The Webinar will be starting shortly

|

|

|

- Emil Watkins

- 5 years ago

- Views:

Transcription

1 Rev. 5/2/2018 The Webinar will be starting shortly 8:30 am CST or 12:30 pm CST We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may be reproduced in any form and by any means without prior written permission from Collin W. Fritz & Associates, Ltd.

2 Reminder: This is copyrighted material. No Video or Audio Recording is permitted without prior written consent from Collin W. Fritz & Associates, Ltd. Thank you for your compliance.

3 Basics of HSAs The Audio Portion of this presentation is available either by phone or by using the speakers and microphone on your PC. The phone number is provided to you in the confirmation from CWF and again at the time you join the meeting. You will need the access code that was ed to you in the confirmation from CWF. The confirmation code is 9 digits in length e.g You will also need the Audio Pin # which is shown to you at the time you join this meeting If you have trouble re-connecting please call CWF at

4 Health Savings Accounts President Bush signed the Medicare Prescription Drug, Improvements, and Modernization act of 2003 on December 8, This new law was generally effective January 1, The Act, in section 1201, authorizes Health Savings Accounts (HSAs) First year for contributions th Year for contributions HSAs go with HDHP (High Deductible Health Plans) 4

5 Business Goals of the HSA Custodian A cash deposit source Short Term (possibly long term) New customer/client relationship businesses and individuals* Strengthening existing relationships Fees DOL and IRS rules allow the employer to require all employees for purposes of receiving the employer s HSA contribution to establish their HSAs with one Financial Institution 5

6 Personal Uses and Goals for HSAs Uses and Goals: Pay Medical Expenses on a tax-free basis Retirement Savings General Savings Tax Reasons: Tax deductible or tax free contributions Tax free distributions Wealth accumulation and transfer to beneficiary(ies) - limited. 6

7 The HSA Life Span Contributions Deductible If by individual. Excludable if by employer Rollovers Transfers QFD HSA Custodial or Trust Account Earnings within Account are not Taxed HSA is Separate Tax Entity Distributions Accountholder Beneficiaries Tax Free if used to pay qualified medical expenses. If not, taxable and subject to 20% penalty tax if not age 65 or disabled. 7

8 Purpose(s) of HSAs: The purpose of HSAs is to create tax incentives so individuals will save for future health needs. The HSA will primarily be used to accumulate funds to pay health expenses on a tax-preferred basis. However, the HSA can also be used to accumulate wealth on a tax-preferred basis. This will happen when the contributed funds are not spent on health expenses. A primary purpose of HSAs is to create an incentive for people to NOT purchase medical products and services or to be better shoppers and to use preventive care. 8

9 Tax Benefits of an HSA: An HSA has more tax favored benefits than any other tax-preferred account. Tax deferred income and most likely, tax-free income. Funds with the HSA grow faster because taxes are not currently owed on the income earned within the HSA and such income is tax free if withdrawn and used to pay a qualified medical expense Tax Exclusion for Employer Contributions Tax Deduction for the individual s contribution Example: Jane Doe has taxable income of $50,000. Her marginal tax rate is assumed to be 20%. No HSA contribution, tax liability = $10,000 ($50,000 x 20%) With $5,000 HSA contribution, tax liability = $9,000 ($45,000 x 20%) She contributed $5,000 into her HSA, but it cost her only $4,000 as the $5,000 deduction reduced her taxable liability by $1,000. Tax-free distributions if withdrawn to pay qualified medical expenses. Potential for distribution to be made when account owner or Inheriting Beneficiary is subject to a lower marginal tax rate. 9

10 HSA Tax Overview Deduct the Contribution A deduction will generally be able to be claimed by the account owner for the amount of the contributions. An exclusion is authorized for employer contributions to HSAs. Example. An employer contributes $200 per month into an employee s HSA. This $2,400 is not included in her income for purposes of income taxes, social security, Medicare and unemployment taxes. Tax-Deferred Earnings (Sometimes tax-free) Earnings in an HSA are generally exempt from tax (like a traditional IRA, a Roth IRA, or Archer MSA), unless it has ceased to be an HSA. Earnings on amounts in an HSA are not includable in gross income while held in the HSA and are taxable if the withdrawn earnings are used to pay a qualified medical expense. 10

11 HSA Tax Overview Tax-Free Distributions Distributions from the HSA will be tax free (i.e. will not be included in income for income tax purposes) if the funds are used exclusively to pay for qualifying medical expenses. Publication 502 discusses the rules and which expenses are qualifying medical expenses. Non-Tax-Free Distributions If the withdrawn funds are not used exclusively to pay qualifying medical expenses, then the person will have to include the distribution in income and also pay an additional 20% tax, unless he or she is disabled or has attained age 65. Upon the death of the account owner, his or her inheriting HSA beneficiary(ies) will be required to include the HSA amount in his or her income for tax purposes for that year, but the 20% additional tax will not be owed. 11

12 HSA Eligibility An HSA is an individual account as is an IRA. Under current law there is no joint or family HSA. However, the HSA owner may use his or her HSA funds to pay his/her medical expenses, a spouse s medical expenses or those of any dependent. One cannot roll over or transfer HSA funds from his or her HSA to their spouse s HSA except when one spouse dies or there is a divorce. 12

13 HSA Tax Overview An HSA may be considered to be a second traditional IRA when the funds are not used to pay medical expenses when the individual is age 65 or older. An HSA distribution is like an IRA distribution and it is included in income, but is not subject to a penalty tax. 13

14 Definition of Health Savings Accounts: What requirements must be met to have an HSA? There must be a written agreement which creates a trust or custodial account. The purpose of the trust is to pay qualified medical expenses. The trust must be created or organized in the U.S. The HSA plan agreement must meet the following requirements. These requirements are very similar to the requirements which apply to traditional IRAs, Roth IRAs and other tax-preferred accounts. The requirements: The trustee or custodian must be a bank, an insurance company or a nonbank trustee as defined for IRA purposes. No part of the HSA assets may be invested in life insurance contracts. The HSA assets cannot be commingled with other assets unless pursuant to a common trust fund or common investment fund. 14

15 Definition of Health Savings Accounts (continued) The account owner s interest in the HSA is non-forfeitable. The HSA assets may not be used to purchase health insurance. However, there are exceptions as discussed later. The contributions must be in the form of cash unless a rollover contribution is made. It will be permissible to roll over funds into an HSA from another HSA or an MSA. Annual HSA contributions are limited depending upon the type of HDHP coverage Single HDHP Single or Family Under Age55 $3,250 $3,300 $3,350 $3,350 $3,400 $3,450 Age 55 or older $4,250 $4,300 $4,350 $4,350 $4,400 $4,450 Family HDHP Under Age 55 $6,450 $6,550 $6,650 $6,750 $6,750 $6,900 Age 55 or older $7,450 $7,550 $7,650 $7,750 $7,750 $7,900 15

16 How is an HSA established? Beginning January 1, 2004, an eligible individual establishes an HSA with a qualified HSA trustee or custodian, in much the same way an individual establishes an IRA with an approved IRA custodian. No permission or authorization from the Internal Revenue Service (IRS) is necessary to establish an HSA. An eligible individual may establish an HSA. Such individual may but is not required to have an employer who makes contributions to their HSA. 16

17 How does an eligible individual establish an HSA? Who is a qualified HSA trustee or custodian? Any insurance company or any bank (including a similar financial institution) as defined in section 408(n) can be an HSA trustee or custodian. In addition, any other person already approved by the IRS to be a trustee or custodian of IRAs or Archer MSAs is automatically approved to be an HSA trustee or custodian. 17

18 The HSA Custodian/Trustee Duties: Offer the deposit, investment or transaction account. Investment options In general, same as the IRA rules. Possible HSA investments debit cards, checking accounts, savings accounts, money market, time deposits, stocks, bonds, debt instruments, loans, mutual funds, real estate, etc. 18

19 The HSA Custodian/Trustee Duties: Offer the deposit, investment or transaction account Perform administrative duties Perform IRS reporting tasks Service the HSA owner 19

20 Establishing HSAs Certain documentation must be completed and provided to the individual when an HSA is established, in order to comply with IRS requirements. Written Plan Agreement IRS Model Forms Custodial-Your bank s DDA accounts - Form 5305-C money market, time deposits, etc Trust - Form 5305-B Custodial Self-Directed - Form 5305-C Written Disclosure Statement - Not required, but recommended. IRS Revised October 2016 Unlike with IRAs, IRS has not indicated there is a 7-day revocation right. 20

21 CWF Form # 40-HSA Custodial Account Application Make sure the agreement is valid and up-to-date. Tax Preferred Revocable Trust Contract between accountholder and the financial institution. A plan agreement establishes a new HSA which is reported separately from other HSAs. 21

