1. New IRA Contribution Limits for IRA Transfers 3. IRA Rollovers (k) Direct Rollovers 5. Fraudulent contributions

|

|

|

- Ursula Lloyd

- 5 years ago

- Views:

Transcription

Direct Rollovers 5.")

1 1. New IRA Contribution Limits for IRA Transfers 3. IRA Rollovers (k) Direct Rollovers 5. Fraudulent contributions Rev

2 Just a Reminder: This is copyrighted material. No Video or Audio Recording is permitted without prior written consent from Collin W. Fritz & Associates, Ltd.

3 The Audio portion of this presentation is available either by phone or by using the speakers and microphone on your PC. The phone number is provided to you in the confirmation from CWF and again at the time you join the meeting. You will need the access code that was ed to you in the confirmation from CWF. The confirmation code is 9 digits in length e.g You will also need the Audio Pin # which is shown to you at the time you join this meeting If you need assistance re-connecting please call CWF at Copyright 2012 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may be reproduced in any form and by any means without prior written permission from Collin W. Fritz & Associates, Ltd.

4 THE TRADITIONAL IRA LIFE SPAN Contributions Deductible Non-Deductible Rollovers Transfers Custodial or Trust Account Earnings Within Account are not Taxed Distributions Accountholder Before Age 59½ Age 59½ to 70½ and older Beneficiaries Original Subsequent In general, the accountholder or beneficiary will include the distribution in income and pay tax 4

5 THE ROTH IRA LIFE SPAN Contributions Deductible Non-Deductible Rollovers Transfers Custodial or Trust Account Earnings Within Account are not Taxed Distributions Accountholder Before Age 59½ Age 59½ to 70½ and older Beneficiaries Original Subsequent In general, the accountholder or beneficiary will include the distribution in income and pay tax 5

6 NEW IRA CONTRIBUTION LIMITS FOR

7 New IRA Contribution Limits for $5,500 and $6,500 After many years, the maximum IRA contribution limits for 2013 will be $500 larger. For , if a person was not age 50 as of December 31, then his or her maximum contribution was $5,000 assuming he or she had compensation of at least $5,000. This limit increases to $5,500 for For , if a person was age 50 or older as of December 31, this his or her maximum contribution was $6,000. This limit increases to $6,500 for The annual catch-up contribution limit for individuals age 50 or older remains at $1,000. Hopefully, contributions for 2013 will be larger than those for 2012 and end the decrease in IRA contributions. NEW IRA CONTRIBUTION LIMITS FOR 2013 Contribution limits for a person who is NOT age 50 or older Tax Year Amount 2008 $5, $5, $5, $5, $5, $5,500 Contribution Limits for a person who is age 50 or older Tax Year Amount 2008 $6, $6, $6, $6, $6, $6,500 7

8 NEW IRA CONTRIBUTION LIMITS FOR 2013 Annual Contributions Lesser of IRA Qualified Compensation or Annual Limit Per Person, Per Year Catch-up Contributions - Age 50 and older Tax Year Contribution Limit Catch-Up Amount Total Contribution 2006 $4,000 $1,000 $5, $4,000 $1,000 $5, $5,000 $1,000 $6, $5,500 $1,000 $6,500 8

9 Traditional IRAs Eligibility for annual contributions must have compensation and must not attain age 70½ or older during the current year for which the contribution is made. Eligibility for other types of contributions Rollovers Transfers SEPs Recharacterizations NEW IRA CONTRIBUTION LIMITS FOR

10 IRA Contributions Deadline When Can Contributions Be Made? NEW IRA CONTRIBUTION LIMITS FOR 2013 Contributions to an IRA for a given year can be made at any time during the year as long as by the due date of the individuals federal income tax return, not including extensions. Special Holiday rules. Special deadline for 2011 was April 17, 2012 Deadline for 2012 is April 15,

11 NEW IRA CONTRIBUTION LIMITS FOR 2013 When does a person have to establish the traditional IRA? A person has until the due date (without extensions) for filing his or her federal income tax return, normally April 15, to establish and fund his or her traditional IRA for the previous tax year. April 15, 2013 is the deadline for When is a person eligible to contribute to a traditional IRA? A person is eligible for a regular contribution if he or she does not reach age 70½ in the calendar year for which he or she wishes to make the contribution, and he or she has compensation (income earned from performing material personal services). He or she may also qualify for a rollover or a transfer contribution or certain recontributions. 11

12 NEW IRA CONTRIBUTION LIMITS FOR 2013 How much is a person eligible to contribute to a traditional IRA for the IRA for the current tax year if he or she will NOT be at least 50 as of December 31? A person is eligible to contribute the lesser of 100% of his or her compensation, or $5,000, for 2009, 2010, 2011, and 2012 as reduced by any amount he or she contributed to a Roth IRA. For 2013, the maximum contribution increases to $5,500. How much is a person eligible to contribute to a traditional IRA for the current tax year if he or she will be at least age 50 as of December 31? A person is eligible to contribute the lesser of 100% of his or her compensation, or $6,000, for 2009, 2010, 2011, and 2012 as reduced by any amount he or she contributed to a Roth IRA for the same tax year. For 2013 the maximum amount increases to $6,500. A person age 50 or older as of December is authorized to make catch-up contributions up to $1,

13 Multiple Traditional IRAs It is permissible to make contributions to more than one IRA, but the $5,000/$6,000 limits applies to the combined contributions. Traditional and Roth Contributions May a person contribute to a traditional IRA and also a Roth IRA for the same year? Yes, but the person s aggregate traditional IRA and Roth IRA contributions are subject to the applicable contribution limit for such year. For example, if a contribution limit is $5,000, then the sum of the person s traditional IRA contributions and his or her Roth IRA contributions must be $5,000 or less. Traditional and Roth $5,000 or $6,000 NEW IRA CONTRIBUTION LIMITS FOR

14 Spousal IRA Limit NEW IRA CONTRIBUTION LIMITS FOR 2013 For 2009, 2010, 2011, and 2012 if a person files a joint return and his or her taxable compensation is less than that of his or her spouse, the most that can be contributed for the year to the IRA is the smaller of the following two amounts: 1. $5,000 ($6,000 if her or she is age 50 or older), or 2. The total compensation includible in the gross income of both spouses for the year, reduced by the following two amounts. a. The individual spouse s IRA contribution for the year to a traditional IRA b. Any contributions for the year to a Roth IRA on behalf of the individual s spouse. This means that the total combined contributions that can be made for the person s IRA and his or her IRA can be as much as $10,000 ($11,000 if only one spouse is age 50 or older or $12,000 if both are age 50 or older). 14

15 Spousal Contribution Exception Married NEW IRA CONTRIBUTION LIMITS FOR 2013 Contribution Eligibility and Contribution Limits Joint Tax Return Joint Earned Income Spouse with Lesser Income uses Joint Earned Income to determine eligibility 15

16 NEW IRA CONTRIBUTION LIMITS FOR 2013 Contribution Eligibility and Contribution Limits Example: Mary age 68, and John, age 73, are married. Mary has 2012 compensation of $28,000. John has $27,000 in compensation, for a total of $55,000. They are eligible for the following contributions. John Mary Traditional IRA $6,000 $6,000 Traditional IRA Roth IRA $6,000 $6,000 Traditional IRA Roth IRA $6,000 $6,000 Roth IRA Roth IRA $6,000 $6,000 Roth IRA 16

17 Contribution Deadline NEW IRA CONTRIBUTION LIMITS FOR 2013 Due date of Individual s Federal Income Tax Return without regard to extensions. Normally April 15th March 1 early filing date for Commercial Farmers and Fisherman Mailed contributions Making early contributions is not allowed. Example: In December of 2012, a person cannot make a contribution for Emancipation Day Impact 17

Contribution to QRP made by or for IRA")

18 NEW IRA CONTRIBUTION LIMITS FOR 2013 Traditional IRAs Annual Contributions - Deductible (Traditional IRA ONLY) Active Participation in Qualified Retirement Plan (QRP) Contribution to QRP made by or for IRA accountholder X 18

19 19 NEW IRA CONTRIBUTION LIMITS FOR 2013 Traditional IRAs Calculating the amount of the IRA contribution which cannot be deducted. The amount equal to or in excess of the AGI phase-out level. Non-deductible amount = $5,000 X MAGI- Threshold Level (or $6,000) $10,000 or $20,000 As applicable As applicable Deductible amount = $5,000 - Nondeductible amount (or $6,000) As applicable

20 NEW IRA CONTRIBUTION LIMITS FOR 2013 Traditional IRAs Income Restriction - Active Participants ONLY Year AGI Threshold Level AGI Phase-out Level Single 2008 $53,000 $63, $55,000 $65, $56,000 $66, $58,000 $68, $59,000 $69,000 Married, Joint Return 2008 $85,000 $105, $89,000 $109, $90,000 $110, $92,000 $112, $95,000 $115,000 Married, Separate Return 1997 to Present $0 $10,000 20

21 NEW IRA CONTRIBUTION LIMITS FOR 2013 Traditional IRAs Income Restriction - Non-Active Participant Spouse One Spouse Active Participant One Spouse NOT Active Participant Year AGI Threshold Level AGI Phaseout Level 2008 $159,000 $169, $166,000 $176, $167,000 $177, $169,000 $179, $173,000 $183, $178,000 $188,000 21

22 NEW IRA CONTRIBUTION LIMITS FOR 2013 Traditional IRAs Non-Deductible Contributions Traditional IRA - Some Important Roth Conversion change in 2010 Increases importance of non-deductible traditional IRA contributions Make non-deductible contributions and then convert = A Roth IRA contribution Example: Jane Smith has modified adjusted gross income of $190,000 for She participates in a 401(k) plan. She is ineligible to make an annual Roth contribution as her income exceeds the eligibility limits. Assuming she currently has no taxable dollars within a traditional, SEP or SIMPLE IRA, she may make a nondeductible contribution and then convert it. 22

