GREATER VANCOUVER REGIONAL DISTRICT PERFORMANCE AND PROCUREMENT COMMITTEE

|

|

|

- Dortha Kennedy

- 5 years ago

- Views:

Transcription

1 GREATER VANCOUVER REGIONAL DISTRICT PERFORMANCE AND PROCUREMENT COMMITTEE REGULAR MEETING Friday, July 17, :00 a.m. 2 nd Floor Boardroom, 4330 Kingsway, Burnaby, British Columbia. 1. ADOPTION OF THE AGENDA A G E N D A July 17, 2015 Regular Meeting Agenda That the Performance and Procurement Committee adopt the agenda for its regular meeting scheduled for July 17, 2015 as circulated. 2. ADOPTION OF THE MINUTES 2.1 April 15, 2015 Regular Meeting Minutes That the Performance and Procurement Committee adopt the minutes of its regular meeting held April 15, 2015 as circulated. 3. DELEGATIONS No items presented. 4. INVITED PRESENTATIONS No items presented. 5. REPORTS FROM COMMITTEE OR STAFF 5.1 Financial Performance Report as of May 2015 Designated Speaker: Phil Trotzuk That the Performance and Procurement Committee receive the report titled Financial Performance Report as of May 2015, dated June 26, 2015 for information. 1 Note: Recommendation is shown under each item, where applicable. P&P - 1

2 5.2 GVWD Borrowing Bylaw No. 248, 2015 Designated Speaker: Phil Trotzuk That the GVWD Board: a) approve a borrowing limit of $700,000. b) give first, second and third readings to Greater Vancouver Water District Borrowing Bylaw Number 248, 2015 and forward to the Inspector of Municipalities for approval. 5.3 GVRD Security Issuing Bylaw No. 1224, 2015 Regarding GVWD Borrowing Bylaw No. 248, 2015 Designated Speaker: Phil Trotzuk That GVRD Board: a) give first, second and third reading to "Greater Vancouver Regional District Security Issuing Bylaw No. 1224, 2015". b) forward "Greater Vancouver Regional District Security Issuing Bylaw No. 1224, 2015" to the Inspector of Municipalities for approval. 5.4 Amendment to Corporate Investment Policy Designated Speaker: Dean Rear That the GVRD Board approve the Corporate Investment Policy as presented in the report titled Investment Policy Update, dated June 16, Continuous Improvement Actions at Metro Vancouver Designated Speaker: Dean Rear That the Performance and Procurement Committee receive the report titled Continuous Improvement Actions at Metro Vancouver, dated June 25, 2015 for information. 5.6 AGLG Audit Topic 3: Capital Procurement Projects and Asset Management Programs Designated Speaker: Dean Rear That the Performance and Procurement Committee receive the report titled AGLG Audit Topic 3 Capital Procurement Projects and Asset Management Programs, dated July 3, 2015 for information. 5.7 Investment Position and Returns January 1 to April 30, 2015 Designated Speaker: Dean Rear That the Performance and Procurement Committee receive the report titled Investment Position and Returns January 1 to April 30, 2015, dated June 22, 2015 for information. P&P - 2

3 5.8 Status of Water, Liquid Waste and Solid Waste Capital Expenditures to April 30, 2015 Designated Speaker: Dean Rear That the Performance and Procurement Committee receive the report titled Status of Water, Liquid Waste and Solid Waste Capital Expenditures to April 30, 2015, dated June 26, 2015 for information Legal Expenditures Designated Speaker: Phil Trotzuk That the Performance and Procurement Committee receive the report titled 2014 Legal Expenditures, dated June 5, 2015 for information Tender/Contract Award Information April to June 2015 Designated Speaker: Tracey Husoy That the Performance & Procurement Committee receive the report titled Tender/Contract Award Information April to June 2015, dated June 26, 2015 for information Manager s Report Designated Speaker: Phil Trotzuk That the Performance and Procurement Committee receive the report titled Manager s Report, dated July 6, 2015 for information. 6. INFORMATION ITEMS No items presented. 7. OTHER BUSINESS No items presented. 8. BUSINESS ARISING FROM DELEGATIONS No items presented. 9. RESOLUTION TO CLOSE MEETING That the Performance and Procurement close its regular meeting schedule for July 17, 2015 pursuant to the Community Charter provisions, Section 90 (1) (i) as follows: 90 (1) A part of a meeting may be closed to the public if the subject matter being considered relates to or is one of more of the following: (i) the receipt of advice that is subject to solicitor-client privilege, including communications necessary for that purpose; P&P - 3

4 10. ADJOURNMENT/CONCLUSION That the Performance and Procurement Committee adjourn/conclude its regular meeting of July 17, Membership: Clay, Mike (C) Port Moody Jordan, Colleen (VC) Burnaby Baldwin, Wayne White Rock Brodie, Malcolm Richmond Coté, Jonathan New Westminster Fox, Charlie Langley Township Gill, Tom Surrey McEwen, John Anmore Meggs, Geoff - Vancouver Mussatto, Darrell North Vancouver City Reid, Mae Coquitlam Bell, Corisa Maple Ridge Smith, Michael West Vancouver P&P - 4

5 2.1 GREATER VANCOUVER REGIONAL DISTRICT PERFORMANCE AND PROCUREMENT COMMITTEE Minutes of the Regular Meeting of the Greater Vancouver Regional District (GVRD) Performance and Procurement Committee held at 9:00 a.m. on Wednesday, April 15, 2015 in the 2nd Floor Boardroom, 4330 Kingsway, Burnaby, British Columbia. MEMBERS PRESENT: Chair, Mayor Mike Clay, Port Moody Vice Chair, Councillor Colleen Jordan, Burnaby Councillor Corisa Bell, Maple Ridge Mayor Malcolm Brodie, Richmond Mayor Jonathan Coté, New Westminster (arrived at 9:02 a.m.) Councillor Charlie Fox, Langley Township Councillor Tom Gill, Surrey Mayor John McEwen, Anmore (arrived at 9:01 a.m.) Councillor Geoff Meggs, Vancouver (arrived at 9:01 a.m.) Mayor Darrell Mussatto, North Vancouver City Councillor Mae Reid, Coquitlam Mayor Michael Smith, West Vancouver MEMBERS ABSENT: Mayor Wayne Baldwin, White Rock STAFF PRESENT: Phil Trotzuk, Chief Financial Officer Carol Mason, Commissioner/Chief Administrative Officer Janis Knaupp, Assistant to Regional Committees, Board and Information Services, Legal and Legislative Services 1. ADOPTION OF THE AGENDA 1.1 April 15, 2015 Regular Meeting Agenda It was MOVED and SECONDED That the Performance and Procurement Committee: a) amend the agenda for its regular meeting scheduled for April 15, 2015 by adding on-table replacement Item 5.6, page Appendix D Page No. 1 Amendment to a Previously Reported Contract Sole Source Purchase Order No A; and b) adopt the agenda as amended. CARRIED P&P - 5

6 2. ADOPTION OF THE MINUTES 1.1 February 6, 2015 Regular Meeting Minutes It was MOVED and SECONDED That the Performance and Procurement Committee: a) correct the minutes of its regular meeting held February 6, 2015, on page 1 in Attendance, by replacing the name Corsica with the name Corisa ; and b) adopt the minutes as corrected. CARRIED 3. DELEGATIONS No items presented. 4. INVITED PRESENTATIONS No items presented. 9:01 a.m. Mayor McEwen and Councillor Meggs arrived at the meeting. 5. REPORTS FROM COMMITTEE OR STAFF 5.1 Draft Audited 2014 Financial Statements Report dated March 25, 2015 from Phil Trotzuk, Chief Financial Officer, presenting for approval the 2014 Audited Financial Statements for the Greater Vancouver Districts and the Metro Vancouver Housing Corporation. Members were provided a presentation on 2014 Metro Vancouver finances and the 2014 year-end financial results highlighting: the operations surplus; surplus results; and financial position, equity in capital assets, and liquidity as of December 31, Presentation material titled 2014 Metro Vancouver Finances is retained with the April 15, 2015 Performance and Procurement Committee agenda. 9:02 a.m. Mayor Coté arrived at the meeting. It was MOVED and SECONDED a) That the GVRD Board approve the Audited 2014 Consolidated Financial Statements for the Greater Vancouver Regional District, and receive for information the Metro Vancouver Housing Corporation Audited 2014 Financial Statements; b) That the GVS&DD Board approve the Audited 2014 Financial Statements for the Greater Vancouver Sewerage and Drainage District; c) That the GVWD Board approve the Audited 2014 Financial Statements for the Greater Vancouver Water District. CARRIED P&P - 6

