Health Savings Accounts

|

|

|

- Molly Dickerson

- 6 years ago

- Views:

Transcription

1 Your State Association Presents Health Savings Accounts Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast. Be sure to print enough copies for all listeners. Tuesday, January 26, 2016 Presenter: Christy Crawford Technical Support (for faster service please submit inquiries via or online): (Registration & Tech Support): - Phone- (877) FOR ADDITIONAL ASSISTANCE PLEASE REFER TO OUR FAQs

2 Health Savings Accounts Instructor Christy Crawford Hello and welcome to the program. If you have any questions just call us at or us at christyjcrawford@msn.com Christy Crawford is president of Christy Crawford Consulting specializing in the education of banks and credit unions across the nation. Christy is an associate speaker for Gettechnical Inc. As a former trainer for Wal Mart Corporation, and former V.P. of Gettechnical Inc. she brings her previous 12 years of sales and training experience to your financial institution. She earned a bachelor's degree from Louisiana State University and is BSA/AML certified. Her expertise is in the deposit side of the financial institution and focuses on teller, new accounts, IRAs, HSAs, robbery, security and BSA for the frontline training. Robbery Prevention 2 1

3 Overview Medical Savings Accounts (MSAs) Program The pilot program for Archer MSAs ended December 31, Your accountholder can participate in an Archer MSA after 2003 only if: Your accountholder was an active Archer MSA participant before January 1, 2004, or Your accountholder becomes an active Archer MSA participant after 2003 because your accountholder is covered by a high deductible health plan of an Archer MSA participating employer 4 2

, discussed later.")

4 (HSAs) A health savings account (HSA) is a tax exempt trust or custodial account that your accountholder sets up with a U.S. financial institution (such as a bank or an insurance company) which allows your accountholder to pay or be reimbursed for certain medical expenses. This account must be used in conjunction with a high deductible health plan (HDHP), discussed later. 5 The HSA can be established using a qualified trustee or custodian that is different from the HDHP provider. Contributions to an HSA must be made in cash (includes checks) or through a cafeteria plan. Contributions of stock or property are not allowed. High Deductible Health Plan HSA Account 6 3

5 Health Savings Account What is a Health Savings Account? Tax-exempt trust or custodial account at a financial institution Established exclusively for the purpose of paying qualified medical expenses Contributions are made for those covered by HDHP Eligibility is determined each month 7 If your accountholder has an Archer MSA, your accountholder can generally roll it over into an HSA tax free. are individually owned plans. 8 4

6 He can have an HSA! She can have an HSA! Can they have a Joint HSA? NO But now can have Authorized Signers on the Account. Notice question 28 9 Benefits of an HSA to your accountholder Your accountholder can claim tax deduction for contributions he or she made Benefits An HSA is portable Contributions made by accountholder s employer may be excluded from gross income. If you do not use your contributions, you do not lose them. Tax free interest Distributions may be tax free if your accountholder pays qualified medical expenses. 10 5

7 To qualify for Health Savings Account To Qualify Be covered by a high deductible health plan (HDHP). The HSA owner may have no other health insurance coverage The accountholder is not enrolled in Medicare The HSA owner cannot be claimed as a dependent 11 Watch Medicare. Once the accountholder is enrolled in Medicare he or she is no longer eligible for a contribution in the month they enroll. 12 6

8 High Deductible Health Plan (HDHP) High Deductible Health Plan A higher annual deductible than typical health plans A maximum limit on the sum of the annual deductible and out of pocket medical expenses that your accountholder must pay for covered expenses. Out of pocket expenses include deductible, co payments and other amounts, but do not include premiums 14 7

9 Limits The following table shows the minimum annual deductible and maximum annual deductible and other out of pocket expenses for HDHPs. 15 Types of Coverage Self only coverage Minimum annual deductible of $1,300 for 2015 $1,300 for 2016 (no change) Maximum out-of-pocket expenses $6,450 for 2015 $6,550 for 2016 Family Coverage Minimum annual deductible of $2,600 for 2015 $2,600 for 2016 (no change) Maximum out-of-pocket expenses $12,900 for 2015 $13,100 for

10 Other health insurance The accountholder (or the accountholder s spouse if he or she files jointly) generally cannot have any other health plan that is not an HDHP. 17 However, this rule does not apply if the other health plan(s) only covers the following items: Accidents. Disability. Dental care. Vision care. Long term care. Benefits related to workers' compensation laws, tort liabilities, or ownership or use of property. A specific disease or illness. A fixed amount per day (or other period) of hospitalization. 18 9

11 Plans in which substantially all of the coverage is through the above listed items are not HDHPs. For example, if the accountholder s plan provides coverage substantially all of which is for a specific disease or illness, the plan is not an HDHP for purposes of establishing an HSA. 19 Preventative Care A HDHP may provide preventive care benefits without a deductible or with a deductible below the minimum annual deductible. Preventative care includes but is not limited to the following: Periodic health evaluations, including tests and diagnostic procedures ordered in connection with routine examinations, such as annual physicals. Routine prenatal and well child care. Child and adult immunizations. Tobacco cessation programs. Obesity weight loss programs Screen services

12 Screen services. This includes screening for the following: Cancer Heart and vascular diseases Infectious diseases Mental health conditions Substance abuse Metabolic, nutritional, and endocrine conditions Musculoskeletal disorders Obstetric and gynecological conditions Pediatric conditions Vision and hearing disorders 21 Prescription Drug Plans The accountholder can have a prescription drug plan, either as part of his or her HDHP or a separate plan (or rider), and qualify as an eligible individual if the plan does not provide benefits until the minimum annual deductible of the HDHP has been met. The accountholder is not an eligible individual if he or she receives benefits before the deductible is met. Also, discount cards do not affect eligibility for a Health Savings Account

13 Other employee health plans An employee may have an option between High Deductible insurance and a low deductible plan. If the employee chooses the high deductible plan, he or she is eligible for a Health Savings Account. It does not matter that the employee could have chosen a low deductible plan. 23 Other employee health plans An employee covered by a High Deductible Health Plan (HDHP) and a Flexible Spending Arrangement (FSA) or a Health Reimbursement Arrangement (HRA) cannot generally make contributions to a Health Savings Account (HSA). However, the employee or your accountholder can make contributions to a HSA while covered by HDHP and one or more of the following: Limited purpose health FSA or HRA Suspended HRA Post deductible health FSA or HRA Retirement HRA 24 12

14 Eligibility and Contributions The amount the accountholder, the accountholder s family members, or the accountholder s employer can contribute to the HSA depends on: the type of HDHP coverage he or she has age 26 13

15 If the accountholder has self only coverage, he or she can contribute up to the amount of $3,350 (2015 & 2016) and ($1,000 catch up if he or she is age 55 or older). If the accountholder has family coverage, the customer can contribute up to the amount of $6,650 (2015)/$6,750 (2016) ($1,000 catch up if your accountholder is age 55 or older). See Rules for married people (discussed later). 27 How Much Can The Customer Contribute? Self Only Coverage Family Coverage $3,350 (2015) $3,350 (2016) (55 or older add $1,000 catch-up contribution) $6,650 (2015) $6,750 (2016) (55 or older add $1,000 catch-up contribution) 28 14

16 Contribution Limit Contributions to a health savings account (HSA) are no longer limited to the annual health plan deductible. 29 The annual contribution deduction limit is $3,300 (2014) /$3,350 (2015) if your accountholder has a high deductible health plan with self only coverage, or $6,550 (2014) /$6,650 (2015) if he or she has family coverage. If he or she is age 55 or older at the end of the year, the additional contribution amount is $1,

17 Your accountholder s maximum contribution is the greater of the following: 1. Sum of the months first day of each month plus catch up; or 2. Maximum annual contribution based on first day of the last month of the individual s tax year. 31 Sum of the monthly contribution limits The maximum annual contribution to an HSA is the sum of the contribution limits determined separately for each month, based on eligibility and health plan coverage on the first day of the month

18 Sum of the months for 2016 Contribution Amount January Self only coverage February Self only coverage March April May June July August September October November December Total for the year $ $ $ Full contribution rule An individual who is an eligible individual on the first day of the last month of the taxable year is treated as an eligible individual for the entire year and may increase, but not decrease, the contribution limit for such an individual. Thus, in order to make a full contribution for the year, a taxpayer must be an eligible individual on the first day of the last month of his or her taxable year (December 1 for calendar year taxpayers)

19 Full Contribution for 2016 contribution amount January no coverage February no coverage March no coverage April no coverage May no coverage June no coverage July no coverage August no coverage September no coverage October no coverage November no coverage December Full Family coverage Total for the year $6, $6, This full contribution rule also applies to catch up contributions. The full contribution rule applies without regard to whether the individual was an eligible individual for the entire year, had HDHP coverage for the entire year, or had disqualifying non HDHP coverage for part of the year. However, a testing period applies for purposes of the full contribution rule

20 The Testing Period The testing period applies to an individual who is an eligible individual on the first day of the last month of the taxable year. The testing period begins on the first day of the last month of the taxable year and ends on the last day of the 12 month following that month. 37 In other words. For a calendar year taxpayer, the testing period is from December 1 of the current year to December 31 of the following year. If they fail to remain eligible during the testing period.oops they pay 10% penalty

