Crescat Capital LLC 1560 Broadway Denver, CO (303) November 16, Dear Fellow Investors,

|

|

|

- Job Wiggins

- 5 years ago

- Views:

Transcription

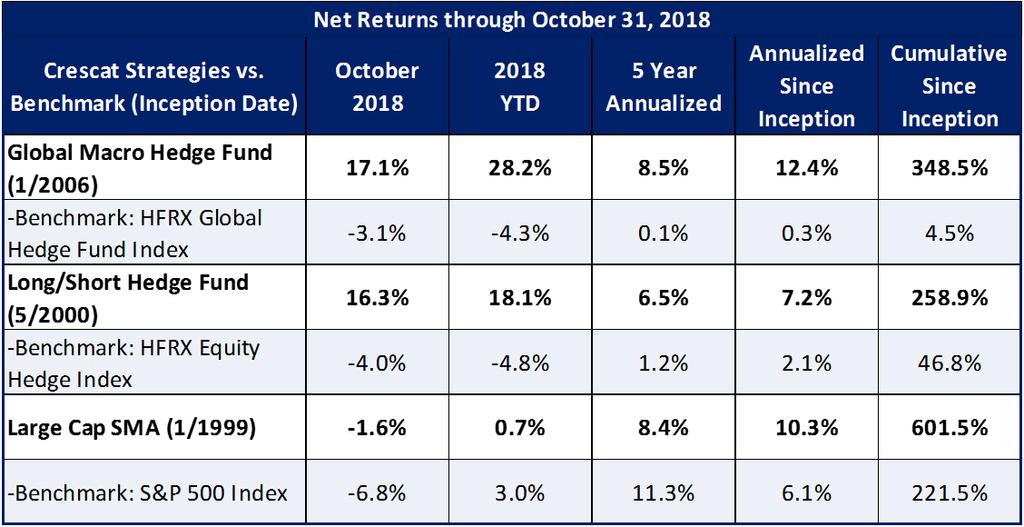

1 November 16, 2018 Crescat Capital LLC 1560 Broadway Denver, CO (303) Dear Fellow Investors, October was a frightening month for investors around the world. From Hong Kong to New York, stock markets were slammed by a wave of fears about slowing growth, trade wars, and higher interest rates. The Nasdaq took the brunt of the damage. Stocks like Amazon and Netflix both lost around one-fifth of their value as the Nasdaq Composite tumbled 9.2% in October. That's the biggest monthly drop for the Nasdaq since November The S&P 500 Index lost 6.8% in October, its worst month since September The pain was equally bad in overseas markets which were already slumping because of weaker economic growth along with rising trade and geopolitical tensions. Hong Kong and Chinese stocks sank deeper into a bear market in October as China s trade conflict with the US intensified. Crescat s hedge funds capitalized on the turmoil in October and climbed to the top of the US hedge fund performance tables for the month and year as compiled by Bloomberg Hedge Fund Brief: Source: Bloomberg 1

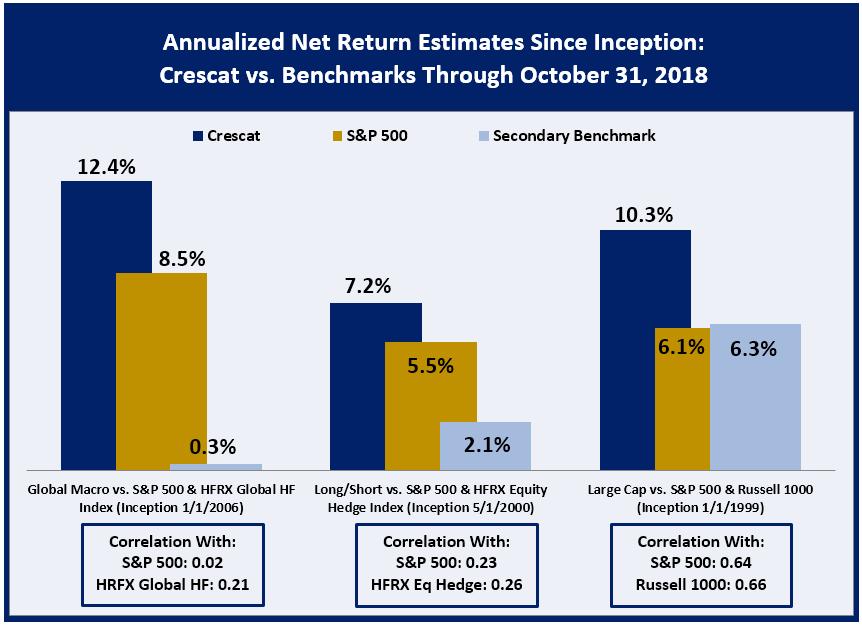

2 Crescat s flagship global macro fund was up 17.1% net in October and rose to 28.2% net year to date. Our long short equity fund rose 16.3% net for the month and finished up 18.1% net year to date. Crescat s long-only Large Cap SMA composite was down 1.6% net in October and is up 0.7% net year to date. Our mission is to protect and grow wealth by capitalizing on the most compelling macro themes of our time. We do this by deploying proprietary value-driven models to develop tactical investment themes. Our global macro themes permeate all our investment strategies. Our goal is high absolute and risk-adjusted returns over the long term with low correlation to benchmarks. Today, our three highest conviction macro ideas and portfolio exposures continue to be: 1. US Equities: The market is damaged and finally breaking down from truly record valuations while US profit growth has peaked. Crescat s hedge funds remain tactically net short. 2. China: China's economy is in the early stages of a collapse which will be globally contagious. The trade war with the United States is just one catalyst, not the primary cause of China s economic downfall. We expect China s currency to soon enter a full-blown crisis and have shifted our global macro hedge fund short exposure slightly less towards Chinese stocks and slightly more towards the currency. 3. Precious Metals: Left for dead. Precious metals are an extremely undervalued alternative to cash today as a haven trade that can also help us capitalize on financial turmoil and beat inevitable future inflation. US Equities and High Yield Corporate Credit It was just two months ago that the US stock market hit all-time high valuation multiples across eight different measures that we have been featuring in our quarterly letters. Our macro model is signaling that a cyclical bear market in US stocks remains in the early stages of developing with much further to play out over the next one to two years. We remain fundamental bears on US equity and high-yield credit markets. Corporate leverage is at record levels while credit spreads are near all-time lows. It is late in the economic cycle with the Fed continuing to remove liquidity from markets by raising interest rates and unwinding its balance sheet. With many global stock markets already in bear territory, US markets are finally showing signs of cracking. Now is a great time to be short overvalued US stocks such as those identified by Crescat s fundamental equity model. That is how Crescat s hedge funds remain positioned currently. Our global macro fund also continues to be short high yield bonds through put options on select ETFs. China A global macroeconomic downturn is already in motion with the unwinding of record debt-to-gdp bubbles globally. China, the largest credit bubble ever based on our analysis, is already in a full-scale credit bust with the median Chinese-listed equity recently down almost 40% from its 12-month high. We believe China is already in a serious recession despite popular fiction regarding its positive reported GDP numbers that omit losses on bad debt. Chinese stocks have already lost over $5 trillion of market value since January of this year, about 26% of GDP. Yet, no commensurate value of bad debt has been marked down yet. By comparison, in 2008 when US stocks had lost a similar proportion of GDP in market value, the US economy was already in deep recession. China is almost certainly in recession now. As we have been writing about for several years now, China s GDP has been vastly overstated due to the lack of write-downs of its non-performing loans. By our estimates, bad loans today still on the books of Chinese banks could be as much as $8 trillion, 60% of its GDP and about four times the book value of equity in its banking system. These are insanely large numbers that portend systemic bank runs and social unrest. The Chinese 2

3 economy has been a failed experiment in Ponzi finance. China can no longer fool the world regarding its GDP growth. The result is a historic credit bubble that is finally bursting under its own weight. The Trump trade war has been just one of the many catalysts for the burst, but it is not the root cause of it. The cause was excessive bank credit expansion along with the continued rolling over of bad debt. That playbook is now coming to an end with a dramatic slowdown in China s M1 and M2 growth proving that its credit expansion is unsustainable. China is now experiencing its time of economic reckoning, its Minsky Moment. The Chinese banking imbalances are so large that it is too late to undo the bursting of the credit bubble regardless of the direction impending trade negotiations with the U.S. take. China is careening towards the inevitable: its central bank will soon have no choice but to print record new levels of yuan (M0) to bail out its banks and attempt to quell social unrest. Like other economic collapses of centrally-planned, totalitarian communist countries, we continue to expect that the Chinese currency will plunge as money printing and capital flight accelerates. In our global macro fund, we remain short the Chinese yuan through put options laddered out in different durations. The yuan short has contributed to the fund s strong performance year to date, but we haven t seen anything yet in terms of our expected return from a coming yuan plunge. We also have significant short exposure to the other Chinese currency, the Hong Kong dollar, structured similarly through laddered put options to play a likely de-pegging of that currency. HKD presents an extreme asymmetric risk/reward investment opportunity to profit from yet another huge credit imbalance in the world today. Hong Kong has the largest credit-to-gdp gap and debt service ratio of all countries tracked by the Bank for International Settlements. The BIS considers each of these important early-warning indicators for banking and currency crises. Hong Kong is part of China, and therefore part of China s credit bubble. It is China s financial hub with the rest of the world and has its own housing and banking bubbles. Its financial markets are already being swept up in China s economic crisis. We expect the Hong Kong dollar to de-peg and devalue as China s credit bust continues to play out and Hong Kong is further absorbed politically and economically by China. Precious Metals and Global Fiat Debasement With a decade of money printing and interest rate suppression in the wake of the global financial crisis, central banks have created truly record global debt and financial asset bubbles. At the same time, they have created a corresponding record low valuation of global above-ground gold holdings relative to fiat money. The depressed gold price relative to the of high cost of finding and extracting it has wreaked havoc on the mining stock fundamentals. It s been a seven-year free cash flow and stock price drought. Declining industry-wide capital investment over this period has created a steady decline in new gold discoveries leading to peak gold production fears that have large miners scrambling to acquire new in-the-ground reserves. Gold and silver miners represent historic deep value today according to Crescat s fundamental equity model at a time when the broad competing stock market is at record fundamental valuations. Already activist hedge funds are taking note and industry consolidation is underway which has been benefiting several of Crescat s gold and silver mining holdings. We strongly believe it is poised to be one of strongest performers in the coming months and quarters. Why? Because we expect gold and silver to soar at the first hint of the end of Fed rate hikes which we believe is just around the corner and much sooner than priced into the Fed Funds futures curve today. The Fed has already been raising interest rates for three years now trying to lead the world out of global central bank life support, but it is hamstrung. Its tight monetary policy has already served as a key catalyst to burst global debt and financial asset bubbles in China and other emerging markets. Meanwhile, the Fed s tightening has likely not been enough to fight rising real-world inflationary pressures at home. As record over-valued financial asset bubbles burst, it is likely that the Fed will stop raising rates soon. Next, it would likely end its balance sheet reduction, reduce rates, and re-engage in QE. The end to rate hikes will come first and the signal to watch for that will be a drop in the Fed Funds futures curve. It s already been slipping in recent weeks. 3

4 Yield Curve Inversion We take issue with the economists and market prognosticators who say we shouldn t be concerned about a coming recession anytime soon because the Fed hasn t inverted the Treasury yield curve yet. For those who obsess over the need for an inverted yield curve to signal a coming financial collapse and recession, be advised that the Fed has already inverted the global yield curve today, just as it did ahead of the last two U.S. stock market crashes and recessions. See our chart below. 4

5 Performance 5

6 Profit Attribution In Closing We think it s a great time to invest in tactical global macro strategies like Crescat s that have a proven history of strong performance during previous times of market turmoil as well as strong overall long-term performance through complete business cycles. We urge all investors to consider making an investment allocation to Crescat and we stand ready to answer questions or discuss themes. Sincerely, The Crescat Capital Team For further information, contact: Derek Chow Director of Marketing and Business Development dchow@crescat.net 2018 Crescat Capital LLC 6

7 Case studies are included for informational purposes only and are provided as a general overview of our general investment process, and not as indicative of any investment experience. There is no guarantee that the case studies discussed here are completely representative of our strategies or of the entirety of our investments, and we reserve the right to use or modify some or all of the methodologies mentioned herein. Only accredited investors and qualified clients will be admitted as limited partners to a Crescat fund. For natural persons, investors must meet SEC requirements including minimum annual income or net worth thresholds. Crescat funds are being offered in reliance on an exemption from the registration requirements of the Securities Act of 1933 and are not required to comply with specific disclosure requirements that apply to registration under the Securities Act. The SEC has not passed upon the merits of or given its approval to the Crescat funds, the terms of the offering, or the accuracy or completeness of any offering materials. A registration statement has not been filed for any Crescat fund with the SEC. Limited partner interests in the Crescat funds are subject to legal restrictions on transfer and resale. Investors should not assume they will be able to resell their securities. Investing in securities involves risk. Investors should be able to bear the loss of their investment. Investments in the Crescat funds are not subject to the protections of the Investment Company Act of Performance data represents past performance, and past performance does not guarantee future results. Performance data is subject to revision following each monthly reconciliation and annual audit. Current performance may be lower or higher than the performance data presented. Crescat is not required by law to follow any standard methodology when calculating and representing performance data. The performance of Crescat funds may not be directly comparable to the performance of other private or registered funds. Investors may obtain the most current performance data and private offering memorandum for a Crescat fund by contacting Linda Smith at (303) or by sending a request via to lsmith@crescat.net. See the private offering memorandum for each Crescat fund for complete information and risk factors. 7

March 16, Dear Investors:

March 16, 2019 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors: At Crescat we remain positioned to capitalize on a downturn in the economic

March 16, 2019 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors: At Crescat we remain positioned to capitalize on a downturn in the economic

We are positioned to capitalize on these themes in unique ways across all three of our investment strategies:

6/25/18 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors, We strongly believe that the global macro investment cycle is turning down right

6/25/18 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors, We strongly believe that the global macro investment cycle is turning down right

February 21, Dear Investors:

February 21, 2019 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors: There is indeed a business cycle and timing it ahead of key inflection

February 21, 2019 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors: There is indeed a business cycle and timing it ahead of key inflection

Crescat Capital LLC 1560 Broadway Denver, CO (303) January 27, 2018.

January 27, 2018.") January 27, 2018 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors, Believe me: We re in a bubble right now. And the only thing that looks

January 27, 2018 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors, Believe me: We re in a bubble right now. And the only thing that looks

Crescat Capital LLC 1560 Broadway Denver, CO (303) September 15, 2018.

September 15, 2018.") Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net September 15, 2018 Dear Investors: Our current three best macro ideas today are complementary plays on

Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net September 15, 2018 Dear Investors: Our current three best macro ideas today are complementary plays on

The year-to-date rally in global risk assets after the Fed flip appears to us to be a last gasp of speculative mania for the current economic cycle.

Crescat Q1 2019 Quarterly Research Letter April 18, 2019 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors: The year-to-date rally in global

Crescat Q1 2019 Quarterly Research Letter April 18, 2019 Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net Dear Investors: The year-to-date rally in global

Fourth Quarter Market Outlook. Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2018 Market Outlook Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA Economic Outlook Growth: Strong 2018, But Expecting Slowdown in 2019 Growth & Jobs 2018 2017 2016 2015 2014

Fourth Quarter 2018 Market Outlook Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA Economic Outlook Growth: Strong 2018, But Expecting Slowdown in 2019 Growth & Jobs 2018 2017 2016 2015 2014

iw PARTNERS asset management - asset services - asset solutions Commentary for the first quarter of 2019

Gold and gold equities in 2019: Recovery amid rising financial market risk conditions which has historically signalled an imminent economic slowdown, and rising volatility at time of historically high

Gold and gold equities in 2019: Recovery amid rising financial market risk conditions which has historically signalled an imminent economic slowdown, and rising volatility at time of historically high

GOLD OUTLOOK 2019: RECOVERY EXPECTED TO CONTINUE

GOLD OUTLOOK 2019: RECOVERY EXPECTED TO CONTINUE January 2019 Gold staged a recovery late in 2018. The yellow metal has recovered most of its losses since June 2018. A collapse in speculative positioning

GOLD OUTLOOK 2019: RECOVERY EXPECTED TO CONTINUE January 2019 Gold staged a recovery late in 2018. The yellow metal has recovered most of its losses since June 2018. A collapse in speculative positioning

BCA 4Q 2018 Review and 2019 Outlook Russ Allen, CIO. Summary Outlook

BCA 4Q 2018 Review and 2019 Outlook Russ Allen, CIO Summary Outlook January 15, 2019 Markets in 2019 will be choppy with volatility more like this past year than the placid trading of 2017. The Fed is

BCA 4Q 2018 Review and 2019 Outlook Russ Allen, CIO Summary Outlook January 15, 2019 Markets in 2019 will be choppy with volatility more like this past year than the placid trading of 2017. The Fed is

Gundlach s Forecast for 2016

Gundlach s Forecast for 2016 January 19, 2016 by Robert Huebscher Jeffrey Gundlach is a prescient and accurate forecaster. Last week, as he does each January, he offered his market outlook. But unlike

Gundlach s Forecast for 2016 January 19, 2016 by Robert Huebscher Jeffrey Gundlach is a prescient and accurate forecaster. Last week, as he does each January, he offered his market outlook. But unlike

Summary. Chinese equities remained mired in a bear market, with the Shanghai composite losing nearly

Summary Editor: Tristan Zhuo Senior Economist Phone: +852 2826 6193 Email: tristanzhuo@bochk.com In spite of fixed asset investment, industrial production, and exports all missing their targets, China

Summary Editor: Tristan Zhuo Senior Economist Phone: +852 2826 6193 Email: tristanzhuo@bochk.com In spite of fixed asset investment, industrial production, and exports all missing their targets, China

The Recession Cometh (Eventually)

") The Recession Cometh (Eventually) March 27, 2019 Tom Cohn, Principal Ben Pace, Chief Investment Officer Cerity Partners The Recession Cometh (Eventually) Executive Summary Should we worry about a recession

The Recession Cometh (Eventually) March 27, 2019 Tom Cohn, Principal Ben Pace, Chief Investment Officer Cerity Partners The Recession Cometh (Eventually) Executive Summary Should we worry about a recession

A Detailed Analysis of U.S. Bear Markets

March 2016 CONTENTS 1. Abstract 1. Definition and characteristics of bear markets 2. Length of bear markets 4. Bear market severity 5. Recovery periods 6. Bear markets and the economy 8. Bear markets and

March 2016 CONTENTS 1. Abstract 1. Definition and characteristics of bear markets 2. Length of bear markets 4. Bear market severity 5. Recovery periods 6. Bear markets and the economy 8. Bear markets and

However, while prices are likely to fall a bit further, we also continue to believe that we could be with a. Wednesday, November

Wednesday, November 28 2018 In our last update, we noted that Gold Stocks had resistance in the $19.75 to $19.80 area and that the odds were about 62% that GDX could be near a short term high of importance.

Wednesday, November 28 2018 In our last update, we noted that Gold Stocks had resistance in the $19.75 to $19.80 area and that the odds were about 62% that GDX could be near a short term high of importance.

Crescat Capital LLC 1560 Broadway Denver, CO (303) August 5, 2017.

August 5, 2017.") August 5, 2017 Dear Investors, Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net History has proven that credit bubbles always burst. China by far is the

August 5, 2017 Dear Investors, Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net History has proven that credit bubbles always burst. China by far is the

The yellow highlighted areas are bear markets with NO recession.

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

A secular bear in bonds? Not so fast

MARKETS A secular bear in bonds? Not so fast Government bond yields could still move higher in the near term but the low rate environment is here for a long while yet David Stonehouse, MBA, CFA Vice-President

MARKETS A secular bear in bonds? Not so fast Government bond yields could still move higher in the near term but the low rate environment is here for a long while yet David Stonehouse, MBA, CFA Vice-President

A Guide to 2016 s Market Volatility. CONGRESS WEALTH MANAGEMENT, LLC 250 Northern Ave, Suite 310, Boston, MA

CONGRESS WEALTH MANAGEMENT, LLC 250 Northern Ave, Suite 310, Boston, MA 02210 www.congresswealth.com Contents What will it take to calm the markets? Will the correction in U.S. stocks turn into a bear

CONGRESS WEALTH MANAGEMENT, LLC 250 Northern Ave, Suite 310, Boston, MA 02210 www.congresswealth.com Contents What will it take to calm the markets? Will the correction in U.S. stocks turn into a bear

Tactical Money Management-- Strategy Overviews and Forecasting 2016

Tactical Money Management-- Strategy Overviews and Forecasting 2016 1 2015 Strategy Performance A YEAR IN TRANSITION The end of QE in the U.S. First Interest Rate Hike in 8 Years. Late economic cycle slowing.

Tactical Money Management-- Strategy Overviews and Forecasting 2016 1 2015 Strategy Performance A YEAR IN TRANSITION The end of QE in the U.S. First Interest Rate Hike in 8 Years. Late economic cycle slowing.

On Our Radar September 2015

On Our Radar September 2015 The Dow Jones Industrial Average (DJIA), S&P 500 and NASDAQ Composite fell 6.56 percent, 6.25 percent, and 6.85 percent, respectively, in August, which was highlighted by a

On Our Radar September 2015 The Dow Jones Industrial Average (DJIA), S&P 500 and NASDAQ Composite fell 6.56 percent, 6.25 percent, and 6.85 percent, respectively, in August, which was highlighted by a

Fund Management Diary

Fund Management Diary Meeting held on 11 th December 2018 Losing Momentum After a strong start to the year, global growth peaked in the first of 2018 and doesn t look like regaining momentum. Trade tensions

Fund Management Diary Meeting held on 11 th December 2018 Losing Momentum After a strong start to the year, global growth peaked in the first of 2018 and doesn t look like regaining momentum. Trade tensions

YIELD CURVE INVERSION: A CLEAR BUT UNLIKELY DANGER

1-year minus -year UST (%) INVESTMENT STRATEGY COMMENTARY YIELD CURVE INVERSION: A CLEAR BUT UNLIKELY DANGER December 4, 17 Investors focus on the yield curve with good reason an inverted curve has historically

1-year minus -year UST (%) INVESTMENT STRATEGY COMMENTARY YIELD CURVE INVERSION: A CLEAR BUT UNLIKELY DANGER December 4, 17 Investors focus on the yield curve with good reason an inverted curve has historically

Market Watch. July Review Global economic outlook. Australia

Market Watch Latest monthly commentary from the Investment Markets Research team at BT. Global economic outlook Australia Available data for the June quarter is consistent with a moderation in GDP growth

Market Watch Latest monthly commentary from the Investment Markets Research team at BT. Global economic outlook Australia Available data for the June quarter is consistent with a moderation in GDP growth

Struthers Report V22 # 1.1 Outlook, Markets, Gold, K, NGD, G Call Options January

Struthers Report V22 # 1.1 Outlook, Markets, Gold, K, NGD, G Call Options January 6 2016 rhstruthers@gmail.com ********************************************************************************** As you

Struthers Report V22 # 1.1 Outlook, Markets, Gold, K, NGD, G Call Options January 6 2016 rhstruthers@gmail.com ********************************************************************************** As you

Sub-3% GDP Growth: A Lost Decade For The US Economy

Sub-3% GDP Growth: A Lost Decade For The US Economy February 3, 2016 by Gary Halbert of Halbert Wealth Management IN THIS ISSUE: 1. 4Q GDP Up Only 0.7% Economy Started and Ended Weak 2. A Controversy Over

Sub-3% GDP Growth: A Lost Decade For The US Economy February 3, 2016 by Gary Halbert of Halbert Wealth Management IN THIS ISSUE: 1. 4Q GDP Up Only 0.7% Economy Started and Ended Weak 2. A Controversy Over

Monthly Report. September ,69

NAV SEPTEMBER 2018 1 YEAR 3 YEARS 5 YEARS SINCE INCEPTION Global Allocation Fund* 97,76-2,33% -5,31% -9,41% -2,08% 34,18% 157,61% 350.000 Performance of 100.000 March 31, 2006 to September 30, 2018 300.000

NAV SEPTEMBER 2018 1 YEAR 3 YEARS 5 YEARS SINCE INCEPTION Global Allocation Fund* 97,76-2,33% -5,31% -9,41% -2,08% 34,18% 157,61% 350.000 Performance of 100.000 March 31, 2006 to September 30, 2018 300.000

Global Markets. CHINA AND GLOBAL MARKET VOLATILITY.

PRICE POINT August 015 Timely intelligence and analysis for our clients. Global Markets. CHINA AND GLOBAL MARKET VOLATILITY. EXECUTIVE SUMMARY Eric Moffett Portfolio Manager, Asia Opportunities Strategy

PRICE POINT August 015 Timely intelligence and analysis for our clients. Global Markets. CHINA AND GLOBAL MARKET VOLATILITY. EXECUTIVE SUMMARY Eric Moffett Portfolio Manager, Asia Opportunities Strategy

HOPE FOR ROTATION. So, let me talk a little about each of these. Tariffs. Tariffs are restrictions to trade; they are a tax and they cause inflation.

HOPE FOR ROTATION We ve said repeatedly that we believe the current bull market will continue until there is either a recession or a restrictive monetary policy. So far, that position has been accurate

HOPE FOR ROTATION We ve said repeatedly that we believe the current bull market will continue until there is either a recession or a restrictive monetary policy. So far, that position has been accurate

Odds Rise For "Inverted Yield Curve" & New Recession

Odds Rise For "Inverted Yield Curve" & New Recession June 14, 2017 by Gary Halbert of Halbert Wealth Management 1. Policy Committee Set to Hike Fed Funds Rate Tomorrow 2. Yield Curve Flattening Could It

Odds Rise For "Inverted Yield Curve" & New Recession June 14, 2017 by Gary Halbert of Halbert Wealth Management 1. Policy Committee Set to Hike Fed Funds Rate Tomorrow 2. Yield Curve Flattening Could It

Chart 1: Market Cap to GDP (Buffett Indicator) - The US stock market is still highly valued despite the recent performance. 2

- The US stock market is still highly valued despite the recent performance. 2") December 24th, 2018 1 Since our framework turned negative in October, we have suggested that being defensive was the proper posture. We continue to support that assertion given the current market environment.

December 24th, 2018 1 Since our framework turned negative in October, we have suggested that being defensive was the proper posture. We continue to support that assertion given the current market environment.

October Stock Indexes September 2009 Market Indexes September S&P 500 Index +3.6% +17.0% HFRX Global Hedge Fund Index +2.2% +11.

October 2009 Dear Investor, In September, stocks continued modestly higher, both in the US and globally. There have been a few notable exceptions to the gains, as stock indexes in China and Japan (among

October 2009 Dear Investor, In September, stocks continued modestly higher, both in the US and globally. There have been a few notable exceptions to the gains, as stock indexes in China and Japan (among

Market Watch. Latest monthly commentary from the Investment Markets Research team at BT. March Review Developments in Financial Markets

Market Watch Latest monthly commentary from the Investment Markets Research team at BT. March Review 2018 INSIDE THIS ISSUE Stock markets were blindsided on the first day of March, when US President Donald

Market Watch Latest monthly commentary from the Investment Markets Research team at BT. March Review 2018 INSIDE THIS ISSUE Stock markets were blindsided on the first day of March, when US President Donald

UTILITIES SELECT SECTOR SPDR FUND (XLU)

") UTILITIES SELECT SECTOR SPDR FUND (XLU) $53.06 USD Risk: Med Zacks ETF Rank 5 - Strong Sell Fund Type Issuer Benchmark Index Utilities/Infrastructure ETFs STATE STREET GLOBAL ADVISORS UTILITIES SELECT

UTILITIES SELECT SECTOR SPDR FUND (XLU) $53.06 USD Risk: Med Zacks ETF Rank 5 - Strong Sell Fund Type Issuer Benchmark Index Utilities/Infrastructure ETFs STATE STREET GLOBAL ADVISORS UTILITIES SELECT

10.2 Recent Shocks to the Macroeconomy Introduction. Housing Prices. Chapter 10 The Great Recession: A First Look

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Investment Perspectives. From The Global Investment Committee

Investment Perspectives From The Global Investment Committee Global Risk Aversion Reached Extreme Levels Morgan Stanley Standardized Global Risk Demand Index As of October 15, 2014 Complacent Extreme Fear

Investment Perspectives From The Global Investment Committee Global Risk Aversion Reached Extreme Levels Morgan Stanley Standardized Global Risk Demand Index As of October 15, 2014 Complacent Extreme Fear

Crescat Capital LLC 1560 Broadway Denver, CO (303) November 18, 2017.

November 18, 2017.") November 18, 2017 Dear Investors, Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net US large cap stocks are the most overvalued in history, higher than

November 18, 2017 Dear Investors, Crescat Capital LLC 1560 Broadway Denver, CO 80202 (303) 271-9997 info@crescat.net www.crescat.net US large cap stocks are the most overvalued in history, higher than

Welcoming the Dark Side December 20, 1015

Welcoming the Dark Side December 20, 1015 Summary: I believe after a few false starts that we re now in a major Bear Market for stocks. A Bear Market is a market that can fall in excess of 20% or more.

Welcoming the Dark Side December 20, 1015 Summary: I believe after a few false starts that we re now in a major Bear Market for stocks. A Bear Market is a market that can fall in excess of 20% or more.

Economy Check-In: Post 2008 Crisis Market Update Special Report

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

10º Congresso Value Investing Brasil

www.cvib.com.br 10º Congresso Value Investing Brasil 23 de maio de 2017 Macro global coerente insights variantes Jonathan Tepper Variant Perception Our Company Who We Are: Variant Perception is an independent

www.cvib.com.br 10º Congresso Value Investing Brasil 23 de maio de 2017 Macro global coerente insights variantes Jonathan Tepper Variant Perception Our Company Who We Are: Variant Perception is an independent

HARD OR SOFT LANDING?

# The Collapse of Communism is Bullish #1 The Baby Boom Chart Book 1991 # Apocalypse Now? (NOT!) #3 The End Of The Cold War Is Bullish Topical Study # HARD OR SOFT LANDING? February, 199 Dr. Edward Yardeni

# The Collapse of Communism is Bullish #1 The Baby Boom Chart Book 1991 # Apocalypse Now? (NOT!) #3 The End Of The Cold War Is Bullish Topical Study # HARD OR SOFT LANDING? February, 199 Dr. Edward Yardeni

The good oil: why invest in commodities?

The good oil: why invest in commodities? Client Note 4 September 2013 Historical analysis shows that commodities have been a consistently strong performer from a relative investment performance perspective

The good oil: why invest in commodities? Client Note 4 September 2013 Historical analysis shows that commodities have been a consistently strong performer from a relative investment performance perspective

PINECONE MACRO RESEARCH SPECIAL REPORT JANUARY Could Oil End the Global Super Cycle?

Could Oil End the Global Super Cycle? Super cycles are made up of multiple business cycles or short term debt cycles the kind we as investors have to deal with once or twice per decade. Super cycles, or

Could Oil End the Global Super Cycle? Super cycles are made up of multiple business cycles or short term debt cycles the kind we as investors have to deal with once or twice per decade. Super cycles, or

ANALYSIS OF THE STOCKMARKET CORRECTION

ANALYSIS OF THE STOCKMARKET CORRECTION 12.10.2018 For investment professional use only The US equity markets nosedived on Wednesday last week, dragging Asian and European markets down in their wake. The

ANALYSIS OF THE STOCKMARKET CORRECTION 12.10.2018 For investment professional use only The US equity markets nosedived on Wednesday last week, dragging Asian and European markets down in their wake. The

The cabal is setting its own trap! A reset this weekend?

The cabal is setting its own trap! A reset this weekend? On April 11 gold rose to $1365 and silver to $16.85 as the possibility of a war in the Middle East took center stage. Libor rose for the 45th consecutive

The cabal is setting its own trap! A reset this weekend? On April 11 gold rose to $1365 and silver to $16.85 as the possibility of a war in the Middle East took center stage. Libor rose for the 45th consecutive

2018 ECONOMIC OUTLOOK

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

Is China the New France?

Is China the New France? August 6, 2013 by Marianne Brunet Imagine a country that grows its economy by greatly devaluing against the reserve currency to develop a strong export sector. As the country becomes

Is China the New France? August 6, 2013 by Marianne Brunet Imagine a country that grows its economy by greatly devaluing against the reserve currency to develop a strong export sector. As the country becomes

U.S. Debt Tops $20 Trillion - Stocks Soar To Record Highs

U.S. Debt Tops $20 Trillion - Stocks Soar To Record Highs September 20, 2017 by Gary Halbert of Halbert Wealth Management 1. National Debt Tops $20 Trillion, Equal to 107% of GDP 2. Debt Held by the Public

U.S. Debt Tops $20 Trillion - Stocks Soar To Record Highs September 20, 2017 by Gary Halbert of Halbert Wealth Management 1. National Debt Tops $20 Trillion, Equal to 107% of GDP 2. Debt Held by the Public

Another Strong Jobs Report, But Economy Remains Weak

Another Strong Jobs Report, But Economy Remains Weak August 9, 2016 by Gary D. Halbert of Halbert Wealth Management IN THIS ISSUE: 1. July Jobs Report Stronger Than Expected, 2 Month in a Row 2. The Real

Another Strong Jobs Report, But Economy Remains Weak August 9, 2016 by Gary D. Halbert of Halbert Wealth Management IN THIS ISSUE: 1. July Jobs Report Stronger Than Expected, 2 Month in a Row 2. The Real

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001 By Dean Baker December 20, 2001 Now that it is officially acknowledged that a recession has begun, most economists are predicting that it will soon be

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001 By Dean Baker December 20, 2001 Now that it is officially acknowledged that a recession has begun, most economists are predicting that it will soon be

China: The Long and Short of Economic Reform

Global Economics Monthly July 2014 China: The Long and Short of Economic Reform Robert Kahn, Steven A. Tananbaum Senior Fellow for International Economics O V E R V I E W Bottom Line: China looks on track

Global Economics Monthly July 2014 China: The Long and Short of Economic Reform Robert Kahn, Steven A. Tananbaum Senior Fellow for International Economics O V E R V I E W Bottom Line: China looks on track

Channel the Capital to the Real Economy

Channel the Capital to the Real Economy China Liquidity Analysis February 2016 Fundamental structural issues in the Chinese economy is a theme we at Bin Yuan have discussed in past quarterly newsletters.

Channel the Capital to the Real Economy China Liquidity Analysis February 2016 Fundamental structural issues in the Chinese economy is a theme we at Bin Yuan have discussed in past quarterly newsletters.

Market Review, and 2019 outlook Brace for the impact. If you are still standing, you are the WINNER The year when nothing worked.

Market Review, and 2019 outlook Brace for the impact. If you are still standing, you are the WINNER The year when nothing worked. The chart, below, from Deutsche bank shows a striking observation of a

Market Review, and 2019 outlook Brace for the impact. If you are still standing, you are the WINNER The year when nothing worked. The chart, below, from Deutsche bank shows a striking observation of a

Should we worry about the yield curve?

A feature article from our U.S. partners INSIGHTS AUGUST 2018 Should we worry about the yield curve? If and when the yield curve inverts, its signal may well be premature. Jurrien Timmer l Director of

A feature article from our U.S. partners INSIGHTS AUGUST 2018 Should we worry about the yield curve? If and when the yield curve inverts, its signal may well be premature. Jurrien Timmer l Director of

The Importance of Precious Metals During Economic Crisis Free Report

The Importance of Precious Metals During Economic Crisis Free Report This short report is intended to raise awareness to the increasing importance of precious metals during economic turmoil. We ll take

The Importance of Precious Metals During Economic Crisis Free Report This short report is intended to raise awareness to the increasing importance of precious metals during economic turmoil. We ll take

What s the Yield Curve? A Powerful Signal of Recessions Has Wall Street s Attention

BUSINESS DAY What s the Yield Curve? A Powerful Signal of Recessions Has Wall Street s Attention By Matt Phillips June 25, 2018 You can try to play down a trade war with China. You can brush off the impact

BUSINESS DAY What s the Yield Curve? A Powerful Signal of Recessions Has Wall Street s Attention By Matt Phillips June 25, 2018 You can try to play down a trade war with China. You can brush off the impact

Global Economic and Market Outlook for Gavyn Davies, Chairman, Fulcrum Asset Management

Global Economic and Market Outlook for 2018 Gavyn Davies, Chairman, Fulcrum Asset Management After many years of persistent downgrades to consensus GDP forecasts, 2017 has seen the first upgrades since

Global Economic and Market Outlook for 2018 Gavyn Davies, Chairman, Fulcrum Asset Management After many years of persistent downgrades to consensus GDP forecasts, 2017 has seen the first upgrades since

Gundlach: Federal Debt is on a Suicide Mission

Gundlach: Federal Debt is on a Suicide Mission June 13, 2018 by Robert Huebscher The federal deficit and the cost to service that debt are rising at the same time. This historical anomaly is putting the

Gundlach: Federal Debt is on a Suicide Mission June 13, 2018 by Robert Huebscher The federal deficit and the cost to service that debt are rising at the same time. This historical anomaly is putting the

Asia/Pacific Economic Overview

Copyright E. I. du Pont de Nemours and Company. All rights reserved. Distribution, reproduction or copying of this copyrighted work without express written permission of DuPont is prohibited. Asia/Pacific

Copyright E. I. du Pont de Nemours and Company. All rights reserved. Distribution, reproduction or copying of this copyrighted work without express written permission of DuPont is prohibited. Asia/Pacific

Chart 1: S&P 500 Death Crosses since 1923;

December 10th, 2018 1 Last week we had a death cross in the S&P 500 and the 3 year minus 5 year Treasury yield curve went negative (inverted). These two events had talking heads claiming everything from

December 10th, 2018 1 Last week we had a death cross in the S&P 500 and the 3 year minus 5 year Treasury yield curve went negative (inverted). These two events had talking heads claiming everything from

st Quarter Review

US Large Cap US Mid Cap US Small Cap International Equity Emerging Markets Real Estate Precious Metals Inflation Cash 10-year Treasury Global Bonds Corporate Bonds High Yield Corp Bonds Intmd-Term Muni

US Large Cap US Mid Cap US Small Cap International Equity Emerging Markets Real Estate Precious Metals Inflation Cash 10-year Treasury Global Bonds Corporate Bonds High Yield Corp Bonds Intmd-Term Muni

A Tactical Opportunity: Sell High, Buy Low

Outlook 2016 1 Real Gold vs. A Promise of Gold A Tactical Opportunity: Sell High, Buy Low By Nick Barisheff January 2016 T he market outlook for 2016 presents Many Canadians have profited by investing

Outlook 2016 1 Real Gold vs. A Promise of Gold A Tactical Opportunity: Sell High, Buy Low By Nick Barisheff January 2016 T he market outlook for 2016 presents Many Canadians have profited by investing

Should We Worry About the Yield Curve?

LEADERSHIP SERIES AUGUST 2018 Should We Worry About the Yield Curve? If and when the yield curve inverts, its signal may well be premature. Jurrien Timmer l Director of Global Macro l @TimmerFidelity Key

LEADERSHIP SERIES AUGUST 2018 Should We Worry About the Yield Curve? If and when the yield curve inverts, its signal may well be premature. Jurrien Timmer l Director of Global Macro l @TimmerFidelity Key

QUARTERLY MARKET UPDATE January 2019

Year-End Market Reversal Symbol Name 2018 Return (%) AGG ishares Core US Aggregate Bond ETF 0.0 HYG ishares iboxx $ High Yield Corp Bd ETF -1.9 LQD ishares iboxx $ Invmt Grade Corp Bd ETF -3.8 SPY SPDR

Year-End Market Reversal Symbol Name 2018 Return (%) AGG ishares Core US Aggregate Bond ETF 0.0 HYG ishares iboxx $ High Yield Corp Bd ETF -1.9 LQD ishares iboxx $ Invmt Grade Corp Bd ETF -3.8 SPY SPDR

Value versus Growth: History Stands on the Side of Value Investing

Value versus Growth: History Stands on the Side of Value Investing October 2015 Executive Summary Since the global financial crisis struck in 2008, we have been witnessing a new chapter in the history

Value versus Growth: History Stands on the Side of Value Investing October 2015 Executive Summary Since the global financial crisis struck in 2008, we have been witnessing a new chapter in the history

Running out of fuel?

China s economy: How fit is the panda? China s booming economy is helping to support global growth as America turns sickly. So now it has to keep up the pace September 27, 2007 The Economist No country

China s economy: How fit is the panda? China s booming economy is helping to support global growth as America turns sickly. So now it has to keep up the pace September 27, 2007 The Economist No country

The Bull vs. Bear Case for Emerging Markets

Epoch Investment Partners, Inc. Insights April 2018 The Bull vs. Bear Case for Emerging Markets Kevin Hebner, PhD Managing Director, Global Portfolio Management We are in the midst of a synchronized global

Epoch Investment Partners, Inc. Insights April 2018 The Bull vs. Bear Case for Emerging Markets Kevin Hebner, PhD Managing Director, Global Portfolio Management We are in the midst of a synchronized global

Emerging Market Equities SPRING The Current Opportunity SBH INTERNATIONAL EQUITY TEAM WHITE PAPER

Emerging Market Equities The Current Opportunity SPRING 2017 SBH INTERNATIONAL EQUITY TEAM WHITE PAPER KEY POINTS Emerging market (EM) equities have offered significant return and diversification potential

Emerging Market Equities The Current Opportunity SPRING 2017 SBH INTERNATIONAL EQUITY TEAM WHITE PAPER KEY POINTS Emerging market (EM) equities have offered significant return and diversification potential

CMG Mauldin Smart Core Strategy Update

CMG Mauldin Smart Core Strategy Update John Mauldin Chief Economist & Co-Portfolio Manager Steve Blumenthal Executive Chairman, CIO & Co-Portfolio Manager 2018 Market Summary After reaching all-time highs

CMG Mauldin Smart Core Strategy Update John Mauldin Chief Economist & Co-Portfolio Manager Steve Blumenthal Executive Chairman, CIO & Co-Portfolio Manager 2018 Market Summary After reaching all-time highs

Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand.

Mizuho Economic Outlook & Analysis November 15, 218 Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand. < Summary > Expanding private debt

Mizuho Economic Outlook & Analysis November 15, 218 Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand. < Summary > Expanding private debt

January 29, 2015 ANNUAL MARKET REVIEW Dear Client, We hope this finds you and yours well and enjoying a great start to the New Year.

Financial Concepts Unlimited, Inc. 30B West Street Annapolis, MD 21401 Phone: (301) 315-6344 Fax: (301) 315-6343 Toll Free:(866)-444-5122 http://www.fcuinc.com John R. Taylor Jr. President & CEO January

Financial Concepts Unlimited, Inc. 30B West Street Annapolis, MD 21401 Phone: (301) 315-6344 Fax: (301) 315-6343 Toll Free:(866)-444-5122 http://www.fcuinc.com John R. Taylor Jr. President & CEO January

NO PAIN, NO GAIN: 2016 MAY REQUIRE TOLERANCE FOR VOLATILITY

LPL RESEARCH WEEKLY MARKET COMMENTARY December 07 2015 NO PAIN, NO GAIN: 2016 MAY REQUIRE TOLERANCE FOR VOLATILITY Burt White Chief Investment Officer, LPL Financial Jeffrey Buchbinder, CFA Market Strategist,

LPL RESEARCH WEEKLY MARKET COMMENTARY December 07 2015 NO PAIN, NO GAIN: 2016 MAY REQUIRE TOLERANCE FOR VOLATILITY Burt White Chief Investment Officer, LPL Financial Jeffrey Buchbinder, CFA Market Strategist,

Picton Mahoney Asset Management Synergy Funds

Picton Mahoney Asset Management Synergy Funds Investors emotions remain fickle. In late April, the market seemed convinced that the global economy would be on a high-growth recovery. By the end of June,

Picton Mahoney Asset Management Synergy Funds Investors emotions remain fickle. In late April, the market seemed convinced that the global economy would be on a high-growth recovery. By the end of June,

Macro Monthly UBS Asset Management June 2018

Macro Monthly UBS Asset Management June 18 Investing in a mature cycle Erin Browne Head of Asset Allocation Evan Brown, CFA Director, Asset Allocation Roland Czerniawski, CFA Associate Director, Asset

Macro Monthly UBS Asset Management June 18 Investing in a mature cycle Erin Browne Head of Asset Allocation Evan Brown, CFA Director, Asset Allocation Roland Czerniawski, CFA Associate Director, Asset

QUICK PIVOT FRIDAY, JANUARY 7, 2011 BOB HOYE PUBLISHED BY INSTITUTIONAL ADVISORS. Surreal Policymakers Are Blowing Serial Bubbles

QUICK PIVOT FRIDAY, JANUARY 7, 2011 BOB HOYE PUBLISHED BY INSTITUTIONAL ADVISORS Surreal Policymakers Are Blowing Serial Bubbles The above is more a sarcastic observation than a title for this edition.

QUICK PIVOT FRIDAY, JANUARY 7, 2011 BOB HOYE PUBLISHED BY INSTITUTIONAL ADVISORS Surreal Policymakers Are Blowing Serial Bubbles The above is more a sarcastic observation than a title for this edition.

Feel No Pain: Why a Deficit In Times of High Unemployment Is Not a Burden

Issue Brief September 2010 Feel No Pain: Why a Deficit In Times of High Unemployment Is Not a Burden BY DEAN BAKER* With the economy suffering from near double-digit unemployment, public debate is dominated

Issue Brief September 2010 Feel No Pain: Why a Deficit In Times of High Unemployment Is Not a Burden BY DEAN BAKER* With the economy suffering from near double-digit unemployment, public debate is dominated

January 25th, Dear Turtle Creek Client,

January 25th, 2019 Dear Turtle Creek Client, 2018 was a year in which literally nothing worked for investors. Every major asset class from stocks to bonds to commodities posted negative returns and the

January 25th, 2019 Dear Turtle Creek Client, 2018 was a year in which literally nothing worked for investors. Every major asset class from stocks to bonds to commodities posted negative returns and the

Global Bond Markets to Enter New Phase in 2018

Global Bond Markets to Enter New Phase in 2018 January 8, 2018 by Douglas Peebles of AllianceBernstein 2017 was supposed to be the year that would put an end to modest growth, lukewarm inflation and anemic

Global Bond Markets to Enter New Phase in 2018 January 8, 2018 by Douglas Peebles of AllianceBernstein 2017 was supposed to be the year that would put an end to modest growth, lukewarm inflation and anemic

Fund Management Diary

Fund Management Diary Meeting held on 15 th May 2018 IT sector to struggle when the S&P 500 slumps Capital Economics expects the United States economy to slow next year and cause the S&P 500 to fall to

Fund Management Diary Meeting held on 15 th May 2018 IT sector to struggle when the S&P 500 slumps Capital Economics expects the United States economy to slow next year and cause the S&P 500 to fall to

Global Fixed Income WHY VOLATILITY STILL MATTERS

PRICE POINT April 2018 Global Fixed Income WHY VOLATILITY STILL MATTERS Timely intelligence and analysis for our clients. KEY POINTS Until its recent comeback, volatility has been notable for its absence

PRICE POINT April 2018 Global Fixed Income WHY VOLATILITY STILL MATTERS Timely intelligence and analysis for our clients. KEY POINTS Until its recent comeback, volatility has been notable for its absence

Investment opportunities in the late-expansion stage of the business cycle

Late-expansion investing White paper Investment opportunities in the late-expansion stage of the business cycle Key highlights Economic expansions do not follow a timetable; they typically come to an end

Late-expansion investing White paper Investment opportunities in the late-expansion stage of the business cycle Key highlights Economic expansions do not follow a timetable; they typically come to an end

Forecasting the Next Recession

Forecasting the Next Recession November 30, 2017 by Scott Minerd, Brian Smedley, Matt Bush of Guggenheim Partners Guggenheim s Model Points to Recession in Late 2019 or 2020 Report Highlights It is critical

Forecasting the Next Recession November 30, 2017 by Scott Minerd, Brian Smedley, Matt Bush of Guggenheim Partners Guggenheim s Model Points to Recession in Late 2019 or 2020 Report Highlights It is critical

DEAR JEROME, (Jerome Powell, Chairman of the U.S. Federal Reserve)

") Quarterly Commentary January 2019 DEAR JEROME, (Jerome Powell, Chairman of the U.S. Federal Reserve) Stocks experienced their worst December since the Great Depression largely because you and the rest

Quarterly Commentary January 2019 DEAR JEROME, (Jerome Powell, Chairman of the U.S. Federal Reserve) Stocks experienced their worst December since the Great Depression largely because you and the rest

THE CHAPMAN REPORT FOR DECEMBER 22, 2008

THE CHAPMAN REPORT FOR DECEMBER 22, 2008 Charts and technical commentary by David Chapman Union Securities Ltd, 33 Yonge Street, Suite 901, Toronto, Ontario, M5E 1G4 fax (416) 604-0533, (416) 604-0557,

THE CHAPMAN REPORT FOR DECEMBER 22, 2008 Charts and technical commentary by David Chapman Union Securities Ltd, 33 Yonge Street, Suite 901, Toronto, Ontario, M5E 1G4 fax (416) 604-0533, (416) 604-0557,

Monthly Report. August ,83

Monthly Report NAV AUGUST 2018 1 YEAR 3 YEARS 5 YEARS SINCE INCEPTION Global Allocation Fund* 100,09-0,46% -3,05% -1,52% -2,47% 47,02% 163,75% 350.000 Performance of 100.000 March 31, 2006 to August 31,

Monthly Report NAV AUGUST 2018 1 YEAR 3 YEARS 5 YEARS SINCE INCEPTION Global Allocation Fund* 100,09-0,46% -3,05% -1,52% -2,47% 47,02% 163,75% 350.000 Performance of 100.000 March 31, 2006 to August 31,

Recessions are Unavoidable. WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS December 19, 2017 Recession Indicators Agree the Expansion Continues

Austin Pickle, CFA Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS December 19, 2017 Recession Indicators Agree the Expansion Continues Key Takeaways» There are several

Austin Pickle, CFA Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS December 19, 2017 Recession Indicators Agree the Expansion Continues Key Takeaways» There are several

Market Outlook As of March 4, 2016

Financial & Investment Newsletter Market Outlook As of March 4, 2016 By George M. Hiller JD, LLM, MBA, CFP The 7-year old bull market, got off to a rocky start in early 2016 moving into correction territory,

Financial & Investment Newsletter Market Outlook As of March 4, 2016 By George M. Hiller JD, LLM, MBA, CFP The 7-year old bull market, got off to a rocky start in early 2016 moving into correction territory,

2013 SECOND QUARTER ACCOUNT MANAGEMENT REVIEW July 13, 2013

2013 SECOND QUARTER ACCOUNT MANAGEMENT REVIEW July 13, 2013 HIGHLIGHTS Markets fall worldwide on nervousness about higher US interest rates Housing continues to recover, but may be slowing due to higher

2013 SECOND QUARTER ACCOUNT MANAGEMENT REVIEW July 13, 2013 HIGHLIGHTS Markets fall worldwide on nervousness about higher US interest rates Housing continues to recover, but may be slowing due to higher

Chart 2: Oil prices are down considerably. This suggests that inflation is slowing.

November 12th, 2018 1 This is provided for informational purposes only and should not be considered a recommendation to buy or sell a particular security. Past performance is no guarantee of future returns.

November 12th, 2018 1 This is provided for informational purposes only and should not be considered a recommendation to buy or sell a particular security. Past performance is no guarantee of future returns.

What Rising Interest Rates Mean for the Economy and You

What Rising Interest Rates Mean for the Economy and You BROUGHT TO YOU BY: In March of this year, the Federal Reserve voted to raise its target federal funds rate to a range of 0.75-1%. Not only that,

What Rising Interest Rates Mean for the Economy and You BROUGHT TO YOU BY: In March of this year, the Federal Reserve voted to raise its target federal funds rate to a range of 0.75-1%. Not only that,

The Hong Kong Economy in Contraction Mode

Irina Fan Senior Economist irinafan@hangseng.com Joanne Yim Chief Economist joanneyim@hangseng.com 22 December 08 The Hong Kong Economy in Contraction Mode Hong Kong is in recession and leading economic

Irina Fan Senior Economist irinafan@hangseng.com Joanne Yim Chief Economist joanneyim@hangseng.com 22 December 08 The Hong Kong Economy in Contraction Mode Hong Kong is in recession and leading economic

Global Financial Crisis and China s Countermeasures

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Gold. Denver Gold Group Denver 16 January 2018

Gold Denver Gold Group Denver 16 January 218 Today s Themes Gold price expectations in 218 and beyond. From Fear to Greed: The changing character of gold investment demand. The Enormous Asymmetry Of Gold

Gold Denver Gold Group Denver 16 January 218 Today s Themes Gold price expectations in 218 and beyond. From Fear to Greed: The changing character of gold investment demand. The Enormous Asymmetry Of Gold

The $VIX, the Dow, and China. 3/15/2008

The $VIX, the Dow, and China. 3/15/2008 In the past few days, I have received some questions from a few members. These questions cannot be answered in a few words, and because other members may be interested,

The $VIX, the Dow, and China. 3/15/2008 In the past few days, I have received some questions from a few members. These questions cannot be answered in a few words, and because other members may be interested,

The Worst Week In A Decade For US Stocks

The Worst Week In A Decade For US Stocks February 15, 2018 by Gary Halbert of Halbert Wealth Management 1. The Worst Week For US Stock Markets Since 2008 2. Confluence of Negative Factors Became Important

The Worst Week In A Decade For US Stocks February 15, 2018 by Gary Halbert of Halbert Wealth Management 1. The Worst Week For US Stock Markets Since 2008 2. Confluence of Negative Factors Became Important

Third Quarter Market Review

Third Quarter Market Review The S&P 500 continued its winning streak, with the index appreciating in value by 3.96% for the quarter (see chart below). This market barometer was up all three months of the

Third Quarter Market Review The S&P 500 continued its winning streak, with the index appreciating in value by 3.96% for the quarter (see chart below). This market barometer was up all three months of the

WHERE DO WE GO FROM HERE? JANUARY 9 TH, 2019

WHERE DO WE GO FROM HERE? JANUARY 9 TH, 2019 MY GOAL TODAY. AGENDA 1. Looking Back at 2018 2. Three Types of Bear Markets 3. The Economic Backdrop 4. Two Paths Forward 5. Q&A TOUGH YEAR TO MAKE MONEY #1

WHERE DO WE GO FROM HERE? JANUARY 9 TH, 2019 MY GOAL TODAY. AGENDA 1. Looking Back at 2018 2. Three Types of Bear Markets 3. The Economic Backdrop 4. Two Paths Forward 5. Q&A TOUGH YEAR TO MAKE MONEY #1

Markets update August 2013

Markets update August 2013 Global share markets retreated in August amid increasing US Federal Reserve taper talk and escalating geopolitical tensions. The Australian share market made good gains, commodities

Markets update August 2013 Global share markets retreated in August amid increasing US Federal Reserve taper talk and escalating geopolitical tensions. The Australian share market made good gains, commodities

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Gundlach s Top ETF Recommendation

Gundlach s Top ETF Recommendation November 17, 2017 by Robert Huebscher The money to be made is in non-u.s. markets, according to Jeffrey Gundlach. For long-term investors, he recommends a specific ETF.

Gundlach s Top ETF Recommendation November 17, 2017 by Robert Huebscher The money to be made is in non-u.s. markets, according to Jeffrey Gundlach. For long-term investors, he recommends a specific ETF.