RESPA REFORM TRAINING Effective January 1, FOR MORTGAGE PROFESSIONALS ONLY Rev 1, 12/29/09

|

|

|

- Johnathan Anthony

- 5 years ago

- Views:

Transcription

1 RESPA REFORM TRAINING Effective January 1, 2010

2 OVERVIEW In November 2008, HUD published its final rule amending Regulation X of the Real Estate Settlement Procedures Act (RESPA). The final rule includes significant changes to the Good Faith Estimate (GFE) and the HUD-1 Settlement Statement (HUD-1). The final RESPA rule along with the new GFE and HUD-1/1A forms, training guide, and FAQ s can be accessed on HUD s web site at ACBN requires the new GFE and HUD-1 forms be used on all applications received on or after January 1, 2010.* Any new file or file in process that needs a GFE or re-disclosure of a GFE on or after January 1, 2010 will use the new standardized GFE form. New Definition of Loan Application Under the new RESPA rule, what constitutes an application is being redefined. The term application means the submission of a borrower s financial information in anticipation of a credit decision relating to a federally related mortgage loan, which must include all of the following: 1. Borrower s name 2. Borrower s monthly income 3. Borrower s social security number 4. Property address (not TBD) 5. Estimated value of the property 6. Mortgage loan amount 7. Interest rate 8. Product type ACBN will consider a transaction to be an application when the above elements are obtained for each applicant AND there is intention to apply on the part of the borrower(s). A loan transaction must meet the definition of an application before a GFE can be issued. GFE The new standardized GFE is designed to provide the borrower with more transparency regarding key loan terms, fees, and charges so borrowers may shop among lenders for the best loan. The main goal is to give borrowers more accurate figures as to the true cost of the loan at time of application and avoid surprises at closing. All charges are disclosed on the GFE regardless of whether the charges will be paid by the borrower, seller, or other party. The loan originator (lender or mortgage broker) is required to issue the new GFE no later than 3 business days after the application or information sufficient to complete an application is received. (See above definition of a Loan Application.)

3 The initial GFE distributed by any loan originator in a transaction becomes the binding GFE. Except for interest rate dependent charges, the loan originator is bound by the GFE for at least ten (10) business days after the GFE is provided (or longer if so specified by the loan originator.) There is no requirement that the borrower sign the GFE. No GFE disclosure is required if the application is withdrawn or denied within 3 business days of application. The loan originator may not charge any fee, except for a credit report fee, until after the applicant has received the GFE and indicates an intention to proceed with the loan request. (See ACBN Certification of Receipt of GFE and Intent to Proceed form.) Fees paid outside of closing will no longer be designated as POC on the GFE. All fees typically paid by the borrower must be shown on the GFE as if paid by the borrower at closing. All charges for settlement services must be placed in the appropriate categories on the GFE. RECOMMENDATION: Do not issue an initial GFE until all of the above mentioned items are collected on the loan application. Prior to a completed loan application, use a generic fee worksheet to provide an interest rate and fee quote to the borrower. *Pre-Quals/TBD properties are still acceptable at ACC/ACBN; no GFE required.

4 Instructions on Completing the New GFE The new GFE consists of three pages: Page 1: Provides important dates regarding availability of interest rate and settlement charges Summarizes key loan information and escrow details Shows the total estimated settlement charges for the loan Page 2: Breaks down all settlement charges into two major categories: Your Adjusted Origination Charges and Your Charges for All Other Settlement Services The two major categories are broken down into eleven blocks of charges Page 3: Provides information to help borrowers understand which settlement charges can change at closing (tolerance limits) Shopping chart provided to assist the borrower when comparing GFEs from other lenders

5 - PAGE 1 -

6 Name of Originator Originator provided: originator company name AKT provider on re-disclosure: AKT American Capital, Inc. Originator Address Originator provided: originator branch address AKT provider on re-disclosure: AKT American Capital, Inc. address Originator Phone Number Originator provided: originator phone number AKT provider on re-disclosure: blank Borrower Name Applicant Name(s) Property Address Subject Property Address Date of GFE Originator provided: Date generated by originator AKT provider on re-disclosure: Date generated by system Originator Originator provided: originator AKT provider on re-disclosure: blank

7 Important dates details: 1. If loan is locked: lock expiration date If loan is floating: date and time stamp equal date GFE generated by originator s system AKT provider on re-disclosure: date and time stamp equal date GFE generated from the system 2. If loan is locked: lock expiration date If loan is floating: 10 rescission business days from originator s system AKT provider on re-disclosure: 10 rescission business days from the system 3. If loan is locked: the lock period If loan is floating: N/A 4. If loan is locked: N/A If loan is floating: 10 calendar days (Monday Sunday). AKT has option to be flexible with this timeframe. NOTE: The interest rate and other settlement charges dates are independent of each other. At lock, an updated GFE must be issued by ACBN with Important Dates sections updated.

, interest and mortgage insurance; do NOT include")

8 Summary of your loan details: Your initial loan amount is: FINAL Loan Amount that would appear on the Note Your loan term is: Term in years Your initial interest rate is: Interest rate that would be applicable on the date of Note Your initial monthly amount owned for principal, interest and any mortgage insurance is: Principal (if applicable), interest and mortgage insurance; do NOT include taxes, insurance, HOA, etc. Can your interest rate rise?: - ARM products: mark YES; the second blank must state the maximum rate to which the rate can rise over the life of the loan and the number of months until the interest rate can first change. - Fixed rate products: mark NO. Even if you make your payments on time, can your loan balance rise?: - Mark NO. ACBN does not offer loan products that include the possibility of negative amortization.

9 Even if you make your payments on time, can your monthly amount owed for principal, interest and mortgage insurance rise?: - Fixed rate products: mark NO. - ARM products: mark YES and state the period of time to the first change, the maximum amount the payment can rise with the first change, and the maximum it can raise over the life of the loan. Does your loan have a prepayment penalty?: Mark YES if there is a prepayment penalty on the new loan and state the maximum amount of the penalty. Otherwise, mark NO. Note: FHA interest charged from the date of prepayment until the next installment due date is not a prepayment penalty. Does your loan have a balloon payment?: Mark YES if there is a balloon payment and state the amount of the balloon payment and the number of years until the balloon payment is due. Otherwise, mark NO. Escrow account information details: Input the initial monthly amount owed as calculated above in "Summary of your loan": Principal (if applicable), interest and any mortgage insurance. Mark YES if there will be an escrow account; Mark NO if there will not be an escrow account.

10 Summary of your settlement charges A. Calculated on page 2 of the GFE. See below. B. Calculated on page 2 of the GFE. See below. A +B. Total of adjusted origination charges and charges for all other settlement services.

11 PAGE 2

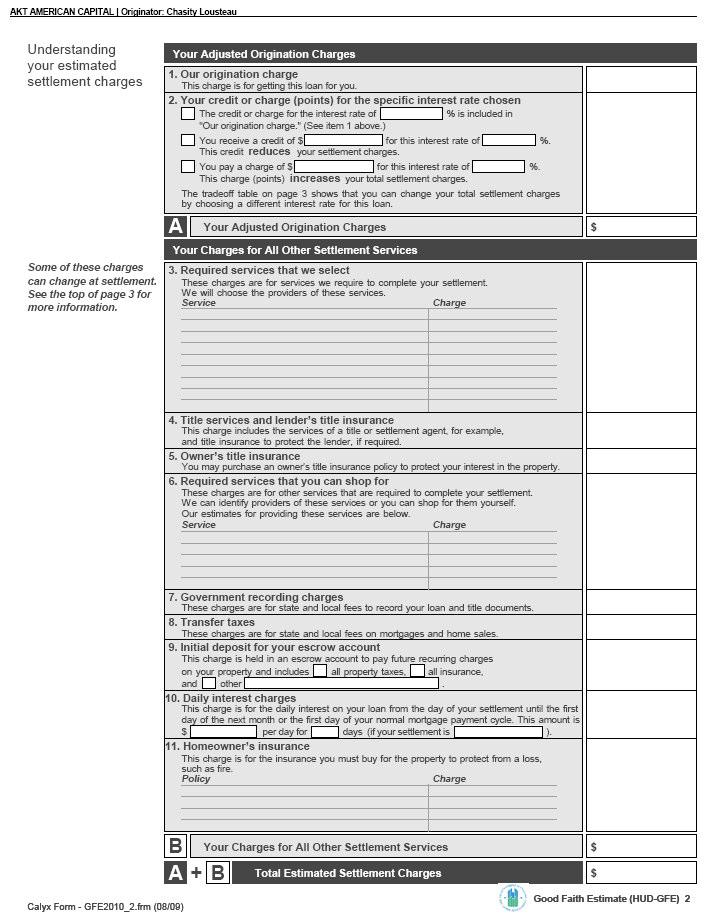

12 ZERO TOLERANCE Amounts reflected in Blocks 1 & 2 cannot change unless there is a Changed Circumstance. Understanding your estimated settlement charges details: Block 1 Origination Charge. TOTAL of all AKT lender fees and originator/broker fees for originating the loan, including but not limited to: *Initial YSP / Broker s Compensation Origination Fee Processing Fee Administrative Fee Application Fee Commitment Fee Underwriting Fee Courier Fee Wire Fee Attorney s Document Preparation Fee MERS Registration Fee Verification of Tax Return/SSN Verification of Income/Employment Extended Lock Fee Sum of all these fees appears on GFE and HUD-1 but must be itemized on separate fee worksheet (i.e. Initial Fees Worksheet in Point) and noted if fee is a prepaid finance charge as well as if fee is to be paid by the borrower, seller, or other party. *The initial YSP / Broker s Compensation cannot increase after the initial GFE even though the premium/credit on the loan may increase after the GFE is issued.