21 Failure to remain an eligible individual during the testing period If an individual who is an eligible individual on the first day of the last month of the taxable year contributes an amount to his or her HSA greater than the sum of the monthly contribution limits and at any time during the testing period, the individual ceases to meet all requirements to be an eligible individual, an amount is included in the individual's gross income and subject to an additional 10 percent tax, unless the failure is due to disability or death. 39 To remain an eligible individual during the testing period, an individual is not required to keep the same level of HDHP coverage during the testing period. Thus, changing from family HDHP coverage to single HDHP coverage during the testing period does not result in inclusion of amounts in gross income or an additional 10 percent testing period tax

for filing the individual's federal")

22 Opening an HSA An individual may establish an HSA at any time on or after the date the individual becomes HSA eligible. 41 Contributions for the taxable year can be made in one or more payments, at any time prior to the time (without extensions) for filing the individual's federal income tax return for the taxable year

23 An individual who becomes an eligible individual after January 1 may make the maximum contribution to an HSA on the first day he or she is an eligible individual. Notice , Q&A No Effect On HSA Establishment Date Expenses incurred before an HSA is established are not qualified medical expenses

24 Reporting Neither employers nor trustees are responsible for reporting whether an individual remains an eligible individual during the testing period. 45 In order for both spouses to contribute a catch up contribution amount both must have HSAs. The accountholder can make contributions to his or her HSA for 2015 until April 15, Between January 1 st and April 15 th your accountholder can be making contributions for two tax years

25 Accountholder Tax Issues on Contributions 48 24

26 IN OUT

27 Financial Institution s Compliance Issues on Contributions CONTRIBUTIONS May be made by THE HSA OWNER EMPLOYER FAMILY accountholder 52 26

28 Type of contributions: Regular Catch up contributions Rollover from another Health Savings Account Rollover from an Archer Medical Savings Account Transfer from a Health Savings Account Transfer from an Archer Medical Savings Account One time rollover from FSA or HRA One time rollover from IRA 53 Note: Remember the Archer Medical Savings Account is grandfathered in. It was the original product. It was upgraded and turned into a permanent product with the Health Savings Account. Many accountholders are moving funds from the old Archer Medical Savings Account into the new Health Savings Account. That is why you will see rollovers and transfers from these accounts

29 When does the accountholder make the contributions The accountholder qualifies for the contribution on the first day of every month. However, the accountholder does not have to fund the HSA until April 15th of the year following the year it is for. The accountholder may not use it for a qualified expense that was incurred before the establishment of the HSA. The 2014 tax deadline is April 15th, Forms used by financial institutions There are many forms companies for financial institutions to choose from in setting up the. Most of the forms companies use the IRS model contracts Forms 5305C and 5305B. The forms companies usually provide a disclosure, beneficiary designation and spousal consent (community property states) which are familiar to most IRA accounts. You will not see a financial projection like you do on IRA accounts

Truth in Savings Disclosure (Regulation DD) Beneficiary designation (not required by IRS) 57 58")

30 Forms to open: Contract (5305B (Trust) or 5305C (Custodial) or Prototype) Disclosure (not required by IRS) Contribution form (not required by IRS) Truth in Savings Disclosure (Regulation DD) Beneficiary designation (not required by IRS)

31 59 may be invested in investments approved for IRAs. Certificates of Deposit Now Accounts Savings MMF Annuities Stocks, bonds or mutual funds And many more See IRS Guidance under section 408 (m) 60 30

32 The financial institution may restrict the type of accounts you will put them in under your trust or custodial agreement. You will have to give a Truth in Savings Disclosure to describe whatever investment you put the accountholder in. 61 More Than One Health Savings Account The accountholder may establish more than one health savings account. As long as, the amount that he or she is eligible for is not exceeded

33 Prohibited Transactions Our accountholders are bound by rules similar to IRAs on. The owner may not enter into prohibited transactions with the Health Savings Account. For example, the owner may not sell, exchange or lease property, borrow or lend money, furnish goods, services or facilities, transfer to or use by or for the benefit of himself/herself any assets, pledge the HSA assets. 63 Any amount used for a prohibited transaction will not be treated as used to pay for qualified medical expenses. The account beneficiary must, therefore, include the distribution in gross income and generally will be subject to the additional 20 % penalty on distributions not used to pay medical expenses

34 Fees If the financial institution charges fees for administration and account maintenance, the fees are not treated as taxable to the owner of the account. They will not be shown out of our product as a taxable distribution. The owner of the HSA cannot increase the amount of his or her contribution to cover the fee. If his or her limit is $3,350, he or she cannot add $25 more to cover the annual fee. 65 If the employer is paying administrative fees to a financial institution to handle all of the, these fees do not count towards the individual s contribution. This would be similar to a 401K. The employer pays a firm to administer a 401K but it is not considered a contribution to the retirement account of each employee

35 Trustees and Custodians Any bank, credit union or insurance company may act as trustee or custodian. The financial institution is not responsible for determining whether contributions exceed the amount allowed for the accountholder. It is our accountholder s responsibility to notify us if there is an excess in his or her account and withdrawing the excess. 67 In the contract, the financial institution has some responsibilities that cannot be changed. These include: Contributions except for rollovers and transfers must be in cash Contributions cannot exceed $7,750 ($6,750+$1,000 for 2016). Accountholder cannot invest Health Savings Account in life insurance Contribution is not forfeitable Cannot be commingled with other property unless in a common fund for investment purposes

36 The trustee and custodian responsibilities have to do with the proper opening and reporting of the accounts to the IRS. It is our responsibility to know the accountholder s age. We are allowed however to rely on the representation of the accountholder about his or her age. If they tell us incorrect ages, we will not be held accountable for that. 69 Trustees and custodians may place reasonable product restrictions on the number of withdrawals, minimum contributions, and minimum distributions. In Article XI of the contract under Specific Instructions and any that follow it, the financial institution may incorporate additional provisions

37 These may include: Rollover rules Investment Powers Voting rights Amendment and termination Removal of trustee and trustee s fees State law requirements Treatment of excess contributions Distribution procedures including fees and minimum amounts Use of debit or credit or stored value cards Return of Mistaken distributions Prohibited transactions 71 Regulation E Some financial institutions issue debit cards. Trust accounts are an exception to Regulation E. This means that you should not put the Error Resolution disclosure for Regulation E on the back of the HSA statement. You will need to set up by contract the liabilities between the parties for unauthorized use of the debit card as you do for business accounts

38 CIP Customer Identification Program (CIP) All accountholders have to be put through your institution s CIP. In this case, the accountholder would be the IRA HSA owner. On Education Savings Accounts you CIP the person acting for the child. You do not have to run CIP on the beneficiaries. At the death of the owner, the HSA becomes the spouse s HSA on the date of death. At that time, the accountholder would switch to the spouse and you would have to run the CIP on the spouse. 73 OFAC (Office of Foreign Assets Control) You must also run your accountholder and beneficiaries through the OFAC list. Your system may be automatically checking the owner, but may not check beneficiaries. Since we are not allowed to give funds to someone on the OFAC list you should check the beneficiaries to make sure not on list before turning the funds over at the death of the owner

39 Truth In Savings (TISA) TIS require financial institutions to provide disclosures regarding interest/dividends on deposits and fees that may be assessed against deposit accounts, so that consumers can compare the products offered by different financial institutions. are covered as deposits in TIS. 75 TISA Account Disclosures Must be delivered at account opening, upon request and within 10 days after opening an account by mail or receiving a request in writing. Content must include: rate information, balance information, fees, transaction limitations, features of time accounts

40 TISA Subsequent Disclosures If the financial institution makes an adverse change in a product the accountholder must receive a 30 day notice of the change. (No notice is required for short term time deposits of 30 days or less, variable rate accounts or check printing fees.) You must also give notices of maturity on time deposits within TIS guidelines. 77 TISA Periodic Statement Disclosures If a financial institution sends periodic statements, the statements must include the following disclosures to the extent that they apply to the account represented by the statement: Annual percentage yield earned, amount of interest, fees imposed, and number of days in a period

41 TISA Payment Of Interest Average Daily Balance Method Daily Balance Method 79 Another Signature Card Possibility 1 OWNERSHIP Trust Separate Agreement Beneficiaries: See Health Savings Account Application 5 TAXPAYER IDENTIFICATION NUMBER Sally Jane Smith 2 TITLE Sally Jane Smith Health Savings Account under Trust dated 2/16/20xx 3 FEDERAL REGULATIONS 4 SIGNATURES (Access) Sally Jane Smith 80 40

