IRA to his/her own IRA and then convert it to a Roth IRA Careful documentation is required 96

97 Roth IRA Conversions 1. Will increase as the economy improves 2. Converting traditional IRA funds when Funds are All Taxable IRA Balance = $60,000 Convert $10,000 each year for 6 years Convert $15,000 each year for 4 years Convert $20,000 each year for 3 years Conversions can be recharacterized if certain rules are met. 97

98 Roth IRA Conversions 3. Converting traditional IRA funds when a portion is taxable and a portion is not. Many individuals choose to not do a conversion because they do not want to pay taxes on the taxable portion of the distribution. Example: John s IRA Deductible IRA contribution $50,000 Taxable Earnings $15,000 Taxable Non-Deductible IRA Contributions $30,000 Not Taxable Earnings $5,000 Taxable Total $100,000 Ratio 70% taxable 30 % non-taxable John Converts $100,000. He pays tax on $70,000 (70%) of $100,000. John Converts $50,000. He pays tax on $35,000 70%) of $50,

99 CWF #65- R1 CWF #65- MDG CWF #65- R6 99

100 ROTH IRA CONVERSION CONTRIBUTIONS Requirements 60-Day Rule applies to conversion by rollover method Does not count for the once-per-year rule Reportable distribution from traditional IRA on Form 1099-R on calendar year basis IRS Code 2(Under 59½) or 7 in Box 7, Distribution code(s) Reportable Roth contribution on Form 5498 on calendar year basis Box 3, Roth IRA conversion amount Conversion amount has same five-year period for qualified distribution purposes Conversion has separate five-year period for penalty tax purposes 100

101 ROTH IRA CONVERSION CONTRIBUTIONS Requirements Required Minimums cannot be converted IRA RMDs must be satisfied first RMDs cannot be converted Separate Roth IRA Plan Agreement is not required SEP IRAs can be converted to a Roth IRA SIMPLE IRAs can be converted to a Roth IRA after its 2-year holding period Other retirement accounts can not be converted directly to a Roth IRA before January 1, 2008 Inheriting beneficiary cannot convert an inherited traditional IRA directly to Roth IRA Sole spouse beneficiary can elect to treat it as his/her own or any spouse beneficiary can rollover the inherited IRA to his/her own IRA and then convert it to a Roth IRA Careful documentation is required 101

102 Reporting of IRA Conversion Contributions 2017 Special reporting if basis from a 401(k) plan is rolled over into a traditional IRA 102

103 Converting a Traditional IRA with 100% Basis Make a non-deductible contribution and the convert it immediately to a Roth IRA Example: Jane Smith has a modified gross income of $198,000 for She participates in a 401(k) plan. She is ineligible to make an annual Roth contribution as her income exceeds the eligibility limits. Assuming she currently has no taxable dollars within a traditional, SEP or SIMPLE IRA, she may make a non-deductible contribution and then convert it. 103

104 Converting a Traditional IRA with 100% Basis John s IRA Deductible IRA contribution $ 55,000 Earnings $ 15,000 Non-Deductible IRA Contributions $ 24,000 Earnings $ 6,000 Total $100,000 Step 1 Step 2 Step 3 Roll taxable amount ($76,000) into a pension plan Roll/Convert ($24,000) into a Roth IRA Return the $76,000 to an IRA, if desired and permitted IRA 401(k) Plan $76,000 $76,000 $24,000 IRA Roth IRA $24,

105 Trustee-to-Trustee Transfer Roth IRA to Roth IRA 105

106 Transfers and Rollovers are exceptions to the general tax rule that a distribution is taxable. Transfers Rollovers There is no taxable event when a transfer occurs and a transfer is not required to be requested A rollover transaction is a reportable event, but it is a nontaxable event Transfer Rollover Direct Rollover Plan to Plan Plan to Person to Plan Pension Plan to IRA fbo person 106

