NCREIF Summer Conference 2012!

|

|

|

- Jody Grant

- 5 years ago

- Views:

Transcription

1 NCREIF Summer Conference 2012! July 12, 2012 Presented By:

2

")

3 Where We Are Today July April Last Year At the Worst DOW 12,641 13,160 12,763 6,626 REIT Index $65.65 $60.90 $62.19 $ YR T 1.51% 1.93% 3.33% 3.84% LIBOR (3 month).466%.47%.25% 4.056% Natural Gas $/Cu Feet $3.13 $2.89 $4.12 $9.96 OIL $85 $104 $111 $147 (2008) UNEMPLOYMENT 8.2% 8.1% 8.9% 10% CONSUMER CONFIDENCE USD/YEN (10/11) 127 U.S. Auto Sales 14.04MM 14.37MM 11.69MM 9.3MM HFF, L.P. Page 3

4

5

6 Capital Markets Overview Rankings Market Sales Volume YOY ($M) Change Market YOY% Change Manhattan $27,846,973,164 92% $27,847 Manhattan 92% $27,846,973, DC Metro** $16,156,034,409 $16,15638% DC Metro** 38% $16,156,034, Los Angeles $14,007,733,862 $14,008 88% Los Angeles 88% $14,007,733, Chicago $10,992,120,975 $10,992 86% Chicago 86% $10,992,120, Boston $7,988,925,546 $7,989 69% Boston 69% $7,988,925, Dallas $7,712,862,959 $7,713 59% Dallas 59% $7,712,862, Houston $7,396,877,211 $7,397 48% Houston 48% $7,396,877, San Francisco $7,113,190,230 63% San Francisco 63% $7,113,190, Atlanta $6,731,685,811 $6, % Atlanta 118% $6,731,685, San Diego $5,470,862,375 $5,471 77% San Diego 77% $5,470,862, No NJ $5,450,246,990 67% No NJ 67% $5,450,246, Phoenix $5,153,673,933 $5,154 62% Phoenix 62% $5,153,673, Seattle $4,901,183,389 55% Seattle 55% $4,901,183, Denver $4,777,451, % Denver 137% $4,777,451, San Jose $4,255,827,363 $4,256 49% San Jose 49% $4,255,827, NYC Boroughs $3,871,640,190 $3,872 72% NYC Boroughs 72% $3,871,640, East Bay $3,526,189,400 53% East Bay 53% $3,526,189, Miami $3,296,317,805 34% Miami 34% $3,296,317, Inland Empire $3,108,315,511 24% Inland Empire 24% $3,108,315, Orange Co $3,003,744,347-4% -4% Orange Co $3,003,744,3 **DC, DC MD Burbs & DC VA Burbs combined

7

8

9

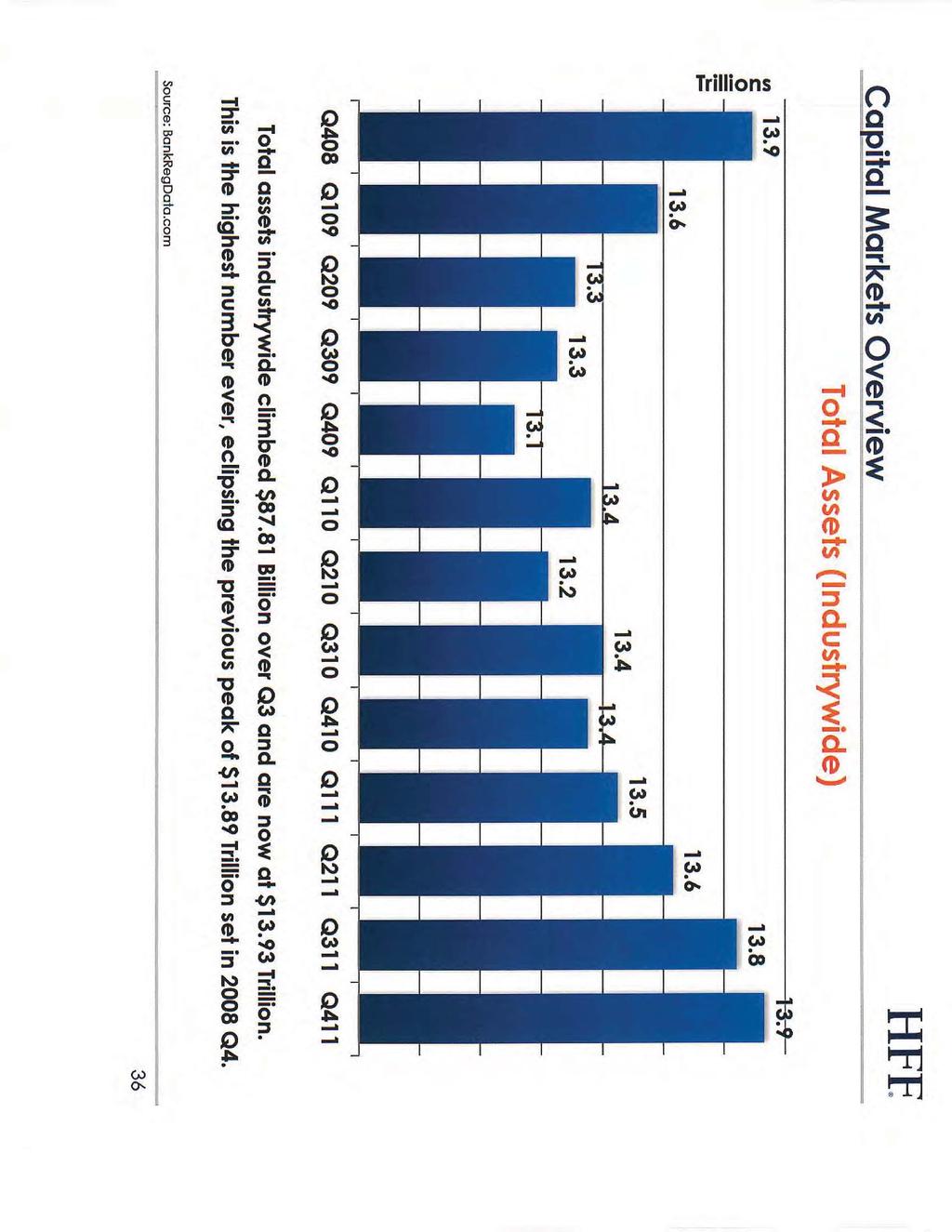

10

11 Capital Markets Overview CMBS Overview Volume was well on way to reach $50 Billion until July when the following occurred: US downgrade S&P pulled rating on Goldman European volatility Result: Rated bonds % of Total 01/11 08/11 11/11 03/12 AAA 70% BBB 6-11% Unrated 6% 17% 19% 19% 18-20% 1

12

13 Capital Markets Overview All Cash IRR Yield Targets by Asset Class 15% 14% 13% 12% 11% 10% 9% 8% 7% 6% 5% 4% 7.5% 7.5% 6.5% 9.5% Office 9.5% 7.5% 9% 6.5% Initial Yield: 6.0% - 6.5% 5.5% - 6.5% 4.5% - 5.0% 6.0% - 6.5% 4.0% - 6.0% Source: HFF, April % 6.5% 8% 11+% 9% Grocery/Discount Anchored Retail 7.5% 9% 7.5% Multi-Housing 11+% 9% 7.5% 6.5%% 9.5% 8% Industrial 11+% 9.5% 11.75% 10.75% 13.5% 12% Hotel 15+% 13.5% 2

14 Capital Markets Overview Big Themes for 2012 Continue to have flight capital to US as evidenced by fund flows into treasuries, money market funds, etc. Capital reallocating from financial assets to hard assets. Real Estate is favored asset class on a risk adjusted basis as compared to stocks, bonds and other alternatives such as private equity, hedge funds and commodities. The above factors will result in abundant capital for CRE in 2012 across both the debt and equity markets. We are expecting allocations to increase 20%-30% over 2011 levels. Equity will be plentiful across all major providers in 2012 including foreign, institutional (state plans/endowment), public REIT, private REIT, HNW investors. 3

15 Capital Markets Overview Debt capital from banks and insurance companies will also be abundant, although underwriting will remain measured. The CMBS market will stabilize and could easily reach $ 50 Billion not withstanding the negative commentary at present. Size will not be a limiting factor in 2012 either for a single asset or portfolios. Portfolio premium will likely re-emerge only for core/core plus assets which would allow buyers to gain scale in a given market(s)/product type. Capital will most certainly continue migrating up the risk curve either by market (Gateway/Primary/Secondary) or by project risk (Stabilized/Unstabilized). 4

