FNMA HomeStyle Steps to Success

|

|

|

- Terence Fitzgerald

- 5 years ago

- Views:

Transcription

1 WHOLESALE EDITION - Nov 2013

2 FNMA HomeStyle Steps to Success Step One- Program Education Register for classes at M&T University Review Program Product Pages and M&T Agency Underwriting and Eligibility Standards on M&T website Identify Marketing Needs Step Two- Educate your Business Partners and Consumers Educate Realtors on how the product works and what the process is Educate Consumers on the renovation process using the Renovation Loan Step-By-Step Guide Contract should be contingent upon loan approval Seller should allow access to the property for the inspectors, contractors, and/or consultant who will be estimating the remodeling of the property Encourage the borrower to write up a wish list of repairs to discuss with contractor before meeting at property Set expectations- Renovation loans take between days to close Step Three- Originate the loan and Submit to M&T Bank Take the loan application once the borrower has all their contractor bids. Remember to use the Maximum Mortgage Worksheet to calculate the loan amount. Register the loan with M&T Bank through our website nationalwholesale@mtb.com the GFE, the GFE Cost Breakdown and Intent to Proceed (Forms c), and Max Mortgage Worksheet. You can these documents to your AE or SSR prior to disclosure to the borrower and our Registration Dept. to ensure compliance. To expedite the delivery of the TIL to the borrower, include their address so the borrower can acknowledge receipt electronically. Remember, no fees should be collected prior to the M&T Bank disclosure of the TIL, this includes the FHA Consultant and Appraisal Management Company. If the loan is a Standard HomeStyle loan, contact an FHA Consultant to provide the Specification of Repairs. If the consultant identifies additional repairs to be performed, have the contractor add this work to their bid. All final numbers should match. If the renovation costs change, make sure the HomeStyle Max Mortgage Worksheet is updated and a Change of Circumstance is completed and sent to AlbanyConditions@mtb.com within 24 hrs of receiving the information. Order the appraisal through Streetlinks or Solidifi use referral code MTBROKER File may be submitted to M&T once the appraisal report is completed. Use the attached Renovation Checklist (Form 2019) and provide information for all bulleted items ( ) under the Ready/Not Ready column. the file to Albanywholesale@mtb.com. There is a max of 20 MB per so you may have to break down the loan file into several separate s. Reference the borrower s name and loan number on the subject line of each . Findings must be run through DO and finalized to M&T East Coast. Step Four- Clearing Conditions & Preparing for Close Conditions will be ed to the broker and listed on our website. Please send all conditions at one time to AlbanyConditions@mtb.com Once the loan is approved, the rate can no longer be locked online. To lock in or extend a rate, NationalWholesale@mtb.com When the file has been cleared for close, M&T will ask you to schedule the loan for closing by ing AlbanyClosings@mtb.com. The Closing Dept. requires 72 hours scheduling notice once the file is cleared to close and the actual closing is subject to TILA directives. Once the file is scheduled, the completed M&T Bank Closing Scheduling Form with the borrower s Hazard Insurance Dec page and paid in full receipt to our closing dept. Step Five- Renovation begins for the borrower The borrower will receive a Welcome Kit and call from M&T Bank within 5 days of closing. The project must begin within 30 days of close and must be completed within 6 month of their close date. The borrower will work with the M&T Draw Dept for progress inspections and draw disbursements. Funds will be disbursed as a 2-party check made payable to both the borrower and contractor- mailed to the borrower.

3 What Type of HomeStyle Loan does my Borrower Need? M&T HomeStyle- Standard M&T HomeStyle- Streamline Repair Amounts Repair Types Plan Review / Specification of Repairs Contingency Reserve Draw Disbursements Inspections and Title Updates Mortgage Payment Reserve Project Conversions No Minimum; max reno costs can be as much as 50% of the as-completed value (this amt. represents the cost of repairs only (contractor estimates for labor/material) and should NOT include any contingency reserves, fees etc. Line C-1a of the HomeStyle MMWS cannot exceed 50% of the ascompleted appraised value) Structural and non-structural. Non-structural. No minimum; maximum rehabilitation amount is $35,000 including any contingency reserves, fees, etc. as well as cash paid out of pocket. (Line C2 of the HomeStyle MMW cannot exceed $35,000), and Line C-1a cannot exceed 50% of the ascompleted appraised value) Landscaping or site amenities. Landscaping or site amenities. No outbuildings. No outbuildings. All work must be performed by a Qualified contractor (must be licensed if applicable). Plans and specs, if applicable, must be prepared by a qualified, licensed general contractor, renovation consultant or architect. For renovation amounts of $35,000 or greater, a plan reviewer is required. A plan reviewer is defined as a HUD consultant, a renovation consultant or architect with equivalent experience. 10% minimum required. 10% minimum required. If Consultant quotes > 15%, the higher amount must be used. Unused contingency funds must be applied to reduce the balance of the mortgage unless the contingency reserve was provided from the borrower s own funds. Appraiser / Consultant inspects property and identifies the percentage of work complete to date. (Appraiser may inspect for repairs < = $35,000) Maximum 5 draws. Maximum 2 draws. All work must be performed by a Qualified contractor (must be licensed if applicable). Plans and specs, if applicable, must be prepared by a qualified, licensed or general contractor, renovation consultant or architect. 15% required if utilities not on or if property is vacant. Unused contingency funds must be applied to reduce the balance of the mortgage unless the contingency reserve was provided from the borrower s own funds. Appraiser inspects property and identifies the percentage of work complete to date. 10% holdback on each disbursement. 10% holdback on each disbursement. Checks cut in contractor and borrower s names. No draws are permitted without an inspection Inspections are required prior to each disbursement. Two bringdowns performed: one at 50% of renovation dollars advanced and one at final draw Up to 6 months of PITI can be financed, if the home is not habitable during renovation. Not allowed Checks cut in contractor and borrower s names No draws are permitted without an inspection Inspections are required prior to each disbursement. Two bringdowns performed: one at 50% of renovation dollars advanced and one at final draw Borrower must move into property within 30 days of closing. Mortgage payments may not be escrowed. Not allowed Partially Completed Projects M&T will consider disaster-area properties that need finish funds or those that require raising of foundations to increase elevation due to flood zone Not allowed