107 Trustee-to-Trustee Transfer A contractual right, not a legal right IRS Administrative creation Difficulty - IRS has never in writing defined what must be done to have a transfer 107

108 Trustee-to-Trustee Transfer Two types of transfers Non-reportable - No 1099-R or 5498 Reportable - A 1099-R or 5498 must be prepared 108

109 Move Roth IRA Asset from one Roth IRA to another, one Roth IRA custodian/trustee to another Roth IRA custodian trustee, on a Tax-Free Basis Requirements: IRS Requirements for a non-reportable transfer need to use a transfer form Check/Draft/Wire made payable to new IRA custodian/trustee ABC Financial Institution as Custodian/Trustee for John Jones (traditional, SEP, SIMPLE, Roth) IRA No IRS Limit Reasonable Custodian/Trustee restrictions allowed Not Reportable to IRS Federal Income Tax withholding rules do not apply 109

110 Trustee-to-Trustee Transfer Non-reportable Transfer must be from same type of IRA Traditional IRA to Traditional IRA Traditional IRA to SEP IRA SEP IRA to SEP IRA ** SEP IRA to Traditional IRA Roth IRA to Roth IRA SIMPLE IRA to SIMPLE IRA SIMPLE IRA to Traditional IRA Traditional IRA to SIMPLE IRA (SIMPLE 2 year rule met) Traditional IRA to SIMPLE IRA (SIMPLE 2 year rule met) 110

111 Trustee-to-Trustee Transfer - Reportable Direct Rollover - Non-Like Kind 401(k) - Traditional IRA 401(k) - Roth IRA Traditional IRA - Roth IRA A Roth IRA Conversion Recharacterizations Traditional IRA - HSA Qualified HSA Funding Distribution Traditional IRA - 401(k) Reverse Direct Rollover 111

112 CWF Form # 56 CWF Form # 56-R CWF # 56 CWF # 56R 112

113 Trustee-to-Trustee Transfer Trustee-to-Trustee Transfer CWF Form # 54 CWF Form # 54-R 113

114 Inherited IRAs can be Transferred Trustee-to-Trustee Transfer CWF Form # 56-I CWF Form # 56-RI 114

115 Trustee-to-Trustee Transfer Roth IRAs and Divorces or Legal Separations Roth IRAs can only be transferred to an ex-spouse s Roth IRA Decree must be specific How, How much, When, etc. Have Roth IRA s (former) owner complete distribution form CANNOT be done as a distribution and a rollover. -Court order may be needed to correct. 115

116 Roth IRA-to-Roth IRA Rollovers 116

117 Roth IRA-to-Roth IRA Rollovers Purpose Usually to move Roth IRA assets from one Roth IRA to another Roth IRA Rollover can be brought back to the same Roth IRA Roth IRA Individual Roth IRA 117

118 Roth IRA-to-Roth IRA Rollovers Purpose Usually to move Roth IRA assets from one Roth IRA to another Roth IRA Rollover can be brought back to the same Roth IRA Requirements. One rollover per 12-month period. Check/Draft/Wire is made payable to or for the IRA accountholder. Roth IRA Assets must be deposited into Roth IRA within 60 calendar days. Must be same type of IRA * Traditional IRA to Traditional IRA * Traditional IRA to SEP IRA * SEP IRA to SEP IRA * SEP IRA to Traditional IRA * Roth IRA to Roth IRA * SIMPLE IRA to SIMPLE IRA * SIMPLE IRA to Traditional IRA (SIMPLE 2yr Holding Period) 118

119 Roth IRA-to-Roth IRA Rollovers General Rule: A rollover is one of the exceptions to the rule that a person will be taxed when he or she is paid the Roth IRA assets. When the assets are properly rolled over, taxation will be delayed until a later taxable distribution occurs. The general rule is that only the Roth IRA accountholder is eligible to roll over Roth IRA assets that have been paid from his or her own Roth IRA to another Roth IRA. However, a surviving spouse beneficiary may roll over a distribution paid from a deceased spouse s Roth IRA into their own Roth IRA. A divorced Roth IRA owner cannot roll over a distribution from his/her former spouse s Roth IRA into his/her own Roth IRA. 119