7 Financial Results Year-End Report dated March 27, 2015 from Phil Trotzuk, Chief Financial Officer, updating the GVRD Board on financial performance for the year ending December 31, 2014 as compared to the 2014 annual budget. It was MOVED and SECONDED That the GVRD Board receive the report dated March 27, 2015 titled 2014 Financial Results Year-End for information. CARRIED 5.3 Greater Vancouver Sewerage and Drainage District Development Cost Charge Reserve Fund Expenditure Bylaw No. 290, 2015 Report dated March 6, 2015 from Dean Rear, Director, Financial Planning and Operations, bringing forward to the GVS&DD Board for consideration, a bylaw to meet the statutory requirements to use Development Cost Charges for funding of the growth capital program. It was MOVED and SECONDED That the GVS&DD Board: a) give first, second and third reading to Greater Vancouver Sewerage and Drainage District Development Cost Charge Reserve Fund Expenditure Bylaw No. 290, 2015 ; and b) pass and finally adopt Greater Vancouver Sewerage and Drainage District Development Cost Charge Reserve Fund Expenditure Bylaw No. 290, CARRIED 5.4 Semi-Annual Report on GVS&DD Development Cost Charges Report dated March 6, 2015 from Dean Rear, Director, Financial Planning and Operations, Financial Services, providing a report to the Committee on the 2014 GVS&DD Development Cost Charge revenues as required in the Board s policy. It was MOVED and SECONDED That the Performance and Procurement Committee receive the report dated March 6, 2015 titled Semi-Annual Report on GVS&DD Development Cost Charges for information. CARRIED 5.5 Status of Water, Liquid Waste and Solid Waste Capital Expenditures to December 31, 2014 Report dated March 6, 2015 from Dean Rear, Director, Financial Planning and Operations, providing a report on the status of the capital projects for Water, Liquid Waste and Solid Waste. Members were provided a presentation highlighting water utility capital projects including: the Seymour-Capilano Twin Tunnels Capilano shaft enclosures; Seymour-Capilano Twin Tunnels commissioning; Port Mann Water Supply Tunnel P&P - 7

8 (PMWST); PMWST north shaft valve chamber; Barnston/Maple Ridge Pump Station; Angus Drive Main; and Phase I of the Capilano Main No. 9; and liquid waste utility capital projects including: the Northwest Langley Wastewater Treatment Plant Phase IV upgrade; Gilbert Trunk Sewer No. 2; Burnaby Lake North Interceptor No. 2; and Annacis Island Wastewater Treatment Plant Stage 5 expansion ground improvement works. Presentation material titled Status of Utilities Capital Expenditures to December 31, 2014 Project Photos is retained with the April 15, 2015 Performance and Procurement Committee agenda. It was MOVED and SECONDED That the Performance and Procurement Committee receive the report titled Status of Water, Liquid Waste and Solid Waste Capital Expenditures to December 31, 2014, dated March 6, 2015 for information. CARRIED 5.6 Tender/Contract Award Information January to March 2015 Report dated April 7, 2015 from Tracey Husoy, Division Manager, Purchasing and Risk Management, Financial Services, informing the Committee about contracts, handled through the Purchasing Division, with a total anticipated value at or in excess of $500,000 (exclusive of tax). Members were informed that on page 3 of the report the reference to removal of asbestos by Hatch MacDonald Ltd. was an error. In response to questions, members were informed about the competitive procurement process for employee benefits, how contingency funds and legal costs are reflected in the budget, and general government costs. Comments were offered about exploring how legal costs are allocated and procured and what is included in general government as part of the budget. Request of Staff Staff was requested to report back to the Performance and Procurement Committee at its July 17, 2015 meeting with a breakdown of legal fees incurred by Metro Vancouver. It was MOVED and SECONDED That the Performance and Procurement Committee receive the report titled Tender/Contract Award Information January to March 2015, dated April 7, 2015 for information. CARRIED P&P - 8

9 5.7 Manager s Report Report dated March 24, 2015 from Phil Trotzuk, Chief Financial Officer, informing the Performance and Procurement Committee of the Committee s 2015 Work Plan, the George Ross Bequest Announcement and Recognition, the new budget and financial systems, and the Municipal Finance Authority. 6. INFORMATION ITEMS No items presented. 7. OTHER BUSINESS No items presented. Members were provided a presentation on Metro Vancouver s new financial system upgrades highlighting purpose, timing, key improvements, reporting structure, an example of budget entry and dashboard reporting features, and next steps. Presentation material titled Finance Systems Update is retained with the April 15, 2015 Performance and Procurement Committee agenda. It was MOVED and SECONDED That the Performance and Procurement Committee receive the report titled Manager s Report dated March 24, 2015 for information. CARRIED 8. BUSINESS ARISING FROM DELEGATIONS No items presented. 9. RESOLUTION TO CLOSE MEETING Members considered adding a resolution to close the meeting related to intergovernmental relations. It was MOVED and SECONDED That the Performance and Procurement close its regular meeting schedule for April 15, 2015 pursuant to the Community Charter provisions, Section 90 (1) (l) and 90 (2) (b) as follows: 90 (1) A part of a meeting may be closed to the public if the subject matter being considered relates to or is one or more of the following: (l) discussions with regional district officers and employees respecting regional district objectives, measures and progress reports for the purposes of preparing an annual report under section 98 [annual municipal report] of the Charter; and 90 (2) A part of a meeting must be closed to the public if the subject matter being considered relates to one or more of the following: (b) the consideration of information received and held in confidence relating to negotiations between the regional district and a provincial P&P - 9

10 10. ADJOURNMENT/CONCLUSION government or the federal government or both, or between a provincial government or the federal government or both and a third party. CARRIED It was MOVED and SECONDED That the Performance and Procurement Committee adjourn its regular meeting of April 15, CARRIED (Time: 10:13 a.m.) Janis Knaupp, Assistant to Regional Committees Mike Clay, Chair FINAL P&P - 10

11 5.1 To: From: Performance and Procurement Committee Phil Trotzuk, Chief Financial Officer Date: June 26, 2015 Meeting Date: July 17, 2015 Subject: Financial Performance Report as of May 2015 RECOMMENDATION That the Performance and Procurement Committee receive the report titled Financial Performance Report as of May 2015, dated June 26, 2015 for information. PURPOSE To present the Committee with an update on financial performance to the end of May 2015 including a projection to the end of the fiscal year. BACKGROUND Board policy requires that the Performance and Procurement Committee be provided, three times per year, an update on the actual financial performance of the Metro Vancouver Districts and Metro Vancouver Housing Corporation with the report on the year-end results also sent to the Board. This is the first of such reports for Year-to-date results as presented are based on the actual results for the first five months of the year with the main focus on the projections to year-end operations of the Metro Vancouver Districts and Metro Vancouver Housing Corporation are projected to be in an overall surplus position of $17.1 million as compared to budget. Throughout the course of a year, staff vacancies exist as a result of staff turnover, staff leaves, staff moving positions as coverage, promotion and so on. This leads to labour savings from vacancies until the positions are filled which results in surpluses to budget. HIGHLIGHTS Overall, the Districts and Housing Corporation are projecting a surplus position of approximately $17.1 million for the 2015 fiscal year. The overall projected surplus is mainly due to increased revenues in water, the deferral of some operating and capital projects, some staff vacancies, savings in miscellaneous operating costs and slightly lower debt service costs in the utilities. More detailed information by district and / or function is included in Attachment 1. P&P - 11

12 The breakdown of the overall $17.1 million projected 2015 surplus, by district/function is as follows: Regional District - $1.3 million Water District - $11.3 million Liquid Waste - $3.7 million Solid Waste - $0.2 million Housing - $0.6 million The projected operating surplus in the Regional District can be mainly attributed to the delay in some Regional Parks project initiatives, fewer Board and Committee meetings than planned, savings from staff vacancies as recruitment continues and some savings in miscellaneous operating costs. The Water District s projected surplus is largely the result of projected revenue from water sales in excess of budget estimates along with expenditure savings in system operating contingency, labour savings from staff vacancies and the delay and/or deferral of some projects. The Liquid Waste projected surplus in 2015 is primarily due to deferral of some minor capital and maintenance projects funded through operations. In addition, some projected savings in miscellaneous operating costs along with labour savings due to several staff vacancies are expected. Solid Waste is expected to be close to break even in Higher than expected waste flows, due to less than anticipated waste migration, combined with management of expenditures has the function projected at slightly better than budget. The Housing Corporation has a surplus net income position primarily due to higher than projected rental revenue. In addition to the above surpluses, corporate programs are also projecting a surplus position for 2015 of approximately $133,000 primarily due to staff vacancies savings as recruitment continues. ALTERNATIVES This is an information report. No alternatives are presented. FINANCIAL IMPLICATIONS This report provides information on projected results for 2015 operations which, at this time, shows an overall year-end surplus of $17.1 million. This surplus would be available in future years to either avoid debt or pay for regional projects thereby reducing the funding requirements. Should circumstances change and this projected surplus increase or decrease, then more or less would be available to reduce future funding requirements. P&P - 12

