When Do Farm Booms Become Bubbles?

|

|

|

- Monica Higgins

- 6 years ago

- Views:

Transcription

1 When Do Farm Booms Become Bubbles? Brent Gloy Director, Center for Commercial Agriculture 2012 Agricultural Symposium Federal Reserve Bank of Kansas City Kansas City, MO July 16, 2012

2 Background Agriculture s history includes periods of remarkable boom and bust Agriculture is capital intensive Large increases in profitability make fixed assets priced in less profitable times look cheap Key Questions: Will these times last or will we retreat to previous levels? Are farmland values in a speculative bubble or responding normally to economic conditions?

3 Types of Shocks which Alter Farming Profitability Demand driven: Expansion of demand which calls for more output at all price levels For example, biofuels and income growth and food demand in emerging markets Persistent demand growth can substantially increase land values and capital investment Supply induced: Supply contraction where less is available at all price levels Short-term weather shocks do not typically impact fixed asset values Inability of supply to keep up with normal demand expansion. If true could lead asset value increases Current situation is complicated by interaction of both impacts and extremely low interest rates which make future income more valuable

4 So How Big are the Recent Increases in Farmland Values?

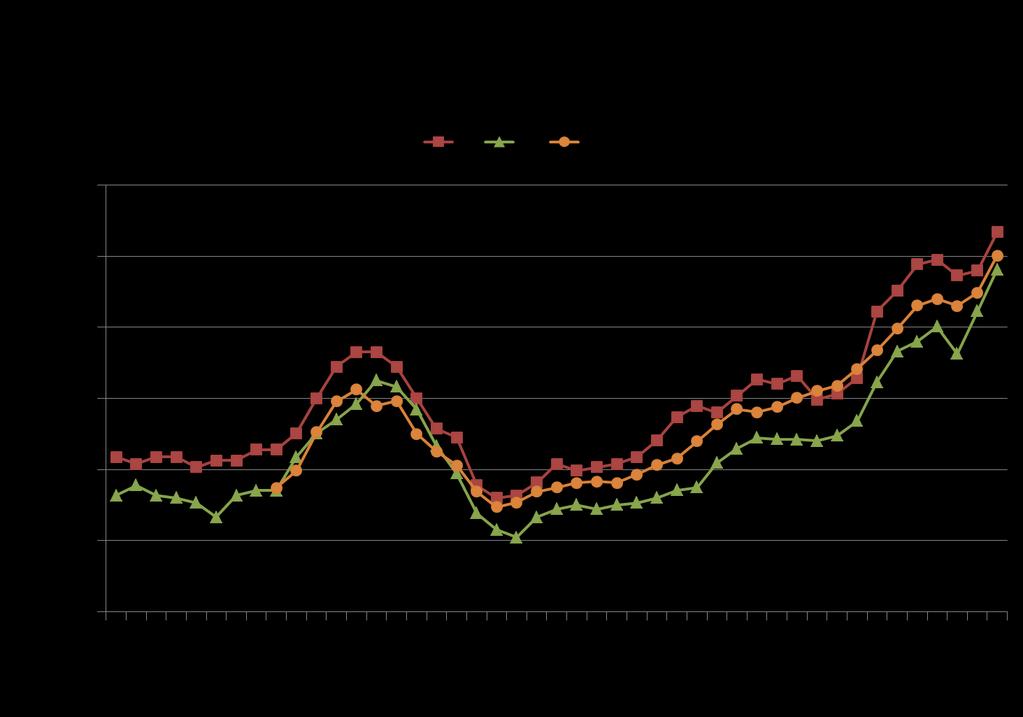

5 In Real Terms, Today s Farmland Value Increases are on Par with those of the 70 s Region Nominal Change Annualized Growth Rate Real Change and Annualized Growth Rate Iowa Percent Illinois Indiana a Iowa farmland values from the Iowa State Farmland Survey (Duffy). Indiana, Illinois, and U.S. Values from National Agricultural Statistics Service. Real values calculated using the CPI index.

6 What is a Bubble? Economists: Substantial and long-lasting divergence of asset prices from what would be determined from the rational expectation of the present value of cash flows from the asset (Malkiel) If the reason that the price is high today is only because investors believe that the selling price will be high tomorrow when fundamental factors do not seem to justify such a price then a bubble exists. (Stiglitz)

7 Economists Investors value assets on expectations of fundamentals (the value of future earnings) Problem: We don t really observe expectations just asset prices Bubbles nearly impossible to predict ex ante Most examples of bubbles (tulips, South Sea, etc.) could be plausibly rationalized in hindsight Speculative bubbles by this definition are very rare

8 On the Other Hand Most people associate the term bubble with large price increases and decreases over a short time Usually started by shifts that greatly increase the expectations of future profits generated by an asset (Malkiel) Investor psychology can play a key role (Shiller) Can be prone to feedback loops high prices encourage higher prices Shortage illusions Other irrational behavior

9 Bubbles. you get a bubble when a very high percentage of the population buys into some originally sound premise. that (the premise) becomes distorted as time passes and people forget the original sound premise and start focusing solely on the price action. Excerpt from Warren Buffett s interview with the Financial Crisis Inquiry Commission

10 How Does This Apply to the Farmland Situation? Fundamentals have undergone dramatic changes Increased demand Reduced interest rates Supply shocks Are market participants evaluating these factors when pricing farmland?