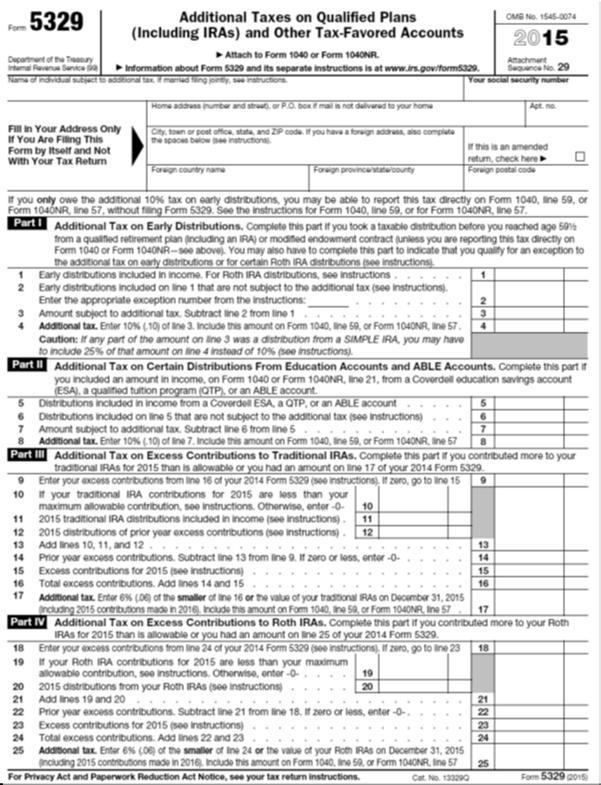

42 EXCESS CONTRIBUTIONS If your accountholder puts in more than is allowed by law into a Health Savings Account, the accountholder will have an excess in the account. An excess can be corrected by tax due date plus extensions like our friend the IRA. If the accountholder withdraws the excess contributions and earnings by tax due date plus extensions, the accountholder will have to claim the interest as income and pay a 20% penalty on the interest alone. 81 EXCESS CONTRIBUTIONS If the accountholder does not correct it at that time, the excess is subject to a 6% penalty for every year it is in the account. This is shown on Form 5329 and paid on the accountholder s tax return just like IRAs

43 Exercise A: Bob or Carol who are both 55 contribute to Bob s HSA $6,750 + $1,000 +$1,000 = $8,750. This creates an excess in the account of $1,000. In order for both to take advantage of the catch up contribution, they have to set up two separate HSAs. 83 Solution A: Remove the $1,000 as an excess plus earnings. Contribute $1,000 to Carol s HSA

44 Exercise B: Stan who took out $500 for a medical procedure was later reimbursed by his insurance company. Instead of telling the Financial Institution, he deposited it at the teller window as a contribution. $3,350 +$500 =$3, Solution B: Recode $500 as a nonreportable contribution. Correct 1099 SA 86 43

45 Exercise C: Lily put in $6,750 in her HSA and she had only individual coverage. She has an excess of $3, Solution C: Remove $3,400 as an excess plus earnings

46 Moving and Changing Summary of Rollovers and Transfers from HSAs Source of Funds HSA or MSA Check made payable to person Check made payable to financial institution Rollover 60 days 1 per 12 months Transfer unlimited number 90 45

47 Rollover From HSA To HSA An accountholder may withdraw all or part of the assets from his or her HSA, and as long as he or she reinvests them within 60 days from day of receipt in another HSA, it is nontaxable. 91 One Time Rollover From IRA To HSA 1. A qualified funding distribution may be made from a Traditional or a Roth IRA but not from an on going SEP or SIMPLE into a Health savings Account. An owner of an IRA may make the transfer or the owner of an inherited IRA. 2. The individual must be eligible for a HSA (have high deductible health insurance) and the contribution must be less than or equal to the individual s maximum annual contribution including catch up contributions

48 3. The maximum contribution is based on: The individual s age at the end of the taxable year, and The individual s type of high deductible health plan (self only or family). 4. The transfer is only allowed one time in a lifetime unless the accountholder changes policies mid year from single to family coverage. The money has to be transferred to the accountholder s own HSA and not to a family member or friend. If the individual owns two IRAs these must be transferred together before funding the HSA The funding distribution date is the year that it is made. You do not use tax years like IRAs up to April 15th. 6. Transfer is done as a trustee to trustee transfer from an IRA or Roth to a HSA. The check will be made payable to the custodian for the benefit of the owner

49 7. The accountholder must meet a testing period to avoid taxes and a 10% penalty. The testing period begins with the month in which the qualified HSA funding was made and ends on the last day of the 12 month following that month. The funds not used for medical purposes are still included in income and subject to 20% tax no matter what else is going on. 95 IRA To HSA Rollover REPORTING Financial Institution B Shows Money IN Put in: IRA to HSA Transfers Financial Institution B 3,350 Sally Jane Smith X 12/31 Bal

50 Distributions Distributions The accountholder can make tax free withdrawals from his or her HSA to pay or be reimbursed for qualified medical expenses are incurred after the HSA has been established. If the accountholder makes withdrawals for other reasons, the amount he or she withdraws will be subject to income tax and may be subject to an additional 20% tax as well. The accountholder does not have to make withdrawals from the HSA each year

51 The accountholder will generally pay medical expenses during the year without being reimbursed by his or her HDHP until the accountholder reaches the annual deductible for the plan. When the accountholder pays medical expenses during the year that are not reimbursed by the HDHP, the accountholder can ask the trustee of his or her HSA to send a distribution from the HSA. At age 65, the accountholder may take the funds out for other purposes without being subject to the 20% penalty, but the accountholder will have to pay taxes on the distribution if not used for medical purposes. 99 You can receive distributions from a HSA even if you are not currently eligible to have contributions made to the HSA. However, any part of a distribution not used to pay qualified medical expenses is includible in gross income and is subject to an additional 20% tax unless an exception applies

52 Forms for distributions: Not required by law Distribution Form Rollover Form Transfer Request form 101 Withholding on Since most of the distributions from a Health Savings Account are tax free and penalty free, we are not required to withhold for accountholders as we do with IRAs

53 Mistaken Distributions If amounts were distributed during the year from a HSA because of a mistake of fact due to reasonable cause, the account beneficiary may repay the mistaken distribution no later than April 15 following the first year the account beneficiary knew or should have known the distribution was a mistake. 103 There is no 20% penalty at death, age 65 or disability. Strength of the Health Savings Account is that it can be used for living expenses like an IRA at age 65. However when it is used for living expenses, it is not tax free it is penalty free

54 QUALIFIED MEDICAL EXPENSES If the distribution from the Health Savings Account is not used for a qualified medical expense, the owner of the Health Savings Account will pay an IRS imposed 20% penalty. Usually the form for penalties on HSAs is paid on the 1040 by our accountholders attaching form Qualified medical expenses are those that qualify for the medical and dental expenses deduction. These are explained in Publication 502, Medical and Dental Expenses. Examples include amounts paid for doctors' fees, prescription medicines, and necessary hospital services not paid for by insurance. Qualified medical expenses must be incurred after the HSA has been established

55 The accountholder cannot deduct qualified medical expenses as an itemized deduction on Schedule A (Form 1040) that are equal to the tax free amount of the distribution from his or her HSA. 107 Special Rules For Insurance Premiums. Generally, the accountholder cannot treat insurance premiums as qualified medical expenses for HSAs. The accountholder can, however, treat premiums for long term care coverage, health care coverage while he or she receives unemployment benefits, or health care continuation coverage required under any federal law as qualified medical expenses for HSAs

56 If the accountholder is age 65 or older, he or she can treat insurance premiums (other than premiums for a Medicare supplemental policy, such as Medigap) as qualified medical expenses for HSAs. 109 However, you cannot treat insurance premiums as qualified medical expense unless the premiums are for: Long term care (LTC) insurance, Health care continuation coverage (such as coverage under COBRA), Health care coverage while receiving unemployment compensation under federal or state law, or Medicare and other health care coverage if you were 65 or older (other than premiums for a Medicare supplemental policy, such as Medigap)

57 Death Distributions Upon the death of the HSA owner, the funds belong to the named beneficiary. If it is a spouse the spouse may treat the HSA as his or her own. Once that happens, the spouse may use the HSA the same way and receive the same tax benefits as the original owner. 111 If a nonspouse is the beneficiary of the HSA, the account ceases to be a HSA as of the date of death. The beneficiary will include the balance in his or her taxable income. For such beneficiary, except for an estate this amount is reduced by any medical payments if paid within one year after the owner s death. The beneficiary does not pay 20% penalty

58 IRS Reporting

59 115 REPORTING DEADLINES: HSA REQUIRED REPORTING REPORTS PURPOSE IRS DEADLINES HSA OWNER 5498 SA Contribution reporting May 31 May 31st 1099 SA Distributions February 28 th March 31 st January 31 st

60 STATE LAW Generally, if your state law requires a health plan to provide certain benefits without a deductible or at a deductible that is less than the minimum annual deductibles, the plan may not be an HDHP. 117 Christy Crawford christyjcrawford@msn.com Gettechnical Inc gettechnical@msn.com

Health Savings Account (HSA) Information for 2018

Information for 2018") Health Savings Account (HSA) Information for 2018 Note: The information contained herein may not necessarily apply to your unique situation and circumstances or take into account your tax situation. There

Health Savings Account (HSA) Information for 2018 Note: The information contained herein may not necessarily apply to your unique situation and circumstances or take into account your tax situation. There

Q&A on Federal Tax Aspects of Health Savings Accounts

Q&A on Federal Tax Aspects of Health Savings Accounts OVERVIEW AND ELIGIBILITY REQUIREMENTS What is a Health Savings Account? A Health Savings Account (HSA) is a tax-exempt trust or custodial account created

