Gateway NACM Credit Conference Presented by: Curtis Litchfield, CCE September 19, 2018

|

|

|

- Maurice Burns

- 5 years ago

- Views:

Transcription

1 Welcome

2 Gateway NACM Credit Conference Presented by: Curtis Litchfield, CCE September 19, 2018

3 Financial Statement Analysis Tools and Techniques Common-Size Financial Statements Key Financial Ratios Trend Analysis Structural Analysis Industry Comparisons Common Sense and Judgment

4

5 Financial Statement Analysis Two types of Balance Sheet and Income Statement Analysis Comparative (Horizontal) Comparative Common Size (Vertical) Why use these comparative types Facilitate internal or structural analysis Evaluate trends Make industry comparisons

6 Financial Statement Analysis Common Sizing Express each account on the Balance Sheet as a percentage of total assets Express each account on the Income Statement as a percentage of net sales

7 Financial Statement Analysis Comparative (Horizontal) Requires two consecutive periods of information Objective is to find and identify changes that have occurred over the accounting period This is done in absolute and relative change values Relative Change is done by taking change and divided it by the prior period amount to determine the percentage change

8 Financial Statement Analysis Comparative Common Size (Vertical) Requires only one time period Common Size means that every numerical item of the Balance Sheet and Income Statement is converted to represent a fraction part of Total Assets or Total Revenue/Sales Shows the relative magnitude and the relative importance of various accounts to the total You may do further analysis where you look at the fraction percentage within a subset like Current Assets and Current Liabilities

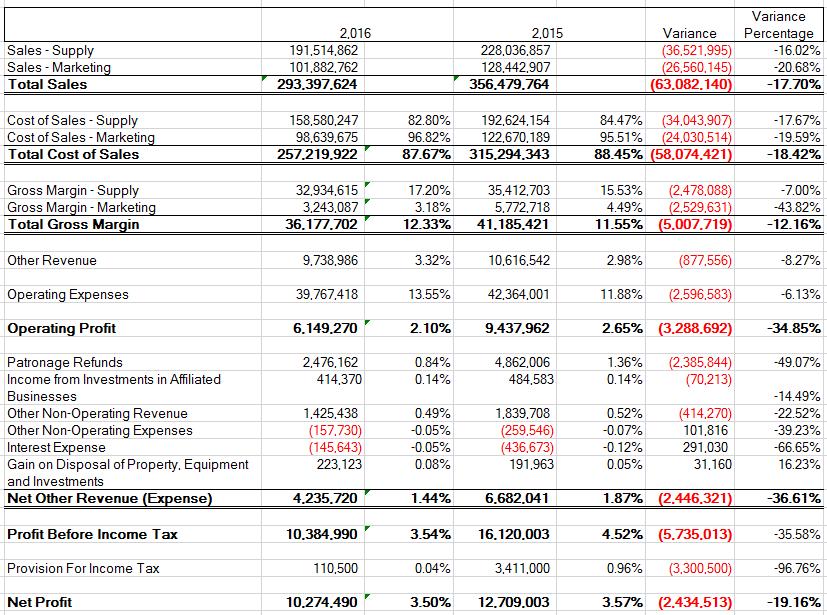

9 Financial Statement Analysis Key Link between Income Statement and Balance Sheet Beginning Retained Earnings [plus/minus] Net Income (loss) [minus] Dividends [equals] Ending Retained Earnings Beginning Retained Earnings 104,043,978 Net Income 10,274,490 Ending Retained Earnings 114,318,468 Why? Retained Earnings Show 111,408,375 Difference 2,910,093

10 Financial Statement Analysis

11 Financial Statement Analysis Five categories of ratios Liquidity ratios Leverage ratios Profitability ratios Activity ratios Market ratios

12 Financial Statement Analysis Ratios are valuable analytical tools and serve as screening devices, but they Do not provide answers in and of themselves Are not predictive Should be used with other elements of financial analysis

13 Liquidity Ratios Measure of a company s ability to pay off debts as they come due Measure a firm s ability to meet cash needs as they arise

14 Liquidity ratios include: Current ratio Quick or acid-test ratio Cash flow liquidity ratio Average collection period Days inventory held Days payable outstanding Liquidity Ratios

15 Working Capital Liquidity Ratios Measures the absolute dollar amount that Current Assets exceed Current Liabilities Current Assets - Current Liabilities

16 Current Ratio Liquidity Ratios Measures the ability of a firm to meet debt requirements as they come due Least stringent liquidity ratio Current Assets Current Liabilities

17 Quick or Acid-Test Ratio Liquidity Ratios Measures ability to meet short-term cash needs more rigorously by eliminating inventory Current Assets - Inventory Current Liabilities

18 Liquidity Ratios

19 Leverage Ratios The use of debt is referred to as financial leverage Leverage ratios measure the extent of a firm s financing with debt relative to equity and its ability to cover interest and other fixed charges.

20 Leverage Ratios Leverage ratios include: Debt to equity Debt ratio Long-term debt to total capitalization Times interest earned Fixed charge coverage Cash flow adequacy

21 Debt to Equity Leverage Ratios Measures the riskiness of the firm s capital structure in terms of the relationship between the funds supplied by creditors (debt) and investors (equity) Total Liabilities Stockholder (Owner) Equity

22 Debt to Asset Ratio Leverage Ratios Considers the proportion of all assets that are financed with debt Total Liabilities Total Assets

23 Leverage Ratios Stockholder (Owner) Equity Measures how much of the business the owners own Total Equity Total Assets

24 Leverage Ratios 2,016 2,015 Variance Variance Percentage Curre nt Asse ts T o ta l Curre nt A s s e ts 76,802, % 75,167, % 1,634, % Pro p e rty a nd Eq uip me nt Land and Land Improvements 3,728, % 3,517, % 211, % Buildings 34,776, % 34,434, % 341, % Equipment 62,453, % 57,322, % 5,131, % Construction In Progress 57, % 110, % (53,557) % 101,016, % 95,384, % 5,631, % Less: Accumulated Depreciation (72,996,451) % (68,822,260) % (4,174,191) 6.07% Net Pro p e rty a nd Eq uip me nt 28,019, % 26,562, % 1,456, % Inve stme nts a nd Othe r Asse ts Investment in Cooperatives 24,173, % 24,744, % (570,917) -2.31% Investment in LLC's 4,399, % 3,992, % 406, % Intangible Assets % 10, % (10,389) % Note Receivables 160, % 76, % 83, % Account Receivables 926, % 1,223, % (296,715) % T o ta l Othe r A s s e ts 29,659, % 30,046, % (387,233) -1.29% T o ta l A s s e ts 134,481, % 131,777, % 2,704, % Curre nt Lia b ilitie s T o ta l Curre nt Lia b ilitie s 25,018, % 28,511, % (3,493,731) % Lo ng T e rm Lia b ilitie s Other Long Term Liabilities 146, % 232, % (85,920) % Pension Obligations 9,837, % 9,035, % 801, % Deferred federal Income Taxes 952, % 715, % 236, % T o ta l Lo ng T e rm Lia b ilitie s 10,935, % 9,983, % 952, % T o ta l Lia b ilitie s 35,953, % 38,495, % (2,541,453) -6.60% Sha re ho ld e rs' a nd Pa tro ns' Eq uity Capital Stock 27, % 26, % % Patrons' Equity Credits % 1,096, % (1,096,128) % General Reserve 111,408, % 104,043, % 7,364, % Accumulated Other Comprehensive Loss (12,908,032) -9.60% (11,884,837) -9.02% (1,023,195) 8.61% T o ta l Sha re ho ld e rs' a nd Pa tro n Eq uity 98,527, % 93,281, % 5,245, % T o ta l Lia b ilitie s a nd E q uity 134,481, % 131,777, % 2,704, %

