A unified "Bang-Bang" Principle with respect to a class of non-anticipative benchmarks

|

|

|

- Zoe Fowler

- 5 years ago

- Views:

Transcription

1 A unified "Bang-Bang" Principle with respect to a class of non-anticipative benchmarks Phillip Yam (Joint work with Prof. S. P. Yung (Math, HKU), W. Zhou (Math, HKU), John Wright (Math, HKU), Prof. Eddie Hui (BRE, HKPU))

2 Outline: What is the right time to sell a stock? A unified Bang-Bang (algebraic) principle How long is a financial crisis? Sell-in-May? Halloween effect?

3 What is the right time to sell a stock? (Supported by HKRGC: HKGRF ) (Joint work with Prof. S. P. Yung and W. Zhou (Math, HKU))

4 A voice from an individual investor: down-to-earth concern In a finite time horizon [0, T], (1) Selling it at the highest price, (2) Buying a stock at the lowest price with NO RISK. Mission impossible! At any time, nobody can anticipate the future, Better ask: (1) How can we minimize the gap between the selling (resp. buying) price of a stock and its ultimate maximum (resp. minimum)? Or (2) How can maximize the chance to sell (resp. buy) a stock precisely at its ultimate maximum (resp. ultimate minimum)? Or (3) Avoiding selling stock at least price, i.e. maximizing the gap between selling price (resp. buying) and the ultimate minimum price (resp. maximum), etc. Can technical analysis help? For example, looking at chart to seek for patterns, trends, waves, etc.

5 An inquiry from Mathematics Community A. N. Shiryaev (1999) S t follows a geometric Brownian motion ds t = S t ( µ dt + σ db t ) Measuring the gap by using: (1) Mean Square Difference, see Peskir and Shiryaev (2001) & (2006) and Du Toit and Peskir (2007); for partial results with p(>1)-power, see Gaversen, Shiryaev and Peskir (2001), Pedersen (2003), Du Toit and Peskir (2007) (2) Mean Relative Error of the selling price to the highest price S T * over [0, T]: Relative error = (S T* S t ) / S T * i.e. define: (i) PDE method: Shiryaev, Xu and Zhou (2009) (ii) Probabilistic method: Du Toit and Peskir (2009), Yam, Yung and Zhou (2009).

6 Optimal selling time For any stopping time, we define The optimal stopping times for different cases are: where

7 Superior, neutral and inferior stocks A stock with (µ, σ ) is called: 1) Superior if µ / σ 2 > ½ 2) Neutral if µ / σ 2 = ½ 3) Inferior if µ / σ 2 < ½ In honor of the problem-poser, we call µ / σ 2 Shiryaev index of the stock.

8 In a nutshell, Warren Buffett is possibly correct: Choose the best superior stock, i.e. the stock with the highest index (µ / σ 2 ) in the market, and then buy-and-hold

9 Idea of Proof

10 A Princess looking for her Prince Charming (Secretary Problem) For if a princess can expect to meet exactly N eligible gentlemen in her life, what strategy should she use to maximize her chance of choosing the best one? An optimal strategy for selecting the best of these N candidates in row is to skip the first j*-1 candidates, and then select the next "best so far" that she would encounter. Here j* =4 for N = 10, say.

11 Inspired by the Princess For any stopping time, we define

12 Idea behind our approach We shall only illustrate our solution for the critical case µ = ½ σ 2. Dominant stopping: Given a Wiener functional G, we say there is a dominant stopping ρ: L 1 L 1 if there is another Wiener functional F > G a.s. such that for any stopping time τ so that E(G ρ(τ) ) = E(F τ ).

13 Sketch of the proof for µ / σ 2 = ½ We first use Strong Markov Property to simplify: where is the reflected Brownian motion at zero and

14 Similarly, we also have where

15 F > G They agree along the boundaries x = 0 and t = 0. Both F and G approach zero as either x and t gets large. Show by contradiction that there is no interior global minimum with negative value.

16 Good notations can ease the argument where

17 A contradiction! Therefore,

= 0 and together")

18 is actually constant! Let Using Ito-Tanaka s formula: F x (t, 0) = 0 and together with Optional Stopping Theorem, we have

19 Hence we have It is optimal to sell the stock when the underlying governing Brownian motion hits its running maximum or at the terminal time.

20 A unified Bang-Bang principle

Maximizing the probability to sell a stock at ultimate maximum (Yam, Yung and Zhou (2009)); (ii) (behavioral sense) non-increasing and convex function f: Dai, Jin, Zhong and")

21 Generalizations General processes (Probabilistic methods): (i) Binomial tree (CRR) processes (Yam, Yung and Zhou (2009)); (ii) Levy processes (Allaart (2009a, b)). General benchmarks: (i) Maximizing the probability to sell a stock at ultimate maximum (Yam, Yung and Zhou (2009)); (ii) (behavioral sense) non-increasing and convex function f: Dai, Jin, Zhong and Zhou (2009) (PDE methods); (iii) (Conservative mind) Selling as far as possible from the lowest price Dai, Jin, Zhong and Zhou (2009) (PDE methods); (iv) Selling as close as average price (See Dai and Zhong (2009) (PDE methods)) where

Buying stock as far as possible from the highest price (3) In addition to average, maximum or minimum, how about selling at an ultimate α-quantile of the stock price (4) Is there a unified")

22 Some more open questions (1) Gaversen, Shiryaev and Peskir (2001), Pedersen (2003), Du Toit and Peskir (2007) for 0 < p < 1. (2) Buying stock as far as possible from the highest price (3) In addition to average, maximum or minimum, how about selling at an ultimate α-quantile of the stock price (4) Is there a unified approach to all the problems mentioned on previous page? Probabilistic or PDE method?

23 A unified (algebraic) principle Yes, a probabilistic approach! One result for all! D[0,T] = space of all piecewise continuous paths with at most finitely many ordinary jump points Using Permutation and/or time reversing of different pieces of a path in D[0,T] to define an equivalent relation R in D[0,T] ~

24 A universal benchmark F Consider a Wiener functional F such that: 1. Translation invariant: F(w + c) = F(w) + c ; 2. Monotonicity: For every t, w 1 (t) w 2 (t), implies F(w 1 ) F(w 2 ); 3. F is R-invariant.

25 Main theorem Given a monotone, convex function f:r R, and a universal benchmark F:D[0,T] R. Consider the optimal stopping problem: f λ 0 λ < 0 (i) non-increasing τ* = T τ* = 0 (ii) non-decreasing τ* = 0 τ* = T

26 Idea of proof 1. Comparison of stopping times is equivalent to comparison of magnitude of functions; 2. Application of time reversibility of Brownian motion (or in general infinitely divisible processes) leads convexity of f to come to play; indeed, the difference of functions in (1) can now be expressed as an integral of difference of increments of f over consecutive disjoint intervals; 3. Simple convexity analysis deduces the nonnegativity of the difference of functions in (1).