Q&A on Federal Tax Aspects of Health Savings Accounts OVERVIEW AND ELIGIBILITY REQUIREMENTS What is a Health Savings Account? A Health Savings Account (HSA) is a tax-exempt trust or custodial account created

Health Savings Accounts

Health Savings Accounts In an effort to respond to the rising cost of health insurance, many employers have made use of tax-favored accounts such as health flexible spending accounts (health FSAs), health

Health Savings Accounts In an effort to respond to the rising cost of health insurance, many employers have made use of tax-favored accounts such as health flexible spending accounts (health FSAs), health

Health Savings Accounts, Medical Savings Accounts and Long-Term Care Contracts

Health Savings Accounts, Medical Savings Accounts and Long-Term Care Contracts Contents In this module the student will review Health Savings Accounts, Archer Medical Savings Accounts and Long -Term Care

Health Savings Accounts, Medical Savings Accounts and Long-Term Care Contracts Contents In this module the student will review Health Savings Accounts, Archer Medical Savings Accounts and Long -Term Care

Instructions for Form 8889

2017 Instructions for Form 8889 Health Savings Accounts (HSAs) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future Developments

2017 Instructions for Form 8889 Health Savings Accounts (HSAs) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future Developments

The Webinar will be starting shortly

Rev. 5/2/2018 The Webinar will be starting shortly 8:30 am CST or 12:30 pm CST We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar Copyright 2018 Collin W. Fritz &

Rev. 5/2/2018 The Webinar will be starting shortly 8:30 am CST or 12:30 pm CST We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar Copyright 2018 Collin W. Fritz &

AN EMPLOYER S GUIDE TO HEALTH SAVINGS ACCOUNTS (HSAs)

") AN EMPLOYER S GUIDE TO HEALTH SAVINGS ACCOUNTS (HSAs) By Larry Grudzien Attorney at Law Updated May 2012 2012 Larry Grudzien, Attorney at Law All Right Reserved QUESTIONS AND ANSWERS PAGE 1 Why should

AN EMPLOYER S GUIDE TO HEALTH SAVINGS ACCOUNTS (HSAs) By Larry Grudzien Attorney at Law Updated May 2012 2012 Larry Grudzien, Attorney at Law All Right Reserved QUESTIONS AND ANSWERS PAGE 1 Why should

HSAs. Health Savings Accounts and 2018 Limits. Questions & Answers

HSAs Health Savings Accounts 2017 and 2018 Limits Questions & Answers What is a Health Savings Account (HSA)? An HSA is a tax-exempt trust or custodial account established for the purpose of paying medical

HSAs Health Savings Accounts 2017 and 2018 Limits Questions & Answers What is a Health Savings Account (HSA)? An HSA is a tax-exempt trust or custodial account established for the purpose of paying medical

Employee Health Benefits

Employee Health Benefits Table of Contents 1. Overview... 1 2. Training Objectives... 2 3. Resources... 3 4. Health Savings Accounts... 4 a. Benefits of an HSA account... 4 b. Who Qualifies for an HSA?...

Employee Health Benefits Table of Contents 1. Overview... 1 2. Training Objectives... 2 3. Resources... 3 4. Health Savings Accounts... 4 a. Benefits of an HSA account... 4 b. Who Qualifies for an HSA?...

Santa Paula Unified School District (SPUSD) Health Savings Account (HSA) FAQs

Health Savings Account (HSA) FAQs") Santa Paula Unified School District (SPUSD) Health Savings Account (HSA) FAQs Does SPUSD offer a Health Savings Account (HSA) option for medical benefits? Starting with the 2016-2017 Benefit Plan Year,

Santa Paula Unified School District (SPUSD) Health Savings Account (HSA) FAQs Does SPUSD offer a Health Savings Account (HSA) option for medical benefits? Starting with the 2016-2017 Benefit Plan Year,

HEALTH SAVINGS ACCOUNT. Straight Answers to Your HSA Questions HSA OVERVIEW HSA ELIGIBILITY. What is a Health Savings Account?

Straight Answers to Your HSA Questions HSA OVERVIEW What is a Health Savings Account? A Health Savings Account (HSA) is a taxexempt trust or custodial account established for the purpose of paying or reimbursing

Straight Answers to Your HSA Questions HSA OVERVIEW What is a Health Savings Account? A Health Savings Account (HSA) is a taxexempt trust or custodial account established for the purpose of paying or reimbursing

Andrews University. Healthcare Savings Accounts (HSA) And High Deductible Health Plans (HDHP)

And High Deductible Health Plans (HDHP)") Andrews University Healthcare Savings Accounts (HSA) And High Deductible Health Plans (HDHP) Andrews University HSA/HDHP Why? A tax vehicle to set aside money for current and future medical expenses The

Andrews University Healthcare Savings Accounts (HSA) And High Deductible Health Plans (HDHP) Andrews University HSA/HDHP Why? A tax vehicle to set aside money for current and future medical expenses The

Employees Frequently Asked Questions

Principal Health Savings Accounts Employees Frequently Asked Questions BACKGROUND QUESTION Why were health savings accounts (HSAs) created? What are the key advantages of HSAs? ANSWER The state of the

Principal Health Savings Accounts Employees Frequently Asked Questions BACKGROUND QUESTION Why were health savings accounts (HSAs) created? What are the key advantages of HSAs? ANSWER The state of the

Contents. What s New... 1 Reminder... 1 Publication 969. Cat. No S Health Savings Accounts (HSAs)... 2 Medical Savings Accounts (MSAs)...

... 2 Medical Savings Accounts (MSAs)...") Department of the Treasury Internal Revenue Service Contents What s New... 1 Reminder... 1 Publication 969 Introduction... 1 Cat. No. 24216S Health Savings Accounts (HSAs)... 2 Medical Savings Accounts

Department of the Treasury Internal Revenue Service Contents What s New... 1 Reminder... 1 Publication 969 Introduction... 1 Cat. No. 24216S Health Savings Accounts (HSAs)... 2 Medical Savings Accounts

ARTICLE I ARTICLE II ARTICLE III ARTICLE V

Health Savings Custodial Account (Under section 223(a) of the Internal Revenue Code) Form 5305-C (Rev. December 2011) Department of the Treasury, Internal Revenue Service. Do not file with the Internal

Health Savings Custodial Account (Under section 223(a) of the Internal Revenue Code) Form 5305-C (Rev. December 2011) Department of the Treasury, Internal Revenue Service. Do not file with the Internal

Health Savings Accounts: Overview of Rules for 2010

Health Savings Accounts: Overview of Rules for 2010 Janemarie Mulvey Specialist in Aging and Income Security September 9, 2010 Congressional Research Service CRS Report for Congress Prepared for Members

Health Savings Accounts: Overview of Rules for 2010 Janemarie Mulvey Specialist in Aging and Income Security September 9, 2010 Congressional Research Service CRS Report for Congress Prepared for Members

HEALTH SAVINGS ACCOUNT

HEALTH SAVINGS ACCOUNT Under 223(a) of the Internal Revenue Code TRUST AGREEMENT AND DISCLOSURE STATEMENT Form 5305-B (August 2004) Department of the Treasury Internal Revenue Service HSA Health Savings

HEALTH SAVINGS ACCOUNT Under 223(a) of the Internal Revenue Code TRUST AGREEMENT AND DISCLOSURE STATEMENT Form 5305-B (August 2004) Department of the Treasury Internal Revenue Service HSA Health Savings

HSA Frequently Asked Questions

HSA Frequently Asked Questions Overview Q1. WHAT IS A HEALTH SAVINGS ACCOUNT (HSA)? An HSA is a tax-exempt trust or custodial account established exclusively for the purpose of paying qualified medical

HSA Frequently Asked Questions Overview Q1. WHAT IS A HEALTH SAVINGS ACCOUNT (HSA)? An HSA is a tax-exempt trust or custodial account established exclusively for the purpose of paying qualified medical

Employers Frequently Asked Questions

Principal Health Savings Accounts Employers Frequently Asked Questions BACKGROUND QUESTION Why were health savings accounts (HSAs) created? ANSWER People are more careful about their health care purchases

Principal Health Savings Accounts Employers Frequently Asked Questions BACKGROUND QUESTION Why were health savings accounts (HSAs) created? ANSWER People are more careful about their health care purchases

Health Savings Account Overview. Findlay City Schools USI Insurance Services LLC Innovation Drive, Suite 220 Miamisburg, OH 45342

Health Savings Account Overview Findlay City Schools 2018 USI Insurance Services LLC 10100 Innovation Drive, Suite 220 Miamisburg, OH 45342 What is an HSA? Created in Medicare legislation and signed into

Health Savings Account Overview Findlay City Schools 2018 USI Insurance Services LLC 10100 Innovation Drive, Suite 220 Miamisburg, OH 45342 What is an HSA? Created in Medicare legislation and signed into

Kitsap Bank Health Savings Account Guide. A tax-smart way for you to manage growing healthcare costs.