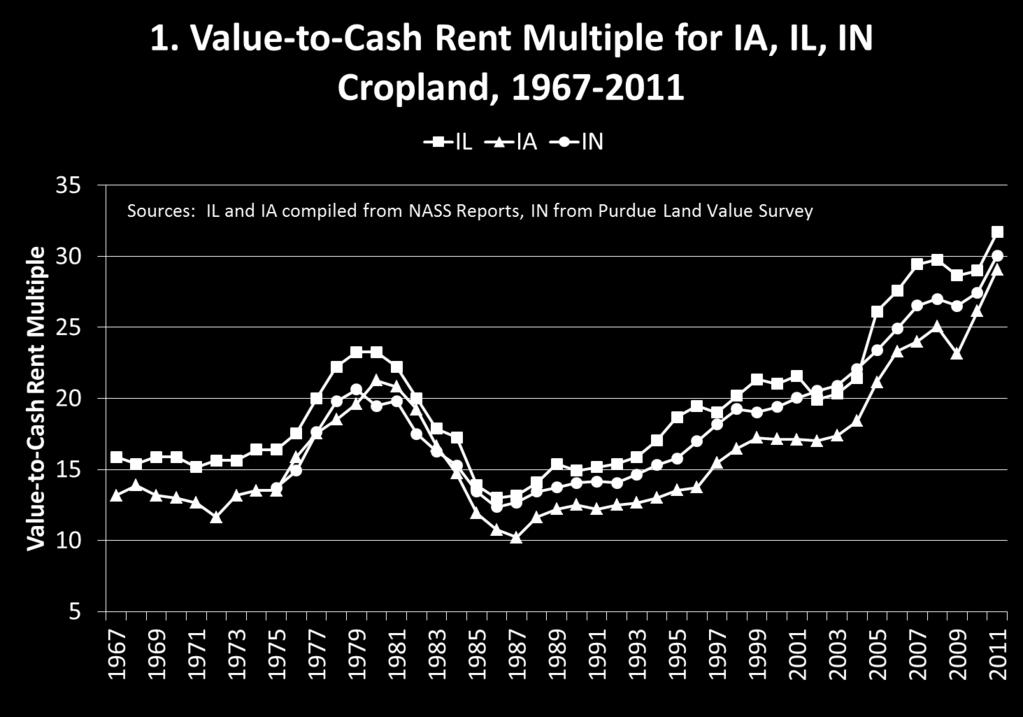

11 Let s Examine the Fundamentals 1. The price of earnings and interest rates 2. Sector level relationship between returns and values 3. Farm level returns 4. Farm level interaction of returns and interest rates

12

13

140.0 120.0 100.0 80.0 60.0 40.0 20.")

14 F Billion Dollars Returns to Farm Operators plus Interest and Rent, (2005 USD)

15 F 12% 2.Returns to Farm Operators plus Interest and Rent Divided by Farm Production Assets, (2005 USD) Rate of Return 10 Yr Rolling Avg 5 Yr Rolling Average 10% 8% 6% 4% 2% 0%

16

17

18 Investor Expectations Drive Prices Current values are dependent upon continuation of low interest rates and high farm returns over variable costs Conducted and internet survey in Spring 2012 What do farmland investors think about future Farmland prices Cash rents Crop prices

19 The Respondents Individuals in CCA database with interest in farmland and farming 246 complete responses (28%) 73% owned farmland 74% want to purchase more farmland in the next 5 years Median acres owned = 500 rented from others = 1,200 rented to others = 240

20

21 Respondents asked to consider: 80 Acres of Farmland with a production capability of 165 bushels of corn per acre under normal rain-fed conditions

22

23 Farmland Values Average There is a 1 in 10 chance that the 4,550 farm will be worth less than The farm will most likely be worth 6,953 There is a 1 in 10 chance that the farm would be worth more than 9,145

24 Cash Rental Rate Average There is a 1 in 10 chance that the cash 201 rental rate will be less than The cash rental rate will most likely be 267 There is a 1 in 10 chance that the cash 342 rental rate will be greater than

25 On average, respondents expect similar multiples in the future

26 Corn price expectations all over the map but generally above $5.00/bu Corn Prices Average There is a 1 in 10 Chance that the average corn price will be less than $3.93 The average corn price will most likely be $5.41 There is a 1 in 10 Chance that the average corn price will be greater than $7.19

27 Almost no systematic relationship between perception of land value and expected corn prices

28 Most would use some debt to fund additional purchases

29 Summary Price increases are on par with most dramatic seen in the last 50 years Prices clearly reflect view that returns over variable costs stay high and rates stay low It is unlikely that farmland fits the classic economic definition of a bubble, but this does not rule out the possibility that prices could fall substantially

30 Summary Investors: Show cautious optimism about farmland investments Have some concern that market in a bubble Appear to be comfortable with multiples approaching expect them to be maintained Expect corn prices to exceed $5.00/bu on average When values compared against corn prices there is little relationship

31 Conclusions Current rates of return are falling to relatively low levels should point to asset prices leveling off Negative demand shock would create significant pressure on land prices Despite some warning signs investors appear to be rationally evaluating fundamentals Most investors expect modest price increases going forward Those with very optimistic views may push prices higher but there is obvious concern on part of others

Farmland Values Will the Boom Turn Bust?

Farmland Values Will the Boom Turn Bust? Top Producer Seminar January 30, 2013 Brent Gloy Director, Center for Commercial Agriculture Bgloy@purdue.edu 765 494 0468 Agenda Is it a bubble? How much higher

Farmland Values Will the Boom Turn Bust? Top Producer Seminar January 30, 2013 Brent Gloy Director, Center for Commercial Agriculture Bgloy@purdue.edu 765 494 0468 Agenda Is it a bubble? How much higher

What s Ahead for Farmland Trends? How do Young Farmers Fit In?

What s Ahead for Farmland Trends? How do Young Farmers Fit In? Tomorrow s Top Producer Seminar January 29, 2013 Brent Gloy Director, Center for Commercial Agriculture Bgloy@purdue.edu 765-494-0468 Agenda

What s Ahead for Farmland Trends? How do Young Farmers Fit In? Tomorrow s Top Producer Seminar January 29, 2013 Brent Gloy Director, Center for Commercial Agriculture Bgloy@purdue.edu 765-494-0468 Agenda

A Symposium Sponsored by the Federal Reserve Bank of Kansas City July 16-17, Session 1: When Do Farm Booms Become Bubbles?

A Symposium Sponsored by the Federal Reserve Bank of Kansas City July 16-17, 2012 Session 1: When Do Farm Booms Become Bubbles? When Do Farm Booms Become Bubbles? (Manuscript) Dr. Brent Gloy Director,

A Symposium Sponsored by the Federal Reserve Bank of Kansas City July 16-17, 2012 Session 1: When Do Farm Booms Become Bubbles? When Do Farm Booms Become Bubbles? (Manuscript) Dr. Brent Gloy Director,

Finding Your Financial Footing in 2016

Finding Your Financial Footing in 2016 York Ag Expo York, NE January 13, 2016 Brent Gloy, LLC www.ageconomists.com bgloy@ageconomists.com Twitter: @BrentGloy Agenda The situation The outlook in 12 questions

Finding Your Financial Footing in 2016 York Ag Expo York, NE January 13, 2016 Brent Gloy, LLC www.ageconomists.com bgloy@ageconomists.com Twitter: @BrentGloy Agenda The situation The outlook in 12 questions

MANAGING THE RISK CAPTURING THE OPPORTUNITY IN CROP FARMING. Michael Boehlje and Brent Gloy Center for Commercial Agriculture Purdue University

MANAGING THE RISK CAPTURING THE OPPORTUNITY IN CROP FARMING by Michael Boehlje and Brent Gloy Center for Commercial Agriculture Purdue University Farming has always been a risky business with the returns

MANAGING THE RISK CAPTURING THE OPPORTUNITY IN CROP FARMING by Michael Boehlje and Brent Gloy Center for Commercial Agriculture Purdue University Farming has always been a risky business with the returns