16 Capital Markets Overview The underlying fiscal infrastructure of a state/ municipality/region will continue to gain in importance in investor allocation models. Fiscal Infrastructure being defined as the financial health of the state/city, taxation policies, historical/projected job and population growth, and cost of living. CRE pricing is highly correlated not only to interest rates but also to public market metrics including the public REIT sector and the corporate bond market. The institutional equity market uses the BBB corporate as a cap rate benchmark, and the insurance company industry looks to the BBB-AAA corporate bond pricing as its deployment benchmark. 5

17 Capital Markets Overview There will be no scarcity of product coming to the market; therefore, we expect transactional volume to approximate the level of $250-$300 Billion for The one exception being core product in gateway markets which could easily garner scarcity premiums in price. Foreign banks will continue to sell down CRE assets in larger denominations/portfolios. Domestic banks will likely continue a one-off asset sale strategy in general. 6

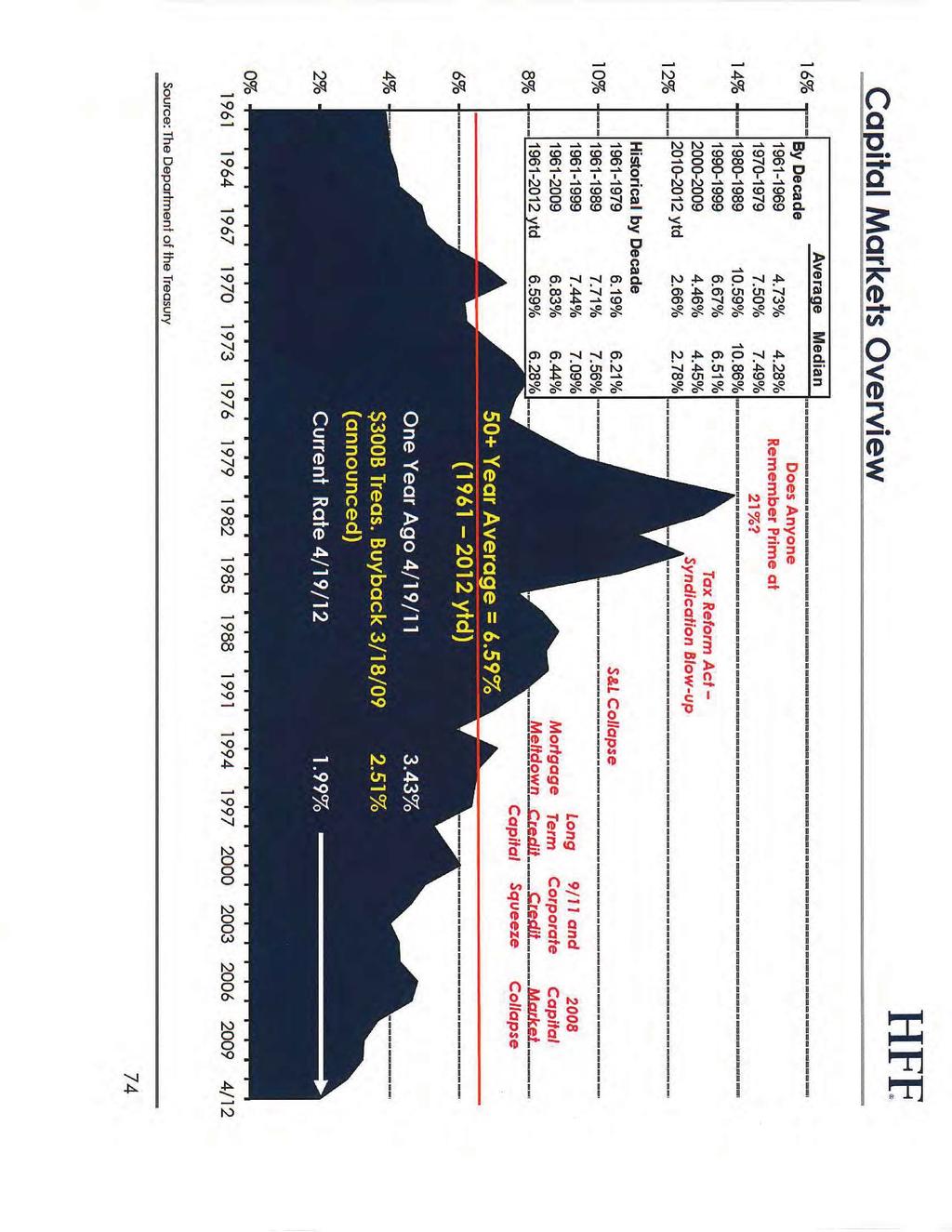

18 Capital Markets Overview HFF continues to emphasize the risk of rising interest rates relative to a hold/sell strategy decision. We believe cap rates and interest rates are correlated, and our regression analysis concludes NOIs must increase 10-15% to offset a 100 basis point move in interest rate/cap rates. Once again, 2012, like 2011, will be a nearly perfect capital markets environment given the abundance and low cost of available capital. HFF Recommendation: Consume capital and integrate a smart ALM strategy. 7

Housing Affordability Index at the highest level ever Washington DC Metro 5th largest economy in the U.S.")

19 What the Pragmatists Know: End of Q US best six months of job growth since 2006 Stock market up 9% YTD (April 27) 3% (June 13) Unemployment is at a 3 year low went up in May Oil prices have fallen 7% YTD and 29% since all time high in 2008 (Nov 44%) Housing Affordability Index at the highest level ever Washington DC Metro 5th largest economy in the U.S. 1st nationally in job growth last decade 2nd largest employer of technology workers in U.S. Nation s most-educated workforce More than 50 colleges and universities Highest per capita government R and D - Global More than 530 weekly international non-stop flights More than 1,000 international firms from 50 countries Most Inc. 500 fastest growing companies Wealthiest households in the country #1 U.S port of Baltimore cargo surge Wall St. moves to Pennsylvania Ave: record 4.3MM SF of Net Absorption 2012 Actual and feared U.S. austerity and sequestration, BRAC lowest demand since 2002 HFF, L.P. Page 2

and Education/Health (9,700) Historic average is 36M 1990-2010 expected to resume in 2014 Job growth slowed in")

20 DC the Only Major East Coast Market that did not have a Recession Employment Growth VS DC Metro US -.8% US 1.4% DC 1.5% DC 1% Most growth in Leisure/Hospitality (12,500) and Education/Health (9,700) Historic average is 36M expected to resume in 2014 Job growth slowed in 2011: Tsunami. Greece, Debt Crisis

2010 Regional Overview DC (31 Deals) $3.4B $520 psf average MD (17 Deals) $0.")

21 Historical Investment Sales Volume: Washington, DC Metro Area (Office) Approx. $8.2B in regional investment sales in 2011, going into 2012 with $2.6B under contract 2011 Core: 60% Core Plus: 26% Value Add: 14% 57 Deals inside the beltway (63% volume) 2010 Regional Overview DC (31 Deals) $3.4B $520 psf average MD (17 Deals) $0.4B $168 psf average VA (59 Deals) $2.2B $227 psf average 107 Deals Total, $6.0B 2011 Regional Overview DC (34 Deals) $3.9B $449 psf average MD (30 Deals) $0.9B $198 psf average VA (41 Deals) $3.4B $272 psf average 105 Deals Total, $8.2B - Peak pricing in DC and MD in deals outside the beltway (37% volume) 8

22 Historical DC Metro Office New Construction Volume Millions SF % Total Supply 4.54% 3.50% 3.69% 1.67% 2.09% 1.99% 2.65% 2.46% 2.00% 1.24% 0.98% 0.54% 0.68% *3.95 number for 2011 includes 1.75 msf Mark Center 12

Capital Market Update. February 10, 2011 Marc Louargand, Ph.D., CRE, FRICS Principal SALTASH PARTNERS LLC investing in American ingenuity

Capital Market Update February 10, 2011 Marc Louargand, Ph.D., CRE, FRICS Principal SALTASH PARTNERS LLC investing in American ingenuity A Brief Tour of the Capital Market What s happened in the past year?

Capital Market Update February 10, 2011 Marc Louargand, Ph.D., CRE, FRICS Principal SALTASH PARTNERS LLC investing in American ingenuity A Brief Tour of the Capital Market What s happened in the past year?