27 Application of the theorem Selling as close as average price (See Dai and Zhong (2009) (PDE methods)) Translation invariant and monotonicity are clear; Lebesgue measure is invariant under translation and reflection, hence the integral is R-invariant. Hence, τ* = T when λ 0, and τ* = 0 when λ < 0. Gaversen, Shiryaev and Peskir (2001), Pedersen (2003), Du Toit and Peskir (2007) for 0 < p < 1. (i) f = - x p is decreasing and convex; (ii) maximal operator is translation invariant, monotonic and R-invariant (ordering of a set of elements has no effect on their maximum value) Hence, τ* = T when λ 0, and τ* = 0 when λ < 0.

28 Future works A partial result that for time-dependent drift and volatility with µ (t) > ½ σ 2 (t), it is still optimal to buy-and-hold (Yam, Yung and Zhou (2009); Open problem: In general, consider a positive geometric diffusion process ds t = S t ( µ(ω,t) dt + σ (ω,t) db t ) provided that µ (ω,t) > ½ σ 2 (ω,t) a. s., shall we also buy-and-hold? Question: How about for any µ (ω,t) and σ (ω,t), when will be the optimal time to sell under the same rationale? Under what other simple criteria, can we still have explicit/analytic optimal stopping strategy? Answer: some partial results has been obtained by us.

29 Implication of Shiryaev index on Seasonal Effects in Markets How long will a financial crisis be? Sell-in-May and Go-Away? Welcome Halloween? (Supported by HKPU Interdisciplinary Grant, and HKPU IRG A-PC0D) (Joint work with John Wright (Math, HKU) and Prof. Eddie C. M. Hui (BRE, HKPU))

30 Sell-In-May, Welcome Halloween? ( Sell in May and go away, the belief that the period from November to April inclusive has significantly stronger growth on average than the other months stocks are sold at the start of May and the proceeds held in bonds or a deposit account; stocks are bought again in the autumn, typically around Halloween. Halloween indicator is more prevalent in Europe than in the United States, There is no consensus on what causes this phenomenon, although theories include an impact from summer vacations and draw comparisons to the January effect.

31 Preliminaries on modeling Any continuous semimartingale is a sum of finite variation process and a Brownian motion up to change of time (continuous local martinagale); It is reasonable to model positive stock price dynamics as a general geometric diffusion process with adapted stochastic drift and volatility From experience, stock price time series seems to have long-memory (or longrange) dependence. Why not use fractional Brownian motion as a model? 1) Most statistical tests are only testing the autocorrelation structure of a time series, no immediate test can differentiate whether the underlying process is a fbm or a Gaussian process with the same autocorrelation structure (see L. C. G. Rogers (1997)); 2) Apart from a few results, e.g. no-arbitrage nature of market driven by fbm with appropriate proportional transaction cost (and the corresponding fundamental theorem of asset pricing but no pricing formula is provided), there is no convenient stochastic calculus for non-semimartingales (perhaps rough path theory, see T. Lyons (1998)).

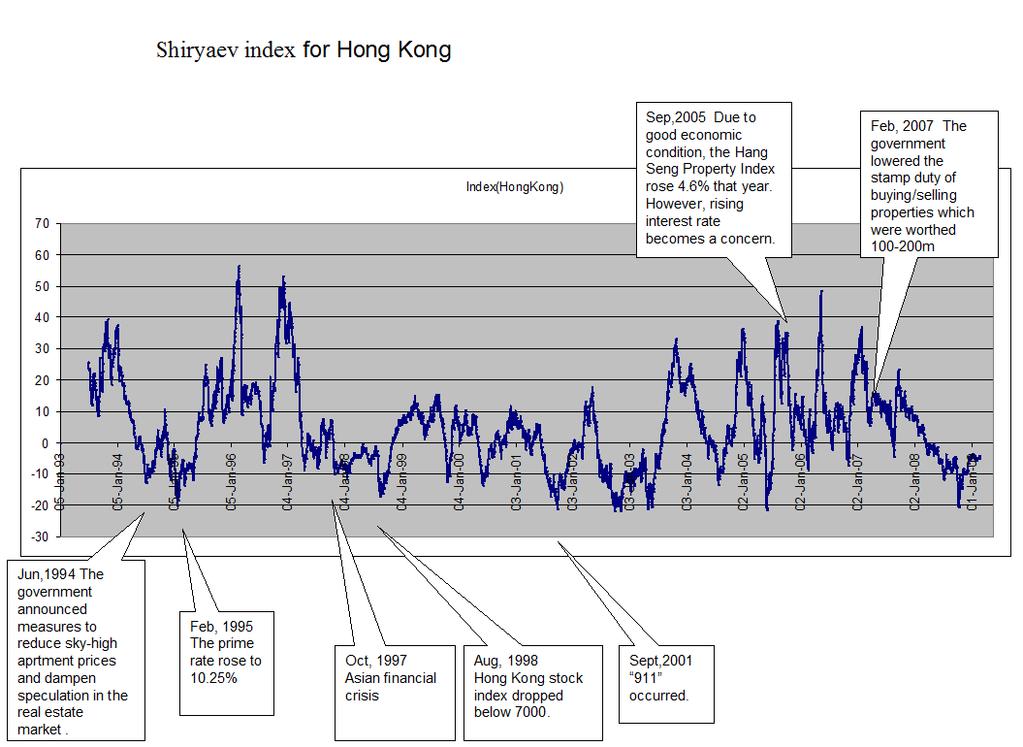

32 Model in Practice (Moving Average) Source of data: 20+ years of Hang-Seng index; We assume that the Hang-Seng index S t follows a geometric Brownian motion over a moving window (reasonably to take 4 to 6 months): dst = µ dt + σ dbt St Or 1 2 log( St ) = log( S0) + ( µ σ ) t + σ Bt 2 Treating drift and volatility as if constant over the moving window; Using AR(1) model to fit the data over the moving window, and hence the estimation of parameters. No significant statistical rejection had observed; Using Graduation (smoothing) method to produce secondary estimates of parameters. Perhaps More sophisticated modeling, e.g. GARCH and their generalized versions, may provide similar figures.