13 Block 2 Credit/Charge for Interest Rate. Any credit or charge for the interest rate chosen on the loan. Only one of the boxes may be checked per loan; a credit and a charge cannot occur together in the same transaction. Box 1 Check if no additional charges or credits apply (i.e. par pricing with no YSP) Box 2 Check if loan contains lender credits to the borrower to cover origination and/or fees OR contains a Yield Spread Premium and any additional payments made to the broker from the lender; reflect as a negative number; zero should be entered if there is no credit or YSP of any kind. Box 3 Check if there are any interest rate related charges (i.e. discount points); enter zero if no points are collected. Example 1: Consumer locked at 6.0%, par pricing $1,500 origination fee No discount points - SCENARIO EXAMPLES - Your Adjusted Origination Charges 1. Our origination charge This charge is for getting this loan for you. 2. Your credit or charge (points) for the specific interest rate chosen. X The credit or charge for the interest rate of 6 % is included in "Our origination charge." See item 1 above. $3, $ 0 You receive a credit of $2,000 for this interest rate of 6.50%. This credit reduces your settlement charges. You pay a charge of $ for this interest rate of %. This charge (points) increases your total settlement charges. A. Your Adjusted Origination Charges $1,500.00

14 Example 2: Par rate = 6% $1,500 origination fee No discount points Consumer locked at 6.5% for which the lender will pay a $2,000 yield spread premium to broker Your Adjusted Origination Charges 1. Our origination charge This charge is for getting this loan for you. 2. Your credit or charge (points) for the specific interest rate chosen. The credit or charge for the interest rate of % is included in "Our origination charge." See item 1 above. $3, $ (2,000.00) X You receive a credit of $2,000 for this interest rate of 6.50%. This credit reduces your settlement charges. You pay a charge of $ for this interest rate of %. This charge (points) increases your total settlement charges. A. Your Adjusted Origination Charges $1,500.00

15 Example 3: Par rate = 6%, $1,500 origination fee 2 discount points for rate of 5.50% Consumer locked at 6.5% that had premium pricing Your Adjusted Origination Charges 1. Our origination charge This charge is for getting this loan for you. 2. Your credit or charge (points) for the specific interest rate chosen. The credit or charge for the interest rate of % is included in "Our origination charge." See item 1 above. $1, $ 2, You receive a credit of $2,000 for this interest rate of 6.50%. This credit reduces your settlement charges. X You pay a charge of $ for this interest rate of %. This charge (points) increases your total settlement charges. A. Your Adjusted Origination Charges $3,500.00

16

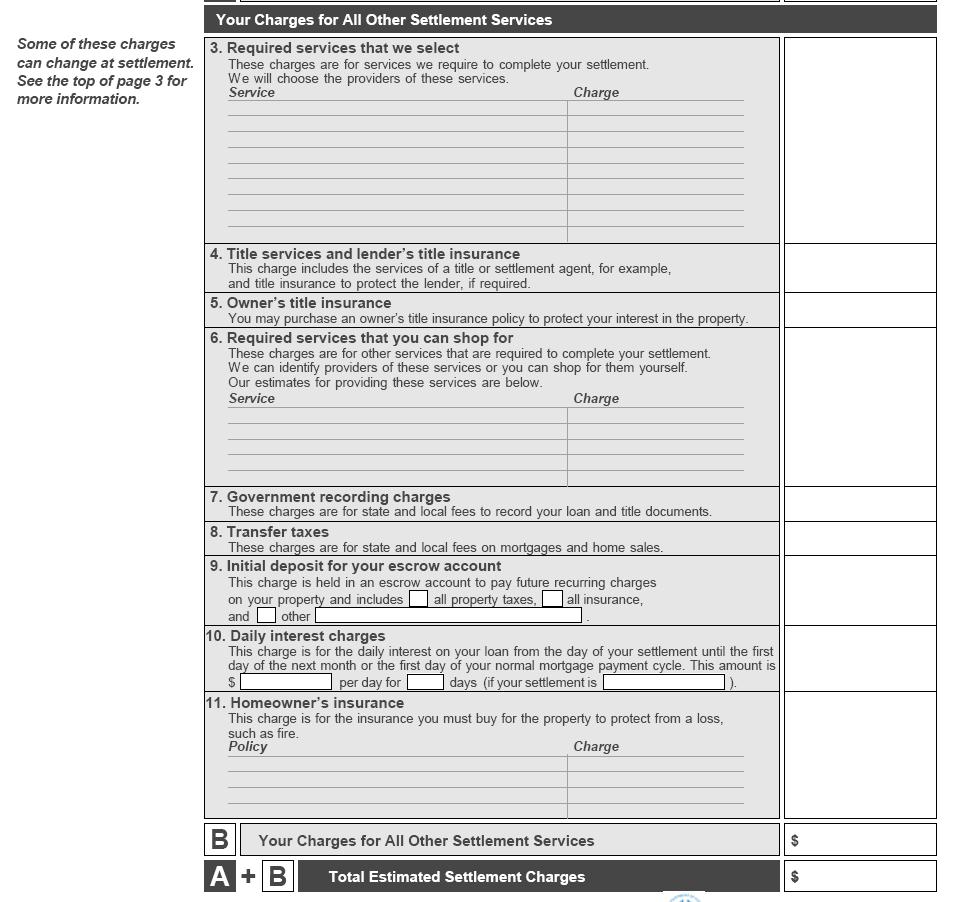

17 Your charges for all other settlement services details: Block 3 Required Services We Select. Identify each third party settlement service required as a condition of the loan and selected by the lender/originator (excluding title services) along with the estimated price to be paid to the provider of each service. The name of the actual provider is not disclosed on the GFE. EXAMPLES: credit reports, appraisals, AVMs, flood certificate, tax service, government loan charges (VA Funding Fee, FHA, USDA Rural Housing Guarantee Fee, and bond programs), any upfront mortgage insurance premium (FHA MIP, Conventional PMI), HOA certification, any fee charged by provider for evidence of insurance from a hazard/flood insurer, pest inspection, well/septic inspection. NOTE: Appraisal, Tax Service, and Flood Cert fees may be listed in this block. (When these services are listed in Block 3, they do not appear on the Settlement Services Providers List.) Block 3 subject to10% aggregate tolerance (along with other services below where provider was chosen from the list.) Block 4 Title Services and Lender s Title Insurance. State the estimated TOTAL charge for third party settlement service providers for all closing services, regardless of whether the providers are selected or paid for by the borrower, seller or lender/mortgage broker. Also include any lender's title insurance premiums, when required, regardless of whether the provider is selected or paid for by the borrower, seller or lender/mortgage broker. EXAMPLE FEES (ANY SERVICE INVOLVED IN THE PROVISION OF TITLE INSURANCE): title search, title examination, endorsements and evaluation, preparation and issuance of commitment, clearance of underwriting objections, preparation and issuance of policies, all processing and administrative services, conducting settlement, delivery fees, notary fees, lender title insurance premium, survey. REFINANCES: A title/settlement service provider must be disclosed on the Required Services Providers List. PURCHASES: The sales contract identifies the title/settlement services provider. Block 4 subject to 10% aggregate tolerance if listed service provider is chosen. Not subject to tolerance if listed service provider is not chosen. Must list at least one service provider on Settlement Services Providers List, if borrower is allowed to shop.