Office-Using Jobs and Net Migration Point to Continued Strength

October 20, 2017 Office-Using Jobs and Net Migration Point to Continued Strength Key Takeaways Secondary Sunbelt office markets are priced to offer attractive, risk-adjusted returns relative to the Gateway²

October 20, 2017 Office-Using Jobs and Net Migration Point to Continued Strength Key Takeaways Secondary Sunbelt office markets are priced to offer attractive, risk-adjusted returns relative to the Gateway²

Emerging Trends in Real Estate 2014

Canada Emerging Trends in Real Estate 2014 Emerging Trends is the industry s most predictive forecast 35th annual outlook Based on over 1,000 interviews and surveys of industry leaders Sponsored by PwC

Canada Emerging Trends in Real Estate 2014 Emerging Trends is the industry s most predictive forecast 35th annual outlook Based on over 1,000 interviews and surveys of industry leaders Sponsored by PwC

20 th Annual LA/OC Market Trends Seminar

20 th Annual LA/OC Market Trends Seminar Everett (Allen) Greer January 24, 2013 Goals of Presentation Disclaimers Market Drivers Economy, Interest Rates Financial Regulations (Dodd-Frank) Capital Market

20 th Annual LA/OC Market Trends Seminar Everett (Allen) Greer January 24, 2013 Goals of Presentation Disclaimers Market Drivers Economy, Interest Rates Financial Regulations (Dodd-Frank) Capital Market

CBRE CAP RATE SURVEY. A CBRE Publication. First Half Click to Enter

CBRE CAP RATE SURVEY A CBRE Publication In This Issue: pg 2 pg 8 pg 17 pg 26 pg 36 pg 41 pg 44 Click to Enter United States The 10-year Treasury (UST) was measurably lower than 2% from April 2012 through

CBRE CAP RATE SURVEY A CBRE Publication In This Issue: pg 2 pg 8 pg 17 pg 26 pg 36 pg 41 pg 44 Click to Enter United States The 10-year Treasury (UST) was measurably lower than 2% from April 2012 through

2015 REAL ESTATE ECONOMIC FORECAST The National Economy and What It Means For Real Estate

2015 REAL ESTATE ECONOMIC FORECAST The National Economy and What It Means For Real Estate February 5, 2015 Jeanette I. Rice Kentucky Chapter National economy in great shape for 2015 Creating excellent

2015 REAL ESTATE ECONOMIC FORECAST The National Economy and What It Means For Real Estate February 5, 2015 Jeanette I. Rice Kentucky Chapter National economy in great shape for 2015 Creating excellent

Captain CREDIT Crunch

Captain CREDIT Crunch April 9, 2008 Presented by: Patrick Devereaux Senior Director The Times They Are A-Changin Post Credit Crunch Investment Market Fundamentals Of Commercial Real Estate Remain Strong

Captain CREDIT Crunch April 9, 2008 Presented by: Patrick Devereaux Senior Director The Times They Are A-Changin Post Credit Crunch Investment Market Fundamentals Of Commercial Real Estate Remain Strong

WA S H I N G TO N / BALT I M O R E

D E L T A A S S O C I A T E S WA S H I N G TO N / BALT I M O R E R E A L E S T A T E M A R K E T O V E R V I E W MULTIFAMILY MARKET OVERVIEW 0 9. 2 9. 2 0 1 5 B y W i l l i a m R i c h, C R E P r e s i

D E L T A A S S O C I A T E S WA S H I N G TO N / BALT I M O R E R E A L E S T A T E M A R K E T O V E R V I E W MULTIFAMILY MARKET OVERVIEW 0 9. 2 9. 2 0 1 5 B y W i l l i a m R i c h, C R E P r e s i

CAPITALIZATION RATES BY PROPERTY TYPE

RATES BY PROPERTY TYPE MID-YEAR 2014 0 RATES BY ASSET TYPE MID-YEAR 2014 O V E R V I E W Capital continues to flow steadily into the U.S. real estate market, as both domestic and foreign investors increase

RATES BY PROPERTY TYPE MID-YEAR 2014 0 RATES BY ASSET TYPE MID-YEAR 2014 O V E R V I E W Capital continues to flow steadily into the U.S. real estate market, as both domestic and foreign investors increase

ZipRealty, Inc. Supplemental Data Reclassification of Consolidated Statement of Operations

Reclassification of Consolidated Statement of Operations Effective January 1, 2007, for income statement presentation purposes, we have reclassified sales support and marketing expenses from general and

Reclassification of Consolidated Statement of Operations Effective January 1, 2007, for income statement presentation purposes, we have reclassified sales support and marketing expenses from general and

U.S. Investment Outlook

U.S. Investment Outlook Quarterly Investor Research update Q2 2015 U.S. Investment overview 37% 21% 15% 15% U.S. cities dominating global investment activity Top 20 Cities for Transactional Volumes H1

U.S. Investment Outlook Quarterly Investor Research update Q2 2015 U.S. Investment overview 37% 21% 15% 15% U.S. cities dominating global investment activity Top 20 Cities for Transactional Volumes H1

US CAPITAL MARKETS REPORT

US CAPITAL MARKETS REPORT Capitalization Rates By Property Type Fall 2016 US Capital Markets Report Capitalization Rates By Asset Type OVERVIEW Year-to-date investment sales volume lagged on a year-over-year

US CAPITAL MARKETS REPORT Capitalization Rates By Property Type Fall 2016 US Capital Markets Report Capitalization Rates By Asset Type OVERVIEW Year-to-date investment sales volume lagged on a year-over-year

TEXAS MULTIFAMILY FOLLOW THE MONEY. THE CAPITAL MARKETS PERSPECTIVE Jeanette I. Rice, Americas Head of Investment Research February 12, 2016

TEXAS MULTIFAMILY FOLLOW THE MONEY THE CAPITAL MARKETS PERSPECTIVE Jeanette I. Rice, Americas Head of Investment Research February 12, 2016 MULTIFAMILY ON TOP OF THE MARKET 2 MONEY IS FOLLOWING MULTIFAMILY

TEXAS MULTIFAMILY FOLLOW THE MONEY THE CAPITAL MARKETS PERSPECTIVE Jeanette I. Rice, Americas Head of Investment Research February 12, 2016 MULTIFAMILY ON TOP OF THE MARKET 2 MONEY IS FOLLOWING MULTIFAMILY

CAPITAL MARKETS UPDATE. Suburban Office: Is this the Next Play?

CAPITAL MARKETS UPDATE Suburban Office: Is this the Next Play? October 2016 Investment Thesis Background Suburban office product has lagged the property recovery cycle. Most of the lag is the result of

CAPITAL MARKETS UPDATE Suburban Office: Is this the Next Play? October 2016 Investment Thesis Background Suburban office product has lagged the property recovery cycle. Most of the lag is the result of

Perspectives JAN Market Preview: Real Estate

Perspectives JAN 2019 2019 Market Preview: Real Estate NAVIGATING THROUGH A LATE MARKET CYCLE The real estate sector managed to pull off another strong year in 2018, delivering a total return of 8.35%,

Perspectives JAN 2019 2019 Market Preview: Real Estate NAVIGATING THROUGH A LATE MARKET CYCLE The real estate sector managed to pull off another strong year in 2018, delivering a total return of 8.35%,

Wall Street and Commercial Real Estate

Wall Street and Commercial Real Estate Everett Allen Greer Director of Research October 22, 28 Goals of Presentation Two Fundamentals of Real Estate CMBS / CDO / REIT Industries Size / Impact of Capital

Wall Street and Commercial Real Estate Everett Allen Greer Director of Research October 22, 28 Goals of Presentation Two Fundamentals of Real Estate CMBS / CDO / REIT Industries Size / Impact of Capital

Investing in a Volatile Market

Investing in a Volatile Market RCLCO Institutional Advisory Services March 2016 Robert Charles Lesser & Co. Real Estate Advisors rclco.com Price Index, All Equity REITs % REIT Markets are Recently Volatile:

Investing in a Volatile Market RCLCO Institutional Advisory Services March 2016 Robert Charles Lesser & Co. Real Estate Advisors rclco.com Price Index, All Equity REITs % REIT Markets are Recently Volatile:

Strong conclusion to 2015, some caution ahead in 2016

MARKETVIEW U.S. Office, Q4 215 Strong conclusion to 215, some caution ahead in 216 Vacancy Rate 13.1% Lease Rate $29.7 PSF Net Absorption 19.4 MSF Completions 12.1 MSF *Arrows indicate change from previous

MARKETVIEW U.S. Office, Q4 215 Strong conclusion to 215, some caution ahead in 216 Vacancy Rate 13.1% Lease Rate $29.7 PSF Net Absorption 19.4 MSF Completions 12.1 MSF *Arrows indicate change from previous

COMMERCIAL REAL ESTATE PRICING LEAPS FORWARD IN AUGUST BOOSTED BY STRONG NET ABSORPTION IN FIRST HALF OF YEAR

CCRSI RELEASE OCTOBER 2012 (With data through AUGUST 2012) COMMERCIAL REAL ESTATE PRICING LEAPS FORWARD IN AUGUST BOOSTED BY STRONG NET ABSORPTION IN FIRST HALF OF YEAR CCRSI INDICES POST STRONGEST GAINS