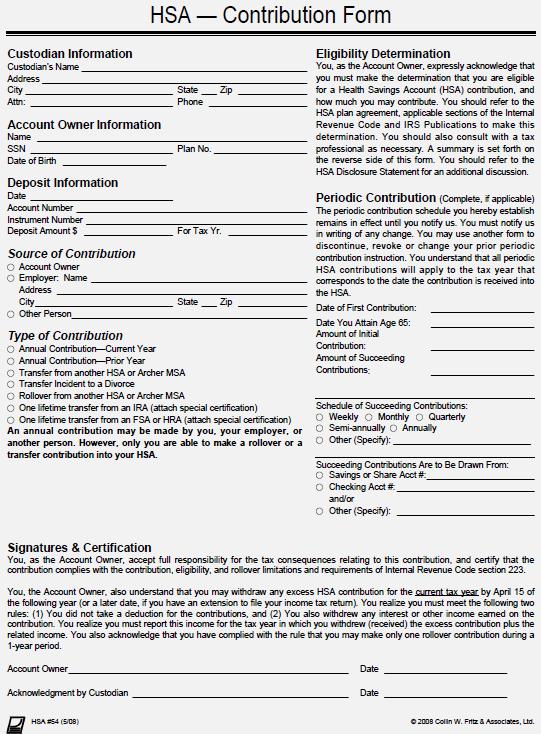

22 Completion of the HSA Application 22

23 Completion of the HSA Application Custodian/Trustee Information 23

24 Completion of the HSA Application Account Owner Information Name, Address, SSN, and Date of Birth 24

25 Designation of Type of Contribution 25

26 Designation of Beneficiaries The beneficiary(ies) of the HSA will be the recipients of the HSA proceeds upon death of the accountholder. Accountholders are not required to name beneficiaries to have a valid HSA. 26

27 Designation of Beneficiaries Who can be named as a beneficiary? Any living individual Estate Trust Church Charity Foundation Etc. 27

28 No Named Beneficiary If no named beneficiary, generally assets go to the HSA owner s estate. HSA plan agreement should discuss. 28

29 Continuing Distribution Instruction Indicate with an X if there will be ongoing distributions with Debit Cards, Checking Accounts, etc. 29

30 Date, Amount, Type, and Tax Year 30

31")

31 Power of Attorney Power of Attorney (7/14) 31

32 Power of Attorney for HSA Transactions CWF # HSA-43 32

33 Requirements Provide signed and dated copy of HSA application Provide copy of an up-to-date and current Plan Agreement Furnish a copy of an up-to-date HSA Disclosure Statement (optional) 33

34 Provide copy of other Disclosures Customer Identification Program (CIP), if applicable Truth-In-Savings Act (TISA) Federal Deposit Insurance Corporation (FDIC)/ National Credit Union Administration (NCUA) Security Exchange Commission (SEC) Other Investment Disclosures 34

35 HSA Eligibility Definition of an Account Owner Who qualifies to be the account owner of an HSA? A person must meet the following requirements: In Notice the IRS has provided the following expanded definition of an eligible employee: An eligible individual can establish an HSA. An eligible individual means, with respect to any month, an individual who: Is covered under a high-deductible health plan (HDHP) on the first day of such month; Is not also covered by any other health plan that is not an HDHP (with certain exceptions for plans providing certain limited types of coverage); Is not enrolled to receive benefits under Medicare (generally, has not yet reached age 65); and Not eligible to be claimed as a dependent on another person s tax return. Observation: There is no requirement to have compensation or to be employed. Having substantial compensation or wealth does not make a person ineligible. 35

36 Definition of a High Deductible Health Plan What Health Plans are qualifying high deductible health plans? Two requirements. Not all HDHP are qualifying so that one is eligible for an HSA. 1. The HDHP must have an annual deductible which is not less than a certain amount and 2. The plan must have an annual out-of-pocket limit not exceeding a certain amount. The sum of the annual deductible and the other annual out-ofpocket expenses required to be paid by the individual under the plan (other than for premiums) cannot exceed the out-of-pocket limit. CWF Observation: Expenses in excess of the out of pocket limit must be covered by the health plan in order to qualify as HDHP, so an individual will be covered for catastrophic situations 36

37 High Deductible Health Plan Requirements (HDHP) HSA Limits are Adjusted Annually by a COLA Minimum Annual Deductible Single HDHP Plan / $1,000 $1,000 $1,050 $1,100 $1,100 $1,150 $1,200 $1,250 $1,250 $1,300 $1,350 Family HDHP Plan / $2,000 $2,000 $2,100 $2,200 $2,200 $2,300 $2,400 $2,500 $2,500 $2,600 $2,700 For 2018 the Deductible limit within the HDHP may be set to be more than the $1,350 or the $2,700. For example, the deductible for a single HDHP could be $1,500, $2,000 or $2,500, etc. IRS will announce 2019 limits in April/May of

38 Basic Concept of HSAs and the Qualifying HDHP An individual must use personal funds to meet the deductible requirement. Hopefully, the individual will have sufficient funds with their HSA to pay the medical expenses which are not paid for by the HDHP whether on account of the deductible requirement or a co-payment requirement. Certain individuals are eligible to make an annual HSA contribution. Employers may make HSA Contributions on behalf of their employees, but an employer is not required to do so. There are non-discrimination rules applying to an employer. 38

39 High Deductible Health Plan Requirements (HDHP) Maximum Annual Out-of-Pocket Expenses Single Plan ,000 5,100 5,250 5,500 5,600 5,800 5,950 6,050 6,250 6,350 6,450 6,550 6, Family Plan ,000 10,200 10,500 11,000 11,200 11,600 $11,900 12,100 12,500 12,700 12,900 13,100 13, A person s out of pocket expense is the sum of his/her deductible, co-payments etc. Note, the law imposes a cap of an annual maximum limit on the amount of medical expenses an individual will have to pay. However, the purchaser of the HDHP may choose to set this limit at an amount less than the maximum amount. For example, a person ( or an employer ) with a Single HDHP could have the limit set at $5,500 rather than the $6,650 or a person with a Family HDHP could have the limit set at $11,000 rather than the $13,

40 Major Exception to the Deductible Requirement Preventive Care Statutory Exception An individual or an employer may add a preventive care provision to the qualifying HDHP. By doing so, if an individual goes in for a preventive care visit and a medical expense is incurred as a result of this visit, the qualifying HDHP may pay the medical expense even though the deductible limit has not been met. Preventive care includes, but is not limited to the following: Periodic health evaluations, including tests and diagnostic procedures ordered in connection with routine examinations, such as annual physicals. Routine prenatal and well-child care Child and adult immunizations Tobacco cessation programs Obesity weight-loss programs Screening services Preventive care does not include any service or benefit intended to treat an existing illness, injury, or condition. 40

41 HSA Eligibility Who Determines? The individual does. He or she should have written document from the insurance company and/or the employer stating that the health plan does qualify as a HDHP for HSA purposes. The HSA custodian is not responsible to make this determination. CWF suggests the individual will want to receive a written statement from the provider of the health plan that it qualifies as an HDHP for HSA purposes. Presumably, the HSA application will be so written that the individual will certify that he or she is an eligible individual, including that he or she is covered by a health plan that meets all of the requirements of an HDHP for HSA purposes. 41

42 What kind of other health coverage makes an individual ineligible for an HSA? Generally, an individual is ineligible for an HSA if the individual, while covered under an HDHP, is also covered under a health plan (whether as an individual, spouse, or dependent) that is not an HDHP. 42

43 What other kinds of health coverage may an individual maintain without losing eligibility for an HSA? An individual does not fail to be eligible for an HSA merely because, in addition to an HDHP, the individual has coverage for any benefit provided by permitted insurance. Permitted insurance is insurance under which substantially all of the coverage provided prelates to liabilities incurred under workers compensation laws, tort liabilities, liabilities relating to ownership or use of property (e.g. automobile insurance), insurance for a specified disease or illness, and insurance that pays a fixed amount per day (or other period) of hospitalization. 43

44 Permitted Insurance In addition to permitted insurance, an individual does not fail to be eligible for an HSA merely because, in addition to an HDHP, the individual has coverage (whether provided through insurance or otherwise) for accidents, disability, dental care, vision care, or long-term care. If a plan that is intended to be an HDHP is one in which substantially all of the coverage of the plan is through permitted insurance or other coverage as described in this answer, if is not an HDHP. 44

45 What is the deadline for establishing and contributing to an HSA? A person has until the due date (without extensions) for filing his or her federal income tax return, normally April 15, to establish and fund his or her HSA for the previous tax year. The Emancipation Day holiday may impact the deadline April 17, 2018, is the deadline for 2017 April 15, 2019, is the deadline for 2018 Special age 65 / Medicare Rule No contribution may be made for the month a person enrolls in Medicare and any subsequent month. For example, Sarah enrolled in Medicare in July 2017 on She was HSA eligible for January 1 to June 30. Since she had single HDHP coverage, she is eligible to contribute $2,200 ($4,400 x 6/12) for Her deadline to contribute is April 17,

46 Tax Deduction and Contribution Limits Who is responsible to calculate the permissible and/or maximum contribution amount? The individual (or the tax preparer.) Not the HSA Custodian 46

47 Tax Deduction and Contribution Limits Will a person be allowed to claim a deduction for contributions to his or her HSA? Yes, but there are limits. Contributions made by an eligible individual to an HSA are deductible by the eligible individual in determining adjusted gross income. The contributions are deductible whether or not the eligible individual itemizes deductions. 47

48 Maximum HSA Contributions HSA Limits are Adjusted Annually by a COLA HSA owner - not Age 55 or Older Single HDHP Family HDHP $3,350 $3,400 $3,450 $6,750 $6,750 $6,900 These are the maximum contribution limits for a person who was HDHP coverage for 12 months or who qualifies to use the last month rule. 48

