Banking Market Overview

|

|

|

- Adrian Casey

- 5 years ago

- Views:

Transcription

1 Banking Market Overview CEE and Romania Executive Summary Central and Eastern Europe (CEE)1 banking market overview Similar to 2009, in 2010 as well, the total CEE banking assets had a general positive trend and slightly increased in value by ~2%. Romania was the 4th biggest banking market in CEE, with total banking assets below the CEE average. The overall trend of bank loans at CEE level increased by ~13% in nominal terms compared to 2009 values. The high increase was mainly driven by Poland (considering the market s dimension), while countries like Bulgaria, Slovenia, Hungary and Romania had a low increase in total bank loans. The overall bank deposits had also a general positive trend in many CEE countries in Thus, as opposed to the pre-crisis years ( ), in many CEE countries the growth of deposit collection outpaced or was closer to the evolution of granted loans. As payment instruments are concerned, Romania and Bulgaria have the lowest values of card transactions per inhabitant among CEE countries that are part of EU Romanian banking market overview The dynamic of the aggregated net bank assets increased with 3.5% in nominal terms in RON in However, it is still a low level compared to the high growth values registered in previous years (before 2009). Total banking loans continued their declining trend in 2011 as well. The evolution was determined partly by the banks risk aversion due to increased non-performing loans and profitability issues. On the other side, the contraction of the population s disposable income and an increased trend towards savings had an influence as well. Concerning the loans structure per destination, corporate loans continued their increase in 2011 as well, reaching a level of 26.7 bneur in 2011, while household loans were fairly stable in 2011 in nominal values. The nominal value of the total deposits continued its increase up to ~40.5 bn EUR in Dec The population s increased tendency towards savings was visible in 2011 as well. The higher appetite towards savings is also due to a more prudent liquidity management of the population. Both the overall number of valid cards and the value of payment transactions increased in 2011 compared to Thus, in Dec there were ~13 mil. units of valid cards in circulation and the value of cards payment transactions was of ~ mil. EUR. Non-performing loans continued their ascending trend in 2011, even if at a slower pace, and thus lead to a further worsening of credit quality for many banks. As a consequence, the overall banking system s profitability was heavily impacted once again in 2011 and reached significant negative territory, posting at the end of the year an aggregated loss of ~ -100 meur. Therefore, some of the main short and medium term trends on the Romanian banking system include: increased financing pressures, reduced credit activity, increased focus on EU funds cofinancing, cost control/ branch network optimization, change of the competitive landscape, increased competition for good customers etc. Note: Upon writing this study, official data regarding the evolution of the banking market in 2011 is still being published. The analysis and formulated trends have been realized based on data available until February As future official data will be published, the study will be updated accordingly. 1 The study included the following countries: Poland, Czech Republic, Hungary, Romania, Slovakia, Croatia, Slovenia, Bulgaria, Serbia, Bosnia Herzegovina, Albania

Poland, the CEE")

2 2. CEE Banking Market 2.1. Banking market size in CEE Total bank assets, CEE, 2010 (bneur) 2.2. Similar to 2009, in 2010 as well, the total CEE banking assets had a general positive trend and increased in value by ~2% Still in some countries the total asset base has decreased in absolute terms in 2010, compared to 2009 (either in EUR-term or both EUR and LCY2-terms) Poland, the CEE country with the most developed banking system cumulated at the end of 2010 ~292 bneur in banking assets, more than 3 times higher than the CEE average of bneur Czech Republic and Hungary have also total banking assets higher than the average However, considering the current macroeconomic environment, the near term outlook for the banking sector needs to be considered with caution3 Banking loans in CEE Total bank loans, CEE, 2010 (bneur) 2 Local currency 3 Source: EBF databases, 2010; Ensight analysis

3 Loan growth in CEE accelerated in 2010, the overall trend of bank loans at CEE level increasing in 2010 by ~13% in nominal terms compared to 2009 values No country showed decreases in total bank loans While, the high increase was mainly driven by Poland, countries like Bulgaria, Slovenia, Hungary and Romania had a low increase in total bank loans4 Bank loans per destination, CEE, 2010 (bneur) The distribution of bank loans per destination still shows differences between the CEE country banking sectors, with a different focus on either corporate or household loans In 2010, corporate lending has been mainly outpacing household lending and it seems there is still further catch up potential; on the other hand, consumer credit has had mainly a negative trend5 4 Idem 5 Idem

![2.3. Non-performing loans Non-performing loans [% total loans], June 2011, CEE 2.4.](/docs-images/84/89720009/images/4-1.jpg "Non-performing loans continued to put pressure on the CEE banking system Thus, the level of non-performing loans continued to increase in some countries (like, for example, in Romania), even if at a")

4 2.3. Non-performing loans Non-performing loans [% total loans], June 2011, CEE 2.4. Non-performing loans continued to put pressure on the CEE banking system Thus, the level of non-performing loans continued to increase in some countries (like, for example, in Romania), even if at a lower pace than in 2010 In some other countries it already seems to have reached a peak compared to the values in 2010 On the other hand, there are countries like Slovenia that have very good credit quality compared to the other CEE countries6 Banking deposits in CEE Total bank deposits, CEE, 2010, (bneur) 6 Source: Raiffeisen Outlook 2011, National Banks, Ensight analysis

5 Bank deposits per category, CEE, 2010, (bneur) 2.5. Overall bank deposits had a general positive trend in most of the CEE countries, the average total bank deposits in CEE increasing in 2010 to 47.4 bneur from 42.6 bneur in 2009; however, similarly to total bank loans, Poland market size is considerably larger than the other CEE countries and thus highly impacts the average Still, as opposed to the pre-crisis years ( ), in many CEE countries the growth of deposit collection outpaced or was closer to the evolution of granted loans Deposits, as a traditional funding source, will most likely gain weight in terms of financing of the bank s general activities and thus regain attractiveness, also due to the expected lower availability of external financing7 Banking leverage needs in CEE 7 Source: EBF databases, 2010; Ensight analysis

6 Loans-to-deposits ratio, CEE, Before 2008, in the context of a good level of international liquidity, low cost of country risk and low saving rates, CEE local banks had a big support for their funding needs through capital inflows from the group As a consequence, loans-to-deposits ratios had also an upward trend, in some countries reaching high imbalances After 2008, given the current economic context, the average rising trend has stopped However, on an individual country level, the ratio has decreased only in a limited number of countries and in other it either stabilized or continued its increase with a different pace Thus, the overall loans-to-deposit CEE average in 2010 was of 1.09, compared to a value of 1.08 in 2009 There are still countries like Bulgaria, Croatia or Slovakia that have high imbalances between corporate loans and deposits8 Payment terminals in CEE Number of ATM s, CEE countries part of EU, Source: EBF databases, 2010; Ensight analysis

7 Based on official ECB data, in terms of number of ATMs per million of inhabitants, Slovenia ranks first with 758 ATMs, while Czech Republic has 355 The average number of ATMs per million of inhabitants in CEE countries which are part of the EU is 546 In comparison, Romania has 471 ATMs per million of inhabitants and is thus under the average of the selected countries, and 10,102 ATMs in total Note: The countries in scope of the analysis are CEE countries that are in the EU Number of POS terminals, CEE countries part of EU, 2010

9 Payment instruments in CEE Number of credit and debit cards (mil.")

8 2.7. Slovenia ranks first also as the number of POS devices per million of inhabitants is concerned, with 17,387 POS; this is a very high value compared to the other CEE countries and even is the average in some west European countries or Euro Area Considering its population size, Poland has the largest total number of POS terminals among the analyzed countries Romania is on the last place among the analyzed countries regarding the no. of POS devices per mil. inhabitants (4,995)9 Payment instruments in CEE Number of credit and debit cards (mil.), CEE, Source: ECB database, 2010; Ensight analysis

per inhabitant, Romania has the lowest level among the CEE countries that are part of EU, with 0.")