23 NEW IRA CONTRIBUTION LIMITS FOR 2013 Contributions may be deductible and/or nondeductible. Individual bears responsibility to determine and administer. Form

24 24 NEW IRA CONTRIBUTION LIMITS FOR 2013 Savers Tax Credit Special/Additional Tax Benefit for Individuals with low or moderate incomes. Tax Credit = IRA Contributions x Applicable Percentage (Limited to $2,000)

25 Tax Credit for IRA Contributions NEW IRA CONTRIBUTION LIMITS FOR 2013 Income Limits-2012 Joint Return Over Not Over Adjusted Gross Income 2012 Head of Household Over Not Over All Others Over Not Over Credit % $0 $34,500 $0 $25,875 $0 $17,250 50% $34,500 $37,500 $28,875 $28,125 $17,250 $18,750 20% $37,500 $57,500 $28,125 $43,125 $18,750 $28,750 10% $57,500 $43,125 $28,750 0% 25

26 Tax Credit for IRA Contributions NEW IRA CONTRIBUTION LIMITS FOR 2013 Income Limits-2013 Joint Return Over Not Over Adjusted Gross Income 2013 Head of Household Over Not Over All Others Over Not Over Credit % $0 $35,500 $0 $26,625 $0 $17,750 50% $35,500 $38,500 $26,625 $28,875 $17,750 $19,250 20% $38,500 $59,000 $28,875 $44,250 $19,250 $29,500 10% $59,500 $44,250 $29,500 0% 26

27 27 NEW IRA CONTRIBUTION LIMITS FOR 2013 Savers Tax Credit Illustration # 1 Total Income $28,000 $28,000 <IRA Deduction> 0 $2,000 Adjusted Gross Income $28,000 $26,000 Std. Deductions & Exemptions $9,500 $9,500 Taxable Income $18,500 $16,500 Tax $2354 $2,054 IRA Credit 0 $200 Net Tax $2354 $1854 Other Taxes 0 0 Total Tax $2354 $1854 Less Withholding $ Owe/Refund $46 (Refund) $546 (Refund)

28 28 NEW IRA CONTRIBUTION LIMITS FOR 2013 Savers Tax Credit Illustration # 2 Total Income $35,000 $35,000 <IRA Deduction> 0 $2,000 Adjusted Gross Income $35,000 $33,000 Std. Deductions & Exemptions $9,500 $9,500 Taxable Income $25,500 $23,500 Tax $3404 $3,104 IRA Credit 0 <$200> Net Tax $3404 $2904 Other Taxes 0 0 Total Tax $3404 $2904 Less Withholding $ Owe/Refund $404 (Owe) $96 (Refund)

29 NEW IRA CONTRIBUTION LIMITS FOR 2013 To what extent is a person entitled to a tax credit for an IRA contribution? A formula is used to calculate the credit. Allowed credit = contribution (no more than $2,000) x applicable percentage. The credit may vary from $1 to $1,000, depending on the amount the person contributes to the IRA, his or her filing status and his or her modified adjusted gross income. If the following requirements are met for a given tax year, then this person will qualify for this credit. 1. Be at least 18 years of age as of December 31 of such year 2. Not a dependent on someone else s tax return 3. Not a student as defined in Internal Revenue Code section 25B(c) 4. Have adjusted gross income under certain limits, which are based on your filing status: Joint Filers $55, $56, $57, $59, Head of Household $41, $42, $43, $44, All other filers $27, $28, $28, $29, Must not have received certain distributions which disqualify the person from claiming the credit, or certain distributions which were made to his or her spouse. Because of the complexity of this credit, a person will want to review IRS Publication 590 for a complete explanation. 29

30 Rollovers and Transfers are exceptions to the general tax rule that a distribution is taxable. Rollovers Special rule grants non-taxation if certain rules are met Transfers A non-taxable transaction since a reportable distribution does not occur. Transfer Rollover Plan to Plan Plan to Person to Plan Direct Rollover Pension Plan to IRA 30

31 Trustee-to-Trustee Transfer A contractual right Not a legal or statutory right IRA Plan Agreement Discretion of IRA Custodian An IRS Administrative Creation No distribution is made to the accountholder or beneficiary, so it is not reportable for 1099-R and 5498 purposes. Difficulty - IRS has never in writing defined what must be done to have a transfer 31

32 Trustee-to-Trustee Transfer IRA custodians/trustees do not prepare 1099-R and 5498 forms Fee or not 32

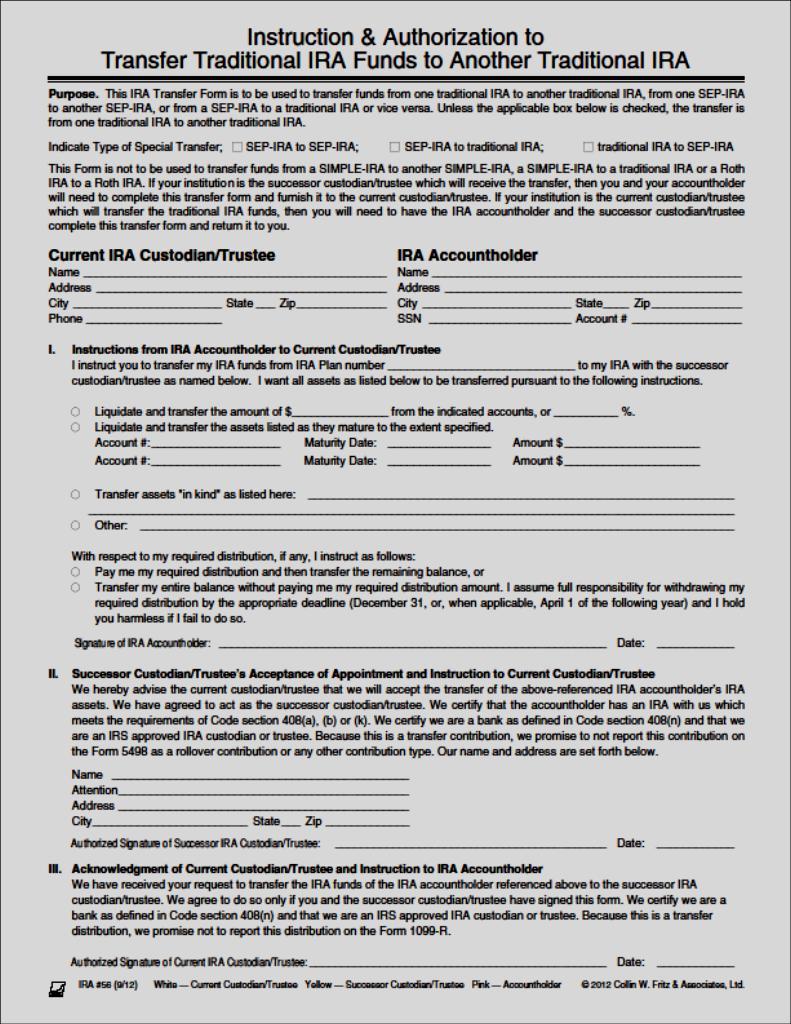

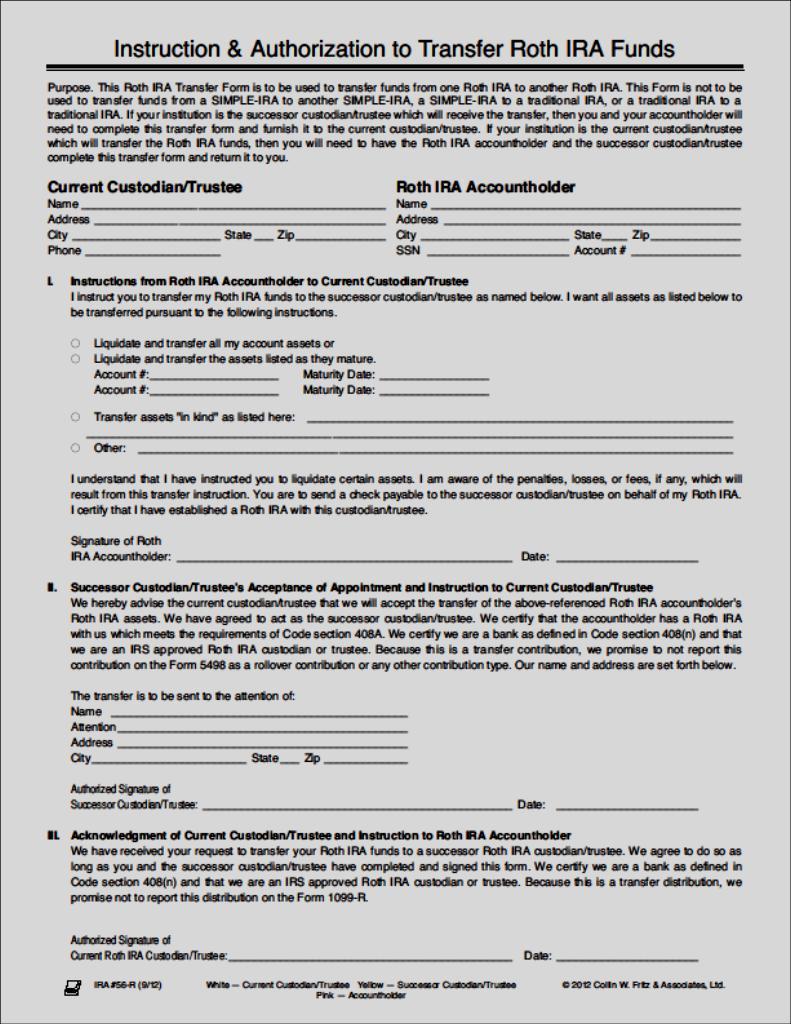

33 Trustee-to-Trustee Transfer Forms CWF Form # 56 CWF Form # 56-R 33

34 Purpose of Trustee to Trustee Transfer Move IRA Asset from one IRA to another, one IRA custodian/trustee to another IRA custodian trustee, on a Tax-Free Basis Requirements: Check/Draft/Wire made payable to new IRA custodian/trustee ABC Financial Institution as Custodian/Trustee for John Jones (Traditional, SEP, SIMPLE, Roth) IRA No IRS Limit Reasonable Custodian/Trustee restrictions allowed Not Reportable to IRS Federal Income Tax withholding rules do not apply 34

