Financial Statement Analysis. Cash Flow Statement

|

|

|

- Kenneth Farmer

- 5 years ago

- Views:

Transcription

1 Financial Statement Analysis Cash Flow Statement 1

2 The Articulation of the Financial Statements Beginning stocks Flows Ending stocks Cash Flow Statement Beginning Balance Sheet Cash Cash from operations Cash from investing Cash from financing Net change in cash Ending Balance Sheet Cash + Other Assets Total Assets - Liabilities Owners equity Statement of Shareholders Equity Investment and disinvestment by owners Net income and other earnings Net change in owners equity + Other Assets Total Assets - Liabilities Owners equity Income Statement Revenues Expenses Net income

3 Cash Flow Statement The statement of cash flows explains the change in cash during the period in terms of cash provided by or used for operating, investing and financing activities. 3

4 Analyzing the Statement of Cash Flows The statement of cash flows is an important analytical tool for creditors, investors, and other users of financial statement data. 4-4

5 5

6 6

7 Analyzing the Statement of Cash Flows Statement of cash flows helps to determine a firm s ability to generate cash flows in the future capacity to meet cash obligations future external financing needs success in productively managing investing activities effectiveness in implementing financing and investing strategies 4-7

8 Cash Flow It is possible for a firm to be highly profitable and not be able to pay dividends not be able to invest in new equipment not be able to service debt go bankrupt How? The problem is cash. 4-8

9 Statement of Cash Flows Positive net income on the income statement is ultimately insignificant unless a company can translate its earnings into cash 4-9

10 Cash Flow from Operations Ongoing operation depends upon its success in generating cash from operations. Firms need cash to satisfy creditors and investors. Temporary shortfalls of cash can be satisfied by borrowing or other means, but ultimately a firm must generate cash. 4-10

11 Nocash Corporation The Nocash Corporation had sales of $100,000 in its second year of operations, up from $50,000 in the first year. Expenses, including taxes, amounted to $70,000 in year 2, compared with $40,000 in year

12 Nocash Corporation Nocash Corporation Income Statement for Year 1 and Year 2 Year 1 Year 2 Sales $50,000 $100,000 Expenses 40,000 70,000 Net income $10,000 $30,000 The comparative income statements for the two years indicate substantial growth. 4-12

13 Nocash Corporation Other relevant facts that do not appear on income statement. Nocash eased credit policies in year 2, attracting customers of lower quality. purchased a new line of inventory near the end of year 1 and had to sell it below cost. had problems with accounts receivable causing suppliers to refuse the sale of goods on credit. The effect of these factors can be found on Nocash s balance sheet. 4-13

14 Nocash Corporation Balance Sheet at December 31 Year 1 Year 2 $Change Cash $2,000 $2,000 0 Accounts Receivable 10,000 30, ,000 Inventories 10,000 25, ,000 Total Assets $22,000 $57, ,000 Accounts payable 7,000 2,000-5,000 Notes payable to banks 0 10, ,000 Equity 15,000 45, ,000 Total liabilities and equity $22,000 $57, ,

15 Nocash Corporation If Nocash s net income is recalculated on a cash basis, the following adjustments would be made: Net income $30,000 Accounts receivable (20,000) Inventories (15,000) Accounts payable (5,000) Cash Income ($10,000) 4-15

16 Nocash Corporation Increase in accounts receivable is subtracted, because more sales revenue was recognized in computing net income than was collected in cash. Increase in inventory is deducted, reflecting the cash outflow for inventory purchases in excess of the expense recognized through cost of goods sold. 4-16

17 Nocash Corporation Decrease in accounts payable is deducted, because the cash payments to suppliers in year 2 were greater than the amount of expense recorded. Appearance of a $10,000 note payable indicates that borrowing has enable Nocash to operate, but unless it can generate cash, its problems will compound. 4-17

18 Statement of Cash Flows Provides information about cash inflows and outflows during an accounting period Extremely important as an analytical tool Only source in financial statement data for learning about the generation of cash from operations 4-18

19 Four Parts of a Statement of Cash Flows Cash Operating activities Investing activities Financing activities 4-19

20 20

21 Four Parts of a Statement of Cash Flows Cash Cash and highly liquid short-term marketable securities Also called cash equivalents If a company separates marketable securities into two accounts (cash and cash equivalents and short-term investments), the short-term investments are classified as investing activities. 4-21

22 22

23 23

24 Four Parts of a Statement of Cash Flows Operating activities Delivering or producing goods for sale and providing services Cash effects of transactions and other events 4-24

25 Four Parts of a Statement of Cash Flows Investing activities Acquiring and selling or otherwise disposing of securities that are not cash equivalents productive assets that are expected to benefit the firm for long periods of time Lending money and collecting on loans 4-25

26 Four Parts of a Statement of Cash Flows Financing activities Borrowing from creditors and repaying the principal Obtaining resources from owners and providing them with a return on the investment 4-26

27 GAAP Differences can matter 27

28 Direct and Indirect methods of calculating operating cash flow Direct and indirect methods yield identical figures for net cash flow from operating activities, because the underlying accounting concepts are the same. 594 firms out of 600 used the indirect method in 2007 according to Accounting Trends and Techniques. Chinese accounting standards require use of direct method with reconciliation using indirect method in the footnotes. 4-28

29 Direct Method Shows cash collections from customers interest and dividends collected other operating cash receipts cash paid to suppliers and employees interest paid taxes paid other operating cash payments 4-29

30 Cash Flow Statement Direct Method 30

31 Reconciliation to Indirect method 31

32 32

33 Indirect Method Starts with net income and adjusts for deferrals accruals noncash items, such as depreciation and amortization nonoperating items, such as gains and losses on asset sales 4-33

34 Indirect Method 34

35 Net Cash Flow from Operating Activities Indirect Method Depreciation and amortization are added to net income. Increase in deferred tax liability is added. Decrease in deferred tax liability is deducted. Increase in deferred tax asset is deducted. Decrease in deferred tax asset is added. 4-35

36 Net Cash Flow from Operating Activities Indirect Method Increase in investment account from equity income is deducted. Decrease in investment account from equity income is added. Gain on sale of assets is deducted. Loss on sale of assets is added. 4-36

37 Net Cash Flow from Operating Activities Indirect Method Increase in accounts receivable is deducted. Decrease in accounts receivable is added. Increase in inventory is deducted. Decrease in inventory is added. Increase in prepaid expenses is deducted. Decrease in prepaid expenses is added. 4-37

38 Net Cash Flow from Operating Activities Indirect Method Increase in interest receivable is deducted. Decrease in interest receivable is added. Increase in accounts payable is added. Decrease in accounts payable is deducted. 4-38

