Lecture 4: From capital/income ratios to capital shares

|

|

|

- Amos Owen

- 5 years ago

- Views:

Transcription

1 Economics of Inequality (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year Lecture 4: From capital/income ratios to capital shares (Tuesday October 14 th 2014) (check on line for updated versions)

2 Capital-income ratios β vs. capital shares α Capital/income ratio β=k/y Capital share α = Y K /Y with Y K = capital income (=sum of rent, dividends, interest, profits, etc.: i.e. all incomes going to the owners of capital, independently of any labor input) I.e. β = ratio between capital stock and income flow While α = share of capital income in total income flow By definition: α = r x β With r = Y K /K = average real rate of return to capital If β=600% and r=5%, then α = 30% = typical values

3 In practice, the average rate of return to capital r (typically r 4-5%) varies a lot across assets and over individuals (more on this in Lecture 6) Typically, rental return on housing = 3-4% (i.e. the rental value of an appartment worth is generally about /year) (+ capital gain or loss) Return on stock market (dividend + k gain) = as much as 6-7% in the long run Return on bank accounts or cash = as little as 1-2% (but only a small fraction of total wealth) Average return across all assets and individuals 4-5%

4 The Cobb-Douglas production function Cobb-Douglas production function: Y = F(K,L) = K α L 1-α With perfect competition, wage rate v = marginal product of labor, rate of return r = marginal product of capital: r = F K = α K α-1 L 1-α and v = F L = (1-α) K α L -α Therefore capital income Y K = r K = α Y & labor income Y L = v L = (1-α) Y I.e. capital & labor shares are entirely set by technology (say, α=30%, 1-α=70%) and do not depend on quantities K, L Intuition: Cobb-Douglas elasticity of substitution between K & L is exactly equal to 1 I.e. if v/r rises by 1%, K/L=α/(1-α) v/r also rises by 1%. So the quantity response exactly offsets the change in prices: if wages by 1%, then firms use 1% less labor, so that labor share in total output remains the same as before

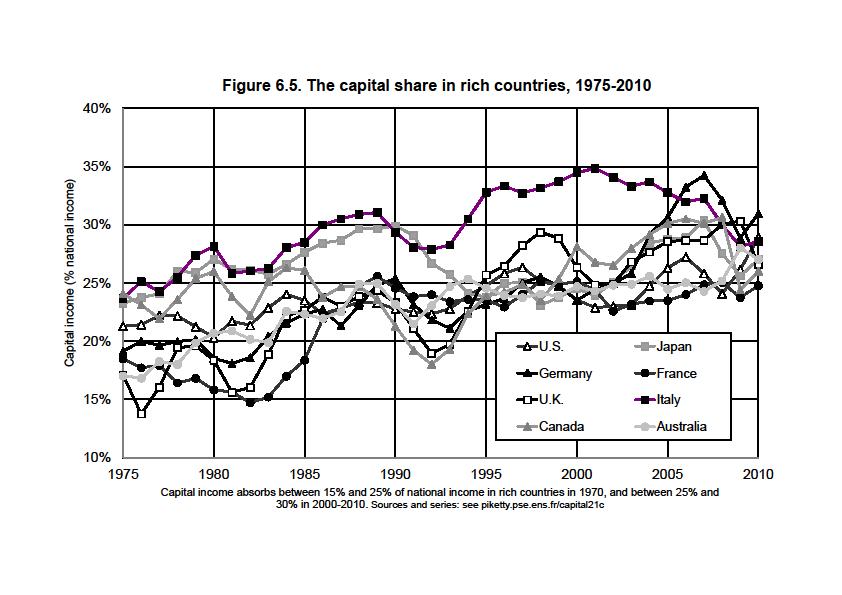

5 The limits of Cobb-Douglas Economists like Cobb-Douglas production function, because stable capital shares are approximately stable However it is only an approximation: in practice, capital shares α vary in the 20-40% range over time and between countries (or even sometime in the 10-50% range) In 19c, capital shares were closer to 40%; in 20c, they were closer to 20-30%; structural rise of human capital (i.e. exponent α in Cobb-Douglas production function Y = K α L 1-α?), or purely temporary phenomenon? Over period, capital shares have increased from 15-25% to 25-30% in rich countries : very difficult to explain with Cobb-Douglas framework

6

7

8

9 The CES production function CES = a simple way to think about changing capital shares CES : Y = F(K,L) = [a K (σ-1)/σ + b L (σ-1)/σ ] σ/(σ-1) with a, b = constant σ = constant elasticity of substitution between K and L σ : linear production function Y = r K + v L (infinite substitution: machines can replace workers and vice versa, so that the returns to capital and labor do not fall at all when the quantity of capital or labor rise) ( = robot economy) σ 0: F(K,L)=min(rK,vL) (fixed coefficients) = no substitution possibility: one needs exactly one machine per worker σ 1: converges toward Cobb-Douglas; but all intermediate cases are also possible: Cobb-Douglas is just one possibility among many Compute the first derivative r = F K : the marginal product to capital is given by r = F K = a β -1/σ (with β=k/y) I.e. r as β (more capital makes capital less useful), but the important point is that the speed at which r depends on σ

10 With r = F K = a β -1/σ, the capital share α is given by: α = r β = a β (σ-1)/σ I.e. α is an increasing function of β if and only if σ>1 (and stable iff σ=1) The important point is that with large changes in the volume of capital β, small departures from σ=1 are enough to explain large changes in α If σ = 1.5, capital share rises from α=28% to α =36% when β rises from β=250% to β =500% = more or less what happened since the 1970s In case β reaches β =800%, α would reach α =42% In case σ =1.8, α would be as large as α =53%

11

12

13

14 Measurement problems with capital shares In many ways, β is easier to measure than α In principle, capital income = all income flows going to capital owners (independanty of any labor input); labor income = all income flows going to labor earners (independantly of any capital input) But in practice, the line is often hard to draw: family firms, selfsemployed workers, informal financial intermediation costs (=the time spent to manage one s own portfolio) If one measures the capital share α from national accounts (rent+dividend+interest+profits) and compute average return r=α/β, then the implied r often looks very high for a pure return to capital ownership: it probably includes a non-negligible entrepreneurial labor component, particularly in reconstruction periods with low β and high r; the pure return might be 20-30% smaller (see estimates) Maybe one should use two-sector models Y=Y h +Y b (housing + business); return to housing = closer to pure return to capital

15

16

17

18

19

20

21

22 Recent work on capital shares Imperfect competition and globalization: see Karabarmounis-Neiman 2013, «The Global Decline in the Labor Share»; see also KN2014 Public vs private firms: see Azmat-Manning- Van Reenen 2011, «Privatization and the Decline of the Labor Share in GDP: A Cross- Country Aanalysis of the Network Industries» Capital shares and CEO pay: see Pursey 2013, «CEO Pay and Factor shares: Bargaining effects in US corporations »