CCRSI RELEASE OCTOBER 2012 (With data through AUGUST 2012) COMMERCIAL REAL ESTATE PRICING LEAPS FORWARD IN AUGUST BOOSTED BY STRONG NET ABSORPTION IN FIRST HALF OF YEAR CCRSI INDICES POST STRONGEST GAINS

The Five Retail Trends to Watch in January 14, 2015

The Five Retail Trends to Watch in 2015 January 14, 2015 U.S. ECONOMIC TRENDS Inflation Adjusted Crude Oil Prices Fall Below Long-Term Average Price per Barrel (Nov. 2014 Dollars) $160 $120 $80 $40 $0

The Five Retail Trends to Watch in 2015 January 14, 2015 U.S. ECONOMIC TRENDS Inflation Adjusted Crude Oil Prices Fall Below Long-Term Average Price per Barrel (Nov. 2014 Dollars) $160 $120 $80 $40 $0

Presented By: Doug Herzbrun Managing Director January 26, 2000

NORTHWEST CONSTRUCTION CONSUMER COUNCIL Presented By: Doug Herzbrun Managing Director January 26, 2000 U.S. Real Estate Capital Markets Overview INVESTABLE UNIVERSE $1.1 TRILLION 3 INVESTABLE UNIVERSE

NORTHWEST CONSTRUCTION CONSUMER COUNCIL Presented By: Doug Herzbrun Managing Director January 26, 2000 U.S. Real Estate Capital Markets Overview INVESTABLE UNIVERSE $1.1 TRILLION 3 INVESTABLE UNIVERSE

RETAIL SECTOR CONTINUES TO IMPROVE, DESPITE DROP IN CONSUMER CONFIDENCE

RETAIL MARKET REPORT: 3Q RETAIL SECTOR CONTINUES TO IMPROVE, DESPITE DROP IN CONSUMER CONFIDENCE KEY INDICATORS: Key retail market indicators continue to send mixed signals. Monthly retail sales (ex: motor

RETAIL MARKET REPORT: 3Q RETAIL SECTOR CONTINUES TO IMPROVE, DESPITE DROP IN CONSUMER CONFIDENCE KEY INDICATORS: Key retail market indicators continue to send mixed signals. Monthly retail sales (ex: motor

The U.S. and California Is The Recovery Here at Last? UCLA Anderson School of

The U.S. and California Is The Recovery Here at Last? Jerry Nickelsburg Senior Economist UCLA Anderson Forecast State of the County January 20, 2010 SEPTEMBER 2008 In September 2008 Financial Markets Stopped

The U.S. and California Is The Recovery Here at Last? Jerry Nickelsburg Senior Economist UCLA Anderson Forecast State of the County January 20, 2010 SEPTEMBER 2008 In September 2008 Financial Markets Stopped

Emerging Trends in Real Estate Navigating at Altitude

Emerging Trends in Real Estate 2018 Navigating at Altitude Emerging Trends in Real Estate 2018 Navigating at Altitude We are in a long cycle, not in boom/bust. The key to the next few years is to expand

Emerging Trends in Real Estate 2018 Navigating at Altitude Emerging Trends in Real Estate 2018 Navigating at Altitude We are in a long cycle, not in boom/bust. The key to the next few years is to expand

US Hotel Industry Overview. Chris Crenshaw

US Hotel Industry Overview Chris Crenshaw ccrenshaw@str.com July 2014 (12 MMA): All Signs Point To A Sellers Market % Change Room Supply* 1.8 bn 0.8% Room Demand* 1.1 bn 3.4% Occupancy 63 % 2.6% A.D.R.*

US Hotel Industry Overview Chris Crenshaw ccrenshaw@str.com July 2014 (12 MMA): All Signs Point To A Sellers Market % Change Room Supply* 1.8 bn 0.8% Room Demand* 1.1 bn 3.4% Occupancy 63 % 2.6% A.D.R.*

Metro Washington, DC State of the Market

Metro Washington, DC State of the Market Q1 2016 U.S. office clock San Francisco Peninsula Silicon Valley Houston Dallas, San Francisco Austin Nashville Peaking phase Falling phase Denver, Minneapolis,

Metro Washington, DC State of the Market Q1 2016 U.S. office clock San Francisco Peninsula Silicon Valley Houston Dallas, San Francisco Austin Nashville Peaking phase Falling phase Denver, Minneapolis,

Metropolitan Area Statistics (4Q 2012)

") Metropolitan Area Statistics (4Q 2012) Apartment Completions 4Q 2011 4Q 2012 % Chg. Atlanta 490 288-41% Boston 678 995 47% Chicago 506 711 41% Cleveland 4 13 225% Columbus 255 322 26% Dallas-Ft. Worth

Metropolitan Area Statistics (4Q 2012) Apartment Completions 4Q 2011 4Q 2012 % Chg. Atlanta 490 288-41% Boston 678 995 47% Chicago 506 711 41% Cleveland 4 13 225% Columbus 255 322 26% Dallas-Ft. Worth

State Of The U.S. Industrial Market: 2017 Q2

State Of The U.S. Industrial Market: 2017 Q2 Copyright 2017 CoStar Realty Information, Inc. No reproduction or distribution without permission. The following information includes projections and analyses

State Of The U.S. Industrial Market: 2017 Q2 Copyright 2017 CoStar Realty Information, Inc. No reproduction or distribution without permission. The following information includes projections and analyses

S&P/Case-Shiller Home Price Indices

Home Prices Off to a Dismal Start in 2011 According to the S&P/Case-Shiller Home Price Indices New York, March 29, 2011 Data through January 2011, released today by Standard & Poor s for its S&P/Case-Shiller

Home Prices Off to a Dismal Start in 2011 According to the S&P/Case-Shiller Home Price Indices New York, March 29, 2011 Data through January 2011, released today by Standard & Poor s for its S&P/Case-Shiller

Office. Office. IRR Viewpoint 2015

IRR Viewpoint 05 Above: Designed in 95 in the Art Deco style by architect Timothy Pflueger as the Pacific Telephone and Telegraph Building, 40 New Montgomery Street, San Francisco, CA has been the subject

IRR Viewpoint 05 Above: Designed in 95 in the Art Deco style by architect Timothy Pflueger as the Pacific Telephone and Telegraph Building, 40 New Montgomery Street, San Francisco, CA has been the subject

Hotels & Hospitality Group

Hotels & Hospitality Group January 2018 North America Hotel Investor Sentiment Survey North America Hotel Investor Sentiment Survey Renewed freshness and energy in hotel investment community Despite entering

Hotels & Hospitality Group January 2018 North America Hotel Investor Sentiment Survey North America Hotel Investor Sentiment Survey Renewed freshness and energy in hotel investment community Despite entering

Multifamily Outlook. United States Fall 2014

Multifamily Outlook United States Fall 2014 Markets continue to perform at peak levels... with nearterm, pocketed softening on the horizon On the heels of seven quarters of peak-level investment sale volumes,

Multifamily Outlook United States Fall 2014 Markets continue to perform at peak levels... with nearterm, pocketed softening on the horizon On the heels of seven quarters of peak-level investment sale volumes,

Emerging Trends in Real Estate Sustaining Momentum but Taking Nothing for Granted

Emerging Trends in Real Estate 2015 Sustaining Momentum but Taking Nothing for Granted DALLAS November 6, 2014 36th annual outlook 1,400+ interviews and surveys of industry leaders Rewind: 2014 Emerging

Emerging Trends in Real Estate 2015 Sustaining Momentum but Taking Nothing for Granted DALLAS November 6, 2014 36th annual outlook 1,400+ interviews and surveys of industry leaders Rewind: 2014 Emerging

PAYROLL JOB GROWTH Selected Large Metro Areas 12 Months Ending August 2017

THE ECONOMY P AY R O L L J O B S ( T H O U S A N D S ) PAYROLL JOB GROWTH Selected Large Metro Areas 12 Months Ending August 2017 160 140 120 100 80 67 60 40 20 0 NY DFW Atl LA Basin Was Bos South FL Hou

THE ECONOMY P AY R O L L J O B S ( T H O U S A N D S ) PAYROLL JOB GROWTH Selected Large Metro Areas 12 Months Ending August 2017 160 140 120 100 80 67 60 40 20 0 NY DFW Atl LA Basin Was Bos South FL Hou

University of Tokyo Center for Advanced Research in Finance (CARF) Workshop on Real Estate Finance March 26, 2018

Workshop on Real Estate Finance March 26, 2018") University of Tokyo Center for Advanced Research in Finance (CARF) Workshop on Real Estate Finance March 26, 2018 Analytical Tools & Recent Findings: Selected Research Projects of the MIT Real Estate Price