Investing Agricultural Land. Michael Swanson Ph.D. Wells Fargo

Investing Agricultural Land Michael Swanson Ph.D. Wells Fargo Economic and Commodity Risk Everything is connected. We just can t see how. A single loop from a subsystem Livestock Corn Ethanol Gasoline

Investing Agricultural Land Michael Swanson Ph.D. Wells Fargo Economic and Commodity Risk Everything is connected. We just can t see how. A single loop from a subsystem Livestock Corn Ethanol Gasoline

Jason Henderson Vice President and Branch Executive Federal Reserve Bank of Kansas City Omaha Branch April 10, 2012

Jason Henderson Vice President and Branch Executive April 1, 212 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or the

Jason Henderson Vice President and Branch Executive April 1, 212 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or the

Purdue Agricultural Economics Report

Purdue Agricultural Economics Report November 2011 Managing The Risk Capturing The Opportunity In Crop Farming Michael Boehlje and Brent Gloy*, Center for Commercial Agriculture Farming has always been

Purdue Agricultural Economics Report November 2011 Managing The Risk Capturing The Opportunity In Crop Farming Michael Boehlje and Brent Gloy*, Center for Commercial Agriculture Farming has always been

Farm Finance Update. Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City. March 17, 2017

Farm Finance Update March 17, 2017 Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City The views expressed are those of the author and do not necessarily reflect the

Farm Finance Update March 17, 2017 Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City The views expressed are those of the author and do not necessarily reflect the

Macroeconomic Outlook for U.S. Agriculture

Macroeconomic Outlook for U.S. Agriculture Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City May 18, 216 The views expressed are those of the author and do not necessarily

Macroeconomic Outlook for U.S. Agriculture Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City May 18, 216 The views expressed are those of the author and do not necessarily

THE ROLE OF DEBT IN FARMLAND OWNERSHIP

2nd Quarter 2011 26(2) THE ROLE OF DEBT IN FARMLAND OWNERSHIP Brian C. Briggeman JEL Classifications: Q14, Q15 Keywords: Agricultural Finance, Debt, Farmland Farm real estate debt often plays a key role

2nd Quarter 2011 26(2) THE ROLE OF DEBT IN FARMLAND OWNERSHIP Brian C. Briggeman JEL Classifications: Q14, Q15 Keywords: Agricultural Finance, Debt, Farmland Farm real estate debt often plays a key role

Risk & Rewards A Roadmap for Your Farm in By: Mark Jensen SVP & Chief Risk Officer Farm Credit Services of America & Frontier Farm Credit

Risk & Rewards A Roadmap for Your Farm in 2017 By: Mark Jensen SVP & Chief Risk Officer Farm Credit Services of America & Frontier Farm Credit Service Area Overview Serve all of Iowa, Nebraska, South Dakota,

Risk & Rewards A Roadmap for Your Farm in 2017 By: Mark Jensen SVP & Chief Risk Officer Farm Credit Services of America & Frontier Farm Credit Service Area Overview Serve all of Iowa, Nebraska, South Dakota,

DCP VERSUS ACRE in 2013 For Indiana Farms

DCP VERSUS ACRE in 2013 For Indiana Farms The extension of the last farm bill for 2013 crops means that individuals need to make the decision of whether to participate in the regular Direct and Countercyclical

DCP VERSUS ACRE in 2013 For Indiana Farms The extension of the last farm bill for 2013 crops means that individuals need to make the decision of whether to participate in the regular Direct and Countercyclical

How Does an FSA Work?

Andrew Novakovic The EV Baker Professor of Agricultural Economics with acknowledgements to Brent Gloy, Associate Professor, Purdue University and Wayne Knoblauch, Professor, Cornell University May 2011

Andrew Novakovic The EV Baker Professor of Agricultural Economics with acknowledgements to Brent Gloy, Associate Professor, Purdue University and Wayne Knoblauch, Professor, Cornell University May 2011

An Analysis of Historical Illinois Farmland Valuations

Southern Illinois University Carbondale OpenSIUC Research Papers Graduate School Fall 2016 An Analysis of Historical Illinois Farmland Valuations Benjamin Johnson bj89@siu.edu Follow this and additional

Southern Illinois University Carbondale OpenSIUC Research Papers Graduate School Fall 2016 An Analysis of Historical Illinois Farmland Valuations Benjamin Johnson bj89@siu.edu Follow this and additional

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 21 ASSET PRICE BUBBLES APRIL 11, 2018

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 21 ASSET PRICE BUBBLES APRIL 11, 2018 I. BUBBLES: BASICS A. Galbraith s and Case, Shiller, and Thompson

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 21 ASSET PRICE BUBBLES APRIL 11, 2018 I. BUBBLES: BASICS A. Galbraith s and Case, Shiller, and Thompson

2009 Rental Decisions Given Volatile Commodity Prices and Higher Input Costs. Gary Schnitkey and Dale Lattz. October 15, 2008 IFEU 08-05

2009 Rental Decisions Given Volatile Commodity Prices and Higher Input Costs Gary Schnitkey and Dale Lattz October 15, 2008 IFEU 08-05 Turmoil within the financial sector has caused concerns about the

2009 Rental Decisions Given Volatile Commodity Prices and Higher Input Costs Gary Schnitkey and Dale Lattz October 15, 2008 IFEU 08-05 Turmoil within the financial sector has caused concerns about the

Impact of Crop Insurance on Land Values. Michael Duffy

Impact of Crop Insurance on Land Values Michael Duffy Introduction Federal crop insurance programs started in the 1930s in response to the Great Depression. The Federal Crop Insurance Corporation (FCIC)

Impact of Crop Insurance on Land Values Michael Duffy Introduction Federal crop insurance programs started in the 1930s in response to the Great Depression. The Federal Crop Insurance Corporation (FCIC)

Nebraska Economic Update

Nebraska Economic Update Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City March 26, 215 Overview of the Federal Reserve System The Fed is the Central Bank of the

Nebraska Economic Update Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City March 26, 215 Overview of the Federal Reserve System The Fed is the Central Bank of the

AAPEX February Two Iowa Sales Sioux County. Chicago Fed Survey October Iowa Realtors Survey November, 2010

The Farmland Market: Buy, Sell, Hold Average Value Per Acre of Iowa Farmland Source: Iowa Agriculture Experiment Station The Market Two Iowa Sales Sioux County Parcel 1 80 acres, 70+ GSR - $3,260 Parcel

The Farmland Market: Buy, Sell, Hold Average Value Per Acre of Iowa Farmland Source: Iowa Agriculture Experiment Station The Market Two Iowa Sales Sioux County Parcel 1 80 acres, 70+ GSR - $3,260 Parcel