33 Graphs of log(s t -S t-1 ) T Line Fit Plot 1990 T Line Fit Plot u_i u_i T T 1991 T Line Fit Plot 1992 T Line Fit Plot u_i T u_i T

34 Graphs of log(s t -S t-1 ) T Line Fit Plot 1994 T Line Fit Plot u_i u_i T -0.1 T 1995 T Line Fit Plot 1996 T Line Fit Plot u_i u_i T T

35 Graphs of log(s t -S t-1 ) T Line Fit Plot 1998 T Line Fit Plot u_i u_i T T 1999 T Line Fit Plot 2000 T Line Fit Plot u_i u_i T T

36 Graphs of log(s t -S t-1 ) T Line Fit Plot 2002 T Line Fit Plot u_i u_i T T 2003 T Line Fit Plot 2004 T Line Fit Plot u_i u_i T T

37 Graphs of log(s t -S t-1 ) T Line Fit Plot 2006 T Line Fit Plot u_i u_i T T 2007 T Line Fit Plot 2008 T Line Fit Plot u_i u_i T T

38 Projecting the duration of a financial crisis based on Shiryaev index (Moving window before each time point)

39

40 Seasonal Effects and Shiryaev index: Sell-in-May? And Halloween Effect? (Each time point is the mid-point of the moving window)

41 United Kingdom market Monthly Comparison 26.79% 36.36% 40.20% 42.22% 46.45% 51.48% 53.92% 49.64% 50.74% 49.29% 41.03% 35.95% 100% 80% 60% 73.21% 63.64% 59.80% 57.78% 53.55% 48.52% 46.08% 50.36% 49.26% 50.71% 58.97% 64.05% 40% 20% 0% Month positive negative

42 United States market Monthly Comparison 48.62% 38.40% 34.62% 37.28% 34.60% 46.93% 49.48% 62.72% 70.86% 67.32% 64.38% 58.39% 100% 80% 60% 51.38% 61.60% 65.38% 62.72% 65.40% 53.07% 50.52% 37.28% 29.14% 32.68% 35.62% 41.61% 40% 20% 0% Month positive negative

43 In a given year, western market seems to lull in summers after May and to get better in winters.

44 Hong Kong market Monthly Comparison 52.55% 57.76% 59.94% 48.67% 47.32% 42.57% 40.23% 32.96% 42.57% 36.16% 21.13% 29.31% 100% 80% 60% 47.45% 42.24% 40.06% 51.33% 52.68% 57.43% 59.77% 67.04% 57.43% 63.84% 78.87% 70.69% 40% 20% 0% Month Positive Negative

45 In a given year, market seems to fall silent after Lunar New Year, yet it seems to get better after Dragon-Boat festival.

46 A Neo-adage 未食五月粽, 寒衣不敢送 (Before Dragon-Boat Festival, the weather could still be very cold) However, it may not still be valid nowadays because of global warming! 未食五月粽, 持股量勿重 (Not be so ambitious in investment in stock market before Dragon-Boat Festival)

47 Thank you!

Beyond the Black-Scholes-Merton model

Econophysics Lecture Leiden, November 5, 2009 Overview 1 Limitations of the Black-Scholes model 2 3 4 Limitations of the Black-Scholes model Black-Scholes model Good news: it is a nice, well-behaved model

Econophysics Lecture Leiden, November 5, 2009 Overview 1 Limitations of the Black-Scholes model 2 3 4 Limitations of the Black-Scholes model Black-Scholes model Good news: it is a nice, well-behaved model

Stochastic Dynamical Systems and SDE s. An Informal Introduction

Stochastic Dynamical Systems and SDE s An Informal Introduction Olav Kallenberg Graduate Student Seminar, April 18, 2012 1 / 33 2 / 33 Simple recursion: Deterministic system, discrete time x n+1 = f (x

Stochastic Dynamical Systems and SDE s An Informal Introduction Olav Kallenberg Graduate Student Seminar, April 18, 2012 1 / 33 2 / 33 Simple recursion: Deterministic system, discrete time x n+1 = f (x

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

Modeling via Stochastic Processes in Finance

Modeling via Stochastic Processes in Finance Dimbinirina Ramarimbahoaka Department of Mathematics and Statistics University of Calgary AMAT 621 - Fall 2012 October 15, 2012 Question: What are appropriate

Modeling via Stochastic Processes in Finance Dimbinirina Ramarimbahoaka Department of Mathematics and Statistics University of Calgary AMAT 621 - Fall 2012 October 15, 2012 Question: What are appropriate

1 The continuous time limit

Derivative Securities, Courant Institute, Fall 2008 http://www.math.nyu.edu/faculty/goodman/teaching/derivsec08/index.html Jonathan Goodman and Keith Lewis Supplementary notes and comments, Section 3 1

Derivative Securities, Courant Institute, Fall 2008 http://www.math.nyu.edu/faculty/goodman/teaching/derivsec08/index.html Jonathan Goodman and Keith Lewis Supplementary notes and comments, Section 3 1

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

Pricing Dynamic Solvency Insurance and Investment Fund Protection

Pricing Dynamic Solvency Insurance and Investment Fund Protection Hans U. Gerber and Gérard Pafumi Switzerland Abstract In the first part of the paper the surplus of a company is modelled by a Wiener process.

Pricing Dynamic Solvency Insurance and Investment Fund Protection Hans U. Gerber and Gérard Pafumi Switzerland Abstract In the first part of the paper the surplus of a company is modelled by a Wiener process.

Introduction to Stochastic Calculus With Applications

Introduction to Stochastic Calculus With Applications Fima C Klebaner University of Melbourne \ Imperial College Press Contents Preliminaries From Calculus 1 1.1 Continuous and Differentiable Functions.

Introduction to Stochastic Calculus With Applications Fima C Klebaner University of Melbourne \ Imperial College Press Contents Preliminaries From Calculus 1 1.1 Continuous and Differentiable Functions.

CONTINUOUS TIME PRICING AND TRADING: A REVIEW, WITH SOME EXTRA PIECES

CONTINUOUS TIME PRICING AND TRADING: A REVIEW, WITH SOME EXTRA PIECES THE SOURCE OF A PRICE IS ALWAYS A TRADING STRATEGY SPECIAL CASES WHERE TRADING STRATEGY IS INDEPENDENT OF PROBABILITY MEASURE COMPLETENESS,

CONTINUOUS TIME PRICING AND TRADING: A REVIEW, WITH SOME EXTRA PIECES THE SOURCE OF A PRICE IS ALWAYS A TRADING STRATEGY SPECIAL CASES WHERE TRADING STRATEGY IS INDEPENDENT OF PROBABILITY MEASURE COMPLETENESS,

Lecture 3: Review of mathematical finance and derivative pricing models

Lecture 3: Review of mathematical finance and derivative pricing models Xiaoguang Wang STAT 598W January 21th, 2014 (STAT 598W) Lecture 3 1 / 51 Outline 1 Some model independent definitions and principals

Lecture 3: Review of mathematical finance and derivative pricing models Xiaoguang Wang STAT 598W January 21th, 2014 (STAT 598W) Lecture 3 1 / 51 Outline 1 Some model independent definitions and principals

Continuous Processes. Brownian motion Stochastic calculus Ito calculus

Continuous Processes Brownian motion Stochastic calculus Ito calculus Continuous Processes The binomial models are the building block for our realistic models. Three small-scale principles in continuous

Continuous Processes Brownian motion Stochastic calculus Ito calculus Continuous Processes The binomial models are the building block for our realistic models. Three small-scale principles in continuous

Optimal stopping problems for a Brownian motion with a disorder on a finite interval

