METRO VANCOUVER REGIONAL DISTRICT PERFORMANCE AND AUDIT COMMITTEE

|

|

|

- Marcus Patrick

- 6 years ago

- Views:

Transcription

1 METRO VANCOUVER REGIONAL DISTRICT PERFORMANCE AND AUDIT COMMITTEE REGULAR MEETING Friday, July 7, :00 a.m. 2 nd Floor Boardroom, 4330 Kingsway, Burnaby, British Columbia. 1. ADOPTION OF THE AGENDA A G E N D A July 7, 2017 Regular Meeting Agenda That the Performance and Audit Committee adopt the agenda for its regular meeting scheduled for July 7, 2017 as circulated. 2. ADOPTION OF THE MINUTES 2.1 April 13, 2017 Regular Meeting Minutes That the Performance and Audit Committee adopt the minutes of its regular meeting held April 13, 2017 as circulated. 3. DELEGATIONS 4. INVITED PRESENTATIONS 5. REPORTS FROM COMMITTEE OR STAFF 5.1 Corporate Allocation Policy Designated Speaker: Phil Trotzuk That the Performance and Audit Committee endorse the Corporate Allocation Policy as presented in the attached report, dated June 27, 2017, titled Corporate Allocation Policy. 5.2 GVS&DD Development Cost Charge Program Review - Update Designated Speaker: Dean Rear That the Performance and Audit Committee endorse the updated GVS&DD Development Charge rates and consultation plan as presented in the attached report, dated June 23, 2017, titled GVS&DD Development Cost Charge Program Review - Update. 1 Note: Recommendation is shown under each item, where applicable. June 28, 2017 PAU - 1

2 Performance and Audit Committee Regular Agenda July 7, 2017 Agenda Page 2 of City of White Rock Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 Designated Speaker: Dean Rear That the MVRD Board: a) pursuant to Sections 182(1)(b) and 182(2)(a) of the Community Charter, give consent to the request for financing from the City of White Rock in the amount of $2,062,000; and b) give first, second and third reading to Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 being a bylaw to authorize the entering into an Agreement respecting financing between the Metro Vancouver Regional District and the Municipal Finance Authority of British Columbia; and c) pass and finally adopt Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 ; and d) forward Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 to the Inspector of Municipalities for Certificate of Approval. 5.4 Township of Langley Metro Vancouver Regional District Security Issuing Bylaw No. 1248, 2017 Designated Speaker: Dean Rear That the MVRD Board: a) pursuant to Sections 182(1)(b) and 182(2)(a) of the Community Charter, give consent to the request for financing from the Township of Langley in the amount of $25,460,000; and b) give first, second and third reading to Metro Vancouver Regional District Security Issuing Bylaw No. 1248, 2017 being a bylaw to authorize the entering into an Agreement respecting financing between the Metro Vancouver Regional District and the Municipal Finance Authority of British Columbia; and c) pass and finally adopt Metro Vancouver Regional District Security Issuing Bylaw No. 1248, 2017 ; and d) forward Metro Vancouver Regional District Security Issuing Bylaw No. 1248, 2017 to the Inspector of Municipalities for Certificate of Approval. 5.5 Village of Lions Bay Metro Vancouver Regional District Security Issuing Bylaw No. 1249, 2017 Designated Speaker: Dean Rear That the MVRD Board: a) pursuant to Sections 182(1)(b) and 182(2)(a) of the Community Charter, give consent to the request for financing from the Village of Lions Bay in the amount of $460,900; and b) give first, second and third reading to Metro Vancouver Regional District Security Issuing Bylaw No. 1249, 2017 being a bylaw to authorize the entering into an Agreement respecting financing between the Metro Vancouver Regional District and the Municipal Finance Authority of British Columbia; and c) pass and finally adopt Metro Vancouver Regional District Security Issuing Bylaw No. 1249, 2017 ; and PAU - 2

3 Performance and Audit Committee Regular Agenda July 7, 2017 Agenda Page 3 of 4 d) forward Metro Vancouver Regional District Security Issuing Bylaw No. 1249, 2017 to the Inspector of Municipalities for Certificate of Approval. 5.6 Interim Financial Performance Report - May 2017 Designated Speaker: Dean Rear That the Performance and Audit Committee receive for information the report dated June 16, 2017, titled Interim Financial Performance Report - May Investment Position and Returns - January 1 to April 30, 2017 Designated Speaker: Dean Rear That the Performance and Audit Committee receive for information the report dated June 19, 2017, titled Investment Position and Returns January 1 to April 30, Status of Water, Liquid Waste and Solid Waste Capital Expenditures to April 30, 2017 Designated Speaker: Dean Rear That the Performance and Audit Committee receive for information the report dated June 12, 2017, titled Status of Water, Liquid Waste and Solid Waste Capital Expenditures to April 30, Metro Vancouver Banking Services Designated Speaker: Dean Rear That the Performance and Audit Committee receive for information the report dated June 18, 2017, titled Metro Vancouver Banking Services Tender/Contract Award Information March to May 2017 Designated Speaker: Roy Moulder That the Performance and Audit Committee receive for information the report dated June 23, 2017, titled Tender/Contract Award Information March to May Manager s Report Designated Speaker: Phil Trotzuk That the Performance and Audit Committee receive for information the report dated June 23, 2017, titled Manager s Report. 6. INFORMATION ITEMS 7. OTHER BUSINESS 8. BUSINESS ARISING FROM DELEGATIONS PAU - 3

4 Performance and Audit Committee Regular Agenda July 7, 2017 Agenda Page 4 of 4 9. RESOLUTION TO CLOSE MEETING That the Performance and Audit close its regular meeting schedule for July 7, 2017 pursuant to the Community Charter provisions, Section 90 (1) (i) as follows: 90 (1) A part of the meeting may be closed to the public if the subject matter being considered relates to or is one or more of the following: (i) the receipt of advice that is subject to solicitor-client privilege, including communications necessary for that purpose. 10. ADJOURNMENT/CONCLUSION That the Performance and Audit Committee adjourn/conclude its regular meeting of July 7, Membership: Walton, Richard (C) North Vancouver District Baldwin, Wayne (VC) White Rock Bell, Corisa Maple Ridge Brodie, Malcolm Richmond Coté, Jonathan New Westminster Fox, Charlie Langley Township Gill, Tom Surrey Jordan, Colleen Burnaby McEwen, John Anmore Meggs, Geoff - Vancouver Mussatto, Darrell North Vancouver City O Neill, Terry Coquitlam Smith, Michael West Vancouver PAU - 4

5 METRO VANCOUVER REGIONAL DISTRICT PERFORMANCE AND AUDIT COMMITTEE Minutes of the Regular Meeting of the Metro Vancouver Regional District (MVRD) Performance and Audit Committee held at 9:02 a.m. on Thursday, April 13, 2017 in the 2 nd Floor Boardroom, 4330 Kingsway, Burnaby, British Columbia. MEMBERS PRESENT: Chair, Mayor Richard Walton, North Vancouver District Vice Chair, Mayor Wayne Baldwin, White Rock (arrived at 9:05 a.m.) Mayor Jonathan Coté, New Westminster Councillor Charlie Fox, Langley Township Councillor Tom Gill, Surrey Councillor Colleen Jordan, Burnaby Mayor John McEwen, Anmore Mayor Darrell Mussatto, North Vancouver City (departed at 10:58 a.m.) Councillor Terry O Neill, Coquitlam Mayor Michael Smith, West Vancouver (departed at 10:59 a.m.) MEMBERS ABSENT: Councillor Corisa Bell, Maple Ridge Mayor Malcolm Brodie, Richmond Councillor Geoff Meggs, Vancouver STAFF PRESENT: Phil Trotzuk, Chief Financial Officer Carol Mason, Chief Administrative Officer Agata Kosinski, Assistant to Regional Committees, Board and Information Services 1. ADOPTION OF THE AGENDA 1.1 April 13, 2017 Regular Meeting Agenda It was MOVED and SECONDED That the Performance and Audit Committee adopt the agenda for its regular meeting scheduled for April 13, 2017 as circulated. CARRIED Minutes of the Regular Meeting of the MVRD Performance and Audit Committee held on Friday, April 13, 2017 Page 1 of 7 PAU - 5

6 2. ADOPTION OF THE MINUTES 2.1 February 2, 2017 Regular Meeting Minutes It was MOVED and SECONDED That the Performance and Audit Committee adopt the minutes of its regular meeting held February 2, 2017 as circulated. CARRIED 2.2 February 10, 2017 Special Joint Finance and Intergovernment Committee and Performance and Audit Committee Meeting Minutes 3. DELEGATIONS No items presented. It was MOVED and SECONDED That the Performance and Audit Committee receive for information the minutes of the Special Joint Finance and Intergovernment Committee and Performance and Audit Committee Meeting held February 10, CARRIED 4. INVITED PRESENTATIONS No items presented. 5. REPORTS FROM COMMITTEE OR STAFF 5.1 Draft Audited 2016 Financial Statements Report dated March 30, 2017 from Phil Trotzuk, Chief Financial Officer and Linda Sabatini, Division Manager, Finance Operations and Systems, seeking Board approval of the Audited 2016 Financial Statements for the Greater Vancouver Districts and the Metro Vancouver Housing Corporation. 9:05 a.m. Vice Chair, Mayor Baldwin arrived at the meeting. Phil Trotzuk, Chief Financial Officer, provided the Committee with a presentation outlining the Draft Audited 2016 Financial Statements and the 2016 Financial Results Year-End. Members suggested consideration be given to: Evaluating the increases in expenses for Electoral Area A Accounting for the large surpluses in the budget Deferred projects Presentation material titled 2016 Metro Vancouver Finances is retained with the April 13, 2017 Performance and Audit Committee agenda. Minutes of the Regular Meeting of the MVRD Performance and Audit Committee held on Friday, April 13, 2017 Page 2 of 7 PAU - 6