Kitsap Bank Health Savings Account Guide A tax-smart way for you to manage growing healthcare costs. At Kitsap Bank, we believe that helping you prepare for the rising cost of health care is key to helping

Kitsap Bank Health Savings Account Guide A tax-smart way for you to manage growing healthcare costs. At Kitsap Bank, we believe that helping you prepare for the rising cost of health care is key to helping

Health Savings Account (HSA) Amendment-Custodial

Amendment-Custodial") Health Savings Account (HSA) Amendment Dear HSA Owner: The purpose of this Amendment is to incorporate changes in law and policy that affect your Health Savings Account (HSA) agreement. This Amendment

Health Savings Account (HSA) Amendment Dear HSA Owner: The purpose of this Amendment is to incorporate changes in law and policy that affect your Health Savings Account (HSA) agreement. This Amendment

2018 Employee Benefits Webinar Series. Introduction to Consumer Directed Healthcare and Account-Based Plans (HSAs, FSAs, and HRAs) November 15, 2018

November 15, 2018") 2018 Employee Benefits Webinar Series Introduction to Consumer Directed Healthcare and Account-Based Plans (HSAs, FSAs, and HRAs) November 15, 2018 Stacy H. Barrow Marathas Barrow Weatherhead Lent LLP

2018 Employee Benefits Webinar Series Introduction to Consumer Directed Healthcare and Account-Based Plans (HSAs, FSAs, and HRAs) November 15, 2018 Stacy H. Barrow Marathas Barrow Weatherhead Lent LLP

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt

Health Savings Accounts and High Deductible Health Plans

Dean, Mead, Egerton, Bloodworth, Capouano & Bozarth, P.A. 800 North Magnolia Avenue, Suite 1500 P.O. Box 2346 (ZIP 32802-2346) Orlando, FL 32803 Orlando Fort Pierce Viera 407-841-1200 407-423-1831 Fax

Dean, Mead, Egerton, Bloodworth, Capouano & Bozarth, P.A. 800 North Magnolia Avenue, Suite 1500 P.O. Box 2346 (ZIP 32802-2346) Orlando, FL 32803 Orlando Fort Pierce Viera 407-841-1200 407-423-1831 Fax

Health Savings Accounts

Entire lesson Health Savings Accounts (optional certification) Pub 4012 Tab E Pubs 969 and 4942 Form 8889 Instructions IRS Certification VITA/TCE Counselors must be certified by passing the HSA test Refer

Entire lesson Health Savings Accounts (optional certification) Pub 4012 Tab E Pubs 969 and 4942 Form 8889 Instructions IRS Certification VITA/TCE Counselors must be certified by passing the HSA test Refer

CRS Report for Congress

Order Code RL33257 CRS Report for Congress Received through the CRS Web Health Savings Accounts: Overview of Rules for 2006 January 31, 2006 Bob Lyke Specialist in Social Legislation Domestic Social Policy

Order Code RL33257 CRS Report for Congress Received through the CRS Web Health Savings Accounts: Overview of Rules for 2006 January 31, 2006 Bob Lyke Specialist in Social Legislation Domestic Social Policy

Health Savings Accounts

Oppenheimer & Co. Inc. Spencer Nurse Executive Director - Investments 500 108th Ave. NE Suite 2100 Bellevue, WA 98004 425-709-0540 800-531-3110 spencer.nurse@opco.com http://fa.opco.com/spencer.nurse/index.htm

Oppenheimer & Co. Inc. Spencer Nurse Executive Director - Investments 500 108th Ave. NE Suite 2100 Bellevue, WA 98004 425-709-0540 800-531-3110 spencer.nurse@opco.com http://fa.opco.com/spencer.nurse/index.htm

Health Savings Account (HSA)

") What is a Health Savings Account? Health Savings Account (HSA) A Health Savings Account (HSA) is a tax-advantaged health care account that you own. You contribute to it with tax-free or tax-deductible

What is a Health Savings Account? Health Savings Account (HSA) A Health Savings Account (HSA) is a tax-advantaged health care account that you own. You contribute to it with tax-free or tax-deductible

Frequently Asked Questions

Page 1 of 22 Anthem Blue Cross and Blue Shield High-deductible Health Plans and Health Savings Accounts Frequently Asked Questions November 30, 2004 Page 2 of 22 Anthem Blue Cross and Blue Shield High-Deductible

Page 1 of 22 Anthem Blue Cross and Blue Shield High-deductible Health Plans and Health Savings Accounts Frequently Asked Questions November 30, 2004 Page 2 of 22 Anthem Blue Cross and Blue Shield High-Deductible

HSA Questions and Answers

Brought to you by Sentinel Benefits & Financial Group HSA Questions and Answers This Legislative Brief sets out Questions and Answers regarding Health Savings Accounts (HSAs), as provided by the Internal

Brought to you by Sentinel Benefits & Financial Group HSA Questions and Answers This Legislative Brief sets out Questions and Answers regarding Health Savings Accounts (HSAs), as provided by the Internal

Q&A on Qualified High Deductible Health Plans (HDHP s) and Health Savings Accounts (HSA s)

and Health Savings Accounts (HSA s)") Q&A on Qualified High Deductible Health Plans (HDHP s) and Health Savings Accounts (HSA s) Q. What is a Health Savings Account ( HSA )? A. A Health Savings Account is an alternative to traditional health

Q&A on Qualified High Deductible Health Plans (HDHP s) and Health Savings Accounts (HSA s) Q. What is a Health Savings Account ( HSA )? A. A Health Savings Account is an alternative to traditional health

pay or reimburse qualified medical expenses.

Health Savings Accounts (HSAs) Notice 2004 2 PURPOSE This notice provides guidance on Health Savings Accounts. BACKGROUND Section 1201 of the Medicare Prescription Drug, Improvement, and Modernization

Health Savings Accounts (HSAs) Notice 2004 2 PURPOSE This notice provides guidance on Health Savings Accounts. BACKGROUND Section 1201 of the Medicare Prescription Drug, Improvement, and Modernization

11. I understand that I may update or change my account beneficiaries at any time using the beneficiary change form on the HSA website.

1. I hereby establish a Health Savings Account ("HSA") under the terms and conditions contained in the accompanying HSA Custodial Account Agreement. This HSA becomes effective upon the acceptance of the

1. I hereby establish a Health Savings Account ("HSA") under the terms and conditions contained in the accompanying HSA Custodial Account Agreement. This HSA becomes effective upon the acceptance of the

Health Savings Accounts

Health Savings Accounts Who s Eligible? Covered by a high deductible health plan (HDHP) Not covered by other health insurance Not enrolled in Medicare Not claimed as a dependent on someone else s tax return

Health Savings Accounts Who s Eligible? Covered by a high deductible health plan (HDHP) Not covered by other health insurance Not enrolled in Medicare Not claimed as a dependent on someone else s tax return

Health Savings Accounts (HSA) Overview

Overview") Health Savings Accounts (HSA) Overview What You See Taxpayer presents a W-2 with a W in box 12. This represents his and/or his company s contribution to the HSA. This contribution has already been deducted

Health Savings Accounts (HSA) Overview What You See Taxpayer presents a W-2 with a W in box 12. This represents his and/or his company s contribution to the HSA. This contribution has already been deducted

Health Savings Accounts: Innovative Health Care Financing

Health Savings Accounts: Innovative Health Care Financing Would you be interested in a health insurance program that puts you in control of your own health care dollars, while protecting you and your family

Health Savings Accounts: Innovative Health Care Financing Would you be interested in a health insurance program that puts you in control of your own health care dollars, while protecting you and your family

Introduction to Health Savings Accounts (HSA)

") Introduction to Health Savings Accounts (HSA) 2018 Employee Benefits Corporation 1 Sue Sieger, ACFCI, CAS Senior Compliance Consultant Employee Benefits Corporation sue.sieger@ebcflex.com The material

Introduction to Health Savings Accounts (HSA) 2018 Employee Benefits Corporation 1 Sue Sieger, ACFCI, CAS Senior Compliance Consultant Employee Benefits Corporation sue.sieger@ebcflex.com The material

Health Savings Accounts

Health Savings Accounts Forrest T. Jones & Company, Inc. Updated for 2013 What is an HSA? PART 1 HDHP High Deductible Health Plan PART 2 HSA Health Savings Account 2 Parts to an HSA Intended to cover serious

Health Savings Accounts Forrest T. Jones & Company, Inc. Updated for 2013 What is an HSA? PART 1 HDHP High Deductible Health Plan PART 2 HSA Health Savings Account 2 Parts to an HSA Intended to cover serious

Frequently Asked Questions: HDHP with HSA 2011 Annual Enrollment. What s New for 2011

Frequently Asked Questions: HDHP with HSA What s New for 2011 1. Will my High Deductible Health Plan with Health Savings Account (HDHP with HSA) vendor be the same in 2011? 2. If my medical plan vendor

Frequently Asked Questions: HDHP with HSA What s New for 2011 1. Will my High Deductible Health Plan with Health Savings Account (HDHP with HSA) vendor be the same in 2011? 2. If my medical plan vendor