Center for Commercial Agriculture

Center for Commercial Agriculture The Great Margin Squeeze: Strategies for Managing Through the Cycle by Brent A. Gloy, Michael Boehlje, and David A. Widmar After many years of high commodity prices and

Center for Commercial Agriculture The Great Margin Squeeze: Strategies for Managing Through the Cycle by Brent A. Gloy, Michael Boehlje, and David A. Widmar After many years of high commodity prices and

Crop Risk Management

Crop Risk Management January 28 th, 2010 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957 5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farmmanagement.htm Source: Johnson,

Crop Risk Management January 28 th, 2010 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957 5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farmmanagement.htm Source: Johnson,

Jason Henderson Vice President and Branch Executive Federal Reserve Bank of Kansas City Omaha Branch September 2012

Jason Henderson Vice President and Branch Executive September 2012 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or

Jason Henderson Vice President and Branch Executive September 2012 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or

M A R K E T E F F I C I E N C Y & R O B E R T SHILLER S I R R A T I O N A L E X U B E R A N C E

M A R K E T E F F I C I E N C Y & R O B E R T SHILLER S I R R A T I O N A L E X U B E R A N C E K E L L Y J I A N G E C O N 4 9 0 5 : F I N A N C I A L F R A G I L I T Y O F T H E M A C R O E C O N O M

M A R K E T E F F I C I E N C Y & R O B E R T SHILLER S I R R A T I O N A L E X U B E R A N C E K E L L Y J I A N G E C O N 4 9 0 5 : F I N A N C I A L F R A G I L I T Y O F T H E M A C R O E C O N O M

What is in Store for the Agricultural Land Market?

February 2015 What is in Store for the Agricultural Land Market? Michael Langemeier, Associate Director, Center for Commercial Agriculture Michael Boehlje, Distinguished Professor, Center for Commercial

February 2015 What is in Store for the Agricultural Land Market? Michael Langemeier, Associate Director, Center for Commercial Agriculture Michael Boehlje, Distinguished Professor, Center for Commercial

What s Moving in Markets in Top Producer January 30, Presented by Dave Fogel, Risk Management Advisor

What s Moving in Markets in 2014 2014 Top Producer January 30, 2014 Presented by Dave Fogel, Risk Management Advisor 800 664 2321 www.advance trading.com Who we are. Company started in 1979 and was incorporated

What s Moving in Markets in 2014 2014 Top Producer January 30, 2014 Presented by Dave Fogel, Risk Management Advisor 800 664 2321 www.advance trading.com Who we are. Company started in 1979 and was incorporated

Econ 323 Economic History of the U.S. Prof. Eschker Spring 2018

Econ 323 Economic History of the U.S. Prof. Eschker Spring 2018 Today s Topics Dow Jones Industrial Average History Declines Bubbles Fundamentals Buying on Margin Speculative Bubbles Barber & Odean Next

Econ 323 Economic History of the U.S. Prof. Eschker Spring 2018 Today s Topics Dow Jones Industrial Average History Declines Bubbles Fundamentals Buying on Margin Speculative Bubbles Barber & Odean Next

Lynn Paulson SVP, Director of Agri-Business Development, Bell State Bank & Trust

Lynn Paulson SVP, Director of Agri-Business Development, Bell State Bank & Trust Email: lpaulson@bellbanks.com o Nearly unprecedented period of prosperity and profitability for row crop and grain producers

Lynn Paulson SVP, Director of Agri-Business Development, Bell State Bank & Trust Email: lpaulson@bellbanks.com o Nearly unprecedented period of prosperity and profitability for row crop and grain producers

WHY WE AREN T LIKELY TO SEE A REPLAY OF THE 1980s FARM CRISIS

WHY WE AREN T LIKELY TO SEE A REPLAY OF THE 1980s FARM CRISIS Wendong Zhang Assistant Professor, Dept. of Economics Iowa State University Why We Aren t Likely to See A Replay of 1980s Farm Crisis Dr. Wendong

WHY WE AREN T LIKELY TO SEE A REPLAY OF THE 1980s FARM CRISIS Wendong Zhang Assistant Professor, Dept. of Economics Iowa State University Why We Aren t Likely to See A Replay of 1980s Farm Crisis Dr. Wendong

Will We See A Recession This Year?

Will We See A Recession This Year? Rising Rates Are Here This week, the Federal Reserve Bank (Fed) signaled their intention to raise their target interest rate when they meet in mid-march. If they do,

Will We See A Recession This Year? Rising Rates Are Here This week, the Federal Reserve Bank (Fed) signaled their intention to raise their target interest rate when they meet in mid-march. If they do,

What variables have historically impacted Kentucky and Iowa farmland values? John Barnhart

What variables have historically impacted Kentucky and Iowa farmland values? John Barnhart Abstract This study evaluates how farmland values and farmland cash rents are affected by cash corn prices, soybean

What variables have historically impacted Kentucky and Iowa farmland values? John Barnhart Abstract This study evaluates how farmland values and farmland cash rents are affected by cash corn prices, soybean

Presentation Outline

The Current and Future Farm Policy Outlook for Corn and Soybeans Joe L. Outlaw Professor & Extension Economist Co-Director, AFPC Minnesota Crop Insurance Conference Mankato, MN September 12, 2013 Presentation

The Current and Future Farm Policy Outlook for Corn and Soybeans Joe L. Outlaw Professor & Extension Economist Co-Director, AFPC Minnesota Crop Insurance Conference Mankato, MN September 12, 2013 Presentation

Future of the Agricultural Sector: Purdue Extension and Financial Markets

Future of the Agricultural Sector: Purdue Extension and Financial Markets Jason Henderson, Ph.D. Director of Purdue Extension July 7, 2015 Community Forums: Spring 2015 Nearly 800 attendees 21 Community

Future of the Agricultural Sector: Purdue Extension and Financial Markets Jason Henderson, Ph.D. Director of Purdue Extension July 7, 2015 Community Forums: Spring 2015 Nearly 800 attendees 21 Community

Business 33001: Microeconomics

Business 33001: Microeconomics Owen Zidar University of Chicago Booth School of Business Week 6 Owen Zidar (Chicago Booth) Microeconomics Week 6: Capital & Investment 1 / 80 Today s Class 1 Preliminaries

Business 33001: Microeconomics Owen Zidar University of Chicago Booth School of Business Week 6 Owen Zidar (Chicago Booth) Microeconomics Week 6: Capital & Investment 1 / 80 Today s Class 1 Preliminaries

Revenue and Costs for Illinois Grain Crops, Actual for 2012 through 2017, Projected 2018 and 2019

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Illinois Grain Crops, Actual for 2012 through 2017, Projected 2018 and 2019 Department of Agricultural

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Illinois Grain Crops, Actual for 2012 through 2017, Projected 2018 and 2019 Department of Agricultural

Revenue and Costs for Corn, Soybeans, Wheat, and Double-Crop Soybeans, Actual for 2011 through 2016, Projected 2017 and 2018

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Corn, Soybeans, Wheat, and Double-Crop Soybeans, Actual for 2011 through 2016, Projected 2017 and

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Corn, Soybeans, Wheat, and Double-Crop Soybeans, Actual for 2011 through 2016, Projected 2017 and

Basis for Grains. Why is basis predictable?

