Farmland Values Will the Boom Turn Bust?

|

|

|

- Antony Barnett

- 5 years ago

- Views:

Transcription

1 Farmland Values Will the Boom Turn Bust? Top Producer Seminar January 30, 2013 Brent Gloy Director, Center for Commercial Agriculture

2 Agenda Is it a bubble? How much higher will they go? Are they too high already? What could change things? What are the concerns/risks?

3 Is it a Bubble? Economists almost certainly not Is this reassuring? Not very We have a very difficult time identifying irrationality (disconnect from fundamentals) ex ante Are there troubling signs in the marketplace? Yes a few

4 Putting it in Perspective Agriculture s history includes periods of remarkable boom and bust Agriculture is capital intensive Large increases in profitability make fixed assets priced in less profitable times look cheap MAJOR capital restructuring underway Key Questions: Will these times last or will we retreat to previous levels? Are farmland values in a speculative bubble or responding normally to economic conditions?

5 Types of Shocks which Alter Farming Profitability Demand driven: Expansion of demand which calls for more output at all price levels For example, biofuels and income growth and food demand in emerging markets Persistent demand growth can substantially increase land values and capital investment Supply induced: Supply contraction where less is available at all price levels Short term weather shocks do not typically impact fixed asset values Inability of supply to keep up with normal demand expansion. If true could lead asset value increases Current situation is complicated by interaction of both impacts and extremely low interest rates which make future income more valuable

6 So How Big are the Recent Increases in Farmland Values?

7 In Real Terms, Today s Farmland Value Increases are on Par with those of the 70 s Region Nominal Change Annualized Growth Rate Real Change and Annualized Growth Rate Iowa Percent Illinois Indiana a Iowa farmland values from the Iowa State Farmland Survey (Duffy). Indiana, Illinois, and U.S. Values from National Agricultural Statistics Service. Real values calculated using the CPI index.

8 Dramatic Price Increases Set Against Backdrop of: Numerous spectacular price increases and declines in the broader economy Housing, tech stocks Will farmland follow suit?

9 Bubbles. you get a bubble when a very high percentage of the population buys into some originally sound premise. that (the premise) becomes distorted as time passes and people forget the original sound premise and start focusing solely on the price action. Excerpt from Warren Buffett s interview with the Financial Crisis Inquiry Commission

10 How Does This Apply to the Farmland Situation? Fundamentals have undergone dramatic changes Increased demand Reduced interest rates Supply shocks Are market participants evaluating these factors when pricing farmland?

11 These multiples require either sustained income growth or continuing low interest rates (and likely both)

12 Will rates move up as slowly as they have moved down? Rate impact would likely felt on valuations today Cash flow impact will be secondary impact unlike 70 s Warning sign 1 something changes to take us out of accommodation

13 Aside from last two, recent years have been good but not spectacular

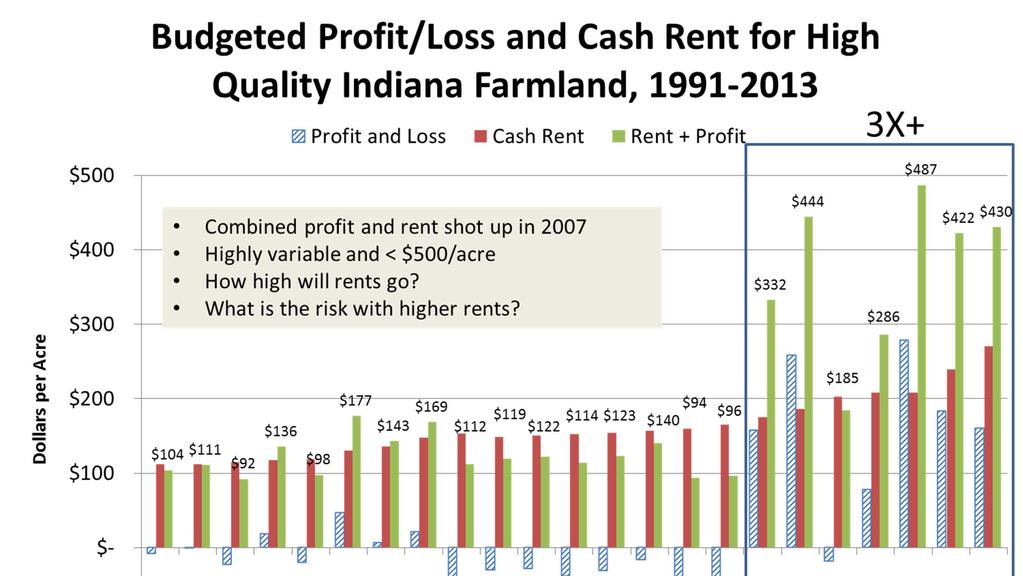

14

15 Land Values Under Alternative Capitalization Rates (Multiples) and Income Levels Value per Acre 12,000 10,000 8,000 3% (33) 4% (25) 5% (20) 6% (17) 8% (13) 2012 Value HQ IN Farmland $7,704 6,000 4,000 2, Current Cash Rental Rate HQ IN Farmland, $265 per Acre Income per Acre

16 Cap Rate Risk Monetary policy change = cap rate Economic recovery = cap rate Inflation = cap rate Increased volatility/risk = cap rate Slowing income growth in ag = cap rate

17 Percent Relationship Between Real Interest Rate and Returns to Operators, Real Interest Rate on 1 Yr UST (Left Axis) Ret to Op (Right Axis) It is somewhat unlikely that incomes would rise with increasing real rates Billion 2005 USD

18 Exports Play a Key Role In Price Increases SOURCE: Henderson, J., B.A. Gloy, and M.D. Boehlje. Agriculture s Boom Bust Cycles: Is This Time Different. The Economic Review, Kansas City Federal Reserve Bank, 96:4(2011):

19 Million Acres 2,400 2,300 2,200 2,100 2,000 1,900 1,800 Figure 6: World Harvested ACRES 13 Major Crops Total: (Millions) 1972/73= 1, /82= 2, /07= 2,104 Acreage response is underway! 2002= 2, /06= 2, /13= 2, Million acres added in 7years 1,700 1,600

20 35 30 Renewable Fuel Standard ( ) Where to with biofuels? 25 Billions of Gallons Biomass-based Diesel Non-celulosic Advanced Celulosic Advanced Conventional Biofuels

21 Land rent has averaged 35% of revenue over this period, high = 45%, low = 22%

22

23 So What About Corn Prices? Darrel Good and Scott Irwin forecast the new plateau prices as follows: Corn Soybeans Wheat Post Dec 2006 Monthly Price $ s per Bushel Average High Low SOURCE: Good, D. and S. Irwin. The New Era of Corn, Soybean, and Wheat Prices. Marketing and Outlook Briefs, MOBR 08 04, September 2, 2008 Dept. of Agr. Cons. Econ, University of Illinois.