IRS PROVIDES GUIDANCE ON HEALTH SAVINGS ACCOUNTS

IRS PROVIDES GUIDANCE ON HEALTH SAVINGS ACCOUNTS Page 1 of 5 IRS has issued guidance on Health Savings Accounts (HSAs), a new type of tax-favored vehicle created by the Medicare Act of 2003, which was

IRS PROVIDES GUIDANCE ON HEALTH SAVINGS ACCOUNTS Page 1 of 5 IRS has issued guidance on Health Savings Accounts (HSAs), a new type of tax-favored vehicle created by the Medicare Act of 2003, which was

Introduction to Health Savings Accounts (HSA)

") Introduction to Health Savings Accounts (HSA) 2017 Employee Benefits Corporation 1 Sue Sieger, ACFCI, CAS Senior Compliance Consultant Employee Benefits Corporation sue.sieger@ebcflex.com The material

Introduction to Health Savings Accounts (HSA) 2017 Employee Benefits Corporation 1 Sue Sieger, ACFCI, CAS Senior Compliance Consultant Employee Benefits Corporation sue.sieger@ebcflex.com The material

Health Savings Accounts: An Employer Overview

Health Savings Accounts: An Employer Overview Since salary alone is often not enough to attract and retain valued employees, what can your business do to enhance its employee benefits package? Table of

Health Savings Accounts: An Employer Overview Since salary alone is often not enough to attract and retain valued employees, what can your business do to enhance its employee benefits package? Table of

HEALTH SAVINGS CUSTODIAL ACCOUNT AGREEMENT

HEALTH SAVINGS CUSTODIAL ACCOUNT AGREEMENT Form 5305-C under section 223(a) of the Internal Revenue Code. FORM (December 2011) The account owner named on the application is establishing this health savings

HEALTH SAVINGS CUSTODIAL ACCOUNT AGREEMENT Form 5305-C under section 223(a) of the Internal Revenue Code. FORM (December 2011) The account owner named on the application is establishing this health savings

Your Benefits Solutions Partner Health Savings Account Reference Guide. Plan Services Provided By

EBAS Employee Benefits Administration Services, LLC Your Benefits Solutions Partner 2014 Health Savings Account Reference Guide Plan Services Provided By Employee Benefits Administration Services, LLC

EBAS Employee Benefits Administration Services, LLC Your Benefits Solutions Partner 2014 Health Savings Account Reference Guide Plan Services Provided By Employee Benefits Administration Services, LLC

HEALTH SAVINGS ACCOUNT. Answers to Your HSA Questions

HEALTH SAVINGS ACCOUNT Answers to Your HSA Questions WHAT IS A HEALTH SAVINGS ACCOUNT? A Health Savings Account (HSA) is a taxexempt trust or custodial account established for the purpose of paying or

HEALTH SAVINGS ACCOUNT Answers to Your HSA Questions WHAT IS A HEALTH SAVINGS ACCOUNT? A Health Savings Account (HSA) is a taxexempt trust or custodial account established for the purpose of paying or

All Things Medical. Presented by: Keith Altobelli, EA

Presented by: Keith Altobelli, EA 2 At the end of this webinar, you should be able to: Recognize the benefits of Health Savings Accounts (HSAs) Identify Eligibility Requirements Determine deductible and

Presented by: Keith Altobelli, EA 2 At the end of this webinar, you should be able to: Recognize the benefits of Health Savings Accounts (HSAs) Identify Eligibility Requirements Determine deductible and

Business & Health Savings Accounts

HSAs Business & Health Savings Accounts 2017 and 2018 Limits Questions & Answers Purpose The purpose of this brochure is to present a business decision-maker with basic information about HSAs so a business

HSAs Business & Health Savings Accounts 2017 and 2018 Limits Questions & Answers Purpose The purpose of this brochure is to present a business decision-maker with basic information about HSAs so a business

Health Savings Account (HSA) Contribution Rules

Contribution Rules") Provided by [B_Officialname] Health Savings Account (HSA) Contribution Rules Many employers offer high deductible health plans (HDHPs) to control premium costs and then pair this coverage with health savings

Provided by [B_Officialname] Health Savings Account (HSA) Contribution Rules Many employers offer high deductible health plans (HDHPs) to control premium costs and then pair this coverage with health savings

... HSA ... Health Savings Account. Custodial Booklet. (includes self-direction)

") HSA Health Savings Account Custodial Booklet (includes selfdirection) HEALTH SAVINGS CUSTODIAL ACCOUNT (Under section 223(a) of the Internal Revenue Code) Form 5305C (December 2011) Department of the Treasury

HSA Health Savings Account Custodial Booklet (includes selfdirection) HEALTH SAVINGS CUSTODIAL ACCOUNT (Under section 223(a) of the Internal Revenue Code) Form 5305C (December 2011) Department of the Treasury

Health Savings Account (HSA) FAQ s

FAQ s") Health Savings Account (HSA) FAQ s 1. What is a Health Savings Account? (Also known as a HSA) A Health Savings Account (HSA) combines a high deductible health plan with a savings account to help pay for

Health Savings Account (HSA) FAQ s 1. What is a Health Savings Account? (Also known as a HSA) A Health Savings Account (HSA) combines a high deductible health plan with a savings account to help pay for

Health Savings Account (HSA) Overview

Overview") ... 2 Contributions... 4 Disbursements... 5 Disbursement Options... 6 HSA Base Account... 7 Self-Directed Brokerage Account Option... 8 About UMB... 9 Appendix A: HSA Website Navigation... 10 Appendix

... 2 Contributions... 4 Disbursements... 5 Disbursement Options... 6 HSA Base Account... 7 Self-Directed Brokerage Account Option... 8 About UMB... 9 Appendix A: HSA Website Navigation... 10 Appendix

2019 Health Savings Plan and Health Savings Account Questions

2019 Health Savings Plan and Health Savings Account Questions Contents Health Savings Plan (HSP)... 2 Health Savings Account (HSA) Overview... 4 Opening and Funding Your HSA... 5 Managing Your HSA... 8

2019 Health Savings Plan and Health Savings Account Questions Contents Health Savings Plan (HSP)... 2 Health Savings Account (HSA) Overview... 4 Opening and Funding Your HSA... 5 Managing Your HSA... 8

Health Savings Accounts Frequently Asked Questions

Health Savings Accounts Frequently Asked Questions Health savings accounts put your health care spending in your own hands. You decide when and how to use your health care dollars and you can save on taxes

Health Savings Accounts Frequently Asked Questions Health savings accounts put your health care spending in your own hands. You decide when and how to use your health care dollars and you can save on taxes

HEALTH SAVINGS ACCOUNT INVESTING GUIDE. Combine HSA tax advantages with investment opportunities.

HEALTH SAVINGS ACCOUNT INVESTING GUIDE Combine HSA tax advantages with investment opportunities. Why Have an HSA? Short term benefit Save 10-40% on every medical expense. Because HSA contributions are

HEALTH SAVINGS ACCOUNT INVESTING GUIDE Combine HSA tax advantages with investment opportunities. Why Have an HSA? Short term benefit Save 10-40% on every medical expense. Because HSA contributions are

Health Savings Accounts

Health Savings Accounts A Guide for Missouri School Districts January, 2007 Forrest T. Jones & Company, Inc. 3130 Broadway Kansas City, MO 64111 800-821-7303 What is a Health Savings Account (HSA)? Health

Health Savings Accounts A Guide for Missouri School Districts January, 2007 Forrest T. Jones & Company, Inc. 3130 Broadway Kansas City, MO 64111 800-821-7303 What is a Health Savings Account (HSA)? Health

NEXT : Eligibility guidelines of a Health Savings Account.

Issue 1 What is a Health Savings Account (HSA)? A health savings account is a special tax-advantaged account owned by an individual where contributions to the account are to pay for current and future

Issue 1 What is a Health Savings Account (HSA)? A health savings account is a special tax-advantaged account owned by an individual where contributions to the account are to pay for current and future

Frequently Asked Questions High-Deductible Health Plan (HDHP) with Health Savings Account (HSA)

with Health Savings Account (HSA)") Frequently Asked Questions High-Deductible Health Plan (HDHP) with Health Savings Account (HSA) BASICS OF A HIGH-DEDUCTIBLE HEALTH PLAN (HDHP) What is a high-deductible health plan (HDHP)? An HDHP is a

Frequently Asked Questions High-Deductible Health Plan (HDHP) with Health Savings Account (HSA) BASICS OF A HIGH-DEDUCTIBLE HEALTH PLAN (HDHP) What is a high-deductible health plan (HDHP)? An HDHP is a

Health Savings Account (HSA) Overview

Overview") Health Savings Account (HSA) Overview Health Savings Account (HSA) Overview Health Savings Account (HSA) Overview... 2 Contributions... 4 Disbursements... 5 Disbursement Options... 6 HSA Base Account...

Health Savings Account (HSA) Overview Health Savings Account (HSA) Overview Health Savings Account (HSA) Overview... 2 Contributions... 4 Disbursements... 5 Disbursement Options... 6 HSA Base Account...