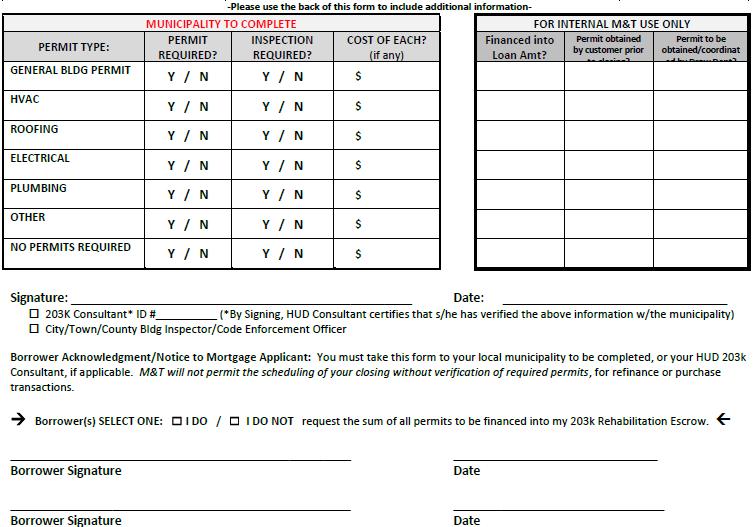

4 Consultant Fees (Required on the Standard HomeStyle product) The easiest way to find a qualified consultant is to use the same list provided by HUD for the FHA 203k program. Finding a Consultant (if applicable): Go to HUD s website at Go to the Search option (top right corner), search for Inspector. Pick the option for 203(k) Consultant. Select the appropriate state. It is highly recommended that a Consultant is used when originating a HomeStyle mortgage to ensure the work write-up and estimates are adequate The Consultant must inspect the property and may also act as a home inspector for the borrower. Consultant, Architectural and Engineering fees are not restricted as long as they are customary and reasonable for the type of repairs. Consultants typically charge the borrower based on the amount of renovation work being performed. Consultant Fee Estimates: <$7,500 $400 $7,501-$15,000 $500 $15,001-$30,000 $600 $30,001-$50,000 $700 $50,001-$75,000 $800 $75,001-$100,000 $900 $100,001+ $1,000 NOTE: If the borrower wishes to have the Consultant complete a feasibility study prior to submitting a sales contract to a seller, an additional fee may apply. Best Practices to Follow When Originating a Renovation Loan: 1. Contractor estimates must be on business letterhead, be legible, and include all labor and material required to complete the job. Borrowers and contractors will have to sign and date. 2. For each contractor, in addition to the estimate, we require: a. Homeowner/Contractor Agreement b. Contractor License covering the type of work being performed ( if applicable) c. General Liability Insurance (a minimum of 1 million dollars) d. Contractor Resume fully completed with 3 residential references e. For a Standard HomeStyle loan, the contractor should also sign the Recap page of the Specification of Repairs 3. Self- Help is not permitted 4. Be aware of the contingency reserve requirements. Unused contingency funds must be applied to reduce the balance of the mortgage unless the contingency reserve was provided from the borrower s own funds. 5. FNMA does not allow up-front money to be disbursed on the HomeStyle program. 6. A 10% holdback will be retained on each disbursement 7. The FNMA HomeStyle limits the amount of repairs to 50% of the future appraised value. (This amt. represents the cost of repairs only (contractor estimates for labor/material) and should NOT include any contingency reserves, fees etc. (Line C-1a of the HomeStyle MMWS cannot exceed 50% of the as-completed appraised value) 8. Condo s and PUD s must be FNMA eligible and repairs may only be performed on the interior of a condo unit 9. Complete the HomeStyle Max Mortgage Worksheet prior to completing the GFE. a. Be sure to include all necessary fees: Inspection Fees, Consultant Fee, Permit Fee, Draw Administration Fee $500, and Architectural and Engineering Fees b. The amount of Rehab and the contingency reserve do NOT belong as line items on the GFE, they should only appear on the Max Mortgage Worksheet.

5 GFE Fees Box 1 M&T Origination charge $ Include your broker compensation Draw Admin. charge $ (Line C1i of the HomeStyle MMWS) The cost of title bringdowns are absorbed by M&T. As a result, the cost of the bringdowns must NOT be quoted on the GFE or the Max Mortgage Worksheet. Box 2 Buydown funds or loan discount points Interest rate related credit to borrower in Box 2, Block 2 Box 3 HomeStyle Inspection Fees (Line C1e of the MMWS)* Appraisal Fee Flood Certification $8.00 Building Permits (Line C1g of the MMWS)* Tax Service Fee $75.00 Box 4 Title Insurance Judgment Search Title Exam Fee Abstract Title Search Settlement Agent/Closing Attorney Closing Protection Letter Title Insurance Binder Box 5 Owner s Title Insurance Box 6 Consultant Fees, if applicable (Line C1d of the MMWS) Architectural and Engineering Fees (Line C1c of the MMWS) Plan Review Fee Survey Pest/Well/Septic/Water Purity Mtg Payments escrowed if uninhabitable. (Line C1h of the MMWS) Note: Contingency Reserve and Repair Costs do not show as a line item on the GFE Forms General M&T Forms: GFE Cost Breakdown and Intent to Proceed [Form c] Renovation Checklist [Form 2019] Anti-Steering Disclosure [Form 1801 or from your LOS] GFE Acceptance Certification [Form b] Loan Submission Contact Information [search by name] Broker Certification of Fees Collected [Form 3111] M&T Fee Sheet [Form 2739] HomeStyle Specific Forms: HomeStyle Maximum Mortgage Worksheet [Form 2609] Homeowner Contractor Agreement [Form 2101] Rehab Permit Certification [Form 8000] HomeStyle Borrowers Acknowledgement [Form 2600] HomeStyle Renovation Consumer Tips [Form 2602] Documents each contractor will provide: o Cost Estimates for each contractor on their letterhead. Must be signed and dated by borrower and contractor. o Contractor License (as required per state and local requirements) o Contractor Liability Insurance o Contractor Resume [Form 2605] Documents the Consultant would provide on a Standard HomeStyle loan o Specification of Repairs/Work Write-Up [Fully Executed/All Pages] o Draw Request [HUD9746-A]

6 BROKER OR LOAN OFFICER OPERATIONS READY/ NOT READY DOCS RENOVATION LOAN CHECKLIST REQUIRED DOCUMENTS FOR ALL FILES LEFT SIDE OF FILE 1 FHA Transmittal [HUD92900-LT] *or* Uniform Transmittal [FNMA HomeStyle/Sonyma Rebuild - FNMA1008] 2 LDP/GSA Print Out [ALL LOANS: Borrowers/Sellers/LO/Realtor/Broker Company/Appraiser] 3 Core Logic/Loan Safe 4 AUS Findings [DU/LP] 5 Final Application [FNMA1003] and HUD Addendum to Application [HUD92900-A] (M&T to Issue) 6 Cover Letter for Mail and Telephone Applications [NYS Only] 7 Initial fully executed and signed Application [FNMA1003] 8 Initial fully executed and signed HUD Addendum to Application [HUD92900-A] 9 Credit Report [Dated within 90 days of submission to Underwriting] 10 Credit Explanations / Supporting Credit Documentation 11 Divorce Decree / Separation Agreement [if applicable] 12 Bankruptcy Papers [if applicable] 13 VOM/VOR/Canceled Checks/12mHELOC History 14 VOE 15 "Other" type of Income Docs 16 Paystubs [covering 30 day period] 17 W-2 Statements [most recent 2 years] 18 Federal Tax Returns [Signed/Dated; Only Required for 2 Years for Self-Employed & Rental Properties] 19 Tax Return Transcripts [ID Check Direct/M&T Function] 20 Bank Statements [most recent months/all pages/sufficient cash to close/explain & document all large deposits] 21 Sales Contract w/all Addendums [Fully executed/initialed] 22 FHA Amendatory Clause/RE Cert [a/k/a All Parties Agreement] 23 HUD REO ONLY: Property Condition Report 24 HUD REO ONLY: Lead Paint Addendum/Assessment Report 25 FHA Conditional Commitment [HUD b] - Completed by Underwriter 26 AVM Reconciliation 27 Property Inspections [Pest/Final Compliance Inspection, etc.] 28 Appraisal [Kirchmeyer or Streetlinks Order] 29 HUD REO ONLY: M&M Appraisal 30 Foreclosure Deed [for Property Flipping] 31 FHA Connection: Appraisal Logging [M&T to issue] 32 Condo/PUD Questionnaire 33 FHA New Construction: Builder's Certification of Plans, Specs & Site [HUD92541] 34 Escrow Holdbacks Only: Mortgagors Assurance of Completion [HUD92300] 35 Repair Conditions Documentation [Escrow Holdbacks] Checklist Pg 1 of 4

7 BROKER OR LOAN OFFICER OPERATIONS READY/ NOT READY DOCS Responsible Party RENOVATION LOAN CHECKLIST REQUIRED DOCUMENTS FOR ALL FILES RIGHT SIDE OF FILE 36 Loan Submission Contact Sheet [from "How to do Business with M&T Packet"] - Wholesale Transactions Only 37 Wholesale Receipt of Application Acknowledgement & File Tracking Form [Wholesale Transaction Only Internal Operational Form] 38 Here's the Story [Retail Transactions Only] 39 Closing Agent Notification Form/Wiring/Closing Info [M&T Closer and Settlement Agent to complete] 40 P1 Checklist [Retail Transactions] 41 Clear to Close Checklist [Retail Transactions] 42 Clear to Close Confirmation [include any Quality Control Reviews] 43 HIGH COST ONLY: PCI Results 44 Broker Fee Sheet [MT4593] - Wholesale Transactions Only 45 Invoices to be Paid at Closing 46 Prelim HUD-1 Settlement Statement 47 Current Payoff Letter 48 Power of Attorney T [Fully Executed] 50 Commitment Letter/Approval Certificate (M&T Issued) Day Letter or Pend Notices (M&T Issued) K Maximum Mortgage Worksheet [Required on 203(k) Transactions] 53 Fannie Mae HomeStyle Maximum Mortgage Worksheet [Required on HomStyle Transactions] 54 Rehab Permit Certification [Form 8000] 55 FULL 203K: Consultant Agreement / Consultant Invoice(s) 56 FULL 203K: Consultant Identity of Interest 57 FULL 203K or FULL HomeStyle: Specification of Repairs/Work Write-Up [Fully Executed/All Pages] 58 M&T Contractor Acceptance Checklist [MT Exh ] 59 FHA 203K Homeowner Contractor Agreement [Form 2420] OR HomeStyle Homeowner Contractor Agreement [Form2101] [Fully Executed/One for each Contractor] 60 Cost Estimates 61 Contractor License [for each Contractor] 62 Contractor Liability Insurance [for each Contractor] 63 Contractor Resume [for each Contractor] 64 Contractor Research [M&T Issued/Nexis search/supporting Docs] K Borrowers Acknowledgment [HUD92700-A] OR HomeStyle Borrowers Acknowledgement [Form 2600] K Borrower Identity of Interest Form [Fully Executed] 67 HomeStyle Renovation Consumer Tips [Form 2602] 68 Draw Request [HUD9746-A] 69 Closing Protection Letter 70 Preliminary Title Policy 71 Flood Certification 72 Hazard Insurance and/or Flood Insurance