7 It was MOVED and SECONDED a) That the MVRD Board approve the Audited 2016 Consolidated Financial Statements for the Greater Vancouver Regional District; b) That the GVS&DD Board approve the Audited 2016 Financial Statements for the Greater Vancouver Sewerage and Drainage District; c) That the GVWD Board approve the Audited 2016 Financial Statements for the Greater Vancouver Water District; d) That the MVHC Board approve the Audited 2016 Financial Statements for the Metro Vancouver Housing Corporation. CARRIED Financial Results Year-End Report dated April 6, 2017 from Dean Rear, Director, Financial Planning and Operations, updating the Board on financial performance for the year ending December 31, 2016 as compared to the 2016 annual budget. It was MOVED and SECONDED That the MVRD Board receive for information the report dated April 6, 2017, titled 2016 Financial Results Year-End. CARRIED Agenda Varied The order of the agenda was varied to consider a resolution to close the meeting at this point. 9. RESOLUTION TO CLOSE MEETING It was MOVED and SECONDED That the Performance and Audit close its regular meeting schedule for April 13, 2017 pursuant to the Community Charter provisions, Section 90 (1) (l) as follows: 90 (1) A part of a meeting may be closed to the public if the subject matter being considered relates to or is one of more of the following: (l) discussions with regional district officers and employees respecting regional district objectives, measures and progress reports for the purposes of preparing an annual report under section 98 [annual municipal report] of the Charter. CARRIED Adjournment The Performance and Audit Committee adjourned its regular meeting of April 13, 2017 at 9:54 a.m. to go into a closed meeting. Reconvene The Performance and Audit Committee reconvened its meeting of April 13, 2017 at 10:10 a.m. with the same members being in attendance. Minutes of the Regular Meeting of the MVRD Performance and Audit Committee held on Friday, April 13, 2017 Page 3 of 7 PAU - 7

8 5.3 Greater Vancouver Sewerage and Drainage District Development Cost Charge Reserve Fund Expenditure Bylaw No. 303, 2017 Report dated March 10, 2017 from Dean Rear, Director, Financial Planning and Operations, requesting that the GVS&DD Board give first, second and third reading to Greater Vancouver Sewerage and Drainage District Development Cost Charge Reserve Fund Expenditure Bylaw No. 303, 2017, and pass and finally adopt Greater Vancouver Sewerage and Drainage District Development Cost Charge Reserve Fund Expenditure Bylaw No. 303, It was MOVED and SECONDED That the GVS&DD Board: a) give first, second and third reading to Greater Vancouver Sewerage and Drainage District Development Cost Charge Reserve Fund Expenditure Bylaw No. 303, b) pass and finally adopt Greater Vancouver Sewerage and Drainage District Development Cost Charge Reserve Fund Expenditure Bylaw No. 303, CARRIED Mayor Mussatto absent at the vote. 5.4 Performance and Audit Committee Terms of Reference Report dated April 6, 2017 from Carol Mason, Chief Administrative Officer, providing the Board with a revised Terms of Reference based on input received at the joint meeting on financial planning and oversight with the Finance and Intergovernment Committee. In response to questions, members were informed about performance tracking and the internal audit system. Members were invited to show reporting styles implemented by their local municipalities to provide as examples of possible future options for Metro Vancouver reporting metrics. It was MOVED and SECONDED That the MVRD Board receive for information the report dated April 6, 2017, titled Performance and Audit Committee Terms of Reference. CARRIED 5.5 Semi-Annual Report on GVS&DD Development Cost Charges Report dated March 10, 2017 from Dean Rear, Director, Financial Planning and Operations, presenting the Committee with a report on the 2016 GVS&DD Development Cost Charge (DCC) revenues and any implications on their adequacy, as required in the Board s policy. It was MOVED and SECONDED That the Performance and Audit Committee receive for information the report dated March 10, 2017, titled Semi-Annual Report on GVS&DD Development Cost Charges. CARRIED Minutes of the Regular Meeting of the MVRD Performance and Audit Committee held on Friday, April 13, 2017 Page 4 of 7 PAU - 8