18 Block 5 Owner s Title Insurance. For all purchase transactions, provide an estimate of the likely charge for the owner's title insurance and related endorsements, regardless of whether the providers are selected for or paid by the borrower, seller or lender/mortgage broker. REFINANCES: You may enter N/A in this block. Block 5 subject to 10% aggregate tolerance if listed service provider is chosen. Not subject to tolerance if listed service provider is not chosen. Must list at least one service provider on Settlement Services Providers List, if borrower is allowed to shop. Block 6 Required Services You Can Shop For. Identify each third party settlement service required for the loan transaction where the borrower is permitted to shop for and select the settlement service provider (excluding title services) along with the estimate charge to be paid to the provider of each service. Block 6 subject to 10% aggregate tolerance if listed service provider is chosen. Not subject to tolerance if listed service provider is not chosen. Must list at least one service provider on Settlement Services Providers List. Block 7 Government Recording Charges. Estimate the state and local government fees for recording. CHARGES INCLUDE BUT ARE NOT LIMITED TO: state and local fees for recording the deed, mortgage, deed of trust, releases, and any other instrument or document recorded to preserve marketable title or to perfect AKT s security interest in the property. Block 7 subject to 10% aggregate tolerance. Block 8 Transfer Taxes. Enter the buyer s portion all state and local government fees on mortgages and home sales based upon the proposed loan amount or sales price and on the property address. (City/County Tax/Stamps, State Tax/Stamps). Block 8 subject to zero tolerance.

19 Block 9 Initial Deposit for Escrow Account. Estimate the amount that will be required to place into a reserve or escrow account to be applied to recurring charges for property taxes, homeowner's and other similar insurance, mortgage insurance and other periodic charges. Check the appropriate box and show the total in the right column. If the reserve or escrow account includes mortgage insurance, check "other" and then list the items included. If escrow is being waived, zero will be in this block. Block 9 has no tolerance limitation. NOTE: If escrows are being waived, the loan level price adjustment to waive escrows is included in Block 2. Block 10 - Daily Interest Charges. Estimate the total amount that will be due at settlement for the daily interest on the loan from the date of settlement until the first day of the first period covered by scheduled mortgage payments. Originator must also indicate how this total is calculated by providing the amount of the interest charges per day and the number of days used in the calculation, based on the stated projection closing date. Block 10 has no tolerance limitation. Block 11 - Homeowner's Insurance. Estimate the total amount of the premiums for any hazard, flood and earthquake insurance policy that must be purchased. Separately indicate the nature of each type of insurance required along with the charges. Enter the total for all premiums in the right column. To the extent a lender/mortgage broker requires that such insurance be part of an escrow account, the amount of the initial escrow deposit must be included in block 9. Block 11 has no tolerance limitation.

20 - PAGE 3 -

21 Using the tradeoff table details: This section is designed to make borrowers aware of the relationship between their total estimated settlement charges, interest rate and resulting monthly payment. Complete the left hand column using the loan amount, interest rate, monthly payment figure, and the total estimated settlement charges from page 1 of the GFE. The originator may provide the borrower with the same information for two alternative loans, one with a higher interest rate and one with a lower interest rate. The alternative loans must use the same amount and be otherwise identical to the loan in the GFE. Using the shopping cart table is a shopping tool for the borrower to complete, in order to compare GFEs from different lenders. The first column will be completed with the subject loan information.

22 CHANGED CIRCUMSTANCES REDISCLOSURE OF GFE Except for any permitted tolerances, loan originators must be accurate when disclosing initial settlement charges to the borrower on the GFE. Without a valid changed circumstance that is documented, the originator and lender are bound by the amounts shown on the last disclosed GFE subject to any permitted tolerances. Only charges or terms directly related to the changed circumstance may be changed. The revised GFE must be issued within 3 business days of receiving information sufficient to establish the changed circumstance. The 3 business day requirement is triggered from the time of receipt by either the originator or the lender, whoever receives the information first. Documentation evidencing the changed circumstance must be kept in the loan file. The term "changed circumstances" means: Acts of God, war, disaster, or other emergency; Information particular to the borrower or transaction that was relied on in providing the GFE that changes or is found to be inaccurate after the GFE has been provided. This may include information about the credit quality of the borrower, new loan amount, program change requested by the borrower, the estimated value of the property, loan locked after submission, occupancy change, or any other information that was used in providing the GFE; New information particular to the borrower or transaction that was not relied on in providing the GFE; or Other circumstances that are particular to the borrower or transaction, including underwriting conditions, boundary disputes, the need for flood insurance, environmental problems, or additional conditions required from Title Binder. EXAMPLES: - If pricing changes due to a changed circumstance, or a borrower requested change, only the interest rate dependant charges and terms may change. This includes only those charges and credits in Block 2 which will, in turn, impact the Adjusted Origination Charges. - If pricing changed due to going from a float to a lock or due to a lock expiration, only the interest rate dependant charges and terms may change (Block 2 and the impacted Adjusted Origination Charges. )

23 "Changed circumstances" do not include: The borrower's name, the borrower's monthly income, the property address, any information contained in any credit report obtained by the loan originator prior to providing the GFE, unless the information changes or is found to be inaccurate after the GFE has been provided, etc.; or Market price fluctuations by themselves. EXAMPLES: - Block 1 fees CANNOT change, even with a changed circumstance; EXCEPTION: if the loan amount changes and a portion of the Origination Charge is a percentage of the loan amount or the overall loan program changes. ACTION REQUIRED: Upon the borrower s request for a change or loan originator s knowledge of a changed circumstance, notify ACBN within 24 hours by ing redisclosure@acbnonline.com with the detail of the changed circumstance and request to re-issue a revised GFE. (See Request for Changed Circumstance form). A revised GFE may only be issued to a borrower by ACBN within 3 business days of the change and prior to closing where there exists "changed circumstances". APPRAISAL REVIEWS: Appraisal reviews are not always due to a changed circumstance and may need to be accounted for at time of initial GFE disclosure. See ACBN Appraisal Review Policy and ACBN fee sheet posted on the ACBN web site.

24 TOLERANCE LIMITATIONS HUD has created limitations which restrict the amount that settlement charges to borrowers can change between the GFE and the actual fees charged at settlement. These tolerance limitations are designed to help borrowers receive a more accurate GFE and to enable the borrower to easily compare the fees noted on the GFE with those on the HUD-1. The tolerance limitations are divided into three categories: 1. Settlement charges that cannot increase: origination charges (including broker fees), borrower's credit or charge for specific interest rate chosen (after locking in the rate), and transfer taxes. (0% Tolerance) 2. Settlement charges that can increase up to 10%: required services selected by the originator, title services and lender's title insurance (if selected by loan originator or borrower uses companies identified by loan originator), owner's title insurance (if borrower uses companies identified by loan originator), required services that the borrower shops for (if borrower uses companies identified by the loan originator), and government recording charges. (Up to 10% Aggregate Tolerance) 3. Settlement charges that can increase without restriction: required services that borrower shops for, title services and lender's title insurance, and owner's title insurance (where the borrower does not use companies identified by the loan originator); initial deposit for escrow deposit, daily interest charges, and homeowner's insurance. (No Tolerance Limitation) These tolerances are clearly described to the borrower on the third page of the GFE and carry over to page 3 of the HUD-1.

25 Additional Disclosures The new RESPA rules require loan originators to provide the borrower with a list of Settlement Service Providers. The Itemization of Fees and the Lender/Seller Paid Fees & Credits are not required by the new RESPA rule but are necessary additions based on the changes to the GFE and HUD-1. It is the loan originator s responsibility to communicate to the settlement agent all the information needed to complete the HUD-1. Settlement Service Provider List: For blocks 4, 5 & 6 of the new GFE, the loan originator must identify each third party settlement service required by the loan originator where the borrower is permitted to shop for and select the settlement service provider. Only one settlement service provider is required to be listed per service. If no service providers are listed, then it is assumed the borrower could not shop and fees will be bound by the tolerances. The borrower is not required to select a vendor from the list provided. Where a borrower is permitted to shop for third party settlement services, the loan originator must provide the borrower with a written list of settlement service providers on a separate sheet of paper at the time the GFE is issued. The list must include those services addressed in Blocks 4, 5 and 6 of the GFE. The list must contain settlement service providers that are likely available to provide the settlement service in the borrower's local area. The list must include the name, address, and phone number for each provider and with the estimated charge to be paid. Additional disclosure may be added to the list stating that the originator is not endorsing the service providers. Lenders may list their affiliate as the only service provider, but must distribute the Affiliated Business Arrangement disclosure. No standard format is required. (Point users: see Settlement Service Provider List with the 2010 GFE in Point as a sample format to use.) The content of the Settlement Service Provider List will vary depending upon which services the borrower is permitted to shop for. If the borrower selects a provider identified on the list, the amount paid for that service would fall within the 10% tolerance for that category. If the borrower chooses a different provider, the amount paid for that service is not subject to any tolerance restriction.