Optimal stopping problems for a Brownian motion with a disorder on a finite interval A. N. Shiryaev M. V. Zhitlukhin arxiv:1212.379v1 [math.st] 15 Dec 212 December 18, 212 Abstract We consider optimal

Optimal stopping problems for a Brownian motion with a disorder on a finite interval A. N. Shiryaev M. V. Zhitlukhin arxiv:1212.379v1 [math.st] 15 Dec 212 December 18, 212 Abstract We consider optimal

DRAFT. 1 exercise in state (S, t), π(s, t) = 0 do not exercise in state (S, t) Review of the Risk Neutral Stock Dynamics

, π(s, t) = 0 do not exercise in state (S, t) Review of the Risk Neutral Stock Dynamics") Chapter 12 American Put Option Recall that the American option has strike K and maturity T and gives the holder the right to exercise at any time in [0, T ]. The American option is not straightforward

Chapter 12 American Put Option Recall that the American option has strike K and maturity T and gives the holder the right to exercise at any time in [0, T ]. The American option is not straightforward

Continuous Time Finance. Tomas Björk

Continuous Time Finance Tomas Björk 1 II Stochastic Calculus Tomas Björk 2 Typical Setup Take as given the market price process, S(t), of some underlying asset. S(t) = price, at t, per unit of underlying

Continuous Time Finance Tomas Björk 1 II Stochastic Calculus Tomas Björk 2 Typical Setup Take as given the market price process, S(t), of some underlying asset. S(t) = price, at t, per unit of underlying

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL YOUNGGEUN YOO Abstract. Ito s lemma is often used in Ito calculus to find the differentials of a stochastic process that depends on time. This paper will introduce

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL YOUNGGEUN YOO Abstract. Ito s lemma is often used in Ito calculus to find the differentials of a stochastic process that depends on time. This paper will introduce

Hedging under Arbitrage

Hedging under Arbitrage Johannes Ruf Columbia University, Department of Statistics Modeling and Managing Financial Risks January 12, 2011 Motivation Given: a frictionless market of stocks with continuous

Hedging under Arbitrage Johannes Ruf Columbia University, Department of Statistics Modeling and Managing Financial Risks January 12, 2011 Motivation Given: a frictionless market of stocks with continuous

Optimal trading strategies under arbitrage

Optimal trading strategies under arbitrage Johannes Ruf Columbia University, Department of Statistics The Third Western Conference in Mathematical Finance November 14, 2009 How should an investor trade

Optimal trading strategies under arbitrage Johannes Ruf Columbia University, Department of Statistics The Third Western Conference in Mathematical Finance November 14, 2009 How should an investor trade

Introduction to Probability Theory and Stochastic Processes for Finance Lecture Notes

Introduction to Probability Theory and Stochastic Processes for Finance Lecture Notes Fabio Trojani Department of Economics, University of St. Gallen, Switzerland Correspondence address: Fabio Trojani,

Introduction to Probability Theory and Stochastic Processes for Finance Lecture Notes Fabio Trojani Department of Economics, University of St. Gallen, Switzerland Correspondence address: Fabio Trojani,

Equivalence between Semimartingales and Itô Processes

International Journal of Mathematical Analysis Vol. 9, 215, no. 16, 787-791 HIKARI Ltd, www.m-hikari.com http://dx.doi.org/1.12988/ijma.215.411358 Equivalence between Semimartingales and Itô Processes

International Journal of Mathematical Analysis Vol. 9, 215, no. 16, 787-791 HIKARI Ltd, www.m-hikari.com http://dx.doi.org/1.12988/ijma.215.411358 Equivalence between Semimartingales and Itô Processes

Replication and Absence of Arbitrage in Non-Semimartingale Models

Replication and Absence of Arbitrage in Non-Semimartingale Models Matematiikan päivät, Tampere, 4-5. January 2006 Tommi Sottinen University of Helsinki 4.1.2006 Outline 1. The classical pricing model:

Replication and Absence of Arbitrage in Non-Semimartingale Models Matematiikan päivät, Tampere, 4-5. January 2006 Tommi Sottinen University of Helsinki 4.1.2006 Outline 1. The classical pricing model:

The Mathematics of Currency Hedging

The Mathematics of Currency Hedging Benoit Bellone 1, 10 September 2010 Abstract In this note, a very simple model is designed in a Gaussian framework to study the properties of currency hedging Analytical

The Mathematics of Currency Hedging Benoit Bellone 1, 10 September 2010 Abstract In this note, a very simple model is designed in a Gaussian framework to study the properties of currency hedging Analytical

From Discrete Time to Continuous Time Modeling

From Discrete Time to Continuous Time Modeling Prof. S. Jaimungal, Department of Statistics, University of Toronto 2004 Arrow-Debreu Securities 2004 Prof. S. Jaimungal 2 Consider a simple one-period economy

From Discrete Time to Continuous Time Modeling Prof. S. Jaimungal, Department of Statistics, University of Toronto 2004 Arrow-Debreu Securities 2004 Prof. S. Jaimungal 2 Consider a simple one-period economy

AMH4 - ADVANCED OPTION PRICING. Contents

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

Stochastic Calculus, Application of Real Analysis in Finance

, Application of Real Analysis in Finance Workshop for Young Mathematicians in Korea Seungkyu Lee Pohang University of Science and Technology August 4th, 2010 Contents 1 BINOMIAL ASSET PRICING MODEL Contents

, Application of Real Analysis in Finance Workshop for Young Mathematicians in Korea Seungkyu Lee Pohang University of Science and Technology August 4th, 2010 Contents 1 BINOMIAL ASSET PRICING MODEL Contents

How to hedge Asian options in fractional Black-Scholes model

How to hedge Asian options in fractional Black-Scholes model Heikki ikanmäki Jena, March 29, 211 Fractional Lévy processes 1/36 Outline of the talk 1. Introduction 2. Main results 3. Methodology 4. Conclusions

How to hedge Asian options in fractional Black-Scholes model Heikki ikanmäki Jena, March 29, 211 Fractional Lévy processes 1/36 Outline of the talk 1. Introduction 2. Main results 3. Methodology 4. Conclusions

Characterization of the Optimum

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

Optimal Selling Strategy With Piecewise Linear Drift Function

Optimal Selling Strategy With Piecewise Linear Drift Function Yan Jiang July 3, 2009 Abstract In this paper the optimal decision to sell a stock in a given time is investigated when the drift term in Black

Optimal Selling Strategy With Piecewise Linear Drift Function Yan Jiang July 3, 2009 Abstract In this paper the optimal decision to sell a stock in a given time is investigated when the drift term in Black

The value of foresight

Philip Ernst Department of Statistics, Rice University Support from NSF-DMS-1811936 (co-pi F. Viens) and ONR-N00014-18-1-2192 gratefully acknowledged. IMA Financial and Economic Applications June 11, 2018

Philip Ernst Department of Statistics, Rice University Support from NSF-DMS-1811936 (co-pi F. Viens) and ONR-N00014-18-1-2192 gratefully acknowledged. IMA Financial and Economic Applications June 11, 2018

Path Dependent British Options

Path Dependent British Options Kristoffer J Glover (Joint work with G. Peskir and F. Samee) School of Finance and Economics University of Technology, Sydney 18th August 2009 (PDE & Mathematical Finance

Path Dependent British Options Kristoffer J Glover (Joint work with G. Peskir and F. Samee) School of Finance and Economics University of Technology, Sydney 18th August 2009 (PDE & Mathematical Finance

Lecture 17. The model is parametrized by the time period, δt, and three fixed constant parameters, v, σ and the riskless rate r.