PNC BENEFIT PLUS HEALTH SAVINGS ACCOUNT DISCLOSURE STATEMENT AND CUSTODIAL ACCOUNT AGREEMENT AND PRIVACY POLICY. (EFFECTIVE DATE December 1, 2017)

") PNC BENEFIT PLUS HEALTH SAVINGS ACCOUNT DISCLOSURE STATEMENT AND CUSTODIAL ACCOUNT AGREEMENT AND PRIVACY POLICY (EFFECTIVE DATE December 1, 2017) TABLE OF CONTENTS Health Savings Account (HSA) Disclosure

PNC BENEFIT PLUS HEALTH SAVINGS ACCOUNT DISCLOSURE STATEMENT AND CUSTODIAL ACCOUNT AGREEMENT AND PRIVACY POLICY (EFFECTIVE DATE December 1, 2017) TABLE OF CONTENTS Health Savings Account (HSA) Disclosure

Health Savings Accounts

2013 Health Savings Accounts Frequently Asked Questions Gallagher Benefit Services, Inc. HSA FREQUENTLY ASKED QUESTIONS for Employers Basics Q-1: What is an HSA? A-1: A Health Savings Account ( HSA ) is

2013 Health Savings Accounts Frequently Asked Questions Gallagher Benefit Services, Inc. HSA FREQUENTLY ASKED QUESTIONS for Employers Basics Q-1: What is an HSA? A-1: A Health Savings Account ( HSA ) is

Health Savings Accounts

Health Savings Accounts A Guide for Missouri School District Employees Over 70% of employees and retirees in the Missouri Educators Unified Health Plan (MEUHP) are enrolled in an HSA Plan., Projected Plan

Health Savings Accounts A Guide for Missouri School District Employees Over 70% of employees and retirees in the Missouri Educators Unified Health Plan (MEUHP) are enrolled in an HSA Plan., Projected Plan

Sanford Health Value Plan (HDHP+HSA) Frequently Asked Questions

Frequently Asked Questions") Sanford Health Value Plan (HDHP+HSA) Frequently Asked Questions August 2017 This document is intended to answer frequently asked questions regarding Sanford Health s Value Plan (HDHP+HSA). Additional information

Sanford Health Value Plan (HDHP+HSA) Frequently Asked Questions August 2017 This document is intended to answer frequently asked questions regarding Sanford Health s Value Plan (HDHP+HSA). Additional information

HEALTH SAVINGS ACCOUNT. Under 223(a) of the Internal Revenue Code CUSTODIAL AGREEMENT AND DISCLOSURE STATEMENT

of the Internal Revenue Code CUSTODIAL AGREEMENT AND DISCLOSURE STATEMENT") HEALTH SAVINGS ACCOUNT Under 223(a) of the Internal Revenue Code CUSTODIAL AGREEMENT AND DISCLOSURE STATEMENT Form 5305-C (December 2011) Department of the Treasury Internal Revenue Service HSA Health

HEALTH SAVINGS ACCOUNT Under 223(a) of the Internal Revenue Code CUSTODIAL AGREEMENT AND DISCLOSURE STATEMENT Form 5305-C (December 2011) Department of the Treasury Internal Revenue Service HSA Health

Health+Savings FAQs. The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan.

Health+Savings FAQs The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan. Note: Health Savings Account (HSA) tax laws vary by state. You might

Health+Savings FAQs The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan. Note: Health Savings Account (HSA) tax laws vary by state. You might

Health Savings Accounts and Medicare

A Guide to Health Savings Accounts and Medicare Discover how Medicare impacts your HSA, and get answers to frequently asked questions. A Guide to Discover how Medicare impacts your HSA, and get answers

A Guide to Health Savings Accounts and Medicare Discover how Medicare impacts your HSA, and get answers to frequently asked questions. A Guide to Discover how Medicare impacts your HSA, and get answers

Your Health Savings Account Reference Guide. Your Guide to Understanding a Health Savings Account

Your Health Savings Account Reference Guide Your Guide to Understanding a Health Savings Account The Fidelity HSA A tax-advantaged way to pay for health care expenses.* A health savings account (HSA),

Your Health Savings Account Reference Guide Your Guide to Understanding a Health Savings Account The Fidelity HSA A tax-advantaged way to pay for health care expenses.* A health savings account (HSA),

Frequently Asked Questions about the High Deductible (HDHP) HMO Plan with Health Savings Account (HSA)

HMO Plan with Health Savings Account (HSA)") Frequently Asked Questions about the High Deductible (HDHP) HMO Plan with Health Savings Account (HSA) The following questions and answers will help you better understand the High Deductible HMO Plan (HDHP)

Frequently Asked Questions about the High Deductible (HDHP) HMO Plan with Health Savings Account (HSA) The following questions and answers will help you better understand the High Deductible HMO Plan (HDHP)

Ameren Health Savings Account Program

Ameren Health Savings Account Program Amended January 1, 2016 Ameren Health Savings Account Program 1 Ameren Health Savings Account Program Table of Contents SECTION PAGE Purpose... 3 Program Eligibility...

Ameren Health Savings Account Program Amended January 1, 2016 Ameren Health Savings Account Program 1 Ameren Health Savings Account Program Table of Contents SECTION PAGE Purpose... 3 Program Eligibility...

Health. Savings. FAQs. The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan.

Health Savings FAQs The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan. Note: Health Savings Account (HSA) tax laws vary by state. You might

Health Savings FAQs The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan. Note: Health Savings Account (HSA) tax laws vary by state. You might

Click on a section or question to be taken directly to the answer you re looking for, or read through all the questions and answers.

Frequently Asked Questions: HDHP with HSA 2012 Annual Enrollment Table of Contents Click on a section or question to be taken directly to the answer you re looking for, or read through all the questions

Frequently Asked Questions: HDHP with HSA 2012 Annual Enrollment Table of Contents Click on a section or question to be taken directly to the answer you re looking for, or read through all the questions

Advanced HSA Concepts

Advanced HSA Concepts 1 Sue Sieger, ACFCI, CAS Senior Compliance Consultant Employee Benefits Corporation sue.sieger@ebcflex.com The material provided in this webinar is by Employee Benefits Corporation

Advanced HSA Concepts 1 Sue Sieger, ACFCI, CAS Senior Compliance Consultant Employee Benefits Corporation sue.sieger@ebcflex.com The material provided in this webinar is by Employee Benefits Corporation

Employee HSAs, HRAs and FSAs: Issues for Benefits Counsel

Presenting a live 90-minute webinar with interactive Q&A Employee HSAs, HRAs and FSAs: Issues for Benefits Counsel Navigating the Compliance Requirements Regarding Account Administration, Funding, and

Presenting a live 90-minute webinar with interactive Q&A Employee HSAs, HRAs and FSAs: Issues for Benefits Counsel Navigating the Compliance Requirements Regarding Account Administration, Funding, and

HEALTH CONCEPTS AND TAX CONSIDERATIONS

14 HEALTH CONCEPTS AND TAX CONSIDERATIONS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Recognize the features of health insurance policies that have been mandated by

14 HEALTH CONCEPTS AND TAX CONSIDERATIONS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Recognize the features of health insurance policies that have been mandated by

Get Started with a Health Savings Account

Get Started with a Health Savings Account www.discoverybenefits.com Health saving account a triple savings Contribute tax- free Grow your funds tax-free Spend tax-free Benefits of an HSA A combination

Get Started with a Health Savings Account www.discoverybenefits.com Health saving account a triple savings Contribute tax- free Grow your funds tax-free Spend tax-free Benefits of an HSA A combination

Frequently Asked Questions: The Health Savings Plan

Frequently Asked Questions: The Health Savings Plan Comparing the Plans What are the major differences between the Health Savings Plan (HDHP) and the Traditional Plan (PPO)? The two plans have been designed

Frequently Asked Questions: The Health Savings Plan Comparing the Plans What are the major differences between the Health Savings Plan (HDHP) and the Traditional Plan (PPO)? The two plans have been designed

Health. Savings. FAQs. The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan.

Health Savings FAQs The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan. Note: Health Savings Account (HSA) tax laws vary by state. You might

Health Savings FAQs The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan. Note: Health Savings Account (HSA) tax laws vary by state. You might

Health Savings Account Welcome Guide

Health Savings Account Welcome Guide Your Health Savings Account Health care made more affordable To help you better manage healthcare costs, a Health Savings Account (HSA) is designed to save you money

Health Savings Account Welcome Guide Your Health Savings Account Health care made more affordable To help you better manage healthcare costs, a Health Savings Account (HSA) is designed to save you money

Establishing a SEP for 2014

Published Since 1984 ALSO IN THIS ISSUE Understanding Box 2 (Rollover Contributions) on the 2014 Form 5498, Page 2 Administering An HSA After the HSA Owner Dies, Page 4 Email Guidance - No Authority Exists

Published Since 1984 ALSO IN THIS ISSUE Understanding Box 2 (Rollover Contributions) on the 2014 Form 5498, Page 2 Administering An HSA After the HSA Owner Dies, Page 4 Email Guidance - No Authority Exists

Frequently Asked Questions about the GVSU High Deductible PPO Plan (HDHP) with Health Savings Account (HSA)

with Health Savings Account (HSA)") Frequently Asked Questions about the GVSU High Deductible PPO Plan (HDHP) with Health Savings Account (HSA) The following questions and answers will help you better understand the GVSU High Deductible

