1 2. Financial ratios

|

|

|

- Miles Matthews

- 5 years ago

- Views:

Transcription

1 1 2. Financial ratios

2 Warning 2 Remember that accounting statements are based on book values. We would prefer to make decisions based on market values, but such information may not be easy to obtain, and is subject to dispute.

3 Standardized statements 3 When comparing financial statements for different companies (or the same company for different years) it is often more convenient to standardize them in some way. One way to do so is common-size statements. To construct a common-size balance sheet, express each item as a percentage of total assets. To construct a common-size income statement, express each item as a percentage of total sales.

4 4

5 5

6 Ratio analysis 6 Financial ratios provide a convenient way of summarizing information Useful for comparisons across companies or time. There are many ratios that one might be interested in. We look at a few...

7 Liquidity measures 7 Current ratio = current assets current liabilities Liquidity is a measure of short-term solvency (ability to meet short-term obligations). A high current ratio indicates liquidity, but may also imply an inefficient use of cash and other short-term resources. Current ratio should normally be greater than 1. Note similarity to NWC. Quick ratio = Also known as acid-test ratio. Inventory is less liquid than other current assets. current assets inventory current liabilities Large inventory may also be a sign of trouble (some may turn out to be damaged, obsolete, or lost). Some companies may try to keep unsaleable merchandise on the books to inflate their current ratio. Cash ratio = cash current liabilities Cash ratio might be of interest for a very short term creditor.

8 Ethics: Stuffing the channel 8 One way to reduce inventory on the books and increase accounts receivable is known as channel stuffing. Example Bristol-Myers On August 4, 2004, the Commission (SEC) filed a civil action against Bristol-Myers alleging channel stuffing. The Commission s Complaint alleged that, from the first quarter of 2000 through the fourth quarter of 2001, Bristol-Myers engaged in a fraudulent scheme to overstate its sales and earnings in order to create the false appearance that the Company had met or exceeded financial projections set by the Company s officers ( targets ) and earnings estimates established by Wall Street securities analysts. Bristol-Myers inflated its results primarily by: stuffing its distribution channels with excess inventory near the end of every quarter in amounts sufficient to meet sales and earnings targets set by officers ( channel-stuffing ); and improperly recognizing about $1.5 billion in revenue from sales associated with the channelstuffing in violation of generally accepted accounting principles. When Bristol-Myers results fell short of the Wall Street analysts earnings estimates, the Company used improper accounting, including cookie jar reserves, to further inflate its earnings. In March 2003, Bristol-Myers restated its prior financial statements and disclosed its channelstuffing activities and improper accounting. Reference:

9 Figure Bristol-Myers 9

10 Market measures of equity and capitalization 10 Market capitalization = market value of equity = shares outstanding x price per share Total capitalization = market value of equity + LTD Enterprise value = market cap + net debt Notes: Debt = LTD + notes payable + current maturities of LTD Net debt = Debt - cash and cash equivalents Book suggests using book value of debt even though these are market measures (book and market values of debt generally are close).

11 Leverage ratios 11 Debt-equity ratio = debt / equity Debt-to-capital ratio = debt / (debt + equity) Debt-to-enterprise value (market) = net debt / enterprise value Equity multiplier (book) = total assets / book value of equity Equity multiplier (market) = enterprise value / market value of equity Notes: These leverage ratios are generally considered to be book measures unless otherwise specified.

12 Measures of income 12 Gross profit = Sales - COGS Operating profit = Operating income = Sales - COGS - period costs Net profit = Net income EBIT = Net income + Interest + Tax EBITDA = Net income + Interest + Tax + Depreciation & amortization Notes: Period costs include general and administrative expenses, R&D, etc. EBITDA includes other income whereas operating income does not.

13 Profitability measures 13 Gross margin = Gross profit / sales Operating margin = operating income / sales Net profit margin = Profit margin = Return on sales = Net income / sales EBIT margin = EBIT / sales

14 Asset management measures 14 AKA turnover ratios... Total asset turnover = sales total assets Capital intensity = total assets sales Fixed asset turnover is a measure of the firm s capital intensity. Reducing asset needs while maintaining net income increases ROA.

15 Working capital measures (SKIP) 15 Accounts receivable days = accounts receivable / average daily sales Accounts payable days = accounts payable / average daily COGS Inventory days = inventory / average daily COGS Accounts receivable turnover = sales / accounts receivable Accounts payable turnover = COGS / accounts payable Inventory turnover = COGS / inventory

16 Interest coverage ratios 16 EBIT/interest coverage = EBIT / interest EBITDA/interest coverage = EBITDA / interest

17 Operating returns 17 ROE = return on equity = net income / book value of equity ROA = return on assets = net income / book value of assets ROS = return on sales = net profit margin = net income / sales ROIC = return on invested capital = EBIT x (1 - tax rate) / (book value of equity + net debt) Notes: Denominator of ROIC is book analog of enterprise value. Book defines ROA differently. We will use the standard definition. EBIT (1-T) is sometimes known as unlevered net income or NOPAT (net operating profit after taxes). Use the firm s average tax rate. ROIC is generally the most useful of these. But note that the tax deduction due to interest payments is ignored. (It might make more sense to use NI + Interest in the numerator, like the book s definition of ROA.)

18 Valuation ratios 18 EPS = net income / shares outstanding P/E ratio = share price / EPS = market cap / net income Enterprise value ratios = enterprise value / (EBIT or EBITDA or Sales) Market-to-book = market value of equity / book value of equity

19 Historical PE ratios, S&P Note the spikes around 2001 and What is going on there? Does the increase in PE ratios recently mean that shares are over-valued, or has there been some underlying changes that provide a rational basis for these valuations?