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

Randomness and Fractals

Randomness and Fractals Why do so many physicists become traders? Gregory F. Lawler Department of Mathematics Department of Statistics University of Chicago September 25, 2011 1 / 24 Mathematics and the

Randomness and Fractals Why do so many physicists become traders? Gregory F. Lawler Department of Mathematics Department of Statistics University of Chicago September 25, 2011 1 / 24 Mathematics and the

Chapter 15: Jump Processes and Incomplete Markets. 1 Jumps as One Explanation of Incomplete Markets

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

SYSM 6304: Risk and Decision Analysis Lecture 6: Pricing and Hedging Financial Derivatives

SYSM 6304: Risk and Decision Analysis Lecture 6: Pricing and Hedging Financial Derivatives M. Vidyasagar Cecil & Ida Green Chair The University of Texas at Dallas Email: M.Vidyasagar@utdallas.edu October

SYSM 6304: Risk and Decision Analysis Lecture 6: Pricing and Hedging Financial Derivatives M. Vidyasagar Cecil & Ida Green Chair The University of Texas at Dallas Email: M.Vidyasagar@utdallas.edu October

Math 6810 (Probability) Fall Lecture notes

Fall Lecture notes") Math 6810 (Probability) Fall 2012 Lecture notes Pieter Allaart University of North Texas April 16, 2013 2 Text: Introduction to Stochastic Calculus with Applications, by Fima C. Klebaner (3rd edition),

Math 6810 (Probability) Fall 2012 Lecture notes Pieter Allaart University of North Texas April 16, 2013 2 Text: Introduction to Stochastic Calculus with Applications, by Fima C. Klebaner (3rd edition),

The Forward PDE for American Puts in the Dupire Model

The Forward PDE for American Puts in the Dupire Model Peter Carr Ali Hirsa Courant Institute Morgan Stanley New York University 750 Seventh Avenue 51 Mercer Street New York, NY 10036 1 60-3765 (1) 76-988

The Forward PDE for American Puts in the Dupire Model Peter Carr Ali Hirsa Courant Institute Morgan Stanley New York University 750 Seventh Avenue 51 Mercer Street New York, NY 10036 1 60-3765 (1) 76-988

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 MAS3904. Stochastic Financial Modelling. Time allowed: 2 hours

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

1 Mathematics in a Pill 1.1 PROBABILITY SPACE AND RANDOM VARIABLES. A probability triple P consists of the following components:

1 Mathematics in a Pill The purpose of this chapter is to give a brief outline of the probability theory underlying the mathematics inside the book, and to introduce necessary notation and conventions

1 Mathematics in a Pill The purpose of this chapter is to give a brief outline of the probability theory underlying the mathematics inside the book, and to introduce necessary notation and conventions

Limit Theorems for the Empirical Distribution Function of Scaled Increments of Itô Semimartingales at high frequencies

Limit Theorems for the Empirical Distribution Function of Scaled Increments of Itô Semimartingales at high frequencies George Tauchen Duke University Viktor Todorov Northwestern University 2013 Motivation

Limit Theorems for the Empirical Distribution Function of Scaled Increments of Itô Semimartingales at high frequencies George Tauchen Duke University Viktor Todorov Northwestern University 2013 Motivation

MASSACHUSETTS INSTITUTE OF TECHNOLOGY 6.265/15.070J Fall 2013 Lecture 19 11/20/2013. Applications of Ito calculus to finance

MASSACHUSETTS INSTITUTE OF TECHNOLOGY 6.265/15.7J Fall 213 Lecture 19 11/2/213 Applications of Ito calculus to finance Content. 1. Trading strategies 2. Black-Scholes option pricing formula 1 Security

MASSACHUSETTS INSTITUTE OF TECHNOLOGY 6.265/15.7J Fall 213 Lecture 19 11/2/213 Applications of Ito calculus to finance Content. 1. Trading strategies 2. Black-Scholes option pricing formula 1 Security

The stochastic calculus

Gdansk A schedule of the lecture Stochastic differential equations Ito calculus, Ito process Ornstein - Uhlenbeck (OU) process Heston model Stopping time for OU process Stochastic differential equations

Gdansk A schedule of the lecture Stochastic differential equations Ito calculus, Ito process Ornstein - Uhlenbeck (OU) process Heston model Stopping time for OU process Stochastic differential equations

Basic Arbitrage Theory KTH Tomas Björk

Basic Arbitrage Theory KTH 2010 Tomas Björk Tomas Björk, 2010 Contents 1. Mathematics recap. (Ch 10-12) 2. Recap of the martingale approach. (Ch 10-12) 3. Change of numeraire. (Ch 26) Björk,T. Arbitrage

Basic Arbitrage Theory KTH 2010 Tomas Björk Tomas Björk, 2010 Contents 1. Mathematics recap. (Ch 10-12) 2. Recap of the martingale approach. (Ch 10-12) 3. Change of numeraire. (Ch 26) Björk,T. Arbitrage

Advanced Stochastic Processes.

Advanced Stochastic Processes. David Gamarnik LECTURE 16 Applications of Ito calculus to finance Lecture outline Trading strategies Black Scholes option pricing formula 16.1. Security price processes,

Advanced Stochastic Processes. David Gamarnik LECTURE 16 Applications of Ito calculus to finance Lecture outline Trading strategies Black Scholes option pricing formula 16.1. Security price processes,

General Examination in Macroeconomic Theory. Fall 2010

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory Fall 2010 ----------------------------------------------------------------------------------------------------------------

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory Fall 2010 ----------------------------------------------------------------------------------------------------------------

3.1 Itô s Lemma for Continuous Stochastic Variables

Lecture 3 Log Normal Distribution 3.1 Itô s Lemma for Continuous Stochastic Variables Mathematical Finance is about pricing (or valuing) financial contracts, and in particular those contracts which depend

Lecture 3 Log Normal Distribution 3.1 Itô s Lemma for Continuous Stochastic Variables Mathematical Finance is about pricing (or valuing) financial contracts, and in particular those contracts which depend

Risk Neutral Valuation

copyright 2012 Christian Fries 1 / 51 Risk Neutral Valuation Christian Fries Version 2.2 http://www.christian-fries.de/finmath April 19-20, 2012 copyright 2012 Christian Fries 2 / 51 Outline Notation Differential

copyright 2012 Christian Fries 1 / 51 Risk Neutral Valuation Christian Fries Version 2.2 http://www.christian-fries.de/finmath April 19-20, 2012 copyright 2012 Christian Fries 2 / 51 Outline Notation Differential

Computational Finance. Computational Finance p. 1

Computational Finance Computational Finance p. 1 Outline Binomial model: option pricing and optimal investment Monte Carlo techniques for pricing of options pricing of non-standard options improving accuracy

Computational Finance Computational Finance p. 1 Outline Binomial model: option pricing and optimal investment Monte Carlo techniques for pricing of options pricing of non-standard options improving accuracy

MATH3075/3975 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS

MATH307/37 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS School of Mathematics and Statistics Semester, 04 Tutorial problems should be used to test your mathematical skills and understanding of the lecture material.