49 HSA Catch-Up Contributions Not Adjusted By a COLA For individuals Age 55 and older $1,000 $1,000 $1,000 $1,000 $1,000 49

50 Maximum HSA Contributions HSA Limits are Adjusted Annually by a COLA HSA owner - Age 55 or Older Single HDHP Family HDHP $4,350 $4,400 $4,450 $7,750 $7,750 $7,900 50

51 HSA Owner- Eligible Individuals Maximum Annual HSA Contribution Single HDHP Plan ,600 2,650 2,700 2,850 2,900 3,000 3,050 3,100 3,250 3,300 3,350 3,350 3,400 3, Family HDHP Plan ,150 5,250 5,450 5,650 5,800 5,950 6,150 6,250 6,450 6,550 6,650 6,750 6,750 6,900 Subject to cost-of-living adjustments HSA Owner s Responsibility to determine 51

52 HSA Owner- Eligible Individuals Combined Single HDHP $3,100 $3,250 $3,400 $3,650 $3,800 $4,000 $4,050 $4,100 $4,250 $4,300 $4,350 $4,400 $4, Combined Family HDHP $5,650 $5,250 $6,150 $6,450 $6,700 $6,950 $7,150 $7,250 $7,450 $7,550 $7,650 $7,750 $7,900 52

53 HSA Contributions 2 Methods for Calculating a Person s Maximum Contribution 1. Pro-rata method 2. Full Year Contribution Method or the Last-Month Rule 53

54 HSA Contributions 2 Methods for Calculating a Person s Maximum Contribution Pro-Rata Method The Pro-Rata Calculation: A person s contribution is the sum of the monthly limitations. For example, if he or she is covered by the HDHP on the first day of each month for 2018, then he or she is entitled to the full annual contribution amount (i.e. $3,450 or $6,900, as applicable). If he or she is not covered on the first day of every month, then he or she is only entitled to a pro rata contribution as follows: * If covered for 1 month, then would be entitled to contribute 1/12 of the applicable amount; * If covered for 3 months, then would be entitled to contribute 3/12 of the applicable amount; * If covered for 11 months, then would be entitled to contribute 11/12 of the applicable amount; etc. Note that if a person has coverage under an HDHP as of January 1, but he or she is not covered under the HDHP as of December 1, then a pro rata contribution method will apply. 54

55 HSA Contributions 2 Methods for Calculating a Person s Maximum Contribution Full Year Contribution Method If covered by a qualifying HDHP on 12/31/2017 or 12/1/2018 the individual may contribute 100% of the maximum permissible amount even though such coverage was not in place for all 12 months. In fact, only one month of HDHP coverage is required(december). This method obviously allows a person to contribute a larger amount than under the pro-rata method. An individual is not required to use the last month method. There is a special tax penalty rule which will apply if the person does not retain coverage under the HDHP for the entire subsequent calendar year. Beyond the scope of this Basic Webinar. 55

56 HSA Contribution Limits are Impacted By Marriage Situation # 1. An individual age 59 and a daughter age 24 are both covered under a HDHP originating with the individual who is age 59. Both are eligible to contribute $6,900 to their respective HSAs. The individual age 59 may contribute an additional $1,000 because of the catch-up rule. Situation # 2. Jane is age 59 and John is age 56. They are not married. Both are covered under a HDHP because they have purchased such a policy. Both are eligible to contribute $7,900 ($6,900 + $1,000) to their respective HSAs. Rules for individuals who are not married: Each is able to make his or her own contribution and his or her contribution is not limited by what the other person contributed. 56

57 HSA Contribution Limits are Impacted By Marriage Situation # 3. Jane is age 50 and John is age 56. They are married. Both are covered under a HDHP originating with Jane s employment and/or John s employment. Rules for married individuals: If either spouse has family HDHP coverage, both spouses are treated as having family HDHP coverage. The contribution limit for 2018 is $6,900. This $6,900 limit is split equally between the spouses unless they agree on a different division. The rules for married people apply only if both spouses are eligible individuals. 57

58 HSA Owner- Eligible Individuals Spousal HDHP Eligibility Situations Husband Wife Permissible Contribution(s) Single HDHP Single HDHP 2 Single HSA Contributions Family HDHP Family HDHP 1 Family HSA Contribution Family HDHP Single HDHP 1 Family HSA Contribution No HDHP Family HDHP 1 Family HSA Contribution No HDHP Single HDHP 1 Single HSA Contribution 58

59 HSA Contribution Rules for Married Individuals Husband and Wife who are Younger than Age 55 and both are HSA Eligible for Each may have own HSA May only have one HSA Example H-HSA W-HSA Total Allowed $6,750 0 $6,750 Allowed 0 $6,750 $6,750 Allowed $3,375 $3,375 $6,750 Allowed $2,000 $4,750 $6,750 Allowed $1,500 $5,250 $6,750 59

60 HSA Contribution Rules for Married Individuals Spousal HDHP Eligibility Situations for Husband over 55 + Wife over 55 (Both Eligible) require two HSAs to maximize contributions Example H-HSA W-HSA Total Allowed $7,750 $1,000 $8,750 Allowed $1,000 $7,750 $8,750 Allowed $4,375 $4,375 $8,750 Not Allowed $8,750 0 $8,750 Not Allowed 0 $8,750 $8,750 60

61 HSA Contribution Rules for Married Individuals Husband and Wife who are Younger than Age 55 and both are HSA Eligible for 2018 Each may have own HSA May only have one HSA Example H-HSA W-HSA Total Allowed $6,900 0 $6,900 Allowed 0 $6,900 $6,900 Allowed $3,450 $3,450 $6,900 Allowed $2,000 $4,900 $6,900 Allowed $1,500 $5,400 $6,900 61

62 HSA Contribution Rules for Married Individuals Spousal HDHP Eligibility Situations for 2018 Husband over 55 + Wife over 55 (Both Eligible) require two HSAs to maximize contributions Example H-HSA W-HSA Total Allowed $7,900 $1,000 $8,900 Allowed $1,000 $7,900 $8,900 Allowed $4,450 $4,450 $8,900 Not Allowed $8,900 0 $8,900 Not Allowed 0 $8,900 $8,900 62

63 Who can make the HSA contribution? Eligible HSA Owner Employer for eligible employee Any person or entity for an eligible HSA owner Any eligible individual may establish and contribute to an HSA. A person need not be an employee to contribute to an HSA. A person may be self-employed, unemployed or employed and contribute to an HSA. An employer can contribute to an HSA on behalf of an employee. Family members may also make contributions to an HSA on behalf of another family member as long as that other family member is an eligible individual. For example, a mother could contribute funds to her daughter s HSA as long as the daughter was not eligible to be claimed as a dependent and is eligible for an HSA. For example, a church could make a contribution into a member s HSA In Notice , the IRS set forth the rule that any person can make an HSA contribution for another person; it is not required that they be a family member. 63

64 What is the tax treatment of contributions made by a family member on behalf of an eligible individual? Contributions made to an HSA by a family member on behalf of an eligible individual are deductible by the eligible individual in computing adjusted gross income. The contributions are deductible whether or not the eligible individual itemizes deductions. An individual who may be claimed as a dependent on another person s tax return is not an eligible individual and may not deduct contributions to an HSA. 64

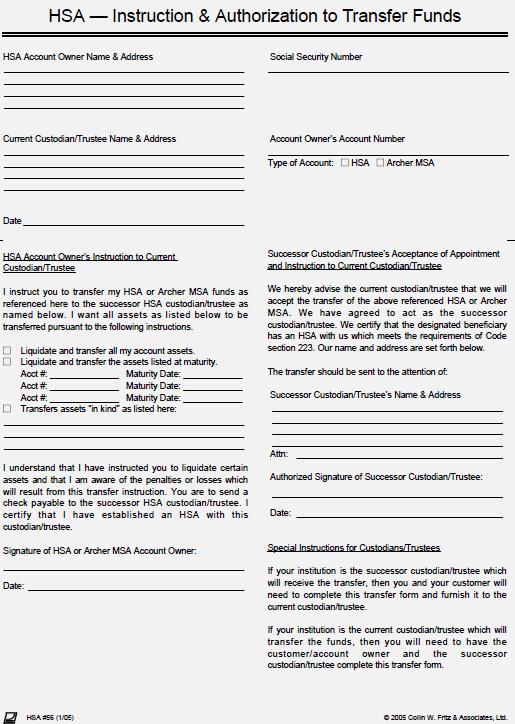

65 What is the tax treatment of employer contributions to an employee s HSA? Very favorable. In the case of an employee who is an eligible individual, employer contributions (provided they are within the limits) to the employee s HSA are treated as employer-provided coverage for medical expenses under an accident or health plan and are excludable from the employee s gross income. The employer contributions are not subject to withholding from wages for income tax or subject to the Federal Insurance Contributions Act (FICA), the Federal Unemployment Tax Act (FUTA), or the Railroad Retirement Tax Act. Contributions to an employee s HSA through a cafeteria plan are treated as employer contributions. For purposes of the maximum contribution limit, the amount the employer contributes must be added to the amount the individual contributes. 65