8 BROKER OR LOAN OFFICER OPERATIONS READY/ NOT READY DOCS Responsible Party RENOVATION LOAN CHECKLIST REQUIRED DOCUMENTS FOR ALL FILES 73 Special Flood Hazard Determination Disclosure 74 Registration/Lock/Extension Confirmations 75 Authorization to Release Mortgage Information - [Retail Transactions Only] 76 Broker Certification of Fees Collected Form [MT3111] - Wholesale Transactions Only 77 FHA: Case Number Assignment / Refi Authorization 78 FHA: CAIVRS - All Borrowers 79 ACH Information Form (if applicable) [Retail Transactions Only] 80 Required Fees Collected/Fee Authorization Form [Retail Transactions Only] 81 Change of Circumstance/Revised GFE(s) in the order of disclosure [Most recent on top] Retail Transactions - Changed Circumstance Worksheets and Changed Circumstance GFEs are completed by mortgage operations. Wholesale Transactions - The broker is responsible for the completion of the changed circumstance worksheet and changed circumstance GFE for changed circumstances that occur prior to the submission of the loan to M&T. Any changed circumstances GFEs that are issued by the broker between the time of registration and submission must be included in the submission package. M&T is responsible for the completion of the changed circumstance worksheet and changed circumstance GFE for changed circumstances that occur once the loan is in M&T's possession. 82 Good Faith Estimate Accepted by Registration 83 Breakdown of Box 1 and 4 of Title Fees [Retail Transactions Only] 84 Good Faith Estimate Cost Breakdown and Intent to Proceed - [Wholesale Transactions Only] 85 Good Faith Estimate Acceptance Certification Form 86 Settlement Service Provider Disclosures 87 LSS Affiliated Business Arrangement Disclosure [Retail Transaction Only - if applicable] 88 Broker Fee Agreement [Wholesale Transactions Only] 89 Anti-Steering Disclosure [Wholesale Transactions Only] Truth In Lending(s) Issued by M&T or Table Funded Broker in order of issuance [Most recent should always be on top] M&T Servicing Transfer Disclosure [MT2240] Retail Transactions - This document must be submitted with a "ready" package. Wholesale Transactions - This document is issued by M&T Mortgage Operations within 3 business days of receiving the submission package. 92 M&T Right to Receive an Appraisal Disclosure [Wholesale Transactions Only] 93 M&T Lock In Disclosure in CT (Floating/Lock) [Wholesale Transactions Only] 94 Lock-in or Floating Rate Agreement/Disclosure [Retail Transactions Only] 95 BROKER: Servicing Transfer Disclosure [Table Funded Wholesale Transactions Only] 96 BROKER: Right to Receive an Appraisal Disclosure [Table Funded Wholesale Transactions Only] 97 Photo Id / Social Security Card 98 ECOA Disclosure [Wholesale Transactions Only] 99 Patriot Act Disclosure [Wholesale Transactions Only] NYS Credit Report Disclosure Notice to Home Loan Applicant AND FACTA Disclosure [Delivered to borrower by Credit Bureau when M&T orders credit] 102 Risk Based Pricing Disclosure [Delivered to borrower by Credit Bureau when M&T orders credit]

9 BROKER OR LOAN OFFICER OPERATIONS READY/ NOT READY DOCS Responsible Party RENOVATION LOAN CHECKLIST REQUIRED DOCUMENTS FOR ALL FILES 103 ARM Disclosure (if applicable) 104 FHA 2-4 Unit Hotel and Transient Use form [HUD92561] 105 Borrower(s) Certification and Authorization [MT2096] 106 FHA: Informed Consumer Choice Disclosure 107 FHA: Important Notice to Homebuyer [HUD92900-B] 108 FHA: Notice to Homeowner/Assumption 109 State Specific Requirements [as per MEME guidance]

10

11 HOMESTYLE HOMEOWNER/CONTRACTOR AGREEMENT Owner's Name(s): Address: City: State: Zip Code: Telephone Number: Work: Home: Contractor s Name(s): License No: Address: City: State: Zip Code: Telephone Number: Work: Home: THIS AGREEMENT, made this date,, between the above mentioned Homeowner (Owner) and Contractor, is for the rehabilitation of the property located at that has been approved for a Fannie Mae HomeStyle rehabilitation mortgage. The Owner(s) shall pay the Contractor the sum of $ for completion of the work, including all sales tax due by law, together with such increases or decreases in the contract price as may be approved in writing by the Lender. The work will begin within 30 days of loan closing with the Lender and will be completed by, unless delayed beyond the Contractor's control. The General Provisions listed below are made a part of this Agreement. The contract documents consist of the architectural exhibits listed in the Rehabilitation Loan Agreement between the Owner(s) and the Lender, or as described below (or on an attached sheet): Owner(s) Signature(s) and Date Contractor's Signature and Date 1. Contract Documents: This Agreement includes all general provisions, special provisions and architectural exhibits that were accepted by the lender. Work not covered by this agreement will not be required unless it is required by reasonable inference as being necessary to produce the intended result. By executing this Agreement, the contractor represents that he/she has visited the site and understands local conditions, including state and local building regulations and conditions under which the work is to be performed. 2. Owner: Unless otherwise provided for in the Agreement, the owner will secure and pay for necessary easements, exceptions from zoning requirements, or other actions which must precede the approval of a permit for this project. If owner fails to do so then the contract is void. If the contractor fails to correct defective work or persistently fails to carry out the work in accordance with the agreement or general provisions, the owner may order the contractor in writing to stop such work, or a part of the work, until the cause for the order has been eliminated. 3. Contractor: The contractor will supervise and direct the work and the work of all subcontractors. He/she will use the best skill and attention and will be solely responsible for all construction methods and materials and for coordinating all portions of the work. Unless otherwise specified in the Agreement, the contractor will provide for and/or pay for all labor, materials, equipment, tools, machinery, transportation, and other goods, facilities, and services necessary for the proper execution and completion of the work. The contractor will maintain order and discipline among employees and will not assign anyone unfit for the task. The contractor warrants to the owner that all materials and equipment incorporated are new and that all work will be of good quality and free of defects or faults. The contractor will pay all sales, use and other taxes related to the work and will secure and pay for building permits and/or other permits, fees, inspections and licenses necessary for the completion of the work unless otherwise specified in the Agreement. The contractor will indemnify and hold harmless the owner from and against all claim, damages, losses, expenses, legal fees or other costs arising or resulting from the contractors performance of the work or provisions of this section. The contractor will comply with all rules, regulations, laws, ordinances and orders of any public authority or HUD inspector 9if applicable) bearing on the performance of the work. The contractor is responsible for, and indemnifies the Owner against, acts and omissions of employees, subcontractors and their employees, or others performing the work under this Agreement with the contractor.

12 The contractor will provide shop drawings, samples, product data or other information provided for in this Agreement, where necessary. 4. Subcontractor: Selected by the contractor, except that the contractor will not employ any subcontractor to whom the owner may have a reasonable objection, nor will the contractor be required by the owner to employ any subcontractor to whom the contractor has a reasonable objection. 5. Work By Owner or Other Contractor: The owner reserves the right to perform work related to the project, but which is not a part of this Agreement, and to award separate contracts in connection with other portions of the project not detailed in this Agreement. All contractors and subcontractors will be afforded reasonable opportunity for the storage of materials and equipment by the owner and by each other. Any costs arising by defective or ill-timed work will be borne by the responsible party. 6. Binding Arbitration: Claims or disputes relating to the Agreement or General Provisions will be resolved by the Construction Industry Arbitration Rules of the American Arbitration Association (AAA) unless both parties mutually agree to other methods. The notice of the demand for arbitration must be filed in writing with the other party to this Agreement and with the AAA and must be made in a reasonable time after the dispute has arisen. The award rendered by the arbitrator(s) will be considered final and judgment may be entered upon it in accordance with applicable law in any court having jurisdiction thereof. 7. Cleanup and Trash Removal: The contractor will keep the owner s residence free from waste or rubbish resulting from the work. All waste, rubbish, tools, construction materials, and machinery will be removed promptly after completion of the work by the contractor. 8. Time: With respect to the scheduled completion of the work, time is of the essence. If the contractor is delayed at anytime in the progress of the work by change orders, fire, labor disputes, acts of God or other causes beyond the contractor's control, the completion schedule for the work or affected parts of the work may be extended by the same amount of time caused by the delay. The contractor must begin work no later than 30 days after loan dosing and will not cease work for more than 30 consecutive days. 9. Payments and Completion: Payments may be withheld because of. (1) defective work not remedied; (2) failure of contractor to make proper payments to subcontractors, workers, or suppliers; (3) persistent failure to carry out work in accordance with this Agreement or these general conditions, or (4) legal claims. Final payment will be due after complete release of any and all liens arising out of the contract or submission of receipts or other evidence of payment covering all subcontractors or suppliers who could file such a lien. The contractor agrees to indemnify the Owner against such liens and will refund all monies including costs and reasonable attorney's fees paid by the owner in discharging the liens. A 10 percent holdback is required by the lender to assure the work has been properly completed and there are no liens on the property. 10. Protection of Property and Persons: The contractor is responsible for initiating. maintaining, and supervising all necessary or required safety programs. The contractor must comply with all applicable laws, regulations, ordinances, orders or laws of federal, state, county or local governments. The contractor will indemnify the owner for all property loss or damage to the owner caused by his/ her employees or his/her direct or subtier subcontractors. 11. Insurance: The contractor will purchase and maintain such insurance necessary to protect from claims under workers compensation and from any damage to the owner(s) property resulting from the conduct of this contract. 12. Changes in the Contract: The owner may order changes, additions or modifications (using Fannie form 1200) without invalidating the contract. Such changes must be in writing and signed by the owner and accepted by the lender. Not all change order requests may be accepted by the lender, therefore, the contractor proceeds at his/her own risk if work is completed without an accepted change order. 13. Correction of Deficiencies: The contractor must correct promptly any work of his/her own or his/her subcontractors found to be defective or not complying with the terms of the contract. 14. Warranty: The contractor will provide a one-year warranty on all labor and materials used in the rehabilitation of the property. This warranty must extend one year from the date of completion of the contract or longer if prescribed by law unless otherwise specified by other terms of this contract. Disputes will be resolved through the Construction Industry Arbitration Rules of the American Arbitration Association. I5. Termination: If the owner fails to make a payment under the terms of this Agreement, through no fault of the contractor, the contractor may, upon ten working days written notice to the owner, and if not satisfied, terminate this Agreement. The owner will be responsible for paying the contractor for all work completed. If the contractor fails or neglects to carry out the terms of the contract, the owner, after ten working days written notice to the contractor, may terminate this Agreement. Owner s Initials: Contractor s Initials:

13

14 HomeStyle Borrower s Acknowledgment Condition of Property: I/We understand that the property I/we am/are purchasing is not Fannie Mae approved, and FannieMae does not warrant the condition or the value of the property. I/We understand the Fannie Mae plan review (where performed) and the appraisal are performed to determine compliance with the required architectural exhibits and to estimate the value of the property, but neither guarantees the house is free of defects. I/We understand I/we have the option to retain an independent consultant and/or a professional home inspection service to perform an inspection of the property. The cost of this inspection can (or could be) included in the mortgage. Loan Requirements: I/We understand at the time of the loan closing of a Home Improvement Mortgage Loan, for which I/we have applied to my lender, the proceeds designated for the rehabilitation or improvement (including a contingency reserve, mortgage payments, and any other fees where applicable) are to be placed in an interest bearing escrow account. The Rehabilitation Escrow Account is not, nor will it be treated as, an escrow for the paying of real estate taxes, insurance premiums, delinquent notes, ground rents or assessments. I/We hereby request the lender, after the Final Release Notice is issued to: pay the net interest income directly to me/us. apply the net interest income directly to the mortgage principal balance for an equal amount of principal reduction. I/We understand that the Rehabilitation Escrow Account will cease paying interest to me/us if (1) the loan payments are delinquent for more than 30 days; or (2) the completion date (or an approved extension) has expired. During this period, the interest will be paid down on the mortgage principal. I/We understand that if I/we clear up the delinquent or default status and/or the completion date has not expired or an extension date has been approved, then the interest on the escrow account will begin again to be paid according to the request above. I/We understand that no draws on the escrow account can be made until all permits have been issued by the local or state building departments, where required. I/We further understand I/we can only request moneys for the actual cost of rehabilitation. If any cost savings result on any line item of the Draw Request, the amount saved must be used to prepay the mortgage principal. I/We understand the contractor(s) is responsible to complete the work described in the architectural exhibits in a workmanlike manner. If I/we agree that the work has been properly completed I/we will sign the Draw Request form, thereby accepting the responsibility that the completed work is acceptable and payment is justified. I/We understand there may be, at the sole discretion of the lender, a ten percent (10%) holdback on each Draw Request to assure that the work is properly completed and for lien protection. I/We understand I/we am/are responsible to negotiate any and all agreements with the contractor(s) I/we select, and that Fannie Mae suggests that the agreement with the contractor(s) should include a provision for binding arbitration with the American Arbitration Association on any dispute. I/We understand if I/we change a contractor for any reason, I/we may be obligated under the terms of the original contractor(s) agreement, and I/we should seek legal advice before taking such action. If I/we disagree with the contractor regarding the acceptable completion of the work I/we can request an inspection by the fee inspector to determine if the work has been property completed. If an agreement cannot be made with the contractor, the lender may hold the money until such time as an agreement is reached, or an arbitrator=s decision is rendered. I/We understand that neither the lender nor FannieMae provides any warranty on the completed work on the property. I/we am/are responsible to obtain such warranty(s) from the contractor(s), and the warranty should be stated in the Homeowner-Contractor Agreement. I/we understand I/we am/are responsible to make the mortgage payments during the term of the loan, including the rehabilitation period, to ensure that the property will not go into default. The construction on the home must start within 30 days; if the construction ceases for more than 30 days, the lender may consider the loan in default, or the lender may use the escrow money to have the work completed. If the work stops or is not progressing as it should or if the work does not comply with accepted architectural exhibits, the lender may require additional compliance inspections to protect the security of the loan and I will be responsible to pay for the inspections, and the cost of the inspections may be withheld at the next draw request. I/We understand no changes to the architectural exhibits can be made without written approval by the lender on a letter or on a form (HUD-9746-A) which I submit to the lender. Also, the contingency fund is set up for changes that affect the health, safety, or items of necessity of the occupants of the property. If the contingency reserve is insufficient, I must place additional moneys into the account for payment upon acceptance of the change. A change order will be made to assure that the moneys are available to the contractor upon completion of the changed work. I/We understand if there are unused contingency funds, mortgage payments, inspection fees or other monies in the Rehabilitation Escrow Account after the Final Release is processed, the lender, in compliance with Fannie Mae regulations, must apply these funds to prepay the mortgage principal, provided those items are a part of the mortgage. I/We understand the lender, at lenders sole discretion, may retain the ten percent (10%) holdback from each draw, for a period not to exceed 35 days or the time period required by law to file a lien (whichever is longer), to ensure compliance with state lien waiver laws or other state requirements. Upon completion of the work, I understand I will be provided: (1) the Final Draw Request; (2) the Final Release Notice; (3) an accounting of the final distribution of all funds. This statement must be delivered to you prior to closing the loan. Return one copy to your lender as proof that you have read the entire document. Keep one copy for your records. You, the borrower(s), must be certain that you understand this information. Sign here only after you have read this entire document. Seek professional advice if you are uncertain. x Borrower s Signature and Date x Co-Borrower s Signature and Date I, the lender, certify this information was delivered to the borrower(s) prior to the time of loan closing. x Lender s Signature and Date FNMA HomeStyle Borrower s Acknowledgement Form 2600 Borrower: Loan#:

15 HomeStyle Renovation Consumer Tips Case Number: Date: Borrower Names: Please review the important tips listed below about Fannie Mae HomeStyle Renovation Mortgages and home improvement projects. For the HomeStyle Renovation Mortgage, you do not receive any cash at the loan closing. The funds provided for renovation are placed in an interest-bearing escrow account (Renovation Escrow Account). The lender may require that a contingency reserve be placed in the Renovation Escrow Account to cover unforeseen repairs or deficiencies during the renovation. If funds remain after the renovation is complete, they can be applied to additional elective repairs or improvements or can be used to reduce the principal balance. If you deposit funds into the account, the funds you deposited can be paid directly back to you at your option. When selecting a contractor, always review the contractor s references, licensing, and financial background. Ask the lender for a Contractor Profile form to assist in your review, or locate one at You are responsible for negotiating any agreements or warranties with the contractor. The lender does not provide any warranty on the contractor s work. You are responsible for overseeing the renovation and ensuring that it is done as specified in the Construction Contract with the contractor. If work stops for an extended period of time, or there are problems with the work performed that may cause significant delays, you must contact the lender. If you are purchasing a home to renovate it, please note that the lender does not warrant or guarantee the condition of the property being purchased or the renovation. You are responsible for making the mortgage payment each month, even if the renovation is not satisfactorily completed. Funds for the renovation are paid in accordance with a schedule acceptable to you, the contractor, and the lender. Funds are released to the contractor after an inspection of each phase of the renovation. The funds are provided in a check made payable jointly to both you and the contractor. You request these payments on a draw request form submitted to the lender. Do not approve funds be released to the contractor if you are not happy with the work. Do not accept unsatisfactory work. Do not pay the contractor up front out of your own funds before the renovation is satisfactorily completed. The lender may withhold some of the funds from each Draw Request. These funds are paid to the contractor when the work is completed. This helps to protect you from a contractor failing to complete the renovation If you would like to revise the original approved renovation, you must submit a Change Order Request to the lender for approval, and deposit any additional required funds (including contingency reserve) in the Renovation Escrow Account. When the renovation is completed, you and the contractor sign a Completion Certificate. The lender should provide you an accounting for all distribution of funds in the Renovation Escrow Account. I acknowledge that I have read these Consumer Tips and that I understand them. Borrower s Signature: Co-borrower s Signature: The lender certifies the Borrower(s) has received these Consumer Tips. Lender s Signature: Date: Date: Date: FNMA HomeStyle Consumer Tips Disclosure Loan # Form 2602/MT4617 Rev. 11/1/01 Borrower

16 Answer all Questions Below: 1. Are any of your income taxes past due? YES NO 2. Have you or any principals of your company, or your company declared bankruptcy? YES NO 3. Are there any outstanding judgments or legal actions pending against you or the company? YES NO If any answers were YES, please explain below: To M&T Bank: INFORMATION: All information given in this document is true, correct and complete as of the date of this document. I/We authorize you to verify any information given. In addition, I/we authorize you to obtain any information you feel is necessary or in connection with any review, update, extension or renewal in maintaining an approved status with M&T. Finally, I/we authorize you to give information about me (us) and your credit experience with me/us to others. CREDIT REPORTS: I/we understand that you may request a credit report from a credit reporting agency in connection with this document or in connection with any update, extension or renewal of any credit you extend based upon this document. In addition, I/we understand that, if asked, you will tell me/us if a credit report was requested, and if so, the name and address of the credit reporting agency furnishing the credit report. To request the information, I/we should write or call the Construction Lending Department; M&T Bank P. O. Box 4009; Buffalo, New York (800) KEEPING RESUME: I/we agree that you may keep this resume for your file. Name of Applicant By Signature and Title Contractor s Resume Loan #: Form 2605 Rev Borrower:

HomeStyle Renovation Submission Checklist

HomeStyle Renovation Submission Checklist Borrower Name: Loan #: Homestyle Calculation Worksheet (LoanBuilder) * HomeStyle Renovation Consumer Tips (Form 1204) signed by borrower Appraisal with all improvements

HomeStyle Renovation Submission Checklist Borrower Name: Loan #: Homestyle Calculation Worksheet (LoanBuilder) * HomeStyle Renovation Consumer Tips (Form 1204) signed by borrower Appraisal with all improvements

Document Checklist for 203k Loans

Document Checklist for 203k Loans HUD-92700: 203(k) and Streamlined (k) Maximum Mortgage Worksheet HUD-92700a: 203(k) Borrower's Acknowledgment Appraisal with all improvements listed on Repairs & Updates

Document Checklist for 203k Loans HUD-92700: 203(k) and Streamlined (k) Maximum Mortgage Worksheet HUD-92700a: 203(k) Borrower's Acknowledgment Appraisal with all improvements listed on Repairs & Updates

LIST OF REQUIRED DOCUMENTS FROM CONTRACTORS FOR 203K S:

LIST OF REQUIRED DOCUMENTS FROM CONTRACTORS FOR 203K S: 1. BID TO MATCH SCOPE OF WORK 2. BUYER-CONTRACTOR AGREEMENT 3. COPY OF YOUR GENERAL CONTRACTOR IDENTIFICATION CARD 4. CONTRACTOR PROFILE 5. RENOVATION

LIST OF REQUIRED DOCUMENTS FROM CONTRACTORS FOR 203K S: 1. BID TO MATCH SCOPE OF WORK 2. BUYER-CONTRACTOR AGREEMENT 3. COPY OF YOUR GENERAL CONTRACTOR IDENTIFICATION CARD 4. CONTRACTOR PROFILE 5. RENOVATION

Checklist for Contractor. FHA 203Ks Program

Contractor are For acompleted A request to use contingency funds can be submitted to address unforeseen deficiencies affecting the health, safety and structure of the property. Checklist for Contractor

Contractor are For acompleted A request to use contingency funds can be submitted to address unforeseen deficiencies affecting the health, safety and structure of the property. Checklist for Contractor

203(K) STANDARD OWNER/CONTRACTOR AGREEMENT

STANDARD OWNER/CONTRACTOR AGREEMENT") 203(K) STANDARD OWNER/CONTRACTOR AGREEMENT Loan Number: : Provided By: Primary Borrower: CARRINGTON MORTGAGE SERVICES, LLC Property Address: Homeowner (s) ( Homeowner and/or Borrower ) FHA Case #: Address:

203(K) STANDARD OWNER/CONTRACTOR AGREEMENT Loan Number: : Provided By: Primary Borrower: CARRINGTON MORTGAGE SERVICES, LLC Property Address: Homeowner (s) ( Homeowner and/or Borrower ) FHA Case #: Address:

CONTRACTOR'S GUIDE 203(K) STANDARD

STANDARD") CONTRACTOR'S GUIDE 203(K) STANDARD CONTRACTOR'S CHECKLIST Contractor Profile W-9 Contractor's License(s) General Liability (Certificate of Insurance) Workman's Comp (Certificate of Insurance) Disclosures

CONTRACTOR'S GUIDE 203(K) STANDARD CONTRACTOR'S CHECKLIST Contractor Profile W-9 Contractor's License(s) General Liability (Certificate of Insurance) Workman's Comp (Certificate of Insurance) Disclosures

Self Help Letter & Documentation If Applicable, proof of experience in scope of work

FHA 203(K) LIMITED CHECKLIST BORROWER FORMS & DISCLOSURES Notice to Borrowers Limited (attached) Borrower s Acknowledgement (attached) Borrower s Identity of Interest (attached) Project Maturity Disclosure

FHA 203(K) LIMITED CHECKLIST BORROWER FORMS & DISCLOSURES Notice to Borrowers Limited (attached) Borrower s Acknowledgement (attached) Borrower s Identity of Interest (attached) Project Maturity Disclosure

203K Steps to Success

203K Steps to Success Disclosing the Loan estimate for a 203K Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit Report (if locked

203K Steps to Success Disclosing the Loan estimate for a 203K Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit Report (if locked

Low down payment option; qualify with as little as 3.5% down

Not every home is move-in ready. The FHA 203(k) Renovation Loan allows you to broaden your home shopping horizons and create the home you want from the start. The FHA 203(k) Renovation Loan combines the

Not every home is move-in ready. The FHA 203(k) Renovation Loan allows you to broaden your home shopping horizons and create the home you want from the start. The FHA 203(k) Renovation Loan combines the

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

Properties listed with the following two logos are eligible: and

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate FNMA only Eligible properties must be owned by Fannie Mae (as a result of foreclosure or other similar action such as deed-in-lieu of foreclosure), sold by

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate FNMA only Eligible properties must be owned by Fannie Mae (as a result of foreclosure or other similar action such as deed-in-lieu of foreclosure), sold by

203(k) Program Full and Streamline

Program Full and Streamline") General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home The new first mortgage includes the purchase price or

General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home The new first mortgage includes the purchase price or

HomeStyle Renovation Product Offering 8/29/14

HomeStyle Renovation Product Offering 8/29/14 Overview of HomeStyle Offering Define the HomeStyle product and features Discuss benefits of the HomeStyle renovation loan Learn how to determine eligibility

HomeStyle Renovation Product Offering 8/29/14 Overview of HomeStyle Offering Define the HomeStyle product and features Discuss benefits of the HomeStyle renovation loan Learn how to determine eligibility

RESIDENTIAL CONSTRUCTION LENDING POLICY

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

Benefits to Borrower - Why Renovation?