MATH307/37 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS School of Mathematics and Statistics Semester, 04 Tutorial problems should be used to test your mathematical skills and understanding of the lecture material.

Martingale Approach to Pricing and Hedging

Introduction and echniques Lecture 9 in Financial Mathematics UiO-SK451 Autumn 15 eacher:s. Ortiz-Latorre Martingale Approach to Pricing and Hedging 1 Risk Neutral Pricing Assume that we are in the basic

Introduction and echniques Lecture 9 in Financial Mathematics UiO-SK451 Autumn 15 eacher:s. Ortiz-Latorre Martingale Approach to Pricing and Hedging 1 Risk Neutral Pricing Assume that we are in the basic

Risk Measures for Derivative Securities: From a Yin-Yang Approach to Aerospace Space

Risk Measures for Derivative Securities: From a Yin-Yang Approach to Aerospace Space Tak Kuen Siu Department of Applied Finance and Actuarial Studies, Faculty of Business and Economics, Macquarie University,

Risk Measures for Derivative Securities: From a Yin-Yang Approach to Aerospace Space Tak Kuen Siu Department of Applied Finance and Actuarial Studies, Faculty of Business and Economics, Macquarie University,

Insurance against Market Crashes

Insurance against Market Crashes Hongzhong Zhang a Tim Leung a Olympia Hadjiliadis b a Columbia University b The City University of New York June 29, 2012 H. Zhang, T. Leung, O. Hadjiliadis (Columbia Insurance

Insurance against Market Crashes Hongzhong Zhang a Tim Leung a Olympia Hadjiliadis b a Columbia University b The City University of New York June 29, 2012 H. Zhang, T. Leung, O. Hadjiliadis (Columbia Insurance

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS.

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS May/June 2006 Time allowed: 2 HOURS. Examiner: Dr N.P. Byott This is a CLOSED

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS May/June 2006 Time allowed: 2 HOURS. Examiner: Dr N.P. Byott This is a CLOSED

Risk Neutral Measures

CHPTER 4 Risk Neutral Measures Our aim in this section is to show how risk neutral measures can be used to price derivative securities. The key advantage is that under a risk neutral measure the discounted

CHPTER 4 Risk Neutral Measures Our aim in this section is to show how risk neutral measures can be used to price derivative securities. The key advantage is that under a risk neutral measure the discounted

Lattice (Binomial Trees) Version 1.2

Version 1.2") Lattice (Binomial Trees) Version 1. 1 Introduction This plug-in implements different binomial trees approximations for pricing contingent claims and allows Fairmat to use some of the most popular binomial

Lattice (Binomial Trees) Version 1. 1 Introduction This plug-in implements different binomial trees approximations for pricing contingent claims and allows Fairmat to use some of the most popular binomial

Are stylized facts irrelevant in option-pricing?

Are stylized facts irrelevant in option-pricing? Kyiv, June 19-23, 2006 Tommi Sottinen, University of Helsinki Based on a joint work No-arbitrage pricing beyond semimartingales with C. Bender, Weierstrass

Are stylized facts irrelevant in option-pricing? Kyiv, June 19-23, 2006 Tommi Sottinen, University of Helsinki Based on a joint work No-arbitrage pricing beyond semimartingales with C. Bender, Weierstrass

Mathematics of Finance Final Preparation December 19. To be thoroughly prepared for the final exam, you should

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Stochastic Processes and Stochastic Calculus - 9 Complete and Incomplete Market Models

Stochastic Processes and Stochastic Calculus - 9 Complete and Incomplete Market Models Eni Musta Università degli studi di Pisa San Miniato - 16 September 2016 Overview 1 Self-financing portfolio 2 Complete

Stochastic Processes and Stochastic Calculus - 9 Complete and Incomplete Market Models Eni Musta Università degli studi di Pisa San Miniato - 16 September 2016 Overview 1 Self-financing portfolio 2 Complete

EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

M5MF6. Advanced Methods in Derivatives Pricing

Course: Setter: M5MF6 Dr Antoine Jacquier MSc EXAMINATIONS IN MATHEMATICS AND FINANCE DEPARTMENT OF MATHEMATICS April 2016 M5MF6 Advanced Methods in Derivatives Pricing Setter s signature...........................................

Course: Setter: M5MF6 Dr Antoine Jacquier MSc EXAMINATIONS IN MATHEMATICS AND FINANCE DEPARTMENT OF MATHEMATICS April 2016 M5MF6 Advanced Methods in Derivatives Pricing Setter s signature...........................................

No-arbitrage theorem for multi-factor uncertain stock model with floating interest rate

Fuzzy Optim Decis Making 217 16:221 234 DOI 117/s17-16-9246-8 No-arbitrage theorem for multi-factor uncertain stock model with floating interest rate Xiaoyu Ji 1 Hua Ke 2 Published online: 17 May 216 Springer

Fuzzy Optim Decis Making 217 16:221 234 DOI 117/s17-16-9246-8 No-arbitrage theorem for multi-factor uncertain stock model with floating interest rate Xiaoyu Ji 1 Hua Ke 2 Published online: 17 May 216 Springer

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN LECTURE 6: EXTENSIONS OF BLACK AND SCHOLES RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 6: EXTENSIONS OF BLACK AND SCHOLES RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK In this section we look at some easy extensions of the Black

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 6: EXTENSIONS OF BLACK AND SCHOLES RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK In this section we look at some easy extensions of the Black

Constructing Markov models for barrier options

Constructing Markov models for barrier options Gerard Brunick joint work with Steven Shreve Department of Mathematics University of Texas at Austin Nov. 14 th, 2009 3 rd Western Conference on Mathematical

Constructing Markov models for barrier options Gerard Brunick joint work with Steven Shreve Department of Mathematics University of Texas at Austin Nov. 14 th, 2009 3 rd Western Conference on Mathematical

Risk Minimization Control for Beating the Market Strategies

Risk Minimization Control for Beating the Market Strategies Jan Večeř, Columbia University, Department of Statistics, Mingxin Xu, Carnegie Mellon University, Department of Mathematical Sciences, Olympia

Risk Minimization Control for Beating the Market Strategies Jan Večeř, Columbia University, Department of Statistics, Mingxin Xu, Carnegie Mellon University, Department of Mathematical Sciences, Olympia