25 Leverage Ratios Leverage Ratios With Specific Investments Included Va ria nce 2,016 2,015 Va ria nce Pe rce nta g e T o ta l As s e ts 134,481, % 131,777, % 2,704, % T o ta l Lia b ilitie s 35,953, % 38,495, % (2,541,453) -6.60% T o ta l Sha re ho ld e rs' a nd Pa tro n Eq uity 98,527, % 93,281, % 5,245, % De b t to Eq uity 36.49% 41.27% De b t to Asse t 26.74% 29.21% Sto ckho ld e r (Owne r) Eq uity 73.26% 70.79% Leverage Ratios With Specific Investments Excluded 2,016 2,015 Va ria nce Va ria nce Pe rce nta g e T o ta l As s e ts 110,307, % 107,032, % 3,275, % T o ta l Lia b ilitie s 35,953, % 38,495, % (2,541,453) -6.60% T o ta l Sha re ho ld e rs' a nd Pa tro n Eq uity 74,354, % 68,537, % 5,816, % De b t to Eq uity 48.35% 56.17% De b t to Asse t 32.59% 35.97% Sto ckho ld e r (Owne r) Eq uity 67.41% 64.03%

26 Profitability Ratios Profitability ratios include: Gross Profit Margin Operating Profit Margin Net Profit Margin Cash Flow Margin Return on Total Assets (ROA) Return on Investment (ROI) Return on Equity (ROE) Cash Return on Assets

27 Profitability Ratios Gross Profit and Gross Profit Margin First step of profit measurement Difference between Net Sales and Cost of Good Sold (COGS) The relationship between Gross Profit and Net Sales is called Gross Profit Margin Measures ability of a company to control costs of inventories or manufacturing of products and to pass along price increases through sales to customers Change in the COGS percentage may be caused by changes in cost or changes in selling price

28 Profitability Ratios Gross Profit and Gross Profit Margin Gross profit margin remain relatively constant in stable industries and may change significantly in volatile industries Generally speaking, business try to maintain or increase Gross Profit and Gross Profit Margin Net Sales -Cost of Good Sold Gross Profit Gross Profit Net Sales

29 Profitability Ratios Operating Profit and Operating Profit Margin Second step of profit measurement Operating Profit is also referred to as EBIT The relationship between Operating Profit and Net Sales is called Operating Profit Margin Measures overall operating efficiency and incorporates all of the expenses associated with ordinary business activities

30 Profitability Ratios Operating Profit and Operating Profit Margin Provides a basis for assessing success of a business apart from financing and investing activities and separate from tax considerations Gross Profit - Operating Expenses Operating Profit Operating Profit Net Sales

31 Profitability Ratios Net Profit and Net Profit Margin Third step of profit measurement The relationship between Net Profit and Net Sales is called Net Profit Margin Net Profit Margin shows the percentage of profit earned on every sales dollar

32 Profitability Ratios Net Profit and Net Profit Margin Measures profitability after consideration of all revenue and expense, including interest, taxes, and non-operating items Operating Profit -Interest, taxes & etc Net Profit Net Income Net Sales

33 Profitability Ratios

34 Profitability Ratios Earnings Before Interest & Tax Referred to as EBIT Measures the profitability of a company without taking into account its cost of capital or tax implications. It is the difference between operating revenues and operating expenses. If the business does not have non-operating income, then operating income is sometimes referred to as EBIT or Operating Profit

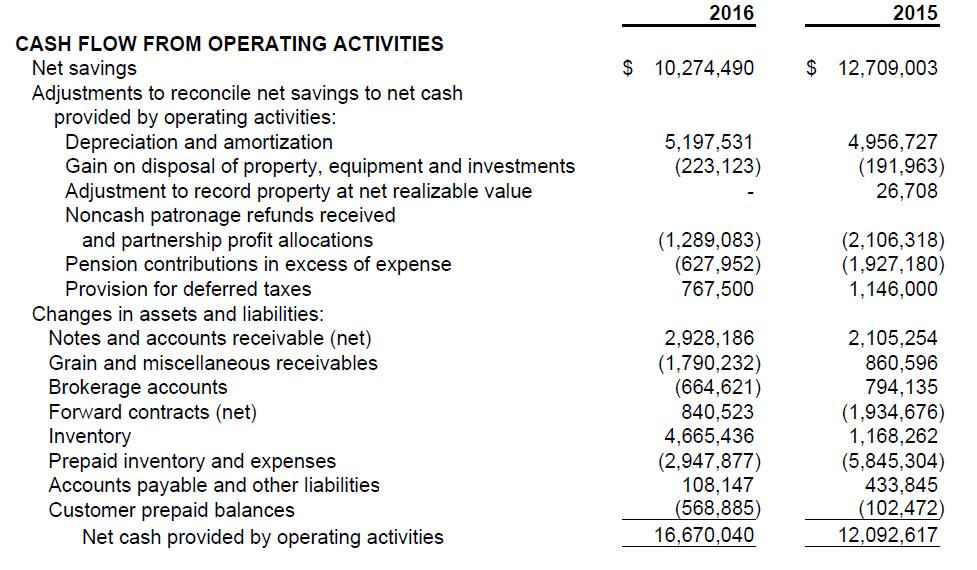

35 Cash Flow When analyzing the Statement of Cash Flow, one should consider Cash Flow from Operating Activities Fluctuation in Cash Flow from Operation over time Magnitude of positive or negative Cash Flow From Operation Understand the causes of the positive or negative Cash Flow from Operations Generating cash from operations is the preferred method for obtaining excess cash to finance capital expenditures and expansion repayment of debt payment of dividends

36 Cash Flow Success or failure of the business is in generating cash from operations Cash inflows Cash outflows The necessity of the outflow How are outflows financed Importance of internal cash generation and the implications for investing and financing activities when this does and does not occur

37 Cash Flow Generally, it is best to finance Short term assets with short-term debt Long term assets with long-term debt or issuance of stock Notes reveal future debt repayments and are useful in assessing how much cash will be needed in upcoming years to repay outstanding debt.