20 Du Pont identity 20 ROE = = = net income total equity net income assets net income sales assets total equity sales assets assets total equity The DuPont identity shows that ROE is determined by three factors: operating efficiency (profit margin) asset use efficiency (asset turnover) financial leverage (equity multiplier)

21 Du Pont identity continued 21 What we learn from the Du Pont identity is that if the firm is looking to increase ROE, there are three areas to look: increase the profit margin (raise prices or reduce costs) utilize assets more efficiently (NWC and/or fixed assets) increase leverage

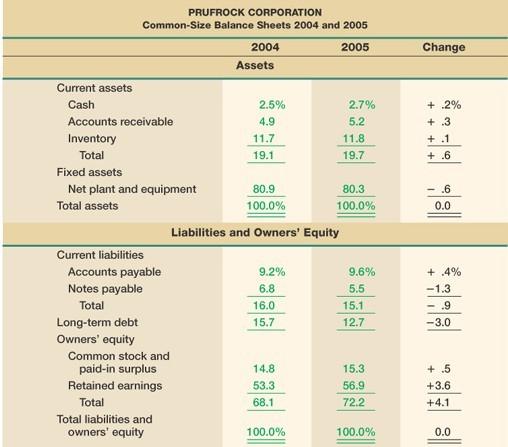

22 Example 22 Rocky Flats Mineral Water (RFMW)* Balance sheet (millions of $) Assets Current assets: Cash Accounts receivable Inventory Total Fixed assets Total assets Liabilities and Owners Equity Current liabilities: Accounts payable Notes payable Total Long-term debt Owners equity Retained earnings Total liabilities and owners equity

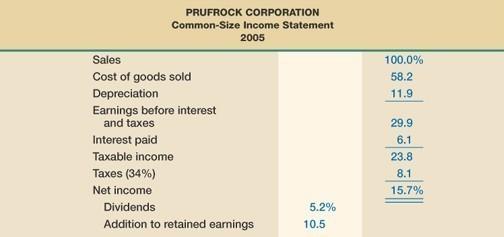

23 Example continued 23 Income statement (2005) (millions of $) Net sales 2000 Cost of goods sold 1800 Depreciation 150 EBIT 50 Interest paid 20 Taxable income 30 Taxes 9 Net income 21 Dividends 6 Addition to retained earnings 15

24 Example continued 24 Current ratio Quick ratio Cash ratio Debt-equity ratio Debt-to-capital ratio Equity multiplier Total asset turnover Capital intensity Profit margin ROIC ROA ROE

25 Example continued 25 Suppose RFMW has 13 million shares of common stock outstanding. Shares are currently trading at $12. What is RFMW s EPS? What is RFMW s PE ratio? What is RFMW s market/book ratio? Is RFMW a value or growth stock?

26 Example continued 26 RFMW also has 325,000 bonds outstanding. The bonds have a face value of $1000 and are currently trading for $925. What are the book and market values of RFMW s long-term debt? Why might RFMW s bonds be trading at a discount? What is RFMW s market capitalization? Total capitalization? Enterprise value?

27 (Brief) ratio analysis 27

Wikipedia: "Financial Ratio" Contents. Sources of Data for Financial Ratios. Purpose and Types of Ratios

Wikipedia: "Financial Ratio" A financial ratio or accounting ratio is a relative magnitude of two selected numerical values taken from an enterprise's financial statements. Often used in accounting, there

Wikipedia: "Financial Ratio" A financial ratio or accounting ratio is a relative magnitude of two selected numerical values taken from an enterprise's financial statements. Often used in accounting, there

Chapter 3 Analysis of Financial Statements. Ratio Analysis Please refer to the attached financial statements, and industry average ratios

Chapter 3 Analysis of Financial Statements Ratio Analysis Please refer to the attached financial statements, and industry average ratios In this chapter, we will cover Liquidity ratios Asset management

Chapter 3 Analysis of Financial Statements Ratio Analysis Please refer to the attached financial statements, and industry average ratios In this chapter, we will cover Liquidity ratios Asset management

CMA 2010 Support Package

CMA 2010 Support Package Ratio Definitions CMA EXAM RATIO DEFINITIONS Abbreviations EBIT = Earnings before interest and taxes EBITDA = Earnings before interest, taxes, depreciation and amortization EBT

CMA 2010 Support Package Ratio Definitions CMA EXAM RATIO DEFINITIONS Abbreviations EBIT = Earnings before interest and taxes EBITDA = Earnings before interest, taxes, depreciation and amortization EBT

Week-2 FINC Analysis of Financial Statements. Balance Sheets

Dr. Ahmed FINC 5000 Week-2 Name Analysis of Financial Statements Balance Sheets Assets 2003 2004 2005e Cash $ 9,000 $ 7,282 $ 14,000 Short-Term Investments. 48,600 20,000 71,632 Accounts Receivable 351,200

Dr. Ahmed FINC 5000 Week-2 Name Analysis of Financial Statements Balance Sheets Assets 2003 2004 2005e Cash $ 9,000 $ 7,282 $ 14,000 Short-Term Investments. 48,600 20,000 71,632 Accounts Receivable 351,200

Working with Financial Statements, Part II

Working with Financial Statements, Part II Faculty of Business Administration Lakehead University Spring 2003 May 7, 2003 Outline of Chapter 3, Part II 3.3 Ratio Analysis 3.4 The DuPont Identity 3.5 Using

Working with Financial Statements, Part II Faculty of Business Administration Lakehead University Spring 2003 May 7, 2003 Outline of Chapter 3, Part II 3.3 Ratio Analysis 3.4 The DuPont Identity 3.5 Using

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS. Note on Financial Statements and Financial Ratios

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Financial Statements and Financial Ratios I. Review of Financial Statements The Balance Sheet Financial

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Financial Statements and Financial Ratios I. Review of Financial Statements The Balance Sheet Financial

Appendix: Financial Definitions. Basic Accounting Reports

Appendix: Financial Definitions Several standardized methods have been created to analyze business financial data. These numbers are easily computed from the standard reported accounting data. The various

Appendix: Financial Definitions Several standardized methods have been created to analyze business financial data. These numbers are easily computed from the standard reported accounting data. The various

Working with Financial Statements

Working with Financial Statements Lakehead University September 2005 Overview of the Lecture 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity 3.5 Using Financial Statement Information

Working with Financial Statements Lakehead University September 2005 Overview of the Lecture 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity 3.5 Using Financial Statement Information

Working with Financial Statements

Working with Financial Statements Lakehead University September 2005 Overview of the Lecture 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity 3.5 Using Financial Statement Information

Working with Financial Statements Lakehead University September 2005 Overview of the Lecture 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity 3.5 Using Financial Statement Information