35 Purpose of Trustee to Trustee Transfer Trustee-to-Trustee Transfer Two types of transfers Non-reportable - No 1099-R or 5498 Reportable - A 1099-R or 5498 must be prepared 35

36 Purpose of Trustee to Trustee Transfer Trustee-to-Trustee Transfer Non-reportable Transfer must be from same type of IRA * Traditional IRA to Traditional IRA * Traditional IRA to SEP IRA * SEP IRA to SEP IRA * SEP IRA to Traditional IRA * Roth IRA to Roth IRA * SIMPLE IRA to SIMPLE IRA * SIMPLE IRA to Traditional IRA (SIMPLE 2 year Holding Period) 36

37 37 Purpose of Trustee to Trustee Transfer Trustee-to-Trustee Transfer - Reportable - Non-Like Kind 401(k) - Traditional IRA 401(k) - Roth IRA Traditional IRA - Roth IRA Recharacterizations Traditional IRA - HSA Traditional IRA - 401(k)

38 Requirements Purpose of Trustee to Trustee Transfer Required minimum distributions from traditional/sep/simple: May be transferred (Since 2002) Recommend noting RMD Note outgoing Follow-Up any incoming 38

39 Purpose of Trustee to Trustee Transfer Procedures Transfer documentation may be initiated either by the losing or gaining IRA Custodian. 39

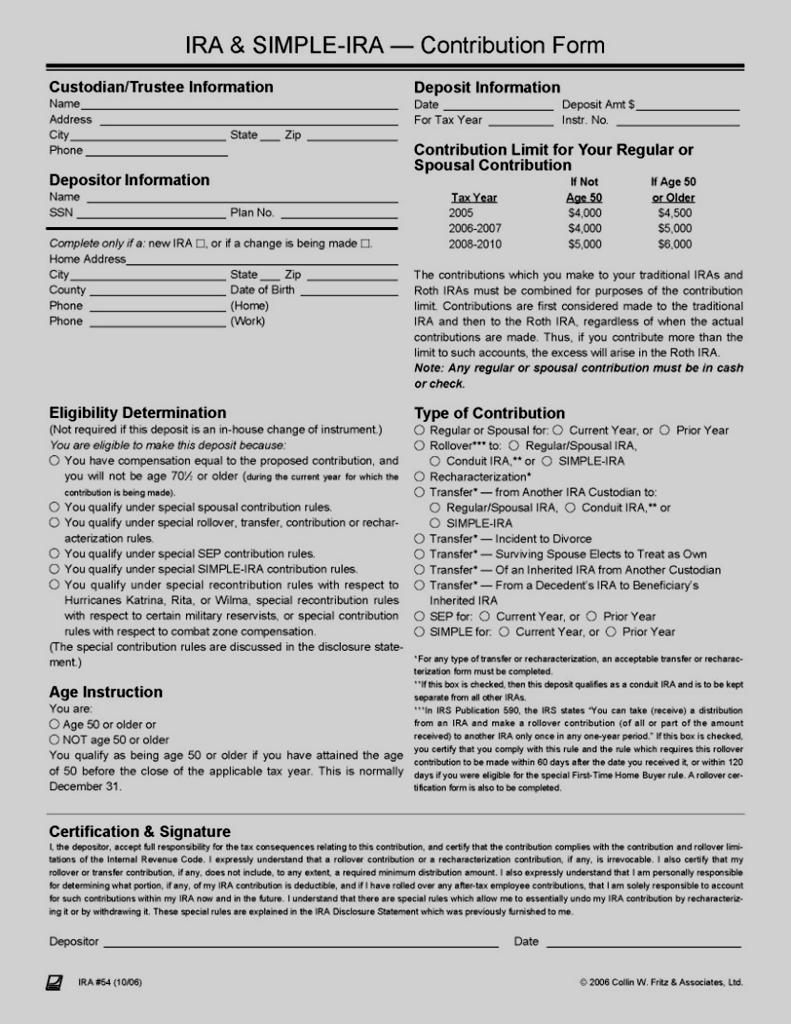

40 CWF Form # 54 Trustee-to-Trustee Transfer Forms CWF Form # 54-R Trustee-to-Trustee Transfer 40 40

41 Trustee-to-Trustee Transfer Procedures - New IRA Custodian/Trustee Request is sent to current IRA custodian/trustee Could be completed at current custodian/trustee but must be approved by New IRA custodian/trustee before sending IRA funds. Upon receipt of transfer amount, verify all information 41

42 Trustee-to-Trustee Transfer Procedures - New IRA Custodian/Trustee Note RMD status and setup follow-up if applicable Upon receipt of transfer request Verify all information Contact IRA owner Complete distribution form 42

43 Trustee-to-Trustee Transfer Forms CWF Form # 57 CWF Form # 57-R 43

44 Trustee-to-Trustee Transfer Procedures - Current IRA Custodian/Trustee Federal Income Tax withholding rules do NOT apply Issue check/draft/wire to new IRA custodian/trustee Note RMD status and amount Send check/draft directly to new IRA custodian/trustee do not give the check/draft to the new IRA owner Inherited IRAs Can Also Be Transferred Document carefully Caution: Be sure to indicate IRA and type of IRA, not just IRA Accountholder s name 44

45 CWF Form # 56-I Trustee-to-Trustee Transfer Inherited IRAs can be Transferred CWF Form # 56-RI 45

46 Trustee-to-Trustee Transfer IRAs and Divorces or Legal Separations IRAs can only be transferred to an ex-spouse s IRA Decree must be specific How, How much, When, etc. Have IRA s (former) owner complete distribution form CANNOT be done as a distribution and a rollover. -Court order may be needed to correct. 46

47 Trustee-to-Trustee Transfer CWF Form # 57 CWF Form # 57-R 47

48 ROLLOVERS INTO AN IRA May generate large Deposits Special administrative procedures apply since IRA plan agreement authorizes contributions larger than $5,000 or $6,000 only if the contribution is a SEP contribution, recharacterization or a qualifying rollover. Rollovers from employer plans Rollovers from another IRA 48

49 ROLLOVER STATISTICS Number of Taxpayers Rollover Amounts (1,000 s) Average ,636,027 $214,878,446 $59, ,754,759 $228,495,888 $60, , $281,976,971 $67, ,478,322 $316,646,832 $70, ,609,522 $272,104,973 $48,508 Total 21,628,770 $1,314,103,110 $60,757 Observations 1. Over the 5-year period, 1.3 trillion of assets were rolled into traditional IRAs from 401(k) plans, other pension plans, and other traditional IRAs. 2. The annual rollover amount is 263 billion on average 3. The average per person rollover amount is $60,757 over the 5-year period 4. The 2008 recession is again evident. A large increase in the number of persons making a rollover contribution and a substantial decrease ($48,508 on average) in the amount being rolled over. Very likely the difference was taken as a taxable distribution and used for current living expenses. 5. At this point the IRS is not reporting separately rollovers into Roth IRAs from other Roth IRAs. Now that funds can be rolled over into Roth IRAs from 401(k) plans one can expect that such rollovers will be reported in future statistical reports. 49

50 ROLLOVER STATISTICS End-of-Year Fair Market values for IRAs for The following charts show the fair market values for traditional IRAs, Roth IRAs, SEP-IRAs and SIMPLE- IRAs. These amounts do vary. They were certainly impacted by the economic recession of The annual percentages surprising stay quite constant: Traditional IRAs 88.5% SEP-IRAs 5.5% SIMPLE-IRAs 1.2% Roth IRAs 4.8% Total % The FMC charts below show that the FMV for all IRAs was 3.7 trillion as of December 31, The DOL reported this value as being 4.7 trillion as of December 31, 2010 as the economy and the markets did improve during End-of-Year Fair Market Value 2008 Number of Taxpayers FMV Amount Percent Traditional 43,054,097 $3,257,294, SEP 3,726,835 $201,497, SIMPLE 2,896,031 $45,634, Roth 15,951,065 $176,638, Total 65,628,028 $3,681,065, % 50

51 REPORTING OF IRA ROLLOVER CONTRIBUTIONS Forms 1040, 5329 and 8606 Forms 5498 and 1099-R 51

52 REPORTING OF IRA ROLLOVER CONTRIBUTIONS 52

53 REPORTING OF IRA ROLLOVER CONTRIBUTIONS 53

54 REPORTING OF IRA ROLLOVER CONTRIBUTIONS 54

55 REPORTING OF IRA ROLLOVER CONTRIBUTIONS X G From pension plans to an IRA 55

56 REPORTING OF IRA ROLLOVER CONTRIBUTIONS X or 7 X From an IRA to an IRA (traditional) 56

")

57 REPORTING OF IRA ROLLOVER CONTRIBUTIONS X Q, J or T From an IRA to an IRA (Roth) 57

58 REPORTING OF IRA ROLLOVER CONTRIBUTIONS 2012 Instructions for Form 5498 The IRS has created the Form 5498 and requires the IRA custodian to prepare and file it, because it will assist the IRS in determining if an individual has properly reflected on his or her federal income tax return the contributions he or she claims being made on his or her tax return. Rollover contributions are reported in box 2. IRA type is checked in box 7. 58

.")