23 Summing up The rate of return to capital r is determined mostly by technology: r = F K = marginal product to capital, elasticity of substitution σ The quantity of capital β is determined by saving attitudes and by growth (=fertility + innovation): β = s/g The capital share is determined by the product of the two: α = r x β Anything can happen

24 Note: the return to capital r=f K is dermined not only by technology but also by psychology, i.e. saving attitudes s=s(r) might vary with the rate of return In models with wealth or bequest in the utility function U(c t,w t+1 ), there is zero saving elasticity with U(c,w)=c 1-s w s, but with more general functional forms on can get any elasticity In pure lifecycle model, the saving rate s is primarily determined by demographic structure (more time in retirement higher s), but it can also vary with the rate of return, in particular if the rate of return becomes very low (say, below 2%) or very high (say, above 6%)

25 In the dynastic utility model, the rate of return is entirely set by the rate of time preference (=psychological parameter) and the growth rate: Max Σ U(c t )/(1+δ) t, with U(c)=c 1-1/ξ /(1-1/ξ) unique long rate rate of return r t r = δ +ξg > g (ξ>1 and transverality condition) This holds both in the representative agent version of model and in the heteogenous agent version (with insurable shocks); more on this in Lecture 6

Econ 133 Global Inequality and Growth. Inequality between labor and capital. Gabriel Zucman

Econ 133 Global Inequality and Growth Inequality between labor and capital zucman@berkeley.edu 1 What we ve learned so far: All income derives from labor or capital The share of income that goes to capital

Econ 133 Global Inequality and Growth Inequality between labor and capital zucman@berkeley.edu 1 What we ve learned so far: All income derives from labor or capital The share of income that goes to capital

Capital in the 21 st century. Thomas Piketty Paris School of Economics Visby, June

Capital in the 21 st century Thomas Piketty Paris School of Economics Visby, June 30 2014 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book studies

Capital in the 21 st century Thomas Piketty Paris School of Economics Visby, June 30 2014 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book studies

Capital in the 21 st century. Thomas Piketty Paris School of Economics Cologne, December 5 th 2013

Capital in the 21 st century Thomas Piketty Paris School of Economics Cologne, December 5 th 2013 This lecture is based upon Capital in the 21 st century (Harvard Univ. Press, March 2014) This book studies

Capital in the 21 st century Thomas Piketty Paris School of Economics Cologne, December 5 th 2013 This lecture is based upon Capital in the 21 st century (Harvard Univ. Press, March 2014) This book studies

Inequality and growth Thomas Piketty Paris School of Economics

Inequality and growth Thomas Piketty Paris School of Economics Bercy, January 23 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book studies

Inequality and growth Thomas Piketty Paris School of Economics Bercy, January 23 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book studies

Capital in the 21 st century

Capital in the 21 st century Thomas Piketty Paris School of Economics Santiago de Chile, January 13 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014)

Capital in the 21 st century Thomas Piketty Paris School of Economics Santiago de Chile, January 13 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014)

Capital in the 21 st century

Capital in the 21 st century Thomas Piketty Paris School of Economics Lisbon, April 27 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book

Capital in the 21 st century Thomas Piketty Paris School of Economics Lisbon, April 27 2015 This presentation is based upon Capital in the 21 st century (Harvard University Press, March 2014) This book

Why are real interest rates so low? Secular stagnation and the relative price of capital goods

The facts Why are real interest rates so low? Secular stagnation and the relative price of capital goods Bank of England and LSE June 2015 The facts This does not reflect the views of the Bank of England

The facts Why are real interest rates so low? Secular stagnation and the relative price of capital goods Bank of England and LSE June 2015 The facts This does not reflect the views of the Bank of England

A 2 period dynamic general equilibrium model

A 2 period dynamic general equilibrium model Suppose that there are H households who live two periods They are endowed with E 1 units of labor in period 1 and E 2 units of labor in period 2, which they

A 2 period dynamic general equilibrium model Suppose that there are H households who live two periods They are endowed with E 1 units of labor in period 1 and E 2 units of labor in period 2, which they

Elements of Economic Analysis II Lecture II: Production Function and Profit Maximization

Elements of Economic Analysis II Lecture II: Production Function and Profit Maximization Kai Hao Yang 09/26/2017 1 Production Function Just as consumer theory uses utility function a function that assign

Elements of Economic Analysis II Lecture II: Production Function and Profit Maximization Kai Hao Yang 09/26/2017 1 Production Function Just as consumer theory uses utility function a function that assign

The historical evolution of the wealth distribution: A quantitative-theoretic investigation

The historical evolution of the wealth distribution: A quantitative-theoretic investigation Joachim Hubmer, Per Krusell, and Tony Smith Yale, IIES, and Yale March 2016 Evolution of top wealth inequality

The historical evolution of the wealth distribution: A quantitative-theoretic investigation Joachim Hubmer, Per Krusell, and Tony Smith Yale, IIES, and Yale March 2016 Evolution of top wealth inequality

Lecture notes 2: Physical Capital, Development and Growth

Lecture notes 2: Physical Capital, Development and Growth These notes are based on a draft manuscript Economic Growth by David N. Weil. All rights reserved. Lecture notes 2: Physical Capital, Development

Lecture notes 2: Physical Capital, Development and Growth These notes are based on a draft manuscript Economic Growth by David N. Weil. All rights reserved. Lecture notes 2: Physical Capital, Development

Macroeconomics Module 3: Cobb-Douglas production function practice problems. (The attached PDF file has better formatting.)

") Macroeconomics Module 3: Cobb-Douglas production function practice problems (The attached PDF file has better formatting.) The final exam has three types of problems on economic growth! Problems on convergence

Macroeconomics Module 3: Cobb-Douglas production function practice problems (The attached PDF file has better formatting.) The final exam has three types of problems on economic growth! Problems on convergence

About Capital in the 21 st Century

About Capital in the 21 st Century Thomas Piketty December 31, 2014 Thomas Piketty is Professor of Economics at the Paris School of Economics, Paris, France. His email address is piketty@psemail.eu. In

About Capital in the 21 st Century Thomas Piketty December 31, 2014 Thomas Piketty is Professor of Economics at the Paris School of Economics, Paris, France. His email address is piketty@psemail.eu. In

Capital is Back: Wealth-Income Ratios in Rich Countries Thomas Piketty & Gabriel Zucman Paris School of Economics October 2012

Capital is Back: Wealth-Income Ratios in Rich Countries 1870-2010 Thomas Piketty & Gabriel Zucman Paris School of Economics October 2012 How do aggregate wealth-income ratios evolve in the long run, and