13 SUMMARY / CONCLUSION The 2015 projected financial results for the Metro Vancouver entities and functions are favourable to budget. Attachments and References: Attachment Financial Performance as of May P&P - 13

14 ATTACHMENT 1 Greater Vancouver Districts 2015 Financial Performance As of May 2015 P&P - 14

15 Table of Contents Statement of Surplus/(Deficit) District Summaries Regional District Summary Water District Summary... 7 Sewerage & Drainage District Summaries Liquid Waste... 8 Solid Waste... 8 Housing Corporation Summary... 9 Corporate Programs Financial Indicators P&P - 15

16 P&P - 16

17 P&P - 17

18 P&P - 18

19 P&P - 19

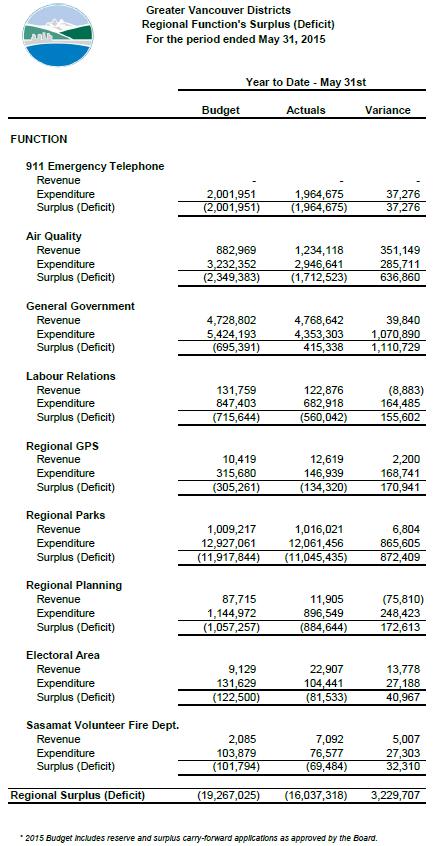

20 Greater Vancouver Districts 2015 Financial Performance District Summaries Greater Vancouver Regional District The Regional District at the end of May 2015 is in a surplus position of approximately $3.2 million. This surplus is due to the timing of actual expenditures being slower than that anticipated in the budget primarily in General Government, Regional Parks, and Air Quality. At this time, it is expected that the majority of the delayed expenditures will be incurred by year-end and the surplus will be reduced to close to $1.4 million due to savings from staff vacancies, savings in Board and Committee meeting costs and delay in some of Regional Park function s planned projects. 911 Emergency Telephone E911 is in a surplus position of $37,000 due to savings in E-Comm contract fees and timing of some expenditures. E911 is projecting a surplus of $18,000 by the end of the year as a result of contract fee savings. Air Quality At the end of May, Air Quality is in a surplus position of $637,000 primarily due to staff vacancies, a late start in some consulting studies, receiving permit fees earlier than expected and increased revenue from higher than expected registration of Non Road Diesel Engines. With the staff vacancies expected to be filled by September, the function is expected to be in a surplus position of $172,000 by year end due to position vacancies, to date, and Non Road Diesel Engine revenues. General Government General Government is in a surplus position of approximately $1.1 million at the end of May, due to the timing of expenditures. The Homelessness Partnering Strategy (HPS) program is currently in a surplus position of $448,000 due to the timing of projects and related funding. The HPS program is fully funded by the federal government and is expected on be on budget at year end. While the majority of the initiatives are expected to be completed by year end, General Government is projecting a surplus to $245,000 for 2015 due primarily to savings in Board and Committee meeting costs and unbudgeted interest income. Labour Relations Labour Relations is in a surplus position of close to $156,000 at the end of May due primarily to staff vacancies from staff on leave. At year end, Labour Relations is projecting a surplus of $220,000 due to continued staff vacancies. Regional Global Positioning System (GPS) At the end of May, the GPS function is under spent by approximately $170,000 due to the timing of expenditures. By year end, the function is forecasting revenues and expenditures to be near budget. P&P - 20

21 Regional Parks Regional Parks is in a surplus position at the end of May of approximately $872,000 due primarily to delays in hiring some seasonal staff, other staff vacancies, currently being recruited for, the deferral of some project related expenditures until later in the year and the deferral of some asset purchases and materials and supply expenditures to the summer and fall months. At this time, while it is expected that most delayed expenditures will be incurred by year end, Regional Parks is expected to be in a surplus position of $405,000 for the year. This is mostly due to some staff vacancies, in the early part of the year and the delay of Central Area s contaminated site study to Regional Planning As of the end of May, Regional Planning is in a surplus position of $173,000 primarily due to staff vacancies resulting from a redefining of focus and environmental planning. As these positions are expected to be filled in the latter part of 2015, Regional Planning is expected to be in a surplus position of $230,000 at year end. Electoral Areas Electoral Areas is currently in a surplus position of $41,000 due to a staff vacancy early in the year and timing of building permit fees received. Electoral Areas is expected to be in a surplus position of $30,000 by year end. Sasamat Volunteer Fire Department Sasamat Volunteer Fire Department is currently in a surplus position of $32,000 as a result of timing of actual expenditures being slower than budget. As most of these expenditures are expected to be incurred by year end, the function is expected to be close to budget. P&P - 21

22 Greater Vancouver Water District The Water District is in a surplus position of approximately $8.2 million as at the end of May. The District, however, is projecting this surplus to increase to $11.3 million by year end. Water District revenues to the end of May are $1.2 million greater than budget. Water consumption proved to be approximately 1% greater than budget to the end of May. Revised estimates indicate a projected revenue surplus of $8.2 million overall for The revenues are based on high water demands due to the unseasonably warm start to the summer as well as long term weather forecasts for the remainder of the summer and fall. Any increased demand will result in revenue increases. Water District expenditures are currently $7 million below budget due primarily to the planned implementation of several engineering and maintenance projects later in the year, operating staff vacancies, lower than anticipated leak repair costs and delays in commissioning of new capital facilities. It is expected that by year end that the final expenditure surplus will reduce to $3.1 million. This surplus is largely the result of savings in engineering and maintenance project costs, savings from staff vacancies and savings of the operating contingency. P&P - 22

23 Greater Vancouver Sewerage and Drainage District Liquid Waste Liquid Waste is anticipating a surplus of approximately $3.7 million primarily due to operational costs that are projected less than budget. The projected surplus can be split as follows: FSA $1.7 million, LIWSA $0.2 million, VSA $1.3 million, NSSA $0.3 million and Drainage $0.2 million. Operations costs year-to-date to the end of May 2015 are approximately $8.9 million under spent compared to budget due primarily to delays of some general operational expenditures for minor capital, maintenance, wastewater treatment, residuals along with several staff vacancies currently being recruited. Operations costs are projected to be $4.3 million under budget due primarily to some minor capital, maintenance and residuals program costs less than budget along with some labour savings from several staff vacancies. The minor capital projects for 2015 are expected to fall behind due to some unforeseen complexities in the project work. The movement of Biosolids from the Iona wastewater treatment plant is expected to be delayed and will be less than budget in the amount of approximately $650,000. The under expenditure will be offset by a lower than expected application of reserve funding due to some of the above noted delayed expenditures. Solid Waste The approved 2015 budget included a $4.5 million contribution from reserves to balance the budget based on expected continued migration of waste out of the Metro Vancouver solid waste system. The Solid Waste function is now expected to break even as a result of a combination of managing expenditures along with higher than anticipated waste flows realized primarily because of changes to the tipping fee structure implemented in April. A number of remaining uncertainties such as landfill closure liability, Vancouver Landfill operating costs, Wastech operating costs, along with any additional changes in waste flow will likely impact the final 2015 position compared to budget. P&P - 23