Whether your borrower is looking to purchase a home that needs renovations or repairs or are refinancing an existing mortgage and looking to make home improvements, the Fannie Mae Homestyle Renovation

Whether your borrower is looking to purchase a home that needs renovations or repairs or are refinancing an existing mortgage and looking to make home improvements, the Fannie Mae Homestyle Renovation

FHA Renovation Loan Program, or 203K

FHA Renovation Loan Program, or 203K The Federal Housing Administration (FHA), which is part of the Department of Housing and Urban Development (HUD), administers various single family mortgage insurance

FHA Renovation Loan Program, or 203K The Federal Housing Administration (FHA), which is part of the Department of Housing and Urban Development (HUD), administers various single family mortgage insurance

FHA 203(K) PROGRAM. General Description. Overlays. Available Options

PROGRAM. General Description. Overlays. Available Options") General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home. The new first mortgage includes the purchase price or

General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home. The new first mortgage includes the purchase price or

Under Construction. Construction and Rehab Loan Programs

Under Construction Construction and Rehab Loan Programs Sources: FNMA FHA Portfolio Lenders Home equity lines of credit for homes already owned FNMA Homestyle Renovation Loan Loan Purpose Purchase Terms

Under Construction Construction and Rehab Loan Programs Sources: FNMA FHA Portfolio Lenders Home equity lines of credit for homes already owned FNMA Homestyle Renovation Loan Loan Purpose Purchase Terms

Products. Loan Amount

Freedom Mortgage FHA 203(k) FRM & ARM Product Guide Loan Program Overview This document is not all encompassing. It is a summary reference tool to be utilized in conjunction with Agency guidelines and

Freedom Mortgage FHA 203(k) FRM & ARM Product Guide Loan Program Overview This document is not all encompassing. It is a summary reference tool to be utilized in conjunction with Agency guidelines and

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage General Eligibility Requirements Loans must fully comply with all requirements of this Product Guide, Desktop Underwriter

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage General Eligibility Requirements Loans must fully comply with all requirements of this Product Guide, Desktop Underwriter

203k Quick Reference Guide

Table of Contents 203(K) Quick Reference Consumer Renovation Information 203(K) Borrower s Acknowledgement Rehabilitation Loan Agreement Consultant s Identity of Interest Certification Borrower s Identify

Table of Contents 203(K) Quick Reference Consumer Renovation Information 203(K) Borrower s Acknowledgement Rehabilitation Loan Agreement Consultant s Identity of Interest Certification Borrower s Identify

FNMA Homestyle Steps to Success

FNMA Homestyle Steps to Success Disclosing the Loan estimate for a FNMA Homestyle Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit

FNMA Homestyle Steps to Success Disclosing the Loan estimate for a FNMA Homestyle Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit

Renovation Lending Suite

Renovation Lending Suite M A R C H, 2 0 1 9 4/10/2019 1 Agenda Renovation Loans FHA 203(k): Limited & Standard FNMA HomeStyle Renovation Need to Knows Processing Renovation Loans Reference Materials Why

Renovation Lending Suite M A R C H, 2 0 1 9 4/10/2019 1 Agenda Renovation Loans FHA 203(k): Limited & Standard FNMA HomeStyle Renovation Need to Knows Processing Renovation Loans Reference Materials Why

Standard Form of Agreement Between Owner and Contractor for a Residential or Small Commercial Project

Document A105 2007 Standard Form of Agreement Between Owner and Contractor for a Residential or Small Commercial Project AGREEMENT made as of the in the year (In words, indicate day, month and year.) BETWEEN

Document A105 2007 Standard Form of Agreement Between Owner and Contractor for a Residential or Small Commercial Project AGREEMENT made as of the in the year (In words, indicate day, month and year.) BETWEEN

M&T s Guide for SONYMA Loans

M&T s Guide for SONYMA Loans 4/6/11-1 - TABLE OF CONTENTS I. SONYMA A. General Information 1. M&T Responsibilities 2. Broker Responsibilities 3. First-time Home-buyer Definition 4. Recapture Tax 5. SONYMA

M&T s Guide for SONYMA Loans 4/6/11-1 - TABLE OF CONTENTS I. SONYMA A. General Information 1. M&T Responsibilities 2. Broker Responsibilities 3. First-time Home-buyer Definition 4. Recapture Tax 5. SONYMA

***PROVIDE PRELIM HUD FROM TITLE SHOWING THEIR FEE BREAKDOWN***

CCI DOC ORDER FORM INVESTOR: LOAN #: CIRCLE ONE: CONV / FHA / VA / 2ND INVESTOR PROGRAM CODE: CLOSING DATE & TIME: DISBURSEMENT DATE: FIRST PYMT DUE DATE: BASE LOAN AMOUNT: TOTAL LOAN AMT: INTEREST RATE:

CCI DOC ORDER FORM INVESTOR: LOAN #: CIRCLE ONE: CONV / FHA / VA / 2ND INVESTOR PROGRAM CODE: CLOSING DATE & TIME: DISBURSEMENT DATE: FIRST PYMT DUE DATE: BASE LOAN AMOUNT: TOTAL LOAN AMT: INTEREST RATE:

A1 Mortgage Processing Services, Inc., Contract Processing Agreement

A1 Mortgage Processing Services, Inc., Contract Processing Agreement This agreement is made and entered into this day of,, by and between (Broker name), hereinafter referred to as "the Broker", and A1

A1 Mortgage Processing Services, Inc., Contract Processing Agreement This agreement is made and entered into this day of,, by and between (Broker name), hereinafter referred to as "the Broker", and A1

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist First Time Home Buyer Program

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist First Time Home Buyer Program BORROWER NAME(S): HMFA Loan # Smart Start Loan # Address: City State Zip Code Lender Name:

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist First Time Home Buyer Program BORROWER NAME(S): HMFA Loan # Smart Start Loan # Address: City State Zip Code Lender Name:

RENOVATION LOAN AGREEMENT

THIS IS A MODEL DOCUMENT FOR USE IN FANNIE MAE RENOVATION LOAN TRANSACTIONS. THIS FORM IS PROVIDED AS AN EXAMPLE AND HAS NOT BEEN EVALUATED FOR VALIDITY AND ENFORCEABILITY IN ANY JURISDICTION. LENDERS

THIS IS A MODEL DOCUMENT FOR USE IN FANNIE MAE RENOVATION LOAN TRANSACTIONS. THIS FORM IS PROVIDED AS AN EXAMPLE AND HAS NOT BEEN EVALUATED FOR VALIDITY AND ENFORCEABILITY IN ANY JURISDICTION. LENDERS

INSURING QUALITY ASSURANCE CHECKLIST

Borrower: Loan #: Late Endorsement Letter Yes No N/A 1. Present in the file if endorsed 60 days or more after disbursement date: a. If PR applied on loan, payment history reflects PR amount as well as

Borrower: Loan #: Late Endorsement Letter Yes No N/A 1. Present in the file if endorsed 60 days or more after disbursement date: a. If PR applied on loan, payment history reflects PR amount as well as

***UPDATED 9/5/18*** TPO Fannie Mae HomeStyle Renovation Product

***UPDATED 9/5/18*** Updated items have been highlighted in yellow. TPO Fannie Mae HomeStyle Renovation Product Overview HomeStyle is Fannie Mae s renovation loan program. This loan will be locked in,

***UPDATED 9/5/18*** Updated items have been highlighted in yellow. TPO Fannie Mae HomeStyle Renovation Product Overview HomeStyle is Fannie Mae s renovation loan program. This loan will be locked in,

Limited FHA 203K. Village Mortgage NMLS Intended for Mortgage Professionals Only 1

Limited FHA 203K Before After Village Mortgage NMLS 6331 Intended for Mortgage Professionals Only 1 Program Highlights Up to $35,000 in repairs with no minimum No consultant required Up to 3 Contractors

Limited FHA 203K Before After Village Mortgage NMLS 6331 Intended for Mortgage Professionals Only 1 Program Highlights Up to $35,000 in repairs with no minimum No consultant required Up to 3 Contractors

Revised 4/6/18. FHA 203K Renovation

Revised 4/6/18 FHA 203K Renovation Important Notice While every effort has been made to ensure the reliability of the training content, PRMG s product profiles and their updates, are the official statements

Revised 4/6/18 FHA 203K Renovation Important Notice While every effort has been made to ensure the reliability of the training content, PRMG s product profiles and their updates, are the official statements

CONSTRUCTION CONTRACT EXAMPLE

P a g e 1 CONSTRUCTION CONTRACT EXAMPLE THIS AGREEMENT, made and entered into this date, by and between, hereinafter called CONTRACTOR, and NPC QUALITY BURGER, INC., hereinafter called OWNER. IT IS HEREBY

P a g e 1 CONSTRUCTION CONTRACT EXAMPLE THIS AGREEMENT, made and entered into this date, by and between, hereinafter called CONTRACTOR, and NPC QUALITY BURGER, INC., hereinafter called OWNER. IT IS HEREBY

BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name:

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Signed 4506 T BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name: Required Items

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Signed 4506 T BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name: Required Items

FHA 203(k) Standard Product Guide

Standard Product Guide") FHA 203(k) Standard Product Guide Section 203(k) Financing enables homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single

FHA 203(k) Standard Product Guide Section 203(k) Financing enables homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single

PURCHASE. Max LTV w/o Sec. Fin. Max LTV w/ Sec. Fin. Max TLTV w/ Sec. Fin.