39 Net Cash Flow from Operating Activities Indirect Method Increase in accrued liabilities is added. Decrease in accrued liabilities is deducted. Increase in deferred revenue is added. Decrease in deferred revenue is deducted. 4-39

40 Analysis of the Statement of Cash Flows Should, at a minimum, cover the following areas: Cash flow from operating activities Cash inflows Cash outflows 4-40

41 Analysis of the Statement of Cash Flows Analyst Concerns Success or failure of the firm in generating cash from operations Underlying causes of the positive or negative operating cash flow Magnitude of positive or negative operating cash flow Fluctuations in cash flow from operations over time 4-41

42 Analysis of Cash Inflows Generating cash from operations is the preferred method for obtaining excess cash to finance capital expenditures and expansion repayment of debt payment of dividends 4-42

43 Analysis of Cash Outflows When analyzing the cash outflows, the analyst should consider the necessity of the outflow how the outflow was financed Generally, it is best to finance short-term assets with short-term debt long-term assets with long-term debt or issuance of stock 4-43

44 Analysis of Cash Outflows Repayment of debt is a necessary outflow. Notes reveal future debt repayments and are useful in assessing how much cash will be needed in upcoming years to repay outstanding debt. 4-44

45 Free Cash Flow Cash basis net income less capital expenditures Some argue it is a better measure than net income. No estimates! You cannot calculate either cash basis net income or capital expenditures from an income statement or balance sheet (but you can make a pretty good guess) The cash flow statement supplies the missing information. 45

Free Cash Flow (14,090) 46")