, compared to the other CEE countries that are part of EU and even to the average of the Euro area In comparison, the average number of cards per inhabitant in the Euro area is")

9 Number of cards (debit and credit)/inhabitant, CEE, 2010 Considering the size of the population, Poland has the largest total number of debit and credit cards When benchmarked regarding the number of total cards (debit and credit) per inhabitant, Romania has the lowest level among the CEE countries that are part of EU, with 0.59 cards per inhabitant On the other hand, Slovenia has a large number of cards per inhabitant (1.73), compared to the other CEE countries that are part of EU and even to the average of the Euro area In comparison, the average number of cards per inhabitant in the Euro area is Value of all transactions credit and debit cards, CEE, Source: ECB database, 2010; Ensight analysis

10 Value of all transactions per inhabitant credit and debit cards, CEE, 2010 Regarding the value of all transactions made with debit and credit cards per inhabitant, Romania and Bulgaria have the lowest values among the CEE countries that are part of EU Thus, even though it has a large number of cards per inhabitant, the value of all transactions (payments, withdrawals etc.) made with cards in Bulgaria is low compared to the other countries

11")

Concentration degree of the Romanian banking sector Over 75% of the Romanian banking system has foreign ownership, out of which Greece has")

11 3. Slovenia has the highest value of transactions made with debit cards per inhabitant, while in Poland there is the highest value for credit cards (also due to the fact that in Poland there is the highest number of credit cards per inhabitant)11 Romanian Banking Market 3.1. Romanian banking system Ownership structure of the Romanian banking sector (Dec. 2010) Concentration degree of the Romanian banking sector Over 75% of the Romanian banking system has foreign ownership, out of which Greece has ~30%, Austria ~21%, Holland ~15%* 11 Source: ECB database, 2010; Ensight analysis

**estimate 3.2. Banking penetration Banking penetration, comparative analysis CEE, 2010 12 NBR 2010, 2011, INS, Ensight analysis")

12 The dynamic of the aggregated net bank assets increased with 3,5% in nominal terms in RON in 2011; it is still a low level compared to the high growth values registered in previous years As regards the proportion of the banking assets in GDP, it had similar levels in the last 3 years The Top 5 banks in Romania covered in Q1/2011 ~54% of the total banking assets; the trend has been slightly increasing in 2010, and continued to be until 2011, but it is lower than EU average12 *Dec Total net banking assets evolution (bneur) **estimate 3.2. Banking penetration Banking penetration, comparative analysis CEE, NBR 2010, 2011, INS, Ensight analysis

13 Note: CEE countries included: Slovakia, Slovenia, Bulgaria, Czech Republic, Hungary, Poland, Romania, Albania, Bosnia & Herzegovina, Croatia *Non-government., non-bank companies 3.3. The level of banking penetration remained fairly stable both in Romania and CEE Thus, Romania has still a more reduced penetration level compared to CEE values This is especially true for the deposits gathered in Romania, which represented 34% of GDP, while in CEE they were 55% in 2010 Households deposits represented in Romania in % of GDP (similar with the level from 2009), while for CEE they were 55% As regards the level of total loans as share of GDP, in 2010 in Romania it was 40%, compared to 60% for CEE countries13 Loans - structure and growth rate Loans structure per destination (bneur), nominal values 13 Source: NBR 2011, EBF 2010, NIS (National Institute of Statistics), 2009; Ensight analysis

, non-residents Annual growth rate, non-government* loans, real values *Non-government, non-bank companies After the high levels reached up to 2009, the value of the total loans granted by")

14 * Non-government, non-bank companies ** Financial companies (incl. insurance), non-residents Annual growth rate, non-government* loans, real values *Non-government, non-bank companies After the high levels reached up to 2009, the value of the total loans granted by banks started to decline in 2010 and continued on the same descending trend in 2011 as well; thus, the total loans granted by banks in 2011 decreased with 3.1% in nominal terms compared to 2010 This evolution is determined partly by the banks risk aversion due to increased non-performing loans and profitability issues. On the other side, the contraction of the population s disposable income and an increased tendency towards savings had an influence as well Concerning the loans structure per destination, corporate loans continued their increase in 2011 as well, reaching a level of 26.7 bneur in 2011; on the other hand, household loans were fairly stable in 2011 Even if they had a slightly decreasing trend in 2011 compared to 2010, the weight of public administration in total banking loans is still higher then in 2008, on the basis of the financing of the budget deficit From a currency point of view, after more than 2 years of negative values, RON denominated loans reached a positive real annual growth rate at the end of Loans denominated in foreign currency had a more positive and fluctuating evolution in both 2010 and 2011, reaching negative levels during the middle of the year and then regaining positive growth value Source: NBR 2011, INS; Ensight analysis

in December 2011, compared to the values reached in December 2010 Correlated with a general CEE trend, the NBR has introduced in 2011 regulation aiming to")

15 3.4. Loans households and currency structure Loans structure per type of currency The weight of foreign currency loans has remained fairly stable for both households (~66%) and corporate loans (~61%) in December 2011, compared to the values reached in December 2010 Correlated with a general CEE trend, the NBR has introduced in 2011 regulation aiming to reduce the level of foreign currency denominated consumer loans 15 Households loans structure per destination (bneur) As households loans structure per destination is concerned, consumer credits were in Dec of 14.4 bneur, with ~22% lower than their value in 2008 Thus, the contraction that started in 2009 continued in 2011 as well 15 Source: NBR 2011, Ensight analysis

, driven mainly by the national program Prima Casa which is currently at its 4 th edition16 Deposits Deposits structure per destination (bneur), nominal values")

16 3.5. Despite the current economic environment and the local demand, mortgage has a small positive trend in nominal terms in 2011 as well (+14.4% in Dec. 2011, compared to Dec 2010), driven mainly by the national program Prima Casa which is currently at its 4 th edition16 Deposits Deposits structure per destination (bneur), nominal values *Non-government, non-bank companies Deposits structure per type of currency The nominal value of the total deposits continued its increase up to ~40.5 bneur in Dec The population s increased tendency towards savings was visible in 2011 as well. It thus shows a trend in the population s behavior, with a higher appetite towards savings. This tendency is also a reflection of a more prudent liquidity management Thus, households deposits amounted in 2011 to the equivalent of 26.1 bneur according to official data, an increase of over 7% compared to 2010, while corporate* loans were 14.4 bneur, ~1% lower than in 2010 (in nominal values) From a currency point of view, RON denominated deposits accounted for 66.3% of total deposits in 2011, showing a slight increase in their weight compared to Thus, savings in 16 Idem

After a high growth period, in late 2008/ beginning of 2009 the local banks started to reduce their loans interest rates and increased the competition for new deposits In the second semester of")

17 RON currency are preferred due to higher interest rates and also on the basis of a decreased fear of RON depreciation Interest rates New term deposits - average interest rate (%p.a.) *Non-bank companies New credits - average interest rate (%p.a.) After a high growth period, in late 2008/ beginning of 2009 the local banks started to reduce their loans interest rates and increased the competition for new deposits In the second semester of 2010 the banks have stopped the descending adjustment of their interest rates for households new credits in RON. Thus, in Dec the average interest rate for RON new credits was 12.66% (p.a.), higher than its Dec value. For EUR new credits, the interest rates values were similar with the ones in Dec The average interest rates used for corporate loans, both RON and EUR were higher in Dec than their values in Dec. 2010; however, for new credits in RON the gap was smaller for corporate loans than for households 17 Source: NBR 2011, Ensight analysis

18 The competition for new deposits collected from the population continued towards the end of 2010 when the interest rates offered had an ascending trend, and then started to decline in 2011, considering banks efforts to boost operational revenues However, the deposits increased during 2011 based on an increased tendency towards savings from households Cards Number of valid cards (mil. units) *Including deferred debit cards After a descending trend in the last 2 years, the number of total valid cards increased in 2011 (+5.9% in Dec compared to Dec. 2010) Thus, the number of total valid debit cards increased in Dec with 6.8%, compared to Dec values, reaching a number of ~11.2 mil. units Similarly, the number of total valid credit cards increased as well, reaching in Dec the number of ~2.2. mil. units compared to 2010 (with 1.6% higher than in Dec. 2010)19 Value of cards transactions 18 Source: NBR 2011, Ensight analysis 19 Source: NBR 2011, Ensight analysis

19 *Including deferred debit cards The value** of ATM withdrawals increased in 2011 with 13% to ~6.1 bneur, compared to a 2.3% increase in 2010 and after a decrease in 2009 of -5.2% Cards payment transactions also had a positive growth rate in 2011 (24.7%) Similarly to the increase in their number, the value of payment transactions with credit cards has increased in 2011 with 35.1% compared to Dec. 2010, while payment transactions with debit cards increased with 22.7%20 **Calculated in EUR values 3.8. Online and mobile banking Number of clients, online banking*, 2010 *19 financial institutions The number of online banking clients continued to increase in 2010 as well, even if the growth rate was not as high as in previous years Based on number of clients in 2010, the top 3 payers are: BCR, Raiffeisen Bank and ING Bank (closely followed by BRD) At the end of 2010, there were 6 banks with more than 100,000 clients in online banking representing over 80% of the total market 20 Idem

20 Value and number of transactions, online banking, As regards the value of the transactions, ING Bank is the clear leader with ~28.4 meur in 2010, followed by UniCredit Tiriac with ~12 meur ING Bank also has a high number of transactions, followed by BCR which has a large number of transactions with low value Even though there are no official estimates regarding the online banking market, according to the existing market data, ING has more than 30% market share based on the value of transactions The mobile banking market is less developed; the two first players on the market were BRD Société Générale and Raiffeisen Bank and it was recently introduced by other banks as well21 Credit quality Non-performing loans evolution (%) 21 Source: efinance 2010, Ensight analysis

21 *Gross exposure of non-bank loans and interest classified as loss category 2, with debt service >90 days and/or for which there were initiated judicial procedures / Total classified non-bank loans and related interest, excluding off-balance sheet items **Gross exposure of non-bank loans and interest classified as doubtful and loss / Total classified non-bank loans and related interest, excluding off-balance sheet items The consequence of the aggressive credit strategy during previous years, cumulated with financial pressures for households and companies and a RON devaluation are still visible in the credit quality in Romania Non-performing loans continue to put a great pressure on local banks profitability Thus, financial indicators measuring the credit quality have worsened in 2011 as well, even if the trend continued at a lower pace According to official data, the ratio of non-performing loans in Dec was 14.1%, compared to a value of 13.4% in Dec The credit risk ratio also increased in 2011 and reached the value of 23.3% in Dec However, the good level of capital adequacy was maintained in 2011 as well, providing thus a safety net for potential constraints due to increasing non-performing loans22 22 Source: NBR 2011, Ensight analysis