University of Tokyo Center for Advanced Research in Finance (CARF) Workshop on Real Estate Finance March 26, 2018 Analytical Tools & Recent Findings: Selected Research Projects of the MIT Real Estate Price

The Vision Series,

The Vision Series, 212-213 The Washington Area Economy: Transitioning From Federal Dependency to a Global Business Base Stephen S. Fuller, Ph.D. Dwight Schar Faculty Chair and University Professor Director,

The Vision Series, 212-213 The Washington Area Economy: Transitioning From Federal Dependency to a Global Business Base Stephen S. Fuller, Ph.D. Dwight Schar Faculty Chair and University Professor Director,

Commercial Real Estate Outlook June Must Own Property Names to Buy During Interest Rate Fears

Jonathan Litt Founder & CEO Must Own Property Names to Buy During Interest Rate Fears REITs have sold off 9.5% since their peak in mid-may on fears of rising interest rates. Historically, sell-offs related

Jonathan Litt Founder & CEO Must Own Property Names to Buy During Interest Rate Fears REITs have sold off 9.5% since their peak in mid-may on fears of rising interest rates. Historically, sell-offs related

SOUTHERN NEVADA 2015 ECONOMIC OUTLOOK

SOUTHERN NEVADA 2015 ECONOMIC OUTLOOK NAIOP Washington D.C. Legislative Retreat February 9-11, 2015 Prepared by: ECONOMIC OVERVIEW 2 Nevada job recovery from Great Recession after 90 months. Nevada Recession

SOUTHERN NEVADA 2015 ECONOMIC OUTLOOK NAIOP Washington D.C. Legislative Retreat February 9-11, 2015 Prepared by: ECONOMIC OVERVIEW 2 Nevada job recovery from Great Recession after 90 months. Nevada Recession

AUSTIN: MOVING FORWARD

AUSTIN: MOVING FORWARD Angelos Angelou 32 nd Annual Austin Forecast January 26 th, 2017 1 TODAY S AGENDA o2016: The Year in Review oaustin s Economic Drivers ochallenges to Overcome o2017-18 Forecast 2

AUSTIN: MOVING FORWARD Angelos Angelou 32 nd Annual Austin Forecast January 26 th, 2017 1 TODAY S AGENDA o2016: The Year in Review oaustin s Economic Drivers ochallenges to Overcome o2017-18 Forecast 2

L&B Realty Advisors, LLP Client Focused. Performance Driven. US Property Investment 5 Ws and 1 H

L&B Realty Advisors, LLP Client Focused. Performance Driven US Property Investment 5 Ws and 1 H November 2017 Presenter Biography Eric R. Smith, Executive Vice President, Business Development Mr. Smith

L&B Realty Advisors, LLP Client Focused. Performance Driven US Property Investment 5 Ws and 1 H November 2017 Presenter Biography Eric R. Smith, Executive Vice President, Business Development Mr. Smith

Struggling to Escape the Fallout of the Great Recession MARISA Di NATALE, MANAGING DIRECTOR

Struggling to Escape the Fallout of the Great Recession MARISA Di NATALE, MANAGING DIRECTOR FROM MOODY S ECONOMY.COM Broad-Based Slowing Across the Nation Total employment excluding federal government,

Struggling to Escape the Fallout of the Great Recession MARISA Di NATALE, MANAGING DIRECTOR FROM MOODY S ECONOMY.COM Broad-Based Slowing Across the Nation Total employment excluding federal government,

State of the U.S. Multifamily Market. Q Review and Forecast

State of the U.S. Multifamily Market Q1 2015 Review and Forecast Agenda Economy Leasing Fundamentals Rent and NOI Trends Single-Family Market Capital Markets Economy page 3 GDP Growth Contributions To

State of the U.S. Multifamily Market Q1 2015 Review and Forecast Agenda Economy Leasing Fundamentals Rent and NOI Trends Single-Family Market Capital Markets Economy page 3 GDP Growth Contributions To

Fisher Center-Real Estate & Economics Symposium. November 19 th, 2018

Fisher Center-Real Estate & Economics Symposium November 19 th, 2018 SALES VOLUME AND PRIMARY MARKET CAP RATES 12-MONTHTOTALS Demand for product in major markets has driven cap rate compression, and forced

Fisher Center-Real Estate & Economics Symposium November 19 th, 2018 SALES VOLUME AND PRIMARY MARKET CAP RATES 12-MONTHTOTALS Demand for product in major markets has driven cap rate compression, and forced

U.S. Economic and Medical Office Market Overview and Outlook. November, 2014

2014 U.S. Economic and Medical Office Market Overview and Outlook November, 2014 Economic & Demographic Overview U.S. GDP Growth and Health Care Spending Trends GDP Health Care Expenditures Annualized

2014 U.S. Economic and Medical Office Market Overview and Outlook November, 2014 Economic & Demographic Overview U.S. GDP Growth and Health Care Spending Trends GDP Health Care Expenditures Annualized

Wall Street and Commercial Real Estate

Wall Street and Commercial Real Estate Everett (Allen) Greer April 26, 2012 Los Angeles, CA City National Bank Goals of Presentation Disclaimers Market Drivers Economy, Interest Rates Financial Regulations

Wall Street and Commercial Real Estate Everett (Allen) Greer April 26, 2012 Los Angeles, CA City National Bank Goals of Presentation Disclaimers Market Drivers Economy, Interest Rates Financial Regulations

MEGATREND 1: WAGE GROWTH IS FLAT, BUT DISCRETIONARY INCOME IS UP

MEGATRENDS MegaTrends 1. Wage growth is flat, but discretionary income is up 2. The regional economy is recovering but not yet recovered 3. Consumer behavior is changing 4. Tenant behavior is changing

MEGATRENDS MegaTrends 1. Wage growth is flat, but discretionary income is up 2. The regional economy is recovering but not yet recovered 3. Consumer behavior is changing 4. Tenant behavior is changing

Was it all for N 0 u g h t? The 00 Decade and the Year Ahead. Tony Pierson Cornerstone Real Estate Advisers LLC. Real Estate Conference

Disclaimer This presentation is not intended to be and does not constitute investment advice. This is provided as an accommodation and shall not be relied upon as investment advice. This presentation includes

Disclaimer This presentation is not intended to be and does not constitute investment advice. This is provided as an accommodation and shall not be relied upon as investment advice. This presentation includes

Washington Area Economy: Performance and Outlook

Washington Area Economy: Performance and Outlook Presentation to: Greater Washington Association of Financial Professionals Mark C. White, Ph.D. Deputy Director Center for Regional Analysis Schar School

Washington Area Economy: Performance and Outlook Presentation to: Greater Washington Association of Financial Professionals Mark C. White, Ph.D. Deputy Director Center for Regional Analysis Schar School

U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE

AEW RESEARCH U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE Q2 2018 AEW RESEARCH U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE Q 2 2018 1 Prepared by AEW Research, June 2018 This material is intended for information

AEW RESEARCH U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE Q2 2018 AEW RESEARCH U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE Q 2 2018 1 Prepared by AEW Research, June 2018 This material is intended for information

CCRSI RELEASE APRIL 2014 (With data through FEBRUARY 2014)

") CCRSI RELEASE APRIL 2014 (With data through FEBRUARY 2014) PRICE MOMENTUM FOR COMMERCIAL REAL ESTATE CONTINUED TO BUILD IN FEBRUARY REFLECTING BROAD RECOVERY IN MARKET FUNDAMENTALS AND PRICING, EQUAL-WEIGHTED

CCRSI RELEASE APRIL 2014 (With data through FEBRUARY 2014) PRICE MOMENTUM FOR COMMERCIAL REAL ESTATE CONTINUED TO BUILD IN FEBRUARY REFLECTING BROAD RECOVERY IN MARKET FUNDAMENTALS AND PRICING, EQUAL-WEIGHTED

Addendum to: The Community Reinvestment Act: A Welcome Anomaly in the Foreclosure Crisis

Addendum to: The Community Reinvestment Act: A Welcome Anomaly in the Foreclosure Crisis Relevant Figures Recalculated to Include CRA Bank Affiliate Lending January 14, 2008 Prepared by: Attorneys at Law

Addendum to: The Community Reinvestment Act: A Welcome Anomaly in the Foreclosure Crisis Relevant Figures Recalculated to Include CRA Bank Affiliate Lending January 14, 2008 Prepared by: Attorneys at Law

Emerging Trends in Real Estate 2016

Emerging Trends in Real Estate 2016 PwC ULI 12 Month Outlook on Trends 37 th Edition 1,800+ Real Estate leaders surveyed 75 Cities Profitability outlook 2010 17.7% 60.6% 21.6% Abysmal to Poor Fair Good