24 Metro Vancouver Housing Corporation (MVHC) As at May 31, 2015, the MVHC is in a surplus position of approximately $1.2 million. This is typical at this point in the year, as the timing of many operating expenses is more heavily weighted in the latter part of the year. As the delayed expenditures are incurred, the surplus is expected to decline to approximately $629,000 by year-end. Any surplus from operations is allocated to reserves each year, providing an important and essential source of funding for the long-term capital plan. Revenues for the first five months are $254,000 ahead of budget. This is mainly due to higher than budgeted rent increases with some tenant rent subsidies received in advance. The impact of the rent increases will result in a year-end revenue surplus of $427,000. Expenditures through May are approximately $1 million less than budget largely due to maintenance expenditures that are weighted more heavily in the latter part of the year as well as some labour surplus due to vacancies that have since been filled. As the delayed expenditures are incurred, the overall actual expenditures are expected to be $202,000 under budget by year-end. The 2015 capital program included an annual budget of $9.5 million for capital replacement expenditures and development. As at May 31, 2015, approximately $1.0 million was spent for capital replacement. With the preparation of project specifications now completed, the capital replacement program is expected to be on budget. For the development program, $409,000 was spent for the first five months. As MVHC expects to push the construction and related consulting costs to 2016, it is anticipated that $1.6 million of the $2.8 million budgeted will be spent in The 2015 MVHC capital and development programs are funded from reserves so they have no impact on operations. P&P - 24

25 P&P - 25

26 Corporate Programs Overall, Corporate Programs are in a surplus position of approximately $2.3 million for the first five months of This surplus is largely due to the timing of actual expenditures being slower than that anticipated and staff vacancies from turnover an delays in recruiting. As these delayed expenditures are expected to be incurred during the year, the overall projected surplus for Corporate Programs will be approximately $133,000 due primarily to staff vacancies to date in Corporate Strategies and Financial Services. Chief Administrative Office The CAO s Office is currently close to $36,000 under budget and is forecast to under budget by approximately $31,000 at year-end as a result of labour savings. External Relations External Relations is currently in a surplus position of approximately $765,000 due mainly to work on the advertising campaigns and some outreach initiatives to occur later in the year, and several temporarily vacant positions. The majority of this work is expected to be complete by year-end, leaving External Relations with a $175,000 surplus. Human Resources The Human Resources department is currently under budget by close to $290,000 due to several senior staff vacancies and delays in some recruitment initiatives. By year-end, Human Resources is projected to be on budget. Financial Services The Financial Services department is in a surplus position of approximately $360,000 to date due primarily to savings from labour savings from staff vacancies currently being recruited for and timing of expenditures being different from budget. The surplus for Financial Services is projected to be approximately $370,000 for 2015 due primarily to some staff vacancies. Legal and Legislative Services Legal and Legislative Services is currently in a surplus position of approximately $175,000 to date due to the timing of external legal services being different than anticipated in the budget and delayed expenditures in Information Management. As these services are expected to be incurred, Legal and Legislative Services is projected to be primarily on budget at year-end. P&P - 26

27 Corporate Services Corporate Services is currently in a surplus position of approximately $700,000 through May Building Operations and Corporate Safety, Security and Emergency Management services are currently in a surplus position of approximately $1.0 million primarily due to some head office maintenance and renovation projects to be incurred in the latter part of the year, lower contract price for contracted security services, and timing of safety training initiatives. Information Technology (IT) services are currently in a deficit position of $300,000. This is due to the purchase of new software occurring sooner than expected in the budget. IT is projected to be on budget for By end of year, Corporate Services is expecting a deficit of $443,000. Major projects including west wall remediation, elevator replacement and office renovation are expected to exceed budget by $479,000. Reduction in tenant rent is forecasted at $34,000 for the year. This is mitigated by some forecast savings $70,000 related to building debt, staff vacancies and contract security services in Corporate Safety, Security and Emergency Management services. The deficit in corporate services will be offset by savings in other corporate areas. P&P - 27

28 Greater Vancouver Districts Financial Indicators These ratios are intended to help indicate the Greater Vancouver District s financial ability to continue to provide services to the region on a sustainable basis. This involves evaluating a number of factors, including the ongoing ability to ensure revenues meet expenditures, ability to meet debt obligations, and the flexibility to address unexpected contingencies. Forecast ratios can help to identify potential financial problems in advance. 1) Municipal Property Tax and Levies / Total Revenue This ratio is a measure of the diversification of revenues. A high ratio indicates a reliance on property tax related levies / fees. A low ratio illustrates a greater range of revenues which is seen as beneficial. However, other revenue streams may not be sustainable or fluctuate more than tax requisitions Actual 2013 Actual 2014 Actual 2015 Budget 2015 Actual Total Property tax/levies $218,931, % $226,403, % $232,429, % $239,867, % $239,867, % Total Revenue** $631,850,995 $644,494,910 $653,970,533 $660,635,674 $668,471,750 The GVRD has a reasonably well diversified revenue base. Some revenue streams such as Water Sales and Solid Waste User Fees are subject to fluctuations during the year. 2) i) Debt Service Costs/ Total Revenue This is the percentage of revenue committed to payment of interest and principal on temporary and long-term debt for the regional, sewer, solid waste and water operations. A high percentage indicates greater use of revenues for the repayment of debt, and less ability to adjust to unplanned events and changing circumstances Actual 2013 Actual 2014 Actual 2015 Budget 2015 Actual Debt Service Costs $134,582, % $131,044, % $122,877, % $127,669, % $127,165, % Total Revenue** $631,850,995 $644,494,910 $653,970,533 $660,635,674 $668,471,750 ** 2015 Budget includes reserve and surplus carry-forward applications as approved by the Board. P&P - 28

29 2) ii) Interest Costs/ Total Revenue This is the percentage of revenue committed to payment of interest on temporary and long-term debt for the regional, sewer, solid waste and water operations. A high percentage indicates greater use of revenues for servicing interest on outstanding debt, and less ability to adjust to unplanned events and changing circumstances Actual 2013 Actual 2014 Actual 2015 Budget 2015 Actual Interest Costs $60,955, % $54,875, % $49,744, % $55,527, % $54,935, % Total Revenue** $631,850,995 $644,494,910 $653,970,533 $660,635,674 $668,471,750 Both debt service costs and interest costs as a percentage of revenue are down compared to current budget (and prior years with the exception of 2014) indicating less of revenues are required to service outstanding debt (principal and interest) and more is available to fund priority projects. 3) Operating Reserves/ Total Revenues Reserve levels are an indicator of financial strength since they provide the ability to meet unforeseen expenditures or revenue losses Actual 2013 Actual 2014 Actual 2015 Budget 2015 Actual Operating Reserves $93,564, % $74,092, % $77,547, % $46,635, % $63,034, % Total Revenue** $631,850,995 $644,494,910 $653,970,533 $660,635,674 $668,471,750 Projected operating reserve levels are slightly higher than that projected in the current budget but are down from the prior years reserve levels. The level of operating reserves remains adequate to meet potential unexpected contingencies. ** 2015 Budget includes reserve and surplus carry-forward applications as approved by the Board. P&P - 29

30 4) Total Municipal Taxes, Water, Sewer and Solid Waste Charges / Per Capita This indicator is a representation of the per capita cost impact of the regions tax payer supported services. These costs are passed on to the tax payer through our member municipalities. The 2015 population is assumed to increase at a rate of 1.5% over Actual Per Capita 2013 Actual Per Capita 2014 Actual Per Capita 2015 Budget Per Capita 2015 Actual Per Capita Total Tax Revenue *** $543,413,853 $225 $548,156,267 $224 $559,403,266 $226 $559,498,217 $223 $571,188,804 $227 Total Population **** 2,410,000 2,442,604 2,474,123 2,511,235 2,511,235 The projected increase in the actuals over the budget for 2015 is primarily a result of an increase in projected revenues for Water Sales and Solid Waste User Fees. ** 2015 Budget includes budgeted reserve, surplus carry-forward items or other additional reserve applications as approved by the Board. *** Total Tax Revenue defined as Regional District tax requisition, Water Sales, Sewer & Drainage Levy and Solid Waste User Fees. **** Based on Demographic Analysis Section, BC Stats, Ministry of Technology, Innovation and Citizens Services, Government of British Columbia, December P&P - 30