ANALYSIS OF FINANCIAL STATEMENTS

ANALYSIS OF FINANCIAL STATEMENTS 1. Basic concept of financial statement analysis 2. Liquidity ratios 3. Asset management ratios 4. Debt management ratios 5. Profitability ratios 6. Market value ratios

ANALYSIS OF FINANCIAL STATEMENTS 1. Basic concept of financial statement analysis 2. Liquidity ratios 3. Asset management ratios 4. Debt management ratios 5. Profitability ratios 6. Market value ratios

Role of Financial Manager. Assessing Financial Performance. Analysis of Financial Statements. To create value, the financial manager should:

Role of Financial Manager To create value, the financial manager should: 1. Make sound investment decisions. 2. Make sound financing decisions. Importance of Assessing Financial Performance Assessing Financial

Role of Financial Manager To create value, the financial manager should: 1. Make sound investment decisions. 2. Make sound financing decisions. Importance of Assessing Financial Performance Assessing Financial

Chapter 3 Financial Statements Analysis

Chapter 3 Financial Statements Analysis 1 Acknowledgement This work is reproduced, based on the book [Ross, Westerfield, Jaffe and Jordan Core Principles and Applications of Corporate Finance ]. This work

Chapter 3 Financial Statements Analysis 1 Acknowledgement This work is reproduced, based on the book [Ross, Westerfield, Jaffe and Jordan Core Principles and Applications of Corporate Finance ]. This work

Financial Statement Analysis

Financial Statement Analysis Lakehead University September 2003 Overview of the Lecture 2.1 Financial Statements 2.2 Ratio Analysis 2.4 Common-Size Analysis 2.3 Changing Prices 2.5 International Considerations

Financial Statement Analysis Lakehead University September 2003 Overview of the Lecture 2.1 Financial Statements 2.2 Ratio Analysis 2.4 Common-Size Analysis 2.3 Changing Prices 2.5 International Considerations

MBF1223 Financial Management. Lecture 8: Financial Ratios and Firm Performance

MBF1223 Financial Management Lecture 8: Financial Ratios and Firm Performance Learning Objectives 1. Create, understand, and interpret common-size financial statements. 2. Calculate and interpret financial

MBF1223 Financial Management Lecture 8: Financial Ratios and Firm Performance Learning Objectives 1. Create, understand, and interpret common-size financial statements. 2. Calculate and interpret financial

Working with Financial Statements

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

The Du Pont System of the Analysis of Return Ratios Applied to Sears, Roebuck & Co.

The Du Pont System of the Analysis of Return Ratios Applied to Sears, Roebuck & Co. Return on Assets (ROA) 1 Return on Equity (ROE) 2 Calculation for fiscal year 2003 Calculation for fiscal year 2003 (

The Du Pont System of the Analysis of Return Ratios Applied to Sears, Roebuck & Co. Return on Assets (ROA) 1 Return on Equity (ROE) 2 Calculation for fiscal year 2003 Calculation for fiscal year 2003 (

Corporate Finance, 3e (Berk/DeMarzo) Chapter 2 Introduction to Financial Statement Analysis. 2.1 Firms' Disclosure of Financial Information

Chapter 2 Introduction to Financial Statement Analysis. 2.1 Firms' Disclosure of Financial Information") Corporate Finance, 3e (Berk/DeMarzo) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) U.S. public companies are required to file their annual financial

Corporate Finance, 3e (Berk/DeMarzo) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) U.S. public companies are required to file their annual financial

0. Introduction. What is finance? What are the two main branches of finance? What are the three main aspects of corporate finance?

1 0. Introduction What is finance? What are the two main branches of finance? What are the three main aspects of corporate finance? 2 1. Financial statements and cash flow A quick review of balance sheet

1 0. Introduction What is finance? What are the two main branches of finance? What are the three main aspects of corporate finance? 2 1. Financial statements and cash flow A quick review of balance sheet

Problem Set One. Name

MK602 Problem Set One Name The first part of the case, presented in Chapter 3 (pages 123-125), discussed the situation that Computron Industries was in after an expansion program. Thus far, sales have

MK602 Problem Set One Name The first part of the case, presented in Chapter 3 (pages 123-125), discussed the situation that Computron Industries was in after an expansion program. Thus far, sales have

Curriculum designed for use with the Iowa Electronic Markets Cynthia J. Brown Marilyn M. Dutton Thomas A. Rietz

Financial Statement Analysis Curriculum designed for use with the Iowa Electronic Markets by Cynthia J. Brown Marilyn M. Dutton Thomas A. Rietz ١ Financial Statement Analysis: Lecture Outline Review of

Financial Statement Analysis Curriculum designed for use with the Iowa Electronic Markets by Cynthia J. Brown Marilyn M. Dutton Thomas A. Rietz ١ Financial Statement Analysis: Lecture Outline Review of

chapter4 To guide or not to guide, that is the Analysis of Financial Statements

chapter4 Analysis of Financial Statements To guide or not to guide, that is the question. Or at least it s the question many companies are wrestling with regarding earnings forecasts. Should a company

chapter4 Analysis of Financial Statements To guide or not to guide, that is the question. Or at least it s the question many companies are wrestling with regarding earnings forecasts. Should a company

FINANCIAL ANALYSIS TOOLS: DESCRIPTION CHAPTER 7 FINANCIAL ANALYSIS TECHNIQUES GRAPHICS: EXAMPLE GRAPHICS: EXAMPLE

Presenter s name Presenter s title dd Month yyyy CHAPTER 7 FINANCIAL ANALYSIS TECHNIQUES FINANCIAL ANALYSIS TOOLS: DESCRIPTION Graphics Regression Common-Size Analysis Financial Ratio Analysis Copyright

Presenter s name Presenter s title dd Month yyyy CHAPTER 7 FINANCIAL ANALYSIS TECHNIQUES FINANCIAL ANALYSIS TOOLS: DESCRIPTION Graphics Regression Common-Size Analysis Financial Ratio Analysis Copyright

FINANCIAL ANALYSIS TYPES OF FINANCIAL STATEMENTS FINANCIAL RATIOS BASIC SOURCES AND USES OF FUNDS TOPIC PREVIEW LEARNING OBJECTIVE

FINANCIAL ANALYSIS TOPIC PREVIEW TYPES OF FINANCIAL STATEMENTS FINANCIAL RATIOS BASIC SOURCES AND USES OF FUNDS LEARNING OBJECTIVE Students be able to: Distinguish the different types of financial statements