22 3.10. Banking system profitability Net profit aggregated banking system (meur) The pressure on the Romanian banking system s profitability continued in 2011 as well The driving factors were similar with the ones in 2010: non-performing loans, cumulated with reduced revenues due to lower credit activity, to which also summed up the funding pressures registered at group level due to the growing concerns regarding the euro zone debt crisis Thus, the aggregated banking system s net profit up to Sep outpaced the negative result from the entire 2010 year and reached a net aggregated loss of ~-198 meur. In December 2011, the banks compensated for almost half of the loss, posting at the end of the year an aggregated loss of ~-100 meur Consequently, profitability indexes ROA and ROE* had negative values23 *Return on net assets (ROA) = Net profit/ Total assets Return on equity (ROE) = Net profit / Equity 23 Source: NBR 2011, Ensight analysis

23 3.11. Costs and distribution network Evolution of branch network and number of employees Cost reduction The continuing economic decline has led the banks to further cost control Thus, the reduction of the number of branches continued in 2011 as well, reaching in June 2011 a number of ~5,950 branches The number of employees also declined compared to the values from Dec. 2010, reaching in 2011 ~65,600 employees at the overall banking system s level Distribution network As concerns Romania s number of branch units per 100,000 inhabitants, it is still lower than EU 27 average As regards the distribution network, besides the branches, the number of ATMs have been steadily growing, in Sep increasing with 4.6% compared to Dec The number of POS terminals have also continued their increase (7.9% in 2011 compared to 2010) Also, similar to European trends, banks are focusing more on developing their alternative channels (i.e. mobile, internet banking)24 24 Source: NBR 2011, Ensight analysis

24 3.12. Competition overview market share Competition overview Top 10 banks 2011, market share Source: NBR 2010, Press releases, Ensight analysis 26 Source: NBR, Press releases , Ensight analysis

28 27")

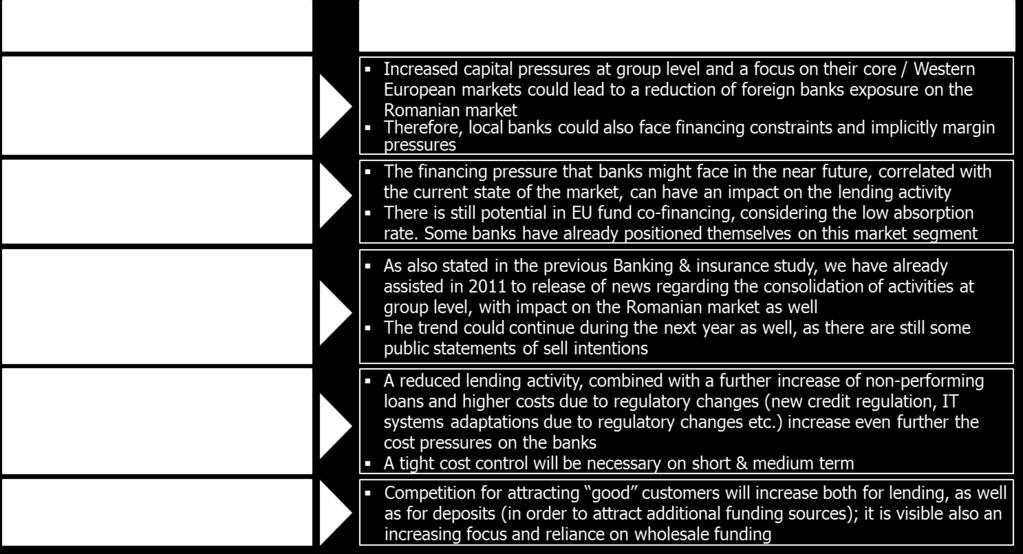

25 3.14. Main regulations overview (extract) Trends on the Romanian banking sector short & medium term (extract) Source: NBR 2011, Ensight analysis 28 Idem

26

Banking Market Overview

Banking Market Overview CEE and Romania Bucharest, March 212 212 Ensight Management Consulting. 2 Agenda Banking Sector Overview CEE banking market Romanian banking market 3 CEE and Romanian banking market

Banking Market Overview CEE and Romania Bucharest, March 212 212 Ensight Management Consulting. 2 Agenda Banking Sector Overview CEE banking market Romanian banking market 3 CEE and Romanian banking market

BANKING IN CEE: adequate risk appetite crucial to win the upside

BANKING IN CEE: adequate risk appetite crucial to win the upside UniCredit Group CEE Strategic Analysis Vienna, November 9, 2009 Executive Summary 1 World economic growth is recovering and this boosts

BANKING IN CEE: adequate risk appetite crucial to win the upside UniCredit Group CEE Strategic Analysis Vienna, November 9, 2009 Executive Summary 1 World economic growth is recovering and this boosts

FINANCIAL CRISIS AND BANK PROFITABILITY THE CASE OF ROMANIA

FINANCIAL CRISIS AND BANK PROFITABILITY THE CASE OF ROMANIA Lect. Imola Drigă Ph. D. University of Petrosani Faculty of Sciences Petrosani, Romania Abstract: The purpose of this paper is to provide a global

FINANCIAL CRISIS AND BANK PROFITABILITY THE CASE OF ROMANIA Lect. Imola Drigă Ph. D. University of Petrosani Faculty of Sciences Petrosani, Romania Abstract: The purpose of this paper is to provide a global

ESTONIA, LATVIA, LITHUANIA - BANKING MARKET IN THE BALTICS CEE BANKING BRIEF

ESTONIA, LATVIA, LITHUANIA - BANKING MARKET IN THE BALTICS 2008 - CEE BANKING BRIEF by Marcin Mazurek, March 2008 Version: 2008/03 REPORT ORDER FORM Intelace We order following report: Banking Market in

ESTONIA, LATVIA, LITHUANIA - BANKING MARKET IN THE BALTICS 2008 - CEE BANKING BRIEF by Marcin Mazurek, March 2008 Version: 2008/03 REPORT ORDER FORM Intelace We order following report: Banking Market in

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA THIRD QUARTER OF 2018 SOFIA HIGHLIGHTS The Bulgarian economy recorded growth of 3,2% on an annual basis in Q2 2018, driven by the private consumption and

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA THIRD QUARTER OF 2018 SOFIA HIGHLIGHTS The Bulgarian economy recorded growth of 3,2% on an annual basis in Q2 2018, driven by the private consumption and

The solid performance of CEE. Central and Eastern Europe pulled along by banks

The opening of the credit sector to outside investors has been a key part of the process of transforming and modernising the entire area and its economy. Western banks now play a leading role in many countries,

The opening of the credit sector to outside investors has been a key part of the process of transforming and modernising the entire area and its economy. Western banks now play a leading role in many countries,

NPL resolution in the case of Romania

National Bank of Romania NPL resolution in the case of Romania June 2015 Financial Stability Department National Bank of Romania 1 Summary Main features of the Romanian banking sector Definition of NPL:

National Bank of Romania NPL resolution in the case of Romania June 2015 Financial Stability Department National Bank of Romania 1 Summary Main features of the Romanian banking sector Definition of NPL:

CESEE DELEVERAGING AND CREDIT MONITOR 1

CESEE DELEVERAGING AND CREDIT MONITOR 1 November 17, 215 Key developments in BIS Banks External Positions and Domestic Credit The reduction of external positions of BIS reporting banks vis-à-vis Central,

CESEE DELEVERAGING AND CREDIT MONITOR 1 November 17, 215 Key developments in BIS Banks External Positions and Domestic Credit The reduction of external positions of BIS reporting banks vis-à-vis Central,

BANKING IN CEE. Carlo Vivaldi CFO UniCredit Bank Austria

BANKING IN CEE Carlo Vivaldi CFO UniCredit Bank Austria Brussels, November 10, 2009 EU Parliament Committee on the Financial, Economic and Social Crisis Executive Summary Macroeconomic and Global Banking

BANKING IN CEE Carlo Vivaldi CFO UniCredit Bank Austria Brussels, November 10, 2009 EU Parliament Committee on the Financial, Economic and Social Crisis Executive Summary Macroeconomic and Global Banking

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA SECOND QUARTER OF 2018 SOFIA HIGHLIGHTS The Bulgarian economy recorded growth of 3,6% on an annual basis in Q1 2018, driven by the private consumption and

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA SECOND QUARTER OF 2018 SOFIA HIGHLIGHTS The Bulgarian economy recorded growth of 3,6% on an annual basis in Q1 2018, driven by the private consumption and

4. Balance of Payments and Foreign Trade

24 4. Balance of Payments and Foreign Trade 4. Balance of Payments and Foreign Trade Current account deficit in 2014 was lower than the one realised in 2013 In the period January- November 2014, current

24 4. Balance of Payments and Foreign Trade 4. Balance of Payments and Foreign Trade Current account deficit in 2014 was lower than the one realised in 2013 In the period January- November 2014, current

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA IN 2017

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA IN 2017 Sofia HIGHLIGHTS In 2017 the Bulgarian economy recorded growth of 3,6% compared to the previous year, driven by the private consumption and the investments

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA IN 2017 Sofia HIGHLIGHTS In 2017 the Bulgarian economy recorded growth of 3,6% compared to the previous year, driven by the private consumption and the investments

Fact Sheet Fourth Quarter 2016

Profile Banca Comerciala Romana (BCR) was established in 1990 taking over the commercial banking operations of the National Bank of Romania. Today, BCR is the most important financial group in Romania,

Profile Banca Comerciala Romana (BCR) was established in 1990 taking over the commercial banking operations of the National Bank of Romania. Today, BCR is the most important financial group in Romania,

BANCA NAŢIONALĂ BANCA ROMÂNIEI

BANCA NAŢIONALĂ BANCA ROMÂNIEI A Stylized facts Report by McKinsey Global Institute (2010): Almost every major financial crisis in modern history has been followed by a significant period of deleveraging

BANCA NAŢIONALĂ BANCA ROMÂNIEI A Stylized facts Report by McKinsey Global Institute (2010): Almost every major financial crisis in modern history has been followed by a significant period of deleveraging

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA SECOND QUARTER OF 2017 Sofia HIGHLIGHTS The Bulgarian economy recorded growth of 3,9% on an annual basis in Q1 2017, driven by the domestic demand; The inflation

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA SECOND QUARTER OF 2017 Sofia HIGHLIGHTS The Bulgarian economy recorded growth of 3,9% on an annual basis in Q1 2017, driven by the domestic demand; The inflation

CESEE DELEVERAGING AND CREDIT MONITOR 1

CESEE DELEVERAGING AND CREDIT MONITOR 1 May 11, 217 Key developments in BIS Banks External Positions and Domestic Credit and Key Messages from the CESEE Bank Lending Survey The external positions of BIS

CESEE DELEVERAGING AND CREDIT MONITOR 1 May 11, 217 Key developments in BIS Banks External Positions and Domestic Credit and Key Messages from the CESEE Bank Lending Survey The external positions of BIS

Regional Benchmarking Report

Financial Sector Benchmarking System Regional Benchmarking Report October 2011 About the Financial Sector Benchmarking System This Regional Benchmarking Report is part of a series of benchmarking reports

Financial Sector Benchmarking System Regional Benchmarking Report October 2011 About the Financial Sector Benchmarking System This Regional Benchmarking Report is part of a series of benchmarking reports

Romania the next best thing. Generali Romania November 12, 2009 Bucharest

Romania the next best thing Generali Romania November 12, 2009 Bucharest Content Current Romanian economic outlook. And impact on the insurance industry Generali PPF on the CEE markets Why could Romania

Romania the next best thing Generali Romania November 12, 2009 Bucharest Content Current Romanian economic outlook. And impact on the insurance industry Generali PPF on the CEE markets Why could Romania

CONFERENCE CALL FOR THE FIRST QUARTER REPORT 2009 HERBERT STEPIC CEO MARTIN GRÜLL CFO

CONFERENCE CALL FOR THE FIRST QUARTER REPORT 2009 HERBERT STEPIC CEO MARTIN GRÜLL CFO 14 May 2009 Main Developments Managing the Crisis Outlook Financials Risk Management Appendix Main Developments HERBERT

CONFERENCE CALL FOR THE FIRST QUARTER REPORT 2009 HERBERT STEPIC CEO MARTIN GRÜLL CFO 14 May 2009 Main Developments Managing the Crisis Outlook Financials Risk Management Appendix Main Developments HERBERT

DYNAMICS OF BUDGETARY REVENUE IN THE CONDITIONS OF ROMANIAN INTEGRATION IN THE EUROPEAN UNION - A CONSEQUENTLY OF THE TAX AND HARMONIZATION POLICY

260 Finance Challenges of the Future DYNAMICS OF BUDGETARY REVENUE IN THE CONDITIONS OF ROMANIAN INTEGRATION IN THE EUROPEAN UNION - A CONSEQUENTLY OF THE TAX AND HARMONIZATION POLICY Mădălin CINCĂ, PhD

260 Finance Challenges of the Future DYNAMICS OF BUDGETARY REVENUE IN THE CONDITIONS OF ROMANIAN INTEGRATION IN THE EUROPEAN UNION - A CONSEQUENTLY OF THE TAX AND HARMONIZATION POLICY Mădălin CINCĂ, PhD

Romania Riding the Convergence Wave by Steven van Groningen CEO Romania

Romania Riding the Convergence Wave by Steven van Groningen CEO Romania Capital Markets Day, September 28 Slide 1 Inflation Increased in 27, But Under Control Real GDP Development 8.5% 7.9% 5. 6. 4. Downward

Romania Riding the Convergence Wave by Steven van Groningen CEO Romania Capital Markets Day, September 28 Slide 1 Inflation Increased in 27, But Under Control Real GDP Development 8.5% 7.9% 5. 6. 4. Downward

CESEE DELEVERAGING AND CREDIT MONITOR 1

CESEE DELEVERAGING AND CREDIT MONITOR 1 December 6, 216 Key developments in BIS Banks External Positions and Domestic Credit and Key Messages from the CESEE Bank Lending Survey The external positions of

CESEE DELEVERAGING AND CREDIT MONITOR 1 December 6, 216 Key developments in BIS Banks External Positions and Domestic Credit and Key Messages from the CESEE Bank Lending Survey The external positions of

CESEE DELEVERAGING AND CREDIT MONITOR 1

CESEE DELEVERAGING AND CREDIT MONITOR 1 May 27, 214 In 213:Q4, BIS reporting banks reduced their external positions to CESEE countries by.3 percent of GDP, roughly by the same amount as in Q3. The scale

CESEE DELEVERAGING AND CREDIT MONITOR 1 May 27, 214 In 213:Q4, BIS reporting banks reduced their external positions to CESEE countries by.3 percent of GDP, roughly by the same amount as in Q3. The scale

BANK PEKAO SA. Delivering sustainable profitability on the back of scale and market leadership

BANK PEKAO SA Delivering sustainable profitability on the back of scale and market leadership Bank of America Merrill Lynch Banking & Insurance CEO Conference London, 26.09.2012 DISCLAIMER This presentation

BANK PEKAO SA Delivering sustainable profitability on the back of scale and market leadership Bank of America Merrill Lynch Banking & Insurance CEO Conference London, 26.09.2012 DISCLAIMER This presentation

INTEREST RATES ON CORPORATE LOANS IN CROATIA AS AN INDICATOR OF IMBALANCE BETWEEN THE FINANCIAL AND THE REAL SECTOR OF NATIONAL ECONOMY

Category: preliminary communication Branko Krnić 1 INTEREST RATES ON CORPORATE LOANS IN CROATIA AS AN INDICATOR OF IMBALANCE BETWEEN THE FINANCIAL AND THE REAL SECTOR OF NATIONAL ECONOMY Abstract: Interest

Category: preliminary communication Branko Krnić 1 INTEREST RATES ON CORPORATE LOANS IN CROATIA AS AN INDICATOR OF IMBALANCE BETWEEN THE FINANCIAL AND THE REAL SECTOR OF NATIONAL ECONOMY Abstract: Interest

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA IN 2018

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA IN 2018 SOFIA HIGHLIGHTS In 2018 the Bulgarian economy recorded growth of 3,1% on an annual basis, driven by the private consumption and investments; The

THE ECONOMY AND THE BANKING SECTOR IN BULGARIA IN 2018 SOFIA HIGHLIGHTS In 2018 the Bulgarian economy recorded growth of 3,1% on an annual basis, driven by the private consumption and investments; The

Consumer credit market in Europe 2013 overview

Consumer credit market in Europe 2013 overview Crédit Agricole Consumer Finance published its annual survey of the consumer credit market in 28 European Union countries for seven years running. 9 July

Consumer credit market in Europe 2013 overview Crédit Agricole Consumer Finance published its annual survey of the consumer credit market in 28 European Union countries for seven years running. 9 July

CIT rate development in CEE

CIT rate development in CEE Where do we find the lowest rate? www.accace.com accace@accace.com Corporate income tax (CIT) rate is one of the key elements explored by entrepreneurs when considering operating

CIT rate development in CEE Where do we find the lowest rate? www.accace.com accace@accace.com Corporate income tax (CIT) rate is one of the key elements explored by entrepreneurs when considering operating

Q FINANCIAL RESULTS IFRS non-consolidated

Q1 2014 - FINANCIAL RESULTS IFRS non-consolidated Disclaimer THE INFORMATION CONTAINED IN THIS DOCUMENT HAS NOT BEEN INDEPENDENTLY VERIFIED AND NO REPRESENTATION OR WARRANTY EXPRESSED OR IMPLIED IS MADE

Q1 2014 - FINANCIAL RESULTS IFRS non-consolidated Disclaimer THE INFORMATION CONTAINED IN THIS DOCUMENT HAS NOT BEEN INDEPENDENTLY VERIFIED AND NO REPRESENTATION OR WARRANTY EXPRESSED OR IMPLIED IS MADE

Macroeconomic overview SEE and Macedonia

Macroeconomic overview SEE and Macedonia Zoltan Arokszallasi Chief Analyst, Macro & FX/FI Research Erste Group Bank Erste Investors Breakfast, 29 September, Skopje 02. Oktober SEE shows mixed performance

Macroeconomic overview SEE and Macedonia Zoltan Arokszallasi Chief Analyst, Macro & FX/FI Research Erste Group Bank Erste Investors Breakfast, 29 September, Skopje 02. Oktober SEE shows mixed performance

BRD - GROUP R E S U LT S 3 R D Q U AR T E R AN D F I R S T 9 M O N T H S N O V E M B E R

BRD - GROUP R E S U LT S 3 R D Q U AR T E R AN D F I R S T 9 M O N T H S 2 0 1 7 0 6 N O V E M B E R 2 0 1 7 DISCLAIMER The consolidated and separate financial position and income statement for the period

BRD - GROUP R E S U LT S 3 R D Q U AR T E R AN D F I R S T 9 M O N T H S 2 0 1 7 0 6 N O V E M B E R 2 0 1 7 DISCLAIMER The consolidated and separate financial position and income statement for the period

Report on financial stability

Report on financial stability Márton Nagy MNB Club 26 April 212 Key risks Deteriorating lending capacity stemming particularly from liquidity side raises the risk of a credit crunch, mainly in the corporate

Report on financial stability Márton Nagy MNB Club 26 April 212 Key risks Deteriorating lending capacity stemming particularly from liquidity side raises the risk of a credit crunch, mainly in the corporate

GROWTH AND PROSPECTS OF SYSTEM BANKING IN ROMANIA. VLAD MARIANA LECTURER PHD, UNIVERSITY OF SUCEAVA, ROMANIA,

GROWTH AND PROSPECTS OF SYSTEM BANKING IN ROMANIA VLAD MARIANA LECTURER PHD, UNIVERSITY OF SUCEAVA, ROMANIA, marianav@seap.usv.ro Abstract: The years of crisis were characterized by a moderation of the

GROWTH AND PROSPECTS OF SYSTEM BANKING IN ROMANIA VLAD MARIANA LECTURER PHD, UNIVERSITY OF SUCEAVA, ROMANIA, marianav@seap.usv.ro Abstract: The years of crisis were characterized by a moderation of the

Erste Group posts net profit of EUR million in H1 17. Press conference 4 August Page 1

Erste Group posts net profit of EUR 624.7 million in H1 17 Press conference 4 August 2017 Page 1 Business environment Central and Eastern Europe is the fastest growing EU region 2017 2018 Real GDP growth

Erste Group posts net profit of EUR 624.7 million in H1 17 Press conference 4 August 2017 Page 1 Business environment Central and Eastern Europe is the fastest growing EU region 2017 2018 Real GDP growth

Bank Austria posts net profit of EUR 59 million for the first quarter

Bank Austria IR Release Günther Stromenger +43 (0) 50505 57232 Vienna, 11 May 2016 Bank Austria s results for the first three months of 2016: Bank Austria posts net profit of EUR 59 million for the first

Bank Austria IR Release Günther Stromenger +43 (0) 50505 57232 Vienna, 11 May 2016 Bank Austria s results for the first three months of 2016: Bank Austria posts net profit of EUR 59 million for the first

CESEE Deleveraging and Credit Monitor 1

CESEE Deleveraging and Credit Monitor 1 June 5, 218 Key Developments in BIS Banks External Positions and Domestic Credit and Key Messages from the CESEE Bank Lending Survey Deleveraging of western banks

CESEE Deleveraging and Credit Monitor 1 June 5, 218 Key Developments in BIS Banks External Positions and Domestic Credit and Key Messages from the CESEE Bank Lending Survey Deleveraging of western banks

Erste Group Bank AG Annual results 2012

Erste Group Bank AG Annual results 2012 Andreas Treichl, Chief Executive Officer Manfred Wimmer, Chief Financial Officer Gernot Mittendorfer, Chief Risk Officer Presentation topics Erste Group s development

Erste Group Bank AG Annual results 2012 Andreas Treichl, Chief Executive Officer Manfred Wimmer, Chief Financial Officer Gernot Mittendorfer, Chief Risk Officer Presentation topics Erste Group s development

R E S U LT S 3 R D Q U A R T E R AN D 9 M O N T H S N O V E M B E R

BRD - GROUP R E S U LT S 3 R D Q U A R T E R AN D 9 M O N T H S 2 0 1 8 9 N O V E M B E R 2 0 1 8 DISCLAIMER The consolidated and separate financial position and income statement for the period ended September

BRD - GROUP R E S U LT S 3 R D Q U A R T E R AN D 9 M O N T H S 2 0 1 8 9 N O V E M B E R 2 0 1 8 DISCLAIMER The consolidated and separate financial position and income statement for the period ended September

BCR achieved an improved quarterly profit consolidating its market share in Q in a continued difficult economic context

BCR achieved an improved quarterly profit consolidating its market share in Q1 2011 in a continued difficult economic context I.HIGHLIGHTS FOR THE BCR GROUP 1 : Improved quarterly results in a still difficult

BCR achieved an improved quarterly profit consolidating its market share in Q1 2011 in a continued difficult economic context I.HIGHLIGHTS FOR THE BCR GROUP 1 : Improved quarterly results in a still difficult

> Central and Eastern Europe A journey through Erste Bank s home market

> Central and Eastern Europe > 4 th Capital Markets Day > Bucharest, > Reinhard Ortner, CFO, Erste Bank > Disclaimer Cautionary note regarding forward-looking statements THE INFORMATION CONTAINED IN THIS

> Central and Eastern Europe > 4 th Capital Markets Day > Bucharest, > Reinhard Ortner, CFO, Erste Bank > Disclaimer Cautionary note regarding forward-looking statements THE INFORMATION CONTAINED IN THIS

Welcome to the Annual General Meeting of Raiffeisen International Bank-Holding AG

Welcome to the Annual General Meeting of Raiffeisen International Bank-Holding AG Agenda Item One Presentation of the adopted financial statements and the management report and of the consolidated financial

Welcome to the Annual General Meeting of Raiffeisen International Bank-Holding AG Agenda Item One Presentation of the adopted financial statements and the management report and of the consolidated financial

Retail Banking - Building a Growth Machine. By Aris Bogdaneris Board Member RI Group. The Current Environment. Slide 1. Slide 2

Retail Banking Building a Growth Machine By Aris Bogdaneris Board Member RI Group Slide 1 Capital Markets Day, September 2008 The Current Environment Slide 2 Capital Markets Day, September 2008 Investor

Retail Banking Building a Growth Machine By Aris Bogdaneris Board Member RI Group Slide 1 Capital Markets Day, September 2008 The Current Environment Slide 2 Capital Markets Day, September 2008 Investor

TWO THOUCEEND AND FIFTEEN

TWO THOUCEEND AND FIFTEEN ANNUAL FINANCIAL REPORT 2015 VIENNA INSURANCE GROUP pursuant to 82 sec. 4 of the Austrian Stock Exchange Act Table of contents GROUP MANAGEMENT REPORT 003 Group management report

TWO THOUCEEND AND FIFTEEN ANNUAL FINANCIAL REPORT 2015 VIENNA INSURANCE GROUP pursuant to 82 sec. 4 of the Austrian Stock Exchange Act Table of contents GROUP MANAGEMENT REPORT 003 Group management report

Strategy and Positioning in Emerging Europe Gerhard Randa Member of the Board of Managing Directors. Berlin, September 16, 2003

Strategy and Positioning in Emerging Europe Gerhard Randa Member of the Board of Managing Directors Berlin, September 16, 2003 Sustained financial turnaround and consistent execution of 2003 transformation

Strategy and Positioning in Emerging Europe Gerhard Randa Member of the Board of Managing Directors Berlin, September 16, 2003 Sustained financial turnaround and consistent execution of 2003 transformation

Leasing in Europe State of Play and Outlook. Bucharest, Romania 19 November

Leasing in Europe State of Play and Outlook Bucharest, Romania 19 November Agenda o About Leaseurope o Leasing in Europe o Leased Assets & Customers o State of the Industry o Industry Performance o Business

Leasing in Europe State of Play and Outlook Bucharest, Romania 19 November Agenda o About Leaseurope o Leasing in Europe o Leased Assets & Customers o State of the Industry o Industry Performance o Business

Transform UniCredit Company Profile as at June, 2018

Transform 2019 UniCredit Company Profile as at June, 2018 Our vision is to be One Bank, One UniCredit. UniCredit is and will remain a simple successful pan-european Commercial Bank, with a fully plugged

Transform 2019 UniCredit Company Profile as at June, 2018 Our vision is to be One Bank, One UniCredit. UniCredit is and will remain a simple successful pan-european Commercial Bank, with a fully plugged