59 REPORTING OF IRA ROLLOVER CONTRIBUTIONS 2012 Instructions for Form 5498 Note that the Form 5498, in addition to reporting contributions is used to report the IRA s fair market value as of December 31. Filing a Form 5409 is required for a person who is no longer eligible to make annual contributions (i.e. he or she must receive a RMD). The fact that an IRA is revoked or close under special account closure rules does not negate the requirement that the contribution be reported on the Form X 59

60 REPORTING OF IRA ROLLOVER CONTRIBUTIONS 2012 Instructions for Form 5498 The IRS can and will assess a penalty of $50 per form when a Form 5498 is prepared incorrectly, late or not at all. When must a Form 5498 be prepared? The individual has made one or more reportable contributions The FMV is greater than 0.00 as of December 31. That is, box 5 needs to be completed. Special rule for decedents. 60

61 REPORTING OF IRA ROLLOVER CONTRIBUTIONS 2012 Instructions for Form 5498 All IRA contributions are reportable, except true direct transfer contributions are not. The IRS instructions do not define the conditions which must be met to have a direct transfer. The IRS defines a direct transfer as occurring between the two IRA trustees and as 1. A Traditional IRA to a Traditional IRA or a SEP-IRA 2. A SEP-IRA to a SEP IRA or a Traditional IRA 3. A Simple-IRA to a SIMPLE-IRA 4. A Roth IRA to a Roth IRA 61

62 REPORTING OF IRA ROLLOVER CONTRIBUTIONS 2012 Instructions for Form 5498 Reportable IRA Contributions are annual contributions, recharacterizations, Roth conversions, rollovers, postponed contributions and repayments, and transfer contributions other than defined above. 62

63 IRA-to-IRA Rollovers Purpose Usually to move IRA assets from one IRA to another IRA Rollover can be brought back to the same IRA Requirements One rollover per IRA, per 12-month period (not per investment) IRA Assets must be deposited into IRA within 60 calendar days A required distribution is ineligible to be rolled over. Check/Draft/Wire is normally made payable to the IRA accountholder The same property must be rolled over. If property is distributed to you from an IRA and you complete the rollover by contributing property to an IRA, your rollover is tax-free only if the property you contribute is the same property that was distributed to you. You are unable to sell the property distributed and rollover the proceeds. A distribution from an inherited IRA to a non spouse beneficiary is ineligible to be rolled over. 63

64 IRA-to-IRA Rollovers General Rule: A rollover is one of the exceptions to the rule that a person will be taxed when he or she is paid the IRA assets. When the assets are properly rolled over, taxation will be delayed until a later taxable distribution occurs. The general rule is that only the IRA accountholder is eligible to roll over IRA assets that have been paid from his or her own IRA to another IRA. However, a surviving spouse beneficiary may roll over a distribution paid from a deceased spouse s IRA into their own IRA. A divorced IRA owner cannot roll over a distribution from his/her former spouse s IRA into his/her own IRA. 64

65 Must be same type of IRA: IRA-to-IRA Rollovers Traditional IRA to Traditional IRA Traditional IRA to SEP IRA SEP IRA to SEP IRA SEP IRA to Traditional IRA Roth IRA to Roth IRA Simple IRA to Simple IRA Simple IRA to Traditional IRA (SIMPLE 2 year Holding Period) 65

66 The Once Per Year Rule IRA-to-IRA Rollovers An IRA accountholder is authorized to take a distribution from his or her IRA and roll it over once per year. Although the statutory law could be read that a person with multiple IRA plan agreements is allowed to do only one rollover per year, the IRS has adopted the rule administratively that a person may do one rollover per year per plan agreement. A person who only has one plan agreement comprised of 5 different CDs is permitted to do only one rollover per year. In contrast, a person with 5 different IRA plan agreements, would be eligible to do a rollover within one year from each of the five plan agreements. 66

67 The Once Per Year Rule IRA-to-IRA Rollovers It is permissible for the IRA accountholder to make multiple Rollover contributions of the one IRA distribution. Example. John withdraws $15,000 from his IRA on March 20, He makes three $5,000 rollover contributions, one on April 2, one on April 18 th and one on May 10, The three rollover contributions are permissible since they relate to the one distribution. 67

68 IRA-to-IRA Rollovers The Once Per Year Rule Example # 1: A person who took a distribution April 20, 2011, and rolled it over within the 60 day limit, is eligible to rollover a subsequent distribution from the same IRA only if such distribution occurs on April 20, 2012 or later. Example # 2: A person is authorized to rollover one distribution in a one year period. A person who withdraws $3,000 on May 11 and then withdraws $15,000 on May 25 from the same IRA, will have to decide which of the two distributions to rollover since only one rollover per year is authorized. There is an exception for bank closure. An additional rollover is permitted. 68

69 Rollovers are reportable to the IRS Distributions on Form 1099-R Regular IRA reporting codes IRA-to-IRA Rollovers Rollover contributions on Form 5498 Box 2 69

70 IRA-to-IRA Rollovers Procedures - Current IRA Custodian/Trustee Complete distribution form as any other distribution Complete withholding documentation when applicable Check/Draft/Wire is made payable to or for the IRA accountholder Document and Report as any IRA distribution Regular IRA distribution codes 70

71 IRA-to-IRA Rollovers Complete distribution form as any other distribution CWF Form # 57 CWF Form # 57-R 71

72 IRA-to-IRA Rollovers Federal Income tax withholding rules apply to the distribution State Income tax withholding rules may also apply Traditional/SEP/SIMPLE IRA required minimum distributions (RMDs) CANNOT be rolled over 72

73 IRA-to-IRA Rollovers Procedures - Subsequent IRA Custodian/Trustee Could be current or new IRA custodian/trustee Proper IRA must be established to receive rollover Plan agreement, Disclosure statement, Financial disclosure with financial projection (when applicable), using the Rollover projection calculation Document irrevocable rollover election Document rollover contribution 73

74 IRA-to-IRA Rollovers Procedures - Subsequent IRA Custodian/Trustee Could be current or new IRA custodian/trustee Proper IRA must be established to receive rollover Plan Agreement, Disclosure Statement, Financial Disclosure with financial projection (when applicable), using the rollover projection calculation Document irrevocable rollover election 74

75 CWF Form # 65 IRA-to-IRA Rollovers Procedures - Subsequent IRA Custodian/Trustee CWF Form # 65-R2 75

76 IRA-to-IRA Rollovers Requirements Traditional/SEP/SIMPLE IRA required minimum distributions RMDs CANNOT be rolled over, must be satisfied first Rollover election must be irrevocable Document carefully Example: Lynn is age 74. She has established a periodic distribution where her RMD is paid to her checking account in November of each year. Her RMD for 2012 is $600. On March 20, 2012 she needs funds to pay her property taxes. She withdraws $1,500. She wants to rollover the entire $1,500. She may only Rollover $900. She will not need to take her November distribution. 76

77 IRA-to-IRA Rollovers CWF Form # 54 CWF Form # 54-R Rollover 77 77

78 Spouse Beneficiary Exception Inherited IRA distribution to spouse beneficiary is eligible for rollover to spouse beneficiary s own IRA less any RMD. Same 60-Day rule applies IRA-to-IRA Rollovers 78

79 IRA-to-IRA Rollovers Special Waiver to 60-Day Rule issued in writing by IRS Request Waiver from IRS IRA owner hardships beyond reasonable control Against equity, good conscience, casualty, disaster, death, disability, hospitalization, incarceration, foreign country restriction, or postal error Waiver must be requested and received by the IRA owner BEFORE completing rollover. IRA custodian/trustee should receive copy of approved waiver Report and document as any other rollover Note: Do not accept rollover without the IRS approved waiver. 79

80 Automatic Waiver by IRS No Special Waiver Required Custodian/Trustee error IRA-to-IRA Rollovers Must have received rollover assets timely As usual rollover documentation completed timely IRA timely established for rollover Must be within one year of distribution If bank error is not discovered and corrected within the one year time period, the IRS filing procedure would need to be used to correct the situation. 80

81 IRA-to-IRA Rollovers Failed Rollovers and Non-qualifying Rollover A failed rollover exists when the funds never went into an IRA. This means the distribution received by the accountholder or beneficiary is taxable. A non-qualifying rollover exists when the funds did not qualify to go into the IRA via a rollover. It is an excess contribution. The 6% tax will apply unless timely corrected. 81

82 Standard Rollover Rules Apply: Once per year 60 Day Rule No RMD rule Roth IRA-to- Roth IRA Rollovers 82

83 ROTH IRAS Special Rollover Rules Military Death Gratuities and Service members Group Life Insurance (SGLI) Payments Rollover of Exxon Valdez Settlement Income Rollover of Airline Payments 83

84 CWF #54-R Special Special Roth Rollover Forms Forms CWF #65-AP 84

85 Rolling Funds from a Traditional IRA to a Roth IRA Or Roth Conversion Contributions Discussed in Session # 2 85

86 Direct Rollovers to 401 (K) Plans from IRAs 86

87 Qualified Retirement Plan (QRP)-to-IRA Rollovers Purpose To move QRP assets to IRA on a Tax-Free Basis Requirements Employer/401(k) Administrator must furnish Section 402(f) Notice (401(k) Distribution form). Form must provide 3 options: 1. Direct Rollover Entire Balance 2. Be paid cash- 80% to individual - 20% withhold and paid to IRS for the IRS for the individual 3. Combination of Options 1 and 2. With option #2, the individual would be eligible to rollover the amount distributed. Cardinal Rule: Obtain a copy of the 402(f) Notice/Election Form 87

88 QRP-to-IRA Rollovers Traditional IRAs Rollover From Employer s Plan into a Traditional IRA A person can roll over into a Traditional IRA all or part of an eligible rollover distribution he or she receives from his or her (or his or her deceased spouse s): Employer s qualified pension, profit-sharing or stock bonus plan (including a 401(k) plan), Annuity plan, Tax-sheltered annuity plan (section 403(b) plan), or Governmental deferred compensation plan (section 457 plan). Cardinal Rule: Be furnished a copy of the form furnished the individual by the employer. 88

