Company presentation. Milan - March 24-25, 2015

|

|

|

- Shanon Peters

- 5 years ago

- Views:

Transcription

1 Company presentation Milan - March 24-25, 2015

2 Important information This presentation is being shown to you solely for your information and may not be reproduced, distributed to any other person or published, in whole or in part, for any purpose. The information in this presentation could include forward-looking statements which are based on current expectations and projections about future events. These forward-looking statements are subject to risks, uncertainties and assumptions about the Company and its subsidiaries and investments. Including, among other things, the development of its business, trends in its operating industry, and future capital expenditures and acquisitions. In light of these risks, uncertainties and assumptions, the events in the forward-looking statements may not occur. No one undertakes to publicly update or revise any such forward-looking statements. The Group s business is also correlated to tourism flows. Q1 and Q4 represent the low point of the business year, whereby Q2 and Q3 the peak of the seasonality. Therefore quarterly sales, operating results, trade net working capital and net financial indebtedness are impacted by the seasonality and may not be directly compared or extrapolated to obtain forecasts of year-end results. 2

3 Table of contents MARR Group Reference market Business overview Financials FY 2014 Appendix 3

4 MARR at a glance leader in Food supply to Foodservice in Italy market consolidator with 42 years of track record and a conservative approach C&C C&C C&C C&C AG over 38,000 clients served with a range of C&C over 10,000 food products including over 700 private labels AG only player with nationwide coverage: 33 distribution centres with 3 stocking platforms and 5 cash&carry 4 agents with warehouse and over 20 logistic partnerships with local distributors of fresh products (fruits&vegetables and seafood) over 700 sales agents and ca 750 trucks to ensure the delivery within 24h from the order C&C AG AG AG Distribution centres Cash & carry Agents with warehouse artnership rocessing facilities (meat and seafood) Stocking platforms 4

5 Steady and sustainable growth m Consolidated Total Revenues CAGR: +6.1% Acquisition of Sogema in Turin expansion in Large Cities 795 IO 882 Acquisition of specialization in products (ie Baldini) and clients 973 1,065 Diversification in bar segment with acquisition of New Catering and Emigel 1,109 1,138 1,193 1,249 1,260 Scapa acquisition 1,365 1,

6 Table of contents MARR Group Reference market Business overview Financials FY 2014 Appendix 6

7 Italian Foodservice Italian Foodservice, a market worth over 60 bln Euros (ca 5% GD) Italian Foodservice breakdown in value 14% Canteens 20% Structured operators The Commercial Catering (i.e. Restaurants, pizzerias, hotels etc) represents the main segment of the Italian Foodservice. A fragmented 86% Commercial Catering 80% Independent operators segment characterized by Independent operators Source: GIRA Foodservice

8 Supply to Italian Foodservice Supply* to Foodservice ~ 16-17bn *(Food and Beverage) Wholesalers segment ~ 11bn roducers 19% Wholesalers 64% Other Wholesalers 83% MARR ~ 13% Top 3 followers DAC 1.9% regis 1.4% Retail Quartiglia 1.0% 17% Market fragmentation and the coverage of the existing clients provide a solid base for further Organic Growth MARR serves approx. 38,000 clients out of ca 140,000 foodservice operators in Italy (excluding bars) Market Share in number of clients MARR ~ 27% Source: Company estimates 8

9 Table of contents MARR Group Reference market Business overview Financials FY 2014 Appendix 9

10 Sales - breakdown Client segments Direct sales to Foodservice clients Wholesaler clients National Account 22.0% roducts Conservation Consolidated Sales breakdown - FY

11 Sales - breakdown by geography Extra EU 2% EU 6% 0% 12% 5% 3% 2% 8% 15% 2% Italy 92% 7% 5% 1% 2% 13% 0% 4% 5% 1% Southern Italy 22% Central Italy 31% Northern Italy 48% Label: 5% +10% 4-10% 1-3% 5% 4% 0% breakdown as at December 31,

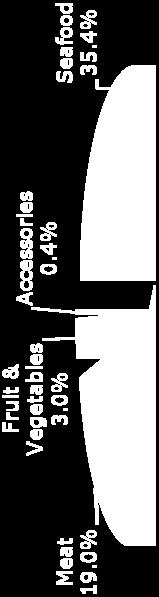

12 Diversification Customers Suppliers Client segment No. customers roduct category No. suppliers Street Market Chains and Groups Canteens Wholesalers > 38,000 ca 100 ca 500 ca 750 Grocery Seafood Meat Fruit&Vegetables Accessories 1, Total > 39,000 Total 2,200 Top customers on consolidated Total Revenues Top suppliers on consolidated COG's 12.8% 10.7% 14.4% 14.6% 11.4% 11.4% 21.3% 14.4% 19.1% 12.1% 14.5% 22.0% 6.8% 5.9% 5.3% 6.0% 5.8% 7.0% top 3 top 10 top top 3 top 10 top 20 12

13 Operations efficiency and variable costs Operating activities Supply Warehousing Logistics / Distribution Other operating activities > 38,000 clients 2,200 suppliers worldwide with products in exclusivity 33 distribution centres (9 owned) 4 local stores (agents with warehouse) > 20 logistic partnerships ca 750 trucks > 700 sales agents Truck drivers and sales agents are self employed ca 1,000 employees Operating costs 77.9% Over 90% of Operating costs are variable other var. 1.6% 0.6% 4.2% 3.0% other fixed 3.0% personnel 2.6% % of total revenues COGS leases & rents transport costs sales costs variable costs fixed costs personnel & other Consolidated data as at Dec. 31,

14 Logistics / distribution system Target Completion of Operating Cycle Within 24 Hours from Order Client servicing rocurement Agent - Client Contact Order Entry Grocery-Meat-Seafood Central Division Credit check Data rocessing Goods in Client Bill of Carriage and Invoice Issuance ED Delivery Scheduling icking List Storage Loading icking 3 stocking platforms MARR s platforms 14

15 Operating priorities TAKE CARE OF MARR S FUTURE EOLE COVERAGE CLIENTS WORKING CAITAL ROFITA BILITY 15

16 Table of contents MARR Group Reference market Business overview Financials FY 2014 Appendix 16

17 FY Highlights Reference Market According to Confcommercio data (March, 2015) consumption (in quantity) for Hotels and out of home food consumption in 2014 was -1.4%, with an improvement in 4Q (-0.6%) Sales Against this background, MARR s Organic growth towards clients of Street Market and National Account segments in 2014 was +3.8% Operating profitability EBITDA exceeded 100 million Euros (101.8 m) and remained in the 7% area: 7.1% in 2014 vs 7.0% of the previous year Cash generation Free cash flow before dividends in 2014 was 58.4 m Dividend proposal A gross DS of 0.62 is proposed with an increase of 4 cents versus 0.58 of the previous year 17

18 FY 2014 Sales FY 2013 %ch FY 2014 Total revenues 1, % 1,441.4 Total sales 1, % 1, % % % Wholesale National Account Street Market Sales increased in all segments, with also a positive contribution from sales of frozen seafood to Wholesalers, that in 2014 benefitted from an improved price scenario in the seafood category 18

19 FY 2014 Trend in SM and NA segments m 1, % -0.5% 1,162.5 * Management of Scapa going concern +3.3% from February 2013 and divestment of Alisea in March M 13 Organic Divestment/ 12M 14 Acquisition* Organic growth in Street Market and National Account segments (+43.1 m) was driven by sales (+26.8 m) to Independent hotels and restaurants - the Street Market that are the client segments that represents ca 80% of the value of the Italian Foodservice (Gira Foodservice, 2014) 19

20 FY rice/mix - volume m Street Market - National Account client segments 1, % +1.9% 1,162.5 % change rice/mix Volume +3.3% Grocery Meat Seafood M 13 rice/mix Volume 12M 14 In 2014, the price/mix contribution remained above +1% (+1.5% as at September 30 last) and driven by inflation in Seafood. 20

21 FY Income statement m FY 2013 % FY 2014 % % ch Total Revenues 1, % 1, % +5.6 COG s (1,055.2) -77.4% (1,122.4) -77.9% Services (162.1) -11.8% (169.1) -11.8% Other operating costs (12.6) -0.9% (10.9) -0.7% ersonnel costs (39.8) -2.9% (37.1) -2.5% EBITDA % % +7.2 D&A (4.5) -0.3% (4.9) -0.4% rovisions (10.4) -0.8% (11.2) -0.8% EBIT % % +7.1 Net interest (6.8) -0.5% (8.8) -0.6% Non recurrent items (1.9) -0.2% % rofit before tax % % +8.0 Divestment (March 2014) of Alisea (catering service to hospitals) affected: i) negatively GM (Alisea < Cogs); ii) positively ersonnel costs (Alisea > workforce) EBITDA passed 100 m and operating margin is confirmed in the 7% area Confirmed the cautious determination of provisions one off costs of 2013 were due to integration of Scapa Taxes (24.0) -1.7% (25.9) -1.8% Net income % % +8.0 Tax rate 33.7% 33.7% 21