26 Itemization of Fees: Certain fees must be consolidated into a single block on the new GFE form and a single line on the new HUD-1. EXAMPLE: The total of all charges assessed by loan originators on the transaction (including lenders and brokers), except any charge for the specific interest rate chosen, must be shown in Block 1, "our origination charge", on the GFE and in line 801 on the HUD-1. ACTION REQUIRED: Since the individual fee detail will no longer be shown on the GFE and HUD-1, ACBN will require originators to provide that detail on a separate form. This form is necessary in order to correctly re-calculate the APR and test compliance with Federal and state high cost restrictions. (See initial Fees Worksheet in Point, formerly known as the GFE.) Although use of this specific form is optional, loans will be suspended if an itemization of the individual fees comprising the totals shown on the GFE and HUD-1 is not provided. NOTE: an Itemization of Amount Financed will not satisfy this requirement entirely as that form only provides the detail on finance charges. ACBN fees are posted at => Member Info Tab (or, on the ACC Village). Lender/Seller Paid Fees/Credits: All charges typically paid by the borrower must be disclosed on the GFE regardless of whether the charges will be paid for by the borrower, the seller, or other party. Fees disclosed, but paid by others are still bound by tolerances. EXAMPLE: In order to promote comparability between the charges on the GFE and the charges on the HUD-1, if a loan originator pays for a charge that is included on the GFE, the charge should be listed in the borrower's column on Page 2 of the HUD-1. That charge must also be offset by listing a credit in that amount to the borrower on lines on Page 1 of the HUD-1. Similar to the lender/broker paid fees, fees and charges typically paid by the borrower that are to be paid by the seller must also be disclosed on the GFE. EXAMPLE: If a seller pays for a charge that was included on the GFE, the charge must be listed in the borrower's column on Page 2 of the HUD-1. That charge should also be offset by listing a credit in that amount to the borrower on lines on Page 1 of the HUD-1, and by a charge to the seller in lines on Page 1 of the HUD-1.

27 Depending upon the number of fees paid by the lender / broker and fees paid by the seller on each transaction, there may not be enough lines available in the 200 or 500 series on the HUD-1 to detail each fee. In those cases, ACBN will require that detail be provided on an addendum to the HUD-1. For brokers, on a transaction in which the borrower requests a Lender Credit to be applied to closing costs in exchange for a higher interest rate, the premium pricing credit must be reflected as a negative number in Block 2 on the GFE and on line 802 on the HUD-1. ACBN will require clients to include the allocation of the premium pricing credit on an addendum to the HUD-1. This detail is necessary in order to correctly re-calculate the APR and test compliance with Federal and state high cost restrictions. New HUD Settlement Cost Booklet Shopping for Your Home Loan : Required to be provided along with the GFE either by mail or on ALL purchase and refinance loans. New Construction GFE Disclosure: On New Construction purchase transactions, if settlement is expected to occur more than 60 calendar days from the time a GFE is provided, the Good Faith Estimate Construction Loan Disclosure must be provided along with the GFE in order to issue a revised GFE without a Changed Circumstance. If this disclosure is not provided at the time of the initial GFE, a revised GFE can only be issued if there is a valid and documented Changed Circumstance.

28 Fee Tolerances / Curative Process Settlement fees and charges disclosed on the GFE must remain within the RESPA tolerances both initially and throughout the process. (It is permissible for charges to the borrower to decrease.) Unless there is a valid, documented Changed Circumstance, ACBN is not allowed to exceed certain fee tolerances listed on the GFE as compared to the HUD-1. The ACBN closer must compare the fees reflected on the GFE to the preliminary HUD-1 prepared by the settlement agent prior to closing to determine if there are any differences. If there are differences that are in violation of the fee tolerances, the violations must be cured and the HUD-1 must be corrected prior to loan closing. In the event an error is not detected prior to closing/disbursement, Post Closing Review will complete the process to cure the error within 30 days of settlement.

29 Tips for Point Users In order to complete the new standardized GFE correctly, follow these steps: 1. Input all fees on the Initial Fees Worksheet (formerly the GFE) in Point; mark all PFCs and which party pays the fee. NOTE: if brokering and getting a YSP, input the YSP in compensation paid to broker field as normal AND add this amount to the origination field along with any other origination fee being charged to the borrower. 2. Complete the Truth In Lending (TIL) 3. Go to the NEW GFE 2010 and complete all remaining boxes that did not auto-populate from the Initial Fees Worksheet and TIL. NOTE: With every change to fee, PFC, or party to pay for the fee, on the new GFE you must press the CALCULATE tab at the bottom of the screen. IDEA: In field #9, you may want to consider adding Supplemental taxes not included on purchases. 4. Complete the Service Providers List, including amount, provider name, address, and phone number. NOTE: In order for the list of providers to print on the form correctly, check both the req d box brw box because the fee is required and the borrower can shop for the service, then print.

30 What ACBN Needs from You at Submission - A fully completed loan application - An acceptable GFE disclosure (dated within 3 business days of the originator application date) - TIL Disclosure (dated within 3 business days of the originator application date) - Mortgage Loan Disclosure Statement - ACBN Fee Acknowledgment Form (see TILA guidelines) - Settlement Services Providers List (dated within 3 business days of the originator application date) - Certification of Receipt of GFE and Intent to Proceed form - Initial Fees Worksheet - All remaining federal, state, and program specific borrower authorizations and disclosures - AUS findings - Income and asset documentation - Contract, if applicable - See ACBN s stacking order for a full list of possible items required on a file at time of submission Prior to accepting a loan package, ACBN must audit the GFE, GFE Acknowledgement, Settlement Services Providers List, and Fee Worksheet for acceptability. Any loan that is not acceptable cannot be cured, will be returned to the originator, and may not be re-submitted. Pre-Quals/TBD properties are acceptable at ACC/ACBN, no GFE required. Additional information and ACBN required forms will be posted on ACBN s web site by January 1, 2010 under Member Info and/or Forms tabs (or posted on the Village for ACC Retail Originators.)

Good Faith Estimate Training 2/3/14

Good Faith Estimate Training 2/3/14 Objectives At the end of this training you will be able to: Understand RESPA Reform Recognize a complete Loan Application Understand GFE requirements Know requirements

Good Faith Estimate Training 2/3/14 Objectives At the end of this training you will be able to: Understand RESPA Reform Recognize a complete Loan Application Understand GFE requirements Know requirements

Guidance for Completing the 2010 Good Faith Estimate

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) General 1) Q: When does the new RESPA Rule take effect? A: The November 2008 RESPA Rule was effective January 16, 2009. Implementation of the provisions are

New RESPA Rule FAQs (New items are in bold) General 1) Q: When does the new RESPA Rule take effect? A: The November 2008 RESPA Rule was effective January 16, 2009. Implementation of the provisions are

Guidance for Completing the 2010 Good Faith Estimate

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

A GFE must be issued when the originator receives an application OR six minimum pieces of information sufficient to complete an application including:

PROVIDENT BANK MORTGAGE RESPA REFORM Effective January 1, 2010 RESPA OVERVIEW The goal of RESPA Reform is to provide consumers with the information needed to readily understand loan terms and total settlement

PROVIDENT BANK MORTGAGE RESPA REFORM Effective January 1, 2010 RESPA OVERVIEW The goal of RESPA Reform is to provide consumers with the information needed to readily understand loan terms and total settlement

WHOLESALE Good Faith Estimate Compliance Manual

WHOLESALE Good Faith Estimate Compliance Manual Understanding the 2010 GFE Compliance Department 2/2/2015 2015 Pacific One Lending. http://www.nmlsconsumeraccess.org. Rates, fees and programs are subjected

WHOLESALE Good Faith Estimate Compliance Manual Understanding the 2010 GFE Compliance Department 2/2/2015 2015 Pacific One Lending. http://www.nmlsconsumeraccess.org. Rates, fees and programs are subjected

How the New RESPA Rule. Impacts Wholesale Lending. By Richard Andreano, Jr.