31 5.2 To: From: Performance and Procurement Committee Phil Trotzuk, Chief Financial Officer Date: July 9, 2015 Meeting Date: July 17, 2015 Subject: GVWD Borrowing Bylaw No. 248, 2015 RECOMMENDATION That the GVWD Board: a) approve a borrowing limit of $700,000. b) give first, second and third readings to Greater Vancouver Water District Borrowing Bylaw Number 248, 2015 and forward to the Inspector of Municipalities for approval. PURPOSE To provide the long term capital borrowing authority for the anticipated requirements of the next five years for the GVWD and to authorize the issuance of debenture debt for this purpose through the Greater Vancouver Regional District (GVRD) and the Municipal Finance Authority of British Columbia (MFA) in the aggregate amount of $700 million dollars. BACKGROUND The MFA is the financing agency for all of the municipalities and Regional Districts in B.C. except the City of Vancouver. It is also the financing agency for the Greater Vancouver Water District and Greater Vancouver Sewerage and Drainage District. The procedure begins with municipalities or greater boards such as GVWD passing a Borrowing Bylaw (or its equivalent) authorizing borrowing from the MFA on their behalf. Borrowing Bylaws are sent to the respective Regional Districts for inclusion in a Regional District Security Issuing Bylaw. Once all legal requirements (such as Inspector of Municipalities approval) are met, the borrowing and security issuing bylaws are forwarded to the MFA as the maximum accumulated borrowing authority and is drawn down over time based on borrowing. As an additional step for the GVWD, the Greater Vancouver Water District Act requires the recommendation of the Commissioner to the GVWD Board to undertake a program of borrowing. The MFA has two bond issues per year, one in the spring and one in the fall. The GVRD (Metro Vancouver) will secure long-term funding for its capital program in one or both of these issues depending on the level of capital spending / funding required. Metro Vancouver does not borrow in advance of spending but borrows when capital expenditures accumulate to such a level that longterm funding is beneficial relative to funding through working capital. Each spring and fall, borrowing requests are sent to the MFA. These request are reviewed by their Board of Trustees and upon approval, included in either the spring or fall bond issues. Net borrowing requirements are estimated annually based on the anticipated capital expenditure program and the required servicing of such debt is included in the annual budget. The estimates serve P&P - 31

32 as the base for the necessary borrowing authority. This authority is sought periodically as required, the last time being in GVWD BORROWING Staff seek Board approval for a block of borrowing authority in advance of any actual borrowing. This approach is required due to the significance and nature of capital spending. With the significance of the capital program, the GVWD is likely to require long-term funding during both MFA Bond issues. As a result, it is not operationally feasible to determine the borrowing requirements, get Board approval of the Borrowing and Security Issuing Bylaws, the necessary approval from the Inspector of Municipalities and the MFA in a timely way to meet the MFA deadlines for participation in their bond issue. The GVWD, with a significant capital program required to maintain, secure and expand current infrastructure to meet the demands of a growing region, estimates long-term borrowing needs of up to approximately $700 million over the next five years in order to help fund that program. Some of the major projects in the capital program are as follows: Major Planned GVWD Capital Expenditures ( ) Second Narrows Crossing (Tunnel) Annacis Main No. 5 (Marine Crossing) Tilbury Main Central Park Main Replacement Lulu Island Delta Main South Surrey Main No. 2 $297 M 168 M 71 M 70 M 64 M 56 M $726 M ALTERNATIVES 1. That the GVWD Board: a) approve a borrowing limit of $700,000. b) give first, second and third readings to Greater Vancouver Water District Borrowing Bylaw Number 248, 2015 and forward to the Inspector of Municipalities for approval. 2. That the GVWD Board provide alternative direction with respect to the borrowing limit as appropriate then give three readings to the Greater Vancouver Water District Borrowing Bylaw Number 248, 2015 and forward to the Inspector of Municipalities for approval. P&P - 32

33 FINANCIAL IMPLICATIONS Under alternative 1, which is recommended, staff will have the necessary authority to make prudent financing decisions as required. This will allow for the appropriate decisions regarding balancing the cost of financing with the associated financing risk. The inability to have the necessary flexibility to make the financing decisions would have an unfavourable financial impact. Should this authority be reduced or not granted as under alternative 2, the ability to make necessary financing decisions in a timely manner would be constrained which may have a negative financial impact. SUMMARY / CONCLUSION This Borrowing Bylaw, as recommended under alternative 1, provides the necessary authorization for the GVWD to long-term borrow funds as and when required up to a maximum of $700 million. Attachments GVWD Borrowing Bylaw No. 248, P&P - 33

34 GREATER VANCOUVER WATER DISTRICT BYLAW NUMBER 248, 2015 A BYLAW TO AUTHORIZE THE ISSUE AND SALE OF DEBT NOT TO EXCEED THE AGGREGATE PRINCIPAL AMOUNT OF $700,000,000 (CANADIAN) WHEREAS: A. It is requisite and expedient for the Greater Vancouver Water District (the District ) to issue and sell to the Greater Vancouver Regional District ( GVRD ) a debenture or debentures or other form of security or indebtedness, not to exceed the aggregate principal amount of $700,000,000 in lawful money of Canada in order to borrow money to be applied for the purpose of undertakings authorized by the Greater Vancouver Water District Act (the Act ) or for the purpose of discharging the payment of any matter or thing contemplated or authorized by the Act, including for the purpose of repaying or refunding either before or at maturity monies which have been borrowed by the District by the issue of temporary securities or other debentures or securities. B. A debenture or debentures or other form of securities, including treasury bills, notes, temporary debentures, or other form of obligation, or indebtedness, not to exceed the aggregate principal amount of $700,000,000 in lawful money of Canada, is required to be issued and sold to realize net the sum required for the purposes aforesaid. C. The Commissioner of the District has provided a report to the Board of the District in which she recommended for the purposes aforesaid the issue and sale to GVRD of a debenture or debentures or other form of security or indebtedness, not to exceed the aggregate principal amount of $700,000,000 in lawful money of Canada, and to enter into an agreement with GVRD all as provided below. NOW THEREFORE the Board of the District in meeting assembled of which and for the purpose of which due notice was given, ENACTS AS FOLLOWS: 1. For the purposes aforesaid and pursuant to the authority contained in the Act it shall be lawful for the District and the District is hereby authorized, with the approval of the Inspector of Municipalities, to borrow money by the issue and sale to GVRD of a debenture or debentures or other form of securities, including treasury bills, notes, temporary debentures, or other form of obligation, or indebtedness (the Debenture or Debentures ) not to exceed the aggregate principal amount of $700,000,000 in lawful money of Canada as hereinafter provided. 2. The Debenture or Debentures shall be dated and issued on such date or dates as the Commissioner of the District shall determine and shall bear interest at such rate or rates and shall be payable on such date or dates during its currency or their currencies all as the Commissioner may determine. The aggregate borrowing authorized by this bylaw may be effected by different series or types of Debenture or Debentures each bearing different dates, maturities and interest rates and having such characteristics all as determined by the Commissioner. Payments in respect of the P&P - 34

35 Debenture or Debentures shall be made to GVRD by the District by cheque or electronic funds transfer. 3. The Debenture or Debentures shall be issued in fully registered form without coupons and shall mature on such date or dates as the Commissioner shall determine. A debenture register shall be maintained at the head office of the District, or that of its Agent. 4. The Debenture or Debentures shall be payable as to principal and interest in lawful money of Canada or in such other currency as the Commissioner shall determine. 5. The District shall raise in each debenture year during the currency or currencies of the Debenture or Debentures a sum or sums sufficient in lawful money of Canada to pay interest and, if applicable, principal falling due from time to time on the Debenture or Debentures. 6. If the Debenture or Debentures are issued as a sinking fund debenture or debentures, a sinking fund shall be established by the District to retire or to assist in retiring the Debenture or Debentures at maturity and for such purpose the District shall raise in each debenture year during the currency or currencies of the Debenture or Debentures in accordance with the Act a sum or sums sufficient for such purpose in lawful money of Canada and deposit the same in the sinking fund or funds. In settling the sum or sums to be raised annually, the rate of interest on investments shall be estimated at 3.5% per annum, capitalized yearly. 7. The Debenture or Debentures, without limiting any other provision of this bylaw, may in the discretion of the Commissioner be issued subject to the District s option to redeem in whole or at any time or from time to time, any part of the Debenture or Debentures on any date in advance of the maturity thereof and upon such terms and conditions as the Commissioner may determine, subject to the place of redemption and the price (including any premium) at which the Debenture or Debentures may be redeemed being specified by the Commissioner. 8. The Debenture or Debentures shall be in such form as the Commissioner of the District shall approve. The Debenture or Debentures shall rank pari passu with all other general obligations of the District except as to sinking funds. 9. The Debenture or Debentures may be sold for such sum or sums whether the same is the par value or more or less than the par value thereof and on such terms and conditions as the Commissioner may determine. 10. The District shall and is hereby authorized to enter into an agreement with GVRD in form and substance approved by the Commissioner which provides, inter alia, that: (a) (b) the District will provide and pay over to GVRD the sums required to discharge its obligations in accordance with the terms of the Debenture or Debentures; and if the sums provided for in the Debenture or Debentures are not sufficient to meet the obligations of GVRD in relation to the financing, the deficiency is a liability of the District. P&P - 35