120 Roth IRA-to-Roth IRA Rollovers Purpose Usually to move Roth IRA assets from one Roth IRA to another Roth IRA Rollover can be brought back to the same Roth IRA Requirements One rollover, per 12-month period (not per investment) Roth IRA Assets must be deposited into Roth IRA within 60 calendar days Check/Draft/Wire is normally made payable to the Roth IRA accountholder The same property must be rolled over. If property is distributed to you from an Roth IRA and you complete the rollover by contributing property to an Roth IRA, your rollover is tax-free only if the property you contribute is the same property that was distributed to you. You are unable to sell the property distributed and rollover the proceeds. A distribution from an inherited Roth IRA to a non spouse beneficiary is ineligible to be rolled over. 120

121 Roth IRA-to-Roth IRA Rollovers What is the time limit for making a rollover contribution? You generally must make a rollover contribution by the 60 th day after the day you receive the distribution from your Roth. Example. You received an eligible rollover distribution from your Roth IRA on October 17, 2017, that you intend to rollover to another Roth IRA. To postpone including the distribution in your income, you must complete the rollover by December 16, 2017, the 60 th day following October 17. The IRS may waive the 60-day requirement where the failure to do so would be against equity or good conscience, in the event of a casualty, disaster, or other event beyond your reasonable control. If the 60 th day falls on a Saturday, Sunday or holiday the individual has until the next business day. 121

122 Roth IRA-to-Roth IRA Rollovers The Once Per Year Rule Example # 1: A person who took a distribution October 17, 2016, and rolled it over within the 60 day limit, is eligible to rollover a subsequent distribution from any other IRA only if such distribution occurs on October 17, 2017 or later. A person who takes a distribution on October 17 th wanting to roll it over is only eligible if he or she did not during the preceding 12 month period (October 17, 2016 to October 16, 2017) take a distribution which was totally or partially rolled over. Example # 2: A person is authorized to rollover one distribution in a one year period. A person who withdraws $3,000 on May 11 and then withdraws $15,000 on May 25 from the same IRA, will have to decide which of the two distributions to rollover since only distribution is eligible to be rolled over. There is an exception for FDIC bank closure. An additional rollover is permitted. The Once Per Year Rule is an IRA rule. It does not apply to distribution from 401(k) or other employer plans 122

123 Roth IRA-to-Roth IRA Rollovers The Once Per Year Rule Old Rule No longer Available An IRA accountholder is authorized to take a distribution from his or her IRA and roll it over once per year. Although the statutory law could be read that a person with multiple IRA plan agreements is allowed to do only one rollover per year, the IRS has adopted the rule administratively that a person may do one rollover per year per plan agreement. A person who only has one plan agreement comprised of 5 different CDs is permitted to do only one rollover per year. In contrast, a person with 5 different IRA plan agreements, would be eligible to do a rollover within one year from each of the five plan agreements. 123

124 Roth IRA-to-Roth IRA Rollovers Requirements (continued): Rollovers are reportable to the IRS Distributions on Form 1099-R Regular IRA reporting codes Rollover contributions on Form 5498 Box 2 60 Day Rule Once per 12 month rule new rule effective Not per investment Not per plan agreement If a person has a traditional IRA and a Roth IRA, the person in 2016 if he or she withdraws funds during a 12 month period from both IRAs will only be able to roll over one of the distributions 124

125 CWF Form # 57-R 125

126 CWF Form # 65-R2 126

127 Roth IRAs Special Rollover Rules Military Death Gratuities and Service members Group Life Insurance (SGLI) Payments Rollover and Exxon Valdez Settlement Income Rollover of Airline Payments 127