89 QRP-TO-IRA ROLLOVERS Direct Rollover or Rollover Qualified Retirement Plan (QRP)-to-Traditional or Roth IRA Requirements: Eligible pension, profit sharing, 401(k), certain tax-sheltered annuities, any employer sponsored qualified retirement plan. Eligible QRP distribution Does NOT include: QRP required minimum distribution Any distribution based on life expectancy of 10 years or more Substantially equal periodic payments based on schedule of 10 years or more Annuity payments over 10 years or more Hardship distribution Corrective distribution Employer 402(f) Notice required to clarify 60-Day Rule when applicable (waiver could apply). In-kind rollover allowed 89

90 QUALIFIED RETIREMENT PLAN (QRP)-TO-IRA ROLLOVERS Almost all QRP Distributions are Eligible to be Rolled Over (Direct), But some are not: QRP required minimum distribution Any distribution based on life expectancy of 10 years or more Substantially equal periodic payments based on schedule of 10 years or more Annuity payments over 10 years or more Hardship distributions Corrective distributions 90

-TO-IRA")

91 QUALIFIED RETIREMENT PLAN (QRP)-TO-IRA ROLLOVERS QP #857 91

92 QUALIFIED RETIREMENT PLAN (QRP)-TO-IRA ROLLOVERS QRP-to-IRA Direct Rollover Send Direct Rollover Request to QRP Administrator Upon Receipt of Direct Rollover Asset Document irrevocable rollover election Document rollover contribution Report as any other rollover 92

93 QRP-TO-IRA DIRECT ROLLOVER Complete Direct Rollover Request QRP s form or IRA custodian s/trustee s form QRP-to-IRA Direct Rollover CWF Form #

94 QUALIFIED RETIREMENT PLAN (QRP)-TO-IRA ROLLOVERS QRP-to-IRA Direct Rollover Establish Traditional IRA Determine if Conduit IRA is required May be needed for certain QRP tax benefits If needed, establish separate Traditional IRA If not, document with waiver CWF Form # 65-W 94

95 IRA-to-IRA Rollover 401(k) Illustration # 1 Jane Doe Amount Subject to income tax $3,500 Amount Subject to SS & Medicare tax $4,000 $4,000 per month $ (k) deferral (Std) Will be taxable when distributed $3, (k) Net Illustration Amount # 2 John Doe Amount Subject to income tax $2,900 Amount Subject to SS & Medicare tax $3,000 $3,000 per month $ (k) deferral (Std) Will be taxable when distributed $ 300 Designated Roth deferred Will not be taxable when distributed $2,600 Net Amount 95

96 QRP- to-ira Rollovers QRP-to-Traditional or Roth IRA» Direct Rollover- Directly to the IRA No Distribution No Distribution No Distribution 96

97 QRP- TO-IRA ROLLOVERS Roth QRP-to-Traditional or Roth IRA» Distribution, and then Rollover.» Not a Direct Rollover» QRP Distribution to QRP Participant/IRA Accountholder» IRA Rollover Contribution Traditional or Roth IRA 97

98 QRP- TO-IRA ROLLOVERS IRA Rollovers and Direct Rollovers» Eligible Retirement Plan to Roth IRA Conversion» Since 2008 other retirement accounts can be converted directly to a Roth IRA» This includes inheriting beneficiary or ERP QRP Direct Rollover / Conversion Roth IRA (Inherited) QRP (Direct) Rollover / Conversion Non-Spouse Beneficiary Inherited Roth IRA 98

99 QUALIFIED RETIREMENT PLAN (QRP)-TO-IRA ROLLOVERS Rolling over after-tax dollars to a Roth IRA: Situation: The bank has been sent two checks on behalf of a participant of a 401(k) plan or other employer sponsored plan. The term 401(k) plan will be used for purposes of this article. One check is for the participant s taxable share of his or her account balance and the other check is for the individual s after-tax contributions. He or she wants to put the after-tax funds directly into a Roth IRA. Do laws/rules permit this? Most likely not. The IRS will argue a pro-rata distribution rule applies. Direct Rollovers from 401(k) plans to Roth IRAs- IRS Guidance Sought by CWF. See November 2010 Newsletter. 99

100 QUALIFIED RETIREMENT PLAN (QRP)-TO-IRA ROLLOVERS Employer/ 401(k) Administrator must determine and inform the individual if the distribution is eligible to be rolled over. Obtain a copy of the 401(k) distribution form. 100

101 QUALIFIED RETIREMENT PLAN (QRP)-TO-IRA ROLLOVERS QRP Rollovers due to a Divorce or Legal Separation QDRO: Ex-Spouse, in general, is now treated as if he or she was a participant of the 401(k) plan. Must be done as a reportable distribution and reportable rollover Can be done as a reportable Direct Rollover CAN NOT be done as a transfer 101

102 QUALIFIED RETIREMENT PLAN (QRP)-TO-IRA ROLLOVERS Automatic Direct Rollover Effective since March 28, 2005 Applies to mandatory distributions for separating/separated QRP participant Only amounts $1, to $5,000 apply QRP must be amended to allow (Employer s Option) Only applies when participant fails to timely respond to QRP options 102

103 Automatic Direct Rollover Must be directly rollover over to a Traditional IRA or IRA Annuity Employer/Plan Administrator selects willing IRA Custodian/Trustee Custodian/Trustee Option Written agreement is required Terms, conditions, and procedures must be spelled out Employer/Representative establishes IRA on behalf of participant IRA Custodian/Trustee documents and discloses to IRA Accountholder IRA Custodian/Trustee administers IRA as usual IRA investment must preserve principal Interest does not need to be guaranteed QUALIFIED RETIREMENT PLAN (QRP)-TO-IRA ROLLOVERS Custodian/Trustee fees and penalties must be comparable to similar accounts IRA Custodian/Trustee can also be the Employer/Plan Administrator 103

104 CWF Form # 80 Automatic Rollover Agreement 104

105 IRA Rollovers and Direct Rollovers Qualified Retirement Plan (QRP)-to-IRA Rollovers QRP-to-IRA Distribution/Rollover Procedures IRA Custodian/Trustee Upon Receipt of QRP Check/Draft/Wire Establish Traditional IRA Determine if Conduit IRA is required Document irrevocable rollover election Document rollover contribution Report as any other rollover 20% Federal Income Tax Withholding can be deposited separately (Same 60 Day Period) QRP-TO-IRA ROLLOVERS Example: The participant takes a distribution of $100,000 from his QRP on June 15, % or $20,000 is withheld for the MANDATORY Federal Income Tax. He rolls over the remaining $80,000 on August 1, By August 14, 2009, he can roll over up to $20,000 into his IRA, replacing the Federal Withholding. 105

106 QRP-TO-IRA ROLLOVERS IRA Rollovers and Direct Rollovers»Eligible Retirement Plan to Roth IRA Conversion» Since 2008 other retirement accounts can be converted directly to a Roth IRA» This includes inheriting beneficiary or ERP QRP Direct Rollover / Conversion Roth IRA (Inherited) QRP (Direct) Rollover / Conversion Non-Spouse Beneficiary Inherited Roth IRA 106

107 QRP-TO-IRA ROLLOVERS QRP-to-Traditional or Roth IRA» Direct Rollover- Directly to the Inherited IRA of a non-spouse beneficiary No Distribution Inherited Traditional IRA No Distribution Inherited Roth IRA No Distribution Inherited Roth IRA 107

108 QRP-TO-IRA ROLLOVERS Cannot Be Done This Way Beneficiary Beneficiary Inherited Traditional IRA Roth Inherited Roth IRA Beneficiary Inherited Roth IRA QRP-to-Traditional or Roth IRA Distribution, and then Rollover Not a Direct Rollover QRP Distribution to QRP Participant/IRA Accountholder IRA Rollover Contribution Traditional or Roth IRA 108

109 QRP-TO-IRA ROLLOVERS QRP Rollover to Roth IRAs Designated Roth Accounts Only Generally same rules and procedures as for rollover to traditional IRAs 109

110 ROLLOVER FROM EMPLOYER S PLAN INTO A ROTH IRA A person can roll over into a Roth IRA all or part of an eligible rollover distribution he or she receives from his or her (or his or her deceased spouse s): Employer s qualified pension, profit-sharing or stock bonus plan (including a 401(k) plan), Annuity plan, Tax-sheltered annuity plan (section 403(b) plan), or Governmental deferred compensation plan (section 457 plan). Cardinal Rule - Be Furnished a copy of the Form Furnished the Individual By the Employer 110

111 Special Administrative Topics New Types of Inherited IRAs Directly Rolling Over Standard Inherited 401(k) The law was changed as of January 1, 2007, to allow a non-spouse beneficiary of a pension plan participant to directly roll over the inherited funds into a new type of inherited IRA. The individual/beneficiary is the required to take required distributions from the inherited IRA. This form is used by the individual/beneficiary to instruct how and when distributions will be taken and what method will be used. Normally an individual/beneficiary would directly roll over standard pension funds into an inherited traditional IRA. Inherited IRA Accountholder s Distribution Instruction and Certification to Comply with RMD rules, CWF IRA #

112 CWF Form 205 Inherited IRA Accountholder s Distribution Instruction and Certification to Comply with RMD Rules 112

113 Inherited IRAs for Non-Spouse Beneficiaries Special Administrative Topics New Types of Inherited IRAs Directly Rolling Over Inherited Designated Roth Funds from 401(k) The law was changed as of January 1, 2007, to allow a non-spouse beneficiary of a pension plan participant to directly roll over the inherited Designated Roth funds into a new type of inherited Roth IRA. The individual/beneficiary is required to take required distributions from the inherited Roth IRA. This form is used by individual/beneficiary to instruct how and when distributions will be taken and what method will be used. Inherited IRA Accountholder s Distribution Instruction and Certification to Comply with RMD rules, CWF IRA # 205R. 113

114 CWF Form 205R Inherited Roth IRA Accountholder s Distribution Instruction and Certification to Comply with RMD Rules 114