36 11. The Commissioner is hereby authorized on behalf of the District to do all such things and to execute, with or without the seal of the District, and deliver all such agreements, documents or instruments that may be necessary or desirable to give effect to this bylaw. Any such agreement, documents or instruments shall also be signed by any one of the Chair of the Board or the Treasurer of the District. 12. This bylaw shall take effect on the date it is passed and adopted. 13. This bylaw shall be cited as Greater Vancouver Water District Borrowing Bylaw Number 248, Read a first, second and third time this day of, Received the approval of the Inspector of Municipalities this day of, Passed and finally adopted this day of, Greg Moore, Chair Chris Plagnol, Corporate Officer P&P - 36

37 5.3 To: From: Performance and Procurement Committee Phil Trotzuk, Chief Financial Officer Date: July 10, 2015 Meeting Date: July 17, 2015 Subject: GVRD Security Issuing Bylaw No. 1224, 2015 Regarding GVWD Borrowing Bylaw No. 248, 2015 RECOMMENDATION That the GVRD Board: a) give first, second and third reading to "Greater Vancouver Regional District Security Issuing Bylaw No. 1224, 2015". b) forward "Greater Vancouver Regional District Security Issuing Bylaw No. 1224, 2015" to the Inspector of Municipalities for approval. PURPOSE To authorize a bylaw for the issuance of debenture debt through the GVRD and the Municipal Finance Authority of British Columbia (MFA) in the amount of $700 million dollars for the GVWD and to provide the long term capital borrowing authority for the anticipated requirements of the next five years. BACKGROUND The GVRD as a member of the MFA is the Board approved borrowing conduit of the Greater Vancouver Water District (GVWD). Through a separate agreement, the GVWD is financially responsible for all debt service costs associated with the debenture financing entered into on its behalf. Net borrowing requirements of the GVWD are estimated annually based on the requirements of the anticipated capital expenditure plan and serves as the base for the necessary borrowing authority. We estimate that our GVWD programs will have expenditures, requiring long-term financing, up to approximately $700 million over the next five years. SECURITY ISSUING BYLAW The attached bylaw, grants the necessary authority for the GVRD to borrow $700 million through the MFA on behalf of the GVWD. This authority is consistent with the borrowing authority included in GVWD Borrowing Bylaw 248, ALTERNATIVES 1. That the GVRD Board: a) give first, second and third reading to "Greater Vancouver Regional District Security Issuing Bylaw No. 1224, 2015". b) forward "Greater Vancouver Regional District Security Issuing Bylaw No. 1224, 2015" to the Inspector of Municipalities for approval. P&P - 37

38 2. That the GVRD Board make adjustments to the authority as appropriate, and give first, second and third reading to Greater Vancouver Regional District Security Issuing Bylaw No. 1224, 2015 and that it be forwarded to the Inspector of Municipalities for approval, as amended. FINANCIAL IMPLICATIONS Under alternative 1, as recommended, staff will have the necessary authority to secure GVWD financing, as required, which will allow the necessary flexibility for the appropriate financial decisions to be made on a timely basis. Should this authority be reduced or not granted under alternative 2, the ability to make necessary financing decisions in a timely manner would be constrained which may have a negative financial impact SUMMARY / CONCLUSION This Security Issuing Bylaw, in conjunction with the approved GVWD Borrowing Bylaw, provides the necessary authorization for the GVRD to borrow up to $700 million on behalf of the GVWD as and when required. Attachments and References: Greater Vancouver Regional District Bylaw No. 1224, P&P - 38

39 ATTACHMENT GREATER VANCOUVER REGIONAL DISTRICT BYLAW NO. 1224, 2015 A BYLAW TO AUTHORIZE THE ENTERING INTO OF A FINANCING AGREEMENT WITH THE MUNICIPAL FINANCE AUTHORITY OF BRITISH COLUMBIA IN THE AMOUNT OF $700,000,000 WHEREAS the Municipal Finance Authority of British Columbia ("the Authority") may provide financing of capital requirements for regional districts by the issue of debentures, or other evidence of indebtedness of the Authority and lending the proceeds therefrom to the regional district on whose request the financing is undertaken; AND WHEREAS the Greater Vancouver Regional District ( The Regional District ) may finance undertakings of the Greater Vancouver Water District on request, on behalf of and at the sole cost of the Greater Vancouver Water District, pursuant to the provisions of the Greater Vancouver Regional District Regulation B.C. Regulation 173/90 as amended, the undertakings to be financed pursuant to the following bylaw adopted by the Greater Vancouver Water District board under the Greater Vancouver Water District Act: District Bylaw Amount Greater Vancouver Water District 248, 2015 $700,000,000 AND WHEREAS for the purpose of providing financing under the Greater Vancouver Regional District Regulation, the Greater Vancouver Regional Board may adopt a security issuing bylaw without adopting a loan authorization bylaw; AND WHEREAS the Regional Board, by this Bylaw, hereby requests that such financing be undertaken through the Authority; NOW THEREFORE the Regional Board of the Greater Vancouver Regional District in open meeting assembled enacts as follows: 1. The Authority is hereby requested and authorized to finance from time to time the aforesaid undertakings at the sole cost and on behalf of the Greater Vancouver Regional District, in Canadian Dollars or in such other currency or currencies as the Authority shall determine so that the amount realized does not exceed Seven Hundred Million Dollars $700,000,000 in Canadian Dollars and/or the equivalent thereto and at such interest and with such discounts or premiums and expenses as the Authority may deem consistent with the suitability of the money market for the sale of securities of the Authority; 2. Upon completion by the Authority of financing undertaken pursuant hereto, the Chair and Chief Financial Officer of the Regional District, on behalf of the Regional District and under its seal shall, at such time or times as the Trustees of the Authority may request, enter into and deliver to the Authority one or more agreements which said agreement or agreements shall be substantially in the form annexed hereto as Schedule "A" and made part of this Bylaw (such agreement or agreements as may be entered into, delivered or substituted hereinafter referred to as the "Agreement") providing for payment by the Regional District to the Authority of the amounts P&P - 39

40 required to meet the obligations of the Authority with respect to its borrowings undertaken pursuant hereto, which Agreement shall rank as debenture debt of the Regional District; 3. The Agreement in the form of Schedule "A" shall be dated and payable in the principal amount or amounts of money in Canadian Dollars, or as the Authority shall determine and subject to the Local Government Act, in such other currency or currencies as shall be borrowed by the Authority pursuant to Section 1 and shall set out the schedule of repayment of the principal amount, together with interest on unpaid amounts as shall be determined by the Treasurer of the Authority; 4. The obligation incurred under the Agreement shall bear interest from a date specified therein, which date shall be determined by the Treasurer of the Authority, and shall bear interest at a rate to be determined by the Treasurer of the Authority; 5. The Agreement shall be sealed with the seal of the Regional District and shall bear the signatures of the Chair and Chief Financial Officer; 6. The obligations incurred under the Agreement as to both principal and interest shall be payable at the Head Office of the Authority in Victoria and at such time or times as shall be determined by the Treasurer of the Authority; 7. During the currency of the obligation incurred under the Agreement to secure borrowing in respect of the Greater Vancouver Water District Bylaw 248, 2015, there shall be requisitioned annually an amount sufficient to meet the annual payment of interest and the repayment of principal; 8. The Regional District shall provide and pay over to the Authority such sums as are required to discharge its obligations in accordance with the terms of the Agreement, provided however that if the sums provided for in the Agreement are not sufficient to meet the obligations of the Authority, any deficiency in meeting such obligations shall be a liability of the Regional District to the Authority and the Regional District shall make provision to discharge such liability; 9. Pursuant to section 15 of the Municipal Finance Authority of British Columbia Act, at the request of the Treasurer of the Authority, the Regional District shall pay over to the Authority such sums and execute and deliver such promissory notes as are required to form part of the Debt Reserve Fund established by the Authority in connection with the financing undertaken by the Authority on behalf of the Regional District pursuant to the Agreement; P&P - 40

41 10. This Bylaw may be cited as Greater Vancouver Regional District Security Issuing Bylaw Number 1224, Read a first, second and third time this day of, Received the approval of the Inspector of Municipalities this day of, Passed and finally adopted this day of, Greg Moore, Chair Chris Plagnol, Corporate Officer P&P - 41