38 Cash Flow Cash Flow Margin Measures the firm's ability to translate sales into cash. The relationship between cash generated from operations and from sales is another measure of operating performance. Cash Flow Margin is cash profits generated internally from operations. Cash Flow Margin is not accrual accounting profits that a firm needs to service debt financing, pay dividends and invest in new capital assets.

39 Cash Flow Cash Flow Margin Cash Flow from Operating Activities Net Sales

40 Cash Flow

41 Cash Flow

42 Times Interest Earned Leverage Ratio Indicates how well operating earnings cover fixed interest expenses Operating Profit Interest Expense

43 Profitability Ratios Earning Before Interest, Taxes, Depreciation and Amortization Expense Referred to as EBITDA EBITDA is more likely to be used in the analysis of capital intensive firms or those amortizing large amounts of intangible assets. Otherwise, the depreciation and/or amortization expense can overwhelm their net earnings, giving the appearance of substantial losses A good metric to evaluate profitability, but not cash flow

44 Profitability Ratios Earning Before Interest, Taxes, Depreciation and Amortization Expense Simplest Formula Operating Profit Depreciation Expense Amortization Expense Literal Formula Net Profit Interest Taxes Amortization Expense Depreciation Expense

45 Cash Conversion Cycle Measures the operating cycle in days of a business that consists of: Purchasing or Manufacturing Inventory Some purchases on credit, thus the creation of accounts payable Selling inventory with some sales on credit, thus the creation of accounts receivable, and Collecting the Cash.

46 Cash Conversion Cycle The cash conversion cycle should be compared to the cash flow from operating activities to understand Why cash flow generation has improved or deteriorated by analyzing the key operating accounts on the balance sheet Inventory Accounts Receivable Accounts Payable

47 Cash Conversion Cycle The time period between the acquisition of goods and the final cash realization from sales Customer A Purchase Inventory Cash Sale To Customer Pay Supplier Customer B Purchase Material Produce Finished Product Sell To Customer On Credit Collect Amount Due From Customer Pay Supplier

48 Collect A/R DSO Cash Sales Cash Conversion Cycle Cash Inventory In Days + + Accounts Receivable In Accounts Receivable Days In Days - - Accounts Payable In Days Accounts Payable In Days Buy Inventory Pay A/P Sell Products Turn Inventory

49 Cash Conversion Cycle Rece iva b le s Sa le s / = Inve nto ry Co st o f Go o d s So ld / 360 = Op e ra ting Cycle - T he numb e r o f d a ys to co nve rt inve nto ry into sa le s p lus the numb e r o f d a ys it ta ke s to co lle ct AR Acco unts Pa ya b le s Co st o f Go o d s So ld / 360 = Ca sh Flo w Cycle

50 Financial Statement Analysis Questions Thank You

Introduction to Finance, Part 2: Cash Flow Statement & Financial Statement Analysis

1 Introduction to Finance, Part 2: Cash Flow Statement & Financial Statement Analysis CHRIS GASTON AND JENNIFER DEBOER Review & Roadmap Balance Sheet: a summary of a company s financial position at a specific

1 Introduction to Finance, Part 2: Cash Flow Statement & Financial Statement Analysis CHRIS GASTON AND JENNIFER DEBOER Review & Roadmap Balance Sheet: a summary of a company s financial position at a specific

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment Profitability Ratios Measure management's ability to control expenses and to earn a return on the resources committed

Professional Designation Ratios: Formulas & Definitions Used in Credit Risk Assessment Profitability Ratios Measure management's ability to control expenses and to earn a return on the resources committed

Financial Statement Analysis. Cash Flow Statement

Financial Statement Analysis Cash Flow Statement 1 The Articulation of the Financial Statements Beginning stocks Flows Ending stocks Cash Flow Statement Beginning Balance Sheet Cash Cash from operations

Financial Statement Analysis Cash Flow Statement 1 The Articulation of the Financial Statements Beginning stocks Flows Ending stocks Cash Flow Statement Beginning Balance Sheet Cash Cash from operations

Business Ratios. Current Ratio

Current Ratio Business Ratios Measures whether or not the firm has enough resources to pay its debt over the next 12 months formula: Current Ratio = Current Assets Current Liabilities Acceptable ratios

Current Ratio Business Ratios Measures whether or not the firm has enough resources to pay its debt over the next 12 months formula: Current Ratio = Current Assets Current Liabilities Acceptable ratios

CHAPTER 3. Topics in Chapter. Analysis of Financial Statements

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis DuPont equation Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis DuPont equation Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

Chapter 4. Funds-Flow Analysis and Forecasting. Overview of the Lecture. September The Statement of Cash Flows. Pro Forma Financial Statements

Chapter 4 Funds-Flow Analysis and Forecasting September 2004 Overview of the Lecture The Statement of Cash Flows Pro Forma Financial Statements 2 The Statement of Cash Flows The statement of cash flows

Chapter 4 Funds-Flow Analysis and Forecasting September 2004 Overview of the Lecture The Statement of Cash Flows Pro Forma Financial Statements 2 The Statement of Cash Flows The statement of cash flows

CMA 2010 Support Package

CMA 2010 Support Package Ratio Definitions CMA EXAM RATIO DEFINITIONS Abbreviations EBIT = Earnings before interest and taxes EBITDA = Earnings before interest, taxes, depreciation and amortization EBT

CMA 2010 Support Package Ratio Definitions CMA EXAM RATIO DEFINITIONS Abbreviations EBIT = Earnings before interest and taxes EBITDA = Earnings before interest, taxes, depreciation and amortization EBT

ANSWER SHEET EXAMINATION #2

ANSWER SHEET EXAMINATION #2 1) D 2) B 26) D 3) C 27) B 4) A 28) B 5) D 29) C 6) D 30) A 7) D 31) B 8) C 32) D 9) D 33) D 10) B 34) D 11) A 12) A 13) D 14) C 15) A 16) C 17) B 18) B 19) C 20) B 21) B 22)

ANSWER SHEET EXAMINATION #2 1) D 2) B 26) D 3) C 27) B 4) A 28) B 5) D 29) C 6) D 30) A 7) D 31) B 8) C 32) D 9) D 33) D 10) B 34) D 11) A 12) A 13) D 14) C 15) A 16) C 17) B 18) B 19) C 20) B 21) B 22)

Quarterly Performance Report

w e a l t h Quarterly Performance Report Client Name Executive Summary REVENUE Revenue (Last quarter $381,226) Positive trend upwards. PROFITABILITY Profitability Ratio 9.83% (Last quarter 30%) Negative

w e a l t h Quarterly Performance Report Client Name Executive Summary REVENUE Revenue (Last quarter $381,226) Positive trend upwards. PROFITABILITY Profitability Ratio 9.83% (Last quarter 30%) Negative

Wikipedia: "Financial Ratio" Contents. Sources of Data for Financial Ratios. Purpose and Types of Ratios

Wikipedia: "Financial Ratio" A financial ratio or accounting ratio is a relative magnitude of two selected numerical values taken from an enterprise's financial statements. Often used in accounting, there