128 IRA-to-IRA Rollovers 60-Day Rollover Waiver (Applies to QRP Rollovers too) Automatic Waiver No IRS permission needed Custodian/Trustee error Must have received rollover assets timely As usual rollover documentation completed timely IRA timely established for rollover Must be within one year of distribution. IRS Filing. New Self-Certification method 128

129 Roth IRA-to-QRP Rollover Roth IRA to QRP Impermissible Traditional IRA to QRP Permissible 129

130 QRP-to-Roth IRA Rollovers 130

131 Qualified Retirement Plan (QRP)-to-IRA Rollovers QRP-to-IRA Direct Rollover Procedures - QRP Administrator 402(f) Notice to participant Must also allow for distribution to participant Upon receipt of Direct Rollover Request Verify all information Make check/draft/wire out to ABC Financial Institution as custodian/trustee for John Jones IRA Send to participant or IRA custodian/trustee Report as Direct Rollover on Form 1099-R IRS Code G 131

132 QRP- to-ira Rollovers Qualified Retirement Plan (QRP)-to-Traditional or Roth IRA Direct Rollover- Directly to the IRA No Distribution No Distribution No Distribution 132

133 IRA Rollovers and Direct Rollovers Eligible Retirement Plan to Roth IRA Conversion Since 2008 other retirement accounts can be converted directly to a Roth IRA This includes inheriting beneficiary or ERP Inherited QRP Inherited QRP Inherited Roth QRP Direct Rollover Non-Spouse Beneficiary (Direct) Rollover/ Conversion Non-Spouse Beneficiary (Direct) Rollover Inherited Traditional IRA Inherited Roth IRA Inherited Roth IRA 133

134 Tax Benefits of a Roth IRA Maximizing Contributions To a Roth IRA A person wants to maximize the amount he or she contributes to a Roth IRA. The tax rules permit eight different types of contributions to a Roth IRA. In some years the person might be eligible to make just one of the types of Roth IRA Contributions. In other years he or she might be eligible to make all eight types or might be ineligible to make any Roth IRA contribution. The Eight types of Roth IRA contributions are: 1. An annual contribution; 2. A conversion contribution from a traditional IRA; 3. A conversion contribution from a SEP-IRA; 4. A conversion contributions from a SIMPLE-IRA; 5. A direct rollover (i.e. a conversion) of non-roth funds; 6. A direct rollover or rollover of Designated Roth funds; 7. A direct rollover or rollover of a deceased spouse s Designated Roth funds; and 8. A direct rollover (i.e. a conversion) of non-roth funds from a deceased spouse s 401(k) plan; 134

135 Special Contributions Recharacterizations Allows one to undo or correct a contribution without having to remove the earnings Effects of Recharacterization The original contribution is treated as having been made to IRA Type # 2 rather than as made to IRA Type # 1. A non-taxable transaction. 135

Roth IRA Conversion")

136 Recharacterization Contribution To a Roth IRA (1) Traditional IRA Annual Contribution Roth IRA Annual Contribution Roth IRA Annual Contribution Traditional IRA Annual Contribution (2) Roth IRA Conversion Traditional IRA 136

137 Recharacterizations Custodian/Trustee Reporting Original contribution is reported on Form 5498 for 1 st IRA Recharacterization is reported on Form 1099-R for 1 st IRA Recharacterized contribution is reported on Form 5498 for 2 nd IRA Individual Reporting - Complete Form 1040 and attach a special note, if applicable Remember No tax amount owing

CWF Form #")

138 Use the Proper Form(s) CWF Form # 54TR1 138

CWF Form #")

139 Use the Proper Form(s) CWF Form # 54TR2 139

CWF Form #")

140 Use the Proper Form(s) CWF Form # 56TRX 140

141 Postponed contributions Repayment contributions

142 Excess Contributions and current year contributions We will address Roth IRA excess contributions 6% Excise Tax Current year contributions are not always excess contributions, but the withdrawal rules allow their withdrawal. For reporting purposes, current year contributions are treated as excess contributions. 6% x $6,500 = $390 6% x $5,500 = $330 6% x $50,000 = $3,