American Foreign Exchange Options and some Continuity Estimates of the Optimal Exercise Boundary with respect to Volatility

American Foreign Exchange Options and some Continuity Estimates of the Optimal Exercise Boundary with respect to Volatility Nasir Rehman Allam Iqbal Open University Islamabad, Pakistan. Outline Mathematical

American Foreign Exchange Options and some Continuity Estimates of the Optimal Exercise Boundary with respect to Volatility Nasir Rehman Allam Iqbal Open University Islamabad, Pakistan. Outline Mathematical

Financial Engineering. Craig Pirrong Spring, 2006

Financial Engineering Craig Pirrong Spring, 2006 March 8, 2006 1 Levy Processes Geometric Brownian Motion is very tractible, and captures some salient features of speculative price dynamics, but it is

Financial Engineering Craig Pirrong Spring, 2006 March 8, 2006 1 Levy Processes Geometric Brownian Motion is very tractible, and captures some salient features of speculative price dynamics, but it is

Tangent Lévy Models. Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford.

Oxford-Man Institute of Quantitative Finance University of Oxford.") Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Reading: You should read Hull chapter 12 and perhaps the very first part of chapter 13.

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Asset Price Dynamics Introduction These notes give assumptions of asset price returns that are derived from the efficient markets hypothesis. Although a hypothesis,

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Asset Price Dynamics Introduction These notes give assumptions of asset price returns that are derived from the efficient markets hypothesis. Although a hypothesis,

Hedging Credit Derivatives in Intensity Based Models

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

FIN FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

Return dynamics of index-linked bond portfolios

Return dynamics of index-linked bond portfolios Matti Koivu Teemu Pennanen June 19, 2013 Abstract Bond returns are known to exhibit mean reversion, autocorrelation and other dynamic properties that differentiate

Return dynamics of index-linked bond portfolios Matti Koivu Teemu Pennanen June 19, 2013 Abstract Bond returns are known to exhibit mean reversion, autocorrelation and other dynamic properties that differentiate

King s College London

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

Multi-period mean variance asset allocation: Is it bad to win the lottery?

Multi-period mean variance asset allocation: Is it bad to win the lottery? Peter Forsyth 1 D.M. Dang 1 1 Cheriton School of Computer Science University of Waterloo Guangzhou, July 28, 2014 1 / 29 The Basic

Multi-period mean variance asset allocation: Is it bad to win the lottery? Peter Forsyth 1 D.M. Dang 1 1 Cheriton School of Computer Science University of Waterloo Guangzhou, July 28, 2014 1 / 29 The Basic

Option pricing in the stochastic volatility model of Barndorff-Nielsen and Shephard

Option pricing in the stochastic volatility model of Barndorff-Nielsen and Shephard Indifference pricing and the minimal entropy martingale measure Fred Espen Benth Centre of Mathematics for Applications

Option pricing in the stochastic volatility model of Barndorff-Nielsen and Shephard Indifference pricing and the minimal entropy martingale measure Fred Espen Benth Centre of Mathematics for Applications

STOCHASTIC CALCULUS AND DIFFERENTIAL EQUATIONS FOR PHYSICS AND FINANCE

STOCHASTIC CALCULUS AND DIFFERENTIAL EQUATIONS FOR PHYSICS AND FINANCE Stochastic calculus provides a powerful description of a specific class of stochastic processes in physics and finance. However, many

STOCHASTIC CALCULUS AND DIFFERENTIAL EQUATIONS FOR PHYSICS AND FINANCE Stochastic calculus provides a powerful description of a specific class of stochastic processes in physics and finance. However, many

1.1 Basic Financial Derivatives: Forward Contracts and Options

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

CHOICE THEORY, UTILITY FUNCTIONS AND RISK AVERSION Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Choice Theory Investments 1 / 65 Outline 1 An Introduction

13.3 A Stochastic Production Planning Model

13.3. A Stochastic Production Planning Model 347 From (13.9), we can formally write (dx t ) = f (dt) + G (dz t ) + fgdz t dt, (13.3) dx t dt = f(dt) + Gdz t dt. (13.33) The exact meaning of these expressions

13.3. A Stochastic Production Planning Model 347 From (13.9), we can formally write (dx t ) = f (dt) + G (dz t ) + fgdz t dt, (13.3) dx t dt = f(dt) + Gdz t dt. (13.33) The exact meaning of these expressions

Financial Derivatives Section 5

Financial Derivatives Section 5 The Black and Scholes Model Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of

Financial Derivatives Section 5 The Black and Scholes Model Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of

Module 10:Application of stochastic processes in areas like finance Lecture 36:Black-Scholes Model. Stochastic Differential Equation.

Stochastic Differential Equation Consider. Moreover partition the interval into and define, where. Now by Rieman Integral we know that, where. Moreover. Using the fundamentals mentioned above we can easily

Stochastic Differential Equation Consider. Moreover partition the interval into and define, where. Now by Rieman Integral we know that, where. Moreover. Using the fundamentals mentioned above we can easily

An Introduction to Point Processes. from a. Martingale Point of View

An Introduction to Point Processes from a Martingale Point of View Tomas Björk KTH, 211 Preliminary, incomplete, and probably with lots of typos 2 Contents I The Mathematics of Counting Processes 5 1 Counting

An Introduction to Point Processes from a Martingale Point of View Tomas Björk KTH, 211 Preliminary, incomplete, and probably with lots of typos 2 Contents I The Mathematics of Counting Processes 5 1 Counting

STOCHASTIC INTEGRALS

Stat 391/FinMath 346 Lecture 8 STOCHASTIC INTEGRALS X t = CONTINUOUS PROCESS θ t = PORTFOLIO: #X t HELD AT t { St : STOCK PRICE M t : MG W t : BROWNIAN MOTION DISCRETE TIME: = t < t 1

Stat 391/FinMath 346 Lecture 8 STOCHASTIC INTEGRALS X t = CONTINUOUS PROCESS θ t = PORTFOLIO: #X t HELD AT t { St : STOCK PRICE M t : MG W t : BROWNIAN MOTION DISCRETE TIME: = t < t 1

MATH 4512 Fundamentals of Mathematical Finance

MATH 4512 Fundamentals of Mathematical Finance Solution to Homework One Course instructor: Prof. Y.K. Kwok 1. Recall that D = 1 B n i=1 c i i (1 + y) i m (cash flow c i occurs at time i m years), where

MATH 4512 Fundamentals of Mathematical Finance Solution to Homework One Course instructor: Prof. Y.K. Kwok 1. Recall that D = 1 B n i=1 c i i (1 + y) i m (cash flow c i occurs at time i m years), where

Optimal robust bounds for variance options and asymptotically extreme models

Optimal robust bounds for variance options and asymptotically extreme models Alexander Cox 1 Jiajie Wang 2 1 University of Bath 2 Università di Roma La Sapienza Advances in Financial Mathematics, 9th January,