46 Free Cash Flow Cash flow operations 1,891 Capex (15,981) Free Cash Flow (14,090) 46

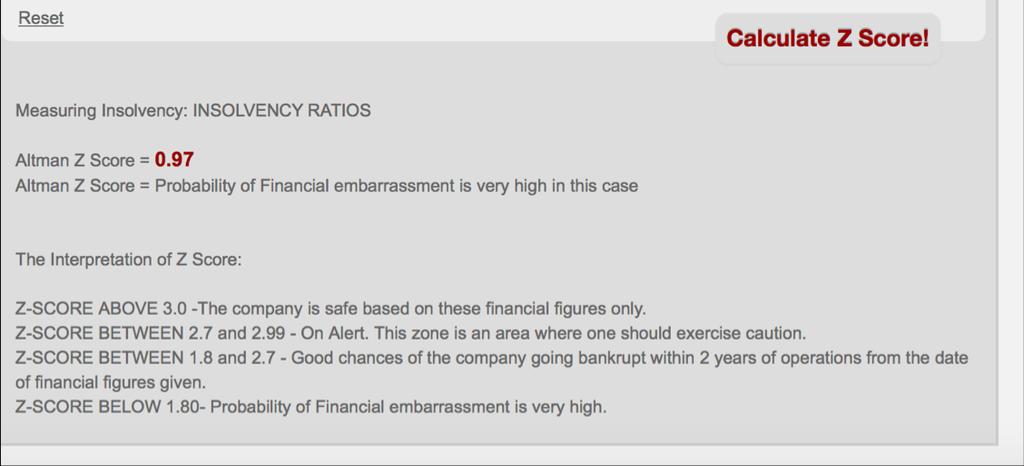

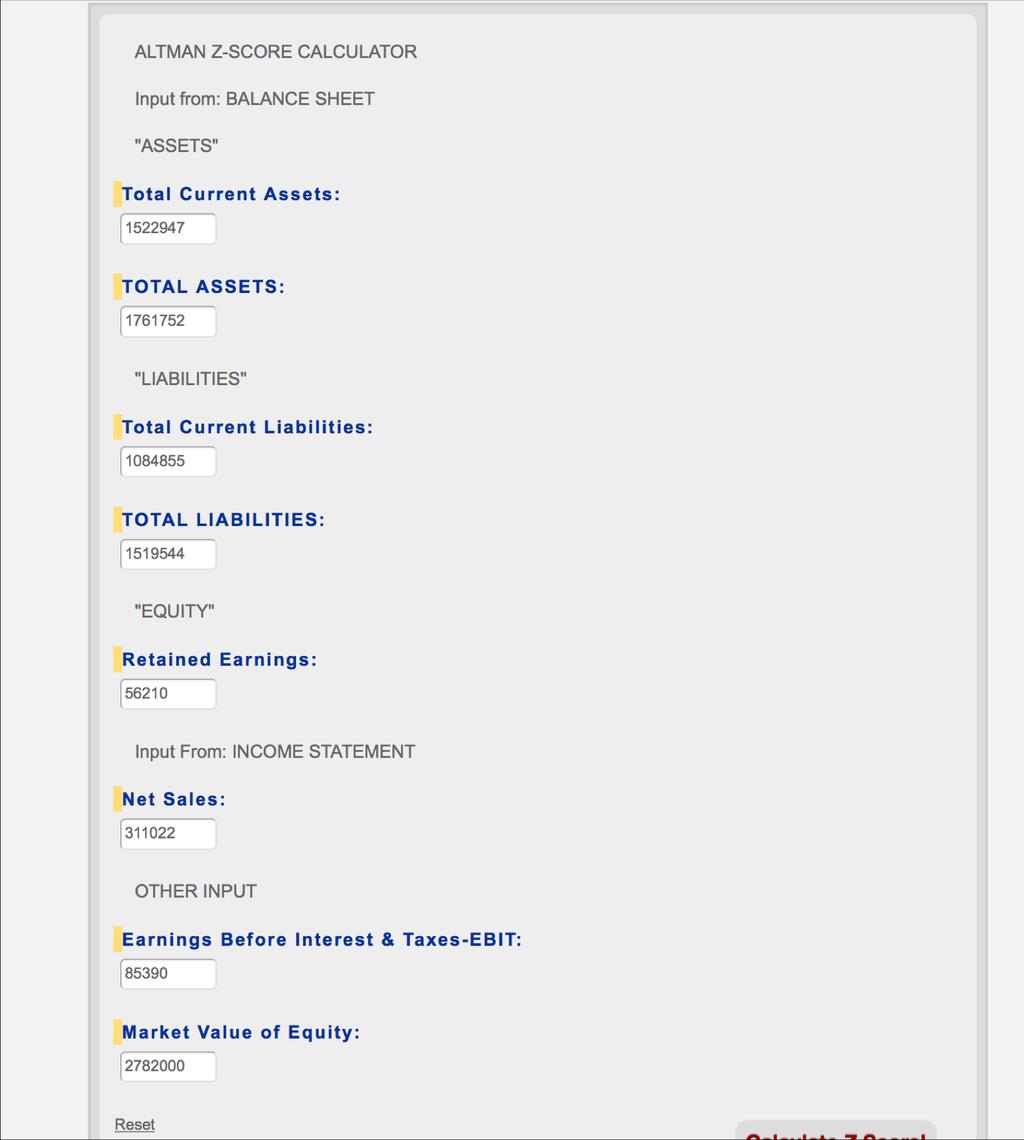

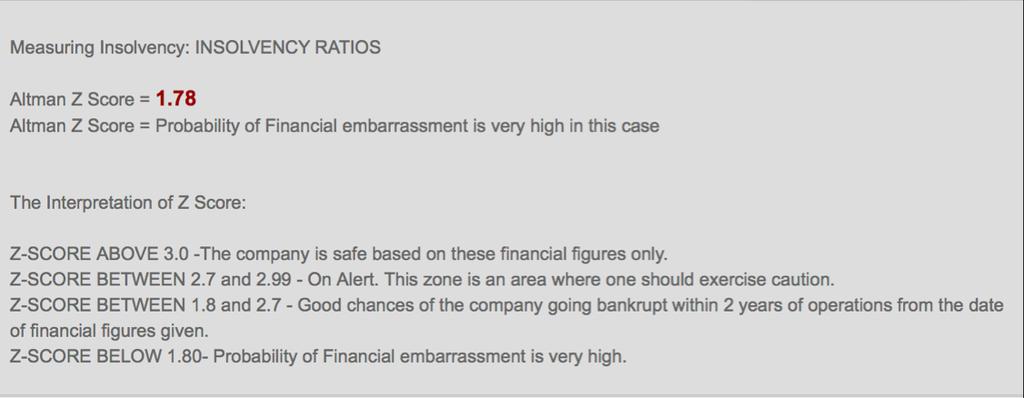

47 Altman s Z

48 Evergrande Altman s Z

49 Piotroski s F Score 1. Return on assets is positive (1 point) 2. Positive operating cash flow in the current year (1 point) 3. Higher return on assets (ROA) in the current period compared to the ROA in the previous year (1 point). 4. Cash flow from operations is greater than net income (1 point). 5. Lower ratio of long term debt to in the current period compared value in the previous year (1 point). 6. Higher current ratio this year compared to the previous year (1 point). 7. No new shares were issued in the last year (1 point). 8. A higher gross margin compared to the previous year (1 point). 9. A higher asset turnover ratio compared to the previous year (1 pt). If a company scores 8 or 9, it is considered to have strong and improving financials, whereas a score between 0-2 points suggests a company has weak and deteriorating financials. 49

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

CHAPTER 12 STATEMENT OF CASH FLOWS

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

ANSWER SHEET EXAMINATION #2

ANSWER SHEET EXAMINATION #2 1) D 2) B 26) D 3) C 27) B 4) A 28) B 5) D 29) C 6) D 30) A 7) D 31) B 8) C 32) D 9) D 33) D 10) B 34) D 11) A 12) A 13) D 14) C 15) A 16) C 17) B 18) B 19) C 20) B 21) B 22)

ANSWER SHEET EXAMINATION #2 1) D 2) B 26) D 3) C 27) B 4) A 28) B 5) D 29) C 6) D 30) A 7) D 31) B 8) C 32) D 9) D 33) D 10) B 34) D 11) A 12) A 13) D 14) C 15) A 16) C 17) B 18) B 19) C 20) B 21) B 22)

Statement of Cash Flows. Statement of Cash Flows. Classification of Business Activities. Learning Objectives

Statement of Cash Flows Learning Objectives 1. Understand the different activities of a business and how this influences the cash flow statement 2. Understand the direct and indirect methods for preparation

Statement of Cash Flows Learning Objectives 1. Understand the different activities of a business and how this influences the cash flow statement 2. Understand the direct and indirect methods for preparation

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES INVESTING ACTIVITIES FINANCING ACTIVITIES

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

Statement of Cash Flows (SCF)

") Statement of Cash Flows (SCF) The statement of cash flows (SCF) or cash flow statement reports a corporation's significant cash inflows and outflows that occurred during an accounting period. This financial

Statement of Cash Flows (SCF) The statement of cash flows (SCF) or cash flow statement reports a corporation's significant cash inflows and outflows that occurred during an accounting period. This financial

Statements of Net Position - Business - Type Activities South Carolina Public Service Authority As of March 31, 2018 and December 31, 2017

Statements of Net Position - Business - Type Activities As of March 31, 2018 and December 31, 2017 ASSETS Current assets Unrestricted cash and cash equivalents $ 207,610 $ 731,758 Unrestricted investments

Statements of Net Position - Business - Type Activities As of March 31, 2018 and December 31, 2017 ASSETS Current assets Unrestricted cash and cash equivalents $ 207,610 $ 731,758 Unrestricted investments

Statements of Net Position - Business - Type Activities South Carolina Public Service Authority As of September 30, 2018 and December 31, 2017

Statements of Net Position - Business - Type Activities As of September 30, 2018 and December 31, 2017 ASSETS Current assets Unrestricted cash and cash equivalents $ 315,796 $ 731,758 Unrestricted investments

Statements of Net Position - Business - Type Activities As of September 30, 2018 and December 31, 2017 ASSETS Current assets Unrestricted cash and cash equivalents $ 315,796 $ 731,758 Unrestricted investments

You are provided with the following transactions that took place during a recent fis-

Chapter 17 PROBLEMS: SET C You are provided with the following transactions that took place during a recent fis- P17-1C cal year. (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) Cash Inflow, Where Reported Outflow,

Chapter 17 PROBLEMS: SET C You are provided with the following transactions that took place during a recent fis- P17-1C cal year. (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) Cash Inflow, Where Reported Outflow,

16 Statement of Cash Flows

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

The statement of cash flows reports cash flows, cash receipts, and cash payments, to show where cash came from and how it was spent.

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows QUESTIONS FOR REVIEW OF KEY TOPICS Question 4 1 The income statement is a change statement that reports transactions

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows QUESTIONS FOR REVIEW OF KEY TOPICS Question 4 1 The income statement is a change statement that reports transactions

CHAPTER 17 PROBLEMS: SET B

CHAPTER 17 PROBLEMS: SET B P17-1B You are provided with the following transactions that took place during a recent fiscal year. Statement of Cash Inflow, Cash Flow Outflow, or Transaction Activity Affected

CHAPTER 17 PROBLEMS: SET B P17-1B You are provided with the following transactions that took place during a recent fiscal year. Statement of Cash Inflow, Cash Flow Outflow, or Transaction Activity Affected

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Name of business Statement of cash flows for the financial year end 31 December 20X1 (DIRECT METHOD) Inflow /(outflow)

Inflow /(outflow)") Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson. The statement of cash flows is a required component of financial statements.