Emerging Trends in Real Estate 2016 PwC ULI 12 Month Outlook on Trends 37 th Edition 1,800+ Real Estate leaders surveyed 75 Cities Profitability outlook 2010 17.7% 60.6% 21.6% Abysmal to Poor Fair Good

Regional Snapshot: The Cost of Living in Metro Atlanta

Regional Snapshot: The Cost of Living in Metro Atlanta Photo by rawpixel.com on Unsplash Atlanta Regional Commission, February 2018 For more information, contact: cdegiulio@atlantaregional.org In Summary

Regional Snapshot: The Cost of Living in Metro Atlanta Photo by rawpixel.com on Unsplash Atlanta Regional Commission, February 2018 For more information, contact: cdegiulio@atlantaregional.org In Summary

S&P/Case-Shiller Home Price Indices

Annual Rates of Change Continue to Improve According to the S&P/Case-Shiller Home Price Indices New York, October 25, 2011 Data through August 2011, released today by S&P Indices for its S&P/Case-Shiller

Annual Rates of Change Continue to Improve According to the S&P/Case-Shiller Home Price Indices New York, October 25, 2011 Data through August 2011, released today by S&P Indices for its S&P/Case-Shiller

HIGH AND WIDE: INCOME INEQUALITY GAP IN THE DISTRICT ONE OF BIGGEST IN THE U.S. By Wes Rivers

An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 510 Washington, DC 20002 (202) 408-1080 Fax (202) 325-8839 www.dcfpi.org March 13, 2014 HIGH AND WIDE: INCOME INEQUALITY

An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 510 Washington, DC 20002 (202) 408-1080 Fax (202) 325-8839 www.dcfpi.org March 13, 2014 HIGH AND WIDE: INCOME INEQUALITY

Highlands Spin-Off & Student Housing Transaction Webcast. January 18, 2016

Highlands Spin-Off & Student Housing Transaction Webcast January 18, 2016 Disclaimer Forward-Looking Statements in this presentation, which are not historical facts, are forward-looking statements within

Highlands Spin-Off & Student Housing Transaction Webcast January 18, 2016 Disclaimer Forward-Looking Statements in this presentation, which are not historical facts, are forward-looking statements within

Freddie Mac Community Lender Presentation State of AAPI Housing August 23 rd, 2016

Freddie Mac Community Lender Presentation State of AAPI Housing August 23 rd, 2016 TABLE OF CONTENTS I. Introduction to AREAA a. Brief History b. Current membership c. Geographic Distribution d. Policy

Freddie Mac Community Lender Presentation State of AAPI Housing August 23 rd, 2016 TABLE OF CONTENTS I. Introduction to AREAA a. Brief History b. Current membership c. Geographic Distribution d. Policy

PRESS RELEASE. Home Prices Continue Climbing in June 2013 According to the S&P/Case-Shiller Home Price Indices

Home Prices Continue Climbing in June 2013 According to the S&P/Case-Shiller Home Price Indices New York, August 27, 2013 Data through June 2013, released today by for its S&P/Case-Shiller 1 Home Price

Home Prices Continue Climbing in June 2013 According to the S&P/Case-Shiller Home Price Indices New York, August 27, 2013 Data through June 2013, released today by for its S&P/Case-Shiller 1 Home Price

RETAIL CONTINUES TO STRUGGLE AS IMPROVEMENTS ARE NOT YET SUSTAINED

RETAIL MARKET REPORT: 2Q RETAIL CONTINUES TO STRUGGLE AS IMPROVEMENTS ARE NOT YET SUSTAINED KEY INDICATORS: Key retail market indicators continue to send mixed signals. Monthly retail sales (excluding

RETAIL MARKET REPORT: 2Q RETAIL CONTINUES TO STRUGGLE AS IMPROVEMENTS ARE NOT YET SUSTAINED KEY INDICATORS: Key retail market indicators continue to send mixed signals. Monthly retail sales (excluding

COMMERCIAL REAL ESTATE PRICE RECOVERY ACCELERATES IN MAY

CCRSI RELEASE JULY 2013 (With data through May 2013) COMMERCIAL REAL ESTATE PRICE RECOVERY ACCELERATES IN MAY STRONG ABSORPTION ACROSS ALLL SIZE AND QUALITY DIMENSIONS OF REAL ESTATEE SECTOR REFLECTED

CCRSI RELEASE JULY 2013 (With data through May 2013) COMMERCIAL REAL ESTATE PRICE RECOVERY ACCELERATES IN MAY STRONG ABSORPTION ACROSS ALLL SIZE AND QUALITY DIMENSIONS OF REAL ESTATEE SECTOR REFLECTED

2019 Outlook. January

2019 Outlook January 2019 0 Performance in the multifamily market remained healthy during 2018 and is expected to continue into 2019, but with more modest growth in comparison to recent years. The multifamily

2019 Outlook January 2019 0 Performance in the multifamily market remained healthy during 2018 and is expected to continue into 2019, but with more modest growth in comparison to recent years. The multifamily

Emerging Trends in Real Estate We are in a long cycle, not in boom/bust.

Emerging Trends in Real Estate 2018 Navigating at Altitude We are in a long cycle, not in boom/bust. The key to the next few years is to expand horizons, market by market, property type by property type.

Emerging Trends in Real Estate 2018 Navigating at Altitude We are in a long cycle, not in boom/bust. The key to the next few years is to expand horizons, market by market, property type by property type.

THE NATIONAL ECONOMY. Source: Delta Associates; October 2018.

THE NATIONAL ECONOMY THE NATIONAL ECONOMY THE NATIONAL ECONOMY THE NATIONAL ECONOMY THE NATIONAL ECONOMY AMAZON HQ2 Will it be Located in the Washington Metro Area? Source: DMPED, Delta Associates, October

THE NATIONAL ECONOMY THE NATIONAL ECONOMY THE NATIONAL ECONOMY THE NATIONAL ECONOMY THE NATIONAL ECONOMY AMAZON HQ2 Will it be Located in the Washington Metro Area? Source: DMPED, Delta Associates, October

CCRSI RELEASE JANUARY 2014 (With data through NOVEMBER 2013)

") CCRSI RELEASE JANUARY 2014 (With data through NOVEMBER 2013) COMMERCIAL REAL ESTATE PRICES POST STEADY GAINS IN NOVEMBER STRONG ABSORPTION ACROSS PROPERTY TYPES SUPPORT BROAD GAINS IN PRICING This month's

CCRSI RELEASE JANUARY 2014 (With data through NOVEMBER 2013) COMMERCIAL REAL ESTATE PRICES POST STEADY GAINS IN NOVEMBER STRONG ABSORPTION ACROSS PROPERTY TYPES SUPPORT BROAD GAINS IN PRICING This month's

COMMERCIAL PRICING SURGE

CCRSI RELEASE MARCH 2013 (With data through JANUARY 2013) COMMERCIAL REAL ESTATE PRICING LEVELS OFF FOLLOWING YEAR-END SURGE IN JANUARY INCREASING LIQUIDITY AND DECLINING DISTRESSED IMPROVING INVESTOR

CCRSI RELEASE MARCH 2013 (With data through JANUARY 2013) COMMERCIAL REAL ESTATE PRICING LEVELS OFF FOLLOWING YEAR-END SURGE IN JANUARY INCREASING LIQUIDITY AND DECLINING DISTRESSED IMPROVING INVESTOR

Moody s/real Commercial Property Price Indices, January 2010

JANUARY 20 STRUCTURED FINANCE SPECIAL REPORT Moody s/real Commercial Property Price Indices, January 20 Table of Contents: OVERVIEW 1 NATIONAL ALL PROPERTY TYPE AGGREGATE INDEX 4 APPENDIX 7 Analyst Contacts

JANUARY 20 STRUCTURED FINANCE SPECIAL REPORT Moody s/real Commercial Property Price Indices, January 20 Table of Contents: OVERVIEW 1 NATIONAL ALL PROPERTY TYPE AGGREGATE INDEX 4 APPENDIX 7 Analyst Contacts

ehealth Inventory Report of Major Medical Health Plans Available Off of Government Exchanges

ehealth Inventory Report of Major Medical Health Available Off of Government Exchanges February 2014 Introduction Beginning January 1, 2014, all new major medical health insurance plans were required to

ehealth Inventory Report of Major Medical Health Available Off of Government Exchanges February 2014 Introduction Beginning January 1, 2014, all new major medical health insurance plans were required to

CRE Capital Markets Update Amid Renewed Financial Instability and Fear of a Global Recession