115 IRA Contributions IRA Contributions 115

116 Fraudulent Rollovers and other Contributions Do Occur Protect Your Institution A financial institution acting as an IRA custodian wants to have procedures in place restricting an IRA accountholders right to withdraw IRA funds if he or she has opened a new IRA by either making a rollover contribution or a transfer contribution. The check must clear or be settled before the IRA accountholder is allowed to take a distribution, including a distribution paid when a person revokes his or her IRA. Fraudulent transactions are occurring with respect to purported rollover contributions. For example, an individual makes a rollover contribution of $30,000 on Monday by endorsing a check issued by a non-existent company either to the individual or the financial institution. On Thursday, the individual comes into the financial institution and withdraws the $30,000. The individual sometimes will instruct to have 10% or 20%, of federal income tax withheld from the IRA which revokes/closes the IRA. For purposes of this article, we will assume the individual instructed to have 15% withheld ($30,000 x 15%) or $4,500. Some time the following week, it is determined the rollover check was fraudulent. The IRS has issued little guidance as to how the IRA custodian is to report the fraudulent IRA contribution of $30,000 and the related distributions and the interplay between the revocation rule and the Truth in Savings Rules. The contribution is not to be reported as a rollover contribution on the Form 5498 since there was no distribution from a qualifying pension plan or IRA. The contribution of $30,000 would need to be reported in box 1 of Form This contribution is an excess contribution, but the withdrawal does serve to correct the excess contribution. The IRA Custodian remitted the $4,500 of withholding to the IRS soon after the individual took the $30,000 distribution. Although we could not get an IRS representative to confirm it, the IRA custodian should be able to get its $4,500 returned by off-setting its $4,500 payment against a future tax withholding payment. Withholding only applies to a distribution it is subject to being taxed; this distribution is not, since it was the withdrawal of an excess contribution. 116

117 This concludes session # 1 of the Intermediate/Advanced IRA Training Webinar. We thank you for attending. If you have call any us questions at regarding or the send subjects an covered to in this webinar please feel free to jmcarlson@pension-specialists.com or visit us on the Internet at Copyright 2012 Collin W. Fritz & Associates, Ltd. The Pension Specialists

Session # 1 Establishing and Contributing

11/15/2018 Session # 1 Establishing and Contributing We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly 8:30 am CST or 12:30

11/15/2018 Session # 1 Establishing and Contributing We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly 8:30 am CST or 12:30

The Webinar will be starting shortly

7/11/2018 The Webinar will be starting shortly 8:45 am CST or 1:00 pm CST Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may

7/11/2018 The Webinar will be starting shortly 8:45 am CST or 1:00 pm CST Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may

Inherited Traditional IRAs for Non-Spouse Beneficiaries.

Rev2/15/2018 Inherited Traditional IRAs for Non-Spouse Beneficiaries. We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly. 8:30

Rev2/15/2018 Inherited Traditional IRAs for Non-Spouse Beneficiaries. We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly. 8:30

IRA Contribution Limits for 2018 Unchanged at $5,500 and $6,500; 401(k) Limits Do Change

Limits Do Change") Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

No Form 1099-R Prepared to Report IRA Funds Moving From the Decedent s IRA to an Inherited IRA

Published Since 1984 2015 Tax Filing Deadline is April 18, 2016 ALSO IN THIS ISSUE 2015 Form 5500 Series Returns Should Not Answer the Compliance Questions, Page 2 Inherited IRA Situation - Daughter Dies,

Published Since 1984 2015 Tax Filing Deadline is April 18, 2016 ALSO IN THIS ISSUE 2015 Form 5500 Series Returns Should Not Answer the Compliance Questions, Page 2 Inherited IRA Situation - Daughter Dies,

The Webinar will be starting shortly

Rev. 5/2/2018 The Webinar will be starting shortly 8:30 am CST or 12:30 pm CST We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar Copyright 2018 Collin W. Fritz &

Rev. 5/2/2018 The Webinar will be starting shortly 8:30 am CST or 12:30 pm CST We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar Copyright 2018 Collin W. Fritz &

IRS Issues 2014 IRA/Pension Limits. IRA Contribution Limits for 2014 Unchanged at $5,500 and $6,500 ALSO IN THIS ISSUE

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Deductibility Charts 2013 and 2014, Page 2 Roth IRA Contribution Charts for 2013 and 2014, Page 3 SEP and SIMPLE Limits, Page 3 Saver s Credit Limits

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Deductibility Charts 2013 and 2014, Page 2 Roth IRA Contribution Charts for 2013 and 2014, Page 3 SEP and SIMPLE Limits, Page 3 Saver s Credit Limits

IRS Issues 2013 COLAs. New IRA Contribution Limits for 2013 $5,500 and $6,500 ALSO IN THIS ISSUE

Published Since 1984 ALSO IN THIS ISSUE New IRA Contribution Limits for 2013 $5,500 and $6,500 IRA Contribution Deductibility Charts for 2012 and 2013, Page 2 Roth IRA Contribution Charts for 2012 and

Published Since 1984 ALSO IN THIS ISSUE New IRA Contribution Limits for 2013 $5,500 and $6,500 IRA Contribution Deductibility Charts for 2012 and 2013, Page 2 Roth IRA Contribution Charts for 2012 and

A Person s 2015 Tax Filing Deadline Is Either April 18, 2016 or April 19, 2016

Published Since 1984 ALSO IN THIS ISSUE IRS Adopts Permanent Penalty Relief Program for Sponsors of One Person Plans Who Failed to File One or More 5500-EZ Forms, Including For a Terminated Plan, Page

Published Since 1984 ALSO IN THIS ISSUE IRS Adopts Permanent Penalty Relief Program for Sponsors of One Person Plans Who Failed to File One or More 5500-EZ Forms, Including For a Terminated Plan, Page

Are IRA Amendments Required For ?

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

Establishing a SEP for 2014

Published Since 1984 ALSO IN THIS ISSUE Understanding Box 2 (Rollover Contributions) on the 2014 Form 5498, Page 2 Administering An HSA After the HSA Owner Dies, Page 4 Email Guidance - No Authority Exists

Published Since 1984 ALSO IN THIS ISSUE Understanding Box 2 (Rollover Contributions) on the 2014 Form 5498, Page 2 Administering An HSA After the HSA Owner Dies, Page 4 Email Guidance - No Authority Exists

Addendum to the Traditional IRA Custodial Agreement and Disclosures

Effective January 1, 2018 Addendum to the Traditional IRA Custodial Agreement and Disclosures This Addendum changes the Traditional IRA Custodial Agreement and Disclosures ( Agreement ) document and uses

Effective January 1, 2018 Addendum to the Traditional IRA Custodial Agreement and Disclosures This Addendum changes the Traditional IRA Custodial Agreement and Disclosures ( Agreement ) document and uses

(PLEASE READ THE ATTACHED INSTRUCTIONS) SEP Traditional IRA Simple. Death. Disability (Physician s statement or Disability Letter from IRS required)

SEP Traditional IRA Simple. Death. Disability (Physician s statement or Disability Letter from IRS required)") IRA DISTRIBUTION REQUEST (PLEASE READ THE ATTACHED INSTRUCTIONS) SEP Traditional IRA Simple I. Account Holder s Information (Complete all sections) Name (please print): Account Number: Social Security

IRA DISTRIBUTION REQUEST (PLEASE READ THE ATTACHED INSTRUCTIONS) SEP Traditional IRA Simple I. Account Holder s Information (Complete all sections) Name (please print): Account Number: Social Security

Recent Changes to IRAs

Recent Changes to IRAs Federal legislation and new IRS regulations have created several changes to IRAs in the past year. Prohibition on recharacterization of IRA conversions: Effective for taxable years

Recent Changes to IRAs Federal legislation and new IRS regulations have created several changes to IRAs in the past year. Prohibition on recharacterization of IRA conversions: Effective for taxable years

is a qualified Hurricane Katrina distribution.

September 2005 Published Since 1984 ALSO IN THIS ISSUE IRA Disclaimers New IRS Guidance, Page 3 Modified Adjusted Gross Income (MAGI) for Roth IRA Contribution Purposes, Page 4 Tax Treatment of HSA Upon

September 2005 Published Since 1984 ALSO IN THIS ISSUE IRA Disclaimers New IRS Guidance, Page 3 Modified Adjusted Gross Income (MAGI) for Roth IRA Contribution Purposes, Page 4 Tax Treatment of HSA Upon

Roth IRAs The Roth IRA

Roth IRAs The Roth IRA 2017 and 2018 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

Roth IRAs The Roth IRA 2017 and 2018 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

SPJST ROTH INDIVIDUAL RETIREMENT ANNUITY DISCLOSURE STATEMENT

SPJST ROTH INDIVIDUAL RETIREMENT ANNUITY DISCLOSURE STATEMENT This disclosure statement explains the rules governing a Roth IRA. The term IRA will be used in this disclosure statement to refer to a Roth

SPJST ROTH INDIVIDUAL RETIREMENT ANNUITY DISCLOSURE STATEMENT This disclosure statement explains the rules governing a Roth IRA. The term IRA will be used in this disclosure statement to refer to a Roth

QCD Season and RMD Season. Moving Nondeductible Funds from a 401(k) into a Roth IRA ALSO IN THIS ISSUE

into a Roth IRA ALSO IN THIS ISSUE") Published Since 1984 ALSO IN THIS ISSUE IRAs and Bankruptcy and a Strict Reading of the Prohibited Transaction Rules, Page 2 Can SEP Contributions be Deposited into a Traditional IRA?, Page 3 2011 Rollover

Published Since 1984 ALSO IN THIS ISSUE IRAs and Bankruptcy and a Strict Reading of the Prohibited Transaction Rules, Page 2 Can SEP Contributions be Deposited into a Traditional IRA?, Page 3 2011 Rollover

President Obama Signs the Budget/Tax Bill on December 18, 2015.