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

VA IRRRL PROGRAM MATRIX

MAXIMUM LTV **Mortgage Only Report IRRRL PROGRAM 1-4 Unit Properties, Condos, and PUD s (Primary Residence) NO FICO PROGRAM MINIMUM FICO MAX LTV 580 100% 620 125% **No FICO 660 UNLIMITED High Balance 100%

MAXIMUM LTV **Mortgage Only Report IRRRL PROGRAM 1-4 Unit Properties, Condos, and PUD s (Primary Residence) NO FICO PROGRAM MINIMUM FICO MAX LTV 580 100% 620 125% **No FICO 660 UNLIMITED High Balance 100%

New Jersey Housing and Mortgage Finance Agency

New Jersey Housing and Mortgage Finance Agency Underwriting Submission Checklist First Time Home Buyer Program Borrower Name(S): HMFA Loan #: Smart Start Loan#: HomeSeeker Loan#: Address: _City: State:

New Jersey Housing and Mortgage Finance Agency Underwriting Submission Checklist First Time Home Buyer Program Borrower Name(S): HMFA Loan #: Smart Start Loan#: HomeSeeker Loan#: Address: _City: State:

Lenders must be approved by PennyMac prior to delivering HomeStyle loans.

PennyMac Correspondent Group Fannie Mae HomeStyle Product Profile 03.19.18 Overlays to Fannie Mae are underlined Lenders must be approved by PennyMac prior to delivering HomeStyle loans. Agency Finance

PennyMac Correspondent Group Fannie Mae HomeStyle Product Profile 03.19.18 Overlays to Fannie Mae are underlined Lenders must be approved by PennyMac prior to delivering HomeStyle loans. Agency Finance

STANDARD MORTGAGE CORP

Contact Information: STANDARD MORTGAGE CORP These email addresses are monitored at all times during the business day. Lock requests and lock modifications should go to lockdesk@stanmor.com General underwriting

Contact Information: STANDARD MORTGAGE CORP These email addresses are monitored at all times during the business day. Lock requests and lock modifications should go to lockdesk@stanmor.com General underwriting

HUNTINGTON PORTFOLIO Fixed and Adjustable Rate Conforming and Non-Conforming Products INVESTOR 1/1, 3/1, 5/1, 7/1 10/1 & 15/1 ARMs

PRODUCTS: 15 yr Fixed Rate INVESTOR 1/1, 3/1, 5/1, 7/1 10/1 & 15/1 ARMs CODE: Conforming & Non-Conforming 085 BUSINESS TYPE: PORTFOLIO SERVICING: RETAINED REVISED: 10/01/2016 PRODUCT CRITERIA 1) PRODUCT

PRODUCTS: 15 yr Fixed Rate INVESTOR 1/1, 3/1, 5/1, 7/1 10/1 & 15/1 ARMs CODE: Conforming & Non-Conforming 085 BUSINESS TYPE: PORTFOLIO SERVICING: RETAINED REVISED: 10/01/2016 PRODUCT CRITERIA 1) PRODUCT

FHA Streamline Changes; MDIA Revision, Reminders; LP RRM Clarification; Conforming Loan Parameter Changes

Wholesale Partner Announcement At MSI Your Interest Is Our Priority! Issue Date 11/05/09 Effective Date As Noted WPA 2009-042 FHA Streamline Changes; MDIA Revision, Reminders; LP RRM Clarification; Conforming

Wholesale Partner Announcement At MSI Your Interest Is Our Priority! Issue Date 11/05/09 Effective Date As Noted WPA 2009-042 FHA Streamline Changes; MDIA Revision, Reminders; LP RRM Clarification; Conforming

YORK HOMEBUYER ASSISTANCE PROGRAM GUIDELINES AND RULES. Funding Source. Program Code. Eligible States Minimum Loan Amount.

Revised 6/8/2015 YORK HOMEBUYER ASSISTANCE PROGRAM GUIDELINES AND RULES Funding Source Program Description - This program is designed to provide down payment & closing cost assistance to low/moderate income

Revised 6/8/2015 YORK HOMEBUYER ASSISTANCE PROGRAM GUIDELINES AND RULES Funding Source Program Description - This program is designed to provide down payment & closing cost assistance to low/moderate income

FHA 203(k) () streamline mortgage Program

() streamline mortgage Program") FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Presented by: Mountain West Financial Why FHA 203(k) Through the Federal

FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Presented by: Mountain West Financial Why FHA 203(k) Through the Federal

Flanagan State Banks Guide to FHA Disclosures

This reference guide outlines the packet that is provided for Initial Disclosures when using FSB Mortgagebot for disclosing. The documents are listed in the order the system prints the forms. Form Name

This reference guide outlines the packet that is provided for Initial Disclosures when using FSB Mortgagebot for disclosing. The documents are listed in the order the system prints the forms. Form Name

FHA 203(k) () streamline mortgage Program. make improvements all with a single loan

() streamline mortgage Program. make improvements all with a single loan") FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Why FHA 203(k) Through the Federal Housing Administration (FHA) 203(k)

FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Why FHA 203(k) Through the Federal Housing Administration (FHA) 203(k)

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist Homeward Bound Borrower Name(s):

:") New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist Homeward Bound Borrower Name(s): HMFA Homeward Bound Loan Number: SS / Homeseeker # Delivery packages are to be sent

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist Homeward Bound Borrower Name(s): HMFA Homeward Bound Loan Number: SS / Homeseeker # Delivery packages are to be sent

Guideline Reference Applies to ALL Products

Guideline Reference Applies to ALL Products 4506-T CG Ch 5E Loan Documents & Notes CG Ch 6F Employment & Documentation CG Ch 7G FHA Employment & Evaluation & Documentation Product summaries IRS Form 4506T

Guideline Reference Applies to ALL Products 4506-T CG Ch 5E Loan Documents & Notes CG Ch 6F Employment & Documentation CG Ch 7G FHA Employment & Evaluation & Documentation Product summaries IRS Form 4506T

BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name:

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Signed 4506 T ***Wholesale Use Only*** Proof of 4506 Tax Audit Ordered (highly recommend fully processed

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Signed 4506 T ***Wholesale Use Only*** Proof of 4506 Tax Audit Ordered (highly recommend fully processed

2 TERMS AND CONDITIONS

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

FULL DOC. PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO. Owner Occupied (O/O) 1 unit 80% 80% unit (see MI section below) 95% 95% 700

1 unit 80% 80% unit (see MI section below) 95% 95% 700") FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

FHA 203(k) Product Offering 8/12/14

Product Offering 8/12/14") FHA 203(k) Product Offering 8/12/14 Overview of 203(k) Offering Define the 203(k) product and features Discuss benefits of the 203(k) products Learn how to determine eligibility Review guideline specifics

FHA 203(k) Product Offering 8/12/14 Overview of 203(k) Offering Define the 203(k) product and features Discuss benefits of the 203(k) products Learn how to determine eligibility Review guideline specifics

WHOLESALE Good Faith Estimate Compliance Manual

WHOLESALE Good Faith Estimate Compliance Manual Understanding the 2010 GFE Compliance Department 2/2/2015 2015 Pacific One Lending. http://www.nmlsconsumeraccess.org. Rates, fees and programs are subjected

WHOLESALE Good Faith Estimate Compliance Manual Understanding the 2010 GFE Compliance Department 2/2/2015 2015 Pacific One Lending. http://www.nmlsconsumeraccess.org. Rates, fees and programs are subjected

HOUSING CONSTRUCTION CONTRACT (Projects up to $10,000)

") HOUSING CONSTRUCTION CONTRACT (Projects up to $10,000) THIS CONTRACT is by and between the Stockbridge-Munsee Community ( TRIBE ), for its Division of Community Housing, whose address is N8618 Oak St.,

HOUSING CONSTRUCTION CONTRACT (Projects up to $10,000) THIS CONTRACT is by and between the Stockbridge-Munsee Community ( TRIBE ), for its Division of Community Housing, whose address is N8618 Oak St.,

FHA 203K MATRIX. Second Appraisal Requirements

FHA 203K MATRIX Self Help Allowed NO NO ELIGIBLE PROPERTIES 1-4 Family including HUD REOs 1-4 FAMILY INCLUDING HUD REOs ALLOWS RELATIVES/EMPLOYERS TO COMPLETE WORK NO NO MIXED USE ACCEPTABLE ONLY UNDER

FHA 203K MATRIX Self Help Allowed NO NO ELIGIBLE PROPERTIES 1-4 Family including HUD REOs 1-4 FAMILY INCLUDING HUD REOs ALLOWS RELATIVES/EMPLOYERS TO COMPLETE WORK NO NO MIXED USE ACCEPTABLE ONLY UNDER

LiftFund (CDC) 504 Checklist and Loan Application

504 Checklist and Loan Application") 1. 2. LiftFund (CDC) 504 Checklist and Loan Application Copy of photo ID (Driver license) History of the Business. (Business Plan for start-ups.) Equal Opportunity Lender 3. Current personal financial

1. 2. LiftFund (CDC) 504 Checklist and Loan Application Copy of photo ID (Driver license) History of the Business. (Business Plan for start-ups.) Equal Opportunity Lender 3. Current personal financial

THIS CONSTRUCTION CONTRACT ( Contract ) dated as of ( Owner ) and ( Contractor ) having a principal place of business at.

dated as of ( Owner ) and ( Contractor ) having a principal place of business at.") Homeowner Contractor HomeStyle Renovation Contract Loan Number: Date: Borrower Name(s): Phone #: Phone #: THIS CONSTRUCTION CONTRACT ( Contract ) dated as of by and between ( Owner ) and ( Contractor )

Homeowner Contractor HomeStyle Renovation Contract Loan Number: Date: Borrower Name(s): Phone #: Phone #: THIS CONSTRUCTION CONTRACT ( Contract ) dated as of by and between ( Owner ) and ( Contractor )

FHA Product Overview. Product and Underwriting Guidelines. U.S. Bank Home Mortgage Wholesale Division CAT CR U.S.

FHA Product Overview Product and Underwriting Guidelines U.S. Bank Home Mortgage Wholesale Division CAT-12896356 CR-12896418 Not for consumer distribution. This document is not a Consumer Credit Advertisement

FHA Product Overview Product and Underwriting Guidelines U.S. Bank Home Mortgage Wholesale Division CAT-12896356 CR-12896418 Not for consumer distribution. This document is not a Consumer Credit Advertisement

CRA PORTFOLIO NON-CONFORMING PROGRAM

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPRAISAL REQUIREMENTS:... 3 ASSUMABILITY:...

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPRAISAL REQUIREMENTS:... 3 ASSUMABILITY:...

10, 15, 20, 25 & 30 YR Fixed Rates

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

State of New York Mortgage Agency

Exhibit 3 State of New York Mortgage Agency Remodel New York Program Pre Closing Application File Checklist SONYMA requires that this checklist and each of the listed documents, as applicable, be submitted

Exhibit 3 State of New York Mortgage Agency Remodel New York Program Pre Closing Application File Checklist SONYMA requires that this checklist and each of the listed documents, as applicable, be submitted

DOCUMENT CHECKLIST. (Borrower)

") DOCUMENT CHECKLIST (Borrower) : You have chosen a rehabilitation loan and contractor for your home repair/ remodeling project with a FNMA Homestyle Renovation loan. In order to complete your loan application,

DOCUMENT CHECKLIST (Borrower) : You have chosen a rehabilitation loan and contractor for your home repair/ remodeling project with a FNMA Homestyle Renovation loan. In order to complete your loan application,

2 TERMS AND CONDITIONS

2 TERMS AND CONDITIONS All House Key loans must be delivered to Lakeview Loan Servicing, LLC Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate

2 TERMS AND CONDITIONS All House Key loans must be delivered to Lakeview Loan Servicing, LLC Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate

Construction Management Contract This agreement is made by (Contractor) and (Owner) on the date written beside our signatures.

and (Owner) on the date written beside our signatures.") Construction Management Contract This agreement is made by (Contractor) and (Owner) on the date written beside our signatures. Contractor City, Zip Work Phone Number: Cell Phone Number: Fax Number: Email

Construction Management Contract This agreement is made by (Contractor) and (Owner) on the date written beside our signatures. Contractor City, Zip Work Phone Number: Cell Phone Number: Fax Number: Email

BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name:

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Utah Fee Agreement (Only required on properties located in Utah) Utah Servicing Disclosure (Only required

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Utah Fee Agreement (Only required on properties located in Utah) Utah Servicing Disclosure (Only required

SONYMA FHA Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

FHLMC Only Conforming and Maximum DTI is the more restrictive of Loan Product Advisor or 50%.

AUS (Automated Underwriting System) GENERAL POLICY OVERLAYS FHA, VA, CONVENTIONAL and USDA FHA, VA & Conventional AUS approval recommendation is required for all FHA, VA, (Purchase and Non-Streamline/Non-IRRRL

AUS (Automated Underwriting System) GENERAL POLICY OVERLAYS FHA, VA, CONVENTIONAL and USDA FHA, VA & Conventional AUS approval recommendation is required for all FHA, VA, (Purchase and Non-Streamline/Non-IRRRL

RESPA REFORM TRAINING Effective January 1, FOR MORTGAGE PROFESSIONALS ONLY Rev 1, 12/29/09

RESPA REFORM TRAINING Effective January 1, 2010 OVERVIEW In November 2008, HUD published its final rule amending Regulation X of the Real Estate Settlement Procedures Act (RESPA). The final rule includes

RESPA REFORM TRAINING Effective January 1, 2010 OVERVIEW In November 2008, HUD published its final rule amending Regulation X of the Real Estate Settlement Procedures Act (RESPA). The final rule includes

Disaster Recovery Toolkit

Disaster Recovery Toolkit Natural disasters test even the toughest people. Experiencing a disaster can be terrifying and tragic, and home recovery is often exhausting. We re here to help in any way we

Disaster Recovery Toolkit Natural disasters test even the toughest people. Experiencing a disaster can be terrifying and tragic, and home recovery is often exhausting. We re here to help in any way we

DOCUMENT CHECKLIST FOR PURCHASED LOANS Crescent Mortgage Company 6600 Peachtree Dunwoody Rd. NE, 600 Embassy Row, Suite 650 Atlanta, GA 30328

1. TITLE POLICY DOCUMENT CHECKLIST FOR PURCHASED LOANS Crescent Mortgage Company 6600 Peachtree Dunwoody Rd. NE, 600 Embassy Row, Suite 650 Atlanta, GA 30328 [ ] Short form title policies with proper ALTA

1. TITLE POLICY DOCUMENT CHECKLIST FOR PURCHASED LOANS Crescent Mortgage Company 6600 Peachtree Dunwoody Rd. NE, 600 Embassy Row, Suite 650 Atlanta, GA 30328 [ ] Short form title policies with proper ALTA

Accenture Mortgage Cadence. Loan Fulfillment Center. Forms Job Aid

Accenture Mortgage Cadence Loan Fulfillment Center f Table of Contents FORM FORMATS...8 1003 UNIFORM RESIDENTIAL LOAN APPLICATION...9 1008 UNIFORM UNDERWRITING AND TRANSMITTAL SUMMARY... 10 1008 Uniform

Accenture Mortgage Cadence Loan Fulfillment Center f Table of Contents FORM FORMATS...8 1003 UNIFORM RESIDENTIAL LOAN APPLICATION...9 1008 UNIFORM UNDERWRITING AND TRANSMITTAL SUMMARY... 10 1008 Uniform

TRID October 3, 2015!

TRID October 3, 2015! Purpose This announcement includes the following topics: Consumer Financial Protection Bureau (CFPB), Truth-in-Lending and RESPA Integrated Disclosures (TRID). Policy It is MSI Policy

TRID October 3, 2015! Purpose This announcement includes the following topics: Consumer Financial Protection Bureau (CFPB), Truth-in-Lending and RESPA Integrated Disclosures (TRID). Policy It is MSI Policy

Standard Form of Agreement Between Contractor and Subcontractor

Standard Form of Agreement Between Contractor and Subcontractor GENERAL TERMS AND CONDITIONS ARTICLE 1 THE SUBCONTRACT DOCUMENTS 1.1 The Subcontract Documents consist of (1) these General Terms and Conditions,

Standard Form of Agreement Between Contractor and Subcontractor GENERAL TERMS AND CONDITIONS ARTICLE 1 THE SUBCONTRACT DOCUMENTS 1.1 The Subcontract Documents consist of (1) these General Terms and Conditions,

AN No 4550 (1980) Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist

Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist") Applicant Information AN No 4550 (1980) Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist Loan Request: $ Loan Purpose: Purchase - Sales Price: $ Refinance

Applicant Information AN No 4550 (1980) Attachment Rural Development - Guaranteed Rural Housing Agency Documentation and Processing Checklist Loan Request: $ Loan Purpose: Purchase - Sales Price: $ Refinance

USDA Guidelines GUSDA30

USDA Guidelines GUSDA30 BSM Direct guidelines have been created to provide guidance and consistency in determining credit decisions. The guides are not all inclusive of different situations that may arise

USDA Guidelines GUSDA30 BSM Direct guidelines have been created to provide guidance and consistency in determining credit decisions. The guides are not all inclusive of different situations that may arise

Osceola County Purchase Assistance Program Guidelines

Osceola County Purchase Assistance Program Guidelines Purchase Assistance Program Objective The Osceola County Down payment Assistance Program (DPA) is made available through the State Housing Initiatives

Osceola County Purchase Assistance Program Guidelines Purchase Assistance Program Objective The Osceola County Down payment Assistance Program (DPA) is made available through the State Housing Initiatives

All Credit Reports - All Pages Including Disclosure Credit Inquries Letter and Credit LOE(s) Deposit Explanation Letter(s) Mortgage Statement(s)