22 FY Trade NWC 18.9 m 16.8 m like for like reported like for like reported m Accounts Receivable Days Inventory Days (319.3) (324.6) (324.6) Accounts ayable (274.3) (274.4) (274.4) Increase of Inventory is due to stocking policies in frozen seafood product category Days Trade Net Working Capital Cash conversion cycle (Days) Trade NWC / Total revenues At the year end the improvement of Days of receivable is confirmed, also like for like, i.e. net of the effect of the securitization programme implemented in second part of the year 16.6% 16.5% 15.4% Absorption of Trade NWC improved, also net of the securitization and despite the increase of stock of seafood: from 16.6% to 16.5% LFL reported 22

23 FY Cash flow and Net debt Cash flow Net Debt m Operating cash flow m Net Debt/EBITDA Change in Total NWC (23.6) 14.0 Investments (20.2) (11.8) 1.8x 2.0x 1.7x Others (4.9) Free cash flow (before dividends) short term m/l term Free cash flow before dividends (38.6 m of dividends paid in 2014) reached 58.4 m Investments of 2014 were: 7.6 m for the acquisition of the going concerns Scapa and Lelli, 1.7 m for the increase of capacity in some distribution centres and 2.5 m for maintenance CapEx. Investments of 2013 were affected by the acquisition of the Carnemilia facilities (15.5 m) The ratio Net Debt on EBITDA went back below 2x and also net of the securitization effect (1.9x) 23

24 FY 2014 Dividend proposal ES DS Board of Directors proposes for the approval of the AGM of next 28 April a gross dividend per share of 0.62 (+4 cents or +6.9% compared to the previous year) Net income not distributed will be allocated to Reserves in order to continue to finance the growth, primarily in terms of financing the absorption of Trade NWC due to the Organic growth 24

MARR s focus remains on: increasing its market share, also continuing to be innovative in")

25 Outlook Expectations for recovery and improvement of internal demand have not yet been evident in the Italian Foodservice End of 2014 and start of 2015 showed a slightly recovering trend: in January consumption for Hotels and out of home food consumption is no longer negative (Confcommercio, March 2015) MARR s focus remains on: increasing its market share, also continuing to be innovative in terms of products and particularly in the private label offer, by introducing top quality products (e.g. Top range arma ham) maintaining the operating profitability achieved, even with a selective approach: for example towards direct supply to ublic Administration, where tender rules changed controlling absorption of Trade NWC EXO 2015 is an opportunity and MARR will be prepared increasing its level of service, towards: i) the operators providing catering service in the exhibition; ii) the hotels and restaurants of Lombardy area and also Big cities, that would benefit from higher tourist flows 25

26 Appendix Share price Shareholding structure Income statement* Balance sheet* Cash flow statement* Seasonality* Debt maturity* eers comparison * As at December 31,

27 Share price Shareholding structure Shareholding structure Cremonini SpA 50.4% Free Float 49.6% of which holdings * > 2% MARR FTSE STAR FTSE ALLSHARES Share price Standard Life Investment 5.0% Allianz Global Investors 2.3% Market cap 1,023 m no. of shares outstanding 66,525,120 * major holdings declared pursuant art 120 Law Decree 58/1998. Information integrated by communications of Servizio Titoli Data as at March 19,

28 Income statement as at December 31,

29 Balance sheet as at December 31, 2014 MARR Consolidated ( thousand) Net intangible assets 106,270 99, , , , ,978 Net tangible assets 68,962 68,282 52,573 54,264 55,817 58,149 Equity investments in other companies Other fixed assets 36,845 36,951 31,262 25,308 14,734 9,706 Total fixed assets (A) 212, , , , , ,129 Net trade receivables from customers 379, , , , , ,743 Inventories 116, ,704 98,736 96,163 99,585 84,588 Suppliers (274,443) (274,334) (270,37 3) (259,722) (260,020) (236,928) Trade net working capit al (B) 221, , , , , ,403 Other current assets 48,465 56,196 48,056 41,778 47,883 33,723 Other current liabilities (23,688) (22,455) (20,17 2) (22,349) (21,505) (21,479) Total current assets/liabilities (C) 24,777 33, , , ,378 12,244 Net worki ng capital (D) = (B+C) 246, , , , , ,647 Other non current liabilities (E) (690) (438) (33 7) (241) (138) (46) Staff Severance rovision (F) (10,960) (11,542) (10,96 5) (9,539) (10,035) (10,063) rovisions for risks and charges (G) (16,066) (15,585) (14,93 3) (14,538) (13,469) (12,675) Net invested capital (H) = (A+D+E+F+G) 430, , , , , ,992 Shareholders' equity attributable to the Group (254,280) (243,015) (228,31 8) (222,732) (206,579) (191,736) Shareholders' equity attributable to minority interests 0 (1,127) (1,16 2) (1,142) (1,131) (999) Consolidated shareholders' equity (I) (25 4,280) (2 44,142) (229,480) (223,874) (207,71 0) (192,7 35) (Net short-term financial debt)/cash (95,102) (29,541) (111,75 5) (99,087) (49,285) (112,844) (Net medium/long-term financial debt) (81,582) (164,590) (53,46 9) (56,901) (107,070) (43,413) Net fi nancial debt (L) (17 6,684) (1 94,131) (165,224) (155,988) (156,35 5) (156,2 57) Net equity and net financial debt (M) = (I+L) (43 0,964) (4 38,273) (394,704) (379,862) (364,06 5) (348,9 92) 29

30 Cash Flow statement as at December 31, 2014 MARR Consolidated ( thousand) Net profit before minority interests 51,105 47,318 48,990 49,608 45,685 38,551 Amortization and depreciation 4,879 4,527 4,252 4,546 4,625 4,753 Change in Staff Severance rovision (582) 577 1,668 (496) (28) 56 Operating cash-flow 55,402 52,422 54,910 53,658 50,282 43,360 (Increase) decrease in receivables from customers 20,611 (19,699) (12,185) (17,743) (7,840) (40,575) (Increase) decrease in inventories (15,662) (1,968) (2,573) 3,422 (14,997) 10,022 Increase (decrease) in payables to suppliers 109 3,961 10,651 (298) 23,092 6,877 (Increase) decrease in other items of the working capital 8,964 (5,857) (8,455) 6,949 (14,134) 9,286 Change in working capital 14,022 (23,563) (12,562) (7,670) (13,879) (14,390) Maintenance CapEx (2,500) (2,400) (2,502) (2,782) (1,904) (1,924) Operating free - cash flow 66,924 26,459 39,846 43,206 34,499 27,046 Extraordinary CapEx and Others (8,515) (22,716) (5,529) (9,401) (3,893) (3,958) Investments in fixed assets (11,015) (25,116) (8,031) (12,183) (5,797) (5,882) Free - cash flow before dividends 58,409 3,743 34,317 33,805 30,606 23,088 Distribution of dividends (38,585) (38,175) (42,124) (32,910) (30,277) (28,302) Capital increase 0 6, Other changes, including those of minority interests (2,377) (1,461) (1,429) (528) (427) (351) Cash-flow from (for) change in shareholders' equity (40,962) (32,650) (43,553) (33,438) (30,704) (28,653) FREE - CASH FLOW 17,447 (28,907) (9,236) 367 (98) (5,565) Opening net financial debt (194,131) (165,224) (155,988) (156,355) (156,257) (150,692) Cash-flow for the period 17,447 (28,907) (9,236) 367 (98) (5,565) Closing net financial debt (176,684) (194,131) (165,224) (155,988) (156,355) (156,257) 30

31 Seasonality as at December 31, 2014 m Total revenues Trade NWC Net debt Consolidated data 31

32 Gross debt maturity as at December 31, 2014 m Non-current debt Y 2Y 2Y-5Y >5Y Consolidated data 32

33 MARR vs peers 7.1% 5.8% 5.9% 4.6% 3.5% 3.4% 3.5% 2.7% 2.0% EBITDA margin EBIT margin Net Income margin 2014 FY 2014 FY FY ended as at 30 June,

34 Contacts Investor Relations Department Antonio Tiso tel mob Léon Van Lancker mob MARR S.p.A. Via Spagna, Rimini (Italy) website 34

1H 2014 Results. Conference call August 4, 2014

1H 2014 Results Conference call August 4, 2014 Important information This presentation is being shown to you solely for your information and may not be reproduced, distributed to any other person or published,

1H 2014 Results Conference call August 4, 2014 Important information This presentation is being shown to you solely for your information and may not be reproduced, distributed to any other person or published,

Financial statements and consolidated financial statements as at December 31, 2009

Financial statements and consolidated financial statements as at December 31, 2009 MARR S.p.A. Via Spagna, 20 47921 Rimini Italy Capital stock 33.262.560 fully paid up Tax code and Trade Register of Rimini

Financial statements and consolidated financial statements as at December 31, 2009 MARR S.p.A. Via Spagna, 20 47921 Rimini Italy Capital stock 33.262.560 fully paid up Tax code and Trade Register of Rimini