Published Since 1984 ALSO IN THIS ISSUE IRA Custodian s Duty to File Corrected Form 1099-Rs Will Change, Page 2 IRA Amendments Being Required For 2015-2016, Page 3 February 1, 2016 Deadline, Page 4 Basic

Published Since 1984 ALSO IN THIS ISSUE IRA Custodian s Duty to File Corrected Form 1099-Rs Will Change, Page 2 IRA Amendments Being Required For 2015-2016, Page 3 February 1, 2016 Deadline, Page 4 Basic

Traditional Individual Retirement Account Disclosure Statement and Custodial Agreement

Traditional Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Page 1 of 26 Table of Contents Section I: Disclosure Statement A. Introduction... B. Contributions

Traditional Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Page 1 of 26 Table of Contents Section I: Disclosure Statement A. Introduction... B. Contributions

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 544260 (Rev 17-06/17) Page 1 of 25 Table of Contents Section I: Disclosure Statement A. Introduction...

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 544260 (Rev 17-06/17) Page 1 of 25 Table of Contents Section I: Disclosure Statement A. Introduction...

President Obama Proposes Radical IRA/Pension Law Changes

Published Since 1984 ALSO IN THIS ISSUE Caution Tax Software Giving People the Wrong Idea About Making a Non-deductible IRA Contribution and Then Converting it, Page 2 Understanding the Impact of Emancipation

Published Since 1984 ALSO IN THIS ISSUE Caution Tax Software Giving People the Wrong Idea About Making a Non-deductible IRA Contribution and Then Converting it, Page 2 Understanding the Impact of Emancipation

ALSO IN THIS ISSUE. There are two new exceptions. The IRS has issued Notice to issue temporary guidance until the IRS issues

Published Since 1984 ALSO IN THIS ISSUE January 31, 2017 Deadlines Page 3 Establishing a SEP Page 4 Important Form 1099-R Rules For An IRA Custodian To Follow and Observations Page 5 Deadline for 2016

Published Since 1984 ALSO IN THIS ISSUE January 31, 2017 Deadlines Page 3 Establishing a SEP Page 4 Important Form 1099-R Rules For An IRA Custodian To Follow and Observations Page 5 Deadline for 2016

Obama Administration Again Proposes Taxing Some Roth IRA Distributions And Other Law Changes

Published Since 1984 ALSO IN THIS ISSUE IRS Increases Filing Fees For Waiver of 60-Day Rollover Rule to $10,000, Page 3 Maximizing Contributions to a Roth IRA, Page 4 Types of IRAs Versus Types of IRA

Published Since 1984 ALSO IN THIS ISSUE IRS Increases Filing Fees For Waiver of 60-Day Rollover Rule to $10,000, Page 3 Maximizing Contributions to a Roth IRA, Page 4 Types of IRAs Versus Types of IRA

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement

Wells Fargo Clearing Services, LLC Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Table of Contents Section I: Disclosure Statement A. Introduction...3

Wells Fargo Clearing Services, LLC Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Table of Contents Section I: Disclosure Statement A. Introduction...3

Street Address. City, State, ZIP

ROTH IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address IRA Owner

ROTH IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address IRA Owner

TRADITIONAL IRA DISCLOSURE STATMENT

TRADITIONAL IRA DISCLOSURE STATMENT The Traditional Individual Retirement Account ( Traditional IRA ) presented with this Disclosure Statement is a retirement plan made available to individuals. An individual

TRADITIONAL IRA DISCLOSURE STATMENT The Traditional Individual Retirement Account ( Traditional IRA ) presented with this Disclosure Statement is a retirement plan made available to individuals. An individual

/ / + Outstanding Rollovers, I. Account Holder s Information (Complete all sections) 2.) Subsequent Years. II. IRA Holder Life Expectancy

2.) Subsequent Years. II. IRA Holder Life Expectancy") Fax to: 646-459-2749 Scan and e-mail to : Maintenance@SogoTrade.com REQUIRED MINIMUM DISTRIBUTION (RMD) (PLEASE READ THE ATTACHED INSTRUCTIONS) I. Account Holder s Information (Complete all sections) Name

Fax to: 646-459-2749 Scan and e-mail to : Maintenance@SogoTrade.com REQUIRED MINIMUM DISTRIBUTION (RMD) (PLEASE READ THE ATTACHED INSTRUCTIONS) I. Account Holder s Information (Complete all sections) Name

No Direct Rollovers From One to Another IRA

Published Since 1984 ALSO IN THIS ISSUE More Than a Check is Needed for an IRA Transfer, Page 2 BE CAREFUL The RMD Must be Completed Before Any Roth IRA Conversion, Page 3 IRA Contribution Due Dates, Page

Published Since 1984 ALSO IN THIS ISSUE More Than a Check is Needed for an IRA Transfer, Page 2 BE CAREFUL The RMD Must be Completed Before Any Roth IRA Conversion, Page 3 IRA Contribution Due Dates, Page

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

IRA Contribution Limits for 2019 $6,000 and $7,000

Published Since 1984 ALSO IN THIS ISSUE IRA Contributions for 2019 Page 1 IRA Contribution Deductibility Charts for 2018 and 2019 Page 2 Roth IRA Contribution Charts for 2018 and 2019 Page 3 SEP and Simple

Published Since 1984 ALSO IN THIS ISSUE IRA Contributions for 2019 Page 1 IRA Contribution Deductibility Charts for 2018 and 2019 Page 2 Roth IRA Contribution Charts for 2018 and 2019 Page 3 SEP and Simple

Three Planning Concepts Why More Individuals Will Want Profit Sharing or One Person 401(k) Plans!

Plans!") Published Since 1984 ALSO IN THIS ISSUE Preparing Two 1099-R Forms is Never Correct When There is Federal Withholding, Page 2 Possible Expansion of the Saver Tax Credit, Page 3 H&H Block Lawsuit Settlement

Published Since 1984 ALSO IN THIS ISSUE Preparing Two 1099-R Forms is Never Correct When There is Federal Withholding, Page 2 Possible Expansion of the Saver Tax Credit, Page 3 H&H Block Lawsuit Settlement

A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA

Rev 7/11/2018 A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting

Rev 7/11/2018 A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

ROTH IRA DISCLOSURE STATMENT

ROTH IRA DISCLOSURE STATMENT The Roth Individual Retirement Account ( Roth IRA ) presented with this Disclosure Statement is a retirement plan made available to individuals. An individual who establishes

ROTH IRA DISCLOSURE STATMENT The Roth Individual Retirement Account ( Roth IRA ) presented with this Disclosure Statement is a retirement plan made available to individuals. An individual who establishes

RECAP FOR COMPLETING THE 2002 FORM 1099-R ALSO IN THIS ISSUE DEADLINE FOR RMD NOTICE REMAINS JANUARY 31, Take note of this...

Published Since 1984 ALSO IN THIS ISSUE RECAP FOR COMPLETING THE 2002 FORM 1099-R QP Communication From the IRS, Page 3 Additional Thoughts on RMD Rules, Page 6 Higher Income Limits for 2003, Page 7 IRS

Published Since 1984 ALSO IN THIS ISSUE RECAP FOR COMPLETING THE 2002 FORM 1099-R QP Communication From the IRS, Page 3 Additional Thoughts on RMD Rules, Page 6 Higher Income Limits for 2003, Page 7 IRS

TRADITIONAL IRA DISCLOSURE STATEMENT

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

IRA Limits for 2010 & 2011

Published Since 1984 ALSO IN THIS ISSUE Review of IRA Contributions Eligibility Rules, Page 2 Is an RMD Due for 2011?, Page 2 IRA Contribution Deductibility Charts, Page 3 Roth IRA Contribution Charts,

Published Since 1984 ALSO IN THIS ISSUE Review of IRA Contributions Eligibility Rules, Page 2 Is an RMD Due for 2011?, Page 2 IRA Contribution Deductibility Charts, Page 3 Roth IRA Contribution Charts,

The Audio portion of this presentation is available either by phone or by using the speakers and microphone on your PC.

6-23-2010 1 2 The Audio portion of this presentation is available either by phone or by using the speakers and microphone on your PC. The phone number is provided to you in the confirmation from CWF and

6-23-2010 1 2 The Audio portion of this presentation is available either by phone or by using the speakers and microphone on your PC. The phone number is provided to you in the confirmation from CWF and

Arkansas Bankers Trust School IRA Update May 16, 2018

Arkansas Bankers Trust School IRA Update May 16, 2018 Presented by: 1 Patrice Konarik Sunwest Training Corp. Kendalia, TX www.sunwesttraining.com patrice@sunwesttraining.com 830.336.3422 2 Trust School

Arkansas Bankers Trust School IRA Update May 16, 2018 Presented by: 1 Patrice Konarik Sunwest Training Corp. Kendalia, TX www.sunwesttraining.com patrice@sunwesttraining.com 830.336.3422 2 Trust School

Traditional IRAs. Understanding Required Distributions at 70 1 / 2. Questions & Answers

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

BNY MELLON INVESTMENT SERVICING TRUST COMPANY. Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement

Disclosure Statement") BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

Traditional Individual Retirement Account (Trust) Disclosure Statement

Disclosure Statement") Traditional Individual Retirement Account (Trust) Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described

Traditional Individual Retirement Account (Trust) Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described

Street Address. PRIMARY Beneficiary(ies) % Column MUST total 100% % Name Mailing Address Relationship Birth Date SS #

% Column MUST total 100% % Name Mailing Address Relationship Birth Date SS #") TRADITIONAL IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address

TRADITIONAL IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address

Single HDHP $3,400 $3,450 Family HDHP $6,750 $6, Single HDHP $4,400 $4,450 Family HDHP $7,750 $7,900

Published Since 1984 ALSO IN THIS ISSUE IRS Issues 2018 Indexed Amounts for HSAs Page 1 RMD Box 11 on Form 5498 Is Not Checked for an IRA Beneficiary Page 2 Completing the 2016 Form 5498-A Page 3 Email