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

AGENDA: STATEMENT OF CASH FLOWS

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

Original SSAP and Current Authoritative Guidance: SSAP No. 69

Statutory Issue Paper No. 92 Statement of Cash Flow STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 69 Type of Issue: Common Area SUMMARY OF ISSUE 1. Current

Statutory Issue Paper No. 92 Statement of Cash Flow STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 69 Type of Issue: Common Area SUMMARY OF ISSUE 1. Current

CHAPTER 4: REPORTING AND ANALYZING CASH FLOWS

M4-22. a. Cash flow from an operating activity. b. Cash flow from an investing activity. c. Cash flow from an investing activity. d. Cash flow from an operating activity. e. Cash flow from a financing

M4-22. a. Cash flow from an operating activity. b. Cash flow from an investing activity. c. Cash flow from an investing activity. d. Cash flow from an operating activity. e. Cash flow from a financing

Schedule 54: Consolidated Statement of Cash Flows

Schedule 54: Consolidated Statement of Cash Flows The consolidated statement of cash flows reflects the effects of a municipality s activities on its cash resources. The statement of cash flows shows how

Schedule 54: Consolidated Statement of Cash Flows The consolidated statement of cash flows reflects the effects of a municipality s activities on its cash resources. The statement of cash flows shows how

Town of Carrboro, North Carolina Balance Sheet Governmental Funds June 30, 2016

Balance Sheet Governmental June 30, 2016 Major Grants Revolving Bond Capital Administration General Fund Loan Fund Fund Projects Fund Fund ASSETS Cash and cash equivalents $ 14,749,029 $ 493,234 $ 1,623,198

Balance Sheet Governmental June 30, 2016 Major Grants Revolving Bond Capital Administration General Fund Loan Fund Fund Projects Fund Fund ASSETS Cash and cash equivalents $ 14,749,029 $ 493,234 $ 1,623,198

Reading & Understanding Financial Statements

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements. A Guide to Financial Reporting

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Statement of Cash Flows

CHAPTER 14 Statement of Cash Flows LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Prepare the operating activities section of a statement of cash flows

CHAPTER 14 Statement of Cash Flows LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Prepare the operating activities section of a statement of cash flows

Schedule 54: Consolidated Statement of Cash Flows

Schedule 54: Consolidated Statement of Cash Flows The consolidated statement of cash flows reflects the effects of a municipality s activities on its cash resources. The statement of cash flows shows how

Schedule 54: Consolidated Statement of Cash Flows The consolidated statement of cash flows reflects the effects of a municipality s activities on its cash resources. The statement of cash flows shows how

Statement of Financial Accounting Standards No. 17. Statements of Financial Accounting Standards No.17. Statement of Cash Flows

Statement of Financial Accounting Standards No. 17 Statements of Financial Accounting Standards No.17 Statement of Cash Flows Revised on 22 September 2005 Translated by TsingZai Wu, Associate Professor

Statement of Financial Accounting Standards No. 17 Statements of Financial Accounting Standards No.17 Statement of Cash Flows Revised on 22 September 2005 Translated by TsingZai Wu, Associate Professor

CHAPTER 17 THE STATEMENT OF CASH FLOWS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. True-False Statements. Multiple Choice Questions

CHAPTER 17 THE STATEMENT OF CASH FLOWS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 K 17. 2 C a

CHAPTER 17 THE STATEMENT OF CASH FLOWS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 K 17. 2 C a

Statement of Cash Flows

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

Lesson 4 Cash Flow Analysis

Advanced Accounting AY 2017/2018 Lesson 4 Cash Flow Analysis Università degli Studi di Trieste D.E.A.M.S. Paolo Altin 90 Statement of Cash Flows The purpose of the statement of cash flows is to provide

Advanced Accounting AY 2017/2018 Lesson 4 Cash Flow Analysis Università degli Studi di Trieste D.E.A.M.S. Paolo Altin 90 Statement of Cash Flows The purpose of the statement of cash flows is to provide

Financial Statement Analysis L7: Cash flow analysis

7-1 Financial Statement Analysis L7: Cash flow analysis 7-2 Statement of Cash Flows Relevance of Cash Cash is the most liquid of assets. Offers both liquidity and flexibility. Both the beginning and the

7-1 Financial Statement Analysis L7: Cash flow analysis 7-2 Statement of Cash Flows Relevance of Cash Cash is the most liquid of assets. Offers both liquidity and flexibility. Both the beginning and the

The Cash Flow Statement

The Cash Flow Statement This statement is also known as the Statement of Changes in Financial Position Statement of Changes in Financial Position A statement of changes in financial position reports the

The Cash Flow Statement This statement is also known as the Statement of Changes in Financial Position Statement of Changes in Financial Position A statement of changes in financial position reports the

Chapter 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

1 Chapter 12 2 The statement of cash flows is a major financial statement as are the income statement, balance sheet, and statement of stockholders' equity. The statement of cash flows is required whenever

1 Chapter 12 2 The statement of cash flows is a major financial statement as are the income statement, balance sheet, and statement of stockholders' equity. The statement of cash flows is required whenever

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations. Exercises

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations 1. Net cash flow from operating activities 2. Change in Cash 3. Cash used to purchase property, plant, and equipment

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations 1. Net cash flow from operating activities 2. Change in Cash 3. Cash used to purchase property, plant, and equipment

Examples of assets that would not be recognized:

Near-Term Financial Resources Overview Information about spending and resources available for spending Report amount available for spending in the next period Near-term would be a specific period of time,

Near-Term Financial Resources Overview Information about spending and resources available for spending Report amount available for spending in the next period Near-term would be a specific period of time,

UNAUDITED FINANCIAL INFORMATION. March 31, 2018

UNAUDITED FINANCIAL INFORMATION March 31, 2018 SCHEDULES OF NET POSITION March 31, 2018 ASSETS Current assets: Cash and cash equivalents $ 2,352 $ 15,172 $ 21,166 $ 32,362 $ 177,840 $ 248,892 Investments

UNAUDITED FINANCIAL INFORMATION March 31, 2018 SCHEDULES OF NET POSITION March 31, 2018 ASSETS Current assets: Cash and cash equivalents $ 2,352 $ 15,172 $ 21,166 $ 32,362 $ 177,840 $ 248,892 Investments

Understanding The Cash Flow Statement

Financial Reporting & Analysis Understanding The Cash Flow Statement Reading - 27 www.proschoolonline.com/ 1 Components and Format of Cash Flow Statement Apple Inc. - Cash Flow Statement Year ended 26

Financial Reporting & Analysis Understanding The Cash Flow Statement Reading - 27 www.proschoolonline.com/ 1 Components and Format of Cash Flow Statement Apple Inc. - Cash Flow Statement Year ended 26

Statement of Cash Flows. Barry M Frohlinger

Statement of Cash Flows Barry M Frohlinger Statement of Cash Flows Page 1 Barry M Frohlinger, Inc. copyright 1981-2010 Companies are required to present a Statement of Cash Flows (cash statement) for each

Statement of Cash Flows Barry M Frohlinger Statement of Cash Flows Page 1 Barry M Frohlinger, Inc. copyright 1981-2010 Companies are required to present a Statement of Cash Flows (cash statement) for each

6 The following terms are used in this Standard with the meanings specified: Cash comprises cash on hand and demand deposits.