66 What is the tax treatment of employer contributions to an employee s HSA (continued)? What are the consequences to the employer and to each employee? The amount which an employer contributes to an HSA goes tax free just as the payment of the health insurance premium is tax free. Once the funds are contributed to the HSA, they belong to the employee/individual. There are 2 situations where the IRS authorizes an HSA custodian to return a mistaken HSA contribution to the employer 1. Employee never HSA eligible or 2. Employer contributes more than $3,450/$4,450 or $6,900/$7,900 as applicable for General Planning Concept. An employer wants to make its HSA contributions on a monthly basis. If the employer makes contributions for more than one month it assumes the risk that the employee will separate from service. Once the HSA funds are in a person s HSA they belong to the individual and not the employer. Withdrawal of such funds because not on account of paying a medical expense would mean the individual will have to include such amount as income and pay the 20% tax, if applicable 66

67 What is the tax treatment of employer contributions to an employee s HSA (continued)? Employer Contributions: Under the tax rules an employer contribution is considered made before the individual s contributions. A person must reduce the amount he or she, or any other person, cancontribute to his/her HSA by the amount of any contributions made by the employer that are excludable from income. This includes amounts contributed to his or her HSA by the employer through a cafeteria plan. 67

68 Health Savings Accounts- Rollovers HSA-to-HSA Rollover and Archer MSA to HSA Purpose To move assets from one HSA to another HSA, or take a distribution from an HSA and return it to the same HSA, on a tax-free basis HSA Person HSA Discuss Archer MSA A predecessor to the HSA. Archer MSAs may still be established, but rarely does this happen 68

69 Health Savings Accounts- Rollovers HSA-to-MSA rollovers are NOT allowed HSA-to-IRA rollovers are NOT allowed 69

70 Health Savings Accounts- Rollovers Rollover contributions from Archer MSAs and other HSAs into an HSA are permitted. Rollover contributions need not be in cash but generally will be. Rollovers are not subject to the annual contribution limits. 70

71 Health Savings Accounts- Rollovers The consequences of rolling funds from an Archer MSA or an HSA to another HSA is that the distribution will not be taxed in the income of the account owner even though the funds were not used to pay the qualified medical expenses of the account owner. Similarly, a distribution from an Archer MSA which is rolled over into an HSA will not be required to be included in the income of the recipient. 71

72 Health Savings Accounts- Rollovers The following rules must be met: First, in order to gain rollover treatment, the funds distributed must be re-contributed no later than the 60 th day after the day on which the account owner received the distribution. Second, an account owner is not eligible to roll over an HSA distribution if he or she received such distribution and he or she had made a prior rollover contribution within one Year of such distribution. 72

73 Health Savings Accounts- Rollovers and Transfer CWF HSA # 65 Certification for Rollovers to an HSA 73

74 Health Savings Accounts- Rollovers and Transfer Documentation for Rollovers from an HSA CWF HSA # 57 HSA Distribution Form 74

75 Health Savings Accounts - Transfers Transfers from Health Savings Accounts allowed Transfers from Archer Medical Savings Accounts allowed into an HSA HSA Archer MSA HSA HSA 75

76 Health Savings Accounts - Transfer HSA-to-MSA transfers are NOT allowed HSA-to-IRA transfers are NOT allowed 76

77 Health Savings Accounts Trustee-to-Trustee Transfer Purpose Move HSA Asset from one HSA to another, one HSA custodian/trustee to another HSA custodian/trustee on a Tax-Free Basis 77

78 Health Savings Accounts Trustee-to-Trustee Transfer Requirements No IRS Limit Not reportable to IRS Federal Income Tax withholding rules do not apply Document carefully 78

79 Health Savings Accounts Trustee-to-Trustee Transfer Document carefully Specify HSA owner, amount, and timing of transfer Document receipt of transfer 79

80 CWF HSA# Trustee-to-Trustee 56 Transfer CWF HSA# 54 80

81 A Special HSA contribution -Qualified HSA Funding Distribution IRA HSA Example Jane has a traditional IRA with a balance of $30,000. She is HSA eligible for She is age 58. She has a family HDHP. NO contributions have yet been made to her HSA for She instructs she wishes to do a QFD of $7,900. IRA HSA $30,000 $7,900 Used to pay qualified med expense = tax-free 81

82 Qualified HSA Funding Distribution IRA HSA Qualified HSA Funding Distribution Must be an Eligible HSA Contribution Must be a trustee-to-trustee transfer (direct rollover) One per Lifetime Testing Period Reported as HSA Contribution on 5498-SA Reported as an IRA Distribution on 1099-R. Individual explains on tax return that it is not taxable Cannot be made from an ongoing SEP-IRA or Simple IRA. 82

83 Qualified HSA Funding Distribution IRA HSA Must be an Eligible HSA Contribution Must be a trustee-to-trustee transfer (direct rollover) Reported as HSA Contribution on 5498-SA Reported as a Distribution on 1099-R. Special tax explanations. One per Lifetime Exception Changing from Single HDHP to Family HDHP Must be accomplished in same calendar year, for same tax year by December 31 Cannot be done between January 1 and April 15 for prior tax year IRAs and Inherited IRAs 83

84 CWF HSA # 66 Certification for One Lifetime Transfer of IRA Funds to an HSA 84

85 IRS Tax Reporting by the HSA Custodian Forms or Reports Prepared by the HSA Custodian: For 2017 For 2018 Fair Market Statements January 31, 2018 (optional) January 31, 2019 (optional) Form 1099-SA January 31, 2018 January 31, 2019 Form 5498-SA May 31, 2018 May 31,

86 IRS Tax Reporting Forms Forms Prepared by the HSA Custodian 5498-SA: Contributions and Fair Market Value 1099-SA: Distributions Forms Prepared by the HSA Owner 1040 and others: Used by the individual to claim a tax credit or a tax deduction plus used to report a distribution which is taxable distribution. 5329: Used to report one or more HSA taxes- 6% or 20% Used to explain contributions and distributions by the individual from HSAs. 86

87")

87 HSA Reporting By the HSA Owner IRS Form 1040 Deduction (Subtraction line 25) 87

$ * $ 88")

88 HSA Reporting HSA Owner IRS Form 1040 Other taxes (Line 58 and 60) $ * $ 88

89 HSA Reporting HSA Owner IRS Form 5329 Other taxes Part VII 89

90 HSA Reporting HSA Owner IRS Form 5329 Other taxes Part VII * 90

91 HSA Reporting HSA Owner IRS Form 1040 Deduction (Subtraction line 25) IRS Form 8889 Part 1 Contributions Part 2 Distributions Part 3 Special Penalty Tax Each married individual must complete their own

92 HSA Reporting HSA Owner IRS Form 1040 Deduction (Subtraction line 25) IRS Form 8889 Part 1 Contributions Part 2 Distributions Part 3 Special Penalty Tax 92

93 HSA Reporting IRS Form 5498-SA Note No indication on this form as to who made the contribution the individual or the employer 93

94 HSA Reporting HSA Custodian/Trustee Contributions IRS Form 5498-SA IRS Form 5498-SA Box 2 - Total contributions made in 2017 For 2016 and for 2017 Includes Qualified funding distributions from IRAs 94

95 HSA Reporting IRS Form 5498-SA Box 3 - Total HSA and Archer MSA contributions made in 2018 for 2017 Note: - Amount in box 3 of this form will also be reported in box 2 of the 2018 Form 5498-SA. 95

96 HSA Reporting IRS Form 5498-SA Box 4 - Rollover contributions 96

97 HSA Reporting IRS Form 5498-SA 97

98 HSA Reporting HSA Owner IRS Form 1040 deduction IRS Form 8889 Employer Contribution for its employee reported on IRS Form W-2 Box 12, Code W and indicates the amount the employer contributed 98

99 HSA Distributions When can an HSA distribution occur? An individual can receive a distribution from their HSA at any time. How will an HSA distribution be taxed? A distribution from an HSA that is used to pay qualified medical expenses not paid or covered by insurance will generally not be included in the account owner s gross income. Distributions that are used for non-medical purposes will be included in gross income and may be subject to an excise tax. A 20% excise tax will apply to any distributions made for nonmedical purposes prior to the account owner s death, disability, or attainment of age 65. The fact that a person is no longer eligible to contribute to his or her HSA does not change how a distribution is taxed. 99

100 HSA Distributions Who is responsible for determining if a distribution is used exclusively to pay a qualifying medical expense? It is the account owner s sole responsibility to determine the purpose and tax effect of any distribution from the HSA. Neither the custodian of the HSA nor the employer is required or able to determine whether HSA distributions are used for medical or non-medical purposes. 100

101 HSA Distributions Is an HSA a Reimbursement Account or a Direct Pay Account? Although many individuals use the HSA as a direct payment account, under existing law an HSA owner should use the HSA as a reimbursement account. That is, use personal non-hsa funds to pay a medical expense, learn to what degree the HDHP will pay that medical expense, and reimburse himself or herself from the HSA for that portion of the medical expense not paid by the HDHP. Why? Tax rules limit how much a person is eligible to contribute to their HSA. Many individuals wrongly believe they are entitled to contribute to their HSA the amount or amounts paid/reimbursed by the HDHP, without there being tax consequences. 101

102 HSA Distributions If a Person Becomes HSA Ineligible, Is the Person Required to Close Their HSA BY a Certain Deadline? Should the person close their HSA? NO. An HSA is a life-long account. There will be times when a person is HSA eligible and times he or she is ineligible. Being ineligible simply means a current year HSA contribution may not be made for the person s benefit. The person will have medical expenses in subsequent years. Even a person who becomes covered by a non-hdhp will have some medical expenses which such plan will not cover. He or she can use their HSA to pay such expenses. If a person under age 65 (and not disabled) decides to close their HSA by withdrawing their HSA balance, the person will be required to include the withdrawn amount in their income and pay the 20% penalty as the withdrawal is not used to pay a qualifying medical expense. 102