42 CANADA PROVINCE OF BRITISH COLUMBIA Schedule A Dollars A G R E E M E N T GREATER VANCOUVER REGIONAL DISTRICT The Greater Vancouver Regional District (the Regional District ) hereby promises to pay to the Municipal Finance Authority of British Columbia at its Head Office in Victoria, British Columbia, (the "Authority") the sum of ($ ) in lawful money of Canada, United States of America or United Kingdom together with interest thereon from the day of 20 at the rate of per annum calculated (annually/ semi-annually) in each and every year during the currency of this Agreement; and payments shall be as specified in the table appearing on the reverse hereof commencing on the day of 20, provided that in the event the payments of principal and interest hereunder are insufficient to satisfy the obligations of the Authority undertaken on behalf of the Regional District, the Regional District shall pay over to the Authority such further sums as are sufficient to discharge the obligations of the Regional District to the Authority. It is understood and agreed between the Regional District and the Municipal Finance Authority of British Columbia that any monies paid by the Regional District to the Municipal Finance Authority of British Columbia in or towards repayment of monies borrowed by the Municipal Finance Authority of British Columbia and loaned to the Regional District pursuant to this agreement that are not applied by the Municipal Finance Authority of British Columbia to the payment of principal or interest or invested pursuant to Section 14 of the Municipal Finance Authority of British Columbia Act shall be paid into a fund to be created and administered by the Municipal Finance Authority of British Columbia in accordance with the provisions of Section 15 of the Municipal Finance Authority of British Columbia Act. Dated at, British Columbia, this day of 20. IN TESTIMONY WHEREOF and under the authority of Bylaw No. 1224, 2015 cited as Greater Vancouver Regional District Security Issuing Bylaw No. 1224, This Agreement is sealed with the Corporate Seal of the Greater Vancouver Regional District and signed by the Chairperson and Treasurer thereof. CHAIR CHIEF FINANCIAL OFFICER P&P - 42

43 5.4 To: From: Performance and Procurement Committee Dean Rear, Director - Financial Planning and Operations Date: July 6, 2015 Meeting Date: July 17, 2015 Subject: Amendment to Corporate Investment Policy RECOMMENDATION That the GVRD Board approve the Corporate Investment Policy as presented in the report titled Investment Policy Update, dated June 16, PURPOSE To seek GVRD Board approval for amendments to the Corporate Investment Policy. BACKGROUND The Board approved Corporate Investment policy provides the guidelines for investment decisions. The primary objective of the policy is to ensure safety of capital but also provides for maintaining sufficient liquidity to meet operational requirements and to provide the highest return on investment possible after considering safety of capital and required liquidity. The defined limits outlined in the policy are reviewed on an ongoing basis and require adjustments from time to time due to market changes, operational needs or other administrative matters. This policy was last amended in June PROPOSED POLICY AMENDMENTS Since the economic downturn following the Financial Crisis of , bond yields have been on a downward trend and reached a historical low point in the first quarter of As illustrated in table 1 below, average yields for the Canada bonds with maturities of 3-5 years and 5-10 years have both declined by more than 300 bps since mid Despite a slight increase experienced in the second quarter of 2015, the bond yields remain volatile and it is not yet clear as to when the rates will turn and start moving in an upward trend. P&P - 43

44 Table 1 5.0% 4.5% 4.0% 3.5% 3.0% 2.5% 2.0% 1.5% 1.0% 0.5% Average Canada Bond Yields 3-5YR 5-10YR Given this challenging market of uncertainty and a prolonged period of low interest rates, we need to identify different ways to maximize our return while meeting the primary objectives of our policy to preserve capital and maintain liquidity. As part of this policy update, we also streamlined and refined the existing investment terms. The proposed changes to the Investment Policy are as follows: 1) To establish maximum limit of $200M for Canadian provinces or entities guaranteed by the Provinces rated AA- or better, previously without any limit. This achieves a more balanced portfolio based on the limits. The maximum dollar limits are also assigned in a systematic and hierarchical order based on risk, as the Provincial have the next highest limit after Canada s federal instruments. 2) To increase the maximum terms for Canada and Provincial bonds from 10 to 30 years to allow expanded selection of products with longer maturities and higher yields. Access to longer-term Canadian government bonds with maturities beyond 10 years up to 30 years will almost double the current number of investment options and will allow additional pick-up in yields up to and more than 60 bps. As illustrated in Table 2 below, the average yield by term ranging from 2 to 30 years for Provincial bonds increase as it moves further out the time curve. The maximum limit as a percent of total portfolio is set conservatively at 5% for all government instruments combined to reflect the interest rate risk in holding a longterm instrument. As we continue to carefully assess the economic conditions and the future of interest rates, we remain cautious and prudent in our approach. We plan to invest beyond 10 years when rates are higher and we are able to realize a significant gain in yield. P&P - 44

45 3) Increased maximum term for National Bank of Canada to 10 years from 5 years. National Bank of Canada is one of the top six largest banks in Canada and offers deposit notes that are competitively priced to the other major Canadian banks. Expanding the term beyond the current limit of 5 years up to 10 years, consistent with the other major banks, will allow access to more products with potentially higher yields. The dollar and percentage maximum will remain at the previously existing levels that are slightly below the top five banks to reflect the lower credit rating. 4) Increased maximum dollar limits for Manulife Bank and Canadian Western Bank. Manulife Bank and Canadian Western Bank offer attractive yields compared to the top six banks. To account to the lower credit rating compared to the major Canadian banks, the maximum term and dollar limit beyond 1 year remain unchanged. The increase in the dollar limit will only apply to short-term investments under 1 year to maximize our rate of return from highly liquid money market products. 5) To add to our list of qualified investment institutions, Prospera Credit Union and First West Credit Union. Each of these institutions will be allowed a maximum dollar limit of $25 million and a maximum term of 3 years, consistent with the other credit unions that we currently invest with. The short-term money market products from banks and governments currently trade at exceptionally low yields. As an example, a 3 month-term bankers acceptance in early June offered yields ranging between 0.80% and 0.85%. In comparison, a credit union s 90-day term deposit offered interest rates up to 1.60%. Expanding the use of credit unions term deposits will allow increased laddering of our short-term portfolio to mitigate interest rate risks while improving our overall rate of return. The credit unions have consistently offered significantly better yields than the banks and governments in the past. Another advantage of credit union term deposits is the flexibility to set our own maturity dates to meet specific cash flow needs. 6) Updated maximum percentage based on dollar limit as percentage of $400M, estimated lower end of the portfolio range, adjusted for other risks. The current maximum percentages were not proportionate to the dollar maximum over the total portfolio value. Each category at the institution level and overall category level were reviewed and assigned a limit based on the dollar maximum as a percentage of the lower end of the estimated portfolio value of $400M, and further adjusted to factor in other risks. This methodology achieves a consistent and systematic approach to building a balanced portfolio. 7) To update the wording for safekeeping of credit union investments as the credit union deposits are neither book-based entry nor physical transfer and therefore are maintained by the respective credit unions. This last proposed change regarding the safekeeping requirement of credit union investments is necessary as the current policy is outdated in definition and practice. P&P - 45

46 Table 2 4.0% Provincial Bonds Average Yield 3.5% 3.0% 2.6% 3.4% 3.2% 2.5% 2.0% 1.5% 1.0% 0.5% 0.0% Ave Yield % Years The changes to the investment terms noted in (1) through (6) are also summarized in Attachment A to this report, as well as a summary table of all proposed changes and impact is included in Attachment B. These recommended changes will not materially impact the safety of capital or liquidity of the portfolio. A copy of the Corporate Investment Policy with a revised Appendix A, incorporating the above noted changes, is included as Attachment C. ALTERNATIVES 1. The GVRD Board approve the Corporate Investment Policy as presented in Attachment C. 2. The GVRD Board make adjustments to the Corporate Investment Policy as appropriate and approve the Corporate Investment Policy as amended. FINANCIAL IMPLICATIONS If the Board approves alternative 1, the proposed changes allow for increased return on investments by expanding available products and increasing maximum terms for high quality government bonds while also maintaining safety of capital. The total peak investment portfolio has been increasing ( $660 million; $648 million; $585 million) and the current limits have become restrictive for generating the highest return available. The proposed changes will not increase the risk to our capital. Not approving these proposed changes to increase investment terms and options will result in an opportunity cost of lost potential returns. P&P - 46