FINANCIAL ANALYSIS TOPIC PREVIEW TYPES OF FINANCIAL STATEMENTS FINANCIAL RATIOS BASIC SOURCES AND USES OF FUNDS LEARNING OBJECTIVE Students be able to: Distinguish the different types of financial statements

Corporate Finance, 3Ce (Berk, DeMarzo, Strangeland) Chapter 2 Introduction to Financial Statement Analysis

Chapter 2 Introduction to Financial Statement Analysis") Corporate Finance, 3Ce (Berk, DeMarzo, Strangeland) Chapter 2 Introduction to Financial Statement Analysis 2.1 The Disclosure of Financial Information 1) Canadian public companies are required to file

Corporate Finance, 3Ce (Berk, DeMarzo, Strangeland) Chapter 2 Introduction to Financial Statement Analysis 2.1 The Disclosure of Financial Information 1) Canadian public companies are required to file

WEEK 10 Analysis of Financial Statements

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

Lecture 4. Interpreting and using financial statements for valuation II. Financial ratio analysis

Lecture 4 Interpreting and using financial statements for valuation II Financial ratio analysis Agenda Use of financial ratios ROE decomposition Growth, risk, and, cash flow 2 What are financial ratios

Lecture 4 Interpreting and using financial statements for valuation II Financial ratio analysis Agenda Use of financial ratios ROE decomposition Growth, risk, and, cash flow 2 What are financial ratios

Business Assignment 2 Solutions. 1. Consider the balance sheets and income statements for Sunrise, Inc. depicted in Table 1 and Table 2.

Business 2019 Assignment 2 Solutions 1. Consider the balance sheets and income statements for Sunrise, Inc. depicted in Table 1 and Table 2. (a) For year 2000, calculate Sunrise s cash flow from assets,

Business 2019 Assignment 2 Solutions 1. Consider the balance sheets and income statements for Sunrise, Inc. depicted in Table 1 and Table 2. (a) For year 2000, calculate Sunrise s cash flow from assets,

CHAPTER 19: FINANCIAL STATEMENT ANALYSIS

CHAPTER 19: FINANCIAL STATEMENT ANALYSIS 1. ROE Net profits/equity Net profits/sales Sales/Assets Assets/Equity Net profit margin Asset turnover Leverage ratio 5.5% 2.0 2.2 24.2% 2. ROA ROS ATO The only

CHAPTER 19: FINANCIAL STATEMENT ANALYSIS 1. ROE Net profits/equity Net profits/sales Sales/Assets Assets/Equity Net profit margin Asset turnover Leverage ratio 5.5% 2.0 2.2 24.2% 2. ROA ROS ATO The only

CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS

CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS 1 Learning Outcomes LO.1 Describe the basic financial information that is produced by corporations and explain how the firm s stakeholders use such information.

CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS 1 Learning Outcomes LO.1 Describe the basic financial information that is produced by corporations and explain how the firm s stakeholders use such information.

CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS

TRUE/FALSE CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS 1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always

TRUE/FALSE CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS 1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always

To guide or not to guide, that is the question. Or at least it s the question

CHAPTER3 Analysis of Financial Statements To guide or not to guide, that is the question. Or at least it s the question many companies are wrestling with regarding earnings forecasts. Should a company

CHAPTER3 Analysis of Financial Statements To guide or not to guide, that is the question. Or at least it s the question many companies are wrestling with regarding earnings forecasts. Should a company

Session 2, Sunday, April 2nd (1:30-5:00) v Association for Financial Professionals. All rights reserved. Session 3-1

v Association for Financial Professionals. All rights reserved. Session 3-1") Session 2, Sunday, April 2nd (1:30-5:00) v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter

Session 2, Sunday, April 2nd (1:30-5:00) v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter

Chapter 3 Working with Financial Statements

Chapter 3 Working with Financial Statements This chapter is a continuation of Chapter 2. We use accounting numbers because of the unavailability of market numbers. We prefer to use market numbers. Common-Size

Chapter 3 Working with Financial Statements This chapter is a continuation of Chapter 2. We use accounting numbers because of the unavailability of market numbers. We prefer to use market numbers. Common-Size

Chapter 2 Financial Statement and Cash Flow Analysis

Chapter 2 Financial Statement and Cash Flow Analysis MULTIPLE CHOICE 1. Which of the following items can be found on an income statement? a. Accounts receivable b. Long-term debt c. Sales d. Inventory

Chapter 2 Financial Statement and Cash Flow Analysis MULTIPLE CHOICE 1. Which of the following items can be found on an income statement? a. Accounts receivable b. Long-term debt c. Sales d. Inventory

Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous

Ratio Analysis Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous Ratio Analysis compares significant numbers from your financial statements. Rather than focusing on specific

Ratio Analysis Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous Ratio Analysis compares significant numbers from your financial statements. Rather than focusing on specific

FAQ: Financial Ratio Analysis

Question 1: What is horizontal analysis of financial statement data? Answer 1: Horizontal analysis is a method of financial ratio analysis. Horizontal analysis is comparing each item on the financial statements

Question 1: What is horizontal analysis of financial statement data? Answer 1: Horizontal analysis is a method of financial ratio analysis. Horizontal analysis is comparing each item on the financial statements

CFIN4 Chapter 2 Analysis of Financial Statements

1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always based on accounting data. Income statement 2. The balance

1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always based on accounting data. Income statement 2. The balance

FUNDAMENTALS OF HEALTHCARE FINANCE. Online Appendix B. Financial Analysis Ratios

FUNDAMENTALS OF HEALTHCARE FINANCE Online Appendix B Financial Analysis Ratios INTRODUCTION In Chapter 13, we indicated that financial ratio analysis is a technique commonly used to help assess a business

FUNDAMENTALS OF HEALTHCARE FINANCE Online Appendix B Financial Analysis Ratios INTRODUCTION In Chapter 13, we indicated that financial ratio analysis is a technique commonly used to help assess a business

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis Answers to End of Chapter Questions 2-1. Financial statement analysis provides information about the company s financial health, and its

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis Answers to End of Chapter Questions 2-1. Financial statement analysis provides information about the company s financial health, and its

COPYRIGHTED MATERIAL. Chapter 1 Comparable Companies Analysis. Chapter 1 Comparable Companies Analysis 1.