103 HSA Distributions What is the result if a person waits to establish their HSA until after the or she incurs a medical expense? The IRS has adopted the rule. A medical expense will be a qualified medical expense only if it is incurred after the HSA is established. An individual wants to establish their HSA as soon as possible once he or she is HSA eligible. 103

104 HSA Reporting - Distributions IRS Form 1099-SA 104

105 HSA Reporting - Distributions HSA Custodian/Trustee Distributions IRS Form 1099-SA IRS Form 1099-SA Box 3 - Distribution code Code 1 - Normal distribution Code 2 - Excess contribution Code 3 - Disability Code 4 - Death distribution other than code 6 Code 5 - Prohibited transaction Code 6 - Death distribution after year of death to a non-spouse beneficiary NOT THE ESTATE What is a normal HSA distribution? It is any distribution not described in 2-6. A normal distribution may or may not be a medical distribution. 105

106 HSA Distributions Health Savings Accounts Distributions For Medical Reasons Not for Medical Reasons 106

107 HSA Distributions Qualified Medical Expense Definition: Medical Expenses incurred by the HSA Owner, the HSA Owner s spouse, and the HSA Owner s dependents on or after the date of the HSA Establishment. 107

108 HSA Distributions What Medical Expenses qualify for tax-free distributions? Medical expenses for HSA purposes are defined in Code section 213. IRS Publication 502 should also be reviewed. They generally include any medical expense that could qualify as a medical expense itemized deduction on the tax return. Note: If a distribution is made from an HSA for medical expenses, those same medical expenses cannot be itemized as a deduction on the individual s tax return. These would include expenses related to the diagnosis, cure, mitigation, treatment or prevention of disease, and transportation to and from a medical care facility for such medical care. Medical expenses for HSAs do not include insurance premiums other than premiums for long-term care insurance, premiums on a health plan during any period of continuation coverage required by Federal law, or premiums on a health plan during a period in which the individual is receiving unemployment benefits under any Federal or State law. 108

109 Qualified Medical Expense IRS Publication

110 CWF HSA # 57 Distribution Form 110

111 May HSA assets be used to pay the premiums for the HDHP? The general answer is No. However, the following insurance premiums for a qualifying HDHP may be paid from an HSA and are considered to be qualified (tax-free) distributions; A period of continuation coverage (i.e.cobra) required under Federal Health Law; A qualified long-term care insurance contract (there are limits); Any period of unemployment as evidenced by the individual receiving unemployment compensation under a Federal or State law; or Any health insurance such as Medicare Part A and Part B other than a Medicare supplemental policy for any account owner who has attained the specified age under section 1811 of the Social Security Act. 111

112 Special Distributions-Excess 112

113 Do excess contribution rules apply to HSAs? Yes. The rules are very similar to the IRA rules. A 6% excise tax will be owed, on an annual basis, with respect to an excess contribution made to an HSA, unless corrected. An excess contribution may arise from contributions made by the eligible individual, his or her employer, or any person. Excess contributions arise when the contribution exceeds the contribution limit or the contribution is a non-qualifying rollover or transfer. 113

114 Health Savings Accounts- Excess Contributions Corrected in similar manner as IRAs withdraw it plus earnings Responsibility to determine HSA Owner- primarily responsible for excess contributions HSA Custodian/Trustee Monitor maximum Family HDHP amount plus catch-up contribution Per the IRS. See Article I of Form 5305-C. Maximum contribution is $7,750 for 2017 and $7,900 for

115 Health Savings Accounts- Excess Contributions Corrected in similar manner as IRAs Must be removed by due date plus extensions to avoid penalty With applicable earnings Earnings taxed in year of distribution Earnings Subject to 20% penalty Document carefully 6% Excise penalty tax per year, if not corrected. 115

116 Health Savings Accounts- Excess Contributions Communicating to HSA owners about excess contributions: It is important for HSA owners to have an understanding how excess contributions arise and that they must be corrected or adverse tax consequences will result. CWF believes it is important that the HSA owner understand that he or she is primarily responsible to monitor and correct any excess HSA contributions. The HSA custodian is NOT primarily responsible for most excess HSA contribution situations. The HSA custodian duty to monitor for excess HSA contribution is limited to two situations as discussed below: The IRS rules for excess HSA contributions are settled. The HSA custodian is not to accept regular HSA contributions for 2016 in excess of $7,750 or $7,750 for

117 CWF HSA #67 Special Explanation Regarding the Withdrawal of an Excess HSA Contribution CWF HSA #67W Worksheet to Calculate the Income Related to the Withdrawal of an Excess HSA Contribution 117

118 Health Savings Accounts- HSA Owner Dies The surviving spouse is the designated beneficiary. The decedent s HSA becomes the HSA of the surviving spouse beneficiary. This happens even if the surviving spouse is not an eligible individual. No income tax will be owed by the surviving spouse unless he or she would take a distribution and use it for non-medical reasons. 118

119 Health Savings Accounts- HSA Owner Dies A non-spouse beneficiary must include their share of the decedent s HSA determined as of day of passing in their income for the year during which the death occurred. This is true even if the funds are distributed to the beneficiary in a later year. The amounts to be included in income is reduced to the extent the HSA was used to pay final medical expenses. 119

120 Health Savings Accounts- HSA Owner Dies The HSAs owner s estate is the designated beneficiary. The FMV of the HSA will be included on the financial income tax return of the decedent. The funds will need to be distributed to the estate. 120

121 Health Savings Accounts- Death Distributions Example. Jane Doe dies on August 3, She has two designated beneficiaries of her HSA, her son, John and her daughter, Ann. Her HSA has a fair market value on August 3 of $18,400. Situation # 1 Death & Distribution to Beneficiary Same Year John and Ann both withdrew $9,250 on December 30, 2017 and so the account balance was 0.00 as of December 31, Situation # 2 Distribution to Beneficiary in Following Year Neither beneficiary with drew his or her balance as of December 31,2017. Thus, the 2017 Form 5498-SA for Jane Doe will show the FMV as of December 31, It is assumed to be 18,500. It is also assumed that John and Ann both withdraw $9,300 on February 20,

122 HSA Reporting - Distributions IRS Form 5498-SA Situation # 1 DOE, JANE x Final Form 5498-SA for Decedent 122

123 HSA Reporting - Distributions IRS Form 1099-SA Situation # Ann 4 x

124 HSA Reporting - Distributions IRS Form 1099-SA Situation # John x 124

125 HSA Reporting - Distributions IRS Form 1099-SA Situation # ANN x 125

126 HSA Reporting - Distributions IRS Form 1099-SA Situation # John x 126

127 Do the Prohibited Transaction Rules Apply to an HSA? Yes. The rules of Code section 4975 will apply to an HSA in the same manner they apply to IRAs. Code section 408(e)(2) provides the rule that the IRA ceases to be an IRA as of the first day of the year during which a prohibited transaction occurs. In such a case, a distribution is deemed to have occurred on the first day of such year. The amount deemed distributed is the fair market value of all assets as of the first day of the year. Code section 408(e)(4) provides the rule that if an individual uses any portion of his or her IRA as security for a loan, then the part so pledged is treated as a distribution. The same result will occur if a person pledges a portion of his or her HSA as collateral for a loan. 127

128 Additional HSA Rules to be Similar to IRA Rules The following additional IRA rules will apply in a similar fashion to HSAs: The no deduction for rollover contribution rule found in section 219(d)(2); A contribution made by the tax-filing deadline will be considered to have been made by December 31 as provided by section 219(f)(3); The community property laws do not apply to HSAs as provided by Code section 408(g); HSAs may be set up as custodial accounts as well as trust accounts pursuant to section 408(h). Payments are permissible pursuant to section 219(f), except as provided in section 106(d). There are rules for the Transfer of HSA Incident to Divorce which are virtually identical to the rules which apply to IRAs. The transfer of an account owner s interest in the HSA to a spouse or former spouse under a divorce decree or a separation agreement is not considered to be a taxable transfer. That is, the transfer is tax free. The receiving spouse is now considered to be the account owner of the HSA. 128

129 Miscellaneous Rules HSAs may be offered under Cafeteria Plans Code section 125(d)(2) has been amended to permit an employee to elect to have the employer pay contributions to an HSA established on behalf of the employee. What discrimination rules apply to HSAs? If an employer makes HSA contributions, the employer must make available comparable contributions on behalf of all comparable participating employee (i.e., eligible employees with comparable coverage) during the same period. Can an HSA be offered under a cafeteria plan? Yes. Both an HSA and an HDHP may be offered as options under a cafeteria plan. Thus, an employee may elect to have amounts contributed as employer contributions to an HSA and an HDHP on a salary-reduction basis. Are HSAs subject to COBRA continuation coverage under section 4980B? No. Like Archer MSAs, HSAs are not subject to COBRA continuation coverage. May eligible individuals use debit, credit, or store-value cards to receive distributions from an HSA for qualified medical expenses? Yes. 129

130 FDIC Insurance Coverage If the HSA account satisfies the revocable trust rules, then the $250,000 limit which applies to such accounts will apply. If the account fails to satisfy the revocable trust rules, then the $250,000 limit which applies to single/individual accounts will apply. 130

131 HSA Reporting Penalties IRS Code 6693(a)(2) calls for $50 minimum penalty for each reporting failure. 131

132 call us at or send an to Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may be reproduced in any form and by any means without prior written permission from Collin W. Fritz & Associates, Ltd.