Optimal robust bounds for variance options and asymptotically extreme models Alexander Cox 1 Jiajie Wang 2 1 University of Bath 2 Università di Roma La Sapienza Advances in Financial Mathematics, 9th January,

Rough volatility models: When population processes become a new tool for trading and risk management

Rough volatility models: When population processes become a new tool for trading and risk management Omar El Euch and Mathieu Rosenbaum École Polytechnique 4 October 2017 Omar El Euch and Mathieu Rosenbaum

Rough volatility models: When population processes become a new tool for trading and risk management Omar El Euch and Mathieu Rosenbaum École Polytechnique 4 October 2017 Omar El Euch and Mathieu Rosenbaum

Lifetime Portfolio Selection: A Simple Derivation

Lifetime Portfolio Selection: A Simple Derivation Gordon Irlam (gordoni@gordoni.com) July 9, 018 Abstract Merton s portfolio problem involves finding the optimal asset allocation between a risky and a

Lifetime Portfolio Selection: A Simple Derivation Gordon Irlam (gordoni@gordoni.com) July 9, 018 Abstract Merton s portfolio problem involves finding the optimal asset allocation between a risky and a

BROWNIAN MOTION Antonella Basso, Martina Nardon

BROWNIAN MOTION Antonella Basso, Martina Nardon basso@unive.it, mnardon@unive.it Department of Applied Mathematics University Ca Foscari Venice Brownian motion p. 1 Brownian motion Brownian motion plays

BROWNIAN MOTION Antonella Basso, Martina Nardon basso@unive.it, mnardon@unive.it Department of Applied Mathematics University Ca Foscari Venice Brownian motion p. 1 Brownian motion Brownian motion plays

IEOR E4703: Monte-Carlo Simulation

IEOR E4703: Monte-Carlo Simulation Simulating Stochastic Differential Equations Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

IEOR E4703: Monte-Carlo Simulation Simulating Stochastic Differential Equations Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

Non-semimartingales in finance

Non-semimartingales in finance Pricing and Hedging Options with Quadratic Variation Tommi Sottinen University of Vaasa 1st Northern Triangular Seminar 9-11 March 2009, Helsinki University of Technology

Non-semimartingales in finance Pricing and Hedging Options with Quadratic Variation Tommi Sottinen University of Vaasa 1st Northern Triangular Seminar 9-11 March 2009, Helsinki University of Technology

LECTURE 4: BID AND ASK HEDGING

LECTURE 4: BID AND ASK HEDGING 1. Introduction One of the consequences of incompleteness is that the price of derivatives is no longer unique. Various strategies for dealing with this exist, but a useful

LECTURE 4: BID AND ASK HEDGING 1. Introduction One of the consequences of incompleteness is that the price of derivatives is no longer unique. Various strategies for dealing with this exist, but a useful

Lecture 8: The Black-Scholes theory

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Hedging with Life and General Insurance Products

Hedging with Life and General Insurance Products June 2016 2 Hedging with Life and General Insurance Products Jungmin Choi Department of Mathematics East Carolina University Abstract In this study, a hybrid

Hedging with Life and General Insurance Products June 2016 2 Hedging with Life and General Insurance Products Jungmin Choi Department of Mathematics East Carolina University Abstract In this study, a hybrid

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

How to hedge Asian options in fractional Black-Scholes model

How to hedge Asian options in fractional Black-Scholes model Heikki ikanmäki St. Petersburg, April 12, 211 Fractional Lévy processes 1/26 Outline of the talk 1. Introduction 2. Main results 3. Conclusions

How to hedge Asian options in fractional Black-Scholes model Heikki ikanmäki St. Petersburg, April 12, 211 Fractional Lévy processes 1/26 Outline of the talk 1. Introduction 2. Main results 3. Conclusions

King s College London

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

King s College London University Of London This paper is part of an examination of the College counting towards the award of a degree. Examinations are governed by the College Regulations under the authority

A note on the existence of unique equivalent martingale measures in a Markovian setting

Finance Stochast. 1, 251 257 1997 c Springer-Verlag 1997 A note on the existence of unique equivalent martingale measures in a Markovian setting Tina Hviid Rydberg University of Aarhus, Department of Theoretical

Finance Stochast. 1, 251 257 1997 c Springer-Verlag 1997 A note on the existence of unique equivalent martingale measures in a Markovian setting Tina Hviid Rydberg University of Aarhus, Department of Theoretical

PDE Methods for the Maximum Drawdown

PDE Methods for the Maximum Drawdown Libor Pospisil, Jan Vecer Columbia University, Department of Statistics, New York, NY 127, USA April 1, 28 Abstract Maximum drawdown is a risk measure that plays an

PDE Methods for the Maximum Drawdown Libor Pospisil, Jan Vecer Columbia University, Department of Statistics, New York, NY 127, USA April 1, 28 Abstract Maximum drawdown is a risk measure that plays an

Illiquidity, Credit risk and Merton s model

Illiquidity, Credit risk and Merton s model (joint work with J. Dong and L. Korobenko) A. Deniz Sezer University of Calgary April 28, 2016 Merton s model of corporate debt A corporate bond is a contingent

Illiquidity, Credit risk and Merton s model (joint work with J. Dong and L. Korobenko) A. Deniz Sezer University of Calgary April 28, 2016 Merton s model of corporate debt A corporate bond is a contingent

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 14 Lecture 14 November 15, 2017 Derivation of the

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 14 Lecture 14 November 15, 2017 Derivation of the

Conformal Invariance of the Exploration Path in 2D Critical Bond Percolation in the Square Lattice

Conformal Invariance of the Exploration Path in 2D Critical Bond Percolation in the Square Lattice Chinese University of Hong Kong, STAT December 12, 2012 (Joint work with Jonathan TSAI (HKU) and Wang

Conformal Invariance of the Exploration Path in 2D Critical Bond Percolation in the Square Lattice Chinese University of Hong Kong, STAT December 12, 2012 (Joint work with Jonathan TSAI (HKU) and Wang

Basic Concepts in Mathematical Finance

Chapter 1 Basic Concepts in Mathematical Finance In this chapter, we give an overview of basic concepts in mathematical finance theory, and then explain those concepts in very simple cases, namely in the

Chapter 1 Basic Concepts in Mathematical Finance In this chapter, we give an overview of basic concepts in mathematical finance theory, and then explain those concepts in very simple cases, namely in the

On Using Shadow Prices in Portfolio optimization with Transaction Costs

On Using Shadow Prices in Portfolio optimization with Transaction Costs Johannes Muhle-Karbe Universität Wien Joint work with Jan Kallsen Universidad de Murcia 12.03.2010 Outline The Merton problem The

On Using Shadow Prices in Portfolio optimization with Transaction Costs Johannes Muhle-Karbe Universität Wien Joint work with Jan Kallsen Universidad de Murcia 12.03.2010 Outline The Merton problem The