BOARD OF DIRECTORS REPORT ON OPERATIONS IN THE 4 TH QUARTER OF 2002

MERLONI ELETTRODOMESTICI SPA Registered office: V.le A. Merloni, 47-60044 Fabriano Rome office: Via della Scrofa, 64 00186 Roma Capital stock: 99,416,219.40 fully paid in Tax/VAT code: 00693740425 Court

MERLONI ELETTRODOMESTICI SPA Registered office: V.le A. Merloni, 47-60044 Fabriano Rome office: Via della Scrofa, 64 00186 Roma Capital stock: 99,416,219.40 fully paid in Tax/VAT code: 00693740425 Court

First Half 2011 Conference Call

Moving ahead First Half 2011 Conference Call 29 th July, 2011 Copyright Datalogic 2007-2011 DISCLAIMER This document has been prepared by Datalogic S.p.A. (the "Company") for use during meetings with investors

Moving ahead First Half 2011 Conference Call 29 th July, 2011 Copyright Datalogic 2007-2011 DISCLAIMER This document has been prepared by Datalogic S.p.A. (the "Company") for use during meetings with investors

Net Financial Position: -5.4 million ( -35,9 million as of December 31, 2016)

") PRESS RELEASE - 2017 RESULTS GEOX HAS CLOSED 2017 WITH SALES AT EURO 884.5 MILLION (-1.8% AT CURRENT FOREX, -1.7% AT CONSTANT FOREX) AND STRONG IMPROVEMENTS IN PROFITABILITY. EBIDTA ADJUSTED 1 UP 40% AND

PRESS RELEASE - 2017 RESULTS GEOX HAS CLOSED 2017 WITH SALES AT EURO 884.5 MILLION (-1.8% AT CURRENT FOREX, -1.7% AT CONSTANT FOREX) AND STRONG IMPROVEMENTS IN PROFITABILITY. EBIDTA ADJUSTED 1 UP 40% AND

Overview of Gruppo Campari & 2008 First Half Results

Overview of Gruppo Campari & 2008 First Half Results Italian Investor Conference Tokyo, 07 October 2008 1 An overview 2 Gruppo Campari is.. > A major player in the global branded beverage industry > A

Overview of Gruppo Campari & 2008 First Half Results Italian Investor Conference Tokyo, 07 October 2008 1 An overview 2 Gruppo Campari is.. > A major player in the global branded beverage industry > A

Financial Results. Full Year March 2017

Financial Results Full Year 2016 March 2017 Disclaimer This presentation is being furnished to you solely for your information and may not be reproduced or redistributed to any other person. This presentation

Financial Results Full Year 2016 March 2017 Disclaimer This presentation is being furnished to you solely for your information and may not be reproduced or redistributed to any other person. This presentation

Quarter ended December 31, High Yield report

Quarter ended December 31, 2013 High Yield report Key Highlights Quarterly Recurring EBITDA in line with guidance provided to markets and above market on revenue and booking growth showing the advantages

Quarter ended December 31, 2013 High Yield report Key Highlights Quarterly Recurring EBITDA in line with guidance provided to markets and above market on revenue and booking growth showing the advantages

title 9 Months 2012 title Conference Call 12 th November 2012 date

title 9 Months 2012 title Conference Call 12 th November 2012 date DISCLAIMER This document has been prepared by Datalogic S.p.A. (the "Company") for use during meetings with investors and financial analysts

title 9 Months 2012 title Conference Call 12 th November 2012 date DISCLAIMER This document has been prepared by Datalogic S.p.A. (the "Company") for use during meetings with investors and financial analysts

On track. Investor and Analyst Presentation On the Occasion of the Release of the Preliminary Figures for Q Hanover, 19 April 2011

On track. Investor and Analyst Presentation On the Occasion of the Release of the Preliminary Figures for Q1 2011 Agenda Delticom at a Glance Business Model Profit & Loss Balance Sheet Outlook 2 Agenda

On track. Investor and Analyst Presentation On the Occasion of the Release of the Preliminary Figures for Q1 2011 Agenda Delticom at a Glance Business Model Profit & Loss Balance Sheet Outlook 2 Agenda

IREN Group: the Board of Directors has approved the results for the year ending 31 December 2017 Improved results (Net profit

IREN Group: the Board of Directors has approved the results for the year ending 31 December 2017 Improved results (Net profit +32%, tripling in the last three years) and a reduction in the net financial

IREN Group: the Board of Directors has approved the results for the year ending 31 December 2017 Improved results (Net profit +32%, tripling in the last three years) and a reduction in the net financial

Logista Q Results. February 1, 2018

Logista Q1 2018 Results February 1, 2018 Logista reports Q1 2018 Results Logista announces today its Q1 Results for 2018. Main highlights: Economic Sales 1 increase by 5.0%, recording improvements over

Logista Q1 2018 Results February 1, 2018 Logista reports Q1 2018 Results Logista announces today its Q1 Results for 2018. Main highlights: Economic Sales 1 increase by 5.0%, recording improvements over

Consolidated income statement figures

The Board of Directors examines the figures for 2 nd quarter and 1 st half 2009 nd Margins increase in 2 nd quarter 2009 and net cash flow generation of 260.4m Consolidated revenues: 1,441.8m, 0.8% vs.

The Board of Directors examines the figures for 2 nd quarter and 1 st half 2009 nd Margins increase in 2 nd quarter 2009 and net cash flow generation of 260.4m Consolidated revenues: 1,441.8m, 0.8% vs.

INTERIM FINANCIAL REPORT AS AT SEPTEMBER 30, 2017 (Translation into English of the original Italian version)

") INTERIM FINANCIAL REPORT AS AT SEPTEMBER 30, 2017 (Translation into English of the original Italian version) JOINT-STOCK COMPANY - SHARE CAPITAL EURO 62.393.755,84 MANTOVA COMPANY REGISTER AND TAX NO.

INTERIM FINANCIAL REPORT AS AT SEPTEMBER 30, 2017 (Translation into English of the original Italian version) JOINT-STOCK COMPANY - SHARE CAPITAL EURO 62.393.755,84 MANTOVA COMPANY REGISTER AND TAX NO.

A Firm Grip. Investor and Analyst Presentation. on the Occasion of the Release of the 9-Monthly Results 2009

A Firm Grip. Investor and Analyst Presentation on the Occasion of the Release of the 9-Monthly Results 2009 Frankfurt am Main, 9th November 2009 Agenda Delticom at a Glance Business Model Seasonalities

A Firm Grip. Investor and Analyst Presentation on the Occasion of the Release of the 9-Monthly Results 2009 Frankfurt am Main, 9th November 2009 Agenda Delticom at a Glance Business Model Seasonalities

PRESS RELEASE. The Board of Directors approves the Consolidated Interim Financial Report for the first half of 2016.

PRESS RELEASE B&C Speakers S.p.A. The Board of Directors approves the Consolidated Interim Financial Report for the first half of 2016. Consolidated revenues of Euro 18.67 million (+0.9% compared with

PRESS RELEASE B&C Speakers S.p.A. The Board of Directors approves the Consolidated Interim Financial Report for the first half of 2016. Consolidated revenues of Euro 18.67 million (+0.9% compared with

2017FY - Results presentation. March 21, 2018

2017FY - Results presentation March 21, 2018 Disclaimer This presentation has been prepared by SIT S.p.A. only for information purposes and for the presentation of the Group s results and strategies. For

2017FY - Results presentation March 21, 2018 Disclaimer This presentation has been prepared by SIT S.p.A. only for information purposes and for the presentation of the Group s results and strategies. For

1Q 14 Results. May 12 th, 2014

Results May 12 th, 2014 First Quarter 2014 - Highlights Results in line with the Group s sustainable approach, gracious growth and healthy profitability, thus laying the foundations for long-term development

Results May 12 th, 2014 First Quarter 2014 - Highlights Results in line with the Group s sustainable approach, gracious growth and healthy profitability, thus laying the foundations for long-term development

Annual Report as at December 31, 2014

Annual Report as at December 31, 2014 MARR S.p.A. Via Spagna, 20 47921 Rimini Italy Capital stock 33.262.560 fully paid up Tax code and Trade Register of Rimini 01836980365 R.E.A. Ufficio di Rimini n.

Annual Report as at December 31, 2014 MARR S.p.A. Via Spagna, 20 47921 Rimini Italy Capital stock 33.262.560 fully paid up Tax code and Trade Register of Rimini 01836980365 R.E.A. Ufficio di Rimini n.

EGP 2.9 BN 51.1% y-o-y. EGP 216 MN 44.9% y-o-y. EGP 92 MN 69.4% y-o-y. EGP 28 MN 46.3% y-o-y. EGP 36 MN 88.4% y-o-y.

EARNINGS RELEASE Ibnsina Pharma Releases Audited Results Ibnsina Pharma starts 2018 off strong with year-on-year revenue and EBITDA growth of 51% and 69% respectively in 1Q2018, ensuring a sustained growth

EARNINGS RELEASE Ibnsina Pharma Releases Audited Results Ibnsina Pharma starts 2018 off strong with year-on-year revenue and EBITDA growth of 51% and 69% respectively in 1Q2018, ensuring a sustained growth

INVESTOR PRESENTATION

INVESTOR PRESENTATION 1Q 2018 RESULTS published on April 20, 2018 Magnit at a Glance Magnit at a Glance As of March 31, 2018 2 764 Cities & Towns 16 625 Total Number of Stores 5 830 Selling Space (thous.sq.m.)

INVESTOR PRESENTATION 1Q 2018 RESULTS published on April 20, 2018 Magnit at a Glance Magnit at a Glance As of March 31, 2018 2 764 Cities & Towns 16 625 Total Number of Stores 5 830 Selling Space (thous.sq.m.)

Milan September 11 th, 2003

Milan September 11 th, 2003 TOD S Group: growth in turnover, speeding up the development plan The Board of Directors of Tod s S.p.A., the Italian company listed on the Milan Stock Exchange and holding

Milan September 11 th, 2003 TOD S Group: growth in turnover, speeding up the development plan The Board of Directors of Tod s S.p.A., the Italian company listed on the Milan Stock Exchange and holding

INVESTOR PRESENTATION

INVESTOR PRESENTATION 9M 2017 OPERATIONAL RESULTS published on October 20, 2017 Magnit at a Glance Magnit at a Glance As of September 30, 2017 2 664 Cities & Towns 15 697 Total Number of Stores 5 563 Selling

INVESTOR PRESENTATION 9M 2017 OPERATIONAL RESULTS published on October 20, 2017 Magnit at a Glance Magnit at a Glance As of September 30, 2017 2 664 Cities & Towns 15 697 Total Number of Stores 5 563 Selling

A Firm Grip. Investor and Analyst Presentation. on the Occasion of the Release of the 3-Monthly Results 2009

A Firm Grip. Investor and Analyst Presentation on the Occasion of the Release of the 3-Monthly Results 2009 Agenda Delticom at a Glance Business Model Seasonalities in the Tyre Trade Financials Outlook

A Firm Grip. Investor and Analyst Presentation on the Occasion of the Release of the 3-Monthly Results 2009 Agenda Delticom at a Glance Business Model Seasonalities in the Tyre Trade Financials Outlook

Financial Results 1H August 2016

Financial Results 1H 2016 August 2016 Disclaimer This presentation is being furnished to you solely for your information and may not be reproduced or redistributed to any other person. This presentation

Financial Results 1H 2016 August 2016 Disclaimer This presentation is being furnished to you solely for your information and may not be reproduced or redistributed to any other person. This presentation

Fare clic per modificare lo stile del titolo FY 2006 Financial Results

Fare clic per modificare lo stile del titolo FY 2006 Financial Results Star Conference Milan, March 1st 2007 THE GROUP DATALOGIC OFFER UPDATE ON PSC FINANCIAL HIGHLIGHTS TRANSFORMATION PLAN 2 Datalogic

Fare clic per modificare lo stile del titolo FY 2006 Financial Results Star Conference Milan, March 1st 2007 THE GROUP DATALOGIC OFFER UPDATE ON PSC FINANCIAL HIGHLIGHTS TRANSFORMATION PLAN 2 Datalogic

Breakdown of Consolidated Sales by Brand: significant growth rates for all the brands. million Euros Q Q % change FY 2006

Milan May 14 th, 2007 TOD S S.p.A.: revenues and profits continue to grow The Board of Directors approved Tod s Group Q1 2007 results. Q1 2007 Group s revenues: 177,7 million Euros, increasing by 10% versus

Milan May 14 th, 2007 TOD S S.p.A.: revenues and profits continue to grow The Board of Directors approved Tod s Group Q1 2007 results. Q1 2007 Group s revenues: 177,7 million Euros, increasing by 10% versus

FY 2012 Results. March 12 th, 2013

FY 2012 Results March 12 th, 2013 Fiscal Year 2012 Results Highlights FY 2012 results showing top line growth and profitability increase*, in line with company expectations Net Revenues up 15.1% to 279.3mln

FY 2012 Results March 12 th, 2013 Fiscal Year 2012 Results Highlights FY 2012 results showing top line growth and profitability increase*, in line with company expectations Net Revenues up 15.1% to 279.3mln

FY 2014 Results Presentation March 5, 2015

FY 2014 Results Presentation March 5, 2015 FY 2014 key facts Sales: Euro 824.2 million +9.3% (+10.1% constant FX) Directly Operated Stores Same Store Sales: +7.9% (vs -3.0% in FY 13) EBITDA: Euro 42.6

FY 2014 Results Presentation March 5, 2015 FY 2014 key facts Sales: Euro 824.2 million +9.3% (+10.1% constant FX) Directly Operated Stores Same Store Sales: +7.9% (vs -3.0% in FY 13) EBITDA: Euro 42.6

NATUZZI: GROUP RESULTS CONTINUE TO IMPROVE POSITIVE EBITDA IN 2015

2015 CONSOLIDATED RESULTS NATUZZI: GROUP RESULTS CONTINUE TO IMPROVE POSITIVE EBITDA IN 2015 CONSOLIDATED NET SALES OF 488.5 MILLION, UP 5.9% FROM 2014 (AT CURRENT EXCHANGE RATES) GROSS MARGIN OF 32.3%,

2015 CONSOLIDATED RESULTS NATUZZI: GROUP RESULTS CONTINUE TO IMPROVE POSITIVE EBITDA IN 2015 CONSOLIDATED NET SALES OF 488.5 MILLION, UP 5.9% FROM 2014 (AT CURRENT EXCHANGE RATES) GROSS MARGIN OF 32.3%,

Forward-Looking Statements

March 2006 0 Forward-Looking Statements This presentation contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are outside our control. These forward-looking

March 2006 0 Forward-Looking Statements This presentation contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are outside our control. These forward-looking

PRESS RELEASE. The Board of Directors approves the Consolidated Interim Financial Report for the first half of 2017.

PRESS RELEASE B&C Speakers S.p.A. The Board of Directors approves the Consolidated Interim Financial Report for the first half of 2017. Consolidated revenues of Euro 20.12 million (+7.7% compared with

PRESS RELEASE B&C Speakers S.p.A. The Board of Directors approves the Consolidated Interim Financial Report for the first half of 2017. Consolidated revenues of Euro 20.12 million (+7.7% compared with

INVESTOR PRESENTATION

INVESTOR PRESENTATION 1H 2018 RESULTS published on July 26, 2018 Magnit at a Glance Magnit at a Glance As of June 30, 2018 2 808 Cities & Towns 16 960 Total Number of Stores 5 945 Selling Space (thous.sq.m.)

INVESTOR PRESENTATION 1H 2018 RESULTS published on July 26, 2018 Magnit at a Glance Magnit at a Glance As of June 30, 2018 2 808 Cities & Towns 16 960 Total Number of Stores 5 945 Selling Space (thous.sq.m.)

Strategy Presentation

2010 2013 Strategy Presentation Milan, March 11 th, 2010 www.snamretegas.it Disclaimer Snam Rete Gas s Chief Financial Officer, Antonio Paccioretti, in his position as manager responsible for the preparation

2010 2013 Strategy Presentation Milan, March 11 th, 2010 www.snamretegas.it Disclaimer Snam Rete Gas s Chief Financial Officer, Antonio Paccioretti, in his position as manager responsible for the preparation

Agenda. Our Business Rock Solid. Performance in last 5 Years. Delivering Returns in CRH. CRH plc, AGM

Agenda Our Business Rock Solid Performance in last 5 Years Delivering Returns in CRH CRH plc, AGM 2018 1 Why invest in Building Materials? Natural demand for construction products driven by: Population

Agenda Our Business Rock Solid Performance in last 5 Years Delivering Returns in CRH CRH plc, AGM 2018 1 Why invest in Building Materials? Natural demand for construction products driven by: Population

1H18 FINANCIAL RESULTS. September 19, 2018

1H18 FINANCIAL RESULTS September 19, 2018 Disclaimer 1 This presentation is being furnished to you solely for your information and may not be reproduced or redistributed to any other person. This presentation

1H18 FINANCIAL RESULTS September 19, 2018 Disclaimer 1 This presentation is being furnished to you solely for your information and may not be reproduced or redistributed to any other person. This presentation

Salvatore Ferragamo S.p.A.

PRESS RELEASE Salvatore Ferragamo S.p.A. The Board of Directors Approves the Consolidated Financial Statement as of 30 June 2017 Salvatore Ferragamo Group First Half Revenue +1.1%, Gross Operating Profit

PRESS RELEASE Salvatore Ferragamo S.p.A. The Board of Directors Approves the Consolidated Financial Statement as of 30 June 2017 Salvatore Ferragamo Group First Half Revenue +1.1%, Gross Operating Profit

H Conference Call

H1 2018 Conference Call August 9, 2018 Disclaimer This document has been prepared by Datalogic S.p.A. (the "Company") for use during meetings with investors and financial analysts and is solely for information

H1 2018 Conference Call August 9, 2018 Disclaimer This document has been prepared by Datalogic S.p.A. (the "Company") for use during meetings with investors and financial analysts and is solely for information

Geox breathes again. BSIC - Equity Research Corporate Finance Team. The new business plan is back on track. December 2014

BSIC - Equity Research Corporate Finance Team December 2014 www.bsic.it Geox breathes again The new business plan is back on track Geox is an Italian footwear and apparel company that focuses on the medium

BSIC - Equity Research Corporate Finance Team December 2014 www.bsic.it Geox breathes again The new business plan is back on track Geox is an Italian footwear and apparel company that focuses on the medium

Consolidated revenues: million Euros, EBITDA: million Euros, EBIT: million Euros, Net income: 83.4 million Euros

Milan March 24 th, 2009 TOD S S.p.A Outstanding growth for Tod s Group s: revenues: +7.7%, net income: + 7.9%. Dividend unchanged at 1.25 Euro per share The Board of Directors approved the 2008 Annual

Milan March 24 th, 2009 TOD S S.p.A Outstanding growth for Tod s Group s: revenues: +7.7%, net income: + 7.9%. Dividend unchanged at 1.25 Euro per share The Board of Directors approved the 2008 Annual

PREMIUM BRANDS HOLDINGS CORPORATION. For the 13 and 26 Weeks Ended June 30, 2012

PREMIUM BRANDS HOLDINGS CORPORATION Management s Discussion and Analysis For the 13 and 26 Weeks Ended June 30, 2012 The following Management s Discussion and Analysis (MD&A) is a review of the financial

PREMIUM BRANDS HOLDINGS CORPORATION Management s Discussion and Analysis For the 13 and 26 Weeks Ended June 30, 2012 The following Management s Discussion and Analysis (MD&A) is a review of the financial

EARNINGS RELEASE 3Q17

LOGISTICS INVESTMENT PLATFORM EARNINGS RELEASE 3Q17 1 Quarterly Results 3Q17 TRAXION S REVENUE AND EBITDA INCREASE 70% AND 56% DURING 3Q17 BOOSTED BY ACQUISITIONS CONSOLIDATION YTD 2017 REVENUE AND EBITDA

LOGISTICS INVESTMENT PLATFORM EARNINGS RELEASE 3Q17 1 Quarterly Results 3Q17 TRAXION S REVENUE AND EBITDA INCREASE 70% AND 56% DURING 3Q17 BOOSTED BY ACQUISITIONS CONSOLIDATION YTD 2017 REVENUE AND EBITDA

1H10 Conference Call. Bologna 30 th July, 2010

1H10 Conference Call Bologna 30 th July, 2010 HIGHLIGHTS 1H10 FINANCIAL RESULTS OUTLOOK 2 Datalogic at a glance Datalogic is a worldwide leader in the Automatic Data Capture (ADC) market and in the Factory

1H10 Conference Call Bologna 30 th July, 2010 HIGHLIGHTS 1H10 FINANCIAL RESULTS OUTLOOK 2 Datalogic at a glance Datalogic is a worldwide leader in the Automatic Data Capture (ADC) market and in the Factory

Forward-Looking Statements

William Blair & Company 27 th Annual Growth Stock Conference June 20, 2007 0 Forward-Looking Statements This presentation contains forward-looking statements that are subject to a number of risks and uncertainties,

William Blair & Company 27 th Annual Growth Stock Conference June 20, 2007 0 Forward-Looking Statements This presentation contains forward-looking statements that are subject to a number of risks and uncertainties,

9M 2018 Conference Call

9M 2018 Conference Call November 13, 2018 Disclaimer This document has been prepared by Datalogic S.p.A. (the "Company") for use during meetings with investors and financial analysts and is solely for

9M 2018 Conference Call November 13, 2018 Disclaimer This document has been prepared by Datalogic S.p.A. (the "Company") for use during meetings with investors and financial analysts and is solely for

1H15 Results Presentation. July 30, 2015

1H15 Results Presentation July 30, 2015 1H15 Key facts Sales: Euro 426.9 million +6.7% (+4.0% constant FX) Directly Operated Stores Same Store Sales: +6.4% (2Q15 +7.9%) EBITDA: Euro 26.6 million +28.3%

1H15 Results Presentation July 30, 2015 1H15 Key facts Sales: Euro 426.9 million +6.7% (+4.0% constant FX) Directly Operated Stores Same Store Sales: +6.4% (2Q15 +7.9%) EBITDA: Euro 26.6 million +28.3%

9M 2016 RESULTS NICE PRESENTATION. November 2016, 11 th

NICE PRESENTATION November 2016, 11 th 1 FINANCIAL OVERVIEW 2 Consolidated Sales: 230.0m (+7.3% vs. 9M 2015) Gross margin: 53.1% (vs. 54.9% in 9M 2015) EBITDA margin: 15.0% (vs. 15.8% in 9M 2015) HIGHLIGHTS

NICE PRESENTATION November 2016, 11 th 1 FINANCIAL OVERVIEW 2 Consolidated Sales: 230.0m (+7.3% vs. 9M 2015) Gross margin: 53.1% (vs. 54.9% in 9M 2015) EBITDA margin: 15.0% (vs. 15.8% in 9M 2015) HIGHLIGHTS

AMPLIFON: THE PATH OF STRONG GROWTH AND IMPROVING

AMPLIFON: THE PATH OF STRONG GROWTH AND IMPROVING PROFITABILITY CONTINUES DOUBLE DIGIT GROWTH IN REVENUES AND SIGNIFICANT INCREASE IN PROFITABILITY STRONG CONTRIBUTION FROM ACQUISITIONS, PARTICULARLY IN

AMPLIFON: THE PATH OF STRONG GROWTH AND IMPROVING PROFITABILITY CONTINUES DOUBLE DIGIT GROWTH IN REVENUES AND SIGNIFICANT INCREASE IN PROFITABILITY STRONG CONTRIBUTION FROM ACQUISITIONS, PARTICULARLY IN

1H 2014 Results Presentation July 31, 2014

1H 2014 Results Presentation July 31, 2014 1H 2014 key facts Sales: Euro 400.2 million +3.5% (+4.1% constant FX) Directly Operated Stores Same Store Sales: +8.2% (vs -7.6% in 1H 13) EBITDA: Euro 20.7 million,

1H 2014 Results Presentation July 31, 2014 1H 2014 key facts Sales: Euro 400.2 million +3.5% (+4.1% constant FX) Directly Operated Stores Same Store Sales: +8.2% (vs -7.6% in 1H 13) EBITDA: Euro 20.7 million,

H Financial Results

H1 2016 Financial Results Gilles Petit, CEO Arnaud Louet, CFO H1 2016 Financial Results FORWARD LOOKING STATEMENTS This presentation does not constitute an offer to sell securities in the United States

H1 2016 Financial Results Gilles Petit, CEO Arnaud Louet, CFO H1 2016 Financial Results FORWARD LOOKING STATEMENTS This presentation does not constitute an offer to sell securities in the United States

Logista FY 2016 Results. November 8, 2016

Logista FY 2016 Results November 8, 2016 Logista reports FY 2016 Results Logista announces today its FY Results for 2016. Main highlights: Revenues growing by 1.7% Economic Sales 1 up by 2.8% Adjusted

Logista FY 2016 Results November 8, 2016 Logista reports FY 2016 Results Logista announces today its FY Results for 2016. Main highlights: Revenues growing by 1.7% Economic Sales 1 up by 2.8% Adjusted

Results Presentation Q1 2017

Results Presentation Q1 2017 May 09 2017 1 IPO Prosegur CASH at a Glance Start of Trading: 17 March 2017 Initial Price: 2 per Share Europe 7% Spain 3% US 37% Subscribed Volume: 412.5 million shares (27.5%

Results Presentation Q1 2017 May 09 2017 1 IPO Prosegur CASH at a Glance Start of Trading: 17 March 2017 Initial Price: 2 per Share Europe 7% Spain 3% US 37% Subscribed Volume: 412.5 million shares (27.5%

STAR Conference. 6 th October 2016, London

STAR Conference 6 th October 2016, London Elica Corporation N#1 PLAYER WORLDWIDE IN HOODS 13% MARKET SHARE 2015 TURNOVER 421.6 M 8 INDUSTRIAL PLANTS WORLDWIDE 2 19 Mln Hoods + Motors Cooking Net Sales:

STAR Conference 6 th October 2016, London Elica Corporation N#1 PLAYER WORLDWIDE IN HOODS 13% MARKET SHARE 2015 TURNOVER 421.6 M 8 INDUSTRIAL PLANTS WORLDWIDE 2 19 Mln Hoods + Motors Cooking Net Sales:

CFA EQUITY RESEARCH CHALLENGE 2014

Milan February 2014 CFA EQUITY RESEARCH CHALLENGE 2014 A tailor-made investment Marta Giampietro Federico Braga Matteo Cataldi Davide Di Bucchianico Giovanni Galvani Agenda Introduction and investment

Milan February 2014 CFA EQUITY RESEARCH CHALLENGE 2014 A tailor-made investment Marta Giampietro Federico Braga Matteo Cataldi Davide Di Bucchianico Giovanni Galvani Agenda Introduction and investment

FY17 FINANCIAL RESULTS. April 18, 2018

FY17 FINANCIAL RESULTS April 18, 2018 Disclaimer 1 This presentation is being furnished to you solely for your information and may not be reproduced or redistributed to any other person. This presentation

FY17 FINANCIAL RESULTS April 18, 2018 Disclaimer 1 This presentation is being furnished to you solely for your information and may not be reproduced or redistributed to any other person. This presentation

Press release August 30, FIRST-HALF 2017 RESULTS Solid sales growth of +6.2% Recurring operating income of 621m

FIRST-HALF 2017 RESULTS Solid sales growth of +6.2% Recurring operating income of 621m Net sales up +6.2% to 38.5bn, reflecting the combination of a good like-for-like performance and the effect of expansion:

FIRST-HALF 2017 RESULTS Solid sales growth of +6.2% Recurring operating income of 621m Net sales up +6.2% to 38.5bn, reflecting the combination of a good like-for-like performance and the effect of expansion:

1Q 2017 Results. 10 May Investor Relations

1Q 2017 Results 10 May 2017 Investor Relations OPENING REMARKS ( m) Key Numbers Var % Revenues 9,759 9,539-2% EBIT 562 526-6% Net Profit 367 351-4% Investor Relations 2 1Q 2017: FIGURES HIGHLIGHTS ( m)

1Q 2017 Results 10 May 2017 Investor Relations OPENING REMARKS ( m) Key Numbers Var % Revenues 9,759 9,539-2% EBIT 562 526-6% Net Profit 367 351-4% Investor Relations 2 1Q 2017: FIGURES HIGHLIGHTS ( m)

PREMIUM BRANDS HOLDINGS CORPORATION

PREMIUM BRANDS HOLDINGS CORPORATION Management s Discussion and Analysis For the 13 Weeks Ended March 31, The following Management s Discussion and Analysis (MD&A) is a review of the financial performance

PREMIUM BRANDS HOLDINGS CORPORATION Management s Discussion and Analysis For the 13 Weeks Ended March 31, The following Management s Discussion and Analysis (MD&A) is a review of the financial performance

Months Results. November 12 th, 2013

2013 9 Months Results November 12 th, 2013 9 Months 2013 Results - Highlights Sustainable growth and healthy profitability in the first nine months 2013, consistent with sophisticated consumer demand,

2013 9 Months Results November 12 th, 2013 9 Months 2013 Results - Highlights Sustainable growth and healthy profitability in the first nine months 2013, consistent with sophisticated consumer demand,

H FINANCIAL RESULTS. August 30,

August 30, 2017 1 Disclaimer This presentation contains both historical and forward-looking statements. These forward-looking statements are based on Carrefour management's current views and assumptions.

August 30, 2017 1 Disclaimer This presentation contains both historical and forward-looking statements. These forward-looking statements are based on Carrefour management's current views and assumptions.

February 10, Astaldi. 4Q 2004 and 2004 Preliminary Results

Astaldi 4Q 2004 and 2004 Preliminary Results February 10, 2005 1 Main Highlights (Million of euro) 2004 yoy 2006 CAGR 03-06 2004 RESULTS ABOVE 2004-2006 STRATEGIC PLAN TARGETS Order backlog 5,011 13.7%

Astaldi 4Q 2004 and 2004 Preliminary Results February 10, 2005 1 Main Highlights (Million of euro) 2004 yoy 2006 CAGR 03-06 2004 RESULTS ABOVE 2004-2006 STRATEGIC PLAN TARGETS Order backlog 5,011 13.7%

1H 2016 RESULTS NICE PRESENTATION. August 2016, 5 TH

NICE PRESENTATION August 2016, 5 TH 1 FINANCIAL OVERVIEW 2 Consolidated Sales: 150.2m (+5.3% vs. 1H 2015) Gross margin: 53.7% (vs. 55.1% in 1H 2015) EBITDA margin: 15.0% (vs. 14.7% in 1H 2015) HIGHLIGHTS

NICE PRESENTATION August 2016, 5 TH 1 FINANCIAL OVERVIEW 2 Consolidated Sales: 150.2m (+5.3% vs. 1H 2015) Gross margin: 53.7% (vs. 55.1% in 1H 2015) EBITDA margin: 15.0% (vs. 14.7% in 1H 2015) HIGHLIGHTS

May 15th, 2018 Consolidated Results 1Q2018 0

May 15 th, 2018 0 Index 2. MISSION 3. COMPANY OVERVIEW- IVS AT A GLANCE 4. COMPANY OFFICERS 5. GROUP STRUCTURE 6. HIGHLIGHTS 7. KPI 1Q2018 8. KEY MESSAGE FOR 1Q2018 10. ADJUSTED CONSOLIDATED INCOME STATEMENT

May 15 th, 2018 0 Index 2. MISSION 3. COMPANY OVERVIEW- IVS AT A GLANCE 4. COMPANY OFFICERS 5. GROUP STRUCTURE 6. HIGHLIGHTS 7. KPI 1Q2018 8. KEY MESSAGE FOR 1Q2018 10. ADJUSTED CONSOLIDATED INCOME STATEMENT

INTERIM FINANCIAL REPORT AS AT MARCH 31, 2018

INTERIM FINANCIAL REPORT AS AT MARCH 31, 2018 (Translation into English of the original Italian version) JOINT-STOCK COMPANY - SHARE CAPITAL EURO 62,461,355.84 MANTOVA COMPANY REGISTER AND TAX CODE 00607460201

INTERIM FINANCIAL REPORT AS AT MARCH 31, 2018 (Translation into English of the original Italian version) JOINT-STOCK COMPANY - SHARE CAPITAL EURO 62,461,355.84 MANTOVA COMPANY REGISTER AND TAX CODE 00607460201

Logista Q Results. July 26, 2018

Logista Q3 2018 Results July 26, 2018 Logista reports Q3 2018 Results Logista announces today its Q3 Results for 2018. Main highlights: Economic Sales 1 increase by 7,8% improving the 1.3% drop in Revenues

Logista Q3 2018 Results July 26, 2018 Logista reports Q3 2018 Results Logista announces today its Q3 Results for 2018. Main highlights: Economic Sales 1 increase by 7,8% improving the 1.3% drop in Revenues

DeA Capital. XXXXXXXXXXX [TITOLO] DeA Capital update. London 1 October 2013 Star Conference

![DeA Capital. XXXXXXXXXXX [TITOLO] DeA Capital update. London 1 October 2013 Star Conference](/thumbs/95/126019269.jpg "DeA Capital. XXXXXXXXXXX [TITOLO] DeA Capital update. London 1 October 2013 Star Conference") DeA Capital XXXXXXXXXXX [TITOLO] DeA Capital update London 1 October 2013 Star Conference 1 1 DeA Capital at a glance Private equity Direct investments Private healthcare 1.9 bn revenues Food retail 2.7

DeA Capital XXXXXXXXXXX [TITOLO] DeA Capital update London 1 October 2013 Star Conference 1 1 DeA Capital at a glance Private equity Direct investments Private healthcare 1.9 bn revenues Food retail 2.7

1H16 Results Investor Presentation

1H16 Results Investor Presentation Ernesto Mauri, CEO Oddone Pozzi, CFO Segrate, July 28th 2016 AGENDA 1-1H16 Highlights 2-1H16 Results 3 - FY 2016 Outlook 1H16 Highlights Transformational deals Consolidated

1H16 Results Investor Presentation Ernesto Mauri, CEO Oddone Pozzi, CFO Segrate, July 28th 2016 AGENDA 1-1H16 Highlights 2-1H16 Results 3 - FY 2016 Outlook 1H16 Highlights Transformational deals Consolidated

9M 2017 Results Massimo Zanetti Beverage Group. Villorba, 9 th of November, 2017

9M 2017 Results Massimo Zanetti Beverage Group Villorba, 9 th of November, 2017 Safe Harbour Statement This document, and in particular the section entitled 2017 Outlook, contains forward-looking statements,

9M 2017 Results Massimo Zanetti Beverage Group Villorba, 9 th of November, 2017 Safe Harbour Statement This document, and in particular the section entitled 2017 Outlook, contains forward-looking statements,

9M 2014 Results Presentation November 13, 2014

9M 2014 Results Presentation November 13, 2014 9M 2014 key facts Sales: Euro 668.4 million +8.1% (+8.8% constant FX) Directly Operated Stores Same Store Sales: +9.4% (vs -5.7% in 9M 13) EBITDA: Euro 46.3

9M 2014 Results Presentation November 13, 2014 9M 2014 key facts Sales: Euro 668.4 million +8.1% (+8.8% constant FX) Directly Operated Stores Same Store Sales: +9.4% (vs -5.7% in 9M 13) EBITDA: Euro 46.3

Autogrill: robust like for like revenue growth of 3.9% in the fist half of 2018

The Board of Directors approves the consolidated results at 30 June 2018 Autogrill: robust like for like revenue growth of 3.9% in the fist half of 2018 Revenue up 5.2% to 2.1 billion 1 All regions contributing

The Board of Directors approves the consolidated results at 30 June 2018 Autogrill: robust like for like revenue growth of 3.9% in the fist half of 2018 Revenue up 5.2% to 2.1 billion 1 All regions contributing

PRESS RELEASE. De'Longhi S.p.A. The Shareholders Annual General Meeting, held today in ordinary session:

PRESS RELEASE De'Longhi S.p.A. The Shareholders Annual General Meeting, held today in ordinary session: (i) approved the consolidated 2017 results, confirming the data approved by the Board of Directors

PRESS RELEASE De'Longhi S.p.A. The Shareholders Annual General Meeting, held today in ordinary session: (i) approved the consolidated 2017 results, confirming the data approved by the Board of Directors

FY 2016 Results Presentation. Milan, 19 th April 2017

FY 2016 Results Presentation Milan, 19 th April 2017 Advertising MEDIASET CONFIDENCE FY 2016 INDEXES Advertising CONSUMERS, revenues MANUFACTURERS growth & vs RETAILERS Total advertising market Total ad

FY 2016 Results Presentation Milan, 19 th April 2017 Advertising MEDIASET CONFIDENCE FY 2016 INDEXES Advertising CONSUMERS, revenues MANUFACTURERS growth & vs RETAILERS Total advertising market Total ad

PRESS RELEASE. Total Revenues: 1,153 million Euros (+17% compared to 986 million Euros of FY 2011)

") PRESS RELEASE Another year of strong growth in Revenues and Profitability for Salvatore Ferragamo Group: Total Turnover +17%, Operating Profit +24% and Group Net Profit +30% Total Revenues: 1,153 million

PRESS RELEASE Another year of strong growth in Revenues and Profitability for Salvatore Ferragamo Group: Total Turnover +17%, Operating Profit +24% and Group Net Profit +30% Total Revenues: 1,153 million

SALES IN LINE WITH LAST YEAR THANKS TO THE POSITIVE

PRESS RELEASE - FIRST HALF 2017 RESULTS SALES IN LINE WITH LAST YEAR THANKS TO THE POSITIVE PERFORMANCE OF THE WHOLESALE CHANNEL, UP 6.7% AND ECOMMERCE UP MORE THAN 30% Biadene di Montebelluna, July 28,

PRESS RELEASE - FIRST HALF 2017 RESULTS SALES IN LINE WITH LAST YEAR THANKS TO THE POSITIVE PERFORMANCE OF THE WHOLESALE CHANNEL, UP 6.7% AND ECOMMERCE UP MORE THAN 30% Biadene di Montebelluna, July 28,

TOD S S.p.A. Outstanding results in the first half of 2009: sales and net income grew, respectively, by 3.4% and by 3.1%

Sant Elpidio a Mare August 26 th, 2009 TOD S S.p.A. Outstanding results in the first half of 2009: sales and net income grew, respectively, by 3.4% and by 3.1% Group s revenues: 359 million Euros; EBITDA:

Sant Elpidio a Mare August 26 th, 2009 TOD S S.p.A. Outstanding results in the first half of 2009: sales and net income grew, respectively, by 3.4% and by 3.1% Group s revenues: 359 million Euros; EBITDA:

PRESS RELEASE. De'Longhi S.p.A.

PRESS RELEASE De'Longhi S.p.A. The Board of Directors has approved today the consolidated results of the first nine months of 2017: growth was accelerating, supported by United States, China and East Europe:

PRESS RELEASE De'Longhi S.p.A. The Board of Directors has approved today the consolidated results of the first nine months of 2017: growth was accelerating, supported by United States, China and East Europe:

PRESENTATION GERMAN CORPORATE CONFERENCE

PRESENTATION GERMAN CORPORATE CONFERENCE 17 January 2018 1 DISCLAIMER To the extent that statements in this presentation do not relate to historical or current facts, they constitute forward-looking statements.

PRESENTATION GERMAN CORPORATE CONFERENCE 17 January 2018 1 DISCLAIMER To the extent that statements in this presentation do not relate to historical or current facts, they constitute forward-looking statements.

MONCLER S.P.A.: THE BOARD OF DIRECTORS APPROVES THE HALF-YEAR FINANCIAL REPORT AS OF 30 JUNE

_ MONCLER S.P.A.: THE BOARD OF DIRECTORS APPROVES THE HALF-YEAR FINANCIAL REPORT AS OF 30 JUNE 2018 1 STRONG DOUBLE-DIGIT REVENUE GROWTH CONTINUED (+27% AT CONST. EXCH. RATES) WITH THE STRENGTHENING OF

_ MONCLER S.P.A.: THE BOARD OF DIRECTORS APPROVES THE HALF-YEAR FINANCIAL REPORT AS OF 30 JUNE 2018 1 STRONG DOUBLE-DIGIT REVENUE GROWTH CONTINUED (+27% AT CONST. EXCH. RATES) WITH THE STRENGTHENING OF

GROWTH A STRONG COMMITMENT

GROWTH A STRONG COMMITMENT INDEX 1. THE GROUP TODAY INDEX 2. STRATEGY OVERVIEW 3. OUTLOOK 2.1. Strategic Pillars 2.2. Strategic Paths 2 1. THE GROUP TODAY 3 1. THE GROUP TODAY PORTUGAL POLAND Supermarkets

GROWTH A STRONG COMMITMENT INDEX 1. THE GROUP TODAY INDEX 2. STRATEGY OVERVIEW 3. OUTLOOK 2.1. Strategic Pillars 2.2. Strategic Paths 2 1. THE GROUP TODAY 3 1. THE GROUP TODAY PORTUGAL POLAND Supermarkets

DeA Capital. XXXXXXXXXXX [TITOLO] DeA Capital update

![DeA Capital. XXXXXXXXXXX [TITOLO] DeA Capital update](/thumbs/91/105675082.jpg "DeA Capital. XXXXXXXXXXX [TITOLO] DeA Capital update") DeA Capital XXXXXXXXXXX [TITOLO] DeA Capital update September 2014 1 1 DeA Capital at a glance Private Equity Direct investments Food retail 2.5 bn sales Private healthcare 1.7 bn revenues Fund Investments

DeA Capital XXXXXXXXXXX [TITOLO] DeA Capital update September 2014 1 1 DeA Capital at a glance Private Equity Direct investments Food retail 2.5 bn sales Private healthcare 1.7 bn revenues Fund Investments

PRESS RELEASE FILA: GROUP INTEGRATION ACCELERATES ***

PRESS RELEASE FILA: GROUP INTEGRATION ACCELERATES 1H2017 Core Business Revenue of Euro 260.5 million, up 29.3% on 1H2016 (Euro 59.0 million), mainly thanks to the acquisitions concluded in the previous

PRESS RELEASE FILA: GROUP INTEGRATION ACCELERATES 1H2017 Core Business Revenue of Euro 260.5 million, up 29.3% on 1H2016 (Euro 59.0 million), mainly thanks to the acquisitions concluded in the previous

Disclaimer: Forward Looking Statements

20 February 2018 Disclaimer: Forward Looking Statements This presentation/announcement may contain forward looking statements with projections regarding, among other things, the Group s strategy, revenues,

20 February 2018 Disclaimer: Forward Looking Statements This presentation/announcement may contain forward looking statements with projections regarding, among other things, the Group s strategy, revenues,

PRESS RELEASE. Damiani S.p.A: The Board of Directors approved the draft Financial Statements as of 31 March

PRESS RELEASE Damiani S.p.A: The Board of Directors approved the draft Financial Statements as of 31 March 2009 1 Consolidated Revenues: Euro 149.8 million (Euro 165.6 million as of 31 March 2008 2 ) Retail

PRESS RELEASE Damiani S.p.A: The Board of Directors approved the draft Financial Statements as of 31 March 2009 1 Consolidated Revenues: Euro 149.8 million (Euro 165.6 million as of 31 March 2008 2 ) Retail

2017 FULL YEAR RESULTS. February 28,

2017 FULL YEAR RESULTS February 28, 2018 1 Disclaimer This presentation contains both historical and forward-looking statements. These forward-looking statements are based on Carrefour management's current

2017 FULL YEAR RESULTS February 28, 2018 1 Disclaimer This presentation contains both historical and forward-looking statements. These forward-looking statements are based on Carrefour management's current

Tourism Holdings. ROCE exceeds 14% long-term target. Key drivers remain positive. Deeper customer relationships to drive yield

Tourism Holdings ROCE exceeds 14% longterm target FY16 results Travel & leisure Tourism Holdings (THL s) FY16 NPAT of NZ$24.4m was in line with company guidance, 21% ahead of FY15 and 1.3% below our forecasts.

Tourism Holdings ROCE exceeds 14% longterm target FY16 results Travel & leisure Tourism Holdings (THL s) FY16 NPAT of NZ$24.4m was in line with company guidance, 21% ahead of FY15 and 1.3% below our forecasts.

Technology for shaping everyday materials. Milan March 2011

Technology for shaping everyday materials Milan March 2011 Group business structure wood glass & stone mechatronic service tooling 1 1 summary: sales breakdown & orders trend main business divisions market

Technology for shaping everyday materials Milan March 2011 Group business structure wood glass & stone mechatronic service tooling 1 1 summary: sales breakdown & orders trend main business divisions market

INTERIM FINANCIAL REPORT AS AT SEPTEMBER 30, 2013 (Translation into English of the original Italian version)

") INTERIM FINANCIAL REPORT AS AT SEPTEMBER 30, 2013 (Translation into English of the original Italian version) JOINTSTOCK COMPANY SHARE CAPITAL EURO 60,924,391.84 MANTOVA COMPANY REGISTER AND TAX CODE 00607460201

INTERIM FINANCIAL REPORT AS AT SEPTEMBER 30, 2013 (Translation into English of the original Italian version) JOINTSTOCK COMPANY SHARE CAPITAL EURO 60,924,391.84 MANTOVA COMPANY REGISTER AND TAX CODE 00607460201

LA DORIA - Board of Directors approves 2018 Third Quarter Report.

PRESS RELEASE LA DORIA - Board of Directors approves 2018 Third Quarter Report. Revenues up thanks to improved sales volumes, with margin reducing due to lower sales prices and increased tomato processing

PRESS RELEASE LA DORIA - Board of Directors approves 2018 Third Quarter Report. Revenues up thanks to improved sales volumes, with margin reducing due to lower sales prices and increased tomato processing

Fitter for the Future Strategic Update

Fitter for the Future Strategic Update 2017-21 Chairman s remarks Global strategic overview Significant market opportunity Basarab Overpass in Bucharest, Romania Naples underground (Toledo Station), Italy

Fitter for the Future Strategic Update 2017-21 Chairman s remarks Global strategic overview Significant market opportunity Basarab Overpass in Bucharest, Romania Naples underground (Toledo Station), Italy

DeA Capital. XXXXXXXXXXX [TITOLO] DeA Capital at a glance. March 2016 Star Conference Milano

![DeA Capital. XXXXXXXXXXX [TITOLO] DeA Capital at a glance. March 2016 Star Conference Milano](/thumbs/91/106044091.jpg "DeA Capital. XXXXXXXXXXX [TITOLO] DeA Capital at a glance. March 2016 Star Conference Milano") DeA Capital XXXXXXXXXXX [TITOLO] DeA Capital at a glance March 2016 Star Conference Milano 1 1 DeA Capital at a glance Alternative Asset Management 9.5 bln AuM RE services Real estate funds Private equity

DeA Capital XXXXXXXXXXX [TITOLO] DeA Capital at a glance March 2016 Star Conference Milano 1 1 DeA Capital at a glance Alternative Asset Management 9.5 bln AuM RE services Real estate funds Private equity

P R E S S R E L E A S E

TXT e-solutions: 2017 Continuing Operations Revenues 35.9 million (+8.4%), EBITDA pre Stock Options 3.5 million ( 3.8 million in 2016), Net Income, including Discontinued Operations 68.6 million Proposed

TXT e-solutions: 2017 Continuing Operations Revenues 35.9 million (+8.4%), EBITDA pre Stock Options 3.5 million ( 3.8 million in 2016), Net Income, including Discontinued Operations 68.6 million Proposed

PRESS RELEASE ISAGRO BOD APPROVES THE RESULTS OF FIRST NINE MONTHS OF 2018

PRESS RELEASE ISAGRO BOD APPROVES THE RESULTS OF FIRST NINE MONTHS OF 2018 Consolidated revenues: 115.2 Euro million (vs. 112.1 million of 9M 2017) Consolidated EBITDA: 12.7 Euro million (vs. 10.5 million

PRESS RELEASE ISAGRO BOD APPROVES THE RESULTS OF FIRST NINE MONTHS OF 2018 Consolidated revenues: 115.2 Euro million (vs. 112.1 million of 9M 2017) Consolidated EBITDA: 12.7 Euro million (vs. 10.5 million

BORSA ITALIANA - STAR segment PRESS RELEASE. INTERIM REPORT AS AT SEPTEMBER 30 th 2018 (in brackets results as at 30/09/2017)

") BORSA ITALIANA - STAR segment PRESS RELEASE INTERIM REPORT AS AT SEPTEMBER 30 th 2018 (in brackets results as at 30/09/2017) THE GROWTH OF THE GROUP CONTINUES ALSO IN THE THIRD QUARTER 2018, DESPITE THE

BORSA ITALIANA - STAR segment PRESS RELEASE INTERIM REPORT AS AT SEPTEMBER 30 th 2018 (in brackets results as at 30/09/2017) THE GROWTH OF THE GROUP CONTINUES ALSO IN THE THIRD QUARTER 2018, DESPITE THE

Sigma Pharmaceuticals Limited

Investor Relations Contact: Gary Woodford Corporate Affairs Manager Gary.Woodford@signet.com.au Phone: 03 9215 9632 Mobile: 0417 399 204 Mark Hooper CEO and Managing Director Gary Woodford Corporate Affairs

Investor Relations Contact: Gary Woodford Corporate Affairs Manager Gary.Woodford@signet.com.au Phone: 03 9215 9632 Mobile: 0417 399 204 Mark Hooper CEO and Managing Director Gary Woodford Corporate Affairs

Press release February 28, FULL-YEAR 2017 RESULTS Recurring Operating Income of 2.0bn Free cash flow (excluding exceptional items) of 950m

of 950m") FULL-YEAR 2017 RESULTS Recurring Operating Income of 2.0bn Free cash flow (excluding exceptional items) of 950m Slowdown in Group like-for-like sales, at +1.6% in 2017 vs. +3.0% in 2016. Recurring Operating

FULL-YEAR 2017 RESULTS Recurring Operating Income of 2.0bn Free cash flow (excluding exceptional items) of 950m Slowdown in Group like-for-like sales, at +1.6% in 2017 vs. +3.0% in 2016. Recurring Operating

Star Conference LONDON. 2015, October 5 th - October 6 th

Star Conference LONDON 2015, October 5 th - October 6 th BOLZONI AT A GLANCE 2 Our market and our customers Dealers of Lift Trucks & Material Handling Lift Truck Manufacturers - OEM Logistics 30% Material

Star Conference LONDON 2015, October 5 th - October 6 th BOLZONI AT A GLANCE 2 Our market and our customers Dealers of Lift Trucks & Material Handling Lift Truck Manufacturers - OEM Logistics 30% Material

Investors: Michael D. Neese VP, Investor Relations (804)

") NEWS RELEASE For Immediate Release August 17, 2016 Investors: Michael D. Neese VP, Investor Relations (804) 287-8126 michael.neese@pfgc.com Media: Joe Vagi Manager, Corporate Communications (804) 484-7737

NEWS RELEASE For Immediate Release August 17, 2016 Investors: Michael D. Neese VP, Investor Relations (804) 287-8126 michael.neese@pfgc.com Media: Joe Vagi Manager, Corporate Communications (804) 484-7737

Results Presentation 1H 2018

Results Presentation 1H 2018 1 2 Highlights of the First Semester Total revenues of 2,011m M&A market entry into new geographies and businesses 8.4% organic growth EBIT 181m Margin improvement in spite

Results Presentation 1H 2018 1 2 Highlights of the First Semester Total revenues of 2,011m M&A market entry into new geographies and businesses 8.4% organic growth EBIT 181m Margin improvement in spite

2015 Full Year Results Presentation. Milan, 22nd March 2016

2015 Full Year Results Presentation Milan, 22nd March 2016 Broadcasting & Advertising ITALY FY 2015 Economic scenario & advertising market HIGHLIGHTS MACRO ECONOMIC KEY INDICATORS ARE SLIGHTLY BUT CONTINUOUSLY

2015 Full Year Results Presentation Milan, 22nd March 2016 Broadcasting & Advertising ITALY FY 2015 Economic scenario & advertising market HIGHLIGHTS MACRO ECONOMIC KEY INDICATORS ARE SLIGHTLY BUT CONTINUOUSLY

PRESENTATION BAADER INVESTMENT CONFERENCE. Munich 18 September 2017

PRESENTATION BAADER INVESTMENT CONFERENCE Munich 18 September 2017 DISCLAIMER AND NOTES To the extent that statements in this presentation do not relate to historical or current facts, they constitute

PRESENTATION BAADER INVESTMENT CONFERENCE Munich 18 September 2017 DISCLAIMER AND NOTES To the extent that statements in this presentation do not relate to historical or current facts, they constitute