HSAs. Health Savings Accounts and 2018 Limits. Questions & Answers

HSAs Health Savings Accounts 2017 and 2018 Limits Questions & Answers What is a Health Savings Account (HSA)? An HSA is a tax-exempt trust or custodial account established for the purpose of paying medical

HSAs Health Savings Accounts 2017 and 2018 Limits Questions & Answers What is a Health Savings Account (HSA)? An HSA is a tax-exempt trust or custodial account established for the purpose of paying medical

Q&A on Federal Tax Aspects of Health Savings Accounts

Q&A on Federal Tax Aspects of Health Savings Accounts OVERVIEW AND ELIGIBILITY REQUIREMENTS What is a Health Savings Account? A Health Savings Account (HSA) is a tax-exempt trust or custodial account created

Q&A on Federal Tax Aspects of Health Savings Accounts OVERVIEW AND ELIGIBILITY REQUIREMENTS What is a Health Savings Account? A Health Savings Account (HSA) is a tax-exempt trust or custodial account created

Health Savings Accounts

Your State Association Presents Health Savings Accounts Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast. Be sure to print enough copies

Your State Association Presents Health Savings Accounts Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast. Be sure to print enough copies

Inherited Traditional IRAs for Non-Spouse Beneficiaries.

Rev2/15/2018 Inherited Traditional IRAs for Non-Spouse Beneficiaries. We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly. 8:30

Rev2/15/2018 Inherited Traditional IRAs for Non-Spouse Beneficiaries. We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly. 8:30

pay or reimburse qualified medical expenses.

Health Savings Accounts (HSAs) Notice 2004 2 PURPOSE This notice provides guidance on Health Savings Accounts. BACKGROUND Section 1201 of the Medicare Prescription Drug, Improvement, and Modernization

Health Savings Accounts (HSAs) Notice 2004 2 PURPOSE This notice provides guidance on Health Savings Accounts. BACKGROUND Section 1201 of the Medicare Prescription Drug, Improvement, and Modernization

HEALTH SAVINGS ACCOUNT

HEALTH SAVINGS ACCOUNT Under 223(a) of the Internal Revenue Code TRUST AGREEMENT AND DISCLOSURE STATEMENT Form 5305-B (August 2004) Department of the Treasury Internal Revenue Service HSA Health Savings

HEALTH SAVINGS ACCOUNT Under 223(a) of the Internal Revenue Code TRUST AGREEMENT AND DISCLOSURE STATEMENT Form 5305-B (August 2004) Department of the Treasury Internal Revenue Service HSA Health Savings

HEALTH SAVINGS ACCOUNT. Straight Answers to Your HSA Questions HSA OVERVIEW HSA ELIGIBILITY. What is a Health Savings Account?

Straight Answers to Your HSA Questions HSA OVERVIEW What is a Health Savings Account? A Health Savings Account (HSA) is a taxexempt trust or custodial account established for the purpose of paying or reimbursing

Straight Answers to Your HSA Questions HSA OVERVIEW What is a Health Savings Account? A Health Savings Account (HSA) is a taxexempt trust or custodial account established for the purpose of paying or reimbursing

ARTICLE I ARTICLE II ARTICLE III ARTICLE V

Health Savings Custodial Account (Under section 223(a) of the Internal Revenue Code) Form 5305-C (Rev. December 2011) Department of the Treasury, Internal Revenue Service. Do not file with the Internal

Health Savings Custodial Account (Under section 223(a) of the Internal Revenue Code) Form 5305-C (Rev. December 2011) Department of the Treasury, Internal Revenue Service. Do not file with the Internal

Instructions for Form 8889

2017 Instructions for Form 8889 Health Savings Accounts (HSAs) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future Developments

2017 Instructions for Form 8889 Health Savings Accounts (HSAs) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future Developments

1. New IRA Contribution Limits for IRA Transfers 3. IRA Rollovers (k) Direct Rollovers 5. Fraudulent contributions

Direct Rollovers 5. Fraudulent contributions") 1. New IRA Contribution Limits for 2013 2. IRA Transfers 3. IRA Rollovers 4. 401(k) Direct Rollovers 5. Fraudulent contributions Rev 12-5-2012 Just a Reminder: This is copyrighted material. No Video or

1. New IRA Contribution Limits for 2013 2. IRA Transfers 3. IRA Rollovers 4. 401(k) Direct Rollovers 5. Fraudulent contributions Rev 12-5-2012 Just a Reminder: This is copyrighted material. No Video or

Business & Health Savings Accounts

HSAs Business & Health Savings Accounts 2017 and 2018 Limits Questions & Answers Purpose The purpose of this brochure is to present a business decision-maker with basic information about HSAs so a business

HSAs Business & Health Savings Accounts 2017 and 2018 Limits Questions & Answers Purpose The purpose of this brochure is to present a business decision-maker with basic information about HSAs so a business

A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA

Rev 7/11/2018 A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting

Rev 7/11/2018 A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting

11. I understand that I may update or change my account beneficiaries at any time using the beneficiary change form on the HSA website.

1. I hereby establish a Health Savings Account ("HSA") under the terms and conditions contained in the accompanying HSA Custodial Account Agreement. This HSA becomes effective upon the acceptance of the

1. I hereby establish a Health Savings Account ("HSA") under the terms and conditions contained in the accompanying HSA Custodial Account Agreement. This HSA becomes effective upon the acceptance of the

AN EMPLOYER S GUIDE TO HEALTH SAVINGS ACCOUNTS (HSAs)

") AN EMPLOYER S GUIDE TO HEALTH SAVINGS ACCOUNTS (HSAs) By Larry Grudzien Attorney at Law Updated May 2012 2012 Larry Grudzien, Attorney at Law All Right Reserved QUESTIONS AND ANSWERS PAGE 1 Why should

AN EMPLOYER S GUIDE TO HEALTH SAVINGS ACCOUNTS (HSAs) By Larry Grudzien Attorney at Law Updated May 2012 2012 Larry Grudzien, Attorney at Law All Right Reserved QUESTIONS AND ANSWERS PAGE 1 Why should

Health Savings Account (HSA) Information for 2018

Information for 2018") Health Savings Account (HSA) Information for 2018 Note: The information contained herein may not necessarily apply to your unique situation and circumstances or take into account your tax situation. There

Health Savings Account (HSA) Information for 2018 Note: The information contained herein may not necessarily apply to your unique situation and circumstances or take into account your tax situation. There

Health Savings Accounts, Medical Savings Accounts and Long-Term Care Contracts

Health Savings Accounts, Medical Savings Accounts and Long-Term Care Contracts Contents In this module the student will review Health Savings Accounts, Archer Medical Savings Accounts and Long -Term Care

Health Savings Accounts, Medical Savings Accounts and Long-Term Care Contracts Contents In this module the student will review Health Savings Accounts, Archer Medical Savings Accounts and Long -Term Care

Health Savings Accounts

Health Savings Accounts Who s Eligible? Covered by a high deductible health plan (HDHP) Not covered by other health insurance Not enrolled in Medicare Not claimed as a dependent on someone else s tax return

Health Savings Accounts Who s Eligible? Covered by a high deductible health plan (HDHP) Not covered by other health insurance Not enrolled in Medicare Not claimed as a dependent on someone else s tax return

Session # 1 Establishing and Contributing

11/15/2018 Session # 1 Establishing and Contributing We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly 8:30 am CST or 12:30

11/15/2018 Session # 1 Establishing and Contributing We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly 8:30 am CST or 12:30

IRS PROVIDES GUIDANCE ON HEALTH SAVINGS ACCOUNTS

IRS PROVIDES GUIDANCE ON HEALTH SAVINGS ACCOUNTS Page 1 of 5 IRS has issued guidance on Health Savings Accounts (HSAs), a new type of tax-favored vehicle created by the Medicare Act of 2003, which was

IRS PROVIDES GUIDANCE ON HEALTH SAVINGS ACCOUNTS Page 1 of 5 IRS has issued guidance on Health Savings Accounts (HSAs), a new type of tax-favored vehicle created by the Medicare Act of 2003, which was

Andrews University. Healthcare Savings Accounts (HSA) And High Deductible Health Plans (HDHP)

And High Deductible Health Plans (HDHP)") Andrews University Healthcare Savings Accounts (HSA) And High Deductible Health Plans (HDHP) Andrews University HSA/HDHP Why? A tax vehicle to set aside money for current and future medical expenses The

Andrews University Healthcare Savings Accounts (HSA) And High Deductible Health Plans (HDHP) Andrews University HSA/HDHP Why? A tax vehicle to set aside money for current and future medical expenses The

Employee Health Benefits

Employee Health Benefits Table of Contents 1. Overview... 1 2. Training Objectives... 2 3. Resources... 3 4. Health Savings Accounts... 4 a. Benefits of an HSA account... 4 b. Who Qualifies for an HSA?...