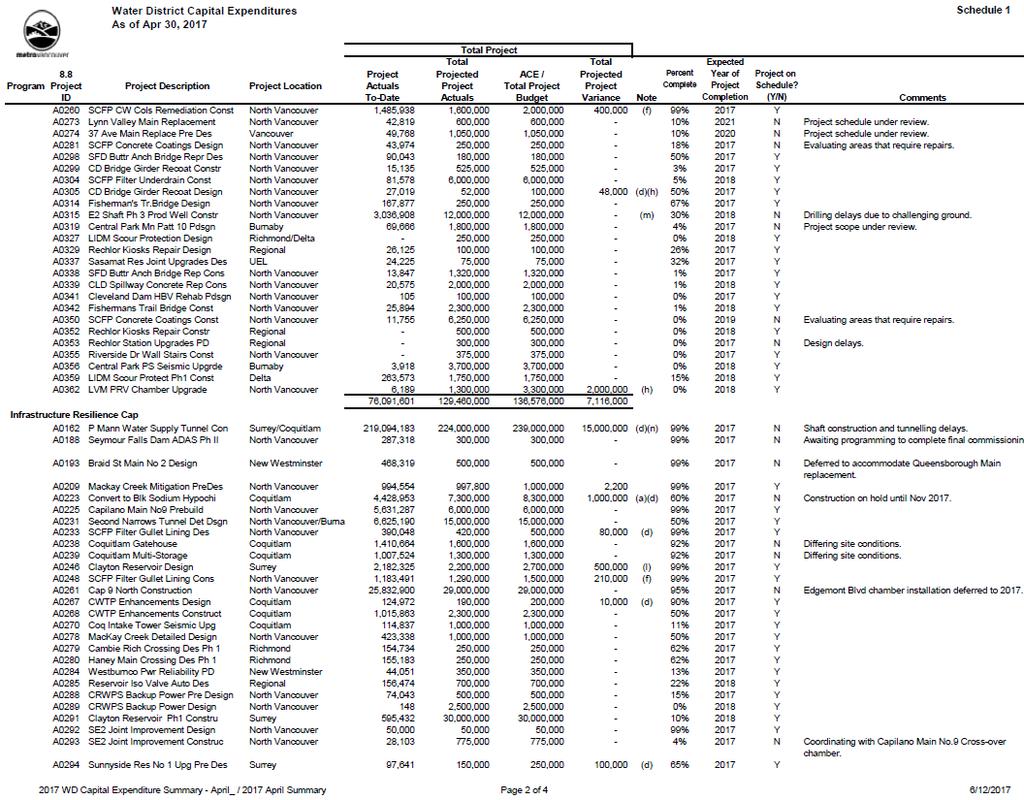

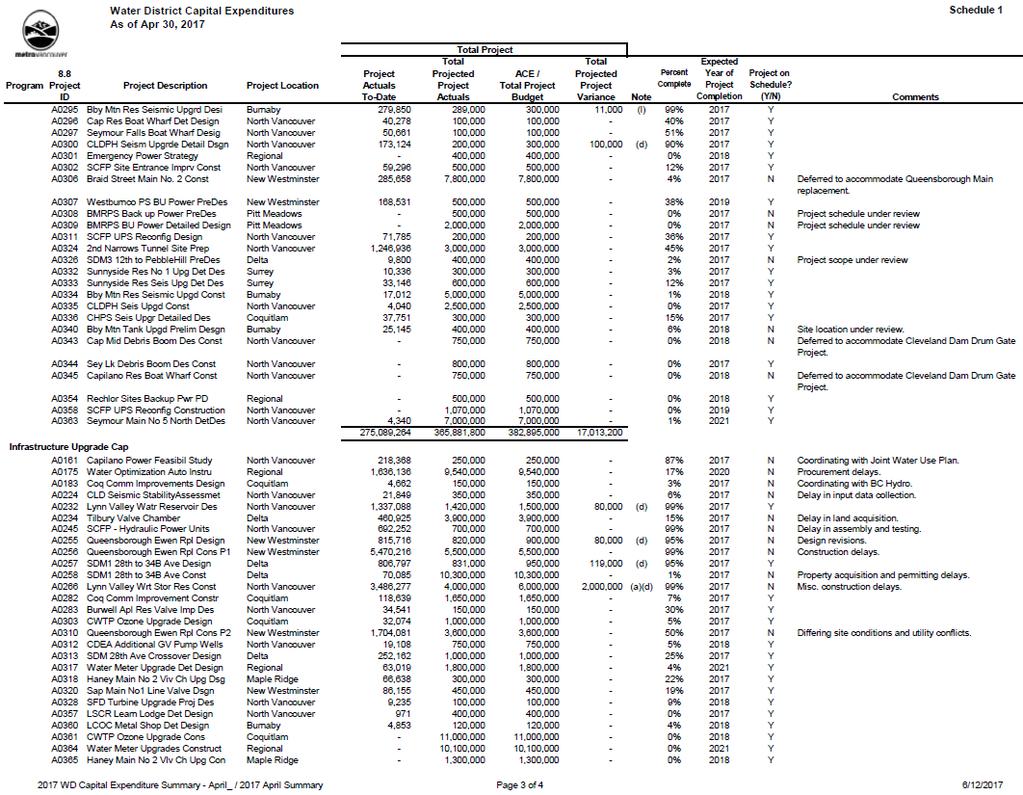

9 5.6 Status of Water, Liquid Waste and Solid Waste Capital Expenditures to December 31, 2016 Report dated March 17, 2017 from Dean Rear, Director, Financial Planning and Operations, reporting on the status of the capital projects for Water, Liquid Waste and Solid Waste. It was MOVED and SECONDED That the Performance and Audit Committee receive for information the report dated March 17, 2017, titled Status of Water, Liquid Waste and Solid Waste Capital Expenditures to December 31, CARRIED 5.7 Corporate Investment Procedures Report dated March 23, 2017 from Dean Rear, Director, Financial Planning and Operations, providing the Committee with information on the process for making corporate investment decisions. Dean Rear, Director, Financial Planning and Operations, provided the Committee with a presentation on corporate investment procedures, outlining corporate investment policy objectives, investing process, investment tendering, changes and improvements, and the government of Canada Bond yields versus Metro Vancouver internal rate of return. Presentation material titled Corporate Investment Procedures is retained with the April 13, 2017 Performance and Audit Committee agenda. It was MOVED and SECONDED That the Performance and Audit Committee receive for information the report dated March 23, 2017, titled Corporate Investment Procedures. CARRIED 5.8 Tender/Contract Award Information December 2016 to February 2017 Report dated April 5, 2017 from Phil Trotzuk, Chief Financial Officer, providing the Committee with information regarding to contracts, handled through the Purchasing Division, with a total anticipated value at, or in excess of, $500,000 (exclusive of taxes). On-table replacement page for Appendix A No. 15. to the April 5, 2017 report titled Tender/Contract Award Information December 2016 to February 2017 was provided and is retained with the April 13, 2017 Performance and Audit Committee Agenda package. Minutes of the Regular Meeting of the MVRD Performance and Audit Committee held on Friday, April 13, 2017 Page 5 of 7 PAU - 9

10 It was MOVED and SECONDED That the Performance and Audit Committee receive for information the report dated April 5, 2017, titled Tender/Contract Award Information December 2016 to February CARRIED 5.9 Manager s Report Report dated April 4, 2017 from Phil Trotzuk, Chief Financial Officer, providing the Performance and Audit Committee with an update on the status of the Committee s key priorities within the 2017 Work Plan, MFA Spring Issue update, and presenting the Metro 2040 Performance Monitoring Dashboard. 10:58 a.m. Mayor Mussatto, departed the meeting. 10:59 a.m. Mayor Smith, departed the meeting. 6. INFORMATION ITEMS No items presented. 7. OTHER BUSINESS No items presented. Heather McNell, Division Manager of Growth Management, Parks, Planning and Environment, and Stephanie McCardle, Policy Coordinator, External Relations, Corporate Communications, provided the Committee with a presentation on the Metro 2040 Performance Monitoring Dashboard. Presentation material titled Metro 2040 Performance Monitoring Dashboard is retained with the April 13, 2017 Performance and Audit Committee agenda. It was MOVED and SECONDED That the Performance and Audit Committee receive for information the report dated April 4, 2017, titled Manager s Report. CARRIED 8. BUSINESS ARISING FROM DELEGATIONS No items presented. 9. RESOLUTION TO CLOSE MEETING This item was previously considered. Minutes of the Regular Meeting of the MVRD Performance and Audit Committee held on Friday, April 13, 2017 Page 6 of 7 PAU - 10

11 10. ADJOURNMENT/CONCLUSION It was MOVED and SECONDED That the Performance and Audit Committee conclude its regular meeting of April 13, CARRIED (Time: 11:08 a.m.) Agata Kosinski, Assistant to Regional Committees Richard Walton, Chair FINAL Minutes of the Regular Meeting of the MVRD Performance and Audit Committee held on Friday, April 13, 2017 Page 7 of 7 PAU - 11

12 5.1 To: From: Performance and Audit Committee Phil Trotzuk, Chief Financial Officer Date: June 28, 2017 Meeting Date: July 7, 2017 Subject: Corporate Allocation Policy RECOMMENDATION That the Performance and Audit Committee endorse the Corporate Allocation Policy as presented in the attached report, dated June 27, 2017, titled Corporate Allocation Policy. The Performance and Audit Committee responsibilities as included in the Committee Terms of Reference includes the following: Reviewing financial policies and recommending to the Finance and Intergovernment Committee on proposed new policies and policy amendments The proposed Corporate Allocation Policy is presented to the Performance and Audit Committee for review and comment prior to consideration at the Finance and Intergovernment Committee on July 19, Attachment: 1. Finance and Intergovernment Committee Report: Corporate Allocation Policy, dated June 27, PAU - 12

13 To: From: Finance and Intergovernment Committee Carol Mason, Commissioner / Chief Administrative Officer Phil Trotzuk, Chief Financial Officer Date: June 27, 2017 Meeting Date: July 19, 2017 Subject: Corporate Allocation Policy RECOMMENDATION That the Board approve the Corporate Allocation Policy as presented in the report dated June 27, 2017, titled Corporate Allocation Policy. PURPOSE To seek Board approval of a Corporate Allocation Policy to provide a framework for establishing the appropriate allocation of costs incurred by centralized support services in delivering support services to all business activities of Metro Vancouver s four legal entities. BACKGROUND Metro Vancouver provides centralized support services that provide a benefit to all business activities of the Metro Vancouver four legal entities. These centralized services are delivered through six departments: Corporate Planning, Corporate Services, External Relations, Financial Services, Human Resources and Legal and Legislative Services. The Local Government Act requires that all costs incurred by a regional district in relation to a service, including the costs of administration attributable to the service, are part of the costs of that service. As such, rates, fees and charges must reflect the full cost of Metro Vancouver services to which they relate including those costs incurred by centralized support services. This policy serves to appropriately account for all costs of providing Metro Vancouver services and matching those costs with supporting revenues. Metro Vancouver currently has a defined process of apportioning these centralized support costs as part of the annual budget process, however, as the allocation of these costs have a direct impact on the rates, fees and charges recovered by Metro Vancouver, formalized Board direction on the allocation of these costs is appropriate. This report outlines the principles and methodology of the proposed policy to allocate these costs for Committee and Board consideration. CENTRALIZED SUPPORT SERVICES Centralized support services provide benefit to all business areas of Metro Vancouver and primarily include: corporate administration, information technology, building operations, corporate safety, corporate communications, financial oversight, staff-related services, in-house legal and information services PAU - 13

14 Corporate Allocation Policy Finance and Intergovernment Committee Meeting Date: July 19, 2017 Page 2 of 5 The total centralized support costs, net of revenues, included in the 2017 Metro Vancouver Budget is $54.8 million ALLOCATION PRINCIPLES AND METHODOLOGY Research and Analysis As part of the Corporate Allocation Policy development process, Metro Vancouver s current allocation rationale was examined along with the practices adopted by other local governments across Canada and the United States. These other local government entities included: Surrey, Richmond, Burnaby, Edmonton, Capital Regional District, York Region, Peel Region and local municipalities in Washington State. In addition, research was gathered on allocation methodologies from major utilities including: Enbridge Gas, Hydro One in Ontario and Alberta Utilities Commission. The practices adopted by other organizations show significant variations on the allocation of centralized support costs being based on the specific circumstances of those organizations. While there are differences in allocation methodologies used by other organizations, the methodologies include some common elements including that centralized support costs should be allocated directly to all benefiting entities and functions where direct benefits can be reasonably determined and in cases where proxies of benefits provided are used as an allocation basis, the establishment of the proxies should be documented including all relevant information on the process and rationale behind the allocation methodology. Metro Vancouver Allocation Principles In cases where it can be demonstrated and quantified that a Metro Vancouver service receives a specific direct benefit from a centralized service activity, the associated costs will be allocated directly to that service. These costs typically include, but are not limited to, costs related to programs such as Metro Vancouver s pooled fleet vehicles and equipment acquisitions, external legal counsel services and contracted security services. For the other centralized service activities, the Corporate Allocation Policy provides a framework that guides the apportionment of Metro Vancouver s centralized support costs to its four legal entities based on a reasonable approximation of services provided in supporting the entity s pursuit of both operational and strategic objectives. The methodology for approximating the level of service provided by each these centralized support services is guided by the following principles: Efficient the method and process of allocating net centralized support costs are easily administered, replicable and comprehensible Equitable net centralized support costs are apportioned fairly across Metro Vancouver services and to the extent possible, upholds a user-pay approach for the level of service provided Consistent net centralized support costs are allocated in a way that mitigates large fluctuations and ensures relative certainty, based on level of use Transparent net centralized support costs allocated to Metro Vancouver services are clearly identified PAU - 14

15 Corporate Allocation Policy Finance and Intergovernment Committee Meeting Date: July 19, 2017 Page 3 of 5 Within these guiding principles is the understanding that the approximate level of service provided to a Metro Vancouver service is often measured by the impact of two primary factors: (1) number of staff or (2) level of business activity. Those services with larger staff complements will require more centralized support in the areas of payroll, recruiting services, organizational support, benefit administration, IT computer support, training and head office building operations and therefore, will be allocated a higher proportion of these centralized support costs. Alternatively, services that incur significant capital expenditures and have broader business operations will require more centralized support in the areas of purchasing, accounts payable, debt management, budgeting, accounts receivable, legal, business applications and corporate planning and consequently, will be allocated a higher proportion of these centralized costs. To ensure the appropriate allocation of corporate costs, it is proposed that direct delivery services will be allocated a proportion of net centralized support costs based on their prior year operating budget using the parameters described above. Salaries and benefits will serve as indicators that reflect the number of staff supported while other expenditures will serve as indicators of the level of business activity. In cases where it can be demonstrated and quantified that a Metro Vancouver service receives a specific direct benefit from an activity, the associated costs are proposed to be allocated directly to that service. These costs typically include, but are not limited to, costs related to programs such as Metro Vancouver s pooled fleet vehicles and equipment acquisitions, external legal counsel services and contracted security services. ALLOCATION OF CENTRALIZED SUPPORT COSTS TO METRO VANCOUVER SERVICES Internal Service Delivery. The majority of Metro Vancouver services are delivered to members through an internal direct service model. This means that Metro Vancouver staff are engaged in the direct delivery of the service, including most or all of the operating and capital activities. These services include the following: Greater Vancouver Water District Greater Vancouver Sewerage and Drainage District (Liquid Waste and Solid Waste) Metro Vancouver Housing Corporation Metro Vancouver Regional District (Air Quality, Electoral Area, General Government, Labour Relations, Regional GPS, Regional Parks and Regional Planning) For these services, proportionate allocation of net centralized support costs is proposed to be apportioned based on the applicable prior year s operation budget excluding those budget items which inflate expenditures but have a lower overall impact on the requirement for centralized support services. These budget items include contributions to reserve, a portion of third party operating contracts and MVHC long-term mortgages and are adjusted for in order to better reflect the level of service provided by the centralized support services. PAU - 15

16 Corporate Allocation Policy Finance and Intergovernment Committee Meeting Date: July 19, 2017 Page 4 of 5 External Service Delivery For three Metro Vancouver Regional District services E911 Emergency Telephone, Regional Emergency Management and Sasamat Volunteer Fire Service an external service provider is used to deliver services to members through an external service delivery model. This means that Metro Vancouver staff are engaged to a lesser extent in the delivery of the service, its operating activities and its capital activities. For these services, the proportionate allocation of net centralized support costs is proposed to be apportioned as follows: E911 Emergency Telephone Service allocated net centralized support costs equal to 2% of its current year s operating program budget excluding contributions to reserve. This reflects the level of service associated with the administration of the E911 Telephone Service operating contract and routine finance support. Regional Emergency Management allocated net centralized support costs equal to 5% of its current year s operating program budget excluding contributions to reserve. This reflects the level of service associated with the overall administration of the program, purchasing support and accounts payable. Sasamat Fire Protection Service allocated net centralized support costs equal to 10% of its current year s operating program budget excluding contributions to reserve and large one-time asset purchases. This reflects the level of service associated with function management, fleet vehicle administration, procurement, accounts payable, payroll, budgeting and accounting. Based on the research undertaken in reviewing policy alternatives and the unique structure of Metro Vancouver in allocating costs, the following alternatives are presented for consideration. ALTERNATIVES 1. That the Board approve the Corporate Allocation Policy as presented in the report dated June 27, 2017, titled Corporate Allocation Policy. 2. That the Board approve the Corporate Allocation Policy in the report dated June 27, 2017, titled Corporate Allocation Policy with amendments. 3. That the Board receive for information the report dated June 27, 2017, titled Corporate Allocation Policy and provide alternate direction. FINANCIAL IMPLICATIONS The Corporate Allocation Policy does not have any impact on the overall amount of centralized support costs included in the budget. The policy does, however, have an impact on the total budgets including rates, fees and charges of individual legal entities and functions which is important as there are differences in the supporting membership of each entity and function. The approval of alternative one will ensure Metro Vancouver has in place a formal policy that accounts for the costs of providing centralized support services and that they are reflected appropriately to legal entities and functions. This will reduce annual budget fluctuations while enhancing financial management and long-term financial planning. PAU - 16

17 Corporate Allocation Policy Finance and Intergovernment Committee Meeting Date: July 19, 2017 Page 5 of 5 The approval of alternatives two or three will have varied financial implications which will need to be quantified accordingly. SUMMARY / CONCLUSION The allocation of centralized support costs to the Metro Vancouver legal entities is an important component in Metro Vancouver s financial planning process as enabling legislation requires that Metro Vancouver rates, fees and charges must reflect the full cost of the Metro Vancouver services to which they relate. The direct allocation or the allocation methodology, based on adjusted operating budgets, included in the policy is reflective of the level of service provided by centralized support services and incorporates the principles of efficiency, equitability, consistency and transparency Staff recommend that the Board approve alternative one with the proposed policy, as attached, to provide clear Board direction for the principles and methodology associated with the allocation of centralized support costs. Attachment: (Doc # ) Corporate Allocation Policy PAU - 17

18 BOARD POLICY CORPORATE ALLOCATION Effective Date: Approved By: PURPOSE To provide a framework for establishing the appropriate allocation of costs incurred by centralized support services in delivering support services to all business activities of Metro Vancouver s four legal entities. DEFINITIONS Centralized Support Services are services delivered by centralized departments to support all four Metro Vancouver legal entities and regional district functions through the following: Corporate Planning, Corporate Services, External Relations, Financial Services, Human Resources, and Legal and Legislative Services. Net Centralized Support Costs means expenditures incurred by centralized support services that are net of any costs allocated directly to a legal entity or function and any revenues generated by the centralized support service. Metro Vancouver Service refers to a service provided by one of the four legal entities to which costs of centralized support services are allocated. The legal entities include the Metro Vancouver Housing Corporation (MVHC), Greater Vancouver Water District (GVWD), Greater Vancouver Sewerage and Drainage District (GVS&DD), which includes the legal functions of Liquid Waste and Solid Waste, and the Metro Vancouver Regional District (MVRD), which includes the statutory functions of Air Quality, Electoral Area, General Government, Labour Relations, Regional GPS, Regional Parks, Regional Planning, E911 Telephone Service, Regional Emergency Management and Sasamat Fire Protection Service. POLICY The Local Government Act requires that all costs incurred by a regional district in relation to a service, including the costs of administration attributable to the service, are part of the costs of that service. As such, rates, fees and charges must reflect the full cost of Metro Vancouver services to which they relate including those costs incurred by centralized support services. This policy serves to appropriately account for all costs of providing Metro Vancouver services and matching those costs with supporting revenues. All costs incurred by centralized support services will be allocated to the benefiting Metro Vancouver service utilizing a methodology approximating the level of service provided. The methodology for calculating corporate allocation based on an approximation of service level is provided below Corporate Allocation Policy Page 1 of 4 PAU - 18

19 BOARD POLICY CORPORATE ALLOCATION PRINCIPLES Every Metro Vancouver service utilizes resources of centralized support departments to some extent in the delivery of that service. The extent of centralized support may range from providing simple contract administration or Metro Vancouver Board and Committee support services, to more extensive support that includes human resources, legal, legislative, communications, financial, information technology, building operations, emergency planning and corporate safety services. The methodology for approximating the level of service provided by each these centralized support services is guided by the following principles: Efficient the method and process of allocating net centralized support costs are easily administered, replicable and comprehensible Equitable net centralized support costs are apportioned fairly across Metro Vancouver services and to the extent possible, upholds a user-pay approach for the level of service provided Consistent net centralized support costs are allocated in a way that mitigates large fluctuations and ensures relative certainty, based on level of use Transparent net centralized support costs allocated to Metro Vancouver services are clearly identified Staffing and Business Activity Requirements Within the guiding principles defined in this policy is the understanding that the approximate level of service provided to a Metro Vancouver service is often measured by the impact of two primary factors: (1) number of staff or (2) level of business activity. For example, those services with larger staff complements will require more centralized support in the areas of payroll, recruiting services, organizational support, benefit administration, IT computer support, training and head office building operations and therefore, will be allocated a higher proportion of these centralized support costs. Alternatively, services that incur significant capital expenditures and procurement activity will require more centralized support in the areas of purchasing, accounts payable, debt management, budgeting, accounts receivable, legal, business applications and corporate planning and consequently, will be allocated a higher proportion of these centralized costs. To ensure the appropriate allocation of corporate costs, direct delivery services will be allocated a proportion of net centralized support costs based on their prior year operating budget using the parameters described above. Salaries and benefits will serve as indicators that reflect the number of staff supported while other expenditures will serve as indicators of the level of business activity. Lower Impact Activity Requirements Some budget items may inflate expenditures but have a lower overall impact on the requirement for centralized support services. These budget items include contributions to reserve, a portion of large third party operating contracts and MVHC long-term mortgages. In order to better reflect the level of service provided by the centralized support services, the calculation of apportionment costs in annual operating budgets will be adjusted for those budget items not requiring centralized support Corporate Allocation Policy Page 2 of 4 PAU - 19

20 BOARD POLICY Specific Direct Service Activity Requirements In cases where it can be demonstrated and quantified that a Metro Vancouver service receives a specific direct benefit from an activity, the associated costs will be allocated directly to that service. These costs typically include, but are not limited to, costs related to programs such as Metro Vancouver s pooled fleet vehicles and equipment acquisitions, external legal counsel services and contracted security services. METRO VANCOUVER SERVICES INTERNAL SERVICE DELIVERY The majority of Metro Vancouver services are delivered to members through an internal direct service model. This means that Metro Vancouver staff are engaged in the direct delivery of the service, including most or all of the operating and capital activities. For these services, the proportionate allocation of net centralized support costs shall be apportioned as follows: Greater Vancouver Water District (GVWD) The GVWD will be allocated a proportionate share of the net centralized support costs based on its prior year s operating budget excluding centralized support cost allocation and contributions to reserve. Greater Vancouver Sewerage and Drainage District (GVS&DD) Liquid Waste The Liquid Waste function will be allocated a proportionate share of the net centralized support costs based on its prior year s operating budget excluding centralized support cost allocation and contributions to reserve. Greater Vancouver Sewerage and Drainage District (GVS&DD) Solid Waste The Solid Waste function will be allocated a proportionate share of the net centralized support costs based on its prior year s operating budget excluding centralized support cost allocation, 80% of large third party operating contracts and contributions to reserve. The adjustment for a portion of third party operating contracts is to reflect that they require a lower level of service compared to other business activities. Metro Vancouver Housing Corporation (MVHC) The MVHC will be allocated a proportionate share of the net centralized support costs based on its prior year s operating budget excluding centralized support cost allocation, contributions to reserve and 80% of annual mortgage payments. Metro Vancouver Regional District (MVRD) The MVRD functions of Air Quality, Electoral Area, General Government, Labour Relations, Regional GPS, Regional Parks and Regional Planning will be allocated a proportionate share of the net centralized support costs based on their prior year s operating budget excluding centralized support cost allocation, contributions to reserve and large one-time asset purchases. METRO VANCOUVER SERVICES EXTERNAL SERVICE DELIVERY While the majority of Metro Vancouver services are provided through the internal service delivery model some regional services engage the use of an external service provider to deliver services to Corporate Allocation Policy Page 3 of 4 PAU - 20

21 BOARD POLICY members through an external service delivery model. This means that Metro Vancouver staff are engaged to a lesser extent in the delivery of the service, its operating activities and its capital activities. For these services, the proportionate allocation of net centralized support costs shall be apportioned as follows: E911 Emergency Telephone Service E911 Emergency Telephone Service will be allocated net centralized support costs equal to 2% of its current year s operating program budget excluding contributions to reserve. This reflects the level of service associated with the administration of the E911 Telephone Service operating contract and routine finance support. Regional Emergency Management Regional Emergency Management will be allocated net centralized support costs equal to 5% of its current year s operating program budget excluding contributions to reserve. This reflects the level of service associated with the overall administration of the program, purchasing support and accounts payable. Sasamat Fire Protection Service Sasamat Volunteer Fire Service will be allocated net centralized support costs equal to 10% of its current year s operating program budget excluding contributions to reserve and large one-time asset purchases. This reflects the level of service associated with function management, fleet vehicle administration, procurement, accounts payable, payroll, budgeting and accounting Corporate Allocation Policy Page 4 of 4 PAU - 21

22 5.2 To: From: Performance and Audit Committee Dean Rear, Director, Financial Planning and Operations, Financial Services Date: June 26, 2017 Meeting Date: July 7, 2017 Subject: GVS&DD Development Cost Charge Program Review - Update RECOMMENDATION That the Performance and Audit Committee endorse, in principle, the updated GVS&DD Development Charge rates and consultation plan as presented in the attached report, dated June 23, 2017, titled GVS&DD Development Cost Charge Program Review - Update. The Performance and Audit Committee responsibilities as included in the Committee Terms of Reference includes the following: Overseeing the GVS&DD (Liquid Waste) Development Cost Charge program: Periodically reviewing the rates and recommending to the Finance and Intergovernment Committee on proposed new policies and policy amendments The proposed GVS&DD Development Cost Charge program amendments and consultation plan is presented to the Performance and Audit Committee for review and comment prior to consideration at the Finance and Intergovernment Committee on July 19, Attachment: 1. Finance and Intergovernment Report: GVS&DD Development Cost Charge Program Review - Update, dated June 23, PAU - 22

23 To: From: Finance and Intergovernment Committee Phil Trotzuk, Chief Financial Officer / General Manager, Financial Services Date: June 23, 2017 Meeting Date: July 19, 2017 Subject: GVS&DD Development Cost Charge Program Review Update RECOMMENDATION That the GVS&DD Board: a) endorse, in principle, the proposed changes to the Development Cost Charge Program with the rates as presented in Attachment 1 of the report dated June 23, 2017, titled GVS&DD Development Cost Charge Program Review Update ; and b) direct staff to proceed with public and stakeholder consultation as presented in the report dated June 23, 2017, titled GVS&DD Development Cost Charge Program Review Update. PURPOSE To present options and recommendations on the development cost charge (DCC) program rate adjustments for purposes of proceeding with consultation with the Province and community stakeholders. BACKGROUND The GVS&DD DCC program has been under review since In November of 2016 the initial results of the review, including the DCC program policy framework, proposed rate adjustments, and the transition plan for implementation of the program amendments for purposes of consultation was presented to the Utilities Committee and the Finance and Intergovernment Committee. At the November 25, 2016 meeting of the GVS&DD Board, the following motion was passed: That the GVS&DD Board direct staff to proceed with public and stakeholder consultation on the proposed changes to the Development Cost Charge Program following the adoption of the 5-year financial plan in March 2017, and direct staff to report back, prior to the consultation, on phasing of and potential strategies to mitigate the impact of the rate increases. Five year financial plan forecasts and scenarios were presented to the Board at a workshop in February 2017 and will be formally presented in October in conjunction with the 2018 annual budget. This report summarizes the options examined to mitigate the increase in the DCC rates, along with the impact of those options on the liquid waste levy, the overall 5-year financial plan and the household impact. EXISTING DCC RATES DCC rates established by sewer area are per unit for residential and per square foot for nonresidential. The existing DCC rates, in effect since 1997, are as follows: PAU - 23

24 GVS&DD Development Cost Charge Program Review Update Finance and Intergovernment Regular Committee Meeting Date: July 19, 2017 Page 2 of 5 Sewer Area Single-Family Townhouse Apartment Non-Residential Vancouver $ 944 $ 826 $ 590 $0.443 sq ft Lulu Island $1,077 $ 942 $ 673 $0.505 sq ft North Shore $1,291 $1,129 $ 807 $0.605 sq ft Fraser $1,731 $1,515 $1,082 $0.811 sq ft As these rates were established almost 20 years ago, cost and growth conditions have changed significantly and they will not be sufficient to sustain funding requirements for the growth in the region, particularly in the Fraser Sewerage Area. The chart below illustrates expected DCC reserve balances for the next 10 years with the rates currently in place. PROPOSED DCC RATES A 30 year model was developed which projects the DCC s required to fund the Liquid Waste infrastructure expansion for population growth, in conjunction with the planned development within a given sewer area. This development includes the following types of land use: single-family detached, townhouses, apartments, and non-residential development. The DCC requirements are based on funding long-term debt for the growth related infrastructure expenditures and includes future funding on existing debt as well as funding for projected debt. The proposed DCC rates presented at the November 25 th GVS&DD Board meeting were calculated assuming the requirement of funding the principal portion only on growth related long-term debt based on the current financial model over the next 30 years. The calculated rates are as follows: Sewer Area Single-Family Townhouse Apartment Non-Residential Vancouver $1,811 $1,618 $1,072 $0.93 sq ft Lulu Island $2,214 $1,915 $1,388 $1.05 sq ft North Shore $2,300 $2,076 $1,416 $1.20 sq ft Fraser $5,428 $4,695 $3,530 $2.67 sq ft Attachment 1 illustrates these rates in comparison to the existing rates and also provides the anticipated household impact of the sewer levy for the years 2017 to Also shown is a chart illustrating anticipated DCC reserve balances. PAU - 24