Basis for Grains Why is basis predictable? Average basis levels (expectations) are determined by transportation and storage costs associated with the commodity. Variations in basis levels (outcomes) are

Basis for Grains Why is basis predictable? Average basis levels (expectations) are determined by transportation and storage costs associated with the commodity. Variations in basis levels (outcomes) are

Comparison of Hedging Cost with Other Variable Input Costs. John Michael Riley and John D. Anderson

Comparison of Hedging Cost with Other Variable Input Costs by John Michael Riley and John D. Anderson Suggested citation i format: Riley, J. M., and J. D. Anderson. 009. Comparison of Hedging Cost with

Comparison of Hedging Cost with Other Variable Input Costs by John Michael Riley and John D. Anderson Suggested citation i format: Riley, J. M., and J. D. Anderson. 009. Comparison of Hedging Cost with

Ruminations on Market Timing with the PE10

Jan-26 Jan-29 Jan-32 Jan-35 Jan-38 Jan-41 Jan-44 Jan-47 Jan-50 Jan-53 Jan-56 Jan-59 Jan-62 Jan-65 Jan-68 Jan-71 Jan-74 Jan-77 Jan-80 Jan-83 Jan-86 Jan-89 Jan-92 Jan-95 Jan-98 Jan-01 Jan-04 Jan-07 Jan-10

Jan-26 Jan-29 Jan-32 Jan-35 Jan-38 Jan-41 Jan-44 Jan-47 Jan-50 Jan-53 Jan-56 Jan-59 Jan-62 Jan-65 Jan-68 Jan-71 Jan-74 Jan-77 Jan-80 Jan-83 Jan-86 Jan-89 Jan-92 Jan-95 Jan-98 Jan-01 Jan-04 Jan-07 Jan-10

Fundamental and Non-Fundamental Explanations for House Price Fluctuations

Fundamental and Non-Fundamental Explanations for House Price Fluctuations Christian Hott Economic Advice 1 Unexplained Real Estate Crises Several countries were affected by a real estate crisis in recent

Fundamental and Non-Fundamental Explanations for House Price Fluctuations Christian Hott Economic Advice 1 Unexplained Real Estate Crises Several countries were affected by a real estate crisis in recent

Opportunities and challenges for agriculture. How will agriculture and the swine industry fare in today s economic climate? Opportunities.

The outlook for the swine industry and its relationship with the global economy Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative Center How will agriculture and the

The outlook for the swine industry and its relationship with the global economy Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative Center How will agriculture and the

Module 12. Alternative Yield and Price Risk Management Tools for Wheat

Topics Module 12 Alternative Yield and Price Risk Management Tools for Wheat George Flaskerud, North Dakota State University Bruce A. Babcock, Iowa State University Art Barnaby, Kansas State University

Topics Module 12 Alternative Yield and Price Risk Management Tools for Wheat George Flaskerud, North Dakota State University Bruce A. Babcock, Iowa State University Art Barnaby, Kansas State University

Macroeconomic Risks for Farmer Cooperatives

Macroeconomic Risks for Farmer Cooperatives KFSA Directors & Management Meeting Hutchinson, KS November 21 st, 2011 Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative

Macroeconomic Risks for Farmer Cooperatives KFSA Directors & Management Meeting Hutchinson, KS November 21 st, 2011 Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative

CASH RENT WITH BONUS LEASING ARRANGEMENT: DESCRIPTION AND EXAMPLE

FEFO 11-17 September 27, 2011 CASH RENT WITH BONUS LEASING ARRANGEMENT: DESCRIPTION AND EXAMPLE A cash rent with bonus leasing arrangement is a variable cash rent lease that has a base rent and the potential

FEFO 11-17 September 27, 2011 CASH RENT WITH BONUS LEASING ARRANGEMENT: DESCRIPTION AND EXAMPLE A cash rent with bonus leasing arrangement is a variable cash rent lease that has a base rent and the potential

INSIGHTS REPORT VOLUME 14 WHAT S INSIDE. Five considerations for effective financial planning in 2018.

INSIGHTS REPORT VOLUME 14 WHAT S INSIDE Five considerations for effective financial planning in 2018. Revisit your risk management strategies to prepare for success in the beef industry. How changes to

INSIGHTS REPORT VOLUME 14 WHAT S INSIDE Five considerations for effective financial planning in 2018. Revisit your risk management strategies to prepare for success in the beef industry. How changes to

Step Up Your Grain Game! Crop Economics for 2018

Step Up Your Grain Game! Crop Economics for 2018............................... Roy Arnott, P.Ag. & Darren Bond, P.Ag. Farm Management Specialists What we already know Doing your cost of production for

Step Up Your Grain Game! Crop Economics for 2018............................... Roy Arnott, P.Ag. & Darren Bond, P.Ag. Farm Management Specialists What we already know Doing your cost of production for

Macroeconomic Outlook: Implications for Agriculture. It has been 26 years since we have experienced a significant recession

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

University Of Balamand Economics and Capital Markets Research Center A Banque Libano-Française Partnered Initiative

University Of Balamand Economics and Capital Markets Research Center A Banque Libano-Française Partnered Initiative Special Report February 5 0 THE IMPACT OF THE ONGOING OIL AND FOOD SHOCKS ON MONETARY

University Of Balamand Economics and Capital Markets Research Center A Banque Libano-Française Partnered Initiative Special Report February 5 0 THE IMPACT OF THE ONGOING OIL AND FOOD SHOCKS ON MONETARY

Steven D. Johnson. Presentation Objectives

January 30, 2013 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management Presentation Objectives Define Shallow Loss

January 30, 2013 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management Presentation Objectives Define Shallow Loss

Incorporating Crop Insurance Subsidies into Conservation Reserve Program (CRP) Design

Design") Incorporating Crop Insurance Subsidies into Conservation Reserve Program (CRP) Design RUIQING MIAO (UNIVERSITY OF ILLINOIS UC) HONGLI FENG (IOWA STATE UNIVERSITY) DAVID A. HENNESSY (IOWA STATE UNIVERSITY)

Incorporating Crop Insurance Subsidies into Conservation Reserve Program (CRP) Design RUIQING MIAO (UNIVERSITY OF ILLINOIS UC) HONGLI FENG (IOWA STATE UNIVERSITY) DAVID A. HENNESSY (IOWA STATE UNIVERSITY)

Ability to Pay and Agriculture Sector Stability. Erin M. Hardin John B. Penson, Jr.

Ability to Pay and Agriculture Sector Stability Erin M. Hardin John B. Penson, Jr. Texas A&M University Department of Agricultural Economics 600 John Kimbrough Blvd 2124 TAMU College Station, TX 77843-2124

Ability to Pay and Agriculture Sector Stability Erin M. Hardin John B. Penson, Jr. Texas A&M University Department of Agricultural Economics 600 John Kimbrough Blvd 2124 TAMU College Station, TX 77843-2124

AGBE 321. Problem Set 5 Solutions

AGBE 321 Problem Set 5 Solutions 1. In your own words (i.e., in a manner that you would explain it to someone who has not taken this course) explain the concept of offsetting futures contracts. When/why

AGBE 321 Problem Set 5 Solutions 1. In your own words (i.e., in a manner that you would explain it to someone who has not taken this course) explain the concept of offsetting futures contracts. When/why

Rebalancing Toward Sustainable Growth. Thomas M. Hoenig President and Chief Executive Officer Federal Reserve Bank of Kansas City

Rebalancing Toward Sustainable Growth Thomas M. Hoenig President and Chief Executive Officer Federal Reserve Bank of Kansas City The Rotary Club of Des Moines and the Greater Des Moines Partnership Des

Rebalancing Toward Sustainable Growth Thomas M. Hoenig President and Chief Executive Officer Federal Reserve Bank of Kansas City The Rotary Club of Des Moines and the Greater Des Moines Partnership Des

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst A year ago USDA shocked the market by cutting its forecast of soybean production, helping

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst A year ago USDA shocked the market by cutting its forecast of soybean production, helping

CROP BUDGETS, ILLINOIS, 2017

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2017 Department of Agricultural and Consumer Economics University of Illinois July 2017 Introduction

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2017 Department of Agricultural and Consumer Economics University of Illinois July 2017 Introduction

CROP BUDGETS, ILLINOIS, 2019

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2019 Department of Agricultural and Consumer Economics University of Illinois September 2018

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2019 Department of Agricultural and Consumer Economics University of Illinois September 2018

Agricultural Economic Update

Agricultural Economic Update March 2, 217 Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City The views expressed are those of the author and do not necessarily reflect

Agricultural Economic Update March 2, 217 Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City The views expressed are those of the author and do not necessarily reflect

CROP BUDGETS, ILLINOIS, 2018

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2018 Department of Agricultural and Consumer Economics University of Illinois February 2018

CROP BUDGETS Department of Agricultural and Consumer Economics University of Illinois CROP BUDGETS, ILLINOIS, 2018 Department of Agricultural and Consumer Economics University of Illinois February 2018

The Stock Market Mishkin Chapter 7:Part B (pp )

") The Stock Market Mishkin Chapter 7:Part B (pp. 152-165) Modified Notes from F. Mishkin (Bus. School Edition, 2 nd Ed 2010) L. Tesfatsion (Iowa State University) Last Revised: 1 March 2011 2004 Pearson

The Stock Market Mishkin Chapter 7:Part B (pp. 152-165) Modified Notes from F. Mishkin (Bus. School Edition, 2 nd Ed 2010) L. Tesfatsion (Iowa State University) Last Revised: 1 March 2011 2004 Pearson

The federal crop insurance program is ripe for reform: TWO CHANGES TO CROP INSURANCE TO IMPROVE EQUITY AND EFFICIENCY

CONTENTS Introduction 1 Means-Testing Crop Insurance Subsidies 1 How Crop Insurance is Subsidized 2 The Crop Insurance Industry s Position 3 Impacts of Limiting Premium Subsidies 3 Eliminating Subsidies

CONTENTS Introduction 1 Means-Testing Crop Insurance Subsidies 1 How Crop Insurance is Subsidized 2 The Crop Insurance Industry s Position 3 Impacts of Limiting Premium Subsidies 3 Eliminating Subsidies

ARC vs. PLC Enrollment Decisions

ARC vs. PLC Enrollment Decisions April 2014 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management FSA Commodity Crop

ARC vs. PLC Enrollment Decisions April 2014 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management FSA Commodity Crop

International financial crises

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

Oxford Energy Comment March 2009

Oxford Energy Comment March 2009 Reinforcing Feedbacks, Time Spreads and Oil Prices By Bassam Fattouh 1 1. Introduction One of the very interesting features in the recent behaviour of crude oil prices

Oxford Energy Comment March 2009 Reinforcing Feedbacks, Time Spreads and Oil Prices By Bassam Fattouh 1 1. Introduction One of the very interesting features in the recent behaviour of crude oil prices

How the Federal Reserve Can Affect Agriculture

How the Federal Reserve Can Affect Agriculture 2012 2013 Ag Profitability Conferences Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative Center The Federal Reserve System

How the Federal Reserve Can Affect Agriculture 2012 2013 Ag Profitability Conferences Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative Center The Federal Reserve System

Review of County Loan Rates for Sorghum and Corn. AFPC Briefing Paper April 2007

Review of County Loan Rates for Sorghum and Corn AFPC Briefing Paper 07-5 April 2007 Agricultural and Food Policy Center The Texas A&M University System 350 300 250 200 150 100 50 AFPC 9 14 0 2004 2005

Review of County Loan Rates for Sorghum and Corn AFPC Briefing Paper 07-5 April 2007 Agricultural and Food Policy Center The Texas A&M University System 350 300 250 200 150 100 50 AFPC 9 14 0 2004 2005

informational Bulletin PA Legislative Changes to Farmland Valuation FY June 2014 Illinois Department of Revenue

Illinois Department of Revenue FY 2014-16 June 2014 Brian Hamer, Director informational Bulletin PA 98-0109 Legislative Changes to Farmland Valuation Historical information of the Farmland Assessment Law.

Illinois Department of Revenue FY 2014-16 June 2014 Brian Hamer, Director informational Bulletin PA 98-0109 Legislative Changes to Farmland Valuation Historical information of the Farmland Assessment Law.

Cary L. Sandell. Wells Fargo Food and Agribusiness Group

Degree of Belief Cary L. Sandell Wells Fargo Food and Agribusiness Group November 2009 Everything is connected. We just can t see it. Every new economic action comes from some other economic action s end

Degree of Belief Cary L. Sandell Wells Fargo Food and Agribusiness Group November 2009 Everything is connected. We just can t see it. Every new economic action comes from some other economic action s end

Penitence after accusations of error,...