24 Land Values Under Alternative Capitalization Rates (Multiples) and Rent per Bushel, HQ IN Farmland $12,000 3% (33) 4% (25) 5% (20) 6% (17) 8% (13) Value per Acre $10,000 $8,000 $6,000 $4,000 $2,000 Last Year's IN Rent per Bu. Current IN Rent per Bu. 35% of G&I New Avg. Corn Price = $1.61 Still room for averages to move higher but sales over $10,000/acre? $12,000 per acre!?!!? $0 $0.78 $0.89 $0.99 $1.09 $1.20 $1.30 $1.41 $1.51 $1.61 $1.72 $1.82 Rent per Bushel $1.93 $2.03 $2.14 $2.24 Box captures I&G s price range if land receives 35% of gross revenue Current yield = 192bpa, current rent = $265/acre $2.34 $2.45

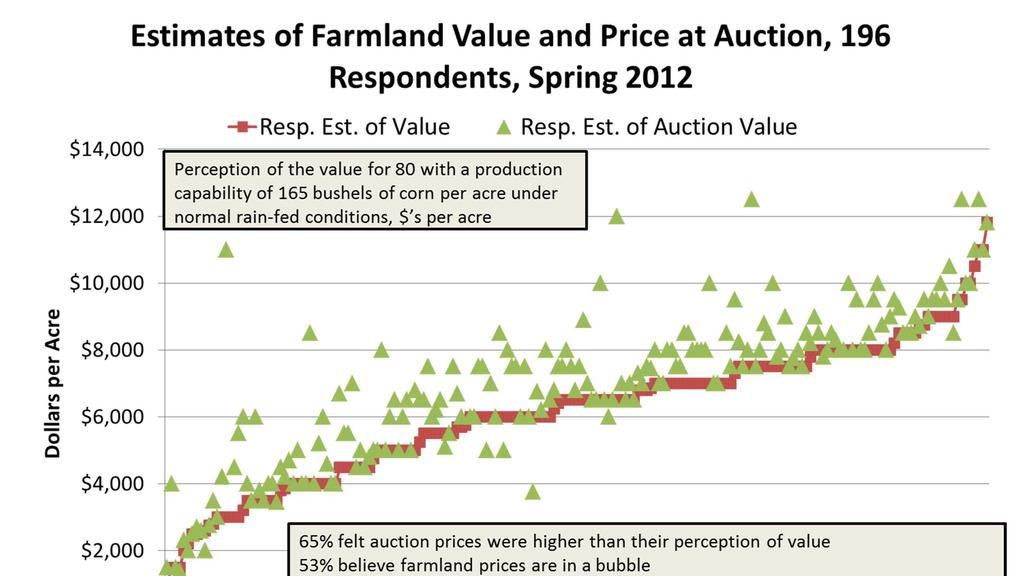

25 What Do Landowners Think? Current values are dependent upon continuation of low interest rates and high farm returns over variable costs Conducted and internet survey in Spring 2012 What do farmland investors think about future Farmland prices Cash rents Crop prices

26 The Respondents Individuals in CCA database with interest in farmland and farming 246 complete responses (28%) 73% owned farmland 74% want to purchase more farmland in the next 5 years Median acres owned = 500 rented from others = 1,200 rented to others = 240

27

28 Respondents asked to consider: 80 Acres of Farmland with a production capability of 165 bushels of corn per acre under normal rain fed conditions

29

30 On average, respondents expect similar multiples in the future

31 $12.00 $11.00 Distribution of Expected Average Cash Corn Prices Over the Next 5 Years, 189 Farmland Value Survey Respondents Box captures I&G s corn price range $10.00 $9.00 $8.00 $'s per Bushel $7.00 $6.00 $5.00 $4.00 $3.00 $2.00 $1.00 $0.00 There is a 1 in 10 chance the average corn price will be less than: The average corn price will most likely be: There is a 1 in 10 chance the average corn price will be greater than: Respondents

32 Almost no systematic relationship between perception of land value and expected corn prices

33 Most would use some debt to fund additional purchases

34 Summary Price increases are on par with most dramatic seen in the last 50 years Prices clearly reflect view that returns over variable costs stay high and rates stay low It is unlikely that farmland fits the classic economic definition of a bubble, but this does not rule out the possibility that prices could fall substantially Negative demand shock would create significant pressure on land prices

35 Summary Investors: Show cautious optimism about farmland investments Have some concern that market in a bubble Appear to be comfortable with multiples approaching 30 expect them to be maintained Expect corn prices to exceed $5.00/bu on average Despite some warning signs investors appear to be rationally evaluating fundamentals Those with very optimistic views may push prices higher but there is obvious concern on part of others

36 Final Thoughts The credit cycle will start to heat up there will be significant pressure to finance rising land values Many farmers have spectacular equity positions Many new entrants and expansions will take place Land market should start to level off if rates/fundamentals change watch the market closely

37 Final Thoughts Tremendous volatility in the ag marketplace For crop farmers it has been all favorable How good are you at managing risk? (It has been easy so far) How exposed are you to other s risk management activities? Volatility creates winners and losers How are you managing costs? What about non land capital investment? When need for operating capital comes it will be substantial and much larger than before the boom

38 Final Thoughts Times in row crop are very good It is conceivable they could get better It is also conceivable they could be worse It is very difficult to predict what takes us out of this cycle, but credit can magnify the outcome either way How favorable is the current risk/return tradeoff for farmland?

When Do Farm Booms Become Bubbles?

When Do Farm Booms Become Bubbles? Brent Gloy Director, Center for Commercial Agriculture 2012 Agricultural Symposium Federal Reserve Bank of Kansas City Kansas City, MO July 16, 2012 Background Agriculture

When Do Farm Booms Become Bubbles? Brent Gloy Director, Center for Commercial Agriculture 2012 Agricultural Symposium Federal Reserve Bank of Kansas City Kansas City, MO July 16, 2012 Background Agriculture

What s Ahead for Farmland Trends? How do Young Farmers Fit In?

What s Ahead for Farmland Trends? How do Young Farmers Fit In? Tomorrow s Top Producer Seminar January 29, 2013 Brent Gloy Director, Center for Commercial Agriculture Bgloy@purdue.edu 765-494-0468 Agenda

What s Ahead for Farmland Trends? How do Young Farmers Fit In? Tomorrow s Top Producer Seminar January 29, 2013 Brent Gloy Director, Center for Commercial Agriculture Bgloy@purdue.edu 765-494-0468 Agenda

A Symposium Sponsored by the Federal Reserve Bank of Kansas City July 16-17, Session 1: When Do Farm Booms Become Bubbles?

A Symposium Sponsored by the Federal Reserve Bank of Kansas City July 16-17, 2012 Session 1: When Do Farm Booms Become Bubbles? When Do Farm Booms Become Bubbles? (Manuscript) Dr. Brent Gloy Director,

A Symposium Sponsored by the Federal Reserve Bank of Kansas City July 16-17, 2012 Session 1: When Do Farm Booms Become Bubbles? When Do Farm Booms Become Bubbles? (Manuscript) Dr. Brent Gloy Director,

MANAGING THE RISK CAPTURING THE OPPORTUNITY IN CROP FARMING. Michael Boehlje and Brent Gloy Center for Commercial Agriculture Purdue University

MANAGING THE RISK CAPTURING THE OPPORTUNITY IN CROP FARMING by Michael Boehlje and Brent Gloy Center for Commercial Agriculture Purdue University Farming has always been a risky business with the returns

MANAGING THE RISK CAPTURING THE OPPORTUNITY IN CROP FARMING by Michael Boehlje and Brent Gloy Center for Commercial Agriculture Purdue University Farming has always been a risky business with the returns

Finding Your Financial Footing in 2016

Finding Your Financial Footing in 2016 York Ag Expo York, NE January 13, 2016 Brent Gloy, LLC www.ageconomists.com bgloy@ageconomists.com Twitter: @BrentGloy Agenda The situation The outlook in 12 questions

Finding Your Financial Footing in 2016 York Ag Expo York, NE January 13, 2016 Brent Gloy, LLC www.ageconomists.com bgloy@ageconomists.com Twitter: @BrentGloy Agenda The situation The outlook in 12 questions

Center for Commercial Agriculture

Center for Commercial Agriculture The Great Margin Squeeze: Strategies for Managing Through the Cycle by Brent A. Gloy, Michael Boehlje, and David A. Widmar After many years of high commodity prices and

Center for Commercial Agriculture The Great Margin Squeeze: Strategies for Managing Through the Cycle by Brent A. Gloy, Michael Boehlje, and David A. Widmar After many years of high commodity prices and

Purdue Agricultural Economics Report

Purdue Agricultural Economics Report November 2011 Managing The Risk Capturing The Opportunity In Crop Farming Michael Boehlje and Brent Gloy*, Center for Commercial Agriculture Farming has always been

Purdue Agricultural Economics Report November 2011 Managing The Risk Capturing The Opportunity In Crop Farming Michael Boehlje and Brent Gloy*, Center for Commercial Agriculture Farming has always been

Lynn Paulson SVP, Director of Agri-Business Development, Bell State Bank & Trust

Lynn Paulson SVP, Director of Agri-Business Development, Bell State Bank & Trust Email: lpaulson@bellbanks.com o Nearly unprecedented period of prosperity and profitability for row crop and grain producers

Lynn Paulson SVP, Director of Agri-Business Development, Bell State Bank & Trust Email: lpaulson@bellbanks.com o Nearly unprecedented period of prosperity and profitability for row crop and grain producers

DCP VERSUS ACRE in 2013 For Indiana Farms

DCP VERSUS ACRE in 2013 For Indiana Farms The extension of the last farm bill for 2013 crops means that individuals need to make the decision of whether to participate in the regular Direct and Countercyclical

DCP VERSUS ACRE in 2013 For Indiana Farms The extension of the last farm bill for 2013 crops means that individuals need to make the decision of whether to participate in the regular Direct and Countercyclical

Macroeconomic Risks for Farmer Cooperatives

Macroeconomic Risks for Farmer Cooperatives KFSA Directors & Management Meeting Hutchinson, KS November 21 st, 2011 Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative

Macroeconomic Risks for Farmer Cooperatives KFSA Directors & Management Meeting Hutchinson, KS November 21 st, 2011 Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative

2008 FARM BILL: FOCUS ON ACRE

2008 FARM BILL: FOCUS ON ACRE (Average Crop Revenue Election) Carl Zulauf Ag. Economist, Ohio State University Updated: October 3, 2008, Presented to USDA Economists Group 1 Seminar Outline 1. Provide

2008 FARM BILL: FOCUS ON ACRE (Average Crop Revenue Election) Carl Zulauf Ag. Economist, Ohio State University Updated: October 3, 2008, Presented to USDA Economists Group 1 Seminar Outline 1. Provide

Macroeconomic Outlook: Implications for Agriculture. It has been 26 years since we have experienced a significant recession

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Crop Risk Management

Crop Risk Management January 28 th, 2010 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957 5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farmmanagement.htm Source: Johnson,

Crop Risk Management January 28 th, 2010 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957 5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farmmanagement.htm Source: Johnson,

Jason Henderson Vice President and Branch Executive Federal Reserve Bank of Kansas City Omaha Branch April 10, 2012

Jason Henderson Vice President and Branch Executive April 1, 212 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or the

Jason Henderson Vice President and Branch Executive April 1, 212 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or the

Farm Finance Update. Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City. March 17, 2017

Farm Finance Update March 17, 2017 Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City The views expressed are those of the author and do not necessarily reflect the

Farm Finance Update March 17, 2017 Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City The views expressed are those of the author and do not necessarily reflect the

Macroeconomic Outlook for U.S. Agriculture

Macroeconomic Outlook for U.S. Agriculture Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City May 18, 216 The views expressed are those of the author and do not necessarily

Macroeconomic Outlook for U.S. Agriculture Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City May 18, 216 The views expressed are those of the author and do not necessarily

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst A year ago USDA shocked the market by cutting its forecast of soybean production, helping

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst A year ago USDA shocked the market by cutting its forecast of soybean production, helping

Fall 2017 Crop Outlook Webinar

Fall 2017 Crop Outlook Webinar Chris Hurt, Professor & Extension Ag. Economist James Mintert, Professor & Director, Center for Commercial Agriculture Fall 2017 Crop Outlook Webinar October 13, 2017 50%

Fall 2017 Crop Outlook Webinar Chris Hurt, Professor & Extension Ag. Economist James Mintert, Professor & Director, Center for Commercial Agriculture Fall 2017 Crop Outlook Webinar October 13, 2017 50%

What is in Store for the Agricultural Land Market?

February 2015 What is in Store for the Agricultural Land Market? Michael Langemeier, Associate Director, Center for Commercial Agriculture Michael Boehlje, Distinguished Professor, Center for Commercial

February 2015 What is in Store for the Agricultural Land Market? Michael Langemeier, Associate Director, Center for Commercial Agriculture Michael Boehlje, Distinguished Professor, Center for Commercial

CASH RENT WITH BONUS LEASING ARRANGEMENT: DESCRIPTION AND EXAMPLE

FEFO 11-17 September 27, 2011 CASH RENT WITH BONUS LEASING ARRANGEMENT: DESCRIPTION AND EXAMPLE A cash rent with bonus leasing arrangement is a variable cash rent lease that has a base rent and the potential

FEFO 11-17 September 27, 2011 CASH RENT WITH BONUS LEASING ARRANGEMENT: DESCRIPTION AND EXAMPLE A cash rent with bonus leasing arrangement is a variable cash rent lease that has a base rent and the potential

Revenue and Costs for Illinois Grain Crops, Actual for 2012 through 2017, Projected 2018 and 2019

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Illinois Grain Crops, Actual for 2012 through 2017, Projected 2018 and 2019 Department of Agricultural

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Illinois Grain Crops, Actual for 2012 through 2017, Projected 2018 and 2019 Department of Agricultural

Revenue and Costs for Corn, Soybeans, Wheat, and Double-Crop Soybeans, Actual for 2011 through 2016, Projected 2017 and 2018

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Corn, Soybeans, Wheat, and Double-Crop Soybeans, Actual for 2011 through 2016, Projected 2017 and

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Corn, Soybeans, Wheat, and Double-Crop Soybeans, Actual for 2011 through 2016, Projected 2017 and

Fundamental Factors Affecting Agricultural and Other Commodities. Research & Product Development Updated July 11, 2008

Fundamental Factors Affecting Agricultural and Other Commodities Research & Product Development Updated July 11, 2008 Outline Review of key supply and demand factors affecting commodity markets World stocks-to-use

Fundamental Factors Affecting Agricultural and Other Commodities Research & Product Development Updated July 11, 2008 Outline Review of key supply and demand factors affecting commodity markets World stocks-to-use

Credit Conditions for Young and Beginning Farmers. by Nathan S. Kauffman 1

Credit Conditions for Young and Beginning Farmers by Nathan S. Kauffman 1 Introduction Agricultural credit conditions for young and beginning farmers are shaped by lenders perception of the trade-off between

Credit Conditions for Young and Beginning Farmers by Nathan S. Kauffman 1 Introduction Agricultural credit conditions for young and beginning farmers are shaped by lenders perception of the trade-off between

Opportunities and challenges for agriculture. How will agriculture and the swine industry fare in today s economic climate? Opportunities.

The outlook for the swine industry and its relationship with the global economy Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative Center How will agriculture and the

The outlook for the swine industry and its relationship with the global economy Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative Center How will agriculture and the

2012 Drought: Yield Loss, Revenue Loss, and Harvest Price Option Carl Zulauf, Professor, Ohio State University August 2012

2012 Drought: Yield Loss, Revenue Loss, and Harvest Price Option Carl Zulauf, Professor, Ohio State University August 2012 This article examines the impact of the 2012 drought on per acre revenue for corn

2012 Drought: Yield Loss, Revenue Loss, and Harvest Price Option Carl Zulauf, Professor, Ohio State University August 2012 This article examines the impact of the 2012 drought on per acre revenue for corn

Basis for Grains. Why is basis predictable?

Basis for Grains Why is basis predictable? Average basis levels (expectations) are determined by transportation and storage costs associated with the commodity. Variations in basis levels (outcomes) are

Basis for Grains Why is basis predictable? Average basis levels (expectations) are determined by transportation and storage costs associated with the commodity. Variations in basis levels (outcomes) are

THE ROLE OF DEBT IN FARMLAND OWNERSHIP

2nd Quarter 2011 26(2) THE ROLE OF DEBT IN FARMLAND OWNERSHIP Brian C. Briggeman JEL Classifications: Q14, Q15 Keywords: Agricultural Finance, Debt, Farmland Farm real estate debt often plays a key role

2nd Quarter 2011 26(2) THE ROLE OF DEBT IN FARMLAND OWNERSHIP Brian C. Briggeman JEL Classifications: Q14, Q15 Keywords: Agricultural Finance, Debt, Farmland Farm real estate debt often plays a key role

Nebraska Economic Update

Nebraska Economic Update Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City March 26, 215 Overview of the Federal Reserve System The Fed is the Central Bank of the

Nebraska Economic Update Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City March 26, 215 Overview of the Federal Reserve System The Fed is the Central Bank of the

Performance of market advisory firms

Price risk management: What to expect? #3 out of 5 articles Performance of market advisory firms Kim B. Anderson & B. Wade Brorsen This is the third of a five part series on managing price (marketing)

Price risk management: What to expect? #3 out of 5 articles Performance of market advisory firms Kim B. Anderson & B. Wade Brorsen This is the third of a five part series on managing price (marketing)

ACE 427 Spring Lecture 6. by Professor Scott H. Irwin

ACE 427 Spring 2013 Lecture 6 Forecasting Crop Prices with Futures Prices by Professor Scott H. Irwin Required Reading: Schwager, J.D. Ch. 2: For Beginners Only. Schwager on Futures: Fundamental Analysis,

ACE 427 Spring 2013 Lecture 6 Forecasting Crop Prices with Futures Prices by Professor Scott H. Irwin Required Reading: Schwager, J.D. Ch. 2: For Beginners Only. Schwager on Futures: Fundamental Analysis,

WHY WE AREN T LIKELY TO SEE A REPLAY OF THE 1980s FARM CRISIS

WHY WE AREN T LIKELY TO SEE A REPLAY OF THE 1980s FARM CRISIS Wendong Zhang Assistant Professor, Dept. of Economics Iowa State University Why We Aren t Likely to See A Replay of 1980s Farm Crisis Dr. Wendong

WHY WE AREN T LIKELY TO SEE A REPLAY OF THE 1980s FARM CRISIS Wendong Zhang Assistant Professor, Dept. of Economics Iowa State University Why We Aren t Likely to See A Replay of 1980s Farm Crisis Dr. Wendong

Risk & Rewards A Roadmap for Your Farm in By: Mark Jensen SVP & Chief Risk Officer Farm Credit Services of America & Frontier Farm Credit

Risk & Rewards A Roadmap for Your Farm in 2017 By: Mark Jensen SVP & Chief Risk Officer Farm Credit Services of America & Frontier Farm Credit Service Area Overview Serve all of Iowa, Nebraska, South Dakota,

Risk & Rewards A Roadmap for Your Farm in 2017 By: Mark Jensen SVP & Chief Risk Officer Farm Credit Services of America & Frontier Farm Credit Service Area Overview Serve all of Iowa, Nebraska, South Dakota,

CROP BUDGETS, ILLINOIS, 2017

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2017 Department of Agricultural and Consumer Economics University of Illinois July 2017 Introduction

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2017 Department of Agricultural and Consumer Economics University of Illinois July 2017 Introduction

CROP BUDGETS, ILLINOIS, 2019

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2019 Department of Agricultural and Consumer Economics University of Illinois September 2018

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2019 Department of Agricultural and Consumer Economics University of Illinois September 2018

CROP BUDGETS, ILLINOIS, 2018

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2018 Department of Agricultural and Consumer Economics University of Illinois February 2018

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2018 Department of Agricultural and Consumer Economics University of Illinois February 2018

Purdue Outlook Update 2011

Percent Purdue Outlook Update 211 211 Indiana Agricultural Outlook Corinne Alexander & Chris Hurt hurtc@purdue.edu Ethanol World Economic Growth Dollar Value Surprises and Uncertainty! Change Wheat Production

Percent Purdue Outlook Update 211 211 Indiana Agricultural Outlook Corinne Alexander & Chris Hurt hurtc@purdue.edu Ethanol World Economic Growth Dollar Value Surprises and Uncertainty! Change Wheat Production

INSIGHTS FROM AGRICULTURAL LENDERS. January 11 th, 2019 Top Farmer Conference Beck Agricultural Center Dr. Brady Brewer

INSIGHTS FROM AGRICULTURAL LENDERS January 11 th, 2019 Top Farmer Conference Beck Agricultural Center Dr. Brady Brewer bebrewer@purdue.edu AGRICULTURAL LENDER SURVEY Survey expectations and past results

INSIGHTS FROM AGRICULTURAL LENDERS January 11 th, 2019 Top Farmer Conference Beck Agricultural Center Dr. Brady Brewer bebrewer@purdue.edu AGRICULTURAL LENDER SURVEY Survey expectations and past results

How Does an FSA Work?

Andrew Novakovic The EV Baker Professor of Agricultural Economics with acknowledgements to Brent Gloy, Associate Professor, Purdue University and Wayne Knoblauch, Professor, Cornell University May 2011

Andrew Novakovic The EV Baker Professor of Agricultural Economics with acknowledgements to Brent Gloy, Associate Professor, Purdue University and Wayne Knoblauch, Professor, Cornell University May 2011

2009 Rental Decisions Given Volatile Commodity Prices and Higher Input Costs. Gary Schnitkey and Dale Lattz. October 15, 2008 IFEU 08-05

2009 Rental Decisions Given Volatile Commodity Prices and Higher Input Costs Gary Schnitkey and Dale Lattz October 15, 2008 IFEU 08-05 Turmoil within the financial sector has caused concerns about the

2009 Rental Decisions Given Volatile Commodity Prices and Higher Input Costs Gary Schnitkey and Dale Lattz October 15, 2008 IFEU 08-05 Turmoil within the financial sector has caused concerns about the

Ability to Pay and Agriculture Sector Stability. Erin M. Hardin John B. Penson, Jr.

Ability to Pay and Agriculture Sector Stability Erin M. Hardin John B. Penson, Jr. Texas A&M University Department of Agricultural Economics 600 John Kimbrough Blvd 2124 TAMU College Station, TX 77843-2124

Ability to Pay and Agriculture Sector Stability Erin M. Hardin John B. Penson, Jr. Texas A&M University Department of Agricultural Economics 600 John Kimbrough Blvd 2124 TAMU College Station, TX 77843-2124

Investing Agricultural Land. Michael Swanson Ph.D. Wells Fargo

Investing Agricultural Land Michael Swanson Ph.D. Wells Fargo Economic and Commodity Risk Everything is connected. We just can t see how. A single loop from a subsystem Livestock Corn Ethanol Gasoline

Investing Agricultural Land Michael Swanson Ph.D. Wells Fargo Economic and Commodity Risk Everything is connected. We just can t see how. A single loop from a subsystem Livestock Corn Ethanol Gasoline

Delayed and Prevented Planting Provisions for Multiple Peril Crop Insurance

Delayed and Prevented Planting Provisions for Multiple Peril Crop Insurance Most crop producers know that to achieve optimum yields it is important to plant early. Once the danger of a frost is past, the

Delayed and Prevented Planting Provisions for Multiple Peril Crop Insurance Most crop producers know that to achieve optimum yields it is important to plant early. Once the danger of a frost is past, the

GRAIN MARKETS SENSITIVE TO EXPORTS, SOUTH AMERICAN WEATHER

December 15, 1999 Ames, Iowa Econ. Info. 1779 GRAIN MARKETS SENSITIVE TO EXPORTS, SOUTH AMERICAN WEATHER October, November, and the first 10 days of December were unusually dry over a large part of southern

December 15, 1999 Ames, Iowa Econ. Info. 1779 GRAIN MARKETS SENSITIVE TO EXPORTS, SOUTH AMERICAN WEATHER October, November, and the first 10 days of December were unusually dry over a large part of southern

Presentation Outline

The Current and Future Farm Policy Outlook for Corn and Soybeans Joe L. Outlaw Professor & Extension Economist Co-Director, AFPC Minnesota Crop Insurance Conference Mankato, MN September 12, 2013 Presentation

The Current and Future Farm Policy Outlook for Corn and Soybeans Joe L. Outlaw Professor & Extension Economist Co-Director, AFPC Minnesota Crop Insurance Conference Mankato, MN September 12, 2013 Presentation

Top Producer Conference Chicago, Illinois January 21, 2009

Top Producer Conference Chicago, Illinois January 21, 2009 A Primer on Risk Management 2009 Jeff Beal JERRY GULKE S STRATEGIC MARKETING SERVICES, INC. PO BOX 6222, ROCKFORD, IL, 61125 Phone: 602-795-5893

Top Producer Conference Chicago, Illinois January 21, 2009 A Primer on Risk Management 2009 Jeff Beal JERRY GULKE S STRATEGIC MARKETING SERVICES, INC. PO BOX 6222, ROCKFORD, IL, 61125 Phone: 602-795-5893

What variables have historically impacted Kentucky and Iowa farmland values? John Barnhart

What variables have historically impacted Kentucky and Iowa farmland values? John Barnhart Abstract This study evaluates how farmland values and farmland cash rents are affected by cash corn prices, soybean

What variables have historically impacted Kentucky and Iowa farmland values? John Barnhart Abstract This study evaluates how farmland values and farmland cash rents are affected by cash corn prices, soybean

Will We See A Recession This Year?

Will We See A Recession This Year? Rising Rates Are Here This week, the Federal Reserve Bank (Fed) signaled their intention to raise their target interest rate when they meet in mid-march. If they do,

Will We See A Recession This Year? Rising Rates Are Here This week, the Federal Reserve Bank (Fed) signaled their intention to raise their target interest rate when they meet in mid-march. If they do,

Whither the CRP: expirations, enrollments, and responses to changing commodity prices

Whither the CRP: expirations, enrollments, and responses to changing commodity prices Extension Section Crops Outlook track session AAEA Annual Meeting, July 2010 Denver, CO Daniel Hellerstein, ERS/USDA

Whither the CRP: expirations, enrollments, and responses to changing commodity prices Extension Section Crops Outlook track session AAEA Annual Meeting, July 2010 Denver, CO Daniel Hellerstein, ERS/USDA

BUYERS, BUBBLES, AND BUTTERFLIES Senior Analyst Darin Newsom. DTN/The Progressive Farmer 2010 Ag Summit December 10, 2010

BUYERS, BUBBLES, AND BUTTERFLIES Senior Analyst Darin Newsom DTN/The Progressive Farmer 2010 Ag Summit December 10, 2010 Buyers -! "In other words, demand driven markets! "Demand driven markets: Increased

BUYERS, BUBBLES, AND BUTTERFLIES Senior Analyst Darin Newsom DTN/The Progressive Farmer 2010 Ag Summit December 10, 2010 Buyers -! "In other words, demand driven markets! "Demand driven markets: Increased

Comparison of Hedging Cost with Other Variable Input Costs. John Michael Riley and John D. Anderson

Comparison of Hedging Cost with Other Variable Input Costs by John Michael Riley and John D. Anderson Suggested citation i format: Riley, J. M., and J. D. Anderson. 009. Comparison of Hedging Cost with

Comparison of Hedging Cost with Other Variable Input Costs by John Michael Riley and John D. Anderson Suggested citation i format: Riley, J. M., and J. D. Anderson. 009. Comparison of Hedging Cost with

2014 Iowa Farm Business Management Career Development Event. INDIVIDUAL EXAM (150 pts.)

") 2014 Iowa Farm Business Management Career Development Event INDIVIDUAL EXAM (150 pts.) Select the best answer to each of the 75 questions to follow (2 pts. ea.). Code your answers on the answer sheet provided.

2014 Iowa Farm Business Management Career Development Event INDIVIDUAL EXAM (150 pts.) Select the best answer to each of the 75 questions to follow (2 pts. ea.). Code your answers on the answer sheet provided.

