INTRODUCTION AND GENERAL RULES. Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance. Section 1

|

|

|

- Mitchell Tobias Cunningham

- 6 years ago

- Views:

Transcription

1 a Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance Focused on flood insurance basics for insurance professionals 1 Section 1 INTRODUCTION AND GENERAL RULES 2 1

2 Here s our AGENDA Section 1 Introduction and General Rules Section 2 - Policy Rating, Elevations, Premiums and More Section 3- Coverage, limitations and Exclusions in the SFIP Section 4- Loss Settlement Provisions Section 5- Flood Insurance Resources 3 NFIP Flood Insurance Manual Access the NFIP Flood Insurance Manual: Online at the Flood Insurance Library: 4 2

3 What is a flood? NFIP definition of flood 6 What is a flood? NFIP definition of flood A general and temporary condition of partial or complete inundation of two or more acres of normally dry land area or of two or more properties (one of which is your property) from: a. Overflow of inland or tidal waters, b. Unusual and rapid accumulation or runoff of surface waters from any source, c. Mudflow. 7 3

4 What is a flood? Mudflow A river of liquid and flowing mud on the surface of normally dry land areas as when earth is carried by a current of water Not Mudflows: Landslide Slope failure Saturated soil mass 8 What is a flood? Flood Related Erosion Collapse or subsidence of land along the shore of a lake or similar body of water Caused by waves or currents of water exceeding cyclical levels Results in flooding 9 4

High Risk")

Low to Moderate Risk Zones B, C, X D (undetermined) 100-year floodplain = 1%")

5 Who has flood risk? All Property Owners All Zones 10 SFHAs and Non-SFHAs Special Flood Hazard Areas (SFHAs) High Risk Zones AE (replaces A1-A30) A, AH, AO, A99, AR VE (replaces V1-V30), V, VO Non-Special Flood Hazard Areas (non-sfhas) Low to Moderate Risk Zones B, C, X D (undetermined) 100-year floodplain = 1% annual chance flood Over 30-year mortgage likelihood grows from 1% to at least 26% 11 5

SFHAs appear as dark shading on a")

6 Training Agenda Flood Insurance Rate Map (FIRM) SFHAs appear as dark shading on a Flood Insurance Rate Map (FIRM) Digital Flood Insurance Rate Map (DFIRM) 13 6

7 FEMA Map Service Center Locating flood maps: 14 How is NFIP flood insurance purchased? How does the NFIP Work? 15 7

8 Who can buy NFIP flood insurance? Community Participation All Zones 16 Participating Communities FEMA agrees to make flood insurance available COMMUNITY agrees to adopt and enforce floodplain management regulations 17 8

9 Community Status Book Report 18 CBRS System Ability to write NFIP policies may be restricted in some: Coastal Barrier Resources Act (CBRA) areas Otherwise Protected Areas (OPA) Coastal Barrier Resources Act and Coastal Barrier Improvement Act enacted: October 18, 1982 November 16, 1990 Buildings may be ineligible for coverage in participating communities, If constructed on or after identification date. 19 9

10 How is NFIP flood insurance purchased? Write Your Own Company NFIP Direct Servicing Agent Licensed Property and Casualty Agent 20 Who MUST buy flood insurance? A or V Zones 21 10

11 Who MUST buy flood insurance? Used as security for a loan 22 Who MUST buy flood insurance? Designated Loan 23 11

12 What is a designated loan?. A loan secured by a building or mobile home that is located or to be located in a Special Flood Hazard Area in which flood insurance is available under the Act Please note: Emphasis on a building or mobile home as collateral 24 Who SHOULD buy flood insurance? Flood Insurance vs. Disaster Assistance 25 12

13 Flood Insurance vs. Disaster Assistance 26 How much NFIP flood insurance can be purchased? NFIP maximums vary by building type and program limits 27 13

Building Contents Other Residential Emergency Program $35,000 $10,000 Regular")

14 How much flood insurance coverage is available? Residential (1-4 family) Building Contents Other Residential Emergency Program $35,000 $10,000 Regular Program $250,000 $100,000 Building $100,000 $500,000 Contents $ 10,000 $100,000 Non-Residential Business/Other Non-Residential Building Contents $100,000 $100,000 $500,000 $500, When does an NFIP policy become effective? 30-day waiting period Exceptions 29 14

Insurance purchased within 13 months of a map revision (1-day wait).")

15 When does an NFIP policy become effective? There is a 30 day waiting period before new or modified flood insurance policies go into effect. Exceptions are provided for: Wildfire exception Insurance in connection with a loan transaction. (MIRE) Insurance purchased within 13 months of a map revision (1-day wait). For detailed information, please see the General Rules section of the Flood Insurance Manual 30 KEY NFIP TERMS, TOOLS, AND RULES To use and to live by 31 15

16 Full Risk Rates Defining Pre-FIRM and Post-FIRM Pre-FIRM Post-FIRM Built before initial FIRM or On or before 12/31/1974 On or After the initial FIRM or After 12/31/ whichever is LATER 32 Full-Risk Rates vs. Subsidized Rates Represent the building s true flood risk. Premium reflects the risk assumed by the program and all administrative expenses. Takes into account the full range of possible flood losses. Do not represent the building s true flood risk. Determined with limited underwriting information Discounted rates that have traditionally been available for Pre-FIRM buildings in A or V zones. Subsidized 33 16

Regular Program Final")

17 Regular vs. Emergency Program Emergency Program Initial participation phase Limited amount of coverage Flood Hazard Boundary Map (FHBM) Regular Program Final phase of participation Full limits of coverage Flood Insurance Rate Map (FIRM) 34 Base Flood Elevations (BFEs) BFE = 1% Chance Flood 35 17

18 Preferred Risk Policy Lower Cost Dwelling Form Preferred Risk Policy B,C,X, A99, AR Zones General Property Form 36 Miscellaneous NFIP Rules NFIP Policy Term 1 year annual term All policies NFIP Direct Write-Your-Own Evidence of Insurance Flood insurance application & premium payment Copy of dec page No binders Community Participation Probation Suspension Rules 37 18

19 Section 2 POLICY RATING, ELEVATIONS, PREMIUMS AND MORE 38 Case Study Facts Your client has just purchased a home in unincorporated Palm Beach County, Florida, and he approaches you to buy a flood insurance policy that is required by his lending institution since the house is in flood zone AE. About the home Palm Beach Rating Case Study It is a single family dwelling with a detached garage that will be his primary residence. The house was built in It is a two-story house and, like most homes in Florida, it does not have a basement. Information to gather What do you need to know in order to provide your client a quote? Let s take a look at the information you would need to gather; how you use and interpret it; and we ll go step-by-step to develop your client s quote. How much flood insurance to buy Since the house and its garage have a replacement cost value well above the NFIP s $250,000 single family maximum building limit, the new homeowner wants to buy the maximum amount of coverage on the building along with $100,000 worth of coverage for his personal property

20 Rating Elements Single family dwelling with detached garage Two-story home with no basement Built in 1995 in Palm Beach County, FL Flood Zone AE $250,000 Building Coverage $100,000 Personal Property Coverage Minimum deductibles Palm Beach Rating Case Study 40 Step 1 Determine Pre-FIRM or Post-FIRM status Utilize Community Status Book Palm Beach Rating Case Study 41 20

21 ` 42 ` 43 21

22 Community Status List 44 Step 1 Determine Pre-FIRM or Post-FIRM status Utilize Community Status Book Initial FIRM Date: 2/01/1979 Year Built: 1995 Post-FIRM Building Palm Beach Rating Case Study 45 22

23 Step 2 Locate a FEMA Elevation Certificate Blank Elevation Certificate Form Palm Beach Rating Case Study 46 What is meant by elevation? Lowest Floor Elevation Elevation Difference 47 23

24 Elevation difference refers to the height of a structure relative to BFE Elevation Difference A structure above BFE is less likely to experience flood damage Less risk = lower premiums 48 What is a Base Flood Elevation? Anticipated floodwater rise Regulatory requirement for elevation or floodproofing 49 24

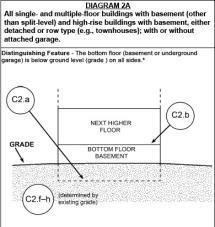

25 What is a Base Flood Elevation? Base flood is a flood that has a 1% chance of being equaled or exceeded. BFE is the expected height of that 1% chance of flood Base Flood Elevation 50 Lowest Floor Elevation BASEMENT 51 25

An EC includes important information for determining a riskbased premium EC shows: Location of the building Lowest floor elevation Building characteristics Flood zones")

26 Why are Elevation Certificates used? Elevation Certificates (EC) An EC includes important information for determining a riskbased premium EC shows: Location of the building Lowest floor elevation Building characteristics Flood zones Base flood elevation See building diagrams in the NFIP Flood Insurance Manual or the EC instructions 53 How are Elevation Certificates used? An Elevation Certificate: Certifies building elevation Documents community compliance Determines policy rates Supports map revisions and amendments 54 26

27 A surveyor, engineer, or architect must certify the building elevation Who Completes an Elevation Certificate? Insurance agents use this information for rating 55 Where to locate an Elevation Certificate for a building: Where to find an Elevation Certificate? Ask the local floodplain manager Ask the sellers Ask developer/builder Check the property deed Hire a licensed land surveyor, professional engineer or certified architect 56 27

")