Penitence after accusations of error,... Comments Martin Eichenbaum NBER, July 2013 Background Economists have long argued about the role that policy played in major macro episodes and the way policy institutions

Penitence after accusations of error,... Comments Martin Eichenbaum NBER, July 2013 Background Economists have long argued about the role that policy played in major macro episodes and the way policy institutions

The Farm Safety Net: The Good and Not So Good Michael Boehlje and Michael Langemeier Center for Commercial Agriculture Purdue University

The Farm Safety Net: The Good and Not So Good Michael Boehlje and Michael Langemeier Center for Commercial Agriculture Purdue University USDA recently announced that they project net farm income to decline

The Farm Safety Net: The Good and Not So Good Michael Boehlje and Michael Langemeier Center for Commercial Agriculture Purdue University USDA recently announced that they project net farm income to decline

Module 19 Equilibrium in the Aggregate Demand Aggregate Supply Model

What you will learn in this Module: The difference between short-run and long-run macroeconomic equilibrium The causes and effects of demand shocks and supply shocks How to determine if an economy is experiencing

What you will learn in this Module: The difference between short-run and long-run macroeconomic equilibrium The causes and effects of demand shocks and supply shocks How to determine if an economy is experiencing

COLLECTIVE INTELLIGENCE A NEW APPROACH TO STOCK PRICE FORECASTING

COLLECTIVE INTELLIGENCE A NEW APPROACH TO STOCK PRICE FORECASTING CRAIG A. KAPLAN Proceedings of the 2001 IEEE Systems, Man, and Cybernetics Conference iq Company (www.iqco.com Abstract A group that makes

COLLECTIVE INTELLIGENCE A NEW APPROACH TO STOCK PRICE FORECASTING CRAIG A. KAPLAN Proceedings of the 2001 IEEE Systems, Man, and Cybernetics Conference iq Company (www.iqco.com Abstract A group that makes

Financial Crisis Impact on Long Term Ag Forecast

1 Financial Crisis Impact on Long Term Ag Forecast Paul N. Ellinger University of Illinois pellinge@illinois.edu www.farmdoc.uiuc.edu/ellinger 217-333-5503 Economic Conditions Surging commodity prices

1 Financial Crisis Impact on Long Term Ag Forecast Paul N. Ellinger University of Illinois pellinge@illinois.edu www.farmdoc.uiuc.edu/ellinger 217-333-5503 Economic Conditions Surging commodity prices

factors that affect marketing

Grain Marketing / no. 26 factors that affect marketing Crop Insurance Coverage Producers who buy at least 80 percent Revenue Protection for corn are more likely to indicate that crop insurance is an important

Grain Marketing / no. 26 factors that affect marketing Crop Insurance Coverage Producers who buy at least 80 percent Revenue Protection for corn are more likely to indicate that crop insurance is an important

Farm Business Analysis Ch.18

Farm Business Analysis Ch.18 What are the strengths and weaknesses of the farm business? How can we measure how well the farm is doing? Which farm would you prefer? Farm A Net worth $400,000 Total acres

Farm Business Analysis Ch.18 What are the strengths and weaknesses of the farm business? How can we measure how well the farm is doing? Which farm would you prefer? Farm A Net worth $400,000 Total acres

Canada s Economic Future: What Have We Learned from the 1990s?

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Canadian Club of Toronto Toronto, Ontario 22 January 2001 Canada s Economic Future: What Have We Learned from the 1990s? It was to the Canadian

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Canadian Club of Toronto Toronto, Ontario 22 January 2001 Canada s Economic Future: What Have We Learned from the 1990s? It was to the Canadian

Stock Market Forecast: Chaos Theory Revealing How the Market Works March 25, 2018 I Know First Research

Stock Market Forecast: Chaos Theory Revealing How the Market Works March 25, 2018 I Know First Research Stock Market Forecast : How Can We Predict the Financial Markets by Using Algorithms? Common fallacies

Stock Market Forecast: Chaos Theory Revealing How the Market Works March 25, 2018 I Know First Research Stock Market Forecast : How Can We Predict the Financial Markets by Using Algorithms? Common fallacies

Nebraska Economic Outlook

Nebraska Economic Outlook Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City August 3, 16 The views expressed are those of the author and do not necessarily reflect

Nebraska Economic Outlook Nathan Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City August 3, 16 The views expressed are those of the author and do not necessarily reflect

LATE PLANTING AND CROP INSURANCE

FEFO 09-09 June 1, 2009 LATE PLANTING AND CROP INSURANCE Adverse planting conditions this spring has resulted in many crop insurance questions related to replant, prevented planting, and late planting

FEFO 09-09 June 1, 2009 LATE PLANTING AND CROP INSURANCE Adverse planting conditions this spring has resulted in many crop insurance questions related to replant, prevented planting, and late planting

Econ 338c. April 12, 2007

60 Econ 338c April 12, 2007 10 Traits of a Successful Grain Marketer Starts Early (before planting) Knows production, storage costs & risk bearing ability Understands basis & mkt. carry Follows several

60 Econ 338c April 12, 2007 10 Traits of a Successful Grain Marketer Starts Early (before planting) Knows production, storage costs & risk bearing ability Understands basis & mkt. carry Follows several

2008 FARM BILL: FOCUS ON ACRE

2008 FARM BILL: FOCUS ON ACRE (Average Crop Revenue Election) Carl Zulauf Ag. Economist, Ohio State University Updated: October 3, 2008, Presented to USDA Economists Group 1 Seminar Outline 1. Provide

2008 FARM BILL: FOCUS ON ACRE (Average Crop Revenue Election) Carl Zulauf Ag. Economist, Ohio State University Updated: October 3, 2008, Presented to USDA Economists Group 1 Seminar Outline 1. Provide

Economics of Money, Banking, and Fin. Markets, 10e

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Market Hypothesis 7.1 Computing the Price of Common Stock

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Market Hypothesis 7.1 Computing the Price of Common Stock

Measuring Iowa s Economy: Output

Measuring Iowa s Economy: Output By Michael A. Lipsman Strategic Economics Group August 2012 Introduction After going through the deepest recession since the 1930s, the United States economy continues

Measuring Iowa s Economy: Output By Michael A. Lipsman Strategic Economics Group August 2012 Introduction After going through the deepest recession since the 1930s, the United States economy continues

The U.S. Economy and Monetary Policy. Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City

The U.S. Economy and Monetary Policy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City Central Exchange Kansas City, Missouri January 10, 2013 The views expressed

The U.S. Economy and Monetary Policy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City Central Exchange Kansas City, Missouri January 10, 2013 The views expressed

Paul Stoddard. Lecturer in Agribusiness University of Illinois College of ACES

Paul Stoddard Lecturer in Agribusiness University of Illinois College of ACES Paul Stoddard Lecturer in Agribusiness Department of Agricultural & Consumer Economics pstoddrd@illinois.edu Copyright 2017,