Chapter 1 Comparable Companies Analysis Chapter 1 Comparable Companies Analysis 1 COPYRIGHTED MATERIAL Comparable Companies Analysis Steps Step I. Select the Universe of Comparable Companies Step II. Locate

Chapter 1 Comparable Companies Analysis Chapter 1 Comparable Companies Analysis 1 COPYRIGHTED MATERIAL Comparable Companies Analysis Steps Step I. Select the Universe of Comparable Companies Step II. Locate

Chapter 7. Analyzing Common Stocks. Security Analysis. Top-Down Approach Kaplan Financial

Chapter 7 Analyzing Common Stocks Security Analysis Process of gathering, organizing, and using information to determine the intrinsic value of a common stock. Intrinsic value is the underlying or inherent

Chapter 7 Analyzing Common Stocks Security Analysis Process of gathering, organizing, and using information to determine the intrinsic value of a common stock. Intrinsic value is the underlying or inherent

Simple Financial Measures

Handout for Business 189 undergraduate course in Strategic Management Simple Financial Measures Simon Rodan Department of Management Lucas College of Business San José State University One Washington Square

Handout for Business 189 undergraduate course in Strategic Management Simple Financial Measures Simon Rodan Department of Management Lucas College of Business San José State University One Washington Square

How Well Am I Doing? Financial Statement Analysis

How Well Am I Doing? Financial Statement Analysis Chapter 16 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Limitations of Financial Statement Analysis Differences

How Well Am I Doing? Financial Statement Analysis Chapter 16 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Limitations of Financial Statement Analysis Differences

AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00)

") AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00) Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter 7 Ratio Analysis: Part I, Domain

AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00) Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter 7 Ratio Analysis: Part I, Domain

Business Ratios. Current Ratio

Current Ratio Business Ratios Measures whether or not the firm has enough resources to pay its debt over the next 12 months formula: Current Ratio = Current Assets Current Liabilities Acceptable ratios

Current Ratio Business Ratios Measures whether or not the firm has enough resources to pay its debt over the next 12 months formula: Current Ratio = Current Assets Current Liabilities Acceptable ratios

Ratio Analysis. Assets = Liabilities + Shareholder s Equity

Ratio Analysis The purpose of a financial statement is to disclose information about the financial position of an entity to interested parties. By reporting the finances, shareholders are able to make

Ratio Analysis The purpose of a financial statement is to disclose information about the financial position of an entity to interested parties. By reporting the finances, shareholders are able to make

n Financial Statement Analysis n Dollar and Percentage Changes n Common Sized Statements n Ratio Analysis McGraw-Hill /Irwin McGraw-Hill /Irwin

14-1 Today s Agenda Management Accounting Lecture 3 (Chapter 14) Financial Statement Analysis Bangor University Transfer Abroad Programme n Financial Statement Analysis n Dollar and Percentage Changes

14-1 Today s Agenda Management Accounting Lecture 3 (Chapter 14) Financial Statement Analysis Bangor University Transfer Abroad Programme n Financial Statement Analysis n Dollar and Percentage Changes

Fin-621 Final term Solved Papers by Fahad Yusha Cell: and

FINALTERM EXAMINATION Spring 2010 FIN621 - Financial Statement Analysis Student Info StudentID: Time: 90 min Marks: 69 Center: ExamDate: Tue, Aug 10, 2010 Question No: 1 After recording the transactions

FINALTERM EXAMINATION Spring 2010 FIN621 - Financial Statement Analysis Student Info StudentID: Time: 90 min Marks: 69 Center: ExamDate: Tue, Aug 10, 2010 Question No: 1 After recording the transactions

Fundamentals of Corporate Finance, 2e (Berk) Chapter 2 Introduction to Financial Statement Analysis. 2.1 Firms' Disclosure of Financial Information

Chapter 2 Introduction to Financial Statement Analysis. 2.1 Firms' Disclosure of Financial Information") Fundamentals of Corporate Finance, 2e (Berk) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) In the United States, publicly traded companies can

Fundamentals of Corporate Finance, 2e (Berk) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) In the United States, publicly traded companies can

Who of the following make a broader use of accounting information?

Who of the following make a broader use of accounting information? Accountants Financial Analysts Auditors Marketers Which of the following is NOT an internal use of financial statements information? Planning

Who of the following make a broader use of accounting information? Accountants Financial Analysts Auditors Marketers Which of the following is NOT an internal use of financial statements information? Planning

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

ASSIGNMENT MEMORANDUM : FINANCIAL MANAGEMENT 2 (FM202)

") Page 1 of 6 ASSIGNMENT MEMORANDUM SUBJECT : FINANCIAL MANAGEMENT 2 () ASSIGNMENT : 2 nd SEMESTER 2012 QUESTION 1 [25] 1.1. e 1.2. a 1.3. b 1.4. b 1.5. a 1.6. b 1.7. d 1.8. a 1.9. a 1.10. b 1.11. c 1.12.

Page 1 of 6 ASSIGNMENT MEMORANDUM SUBJECT : FINANCIAL MANAGEMENT 2 () ASSIGNMENT : 2 nd SEMESTER 2012 QUESTION 1 [25] 1.1. e 1.2. a 1.3. b 1.4. b 1.5. a 1.6. b 1.7. d 1.8. a 1.9. a 1.10. b 1.11. c 1.12.

FINANCIAL RATIOS. LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS

You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS") FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

Net income Net Sales. or in other words Return on equity = Return on sales x Asset turnover x Asset-to-equity ratio

1. Which of the following statements is CORRECT? A. High current and quick ratios always indicate that a firm is managing its liquidity position well. B. A decline in a firm's inventory turnover ratio

1. Which of the following statements is CORRECT? A. High current and quick ratios always indicate that a firm is managing its liquidity position well. B. A decline in a firm's inventory turnover ratio

Kavous Ardalan. Marist College, New York, USA

Journal of Modern Accounting and Auditing, July 2017, Vol. 13, No. 7, 294-298 doi: 10.17265/1548-6583/2017.07.002 D DAVID PUBLISHING Advancing the Interpretation of the Du Pont Equation Kavous Ardalan

Journal of Modern Accounting and Auditing, July 2017, Vol. 13, No. 7, 294-298 doi: 10.17265/1548-6583/2017.07.002 D DAVID PUBLISHING Advancing the Interpretation of the Du Pont Equation Kavous Ardalan

Fundamentals of Finance and Accounting for Nonfinancial Managers Lesson Worksheets

Fundamentals of Finance and Accounting for Nonfinancial Managers Lesson Worksheets 2218V Updated 01/2016 Fundamentals of Finance and Accounting for Nonfinancial Managers i Table of Contents Lesson One

Fundamentals of Finance and Accounting for Nonfinancial Managers Lesson Worksheets 2218V Updated 01/2016 Fundamentals of Finance and Accounting for Nonfinancial Managers i Table of Contents Lesson One

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay. Lecture - 14 Ratio Analysis

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 14 Ratio Analysis Dear students, in our last session we are started the

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 14 Ratio Analysis Dear students, in our last session we are started the

Chapter 2. Learning Objectives. Topics Covered. Cash Flow and Financial Statement Analysis

Chapter 2 Cash Flow and Financial Statement Analysis Learning Objectives Interpret information contained in the balance sheet, income statement, and statement of cash flows. Explain why income differs

Chapter 2 Cash Flow and Financial Statement Analysis Learning Objectives Interpret information contained in the balance sheet, income statement, and statement of cash flows. Explain why income differs

CSCA Reading List. Copyright 2017 Institute of Certified Management Accountants 1. Updated 8/25/17

CSCA Reading List 1 CSCA Reading List Certified in Strategy and Competitive Analysis Strategy Textbooks referenced in the Resource Guide (listed in alphabetical order): Note: Any ONE of these strategic

CSCA Reading List 1 CSCA Reading List Certified in Strategy and Competitive Analysis Strategy Textbooks referenced in the Resource Guide (listed in alphabetical order): Note: Any ONE of these strategic

Finance and Accounting for Interviews

This document was developed and written by Ian Lee. All information is meant for public use and purposed for the free transfer of knowledge to interested parties. Send questions and comments to ianlee@uclalumni.net

This document was developed and written by Ian Lee. All information is meant for public use and purposed for the free transfer of knowledge to interested parties. Send questions and comments to ianlee@uclalumni.net

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment Profitability Ratios Measure management's ability to control expenses and to earn a return on the resources committed

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment Profitability Ratios Measure management's ability to control expenses and to earn a return on the resources committed

Chapter 2. Introduction to Financial Statement Analysis

Chapter 2 Introduction to Financial Statement Analysis 2-1. In a firm s annual report, five financial statements can be found: the balance sheet, the income statement, the statement of cash flows, the

Chapter 2 Introduction to Financial Statement Analysis 2-1. In a firm s annual report, five financial statements can be found: the balance sheet, the income statement, the statement of cash flows, the

CHAPTER 3. Analysis of Financial Statements

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis Du Pont system Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis Du Pont system Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

19/08/2014. Chapter Outline. Chapter 2. Learning Objectives. Learning Objectives. Firms Disclosure of Financial Information (cont'd)

") Chapter 2 Introduction to Financial Statement Analysis - Too much info for our limited time, so focus on my lecture Chapter Outline 2.1 Firms Disclosure of Financial Information 2.2 The Balance Sheet or

Chapter 2 Introduction to Financial Statement Analysis - Too much info for our limited time, so focus on my lecture Chapter Outline 2.1 Firms Disclosure of Financial Information 2.2 The Balance Sheet or

Study Guide. Corporate Finance. A. J. Cataldo II, Ph.D., CPA, CMA

Study Guide Corporate Finance By A. J. Cataldo II, Ph.D., CPA, CMA About the Author A. J. Cataldo is currently a professor of accounting at West Chester University, in West Chester, Pennsylvania. He holds

Study Guide Corporate Finance By A. J. Cataldo II, Ph.D., CPA, CMA About the Author A. J. Cataldo is currently a professor of accounting at West Chester University, in West Chester, Pennsylvania. He holds

Week 14, Chap14 Accounting 1A, Financial Accounting

Week 14, Chap14 Accounting 1A, Financial Accounting Analyzing Financial Statements Instructor: Michael Booth Understanding The Business Return on an equity security investment Dividends Increase in share

Week 14, Chap14 Accounting 1A, Financial Accounting Analyzing Financial Statements Instructor: Michael Booth Understanding The Business Return on an equity security investment Dividends Increase in share

Chapter 2. Data for Financial Decision Making

Chapter 2 Data for Financial Decision Making Data for Financial Decision Making Introductory concepts the need for good data Financial accounting data Financial ratios Managerial accounting data Other

Chapter 2 Data for Financial Decision Making Data for Financial Decision Making Introductory concepts the need for good data Financial accounting data Financial ratios Managerial accounting data Other

Lesson 5 Ratios, at first glance

Advanced Accounting AY 2017/2018 Lesson 5 Ratios, at first glance Università degli Studi di Trieste D.E.A.M.S. Paolo Altin 160 Financial ratios Provide a quick and (relatively) simple means of evaluating

Advanced Accounting AY 2017/2018 Lesson 5 Ratios, at first glance Università degli Studi di Trieste D.E.A.M.S. Paolo Altin 160 Financial ratios Provide a quick and (relatively) simple means of evaluating

CHAPTER 3. Topics in Chapter. Analysis of Financial Statements

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis DuPont equation Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis DuPont equation Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

ACTY 7292 Financial Statement Analysis Final Exam Semester 1, 2015

Faculty of Creative Industries & Business Department of Accounting and Finance Bachelor of Business ACTY 7292 Financial Statement Analysis Final Exam Date: Wednesday 1 st July 2015 Start time: 8.30AM 11.40AM

Faculty of Creative Industries & Business Department of Accounting and Finance Bachelor of Business ACTY 7292 Financial Statement Analysis Final Exam Date: Wednesday 1 st July 2015 Start time: 8.30AM 11.40AM

Ratio Analysis. CA Past Years Exam Question

Ratio Analysis CA Past Years Exam Question Question : 1 Nov, 2009 From the Following Information, Calculate the Amount of Fixed Assets & Proprietors Funds. 1. Ratio of Fixed Assets to Proprietors Funds

Ratio Analysis CA Past Years Exam Question Question : 1 Nov, 2009 From the Following Information, Calculate the Amount of Fixed Assets & Proprietors Funds. 1. Ratio of Fixed Assets to Proprietors Funds

1) Using the information provided for Gasparro Corp., complete the questions regarding fully diluted shares outstanding

Using the information provided for Gasparro Corp., complete the questions regarding fully diluted shares outstanding") Chapter 1 Comparable Companies Analysis 1) Using the information provided for Gasparro Corp., complete the questions regarding fully diluted shares outstanding General Information Company Name Gasparro

Chapter 1 Comparable Companies Analysis 1) Using the information provided for Gasparro Corp., complete the questions regarding fully diluted shares outstanding General Information Company Name Gasparro

Chapter 02 Analysis of Financial Statements

Chapter 02 Analysis of Financial Statements TRUEFALSE 1. The information contained in the annual report is used by investors to form expectations about future earnings and dividends. 2. Noncash assets

Chapter 02 Analysis of Financial Statements TRUEFALSE 1. The information contained in the annual report is used by investors to form expectations about future earnings and dividends. 2. Noncash assets

Writing a Financial Report: Some Guidelines

Writing a Financial Report: Some Guidelines Table of contents 1. A guiding principle... 2 2. An example of analysis grid... 3 3. Financial ratios: the toolkit of the financial analyst... 4 3.1. Growth

Writing a Financial Report: Some Guidelines Table of contents 1. A guiding principle... 2 2. An example of analysis grid... 3 3. Financial ratios: the toolkit of the financial analyst... 4 3.1. Growth

Solutions Manual. Fundamentals of Corporate Finance 9 th edition Ross, Westerfield, and Jordan

Solutions Manual Fundamentals of Corporate Finance 9 th edition Ross, Westerfield, and Jordan Updated 12-20-2008 CHAPTER 1 INTRODUCTION TO CORPORATE FINANCE Answers to Concepts Review and Critical Thinking

Solutions Manual Fundamentals of Corporate Finance 9 th edition Ross, Westerfield, and Jordan Updated 12-20-2008 CHAPTER 1 INTRODUCTION TO CORPORATE FINANCE Answers to Concepts Review and Critical Thinking

Fundamentals of Corporate Finance, 3e (Berk/DeMarzo/Harford) Chapter 2 Introduction to Financial Statement Analysis

Chapter 2 Introduction to Financial Statement Analysis") Fundamentals of Corporate Finance, 3e (Berk/DeMarzo/Harford) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) In the United States, publicly traded

Fundamentals of Corporate Finance, 3e (Berk/DeMarzo/Harford) Chapter 2 Introduction to Financial Statement Analysis 2.1 Firms' Disclosure of Financial Information 1) In the United States, publicly traded

Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international financial statements.

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

financial Analysis Annual Report

financial Analysis Annual Report 217 87 DuPont Analysis Increase in sales volume by 16% coupled with increasing price trend during the year resulted in higher sales and profits due to which EBIT margin

financial Analysis Annual Report 217 87 DuPont Analysis Increase in sales volume by 16% coupled with increasing price trend during the year resulted in higher sales and profits due to which EBIT margin

CVX Chevron Corporation Sector: Energy SELL

Analysts: Zachary Haller, Andrew Paley Brown and Sean Miller Washburn University Applied Portfolio Management CVX Sector: Energy SELL Report Date: 4/18/2016 Market Cap (mm) $157,566 Annual Dividend $4.28

Analysts: Zachary Haller, Andrew Paley Brown and Sean Miller Washburn University Applied Portfolio Management CVX Sector: Energy SELL Report Date: 4/18/2016 Market Cap (mm) $157,566 Annual Dividend $4.28

Chapter 02 Evaluating Financial Performance

Chapter 02 Evaluating Financial Performance Multiple Choice Questions 1. The most popular yardstick of financial performance among investors and senior managers is the: A. profit margin. B. return on equity.

Chapter 02 Evaluating Financial Performance Multiple Choice Questions 1. The most popular yardstick of financial performance among investors and senior managers is the: A. profit margin. B. return on equity.

Today s Agenda. Deriving the Du Pont Identity. Nike & Reebok s Profitability Ratios

Today s Agenda DuPont Identity Market Value Ratios Financial Statement Analysis Uses & Problems Introduction to Bond Valuation Nike & Reebok s Profitability Ratios Profitability Ratios Nike Reebok Profit

Today s Agenda DuPont Identity Market Value Ratios Financial Statement Analysis Uses & Problems Introduction to Bond Valuation Nike & Reebok s Profitability Ratios Profitability Ratios Nike Reebok Profit

C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM

1 C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM What have we done in the course? On a chapter by chapter basis, we primarily have examined specific transactions and the effect on financial

1 C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM What have we done in the course? On a chapter by chapter basis, we primarily have examined specific transactions and the effect on financial

ACTY 7292 Financial Statement Analysis Final Exam Semester 2, 2016

Faculty of Creative Industries & Business Department of Accounting and Finance Bachelor of Business ACTY 7292 Financial Statement Analysis Final Exam Semester 2, 2016 Date: Wednesday 23 rd November 2016

Faculty of Creative Industries & Business Department of Accounting and Finance Bachelor of Business ACTY 7292 Financial Statement Analysis Final Exam Semester 2, 2016 Date: Wednesday 23 rd November 2016

Financial & Managerial Accounting Practice with Ratios and Analysis

Financial & Managerial Accounting Practice with Ratios and Analysis A company had the following income statement for the year and the balance sheet accounts at the end of the year. Use the information

Financial & Managerial Accounting Practice with Ratios and Analysis A company had the following income statement for the year and the balance sheet accounts at the end of the year. Use the information

Chapter 17. Financial Statement Analysis

Chapter 17 Financial Statement Analysis 17-2 Topics Covered Financial Ratios DuPont System Using Financial ratios Measuring Company Performance The Role of Financial Ratios 17-3 Financial Ratios Five types

Chapter 17 Financial Statement Analysis 17-2 Topics Covered Financial Ratios DuPont System Using Financial ratios Measuring Company Performance The Role of Financial Ratios 17-3 Financial Ratios Five types

PRINT Name: Brief Answer Key.

Financial & Managerial Accounting Fall 2009 Exam 2 General Instructions. Make sure you write answers clearly. Make sure to show your work when appropriate partial credit can be given for work shown. Finally,

Financial & Managerial Accounting Fall 2009 Exam 2 General Instructions. Make sure you write answers clearly. Make sure to show your work when appropriate partial credit can be given for work shown. Finally,

KO Financial Analysis, Page 1 of 10

KO Financial Analysis, Page 1 of 10 Enter Firm Ticker KO values in millions Historical Income Statements Income Statement Forecasting Percentages Enter first year in cell B5 2005 2006 2007 2008 2009 2005

KO Financial Analysis, Page 1 of 10 Enter Firm Ticker KO values in millions Historical Income Statements Income Statement Forecasting Percentages Enter first year in cell B5 2005 2006 2007 2008 2009 2005

ACC 501 Quizzes Lecture 1 to 22

ACC501 Business Finance Composed By Faheem Saqib A mega File of MiD Term Solved MCQ For more Help Rep At Faheem_saqib2003@yahoocom Faheemsaqib2003@gmailcom 0334-6034849 ACC 501 Quizzes Lecture 1 to 22

ACC501 Business Finance Composed By Faheem Saqib A mega File of MiD Term Solved MCQ For more Help Rep At Faheem_saqib2003@yahoocom Faheemsaqib2003@gmailcom 0334-6034849 ACC 501 Quizzes Lecture 1 to 22

In March 2005, shares of stock in chipmaker Intel were trading. Financial Statements. How to standardize financial statements for comparison purposes.

and Cash Flow In March 2005, shares of stock in chipmaker Intel were trading for about $23. At that price, Intel had a price-earnings ratio of 20, meaning that investors were willing to pay $20 for every

and Cash Flow In March 2005, shares of stock in chipmaker Intel were trading for about $23. At that price, Intel had a price-earnings ratio of 20, meaning that investors were willing to pay $20 for every

FINANCIAL STATEMENT ANALYSIS & RATING CAMPARI S.P.A.

FINANCIAL STATEMENT ANALYSIS & RATING CAMPARI S.P.A. Year 2012-2014 Report developed on www.cloudfinance.it 2 Sommario Financial Highlights... 3 Reclassified Financials... 8 Structure of Assets & Liabilities...

FINANCIAL STATEMENT ANALYSIS & RATING CAMPARI S.P.A. Year 2012-2014 Report developed on www.cloudfinance.it 2 Sommario Financial Highlights... 3 Reclassified Financials... 8 Structure of Assets & Liabilities...

Business 2019, Spring 2003

Business 2019, Spring 2003 Assignment 1 Suggested Answers 1. Financial Statements and Cash Flow Answer the following questions using Table 1. Bed Rock s tax rate in 2002 was 34%. (a) (6 points) Complete

Business 2019, Spring 2003 Assignment 1 Suggested Answers 1. Financial Statements and Cash Flow Answer the following questions using Table 1. Bed Rock s tax rate in 2002 was 34%. (a) (6 points) Complete

Corporate Finance. Week 3 Financial Statement Analysis II

Corporate Finance 1-1 Week 3 Financial Statement Analysis II 1-1 Asset Efficiency or Turnover Measures 1-2 A first broad measure of efficiency is asset turnover: Sales Asset Turnover = Total Assets Fixed

Corporate Finance 1-1 Week 3 Financial Statement Analysis II 1-1 Asset Efficiency or Turnover Measures 1-2 A first broad measure of efficiency is asset turnover: Sales Asset Turnover = Total Assets Fixed

Understanding Financial Statements. Elizabeth Rankin

Understanding Financial Statements Elizabeth Rankin Overview Accounting Concepts Principles Financial Statements Evaluating Performance Horizontal Analysis Vertical Analysis Ratio Analysis Entity Concept

Understanding Financial Statements Elizabeth Rankin Overview Accounting Concepts Principles Financial Statements Evaluating Performance Horizontal Analysis Vertical Analysis Ratio Analysis Entity Concept

Week 4 and Week 5 Handout Financial Statement Analysis

Week 4 and Week 5 Handout Financial Statement Analysis Introduction After understanding the basic financial statements, one may be interested in analysing the financial statements to understand the performance

Week 4 and Week 5 Handout Financial Statement Analysis Introduction After understanding the basic financial statements, one may be interested in analysing the financial statements to understand the performance

Module 4. Analyzing and Interpreting Financial Statements

Module 4 Analyzing and Interpreting Financial Statements Analysis Structure Return on Equity Return on equity (ROE) is computed as: Operating Return (RNOA) The income statement reflects operating activities

Module 4 Analyzing and Interpreting Financial Statements Analysis Structure Return on Equity Return on equity (ROE) is computed as: Operating Return (RNOA) The income statement reflects operating activities

Chapter 2 Introduction to Financial Statement Analysis

Chapter 2 Introduction to Financial Statement Analysis 2-1. What four financial statements can be found in a firm s 10-K filing? What checks are there on the accuracy of these statements? In a firm s 10-K

Chapter 2 Introduction to Financial Statement Analysis 2-1. What four financial statements can be found in a firm s 10-K filing? What checks are there on the accuracy of these statements? In a firm s 10-K

Chapter 2 Solutions. 2-4 Shares issued = 100,000 Price per share = $7 Par value per share = $3

Chapter 2 CFIN5 Chapter 2 Solutions 2-1 Publically-traded companies are required to provide adequate financial information to their shareholders. Information generally is provided through financial reports

Chapter 2 CFIN5 Chapter 2 Solutions 2-1 Publically-traded companies are required to provide adequate financial information to their shareholders. Information generally is provided through financial reports

Financial Statement Fraud. Improper Recording of Liabilities

Financial Statement Fraud Improper Recording of Liabilities Introduction Similar to deferring costs and expenses, improperly recording liabilities is another method of fraudulently manipulating financial

Financial Statement Fraud Improper Recording of Liabilities Introduction Similar to deferring costs and expenses, improperly recording liabilities is another method of fraudulently manipulating financial

Chapter 17. Page 1. Company Analysis. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 17 Company Analysis Learning Objectives Define fundamental analysis at the company level. Explain the

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 17 Company Analysis Learning Objectives Define fundamental analysis at the company level. Explain the