28 FEMA Elevation Certificates Use of Elevation Certificates Pre-FIRM Construction (SFHAs) Not Required: Pre-FIRM subsidized rating Required: Full-risk rating approach. Non-SFHA zones (B, C, D, and X) Elevation certificates not required Post-FIRM Construction (SFHAs) Elevation certificates are required 57 FEMA Elevation Certificate EC Sections A thru F 58 28

29 FEMA Elevation Certificate EC Sections Section A Section B Section C Section D Sections E,F 59 FEMA Elevation Certificate EC Sections Section A 60 29

30 FEMA Elevation Certificate EC Sections Section B 61 FEMA Elevation Certificate EC Sections Section C 62 30

31 FEMA Elevation Certificate EC Sections Section D 63 FEMA Elevation Certificate EC Sections Sections E & F 64 31

32 FEMA Elevation Certificate Building Diagrams 65 FEMA Elevation Certificate Building Diagrams 66 32

33 FEMA Elevation Certificate Building Diagram 1A 67 EC Fact Sheet Elevation Certificates: Who Needs Them and Why Click here for on-line version How an EC is used Who needs an EC Where to get an EC When you need an EC When you do not need an EC Useful terms Resources 68 33

34 Step 3 Utilize FEMA Elevation Certificate Determine Elevation Difference Palm Beach Rating Case Study 69 FEMA Elevation Certificate EC Sections Palm Beach County* Palm Beach County FL AE 13.0 Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County, FL Post-FIRM construction Flood Zone AE Diagram 1A slab on grade

35 FEMA Elevation Certificate EC Sections 13.0 Palm Beach County* Palm Beach County FL 14.1 AE 13.0 Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County, FL Post-FIRM construction Flood Zone AE Diagram 1A slab on grade Step 3 Utilize FEMA Elevation Certificate Determine Elevation Difference Palm Beach County Case Study Elevation Difference: +1 Lowest Flood Elevation: 14.1 Base Flood Elevation: 13.0 Elevation Difference: +1.1 Rounds down: +1.0 Palm Beach Rating Case Study 72 35

36 Step 4 Determine Rating Approach Subsidized rating vs. Full-risk rates Palm Beach Rating Case Study 73 Reform Legislation Impact Individual premium increases Includes 18% Reserve Fund Assessment Does not include: HFIAA surcharge Federal Policy Fee *Limits increases to Limits increases to 18% 25% Annual 25% Increases Annual Increases Subsidized rates for: Non-primary residences Business properties Severe repetitive loss Substantially Damaged Substantially Improved 74 36

37 Impact of Biggert-Waters Reform Act How are premiums changing? As of January 1, 2013 Non-primary residences* Subsidized rates increase 25% per year upon renewal Until they reach full risk-rate Subsidized 25% 25% 25%? 25%? Full Risk Rates *A non-primary residence is a single family dwelling, condominium unit, apartment unit, or unit within a cooperative building that will not be lived in by the policyholder or the policyholder s spouse for more than 50% of the 365 days following the current policy effective date. A policyholder and the policyholder s spouse can have more than one primary residence provided they submit the required supporting documentation for each 75 residence. (See Flood Manual for complete details) Impact of Biggert-Waters Reform Act How are premiums changing? Effective April 1, 2016 Subsidized rates increase for: Business properties (non-residential)* Subsidized rates increase 25% per year upon renewal until they reach full risk-rate Subsidized 25% 25% 25%? 25%? Full Risk Rates *A non-residential business is a building in which the named insured is a commercial enterprise primarily carried out to generate income and the coverage is for: A building designed as a non-habitational building A mixed use building in which the total floor area devoted to residential uses is: 50% or less for single family or 75% or less for all other residential properties A building designed for use as office or retail space, wholesale space, hospitality space 76 or for similar uses 37

Bldg- $250,000 Contents- $100,000;")

38 Subsidized Rates Pre-FIRM Full-Risk Rates Post-FIRM $4,795/yr 4 ft above BFE $618/yr $4,795/yr 1 ft below BFE $4,531/yr $4,795/yr 4 ft below BFE $11,785/yr *AE Zone (04/01/18 rates) Bldg- $250,000 Contents- $100,000; Primary Residence, Single-story with no basement, crawlspace or enclosure rates; Zone AE; $2K deductible Bldg./Contents Palm Beach County Rating Case Study Single family dwelling with detached garage 2-story home - no basement Built in 1995 in Palm Beach County, FLT Post-FIRM construction Flood Zone AE +1 Elevation Difference $250,000 Building $100,000 Personal Property Minimum deductibles Let me get back to you with a quote! 78 38

39 Step 5 Review Key Rating Components Basic & Additional Limits Increased Cost of Compliance Community Rating System Reserve Fund Assessment Premium Surcharge Federal Policy Fee Palm Beach Rating Case Study 79 How much flood insurance coverage is available? Residential (1-4 family) Building Contents Other Residential Emergency Program $35,000 $10,000 Regular Program $250,000 $100,000 Building $100,000 $500,000 Contents $ 10,000 $100,000 Non-Residential Business/Other Non-Residential Building Contents $100,000 $100,000 $500,000 $500,

40 Rating: Basic and Additional Limits Basic Limit Building Coverage Single family $ 60, family $ 60,000 Other residential $ 175,000 Non-res. Bus./Other Non-res. $ 175,000 Contents Coverage Single family $ 25, fam; other res. $ 25,000 Non-res. Bus./Other Non-res. $ 150,000 Additional Limit $ 190,000 $ 190,000 $ 325,000 $ 325,000 $ 75,000 $ 75,000 $ 350, Palm Beach County Training Agenda Rating Case Study Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County Post-FIRM construction Flood Zone AE +1 Elevation Difference $250,000 Building $100,000 Personal Property Minimum deductibles.71/.08 Let me get back to you with a quote!

41 Palm Beach County Training Agenda Rating Case Study Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County Post-FIRM construction Flood Zone AE +1 Elevation Difference $250,000 Building $100,000 Personal Property Minimum deductibles.38/.12 Let me get back to you with a quote! Palm Beach County Training Agenda Rating Case Study Building Coverage:* Basic: 60,000 X.71 = $ Add l: 190,000 X.08 = $ Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County Post-FIRM construction Flood Zone AE +1 Elevation Difference $250,000 Building $100,000 Personal Property Minimum deductibles Personal Property Coverage:* Basic: 25,000 X.38 = $95.00 Add l: 75,000 X.12 = $90.00 Less 2% Deductible Discount Annual Subtotal: $ * Rates per $100 of coverage limit (4/1/18 rates) Let me get back to you with a quote!

42 Palm Beach County Training Agenda Rating Case Study Annual Subtotal: $ Increased Cost of Compliance: $5.00 Subtotal: $ Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County Post-FIRM construction Flood Zone AE +1 Elevation Difference $250,000 Building $100,000 Personal Property Minimum deductibles Let me get back to you with a quote! Community Rating System (CRS) Encourages communities to exceed minimum NFIP requirements > 1,300 communities participate in CRS CRS classes 1 10: Class 1 = 45% premium discount Class 9 = 5% discount 10: No discount Community Rating System: Class 1 Roseville, CA Class 2 Tulsa, OK Sacramento County, CA Fort Collins, CO King County, WA Pierce County, WA Thurston County, WA 86 42

43 Palm Beach County Training Agenda Rating Case Study Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County, FL Post-FIRM construction Flood Zone AE +1 Elevation Difference $250,000 Building $100,000 Personal Property Minimum deductibles Let me get back to you with a quote! Palm Beach County Training Agenda Rating Case Study Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County, FL Post-FIRM construction Flood Zone AE +1 Elevation Difference $250,000 Building $100,000 Personal Property Minimum deductibles Annual Subtotal: $ Increased Cost of Compliance: $5.00 Subtotal: $ $ X.75 = $ or $ Let me get back to you with a quote!

44 Reserve Fund Assessment Builds reserves to fund future claims activity 15% Assessment Preferred Risk Policy Newly Mapped All other policies Applied after ICC and CRS discount 15% No agent commission paid on reserve fund Introduced October 1, Palm Beach County Training Agenda Rating Case Study Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County, FL Post-FIRM construction Flood Zone AE +1 Elevation Difference $250,000 Building $100,000 Personal Property Minimum deductibles Annual Subtotal: $ Increased Cost of Compliance: $5.00 CRS discount 25% Subtotal: $ $ X 1.15 = $ or $ Let me get back to you with a quote!

45 HFIAA* Premium Surcharge Applies to all new and renewed policies annually $25 for primary residences $250 for all other policies Applies to contents-only policies Surcharge is a fully earned** flat fee based on building occupancy Not subject to earned commissions * HFIAA Homeowner Flood Insurance Affordability Act **See Cancellation and Endorsement sections of the NFIP Flood Insurance Manual for exceptions 91 Palm Beach County Training Agenda Rating Case Study Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County, FL Post-FIRM construction Flood Zone AE +1 Elevation Difference $250,000 Building $100,000 Personal Property Minimum deductibles Annual Subtotal: $ Increased Cost of Compliance: $5.00 CRS discount 25% Reserve Fund Assessment 15% Subtotal: $ HFIAA Surcharge: $25.00 Subtotal: $ Let me get back to you with a quote!

46 Federal Policy Fees Rate Type Standard Rated Policies/ Newly Mapped Properties Preferred Risk Policies/ Tenants contents only policies (ex. RCBAP/GFIP) RCBAP 1 unit units units units - 21 or more - Federal Policy Fee $50 $25 $ per policy $ per policy $ per policy $ per policy $ per policy Charged for all new and renewal policies Fully earned on effective date of policy (except as indicated in Cancellation section of the NFIP Flood Insurance Manual) Not subject to earned commissions 93 Palm Beach County Training Agenda Rating Case Study Single family dwelling 2-story home - no basement Built in 1995 in Palm Beach County, FL Post-FIRM construction Flood Zone AE +1 Elevation Difference $250,000 Building $100,000 Personal Property Minimum deductibles Annual Subtotal: $ Increased Cost of Compliance: $5.00 CRS discount 25% Reserve Fund Assessment 15% HFIAA Surcharge: $25.00 Subtotal: $ Federal Policy Fee: $50.00 Total Amount Due: $ Total w/o CRS discount = $ Let me get back to you with a quote!

47 Step 6 Other Rating Considerations Newly Mapped procedure Grandfather rules Elevated buildings Building enclosures Proper flood openings Breakaway walls Palm Beach Rating Case Study 95 Newly Mapped Procedure Effective April 2015 Newly Mapped procedure Properties in B, C, X, D, AR and A99 zones on the old map to an SFHA on new map Must meet specific loss eligibility requirements 96 47

48 Newly Mapped procedure Newly Mapped procedure applies to: Properties newly mapped into an SFHA from B, C, X, D, AR and A99 zones Policies previously issued under the PRP Eligibility Extension Properties newly mapped into SFHA may be eligible to receive a preferred risk premium for the first year after map revision* *Preferred Risk Policy premium before: Reserve Fund Assessment Federal Policy Fee After first year, policies begin transition to full-risk rates Effective April 1, Newly Mapped procedure Within 12 months of map revision Quick Key: Buildings in Palm Beach County affected by the map change effective 10/5/17 have until 10/4/18 to take advantage of the Newly Mapped procedure. Newly Mapped into SFHA on or after April 1, 2015 Eligible for Newly Mapped procedure: If coverage effective within 12 months of map revision Not eligible for Newly Mapped procedure: If coverage not effective within 12 months of map change Post-FIRM buildings may qualify for built-in-compliance grandfathering Pre-FIRM buildings may qualify for Pre-FIRM subsidized rates NOTE: All Properties must meet Preferred Risk Policy loss requirements to be eligible for Newly Mapped Procedure 98 48

49 Grandfather Rules Continuous Coverage vs. Built-in Compliance Effective April 2015 Newly Mapped procedure Properties in B, C, X and D zones on the old map to an SFHA on new map Must meet specific loss eligibility requirements 99 If policy was obtained prior to the effective date of the map change: Rates can be based on prior zone/bfe Continuous coverage must be maintained Grandfather Rules Continuous Coverage

50 If building was built in compliance with FIRM in effect at time of construction: Grandfather Rules Built in Compliance Use old map s zone or BFE, or Use current rating criteria Submit proof to carrier Continuous coverage not required 101 Grandfather Rules Historic flood maps Find historic flood maps by clicking on: Search All Products

51 Elevated buildings: Do not have basements Lowest elevated floor raised above ground level by: Foundation walls Shear walls Posts Piers Pilings Columns Elevated Buildings Elevated building defined Note: In Zones V and VE, solid foundation perimeter walls are unacceptable for elevated buildings. 103 An enclosure is: Elevated Buildings Building enclosures Portion of an elevated building below the lowest elevated floor Partially or fully shut in by rigid walls Finished Enclosure: Drywall is mudded, taped and painted Painted plywood Unfinished Enclosure: Drywall only painted Drywall is mudded and taped but not painted Block walls even if painted

52 Proper opening requirements: Must automatically equalize flood forces by allowing entry and exit of floodwaters Elevated Buildings Proper Openings A minimum of 2 openings on at least 2 exterior walls Total net area of not less than 1 square inch for every square foot of enclosure Bottoms of openings no higher than 1 foot above the higher of the exterior or interior grade Can only be used for: Building Access Parking Storage 105 Breakaway walls are: Not part of structural support Elevated Buildings Breakaway Walls Intended to collapse under certain lateral loading forces Without causing damage the elevated portion of the building or the supporting foundation system Should be less than 300 square feet Unfinished Used for access, parking or storage only No machinery or equipment V Zones Coastal Areas

53 Section 3 COVERAGE, LIMITATIONS AND EXCLUSIONS IN THE SFIP 108 Case Study Facts Six months later Flash floods strike Palm Beach County. Torrential rains flood the house s first floor with about 2 feet of water. Damage to the first floor consists of: Palm Beach Case Study Other Damage: House has a detached garage inundated by flood waters, destroying all the personal property items in it as well as flooding the family s second car parked in the garage Severe warping of the home s hardwood flooring Carpeting in the bedrooms soaked and muddied by flood waters Drywall and the insulation behind it damaged Appliances and mechanicals damaged and inoperative Furniture, clothing and other personal articles, including the homeowner s valuable baseball card collection severely impacted

54 Standard Flood Insurance Policy (SFIP) NFIP coverage forms 110 Provides building and/or personal property coverage for: Dwelling Form Non-condominium 1-to-4 family dwellings Dwelling unit in a residential condominium building Residential townhouse/rowhouse Mobile Homes/Travel Trailers as dwellings Quick Key: Palm Beach Case Study house uses Dwelling Form watch for coverage specifics

55 Provides building and/or personal property coverage for: Non-condominium Residential Buildings with 5 or more units Apartment building Co-operative building Dormitory Assisted living facility General Property Form Non-residential Buildings Office building School, Church Factory, Warehouse Agricultural building Restaurant, etc. 112 Provides building and, if purchased, contents coverage (commonly owned): Residential Condominium Building Association Policy Condominium buildings with 75% or more of total floor area for residential use Issued to a residential condominium association On behalf of association and unit owners

56 Preferred Risk Policy (PRP) Description & Eligibility Requirements Lower-cost Standard Flood Insurance Policy (SFIP) Uses Dwelling or General Property Forms RCBAP not eligible Buildings in B, C, X, A99 and AR zones In regular program communities Must meet eligibility requirements Not Eligible for PRP, if: Any of following exist:** 2 flood claim payments for separate losses, each > $1,000 3 or more flood claim payments for separate losses, regardless of $ 2 Federal flood disaster relief payments for separate occurrences, each > $1,000 3 Federal flood disaster relief payments for separate occurrences, regardless of amount 1 flood claim payment and 1 Federal disaster relief payment, each for separate losses and each > $1,000 **During any 10-year period, regardless of change of ownership of the building 114 Standard Flood Insurance Policy (SFIP): Coverage A: Building Property Coverage B: Personal Property Coverage C: Other Coverages Coverage D: Increased Cost of Compliance Types of Coverage SFIP is a single peril property policy. Will pay for direct physical loss by or from flood

57 What is a Building? Walled and roofed Affixed to a permanent site Principally above ground level 116 What is a Building? Coverage A Building Property Must have 2 or more outside rigid walls A fully secured roof Affixed to a permanent site Must resist flotation, collapse or lateral movement At least 51% of ACV above ground level

Travel Trailers Must be affixed to a permanent foundation No")

58 What is a Building? Coverage A: Building Property Manufactured/Mobile Homes & Travel Trailers Eligible buildings include: Manufactured (Mobile Homes) Travel Trailers Must be affixed to a permanent foundation No weight supported by wheels or axles Anchored in SFHAs to resist flotation, collapse or lateral movement 118 What is a Building? Coverage A: Building Property Buildings in the Course of Construction Allows issuance of SFIP before building is walled and roofed Offers coverage while work is in progress except when: Construction halted for > 90 days Lowest floor for rating is below BFE Covers materials and supplies while contained in an enclosed building on premises or adjacent to the premises Building deductible is doubled until walled and roofed

59 Coverage A: Building Property Additions and Extensions NFIP insures additions and extensions attached to and in contact with the building, by means of a: Rigid exterior wall Solid load-bearing interior wall Stairway Elevated walkway Roof NOTE: At the insured s option, additions and extensions connected by any of these methods may be separately insured. 120 What is a Building? Coverage A: Building Property Detached Garages At policyholder s option: 10% of building coverage can be applied to a detached garage Applies to Dwelling Form only Not additional coverage Reduces building limit of liability NOTE: Option does not apply to any detached garage used or held for use for residential, business, or farming purposes

60 Coverage A: Building Property Awnings, canopies Blinds Built-in dishwashers Built-in microwave ovens Carpet permanently installed over unfinished flooring Central air conditioners Elevator equipment Fire sprinkler systems Walk-in freezers Furnaces and radiators Garbage disposal units Light fixtures Hot water heaters, including solar water heaters Outdoor antennas & aerials fastened to buildings Permanently installed cupboards, bookcases, cabinets, paneling and wallpaper Plumbing fixtures Pumps and machinery for operating pumps Ranges, cooking stoves and ovens Refrigerators Wall mirrors (permanently installed.) 122 Dwelling Form vs. GPP/RCBAP Quick Key: Palm Beach Case Study house has damage to personal property in detached garage. Detached garage is a building at the described location. Coverage B Personal Property Dwelling Form: If personal property coverage is purchased, the SFIP insures: Personal property inside a building At the described location General Property/RCBAP: If personal property coverage is purchased, the SFIP insures: Personal property inside Fully enclosed insured building

61 Coverage B: Personal Property Dwelling Form Air conditioning units, portable or window type Carpets, not permanently installed, over unfinished flooring Carpets over finished flooring Clothes washers and dryers Cook-out grills Freezers, other than walk-in, and food in any freezer Portable microwave ovens and portable dishwashers Quick Key: Case Study house has carpet damage. Is it Coverage A or B? Luckily insured has purchased both coverages. General Property/RCBAP Air conditioning units Carpet, not permanently installed, over unfinished flooring Carpets over finished flooring Clothes washers and dryers Cook-out grills Freezers, other than walk-in, and food in any freezer Outdoor equipment and furniture stored inside the insured building Ovens and the like Portable microwave ovens and portable dishwashers 124 Coverage B: Personal Property General Property Form If Household Personal Property: Typical household personal property Belonging to the insured or to a member of the insured s household Insured s option: property belonging to a guest or domestic worker If Other than Household: Furniture and fixtures Machinery and equipment Stock Insured may be legally liable for Other personal property owned by insured and use in insured business Under the General Property Form, coverage will be either for household personal property or other than household personal property, while within the insured building, but not both

62 Case Study Facts Just to continue the discussion from a flood loss and coverage standpoint what if this house had a basement? Let s say that portions of the basement are finished with an office and a rec room area included. What s Covered/What s Not? Items damaged in basement: Desk and chair Computer and printer Television and stereo Pool table Carpeting Wall paneling All major mechanicals Appliances, including a refrigerator Electrical outlets Sump pump Other personal items Palm Beach What if? Case Study 126 What is a Basement? Coverage A & B Basements Basement is defined as: Any area of the building, including any sunken room or sunken portion of a room, having its floor below ground level (subgrade) on all sides

63 Coverage A: Basement/Enclosures Covered Building Property in Basements/Enclosures* Central air conditioners Cisterns & the water in them Unfinished drywall (walls, ceilings) in a basement Electrical junction and circuit breaker boxes Electrical outlets and switches Elevators and related equipment Fuel tanks and fuel in them Furnaces and hot water heaters Heat pumps Non-flammable insulation in a basement Pumps and tanks used in solar energy systems Stairways and staircases (attached to building) Sump pumps Water softeners and chemicals in them, water filters and faucets installed as integral part of plumbing system Well water tanks and pumps Required utility connections for items on this list Footings, foundations, posts, etc., required to support building Clean-up *Applies to basements in ANY zone and Post-FIRM enclosures in SFHAs listed. Please see the policy for complete details. 128 Coverage B: Basement/Enclosures Covered Personal Property in Basements/Enclosures If policyholder has purchased personal property coverage: Portable or window air conditioning units Clothes washers and dryers Food freezers (other than walk-in) and food in any freezer If installed in their functioning locations and, if necessary for operation, connected to a power source

64 What s Covered in a Basement*? Furnace Refrigerator Desk Television Washer Stereo Sump pump Computer Desk Chair Printer Carpeting Dryer Wall paneling Pool table Electrical outlets Food in refrigerator Water softener * Also in building enclosure below the lowest elevated floor of a Post-FIRM building in SFHAs listed in SFIP 130 Debris Removal Coverage C Other Coverages The SFIP pays the expense to remove: Non-owned debris on or in insured property Debris of insured property anywhere Value of labor based on Federal minimum wage NOTE: This coverage does not increase the Coverage A or Coverage B limit of liability

No deductible applies to either Loss Avoidance measure Value of labor based on Federal minimum wage NOTE: This coverage does not increase the")

: Assessed to policyholder by condo")

65 Loss Avoidance Measures Coverage C Other Coverages The SFIP pays the expense for: Loss avoidance measures: Sandbags, supplies, labor (up to $1,000) Property removed to safety (up to $1,000) No deductible applies to either Loss Avoidance measure Value of labor based on Federal minimum wage NOTE: This coverage does not increase the Coverage A or Coverage B limit of liability. 132 Condo Loss Assessments Coverage C Other Coverages The SFIP pays the expense for: Condominium loss assessments (Dwelling Form): Assessed to policyholder by condo association Up to the Coverage A limit of liability NOTE: This coverage does not increase the Coverage A or Coverage B limit of liability

66 Pollution Damage Coverage C Other Coverages The SFIP pays the expense for: Pollution Damage (General Property Form): $10,000 maximum limit Does not include testing or monitoring unless required by law or ordinance NOTE: This coverage does not increase the Coverage A or Coverage B limit of liability. 134 Coverage C: Other Coverages Coverage C: Does not increase Coverage A or B Coverage A - $250,000 Coverage B - $100,000 Debris Removal Expense: $15,000 Reduces Coverage A or B limit For example: Coverage A - $235,

67 Coverage D: Increased Cost of Compliance Coverage D: Compliance & Eligibility SFIP pays for complying with state or local floodplain management law or ordinance Compliance activities include: Elevation, Relocation, Demolition, Floodproofing Eligibility requires: Substantial damage 50% of market value, or Lower local standard Repetitive loss 2 flood losses in 10 years 25% of market value ICC Limit of Liability $30,000 See Part III. Property Covered - Section D of SFIP for complete details on eligibility and coverage 136 Property Not Covered Examples of Property Not Covered Quick Key: Case Study house had the family s second car damaged by flood. Vehicles licensed for public road use are not covered. Personal property not inside a building Building, and contents in it, located entirely in, on, or over water Open structures, including a boathouse in, on, or over water Recreational vehicles Self-propelled vehicles or machines licensed for public road use Land, land values, lawns, trees, shrubs, plants, growing crops or animals Accounts, bills, coins, currency, other valuable papers Walks, decks, driveways, etc. Underground structures and equipment, including wells, septic tanks, septic systems Containers & related equipment, such as tanks containing gases and liquid Buildings and their contents if > 49% of ACV is below ground Fences, retaining walls, seawalls, piers, docks, etc. Aircraft, watercraft or their furnishings and equipment Hot tubs and spas that are not bathroom fixtures Swimming pools and their equipment See Standard Flood Insurance Policy coverage forms for more information

68 Exclusions Partial list of SFIP Exclusions Exclusions The SFIP does not provide coverage for: Loss of revenue or profits Loss of access Loss of use Loss from interruption of business or production Additional living expenses 138 Exclusions Partial list of SFIP Exclusions Exclusions SFIP does not pay for losses for: Water or water borne material that: Backs up thru sewers or drains Discharges or overflows from a sump pump Seeps or leaks on or thru covered property Damage from the pressure or weight of water Exception: Unless there is a flood in the area and the flood is the proximate cause of one of the excluded items

69 Flood Insurance Reform Act of 2004 Summary of Coverage Information sent to policyholder by WYO Company or NFIP Servicing Agent: Summary of Coverage Summary of Coverage form Cover letter for enclosures Copy of flood insurance policy 140 Flood Insurance Reform Act of 2004 Claims Handbook Claims Handbook FEMA sends to policyholder: Property s loss history information Claims handbook Acknowledgment form to sign Cover letter referencing enclosures

70 Section 4 LOSS SETTLEMENT PROVISIONS 142 Loss Settlement - Deductibles Minimum deductibles vary based on: Policy rating Amount of coverage NOTE: Deductible doubles for building under construction prior to being walled and roofed

71 Loss Settlement Deductibles 144 Loss Settlement - Deductibles Minimum deductibles vary based on: Policy rating Amount of coverage Optional deductibles are available Non-residential - $50,000 RCBAP - $25,000 Residential - $10,000 NOTE: Deductible doubles for building under construction prior to being walled and roofed

72 Loss Settlement - Deductibles Minimum deductibles vary based on: Policy rating Amount of coverage Optional deductibles are available Separate for building and for contents Non-residential - $50,000 RCBAP - $25,000 Residential - $10,000 No deductible for: Loss avoidance measures Loss assessments ICC NOTE: Deductible doubles for building under construction prior to being walled and roofed 146 Loss Settlement Provisions Loss Settlement and the SFIP Loss Settlement Approaches Replacement Cost Value Actual Cash Value Special Loss Settlement

73 Loss Settlement Provisions Replacement Cost under Dwelling Form Replacement Cost Loss Settlement applies to: Loss Settlement Approaches Single Family Dwelling Building only Contents (ACV) Must be principal residence Insured-to-Value: 80% of replacement cost at time of loss, or Maximum under NFIP Quick Key: Principal Residence: the insured or insured s spouse must have lived there for at least 80% of 365 days immediately before the loss. 148 Loss Settlement Provisions Replacement Cost under RCBAP Loss Settlement Approaches Insures a residential condominium building owned by a condominium association. Replacement cost loss settlement applies to condos other than manufactured homes/travel trailers If insured to at least 80% of its replacement cost value at the time of loss or max limit there is no coinsurance penalty

74 RCBAP Maximum RCBAP Maximum Amount of Insurance The maximum RCBAP building coverage Equals the replacement cost value of the building, or $250,000 per unit times the number of units, whichever is less $250,000 x 10 Units = $2,500,000 $250,000 x 100 Units = $25,000, Loss Settlement Provisions Replacement Cost under RCBAP Loss Settlement Approaches Insures a residential condominium building owned by a condominium association. Replacement cost loss settlement applies to condos other than manufactured homes/travel trailers If insured to at least 80% of its replacement cost value at the time of loss or max limit there is no coinsurance penalty

= Limit of Recovery 152 Loss Settlement Provisions Actual Cash Value Loss Settlement Approaches Actual Cash")

75 RCBAP Co-Insurance Penalty Applies to Building Coverage Limit Amount of insurance at time of loss Amount of insurance required X Amount of loss (before deductible) = Limit of Recovery 152 Loss Settlement Provisions Actual Cash Value Loss Settlement Approaches Actual Cash Value loss settlement applies to: 2-to 4 family dwellings Single family that are not eligible for RCV Other Residential buildings Non-residential buildings Detached garages Personal property Mobile homes under 16 ft. wide and under 600 sq. ft 52-unit Apartment Building

76 Loss Settlement Provisions Manufactured/Mobile Homes and Travel Trailers Loss Settlement Approaches Special Loss Settlement applies to: Mobile homes/travel trailers At least 16 wide; at least 600 square feet Must be principal residence Partial losses settled according to replacement cost loss settlement conditions If it is total loss, coverage is the least of: The building s limit of liability Replacement cost of dwelling 1.5 times ACV 154 Section 5 FLOOD INSURANCE RESOURCES

77 NFIP Flood Insurance Manual Access the NFIP Flood Insurance Manual: Online at the Flood Insurance Library: National Flood Insurance Program Home Page

78 Key Fundamentals Course Page Handouts at: FEMA Map Service Center Locating flood maps:

79 All attendees will be receiving an with a link to a survey and feedback form. Evaluations Please take time to complete and help us improve our training effort! 160 Melanie Graham melanie@h2opartnersusa.com Mike Moye mmoye@h2opartnersusa.com Rich Slevin rich@h2opartnersusa.com Rich Waalkes rwaalkes@h2opartnersusa.com Aaron Montanez/Will Lucas producer@h2opartnersusa.com Contact Info

80 Thank you for attending!

Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance

a Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance Focused on flood insurance basics for insurance professionals (Part 2) 1 Here s our AGENDA Section 1 Introduction and General

a Welcome to The NFIP s Basic Agent Tutorial: Key Fundamentals of Flood Insurance Focused on flood insurance basics for insurance professionals (Part 2) 1 Here s our AGENDA Section 1 Introduction and General

Flood Insurance for Local Officials and Floodplain Managers. What Every Community Official Needs to Know About Flood Insurance

Flood Insurance for Local Officials and Floodplain Managers What Every Community Official Needs to Know About Flood Insurance Illinois Association for Floodplain and Stormwater Management 2011 Annual Conference

Flood Insurance for Local Officials and Floodplain Managers What Every Community Official Needs to Know About Flood Insurance Illinois Association for Floodplain and Stormwater Management 2011 Annual Conference

National Flood Insurance Program. Summary of Coverage

National Flood Insurance Program Summary of Coverage FEMA F-679 / November 2012 This document was prepared by the National Flood Insurance Program (NFIP) to help you understand your flood insurance policy.

National Flood Insurance Program Summary of Coverage FEMA F-679 / November 2012 This document was prepared by the National Flood Insurance Program (NFIP) to help you understand your flood insurance policy.

Summary of Your Flood Insurance Coverage

Summary of Your Flood Insurance Coverage National Flood Insurancee (888) 900-0404 4885 North Wickham Rd Suite 105 Melbourne, FL 32940 Summary of Your Flood Insurance Coverage What is a Flood? A flood is

Summary of Your Flood Insurance Coverage National Flood Insurancee (888) 900-0404 4885 North Wickham Rd Suite 105 Melbourne, FL 32940 Summary of Your Flood Insurance Coverage What is a Flood? A flood is

N F I P P o s t F l o o d W e b i n a r f o r A g e n t s N F I P P o s t F l o o d W e b i n a r f o r A g e n t s

1 2 1 3 4 2 Overview 5 TOPICS Overview Flood Insurance and Disaster Assistance The Claims Process Common Coverage Issues Appeals Process Increased Cost of Compliance (ICC) Impact of Biggert Waters 2012

1 2 1 3 4 2 Overview 5 TOPICS Overview Flood Insurance and Disaster Assistance The Claims Process Common Coverage Issues Appeals Process Increased Cost of Compliance (ICC) Impact of Biggert Waters 2012

FLOOD INSURANCE APPLICATION, PART 1 (OF 2) IMPORTANT PLEASE PRINT OR TYPE; ENTER DATES AS MM/DD/YYYY.

IMPORTANT PLEASE PRINT OR TYPE; ENTER DATES AS MM/DD/YYYY.") Make checks payable to: Wright National Flood Insurance Company P.O. Box 33003 St. Petersburg, FL 33733-8003 Phone (800) 323-8841 FLOOD INSURANCE APPLICATION, PART 1 (OF 2) IMPORTANT PLEASE PRINT OR TYPE;

Make checks payable to: Wright National Flood Insurance Company P.O. Box 33003 St. Petersburg, FL 33733-8003 Phone (800) 323-8841 FLOOD INSURANCE APPLICATION, PART 1 (OF 2) IMPORTANT PLEASE PRINT OR TYPE;

11/18/2011. FEMA All rights reserved. FEMA All rights reserved. Session Overview

3 Session Overview 4 1 Welcome to Session 2 of the FEMA NFIP Agent Training Program! Dorothy Martinez Rich Slevin Recall your learning from the previous session and share at least one important takeaway.

3 Session Overview 4 1 Welcome to Session 2 of the FEMA NFIP Agent Training Program! Dorothy Martinez Rich Slevin Recall your learning from the previous session and share at least one important takeaway.

Key Fundamentals of Flood Insurance

a Welcome to Key Fundamentals of Flood Insurance An entry-level approach for real estate professionals [Photo credit: Oliver Gruener] We will get started in a few minutes. Presented Meanwhile, by: let

a Welcome to Key Fundamentals of Flood Insurance An entry-level approach for real estate professionals [Photo credit: Oliver Gruener] We will get started in a few minutes. Presented Meanwhile, by: let

FLOOD - THE WATER IS RISING AND SO ARE THE RATES! SPONSORED BY

FLOOD - THE WATER IS RISING AND SO ARE THE RATES! SPONSORED BY Flood Insurance The Water is Rising & So Are the Rates!!! Michael C. D Orlando, CIC, LIA, CPIA Insurance Training & Consulting Services 11

FLOOD - THE WATER IS RISING AND SO ARE THE RATES! SPONSORED BY Flood Insurance The Water is Rising & So Are the Rates!!! Michael C. D Orlando, CIC, LIA, CPIA Insurance Training & Consulting Services 11

NFIP Overview Elevation Certificate Flood Insurance Rate Maps. By: Maureen O Shea, AICP, CFM State NFIP Coordinator

NFIP Overview Elevation Certificate Flood Insurance Rate Maps By: Maureen O Shea, AICP, CFM State NFIP Coordinator Example of a flood failure Example of a flood failure Purposes of the NFIP Identify &

NFIP Overview Elevation Certificate Flood Insurance Rate Maps By: Maureen O Shea, AICP, CFM State NFIP Coordinator Example of a flood failure Example of a flood failure Purposes of the NFIP Identify &

Commercial Risks & the NFIP Know the Facts (Intermediate) Student s Guide

Student s Guide") Commercial Risks & the NFIP Know the Facts (Intermediate) Student s Guide Provided by: Kalispell, Montana This training workbook and attendant materials are designed to provide producers with the basic

Commercial Risks & the NFIP Know the Facts (Intermediate) Student s Guide Provided by: Kalispell, Montana This training workbook and attendant materials are designed to provide producers with the basic

Key Fundamentals of Flood Insurance in the NFIP!

a Welcome to Key Fundamentals of Flood Insurance in the NFIP! A Before and After approach for Housing Counselors Presented by: 1 Before the Flood Presenter Melanie Graham After the Flood Presenter Erin

a Welcome to Key Fundamentals of Flood Insurance in the NFIP! A Before and After approach for Housing Counselors Presented by: 1 Before the Flood Presenter Melanie Graham After the Flood Presenter Erin

Key Fundamentals of Flood Compliance!

a Welcome to Key Fundamentals of Flood Compliance! An entry-level approach for lenders [Photo credit: Oliver Gruener] We will get started in a few minutes. Presented Meanwhile, by: let s perform a warm

a Welcome to Key Fundamentals of Flood Compliance! An entry-level approach for lenders [Photo credit: Oliver Gruener] We will get started in a few minutes. Presented Meanwhile, by: let s perform a warm

ATTACHMENT A SUMMARY OF THE NFIP OCTOBER 2013 PREMIUM RATE AND RULE CHANGES

ATTACHMENT A SUMMARY OF THE NFIP OCTOBER 2013 PREMIUM RATE AND RULE CHANGES National Flood Insurance Program October 1, 2013, Premium Rate and Rule Changes: A Summary 1. Premium Increases Premiums will

ATTACHMENT A SUMMARY OF THE NFIP OCTOBER 2013 PREMIUM RATE AND RULE CHANGES National Flood Insurance Program October 1, 2013, Premium Rate and Rule Changes: A Summary 1. Premium Increases Premiums will

General Property Form

General Property Form V-43 GENERAL PROPERTY FORM V-44 GENERAL PROPERTY FORM COMMENTARY LIMITATIONS, RESTRICTIONS, AND EXCLUSIONS The General Property Form does not provide coverage for: A residential condominium

General Property Form V-43 GENERAL PROPERTY FORM V-44 GENERAL PROPERTY FORM COMMENTARY LIMITATIONS, RESTRICTIONS, AND EXCLUSIONS The General Property Form does not provide coverage for: A residential condominium

FLOOD INSURANCE FIRA 3 HOUR

190 FLOOD INSURANCE FIRA 3 HOUR Introduction to Flood Insurance, 5 Introduction to NFIP Program, 9 The Preferred Risk Policy, 22 Standard Flood Policy, 25 Flood Policy Claims, 33 Glossary, 41 Frequently

190 FLOOD INSURANCE FIRA 3 HOUR Introduction to Flood Insurance, 5 Introduction to NFIP Program, 9 The Preferred Risk Policy, 22 Standard Flood Policy, 25 Flood Policy Claims, 33 Glossary, 41 Frequently

PREVIOUS SECTION TOC NEXT SECTION

Dwelling Form V-5 DWELLING FORM V-6 DWELLING FORM COMMENTARY The Dwelling Form covers only: LIMITATIONS, RESTRICTIONS, AND EXCLUSIONS A 1- to 4-family dwelling not under the condominium form of ownership

Dwelling Form V-5 DWELLING FORM V-6 DWELLING FORM COMMENTARY The Dwelling Form covers only: LIMITATIONS, RESTRICTIONS, AND EXCLUSIONS A 1- to 4-family dwelling not under the condominium form of ownership

NOTICE STANDARD FLOOD INSURANCE POLICY DWELLING FORM

NOTICE STANDARD FLOOD INSURANCE POLICY DWELLING FORM Your new policy form is attached. It has been formatted to comply with the provisions of Section 234, Policy Disclosures, of the Biggert-Waters Flood

NOTICE STANDARD FLOOD INSURANCE POLICY DWELLING FORM Your new policy form is attached. It has been formatted to comply with the provisions of Section 234, Policy Disclosures, of the Biggert-Waters Flood

Flood Insurance Information for Prospective Buyers

Flood Insurance Information for Prospective Buyers 25. Who may purchase a flood insurance policy? NFIP coverage is available to all owners of eligible property (a building and/or its contents) located

Flood Insurance Information for Prospective Buyers 25. Who may purchase a flood insurance policy? NFIP coverage is available to all owners of eligible property (a building and/or its contents) located

May 1, Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent

Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent") U.S. Department of Homeland Security 500 C St. SW Washington, D.C. 20472 W-15016 May 1, 2015 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

U.S. Department of Homeland Security 500 C St. SW Washington, D.C. 20472 W-15016 May 1, 2015 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

CONDOMINIUMS I. METHODS OF INSURING CONDOMINIUMS. Important Notice to Agents/Producers:

Previous Section Main Menu Table of Contents Next Section Important Notice to Agents/Producers: CONDOMINIUMS Boards of directors of condominium associations typically are responsible under their by-laws

Previous Section Main Menu Table of Contents Next Section Important Notice to Agents/Producers: CONDOMINIUMS Boards of directors of condominium associations typically are responsible under their by-laws

W October 1, Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent

Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent") U.S. Department of Homeland Security 500 C St. SW Washington, D.C. 20472 W-14053 October 1, 2014 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

U.S. Department of Homeland Security 500 C St. SW Washington, D.C. 20472 W-14053 October 1, 2014 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

Chapter 4: National Flood and Insurance Guide. 4 CE Hours. Learning objectives. Introduction. By:Valerie Wohl

Chapter 4: National Flood and Insurance Guide 4 CE Hours By:Valerie Wohl Learning objectives List three myths about flood insurance that keep property owners from purchasing coverage. Explain the role

Chapter 4: National Flood and Insurance Guide 4 CE Hours By:Valerie Wohl Learning objectives List three myths about flood insurance that keep property owners from purchasing coverage. Explain the role

Disaster Related Real Estate Issues. By Barry T. Bassis. Collecting Information

Disaster Related Real Estate Issues By Barry T. Bassis Collecting Information When a disaster strikes, such as Superstorm Sandy, it may damage or even destroy homes and the surrounding property. The first

Disaster Related Real Estate Issues By Barry T. Bassis Collecting Information When a disaster strikes, such as Superstorm Sandy, it may damage or even destroy homes and the surrounding property. The first

PREFERRED RISK POLICY

Previous Section Main Menu Table of Contents Next Section PREFERRED RISK POLICY I. GENERAL DESCRIPTION The Preferred Risk Policy (PRP) is a lower-cost Standard Fld Insurance Policy (SFIP), written under

Previous Section Main Menu Table of Contents Next Section PREFERRED RISK POLICY I. GENERAL DESCRIPTION The Preferred Risk Policy (PRP) is a lower-cost Standard Fld Insurance Policy (SFIP), written under

Frequently Asked Questions and Answers Concerning Flood Insurance

Frequently Asked Questions and Answers Concerning Flood Insurance Sources Used: (1) www.floodsmart.gov (2) National Flood Insurance Program, Answers to Questions about the NFIP, FEMA F-084/ March 2011.

Frequently Asked Questions and Answers Concerning Flood Insurance Sources Used: (1) www.floodsmart.gov (2) National Flood Insurance Program, Answers to Questions about the NFIP, FEMA F-084/ March 2011.

GENERAL RULES I. COMMUNITY ELIGIBILITY II. POLICIES AND PRODUCTS AVAILABLE

Previous Section Main Menu Table of Contents Next Section GENERAL RULES I. COMMUNITY ELIGIBILITY A. Participating (Eligible) Communities Flood insurance may be written only in those communities that have

Previous Section Main Menu Table of Contents Next Section GENERAL RULES I. COMMUNITY ELIGIBILITY A. Participating (Eligible) Communities Flood insurance may be written only in those communities that have

Dwelling Form. Standard Flood Insurance Policy 2015

Dwelling Form Standard Flood Insurance Policy 2015 STANDARD FLOOD INSURANCE POLICY DWELLING FORM PLEASE READ THE POLICY CAREFULLY. THE FLOOD INSURANCE PROVIDED IS SUBJECT TO LIMITATIONS, RESTRICTIONS,

Dwelling Form Standard Flood Insurance Policy 2015 STANDARD FLOOD INSURANCE POLICY DWELLING FORM PLEASE READ THE POLICY CAREFULLY. THE FLOOD INSURANCE PROVIDED IS SUBJECT TO LIMITATIONS, RESTRICTIONS,

April 2, Write Your Own Principal Coordinators and the NFIP Servicing Agent

U.S. Department of Homeland Security 500 C Street, SW Washington, DC 20472 W-09021 April 2, 2009 MEMORANDUM TO: Write Your Own Principal Coordinators and the NFIP Servicing Agent FROM: SUBJECT: Edward

U.S. Department of Homeland Security 500 C Street, SW Washington, DC 20472 W-09021 April 2, 2009 MEMORANDUM TO: Write Your Own Principal Coordinators and the NFIP Servicing Agent FROM: SUBJECT: Edward

General Property Form. Standard Flood Insurance Policy 2015

General Property Form Standard Flood Insurance Policy 2015 STANDARD FLOOD INSURANCE POLICY GENERAL PROPERTY FORM PLEASE READ THE POLICY CAREFULLY. THE FLOOD INSURANCE COVERAGE PROVIDED IS SUBJECT TO LIMITATIONS,

General Property Form Standard Flood Insurance Policy 2015 STANDARD FLOOD INSURANCE POLICY GENERAL PROPERTY FORM PLEASE READ THE POLICY CAREFULLY. THE FLOOD INSURANCE COVERAGE PROVIDED IS SUBJECT TO LIMITATIONS,

Floodplain Management 101. Mississippi Emergency Management Agency Floodplain Management Bureau

Floodplain Management 101 Mississippi Emergency Management Agency Floodplain Management Bureau Stafford Act The Stafford Disaster Relief and Emergency Assistance Act (Stafford Act) (Public Law 100-707)

Floodplain Management 101 Mississippi Emergency Management Agency Floodplain Management Bureau Stafford Act The Stafford Disaster Relief and Emergency Assistance Act (Stafford Act) (Public Law 100-707)

GENERAL PROPERTY FORM STANDARD FLOOD INSURANCE POLICY

GENERAL PROPERTY FORM STANDARD FLOOD INSURANCE POLICY Summary of Significant Changes, December 31, 2000 1. Section III. Property Covered, A. Coverage A - Building Property, 3. Additions and extensions

GENERAL PROPERTY FORM STANDARD FLOOD INSURANCE POLICY Summary of Significant Changes, December 31, 2000 1. Section III. Property Covered, A. Coverage A - Building Property, 3. Additions and extensions

Lloyd s Certificate. This Insurance is effected with certain Underwriters at Lloyd's, London.

Lloyd s Certificate This Insurance is effected with certain Underwriters at Lloyd's, London. This Certificate is issued in accordance with the limited authorization granted to the Correspondent by certain

Lloyd s Certificate This Insurance is effected with certain Underwriters at Lloyd's, London. This Certificate is issued in accordance with the limited authorization granted to the Correspondent by certain

October 1, Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent

Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent") U.S. Department of Homeland Security Washington, D.C. 20472 October 1, 2015 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent FROM:

U.S. Department of Homeland Security Washington, D.C. 20472 October 1, 2015 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent FROM:

New Beginnings. How Claims Put Peoples Lives Back Together

New Beginnings How Claims Put Peoples Lives Back Together What is the claims process? This is a common question as there are many people, companies, and steps involved. Common Questions from the Insured:

New Beginnings How Claims Put Peoples Lives Back Together What is the claims process? This is a common question as there are many people, companies, and steps involved. Common Questions from the Insured:

Introduction to Lender Compliance. National Flood Insurance Program

Introduction to Lender Compliance National Flood Insurance Program 1 Welcome to Introduction to Lender Compliance! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1

Introduction to Lender Compliance National Flood Insurance Program 1 Welcome to Introduction to Lender Compliance! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1

Pinellas County Flood Map Information Service & Real Estate Disclosure Program Training January 26, 2017 COMMON FLOODPLAIN ACRONYMS

FEMA ASFPM BFE CAV Pinellas County Flood Map Information Service & Real Estate Disclosure Program Training COMMON FLOODPLAIN ACRONYMS Federal Emergency Management Agency Association of State Floodplain

FEMA ASFPM BFE CAV Pinellas County Flood Map Information Service & Real Estate Disclosure Program Training COMMON FLOODPLAIN ACRONYMS Federal Emergency Management Agency Association of State Floodplain

Oak Island 1999 Hurricane Floyd

Oak Island 1999 Hurricane Floyd Topics to be Discussed What is a flood zone Flood zones in Oak Island Special Flood Hazard Areas (SFHA) Flood insurance Base Flood Elevations (BFEs) Building in flood zones

Oak Island 1999 Hurricane Floyd Topics to be Discussed What is a flood zone Flood zones in Oak Island Special Flood Hazard Areas (SFHA) Flood insurance Base Flood Elevations (BFEs) Building in flood zones

National Flood Insurance Program, Biggert-Waters 2012, and Homeowners Flood Insurance Affordability Act 2014

National Flood Insurance Program, Biggert-Waters 2012, and Homeowners Flood Insurance Affordability Act 2014 Janice Mitchell, Insurance Specialist Floodplain Management and Insurance Branch FEMA Region

National Flood Insurance Program, Biggert-Waters 2012, and Homeowners Flood Insurance Affordability Act 2014 Janice Mitchell, Insurance Specialist Floodplain Management and Insurance Branch FEMA Region

TITLE 110 LEGISLATIVE RULE STATE TAX DEPARTMENT

TITLE 110 LEGISLATIVE RULE STATE TAX DEPARTMENT SERIES 15I CONSUMER SALES AND SERVICE TAX AND USE TAX EXECUTIVE ORDERS DECLARING EMERGENCY AND EXEMPTING FROM TAX MOBILE HOMES AND SIMILAR UNITS AND BUILDING

TITLE 110 LEGISLATIVE RULE STATE TAX DEPARTMENT SERIES 15I CONSUMER SALES AND SERVICE TAX AND USE TAX EXECUTIVE ORDERS DECLARING EMERGENCY AND EXEMPTING FROM TAX MOBILE HOMES AND SIMILAR UNITS AND BUILDING

National Flood Insurance Program (NFIP) for Real Estate Professionals

for Real Estate Professionals") National Flood Insurance Program (NFIP) for Real Estate Professionals 1 Joshua Oyer, CFM Outreach Specialist NFIP State Coordinator s Office at the Texas Water Development Board 2 Outline Introduction

National Flood Insurance Program (NFIP) for Real Estate Professionals 1 Joshua Oyer, CFM Outreach Specialist NFIP State Coordinator s Office at the Texas Water Development Board 2 Outline Introduction

Table of Contents. PART 3: ADJUSTING COMMERCIAL FLOOD CLAIMS UNDER THE NFIP S GENERAL PROPERTY POLICY Lesson 1 Overview of the General Property Form

National Online Flood Adjuster Training Program: The 4-Corners of Flood Insurance Table of Contents PART 3: ADJUSTING COMMERCIAL FLOOD CLAIMS UNDER THE NFIP S GENERAL PROPERTY POLICY Lesson 1 Overview

National Online Flood Adjuster Training Program: The 4-Corners of Flood Insurance Table of Contents PART 3: ADJUSTING COMMERCIAL FLOOD CLAIMS UNDER THE NFIP S GENERAL PROPERTY POLICY Lesson 1 Overview

FEMA Elevation Certificates and Hydrostatic Venting Requirements

FEMA Elevation Certificates and Hydrostatic Venting Requirements Tennessee Association of Floodplain Managers Conference Gatlinburg, TN July 30 August 2, 2013 1 What is the National Flood Insurance Program

FEMA Elevation Certificates and Hydrostatic Venting Requirements Tennessee Association of Floodplain Managers Conference Gatlinburg, TN July 30 August 2, 2013 1 What is the National Flood Insurance Program

Article 23-6 FLOODPLAIN DISTRICT

AMENDING THE CODE OF THE CITY OF PITTSFIELD CHAPTER 23, ZONING ORDINANCE SECTION I That the Code of the City of Pittsfield, Chapter 23, Article 23-6 Floodplain District, shall be replaced with the following:

AMENDING THE CODE OF THE CITY OF PITTSFIELD CHAPTER 23, ZONING ORDINANCE SECTION I That the Code of the City of Pittsfield, Chapter 23, Article 23-6 Floodplain District, shall be replaced with the following:

National Flood Insurance Program Making Sense of April 2019 Changes

National Flood Insurance Program Making Sense of April 2019 Changes Foreword The National Flood Insurance Program (NFIP) provides an important means for property owners to protect themselves financially

National Flood Insurance Program Making Sense of April 2019 Changes Foreword The National Flood Insurance Program (NFIP) provides an important means for property owners to protect themselves financially

A Stock Company P.O. Box St. Petersburg, FL Customer Service: Claims: FLOOD DECLARATIONS PAGE

Wright National Flood Insurance Company Policv Number 17 1151438926 A Stock Company P.O. Box 33003 St. Petersburg, FL 33733-8003 Customer Service: 1-800-820-3242 Claims: 1-800-725-9472 FLOOD DECLARATIONS

Wright National Flood Insurance Company Policv Number 17 1151438926 A Stock Company P.O. Box 33003 St. Petersburg, FL 33733-8003 Customer Service: 1-800-820-3242 Claims: 1-800-725-9472 FLOOD DECLARATIONS

F E M A Mapping Changes. FEMA Mapping Changes. National Flood Insurance Program

FEMA Mapping Changes National Flood Insurance Program 1 Welcome to FEMA Mapping Changes! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1 Training Agenda Section 1-

FEMA Mapping Changes National Flood Insurance Program 1 Welcome to FEMA Mapping Changes! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1 Training Agenda Section 1-

MOKAN CRS Users Group Activity 310, Elevation Certificates Packet

http://mokan.stormsmart.org/ MOKAN CRS Users Group Activity 310, Elevation Certificates Packet This packet includes the following documents to be used as applicable to your community: EC checklist EC correction

http://mokan.stormsmart.org/ MOKAN CRS Users Group Activity 310, Elevation Certificates Packet This packet includes the following documents to be used as applicable to your community: EC checklist EC correction

April 16, Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent

Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent") U.S. Department of Homeland Security 500 C Street, SW Washington, DC 20472 W-12028 April 16, 2012 MEMORANDUM TO: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

U.S. Department of Homeland Security 500 C Street, SW Washington, DC 20472 W-12028 April 16, 2012 MEMORANDUM TO: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

Flood Compliance by the Case

Flood Compliance by the Case A CASE STUDY APPROACH FOR LENDERS Presented by: 1 Topic 1: Private Flood Insurance Topic 2: Force Placement Topic 3: Condo Conundrum Here s our agenda for today Topic 4: Escrows

Flood Compliance by the Case A CASE STUDY APPROACH FOR LENDERS Presented by: 1 Topic 1: Private Flood Insurance Topic 2: Force Placement Topic 3: Condo Conundrum Here s our agenda for today Topic 4: Escrows

SPECIAL CERTIFICATIONS

SPECIAL CERTIFICATIONS This section presents detailed instructions for the completion of the National Flood Insurance Program (NFIP) Elevation Certificate (EC) and the NFIP Floodproofing Certificates.

SPECIAL CERTIFICATIONS This section presents detailed instructions for the completion of the National Flood Insurance Program (NFIP) Elevation Certificate (EC) and the NFIP Floodproofing Certificates.

a) Ensure public safety through reducing the threats to life and personal injury.

Ensure public safety through reducing the threats to life and personal injury.") SECTION VII: FLOODPLAIN DISTRICT 7-1 Statement Of Purpose The purposes of the Floodplain District are to: a) Ensure public safety through reducing the threats to life and personal injury. b) Eliminate

SECTION VII: FLOODPLAIN DISTRICT 7-1 Statement Of Purpose The purposes of the Floodplain District are to: a) Ensure public safety through reducing the threats to life and personal injury. b) Eliminate

ATTACHMENT 1. Amendments to Chapter 18.20, Definitions Area of shallow flooding Area of special flood hazard

Amendments to Chapter 18.20, Definitions 18.20.206 Area of shallow flooding Area of shallow flooding means a designated AO, or AH, AR/AO, AR/AH, or VO Zone on the a community's flood insurance rate map

Amendments to Chapter 18.20, Definitions 18.20.206 Area of shallow flooding Area of shallow flooding means a designated AO, or AH, AR/AO, AR/AH, or VO Zone on the a community's flood insurance rate map

2011 National Flood Insurance Program Claims Adjuster Presentation. The Role of Certified Adjusters in the NFIP

2011 National Flood Insurance Program Claims Adjuster Presentation The Role of Certified Adjusters in the NFIP Adjuster Qualifications Purpose Database - Identification 5 Areas of Authorization - Residential

2011 National Flood Insurance Program Claims Adjuster Presentation The Role of Certified Adjusters in the NFIP Adjuster Qualifications Purpose Database - Identification 5 Areas of Authorization - Residential

Mobile homes are eligible if they are permanently located, but may only be covered by the Basic Form. Coverage may not include an attached carport.

4 Dwelling Policy OVERVIEW The Dwelling Policy is used to insure private residential property that is not occupied by its owner, such as rental property, as well as some owner-occupied private residential

4 Dwelling Policy OVERVIEW The Dwelling Policy is used to insure private residential property that is not occupied by its owner, such as rental property, as well as some owner-occupied private residential

National Flood Insurance Program and Biggert-Waters 2012

National Flood Insurance Program and Biggert-Waters 2012 National Flood Insurance Program NFIP was created by Congress in 1968 Coverage underwritten by the Federal Government, administered by FEMA NFIP

National Flood Insurance Program and Biggert-Waters 2012 National Flood Insurance Program NFIP was created by Congress in 1968 Coverage underwritten by the Federal Government, administered by FEMA NFIP

BIGGERT-WATERS 2012 TALKING POINTS

BIGGERT-WATERS 2012 TALKING POINTS No Extension of Subsidy on the Pre-FIRM Properties in SFHA s & Zone D Effective October 1, 2013, the NFIP will no longer provide any extension of premium rate subsidy

BIGGERT-WATERS 2012 TALKING POINTS No Extension of Subsidy on the Pre-FIRM Properties in SFHA s & Zone D Effective October 1, 2013, the NFIP will no longer provide any extension of premium rate subsidy

UHM Insurance Requirements (Hazard, Condominium, H0-6 and Flood)

") This Insurance Guide is provided by Union Home Mortgage Corp. ( UHM ), having its principal place of business at 8241 Dow Circle West, Strongsville, OH 44136. UHM publishes this via its secured website

This Insurance Guide is provided by Union Home Mortgage Corp. ( UHM ), having its principal place of business at 8241 Dow Circle West, Strongsville, OH 44136. UHM publishes this via its secured website

cost of the building. (See Example 4 at the end of this section.)

") . The National Flood Insurance Program (NFIP) General Change Endorsement form or a similar request can be used to make certain types of coverage and rating changes or corrections to the existing policy.

. The National Flood Insurance Program (NFIP) General Change Endorsement form or a similar request can be used to make certain types of coverage and rating changes or corrections to the existing policy.

THE BOP VS THE CPP... THE BATTLE OF THE CENTURY! SPONSORED BY

THE BOP VS THE CPP... THE BATTLE OF THE CENTURY! SPONSORED BY BOP vs CPP Michael C. D Orlando, CIC, LIA, CPIA Insurance Training & Consulting Services 11 Lake Shore Drive Amesbury, MA 01913 mcdorlando@aol.com

THE BOP VS THE CPP... THE BATTLE OF THE CENTURY! SPONSORED BY BOP vs CPP Michael C. D Orlando, CIC, LIA, CPIA Insurance Training & Consulting Services 11 Lake Shore Drive Amesbury, MA 01913 mcdorlando@aol.com

Introduction to the National Flood Insurance Program: A Guide for Coastal Property Owners MAINE BEACHES CONFERENCE 2017

Introduction to the National Flood Insurance Program: A Guide for Coastal Property Owners MAINE BEACHES CONFERENCE 2017 SUE BAKER, CFM STATE NFIP COORDINATOR MAINE DEPT OF AGRICULTURE, CONSERVATION & FORESTRY

Introduction to the National Flood Insurance Program: A Guide for Coastal Property Owners MAINE BEACHES CONFERENCE 2017 SUE BAKER, CFM STATE NFIP COORDINATOR MAINE DEPT OF AGRICULTURE, CONSERVATION & FORESTRY

VIII.Special Adjustment Issues VIII-1 A. Air Conditioning Condensers and Solar Heating Elements VIII-1 B. Bailee Goods VIII-1

National Flood Insurance Program Adjuster Claims Manual 2004adjmanual Effective December 31, 2000 Revision 1 January 1, 2002 Change 1 January 1, 2004 CONTENTS I. National Flood Insurance Program I-1 A.

National Flood Insurance Program Adjuster Claims Manual 2004adjmanual Effective December 31, 2000 Revision 1 January 1, 2002 Change 1 January 1, 2004 CONTENTS I. National Flood Insurance Program I-1 A.

Kevin Wagner Maryland Department of the Environment

Kevin Wagner Maryland Department of the Environment Topics Overview of the National Flood Insurance Program (NFIP) Mapping Regulations Insurance Mitigation Community Rating System (CRS) Questions Know

Kevin Wagner Maryland Department of the Environment Topics Overview of the National Flood Insurance Program (NFIP) Mapping Regulations Insurance Mitigation Community Rating System (CRS) Questions Know

Agenda. Introduction. Introduction -Map Study Lifecycle. Insurance Benefits of New Map

Agenda Introduction Effects of Map Changes on Flood Insurance Lower risk to higher risk ( Grandfathering ) Higher risk to lower risk ( Conversion ) No Change Vertical Datum change Summary Levees Levees

Agenda Introduction Effects of Map Changes on Flood Insurance Lower risk to higher risk ( Grandfathering ) Higher risk to lower risk ( Conversion ) No Change Vertical Datum change Summary Levees Levees

Changes Coming to the National Flood Insurance Program What to Expect. Impact of changes to the NFIP under Section 205 of the Biggert-Waters Act

Changes Coming to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Section 205 of the Biggert-Waters Act Flood Risk Flood risks and the costs of flooding Weather

Changes Coming to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Section 205 of the Biggert-Waters Act Flood Risk Flood risks and the costs of flooding Weather

CITY OF FORT PIERCE BUILDING DEPARTMENT

CITY OF FORT PIERCE BUILDING DEPARTMENT APPLICATION FOR DETERMINATION OF SUBSTANTIAL IMPROVEMENT This is a request for determination by the City s Floodplain Administrator as to whether or not the project

CITY OF FORT PIERCE BUILDING DEPARTMENT APPLICATION FOR DETERMINATION OF SUBSTANTIAL IMPROVEMENT This is a request for determination by the City s Floodplain Administrator as to whether or not the project

Welcome to Demystifying the Interagency Q&A! 10/28/2013. National Flood Insurance Program. Demystifying the Lender Q&As

Demystifying the Lender Q&As National Flood Insurance Program 1 Welcome to Demystifying the Interagency Q&A! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1 Seminar

Demystifying the Lender Q&As National Flood Insurance Program 1 Welcome to Demystifying the Interagency Q&A! We will get started in a few minutes. Meanwhile, let s perform a warm up exercise. 2 1 Seminar

TOP 10 Flood Insurance Changes

TOP 10 Flood Insurance Changes What Every Floodplain Official Should Know Rich Slevin, H 2 O Partners Dorothy Martinez, H 2 O Partners 1 TOP 10 Flood Insurance Changes What Every Floodplain Official Should

TOP 10 Flood Insurance Changes What Every Floodplain Official Should Know Rich Slevin, H 2 O Partners Dorothy Martinez, H 2 O Partners 1 TOP 10 Flood Insurance Changes What Every Floodplain Official Should

210 W Canal Dr Palm Harbor, FL 34684

Flood Analysis Memo Property Address In Partnership with: ** This property is within a high risk flood zone ** BFE = 6 ft This property is located in the FEMA designated high-risk zone, Zone AE - an area

Flood Analysis Memo Property Address In Partnership with: ** This property is within a high risk flood zone ** BFE = 6 ft This property is located in the FEMA designated high-risk zone, Zone AE - an area

The National Flood Insurance Program. Introduction Section I

Introduction Section I Course Material The following course material reflects input gathered by FEMA (Federal Emergency Management Agency) from state insurance regulators, insurers that sell flood insurance

Introduction Section I Course Material The following course material reflects input gathered by FEMA (Federal Emergency Management Agency) from state insurance regulators, insurers that sell flood insurance

National Flood Insurance Program

National Flood Insurance Program FEMA ELEVATION CERTIFICATES PA Surveyor Training Presented by Thomas F. Smith, PE, PLS January 22, 2018 1 FEMA Region III Mitigation Division Floodplain Management & Insurance

National Flood Insurance Program FEMA ELEVATION CERTIFICATES PA Surveyor Training Presented by Thomas F. Smith, PE, PLS January 22, 2018 1 FEMA Region III Mitigation Division Floodplain Management & Insurance

May 5, Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent

Principal Coordinators and the National Flood Insurance Program (NFIP) Servicing Agent") U.S. Department of Homeland Security 500 C Street, SW Washington, DC 20472 W-13026 May 5, 2013 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

U.S. Department of Homeland Security 500 C Street, SW Washington, DC 20472 W-13026 May 5, 2013 MEMORANDUM FOR: Write Your Own (WYO) Principal Coordinators and the National Flood Insurance Program (NFIP)

Questions about the National Flood Insurance Program