Frequently Asked Questions about the GVSU High Deductible PPO Plan (HDHP) with Health Savings Account (HSA) The following questions and answers will help you better understand the GVSU High Deductible

HSA CUSTODIAL AGREEMENT AND DISCLOSURES. Health Savings Custodial Agreement

HSA CUSTODIAL AGREEMENT AND DISCLOSURES Health Savings Custodial Agreement Health Savings Account Terms and Conditions Health Savings Account Disclosure Statement Health Savings Custodial Agreement Form

HSA CUSTODIAL AGREEMENT AND DISCLOSURES Health Savings Custodial Agreement Health Savings Account Terms and Conditions Health Savings Account Disclosure Statement Health Savings Custodial Agreement Form

2018 HSA GUIDE. ...Your Benefits

...Your Benefits 2018 HSA GUIDE The HSA Plan consists of two parts that work together to give you more control over how you receive and pay for medical care and services, both now and in the future: the

...Your Benefits 2018 HSA GUIDE The HSA Plan consists of two parts that work together to give you more control over how you receive and pay for medical care and services, both now and in the future: the

HSAs: How they work to save you money

HSAs: How they work to save you money Recognized expertise in human resources and finance BenefitWallet BenefitWallet and The Bank of New York Mellon (BNY Mellon) provide a seamless Health Savings Account

HSAs: How they work to save you money Recognized expertise in human resources and finance BenefitWallet BenefitWallet and The Bank of New York Mellon (BNY Mellon) provide a seamless Health Savings Account

2015 HSA Plan Quick Guide

2015 HSA Plan Quick Guide The HSA Plan consists of two parts that work together to give you more control over how you receive and pay for medical care and services, both now and in the future: the Health

2015 HSA Plan Quick Guide The HSA Plan consists of two parts that work together to give you more control over how you receive and pay for medical care and services, both now and in the future: the Health

Health Savings Account

Custodial Agreement & Disclosure Statement Page 1 of 16 Health Savings Account Under 223(a) of the Internal Revenue Code 512 E. Township Line Rd 5 Valley Square, Suite 200 Blue Bell, PA 19422-0119 P (866)

Custodial Agreement & Disclosure Statement Page 1 of 16 Health Savings Account Under 223(a) of the Internal Revenue Code 512 E. Township Line Rd 5 Valley Square, Suite 200 Blue Bell, PA 19422-0119 P (866)

Single HDHP $3,400 $3,450 Family HDHP $6,750 $6, Single HDHP $4,400 $4,450 Family HDHP $7,750 $7,900

Published Since 1984 ALSO IN THIS ISSUE IRS Issues 2018 Indexed Amounts for HSAs Page 1 RMD Box 11 on Form 5498 Is Not Checked for an IRA Beneficiary Page 2 Completing the 2016 Form 5498-A Page 3 Email

Published Since 1984 ALSO IN THIS ISSUE IRS Issues 2018 Indexed Amounts for HSAs Page 1 RMD Box 11 on Form 5498 Is Not Checked for an IRA Beneficiary Page 2 Completing the 2016 Form 5498-A Page 3 Email

Health Savings Plan and Health Savings Account. Business Rules and Detailed Design Features for 2016

Health Savings Plan and Health Savings Account Business Rules and Detailed Design Features for 2016 i Table of Contents 1. Definition of Terms 1A High Deductible Health Plan 2 1B Health Savings Plan (HSP)

Health Savings Plan and Health Savings Account Business Rules and Detailed Design Features for 2016 i Table of Contents 1. Definition of Terms 1A High Deductible Health Plan 2 1B Health Savings Plan (HSP)

2018 HEALTH SAVINGS ACCOUNT (HSA) FREQUENTLY ASKED QUESTIONS

FREQUENTLY ASKED QUESTIONS") HSA Overview 2018 HEALTH SAVINGS ACCOUNT (HSA) FREQUENTLY ASKED QUESTIONS 1. What is the Rimkus Consulting Group Health & Savings Plan? The Rimkus Consulting Group Health & Savings Plan is a Consumer Driven

HSA Overview 2018 HEALTH SAVINGS ACCOUNT (HSA) FREQUENTLY ASKED QUESTIONS 1. What is the Rimkus Consulting Group Health & Savings Plan? The Rimkus Consulting Group Health & Savings Plan is a Consumer Driven

2018 Health Savings Account (HSA) Frequently Asked Questions. Table of Contents

Frequently Asked Questions. Table of Contents") 2018 Health Savings Account (HSA) Frequently Asked Questions Table of Contents Health Savings Account (HSA) Plans What is a Health Savings Account (HSA)?...pg. 1 How does an IU Health HSA work?...pg. 1

2018 Health Savings Account (HSA) Frequently Asked Questions Table of Contents Health Savings Account (HSA) Plans What is a Health Savings Account (HSA)?...pg. 1 How does an IU Health HSA work?...pg. 1

Health. Savings. FAQs. The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan.

Health Savings FAQs The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan. Note: Health Savings Account (HSA) tax laws vary by state. You might

Health Savings FAQs The following are frequently asked questions and answers regarding the Health+Savings Option in the BP Medical Plan. Note: Health Savings Account (HSA) tax laws vary by state. You might

Important Disclosure Information

Important Disclosure Information Health Savings Account Custodial Agreement (Under section 223(a) of the Internal Revenue Code) Please keep this agreement with your HSA records. Thank you for choosing

Important Disclosure Information Health Savings Account Custodial Agreement (Under section 223(a) of the Internal Revenue Code) Please keep this agreement with your HSA records. Thank you for choosing

Comparison of Healthcare Reimbursement Programs

June 2016 Presented by Lockton Companies L O C K T O N C O M P A N I E S Table of Contents General 1 Eligibility. 3 Contributions 7 Distributions.. 10 Healthcare Reform Implications. 12 Miscellaneous 15

June 2016 Presented by Lockton Companies L O C K T O N C O M P A N I E S Table of Contents General 1 Eligibility. 3 Contributions 7 Distributions.. 10 Healthcare Reform Implications. 12 Miscellaneous 15

Important Disclosure Information Health Savings Account Custodial Agreement

Important Disclosure Information Health Savings Account Custodial Agreement Under section 223(a) of the Internal Revenue Code I. Agreement PayFlex Systems USA, Inc. ( PayFlex, Custodian, "us" or "we")

Important Disclosure Information Health Savings Account Custodial Agreement Under section 223(a) of the Internal Revenue Code I. Agreement PayFlex Systems USA, Inc. ( PayFlex, Custodian, "us" or "we")

COMMONLY ASKED QUESTIONS AND ANSWERS ABOUT PARTICIPATION IN A HEALTH SAVINGS ACCOUNT

What is a Health Savings Account (HSA)? COMMONLY ASKED QUESTIONS AND ANSWERS ABOUT PARTICIPATION IN A HEALTH SAVINGS ACCOUNT A Health Savings Account (HSA) is a tax-advantaged medical savings account that

What is a Health Savings Account (HSA)? COMMONLY ASKED QUESTIONS AND ANSWERS ABOUT PARTICIPATION IN A HEALTH SAVINGS ACCOUNT A Health Savings Account (HSA) is a tax-advantaged medical savings account that

Is MITRE s HD Care PPO + HSA right for you?

Is MITRE s HD Care PPO + HSA right for you? How to leverage the plan for long-term advantages 2018 Healthcare MITRE Human Resources BOOKMARK What is a High Deductible Health Plan...1 What is a Health Savings

Is MITRE s HD Care PPO + HSA right for you? How to leverage the plan for long-term advantages 2018 Healthcare MITRE Human Resources BOOKMARK What is a High Deductible Health Plan...1 What is a Health Savings

ESB Health Savings Account

ESB-5387-1116 Health Savings Account How Does it Work? Set aside money, pre-tax, to pay for eligible medical expenses ESB-5387-1116 Why a Health Savings Account? 1 2 3 An account you own Triple tax advantage

ESB-5387-1116 Health Savings Account How Does it Work? Set aside money, pre-tax, to pay for eligible medical expenses ESB-5387-1116 Why a Health Savings Account? 1 2 3 An account you own Triple tax advantage

Is MITRE s HD Care PPO + HSA right for you?

Is MITRE s HD Care PPO + HSA right for you? How to leverage the plan for long-term advantages MITRE Human Resources BOOKMARK What is a High Deductible Health Plan...1 What is a Health Savings Account?...3

Is MITRE s HD Care PPO + HSA right for you? How to leverage the plan for long-term advantages MITRE Human Resources BOOKMARK What is a High Deductible Health Plan...1 What is a Health Savings Account?...3

First Choice Health Network, Inc. Flexible Benefits Summary Plan Document

Effective September 1, 2010 First Choice Health Network, Inc. Flexible Benefits Summary Plan Document www.myfirstchoice.fchn.com Table of Contents Introduction to FCH s Cafeteria Plan (Section 125)...

Effective September 1, 2010 First Choice Health Network, Inc. Flexible Benefits Summary Plan Document www.myfirstchoice.fchn.com Table of Contents Introduction to FCH s Cafeteria Plan (Section 125)...

Scott Florsheim, American Fidelity, WASBO May 2016