Capital is Back: Wealth-Income Ratios in Rich Countries 1870-2010 Thomas Piketty & Gabriel Zucman Paris School of Economics October 2012 How do aggregate wealth-income ratios evolve in the long run, and

Econ 230B Graduate Public Economics. Models of the wealth distribution. Gabriel Zucman

Econ 230B Graduate Public Economics Models of the wealth distribution Gabriel Zucman zucman@berkeley.edu 1 Roadmap 1. The facts to explain 2. Precautionary saving models 3. Dynamic random shock models

Econ 230B Graduate Public Economics Models of the wealth distribution Gabriel Zucman zucman@berkeley.edu 1 Roadmap 1. The facts to explain 2. Precautionary saving models 3. Dynamic random shock models

Fluctuations. Shocks, Uncertainty, and the Consumption/Saving Choice

Fluctuations. Shocks, Uncertainty, and the Consumption/Saving Choice Olivier Blanchard April 2005 14.452. Spring 2005. Topic2. 1 Want to start with a model with two ingredients: Shocks, so uncertainty.

Fluctuations. Shocks, Uncertainty, and the Consumption/Saving Choice Olivier Blanchard April 2005 14.452. Spring 2005. Topic2. 1 Want to start with a model with two ingredients: Shocks, so uncertainty.

Economic Growth: Malthus and Solow Copyright 2014 Pearson Education, Inc.

Chapter 7 Economic Growth: Malthus and Solow Copyright Chapter 7 Topics Economic growth facts Malthusian model of economic growth Solow growth model Growth accounting 1-2 U.S. Per Capita Real Income Growth

Chapter 7 Economic Growth: Malthus and Solow Copyright Chapter 7 Topics Economic growth facts Malthusian model of economic growth Solow growth model Growth accounting 1-2 U.S. Per Capita Real Income Growth

Preferences and Utility

Preferences and Utility PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Axioms of Rational Choice Completeness If A and B are any two situations, an individual can always

Preferences and Utility PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Axioms of Rational Choice Completeness If A and B are any two situations, an individual can always

Reflections on capital taxation

Reflections on capital taxation Thomas Piketty Paris School of Economics Collège de France June 23rd 2011 Optimal tax theory What have have learned since 1970? We have made some (limited) progress regarding

Reflections on capital taxation Thomas Piketty Paris School of Economics Collège de France June 23rd 2011 Optimal tax theory What have have learned since 1970? We have made some (limited) progress regarding

Q: How does a firm choose the combination of input to maximize output?

Page 1 Ch. 6 Inputs and Production Functions Q: How does a firm choose the combination of input to maximize output? Production function =maximum quantity of output that a firm can produce given the quanities

Page 1 Ch. 6 Inputs and Production Functions Q: How does a firm choose the combination of input to maximize output? Production function =maximum quantity of output that a firm can produce given the quanities

INTERMEDIATE MACROECONOMICS

INTERMEDIATE MACROECONOMICS LECTURE 6 Douglas Hanley, University of Pittsburgh CONSUMPTION AND SAVINGS IN THIS LECTURE How to think about consumer savings in a model Effect of changes in interest rate

INTERMEDIATE MACROECONOMICS LECTURE 6 Douglas Hanley, University of Pittsburgh CONSUMPTION AND SAVINGS IN THIS LECTURE How to think about consumer savings in a model Effect of changes in interest rate

The Effect of Interventions to Reduce Fertility on Economic Growth. Quamrul Ashraf Ashley Lester David N. Weil. Brown University.

The Effect of Interventions to Reduce Fertility on Economic Growth Quamrul Ashraf Ashley Lester David N. Weil Brown University December 2007 Goal: analyze quantitatively the economic effects of interventions

The Effect of Interventions to Reduce Fertility on Economic Growth Quamrul Ashraf Ashley Lester David N. Weil Brown University December 2007 Goal: analyze quantitatively the economic effects of interventions

Rethinking Wealth Taxation

Rethinking Wealth Taxation Thomas Piketty (Paris School of Economics Gabriel Zucman (London School of Economics) November 2014 This talk: two points Wealth is becoming increasingly important relative to

Rethinking Wealth Taxation Thomas Piketty (Paris School of Economics Gabriel Zucman (London School of Economics) November 2014 This talk: two points Wealth is becoming increasingly important relative to

Sang-Wook (Stanley) Cho

Cho") Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales, Sydney July 2009, CEF Conference Motivation & Question Since Becker (1974), several

Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales, Sydney July 2009, CEF Conference Motivation & Question Since Becker (1974), several

Neoclassical Growth Theory

Neoclassical Growth Theory Ping Wang Department of Economics Washington University in St. Louis January 2018 1 A. What Motivates Neoclassical Growth Theory? 1. The Kaldorian observations: On-going increasing

Neoclassical Growth Theory Ping Wang Department of Economics Washington University in St. Louis January 2018 1 A. What Motivates Neoclassical Growth Theory? 1. The Kaldorian observations: On-going increasing

Modelling Economic Variables

ucsc supplementary notes ams/econ 11a Modelling Economic Variables c 2010 Yonatan Katznelson 1. Mathematical models The two central topics of AMS/Econ 11A are differential calculus on the one hand, and

ucsc supplementary notes ams/econ 11a Modelling Economic Variables c 2010 Yonatan Katznelson 1. Mathematical models The two central topics of AMS/Econ 11A are differential calculus on the one hand, and

A PRODUCER OPTIMUM. Lecture 7 Producer Behavior

Lecture 7 Producer Behavior A PRODUCER OPTIMUM The Digital Economist A producer optimum represents a solution to a problem facing all business firms -- maximizing the profits from the production and sales

Lecture 7 Producer Behavior A PRODUCER OPTIMUM The Digital Economist A producer optimum represents a solution to a problem facing all business firms -- maximizing the profits from the production and sales

Chapter 3 PREFERENCES AND UTILITY. Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved.