Employee Health Benefits Table of Contents 1. Overview... 1 2. Training Objectives... 2 3. Resources... 3 4. Health Savings Accounts... 4 a. Benefits of an HSA account... 4 b. Who Qualifies for an HSA?...

RMD Impact When a Surviving Spouse Elects to Treat the Deceased Spouse s IRA as Their Own

Published Since 1984 ALSO IN THIS ISSUE HSA Contribution Limits for Domestic Partners and Other Unmarried Individuals Versus Married Individuals, Page 3 Handling Excess IRA Contributions for 2008 and 2009,

Published Since 1984 ALSO IN THIS ISSUE HSA Contribution Limits for Domestic Partners and Other Unmarried Individuals Versus Married Individuals, Page 3 Handling Excess IRA Contributions for 2008 and 2009,

Q&A on Qualified High Deductible Health Plans (HDHP s) and Health Savings Accounts (HSA s)

and Health Savings Accounts (HSA s)") Q&A on Qualified High Deductible Health Plans (HDHP s) and Health Savings Accounts (HSA s) Q. What is a Health Savings Account ( HSA )? A. A Health Savings Account is an alternative to traditional health

Q&A on Qualified High Deductible Health Plans (HDHP s) and Health Savings Accounts (HSA s) Q. What is a Health Savings Account ( HSA )? A. A Health Savings Account is an alternative to traditional health

Single HDHP $3,400 $3,450 Family HDHP $6,750 $6, Single HDHP $4,400 $4,450 Family HDHP $7,750 $7,900

Published Since 1984 ALSO IN THIS ISSUE IRS Issues 2018 Indexed Amounts for HSAs Page 1 RMD Box 11 on Form 5498 Is Not Checked for an IRA Beneficiary Page 2 Completing the 2016 Form 5498-A Page 3 Email

Published Since 1984 ALSO IN THIS ISSUE IRS Issues 2018 Indexed Amounts for HSAs Page 1 RMD Box 11 on Form 5498 Is Not Checked for an IRA Beneficiary Page 2 Completing the 2016 Form 5498-A Page 3 Email

Kitsap Bank Health Savings Account Guide. A tax-smart way for you to manage growing healthcare costs.

Kitsap Bank Health Savings Account Guide A tax-smart way for you to manage growing healthcare costs. At Kitsap Bank, we believe that helping you prepare for the rising cost of health care is key to helping

Kitsap Bank Health Savings Account Guide A tax-smart way for you to manage growing healthcare costs. At Kitsap Bank, we believe that helping you prepare for the rising cost of health care is key to helping

Traditional SEP, and SIMPLE IRAs

Traditional SEP, and SIMPLE IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why must I and others age 70 1/2 or older have to take a required distribution? The purpose of an IRA

Traditional SEP, and SIMPLE IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why must I and others age 70 1/2 or older have to take a required distribution? The purpose of an IRA

ALSO IN THIS ISSUE. IRS Issues Guidance on IRA/Roth IRA transfers to an HSA

Published Since 1984 ALSO IN THIS ISSUE Appreciated Guidance on the Special Testing Period Taxes, Page 4 IRS Issues Guidance on HSA Contributions for 2007, 2008 and Later Years, Page 6 Collin W. Fritz

Published Since 1984 ALSO IN THIS ISSUE Appreciated Guidance on the Special Testing Period Taxes, Page 4 IRS Issues Guidance on HSA Contributions for 2007, 2008 and Later Years, Page 6 Collin W. Fritz

Health Savings Accounts

Oppenheimer & Co. Inc. Spencer Nurse Executive Director - Investments 500 108th Ave. NE Suite 2100 Bellevue, WA 98004 425-709-0540 800-531-3110 spencer.nurse@opco.com http://fa.opco.com/spencer.nurse/index.htm

Oppenheimer & Co. Inc. Spencer Nurse Executive Director - Investments 500 108th Ave. NE Suite 2100 Bellevue, WA 98004 425-709-0540 800-531-3110 spencer.nurse@opco.com http://fa.opco.com/spencer.nurse/index.htm

HEALTH SAVINGS CUSTODIAL ACCOUNT AGREEMENT

HEALTH SAVINGS CUSTODIAL ACCOUNT AGREEMENT Form 5305-C under section 223(a) of the Internal Revenue Code. FORM (December 2011) The account owner named on the application is establishing this health savings

HEALTH SAVINGS CUSTODIAL ACCOUNT AGREEMENT Form 5305-C under section 223(a) of the Internal Revenue Code. FORM (December 2011) The account owner named on the application is establishing this health savings

Health Savings Account (HSA)

") What is a Health Savings Account? Health Savings Account (HSA) A Health Savings Account (HSA) is a tax-advantaged health care account that you own. You contribute to it with tax-free or tax-deductible

What is a Health Savings Account? Health Savings Account (HSA) A Health Savings Account (HSA) is a tax-advantaged health care account that you own. You contribute to it with tax-free or tax-deductible

Traditional IRAs. Understanding Required Distributions at 70 1 / 2. Questions & Answers

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

Payroll-Deduction IRA Programs. Keogh Close-Out in 2004 Don t Forget the 2004 Form 5500-EZ ALSO IN THIS ISSUE. November 2004 Published Since 1984

November 2004 Published Since 1984 ALSO IN THIS ISSUE Hardship Distributions from a 401(k) Plan Versus an IRA, Page 2 Completing the 2004 Form 5498-SA, Page 3 Completing the 2004 Form 1099-SA, Page 4 Comparison

November 2004 Published Since 1984 ALSO IN THIS ISSUE Hardship Distributions from a 401(k) Plan Versus an IRA, Page 2 Completing the 2004 Form 5498-SA, Page 3 Completing the 2004 Form 1099-SA, Page 4 Comparison

Warning Don t Move Inherited IRA Funds to the Estate Checking Account Too Quickly

Published Since 1984 ALSO IN THIS ISSUE Transferring of a Credit Union s Inherited IRA, Page 2 Interesting Inherited IRA Situation, Page 3 Should HSAs be Added to Internet Banking Accounts?, Page 4 Special

Published Since 1984 ALSO IN THIS ISSUE Transferring of a Credit Union s Inherited IRA, Page 2 Interesting Inherited IRA Situation, Page 3 Should HSAs be Added to Internet Banking Accounts?, Page 4 Special

Health Savings Account (HSA) Amendment-Custodial

Amendment-Custodial") Health Savings Account (HSA) Amendment Dear HSA Owner: The purpose of this Amendment is to incorporate changes in law and policy that affect your Health Savings Account (HSA) agreement. This Amendment

Health Savings Account (HSA) Amendment Dear HSA Owner: The purpose of this Amendment is to incorporate changes in law and policy that affect your Health Savings Account (HSA) agreement. This Amendment

HEALTH SAVINGS ACCOUNT. Under 223(a) of the Internal Revenue Code CUSTODIAL AGREEMENT AND DISCLOSURE STATEMENT

of the Internal Revenue Code CUSTODIAL AGREEMENT AND DISCLOSURE STATEMENT") HEALTH SAVINGS ACCOUNT Under 223(a) of the Internal Revenue Code CUSTODIAL AGREEMENT AND DISCLOSURE STATEMENT Form 5305-C (December 2011) Department of the Treasury Internal Revenue Service HSA Health

HEALTH SAVINGS ACCOUNT Under 223(a) of the Internal Revenue Code CUSTODIAL AGREEMENT AND DISCLOSURE STATEMENT Form 5305-C (December 2011) Department of the Treasury Internal Revenue Service HSA Health

HSA Frequently Asked Questions

HSA Frequently Asked Questions Overview Q1. WHAT IS A HEALTH SAVINGS ACCOUNT (HSA)? An HSA is a tax-exempt trust or custodial account established exclusively for the purpose of paying qualified medical

HSA Frequently Asked Questions Overview Q1. WHAT IS A HEALTH SAVINGS ACCOUNT (HSA)? An HSA is a tax-exempt trust or custodial account established exclusively for the purpose of paying qualified medical

The Webinar will be starting shortly

7/11/2018 The Webinar will be starting shortly 8:45 am CST or 1:00 pm CST Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may

7/11/2018 The Webinar will be starting shortly 8:45 am CST or 1:00 pm CST Copyright 2018 Collin W. Fritz & Associates, Ltd. The Pension Specialists All rights reserved. No part of this presentation may

Comprehensive Inherited Traditional IRA Amendment. Trust

ified HSA funding distribution, a qualified charitable distribution, the return of certain excess contributions or the return of certain current year contributions. If you are required to file one or more

ified HSA funding distribution, a qualified charitable distribution, the return of certain excess contributions or the return of certain current year contributions. If you are required to file one or more

Health Savings Accounts: Overview of Rules for 2010

Health Savings Accounts: Overview of Rules for 2010 Janemarie Mulvey Specialist in Aging and Income Security September 9, 2010 Congressional Research Service CRS Report for Congress Prepared for Members

Health Savings Accounts: Overview of Rules for 2010 Janemarie Mulvey Specialist in Aging and Income Security September 9, 2010 Congressional Research Service CRS Report for Congress Prepared for Members

HEALTH SAVINGS ACCOUNT (HSA) PROCEDURE MANUAL

PROCEDURE MANUAL") HEALTH SAVINGS ACCOUNT (HSA) PROCEDURE MANUAL January 1, 2018 JM Consultants 6930 Glory Road Baxter, MN 56425 218-831-1858 www.jmcmnelson. Introduction This manual on Health Savings Accounts (HSAs) is

HEALTH SAVINGS ACCOUNT (HSA) PROCEDURE MANUAL January 1, 2018 JM Consultants 6930 Glory Road Baxter, MN 56425 218-831-1858 www.jmcmnelson. Introduction This manual on Health Savings Accounts (HSAs) is

Health Savings Account (HSA) FAQ s

FAQ s") Health Savings Account (HSA) FAQ s 1. What is a Health Savings Account? (Also known as a HSA) A Health Savings Account (HSA) combines a high deductible health plan with a savings account to help pay for

Health Savings Account (HSA) FAQ s 1. What is a Health Savings Account? (Also known as a HSA) A Health Savings Account (HSA) combines a high deductible health plan with a savings account to help pay for

Establishing a SEP for 2014

Published Since 1984 ALSO IN THIS ISSUE Understanding Box 2 (Rollover Contributions) on the 2014 Form 5498, Page 2 Administering An HSA After the HSA Owner Dies, Page 4 Email Guidance - No Authority Exists

Published Since 1984 ALSO IN THIS ISSUE Understanding Box 2 (Rollover Contributions) on the 2014 Form 5498, Page 2 Administering An HSA After the HSA Owner Dies, Page 4 Email Guidance - No Authority Exists

No Form 1099-R Prepared to Report IRA Funds Moving From the Decedent s IRA to an Inherited IRA

Published Since 1984 2015 Tax Filing Deadline is April 18, 2016 ALSO IN THIS ISSUE 2015 Form 5500 Series Returns Should Not Answer the Compliance Questions, Page 2 Inherited IRA Situation - Daughter Dies,

Published Since 1984 2015 Tax Filing Deadline is April 18, 2016 ALSO IN THIS ISSUE 2015 Form 5500 Series Returns Should Not Answer the Compliance Questions, Page 2 Inherited IRA Situation - Daughter Dies,

IRS Issues 2013 COLAs. New IRA Contribution Limits for 2013 $5,500 and $6,500 ALSO IN THIS ISSUE

Published Since 1984 ALSO IN THIS ISSUE New IRA Contribution Limits for 2013 $5,500 and $6,500 IRA Contribution Deductibility Charts for 2012 and 2013, Page 2 Roth IRA Contribution Charts for 2012 and

Published Since 1984 ALSO IN THIS ISSUE New IRA Contribution Limits for 2013 $5,500 and $6,500 IRA Contribution Deductibility Charts for 2012 and 2013, Page 2 Roth IRA Contribution Charts for 2012 and

CRS Report for Congress

Order Code RL33257 CRS Report for Congress Received through the CRS Web Health Savings Accounts: Overview of Rules for 2006 January 31, 2006 Bob Lyke Specialist in Social Legislation Domestic Social Policy

Order Code RL33257 CRS Report for Congress Received through the CRS Web Health Savings Accounts: Overview of Rules for 2006 January 31, 2006 Bob Lyke Specialist in Social Legislation Domestic Social Policy

Health Savings Plan and Health Savings Account. Business Rules and Detailed Design Features for 2016

Health Savings Plan and Health Savings Account Business Rules and Detailed Design Features for 2016 i Table of Contents 1. Definition of Terms 1A High Deductible Health Plan 2 1B Health Savings Plan (HSP)

Health Savings Plan and Health Savings Account Business Rules and Detailed Design Features for 2016 i Table of Contents 1. Definition of Terms 1A High Deductible Health Plan 2 1B Health Savings Plan (HSP)

Health Savings Accounts

Health Savings Accounts Forrest T. Jones & Company, Inc. Updated for 2013 What is an HSA? PART 1 HDHP High Deductible Health Plan PART 2 HSA Health Savings Account 2 Parts to an HSA Intended to cover serious

Health Savings Accounts Forrest T. Jones & Company, Inc. Updated for 2013 What is an HSA? PART 1 HDHP High Deductible Health Plan PART 2 HSA Health Savings Account 2 Parts to an HSA Intended to cover serious

HSA Questions and Answers

Brought to you by Sentinel Benefits & Financial Group HSA Questions and Answers This Legislative Brief sets out Questions and Answers regarding Health Savings Accounts (HSAs), as provided by the Internal

Brought to you by Sentinel Benefits & Financial Group HSA Questions and Answers This Legislative Brief sets out Questions and Answers regarding Health Savings Accounts (HSAs), as provided by the Internal

is a qualified Hurricane Katrina distribution.

September 2005 Published Since 1984 ALSO IN THIS ISSUE IRA Disclaimers New IRS Guidance, Page 3 Modified Adjusted Gross Income (MAGI) for Roth IRA Contribution Purposes, Page 4 Tax Treatment of HSA Upon

September 2005 Published Since 1984 ALSO IN THIS ISSUE IRA Disclaimers New IRS Guidance, Page 3 Modified Adjusted Gross Income (MAGI) for Roth IRA Contribution Purposes, Page 4 Tax Treatment of HSA Upon

Health Savings Accounts: Innovative Health Care Financing

Health Savings Accounts: Innovative Health Care Financing Would you be interested in a health insurance program that puts you in control of your own health care dollars, while protecting you and your family

Health Savings Accounts: Innovative Health Care Financing Would you be interested in a health insurance program that puts you in control of your own health care dollars, while protecting you and your family

IRS Issues 2014 IRA/Pension Limits. IRA Contribution Limits for 2014 Unchanged at $5,500 and $6,500 ALSO IN THIS ISSUE

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Deductibility Charts 2013 and 2014, Page 2 Roth IRA Contribution Charts for 2013 and 2014, Page 3 SEP and SIMPLE Limits, Page 3 Saver s Credit Limits

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Deductibility Charts 2013 and 2014, Page 2 Roth IRA Contribution Charts for 2013 and 2014, Page 3 SEP and SIMPLE Limits, Page 3 Saver s Credit Limits

Health Savings Accounts: An Employer Overview

Health Savings Accounts: An Employer Overview Since salary alone is often not enough to attract and retain valued employees, what can your business do to enhance its employee benefits package? Table of

Health Savings Accounts: An Employer Overview Since salary alone is often not enough to attract and retain valued employees, what can your business do to enhance its employee benefits package? Table of

Health Savings Accounts

Health Savings Accounts In an effort to respond to the rising cost of health insurance, many employers have made use of tax-favored accounts such as health flexible spending accounts (health FSAs), health

Health Savings Accounts In an effort to respond to the rising cost of health insurance, many employers have made use of tax-favored accounts such as health flexible spending accounts (health FSAs), health

IRAs & Roth IRAs. Beneficiary or Inherited IRAs. Questions & Answers

IRAs & Roth IRAs Beneficiary or Inherited IRAs Questions & Answers Purpose The purpose of this brochure is to provide a person who is a beneficiary of a traditional IRA (including SEPs and SIMPLEs) or

IRAs & Roth IRAs Beneficiary or Inherited IRAs Questions & Answers Purpose The purpose of this brochure is to provide a person who is a beneficiary of a traditional IRA (including SEPs and SIMPLEs) or

Get Started with a Health Savings Account

Get Started with a Health Savings Account www.discoverybenefits.com Health saving account a triple savings Contribute tax- free Grow your funds tax-free Spend tax-free Benefits of an HSA A combination

Get Started with a Health Savings Account www.discoverybenefits.com Health saving account a triple savings Contribute tax- free Grow your funds tax-free Spend tax-free Benefits of an HSA A combination

2008 IRS Reporting for a Conversion of Eligible Retirement (ERP) Funds to a Roth IRA

Funds to a Roth IRA") Published Since 1984 ALSO IN THIS ISSUE Required Minimum Distribution Rules for 401(k) Plans & IRAs are similar, Page 5 IRS Announces New Online EIN Application Process, Page 5 Discussion and Illustration

Published Since 1984 ALSO IN THIS ISSUE Required Minimum Distribution Rules for 401(k) Plans & IRAs are similar, Page 5 IRS Announces New Online EIN Application Process, Page 5 Discussion and Illustration

Are IRA Amendments Required For ?

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

Three Planning Concepts Why More Individuals Will Want Profit Sharing or One Person 401(k) Plans!

Plans!") Published Since 1984 ALSO IN THIS ISSUE Preparing Two 1099-R Forms is Never Correct When There is Federal Withholding, Page 2 Possible Expansion of the Saver Tax Credit, Page 3 H&H Block Lawsuit Settlement

Published Since 1984 ALSO IN THIS ISSUE Preparing Two 1099-R Forms is Never Correct When There is Federal Withholding, Page 2 Possible Expansion of the Saver Tax Credit, Page 3 H&H Block Lawsuit Settlement

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt

Understanding What Forms Are Needed to Establish a SIMPLE IRA Plan And a SIM- PLE IRA

* Published Since 1984 ALSO IN THIS ISSUE What Is The IRA Custodian To Do When a SEP-IRA Owner or a SIM- PLE IRA Owner Dies? Page 3 Special Transition Rules To Apply From April 10, 2017 to January 1, 2018

* Published Since 1984 ALSO IN THIS ISSUE What Is The IRA Custodian To Do When a SEP-IRA Owner or a SIM- PLE IRA Owner Dies? Page 3 Special Transition Rules To Apply From April 10, 2017 to January 1, 2018

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy