Module 4. Analyzing and Interpreting Financial Statements

|

|

|

- Ernest Atkinson

- 5 years ago

- Views:

Transcription

1 Module 4 Analyzing and Interpreting Financial Statements

2 Analysis Structure

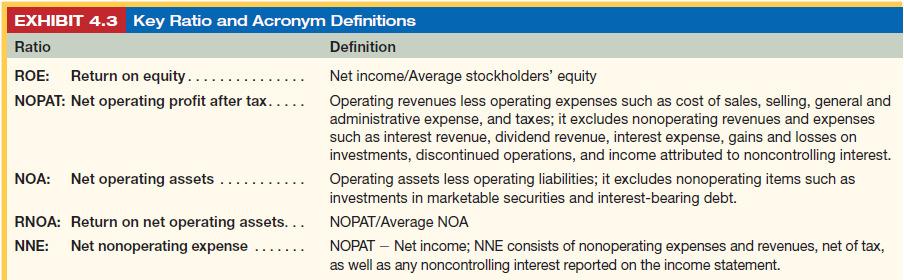

3 Return on Equity Return on equity (ROE) is computed as:

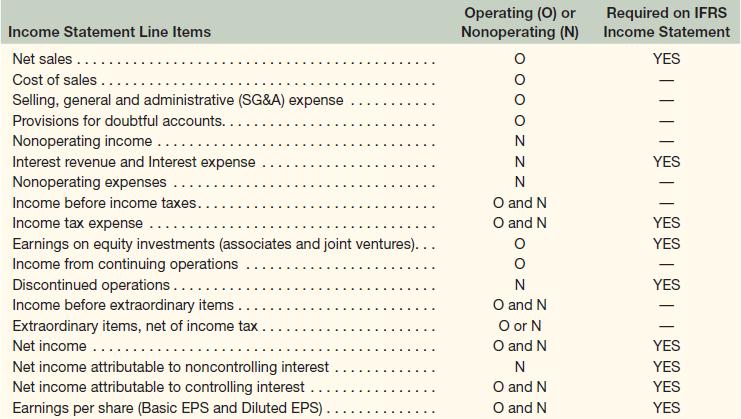

4 Operating Return (RNOA) The income statement reflects operating activities through revenues, costs of goods sold (COGS), and other expenses. Operating assets typically include cash, receivables, inventories, prepaid expenses, property, plant and equipment (PPE), and capitalized lease assets, and exclude short-term and long-term investments in marketable securities.

5 Operating Items in the Income Statement

6 Target s Operating Items

7 Tax on Operating Profit For Target:

8 Treatment of Noncontrolling Interests in Tax Shield Computation Our computation of NOPAT adjusts reported tax expense for the tax shield on net nonoperating expense (NNE). Should noncontrolling interest be included in NNE? While noncontrolling interests are treated as nonoperating, they represent an allocation of net income to the parent company and the noncontrolling shareholders. Noncontrolling interests is not an expense that is deductible for tax purposes. Thus, noncontrolling interest should not be included in the tax shield computation.

9 Net Operating Assets (NOA)

10 For Target

11 Target s NOA

12 Target s RNOA and ROE

13 Key Definitions

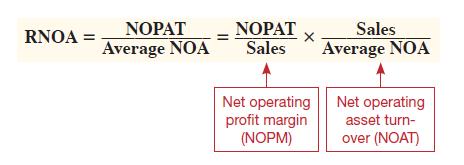

14 Disaggregation of RNOA

15 Net Operating Profit Margin (NOPM) Net operating profit margin (NOPM) reveals how much operating profit the company earns from each sales dollar. NOPM is affected by the level of gross profit the level of operating expenses the level of competition and the company s willingness and ability to control costs.

16 Target s NOPM This result means that for each dollar of sales at Target, the company earns just over 5 profit after all operating expenses and tax. As a reference, the median NOPM for all publicly traded firms is about 6.

17 Net Operating Asset Turnover (NOAT) Net operating asset turnover (NOAT) measures the productivity of the company s net operating assets. This metric reveals the level of sales the company realizes from each dollar invested in net operating assets. All things equal, a higher NOAT is preferable.

18 Target s NOAT This result means that for each dollar of net operating assets, Target realizes $2.27 in sales. As a reference, the median for all publicly traded companies is $1.4.

19 Margin vs. Turnover

20 Nonoperating Return Component of ROE Assume that a company has $1,000 in average assets for the current year in which it earns a 20% RNOA. It finances those assets entirely with equity investment (no debt). Its ROE is computed as follows:

21 Effect of Financial Leverage Next, assume that this company borrows $500 at 7% interest and uses those funds to acquire additional assets yielding the same operating return. Its net operating assets for the year now total $1,500 and its profit is $265.

. The reason for the increased ROE is that the company borrowed $500 at 7% and invested those funds in assets earning 20%.")

22 Effect of Financial Leverage on ROE We see that this company has increased its profit to $265 (up from $200) with the addition of debt, and its ROE is now 26.5% ($265/$1,000). The reason for the increased ROE is that the company borrowed $500 at 7% and invested those funds in assets earning 20%. The difference of 13% accrues to shareholders.

23

24 GAAP Limitations of Ratio analysis 1. Measurability. Financial statements reflect what can be reliably measured. This results in nonrecognition of certain assets, often internally developed assets, the very assets that are most likely to confer a competitive advantage and create value. Examples are brand name, a superior management team, employee skills, and a reliable supply chain. 2. Non-capitalized costs. Related to the concept of measurability is the expensing of costs relating to assets that cannot be identified with enough precision to warrant capitalization. Examples are brand equity costs from advertising and other promotional activities, and research and development costs relating to future products. 3. Historical costs. Assets and liabilities are usually recorded at original acquisition or issuance costs. Subsequent increases in value are not recorded until realized, and declines in value are only recognized if deemed permanent.

25 Global Accounting IFRS companies routinely report financial assets or financial liabilities on the balance sheet. IFRS defines financial assets to include receivables (operating item), loans to affiliates or associates (can be operating or nonoperating depending on the nature of the transactions), securities held as investments (nonoperating), and derivatives (nonoperating). IFRS notes to financial statements usually detail what financial assets and liabilities consist of.

26 Global Accounting

27 Liquidity and Solvency Measures Liquidity refers to cash: how much we have, how much is expected, and how much can be raised on short notice. Solvency refers to the ability to meet obligations; primarily obligations to creditors, including lessors.

28 Current Ratio Current assets are those assets that a company expects to convert into cash within the next operating cycle, which is typically a year. Current liabilities are those liabilities that come due within the next year. An excess of current assets over current liabilities (Current assets Current liabilities), is known as net working capital or simply working capital.

29 Quick Ratio The quick ratio focuses on quick assets. Quick assets include cash, marketable securities, and accounts receivable; they exclude inventories and prepaid assets.

30 Solvency Ratios Solvency refers to a company s ability to meet its debt obligations. Solvency is crucial since an insolvent company is a failed company. Two common solvency ratios:

31 Vertical and Horizontal Analysis

32 Vertical and Horizontal Analysis

33 DuPont Disaggregation Analysis Profit margin is the amount of profit that the company earns from each dollar of sales. Asset turnover is a productivity measure that reflects the volume of sales that a company generates from each dollar invested in assets. Financial leverage measures the degree to which the company finances its assets with debt rather than equity.

34 Return on Assets

35 Return on Assets Adjustment The adjusted numerator better reflects the company s operating profit as it measures return on assets exclusive of financing costs (independent of the capital structure decision).

36 DuPont Disaggregation for Target

Accounting and Ratio Analysis

Accounting and Ratio Analysis Essentials in Management Prof. Sudhakar Balachandran Understanding Financial Performance: Ratio Analysis 1 Objectives: Understanding Financial Performance 1) Introduce the

Accounting and Ratio Analysis Essentials in Management Prof. Sudhakar Balachandran Understanding Financial Performance: Ratio Analysis 1 Objectives: Understanding Financial Performance 1) Introduce the

C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM

1 C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM What have we done in the course? On a chapter by chapter basis, we primarily have examined specific transactions and the effect on financial

1 C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM What have we done in the course? On a chapter by chapter basis, we primarily have examined specific transactions and the effect on financial

WEEK 10 Analysis of Financial Statements

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

FAQ: Financial Ratio Analysis

Question 1: What is horizontal analysis of financial statement data? Answer 1: Horizontal analysis is a method of financial ratio analysis. Horizontal analysis is comparing each item on the financial statements

Question 1: What is horizontal analysis of financial statement data? Answer 1: Horizontal analysis is a method of financial ratio analysis. Horizontal analysis is comparing each item on the financial statements

Financial Analysis. Consolidated financial analysis ( ) Based on IFRS

Based on IFRS") Financial Analysis Consolidated financial analysis (2012-2014) Based on IFRS 2012 2013 2014 Liability to asset ratio (%) 42.58 57.70 56.68 Long-term fund to PP&E ratio (%) 170.33 182.99 199.33 Current

Financial Analysis Consolidated financial analysis (2012-2014) Based on IFRS 2012 2013 2014 Liability to asset ratio (%) 42.58 57.70 56.68 Long-term fund to PP&E ratio (%) 170.33 182.99 199.33 Current

Return on Invested Capital and Profitability Analysis

Return on Invested Capital and Profitability Analysis 8 CHAPTER McGraw-Hill/Irwin 2007, The McGraw-Hill Companies, All Rights Reserved Return on Invested Capital Importance of Joint Analysis Joint analysis

Return on Invested Capital and Profitability Analysis 8 CHAPTER McGraw-Hill/Irwin 2007, The McGraw-Hill Companies, All Rights Reserved Return on Invested Capital Importance of Joint Analysis Joint analysis

Module 3 Transactions, Adjustments, and Financial Statements. Cash Assets 1 Assets 5. Inventory. Inventory (1,200) Accounts receivable

Accounts receivable") 3-36 Module 3 Transactions, Adjustments, and Financial Statements Review 3-2Solution Income Statement Balance Sheet Noncash Cash Assets 1 Assets 5 Liabilities Balance January 1, 2017...............................

3-36 Module 3 Transactions, Adjustments, and Financial Statements Review 3-2Solution Income Statement Balance Sheet Noncash Cash Assets 1 Assets 5 Liabilities Balance January 1, 2017...............................

Lecture 4. Interpreting and using financial statements for valuation II. Financial ratio analysis

Lecture 4 Interpreting and using financial statements for valuation II Financial ratio analysis Agenda Use of financial ratios ROE decomposition Growth, risk, and, cash flow 2 What are financial ratios

Lecture 4 Interpreting and using financial statements for valuation II Financial ratio analysis Agenda Use of financial ratios ROE decomposition Growth, risk, and, cash flow 2 What are financial ratios

Session 2, Sunday, April 2nd (1:30-5:00) v Association for Financial Professionals. All rights reserved. Session 3-1

v Association for Financial Professionals. All rights reserved. Session 3-1") Session 2, Sunday, April 2nd (1:30-5:00) v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter

Session 2, Sunday, April 2nd (1:30-5:00) v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment Profitability Ratios Measure management's ability to control expenses and to earn a return on the resources committed

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment Profitability Ratios Measure management's ability to control expenses and to earn a return on the resources committed

Ratio Analysis. Assets = Liabilities + Shareholder s Equity

Ratio Analysis The purpose of a financial statement is to disclose information about the financial position of an entity to interested parties. By reporting the finances, shareholders are able to make

Ratio Analysis The purpose of a financial statement is to disclose information about the financial position of an entity to interested parties. By reporting the finances, shareholders are able to make

AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00)

") AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00) Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter 7 Ratio Analysis: Part I, Domain

AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00) Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter 7 Ratio Analysis: Part I, Domain

Chapter 5: Using Financial Statement Information

1 Chapter 5: Using Financial Statement Information 2 Control and Prediction Financial accounting numbers are useful in two fundamental ways: They help investors and creditors influence and monitor the

1 Chapter 5: Using Financial Statement Information 2 Control and Prediction Financial accounting numbers are useful in two fundamental ways: They help investors and creditors influence and monitor the

n Financial Statement Analysis n Dollar and Percentage Changes n Common Sized Statements n Ratio Analysis McGraw-Hill /Irwin McGraw-Hill /Irwin

14-1 Today s Agenda Management Accounting Lecture 3 (Chapter 14) Financial Statement Analysis Bangor University Transfer Abroad Programme n Financial Statement Analysis n Dollar and Percentage Changes

14-1 Today s Agenda Management Accounting Lecture 3 (Chapter 14) Financial Statement Analysis Bangor University Transfer Abroad Programme n Financial Statement Analysis n Dollar and Percentage Changes

Index. Business unit, 311, 350 Business-unit level strategies, 309, 311 Business-unit strategies, 311, 350

387 Index A Absenteeism rate, 239 Accounting, 26, 93 Definition, 3 Accounting system, 14 Accrual accounting, 176, 182, 194 Activity-based budgeting, 141 142, 150 Activity-based costing, 67 69, 71, 93,

387 Index A Absenteeism rate, 239 Accounting, 26, 93 Definition, 3 Accounting system, 14 Accrual accounting, 176, 182, 194 Activity-based budgeting, 141 142, 150 Activity-based costing, 67 69, 71, 93,

Working with Financial Statements

Working with Financial Statements Lakehead University September 2005 Overview of the Lecture 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity 3.5 Using Financial Statement Information

Working with Financial Statements Lakehead University September 2005 Overview of the Lecture 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity 3.5 Using Financial Statement Information

Working with Financial Statements

Working with Financial Statements Lakehead University September 2005 Overview of the Lecture 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity 3.5 Using Financial Statement Information

Working with Financial Statements Lakehead University September 2005 Overview of the Lecture 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity 3.5 Using Financial Statement Information

Understanding Financial Statements. Elizabeth Rankin

Understanding Financial Statements Elizabeth Rankin Overview Accounting Concepts Principles Financial Statements Evaluating Performance Horizontal Analysis Vertical Analysis Ratio Analysis Entity Concept

Understanding Financial Statements Elizabeth Rankin Overview Accounting Concepts Principles Financial Statements Evaluating Performance Horizontal Analysis Vertical Analysis Ratio Analysis Entity Concept

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B. Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 5 & 6 FINANCIAL DATA, PERFORMANCE ANALYSIS & MANAGEMENT AND DECISION MAKING June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B. Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 5 & 6 FINANCIAL DATA, PERFORMANCE ANALYSIS & MANAGEMENT AND DECISION MAKING June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B. Com.

ASSIGNMENT MEMORANDUM : FINANCIAL MANAGEMENT 2 (FM202)

") Page 1 of 6 ASSIGNMENT MEMORANDUM SUBJECT : FINANCIAL MANAGEMENT 2 () ASSIGNMENT : 2 nd SEMESTER 2012 QUESTION 1 [25] 1.1. e 1.2. a 1.3. b 1.4. b 1.5. a 1.6. b 1.7. d 1.8. a 1.9. a 1.10. b 1.11. c 1.12.

Page 1 of 6 ASSIGNMENT MEMORANDUM SUBJECT : FINANCIAL MANAGEMENT 2 () ASSIGNMENT : 2 nd SEMESTER 2012 QUESTION 1 [25] 1.1. e 1.2. a 1.3. b 1.4. b 1.5. a 1.6. b 1.7. d 1.8. a 1.9. a 1.10. b 1.11. c 1.12.

Excellence in. Management

Excellence in Financial Management Course 1: Evaluating Financial Performance Prepared by: Matt H. Evans, CPA, CMA, CFM Chapter 1: Return on Equity Why use ratios? It has been said that you must measure

Excellence in Financial Management Course 1: Evaluating Financial Performance Prepared by: Matt H. Evans, CPA, CMA, CFM Chapter 1: Return on Equity Why use ratios? It has been said that you must measure

FINANCIAL ANALYSIS TOOLS: DESCRIPTION CHAPTER 7 FINANCIAL ANALYSIS TECHNIQUES GRAPHICS: EXAMPLE GRAPHICS: EXAMPLE

Presenter s name Presenter s title dd Month yyyy CHAPTER 7 FINANCIAL ANALYSIS TECHNIQUES FINANCIAL ANALYSIS TOOLS: DESCRIPTION Graphics Regression Common-Size Analysis Financial Ratio Analysis Copyright

Presenter s name Presenter s title dd Month yyyy CHAPTER 7 FINANCIAL ANALYSIS TECHNIQUES FINANCIAL ANALYSIS TOOLS: DESCRIPTION Graphics Regression Common-Size Analysis Financial Ratio Analysis Copyright

Financial Statements Analysis

Financial Statements Analysis Agenda I. The Importance of Financial Statements Analysis II. Overview of the 3 Statements a) Income Statement b) Cash Flow Statement c) Balance Sheet III. How Statements

Financial Statements Analysis Agenda I. The Importance of Financial Statements Analysis II. Overview of the 3 Statements a) Income Statement b) Cash Flow Statement c) Balance Sheet III. How Statements

ANSWER SHEET EXAMINATION #2

ANSWER SHEET EXAMINATION #2 1) D 2) B 26) D 3) C 27) B 4) A 28) B 5) D 29) C 6) D 30) A 7) D 31) B 8) C 32) D 9) D 33) D 10) B 34) D 11) A 12) A 13) D 14) C 15) A 16) C 17) B 18) B 19) C 20) B 21) B 22)

ANSWER SHEET EXAMINATION #2 1) D 2) B 26) D 3) C 27) B 4) A 28) B 5) D 29) C 6) D 30) A 7) D 31) B 8) C 32) D 9) D 33) D 10) B 34) D 11) A 12) A 13) D 14) C 15) A 16) C 17) B 18) B 19) C 20) B 21) B 22)

Performance Indicators for 6 years

Performance Indicators for 6 years FINANCIAL POSITION Balance sheet (Rupees in Thousand) Other noncurrent assets Total assets 2,084,856 6,544 2,436,65 2,040,33 11,386 2,257,568 4,417,23 1,803,2 101,268

Performance Indicators for 6 years FINANCIAL POSITION Balance sheet (Rupees in Thousand) Other noncurrent assets Total assets 2,084,856 6,544 2,436,65 2,040,33 11,386 2,257,568 4,417,23 1,803,2 101,268

Company Information. December 27 December 28 December Company Name. Panera Bread Company. Fiscal Year End Dates

Company Information Company Name Fiscal Year End Dates Balance Sheet Units (i.e. 000's) Income Statement Units (i.e. 000's) Most Recent Year for Data Date of Analysis 2011 Calendar Year Industry Comparisons

Company Information Company Name Fiscal Year End Dates Balance Sheet Units (i.e. 000's) Income Statement Units (i.e. 000's) Most Recent Year for Data Date of Analysis 2011 Calendar Year Industry Comparisons

Taxes. Financial Statements: Things to Keep in Mind. Cash Flow and Taxes. BUSI 7110/7116 Yost

Cash Flow and Taxes Financial Statements: Things to Keep in Mind Backward vs. Forward Looking Book Values vs. Market Values Accounting Numbers vs. Cash Flows Tax Deductible vs. Taxable Notes to Financial

Cash Flow and Taxes Financial Statements: Things to Keep in Mind Backward vs. Forward Looking Book Values vs. Market Values Accounting Numbers vs. Cash Flows Tax Deductible vs. Taxable Notes to Financial

CFA-Level-I. Financial. Chartered Financial Analyst Level I (CFA Level I)

") Financial CFA-Level-I Chartered Financial Analyst Level I (CFA Level I) Download Full Version : http://killexams.com/pass4sure/exam-detail/cfa-level-i QUESTION: 566 For which of the following ways of manipulating

Financial CFA-Level-I Chartered Financial Analyst Level I (CFA Level I) Download Full Version : http://killexams.com/pass4sure/exam-detail/cfa-level-i QUESTION: 566 For which of the following ways of manipulating

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS. Note on Financial Statements and Financial Ratios

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Financial Statements and Financial Ratios I. Review of Financial Statements The Balance Sheet Financial

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Financial Statements and Financial Ratios I. Review of Financial Statements The Balance Sheet Financial

Understanding The Cash Flow Statement

Financial Reporting & Analysis Understanding The Cash Flow Statement Reading - 27 www.proschoolonline.com/ 1 Components and Format of Cash Flow Statement Apple Inc. - Cash Flow Statement Year ended 26

Financial Reporting & Analysis Understanding The Cash Flow Statement Reading - 27 www.proschoolonline.com/ 1 Components and Format of Cash Flow Statement Apple Inc. - Cash Flow Statement Year ended 26

CHAPTER 20. Analysis and interpretation of financial statements CONTENTS

CHAPTER 20 Analysis and interpretation of financial statements CONTENTS 20.1 Horizontal and vertical analysis 20.2 Trend analysis 20.3 Effect of transactions on ratios 20.4 Ratio analysis 20.5 Ratio analysis

CHAPTER 20 Analysis and interpretation of financial statements CONTENTS 20.1 Horizontal and vertical analysis 20.2 Trend analysis 20.3 Effect of transactions on ratios 20.4 Ratio analysis 20.5 Ratio analysis

2/2/2009. Financial statement EARNING POWER AND IRREGULAR ITEMS. EARNING POWER AND IRREGULAR ITEMS continued. Chapter 14

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Walter T. Harrison Jr. Baylor University. Charles T. Horngren Stanford University. C. William (Bill) Thomas Baylor University

Thomas Baylor University") G O Ninth Edition Walter T. Harrison Jr. Baylor University Charles T. Horngren Stanford University C. William (Bill) Thomas Baylor University PEARSON Boston Columbus Indianapolis New York San Francisco

G O Ninth Edition Walter T. Harrison Jr. Baylor University Charles T. Horngren Stanford University C. William (Bill) Thomas Baylor University PEARSON Boston Columbus Indianapolis New York San Francisco

Learning Objective. LO1 Analyze an income statement using vertical analysis Cengage Learning. All Rights Reserved.

Learning Objective LO1 Analyze an income statement using vertical analysis. Lesson 17-1 Vertical Analysis Ratios LO1 Vertical analysis ratios measure the relationship between one financial statement item

Learning Objective LO1 Analyze an income statement using vertical analysis. Lesson 17-1 Vertical Analysis Ratios LO1 Vertical analysis ratios measure the relationship between one financial statement item

Analysis of County Business-Type Funds

Analysis of County Business-Type Funds Roderick B. Posey University of Southern Mississippi 118 College Drive #5178 Hattiesburg, MS 39406-0001 601-266-4641 roderick.posey@usm.edu ABSTRACT Occasionally,

Analysis of County Business-Type Funds Roderick B. Posey University of Southern Mississippi 118 College Drive #5178 Hattiesburg, MS 39406-0001 601-266-4641 roderick.posey@usm.edu ABSTRACT Occasionally,

Chapter 3 Working with Financial Statements

Chapter 3 Working with Financial Statements This chapter is a continuation of Chapter 2. We use accounting numbers because of the unavailability of market numbers. We prefer to use market numbers. Common-Size

Chapter 3 Working with Financial Statements This chapter is a continuation of Chapter 2. We use accounting numbers because of the unavailability of market numbers. We prefer to use market numbers. Common-Size

Financial Statements, Forecasts, and Planning Chapter 6

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

Role of Financial Manager. Assessing Financial Performance. Analysis of Financial Statements. To create value, the financial manager should:

Role of Financial Manager To create value, the financial manager should: 1. Make sound investment decisions. 2. Make sound financing decisions. Importance of Assessing Financial Performance Assessing Financial

Role of Financial Manager To create value, the financial manager should: 1. Make sound investment decisions. 2. Make sound financing decisions. Importance of Assessing Financial Performance Assessing Financial

Fin-621 Final term Solved Papers by Fahad Yusha Cell: and

FINALTERM EXAMINATION Spring 2010 FIN621- Financial Statement Analysis (Session - 1) : 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Which one of the following is NOT a type of adjusting

FINALTERM EXAMINATION Spring 2010 FIN621- Financial Statement Analysis (Session - 1) : 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Which one of the following is NOT a type of adjusting

Brandon's Auto Supply Company

Balance Sheet at June 30, 20XX Brandon's Auto Supply Company Vertical Analysis 20X9 % 20X8 % 20X7 % Current Assets Cash $ 88,531 7.5% $ 104,287 9.5% $ 117,910 11.7% Accounts receivable $ 117,793 10.0%

Balance Sheet at June 30, 20XX Brandon's Auto Supply Company Vertical Analysis 20X9 % 20X8 % 20X7 % Current Assets Cash $ 88,531 7.5% $ 104,287 9.5% $ 117,910 11.7% Accounts receivable $ 117,793 10.0%

ACCTG 101 Cramming Sesh

ACCTG 101 Cramming Sesh MODULES 1, 3, 6, 7, 8 & 9 MODULES COVERED 1 Introduction 3 Business Plan: Budgeting 6 Accounting System & Balance Sheet & 7 Accounting System & Income Statement 8 Cash Flow Statement

ACCTG 101 Cramming Sesh MODULES 1, 3, 6, 7, 8 & 9 MODULES COVERED 1 Introduction 3 Business Plan: Budgeting 6 Accounting System & Balance Sheet & 7 Accounting System & Income Statement 8 Cash Flow Statement

FEAR out. Taking the FEAR of Financial Statement Analysis. Toni Drake, CCE TRM Financial Services, Inc.

FEAR out Taking the FEAR of Financial Statement Analysis Toni Drake, CCE TRM Financial Services, Inc. FINANCIAL STATEMENTS Components of a Financial Statement Balance Sheet Income Statement Statement of

FEAR out Taking the FEAR of Financial Statement Analysis Toni Drake, CCE TRM Financial Services, Inc. FINANCIAL STATEMENTS Components of a Financial Statement Balance Sheet Income Statement Statement of

Working with Financial Statements

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Financial Statement Analysis. Cash Flow Statement

Financial Statement Analysis Cash Flow Statement 1 The Articulation of the Financial Statements Beginning stocks Flows Ending stocks Cash Flow Statement Beginning Balance Sheet Cash Cash from operations

Financial Statement Analysis Cash Flow Statement 1 The Articulation of the Financial Statements Beginning stocks Flows Ending stocks Cash Flow Statement Beginning Balance Sheet Cash Cash from operations

Financial Statement Analysis

Financial Statement Analysis Lakehead University September 2003 Overview of the Lecture 2.1 Financial Statements 2.2 Ratio Analysis 2.4 Common-Size Analysis 2.3 Changing Prices 2.5 International Considerations

Financial Statement Analysis Lakehead University September 2003 Overview of the Lecture 2.1 Financial Statements 2.2 Ratio Analysis 2.4 Common-Size Analysis 2.3 Changing Prices 2.5 International Considerations

CMA 2010 Support Package

CMA 2010 Support Package Ratio Definitions CMA EXAM RATIO DEFINITIONS Abbreviations EBIT = Earnings before interest and taxes EBITDA = Earnings before interest, taxes, depreciation and amortization EBT

CMA 2010 Support Package Ratio Definitions CMA EXAM RATIO DEFINITIONS Abbreviations EBIT = Earnings before interest and taxes EBITDA = Earnings before interest, taxes, depreciation and amortization EBT

Analysis and Interpretation of Financial Statements

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Financial Analysis. 2 nd Edition. Steven M. Bragg

Financial Analysis 2 nd Edition Steven M. Bragg Chapter 1 Overview of Financial Analysis... 1 Learning Objectives... 1 Introduction... 1 The Purpose of Financial Analysis... 1 Key Financial Analysis Concepts...

Financial Analysis 2 nd Edition Steven M. Bragg Chapter 1 Overview of Financial Analysis... 1 Learning Objectives... 1 Introduction... 1 The Purpose of Financial Analysis... 1 Key Financial Analysis Concepts...

Financial Statement Analysis for the Boardroom. An Attorney s Guide September 13, 2017

Financial Statement Analysis for the Boardroom An Attorney s Guide September 13, 2017 Contact information For more information, please contact one of the following members of the engagement team: Marc

Financial Statement Analysis for the Boardroom An Attorney s Guide September 13, 2017 Contact information For more information, please contact one of the following members of the engagement team: Marc

Accounting For Managers

Accounting For Managers Professor ZHOU Ning SCHOOL OF ECONOMICS AND MANAGEMENT BEIHANG UNIVERSITY zning80@buaa.edu.cn Chapter 13 Financial Statement Analysis The objectives of Chapter 13 Business objectives

Accounting For Managers Professor ZHOU Ning SCHOOL OF ECONOMICS AND MANAGEMENT BEIHANG UNIVERSITY zning80@buaa.edu.cn Chapter 13 Financial Statement Analysis The objectives of Chapter 13 Business objectives

Chapter 6: Statement of Cash Flows

Chapter 6: Statement of Cash Flows Outline: Why a cash flow statement? Classifications of cash flows Preparation of cash flow statements Determining the change in cash Determining net cash from operating

Chapter 6: Statement of Cash Flows Outline: Why a cash flow statement? Classifications of cash flows Preparation of cash flow statements Determining the change in cash Determining net cash from operating

Accounting & Understanding Financial Statements Disadvantaged Business Enterprise (DBE) Supportive Services Program

Supportive Services Program") Accounting & Understanding Financial Statements Disadvantaged Business Enterprise (DBE) Supportive Services Program The contents of this training course reflect the views of the author who is responsible

Accounting & Understanding Financial Statements Disadvantaged Business Enterprise (DBE) Supportive Services Program The contents of this training course reflect the views of the author who is responsible

Exam 1 Sample Questions FINAN303 Principles of Finance McBrayer Spring 2018

Sample Multiple Choice Questions 1. The effect of a stock dividend (i.e., stock split) is that it a. Reduces owner s equity. b. Increases retained earnings. c. Reduces the liabilities of the firm. d. Increases

Sample Multiple Choice Questions 1. The effect of a stock dividend (i.e., stock split) is that it a. Reduces owner s equity. b. Increases retained earnings. c. Reduces the liabilities of the firm. d. Increases

Nike, Inc. Financial Statement Analysis CHAPTER 17

CHAPTER 17 AP Photo/Matt York Financial Statement Analysis Nike, Inc. J ust do it. These three words identify one of the most recognizable brands in the world, Nike. While this phrase inspires athletes

CHAPTER 17 AP Photo/Matt York Financial Statement Analysis Nike, Inc. J ust do it. These three words identify one of the most recognizable brands in the world, Nike. While this phrase inspires athletes

Financial Statement & Security Analysis Case Study. Bilgin Demir. Master of Science Financial Engineering. Stevens Institute of Technology

Financial Statement & Security Analysis Case Study Bilgin Demir Master of Science Financial Engineering Stevens Institute of Technology School of Systems and Enterprises Hoboken, New Jersey blgndemir@gmail.com

Financial Statement & Security Analysis Case Study Bilgin Demir Master of Science Financial Engineering Stevens Institute of Technology School of Systems and Enterprises Hoboken, New Jersey blgndemir@gmail.com

Course # Analysis of the Corporate Annual Report

Course # 171021 Analysis of the Corporate Annual Report based on the electronic.pdf file(s): Analysis of the Corporate Annual Report by: Dr. Jae K. Shim, Ph.D., 2014, 56 pages 5 CPE Credit Hours Accounting

Course # 171021 Analysis of the Corporate Annual Report based on the electronic.pdf file(s): Analysis of the Corporate Annual Report by: Dr. Jae K. Shim, Ph.D., 2014, 56 pages 5 CPE Credit Hours Accounting

Financial Analysis. 3 rd Edition. Steven M. Bragg

Financial Analysis 3 rd Edition Steven M. Bragg Chapter 1 Overview of Financial Analysis... 1 Learning Objectives... 1 Introduction... 1 The Purpose of Financial Analysis... 1 Key Financial Analysis Concepts...

Financial Analysis 3 rd Edition Steven M. Bragg Chapter 1 Overview of Financial Analysis... 1 Learning Objectives... 1 Introduction... 1 The Purpose of Financial Analysis... 1 Key Financial Analysis Concepts...

Contents. Preface... xiii. CHAPTER 1 Introduction to Management Accounting and Control CHAPTER 2 Management Reporting... 29

v Preface... xiii CHAPTER 1 Introduction to Management Accounting and Control... 1 The Concepts of Management, Accounting, and Control... 2 A Definition of Management... 2 A Definition of Accounting...

v Preface... xiii CHAPTER 1 Introduction to Management Accounting and Control... 1 The Concepts of Management, Accounting, and Control... 2 A Definition of Management... 2 A Definition of Accounting...

ANALYSIS OF FINANCIAL ACCOUNTING METHODOLOGIES AND APPLICATIONS. By: Kate Culbertson. Oxford May 2017

ANALYSIS OF FINANCIAL ACCOUNTING METHODOLOGIES AND APPLICATIONS By: Kate Culbertson A thesis submitted to the faculty of The University of Mississippi in partial fulfillment of the requirements of the

ANALYSIS OF FINANCIAL ACCOUNTING METHODOLOGIES AND APPLICATIONS By: Kate Culbertson A thesis submitted to the faculty of The University of Mississippi in partial fulfillment of the requirements of the

Writing a Financial Report: Some Guidelines

Writing a Financial Report: Some Guidelines Table of contents 1. A guiding principle... 2 2. An example of analysis grid... 3 3. Financial ratios: the toolkit of the financial analyst... 4 3.1. Growth

Writing a Financial Report: Some Guidelines Table of contents 1. A guiding principle... 2 2. An example of analysis grid... 3 3. Financial ratios: the toolkit of the financial analyst... 4 3.1. Growth

FI3300: CORPORATE FINANCE. Problem Set 1 Chapters 1-5

FI3300: CORPORATE FINANCE Problem Set 1 Chapters 1-5 1. The goal of the firm is to. a. maximize profit b. minimize risk c. promote social good d. maximize shareholder wealth 2. Which of the following would

FI3300: CORPORATE FINANCE Problem Set 1 Chapters 1-5 1. The goal of the firm is to. a. maximize profit b. minimize risk c. promote social good d. maximize shareholder wealth 2. Which of the following would

UNISYS CORPORATION CONSOLIDATED STATEMENTS OF INCOME (Unaudited) (Millions, except per share data)

(Millions, except per share data)") CONSOLIDATED STATEMENTS OF INCOME (Millions, except per share data) Three Months Nine Months Ended September 30 Ended September 30 2012 2011 2012 2011 Revenue Services $748.0 $876.3 $2,386.7 $2,519.3 Technology

CONSOLIDATED STATEMENTS OF INCOME (Millions, except per share data) Three Months Nine Months Ended September 30 Ended September 30 2012 2011 2012 2011 Revenue Services $748.0 $876.3 $2,386.7 $2,519.3 Technology

Appendix: Financial Definitions. Basic Accounting Reports

Appendix: Financial Definitions Several standardized methods have been created to analyze business financial data. These numbers are easily computed from the standard reported accounting data. The various

Appendix: Financial Definitions Several standardized methods have been created to analyze business financial data. These numbers are easily computed from the standard reported accounting data. The various

Finance and Accounting for Interviews

This document was developed and written by Ian Lee. All information is meant for public use and purposed for the free transfer of knowledge to interested parties. Send questions and comments to ianlee@uclalumni.net

This document was developed and written by Ian Lee. All information is meant for public use and purposed for the free transfer of knowledge to interested parties. Send questions and comments to ianlee@uclalumni.net

Accounting Building Business Skills. Learning Objectives: Learning Objectives: Paul D. Kimmel. Chapter Eleven: Financial Statement Analysis

Accounting Building Business Skills Paul D. Kimmel Chapter Eleven: Financial Statement Analysis PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia,

Accounting Building Business Skills Paul D. Kimmel Chapter Eleven: Financial Statement Analysis PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia,

FINANCIAL RATIOS 2 Page 1 of 5. The following is information concerning ABC Company and XYZ Company.

FINANCIAL RATIOS 2 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 22,600 42,800 Accounts and Notes Receivable 92,500 101,100

FINANCIAL RATIOS 2 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 22,600 42,800 Accounts and Notes Receivable 92,500 101,100

FINANCIAL RATIOS 3 Page 1 of 5. The following is information concerning ABC Company and XYZ Company.

FINANCIAL RATIOS 3 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 18,700 33,000 Accounts and Notes Receivable 43,000 59,800

FINANCIAL RATIOS 3 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 18,700 33,000 Accounts and Notes Receivable 43,000 59,800

Working with Financial Statements, Part II

Working with Financial Statements, Part II Faculty of Business Administration Lakehead University Spring 2003 May 7, 2003 Outline of Chapter 3, Part II 3.3 Ratio Analysis 3.4 The DuPont Identity 3.5 Using

Working with Financial Statements, Part II Faculty of Business Administration Lakehead University Spring 2003 May 7, 2003 Outline of Chapter 3, Part II 3.3 Ratio Analysis 3.4 The DuPont Identity 3.5 Using

How Well Am I Doing? Financial Statement Analysis

How Well Am I Doing? Financial Statement Analysis Chapter 16 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Limitations of Financial Statement Analysis Differences

How Well Am I Doing? Financial Statement Analysis Chapter 16 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Limitations of Financial Statement Analysis Differences

Social Reality Reports 1,014% Year-Over-Year Revenue Growth for Q3 2015

marketwired.com http://www.marketwired.com/press-release/social-reality-reports-1014-year-over-year-revenue-growth-for-q3-2015-otcqb-scri- 2074098.htm Social Reality Reports 1,014% Year-Over-Year Revenue

marketwired.com http://www.marketwired.com/press-release/social-reality-reports-1014-year-over-year-revenue-growth-for-q3-2015-otcqb-scri- 2074098.htm Social Reality Reports 1,014% Year-Over-Year Revenue

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis Answers to End of Chapter Questions 2-1. Financial statement analysis provides information about the company s financial health, and its

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis Answers to End of Chapter Questions 2-1. Financial statement analysis provides information about the company s financial health, and its

Gleim CMA Review Updates to Part Edition, 1st Printing March 2015

Page 1 of 5 Gleim CMA Review Updates to Part 2 2015 Edition, 1st Printing March 2015 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. Study

Page 1 of 5 Gleim CMA Review Updates to Part 2 2015 Edition, 1st Printing March 2015 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. Study

Ratio Analysis. CA Past Years Exam Question

Ratio Analysis CA Past Years Exam Question Question : 1 Nov, 2009 From the Following Information, Calculate the Amount of Fixed Assets & Proprietors Funds. 1. Ratio of Fixed Assets to Proprietors Funds

Ratio Analysis CA Past Years Exam Question Question : 1 Nov, 2009 From the Following Information, Calculate the Amount of Fixed Assets & Proprietors Funds. 1. Ratio of Fixed Assets to Proprietors Funds

Presented by SCOTT TRANSUE

Presented by SCOTT TRANSUE Cash vs. accrual Key definitions Balance sheets Income statements Cash flow statements Break-even analysis Today s Agenda Ratios Recognizes transactions when they occur Recognizes

Presented by SCOTT TRANSUE Cash vs. accrual Key definitions Balance sheets Income statements Cash flow statements Break-even analysis Today s Agenda Ratios Recognizes transactions when they occur Recognizes

1 2. Financial ratios

1 2. Financial ratios Warning 2 Remember that accounting statements are based on book values. We would prefer to make decisions based on market values, but such information may not be easy to obtain, and

1 2. Financial ratios Warning 2 Remember that accounting statements are based on book values. We would prefer to make decisions based on market values, but such information may not be easy to obtain, and

Novelis Inc. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (unaudited) (in millions)

(in millions)") Novelis Inc. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (unaudited) (in millions) Three Months Ended March 31, Net sales $ 2,621 $ 2,402 $ 9,591 $ 9,872 Cost of goods sold (exclusive of depreciation

Novelis Inc. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (unaudited) (in millions) Three Months Ended March 31, Net sales $ 2,621 $ 2,402 $ 9,591 $ 9,872 Cost of goods sold (exclusive of depreciation

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows QUESTIONS FOR REVIEW OF KEY TOPICS Question 4 1 The income statement is a change statement that reports transactions

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows QUESTIONS FOR REVIEW OF KEY TOPICS Question 4 1 The income statement is a change statement that reports transactions

SRAX Reports Third Quarter 2017 Financial Results

SRAX Reports Third Quarter 2017 Financial Results - Increases Gross Profit Margin to 56% for Q3 2017, Up from 27% in Q3 2016 - - Improves Q3 2017 Operating Loss and Adjusted EBITDA Loss Compared to Q3

SRAX Reports Third Quarter 2017 Financial Results - Increases Gross Profit Margin to 56% for Q3 2017, Up from 27% in Q3 2016 - - Improves Q3 2017 Operating Loss and Adjusted EBITDA Loss Compared to Q3

John A. Jaeger, CCE, MBA

John A. Jaeger, CCE, MBA Session Outline General Info Review Company Introduction & Industry Review Company Financials Ratio Analysis Discussion Strengths & Weaknesses Decision Extend Credit Management

John A. Jaeger, CCE, MBA Session Outline General Info Review Company Introduction & Industry Review Company Financials Ratio Analysis Discussion Strengths & Weaknesses Decision Extend Credit Management

Key Operational and Financial Data

Key Operational and Financial Data Operations Summary Tons Production 217,370 209,524 195,906 134,272 127,384 70,916 Sales 217,043 214,316 181,259 138,923 126,129 64,912 Summary of Statement of Profit

Key Operational and Financial Data Operations Summary Tons Production 217,370 209,524 195,906 134,272 127,384 70,916 Sales 217,043 214,316 181,259 138,923 126,129 64,912 Summary of Statement of Profit

accounts receivable: dollar amount due from customers from sales made on open account.

GLOSSARY 1 above-the-line: income items related to core operations. Typically assumed to have high predictive power for future earnings. accrual accounting: system of accounting that purports to measure

GLOSSARY 1 above-the-line: income items related to core operations. Typically assumed to have high predictive power for future earnings. accrual accounting: system of accounting that purports to measure

COPYRIGHTED MATERIAL. Index

Index Accelerated depreciation, 34 38 asset acquisition and, 76 77 declining balance method, 34, 35 Modified Accelerated Cost Recovery System (MACRS) method, 35 38 sum of the year s digits method, 34 35

Index Accelerated depreciation, 34 38 asset acquisition and, 76 77 declining balance method, 34, 35 Modified Accelerated Cost Recovery System (MACRS) method, 35 38 sum of the year s digits method, 34 35

General Education Competencies Satisfied:

Course Name: Principles of Financial Accounting Course Number: ACC* 113 Credits: 3 Catalog description: A study of the basic principles and procedures of the accounting process as they relate to the recording,

Course Name: Principles of Financial Accounting Course Number: ACC* 113 Credits: 3 Catalog description: A study of the basic principles and procedures of the accounting process as they relate to the recording,

A Manager's Guide to Financial Analysis

A Manager's Guide to Financial Analysis A Manager's Guide to Financial Analysis Fifth Edition Steven D. Grossman Contents About This Course How to Take This Course Introduction ix xi xiii 1 Financial

A Manager's Guide to Financial Analysis A Manager's Guide to Financial Analysis Fifth Edition Steven D. Grossman Contents About This Course How to Take This Course Introduction ix xi xiii 1 Financial

Consolidated Balance Sheets

page 77 Consolidated Balance Sheets Toyota Motor Corporation March 31, 2011 and 2012 ASSETS 2011 2012 2012 Current assets Cash and cash equivalents 2,080,709 1,679,200 $ 20,431 Time deposits 203,874 80,301

page 77 Consolidated Balance Sheets Toyota Motor Corporation March 31, 2011 and 2012 ASSETS 2011 2012 2012 Current assets Cash and cash equivalents 2,080,709 1,679,200 $ 20,431 Time deposits 203,874 80,301

JABIL CIRCUIT, INC. AND SUBSIDIARIES CONDENSED CONSOLIDATED BALANCE SHEETS

CONDENSED CONSOLIDATED BALANCE SHEETS (In thousands) 2011 2010 ASSETS Current assets: Cash and cash equivalents $ 888,611 $ 744,329 Trade accounts receivable, net 1,100,926 1,408,319 Inventories 2,227,339

CONDENSED CONSOLIDATED BALANCE SHEETS (In thousands) 2011 2010 ASSETS Current assets: Cash and cash equivalents $ 888,611 $ 744,329 Trade accounts receivable, net 1,100,926 1,408,319 Inventories 2,227,339

Using Financial Statements in the Credit Review Process. Wendi Rosenblatt, Hearst Television

Using Financial Statements in the Credit Review Process Wendi Rosenblatt, Hearst Television Agenda What is Available Financial Statement Overview DineEquity, Inc. Annual Report/Form 10K Review Availability

Using Financial Statements in the Credit Review Process Wendi Rosenblatt, Hearst Television Agenda What is Available Financial Statement Overview DineEquity, Inc. Annual Report/Form 10K Review Availability

Using Data Analytics to Detect Fraud

Using Data Analytics to Detect Fraud Data Analysis Tests for Detecting Financial Statement Fraud 2018 Association of Certified Fraud Examiners, Inc. Financial Statement Fraud Schemes The fraudster intentionally

Using Data Analytics to Detect Fraud Data Analysis Tests for Detecting Financial Statement Fraud 2018 Association of Certified Fraud Examiners, Inc. Financial Statement Fraud Schemes The fraudster intentionally

NESHAMINY SCHOOL DISTRICT LANGHORNE, PENNSYLVANIA. Course Title ACCOUNTING III

NESHAMINY SCHOOL DISTRICT LANGHORNE, PENNSYLVANIA Course Title ACCOUNTING III Month: September ESSENTIAL QUESTIONS THAT THE COURSE CONTENT ANSWERS: Why is it essential for accountants to analyze and evaluate

NESHAMINY SCHOOL DISTRICT LANGHORNE, PENNSYLVANIA Course Title ACCOUNTING III Month: September ESSENTIAL QUESTIONS THAT THE COURSE CONTENT ANSWERS: Why is it essential for accountants to analyze and evaluate

Chapter 02 Evaluating Financial Performance

Chapter 02 Evaluating Financial Performance Multiple Choice Questions 1. The most popular yardstick of financial performance among investors and senior managers is the: A. profit margin. B. return on equity.

Chapter 02 Evaluating Financial Performance Multiple Choice Questions 1. The most popular yardstick of financial performance among investors and senior managers is the: A. profit margin. B. return on equity.

Chapter 02 Analysis of Financial Statements

Chapter 02 Analysis of Financial Statements TRUEFALSE 1. The information contained in the annual report is used by investors to form expectations about future earnings and dividends. 2. Noncash assets

Chapter 02 Analysis of Financial Statements TRUEFALSE 1. The information contained in the annual report is used by investors to form expectations about future earnings and dividends. 2. Noncash assets

Corporate Finance. Week 3 Financial Statement Analysis II

Corporate Finance 1-1 Week 3 Financial Statement Analysis II 1-1 Asset Efficiency or Turnover Measures 1-2 A first broad measure of efficiency is asset turnover: Sales Asset Turnover = Total Assets Fixed

Corporate Finance 1-1 Week 3 Financial Statement Analysis II 1-1 Asset Efficiency or Turnover Measures 1-2 A first broad measure of efficiency is asset turnover: Sales Asset Turnover = Total Assets Fixed

Financials. Lecture 7

Financials Lecture 7 1 Financial statements Income statement (P/L) Balance sheet Beginning Cash Flow statement Balance sheet Ending Changes in Shareholder Equities 2 Business Financial Flow Collection

Financials Lecture 7 1 Financial statements Income statement (P/L) Balance sheet Beginning Cash Flow statement Balance sheet Ending Changes in Shareholder Equities 2 Business Financial Flow Collection

CBF Exam Review. Income Statement. Disclosure of Items. Financial Statements Part 2. Tom Shimko, CCE

CBF Exam Review Financial Statements Part 2 Tom Shimko, CCE 1 Income Statement Represents estimates for revenues and costs using accrual accounting. Accrual and cash accounting differ Net income not equal

CBF Exam Review Financial Statements Part 2 Tom Shimko, CCE 1 Income Statement Represents estimates for revenues and costs using accrual accounting. Accrual and cash accounting differ Net income not equal

Overview of Financial Reporting, Financial Statement Analysis, and Valuation 1

CONTENTS Preface About the Authors iv xvii Chapter 1 Overview of Financial Reporting, Financial Statement Analysis, and Valuation 1 Overview of Financial Statement Analysis 2 Step 1: Identify the Industry

CONTENTS Preface About the Authors iv xvii Chapter 1 Overview of Financial Reporting, Financial Statement Analysis, and Valuation 1 Overview of Financial Statement Analysis 2 Step 1: Identify the Industry

a $33.17 $33.33 $33.50 $28.57

What is the book value per share for a company that has total stockholders' equity of $10,000,000, preferred stock of $50,000, and 300,000 common shares outstanding? a $33.17 $33.33 $33.50 $28.57 "'Your

What is the book value per share for a company that has total stockholders' equity of $10,000,000, preferred stock of $50,000, and 300,000 common shares outstanding? a $33.17 $33.33 $33.50 $28.57 "'Your

> > > > > > > > Chapter 16. Understanding Accounting and Financial Statements

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

Lecture 2. Financial Statements, Cash Flows, and Taxes and Analysis of Financial Statements (Ch 2, Ch3)

") Lecture 2. Financial Statements, Cash Flows, and Taxes and Analysis of Financial Statements (Ch 2, Ch3) Basic concepts of Financial Statements (FSs) Why the company needs to construct FSs? To provide information

Lecture 2. Financial Statements, Cash Flows, and Taxes and Analysis of Financial Statements (Ch 2, Ch3) Basic concepts of Financial Statements (FSs) Why the company needs to construct FSs? To provide information

Colt Defense LLC. Section 1: Colt Defense LLC's Peer Ratio Analysis. Financial health declining, overall position now very weak FHR: 21

Colt Defense LLC Financial health declining, overall position now very weak FHR: 21 Risk Level: High Risk Default Characteristics Indicator: --- Annual Delta: -3 rating points Ticker: 533839Z Table 1:

Colt Defense LLC Financial health declining, overall position now very weak FHR: 21 Risk Level: High Risk Default Characteristics Indicator: --- Annual Delta: -3 rating points Ticker: 533839Z Table 1: