Everything you always wanted to know about Basel II in 15 minutes

|

|

|

- Shannon Farmer

- 5 years ago

- Views:

Transcription

1 Everything you always wanted to know about Basel II in 15 minutes (a real estate perspective) Erik Kersten Senior Policy Advisor Supervisory Policy Quantitative Risk Management Views and opinions expressed in this presentation are those of the author and do not necessarily reflect the position of the Nederlandsche Bank.

2 Overview of Basel II Outline Real estate issues under Basel II

3 Capital requirements under Basel I Loans 100 (Risk weight 100%) 100 Owners equity 8 Deposits Worst case Performing Loans 92 Loans losses (8) 92 Owners equity 0 Deposits Required Capital = (Risk Weight * Exposure value)*8%

4 Capital requirements under Basel I Mortgage Loans 100 (Risk weight 50%) 100 Owners equity 4 Deposits Worst case Performing Loans 96 Loan losses (4) 96 Owners equity 0 Deposits 96 96

5 Mortgage collateral under Basel I Residential mortgages: if LtV is lower then threshold: lower risk weight, less capital No recognition in capital of commercial real estate (with some exceptions) No realistic assumptions Capital treatment fuelled MBS-market

6 Purposes of the new capital accord a comprehensive approach to addressing risks Risk sensitive capital requirements Promote soundness and safety of the financial system Enhance competitive equality Accommodate industry best practice Result: Widen acceptance of collateral types used in practise and widen acceptance of internal models to Credit risk & Oprisk

7 Structure of Basel II

8 Menu of approaches (pillar 1) For measuring Credit Risk: Standardised Approach Foundation Internal Ratings-based Approach Advanced Internal Ratings-based Approach For measuring Operational Risk: Basic Indicator Approach Standardised Approach Advanced Measurements Approach For measuring Market Risk: Standardised Approach Internal Models Approach

9 Credit risk (Pillar I) The risk of loss due to the fact that an obligor will not meet its credit obligations in full Required Capital = (RW * Exposure value)*8% (no change!) Standardised approach RW Based on External ratings (Moody s, S&P, local rating agencies) Internal ratings based approach RW based on Internal ratings (banks own assessment)

10 Internal Ratings Based Approach Capital requirements for an exposure based on VaR and function of: PD, LGD, EAD and M These functions are given by Accord

11 IRB: the formulae look up PD Φ 1 ( PD) R 1 1 K = LGD ( Φ + Φ ( 0.999) { PD ) 1+ M 2.5 { b *1,06 1 R 1 R 1 1.5* b look up 99.9% account for correlation in the normal distributi on correct for maturity accountfor EL calculate PD stressed at 99.9% RW = K *12, Correlation ( ) 0.12 e PD e PD R = e e For Corporates, Banks & Sovereigns SME correction : R ranging from 0.08 to 0.20 Retail : Mortgages : R = 0.15; credit cards : R = 0.04 and other retail : R ranging from 0.03 to 0.16 ( ln( PD) ) Maturity adjustment( b ) = Only for Corporates,Banks&Sovereigns 2

12 internal refers to the inputs Foundation IRB Advanced IRB Probability of default Own estimates Loss Given Default Supervisory formula Own estimates Exposure at Default Supervisory formula Own estimates Maturity Bank s own estimates or 2.5 yrs Own estimates

13 RW vs PD RW-curves (PD tot 10%) (LGD=45%, Mortgages LGD= 10% M=2,5) 250,00% 200,00% RW 150,00% 100,00% Corporates Corporates(small) mortgages QRE Other Retail 50,00% 0,00% 0,00% 2,00% 4,00% 6,00% 8,00% 10,00% 12,00% PD

14 Conclusion IRB is a more risk sensitive way of calculating capital requirements based on statistical properties of portfolio and enhances internal management of loans

15 Real estate in Basel II

16 Approaches in pillar 1 Measuring Credit Risk in mortgage lending Residential real estate: Standardised Approach RW down from 50% to 35% Monitoring LtV-ratio s (at least every 3 years) Advanced Internal Ratings-based Approach banks now have to estimate PD, LGD & EAD for their retail mortgages (NB collateral management conditions, e.g. LtV-monitoring process)

17 Approaches in pillar 1 Measuring Credit Risk in mortgage lending Commercial real estate: Standardised Approach RW based on external rating (non-rated => RW 100% Commercial real estate eligible as collateral (NB conditions: e.g. yearly LtV monitoring) Foundation Internal Ratings-based Approach RW based on internal estimates of PD Commercial real estate eligible as collateral (NB collateral management conditions, e.g. yearly LtV-monitoring process!) Advanced Internal Ratings-based Approach RW based on internal estimates of PD, LGD, EAD (&M) Commercial real estate eligible as collateral (NB same conditions, but more freedom in way of meeting those conditions)

18 Approach in Pillar 2 Banks are free to develop their own models Ensuring sound internal processes to assess risks and capital adequacy Active dialogue between banks and their supervisors, Identify deficiencies Take prompt and decisive action

19 Focus on IRB Most mortgages will probably be subject to IRBregime (Bigger banks use IRB)

20 What information do we need? How good is the obligor Probability of default; PD What determines a PD? Relation between PD and LtV (low LtV tend to have lower PD?)

21 What information do we need? How much will we recover after default Loss given default; LGD What determines a LGD? Relation between LGD and LtV LGD is more then Loans Current Market Value! economic loss: recovery value, time & costs, down turn effect (remember, we re talking UL)

22 What information do we need? How much money is the obligor likely to owe us when a default occurs Exposure at default; EAD (Credit Conversion Factor) What determines an EAD? All kind of options with mortgage-lending

23 LGD: strong effect on RW LGD = RW Mortgage RW vs PD, at different LGD levels 250,00% 200,00% 150,00% RW LGD = 45% LGD = 25% LGD = 10% 100,00% 50,00% 0,00% 0,00% 1,00% 2,00% 3,00% 4,00% 5,00% 6,00% 7,00% 8,00% 9,00% PD