International Accounting Standard 7 Statement of Cash Flows 1 Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of Cash Flows 1 Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

WRIGHT STATE UNIVERSITY

FINANCE, AUDIT and INFRASTRUCTURE COMMITTEE November 17, 2017 Financial Statement Summary Fiscal Year Ended June 30, 2017 A Component Unit of the State of Ohio Statements of Net Position June 30, 2017

FINANCE, AUDIT and INFRASTRUCTURE COMMITTEE November 17, 2017 Financial Statement Summary Fiscal Year Ended June 30, 2017 A Component Unit of the State of Ohio Statements of Net Position June 30, 2017

Statement of Cash Flows

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate

Reading Understanding. Financial Statements. A Layman s Guide to Financial Reporting

Reading Understanding & Financial Statements A Layman s Guide to Financial Reporting 1 Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted,

Reading Understanding & Financial Statements A Layman s Guide to Financial Reporting 1 Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted,

Statement of Cash Flows

Statement of Cash Flows Statement of cash flows General Principles Mandatory for most of the entities Direct and Indirect method Generally starts with PAT (Profit after tax) 2 Overview of AS 3 Requires

Statement of Cash Flows Statement of cash flows General Principles Mandatory for most of the entities Direct and Indirect method Generally starts with PAT (Profit after tax) 2 Overview of AS 3 Requires

CHAPTER 17. The Cash Flow Statement. Brief Questions Exercises 12, 13 3, 4, 5, 11 6, 7, 8, 9, 10, 11

CHAPTER 17 The Cash Flow Statement ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the purpose and content of the cash flow

CHAPTER 17 The Cash Flow Statement ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the purpose and content of the cash flow

Via Technologies, Inc. and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2015 and 2014

Via Technologies, Inc. and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2015 and 2014-1 - CONSOLIDATED BALANCE SHEETS June 30, 2015 (Reviewed) December 31, 2014 (Audited)

Via Technologies, Inc. and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2015 and 2014-1 - CONSOLIDATED BALANCE SHEETS June 30, 2015 (Reviewed) December 31, 2014 (Audited)

Reporting and Interpreting Cash Flows

C H A P T E R Reporting and Interpreting Cash Flows LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Classify cash flow statement items as part of net cash flows from operating,

C H A P T E R Reporting and Interpreting Cash Flows LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Classify cash flow statement items as part of net cash flows from operating,

AN INVESTIGATION OF FINANCIAL ACCOUNTING STATEMENTS AND REPORTING TECHNIQUES. By: Rachel Ann May. Oxford, MS May 2017

AN INVESTIGATION OF FINANCIAL ACCOUNTING STATEMENTS AND REPORTING TECHNIQUES By: Rachel Ann May A thesis submitted to the faculty of The University of Mississippi in partial fulfillment of the requirements

AN INVESTIGATION OF FINANCIAL ACCOUNTING STATEMENTS AND REPORTING TECHNIQUES By: Rachel Ann May A thesis submitted to the faculty of The University of Mississippi in partial fulfillment of the requirements

Unappropriated retained earnings (accumulated deficit) Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear

Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear") Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

STATEMENT OF CASH FLOWS

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

ACCOUNTING - CLUTCH CH STATEMENT OF CASH FLOWS.

!! www.clutchprep.com CONCEPT: INTRODUCTION TO STATEMENT OF CASH FLOWS The Statement of Cash Flows shows what affected the Cash account balance throughout the period Predictive Value Helps predict future

!! www.clutchprep.com CONCEPT: INTRODUCTION TO STATEMENT OF CASH FLOWS The Statement of Cash Flows shows what affected the Cash account balance throughout the period Predictive Value Helps predict future

CITY OF DES MOINES, IOWA STATEMENT OF NET POSITION PROPRIETARY FUNDS June 30, 2017

CITY OF DES MOINES, IOWA STATEMENT OF NET POSITION PROPRIETARY FUNDS June 30, 2017 BUSINESS-TYPE ACTIVITIES - ENTERPRISE FUNDS PARKING FACILITIES SEWER STORMWATER SYSTEM SYSTEM UTILITY ASSETS Current assets:

CITY OF DES MOINES, IOWA STATEMENT OF NET POSITION PROPRIETARY FUNDS June 30, 2017 BUSINESS-TYPE ACTIVITIES - ENTERPRISE FUNDS PARKING FACILITIES SEWER STORMWATER SYSTEM SYSTEM UTILITY ASSETS Current assets:

ANALYSIS OF FINANCIAL ACCOUNTING METHODOLOGIES AND APPLICATIONS. By: Kate Culbertson. Oxford May 2017

ANALYSIS OF FINANCIAL ACCOUNTING METHODOLOGIES AND APPLICATIONS By: Kate Culbertson A thesis submitted to the faculty of The University of Mississippi in partial fulfillment of the requirements of the

ANALYSIS OF FINANCIAL ACCOUNTING METHODOLOGIES AND APPLICATIONS By: Kate Culbertson A thesis submitted to the faculty of The University of Mississippi in partial fulfillment of the requirements of the

Visit Free Slides and Ebooks : CHAPTER 23. Statement of Cash Flows

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

Learning Outcomes. The Statement of Cash Flows. Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2

Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2 The Statement of Cash Flows Dr. Chula King Intermediate Accounting 1 Learning Outcomes After completing this

Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2 The Statement of Cash Flows Dr. Chula King Intermediate Accounting 1 Learning Outcomes After completing this

TOTAL TRAINING SOLUTIONS

TOTAL TRAINING SOLUTIONS Global Cash Flow Analysis Get Global by Understanding Global Cash Flow Jeffery W. Johnson Bankers Insight Group jeffery.johnson@bankers-insight.com 770-846-4511 September 2015

TOTAL TRAINING SOLUTIONS Global Cash Flow Analysis Get Global by Understanding Global Cash Flow Jeffery W. Johnson Bankers Insight Group jeffery.johnson@bankers-insight.com 770-846-4511 September 2015

INTERNAL SERVICE FUNDS

INTERNAL SERVICE FUNDS A COUNTY OF RIVERSIDE INTERNAL SERVICE FUNDS These funds were established to account for the goods and services provided by a County department to other County departments, or to

INTERNAL SERVICE FUNDS A COUNTY OF RIVERSIDE INTERNAL SERVICE FUNDS These funds were established to account for the goods and services provided by a County department to other County departments, or to

Chapter 6: Statement of Cash Flows

Chapter 6: Statement of Cash Flows Outline: Why a cash flow statement? Classifications of cash flows Preparation of cash flow statements Determining the change in cash Determining net cash from operating

Chapter 6: Statement of Cash Flows Outline: Why a cash flow statement? Classifications of cash flows Preparation of cash flow statements Determining the change in cash Determining net cash from operating

SLAS 9. Sri Lanka Accounting Standard 9. Cash Flow Statements

Sri Lanka Accounting Standard 9 Cash Flow Statements 107 Contents Sri Lanka Accounting Standard 9 Cash Flow Statements Objective Scope Paragraphs 1-2 Benefits of Cash Flow Information 3-4 Definitions 5

Sri Lanka Accounting Standard 9 Cash Flow Statements 107 Contents Sri Lanka Accounting Standard 9 Cash Flow Statements Objective Scope Paragraphs 1-2 Benefits of Cash Flow Information 3-4 Definitions 5

STATEMENT OF CASH FLOWS

Chapter Seventeen STATEMENT OF CASH FLOWS LEARNING OBJECTIVES After reading this chapter, you should be able to Explain why investors and others are interested in cash flows. State the three types of activities

Chapter Seventeen STATEMENT OF CASH FLOWS LEARNING OBJECTIVES After reading this chapter, you should be able to Explain why investors and others are interested in cash flows. State the three types of activities

pt (Definition Report)

") 1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

Gateway NACM Credit Conference Presented by: Curtis Litchfield, CCE September 19, 2018

Welcome Gateway NACM Credit Conference Presented by: Curtis Litchfield, CCE September 19, 2018 Financial Statement Analysis Tools and Techniques Common-Size Financial Statements Key Financial Ratios Trend

Welcome Gateway NACM Credit Conference Presented by: Curtis Litchfield, CCE September 19, 2018 Financial Statement Analysis Tools and Techniques Common-Size Financial Statements Key Financial Ratios Trend

Tiill now you have learnt about the financial

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

BASIC FINANCIAL STATEMENTS- FUND FINANCIAL STATEMENTS

BASIC FINANCIAL STATEMENTS- FUND FINANCIAL STATEMENTS AE (This Page Intentionally Left Blank) 31 Balance Sheet Governmental Funds June 30, 2017 Teeter ASSETS AND DEFERRED OUTFLOWS OF Flood Debt RESOURCES:

BASIC FINANCIAL STATEMENTS- FUND FINANCIAL STATEMENTS AE (This Page Intentionally Left Blank) 31 Balance Sheet Governmental Funds June 30, 2017 Teeter ASSETS AND DEFERRED OUTFLOWS OF Flood Debt RESOURCES:

JABIL CIRCUIT, INC. AND SUBSIDIARIES CONDENSED CONSOLIDATED BALANCE SHEETS

CONDENSED CONSOLIDATED BALANCE SHEETS (In thousands) 2011 2010 ASSETS Current assets: Cash and cash equivalents $ 888,611 $ 744,329 Trade accounts receivable, net 1,100,926 1,408,319 Inventories 2,227,339

CONDENSED CONSOLIDATED BALANCE SHEETS (In thousands) 2011 2010 ASSETS Current assets: Cash and cash equivalents $ 888,611 $ 744,329 Trade accounts receivable, net 1,100,926 1,408,319 Inventories 2,227,339

US Financial Reporting - Primary Terms (Definition Report)

") 1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

4/10/2012. Statement of Cash Flows. Learning Objectives (LO) LO 1 - Purpose of Cash Flow Statement. Learning Objectives (LO)

LO 1 - Purpose of Cash Flow Statement. Learning Objectives (LO)") Statement of Flows CHAPTER Learning Objectives (LO) After studying this chapter, you should be able to 1. Identify the purposes of the statement of cash flows 2. Classify activities affecting cash as operating,

Statement of Flows CHAPTER Learning Objectives (LO) After studying this chapter, you should be able to 1. Identify the purposes of the statement of cash flows 2. Classify activities affecting cash as operating,

Exposure Draft. Accounting Standard (AS) 7. Statement of Cash Flows

7. Statement of Cash Flows") Exposure Draft Accounting Standard (AS) 7 Statement of Cash Flows Last date for the comments: January 21, 2016 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

Exposure Draft Accounting Standard (AS) 7 Statement of Cash Flows Last date for the comments: January 21, 2016 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

IAS 7 : STATEMENT OF CASH FLOWS COMPILED BY: MR. YAGNESH DESAI.

IAS 7 : STATEMENT OF CASH FLOWS CASH FLOWS : TERMINOLOGY Inflows and outflows of cash and cash equivalents. CASH : Comprises cash on hand and demand deposits. CASH EQUIVALENTS : Short-term, highly liquid

IAS 7 : STATEMENT OF CASH FLOWS CASH FLOWS : TERMINOLOGY Inflows and outflows of cash and cash equivalents. CASH : Comprises cash on hand and demand deposits. CASH EQUIVALENTS : Short-term, highly liquid

Governmental Activities

Statement of Net Position June 30, 2015 Activities Business-type Activities Total Component Unit Housing and Community Services Agency Assets Current assets Cash and Investments $ 164,721,343 $ 25,551,358

Statement of Net Position June 30, 2015 Activities Business-type Activities Total Component Unit Housing and Community Services Agency Assets Current assets Cash and Investments $ 164,721,343 $ 25,551,358

BENEFITS OF CASH FLOW INFORMATION

16 Accounting Standard (AS) 3 Cash Flow Statements Contents OBJECTIVE SCOPE Paragraphs 1-2 BENEFITS OF CASH FLOW INFORMATION 3-4 DEFINITIONS 5-7 Cash and Cash Equivalents 6-7 PRESENTATION OF A CASH FLOW

16 Accounting Standard (AS) 3 Cash Flow Statements Contents OBJECTIVE SCOPE Paragraphs 1-2 BENEFITS OF CASH FLOW INFORMATION 3-4 DEFINITIONS 5-7 Cash and Cash Equivalents 6-7 PRESENTATION OF A CASH FLOW

VISTEON CORPORATION AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF OPERATIONS (Dollars in Millions, Except Per Share Data) (Unaudited)

(Unaudited)") CONSOLIDATED STATEMENTS OF OPERATIONS (Dollars in Millions, Except Per Share Data) (Unaudited) Three Months Ended Six Months Ended June 30 June 30 2018 2017 2018 2017 Sales $ 758 $ 774 $ 1,572 $ 1,584

CONSOLIDATED STATEMENTS OF OPERATIONS (Dollars in Millions, Except Per Share Data) (Unaudited) Three Months Ended Six Months Ended June 30 June 30 2018 2017 2018 2017 Sales $ 758 $ 774 $ 1,572 $ 1,584

Cash Flow Statement Analysis

Cash Flow Statement Analysis 1. INTRODUCTION Recall from the article on the income statement that a company will recognize revenue regardless of when payment is received. For example, a company may sell

Cash Flow Statement Analysis 1. INTRODUCTION Recall from the article on the income statement that a company will recognize revenue regardless of when payment is received. For example, a company may sell

Creating a Statement of Cash Flows

MARCH 22, 2018 Creating a Statement of Cash Flows Presented by Nicole Ryan, CPA 1 What is a Cash Flow Statement? A financial statement that provides aggregate data regarding Cash Inflows receipts from

MARCH 22, 2018 Creating a Statement of Cash Flows Presented by Nicole Ryan, CPA 1 What is a Cash Flow Statement? A financial statement that provides aggregate data regarding Cash Inflows receipts from

Financial statements. Chapter One-A. A- Statements of cash flows. 1 IAS 7 Statement of cash flows F5(a)-(h)

-(h)") Chapter One-A Financial statements A- Statements of cash flows Topic list Syllabus reference 1 IAS 7 Statement of cash flows F5(a)-(h) 2 Preparing a statement of cash flows F5(g) Introduction In the long

Chapter One-A Financial statements A- Statements of cash flows Topic list Syllabus reference 1 IAS 7 Statement of cash flows F5(a)-(h) 2 Preparing a statement of cash flows F5(g) Introduction In the long

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT Financial Statement Analysis The process of determining financial strengths and weaknesses of a firm by establishing strategic relationship between the items of the balance sheet,

FINANCIAL MANAGEMENT Financial Statement Analysis The process of determining financial strengths and weaknesses of a firm by establishing strategic relationship between the items of the balance sheet,

Statement of Cash Flows

IAS Standard 7 Statement of Cash Flows In April 2001 the International Accounting Standards Board adopted IAS 7 Cash Flow Statements, which had originally been issued by the International Accounting Standards

IAS Standard 7 Statement of Cash Flows In April 2001 the International Accounting Standards Board adopted IAS 7 Cash Flow Statements, which had originally been issued by the International Accounting Standards

Corporate Accounting Recitation 3. June 18, 2004

15.511 Corporate Accounting Recitation 3 June 18, 2004 Why do we need CF/S? Accrual accounting is often based upon subjective judgments that can introduce measurement error and uncertainty into the reported

15.511 Corporate Accounting Recitation 3 June 18, 2004 Why do we need CF/S? Accrual accounting is often based upon subjective judgments that can introduce measurement error and uncertainty into the reported

CITY OF DES MOINES, IOWA STATEMENT OF NET POSITION PROPRIETARY FUNDS June 30, 2016

CITY OF DES MOINES, IOWA STATEMENT OF NET POSITION PROPRIETARY FUNDS June 30, 2016 ASSETS BUSINESS-TYPE ACTIVITIES - ENTERPRISE FUNDS PARKING FACILITIES SEWER STORMWATER SYSTEM SYSTEM UTILITY Current assets:

CITY OF DES MOINES, IOWA STATEMENT OF NET POSITION PROPRIETARY FUNDS June 30, 2016 ASSETS BUSINESS-TYPE ACTIVITIES - ENTERPRISE FUNDS PARKING FACILITIES SEWER STORMWATER SYSTEM SYSTEM UTILITY Current assets:

Dr. Maddah ENMG 602 Intro. to Financial Eng g 11/04/09. Statement of Cash Flows (Chapter 4, Antle)

") Dr. Maddah ENMG 602 Intro. to Financial Eng g 11/04/09 Statement of Cash Flows (Chapter 4, Antle) Basic definitions Cash is readily transferable value. It is the most common way organizations acquire goods

Dr. Maddah ENMG 602 Intro. to Financial Eng g 11/04/09 Statement of Cash Flows (Chapter 4, Antle) Basic definitions Cash is readily transferable value. It is the most common way organizations acquire goods

Statement of Cash Flows Revisited

21 Statement of Cash Flows Revisited Overview There is not much that is new in this chapter. Rather, this chapter draws on what was learned in Chapter 5 and subsequent chapters with respect to the statement

21 Statement of Cash Flows Revisited Overview There is not much that is new in this chapter. Rather, this chapter draws on what was learned in Chapter 5 and subsequent chapters with respect to the statement

Statement of Cash Flows

Sri Lanka Accounting Standard - LKAS 7 Statement of Cash Flows LKAS 7 CONTENTS SRI LANKA ACCOUNTING STANDARD - LKAS 7 STATEMENT OF CASH FLOWS OBJECTIVE paragraphs SCOPE 1 BENEFITS OF CASH FLOW INFORMATION

Sri Lanka Accounting Standard - LKAS 7 Statement of Cash Flows LKAS 7 CONTENTS SRI LANKA ACCOUNTING STANDARD - LKAS 7 STATEMENT OF CASH FLOWS OBJECTIVE paragraphs SCOPE 1 BENEFITS OF CASH FLOW INFORMATION

02 1. The income statement is the major device for measuring the profitability of a firm over a period of time. True False 2. The income statement

02 1. The income statement is the major device for measuring the profitability of a firm over a period of time. 2. The income statement measures the increase in the assets of a firm over a period of time.

02 1. The income statement is the major device for measuring the profitability of a firm over a period of time. 2. The income statement measures the increase in the assets of a firm over a period of time.

UNAUDITED FINANCIAL INFORMATION. September 30, 2018

UNAUDITED FINANCIAL INFORMATION September 30, 2018 SCHEDULES OF NET POSITION September 30, 2018 ASSETS Current assets: Cash and cash equivalents $ 2,603 $ 11,289 $ 17,924 $ 24,687 $ 155,750 $ 212,253 Investments

UNAUDITED FINANCIAL INFORMATION September 30, 2018 SCHEDULES OF NET POSITION September 30, 2018 ASSETS Current assets: Cash and cash equivalents $ 2,603 $ 11,289 $ 17,924 $ 24,687 $ 155,750 $ 212,253 Investments

IOLKOS DEVELOPMENT ENTERTAINMENT S.A. 85 MESOGEION AVE., Athens, Greece General Commerce Reg. No SA Reg. No.

85 MESOGEION AVE., 11526 Athens, Greece General Commerce Reg. No. 59231 SA Reg. No. 57343/1/Β/4/47 TRANSLATED ABSTRACT OF ANNUAL FINANCIAL STATEMENTS 1 ST JANUARY TO 31 ST DECEMBER 217 STATEMENT OF FINANCIAL

85 MESOGEION AVE., 11526 Athens, Greece General Commerce Reg. No. 59231 SA Reg. No. 57343/1/Β/4/47 TRANSLATED ABSTRACT OF ANNUAL FINANCIAL STATEMENTS 1 ST JANUARY TO 31 ST DECEMBER 217 STATEMENT OF FINANCIAL

Chapter 3. Cash-Flow Statements

Introduction to Cash-Flow Statements 1 Chapter 3 Cash-Flow Statements TABLE OF CONTENTS Introduction 3 Direct Format Operating Section 5 Indirect Format Operating Section 6 Exercise 3.01 7 What Do I See?

Introduction to Cash-Flow Statements 1 Chapter 3 Cash-Flow Statements TABLE OF CONTENTS Introduction 3 Direct Format Operating Section 5 Indirect Format Operating Section 6 Exercise 3.01 7 What Do I See?

THE COMMISSIONERS OF LEONARDTOWN LEONARDTOWN, MARYLAND FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT. For the Year Ended June 30, 2018

LEONARDTOWN, MARYLAND FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT For the Year Ended Table of Contents Page Number INDEPENDENT AUDITORS REPORT 1-3 MANAGEMENT S DISCUSSION AND ANALYSIS 4-13 FINANCIAL

LEONARDTOWN, MARYLAND FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT For the Year Ended Table of Contents Page Number INDEPENDENT AUDITORS REPORT 1-3 MANAGEMENT S DISCUSSION AND ANALYSIS 4-13 FINANCIAL

Practice Multiple Choice Questions

FINAL EXAM REVIEW The comprehensive final exam consists of 50 questions, approximately 2/3 of which are from chapters 10 through 12. The remaining questions are from chapters 1 through 9. The questions

FINAL EXAM REVIEW The comprehensive final exam consists of 50 questions, approximately 2/3 of which are from chapters 10 through 12. The remaining questions are from chapters 1 through 9. The questions

Google Inc. CONSOLIDATED BALANCE SHEETS

Google Inc. CONSOLIDATED BALANCE SHEETS (In millions, except share and par value amounts which are reflected in thousands,and par value per share amounts) As of December 31, 2013 As of March 31, 2014 Assets

Google Inc. CONSOLIDATED BALANCE SHEETS (In millions, except share and par value amounts which are reflected in thousands,and par value per share amounts) As of December 31, 2013 As of March 31, 2014 Assets

Statement of Cash Flows

International Accounting Standard 7 Statement of Cash Flows This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 7 Cash Flow Statements was issued by the International

International Accounting Standard 7 Statement of Cash Flows This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 7 Cash Flow Statements was issued by the International

Understand Financial Statements and Identify Sources of Farm Financial Risk

Agricultural Finance Understand Financial Statements and Identify Sources of Farm Financial Risk By analyzing a complete set of your farm s financial statements you can identify sources and amounts of

Agricultural Finance Understand Financial Statements and Identify Sources of Farm Financial Risk By analyzing a complete set of your farm s financial statements you can identify sources and amounts of

Novelis Inc. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (unaudited) (in millions)

(in millions)") Novelis Inc. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (unaudited) (in millions) Three Months Ended March 31, Net sales $ 2,621 $ 2,402 $ 9,591 $ 9,872 Cost of goods sold (exclusive of depreciation

Novelis Inc. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (unaudited) (in millions) Three Months Ended March 31, Net sales $ 2,621 $ 2,402 $ 9,591 $ 9,872 Cost of goods sold (exclusive of depreciation

This is How Is the Statement of Cash Flows Prepared and Used?, chapter 12 from the book Accounting for Managers (index.html) (v. 1.0).

(v. 1.0).") This is How Is the Statement of Cash Flows Prepared and Used?, chapter 12 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is How Is the Statement of Cash Flows Prepared and Used?, chapter 12 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

ORIGINAL PRONOUNCEMENTS

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED Statement of Financial Accounting Standards No. 104 Statement of Cash Flows Net Reporting of Certain Cash Receipts and Cash Payments

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED Statement of Financial Accounting Standards No. 104 Statement of Cash Flows Net Reporting of Certain Cash Receipts and Cash Payments

Powerchip Semiconductor Corporation and Subsidiaries

Powerchip Semiconductor Corporation and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2005 and Independent Accountants Review Report INDEPENDENT ACCOUNTANTS REVIEW REPORT

Powerchip Semiconductor Corporation and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2005 and Independent Accountants Review Report INDEPENDENT ACCOUNTANTS REVIEW REPORT

CHAPTER 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

CITY OF DES MOINES, IOWA STATEMENT OF NET POSITION PROPRIETARY FUNDS June 30, 2018

CITY OF DES MOINES, IOWA STATEMENT OF NET POSITION PROPRIETARY FUNDS June 30, 2018 ASSETS PARKING FACILITIES SEWER STORMWATER SYSTEM SYSTEM UTILITY Current assets: Unrestricted current assets: Cash and

CITY OF DES MOINES, IOWA STATEMENT OF NET POSITION PROPRIETARY FUNDS June 30, 2018 ASSETS PARKING FACILITIES SEWER STORMWATER SYSTEM SYSTEM UTILITY Current assets: Unrestricted current assets: Cash and

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 441: Financial Statement Analysis 1 Professor Qi Chen

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 441: Financial Statement Analysis 1 Professor Qi Chen Note on the Statement of Cash Flows I. Overview of the Statement of Cash Flows The Statement of

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 441: Financial Statement Analysis 1 Professor Qi Chen Note on the Statement of Cash Flows I. Overview of the Statement of Cash Flows The Statement of

Chapter 12 Question Review 1

Chapter 12 Question Review 1 Chapter 12 Questions Multiple Choice 1. Assume that Mango Corporation uses the indirect method to depict cash flows. Indicate where, if at all, land and building purchased

Chapter 12 Question Review 1 Chapter 12 Questions Multiple Choice 1. Assume that Mango Corporation uses the indirect method to depict cash flows. Indicate where, if at all, land and building purchased