47 SUMMARY / CONCLUSION The corporate investment policy changes highlighted in this report increase our investing flexibility and as a result allow for access to greater investment returns while maintaining the conservative risk exposure appropriate for an organization of our nature. The changes as included under alternative 1 are recommended to the Board for approval. Attachments: Attachment A Proposed Investment Policy Adjustments June 2015 Attachment B Summary Table of Proposed Changes and Impact Attachment C Corporate Investments Policy No.3.08 Revised P&P - 47

48 P&P - 48

49 SUMMARY TABLE OF PROPOSED CHANGES AND IMPACT Proposed Change Set maximum limit of $200M for Canadian provinces or entities guaranteed by provinces rated AA- or better, previously without any limit. Increased maximum term for investments in Government instruments beyond 10 years up to maximum of 30 years. Increased maximum term for National Bank of Canada to 10 years from 5 years. Increased maximum dollar limits for Manulife Bank and Canadian Western Bank. Addition of two new BC Credit Unions: First West Credit Union and Prospera Credit Union. Updated maximum percentage based on dollar limit as percentage of $400M, estimated lower end of the portfolio range, adjusted for other risks. Updated safekeeping requirement for credit union investments. Impact Achieve a more balanced portfolio by limiting maximum dollar. Systematic and hierarchical ordering of limits based on risk. Next highest limit after Canada instruments. Increased products. Higher yields. Laddering of portfolio. Increased products beyond 5 years maturity with competitive pricing. Term consistent with rest of the major Canadian banks. Increased products. Higher yields. Laddering of portfolio, in particular the shorter term. Increased products. Higher yields. Laddering of portfolio, in particular the shorter term. Facilitate cash flow planning as we can set specific maturity dates. Consistent and systematic allocation of percentage maximums. Current and accurate description of safekeeping requirements. P&P - 49

50 ATTACHMENT C BOARD POLICY CORPORATE INVESTMENTS POLICY NUMBER: FN Effective Date: June 4, 2014 Approved By: GVRD BOARD PURPOSE To provide guidelines within which investment decisions are made to ensure safety of capital, adequate liquidity and a reasonable rate of return. APPLICATION This policy applies to all investments on behalf of the corporate entities. POLICY A. General Objectives: i) Safety of Capital This is the foremost objective of this policy. Prudent investments shall be chosen in a manner that ensures preservation of capital. Consideration therefore must be given to both credit and interest rate risk in all investment decisions. ii) Liquidity Investment portfolios will provide sufficient liquidity to meet the ongoing needs of all Metro Vancouver Districts and the Housing Corporation. Investment terms will be structured as much as possible to meet anticipated cash needs. iii) Yield Portfolios will be invested to produce the highest yield after first considering objectives i) and ii) above and within the investment guidelines in Appendix A. B. Standard of Care The standard of care to be applied by staff in carrying out their duties is that of a prudent person, in the context of the management of a diversified portfolio. This in turn translates as the exercise of discretion and judgment, in conformity with policies, with the purpose being investment, rather than speculation. The Employee Code of Ethics Policy requires performance to a high standard of integrity, and specifically forbids conflict of interest situations. 1 Replaces Policy No that was noted in the document adopted by the Board P&P - 50

51 C. Investment Parameters Investments will at all times be governed by legislation, specifically the Community Charter Section 183 (copy attached as Appendix C). Short term investments (maximum term 365 days) are restricted to those with a minimum short term credit rating of R1Low as defined by Dominion Bond Rating Service (DBRS) or the Standard and Poor s (S&P) equivalent of A-1. Short term investments will be permitted in non-qualifying institutions when such investments are guaranteed by a qualified institution. An example of this would be an investment in a Credit Union in BC which is in turn guaranteed by the Province of BC. Long term investments must have at a minimum a long term credit rating of 'A-' by S&P or DBRS equivalent (A-low). Both our short term and long term investments are limited to primarily Government debt (provincial and federal) and Canadian financial institutions. The specific details of the qualified investments as well as the maximum permitted dollar values and portfolio percentages are listed in Appendix A. D. Investment Terms Short Term Investments will have a maximum term of 365 days and are restricted to terms listed on Appendix A attached. Long Term Investments are those with term exceeding 365 days. Long term investments will also be restricted to terms listed on Appendix A attached. E. Tendering Short Term Investments (under 365 days) Investments of terms greater than 15 days require at least three quotes from qualifying dealers. (See comments below concerning Long Term Investments as a potential exception to this rule) Long Term Investments (over 365 days) Long term investments do not necessarily lend themselves to direct comparison. Often there is difficulty in finding the same name or similar credit quality in exactly the same term. This requires that those responsible for long term investing are given and use considerable judgement in determining the investment choice. Where direct comparisons are possible between like or similar investments at least three quotes from qualifying dealers will be required. P&P - 51

52 Where direct product comparisons are not available, those responsible for investing must ensure that the offering under consideration is priced fairly. This can be done by verifying spread levels (over benchmark or equivalent term Canada bonds) obtained from two other dealers which support the offering being considered. These spreads should be recorded for subsequent review by internal audit. F. Safekeeping All investments will be held for safekeeping at either RBC Investor Services (our Safekeeping Agent), Royal Bank Capital Markets (RBC Dominion Securities), the Bank of Montreal, or at Clearing and Depository Services Inc. (CDS) for securities whose transfer is book-based rather than by physical delivery. However, Credit Union deposits are neither CDS book-based entry nor physical transfer and therefore will be maintained by the respective Credit Union. G. Review, Oversight and Reporting The statutory authority of the Treasurer for investment decisions is delegated to the Division Manager, Treasury and Business Processes and to the Treasury Manager, including any appointed in an acting capacity. While day to day investment operations are the responsibility of the Treasury Manager, the Division Manager, Treasury and Business Processes is responsible for its supervision, including review of internal control issues and policy enforcement. Summary reports on investment positions will be prepared monthly for the Treasurer. The Treasurer, Division Manager, Treasury and Business Processes, and Treasury Manager will meet quarterly (or more frequently as required) as an Investment Management Committee to review the investment activities as well as current investments issues. The Committee will establish the percentage split of the portfolio between long and short term investments as well as the average term of the portfolio based on existing market conditions and expected future conditions. A list of approved investments, based on the eligibility criteria, will be developed and maintained by the Division Manager, Treasury and Business Processes, subject to the approval of the Committee. While changes to the 'Approved List of Investments' outlined in Appendix A are subject to the Finance Committee's specific approval, any officer may immediately suspend a previously approved investment at any time on his own authority and, in fact, must do so when he has reason to believe it no longer meets the necessary requirements The officer will immediately advise the other officers connected with investment decisions. Quarterly, the ratings of all approved investments will be reviewed by the Division Manager, Treasury and Business Processes. Upon knowledge of a decrease in the credit rating of an approved investment to a level below the parameters outlined in this policy, the Division Manager, Treasury and Business Processes will immediately advise the Treasurer. As this rating is below the minimum acceptable credit rating, the investment position should be sold within a reasonable period of time. P&P - 52

53 A report will be presented to the Finance Committee as of April 30, August 31, and December 31 each year and will include a position statement, performance results compared to benchmarks, market comment and other relevant issues. The Regional District purchases investments with the intention of holding these until maturity and not with further trading in mind. As such, changes in market value become irrelevant to the actual return. For this reason we will not adjust the portfolio value based on changes in unrealized market value, but rather report investment performance based on actual return to maturity. Our short term investment performance will be compared to the benchmarks detailed on Appendix B. Finding a benchmark for our long term investments is difficult as most available benchmarks will reflect changes in market valuation. With this in mind, we will provide the benchmarks included on Appendix B as a reasonable general comparison to our long term investment performance. In addition to the audit activities and procedures performed annually by the external auditors, the internal audit group will review internal controls and ensure compliance with policy and procedures bi-annually. All changes to this policy require Finance Committee and Board approval. Appendices: Appendix A: Approved Investments (February 2008) (Updated December 12, 2011) Appendix B: Investment Performance Benchmarks Appendix C: Community Charter (Section 183) P&P - 53

54 Approved Investments (July 2014) *Includes Provincially guaranteed Financial Institutions P&P - 54

55 Investment Performance Benchmarks The benchmarks listed below are used as a guideline to assess the performance / investment returns on investments held. Short Term Investments Municipal Finance Authority Money Market Fund* Average One Month Banker's Acceptance Rate** Average Three Month Banker s Acceptance Rate** Long Term Investments Municipal Finance Authority Intermediate Bond Fund Municipal Finance Authority Long-term Bond Fund *Available on the MFA website **Calculated from the Bank of Canada website P&P - 55