How the New RESPA Rule Impacts Wholesale Lending By Richard Andreano, Jr. 1 Overview of Presentation Focus on certain aspects of revised RESPA regulation, Regulation X, that are scheduled to become effective

How the New RESPA Rule Impacts Wholesale Lending By Richard Andreano, Jr. 1 Overview of Presentation Focus on certain aspects of revised RESPA regulation, Regulation X, that are scheduled to become effective

HUD s New RESPA Rule

1300 Nineteenth Street, NW Fifth Floor Washington, DC 20036 202.628.2000 www.wbsk.com HUD s New RESPA Rule November 24, 2008 On November 17, 2008 the United States Department of Housing and Urban Development

1300 Nineteenth Street, NW Fifth Floor Washington, DC 20036 202.628.2000 www.wbsk.com HUD s New RESPA Rule November 24, 2008 On November 17, 2008 the United States Department of Housing and Urban Development

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 9 GFE Interest rate expiration... 9 GFE Expiration... 10 GFE Denial... 10 GFE

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 9 GFE Interest rate expiration... 9 GFE Expiration... 10 GFE Denial... 10 GFE

New RESPA Regulations for Mortgage Finance: Are You Ready? Complying With the Sweeping Changes in Real Estate Settlement Procedures

presents New RESPA Regulations for Mortgage Finance: Are You Ready? Complying With the Sweeping Changes in Real Estate Settlement Procedures A Live 90-Minute Teleconference/Webinar with Interactive Q&A

presents New RESPA Regulations for Mortgage Finance: Are You Ready? Complying With the Sweeping Changes in Real Estate Settlement Procedures A Live 90-Minute Teleconference/Webinar with Interactive Q&A

Good Faith Estimate (GFE)

") OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator Address Borrower Property Address Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan

OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator Address Borrower Property Address Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

Integrated Disclosure Vocabulary List. Term Definition as of 8/1/2015 Adjustments and Other Credits

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

RESP RE A SP A & & Good Good Fa F ith ith Estima tima e R quir quir d e d Disclosure Disclosur s Corresponden Corr esponden t Lending July 22, 2013

RESPA & Good Faith Estimate Required Disclosures Correspondent Lending July 22, 2013 What s Different and When is it Effective? January 1, 2010 (1003 dated on or after) New GFE form: does not indicate

RESPA & Good Faith Estimate Required Disclosures Correspondent Lending July 22, 2013 What s Different and When is it Effective? January 1, 2010 (1003 dated on or after) New GFE form: does not indicate

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law MEMORANDUM. RESPA 101 The New Good Faith Estimate (GFE) Rules

Rules") BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law J. Alton Alsup 10333 Richmond, Suite 860 Telephone 713/468-0400 Board Certified in Residential Real Estate Law Texas Board of Legal Specialization

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law J. Alton Alsup 10333 Richmond, Suite 860 Telephone 713/468-0400 Board Certified in Residential Real Estate Law Texas Board of Legal Specialization

TILA RESPA Integrated Disclosure

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

RESPA Rules and the GFE

REVISED 05/01/2012 PAGE 1 OF 5 RESPA Rules and the GFE Effective Date Per the Real Estate Settlement Procedures Act (RESPA), rules in this policy are effective for all mortgage loans originated on or after

REVISED 05/01/2012 PAGE 1 OF 5 RESPA Rules and the GFE Effective Date Per the Real Estate Settlement Procedures Act (RESPA), rules in this policy are effective for all mortgage loans originated on or after

TRID. Quick Compliance Guide T I L A-RESPA INTEGRAT E D DISCLOSURES Temenos USA. All rights reserved

TRID T I L A-RESPA INTEGRAT E D DISCLOSURES Quick Compliance Guide 09.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636 e: usainfo@temenos.com While the publisher and

TRID T I L A-RESPA INTEGRAT E D DISCLOSURES Quick Compliance Guide 09.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636 e: usainfo@temenos.com While the publisher and

Reasons for Change. Are You Ready for the Regulation Z & RESPA Changes. Past, Present & Future Changes

Are You Ready for the Regulation Z & RESPA Changes Community Bankers Association of Illinois Annual Convention September 26, 2009 Presented by: Young & Associates, Inc. 1 Past, Present & Future Changes

Are You Ready for the Regulation Z & RESPA Changes Community Bankers Association of Illinois Annual Convention September 26, 2009 Presented by: Young & Associates, Inc. 1 Past, Present & Future Changes

GFE/TIL AND COC WORKFLOW

Table of Contents Page 1 of the GFE... 2 Tolerance Levels... 5 Page 2 of the GFE... 7 Box 6 of the GFE... 12 How to Calculate Transfer Tax... 13 Page 3 of the GFE... 14 Events Triggering Re-disclosure...

Table of Contents Page 1 of the GFE... 2 Tolerance Levels... 5 Page 2 of the GFE... 7 Box 6 of the GFE... 12 How to Calculate Transfer Tax... 13 Page 3 of the GFE... 14 Events Triggering Re-disclosure...

Loan Estimates. with the following requirements: Estimate SMF SMF SMF

Loan Estimates with the following requirements: Estimate SMF SMF SMF Please follow the directions below when completing the Initial Loan Application and Disclosure processes. e e cc e and Locked LE, including

Loan Estimates with the following requirements: Estimate SMF SMF SMF Please follow the directions below when completing the Initial Loan Application and Disclosure processes. e e cc e and Locked LE, including

Closing Disclosure Form

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Display the questions that impact the date through which the interest rate is available with a left click on the control.

New Standardized Good Faith Estimate On November 17, 2008, the Department of Housing and Urban Development published its final rule regarding RESPA Reform. The final rule requires mortgage lenders and

New Standardized Good Faith Estimate On November 17, 2008, the Department of Housing and Urban Development published its final rule regarding RESPA Reform. The final rule requires mortgage lenders and

Getting It Right: RESPA GFE & HUD-1/1A Workshop

Getting It Right: RESPA GFE & HUD-1/1A Workshop December 15, 2009 Dial In No.: 1-916-233-3087 Access Code: 150-051-881 # TOTAL Compliance Webinar Series Notice The statements and opinions provided by the

Getting It Right: RESPA GFE & HUD-1/1A Workshop December 15, 2009 Dial In No.: 1-916-233-3087 Access Code: 150-051-881 # TOTAL Compliance Webinar Series Notice The statements and opinions provided by the

RESPA: Regulation & Integration Process Guide

- 1 - Reverse Mortgage Wholesale & Correspondent Lending RESPA: Regulation & Integration Process Guide The Real Estate Settlement and Procedures Act (RESPA) is a consumer protection statute designed to

- 1 - Reverse Mortgage Wholesale & Correspondent Lending RESPA: Regulation & Integration Process Guide The Real Estate Settlement and Procedures Act (RESPA) is a consumer protection statute designed to

SAMPLE REAL ESTATE SETTLEMENT PROCEDURES ACT. Mortgage Lending Compliance Effective January 1, (c)2011 Bankers Advisory, Inc.

2011 Bankers Advisory, Inc.") REAL ESTATE SETTLEMENT PROCEDURES ACT Mortgage Lending Compliance Effective January 1, 2010 GFE Flowchart Borrower meets with Originator Borrower s name, SSN, loan amount, estimated property value, monthly

REAL ESTATE SETTLEMENT PROCEDURES ACT Mortgage Lending Compliance Effective January 1, 2010 GFE Flowchart Borrower meets with Originator Borrower s name, SSN, loan amount, estimated property value, monthly

* PFC = Prepaid Finance Charge Total Loan Amount $ 175,000 Interest Rate: % Term/Due In: 360 / 360 mths

GOOD FAITH ESTIMATE Applicants: John / Jane Application No: borrowerj Property Addr: 1234 TBD Street, Price, UT 84501 Date Prepared: 09/25/2009 Prepared By: Republic Mortgage Home Loans, LLC Ph. 801-426-5500

GOOD FAITH ESTIMATE Applicants: John / Jane Application No: borrowerj Property Addr: 1234 TBD Street, Price, UT 84501 Date Prepared: 09/25/2009 Prepared By: Republic Mortgage Home Loans, LLC Ph. 801-426-5500

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

2010 HUD-1: New RESPA Rule Overview

CB Title Agency of NY, LLC CB Title Group, LLC 140 Mountain Avenue Suite 101 Springfield, NJ 07081 P: 973-921-0990 F: 973-921-0902 www.cbtitlegroup.com Date: November 13, 2009 To: All Clients and Friends

CB Title Agency of NY, LLC CB Title Group, LLC 140 Mountain Avenue Suite 101 Springfield, NJ 07081 P: 973-921-0990 F: 973-921-0902 www.cbtitlegroup.com Date: November 13, 2009 To: All Clients and Friends

Loan Comparison Report. Sample

Loan Comparison Report Prepared for: Jonny Williams Date: Prepared by: April 14, 2008 Taylor Abegg Phone: 801-225-4120 E-mail: TJAbegg@EverySingleHome.com Dear Jonny Williams Attached is the Loan Comparison

Loan Comparison Report Prepared for: Jonny Williams Date: Prepared by: April 14, 2008 Taylor Abegg Phone: 801-225-4120 E-mail: TJAbegg@EverySingleHome.com Dear Jonny Williams Attached is the Loan Comparison