CHS Pro Advantage Update- February Corn

CHS Pro Advantage Update- February 2018 Corn Recap and Outlook- The most important thing that happened in corn since our last update is the breakout of the 2 ½ month trading range that had existed prior

CHS Pro Advantage Update- February 2018 Corn Recap and Outlook- The most important thing that happened in corn since our last update is the breakout of the 2 ½ month trading range that had existed prior

Step Up Your Grain Game! Crop Economics for 2018

Step Up Your Grain Game! Crop Economics for 2018............................... Roy Arnott, P.Ag. & Darren Bond, P.Ag. Farm Management Specialists What we already know Doing your cost of production for

Step Up Your Grain Game! Crop Economics for 2018............................... Roy Arnott, P.Ag. & Darren Bond, P.Ag. Farm Management Specialists What we already know Doing your cost of production for

BUSINESS AND MARKETING TOOLS FOR PROFITABLE FARMING. Summer Crossroads: Volatility and Opportunity. Bryce Knorr Farm Futures Magazine

Summer Crossroads: Volatility and Opportunity Bryce Knorr Farm Futures Magazine Don t Bury The Lead Why were soybeans up more than 50 cents despite higher acres? 2014 crop likely smaller Acreage up in

Summer Crossroads: Volatility and Opportunity Bryce Knorr Farm Futures Magazine Don t Bury The Lead Why were soybeans up more than 50 cents despite higher acres? 2014 crop likely smaller Acreage up in

ARPA Subsidies, Unit Choice, and Reform of the U.S. Crop Insurance Program

CARD Briefing Papers CARD Reports and Working Papers 2-2005 ARPA Subsidies, Unit Choice, and Reform of the U.S. Crop Insurance Program Bruce A. Babcock Iowa State University, babcock@iastate.edu Chad E.

CARD Briefing Papers CARD Reports and Working Papers 2-2005 ARPA Subsidies, Unit Choice, and Reform of the U.S. Crop Insurance Program Bruce A. Babcock Iowa State University, babcock@iastate.edu Chad E.

The Farm Safety Net: The Good and Not So Good Michael Boehlje and Michael Langemeier Center for Commercial Agriculture Purdue University

The Farm Safety Net: The Good and Not So Good Michael Boehlje and Michael Langemeier Center for Commercial Agriculture Purdue University USDA recently announced that they project net farm income to decline

The Farm Safety Net: The Good and Not So Good Michael Boehlje and Michael Langemeier Center for Commercial Agriculture Purdue University USDA recently announced that they project net farm income to decline

Jason Henderson Vice President and Branch Executive Federal Reserve Bank of Kansas City Omaha Branch September 2012

Jason Henderson Vice President and Branch Executive September 2012 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or

Jason Henderson Vice President and Branch Executive September 2012 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or

Kansas State University Department Of Agricultural Economics Extension Publication 08/30/2017

Margin Protection Crop Insurance Coverage Comes to Kansas Monte Vandeveer (montev@ksu.edu) Kansas State University Department of Agricultural Economics August 2017 A new form of crop insurance coverage

Margin Protection Crop Insurance Coverage Comes to Kansas Monte Vandeveer (montev@ksu.edu) Kansas State University Department of Agricultural Economics August 2017 A new form of crop insurance coverage

ARC vs. PLC Enrollment Decisions

ARC vs. PLC Enrollment Decisions April 2014 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management FSA Commodity Crop

ARC vs. PLC Enrollment Decisions April 2014 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management FSA Commodity Crop

Loan Deficiency Payments versus Countercyclical Payments: Do We Need Both for a Price Safety Net?

CARD Briefing Papers CARD Reports and Working Papers 2-2005 Loan Deficiency Payments versus Countercyclical Payments: Do We Need Both for a Price Safety Net? Chad E. Hart Iowa State University, chart@iastate.edu

CARD Briefing Papers CARD Reports and Working Papers 2-2005 Loan Deficiency Payments versus Countercyclical Payments: Do We Need Both for a Price Safety Net? Chad E. Hart Iowa State University, chart@iastate.edu

UK Grain Marketing Series January 19, Todd D. Davis Assistant Extension Professor. Economics

Introduction to Basis, Cash Forward Contracts, HTA Contracts and Basis Contracts UK Grain Marketing Series January 19, 2016 Todd D. Davis Assistant Extension Professor Outline What is basis and how can

Introduction to Basis, Cash Forward Contracts, HTA Contracts and Basis Contracts UK Grain Marketing Series January 19, 2016 Todd D. Davis Assistant Extension Professor Outline What is basis and how can

How the Federal Reserve Can Affect Agriculture

How the Federal Reserve Can Affect Agriculture 2012 2013 Ag Profitability Conferences Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative Center The Federal Reserve System

How the Federal Reserve Can Affect Agriculture 2012 2013 Ag Profitability Conferences Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative Center The Federal Reserve System

Soybeans face long road End to tariffs wouldn t help 2018 exports much By Bryce Knorr, senior grain market analyst

Soybeans face long road End to tariffs wouldn t help 2018 exports much By Bryce Knorr, senior grain market analyst Forecasting grain prices is relatively easy in normal times. Most models assume the future

Soybeans face long road End to tariffs wouldn t help 2018 exports much By Bryce Knorr, senior grain market analyst Forecasting grain prices is relatively easy in normal times. Most models assume the future

What s Moving in Markets in Top Producer January 30, Presented by Dave Fogel, Risk Management Advisor

What s Moving in Markets in 2014 2014 Top Producer January 30, 2014 Presented by Dave Fogel, Risk Management Advisor 800 664 2321 www.advance trading.com Who we are. Company started in 1979 and was incorporated

What s Moving in Markets in 2014 2014 Top Producer January 30, 2014 Presented by Dave Fogel, Risk Management Advisor 800 664 2321 www.advance trading.com Who we are. Company started in 1979 and was incorporated

Does Crop Insurance Enrollment Exacerbate the Negative Effects of Extreme Heat? A Farm-level Analysis

Does Crop Insurance Enrollment Exacerbate the Negative Effects of Extreme Heat? A Farm-level Analysis Madhav Regmi and Jesse B. Tack Department of Agricultural Economics, Kansas State University August

Does Crop Insurance Enrollment Exacerbate the Negative Effects of Extreme Heat? A Farm-level Analysis Madhav Regmi and Jesse B. Tack Department of Agricultural Economics, Kansas State University August

Steven D. Johnson. Presentation Objectives

January 30, 2013 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management Presentation Objectives Define Shallow Loss

January 30, 2013 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management Presentation Objectives Define Shallow Loss

The federal crop insurance program is ripe for reform: TWO CHANGES TO CROP INSURANCE TO IMPROVE EQUITY AND EFFICIENCY

CONTENTS Introduction 1 Means-Testing Crop Insurance Subsidies 1 How Crop Insurance is Subsidized 2 The Crop Insurance Industry s Position 3 Impacts of Limiting Premium Subsidies 3 Eliminating Subsidies

CONTENTS Introduction 1 Means-Testing Crop Insurance Subsidies 1 How Crop Insurance is Subsidized 2 The Crop Insurance Industry s Position 3 Impacts of Limiting Premium Subsidies 3 Eliminating Subsidies

Agricultural Economic Update

Agricultural Economic Update March 2, 217 Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City The views expressed are those of the author and do not necessarily reflect

Agricultural Economic Update March 2, 217 Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City The views expressed are those of the author and do not necessarily reflect

Crop Insurance Strategies for

Crop Insurance Strategies for 2018 Why is Crop Insurance Important for Risk Management? Creates a Foundation to build upon Makes a big impact on marketing throughout the year Changes your Risk/Profitability

Crop Insurance Strategies for 2018 Why is Crop Insurance Important for Risk Management? Creates a Foundation to build upon Makes a big impact on marketing throughout the year Changes your Risk/Profitability

Wheat Outlook August 19, 2013 Volume 22, Number 45

Market Situation Today s Newsletter Market Situation Crop Progress 1 Weather 1 Crop Progress. The winter wheat harvest is 96% complete as of August 18th, just ahead of the normal pace of 94%. The spring

Market Situation Today s Newsletter Market Situation Crop Progress 1 Weather 1 Crop Progress. The winter wheat harvest is 96% complete as of August 18th, just ahead of the normal pace of 94%. The spring

Nebraska Economic Outlook

Nebraska Economic Outlook Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City August 3, 16 The views expressed are those of the author and do not necessarily reflect

Nebraska Economic Outlook Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City August 3, 16 The views expressed are those of the author and do not necessarily reflect

ACE 427 Spring Lecture 5. by Professor Scott H. Irwin

ACE 427 Spring 2013 Lecture 5 Forecasting Crop Prices Using Fundamental Analysis: Ending Stock Models by Professor Scott H. Irwin Required Reading: Westcott, P.C. and L.A. Hoffman. Price Determination

ACE 427 Spring 2013 Lecture 5 Forecasting Crop Prices Using Fundamental Analysis: Ending Stock Models by Professor Scott H. Irwin Required Reading: Westcott, P.C. and L.A. Hoffman. Price Determination

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas Daniel O Brien, Extension Agricultural Economist Kansas State University August 10, 2016 Summary

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas Daniel O Brien, Extension Agricultural Economist Kansas State University August 10, 2016 Summary

Development of a Market Benchmark Price for AgMAS Performance Evaluations. Darrel L. Good, Scott H. Irwin, and Thomas E. Jackson

Development of a Market Benchmark Price for AgMAS Performance Evaluations by Darrel L. Good, Scott H. Irwin, and Thomas E. Jackson Development of a Market Benchmark Price for AgMAS Performance Evaluations

Development of a Market Benchmark Price for AgMAS Performance Evaluations by Darrel L. Good, Scott H. Irwin, and Thomas E. Jackson Development of a Market Benchmark Price for AgMAS Performance Evaluations

Managing Machinery Expenses

Managing Machinery Expenses Dr. Gregg Ibendahl, Mark Wood, & Doug Stucky Kansas State University Email: ibendahl@ksu.edu mawood@ksu.edu dstucky@ksu.edu Phone: 785-477-2071 785-462-6664 620-225-5600 Machinery

Managing Machinery Expenses Dr. Gregg Ibendahl, Mark Wood, & Doug Stucky Kansas State University Email: ibendahl@ksu.edu mawood@ksu.edu dstucky@ksu.edu Phone: 785-477-2071 785-462-6664 620-225-5600 Machinery

FACT SHEET. Fundamentally, risk management. A Primer on Crop Insurance AGRICULTURE & NATURAL RESOURCES JAN 2016 COLLEGE OF

COLLEGE OF AGRICULTURE & NATURAL RESOURCES FACT SHEET DEPARTMENT OF AGRICULTURAL AND RESOURCE ECONOMICS JAN 2016 A Primer on Crop Insurance Most crop insurance takes one of two forms: yield insurance pays

COLLEGE OF AGRICULTURE & NATURAL RESOURCES FACT SHEET DEPARTMENT OF AGRICULTURAL AND RESOURCE ECONOMICS JAN 2016 A Primer on Crop Insurance Most crop insurance takes one of two forms: yield insurance pays

Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC)

vs. Price Loss Coverage (PLC)") Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC) Background The 2014 Farm Bill provides several alternative farm programs for mitigating farm production and price risks. The purpose of the

Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC) Background The 2014 Farm Bill provides several alternative farm programs for mitigating farm production and price risks. The purpose of the

Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University

Agricultural Lender Survey Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University Results: Fall Survey, 2015 Survey Summary

Agricultural Lender Survey Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University Results: Fall Survey, 2015 Survey Summary

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

New Generation Grain Marketing Contracts

New Generation Grain Marketing Contracts by Lewis A. Hagedorn, Scott H. Irwin, Darrel L. Good, Joao Martines-Filho, Bruce J. Sherrick, and Gary D. Schnitkey New Generation Grain Marketing Contracts by

New Generation Grain Marketing Contracts by Lewis A. Hagedorn, Scott H. Irwin, Darrel L. Good, Joao Martines-Filho, Bruce J. Sherrick, and Gary D. Schnitkey New Generation Grain Marketing Contracts by

Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC)

vs. Price Loss Coverage (PLC)") Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC) Background The 2014 Farm Bill provides several alternative farm programs for mitigating farm production and price risks. The purpose of the

Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC) Background The 2014 Farm Bill provides several alternative farm programs for mitigating farm production and price risks. The purpose of the

Module 12. Alternative Yield and Price Risk Management Tools for Wheat

Topics Module 12 Alternative Yield and Price Risk Management Tools for Wheat George Flaskerud, North Dakota State University Bruce A. Babcock, Iowa State University Art Barnaby, Kansas State University

Topics Module 12 Alternative Yield and Price Risk Management Tools for Wheat George Flaskerud, North Dakota State University Bruce A. Babcock, Iowa State University Art Barnaby, Kansas State University

Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC)

vs. Price Loss Coverage (PLC)") Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC) Background The 2014 Farm Bill provides several alternative farm programs for mitigating farm production and price risks. The purpose of the

Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC) Background The 2014 Farm Bill provides several alternative farm programs for mitigating farm production and price risks. The purpose of the

Chapter 4. Agricultural Finance Calum G. Turvey, W.I. Myers Professor of Agricultural Finance

Chapter 4. Calum G. Turvey, W.I. Myers Professor of General Outlook The financial condition of New York s agricultural economy in 2014 is holding steady if not improving over 2013. Although there is some

Chapter 4. Calum G. Turvey, W.I. Myers Professor of General Outlook The financial condition of New York s agricultural economy in 2014 is holding steady if not improving over 2013. Although there is some

Farm Real Estate Investments: Headwinds, Tailwinds and Developing Issues

Farm Real Estate Investments: Headwinds, Tailwinds and Developing Issues ISPFMRA Land Values and Lease Trends March 17, 2016 Bloomington, Illinois Bruce J. Sherrick, Ph.D. TIAA-CREF Center for Farmland

Farm Real Estate Investments: Headwinds, Tailwinds and Developing Issues ISPFMRA Land Values and Lease Trends March 17, 2016 Bloomington, Illinois Bruce J. Sherrick, Ph.D. TIAA-CREF Center for Farmland

Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC)

vs. Price Loss Coverage (PLC)") Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC) Background The 2014 Farm Bill provides several alternative farm programs for mitigating farm production and price risks. The purpose of the

Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC) Background The 2014 Farm Bill provides several alternative farm programs for mitigating farm production and price risks. The purpose of the

1. A put option contains the right to a futures contract. 2. A call option contains the right to a futures contract.

Econ 337 Name Midterm Spring 2017 100 points possible 3/28/2017 Fill in the blanks (2 points each) 1. A put option contains the right to a futures contract. 2. A call option contains the right to a futures

Econ 337 Name Midterm Spring 2017 100 points possible 3/28/2017 Fill in the blanks (2 points each) 1. A put option contains the right to a futures contract. 2. A call option contains the right to a futures

Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC)

vs. Price Loss Coverage (PLC)") Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC) Background The 2014 Farm Bill provides several alternative farm programs for mitigating farm production and price risks. The purpose of the

Agricultural Risk Coverage (ARC) vs. Price Loss Coverage (PLC) Background The 2014 Farm Bill provides several alternative farm programs for mitigating farm production and price risks. The purpose of the

Evaluating the Use of Futures Prices to Forecast the Farm Level U.S. Corn Price

Evaluating the Use of Futures Prices to Forecast the Farm Level U.S. Corn Price By Linwood Hoffman and Michael Beachler 1 U.S. Department of Agriculture Economic Research Service Market and Trade Economics

Evaluating the Use of Futures Prices to Forecast the Farm Level U.S. Corn Price By Linwood Hoffman and Michael Beachler 1 U.S. Department of Agriculture Economic Research Service Market and Trade Economics

Under the 1996 farm bill, producers have increased planting flexibility, which. Producer Ability to Forecast Harvest Corn and Soybean Prices

Review of Agricultural Economics Volume 23, Number 1 Pages 151 162 Producer Ability to Forecast Harvest Corn and Soybean Prices David E. Kenyon Harvest-price expectations for corn and soybeans were obtained

Review of Agricultural Economics Volume 23, Number 1 Pages 151 162 Producer Ability to Forecast Harvest Corn and Soybean Prices David E. Kenyon Harvest-price expectations for corn and soybeans were obtained

2015 COTTON MARKET OUTLOOK AND RISK MANAGEMENT DECISIONS

2015 COTTON MARKET OUTLOOK AND RISK MANAGEMENT DECISIONS A A R O N S M I T H, P H. D. R O W C R O P E C O N O M I S T UNIVERSITY OF TENNESSEE EXTENSION AARON.SMITH@UTK.EDU HTTP://ECONOMICS.AG.UTK.EDU/CROP.HTML

2015 COTTON MARKET OUTLOOK AND RISK MANAGEMENT DECISIONS A A R O N S M I T H, P H. D. R O W C R O P E C O N O M I S T UNIVERSITY OF TENNESSEE EXTENSION AARON.SMITH@UTK.EDU HTTP://ECONOMICS.AG.UTK.EDU/CROP.HTML

AAPEX February Two Iowa Sales Sioux County. Chicago Fed Survey October Iowa Realtors Survey November, 2010

The Farmland Market: Buy, Sell, Hold Average Value Per Acre of Iowa Farmland Source: Iowa Agriculture Experiment Station The Market Two Iowa Sales Sioux County Parcel 1 80 acres, 70+ GSR - $3,260 Parcel

The Farmland Market: Buy, Sell, Hold Average Value Per Acre of Iowa Farmland Source: Iowa Agriculture Experiment Station The Market Two Iowa Sales Sioux County Parcel 1 80 acres, 70+ GSR - $3,260 Parcel

INSIGHTS REPORT VOLUME 08 WHAT S INSIDE. A variable swine market means there are key areas producers should focus on for shortand long-term planning.

INSIGHTS REPORT VOLUME 08 WHAT S INSIDE A variable swine market means there are key areas producers should focus on for shortand long-term planning. With the current state of the ag economy, it s more

INSIGHTS REPORT VOLUME 08 WHAT S INSIDE A variable swine market means there are key areas producers should focus on for shortand long-term planning. With the current state of the ag economy, it s more

Market Outlook. David Reinbott.

Market Outlook David Reinbott Agriculture Business Specialist P.O. Box 187 Benton, MO 63736 (573) 545-3516 http://extension.missouri.edu/scott/agriculture.aspx reinbottd@missouri.edu Cotton Fundamentals

Market Outlook David Reinbott Agriculture Business Specialist P.O. Box 187 Benton, MO 63736 (573) 545-3516 http://extension.missouri.edu/scott/agriculture.aspx reinbottd@missouri.edu Cotton Fundamentals

AGRICULTURAL LENDER SURVEY RESULTS

Summer 2017 AGRICULTURAL LENDER SURVEY RESULTS Summer 2017 / Agricultural Lender Survey Results / 1 Contents Key Takeaways... 3 Introduction... 4 Agricultural Economy... 5 Farm Profitability and Economic

Summer 2017 AGRICULTURAL LENDER SURVEY RESULTS Summer 2017 / Agricultural Lender Survey Results / 1 Contents Key Takeaways... 3 Introduction... 4 Agricultural Economy... 5 Farm Profitability and Economic

October 12, Corn

October 12, 2018 Corn The only program currently open in Corn is the 2-year 2019 expiration contract. The daily chart covers the timeframe that the 2-year contract has been open. The relevant point here

October 12, 2018 Corn The only program currently open in Corn is the 2-year 2019 expiration contract. The daily chart covers the timeframe that the 2-year contract has been open. The relevant point here

Commodity Programs in 2014 Farm Bill. Key Provisions

Commodity Programs in 2014 Farm Bill Gary Schnitkey, Jonathan Coppess, Nick Paulson, and Carl Zulauf University of Illinois The Ohio State University (February 13, 2014) 1 Key Provisions Eliminates direct,

Commodity Programs in 2014 Farm Bill Gary Schnitkey, Jonathan Coppess, Nick Paulson, and Carl Zulauf University of Illinois The Ohio State University (February 13, 2014) 1 Key Provisions Eliminates direct,

factors that affect marketing

Grain Marketing / no. 26 factors that affect marketing Crop Insurance Coverage Producers who buy at least 80 percent Revenue Protection for corn are more likely to indicate that crop insurance is an important

Grain Marketing / no. 26 factors that affect marketing Crop Insurance Coverage Producers who buy at least 80 percent Revenue Protection for corn are more likely to indicate that crop insurance is an important

Reinsuring Group Revenue Insurance with. Exchange-Provided Revenue Contracts. Bruce A. Babcock, Dermot J. Hayes, and Steven Griffin

Reinsuring Group Revenue Insurance with Exchange-Provided Revenue Contracts Bruce A. Babcock, Dermot J. Hayes, and Steven Griffin CARD Working Paper 99-WP 212 Center for Agricultural and Rural Development

Reinsuring Group Revenue Insurance with Exchange-Provided Revenue Contracts Bruce A. Babcock, Dermot J. Hayes, and Steven Griffin CARD Working Paper 99-WP 212 Center for Agricultural and Rural Development