Published Since 1984 ALSO IN THIS ISSUE IRS Issues 2018 Indexed Amounts for HSAs Page 1 RMD Box 11 on Form 5498 Is Not Checked for an IRA Beneficiary Page 2 Completing the 2016 Form 5498-A Page 3 Email

Roth Individual Retirement Account (Trust) Disclosure Statement

Disclosure Statement") Roth Individual Retirement Account (Trust) Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described in

Roth Individual Retirement Account (Trust) Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described in

Traditional IRA SEP IRA Roth IRA. Disclosure Statement & Custodial Account Agreement

Traditional IRA SEP IRA Roth IRA Disclosure Statement & Custodial Account Agreement Table of Contents Page in Document PART I COMBINED DISCLOSURE STATEMENT AND CUSTODIAL ACCOUNT AGREEMENT... 1 TRADITIONAL

Traditional IRA SEP IRA Roth IRA Disclosure Statement & Custodial Account Agreement Table of Contents Page in Document PART I COMBINED DISCLOSURE STATEMENT AND CUSTODIAL ACCOUNT AGREEMENT... 1 TRADITIONAL

Traditional SEP, and SIMPLE IRAs

Traditional SEP, and SIMPLE IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why must I and others age 70 1/2 or older have to take a required distribution? The purpose of an IRA

Traditional SEP, and SIMPLE IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why must I and others age 70 1/2 or older have to take a required distribution? The purpose of an IRA

IRA AND EDUCATION SAVINGS. Retirement and Education Savings Accounts. TRADITIONAL IRAs Who is Eligible for a Traditional IRA?

Retirement and Education Savings Accounts This booklet is designed to highlight traditional individual retirement accounts (IRAs), Roth IRAs, and Coverdell Education Savings Accounts (CESAs). It is not

Retirement and Education Savings Accounts This booklet is designed to highlight traditional individual retirement accounts (IRAs), Roth IRAs, and Coverdell Education Savings Accounts (CESAs). It is not

AMERUS LIFE INSURANCE COMPANY

AMERUS LIFE INSURANCE COMPANY IRA DISCLOSURE STATEMENT INTRODUCTION This Individual Retirement Annuity ("IRA") is an annuity contract issued by AmerUs Life Insurance Company ("AMERUS") to fund an individual's

AMERUS LIFE INSURANCE COMPANY IRA DISCLOSURE STATEMENT INTRODUCTION This Individual Retirement Annuity ("IRA") is an annuity contract issued by AmerUs Life Insurance Company ("AMERUS") to fund an individual's

Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement

Disclosure Statement") BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement Deadline Extension for 2016 Contributions to a Traditional

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement Deadline Extension for 2016 Contributions to a Traditional

IRA Annual Contributions for

Published Since 1984 ALSO IN THIS ISSUE Roth IRA Statistics From 2004-2008, Page 3 Rollover for 2004-2008 Traditional IRAs, Page 4 End-of-Year Fair Market Values for IRAs for 2004-2008, Page 4 IRA and

Published Since 1984 ALSO IN THIS ISSUE Roth IRA Statistics From 2004-2008, Page 3 Rollover for 2004-2008 Traditional IRAs, Page 4 End-of-Year Fair Market Values for IRAs for 2004-2008, Page 4 IRA and

2008 IRS Reporting for a Conversion of Eligible Retirement (ERP) Funds to a Roth IRA

Funds to a Roth IRA") Published Since 1984 ALSO IN THIS ISSUE Required Minimum Distribution Rules for 401(k) Plans & IRAs are similar, Page 5 IRS Announces New Online EIN Application Process, Page 5 Discussion and Illustration

Published Since 1984 ALSO IN THIS ISSUE Required Minimum Distribution Rules for 401(k) Plans & IRAs are similar, Page 5 IRS Announces New Online EIN Application Process, Page 5 Discussion and Illustration

President Barack Obama Makes SEP/Profit Sharing Plan Contributions for

Published Since 1984 ALSO IN THIS ISSUE President Barack Obama Makes SEP/Profit Sharing Plan Contributions for 2007-2011 Seeking More IRA Contributions From Higher Income Clients and Understanding a Special

Published Since 1984 ALSO IN THIS ISSUE President Barack Obama Makes SEP/Profit Sharing Plan Contributions for 2007-2011 Seeking More IRA Contributions From Higher Income Clients and Understanding a Special

IRS Guidance - Errors on Form 5498 by Custodian May Cause Tax Trouble For Everyone

Published Since 1984 ALSO IN THIS ISSUE Final Review 2014 Form 5498, Page 2 CWF s Guide for the IRS Distribution Codes For Box 7 of the 2015 Form 1099-R, Page 6 Using K Code on Form 1099-R, Page 8 Collin

Published Since 1984 ALSO IN THIS ISSUE Final Review 2014 Form 5498, Page 2 CWF s Guide for the IRS Distribution Codes For Box 7 of the 2015 Form 1099-R, Page 6 Using K Code on Form 1099-R, Page 8 Collin

Financial Institutions Complex IRA Issues

Financial Institutions Complex IRA Issues October 1, 2015 Iowa Trust Conference Iowa Bankers Association Des Moines, IA Michael Nelson JM Consultants 6930 Glory Road Baxter, MN 56425 6930 Glory Road Baxter,

Financial Institutions Complex IRA Issues October 1, 2015 Iowa Trust Conference Iowa Bankers Association Des Moines, IA Michael Nelson JM Consultants 6930 Glory Road Baxter, MN 56425 6930 Glory Road Baxter,

NATIONAL WESTERN LIFE INSURANCE COMPANY YOUR ROLLOVER OPTIONS

NATIONAL WESTERN LIFE INSURANCE COMPANY YOUR ROLLOVER OPTIONS This notice explains how you can continue to defer federal income tax on your retirement savings and contains important information you will

NATIONAL WESTERN LIFE INSURANCE COMPANY YOUR ROLLOVER OPTIONS This notice explains how you can continue to defer federal income tax on your retirement savings and contains important information you will

Roth IRA Amendment ROTH INDIVIDUAL RETIREMENT CUSTODIAL ACCOUNT 5305-RA

Roth IRA Amendment Dear Roth IRA Owner: The purpose of this Amendment is to incorporate changes in law and policy that affect your Roth IRA agreement. This Amendment replaces the IRS Form 5305-RA Agreement

Roth IRA Amendment Dear Roth IRA Owner: The purpose of this Amendment is to incorporate changes in law and policy that affect your Roth IRA agreement. This Amendment replaces the IRS Form 5305-RA Agreement

IRS Releases 2011 Publication 590

Published Since 1984 ALSO IN THIS ISSUE Rollovers for 2006-2008 Traditional IRAs by Age, Page 2 Basic Beneficiary RMD Rules, Page 4 Michigan IRA Custodians New Withholding Duties as of January 1, 2012,

Published Since 1984 ALSO IN THIS ISSUE Rollovers for 2006-2008 Traditional IRAs by Age, Page 2 Basic Beneficiary RMD Rules, Page 4 Michigan IRA Custodians New Withholding Duties as of January 1, 2012,

IRAs. You Benefit by Making a Nondeductible IRA Contribution. Questions & Answers

IRAs You Benefit by Making a Nondeductible IRA Contribution Questions & Answers Purpose The purpose of this brochure is to explain the tax benefits so that you can decide whether it is in your best interest

IRAs You Benefit by Making a Nondeductible IRA Contribution Questions & Answers Purpose The purpose of this brochure is to explain the tax benefits so that you can decide whether it is in your best interest

Attached, please find the Distribution form required for distribution requests from your Roth IRA account.

Dear Ally Invest Client: Attached, please find the Distribution form required for distribution requests from your Roth IRA account. Please complete and return to Ally Invest Securities only the first two

Dear Ally Invest Client: Attached, please find the Distribution form required for distribution requests from your Roth IRA account. Please complete and return to Ally Invest Securities only the first two

Comprehensive Inherited Traditional IRA Amendment. Trust

ified HSA funding distribution, a qualified charitable distribution, the return of certain excess contributions or the return of certain current year contributions. If you are required to file one or more

ified HSA funding distribution, a qualified charitable distribution, the return of certain excess contributions or the return of certain current year contributions. If you are required to file one or more

AFPlanServ 403(b) Plan Distribution Authorization Form

Plan Distribution Authorization Form") AFPlanServ 403(b) Plan Distribution Authorization Form Participant Instructions The AFPlanServ 403(b) Distribution Authorization Form must be submitted to AFPlanServ to approve a distribution or plan-to-plan

AFPlanServ 403(b) Plan Distribution Authorization Form Participant Instructions The AFPlanServ 403(b) Distribution Authorization Form must be submitted to AFPlanServ to approve a distribution or plan-to-plan

GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA

Traditional IRA Roth IRA") GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA References to the Custodian mean BNY Mellon Investment Servicing Trust Company. BNY Mellon Investment Servicing Trust Company

GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA References to the Custodian mean BNY Mellon Investment Servicing Trust Company. BNY Mellon Investment Servicing Trust Company

2007 Instructions for Forms 1099-R and 5498

2007 Instructions for Forms 1099-R and 5498 Section references are to the Internal Revenue Code unless otherwise noted. What s New Form 1099-R Certain qualified distributions. A TIP has been added on page

2007 Instructions for Forms 1099-R and 5498 Section references are to the Internal Revenue Code unless otherwise noted. What s New Form 1099-R Certain qualified distributions. A TIP has been added on page

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA.

Traditional IRA SEP IRA.") PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional

Traditional Individual Retirement Account Disclosure Statement

Traditional Individual Retirement Account Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described in

Traditional Individual Retirement Account Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described in

Distribution Request Form. Instructions

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

BNY MELLON INVESTMENT SERVICING TRUST COMPANY. Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement

Disclosure Statement") BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

Rollovers from Employer-Sponsored Retirement Plans