Bulgaria in the EU: Challenges and opportunities

Bulgaria in the EU: Challenges and opportunities 60 days before EU: what to expect, what to do? Sofia, October 18, 2006 Maria Laura Lanzeni Head of Emerging Markets Global Risk Analysis Think tank of Deutsche

Bulgaria in the EU: Challenges and opportunities 60 days before EU: what to expect, what to do? Sofia, October 18, 2006 Maria Laura Lanzeni Head of Emerging Markets Global Risk Analysis Think tank of Deutsche

Quarterly Financial Accounts Household net worth reaches new peak in Q Irish Household Net Worth

Quarterly Financial Accounts Q4 2017 4 May 2018 Quarterly Financial Accounts Household net worth reaches new peak in Q4 2017 Household net worth rose by 2.1 per cent in Q4 2017. It now exceeds its pre-crisis

Quarterly Financial Accounts Q4 2017 4 May 2018 Quarterly Financial Accounts Household net worth reaches new peak in Q4 2017 Household net worth rose by 2.1 per cent in Q4 2017. It now exceeds its pre-crisis

Summary of the June 2010 Financial Stability RevieW

Summary of the June 21 Financial Stability RevieW The primary objective of the s Financial Stability Review (FSR) is to identify the main sources of risk to the stability of the euro area financial system

Summary of the June 21 Financial Stability RevieW The primary objective of the s Financial Stability Review (FSR) is to identify the main sources of risk to the stability of the euro area financial system

Best is yet to come Romania CFO Survey 2016

Best is yet to come Romania CFO Survey 2016 Romania 2016 results 7th edition Contents 5. Introduction 7. CFO Survey key findings in Romania 12. Economic outlook 22. Business environment outlook 34. Company

Best is yet to come Romania CFO Survey 2016 Romania 2016 results 7th edition Contents 5. Introduction 7. CFO Survey key findings in Romania 12. Economic outlook 22. Business environment outlook 34. Company

The New Role of Growth Financing

OMV Aktiengesellschaft The New Role of Growth Financing Conference on European Economic Integration Vienna, 15 November 2010 Wolfgang Ruttenstorfer CEO and Chairman of the Executive Board OMV Aktiengesellschaft

OMV Aktiengesellschaft The New Role of Growth Financing Conference on European Economic Integration Vienna, 15 November 2010 Wolfgang Ruttenstorfer CEO and Chairman of the Executive Board OMV Aktiengesellschaft

THE GREEK BANKING SYSTEM

THE GREEK BANKING SYSTEM During the past two decades, the Greek banking and financial system has undergone momentous transformations, amounting to what the Financial Times once characterized as no less

THE GREEK BANKING SYSTEM During the past two decades, the Greek banking and financial system has undergone momentous transformations, amounting to what the Financial Times once characterized as no less

The Architectural Profession in Europe 2012

The Architectural Profession in Europe 2012 - A Sector Study Commissioned by the Architects Council of Europe Chapter 2: Architecture the Market December 2012 2 Architecture - the Market The Construction

The Architectural Profession in Europe 2012 - A Sector Study Commissioned by the Architects Council of Europe Chapter 2: Architecture the Market December 2012 2 Architecture - the Market The Construction

Erste Group Bank AG H results presentation 30 July 2010, Vienna

Erste Group Bank AG H1 2010 results presentation, Vienna Andreas Treichl, Chief Executive Officer Manfred Wimmer, Chief Financial Officer Bernhard Spalt, Chief Risk Officer Erste Group business snapshot

Erste Group Bank AG H1 2010 results presentation, Vienna Andreas Treichl, Chief Executive Officer Manfred Wimmer, Chief Financial Officer Bernhard Spalt, Chief Risk Officer Erste Group business snapshot

Raiffeisen Bank International Q1/2016 Results

Raiffeisen Bank International Q1/2016 Results Disclaimer Certain statements contained herein may be statements of future expectations and other forward-looking statements, which are based on management's

Raiffeisen Bank International Q1/2016 Results Disclaimer Certain statements contained herein may be statements of future expectations and other forward-looking statements, which are based on management's

2005 Results March 6th, 2006

2005 Results March 6 th, 2006 Foreword! 2005 data are preliminary results and IAS/IFRS compliant. The Financial Statements, that will be approved by the Board of Directors on March 28 th, 2006 and submitted

2005 Results March 6 th, 2006 Foreword! 2005 data are preliminary results and IAS/IFRS compliant. The Financial Statements, that will be approved by the Board of Directors on March 28 th, 2006 and submitted

UniCredit International Investors Conference January 2008, Kitzbühel

UniCredit International Investors Conference 20-22 January 2008, Kitzbühel Operating in a challenging environment Gabriele Werzer, Head of IR, Erste Group Disclaimer Cautionary note regarding forward-looking

UniCredit International Investors Conference 20-22 January 2008, Kitzbühel Operating in a challenging environment Gabriele Werzer, Head of IR, Erste Group Disclaimer Cautionary note regarding forward-looking

Dynamic and Continuous Expansion of the Network

Country Overview Herbert Stepic, CEO Dynamic and Continuous Expansion of the Network Successful greenfield strategy Hungary Poland Czech Republic Bulgaria Russia Ukraine Serbia Slovakia Croatia Romania

Country Overview Herbert Stepic, CEO Dynamic and Continuous Expansion of the Network Successful greenfield strategy Hungary Poland Czech Republic Bulgaria Russia Ukraine Serbia Slovakia Croatia Romania

INVESTMENT FUNDS AND ASSET MANAGEMENT MARKET IN POLAND,

INVESTMENT FUNDS AND ASSET MANAGEMENT MARKET IN POLAND, 2017 2019 by September 2017 Version: 17.4 Report Order Form / formularz zamówienia We order the following report: Investment Funds and the Asset

INVESTMENT FUNDS AND ASSET MANAGEMENT MARKET IN POLAND, 2017 2019 by September 2017 Version: 17.4 Report Order Form / formularz zamówienia We order the following report: Investment Funds and the Asset

PwC. Central & Eastern European Mergers & Acquisition Survey 2005* Romania Report. *connectedthinking. Introduction

Central & Eastern European Mergers & Acquisition Survey 2005* Romania Report Introduction It is a pleasure to present to you our latest report on the mergers and acquisitions (M&A) market in Romania in

Central & Eastern European Mergers & Acquisition Survey 2005* Romania Report Introduction It is a pleasure to present to you our latest report on the mergers and acquisitions (M&A) market in Romania in

Press Conference. VIENNA INSURANCE GROUP 2016 Preliminary Results. Based on preliminary unaudited data. Vienna, 23 March 2017

Press Conference VIENNA INSURANCE GROUP 2016 Preliminary Results Based on preliminary unaudited data Vienna, 23 March 2017 Vienna Insurance Group A reliable partner in times of dynamic change HIGHLIGHTS

Press Conference VIENNA INSURANCE GROUP 2016 Preliminary Results Based on preliminary unaudited data Vienna, 23 March 2017 Vienna Insurance Group A reliable partner in times of dynamic change HIGHLIGHTS

Improved underwriting result mainly driven by continued reduction of operating expenses

UNIQA Insurance Group AG 1H14 Improved underwriting result mainly driven by continued reduction of operating expenses 27 Aug 2014 Hannes Bogner, CFO Kurt Svoboda, CRO 1H14 Highlights Group Strategy & Results

UNIQA Insurance Group AG 1H14 Improved underwriting result mainly driven by continued reduction of operating expenses 27 Aug 2014 Hannes Bogner, CFO Kurt Svoboda, CRO 1H14 Highlights Group Strategy & Results

Erste Group results presentation 29 October 2010, London

Erste Group 1-9 21 results presentation, Strong operating income and strict cost control Andreas Treichl, Chief Executive Officer Manfred Wimmer, Chief Financial Officer Bernhard Spalt, Chief Risk Officer

Erste Group 1-9 21 results presentation, Strong operating income and strict cost control Andreas Treichl, Chief Executive Officer Manfred Wimmer, Chief Financial Officer Bernhard Spalt, Chief Risk Officer

R E S U LT S 1 ST Q U A R T E R M A Y

BRD - GROUP R E S U LT S 1 ST Q U A R T E R 2 0 1 8 M A Y 2 0 1 8 DISCLAIMER The consolidated and separate financial position and income statement for the period ended March 31, 2018 were examined by the

BRD - GROUP R E S U LT S 1 ST Q U A R T E R 2 0 1 8 M A Y 2 0 1 8 DISCLAIMER The consolidated and separate financial position and income statement for the period ended March 31, 2018 were examined by the

6 th Capital Markets Day 12 December 2008, Vienna

ERSTE GROUP, Vienna Solid performance in a Edit Papp, CEO, Erste Bank Hungary Doing business in Hungary Attractive economy evidenced by high capital investments/eu funds and World Bank recognition Since

ERSTE GROUP, Vienna Solid performance in a Edit Papp, CEO, Erste Bank Hungary Doing business in Hungary Attractive economy evidenced by high capital investments/eu funds and World Bank recognition Since

HALF-YEAR FINANCIAL REPORT 2014 / UNIQA GROUP. Deliver.