25 GVS&DD Development Cost Charge Program Review Update Finance and Intergovernment Regular Committee Meeting Date: July 19, 2017 Page 3 of 5 These rates represent that best estimate of the funding required for growth related infrastructure and adheres to the principle of growth paying for growth. While these DCC s represent only a very small portion of the cost of new housing, these rates are a significant increase over the existing rates. It is imperative that the DCC rates be reviewed every three to five years in order to adjust for cost increases as necessary and avoid implementing such significant increases in the future. Varying the Assist Factor Initially, the DCC Review Committee recommended a phase-in period of three years due to the significance of the increase in rates, particularly in the Fraser Sewer Area (FSA). Expanding upon this concept, options for varying the assist factor, primarily within the Fraser Sewerage, were analyzed for additional consideration. An outcome of varying the assist factor in the FSA to reduce the DCC rate resulted in the DCC rate aligning more closely with the proposed rates in the other three areas (Vancouver, North Shore, and Lulu Island). However, this change also resulted in the FSA household rate increasing to offset this loss in DCC revenue. Under this option, the FSA household rate would become closer to the household rates in the three other sewer areas, which are higher primarily due to the fact that much of the growth infrastructure in those sewerage areas was constructed prior to the implementation of the DCC program. In three of the four sewerage areas (Vancouver, Lulu Island and North Shore), the majority of the Tier 1 infrastructure (trunk sewer lines, forcemains, interceptors, pump stations) is generally well established and sufficient to meet most growth needs. The bulk of development reflects infill projects that add capacity but do not trigger significant trunk upgrades. In fact, in two of the sewerage areas (North Shore and Lulu Island) there are no Tier 1 infrastructure projects within the planned DCC program. The FSA, however, is unique in that it includes significant growth development which requires the extension of trunk lines, new pump stations, new interceptors, as well as a river crossing. There are over 70 Tier 1 projects in the FSA DCC program. Despite the fact that significant growth is anticipated within this sewer area, the resulting burden on this one portion of the region is comparatively substantial. To illustrate the impact of varying the assist factor, the table below shows DCC rates with a 50% Assist Factor for Tier 1 Projects in the Fraser Sewerage Area. Sewer Area Single-Family Townhouse Apartment Non-Residential Vancouver $1,811 $1,618 $1,072 $0.93 sq ft Lulu Island $2,214 $1,915 $1,388 $1.05 sq ft North Shore $2,300 $2,076 $1,416 $1.20 sq ft Fraser $4,453 $3,852 $2,897 $2.19 sq ft As noted above, although there would be a decrease in the DCC charges for the FSA, there would be a corresponding increase in the levy with an estimated household impact of $6 (3.5% increase over the prior year) to pay for the growth projects not being covered by the DCC s collected. Several options for varying the assist factor were presented to RAAC on May 25 th. The original proposal retaining the 1% assist factor across all four sewerage areas, without any phase in period, was the preferred approach. PAU - 25

26 GVS&DD Development Cost Charge Program Review Update Finance and Intergovernment Regular Committee Meeting Date: July 19, 2017 Page 4 of 5 WAIVER OF DCC S FOR AFFORDABLE HOUSING The language for the waiver of DCC s with respect to affordable housing development is under review concurrently by the Housing Policy and Planning group. While it s expected to add clarity and be more effective than the waiver language in the existing bylaw, changes to the waiver language is not expected to materially alter DCC revenue available for funding growth GVS&DD infrastructure projects. CONSULTATION PROCESS The consultation process to date has involved feedback from the regional advisory committees of administrators, engineers, planning and finance. Good feedback was received and there was general support for the policy framework, the initial proposed DCC rates and the transition plan. Next steps in the consultation process include expanded dialogue with the Province, meetings with affected stakeholders including the Urban Development Institute and Greater Vancouver Home Builders Association, regional Boards of Trade and Chambers of Commerce, and the initiation of broad public outreach. The proposed Communications and Engagement process, to be initiated in late August through early November, is outlined as follows: 1. Meetings with stakeholders Host a series of public meetings in each of the four sewerage areas (1 each in Lulu, Vancouver, and North Shore, and 2 in Fraser) at which Metro Vancouver representatives from Finance and Liquid Waste Services will explain the proposed DCC Program and answer questions from the audience. (Late August through October) 2. Dedicated Web Page: Create an online portal that includes detailed information the DCC Program and its anticipated impact on overall development costs. 3. Distribution Lists Distribution of materials through the appropriate Metro Vancouver databases 4. Meeting(s) with the Province of BC Ongoing throughout consultation process. (September through Early November) Further, TransLink is currently in the process of examining the feasibility of DCC funding for certain transportation projects. As it is important to recognize the impact of the cost of regional charges, Metro Vancouver and TransLink have committed to work together, where practical, on joint public consultation. IMPLEMENTATION TIMELINE It is expected that the consultation process will wrap up in November, with the results and a new DCC bylaw being brought forward before the end of the year. Staff will consult with municipalities to establish an effective date of bylaw implementation that considers the implications to existing processes and communications materials provided to prospective developers. At this time the effective date is expected to be April 1, PAU - 26

27 GVS&DD Development Cost Charge Program Review Update Finance and Intergovernment Regular Committee Meeting Date: July 19, 2017 Page 5 of 5 ALTERNATIVES 1. That the GVS&DD Board: a) endorse, in principle, the proposed changes to the Development Cost Charge Program with the rates as presented in Attachment 1 of the report dated June 23, 2017, titled GVS&DD Development Cost Charge Program Review Update ; and b) direct staff to proceed with public and stakeholder consultation as presented in the report dated June 23, 2017, titled GVS&DD Development Cost Charge Program Review Update. 2. That the Finance and Intergovernment Committee receive for information the report dated June 23, 2017, titled GVS&DD Development Cost Charge Program Review Update and provide alternate direction. FINANCIAL IMPLICATIONS Alternative 1: If the Finance and Intergovernment Committee approves alternative 1, the report will be forwarded to the GVS&DD Board for approval. The cost of the public and stakeholder engagement and consultation process will be funded through the liquid waste function budget. Details of the DCC sewerage area rate structure, projected household impact and growth projects by sewerage area are included in Attachments 1 and 2. Alternative 2: If the Finance and Intergovernment Committee approves alternative 2, further analysis may be required to determine the resulting financial impacts. SUMMARY / CONCLUSION The GVS&DD DCC program has been under review since 2014 and in November 2016 the initial review results were presented to the Utilities Committee and the Finance and Intergovernment Committee. At the direction of the Board, since that time further work has been undertaken to build the proposed DCC rates into Metro Vancouver s long term financial plan which will be considered this fall as part of the 2018 annual budget and five year financial plan process. Although a variety of options were considered in the development of the proposed DCC rate structure, the Board principle that growth pays for growth has guided the recommendations presented in this report. The current proposed DCC rates as detailed in Attachment 1 represent the best estimate of DCC funding required for growth related infrastructure and adheres to the principle of growth paying for growth. It is recommended that the Board approve the recommendations as presented in alternative one, and that staff proceed to consultation with the public and key stakeholders on the proposed DCC rate structure. Attachments: 1. Proposed DCC Rates 2. Growth Projects by Sewerage Area PAU - 27

28 ATTACHMENT PAU - 28

29 Growth Projects by Sewerage Area ATTACHMENT 2 Project Estimated Cost Vancouver Sewerage Area Collingwood Trunk Sewer $ 5,090,000 Hastings Sanitary Trunk Sewer 13,300,000 Hastings Sanitary Trunk Sewer No. 2 30,000,000 Hastings-Cassiar Intake Connection 750,000 $ 49,140,000 North Shore Sewerage Area North Vancouver Interceptor - Lynn Branch Pre-build $ 3,500,000 Lulu Island Sewerage Area Lulu Island WWTP Digester No 3 $ 53,300,000 Fraser Sewerage Area AIWWTP Effluent Pump Station $ 61,000,000 AIWWTP Site Construction Layout 600,000 Albert Street Trunk Sewer 4,600,000 Annacis Outfall System 375,000,000 Annacis Stage 5 Expansion Phase 1 & 2 595,500,000 Burnaby Lake North Interceptor Cariboo to Piper Section 41,000,000 Burnaby Lake North Interceptor Phillips to Sperling Section 42,341,163 Burnaby Lake North Interceptor Piper to Philips Section 62,100,000 Burnaby South Slope Interceptor Main Branch 9,500,000 Burnaby South Slope Interceptor West Branch Extension 13,200,000 Cloverdale PS Upgrade 31,100,000 Cloverdale Trunk Sewer Upgrade 28,975,000 Glenbrook Combined Trunk Kingsway Sanitary Section 3,400,000 Golden Ears Forcemain and River Crossing 114,000,000 Golden Ears Pump Station 38,100,000 Langley Pump Station Upgrade 14,300,000 Lozells Sanitary Trunk Golf Course Section 22,150,000 Marshend Pump Station Capacity Upgrade 9,900,000 NLWWTP Ground Improvements Phase A 24,000,000 NLWWTP Ground Improvements Phase B 18,000,000 NLWWTP Liquid Stream Phase A 356,000,000 NLWWTP Liquid Stream Phase B 256,000,000 NLWWTP Solids Handling 126,000,000 North Road Trunk Sewer 7,000,000 North Road Trunk Sewer Phase 2 3,938,000 NSI 104th Ave Extension 6,800,000 NSI Flow Management 39,500,000 NWLWWTP Options 5,000,000 NWLWWTP Phase 1 44,728,793 Port Moody PS Upgrade 9,150,000 Port Moody South Interceptor Upgrade 3,450,000 Queensborough Pump Station Replacement 6,500,000 Rosemary Heights Pressure Sewer Upgrade 10,750,000 Sapperton Forcemain Pump Station Connections 5,500,000 Sapperton Pump Station 76,400,000 South Surrey Interceptor Johnston Section 65,350,000 Sperling PS Increase Pump Capacity 3,000,000 SSI - King George Section - Odor Control Facility (OCF) and Grit Chamber 13,500,000 Stoney Creek Trunk Upgrade 10,200,000 Surrey Central Valley Upgrade 60,800,000 $ 2,618,332,956 PAU - 29

30 5.3 To: From: Performance and Audit Committee Dean Rear, Director, Financial Planning and Operations, Financial Services Date: June 26, 2017 Meeting Date: July 7, 2017 Subject: City of White Rock Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 RECOMMENDATION That the MVRD Board: a) pursuant to Sections 182(1)(b) and 182(2)(a) of the Community Charter, give consent to the request for financing from the City of White Rock in the amount of $2,062,000; and b) give first, second and third reading to Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 being a bylaw to authorize the entering into an Agreement respecting financing between the Metro Vancouver Regional District and the Municipal Finance Authority of British Columbia; and c) pass and finally adopt Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 ; and d) forward Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 to the Inspector of Municipalities for Certificate of Approval. PURPOSE To consider the adoption of a Security Issuing Bylaw to authorize a borrowing request from the City of White Rock in the amount of $2,062,000 for the Fall 2017 MFA long term debt issue. BACKGROUND This report is being brought forward to introduce Metro Vancouver Security Issuing Bylaw No. 1247, 2017 and consider its adoption to authorize a borrowing request from the City of White Rock in the amount of $2,062,000 for water system infrastructure construction and improvement for inclusion in the Fall 2017 MFA long term debt issue. MUNICIPAL BORROWING REQUEST Request Details Under provincial legislation, municipal borrowing requests must be approved by the respective council by way of Loan Authorization Bylaw and Security Issuing Resolution. Such borrowings must then be approved by the MVRD Board and included in a MVRD Security Issuing Bylaw to move forward. Upon approval, the request is then considered by the MFA. All debt of the MVRD is a joint and several liability of the member municipalities. The City of White Rock Council adopted Loan Authorization Bylaw 2178 on February 20, 2017 in the amount of $2,062,000 for water system infrastructure and improvement. The City subsequently passed the required Security Issuing Resolution on May 29, 2017 to borrow the full amount authorized by the bylaw. PAU - 30

31 City of White Rock Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 Performance and Audit Committee Regular Meeting Date: July 7, 2017 Page 2 of 3 The City of White Rock has requested that a portion of this borrowing be amortized over a shorter (10 year) period. This has been reflected in the pertinent details of the bylaw are summarized as follows: MVRD Member Member Bylaw Bylaw Purpose 1247, 2017 City of White Rock 2178 Water System Infrastructure Construction and Improvement 1247, 2017 City of White Rock 2178 Water System Infrastructure Construction and Improvement Borrowing Request Term $1,662, years $400, years $2,062,000 The loan authorization bylaw outlined above, has been reviewed by the Inspector of Municipalities and has received the necessary Certificate of Approval. The certificate is included in this report. Financial Analysis Per the latest data provided by the Province, as at December 31, 2016 the City of White Rock had a liability servicing limit of $10,532,604. This limit represents the maximum amount, as prescribed by the Province, that the City can annually pay for servicing debt. The estimated annual debt servicing costs proposed in this bylaw will be approximately $208,100. When combined with the existing debt servicing costs and additional liability servicing the total will be approximately $1,222,200 which is roughly 11.6% of the liability servicing limit. Additional information provided by the City of White Rock to assist in considering this request includes: a copy of their security issuing resolution the adopted Loan Authorization Bylaw along with Certificate of Approval the Amended Financial Plan Bylaw which includes the appropriate proceeds of borrowing and anticipated debt servicing costs 2016 Consolidated Financial Statements which includes a note summarizing accumulated surplus (Note 11) and reserve balances (Note 13) All of which are attached to this report. ALTERNATIVES 1. That the MVRD Board: a) pursuant to Sections 182(1)(b) and 182(2)(a) of the Community Charter, give consent to the request for financing from the City of White Rock in the amount of $2,062,000; and b) give first, second and third reading to Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 being a bylaw to authorize the entering into an Agreement respecting financing between the Metro Vancouver Regional District and the Municipal Finance Authority of British Columbia; and PAU - 31

32 City of White Rock Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 Performance and Audit Committee Regular Meeting Date: July 7, 2017 Page 3 of 3 c) pass and finally adopt Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 ; and d) forward Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 to the Inspector of Municipalities for Certificate of Approval. 2. That the MVRD Board receive for information report titled City of White Rock Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017, dated June 23, FINANCIAL IMPLICATIONS The City of White Rock intends to borrow $2,062,000 to fund Water System Infrastructure Construction and Improvement from the Municipal Finance Authority of BC. Although all member debt is a joint and several liability of all member municipalities, there are no direct financial implications for Metro Vancouver with adoption of the bylaw. Should the bylaw not be adopted, the City of White Rock would be unable to borrow funds as required for the purpose intended and would need to look for other funding sources, potentially causing undue financial challenges for the City. SUMMARY / CONCLUSION As set out in the Community Charter, the MVRD must adopt a security issuing bylaw in order to enable the City of White Rock to proceed with their borrowing request. In light of the joint and several liability of all member municipality debt, the review of borrowing requests is prudent given the role of the Regional District. Staff recommends consenting to the City of White Rock s borrowing and adopting the Security Issuing Bylaw as outlined in Alternative 1. Attachments 1. Metro Vancouver Regional District Security Issuing Bylaw No. 1247, City of White Rock - Additional Information PAU - 32

33 ATTACHMENT 1 Regional District Security Issuing Bylaw METRO VANCOUVER REGIONAL DISTRICT BYLAW NO. 1247, 2017 A BYLAW TO AUTHORIZE THE ENTERING INTO OF AN AGREEMENT RESPECTING FINANCING BETWEEN THE METRO VANCOUVER REGIONAL DISTRICT AND THE MUNICIPAL FINANCE AUTHORITY OF BRITISH COLUMBIA WHEREAS the Municipal Finance Authority of British Columbia (the Authority ) may provide financing of capital requirements for Regional Districts or for their member municipalities by the issue of debentures or other evidence of indebtedness of the Authority and lending the proceeds therefrom to the Regional District on whose request the financing is undertaken; AND WHEREAS the City of White Rock is a member municipality of the Metro Vancouver Regional District (the Regional District ); AND WHEREAS the Regional District is to finance from time to time on behalf of and at the sole cost of the member municipalities, under the provisions of Section 410 (formerly section 824) of the Local Government Act, the works to be financed pursuant to the following loan authorization bylaw: Member Loan Authorization Bylaw Number Purpose 2178 Water System Infrastructure Construction and Improvement 2178 Water System Infrastructure Construction and Improvement Amount of Borrowing Authorized Amount Already Borrowed Borrowing Authority Remaining Term of Amount of Issue Issue $2,062,000 $0 $2,062, years $1,662,000 $2,062,000 $1,662,000 $400, years $400,000 AND WHEREAS the Regional Board, by this bylaw, hereby requests such financing shall be undertaken through the Authority: NOW THEREFORE the Regional Board of the Regional District of Metro Vancouver in open meeting assembled enacts as follows: Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 Page 1 of 5 PAU - 33

34 1. The Regional Board hereby consents to financing the debt of the City of White Rock in the amount of two million and sixty two thousand dollars ($2,062,000) in accordance with the following terms. 2. The Authority is hereby requested and authorized to finance from time to time the aforesaid undertakings at the sole cost and on behalf of the Regional District and its member municipalities up to, but not exceeding two million and sixty two thousand dollars ($2,062,000) in lawful money of Canada (provided that the Regional District may borrow all or part of such amount in such currency as the Trustees of the Authority shall determine but the aggregate amount in lawful money of Canada and in Canadian Dollar equivalents so borrowed shall not exceed $2,062,000 in Canadian Dollars) at such interest and with such discounts or premiums and expenses as the Authority may deem appropriate in consideration of the market and economic conditions pertaining. 3. Upon completion by the Authority of financing undertaken pursuant hereto, the Chair and officer assigned the responsibility of financial administration of the Regional District, on behalf of the Regional District and under its seal shall, at such time or times as the Trustees of the Authority may request, enter into and deliver to the Authority one or more agreements, which said agreement or agreements shall be substantially in the form annexed hereto as Schedule "A" and made part of this bylaw (such Agreement or Agreements as may be entered into, delivered or substituted hereinafter referred to as the "Agreement") providing for payment by the Regional District to the Authority of the amounts required to meet the obligations of the Authority with respect to its borrowings undertaken pursuant hereto, which Agreement shall rank as debenture debt of the Regional District. 4. The Agreement in the form of Schedule A shall be dated and payable in the principal amount or amounts of monies and in Canadian dollars or as the Authority shall determine and subject to the Local Government Act, in such currency or currencies as shall be borrowed by the Authority under Section 1 and shall set out the schedule of repayment of the principal amount together with interest on unpaid amounts as shall be determined by the Treasurer of the Authority. 5. The obligation incurred under the said Agreement shall bear interest from a date specified therein, which date shall be determined by the Treasurer of the Authority, and shall bear interest at a rate to be determined by the Treasurer of the Authority. 6. The Agreement shall be sealed with the seal of the Regional District and shall bear the signature of the Chair and the officer assigned the responsibility of financial administration of the Regional District. 7. The obligations incurred under the said Agreement as to both principal and interest shall be payable at the Head Office of the Authority in Victoria and at such time or times as shall be determined by the Treasurer of the Authority. 8. During the currency of the obligation incurred under the said Agreement to secure borrowings in respect of Water System Infrastructure Construction and Improvement Loan Authorization Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 Page 2 of 5 PAU - 34

35 Bylaw, 2016, No. 2178, there shall be requisitioned annually an amount sufficient to meet the annual payment of interest and the repayment of principal. 9. The Regional District shall provide and pay over to the Authority such sums as are required to discharge its obligations in accordance with the terms of the Agreement, provided, however, that if the sums provided for in the Agreement are not sufficient to meet the obligations of the Authority, any deficiency in meeting such obligations shall be a liability of the Regional District to the Authority and the Regional Board of the Regional District shall make due provision to discharge such liability. 10. The Regional District shall pay over to the Authority at such time or times as the Treasurer of the Authority so directs such sums as are required pursuant to section 15 of the Municipal Finance Authority Act to be paid into the Debt Reserve Fund established by the Authority in connection with the financing undertaken by the Authority on behalf of the Regional District pursuant to the Agreement. This bylaw may be cited as Metro Vancouver Regional District Security Issuing Bylaw No. 1247, READ A FIRST TIME this day of, READ A SECOND TIME this day of, READ A THIRD TIME this day of, PASSED AND FINALLY ADOPTED this day of, Greg Moore, Chair Chris Plagnol, Corporate Officer Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 Page 3 of 5 PAU - 35

36 SCHEDULE "A" to Bylaw No. 1247, 2017 C A N A D A PROVINCE OF BRITISH COLUMBIA A G R E E M E N T Metro Vancouver Regional District The Metro Vancouver Regional District (the Regional District ) hereby promises to pay to the Municipal Finance Authority of British Columbia at its Head Office in Victoria, British Columbia, (the Authority ) the sum of two million and sixty two thousand dollars ($2,062,000) in lawful money of Canada, together with interest calculated semi-annually in each and every year during the currency of this Agreement; and payments shall be as specified in the table appearing below hereof commencing on the day of, 2017 provided that in the event the payments of principal and interest hereunder are insufficient to satisfy the obligations of the Authority undertaken on behalf of the Regional District, the Regional District shall pay over to the Authority further sums as are sufficient to discharge the obligations of the Regional District to the Authority. DATED at, British Columbia, this day of, 20. IN TESTIMONY WHEREOF and under the authority of Bylaw No. 1247, 2017 cited as Metro Vancouver Regional District Security Issuing Bylaw No. 1247, This Agreement is sealed with the Corporate Seal of the Metro Vancouver Regional District and signed by the Chair and the officer assigned the responsibility of financial administration thereof. Chair Treasurer Pursuant to the Local Government Act, I certify that this Agreement has been lawfully and validly made and issued and that its validity is not open to question on any ground whatever in any Court of the Province of British Columbia. Dated, 20 (month, day) Inspector of Municipalities Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 Page 4 of 5 PAU - 36

37 PRINCIPAL AND/ OR SINKING FUND DEPOSIT AND INTEREST PAYMENTS Principal and/or Sinking Fund Date of Payment Deposit Interest Total $ $ $ $ $ $ Metro Vancouver Regional District Security Issuing Bylaw No. 1247, 2017 Page 5 of 5 PAU - 37

38 Attachment CERTIFIED RESOLUTION The City of White Rock Council at their May 29, 2017 Regular Council meeting adopted the following resolution: WATER SYSTEM INFRASTRUCTURE CONSTRUCTION AND IMPROVEMENT LOAN AUTHORIZATION BYLAW NO SECURITY ISSUING RESOLUTIONS THAT Council: 1. Receives for information the May 29, 2017 corporate report from the Director of Financial Services, titled "Water System Infrastructure Construction and Improvement Loan Authorization Bylaw, 2016, No Security Issuing Resolutions;" 2o Approves borrowing from the Municipal Finance Authority of British Columbia, as part of the 2017 Fall Borrowing Session, one million six hundred sixty-two thousand dollars ($1,662,000) as authorized through Water System Infrastructure Construction and Improvement Loan Authorization Bylaw, 2016, No and that the Metro Vancouver Regional District be requested to consent to our borrowing over a ten (10) year term and include the borrowing in their Security Issuing Bylaw; and 3. Approves borrowing from the Municipal Finance Authority of British Columbia, as part of the 2017 Fall Borrowing Session, four hundred thousand dollars ($400,000) as authorized through Water System Infrastructure Construction and Improvement Loan Authorization Bylaw, 2016, No and that the Metro Vancouver Regional District be requested to consent to our borrowing over a thirty (30) year term and include the borrowing in their Security Issuing Bylaw. S~y City Clerk Dated: May 30, 2017 City Clerk's Office P: j F: City of White Rock Buena Vista Avenue, White Rock BC, Canada V4B 1Y6 \\4-llTEJ-:~O_LoCK \ ~C1-o~~~~. PAU - 38

39 THE CORPORATION OF THE CITY OF WHITE ROCK BYLAW2178 A Bylaw to authorize borrowing for constructing and improving water system infrastructure The CITY COUNCIL of the Coworation of the City of White Rock, in an open meeting assembled, ENACTS as follows: 1. The Council is hereby empowered and authorized to: a. undertake and carry out or cause to be carried out the construction and improvement of water system infrastructure including the following projects: i. Total Water Quality Management Project - Phase 2 Merklin ii. New Well - Oxford iii. Water Main Upgrade - Marine Drive, Vidal Street to Martin Street iv. Water Main Upgrade to Marine Drive v. Water Main Upgrade- Satuma Drive and Archibald Road b. borrow upon the credit of the Municipality a sum not exceeding $2,062, The maximum tenn for which debentures may be issued to secure the debt created by this bylaw is 30 years. 3. This Bylaw may be cited for all purposes as the "Water System Infrastructure Construction and hnprovement Loan Authorization Bylaw, 2016, No. 2178". RECENED FIRST READING on the RECEIVED SECOND READING on the RECEIVED THIRD READING on the RECEIVED the approval of the Inspector of Municipalities ADOPTED on the lz'h day of December, th day of December, th day of December, day of January, 2017 February, 2017 I herby certify that this lji ~ and correct copy of Bylaw No..,,.Of.."'i~{...,...::t:b..._. which has not been altered in any way. MAYOR Certified this..3c2._day of~ 2...Q.G- ~. CITY CLERK PAU - 39

40 BRmSH COLUMBIA Certificate of Approval Under the authority of the Local Government Act, I certify that Bylaw No. 2178, cited as the "Water System Infrastructure Construction and Improvement Loan Authorization Bylaw, 2016, No. 2178" of the City of White Rock has been lawfully and validly made and enacted, and that its validity is not open to question on any ground in any court of British Columbia. Dated this of day, 2017 PAU - 40

41 1.. THE CORPORATION OF THE CITY OF WHITE ROCK BYLAW2204 A Bylaw to amend the Financial Plan for 20 I 7 to 2021 WHEREAS the City Council of the Corporation of the City of White Rock is empowered by the provisions of Section 165 of the "Community Charter" to amend the Financial Plan for the fiveyear period ending the thirty-first day of December AND WHEREAS it is necessary for such Financial Plan to be amended The CITY COUNCIL of The Corporation of the City of White Rock in open meeting assembled, ENACTS as follows:- I. Schedule "A" and Schedule "B" attached to and forming part of the.. White Rock Financial Plan ( ) Bylaw, 2016, No. 2175", are hereby repealed and replaced by the Schedules.. A" and ' B" attached hereto and forming part of this bylaw. 2. This Bylaw may be cited for all purposes as the '"Financial Plan ( ) Bylaw. 2016, No. 2175, Amendment No. l, Bylaw No. 2204". RECEIVED FIRST READING on the RECEIVED SECOND READING on the RECEIVED THIRD READING on the ADOPTED on the 24th day of April, day of April, th day of April, 2017 gth day of May, 2017 I nerby certify that this l~~d w-ay-. - which has no Certlfted \his _li_day of~ ~ correct copy of Bytl~:e~~itered in an_y... Mayor City Clerk PAU - 41