Chapter 3 PREFERENCES AND UTILITY Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Axioms of Rational Choice ( 理性选择公理 ) Completeness ( 完备性 ) if A and B are any two

Chapter 3 PREFERENCES AND UTILITY Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Axioms of Rational Choice ( 理性选择公理 ) Completeness ( 完备性 ) if A and B are any two

Should the Rich Pay for Fiscal Adjustment? Income and Capital Tax Options

Should the Rich Pay for Fiscal Adjustment? Income and Capital Tax Options Thomas Piketty Paris School of Economics Brussels, ECFIN Workshop, October 18 2012 This talk: two points 1. The rise of European

Should the Rich Pay for Fiscal Adjustment? Income and Capital Tax Options Thomas Piketty Paris School of Economics Brussels, ECFIN Workshop, October 18 2012 This talk: two points 1. The rise of European

Growth and Inclusion: Theoretical and Applied Perspectives

THE WORLD BANK WORKSHOP Growth and Inclusion: Theoretical and Applied Perspectives Session IV Presentation Sectoral Infrastructure Investment in an Unbalanced Growing Economy: The Case of India Chetan

THE WORLD BANK WORKSHOP Growth and Inclusion: Theoretical and Applied Perspectives Session IV Presentation Sectoral Infrastructure Investment in an Unbalanced Growing Economy: The Case of India Chetan

Optimal Taxation Under Capital-Skill Complementarity

Optimal Taxation Under Capital-Skill Complementarity Ctirad Slavík, CERGE-EI, Prague (with Hakki Yazici, Sabanci University and Özlem Kina, EUI) January 4, 2019 ASSA in Atlanta 1 / 31 Motivation Optimal

Optimal Taxation Under Capital-Skill Complementarity Ctirad Slavík, CERGE-EI, Prague (with Hakki Yazici, Sabanci University and Özlem Kina, EUI) January 4, 2019 ASSA in Atlanta 1 / 31 Motivation Optimal

Sang-Wook (Stanley) Cho

Cho") Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales March 2009 Motivation & Question Since Becker (1974), several studies analyzing

Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales March 2009 Motivation & Question Since Becker (1974), several studies analyzing

WEALTH, CAPITAL ACCUMULATION and LIVING STANDARDS

WEALTH, CAPITAL ACCUMULATION and LIVING STANDARDS Imagine a country where the primary goal of its economic policy is to accumulate a single commodity -- gold for example. Does the accumulation of wealth

WEALTH, CAPITAL ACCUMULATION and LIVING STANDARDS Imagine a country where the primary goal of its economic policy is to accumulate a single commodity -- gold for example. Does the accumulation of wealth

Economic Growth Models and Inequality

Economic Growth Models and Inequality Prof. Goldstein Economic Demography Econ/Demog c175 Week 3: Lecture B Spring 2018 UC Berkeley econ c175 1 Today s agenda Solow cont. Technology Income Shares Piketty

Economic Growth Models and Inequality Prof. Goldstein Economic Demography Econ/Demog c175 Week 3: Lecture B Spring 2018 UC Berkeley econ c175 1 Today s agenda Solow cont. Technology Income Shares Piketty

LECTURE 3: MEASURING THE WEALTH OF NATIONS. Dr. Aidan Regan Website:

LECTURE 3: MEASURING THE WEALTH OF NATIONS Dr. Aidan Regan Email: aidan.regan@ucd.ie Website: www.aidanregan.com Twitter: @aidan_regan Introduction Political economy was born in the 19 th century when

LECTURE 3: MEASURING THE WEALTH OF NATIONS Dr. Aidan Regan Email: aidan.regan@ucd.ie Website: www.aidanregan.com Twitter: @aidan_regan Introduction Political economy was born in the 19 th century when

Convergence of Life Expectancy and Living Standards in the World

Convergence of Life Expectancy and Living Standards in the World Kenichi Ueda* *The University of Tokyo PRI-ADBI Joint Workshop January 13, 2017 The views are those of the author and should not be attributed

Convergence of Life Expectancy and Living Standards in the World Kenichi Ueda* *The University of Tokyo PRI-ADBI Joint Workshop January 13, 2017 The views are those of the author and should not be attributed

Midterm 2 Review. ECON 30020: Intermediate Macroeconomics Professor Sims University of Notre Dame, Spring 2018

Midterm 2 Review ECON 30020: Intermediate Macroeconomics Professor Sims University of Notre Dame, Spring 2018 The second midterm will take place on Thursday, March 29. In terms of the order of coverage,

Midterm 2 Review ECON 30020: Intermediate Macroeconomics Professor Sims University of Notre Dame, Spring 2018 The second midterm will take place on Thursday, March 29. In terms of the order of coverage,

Model for rate of return to capital mathematical spiciness: ********** 10 stars (this appendix uses some advanced calculus) 1 Introduction

1 Introduction") Model for rate of return to capital mathematical spiciness: ********** 10 stars (this appendix uses some advanced calculus) 1 Introduction The purpose of this model is to investigate how different values

Model for rate of return to capital mathematical spiciness: ********** 10 stars (this appendix uses some advanced calculus) 1 Introduction The purpose of this model is to investigate how different values

IN THIS LECTURE, YOU WILL LEARN:

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

Prof. J. Sachs May 26, 2016 FIRST DRAFT COMMENTS WELCOME PLEASE QUOTE ONLY WITH PERMISSION

The Best of Times, the Worst of Times: Macroeconomics of Robotics Prof. J. Sachs May 26, 2016 FIRST DRAFT COMMENTS WELCOME PLEASE QUOTE ONLY WITH PERMISSION Introduction There are two opposing narratives

The Best of Times, the Worst of Times: Macroeconomics of Robotics Prof. J. Sachs May 26, 2016 FIRST DRAFT COMMENTS WELCOME PLEASE QUOTE ONLY WITH PERMISSION Introduction There are two opposing narratives

Advanced Macroeconomics 9. The Solow Model

Advanced Macroeconomics 9. The Solow Model Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) The Solow Model Spring 2015 1 / 29 The Solow Model Recall that economic growth can come from

Advanced Macroeconomics 9. The Solow Model Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) The Solow Model Spring 2015 1 / 29 The Solow Model Recall that economic growth can come from

The Ramsey Model. Lectures 11 to 14. Topics in Macroeconomics. November 10, 11, 24 & 25, 2008

The Ramsey Model Lectures 11 to 14 Topics in Macroeconomics November 10, 11, 24 & 25, 2008 Lecture 11, 12, 13 & 14 1/50 Topics in Macroeconomics The Ramsey Model: Introduction 2 Main Ingredients Neoclassical

The Ramsey Model Lectures 11 to 14 Topics in Macroeconomics November 10, 11, 24 & 25, 2008 Lecture 11, 12, 13 & 14 1/50 Topics in Macroeconomics The Ramsey Model: Introduction 2 Main Ingredients Neoclassical

Wealth, inequality & assets: where is Europe heading?

Wealth, inequality & assets: where is Europe heading? Thomas Piketty Paris School of Economics DG ECFIN Annual Research Conference Brussels, November 23 rd 2010 Can we study macro issues without looking

Wealth, inequality & assets: where is Europe heading? Thomas Piketty Paris School of Economics DG ECFIN Annual Research Conference Brussels, November 23 rd 2010 Can we study macro issues without looking

Topic 2: Consumption

Topic 2: Consumption Dudley Cooke Trinity College Dublin Dudley Cooke (Trinity College Dublin) Topic 2: Consumption 1 / 48 Reading and Lecture Plan Reading 1 SWJ Ch. 16 and Bernheim (1987) in NBER Macro

Topic 2: Consumption Dudley Cooke Trinity College Dublin Dudley Cooke (Trinity College Dublin) Topic 2: Consumption 1 / 48 Reading and Lecture Plan Reading 1 SWJ Ch. 16 and Bernheim (1987) in NBER Macro

WRITTEN PRELIMINARY Ph.D EXAMINATION. Department of Applied Economics. Spring Trade and Development. Instructions

WRITTEN PRELIMINARY Ph.D EXAMINATION Department of Applied Economics Spring - 2005 Trade and Development Instructions (For students electing Macro (8701) & New Trade Theory (8702) option) Identify yourself

WRITTEN PRELIMINARY Ph.D EXAMINATION Department of Applied Economics Spring - 2005 Trade and Development Instructions (For students electing Macro (8701) & New Trade Theory (8702) option) Identify yourself

Economic Growth. (c) Copyright 1999 by Douglas H. Joines 1. Module Objectives

Copyright 1999 by Douglas H. Joines 1. Module Objectives") Economic Growth Module Objectives now what determines the growth rates of aggregate and per capita GDP Distinguish factors that affect the economy s growth rate from those that merely shift the level of

Economic Growth Module Objectives now what determines the growth rates of aggregate and per capita GDP Distinguish factors that affect the economy s growth rate from those that merely shift the level of

SIMON FRASER UNIVERSITY Department of Economics. Intermediate Macroeconomic Theory Spring PROBLEM SET 1 (Solutions) Y = C + I + G + NX

Y = C + I + G + NX") SIMON FRASER UNIVERSITY Department of Economics Econ 305 Prof. Kasa Intermediate Macroeconomic Theory Spring 2012 PROBLEM SET 1 (Solutions) 1. (10 points). Using your knowledge of National Income Accounting,

SIMON FRASER UNIVERSITY Department of Economics Econ 305 Prof. Kasa Intermediate Macroeconomic Theory Spring 2012 PROBLEM SET 1 (Solutions) 1. (10 points). Using your knowledge of National Income Accounting,

Profit Max and RTS. Compare F(tL, tk) to tf(l,k) (where t>1) Which is the same as comparing doubling 1 inputs to doubling outputs

to tf(l,k) (where t>1) Which is the same as comparing doubling 1 inputs to doubling outputs") Profit Max and RTS This handout includes 3 sections: calculating returns to scale, the Impact of RTS on profit max, and an application problem. In this handout, I assume constant price, wage, and rent.

Profit Max and RTS This handout includes 3 sections: calculating returns to scale, the Impact of RTS on profit max, and an application problem. In this handout, I assume constant price, wage, and rent.

Intertemporal choice: Consumption and Savings

Econ 20200 - Elements of Economics Analysis 3 (Honors Macroeconomics) Lecturer: Chanont (Big) Banternghansa TA: Jonathan J. Adams Spring 2013 Introduction Intertemporal choice: Consumption and Savings

Econ 20200 - Elements of Economics Analysis 3 (Honors Macroeconomics) Lecturer: Chanont (Big) Banternghansa TA: Jonathan J. Adams Spring 2013 Introduction Intertemporal choice: Consumption and Savings

Macroeconomics Qualifying Examination

Macroeconomics Qualifying Examination January 211 Department of Economics UNC Chapel Hill Instructions: This examination consists of three questions. Answer all questions. Answering only two questions

Macroeconomics Qualifying Examination January 211 Department of Economics UNC Chapel Hill Instructions: This examination consists of three questions. Answer all questions. Answering only two questions

Wealth inequality, family background, and estate taxation

Wealth inequality, family background, and estate taxation Mariacristina De Nardi 1 Fang Yang 2 1 UCL, Federal Reserve Bank of Chicago, IFS, and NBER 2 Louisiana State University June 8, 2015 De Nardi and

Wealth inequality, family background, and estate taxation Mariacristina De Nardi 1 Fang Yang 2 1 UCL, Federal Reserve Bank of Chicago, IFS, and NBER 2 Louisiana State University June 8, 2015 De Nardi and

Wealth, Inequality & Taxation. Thomas Piketty Paris School of Economics Berlin FU, June 13 th 2013 Lecture 1: Roadmap & the return of wealth

Wealth, Inequality & Taxation Thomas Piketty Paris School of Economics Berlin FU, June 13 th 2013 Lecture 1: Roadmap & the return of wealth These lectures will focus primarily on the following issue: how

Wealth, Inequality & Taxation Thomas Piketty Paris School of Economics Berlin FU, June 13 th 2013 Lecture 1: Roadmap & the return of wealth These lectures will focus primarily on the following issue: how

/papers/dilip/dynamics/aer/slides/slides.tex 1. Is Equality Stable? Dilip Mookherjee. Boston University. Debraj Ray. New York University

/papers/dilip/dynamics/aer/slides/slides.tex 1 Is Equality Stable? Dilip Mookherjee Boston University Debraj Ray New York University /papers/dilip/dynamics/aer/slides/slides.tex 2 Economic Inequality......is

/papers/dilip/dynamics/aer/slides/slides.tex 1 Is Equality Stable? Dilip Mookherjee Boston University Debraj Ray New York University /papers/dilip/dynamics/aer/slides/slides.tex 2 Economic Inequality......is

Introduction to economic growth (2)

") Introduction to economic growth (2) EKN 325 Manoel Bittencourt University of Pretoria M Bittencourt (University of Pretoria) EKN 325 1 / 49 Introduction Solow (1956), "A Contribution to the Theory of Economic

Introduction to economic growth (2) EKN 325 Manoel Bittencourt University of Pretoria M Bittencourt (University of Pretoria) EKN 325 1 / 49 Introduction Solow (1956), "A Contribution to the Theory of Economic

Department of Economics Shanghai University of Finance and Economics Intermediate Macroeconomics

Department of Economics Shanghai University of Finance and Economics Intermediate Macroeconomics Instructor: Min Zhang Answer 2. List the stylized facts about economic growth. What is relevant for the

Department of Economics Shanghai University of Finance and Economics Intermediate Macroeconomics Instructor: Min Zhang Answer 2. List the stylized facts about economic growth. What is relevant for the

Testing the predictions of the Solow model:

Testing the predictions of the Solow model: 1. Convergence predictions: state that countries farther away from their steady state grow faster. Convergence regressions are designed to test this prediction.

Testing the predictions of the Solow model: 1. Convergence predictions: state that countries farther away from their steady state grow faster. Convergence regressions are designed to test this prediction.

Econ 133 Global Inequality and Growth. What is Income? Gabriel Zucman

Econ 133 Global Inequality and Growth What is Income? zucman@berkeley.edu 1 Roadmap 1. Income = domestic output + net foreign 2. Income = labor + capital 3. Functional vs. personal distribution 4. Factor

Econ 133 Global Inequality and Growth What is Income? zucman@berkeley.edu 1 Roadmap 1. Income = domestic output + net foreign 2. Income = labor + capital 3. Functional vs. personal distribution 4. Factor

ECON 2123 Problem Set 2

ECON 2123 Problem Set 2 Instructor: Prof. Wenwen Zhang TA: Mr. Ding Dong Due at 15:00 on Monday, April 9th, 2018 Question 1: The natural rate of unemployment Suppose that the markup of goods prices over

ECON 2123 Problem Set 2 Instructor: Prof. Wenwen Zhang TA: Mr. Ding Dong Due at 15:00 on Monday, April 9th, 2018 Question 1: The natural rate of unemployment Suppose that the markup of goods prices over

Online Appendix for Missing Growth from Creative Destruction

Online Appendix for Missing Growth from Creative Destruction Philippe Aghion Antonin Bergeaud Timo Boppart Peter J Klenow Huiyu Li January 17, 2017 A1 Heterogeneous elasticities and varying markups In

Online Appendix for Missing Growth from Creative Destruction Philippe Aghion Antonin Bergeaud Timo Boppart Peter J Klenow Huiyu Li January 17, 2017 A1 Heterogeneous elasticities and varying markups In

Summer 2016 ECN 303 Problem Set #1

Summer 2016 ECN 303 Problem Set #1 Due at the beginning of class on Monday, May 23. Give complete answers and show your work. The assignment will be graded on a credit/no credit basis. In order to receive

Summer 2016 ECN 303 Problem Set #1 Due at the beginning of class on Monday, May 23. Give complete answers and show your work. The assignment will be graded on a credit/no credit basis. In order to receive

RETURNS TO SCALE. Right.

CHAPTER 7, PART C, KWAN CHOI RETURNS TO SCALE When the price of a good rises, a producer wants to increase output. In the SR, only the variable input can be increased. In the long run, even the quantity

CHAPTER 7, PART C, KWAN CHOI RETURNS TO SCALE When the price of a good rises, a producer wants to increase output. In the SR, only the variable input can be increased. In the long run, even the quantity

Part A: Answer Question A1 (required) and Question A2 or A3 (choice).

and Question A2 or A3 (choice).") Ph.D. Core Exam -- Macroeconomics 10 January 2018 -- 8:00 am to 3:00 pm Part A: Answer Question A1 (required) and Question A2 or A3 (choice). A1 (required): Cutting Taxes Under the 2017 US Tax Cut and

Ph.D. Core Exam -- Macroeconomics 10 January 2018 -- 8:00 am to 3:00 pm Part A: Answer Question A1 (required) and Question A2 or A3 (choice). A1 (required): Cutting Taxes Under the 2017 US Tax Cut and

Keynesian Views On The Fiscal Multiplier

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Course Notes on Basic Theoretical Models of Economic Growth, Wealth Accumulation and Concentration

Introduction to Economic History (Master PPD & APE) (EHESS & Paris School of Economics) Thomas Piketty Academic year 2018-2019 Course Notes on Basic Theoretical Models of Economic Growth, Wealth Accumulation

Introduction to Economic History (Master PPD & APE) (EHESS & Paris School of Economics) Thomas Piketty Academic year 2018-2019 Course Notes on Basic Theoretical Models of Economic Growth, Wealth Accumulation

Financial Autarky and International Business Cycles (JME 2002)

") Financial Autarky and International Business Cycles (JME 2002) Jonathan Heathcote and Fabrizio Perri 9/9/2014 Sargent Reading Group Joseba Martinez Jonathan Heathcote and Fabrizio Perri Financial Autarky

Financial Autarky and International Business Cycles (JME 2002) Jonathan Heathcote and Fabrizio Perri 9/9/2014 Sargent Reading Group Joseba Martinez Jonathan Heathcote and Fabrizio Perri Financial Autarky

Part V: Introduction to Macroeconomics 19. The Wealth of Nations: Defining and Measuring Macroeconomic Aggregates 20.

the Part V: Introduction to Macroeconomics 19. The Wealth of Nations: Defining and Measuring Macroeconomic s 20. 1 / 54 the Chapter 20 2017.8.10. 2 / 54 the 1 2 the 3 4 3 / 54 Chapter 20 the Q: Why is

the Part V: Introduction to Macroeconomics 19. The Wealth of Nations: Defining and Measuring Macroeconomic s 20. 1 / 54 the Chapter 20 2017.8.10. 2 / 54 the 1 2 the 3 4 3 / 54 Chapter 20 the Q: Why is

Lecture 6: The structure of inequality: capital ownership

Economics of Inequality (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2013-2014 Lecture 6: The structure of inequality: capital ownership (Tuesday January 14 th 2014) (check

Economics of Inequality (Master PPD & APE, Paris School of Economics) Thomas Piketty Academic year 2013-2014 Lecture 6: The structure of inequality: capital ownership (Tuesday January 14 th 2014) (check

Deciphering the fall and rise in the net capital share by Matthew Rognlie, MIT BPEA Conference Draft (March, 2015)

") Deciphering the fall and rise in the net capital share by Matthew Rognlie, MIT BPEA Conference Draft (March, 2015) Comments by Rafia Zafar ECON 6470 Growth and Development Spring 2015 Evolution of Net

Deciphering the fall and rise in the net capital share by Matthew Rognlie, MIT BPEA Conference Draft (March, 2015) Comments by Rafia Zafar ECON 6470 Growth and Development Spring 2015 Evolution of Net

Macroeconomics 2. Lecture 6 - New Keynesian Business Cycles March. Sciences Po

Macroeconomics 2 Lecture 6 - New Keynesian Business Cycles 2. Zsófia L. Bárány Sciences Po 2014 March Main idea: introduce nominal rigidities Why? in classical monetary models the price level ensures money

Macroeconomics 2 Lecture 6 - New Keynesian Business Cycles 2. Zsófia L. Bárány Sciences Po 2014 March Main idea: introduce nominal rigidities Why? in classical monetary models the price level ensures money

Lecture 17: Investment (chapter 17)

") Lecture 17: Investment (chapter 17) Lecture notes: 101/105 (revised 12/6/99) topics: business fixed residential inventory Intro: Recall are three categories of investment: Business fixed: equipment and

Lecture 17: Investment (chapter 17) Lecture notes: 101/105 (revised 12/6/99) topics: business fixed residential inventory Intro: Recall are three categories of investment: Business fixed: equipment and

LECTURE 3 NEO-CLASSICAL AND NEW GROWTH THEORY

Intermediate Development Economics 3/Peter Svedberg, revised 2009-01-25/ LECTURE 3 NEO-CLASSICAL AND NEW GROWTH THEORY (N.B. LECTURE 3 AND 4 WILL BE PRESENTED JOINTLY) Plan of lecture A. Introduction B.

Intermediate Development Economics 3/Peter Svedberg, revised 2009-01-25/ LECTURE 3 NEO-CLASSICAL AND NEW GROWTH THEORY (N.B. LECTURE 3 AND 4 WILL BE PRESENTED JOINTLY) Plan of lecture A. Introduction B.

Why are Banks Exposed to Monetary Policy?

Why are Banks Exposed to Monetary Policy? Sebastian Di Tella and Pablo Kurlat Stanford University Bank of Portugal, June 2017 Banks are exposed to monetary policy shocks Assets Loans (long term) Liabilities

Why are Banks Exposed to Monetary Policy? Sebastian Di Tella and Pablo Kurlat Stanford University Bank of Portugal, June 2017 Banks are exposed to monetary policy shocks Assets Loans (long term) Liabilities

Lecture 11. The firm s problem. Randall Romero Aguilar, PhD II Semestre 2017 Last updated: October 16, 2017

Lecture 11 The firm s problem Randall Romero Aguilar, PhD II Semestre 2017 Last updated: October 16, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents 1. The representative

Lecture 11 The firm s problem Randall Romero Aguilar, PhD II Semestre 2017 Last updated: October 16, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents 1. The representative

ECON 450 Development Economics

ECON 450 Development Economics Classic Theories of Economic Growth and Development The Empirics of the Solow Growth Model University of Illinois at Urbana-Champaign Summer 2017 Introduction This lecture

ECON 450 Development Economics Classic Theories of Economic Growth and Development The Empirics of the Solow Growth Model University of Illinois at Urbana-Champaign Summer 2017 Introduction This lecture

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES. Lucas Island Model

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

Testing the predictions of the Solow model: What do the data say?

Testing the predictions of the Solow model: What do the data say? Prediction n 1 : Conditional convergence: Countries at an early phase of capital accumulation tend to grow faster than countries at a later

Testing the predictions of the Solow model: What do the data say? Prediction n 1 : Conditional convergence: Countries at an early phase of capital accumulation tend to grow faster than countries at a later

Comprehensive Exam. August 19, 2013

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Econ 133 Global Inequality and Growth. What is Income? Gabriel Zucman

Econ 133 Global Inequality and Growth What is Income? zucman@berkeley.edu 1 Roadmap 1. Income = domestic output + net foreign income 2. Income = labor income + capital income 3. Functional vs. personal

Econ 133 Global Inequality and Growth What is Income? zucman@berkeley.edu 1 Roadmap 1. Income = domestic output + net foreign income 2. Income = labor income + capital income 3. Functional vs. personal

Annuity Markets and Capital Accumulation

Annuity Markets and Capital Accumulation Shantanu Bagchi James Feigenbaum April 6, 208 Abstract We examine how the absence of annuities in financial markets affects capital accumulation in a twoperiod

Annuity Markets and Capital Accumulation Shantanu Bagchi James Feigenbaum April 6, 208 Abstract We examine how the absence of annuities in financial markets affects capital accumulation in a twoperiod

Dr Piketty on wealth and capital: Accumulation vs. finance

Dr Piketty on wealth and capital: Accumulation vs. finance Jo Michell 1 SOAS Money and Development Seminar 10 December 2014 1 jo.michell@uwe.ac.uk, Department of Accounting, Economics and Finance, University

Dr Piketty on wealth and capital: Accumulation vs. finance Jo Michell 1 SOAS Money and Development Seminar 10 December 2014 1 jo.michell@uwe.ac.uk, Department of Accounting, Economics and Finance, University

ECON 3010 Intermediate Macroeconomics. Chapter 3 National Income: Where It Comes From and Where It Goes

ECON 3010 Intermediate Macroeconomics Chapter 3 National Income: Where It Comes From and Where It Goes Outline of model A closed economy, market-clearing model Supply side factors of production determination

ECON 3010 Intermediate Macroeconomics Chapter 3 National Income: Where It Comes From and Where It Goes Outline of model A closed economy, market-clearing model Supply side factors of production determination

Check your understanding: Solow model 1

Check your understanding: Solow model 1 Bill Gibson March 26, 2017 1 Thanks to Farzad Ashouri Solow model The characteristics of the Solow model are 2 Solow has two kinds of variables, state variables

Check your understanding: Solow model 1 Bill Gibson March 26, 2017 1 Thanks to Farzad Ashouri Solow model The characteristics of the Solow model are 2 Solow has two kinds of variables, state variables

Price Elasticity of Demand

4 ELASTICITY The price elasticity of demand is a units-free measure of the responsiveness of the quantity demanded of a good to a change in its price when all other influences on buying plans remain the

4 ELASTICITY The price elasticity of demand is a units-free measure of the responsiveness of the quantity demanded of a good to a change in its price when all other influences on buying plans remain the

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ariel Zetlin-Jones and Ali Shourideh

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ariel Zetlin-Jones and Ali Shourideh Discussion by Gaston Navarro March 3, 2015 1 / 25 Motivation

External Financing and the Role of Financial Frictions over the Business Cycle: Measurement and Theory Ariel Zetlin-Jones and Ali Shourideh Discussion by Gaston Navarro March 3, 2015 1 / 25 Motivation

Macroeconomics 2. Lecture 12 - Idiosyncratic Risk and Incomplete Markets Equilibrium April. Sciences Po

Macroeconomics 2 Lecture 12 - Idiosyncratic Risk and Incomplete Markets Equilibrium Zsófia L. Bárány Sciences Po 2014 April Last week two benchmarks: autarky and complete markets non-state contingent bonds:

Macroeconomics 2 Lecture 12 - Idiosyncratic Risk and Incomplete Markets Equilibrium Zsófia L. Bárány Sciences Po 2014 April Last week two benchmarks: autarky and complete markets non-state contingent bonds:

Robots, Growth, and Inequality: Should We Fear the Robot Revolution? The Correct Answer is Yes

Robots, Growth, and Inequality: Should We Fear the Robot Revolution? The Correct Answer is Yes Andrew Berg Edward Buffie Felipe Zanna (IMF) (Indiana University) (IMF) ASSA Session on Labor Markets in the

Robots, Growth, and Inequality: Should We Fear the Robot Revolution? The Correct Answer is Yes Andrew Berg Edward Buffie Felipe Zanna (IMF) (Indiana University) (IMF) ASSA Session on Labor Markets in the

Advanced Macroeconomics 8. Growth Accounting

Advanced Macroeconomics 8. Growth Accounting Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Growth Accounting Spring 2015 1 / 20 Growth Accounting The final part of this course will

Advanced Macroeconomics 8. Growth Accounting Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Growth Accounting Spring 2015 1 / 20 Growth Accounting The final part of this course will

Economics 101. Lecture 3 - Consumer Demand

Economics 101 Lecture 3 - Consumer Demand 1 Intro First, a note on wealth and endowment. Varian generally uses wealth (m) instead of endowment. Ultimately, these two are equivalent. Given prices p, if

Economics 101 Lecture 3 - Consumer Demand 1 Intro First, a note on wealth and endowment. Varian generally uses wealth (m) instead of endowment. Ultimately, these two are equivalent. Given prices p, if

Principles of Macroeconomics Lecture Notes L3-L4 (Production and the labor market.) Veronica Guerrieri

Veronica Guerrieri") Principles of Macroeconomics Lecture Notes L3-L4 (Production and the labor market.) Veronica Guerrieri Page 1 of 51 TOPIC 2 The Supply Side of the Economy Page 2 of 51 Goals of Topic 2 Introduce the Supply

Principles of Macroeconomics Lecture Notes L3-L4 (Production and the labor market.) Veronica Guerrieri Page 1 of 51 TOPIC 2 The Supply Side of the Economy Page 2 of 51 Goals of Topic 2 Introduce the Supply

Traditional growth models Pasquale Tridico

1. EYNESIN THEORIES OF ECONOMIC GROWTH The eynesian growth models are models in which a long run growth path for an economy is traced out by the relations between saving, investements and the level of

1. EYNESIN THEORIES OF ECONOMIC GROWTH The eynesian growth models are models in which a long run growth path for an economy is traced out by the relations between saving, investements and the level of

14.13 Economics and Psychology (Lecture 5)

") 14.13 Economics and Psychology (Lecture 5) Xavier Gabaix February 19, 2003 1 Second order risk aversion for EU The agent takes the 50/50 gamble Π + σ, Π σ iff: B (Π) = 1 2 u (x + σ + Π)+1 u (x σ + Π) u

14.13 Economics and Psychology (Lecture 5) Xavier Gabaix February 19, 2003 1 Second order risk aversion for EU The agent takes the 50/50 gamble Π + σ, Π σ iff: B (Π) = 1 2 u (x + σ + Π)+1 u (x σ + Π) u

QI SHANG: General Equilibrium Analysis of Portfolio Benchmarking

General Equilibrium Analysis of Portfolio Benchmarking QI SHANG 23/10/2008 Introduction The Model Equilibrium Discussion of Results Conclusion Introduction This paper studies the equilibrium effect of

General Equilibrium Analysis of Portfolio Benchmarking QI SHANG 23/10/2008 Introduction The Model Equilibrium Discussion of Results Conclusion Introduction This paper studies the equilibrium effect of

Getting Started with CGE Modeling

Getting Started with CGE Modeling Lecture Notes for Economics 8433 Thomas F. Rutherford University of Colorado January 24, 2000 1 A Quick Introduction to CGE Modeling When a students begins to learn general

Getting Started with CGE Modeling Lecture Notes for Economics 8433 Thomas F. Rutherford University of Colorado January 24, 2000 1 A Quick Introduction to CGE Modeling When a students begins to learn general

ECN101: Intermediate Macroeconomic Theory TA Section

ECN101: Intermediate Macroeconomic Theory TA Section (jwjung@ucdavis.edu) Department of Economics, UC Davis November 4, 2014 Slides revised: November 4, 2014 Outline 1 2 Fall 2012 Winter 2012 Midterm:

ECN101: Intermediate Macroeconomic Theory TA Section (jwjung@ucdavis.edu) Department of Economics, UC Davis November 4, 2014 Slides revised: November 4, 2014 Outline 1 2 Fall 2012 Winter 2012 Midterm:

Lecture 05 Production

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology Kharagpur Lecture 05 Production Welcome to the fifth

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology Kharagpur Lecture 05 Production Welcome to the fifth

Lecture 3: Quantifying the Role of Credit Markets in Economic Development

Lecture 3: Quantifying the Role of Credit Markets in Economic Development Francisco Buera UCLA January 18, 2013 Finance and Development: A Tale of Two Sectors Buera, Kaboski & Shin 2011 Development Facts

Lecture 3: Quantifying the Role of Credit Markets in Economic Development Francisco Buera UCLA January 18, 2013 Finance and Development: A Tale of Two Sectors Buera, Kaboski & Shin 2011 Development Facts

Ramsey s Growth Model (Solution Ex. 2.1 (f) and (g))

and (g))") Problem Set 2: Ramsey s Growth Model (Solution Ex. 2.1 (f) and (g)) Exercise 2.1: An infinite horizon problem with perfect foresight In this exercise we will study at a discrete-time version of Ramsey

Problem Set 2: Ramsey s Growth Model (Solution Ex. 2.1 (f) and (g)) Exercise 2.1: An infinite horizon problem with perfect foresight In this exercise we will study at a discrete-time version of Ramsey

Wealth Accumulation in the US: Do Inheritances and Bequests Play a Significant Role

Wealth Accumulation in the US: Do Inheritances and Bequests Play a Significant Role John Laitner January 26, 2015 The author gratefully acknowledges support from the U.S. Social Security Administration

Wealth Accumulation in the US: Do Inheritances and Bequests Play a Significant Role John Laitner January 26, 2015 The author gratefully acknowledges support from the U.S. Social Security Administration

Achieving Actuarial Balance in Social Security: Measuring the Welfare Effects on Individuals

Achieving Actuarial Balance in Social Security: Measuring the Welfare Effects on Individuals Selahattin İmrohoroğlu 1 Shinichi Nishiyama 2 1 University of Southern California (selo@marshall.usc.edu) 2

Achieving Actuarial Balance in Social Security: Measuring the Welfare Effects on Individuals Selahattin İmrohoroğlu 1 Shinichi Nishiyama 2 1 University of Southern California (selo@marshall.usc.edu) 2

Econ 302 Assignment 2 Answer Key

Econ 302 Assignment 2 Answer ey Chapter 6 6.6 (a) In the example in the text, region A uses technology f A (l) to produce output, while region B uses technology (with a higher MPL schedule), f B (l). If

Econ 302 Assignment 2 Answer ey Chapter 6 6.6 (a) In the example in the text, region A uses technology f A (l) to produce output, while region B uses technology (with a higher MPL schedule), f B (l). If