Final RESPA Rule Requirements

Final RESPA Rule Requirements 1 Final RESPA Rule Requirements The Department of Housing and Urban Development (HUD) released its final rule on the Real Estate Settlement Procedures Act (RESPA) on November

Final RESPA Rule Requirements 1 Final RESPA Rule Requirements The Department of Housing and Urban Development (HUD) released its final rule on the Real Estate Settlement Procedures Act (RESPA) on November

CFPB Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

TRID Quick Reference Guide

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

The TILA-RESPA Integrated Disclosures Rule consolidates. Estimate (GFE) into the Loan Estimate and. the Closing Disclosure

into the Loan Estimate and. the Closing Disclosure") Agenda This training consists of three parts explaining the general requirements of the law that consolidated multiple disclosures into two separate forms; the Loan Estimate and the Closing Disclosure:

Agenda This training consists of three parts explaining the general requirements of the law that consolidated multiple disclosures into two separate forms; the Loan Estimate and the Closing Disclosure:

FREQUENTLY ASKED QUESTIONS (FAQ) FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID)

FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID)") Best Practices FREQUENTLY ASKED QUESTIONS (FAQ) FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID) SUMMARY With the upcoming implementation of the Truth in Lending (TILA)/Real Estate Settlement

Best Practices FREQUENTLY ASKED QUESTIONS (FAQ) FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID) SUMMARY With the upcoming implementation of the Truth in Lending (TILA)/Real Estate Settlement

Good Faith Estimate (GFE)

") OMB pproval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator ddress Borrower Property ddress Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan Important

OMB pproval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator ddress Borrower Property ddress Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan Important

Interagency Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

RESPA/TILA Integration

RESPA/TILA Integration 1 Presented by: Richard Hogan, Vice President & Associate General Counsel Tracy Pandolfo, Director Agent Services Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

RESPA/TILA Integration 1 Presented by: Richard Hogan, Vice President & Associate General Counsel Tracy Pandolfo, Director Agent Services Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

Loan Estimate $ NO. Loan Terms. Loan Amount $ NO. Interest Rate 1.75% NO

Pennsylvania Housing Finance Agency 211 N. Front Street Harrisburg, PA 17101 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate DATE ISSUED APPLICANTS PROPERTY PROP. VALUE LOAN

Pennsylvania Housing Finance Agency 211 N. Front Street Harrisburg, PA 17101 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate DATE ISSUED APPLICANTS PROPERTY PROP. VALUE LOAN

TRID (TILA-RESPA ITNEGRATED DISCLOSURE RULE) FAQ

FAQ") TRID (TILA-RESPA ITNEGRATED DISCLOSURE RULE) FAQ This frequently asked questions in this document have been categorized into the following three sections: Loan Estimate Closing Disclosure Miscellaneous

TRID (TILA-RESPA ITNEGRATED DISCLOSURE RULE) FAQ This frequently asked questions in this document have been categorized into the following three sections: Loan Estimate Closing Disclosure Miscellaneous

REAL ESTATE SETTLEMENT PROCEDURES ACT SAMPLE

REAL ESTATE SETTLEMENT PROCEDURES ACT Important Disclaimer The information contained in this presentation is for informational purposes only and is not legal advice. Bankers Advisory, Inc. is not a law

REAL ESTATE SETTLEMENT PROCEDURES ACT Important Disclaimer The information contained in this presentation is for informational purposes only and is not legal advice. Bankers Advisory, Inc. is not a law

Closing Information Transaction Information Loan Information. VA Property Loan ID # Lender MIC # Sale Price $

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

TILA-RESPA Integrated Disclosures (TRID) FAQs

FAQs") TILA-RESPA Integrated Disclosures (TRID) FAQs On July 21, 2015, the Consumer Financial Protection Bureau (CFPB) published the final rule to delay the effective date of the TILA-RESPA Integrated Disclosure

TILA-RESPA Integrated Disclosures (TRID) FAQs On July 21, 2015, the Consumer Financial Protection Bureau (CFPB) published the final rule to delay the effective date of the TILA-RESPA Integrated Disclosure

Closing Information Transaction Information Loan Information. VA Property Lender Loan ID # MIC #

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

DOCUMENT CHECKLIST FOR PURCHASED LOANS Crescent Mortgage Company 6600 Peachtree Dunwoody Rd. NE, 600 Embassy Row, Suite 650 Atlanta, GA 30328

1. TITLE POLICY DOCUMENT CHECKLIST FOR PURCHASED LOANS Crescent Mortgage Company 6600 Peachtree Dunwoody Rd. NE, 600 Embassy Row, Suite 650 Atlanta, GA 30328 [ ] Short form title policies with proper ALTA

1. TITLE POLICY DOCUMENT CHECKLIST FOR PURCHASED LOANS Crescent Mortgage Company 6600 Peachtree Dunwoody Rd. NE, 600 Embassy Row, Suite 650 Atlanta, GA 30328 [ ] Short form title policies with proper ALTA

A. Settlement Statement (HUD-1)

") OMB Approval. 2502-0265 A. Settlement Statement () B. Type of Loan 1. FHA 2. RHS 3. Conv. Unins. 6. File Number: 7. Loan Number: 8. Mortgage Insurance Case Number: 4. VA 5. Conv. Ins. C. te: This form

OMB Approval. 2502-0265 A. Settlement Statement () B. Type of Loan 1. FHA 2. RHS 3. Conv. Unins. 6. File Number: 7. Loan Number: 8. Mortgage Insurance Case Number: 4. VA 5. Conv. Ins. C. te: This form

February 2016 FEBRUARY Sunday Monday Tuesday Wednesday Thursday Friday Saturday. CD is placed in the mail IF DELIVERED BY OVERNIGHT MAIL...

DELIVERY METHODS & TIMING CHEAT SHEET IF DELIVERED BY MAIL... Closing Disclosure (CD) is sent to borrower in the mail 3 day mailing rule applies for the receipt of the disclosure Then 3 day waiting period

DELIVERY METHODS & TIMING CHEAT SHEET IF DELIVERED BY MAIL... Closing Disclosure (CD) is sent to borrower in the mail 3 day mailing rule applies for the receipt of the disclosure Then 3 day waiting period

TRID October 3, 2015!

TRID October 3, 2015! Purpose This announcement includes the following topics: Consumer Financial Protection Bureau (CFPB), Truth-in-Lending and RESPA Integrated Disclosures (TRID). Policy It is MSI Policy

TRID October 3, 2015! Purpose This announcement includes the following topics: Consumer Financial Protection Bureau (CFPB), Truth-in-Lending and RESPA Integrated Disclosures (TRID). Policy It is MSI Policy

The TILA-RESPA Integrated Disclosure (TRID) Rule. Compiled by: 110 Title, LLC

Rule. Compiled by: 110 Title, LLC") The TILA-RESPA Integrated Disclosure (TRID) Rule Compiled by: 110 Title, LLC 1 I. Introductory Note The Dodd-Frank Wall Street Reform Act and Consumer Protection Act of 2010 (Dodd-Frank), ushered in the

The TILA-RESPA Integrated Disclosure (TRID) Rule Compiled by: 110 Title, LLC 1 I. Introductory Note The Dodd-Frank Wall Street Reform Act and Consumer Protection Act of 2010 (Dodd-Frank), ushered in the

Shopping for your Home Loan

Shopping for your Home Loan CFPB's Settlement Cost Booklet ITEM 1583 (01/2012) Greatland Corporation To Order Call 800.968.1099 www.greatland.com Rev. Jan. 2012 L.F. Garlinghouse Co., Inc. Consumer Financial

Shopping for your Home Loan CFPB's Settlement Cost Booklet ITEM 1583 (01/2012) Greatland Corporation To Order Call 800.968.1099 www.greatland.com Rev. Jan. 2012 L.F. Garlinghouse Co., Inc. Consumer Financial

MYSTERIES OF THE NEW HUD-1 UNCOVERED

MYSTERIES OF THE NEW HUD-1 UNCOVERED August 18, 2009 Jim Gosdin, Deborah Yahner and Jennifer Dumas jgosdin@stewart.com dyahner@stewart.com jdumas@stewart.com 2008 Stewart. Purpose of RESPA Reform Promote

MYSTERIES OF THE NEW HUD-1 UNCOVERED August 18, 2009 Jim Gosdin, Deborah Yahner and Jennifer Dumas jgosdin@stewart.com dyahner@stewart.com jdumas@stewart.com 2008 Stewart. Purpose of RESPA Reform Promote