143 Excess Contributions Excess Traditional and Roth IRA Contributions Impermissible contribution Not a Prohibited Transaction Ineligible to contribute Contribute more than permitted More than the annual limit More than qualified compensation Rolled over ineligible IRA amount Rolled over ineligible QRP amount 143

144 Excess Contributions Excess Traditional or Roth IRA Contribution Impermissible contribution Consequences of uncorrected excess contribution 6% penalty If not removed timely 6% per year until corrected Example # 1: Ellen, she had no compensation, age 73, contributes $5,500 to a Roth IRA on March 15, 2015 for Her deadline to avoid the 6% tax for 2014 is October 15, Her deadline to avoid the 6% tax for 2015 is December 31,

145 Excess Contributions Excess Traditional or Roth IRA Contribution Apply it to subsequent year eligibility Withdraw excess contribution By due date of Federal tax return, including extension Must include applicable earnings Must be removed after due date plus extensions or penalty continues Must not have been deducted on IRA Owner s Federal tax return Contribution is tax and penalty free only if IRA Custodian/Trustee Reporting Report original contribution on Form 5498 (Including Excess) Report the distribution/correction on Form 1099-R Traditional IRA Distribution codes 8 or 81 / P or P1 Roth IRA distribution codes J8 or JP 145

146 Roth IRAs Session 1 Establishing and Contributions Any Final Questions? Thank you for your attendance and participation in this webinar. 146

147 call us at or send an to Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may be reproduced in any form and by any means without prior written permission from Collin W. Fritz & Associates, Ltd.

1. New IRA Contribution Limits for IRA Transfers 3. IRA Rollovers (k) Direct Rollovers 5. Fraudulent contributions

Direct Rollovers 5. Fraudulent contributions") 1. New IRA Contribution Limits for 2013 2. IRA Transfers 3. IRA Rollovers 4. 401(k) Direct Rollovers 5. Fraudulent contributions Rev 12-5-2012 Just a Reminder: This is copyrighted material. No Video or

1. New IRA Contribution Limits for 2013 2. IRA Transfers 3. IRA Rollovers 4. 401(k) Direct Rollovers 5. Fraudulent contributions Rev 12-5-2012 Just a Reminder: This is copyrighted material. No Video or

Inherited Traditional IRAs for Non-Spouse Beneficiaries.

Rev2/15/2018 Inherited Traditional IRAs for Non-Spouse Beneficiaries. We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly. 8:30

Rev2/15/2018 Inherited Traditional IRAs for Non-Spouse Beneficiaries. We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly. 8:30

The Webinar will be starting shortly

Rev. 5/2/2018 The Webinar will be starting shortly 8:30 am CST or 12:30 pm CST We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar Copyright 2018 Collin W. Fritz &

Rev. 5/2/2018 The Webinar will be starting shortly 8:30 am CST or 12:30 pm CST We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar Copyright 2018 Collin W. Fritz &

The Webinar will be starting shortly

7/11/2018 The Webinar will be starting shortly 8:45 am CST or 1:00 pm CST Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may

7/11/2018 The Webinar will be starting shortly 8:45 am CST or 1:00 pm CST Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may

Street Address. City, State, ZIP

ROTH IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address IRA Owner

ROTH IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address IRA Owner

is a qualified Hurricane Katrina distribution.