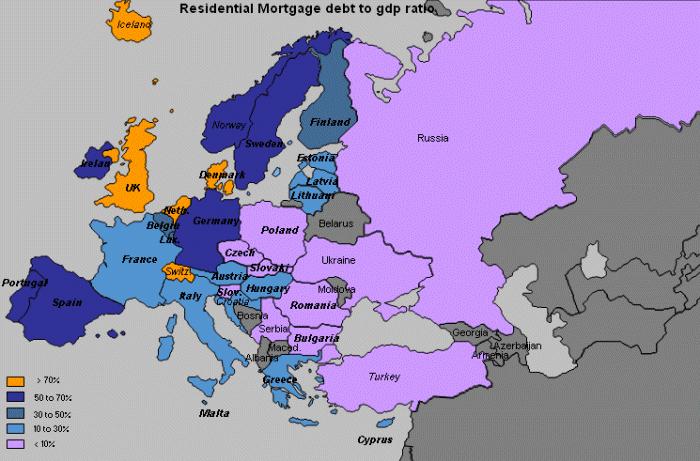

24 Importance?

25 Importance? Overview of EU residential mortgage markets 2005 Netherlands Denmark Switzerland Iceland UK US Ireland Sweden Portugal Norway Spain Germany EU15 EU 25 Finland Luxembourg Malta Belgium France Greece Estonia Austria Latvia Italy Cyprus Croatia Lithuania Hungary Slovakia 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Mortgage Debt to GDP ratio Mortgage debt per capita right hand scale Czech Republic Poland Slovenia Bulgaria Turkey Romania Serbia Russia Ukraine

26 Importance? in 1000 Gemiddelde koopsom en hypotheeksom (per kw) in % Koopsom 270 Hypotheeksom prijsmutatie j/j rechter as ratio Gemiddelde LTV (per kwartaal) 4e kw Bron: Kadaster Bron: Kadaster

27 Mortgage lending important? Yes

Spain France. England Netherlands. Wales Ukraine. Republic of Ireland Czech Republic. Romania Albania. Serbia Israel. FYR Macedonia Latvia

Germany Belgium Portugal Spain France Switzerland Italy England Netherlands Iceland Poland Croatia Slovakia Russia Austria Wales Ukraine Sweden Bosnia-Herzegovina Republic of Ireland Czech Republic Turkey

Germany Belgium Portugal Spain France Switzerland Italy England Netherlands Iceland Poland Croatia Slovakia Russia Austria Wales Ukraine Sweden Bosnia-Herzegovina Republic of Ireland Czech Republic Turkey

EU-28 RECOVERED PAPER STATISTICS. Mr. Giampiero MAGNAGHI On behalf of EuRIC

EU-28 RECOVERED PAPER STATISTICS Mr. Giampiero MAGNAGHI On behalf of EuRIC CONTENTS EU-28 Paper and Board: Consumption and Production EU-28 Recovered Paper: Effective Consumption and Collection EU-28 -

EU-28 RECOVERED PAPER STATISTICS Mr. Giampiero MAGNAGHI On behalf of EuRIC CONTENTS EU-28 Paper and Board: Consumption and Production EU-28 Recovered Paper: Effective Consumption and Collection EU-28 -

Approach to Employment Injury (EI) compensation benefits in the EU and OECD

compensation benefits in the EU and OECD") Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Bank of Cyprus Public Company LTD Actual results at 31 December 2010 million EUR, % Operating profit before impairments 733

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Bank of Cyprus Public Company LTD Actual results at 31 December 2010 million EUR, % Operating profit before impairments 733

EU BUDGET AND NATIONAL BUDGETS

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT ON BUDGETARY AFFAIRS EU BUDGET AND NATIONAL BUDGETS 1999-2009 October 2010 INDEX Foreward 3 Table 1. EU and National budgets 1999-2009; EU-27

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT ON BUDGETARY AFFAIRS EU BUDGET AND NATIONAL BUDGETS 1999-2009 October 2010 INDEX Foreward 3 Table 1. EU and National budgets 1999-2009; EU-27

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE REGIONS

EUROPEAN COMMISSION Brussels,.4.29 COM(28) 86 final/ 2 ANNEXES to 3 ANNEX to the REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE

EUROPEAN COMMISSION Brussels,.4.29 COM(28) 86 final/ 2 ANNEXES to 3 ANNEX to the REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE

Borderline cases for salary, social contribution and tax

Version Abstract 1 (5) 2015-04-21 Veronica Andersson Salary and labour cost statistics Borderline cases for salary, social contribution and tax (Workshop on Labour Cost Survey, Rome, Italy 5-6 May 2015)

Version Abstract 1 (5) 2015-04-21 Veronica Andersson Salary and labour cost statistics Borderline cases for salary, social contribution and tax (Workshop on Labour Cost Survey, Rome, Italy 5-6 May 2015)

Live Long and Prosper? Demographic Change and Europe s Pensions Crisis. Dr. Jochen Pimpertz Brussels, 10 November 2015

Live Long and Prosper? Demographic Change and Europe s Pensions Crisis Dr. Jochen Pimpertz Brussels, 10 November 2015 Old-age-dependency ratio, EU28 45,9 49,4 50,2 39,0 27,5 31,8 2013 2020 2030 2040 2050

Live Long and Prosper? Demographic Change and Europe s Pensions Crisis Dr. Jochen Pimpertz Brussels, 10 November 2015 Old-age-dependency ratio, EU28 45,9 49,4 50,2 39,0 27,5 31,8 2013 2020 2030 2040 2050

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Jyske Bank Actual results at 31 December 2010 million EUR, % Operating profit before impairments 373 Impairment losses on financial

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Jyske Bank Actual results at 31 December 2010 million EUR, % Operating profit before impairments 373 Impairment losses on financial

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Deutsche Bank AG Actual results at 31 December 2010 million EUR, % Operating profit before impairments 6.620 Impairment losses

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Deutsche Bank AG Actual results at 31 December 2010 million EUR, % Operating profit before impairments 6.620 Impairment losses

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 211 EBA EU-wide stress test: Summary (1-3) Name of the bank: Bank of Valletta P.L.C. Actual results at 31 December 21 million EUR, % Operating profit before impairments 17 Impairment losses

Results of the 211 EBA EU-wide stress test: Summary (1-3) Name of the bank: Bank of Valletta P.L.C. Actual results at 31 December 21 million EUR, % Operating profit before impairments 17 Impairment losses

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Svenska Handelsbanken AB (publ) Actual results at 31 December 2010 million EUR, % Operating profit before impairments 1,816

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Svenska Handelsbanken AB (publ) Actual results at 31 December 2010 million EUR, % Operating profit before impairments 1,816

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Irish Life & Permanent plc Actual results at 31 December 2010 million EUR, % Operating profit before impairments 76 Impairment

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Irish Life & Permanent plc Actual results at 31 December 2010 million EUR, % Operating profit before impairments 76 Impairment

Results of the 2011 EU-wide stress testing exercise. Bank of Cyprus successfully passed the stress test exercise

Announcement Results of the 2011 EU-wide stress testing exercise Bank of Cyprus successfully passed the stress test exercise The results reaffirm the solid financial fundamentals of the Bank which by maintaining

Announcement Results of the 2011 EU-wide stress testing exercise Bank of Cyprus successfully passed the stress test exercise The results reaffirm the solid financial fundamentals of the Bank which by maintaining

European Advertising Business Climate Index Q4 2016/Q #AdIndex2017

European Advertising Business Climate Index Q4 216/Q1 217 ABOUT Quarterly survey of European advertising and market research companies Provides information about: managers assessment of their business

European Advertising Business Climate Index Q4 216/Q1 217 ABOUT Quarterly survey of European advertising and market research companies Provides information about: managers assessment of their business

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: NATIONAL BANK OF GREECE SA Actual results at 31 December 2010 million EUR, % Operating profit before impairments 2,072 Impairment

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: NATIONAL BANK OF GREECE SA Actual results at 31 December 2010 million EUR, % Operating profit before impairments 2,072 Impairment

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: DekaBank Deutsche Girozentrale Actual results at 31 December 2010 million EUR, % Operating profit before impairments 858 Impairment

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: DekaBank Deutsche Girozentrale Actual results at 31 December 2010 million EUR, % Operating profit before impairments 858 Impairment

EMPLOYMENT RATE Employed/Working age population (15-64 years)

") 1 EMPLOYMENT RATE 1980-2003 Employed/Working age population (15-64 years 80 % Finland (Com 75 70 65 60 EU-15 Finland (Stat. Fin. 55 50 80 82 84 86 88 90 92 94 96 98 00 02 9.9.2002/SAK /TL Source: European

1 EMPLOYMENT RATE 1980-2003 Employed/Working age population (15-64 years 80 % Finland (Com 75 70 65 60 EU-15 Finland (Stat. Fin. 55 50 80 82 84 86 88 90 92 94 96 98 00 02 9.9.2002/SAK /TL Source: European

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: COLONYA - CAIXA D'ESTALVIS DE POLLENSA Actual results at 31 December 2010 million EUR, % Operating profit before impairments

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: COLONYA - CAIXA D'ESTALVIS DE POLLENSA Actual results at 31 December 2010 million EUR, % Operating profit before impairments

EMPLOYMENT RATE IN EU-COUNTRIES 2000 Employed/Working age population (15-64 years)

") EMPLOYMENT RATE IN EU-COUNTRIES 2 Employed/Working age population (15-64 years EU-15 Denmark Netherlands Great Britain Sweden Portugal Finland Austria Germany Ireland Luxembourg France Belgium Greece Spain

EMPLOYMENT RATE IN EU-COUNTRIES 2 Employed/Working age population (15-64 years EU-15 Denmark Netherlands Great Britain Sweden Portugal Finland Austria Germany Ireland Luxembourg France Belgium Greece Spain

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Actual results at 31 December 2010 million EUR, % Operating profit before impairments 3.526 Impairment losses on financial and non-financial assets

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Actual results at 31 December 2010 million EUR, % Operating profit before impairments 3.526 Impairment losses on financial and non-financial assets

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: CAJA DE AHORROS Y M.P. DE GIPUZKOA Y SAN SEBASTIAN Actual results at 31 December 2010 million EUR, % Operating profit before

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: CAJA DE AHORROS Y M.P. DE GIPUZKOA Y SAN SEBASTIAN Actual results at 31 December 2010 million EUR, % Operating profit before

AIB - CEBS Stress Test. 23rd July 2010

AIB - CEBS Stress Test 23rd July 2010 Allied Irish Banks, p.l.c. ("AIB") [NYSE: AIB] welcomes today s earlier announcements of the EU-wide stress testing exercise co-ordinated by the Committee of European

AIB - CEBS Stress Test 23rd July 2010 Allied Irish Banks, p.l.c. ("AIB") [NYSE: AIB] welcomes today s earlier announcements of the EU-wide stress testing exercise co-ordinated by the Committee of European

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Unione di Banche Italiane Scpa Actual results at 31 December 2010 million EUR, % Operating profit before impairments 1.027 Impairment

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: Unione di Banche Italiane Scpa Actual results at 31 December 2010 million EUR, % Operating profit before impairments 1.027 Impairment

EIOPA Statistics - Accompanying note

EIOPA Statistics - Accompanying note Publication references: Published statistics: [Balance sheet], [Premiums, claims and expenses], [Own funds and SCR] Disclaimer: Data is drawn from the published statistics

EIOPA Statistics - Accompanying note Publication references: Published statistics: [Balance sheet], [Premiums, claims and expenses], [Own funds and SCR] Disclaimer: Data is drawn from the published statistics

EIOPA Statistics - Accompanying note

EIOPA Statistics - Accompanying note Publication reference: Published statistics: [Balance sheet], [Premiums, claims and expenses], [Own funds and SCR] Disclaimer: Data is drawn from the published statistics

EIOPA Statistics - Accompanying note Publication reference: Published statistics: [Balance sheet], [Premiums, claims and expenses], [Own funds and SCR] Disclaimer: Data is drawn from the published statistics

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: CAJA DE AHORROS Y PENSIONES DE BARCELONA Actual results at 31 December million EUR, % Operating profit before impairments 3,364

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: CAJA DE AHORROS Y PENSIONES DE BARCELONA Actual results at 31 December million EUR, % Operating profit before impairments 3,364

EU State aid: Guidelines on State aid for environmental protection and energy making of -

EU State aid: Guidelines on State aid for environmental protection and energy 2014-2020 - making of - NHO Seminar Oslo, 5 November 2014 Guido Lobrano, Senior Legal Adviser Summary What is BUSINESSEUROPE?

EU State aid: Guidelines on State aid for environmental protection and energy 2014-2020 - making of - NHO Seminar Oslo, 5 November 2014 Guido Lobrano, Senior Legal Adviser Summary What is BUSINESSEUROPE?

EIOPA Statistics - Accompanying note

EIOPA Statistics - Accompanying note Publication references: and Published statistics: [Balance sheet], [Premiums, claims and expenses], [Own funds and SCR] Disclaimer: Data is drawn from the published

EIOPA Statistics - Accompanying note Publication references: and Published statistics: [Balance sheet], [Premiums, claims and expenses], [Own funds and SCR] Disclaimer: Data is drawn from the published

How to complete a payment application form (NI)

") How to complete a payment application form (NI) This form should be used for making a payment from a Northern Ireland Ulster Bank account. 1. Applicant Details If you are a signal number indemnity holder,

How to complete a payment application form (NI) This form should be used for making a payment from a Northern Ireland Ulster Bank account. 1. Applicant Details If you are a signal number indemnity holder,

Consumer Credit. Introduction. June, the 6th (2013)

") Consumer Credit in Europe at end-2012 Introduction Crédit Agricole Consumer Finance has published its annual survey of the consumer credit market in 27 European Union countries (EU-27) for the sixth year

Consumer Credit in Europe at end-2012 Introduction Crédit Agricole Consumer Finance has published its annual survey of the consumer credit market in 27 European Union countries (EU-27) for the sixth year

2017 Figures summary 1

Annual Press Conference on January 18 th 2018 EIB Group Results 2017 2017 Figures summary 1 European Investment Bank (EIB) financing EUR 69.88 billion signed European Investment Fund (EIF) financing EUR

Annual Press Conference on January 18 th 2018 EIB Group Results 2017 2017 Figures summary 1 European Investment Bank (EIB) financing EUR 69.88 billion signed European Investment Fund (EIF) financing EUR

Report Penalties and measures imposed under the UCITS Directive in 2016 and 2017

Report Penalties and measures imposed under the Directive in 206 and 207 4 April 209 ESMA34-45-65 4 April 209 ESMA34-45-65 Table of Contents Executive Summary... 3 2 Background and relevant regulatory

Report Penalties and measures imposed under the Directive in 206 and 207 4 April 209 ESMA34-45-65 4 April 209 ESMA34-45-65 Table of Contents Executive Summary... 3 2 Background and relevant regulatory

11 th Economic Trends Survey of the Impact of Economic Downturn

11 th Economic Trends Survey 11 th Economic Trends Survey of the Impact of Economic Downturn 11 th Economic Trends Survey COUNTRY ANSWERS Austria 155 Belgium 133 Bulgaria 192 Croatia 185 Cyprus 1 Czech

11 th Economic Trends Survey 11 th Economic Trends Survey of the Impact of Economic Downturn 11 th Economic Trends Survey COUNTRY ANSWERS Austria 155 Belgium 133 Bulgaria 192 Croatia 185 Cyprus 1 Czech

THE IMPACT OF THE PUBLIC DEBT STRUCTURE IN THE EUROPEAN UNION MEMBER COUNTRIES ON THE POSSIBILITY OF DEBT OVERHANG

THE IMPACT OF THE PUBLIC DEBT STRUCTURE IN THE EUROPEAN UNION MEMBER COUNTRIES ON THE POSSIBILITY OF DEBT OVERHANG Robert Huterski, PhD Nicolaus Copernicus University in Toruń Faculty of Economic Sciences

THE IMPACT OF THE PUBLIC DEBT STRUCTURE IN THE EUROPEAN UNION MEMBER COUNTRIES ON THE POSSIBILITY OF DEBT OVERHANG Robert Huterski, PhD Nicolaus Copernicus University in Toruń Faculty of Economic Sciences

Quarterly Gross Domestic Product of Montenegro 3 rd quarter 2017

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 224 Podgorica, 22 December 2017 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 3 rd quarter 2017 The release

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 224 Podgorica, 22 December 2017 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 3 rd quarter 2017 The release

Quarterly Gross Domestic Product of Montenegro 2st quarter 2016

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro 2st quarter 2016 The release presents the preliminary data for quarterly gross domestic product

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro 2st quarter 2016 The release presents the preliminary data for quarterly gross domestic product

NOTE. for the Interparliamentary Meeting of the Committee on Budgets

NOTE for the Interparliamentary Meeting of the Committee on Budgets THE ROLE OF THE EU BUDGET TO SUPPORT MEMBER STATES IN ACHIEVING THEIR ECONOMIC OBJECTIVES AS AGREED WITHIN THE FRAMEWORK OF THE EUROPEAN

NOTE for the Interparliamentary Meeting of the Committee on Budgets THE ROLE OF THE EU BUDGET TO SUPPORT MEMBER STATES IN ACHIEVING THEIR ECONOMIC OBJECTIVES AS AGREED WITHIN THE FRAMEWORK OF THE EUROPEAN

InnovFin SME Guarantee

InnovFin SME Guarantee Implementation Update Reporting date: 30/09/2017 Disclaimer This presentation contains general information about the implementation results of InnovFin SME Guarantee, a facility

InnovFin SME Guarantee Implementation Update Reporting date: 30/09/2017 Disclaimer This presentation contains general information about the implementation results of InnovFin SME Guarantee, a facility

Households capital available for renovation

Households capital available for Methodical note Copenhagen Economics, 22 February 207 The task at hand has been twofold: firstly, we were to calculate an estimate of households average capital available

Households capital available for Methodical note Copenhagen Economics, 22 February 207 The task at hand has been twofold: firstly, we were to calculate an estimate of households average capital available

Composition of capital as of 30 September 2011 (CRD3 rules)

") Composition of capital as of 30 September 2011 (CRD3 rules) Capital position CRD3 rules September 2011 Million EUR % RWA References to COREP reporting A) Common equity before deductions (Original own funds

Composition of capital as of 30 September 2011 (CRD3 rules) Capital position CRD3 rules September 2011 Million EUR % RWA References to COREP reporting A) Common equity before deductions (Original own funds

Composition of capital as of 30 September 2011 (CRD3 rules)

") Composition of capital as of 30 September 2011 (CRD3 rules) Capital position CRD3 rules September 2011 Million EUR % RWA References to COREP reporting A) Common equity before deductions (Original own funds

Composition of capital as of 30 September 2011 (CRD3 rules) Capital position CRD3 rules September 2011 Million EUR % RWA References to COREP reporting A) Common equity before deductions (Original own funds

Banco Comercial Português, SA Capital Update - EU Wide Stress Test Results.

Banco Comercial Português, SA Capital Update - EU Wide Stress Test Results. Banco Comercial Português was subject to the 2011 EU-wide stress test conducted by the European Banking Authority (EBA), in cooperation

Banco Comercial Português, SA Capital Update - EU Wide Stress Test Results. Banco Comercial Português was subject to the 2011 EU-wide stress test conducted by the European Banking Authority (EBA), in cooperation

Results of the 2011 EBA EU-wide stress test: Summary (1-3)

") Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: HSH Nordbank Actual results at 31 December 2010 million EUR, % Operating profit before impairments 261 Impairment losses on

Results of the 2011 EBA EU-wide stress test: Summary (1-3) Name of the bank: HSH Nordbank Actual results at 31 December 2010 million EUR, % Operating profit before impairments 261 Impairment losses on

2015 EU-wide Transparency Exercise

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name _IT_VLEI Code Nov_ Country Code V3AFM0G2D3A6E0QWDG59 IT Mer Ba 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name _IT_VLEI Code Nov_ Country Code V3AFM0G2D3A6E0QWDG59 IT Mer Ba 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION

2015 EU-wide Transparency Exercise

ound_3 5 TRA Bank Name mittedlei Code Nov_ Country Code 8156009BC82130E7FC43 IT Mer Ba 201412 201506 Capital CRR / CRDIV DEFINITION OF CAPITAL As of 31/12/2014 As of 30/06/2015 COREP CODE REGULATION OWN

ound_3 5 TRA Bank Name mittedlei Code Nov_ Country Code 8156009BC82130E7FC43 IT Mer Ba 201412 201506 Capital CRR / CRDIV DEFINITION OF CAPITAL As of 31/12/2014 As of 30/06/2015 COREP CODE REGULATION OWN

2015 EU-wide Transparency Exercise

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name tted_lei Code Nov_ Country Code 549300OLBL49CW8CT155 ES Mer Ib 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name tted_lei Code Nov_ Country Code 549300OLBL49CW8CT155 ES Mer Ib 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION

2015 EU-wide Transparency Exercise

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name _IT_ LEI Code Nov_ Country Code F1T87K3OQ2OV1UORLH26 IT Mer Ba 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name _IT_ LEI Code Nov_ Country Code F1T87K3OQ2OV1UORLH26 IT Mer Ba 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION

Quarterly Gross Domestic Product of Montenegro 4 th quarter 2018 (p)

") MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 46 Podgorica, 22 March 2019 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 4 th quarter 2018 (p) The release

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 46 Podgorica, 22 March 2019 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 4 th quarter 2018 (p) The release

Summary of key findings

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

2015 EU-wide Transparency Exercise

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name _DK_LEI Code Nov_ Country Code 3M5E1GQGKL17HI6CPN30 DK Mer Jy 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION OF

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name _DK_LEI Code Nov_ Country Code 3M5E1GQGKL17HI6CPN30 DK Mer Jy 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION OF

EU-wide Transparency Exercise 2015

Announcement EU-wide Transparency Exercise 2015 Nicosia, 24 November 2015 Group Profile Founded in 1899, Bank of Cyprus Group is the leading banking and financial services group in Cyprus. The Group provides

Announcement EU-wide Transparency Exercise 2015 Nicosia, 24 November 2015 Group Profile Founded in 1899, Bank of Cyprus Group is the leading banking and financial services group in Cyprus. The Group provides

Electricity & Gas Prices in Ireland. Annex Business Electricity Prices per kwh 2 nd Semester (July December) 2016

2016") Electricity & Gas Prices in Ireland Annex Business Electricity Prices per kwh 2 nd Semester (July December) 2016 ENERGY POLICY STATISTICAL SUPPORT UNIT 1 Electricity & Gas Prices in Ireland Annex Business

Electricity & Gas Prices in Ireland Annex Business Electricity Prices per kwh 2 nd Semester (July December) 2016 ENERGY POLICY STATISTICAL SUPPORT UNIT 1 Electricity & Gas Prices in Ireland Annex Business

2015 EU-wide Transparency Exercise

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name me_ LEI Code Nov_ Country Code 81560097964CBDAED282 IT Mer Un 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION OF

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name me_ LEI Code Nov_ Country Code 81560097964CBDAED282 IT Mer Un 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION OF

2015 EU-wide Transparency Exercise

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name tted_ LEI Code Oct_ Country Code 959800DQQUAMV0K08004 ES Merg Cr 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION

ound_3 2015 EU-wide Transparency Exercise 5 TRA Bank Name tted_ LEI Code Oct_ Country Code 959800DQQUAMV0K08004 ES Merg Cr 2015 EU-wide Transparency Exercise 201412 201506 Capital CRR / CRDIV DEFINITION

Consumer credit market in Europe 2013 overview

Consumer credit market in Europe 2013 overview Crédit Agricole Consumer Finance published its annual survey of the consumer credit market in 28 European Union countries for seven years running. 9 July

Consumer credit market in Europe 2013 overview Crédit Agricole Consumer Finance published its annual survey of the consumer credit market in 28 European Union countries for seven years running. 9 July

2015 EU-wide Transparency Exercise

ound_3 5 TRA Bank Name ed_fi LEI Code Nov_ Country Code VWMYAEQSTOPNV0SUGU82 ES Mer Ba 201412 201506 Capital CRR / CRDIV DEFINITION OF CAPITAL As of 31/12/2014 As of 30/06/2015 COREP CODE REGULATION OWN

ound_3 5 TRA Bank Name ed_fi LEI Code Nov_ Country Code VWMYAEQSTOPNV0SUGU82 ES Mer Ba 201412 201506 Capital CRR / CRDIV DEFINITION OF CAPITAL As of 31/12/2014 As of 30/06/2015 COREP CODE REGULATION OWN

Composition of capital IT044 IT044 POWSZECHNAIT044 UNIONE DI BANCHE ITALIANE SCPA (UBI BANCA)

") Composition of capital POWSZECHNA (in million Euro) Capital position CRD3 rules A) Common equity before deductions (Original own funds without hybrid instruments and government support measures other than

Composition of capital POWSZECHNA (in million Euro) Capital position CRD3 rules A) Common equity before deductions (Original own funds without hybrid instruments and government support measures other than

Comparing pay trends in the public services and private sector. Labour Research Department 7 June 2018 Brussels

Comparing pay trends in the public services and private sector Labour Research Department 7 June 2018 Brussels Issued to be covered The trends examined The varying patterns over 14 years and the impact

Comparing pay trends in the public services and private sector Labour Research Department 7 June 2018 Brussels Issued to be covered The trends examined The varying patterns over 14 years and the impact

DG TAXUD. STAT/11/100 1 July 2011

DG TAXUD STAT/11/100 1 July 2011 Taxation trends in the European Union Recession drove EU27 overall tax revenue down to 38.4% of GDP in 2009 Half of the Member States hiked the standard rate of VAT since

DG TAXUD STAT/11/100 1 July 2011 Taxation trends in the European Union Recession drove EU27 overall tax revenue down to 38.4% of GDP in 2009 Half of the Member States hiked the standard rate of VAT since

Fiscal rules in Lithuania

Fiscal rules in Lithuania Algimantas Rimkūnas Vice Minister, Ministry of Finance of Lithuania 3 June, 2016 Evolution of National and EU Fiscal Regulations Stability and Growth Pact (SGP) Maastricht Treaty

Fiscal rules in Lithuania Algimantas Rimkūnas Vice Minister, Ministry of Finance of Lithuania 3 June, 2016 Evolution of National and EU Fiscal Regulations Stability and Growth Pact (SGP) Maastricht Treaty

LENDING FACILITIES Hire Purchase (HP) 1% % on a case by case basis (fee set by AgriFinance Ltd)

1% % on a case by case basis (fee set by AgriFinance Ltd)") Our Charges This brochure gives a brief description of tariffs as charged by AgriBank plc on some of its products and services. For tariffs on products or services which are not listed in this brochure,

Our Charges This brochure gives a brief description of tariffs as charged by AgriBank plc on some of its products and services. For tariffs on products or services which are not listed in this brochure,

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

34 th Associates Meeting - Andorra, 25 May Item 5: Evolution of economic governance in the EU

34 th Associates Meeting - Andorra, 25 May 2012 - Item 5: Evolution of economic governance in the EU Plan of the Presentation 1. Fiscal and economic coordination: how did it start? 2. Did it work? 3. Five

34 th Associates Meeting - Andorra, 25 May 2012 - Item 5: Evolution of economic governance in the EU Plan of the Presentation 1. Fiscal and economic coordination: how did it start? 2. Did it work? 3. Five

FSMA_2017_05-01 of 24/02/2017

FSMA_2017_05-01 of 24/02/2017 This Communication is addressed to Belgian alternative investment fund managers who intend to market, to professional investors, units or shares of European Economic Area

FSMA_2017_05-01 of 24/02/2017 This Communication is addressed to Belgian alternative investment fund managers who intend to market, to professional investors, units or shares of European Economic Area

Macroeconomic overview SEE and Macedonia

Macroeconomic overview SEE and Macedonia Zoltan Arokszallasi Chief Analyst, Macro & FX/FI Research Erste Group Bank Erste Investors Breakfast, 29 September, Skopje 02. Oktober SEE shows mixed performance

Macroeconomic overview SEE and Macedonia Zoltan Arokszallasi Chief Analyst, Macro & FX/FI Research Erste Group Bank Erste Investors Breakfast, 29 September, Skopje 02. Oktober SEE shows mixed performance

EMPLOYMENT RATE Employed/Working age population (15 64 years)

") EMPLOYMENT RATE 198 26 Employed/Working age population (15 64 years 8 % Finland 75 EU 15 EU 25 7 65 6 55 5 8 82 84 86 88 9 92 94 96 98 2 4** 6** 14.4.25/SAK /TL Source: European Commission 1 UNEMPLOYMENT

EMPLOYMENT RATE 198 26 Employed/Working age population (15 64 years 8 % Finland 75 EU 15 EU 25 7 65 6 55 5 8 82 84 86 88 9 92 94 96 98 2 4** 6** 14.4.25/SAK /TL Source: European Commission 1 UNEMPLOYMENT

Press Release Outside trading hours - Regulated information*

Press Release Outside trading hours - Regulated information* 15 July 2011 KBC Bank Capital Update - EU Wide Stress Test Results KBC Bank was subject to the 2011 EU-wide stress test conducted by the European

Press Release Outside trading hours - Regulated information* 15 July 2011 KBC Bank Capital Update - EU Wide Stress Test Results KBC Bank was subject to the 2011 EU-wide stress test conducted by the European

Sustainability and Adequacy of Social Security in the Next Quarter Century:

Sustainability and Adequacy of Social Security in the Next Quarter Century: Balancing future pensions adequacy and sustainability while facing demographic change Krzysztof Hagemejer (Author) John Woodall

Sustainability and Adequacy of Social Security in the Next Quarter Century: Balancing future pensions adequacy and sustainability while facing demographic change Krzysztof Hagemejer (Author) John Woodall

EFPIA Disclosure Code 2016 Disclosures Shire Pharmaceuticals (including Baxalta US Inc.)

") EFPIA Disclosure Code 2016 Disclosures Shire Pharmaceuticals (including Baxalta US Inc.) 1 Section 1: Reporting Approach for 2016 Data: On June 3rd, 2016, Shire acquired Baxalta. Due to the complexity

EFPIA Disclosure Code 2016 Disclosures Shire Pharmaceuticals (including Baxalta US Inc.) 1 Section 1: Reporting Approach for 2016 Data: On June 3rd, 2016, Shire acquired Baxalta. Due to the complexity

June 2014 Euro area international trade in goods surplus 16.8 bn 2.9 bn surplus for EU28

127/2014-18 August 2014 June 2014 Euro area international trade in goods surplus 16.8 bn 2.9 bn surplus for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

127/2014-18 August 2014 June 2014 Euro area international trade in goods surplus 16.8 bn 2.9 bn surplus for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

Enterprise Europe Network SME growth outlook

Enterprise Europe Network SME growth outlook 2018-19 een.ec.europa.eu 2 Enterprise Europe Network SME growth outlook 2018-19 Foreword The European Commission wants to ensure that small and medium-sized

Enterprise Europe Network SME growth outlook 2018-19 een.ec.europa.eu 2 Enterprise Europe Network SME growth outlook 2018-19 Foreword The European Commission wants to ensure that small and medium-sized

Online Insurance Europe: BEST PRACTICES & TRENDS

Online Insurance Europe: S & TRENDS NEW EDITION 2015 Your Benefits EUROPE S S & TRENDS: The first and only analysis of the current online insurance best practices in all of Europe. Over 100 best practices,

Online Insurance Europe: S & TRENDS NEW EDITION 2015 Your Benefits EUROPE S S & TRENDS: The first and only analysis of the current online insurance best practices in all of Europe. Over 100 best practices,

Enterprise Europe Network SME growth forecast

Enterprise Europe Network SME growth forecast 2017-18 een.ec.europa.eu Foreword Since we came into office three years ago, this European Commission has put the creation of more jobs and growth at the centre

Enterprise Europe Network SME growth forecast 2017-18 een.ec.europa.eu Foreword Since we came into office three years ago, this European Commission has put the creation of more jobs and growth at the centre

EUROPA - Press Releases - Taxation trends in the European Union EU27 tax...of GDP in 2008 Steady decline in top corporate income tax rate since 2000

DG TAXUD STAT/10/95 28 June 2010 Taxation trends in the European Union EU27 tax ratio fell to 39.3% of GDP in 2008 Steady decline in top corporate income tax rate since 2000 The overall tax-to-gdp ratio1

DG TAXUD STAT/10/95 28 June 2010 Taxation trends in the European Union EU27 tax ratio fell to 39.3% of GDP in 2008 Steady decline in top corporate income tax rate since 2000 The overall tax-to-gdp ratio1

FCCC/SBI/2010/10/Add.1

United Nations Framework Convention on Climate Change Distr.: General 25 August 2010 Original: English Subsidiary Body for Implementation Contents Report of the Subsidiary Body for Implementation on its

United Nations Framework Convention on Climate Change Distr.: General 25 August 2010 Original: English Subsidiary Body for Implementation Contents Report of the Subsidiary Body for Implementation on its

Open Day 2017 Clearstream execution-to-custody integration Valentin Nehls / Jan Willems. 5 October 2017

Open Day 2017 Clearstream execution-to-custody integration Valentin Nehls / Jan Willems 5 October 2017 Deutsche Börse Group 1 Settlement services: single point of access to cost-effective, low risk and

Open Day 2017 Clearstream execution-to-custody integration Valentin Nehls / Jan Willems 5 October 2017 Deutsche Börse Group 1 Settlement services: single point of access to cost-effective, low risk and

The Eureka Eurostars Programme

The Eureka Eurostars Programme 29/03/2011 Terence O Donnell, Eureka National Project Co-ordinator What is EUREKA? > 2 > EUREKA is a public network supporting R&D-performing businesses > Established in

The Eureka Eurostars Programme 29/03/2011 Terence O Donnell, Eureka National Project Co-ordinator What is EUREKA? > 2 > EUREKA is a public network supporting R&D-performing businesses > Established in

For further information, please see online or contact

For further information, please see http://ec.europa.eu/research/sme-techweb online or contact Lieve.VanWoensel@ec.europa.eu Sixth Progress Report on participation in the 7 th R&D Framework Programme Statistical

For further information, please see http://ec.europa.eu/research/sme-techweb online or contact Lieve.VanWoensel@ec.europa.eu Sixth Progress Report on participation in the 7 th R&D Framework Programme Statistical

EUREKA Programme A European Research Programme. > Not an EU-Programme (but complementarity and co-operation - ERA)

") EUREKA EUREKA Programme...... Shaping tomorrow s innovations today EUREKA in glance > 2 A European Research Programme > Not an EU-Programme (but complementarity and co-operation - ERA) > Bottom-up project

EUREKA EUREKA Programme...... Shaping tomorrow s innovations today EUREKA in glance > 2 A European Research Programme > Not an EU-Programme (but complementarity and co-operation - ERA) > Bottom-up project

A. INTRODUCTION AND FINANCING OF THE GENERAL BUDGET. EXPENDITURE Description Budget Budget Change (%)

") DRAFT AMENDING BUDGET NO. 2/2018 VOLUME 1 - TOTAL REVENUE A. INTRODUCTION AND FINANCING OF THE GENERAL BUDGET FINANCING OF THE GENERAL BUDGET Appropriations to be covered during the financial year 2018

DRAFT AMENDING BUDGET NO. 2/2018 VOLUME 1 - TOTAL REVENUE A. INTRODUCTION AND FINANCING OF THE GENERAL BUDGET FINANCING OF THE GENERAL BUDGET Appropriations to be covered during the financial year 2018

CANADA EUROPEAN UNION

THE EUROPEAN UNION S PROFILE Economic Indicators Gross domestic product (GDP) at purchasing power parity (PPP): US$20.3 trillion (2016) GDP per capita at PPP: US$39,600 (2016) Population: 511.5 million

THE EUROPEAN UNION S PROFILE Economic Indicators Gross domestic product (GDP) at purchasing power parity (PPP): US$20.3 trillion (2016) GDP per capita at PPP: US$39,600 (2016) Population: 511.5 million

LENDING FACILITIES Hire Purchase (HP) 1% % on a case by case basis (fee set by AgriFinance Ltd)

1% % on a case by case basis (fee set by AgriFinance Ltd)") Our Charges This brochure gives a brief description of tariffs as charged by AgriBank plc on some of its products and services. For tariffs on products or services which are not listed in this brochure,

Our Charges This brochure gives a brief description of tariffs as charged by AgriBank plc on some of its products and services. For tariffs on products or services which are not listed in this brochure,

Quarterly Gross Domestic Product of Montenegro for period 1 st quarter rd quarter 2016

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro for period 1 st quarter 015 - rd quarter 016 The release presents the final results of quarterly

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro for period 1 st quarter 015 - rd quarter 016 The release presents the final results of quarterly

CFA Institute Member Poll: Euro zone Stability Bonds

CFA Institute Member Poll: Euro zone Stability Bonds I. About the Survey... 2 a. Background... 2 b. Purpose and Methodology... 2 II. Full Results... 2 Q1: Requirement of common issuance of sovereign bonds...