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules Covered Transactions Exemptions Title of Instructions for completion of Delivery of Electronic delivery Federally

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules Covered Transactions Exemptions Title of Instructions for completion of Delivery of Electronic delivery Federally

Advertising, Consumer protection, Credit, Credit unions, Mortgages, National banks,

12 CFR part 1026 Advertising, Consumer protection, Credit, Credit unions, Mortgages, National banks, Recordkeeping and recordkeeping requirements, Reporting, Savings associations, Truth in lending. Authority

12 CFR part 1026 Advertising, Consumer protection, Credit, Credit unions, Mortgages, National banks, Recordkeeping and recordkeeping requirements, Reporting, Savings associations, Truth in lending. Authority

Consumer Financial Protection Bureau Rule

Consumer Financial Protection Bureau Rule Presented by Jerry T. Gorman Attorneys Title Guaranty Fund, Inc. Champaign CFPB Rule Consumer Financial Protection Bureau (CFPB) Came into being July 2011 Created

Consumer Financial Protection Bureau Rule Presented by Jerry T. Gorman Attorneys Title Guaranty Fund, Inc. Champaign CFPB Rule Consumer Financial Protection Bureau (CFPB) Came into being July 2011 Created

Change in Circumstance. CIC Instructions and Request Form

Change in Circumstance CIC Instructions and Request Form The following pages show in detail how to complete a CIC with First Community Mortgage. These scenarios are for educational use only. This is not

Change in Circumstance CIC Instructions and Request Form The following pages show in detail how to complete a CIC with First Community Mortgage. These scenarios are for educational use only. This is not

The New GFE - A Line by Line Walk-Through

The New GFE - A Line by Line Walk-Through Webinar February 12, 2010 9-10:30 a.m. CST Presenter Ms. Christine Sisseck Dennis Schwartz & Assoc., Attorneys At Law 1446 Heritage Dr Mc Kinney, TX 75069-3286

The New GFE - A Line by Line Walk-Through Webinar February 12, 2010 9-10:30 a.m. CST Presenter Ms. Christine Sisseck Dennis Schwartz & Assoc., Attorneys At Law 1446 Heritage Dr Mc Kinney, TX 75069-3286

Shopping for your home loan. Settlement cost booklet

Shopping for your home loan Settlement cost booklet CFPB (Consumer Financial Protection Bureau) January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development.

Shopping for your home loan Settlement cost booklet CFPB (Consumer Financial Protection Bureau) January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development.

Chicago Title Insurance Company

Page 1 of 5 You're receiving this email because of your relationship with Chicago Title Insurance Company. Please confirm your continued interest in receiving email from us. You may unsubscribe if you

Page 1 of 5 You're receiving this email because of your relationship with Chicago Title Insurance Company. Please confirm your continued interest in receiving email from us. You may unsubscribe if you

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview Disclaimer Information included is intended for general information purposes only and is current as October 2, 2015. It should not

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview Disclaimer Information included is intended for general information purposes only and is current as October 2, 2015. It should not

What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule.

Rule.") What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule Presented by Overview Know Before You Owe (the TILA RESPA Integrated Disclosure (TRID)

What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule Presented by Overview Know Before You Owe (the TILA RESPA Integrated Disclosure (TRID)

Shopping for your home loan

Consumer Financial Protection Bureau This booklet was initially prepared by the U.S. Department of Housing and Urban Development. The Consumer Financial Protection Bureau (CFPB) has made technical updates

Consumer Financial Protection Bureau This booklet was initially prepared by the U.S. Department of Housing and Urban Development. The Consumer Financial Protection Bureau (CFPB) has made technical updates

TILA/RESPA Integrated Disclosure Rule

TILA/RESPA Integrated Disclosure Rule Solving the Puzzle July 22, 2015 Presented by: Gary D. Clark, CMB Chief Operating Officer Sierra Pacific Mortgage Webinar All lines will be muted You can type your

TILA/RESPA Integrated Disclosure Rule Solving the Puzzle July 22, 2015 Presented by: Gary D. Clark, CMB Chief Operating Officer Sierra Pacific Mortgage Webinar All lines will be muted You can type your

DRAFT SAMPLE. Closing Information Transaction Information Loan Information

REFINANCE Closing Disclosure DRAFT SAMPLE GREEN = HIGHLIGHTED SECTIONS NEEDED FROM CLSG AGENT RED = LENDER WILL PROVIDE Closing Information Transaction Information Loan Information Date Issued 11/19/2015

REFINANCE Closing Disclosure DRAFT SAMPLE GREEN = HIGHLIGHTED SECTIONS NEEDED FROM CLSG AGENT RED = LENDER WILL PROVIDE Closing Information Transaction Information Loan Information Date Issued 11/19/2015

Loan Originator Compensation and Steering Prohibitions. Branch Originations March 2011

Loan Originator Compensation and Steering Prohibitions Branch Originations March 2011 Regulation Z - Loan Originator Compensation Truth in Lending Act, Regulation Z amendments on loan originator compensation

Loan Originator Compensation and Steering Prohibitions Branch Originations March 2011 Regulation Z - Loan Originator Compensation Truth in Lending Act, Regulation Z amendments on loan originator compensation

Wholesale and Correspondent Mortgage Partners Document and Disclosure Matrix

This information is being provided to aid in compliance with the policies and procedures of FirstBank. This list is not all inclusive. Nothing herein should be construed as legal advice and may not be

This information is being provided to aid in compliance with the policies and procedures of FirstBank. This list is not all inclusive. Nothing herein should be construed as legal advice and may not be

***PROVIDE PRELIM HUD FROM TITLE SHOWING THEIR FEE BREAKDOWN***

CCI DOC ORDER FORM INVESTOR: LOAN #: CIRCLE ONE: CONV / FHA / VA / 2ND INVESTOR PROGRAM CODE: CLOSING DATE & TIME: DISBURSEMENT DATE: FIRST PYMT DUE DATE: BASE LOAN AMOUNT: TOTAL LOAN AMT: INTEREST RATE:

CCI DOC ORDER FORM INVESTOR: LOAN #: CIRCLE ONE: CONV / FHA / VA / 2ND INVESTOR PROGRAM CODE: CLOSING DATE & TIME: DISBURSEMENT DATE: FIRST PYMT DUE DATE: BASE LOAN AMOUNT: TOTAL LOAN AMT: INTEREST RATE:

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

FAR/BAR Changes Resulting from the New CFPB Rules What you Need to Know If Your Real Estate Deal MAY Close After October 3, 2015

FAR/BAR Changes Resulting from the New CFPB Rules What you Need to Know If Your Real Estate Deal MAY Close After October 3, 2015 By Melissa Jay Murphy, Esq. General Counsel Attorneys Title Fund Services,

FAR/BAR Changes Resulting from the New CFPB Rules What you Need to Know If Your Real Estate Deal MAY Close After October 3, 2015 By Melissa Jay Murphy, Esq. General Counsel Attorneys Title Fund Services,

FAQs About RESPA for Industry

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

The New CFPB Mortgage Disclosures: What You Need to Know. William A. Anderson Vice President, Best Practices and Legislative Affairs

The New CFPB Mortgage Disclosures: What You Need to Know William A. Anderson Vice President, Best Practices and Legislative Affairs Poll Question Tell us about yourself: o This is my first NSA Webinar

The New CFPB Mortgage Disclosures: What You Need to Know William A. Anderson Vice President, Best Practices and Legislative Affairs Poll Question Tell us about yourself: o This is my first NSA Webinar

Closing Disclosure August 1, CFR

Closing Disclosure August 1, 2015 12 CFR 1026.38 Agent Questions for Lender Clients Who will prepare the Closing Disclosure (CD) Form? How will Agents coordinate with the lender to prepare the Closing

Closing Disclosure August 1, 2015 12 CFR 1026.38 Agent Questions for Lender Clients Who will prepare the Closing Disclosure (CD) Form? How will Agents coordinate with the lender to prepare the Closing

Today s Rates Looking for the best mortgage loan rate

Today s Rates Looking for the best mortgage loan rate by Natalie Danielson www.clockhours.com A Washington State Approved Real Estate School under R.C.W. 18.85. Sponsor S 1353 Today's Rates Looking for

Today s Rates Looking for the best mortgage loan rate by Natalie Danielson www.clockhours.com A Washington State Approved Real Estate School under R.C.W. 18.85. Sponsor S 1353 Today's Rates Looking for

What is T.R.I.D TILA-RESPA Integrated Disclosure

T.R.I.D. What is T.R.I.D TILA-RESPA Integrated Disclosure The CFPB has issued a rule that is aimed to simplify and improve disclosure forms for mortgage transactions. The rule replaces the current forms

T.R.I.D. What is T.R.I.D TILA-RESPA Integrated Disclosure The CFPB has issued a rule that is aimed to simplify and improve disclosure forms for mortgage transactions. The rule replaces the current forms

Contents. Basics of the Integrated Mortgage Disclosures Rule...3. Closing Disclosure Sample...4. Closing Disclosure Delivery Calendar Examples...