Wikipedia: "Financial Ratio" A financial ratio or accounting ratio is a relative magnitude of two selected numerical values taken from an enterprise's financial statements. Often used in accounting, there

CHAPTER 3. Analysis of Financial Statements

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis Du Pont system Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

CHAPTER 3 Analysis of Financial Statements 1 Topics in Chapter Ratio analysis Du Pont system Effects of improving ratios Limitations of ratio analysis Qualitative factors 2 Determinants of Intrinsic Value:

Accounting Title 2014/3/ /12/ /3/31 Balance Sheet

Financial Statement Balance Sheet Accounting Title 2014/3/31 2013/12/31 2013/3/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 7,974,989 6,997,862 6,433,466

Financial Statement Balance Sheet Accounting Title 2014/3/31 2013/12/31 2013/3/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 7,974,989 6,997,862 6,433,466

Analysis and Interpretation of Financial Statements

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

ANALYSIS OF FINANCIAL STATEMENTS

ANALYSIS OF FINANCIAL STATEMENTS 1. Basic concept of financial statement analysis 2. Liquidity ratios 3. Asset management ratios 4. Debt management ratios 5. Profitability ratios 6. Market value ratios

ANALYSIS OF FINANCIAL STATEMENTS 1. Basic concept of financial statement analysis 2. Liquidity ratios 3. Asset management ratios 4. Debt management ratios 5. Profitability ratios 6. Market value ratios

Accounting Functions. The various financial statements are- Income Statement Balance Sheet

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

Chapter 3 Analysis of Financial Statements. Ratio Analysis Please refer to the attached financial statements, and industry average ratios

Chapter 3 Analysis of Financial Statements Ratio Analysis Please refer to the attached financial statements, and industry average ratios In this chapter, we will cover Liquidity ratios Asset management

Chapter 3 Analysis of Financial Statements Ratio Analysis Please refer to the attached financial statements, and industry average ratios In this chapter, we will cover Liquidity ratios Asset management

Corporate Finance, 3Ce (Berk, DeMarzo, Strangeland) Chapter 2 Introduction to Financial Statement Analysis

Chapter 2 Introduction to Financial Statement Analysis") Corporate Finance, 3Ce (Berk, DeMarzo, Strangeland) Chapter 2 Introduction to Financial Statement Analysis 2.1 The Disclosure of Financial Information 1) Canadian public companies are required to file

Corporate Finance, 3Ce (Berk, DeMarzo, Strangeland) Chapter 2 Introduction to Financial Statement Analysis 2.1 The Disclosure of Financial Information 1) Canadian public companies are required to file

BUSINESS FINANCE. Financial Statement Analysis. 1. Introduction to Financial Analysis. Copyright 2004 by Larry C. Holland

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

FINANCIAL RATIOS. LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS

You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS") FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous

Ratio Analysis Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous Ratio Analysis compares significant numbers from your financial statements. Rather than focusing on specific

Ratio Analysis Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous Ratio Analysis compares significant numbers from your financial statements. Rather than focusing on specific

n Financial Statement Analysis n Dollar and Percentage Changes n Common Sized Statements n Ratio Analysis McGraw-Hill /Irwin McGraw-Hill /Irwin

14-1 Today s Agenda Management Accounting Lecture 3 (Chapter 14) Financial Statement Analysis Bangor University Transfer Abroad Programme n Financial Statement Analysis n Dollar and Percentage Changes

14-1 Today s Agenda Management Accounting Lecture 3 (Chapter 14) Financial Statement Analysis Bangor University Transfer Abroad Programme n Financial Statement Analysis n Dollar and Percentage Changes

FEAR out. Taking the FEAR of Financial Statement Analysis. Toni Drake, CCE TRM Financial Services, Inc.

FEAR out Taking the FEAR of Financial Statement Analysis Toni Drake, CCE TRM Financial Services, Inc. FINANCIAL STATEMENTS Components of a Financial Statement Balance Sheet Income Statement Statement of

FEAR out Taking the FEAR of Financial Statement Analysis Toni Drake, CCE TRM Financial Services, Inc. FINANCIAL STATEMENTS Components of a Financial Statement Balance Sheet Income Statement Statement of

Ratio Analysis Part II

Chapter-04 Ratio Analysis Part II Ex: 1.1 Profitability Ratios Profitable Ratios are a class of financial metrics that are used to assess a business's ability to generate earnings as compared to its expenses

Chapter-04 Ratio Analysis Part II Ex: 1.1 Profitability Ratios Profitable Ratios are a class of financial metrics that are used to assess a business's ability to generate earnings as compared to its expenses

CFIN4 Chapter 2 Analysis of Financial Statements

1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always based on accounting data. Income statement 2. The balance

1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always based on accounting data. Income statement 2. The balance

CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS

CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS 1 Learning Outcomes LO.1 Describe the basic financial information that is produced by corporations and explain how the firm s stakeholders use such information.

CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS 1 Learning Outcomes LO.1 Describe the basic financial information that is produced by corporations and explain how the firm s stakeholders use such information.

How Well Am I Doing? Financial Statement Analysis

How Well Am I Doing? Financial Statement Analysis Chapter 16 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Limitations of Financial Statement Analysis Differences

How Well Am I Doing? Financial Statement Analysis Chapter 16 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Limitations of Financial Statement Analysis Differences

Financial Analysis. Consolidated financial analysis ( ) Based on IFRS

Based on IFRS") Financial Analysis Consolidated financial analysis (2012-2014) Based on IFRS 2012 2013 2014 Liability to asset ratio (%) 42.58 57.70 56.68 Long-term fund to PP&E ratio (%) 170.33 182.99 199.33 Current

Financial Analysis Consolidated financial analysis (2012-2014) Based on IFRS 2012 2013 2014 Liability to asset ratio (%) 42.58 57.70 56.68 Long-term fund to PP&E ratio (%) 170.33 182.99 199.33 Current

Foresters Whole Life Insurance STATEMENT OF POLICY COST AND BENEFIT INFORMATION. Life Insurance Illustration

Foresters Whole Life Insurance STATEMENT OF POLICY COST AND BENEFIT INFORMATION Life Insurance Illustration Pro p o sa l o n: Pre p a re d b y: adplus Femaleage45 DCAP Producer 11 Oval Dr Islandia, NY,

Foresters Whole Life Insurance STATEMENT OF POLICY COST AND BENEFIT INFORMATION Life Insurance Illustration Pro p o sa l o n: Pre p a re d b y: adplus Femaleage45 DCAP Producer 11 Oval Dr Islandia, NY,

Foresters Whole Life Insurance STATEMENT OF POLICY COST AND BENEFIT INFORMATION. Life Insurance Illustration

Foresters Whole Life Insurance STATEMENT OF POLICY COST AND BENEFIT INFORMATION Life Insurance Illustration Pro p o sa l o n: Pre p a re d b y: adplus Femaleage35 DCAP Producer 11 Oval Dr Islandia, NY,

Foresters Whole Life Insurance STATEMENT OF POLICY COST AND BENEFIT INFORMATION Life Insurance Illustration Pro p o sa l o n: Pre p a re d b y: adplus Femaleage35 DCAP Producer 11 Oval Dr Islandia, NY,

CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS

TRUE/FALSE CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS 1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always

TRUE/FALSE CHAPTER 2 ANALYSIS OF FINANCIAL STATEMENTS 1. The income statement measures the flow of funds into (i.e. revenue) and out of (i.e. expenses) the firm over a certain time period. It is always

Ratio Analysis. Assets = Liabilities + Shareholder s Equity

Ratio Analysis The purpose of a financial statement is to disclose information about the financial position of an entity to interested parties. By reporting the finances, shareholders are able to make

Ratio Analysis The purpose of a financial statement is to disclose information about the financial position of an entity to interested parties. By reporting the finances, shareholders are able to make

Working with Financial Statements

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Working with Financial Statements Lakehead University September 2004 Overview of the Lecture 3.1 Cash Flow and Financial Statements 3.2 Standardizes Financial Statements 3.3 Ratio Analysis 3.4 Dupont Identity

Financial Statements, Forecasts, and Planning Chapter 6

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 02 Analysis of Financial Statements

Chapter 02 Analysis of Financial Statements TRUEFALSE 1. The information contained in the annual report is used by investors to form expectations about future earnings and dividends. 2. Noncash assets

Chapter 02 Analysis of Financial Statements TRUEFALSE 1. The information contained in the annual report is used by investors to form expectations about future earnings and dividends. 2. Noncash assets

Rocco Sabino MBA, CPA

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

TOTAL TRAINING SOLUTIONS

TOTAL TRAINING SOLUTIONS RATIO ANALYSIS TO DETERMINE FINANCIAL STRENGTH Examining a Borrowers Five Vital Signs Jeffery W. Johnson Bankers Insight Group, LLC jeffery.johnson@bankers-insight.com October

TOTAL TRAINING SOLUTIONS RATIO ANALYSIS TO DETERMINE FINANCIAL STRENGTH Examining a Borrowers Five Vital Signs Jeffery W. Johnson Bankers Insight Group, LLC jeffery.johnson@bankers-insight.com October

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT Financial Statement Analysis The process of determining financial strengths and weaknesses of a firm by establishing strategic relationship between the items of the balance sheet,

FINANCIAL MANAGEMENT Financial Statement Analysis The process of determining financial strengths and weaknesses of a firm by establishing strategic relationship between the items of the balance sheet,

Performance Management

UNIVERSITY OF PAVIA Performance Management Chiara Demartini mariachiara.demartini@unipv.it Master in International Business and Economics 1 Lectures and Test Lectures: Tuesday hr. 11-13 Room 15 Wednesday

UNIVERSITY OF PAVIA Performance Management Chiara Demartini mariachiara.demartini@unipv.it Master in International Business and Economics 1 Lectures and Test Lectures: Tuesday hr. 11-13 Room 15 Wednesday

Financial Statement Analysis

Financial Statement Analysis Lakehead University September 2003 Overview of the Lecture 2.1 Financial Statements 2.2 Ratio Analysis 2.4 Common-Size Analysis 2.3 Changing Prices 2.5 International Considerations

Financial Statement Analysis Lakehead University September 2003 Overview of the Lecture 2.1 Financial Statements 2.2 Ratio Analysis 2.4 Common-Size Analysis 2.3 Changing Prices 2.5 International Considerations

CHAPTER 12 STATEMENT OF CASH FLOWS

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

Digging Into The Balance Sheet and Income Statement. The Balance Sheet

Digging Into The Balance Sheet and Income Statement Jim Menard, CCE email: jsmenard62@gmail.com The Balance Sheet Also called the statement of condition or statement of financial position Financial Condition

Digging Into The Balance Sheet and Income Statement Jim Menard, CCE email: jsmenard62@gmail.com The Balance Sheet Also called the statement of condition or statement of financial position Financial Condition

ACC 501 Quizzes Lecture 1 to 22

ACC501 Business Finance Composed By Faheem Saqib A mega File of MiD Term Solved MCQ For more Help Rep At Faheem_saqib2003@yahoocom Faheemsaqib2003@gmailcom 0334-6034849 ACC 501 Quizzes Lecture 1 to 22

ACC501 Business Finance Composed By Faheem Saqib A mega File of MiD Term Solved MCQ For more Help Rep At Faheem_saqib2003@yahoocom Faheemsaqib2003@gmailcom 0334-6034849 ACC 501 Quizzes Lecture 1 to 22

Performance Highlights. Prepared for. MEGALO Hospitality. CLIENT Restaurant Client. Period. Jun Created on 10th June 2017

Performance Highlights Prepared for CLIENT Restaurant Client Period Jun 2017 Created on 10th June 2017 Executive Summary OBSERVATIONS Comparing Jun 2017 with the same month last year Jun 2016. REVENUE

Performance Highlights Prepared for CLIENT Restaurant Client Period Jun 2017 Created on 10th June 2017 Executive Summary OBSERVATIONS Comparing Jun 2017 with the same month last year Jun 2016. REVENUE

Chapter 2 Financial Statement and Cash Flow Analysis

Chapter 2 Financial Statement and Cash Flow Analysis MULTIPLE CHOICE 1. Which of the following items can be found on an income statement? a. Accounts receivable b. Long-term debt c. Sales d. Inventory

Chapter 2 Financial Statement and Cash Flow Analysis MULTIPLE CHOICE 1. Which of the following items can be found on an income statement? a. Accounts receivable b. Long-term debt c. Sales d. Inventory

Self-Employed Income ON DEMAND. Liquidity Quiz

Self-Employed Income ON DEMAND 1. What is the definition of Liquidity? A. The ability to convert inventory into cash B. The ability of a company to sell its assets C. The ability of a company to meet its

Self-Employed Income ON DEMAND 1. What is the definition of Liquidity? A. The ability to convert inventory into cash B. The ability of a company to sell its assets C. The ability of a company to meet its

Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international financial statements.

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis Answers to End of Chapter Questions 2-1. Financial statement analysis provides information about the company s financial health, and its

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis Answers to End of Chapter Questions 2-1. Financial statement analysis provides information about the company s financial health, and its

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS. Note on Financial Statements and Financial Ratios

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Financial Statements and Financial Ratios I. Review of Financial Statements The Balance Sheet Financial

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Financial Statements and Financial Ratios I. Review of Financial Statements The Balance Sheet Financial

Session 2, Sunday, April 2nd (1:30-5:00) v Association for Financial Professionals. All rights reserved. Session 3-1

v Association for Financial Professionals. All rights reserved. Session 3-1") Session 2, Sunday, April 2nd (1:30-5:00) v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter

Session 2, Sunday, April 2nd (1:30-5:00) v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter

Chapter 2. Learning Objectives. Topics Covered. Cash Flow and Financial Statement Analysis

Chapter 2 Cash Flow and Financial Statement Analysis Learning Objectives Interpret information contained in the balance sheet, income statement, and statement of cash flows. Explain why income differs

Chapter 2 Cash Flow and Financial Statement Analysis Learning Objectives Interpret information contained in the balance sheet, income statement, and statement of cash flows. Explain why income differs

FUNDAMENTALS OF HEALTHCARE FINANCE. Online Appendix B. Financial Analysis Ratios

FUNDAMENTALS OF HEALTHCARE FINANCE Online Appendix B Financial Analysis Ratios INTRODUCTION In Chapter 13, we indicated that financial ratio analysis is a technique commonly used to help assess a business

FUNDAMENTALS OF HEALTHCARE FINANCE Online Appendix B Financial Analysis Ratios INTRODUCTION In Chapter 13, we indicated that financial ratio analysis is a technique commonly used to help assess a business

Financial Analysis. Instructor: Michael Booth Cabrillo College

Financial Analysis Instructor: Michael Booth Cabrillo College Factors in Communicating Useful Information The primary objective of accounting is to provide information useful for decision making. To provide

Financial Analysis Instructor: Michael Booth Cabrillo College Factors in Communicating Useful Information The primary objective of accounting is to provide information useful for decision making. To provide

Strategic Management - The Competitive Edge. Prof. R. Srinivasan. Department of Management Studies. Indian Institute of Science, Bangalore

Strategic Management - The Competitive Edge Prof. R. Srinivasan Department of Management Studies Indian Institute of Science, Bangalore Module No. # 04 Lecture No. # 18 Key Financial Ratios Welcome to

Strategic Management - The Competitive Edge Prof. R. Srinivasan Department of Management Studies Indian Institute of Science, Bangalore Module No. # 04 Lecture No. # 18 Key Financial Ratios Welcome to

Lecture 4. Interpreting and using financial statements for valuation II. Financial ratio analysis

Lecture 4 Interpreting and using financial statements for valuation II Financial ratio analysis Agenda Use of financial ratios ROE decomposition Growth, risk, and, cash flow 2 What are financial ratios

Lecture 4 Interpreting and using financial statements for valuation II Financial ratio analysis Agenda Use of financial ratios ROE decomposition Growth, risk, and, cash flow 2 What are financial ratios

MODULE III RATIO ANALYSIS. Dr. Manoj Shah, Principal Investigator, NMEICT, MHRD Delhi

MODULE III UNIT - II RATIO ANALYSIS Topics to be Enlightened Introduction and Meaning Interpretation of Ratio Usefulness of Ratio Analysis Limitations of Ratio Analysis Classification of Ratio Analysis

MODULE III UNIT - II RATIO ANALYSIS Topics to be Enlightened Introduction and Meaning Interpretation of Ratio Usefulness of Ratio Analysis Limitations of Ratio Analysis Classification of Ratio Analysis

Key Operational and Financial Data

Key Operational and Financial Data Operations Summary Tons Production 217,370 209,524 195,906 134,272 127,384 70,916 Sales 217,043 214,316 181,259 138,923 126,129 64,912 Summary of Statement of Profit

Key Operational and Financial Data Operations Summary Tons Production 217,370 209,524 195,906 134,272 127,384 70,916 Sales 217,043 214,316 181,259 138,923 126,129 64,912 Summary of Statement of Profit

Get Global: Global Cash Flow Analysis

Get Global: Global Cash Flow Analysis Total Training Solutions Bankers Insight Group CASH FLOW NET PROFITS DON T REPAY LOANS What will the customer do with the loan proceeds? How much will your customer

Get Global: Global Cash Flow Analysis Total Training Solutions Bankers Insight Group CASH FLOW NET PROFITS DON T REPAY LOANS What will the customer do with the loan proceeds? How much will your customer

Dynamic 2018 Q3 IFRS Consolidated Financial Statements

Dynamic 2018 Q3 IFRS Consolidated Financial Statements Unit: NT$ thousand Accounting Title 2018/09/30 2017/12/31 2017/09/30 Balance Sheet Assets Current assets Cash and cash equivalents 1,096,797 1,350,015

Dynamic 2018 Q3 IFRS Consolidated Financial Statements Unit: NT$ thousand Accounting Title 2018/09/30 2017/12/31 2017/09/30 Balance Sheet Assets Current assets Cash and cash equivalents 1,096,797 1,350,015

Talking Accounting Definitions

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Analysis write-up at: GOOGLE INC. (GOOG) #2 SUSTAINABLE REVENUE GROWTH

#2 SUSTAINABLE REVENUE GROWTH") GOOGLE INC. (GOOG) NOMINAL REVENUE 35.00% 3 25.00% 2 15.00% 1 5.00% #1 REAL REVENUE PRICE ADJUSTED REVENUE 29.7% 28.3% 23.8% 6.7% #4 OPERATING EXPENSE CONTROL NOI$ GP$ NOI% GP% CORE OPER EXP% 8 $30,000,000

GOOGLE INC. (GOOG) NOMINAL REVENUE 35.00% 3 25.00% 2 15.00% 1 5.00% #1 REAL REVENUE PRICE ADJUSTED REVENUE 29.7% 28.3% 23.8% 6.7% #4 OPERATING EXPENSE CONTROL NOI$ GP$ NOI% GP% CORE OPER EXP% 8 $30,000,000

financial Analysis Annual Report

financial Analysis Annual Report 217 87 DuPont Analysis Increase in sales volume by 16% coupled with increasing price trend during the year resulted in higher sales and profits due to which EBIT margin

financial Analysis Annual Report 217 87 DuPont Analysis Increase in sales volume by 16% coupled with increasing price trend during the year resulted in higher sales and profits due to which EBIT margin

All In One MGT201 Mid Term Papers More Than (10) BY

BY") All In One MGT201 Mid Term Papers More Than (10) BY http://www.vustudents.net MIDTERM EXAMINATION MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Why companies

All In One MGT201 Mid Term Papers More Than (10) BY http://www.vustudents.net MIDTERM EXAMINATION MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Why companies

Chapter 2. Learning Objectives. Topics Covered. Financial Statement and Cash Flow Analysis

Chapter 2 Financial Statement and Cash Flow Analysis 1 Learning Objectives Interpret information contained in the balance sheet, income statement, and statement of cash flows. Explain why income differs

Chapter 2 Financial Statement and Cash Flow Analysis 1 Learning Objectives Interpret information contained in the balance sheet, income statement, and statement of cash flows. Explain why income differs

st IFRS Consolidated Financial Statements

2461 2018 1st IFRS Consolidated Financial Statements Balance Sheet Balance Sheet Unit: NT$ thousand Accounting Title 2018/03/31 2017/12/31 2017/03/31 Assets Current assets Cash and cash equivalents 1,552,283

2461 2018 1st IFRS Consolidated Financial Statements Balance Sheet Balance Sheet Unit: NT$ thousand Accounting Title 2018/03/31 2017/12/31 2017/03/31 Assets Current assets Cash and cash equivalents 1,552,283

Role of Financial Manager. Assessing Financial Performance. Analysis of Financial Statements. To create value, the financial manager should:

Role of Financial Manager To create value, the financial manager should: 1. Make sound investment decisions. 2. Make sound financing decisions. Importance of Assessing Financial Performance Assessing Financial

Role of Financial Manager To create value, the financial manager should: 1. Make sound investment decisions. 2. Make sound financing decisions. Importance of Assessing Financial Performance Assessing Financial

2016/2/25 Financial Statement Balance Sheet

2016/2/25 Financial Statement Balance Sheet Financial Statement Balance Sheet Accounting Title 2015/12/31 2014/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents

2016/2/25 Financial Statement Balance Sheet Financial Statement Balance Sheet Accounting Title 2015/12/31 2014/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay. Lecture - 14 Ratio Analysis

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 14 Ratio Analysis Dear students, in our last session we are started the

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 14 Ratio Analysis Dear students, in our last session we are started the

AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00)

") AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00) Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter 7 Ratio Analysis: Part I, Domain

AFP Financial Planning & Analysis Learning System Session 2, Sunday, April 2nd (1:30-5:00) Chapters Covered Financial Accounting and Reporting: Part I, Domain B Chapter 7 Ratio Analysis: Part I, Domain

Accounting Title 2017/03/ /12/ /03/31 Balance Sheet

1 / 2 Accounting Title 2017/03/31 2016/12/31 2016/03/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,248,992 946,626 1,294,532 Current financial assets

1 / 2 Accounting Title 2017/03/31 2016/12/31 2016/03/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,248,992 946,626 1,294,532 Current financial assets

th IFRS Consolidated Financial Statements

2461 2017 4th IFRS Consolidated Financial Statements Balance Sheet Balance Sheet Unit: NT$ thousand Accounting Title 2017/12/31 2016/12/31 Assets Current assets Cash and cash equivalents Total cash and

2461 2017 4th IFRS Consolidated Financial Statements Balance Sheet Balance Sheet Unit: NT$ thousand Accounting Title 2017/12/31 2016/12/31 Assets Current assets Cash and cash equivalents Total cash and

Effective cash forecasting within reach: Techniques and best practices

Effective cash forecasting within reach: Techniques and best practices Micki Burciaga, VP, Product Manager Wells Fargo Bank March 12th, 2014 2014 Wells Fargo Bank, N.A. All rights reserved. Member FDIC.

Effective cash forecasting within reach: Techniques and best practices Micki Burciaga, VP, Product Manager Wells Fargo Bank March 12th, 2014 2014 Wells Fargo Bank, N.A. All rights reserved. Member FDIC.

Week-2 FINC Analysis of Financial Statements. Balance Sheets

Dr. Ahmed FINC 5000 Week-2 Name Analysis of Financial Statements Balance Sheets Assets 2003 2004 2005e Cash $ 9,000 $ 7,282 $ 14,000 Short-Term Investments. 48,600 20,000 71,632 Accounts Receivable 351,200

Dr. Ahmed FINC 5000 Week-2 Name Analysis of Financial Statements Balance Sheets Assets 2003 2004 2005e Cash $ 9,000 $ 7,282 $ 14,000 Short-Term Investments. 48,600 20,000 71,632 Accounts Receivable 351,200

ENGINEERING FIRM #2 SUSTAINABLE REVENUE GROWTH PRICE ADJ REV SUSTAINABLE REV NOMINAL REV

25.00% 22.50% 2 17.50% 15.00% 12.50% 1 7.50% 5.00% 2.50% 2 15.00% 1 5.00% #1 REAL REVENUE NOMINAL REVENUE PRICE ADJUSTED REVENUE $2,500,000 () () #4 OPERATING EXPENSE CONTROL NOI$ GP$ NOI% GP% CORE OPER

25.00% 22.50% 2 17.50% 15.00% 12.50% 1 7.50% 5.00% 2.50% 2 15.00% 1 5.00% #1 REAL REVENUE NOMINAL REVENUE PRICE ADJUSTED REVENUE $2,500,000 () () #4 OPERATING EXPENSE CONTROL NOI$ GP$ NOI% GP% CORE OPER

condition & operating results in a condensed form. Financial statements are used as a

2.1 FINANCIAL ANALYSIS Financial statements are formal records of the financial activities of a business, person or other entity and provide an overview of a business or person s financial condition in

2.1 FINANCIAL ANALYSIS Financial statements are formal records of the financial activities of a business, person or other entity and provide an overview of a business or person s financial condition in

RATIO ANALYSIS. The preceding chapters concentrated on developing a general but solid understanding

C H A P T E R 4 RATIO ANALYSIS I N T R O D U C T I O N The preceding chapters concentrated on developing a general but solid understanding of accounting principles and concepts and their applications to

C H A P T E R 4 RATIO ANALYSIS I N T R O D U C T I O N The preceding chapters concentrated on developing a general but solid understanding of accounting principles and concepts and their applications to

FINANCIAL STATEMENT ANALYSIS-INTERPRETING THE NUMBERS CORRECTLY! Presented by: Osburn & Associates, LLC

FINANCIAL STATEMENT ANALYSIS-INTERPRETING THE NUMBERS CORRECTLY! Presented by: Osburn & Associates, LLC Author/ Instructor DAVID L. OSBURN, MBA, CCRA David Osburn is the founder of Osburn & Associates,

FINANCIAL STATEMENT ANALYSIS-INTERPRETING THE NUMBERS CORRECTLY! Presented by: Osburn & Associates, LLC Author/ Instructor DAVID L. OSBURN, MBA, CCRA David Osburn is the founder of Osburn & Associates,

Chapter 1: Comparable Companies Analysis

Chapter 1: Comparable Companies Analysis 1) All of the following are reasons why comparable companies analysis should be used in conjunction with other valuation methodologies EXCEPT: I. Markets may be

Chapter 1: Comparable Companies Analysis 1) All of the following are reasons why comparable companies analysis should be used in conjunction with other valuation methodologies EXCEPT: I. Markets may be

TOTAL TRAINING SOLUTIONS

TOTAL TRAINING SOLUTIONS Global Cash Flow Analysis Get Global by Understanding Global Cash Flow Jeffery W. Johnson Bankers Insight Group jeffery.johnson@bankers-insight.com 770-846-4511 September 2015

TOTAL TRAINING SOLUTIONS Global Cash Flow Analysis Get Global by Understanding Global Cash Flow Jeffery W. Johnson Bankers Insight Group jeffery.johnson@bankers-insight.com 770-846-4511 September 2015

FAQ: Financial Ratio Analysis

Question 1: What is horizontal analysis of financial statement data? Answer 1: Horizontal analysis is a method of financial ratio analysis. Horizontal analysis is comparing each item on the financial statements

Question 1: What is horizontal analysis of financial statement data? Answer 1: Horizontal analysis is a method of financial ratio analysis. Horizontal analysis is comparing each item on the financial statements

RATIO ANALYSIS. Inventories + Debtors + Cash & Bank + Receivables / Accruals + Short terms Loans + Marketable Investments

A. LIQUIDITY RATIOS - Short Term Solvency RATIO ANALYSIS Ratio Formula Numerator Denominator Significance/Indicator 1. Current Ratio Current Assets Current Liabilities Inventories + Debtors + Cash & Bank

A. LIQUIDITY RATIOS - Short Term Solvency RATIO ANALYSIS Ratio Formula Numerator Denominator Significance/Indicator 1. Current Ratio Current Assets Current Liabilities Inventories + Debtors + Cash & Bank

5 1. CONSOLIDATED INCOME STATEMENTS (in millions of euros) 2018 2017* REVENUE 2,643 2,505 Cost of sales (1,649) (1,471) GROSS PROFIT 995 1,034 Distribution and marketing costs (250) (224) Research

5 1. CONSOLIDATED INCOME STATEMENTS (in millions of euros) 2018 2017* REVENUE 2,643 2,505 Cost of sales (1,649) (1,471) GROSS PROFIT 995 1,034 Distribution and marketing costs (250) (224) Research

CHAPTER 12 Financial Planning and Forecasting Financial Statements

12-1 CHAPTER 12 Financial Planning and Forecasting Financial Statements Financial planning Additional Funds Needed (AFN) formula Pro forma financial statements Sales forecasts Percent of sales method Financial

12-1 CHAPTER 12 Financial Planning and Forecasting Financial Statements Financial planning Additional Funds Needed (AFN) formula Pro forma financial statements Sales forecasts Percent of sales method Financial

UNDERSTANDING FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS. Chapter 3

1 UNDERSTANDING FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS Chapter 3 2 Learning Objectives (1 of 2) 1. Describe the content of the four basic financial statements and discuss the importance of financial

1 UNDERSTANDING FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS Chapter 3 2 Learning Objectives (1 of 2) 1. Describe the content of the four basic financial statements and discuss the importance of financial

2/2/2009. Financial statement EARNING POWER AND IRREGULAR ITEMS. EARNING POWER AND IRREGULAR ITEMS continued. Chapter 14

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Corporate Accounting Recitation 3. June 18, 2004

15.511 Corporate Accounting Recitation 3 June 18, 2004 Why do we need CF/S? Accrual accounting is often based upon subjective judgments that can introduce measurement error and uncertainty into the reported

15.511 Corporate Accounting Recitation 3 June 18, 2004 Why do we need CF/S? Accrual accounting is often based upon subjective judgments that can introduce measurement error and uncertainty into the reported

Unappropriated retained earnings (accumulated deficit) Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear

Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear") Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

Chapter 02 Evaluating Financial Performance

Chapter 02 Evaluating Financial Performance Multiple Choice Questions 1. The most popular yardstick of financial performance among investors and senior managers is the: A. profit margin. B. return on equity.

Chapter 02 Evaluating Financial Performance Multiple Choice Questions 1. The most popular yardstick of financial performance among investors and senior managers is the: A. profit margin. B. return on equity.

Ratio Analysis. CA Past Years Exam Question

Ratio Analysis CA Past Years Exam Question Question : 1 Nov, 2009 From the Following Information, Calculate the Amount of Fixed Assets & Proprietors Funds. 1. Ratio of Fixed Assets to Proprietors Funds

Ratio Analysis CA Past Years Exam Question Question : 1 Nov, 2009 From the Following Information, Calculate the Amount of Fixed Assets & Proprietors Funds. 1. Ratio of Fixed Assets to Proprietors Funds

A Simple Model. Introduction to Financial Statements

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Financial Statement Balance Sheet

Financial Statement Balance Sheet Page 1 of 1 Financial Statement Balance Sheet Accounting Title 2014/09/30 2013/12/31 2013/09/30 Balance Sheet Assets Current assets Cash and cash equivalents Total cash

Financial Statement Balance Sheet Page 1 of 1 Financial Statement Balance Sheet Accounting Title 2014/09/30 2013/12/31 2013/09/30 Balance Sheet Assets Current assets Cash and cash equivalents Total cash

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

Analysis of Financial Statements

Question 1: What are the key elements in the primary financial statements that are used by executives for firm analysis? The three key financial statements that business executives and financial analysts

Question 1: What are the key elements in the primary financial statements that are used by executives for firm analysis? The three key financial statements that business executives and financial analysts

BEYOND FINANCIAL STATEMENTS

BEYOND FINANCIAL STATEMENTS Prepared by: Rashied Small, Lucinda Smidt & Yaeesh Yassen National CPD Seminar September 2016 CPD SEminar - Beyond Financial Statements 1 CPD SEminar - Beyond Financial Statements

BEYOND FINANCIAL STATEMENTS Prepared by: Rashied Small, Lucinda Smidt & Yaeesh Yassen National CPD Seminar September 2016 CPD SEminar - Beyond Financial Statements 1 CPD SEminar - Beyond Financial Statements

Free Cash Flow Was $280.5 Million For Fiscal 2013

LIONSGATE REPORTS FISCAL 2013 REVENUE OF $2.71 BILLION, ADJUSTED EBITDA OF $329.7 MILLION, NET INCOME OF $232.1 MILLION OR $1.73 BASIC EPS AND ADJUSTED NET INCOME OF $190.1MILLION OR $1.41 ADJUSTED BASIC

LIONSGATE REPORTS FISCAL 2013 REVENUE OF $2.71 BILLION, ADJUSTED EBITDA OF $329.7 MILLION, NET INCOME OF $232.1 MILLION OR $1.73 BASIC EPS AND ADJUSTED NET INCOME OF $190.1MILLION OR $1.41 ADJUSTED BASIC

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

REVIEW OF BASIC UNDERSTANDING AND ANALYSIS OF FINANCIAL STATEMENTS

REVIEW OF BASIC UNDERSTANDING AND ANALYSIS OF FINANCIAL STATEMENTS Payear Sangiumvibool, Ph.D., CPA (US) ดร. พเย ย เสง ยมว บ ล Webster University Thailand Faculty, Accounting and Management สภาว ชาช พบ

REVIEW OF BASIC UNDERSTANDING AND ANALYSIS OF FINANCIAL STATEMENTS Payear Sangiumvibool, Ph.D., CPA (US) ดร. พเย ย เสง ยมว บ ล Webster University Thailand Faculty, Accounting and Management สภาว ชาช พบ

Q U E S T I O N S B A S E D O N F I N A N C I A L M A N A G E M E N T

Q U E S T I O N S B A S E D O N F I N A N C I A L M A N A G E M E N T 1) The Yield to Maturity of a bond is the same as: a) The present value of the bond b) The bonds internal rate of return c) The future

Q U E S T I O N S B A S E D O N F I N A N C I A L M A N A G E M E N T 1) The Yield to Maturity of a bond is the same as: a) The present value of the bond b) The bonds internal rate of return c) The future