CFA Institute Member Poll: Euro zone Stability Bonds I. About the Survey... 2 a. Background... 2 b. Purpose and Methodology... 2 II. Full Results... 2 Q1: Requirement of common issuance of sovereign bonds...

Defining Issues. EU Audit Reforms: The Countdown Begins. April 2016, No Key Facts for U.S. Companies

Defining Issues April 2016, No. 16-12 EU Audit Reforms: The Countdown Begins Only two months remain before the European Union (EU) audit reforms come into full effect. These reforms will affect many U.S.

Defining Issues April 2016, No. 16-12 EU Audit Reforms: The Countdown Begins Only two months remain before the European Union (EU) audit reforms come into full effect. These reforms will affect many U.S.

Reporting practices for domestic and total debt securities

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Macroeconomic scenarios for skill demand and supply projections, including dealing with the recession

Alphametrics (AM) Alphametrics Ltd Macroeconomic scenarios for skill demand and supply projections, including dealing with the recession Paper presented at Skillsnet technical workshop on: Forecasting

Alphametrics (AM) Alphametrics Ltd Macroeconomic scenarios for skill demand and supply projections, including dealing with the recession Paper presented at Skillsnet technical workshop on: Forecasting

Burden of Taxation: International Comparisons

Burden of Taxation: International Comparisons Standard Note: SN/EP/3235 Last updated: 15 October 2008 Author: Bryn Morgan Economic Policy & Statistics Section This note presents data comparing the national

Burden of Taxation: International Comparisons Standard Note: SN/EP/3235 Last updated: 15 October 2008 Author: Bryn Morgan Economic Policy & Statistics Section This note presents data comparing the national

STOXX EMERGING MARKETS INDICES. UNDERSTANDA RULES-BA EMERGING MARK TRANSPARENT SIMPLE

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

EU Pension Trends. Matti Leppälä, Secretary General / CEO PensionsEurope 16 October 2014 Rovinj, Croatia

EU Pension Trends Matti Leppälä, Secretary General / CEO PensionsEurope 16 October 2014 Rovinj, Croatia 1 Lähde: World Bank 2 Pension debt big (implicit debt, % of GDP, 2006) Source:Müller, Raffelhüschen

EU Pension Trends Matti Leppälä, Secretary General / CEO PensionsEurope 16 October 2014 Rovinj, Croatia 1 Lähde: World Bank 2 Pension debt big (implicit debt, % of GDP, 2006) Source:Müller, Raffelhüschen

Gender pension gap economic perspective

Gender pension gap economic perspective Agnieszka Chłoń-Domińczak Institute of Statistics and Demography SGH Part of this research was supported by European Commission 7th Framework Programme project "Employment

Gender pension gap economic perspective Agnieszka Chłoń-Domińczak Institute of Statistics and Demography SGH Part of this research was supported by European Commission 7th Framework Programme project "Employment

Lowest implicit tax rates on labour in Malta, on consumption in Spain and on capital in Lithuania

STAT/13/68 29 April 2013 Taxation trends in the European Union The overall tax-to-gdp ratio in the EU27 up to 38.8% of GDP in 2011 Labour taxes remain major source of tax revenue The overall tax-to-gdp

STAT/13/68 29 April 2013 Taxation trends in the European Union The overall tax-to-gdp ratio in the EU27 up to 38.8% of GDP in 2011 Labour taxes remain major source of tax revenue The overall tax-to-gdp

May 2012 Euro area international trade in goods surplus of 6.9 bn euro 3.8 bn euro deficit for EU27

108/2012-16 July 2012 May 2012 Euro area international trade in goods surplus of 6.9 3.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

108/2012-16 July 2012 May 2012 Euro area international trade in goods surplus of 6.9 3.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

Some Historical Examples of Yield Curves

3 months 6 months 1 year 2 years 5 years 10 years 30 years Some Historical Examples of Yield Curves Nominal interest rate, % 16 14 12 10 8 6 4 2 January 1981 June1999 December2009 0 Time to maturity This

3 months 6 months 1 year 2 years 5 years 10 years 30 years Some Historical Examples of Yield Curves Nominal interest rate, % 16 14 12 10 8 6 4 2 January 1981 June1999 December2009 0 Time to maturity This

EBA TRANSPARENCY EXERCISE

BANCO BPI, S.A. Public Company Registered office: Rua Tenente Valadim, 284, Porto Share capital: 1 293 063 324.98 Registered at Commercial Registry of Porto under Unique taxpayer reference number 501 214

BANCO BPI, S.A. Public Company Registered office: Rua Tenente Valadim, 284, Porto Share capital: 1 293 063 324.98 Registered at Commercial Registry of Porto under Unique taxpayer reference number 501 214

Quarterly Financial Accounts Household net worth reaches new peak in Q Irish Household Net Worth

Quarterly Financial Accounts Q4 2017 4 May 2018 Quarterly Financial Accounts Household net worth reaches new peak in Q4 2017 Household net worth rose by 2.1 per cent in Q4 2017. It now exceeds its pre-crisis

Quarterly Financial Accounts Q4 2017 4 May 2018 Quarterly Financial Accounts Household net worth reaches new peak in Q4 2017 Household net worth rose by 2.1 per cent in Q4 2017. It now exceeds its pre-crisis

January 2014 Euro area international trade in goods surplus 0.9 bn euro 13.0 bn euro deficit for EU28

STAT/14/41 18 March 2014 January 2014 Euro area international trade in goods surplus 0.9 13.0 deficit for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

STAT/14/41 18 March 2014 January 2014 Euro area international trade in goods surplus 0.9 13.0 deficit for EU28 The first estimate for the euro area 1 (EA18) trade in goods balance with the rest of the

First estimate for 2011 Euro area external trade deficit 7.7 bn euro bn euro deficit for EU27

27/2012-15 February 2012 First estimate for 2011 Euro area external trade deficit 7.7 152.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

27/2012-15 February 2012 First estimate for 2011 Euro area external trade deficit 7.7 152.8 deficit for EU27 The first estimate for the euro area 1 (EA17) trade in goods balance with the rest of the world

TAXATION OF TRUSTS IN ISRAEL. An Opportunity For Foreign Residents. Dr. Avi Nov

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,