HALF-YEAR FINANCIAL REPORT 2014 / UNIQA GROUP Deliver. 2 GROUP KEY FIGURES Group Key Figures Figures in million 1 6/2014 1 6/2013 Change Premiums written 2,856.2 2,725.2 + 4.8 % Savings portion from unit-

HALF-YEAR FINANCIAL REPORT 2014 / UNIQA GROUP Deliver. 2 GROUP KEY FIGURES Group Key Figures Figures in million 1 6/2014 1 6/2013 Change Premiums written 2,856.2 2,725.2 + 4.8 % Savings portion from unit-

FINANCEABILITY OF INFRASTRUCTURE PROJECTS IN THE CZECH REPUBLIC

THE CZECH PPP KICK-OFF TRANSPORT INFRASTRUCTURE FINANCEABILITY OF INFRASTRUCTURE PROJECTS IN THE CZECH REPUBLIC Overview of current financing market DISCLAIMER This document has been prepared by Société

THE CZECH PPP KICK-OFF TRANSPORT INFRASTRUCTURE FINANCEABILITY OF INFRASTRUCTURE PROJECTS IN THE CZECH REPUBLIC Overview of current financing market DISCLAIMER This document has been prepared by Société

Current health expenditure increased 3.0% in 2017

Health Satellite Account 15 17Pe June 18 Current health expenditure increased 3. in 17 Current health expenditure continued to increase in 17 (+ 3.), at a slower pace than GDP (+ 4.1), decelerating compared

Health Satellite Account 15 17Pe June 18 Current health expenditure increased 3. in 17 Current health expenditure continued to increase in 17 (+ 3.), at a slower pace than GDP (+ 4.1), decelerating compared

Turkish Economy and Banking Sector. Correlative Growth

Turkish Economy and Banking Sector Correlative Growth Tanju YÜKSEL February, 2008 1 Turkey at a glance Size and economic situation Largest Emerging European market in terms of GDP and population Future

Turkish Economy and Banking Sector Correlative Growth Tanju YÜKSEL February, 2008 1 Turkey at a glance Size and economic situation Largest Emerging European market in terms of GDP and population Future

InnovFin SME Guarantee

InnovFin SME Guarantee Implementation Update Reporting date: 30/09/2017 Disclaimer This presentation contains general information about the implementation results of InnovFin SME Guarantee, a facility

InnovFin SME Guarantee Implementation Update Reporting date: 30/09/2017 Disclaimer This presentation contains general information about the implementation results of InnovFin SME Guarantee, a facility

BANK OF ALBANIA MONETARY POLICY REPORT

MONETARY POLICY REPORT October 2005 MONETARY POLICY REPORT OCTOBER 2005-1 - MONETARY POLICY REPORT October 2005-2 - MONETARY POLICY REPORT October 2005 C O N T E N T S I Main highlights 5 II Inflation

MONETARY POLICY REPORT October 2005 MONETARY POLICY REPORT OCTOBER 2005-1 - MONETARY POLICY REPORT October 2005-2 - MONETARY POLICY REPORT October 2005 C O N T E N T S I Main highlights 5 II Inflation

European Private Equity Outlook Frankfurt am Main, February 2015

European Private Equity Outlook 2015 Frankfurt am Main, February 2015 Preliminary remarks Our sixth European Private Equity ("PE") Outlook reveals how experts view the market and its development in 2015

European Private Equity Outlook 2015 Frankfurt am Main, February 2015 Preliminary remarks Our sixth European Private Equity ("PE") Outlook reveals how experts view the market and its development in 2015

Hungary s balance of payments account remained positive in Q4 2017

Hungary s balance of payments account remained positive in Q4 Persistently positive real economic trends, among them export and import growth, have caused Hungary s balance of payments account to remain

Hungary s balance of payments account remained positive in Q4 Persistently positive real economic trends, among them export and import growth, have caused Hungary s balance of payments account to remain

Investment Funds and Asset Management in Poland,

Investment Funds and Asset Management in Poland, 2018 2020 by September 2018 Version: 18.3 Report Order Form / formularz zamówienia / We order the following report: Investment Funds and the Asset Management

Investment Funds and Asset Management in Poland, 2018 2020 by September 2018 Version: 18.3 Report Order Form / formularz zamówienia / We order the following report: Investment Funds and the Asset Management

Monetary Policy and the Stability of the Banking Systems in the Countries of the Region - A Decade After the Lehman Brothers Bankruptcy

Monetary Policy and the Stability of the Banking Systems in the Countries of the Region - A Decade After the Lehman Brothers Bankruptcy Maja Kadievska Vojnovikj Vice Governor Sector of Financial Market

Monetary Policy and the Stability of the Banking Systems in the Countries of the Region - A Decade After the Lehman Brothers Bankruptcy Maja Kadievska Vojnovikj Vice Governor Sector of Financial Market

IAB Europe AdEx Benchmark 2014

IAB Europe AdEx Benchmark 2014 About the study A meta analysis of online ad spend in Europe GROSS NET RATECARD Revenue Billed Revenue Billed No Agency commissions Campaigns x Ratecard Submissions from

IAB Europe AdEx Benchmark 2014 About the study A meta analysis of online ad spend in Europe GROSS NET RATECARD Revenue Billed Revenue Billed No Agency commissions Campaigns x Ratecard Submissions from

STAT/14/64 23 April 2014

STAT/14/64 23 April 2014 Provision of deficit and debt data for 2013 - first notification Euro area and EU28 government deficit at 3.0% and 3.3% of GDP respectively Government debt at 92.6% and 87.1% In

STAT/14/64 23 April 2014 Provision of deficit and debt data for 2013 - first notification Euro area and EU28 government deficit at 3.0% and 3.3% of GDP respectively Government debt at 92.6% and 87.1% In

34 th Associates Meeting - Andorra, 25 May Item 5: Evolution of economic governance in the EU

34 th Associates Meeting - Andorra, 25 May 2012 - Item 5: Evolution of economic governance in the EU Plan of the Presentation 1. Fiscal and economic coordination: how did it start? 2. Did it work? 3. Five

34 th Associates Meeting - Andorra, 25 May 2012 - Item 5: Evolution of economic governance in the EU Plan of the Presentation 1. Fiscal and economic coordination: how did it start? 2. Did it work? 3. Five

REPORT ON THE ANALYSIS OF FOREIGN INSURANCE BUSINESS OF AUSTRIAN INSURANCE GROUPS. Division II/4 Team Supervision of Insurance Groups

REPORT ON THE ANALYSIS OF FOREIGN INSURANCE BUSINESS OF AUSTRIAN INSURANCE GROUPS Division II/4 Team Supervision of Insurance Groups 24.01.2018 CONTENT Management Summary... 3 1. Analysis of Foreign Insurance

REPORT ON THE ANALYSIS OF FOREIGN INSURANCE BUSINESS OF AUSTRIAN INSURANCE GROUPS Division II/4 Team Supervision of Insurance Groups 24.01.2018 CONTENT Management Summary... 3 1. Analysis of Foreign Insurance

REBOUND OF THE ROMANIAN CARD MARKET AFTER THE CRISIS AND ITS IMPACT ON THE BANKING PROFITABILITY

Scientific Bulletin Economic Sciences, Volume 16/ Issue 1 REBOUND OF THE ROMANIAN CARD MARKET AFTER THE CRISIS AND ITS IMPACT ON THE BANKING PROFITABILITY Magdalena RADULESCU 1, Tatiana ZAMFIROIU (PAUN)

Scientific Bulletin Economic Sciences, Volume 16/ Issue 1 REBOUND OF THE ROMANIAN CARD MARKET AFTER THE CRISIS AND ITS IMPACT ON THE BANKING PROFITABILITY Magdalena RADULESCU 1, Tatiana ZAMFIROIU (PAUN)

SEE macroeconomic outlook Recovery gains traction, fiscal discipline improving. Alen Kovac, Chief Economist EBC May 2016 Ljubljana

SEE macroeconomic outlook Recovery gains traction, fiscal discipline improving Alen Kovac, Chief Economist EBC May 216 Ljubljana Real economy highlights Recent GDP track record reveals more favorable footprint

SEE macroeconomic outlook Recovery gains traction, fiscal discipline improving Alen Kovac, Chief Economist EBC May 216 Ljubljana Real economy highlights Recent GDP track record reveals more favorable footprint

Private Equity Business outlook in the time of change in the CEE Region

Private Equity Business outlook in the time of change in the CEE Region Prepared for Private Equity Forum & Awards Gala 2 Macroeconomic overview Poland and the CEE Region 3 Region of Central and Eastern

Private Equity Business outlook in the time of change in the CEE Region Prepared for Private Equity Forum & Awards Gala 2 Macroeconomic overview Poland and the CEE Region 3 Region of Central and Eastern

Net profit raises to EUR 496.3m driven by strong operating profit and lower risk costs

Erste Group Bank AG H1 2011 results presentation, Vienna Net profit raises to EUR 496.3m driven by strong operating profit and lower risk costs Andreas Treichl, Chief Executive Officer Franz Hochstrasser,

Erste Group Bank AG H1 2011 results presentation, Vienna Net profit raises to EUR 496.3m driven by strong operating profit and lower risk costs Andreas Treichl, Chief Executive Officer Franz Hochstrasser,

> eská spoitelna. Is 15% loan growth in CS core business sustainable? How will we maintain ROE of >20% after tax? > 2 nd Capital Markets Day

> eská spoitelna Is 15% loan growth in CS core business sustainable? How will we maintain ROE of >20% after tax? > 2 nd Capital Markets Day > Budapest > Jack Stack, CEO of!eská spo#itelna > Macroeconomic

> eská spoitelna Is 15% loan growth in CS core business sustainable? How will we maintain ROE of >20% after tax? > 2 nd Capital Markets Day > Budapest > Jack Stack, CEO of!eská spo#itelna > Macroeconomic

NOTE. for the Interparliamentary Meeting of the Committee on Budgets

NOTE for the Interparliamentary Meeting of the Committee on Budgets THE ROLE OF THE EU BUDGET TO SUPPORT MEMBER STATES IN ACHIEVING THEIR ECONOMIC OBJECTIVES AS AGREED WITHIN THE FRAMEWORK OF THE EUROPEAN

NOTE for the Interparliamentary Meeting of the Committee on Budgets THE ROLE OF THE EU BUDGET TO SUPPORT MEMBER STATES IN ACHIEVING THEIR ECONOMIC OBJECTIVES AS AGREED WITHIN THE FRAMEWORK OF THE EUROPEAN

FDI in Central, East and Southeast Europe: Declines due to Disinvestment

Wiener Institut für Internationale Wirtschaftsvergleiche The Vienna Institute for International Economic Studies www.wiiw.ac.at wiiw FDI Report 218 FDI in Central, East and Southeast Europe: Declines due

Wiener Institut für Internationale Wirtschaftsvergleiche The Vienna Institute for International Economic Studies www.wiiw.ac.at wiiw FDI Report 218 FDI in Central, East and Southeast Europe: Declines due

Morgan Stanley Annual European Financials Conference

Morgan Stanley Annual European Financials Conference March 2015, London Erste Group Transforming business models: digital, regulation and macro challenges Gernot Mittendorfer, CFO Erste Group Disclaimer

Morgan Stanley Annual European Financials Conference March 2015, London Erste Group Transforming business models: digital, regulation and macro challenges Gernot Mittendorfer, CFO Erste Group Disclaimer

MIND THE CREDIT GAP. Spring 2015 Regional Economic Issues Report on Central, Eastern and Southeastern Europe (CESEE) recovery. repair.

recovery. repair.") Spring 215 Regional Economic Issues Report on Central, Eastern and Southeastern Europe (CESEE) repair recovery MIND THE CREDIT GAP downturn expansion May, 215 Growth Divergence in 214 Quarterly GDP Growth,

Spring 215 Regional Economic Issues Report on Central, Eastern and Southeastern Europe (CESEE) repair recovery MIND THE CREDIT GAP downturn expansion May, 215 Growth Divergence in 214 Quarterly GDP Growth,

Is economic growth sustainable in Romania?

MPRA Munich Personal RePEc Archive Is economic growth sustainable in Romania? George Ciobanu and Andreea Maria Ciobanu 18. March 2008 Online at http://mpra.ub.uni-muenchen.de/7810/ MPRA Paper No. 7810,

MPRA Munich Personal RePEc Archive Is economic growth sustainable in Romania? George Ciobanu and Andreea Maria Ciobanu 18. March 2008 Online at http://mpra.ub.uni-muenchen.de/7810/ MPRA Paper No. 7810,

BANCA TRANSILVANIA 2016 Preliminary Financial Results. February 2017

1 BANCA TRANSILVANIA 2016 Preliminary Financial Results February 2017 DISCLAIMER 2 The information contained in the present document has not been independently verified and no representation or warranty

1 BANCA TRANSILVANIA 2016 Preliminary Financial Results February 2017 DISCLAIMER 2 The information contained in the present document has not been independently verified and no representation or warranty

6 th Capital Markets Day 12 December 2008, Vienna

, Vienna An in-depth look at assets and asset quality Bernhard Spalt, Chief Risk Officer Presentation topics Analysing customer loans Overview CEE loan book in detail Real estate loans in detail Non-performing

, Vienna An in-depth look at assets and asset quality Bernhard Spalt, Chief Risk Officer Presentation topics Analysing customer loans Overview CEE loan book in detail Real estate loans in detail Non-performing

Statistics Brief. Inland transport infrastructure investment on the rise. Infrastructure Investment. August

Statistics Brief Infrastructure Investment August 2017 Inland transport infrastructure investment on the rise After nearly five years of a downward trend in inland transport infrastructure spending, 2015

Statistics Brief Infrastructure Investment August 2017 Inland transport infrastructure investment on the rise After nearly five years of a downward trend in inland transport infrastructure spending, 2015

> Erste Bank Group Strategy and outlook

> Erste Bank Group > 3rd Capital Markets Day > Prague, 16 September 2005 > Andreas Treichl CEO of Erste Bank Group > Presentation topics 1. Introduction to Novosadska banka 2. Erste Bank s region 3. Strategic

> Erste Bank Group > 3rd Capital Markets Day > Prague, 16 September 2005 > Andreas Treichl CEO of Erste Bank Group > Presentation topics 1. Introduction to Novosadska banka 2. Erste Bank s region 3. Strategic

Single Market Scoreboard

Single Market Scoreboard Performance per Member State Romania (Reporting period: 2017) Transposition of law In 2016, the Member States had to transpose 66 new directives, which represents a large increase

Single Market Scoreboard Performance per Member State Romania (Reporting period: 2017) Transposition of law In 2016, the Member States had to transpose 66 new directives, which represents a large increase

Mark Allen. Market power in CEE banking sectors and the impact of the global financial crisis. Discussion of Paper by Efthyvoulou and Yildirim

Market power in CEE banking sectors and the impact of the global financial crisis Discussion of Paper by Efthyvoulou and Yildirim CASE, Warsaw, February 15, 2013 Mark Allen Senior IMF Resident Representative

Market power in CEE banking sectors and the impact of the global financial crisis Discussion of Paper by Efthyvoulou and Yildirim CASE, Warsaw, February 15, 2013 Mark Allen Senior IMF Resident Representative

ANALYSIS OF NON-PERFORMING LOANS FOR BANKS IN CENTRAL AND EASTERN EUROPE BASED ON THEIR OWNERSHIP STRUCTURE

International Journal of Economics, Commerce and Management United Kingdom Vol. V, Issue 8, August 217 http://ijecm.co.uk/ ISSN 2348 386 ANALYSIS OF NON-PERFORMING LOANS FOR BANKS IN CENTRAL AND EASTERN

International Journal of Economics, Commerce and Management United Kingdom Vol. V, Issue 8, August 217 http://ijecm.co.uk/ ISSN 2348 386 ANALYSIS OF NON-PERFORMING LOANS FOR BANKS IN CENTRAL AND EASTERN

THE FUTURE OF CASH AND PAYMENTS

THE FUTURE OF CASH AND PAYMENTS Retail Banking Research January 2010 CONFIDENTIALITY AND COPYRIGHT This report is published by Retail Banking Research Ltd (RBR). The information and data within this report

THE FUTURE OF CASH AND PAYMENTS Retail Banking Research January 2010 CONFIDENTIALITY AND COPYRIGHT This report is published by Retail Banking Research Ltd (RBR). The information and data within this report

Slovakia: Eurozone country with high growth potential

Erste Group 8 th Capital Markets Day, Jozef Síkela, CEO, Slovenská sporiteľňa Disclaimer Cautionary note regarding forward-looking statements THE INFORMATION CONTAINED IN THIS DOCUMENT HAS NOT BEEN INDEPENDENTLY

Erste Group 8 th Capital Markets Day, Jozef Síkela, CEO, Slovenská sporiteľňa Disclaimer Cautionary note regarding forward-looking statements THE INFORMATION CONTAINED IN THIS DOCUMENT HAS NOT BEEN INDEPENDENTLY

Non-Performing Loans in CESEE

Non-Performing Loans in CESEE Vienna, September 23, 2014 James Roaf Senior Resident Representative IMF Regional Office for Central and Eastern Europe, Warsaw High NPLs ratios need to be addressed Boom-bust

Non-Performing Loans in CESEE Vienna, September 23, 2014 James Roaf Senior Resident Representative IMF Regional Office for Central and Eastern Europe, Warsaw High NPLs ratios need to be addressed Boom-bust

STAT/07/55 23 April 2007

STAT/07/55 23 April 2007 Provision of deficit and debt data for 2006 Euro area and EU27 government deficit at 1.6% and 1.7% of GDP respectively Government debt at 69.0% and 61.7% In 2006, the government

STAT/07/55 23 April 2007 Provision of deficit and debt data for 2006 Euro area and EU27 government deficit at 1.6% and 1.7% of GDP respectively Government debt at 69.0% and 61.7% In 2006, the government