Paul Stoddard Lecturer in Agribusiness University of Illinois College of ACES Paul Stoddard Lecturer in Agribusiness Department of Agricultural & Consumer Economics pstoddrd@illinois.edu Copyright 2017,

of the University of Chicago Booth School of Business Narayana Kocherlakota President Federal Reserve Bank of Minneapolis

61 st Annual Management Conference of the University of Chicago Booth School of Business Narayana Kocherlakota President Federal Reserve Bank of Minneapolis Chicago, Illinois May 17, 2013 During the conference,

61 st Annual Management Conference of the University of Chicago Booth School of Business Narayana Kocherlakota President Federal Reserve Bank of Minneapolis Chicago, Illinois May 17, 2013 During the conference,

Farmers have significantly increased their debt levels

2010 Debt, Income and Farm Financial Stress By Brian C. Briggeman, Economist, Federal Reserve Bank of Kansas City Farmers have significantly increased their debt levels in recent years. Since 2004, real

2010 Debt, Income and Farm Financial Stress By Brian C. Briggeman, Economist, Federal Reserve Bank of Kansas City Farmers have significantly increased their debt levels in recent years. Since 2004, real

Managing Machinery Expenses

Managing Machinery Expenses Dr. Gregg Ibendahl, Mark Wood, & Doug Stucky Kansas State University Email: ibendahl@ksu.edu mawood@ksu.edu dstucky@ksu.edu Phone: 785-477-2071 785-462-6664 620-225-5600 Machinery

Managing Machinery Expenses Dr. Gregg Ibendahl, Mark Wood, & Doug Stucky Kansas State University Email: ibendahl@ksu.edu mawood@ksu.edu dstucky@ksu.edu Phone: 785-477-2071 785-462-6664 620-225-5600 Machinery

6 Capacity CAPACITY 59

CAPACITY 59 6 Capacity Changing climate conditions will have a number of potential impacts on agriculture. Farmers have differing adaptive capacities to adjust and moderate potential damages or take advantage

CAPACITY 59 6 Capacity Changing climate conditions will have a number of potential impacts on agriculture. Farmers have differing adaptive capacities to adjust and moderate potential damages or take advantage

Don t get Caught with Your Marketing and Crop Insurance on the Wrong Side of the Basis When it Narrows 1

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Chapter 4. Agricultural Finance Calum G. Turvey, W.I. Myers Professor of Agricultural Finance

Chapter 4. Calum G. Turvey, W.I. Myers Professor of General Outlook The financial condition of New York s agricultural economy in 2014 is holding steady if not improving over 2013. Although there is some

Chapter 4. Calum G. Turvey, W.I. Myers Professor of General Outlook The financial condition of New York s agricultural economy in 2014 is holding steady if not improving over 2013. Although there is some

Barry J. Barnett Department of Agricultural Economics

Risk and Risk Management Barry J. Barnett Department of Agricultural Economics What is Risk? Reduction in annual net income caused by: Loss of revenue Low yields, low prices Change in government programs

Risk and Risk Management Barry J. Barnett Department of Agricultural Economics What is Risk? Reduction in annual net income caused by: Loss of revenue Low yields, low prices Change in government programs

Ohio Ethanol Producers Association

Economic Impact Analysis of the Ethanol Industry in Ohio for the Ohio Ethanol Producers Association October 2012 Prepared by: Greg Davis, Ph.D. Professor Nancy Bowen, CEcD Field Specialist Ohio State University

Economic Impact Analysis of the Ethanol Industry in Ohio for the Ohio Ethanol Producers Association October 2012 Prepared by: Greg Davis, Ph.D. Professor Nancy Bowen, CEcD Field Specialist Ohio State University

2015 New Crop Marketing. Ed Kordick Iowa Farm Bureau Federation. February, Pre-harvest marketing with Revenue Protection Crop Insurance

2015 New Crop Marketing Ed Kordick Iowa Farm Bureau Federation February, 2015 Objectives Get back to the basics: Understand the tools, Have a revenue perspective And realistic goals Pre-harvest marketing

2015 New Crop Marketing Ed Kordick Iowa Farm Bureau Federation February, 2015 Objectives Get back to the basics: Understand the tools, Have a revenue perspective And realistic goals Pre-harvest marketing

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

The Future Performance of the Canadian Economy

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Canadian Club of Winnipeg Winnipeg, Manitoba 25 March 1998 The Future Performance of the Canadian Economy It can take anywhere from one

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Canadian Club of Winnipeg Winnipeg, Manitoba 25 March 1998 The Future Performance of the Canadian Economy It can take anywhere from one

Executive summary MONETARY POLICY IN 2003

Executive summary The Centre for Monetary Economics (CME) at the BI Norwegian School of Management has for the fifth time invited a committee of economists for Norges Bank Watch with the objective of evaluating

Executive summary The Centre for Monetary Economics (CME) at the BI Norwegian School of Management has for the fifth time invited a committee of economists for Norges Bank Watch with the objective of evaluating

AGRICULTURAL Finance Monitor

n Third Quarter AGRICULTURAL Finance Monitor Selected Quotes from Banker Respondents Across the Eighth Federal Reserve District Because poultry integrators are placing birds on schedule, poultry farm income

n Third Quarter AGRICULTURAL Finance Monitor Selected Quotes from Banker Respondents Across the Eighth Federal Reserve District Because poultry integrators are placing birds on schedule, poultry farm income

Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University

Agricultural Lender Survey Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University Results: Fall Survey, 2015 Survey Summary

Agricultural Lender Survey Brady Brewer, Allen Featherstone, Christine Wilson, and Brian Briggeman Department of Agricultural Economics Kansas State University Results: Fall Survey, 2015 Survey Summary

CropWatch.unl.edu Nov. 6, 2014

University of Nebraska-Lincoln CropWatch.unl.edu Nov. 6, 2014 Tightening Your Belt; Refocusing on Profitability This article by Tina Barrett, executive director of Farm Business Inc., is the first in a

University of Nebraska-Lincoln CropWatch.unl.edu Nov. 6, 2014 Tightening Your Belt; Refocusing on Profitability This article by Tina Barrett, executive director of Farm Business Inc., is the first in a

Climate Policy Initiative Does crop insurance impact water use?

Climate Policy Initiative Does crop insurance impact water use? By Tatyana Deryugina, Don Fullerton, Megan Konar and Julian Reif Crop insurance has become an important part of the national agricultural

Climate Policy Initiative Does crop insurance impact water use? By Tatyana Deryugina, Don Fullerton, Megan Konar and Julian Reif Crop insurance has become an important part of the national agricultural