September 2005 Published Since 1984 ALSO IN THIS ISSUE IRA Disclaimers New IRS Guidance, Page 3 Modified Adjusted Gross Income (MAGI) for Roth IRA Contribution Purposes, Page 4 Tax Treatment of HSA Upon

September 2005 Published Since 1984 ALSO IN THIS ISSUE IRA Disclaimers New IRS Guidance, Page 3 Modified Adjusted Gross Income (MAGI) for Roth IRA Contribution Purposes, Page 4 Tax Treatment of HSA Upon

IRS Issues 2014 IRA/Pension Limits. IRA Contribution Limits for 2014 Unchanged at $5,500 and $6,500 ALSO IN THIS ISSUE

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Deductibility Charts 2013 and 2014, Page 2 Roth IRA Contribution Charts for 2013 and 2014, Page 3 SEP and SIMPLE Limits, Page 3 Saver s Credit Limits

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Deductibility Charts 2013 and 2014, Page 2 Roth IRA Contribution Charts for 2013 and 2014, Page 3 SEP and SIMPLE Limits, Page 3 Saver s Credit Limits

A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA

Rev 7/11/2018 A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting

Rev 7/11/2018 A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting

Roth IRAs The Roth IRA

Roth IRAs The Roth IRA 2017 and 2018 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

Roth IRAs The Roth IRA 2017 and 2018 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

Addendum to the Traditional IRA Custodial Agreement and Disclosures

Effective January 1, 2018 Addendum to the Traditional IRA Custodial Agreement and Disclosures This Addendum changes the Traditional IRA Custodial Agreement and Disclosures ( Agreement ) document and uses

Effective January 1, 2018 Addendum to the Traditional IRA Custodial Agreement and Disclosures This Addendum changes the Traditional IRA Custodial Agreement and Disclosures ( Agreement ) document and uses

IRA Contribution Limits for 2018 Unchanged at $5,500 and $6,500; 401(k) Limits Do Change

Limits Do Change") Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 544260 (Rev 17-06/17) Page 1 of 25 Table of Contents Section I: Disclosure Statement A. Introduction...

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 544260 (Rev 17-06/17) Page 1 of 25 Table of Contents Section I: Disclosure Statement A. Introduction...

Traditional SEP, and SIMPLE IRAs

Traditional SEP, and SIMPLE IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why must I and others age 70 1/2 or older have to take a required distribution? The purpose of an IRA

Traditional SEP, and SIMPLE IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why must I and others age 70 1/2 or older have to take a required distribution? The purpose of an IRA

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement

Wells Fargo Clearing Services, LLC Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Table of Contents Section I: Disclosure Statement A. Introduction...3

Wells Fargo Clearing Services, LLC Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Table of Contents Section I: Disclosure Statement A. Introduction...3

Traditional IRAs. Understanding Required Distributions at 70 1 / 2. Questions & Answers

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

Traditional IRA SEP IRA Roth IRA. Disclosure Statement & Custodial Account Agreement

Traditional IRA SEP IRA Roth IRA Disclosure Statement & Custodial Account Agreement Table of Contents Page in Document PART I COMBINED DISCLOSURE STATEMENT AND CUSTODIAL ACCOUNT AGREEMENT... 1 TRADITIONAL

Traditional IRA SEP IRA Roth IRA Disclosure Statement & Custodial Account Agreement Table of Contents Page in Document PART I COMBINED DISCLOSURE STATEMENT AND CUSTODIAL ACCOUNT AGREEMENT... 1 TRADITIONAL

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

BNY MELLON INVESTMENT SERVICING TRUST COMPANY. Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement

Disclosure Statement") BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

Street Address. PRIMARY Beneficiary(ies) % Column MUST total 100% % Name Mailing Address Relationship Birth Date SS #

% Column MUST total 100% % Name Mailing Address Relationship Birth Date SS #") TRADITIONAL IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address

TRADITIONAL IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address

No Form 1099-R Prepared to Report IRA Funds Moving From the Decedent s IRA to an Inherited IRA

Published Since 1984 2015 Tax Filing Deadline is April 18, 2016 ALSO IN THIS ISSUE 2015 Form 5500 Series Returns Should Not Answer the Compliance Questions, Page 2 Inherited IRA Situation - Daughter Dies,

Published Since 1984 2015 Tax Filing Deadline is April 18, 2016 ALSO IN THIS ISSUE 2015 Form 5500 Series Returns Should Not Answer the Compliance Questions, Page 2 Inherited IRA Situation - Daughter Dies,

Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement

Disclosure Statement") BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement Deadline Extension for 2016 Contributions to a Traditional

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement Deadline Extension for 2016 Contributions to a Traditional

Obama Administration Again Proposes Taxing Some Roth IRA Distributions And Other Law Changes

Published Since 1984 ALSO IN THIS ISSUE IRS Increases Filing Fees For Waiver of 60-Day Rollover Rule to $10,000, Page 3 Maximizing Contributions to a Roth IRA, Page 4 Types of IRAs Versus Types of IRA

Published Since 1984 ALSO IN THIS ISSUE IRS Increases Filing Fees For Waiver of 60-Day Rollover Rule to $10,000, Page 3 Maximizing Contributions to a Roth IRA, Page 4 Types of IRAs Versus Types of IRA

Are IRA Amendments Required For ?

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

UMB BANK, N.A. INFORMATION KIT

UMB BANK, N.A. UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT (EFFECTIVE DECEMBER 1, 2016) UMB Bank, N.A. Universal Individual Retirement Custodial Account Instructions for Opening Your Traditional

UMB BANK, N.A. UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT (EFFECTIVE DECEMBER 1, 2016) UMB Bank, N.A. Universal Individual Retirement Custodial Account Instructions for Opening Your Traditional

BNY MELLON INVESTMENT SERVICING TRUST COMPANY. Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement

Disclosure Statement") BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

Traditional Individual Retirement Account Disclosure Statement and Custodial Agreement

Traditional Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Page 1 of 26 Table of Contents Section I: Disclosure Statement A. Introduction... B. Contributions

Traditional Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Page 1 of 26 Table of Contents Section I: Disclosure Statement A. Introduction... B. Contributions

EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA

Traditional IRA Roth IRA") GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA References to the Custodian mean BNY Mellon Investment Servicing Trust Company. BNY Mellon Investment Servicing Trust Company

GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA References to the Custodian mean BNY Mellon Investment Servicing Trust Company. BNY Mellon Investment Servicing Trust Company

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA.

Traditional IRA SEP IRA.") PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional

IRA Contribution Limits for 2019 $6,000 and $7,000

Published Since 1984 ALSO IN THIS ISSUE IRA Contributions for 2019 Page 1 IRA Contribution Deductibility Charts for 2018 and 2019 Page 2 Roth IRA Contribution Charts for 2018 and 2019 Page 3 SEP and Simple

Published Since 1984 ALSO IN THIS ISSUE IRA Contributions for 2019 Page 1 IRA Contribution Deductibility Charts for 2018 and 2019 Page 2 Roth IRA Contribution Charts for 2018 and 2019 Page 3 SEP and Simple

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA

TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA") Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA TABLE OF CONTENTS SUPPLEMENT TO THE COMBINED IRA DISCLOSURE STATEMENT 3 COMBINED

Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA TABLE OF CONTENTS SUPPLEMENT TO THE COMBINED IRA DISCLOSURE STATEMENT 3 COMBINED

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

Recent Changes to IRAs

Recent Changes to IRAs Federal legislation and new IRS regulations have created several changes to IRAs in the past year. Prohibition on recharacterization of IRA conversions: Effective for taxable years

Recent Changes to IRAs Federal legislation and new IRS regulations have created several changes to IRAs in the past year. Prohibition on recharacterization of IRA conversions: Effective for taxable years

BNY MELLON INVESTMENT SERVICING TRUST COMPANY

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement for Tax Year 2019 DEADLINE EXTENSION FOR 2018 CONTRIBUTIONS

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement for Tax Year 2019 DEADLINE EXTENSION FOR 2018 CONTRIBUTIONS

EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

Individual Retirement Account (IRA)

") Longleaf Partners Funds Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA Contents BNY Mellon Investment Servicing Trust Company 2 Traditional and Roth IRA Combined Disclosure Statement