CRE Capital Markets Update Amid Renewed Financial Instability and Fear of a Global Recession presented to: Center for Real Estate and Urban Economic Studies Jim Clayton, Ph.D. Vice President Research Cornerstone

CRE Capital Markets Update Amid Renewed Financial Instability and Fear of a Global Recession presented to: Center for Real Estate and Urban Economic Studies Jim Clayton, Ph.D. Vice President Research Cornerstone

State of the Banking Industry

State of the Banking Industry Andrew S. Howell President and Chief Executive Officer Challenges and Opportunities Factors Impacting the Banking Industry o Housing Markets o Mortgage Markets Fifth District

State of the Banking Industry Andrew S. Howell President and Chief Executive Officer Challenges and Opportunities Factors Impacting the Banking Industry o Housing Markets o Mortgage Markets Fifth District

Discussion of: Can Securitization Work? Lessons from the U.S. REIT Market

Discussion of: Can Securitization Work? Lessons from the U.S. REIT Market Joseph L. Pagliari, Jr. Clinical Professor of Real Estate June 4, 2013 NAREIT Real Estate Research Conference An Outline of My

Discussion of: Can Securitization Work? Lessons from the U.S. REIT Market Joseph L. Pagliari, Jr. Clinical Professor of Real Estate June 4, 2013 NAREIT Real Estate Research Conference An Outline of My

Washington, DC Metro Region 2014

Washington, DC Metro Region 2014 Washington, DC Metro Region 2014 John Benziger Regional Managing Principal I Cassidy Turley Overview of Program Agenda Company Update Washington Market Overview Capital

Washington, DC Metro Region 2014 Washington, DC Metro Region 2014 John Benziger Regional Managing Principal I Cassidy Turley Overview of Program Agenda Company Update Washington Market Overview Capital

State of the Office Market

State of the Office Market Al Pontius Brian McAuliffe James Street Bill Rogalla Managing Director Marcus & Millichap Head of Transactions RREEF Co-Head, Dispositions Prudential Real Estate Investors Senior

State of the Office Market Al Pontius Brian McAuliffe James Street Bill Rogalla Managing Director Marcus & Millichap Head of Transactions RREEF Co-Head, Dispositions Prudential Real Estate Investors Senior

U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE

AEW RESEARCH U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE Q3 2018 1 Prepared by AEW Research, September 2018 This material is intended for information purposes only and does not constitute investment advice

AEW RESEARCH U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE Q3 2018 1 Prepared by AEW Research, September 2018 This material is intended for information purposes only and does not constitute investment advice

COMMERCIAL REAL ESTATE PRICES INCREASE A MODEST 1.1% IN FOURTH QUARTER AS PROPERTY PRICING LEVELS OFF IN DECEMBER

FEBRUARY 2012 CCRSI RELEASE (With data through December 2011) COMMERCIAL REAL ESTATE PRICES INCREASE A MODEST 1.1% IN FOURTH QUARTER AS PROPERTY PRICING LEVELS OFF IN DECEMBER MULTIFAMILY LED ALL PROPERTY

FEBRUARY 2012 CCRSI RELEASE (With data through December 2011) COMMERCIAL REAL ESTATE PRICES INCREASE A MODEST 1.1% IN FOURTH QUARTER AS PROPERTY PRICING LEVELS OFF IN DECEMBER MULTIFAMILY LED ALL PROPERTY

Emerging Trends in Real Estate Navigating at Altitude

Emerging Trends in Real Estate 2018 Navigating at Altitude We are in a long cycle, not in boom/ bust. The key to the next few years is to expand horizons, market by market, property type by property type.

Emerging Trends in Real Estate 2018 Navigating at Altitude We are in a long cycle, not in boom/ bust. The key to the next few years is to expand horizons, market by market, property type by property type.

STRONG MARKET FUNDAMENTALS SUPPORT BROAD PRICE GAINS IN MAY

CCRSI RELEASE JULY 2014 (With data through MAY 2014) STRONG MARKET FUNDAMENTALS SUPPORT BROAD PRICE GAINS IN MAY VALUE-WEIGHTED U.S. COMPOSITE PRICE INDEX APPROACHES PRERECESSION PEAK LEVELS This month's

CCRSI RELEASE JULY 2014 (With data through MAY 2014) STRONG MARKET FUNDAMENTALS SUPPORT BROAD PRICE GAINS IN MAY VALUE-WEIGHTED U.S. COMPOSITE PRICE INDEX APPROACHES PRERECESSION PEAK LEVELS This month's

Addendum to: The Community Reinvestment Act: A Welcome Anomaly in the Foreclosure Crisis

Addendum to: The Community Reinvestment Act: A Welcome Anomaly in the Foreclosure Crisis Relevant Figures Recalculated to Include CRA Bank Affiliate Lending January 14, 2008 Authored by: WARREN W. TRAIGER

Addendum to: The Community Reinvestment Act: A Welcome Anomaly in the Foreclosure Crisis Relevant Figures Recalculated to Include CRA Bank Affiliate Lending January 14, 2008 Authored by: WARREN W. TRAIGER

NAIOP Maryland/DC Chapter Investment Market Forecast

NAIOP Maryland/DC Chapter vestment Market Forecast 2007 vestment Market Tale of the Hare and Tortoisee? 1 st half of the year 2 nd half of the year Linda Rabbitt, Brookfield Board Member Are You Ready

NAIOP Maryland/DC Chapter vestment Market Forecast 2007 vestment Market Tale of the Hare and Tortoisee? 1 st half of the year 2 nd half of the year Linda Rabbitt, Brookfield Board Member Are You Ready

NCREIF Summer Conference

NCREIF Summer Conference Presented by: Brian D. Berry July 2012 Tishman Speyer Global Who We Are Privately held global real estate fund manager and developer with a 112 year legacy. Today, the company

NCREIF Summer Conference Presented by: Brian D. Berry July 2012 Tishman Speyer Global Who We Are Privately held global real estate fund manager and developer with a 112 year legacy. Today, the company

Lehman Brothers Financial Services Conference. Kerry Killinger Chairman and Chief Executive Officer

Lehman Brothers Financial Services Conference Kerry Killinger Chairman and Chief Executive Officer Forward-Looking Statement This presentation contains forward-looking statements, which are not historical

Lehman Brothers Financial Services Conference Kerry Killinger Chairman and Chief Executive Officer Forward-Looking Statement This presentation contains forward-looking statements, which are not historical

U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE

AEW RESEARCH U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE Q4 2018 AEW RESEARCH U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE Q 4 2018 1 Prepared by AEW Research, March 2019 This material is intended for information

AEW RESEARCH U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE Q4 2018 AEW RESEARCH U.S. ECONOMIC & PROPERTY MARKET PERSPECTIVE Q 4 2018 1 Prepared by AEW Research, March 2019 This material is intended for information

Real Estate Investment and Capital Market Perspectives An evolving and different recovery continues

Real Estate Investment and Capital Market Perspectives An evolving and different recovery continues presented to: NCREIF Valuation Committee Jim Clayton, Ph.D. Vice President Research Cornerstone Real

Real Estate Investment and Capital Market Perspectives An evolving and different recovery continues presented to: NCREIF Valuation Committee Jim Clayton, Ph.D. Vice President Research Cornerstone Real

Multifamily Investing: Expectations, Realities, Assessment of Conventional Wisdoms

REACH RESEARCH RESULTS Multifamily Investing: Expectations, Realities, Assessment of Conventional Wisdoms July 2016 James Halliwell, Managing Director Principal Real Estate Investors PROPERTY SALES VOLUME

REACH RESEARCH RESULTS Multifamily Investing: Expectations, Realities, Assessment of Conventional Wisdoms July 2016 James Halliwell, Managing Director Principal Real Estate Investors PROPERTY SALES VOLUME

2007 Outlook for Southern California Housing

Outlook for Southern Housing Presentation at the RERCSC Quarterly Luncheon Meeting, Cal Poly University, Pomona, March, U.S. Expansion Continues Outlook for Southern Housing Real Estate Research Council

Outlook for Southern Housing Presentation at the RERCSC Quarterly Luncheon Meeting, Cal Poly University, Pomona, March, U.S. Expansion Continues Outlook for Southern Housing Real Estate Research Council

CONTINUED RECOVERY IN THE INDUSTRIAL SECTOR SEVERAL MARKET FUNDAMENTALS IMPROVE

INDUSTRIAL MARKET REPORT: 3Q CONTINUED RECOVERY IN THE INDUSTRIAL SECTOR SEVERAL MARKET FUNDAMENTALS IMPROVE ECONOMY: For 3Q13, real GDP growth increased at an annualized rate of 2.8%, which was better

INDUSTRIAL MARKET REPORT: 3Q CONTINUED RECOVERY IN THE INDUSTRIAL SECTOR SEVERAL MARKET FUNDAMENTALS IMPROVE ECONOMY: For 3Q13, real GDP growth increased at an annualized rate of 2.8%, which was better

Emerging Trends in Real Estate Sustaining Momentum but Taking Nothing for Granted

Emerging Trends in Real Estate 2015 Sustaining Momentum but Taking Nothing for Granted PwC-ULI Outlook on trends 36th edition 368 interviews 1,055 survey responses 1,400+ participants, a record Who? District

Emerging Trends in Real Estate 2015 Sustaining Momentum but Taking Nothing for Granted PwC-ULI Outlook on trends 36th edition 368 interviews 1,055 survey responses 1,400+ participants, a record Who? District

INDUSTRIAL SECTOR REMAINS IN-CHECK AS ECONOMY GIVES MIXED SIGNALS

INDUSTRIAL MARKET REPORT 1Q INDUSTRIAL SECTOR REMAINS IN-CHECK AS ECONOMY GIVES MIXED SIGNALS ECONOMY: During 1Q16, real GDP increased at an annualized rate of 0.8% (second estimate), compared to 1.4%

INDUSTRIAL MARKET REPORT 1Q INDUSTRIAL SECTOR REMAINS IN-CHECK AS ECONOMY GIVES MIXED SIGNALS ECONOMY: During 1Q16, real GDP increased at an annualized rate of 0.8% (second estimate), compared to 1.4%

Retail Investment Outlook. United States Q4 2015

Retail Investment Outlook United States Q4 2015 Retail investment sale volumes (billions of $US) Retail Investors are focusing on safe bets targeting the top gateway markets, Class A malls and credit tenants

Retail Investment Outlook United States Q4 2015 Retail investment sale volumes (billions of $US) Retail Investors are focusing on safe bets targeting the top gateway markets, Class A malls and credit tenants

Pace of Decline in Home Prices Moderates as the First Quarter of 2012 Ends, According to the S&P/Case-Shiller Home Price Indices

PRESS RELEASE Pace of Decline in Home Prices Moderates as the First Quarter of 2012 Ends, According to the S&P/Case-Shiller Home Price Indices New York, May 29, 2012 Data through March 2012, released today

PRESS RELEASE Pace of Decline in Home Prices Moderates as the First Quarter of 2012 Ends, According to the S&P/Case-Shiller Home Price Indices New York, May 29, 2012 Data through March 2012, released today

California Economic Overview Fall 2013

California Economic Overview Fall 2013 Presented by Jon Haveman, Ph.D. Marin Economic Forum Contents Key Findings 3 California Outperforms Nation Normally 4 California Returns 5 Real Estate is Hot in California

California Economic Overview Fall 2013 Presented by Jon Haveman, Ph.D. Marin Economic Forum Contents Key Findings 3 California Outperforms Nation Normally 4 California Returns 5 Real Estate is Hot in California

VOLUME FINANCE HOUSING COMMERCIAL REAL ESTATE EMPLOYMENT TRANSIT & TOURISM

VOLUME 4 2018 EMPLOYMENT FINANCE HOUSING COMMERCIAL REAL ESTATE TRANSIT & TOURISM Published April 2018 VOLUME 4 2018 HIGHLIGHTS Unemployment in New York City remained at a record low in March 2018 Median

VOLUME 4 2018 EMPLOYMENT FINANCE HOUSING COMMERCIAL REAL ESTATE TRANSIT & TOURISM Published April 2018 VOLUME 4 2018 HIGHLIGHTS Unemployment in New York City remained at a record low in March 2018 Median

CCRSI RELEASE OCTOBER 2014 (With data through August 2014)

") CCRSI RELEASE OCTOBER 2014 (With data through August 2014) COMMERCIAL PROPERTY PRICES SUSTAIN UPWARD CLIMB IN AUGUST IMPROVING LABOR MARKET CONDITIONS FUEL STRONG THIRD QUARTER NET ABSORPTION AND PRICE

CCRSI RELEASE OCTOBER 2014 (With data through August 2014) COMMERCIAL PROPERTY PRICES SUSTAIN UPWARD CLIMB IN AUGUST IMPROVING LABOR MARKET CONDITIONS FUEL STRONG THIRD QUARTER NET ABSORPTION AND PRICE

The Economic Backdrop When will this cycle end?

The Economic Backdrop When will this cycle end? How far are we into the current economic expansion? Current expansion in 8 th year; 4 th longest since 1960 Length of economic expansions (months) Apr-91-Feb-01

The Economic Backdrop When will this cycle end? How far are we into the current economic expansion? Current expansion in 8 th year; 4 th longest since 1960 Length of economic expansions (months) Apr-91-Feb-01

ERRATA. To: Recipients of MG-388-RC, Estimating Terrorism Risk, RAND Corporation Publications Department. Date: December 2005

ERRATA To: Recipients of MG-388-RC, Estimating Terrorism Risk, 25 From: RAND Corporation Publications Department Date: December 25 Re: Corrected pages (pp. 23 24, Table 4.1,, Density, Density- Weighted,

ERRATA To: Recipients of MG-388-RC, Estimating Terrorism Risk, 25 From: RAND Corporation Publications Department Date: December 25 Re: Corrected pages (pp. 23 24, Table 4.1,, Density, Density- Weighted,

All Three Home Price Composites End 2011 at New Lows According to the S&P/Case-Shiller Home Price Indices

PRESS RELEASE All Three Home Price Composites End 2011 at New Lows According to the S&P/Case-Shiller Home Price Indices New York, February 28, 2012 Data through December 2011, released today by S&P Indices

PRESS RELEASE All Three Home Price Composites End 2011 at New Lows According to the S&P/Case-Shiller Home Price Indices New York, February 28, 2012 Data through December 2011, released today by S&P Indices

Moody s/real Commercial Property Price Indices, May 2010

MAY 19, 20 STRUCTURED FINANCE SPECIAL REPORT Moody s/real Commercial Property Price Indices, May 20 Table of Contents: OVERVIEW 1 NATIONAL ALL PROPERTY TYPE AGGREGATE INDEX 4 OUT-OF-BOUNDS PHENOMENON 6

MAY 19, 20 STRUCTURED FINANCE SPECIAL REPORT Moody s/real Commercial Property Price Indices, May 20 Table of Contents: OVERVIEW 1 NATIONAL ALL PROPERTY TYPE AGGREGATE INDEX 4 OUT-OF-BOUNDS PHENOMENON 6

COMMERCIAL. first look

CCRSI RELEASE AUGUST 213 (With data through June 213) COMMERCIAL REAL ESTATE PRICES SEE MIDYEAR SURGE WITH STRONGEST QUARTER RLY INCREASE SINCE 211 RECOVERY BROADENS AS GENERAL COMMERCIAL SEGMENT EDGES

CCRSI RELEASE AUGUST 213 (With data through June 213) COMMERCIAL REAL ESTATE PRICES SEE MIDYEAR SURGE WITH STRONGEST QUARTER RLY INCREASE SINCE 211 RECOVERY BROADENS AS GENERAL COMMERCIAL SEGMENT EDGES

VOLUME FINANCE HOUSING COMMERCIAL REAL ESTATE EMPLOYMENT TRANSIT & TOURISM

VOLUME 3 2018 EMPLOYMENT FINANCE HOUSING COMMERCIAL REAL ESTATE TRANSIT & TOURISM Published March 2018 VOLUME 3 2018 HIGHLIGHTS Unemployment in New York City fell to a record low in February 2018 NYC-based

VOLUME 3 2018 EMPLOYMENT FINANCE HOUSING COMMERCIAL REAL ESTATE TRANSIT & TOURISM Published March 2018 VOLUME 3 2018 HIGHLIGHTS Unemployment in New York City fell to a record low in February 2018 NYC-based

Real Estate Investment Trusts. Taking a Public and Private Look at Real Estate Allocations

Real Estate Investment Trusts Taking a Public and Private Look at Real Estate Allocations November 2016 Company REITs: Description The Public and Private Side Overview Publicly traded REITs are unique

Real Estate Investment Trusts Taking a Public and Private Look at Real Estate Allocations November 2016 Company REITs: Description The Public and Private Side Overview Publicly traded REITs are unique

Deutsche Bank Global Industrials and Basic Materials Conference June 14, 2012

Deutsche Bank Global Industrials and Basic Materials Conference June 14, 2012 1 Statement Of Forward-looking Information Certain information included in this presentation is forward-looking within the

Deutsche Bank Global Industrials and Basic Materials Conference June 14, 2012 1 Statement Of Forward-looking Information Certain information included in this presentation is forward-looking within the