Contents Basics of the Integrated Mortgage Disclosures Rule...3 Closing Disclosure Sample...4 Closing Disclosure Delivery Calendar Examples...9 Basics of the Integrated Mortgage Disclosures Rule What

Contents Basics of the Integrated Mortgage Disclosures Rule...3 Closing Disclosure Sample...4 Closing Disclosure Delivery Calendar Examples...9 Basics of the Integrated Mortgage Disclosures Rule What

The new Loan Estimate Form integrates and replaces the existing RESPA Good Faith Estimate and the initial Truth in Lending forms.

The Consumer Financial Protection Bureau s (CFPB) integrated mortgage disclosure rule will be effective August 1, 2015. This rule consolidates four existing disclosures required under Truth-in-Lending

The Consumer Financial Protection Bureau s (CFPB) integrated mortgage disclosure rule will be effective August 1, 2015. This rule consolidates four existing disclosures required under Truth-in-Lending

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist First Time Home Buyer Program

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist First Time Home Buyer Program BORROWER NAME(S): HMFA Loan # Smart Start Loan # Address: City State Zip Code Lender Name:

New Jersey Housing and Mortgage Finance Agency Purchase Review Submission Checklist First Time Home Buyer Program BORROWER NAME(S): HMFA Loan # Smart Start Loan # Address: City State Zip Code Lender Name:

Presented by Powered by Investors Title

CFPB and the Changing Landscape of Real Estate Closings Presented by Powered by Investors Title The only thing constant in life is change. - François de la Rochefoucauld And the CFPB is proof positive!

CFPB and the Changing Landscape of Real Estate Closings Presented by Powered by Investors Title The only thing constant in life is change. - François de la Rochefoucauld And the CFPB is proof positive!

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET. Christopher W. Smart

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET Christopher W. Smart Introduction and Background Residential mortgage lenders have long been required to disclose to their

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET Christopher W. Smart Introduction and Background Residential mortgage lenders have long been required to disclose to their

ABC Lender 2310 W Interstate 20 Arlington, TX Phone: (817)

") {{SIGB1.0}} {{SIGB2.0}} ABC Lender 2310 W Interstate 20 Arlington, TX 76017 Phone: (817) 555-1212 John Doe and Jane Doe 1234 Easy Street Arlington, TX 76017 Dear Applicant(s), Date: 4/11/2012 Re: Initial

{{SIGB1.0}} {{SIGB2.0}} ABC Lender 2310 W Interstate 20 Arlington, TX 76017 Phone: (817) 555-1212 John Doe and Jane Doe 1234 Easy Street Arlington, TX 76017 Dear Applicant(s), Date: 4/11/2012 Re: Initial

The New Loan Estimate & Closing Disclosure Explained. Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. 2015 Chicago Title Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. 2015 Chicago Title Know before you close.

BUYING YOUR HOME. Settlement Costs and Helpful Information. U.S. Department of Housing and Urban Development

BUYING YOUR HOME Settlement Costs and Helpful Information U.S. Department of Housing and Urban Development Office of Housing - Federal Housing Administration June 1997 HUD-398-H(4) Table of Contents I.

BUYING YOUR HOME Settlement Costs and Helpful Information U.S. Department of Housing and Urban Development Office of Housing - Federal Housing Administration June 1997 HUD-398-H(4) Table of Contents I.

Transaction Information. 123 Anywhere Street Anytown, ST NO NO. Payment Calculation Years 1-4 Years x Property Taxes.

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 4/15/2013 Closing Date 4/15/2013 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 4/15/2013 Closing Date 4/15/2013 Disbursement

Closing Module Company Name. Table of Contents

Table of Contents Table of Contents...i Introduction...v Section 1 - General Position Description Closer/ Coordinator...1 Basic Functions...1 Specific Responsibilities...1 Desired Education and Experience...1

Table of Contents Table of Contents...i Introduction...v Section 1 - General Position Description Closer/ Coordinator...1 Basic Functions...1 Specific Responsibilities...1 Desired Education and Experience...1

PPDocs, Inc. Compliance Certificate

PPDocs, Inc. Lender: Peirson & Patterson Borrower(s): Webinar Demo, a single man Property: 2310 W Interstate 20, Arlington, TX 76017 Loan Type: First Lien Fixed Rate Conventional Loan Loan Purpose: Purchase

PPDocs, Inc. Lender: Peirson & Patterson Borrower(s): Webinar Demo, a single man Property: 2310 W Interstate 20, Arlington, TX 76017 Loan Type: First Lien Fixed Rate Conventional Loan Loan Purpose: Purchase

TRID TILA RESPA Integrated Disclosure. September 29, 2015 Select Partner Process Overview

TRID TILA RESPA Integrated Disclosure September 29, 2015 Select Partner Process Overview 1 Objectives Important Definitions Product Delivery SP Workflow Overview CMG Drawn Docs Process SP Drawn Docs Process

TRID TILA RESPA Integrated Disclosure September 29, 2015 Select Partner Process Overview 1 Objectives Important Definitions Product Delivery SP Workflow Overview CMG Drawn Docs Process SP Drawn Docs Process

Closing Disclosure $0 NO. $0 a month. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

24 CFR Ch. XX ( Edition) APPENDIX C TO PART 3500 INSTRUCTIONS FOR

APPENDIX C TO PART 3500 INSTRUCTIONS FOR") Pt. 3500 originator license and registration. This special category recognizes limited, heavily regulated activities that meet strict criteria that are different from the criteria for specific exemptions

Pt. 3500 originator license and registration. This special category recognizes limited, heavily regulated activities that meet strict criteria that are different from the criteria for specific exemptions

6/21/2013. Section III. Federal Rules, Regulations and Their Requirements. Federal Regulations. Federal Regulations

Section III Federal Rules, Regulations and Their Requirements Federal Regulations The federal rules, regulations and requirements in this course are complied into 4 categories for analysis: Laws requiring

Section III Federal Rules, Regulations and Their Requirements Federal Regulations The federal rules, regulations and requirements in this course are complied into 4 categories for analysis: Laws requiring

The Integrated Disclosures Rule Part A: Introduction to the Integrated Disclosures Rule... 5 Topic 1: Consolidated Disclosures...

SA PL M E Contents The Integrated Disclosures Rule... 4 Part A: Introduction to the Integrated Disclosures Rule... 5 Topic 1: Consolidated Disclosures... 5 Topic 2: Integrated Disclosures Requirements...

SA PL M E Contents The Integrated Disclosures Rule... 4 Part A: Introduction to the Integrated Disclosures Rule... 5 Topic 1: Consolidated Disclosures... 5 Topic 2: Integrated Disclosures Requirements...

REAL ESTATE DICTIONARY

Adjustable-rate mortgage (ARM) -- Home loan in which the interest rate is changed periodically based on a standard financial index. Most ARMs have caps on how much an interest rate may increase. Amortization

Adjustable-rate mortgage (ARM) -- Home loan in which the interest rate is changed periodically based on a standard financial index. Most ARMs have caps on how much an interest rate may increase. Amortization

Fee Disclosure Treatment under the Integrated Disclosures A Work in Progress Fee Name Amount Loan Estimate Section

Disclosure Treatment under the Integrated Disclosures A Work in Progress 4-24-2015 ame Amount Loan Estimate Section Tolerance Closing Disclosure Section Section Application Appraisal Attorney Review Closing

Disclosure Treatment under the Integrated Disclosures A Work in Progress 4-24-2015 ame Amount Loan Estimate Section Tolerance Closing Disclosure Section Section Application Appraisal Attorney Review Closing

Prior to Closing Wholesale

Closing Section 5 Prior to Closing Wholesale ------------------------------------------------------------ 5.2 Closing the Loan Wholesale ---------------------------------------------------------- 5.2 Title

Closing Section 5 Prior to Closing Wholesale ------------------------------------------------------------ 5.2 Closing the Loan Wholesale ---------------------------------------------------------- 5.2 Title

TILA RESPA Integrated Disclosure (TRID) Doing Business with NewLeaf

Doing Business with NewLeaf") TILA RESPA Integrated Disclosure (TRID) Doing Business with NewLeaf Presented By Marti Tromley EVP, Chief Risk Officer mtromley@newleafwholesale.com The information contained herein is intended as informational