Longleaf Partners Funds Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA Contents BNY Mellon Investment Servicing Trust Company 2 Traditional and Roth IRA Combined Disclosure Statement

ROTH INDIVIDUAL RETIREMENT CUSTODIAL ACCOUNT AGREEMENT

ROTH INDIVIDUAL RETIREMENT CUSTODIAL ACCOUNT AGREEMENT Form 5305- RA under section 408A of the Internal Revenue Code. FORM (Rev. March 2002) The depositor named on the application is establishing a Roth

ROTH INDIVIDUAL RETIREMENT CUSTODIAL ACCOUNT AGREEMENT Form 5305- RA under section 408A of the Internal Revenue Code. FORM (Rev. March 2002) The depositor named on the application is establishing a Roth

AMG FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") AMG FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

AMG FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

The Audio portion of this presentation is available either by phone or by using the speakers and microphone on your PC.

6-23-2010 1 2 The Audio portion of this presentation is available either by phone or by using the speakers and microphone on your PC. The phone number is provided to you in the confirmation from CWF and

6-23-2010 1 2 The Audio portion of this presentation is available either by phone or by using the speakers and microphone on your PC. The phone number is provided to you in the confirmation from CWF and

IRA Limits for 2010 & 2011

Published Since 1984 ALSO IN THIS ISSUE Review of IRA Contributions Eligibility Rules, Page 2 Is an RMD Due for 2011?, Page 2 IRA Contribution Deductibility Charts, Page 3 Roth IRA Contribution Charts,

Published Since 1984 ALSO IN THIS ISSUE Review of IRA Contributions Eligibility Rules, Page 2 Is an RMD Due for 2011?, Page 2 IRA Contribution Deductibility Charts, Page 3 Roth IRA Contribution Charts,

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

IRA APPLICATION KIT. Roth-IRA

IRA APPLICATION KIT Roth-IRA MH Elite Portfolio of Funds Trust Huntington National Bank, Custodian 43 Highlander Drive Scotch Plains, NJ 07076 Phone: 800.318.7969 Fax: 908.444.8752 INSTRUCTIONS FOR OPENING

IRA APPLICATION KIT Roth-IRA MH Elite Portfolio of Funds Trust Huntington National Bank, Custodian 43 Highlander Drive Scotch Plains, NJ 07076 Phone: 800.318.7969 Fax: 908.444.8752 INSTRUCTIONS FOR OPENING

Roth IRA Amendment ROTH INDIVIDUAL RETIREMENT CUSTODIAL ACCOUNT 5305-RA

Roth IRA Amendment Dear Roth IRA Owner: The purpose of this Amendment is to incorporate changes in law and policy that affect your Roth IRA agreement. This Amendment replaces the IRS Form 5305-RA Agreement

Roth IRA Amendment Dear Roth IRA Owner: The purpose of this Amendment is to incorporate changes in law and policy that affect your Roth IRA agreement. This Amendment replaces the IRS Form 5305-RA Agreement

General Questions 1) Who is GoldStar? 2) What do I need to get started? 3) Can I fax or the documents?

Who is GoldStar? 2) What do I need to get started? 3) Can I fax or the documents?") General Questions: 1) Who is GoldStar? a) GoldStar Trust Company is one of the nation's leading Self-Directed IRA custodians with over twenty years of experience. GoldStar offers unique retirement solutions

General Questions: 1) Who is GoldStar? a) GoldStar Trust Company is one of the nation's leading Self-Directed IRA custodians with over twenty years of experience. GoldStar offers unique retirement solutions

Voya Funds Individual Retirement Account (IRA)

") Voya Funds Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA For financial professional use only. Not for inspection by, distribution or quotation to, the general public. INVESTMENT

Voya Funds Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA For financial professional use only. Not for inspection by, distribution or quotation to, the general public. INVESTMENT

Roth I R A s. General Informa tion and Instr uctions: