Presented by Powered by Investors Title

|

|

|

- Lynn Daniels

- 6 years ago

- Views:

Transcription

1 CFPB and the Changing Landscape of Real Estate Closings Presented by Powered by Investors Title

2 The only thing constant in life is change. - François de la Rochefoucauld And the CFPB is proof positive!

3 QUICK REVIEW 35+ years RESPA/TILA Dodd-Frank requires consolidation Consumer Finance Protection Bureau (CFPB) to carry out Dodd- Frank

4 ROUND TWO Proposed amendments to 12 CFR contained in the Bureau's notice at 77 FR (Aug. 23, 2012) FINAL RULE expected September, 2013 IMPLEMENTATION within 12 months from Final Rule New Loan Estimate -GFE and TILA out New Closing Disclosure -HUD-11 out Limits closing cost increases Redefines APR Additional Consumer Protections Supervision of Service Providers

5 God grant me the serenity to accept the things I cannot change, the courage to change the things I can, and the wisdom to know the difference. - Reinhard Niebuhr

6 GOOD INTENTIONS Simpler Highlights information consumers need Clear warnings about prepayment penalties and an increase in the loan balance (negative amortization) Requires maintenance of electronic copies so regulators will be able to address compliance questions more easily More time to consider choices Limits on closing cost increases

7 CHEERS The negative becomes self fulfilling, gloom creates more gloom Scientific evidence shows pride in our work makes us happier Embrace the changes to be more secure in your closing future

8 NEW(EST) LOAN ESTIMATE Combines final TILA disclosure/gfe Provided by creditor 3 pages Within 3 days of application Application is defined Can only charge for credit report Revisions only if changed circumstance Charges alphabetical-closing charges under title,, Owners insurance quote standard rate

9 EXAMPLE For an adjustable rate mortgage (ARM) monthly costs today projects the monthly payment as adjusts Brings light to the risk-a a rate now in the low 3%s may increase to 8%, it may not be affordable.

10 APPLICABILITY All closed-end end consumer credit secured by RE Excludes HELOCs and Reverse Mortgages (separate, 1/30/2011 Reg Z rules, Subparts B and C )

11 LOAN ESTIMATE

12 LOAN ESTIMATE-Page 3

13 APPLICATION The submission of a borrower s s financial information in anticipation of a credit decision relating to a federally related mortgage loan, which shall include the borrower s s name, the borrower s s monthly income, the borrower s s social security number to obtain a credit report, the property address, an estimate of the value of the property, and the mortgage loan amount sought

14 SHOPPING LISTS Creditor shall identify the services the consumer is permitted to shop for in the Loan Estimate May include affiliates of lender in list-are you on the lists?

15

16

17 NEW(EST) CLOSING DISCLOSURE Combines final TILA disclosure & HUD-1 Must provide at least 3 days prior to closing (exclusive of Sundays, legal holidays) 5 pages Provided by Lender(7 days) or Settlement Agent Revisions require additional 3 day review Limited exceptions for variance of 3 day rule

18 3 Day Exceptions Consumer and seller agree to changes that affect items disclosed- at or before consummation Amount actually paid by the consumer does not exceed the amount disclosed by more than $100- at or before consummation Event occurs after consummation causing disclosures to become inaccurate solely from payments to a government entity in connection with the transaction-no no later than 30 days after consummation

19 3 Day Exceptions-continued Non-numeric numeric clerical errors-asap but no later than 30 days after consummation Amounts paid by the consumer exceed the amounts specified- creditor must refund excess to the consumer asap but no later than 30 days after consummation, AND creditor provides revised disclosures reflecting refund asap but no later than 30 days after consummation

20 NEW(EST) CLOSING DISCLOSURE EXACT amount to bring to closing Prepayment penalties on Page 1 Balloon Payments on Page 1 Alphabetical charges-closing closing charges under title

21 CLOSING DISCLOSURE

22 CLOSING DISCLOSURE-Pages 3&4

23 CLOSING DISCLOSURE-Page 5

24 LIMITS ON INCREASES Zero Tolerance lenders charges for own services, services by an affiliate, broker, ie. processing and underwriting fees (Loan Estimate Page 2, Section A) charges for services consumer not permitted to shop (Loan Estimate Page 2, Section B) Appraisal, Credit Report, Flood/Tax Service Transfer tax

25 EXCEPTIONS TO 10% CAP Update 3 days prior required Consumer requests change Consumer chose provider Information from application inaccurate (or becomes) Loan Estimate expires Recording Fees

26 NO TOLERANCE RESTRICTION Loan originator required services where the borrower selects his or her own third- party provider; Title services, lender s s title insurance, and owner s s title insurance when the borrower selects his or her own provider; Initial escrow deposit; Daily interest charges; and homeowner s insurance

27 Tolerance Existing RESPA Rules Proposed Integration Rules 0 Tolerance May not exceed fees estimated on the GFE Origination Charges Points Transfer Tax Fees paid to the creditor points, yield spread premium, processing & underwriting fee Transfer Tax Fees paid to broker Fees paid to an affiliate Fees paid to unaffiliated third party if consumer is not allowed to shop 10% Tolerance Individual fees may increase or decrease, but the sum of the charges at settlement may not be greater than ten percent above the sum of the amounts included on the GFE. Required services selected by lender Title Services and lenders title insurance if selected by lender or off list Owner s s title if on list Required services selected by consumer off list Government Recording Charges Fees paid to unaffiliated third party settlement agent if consumer can shop, does not choose one, or chooses one off list provided Recording Fees No Tolerance Fees not subject to any tolerance restriction, can change at settlement and the amount of the change is not limited. Required services selected by consumer Title services and lenders title if selected by consumer and not on list Owners title not on list Initial escrow deposit Daily interest charge Homeowners insurance Prepaid interest Property insurance Escrow Charges paid to third party selected by consumer and not identified by creditor *Provided estimates are consistent with best information available to creditor at time loan estimate is made

28 FINANCE CHARGE Includes title examination, abstract of title, title insurance, property survey, and similar items; preparing loan-related documents, such as deeds, mortgages, and reconveyance or settlement documents; notary and credit report fees; property appraisal or inspections to assess the value or condition of the property prior to closing, including pest-infestation or flood-hazard determination; and amounts required to be paid into escrow or trustee accounts if the amounts would not otherwise be included in the finance charge Also government recording taxes and related fees

29 WHO PROVIDES DISCLOSURE? Creditor solely responsible for the provision of the closing disclosures Alternative: settlement agent may provide a consumer with the disclosures, provided the settlement agent complies with all requirements of (f) as if it were the creditor. Not intended to relieve the creditor s responsibility under TILA and creditor remains responsible to ensure disclosures are provided in accordance with the requirements of (f)

30 SELLER Seller Transaction Coverage The person conducting the settlement shall provide the seller with the disclosures that relate to the seller No later than the day of consummation. Revised disclosures to the seller no later than 30 days after consummation The amount imposed upon the seller for any settlement service shall not exceed the amount actually received by the service provider for that service, except for average charges

31 CAN I CHARGE????? (Insert laugh track) No fee may be imposed on any person, as a part of settlement costs or otherwise, by a creditor or by a servicer for the preparation or delivery of the disclosures, escrow account statements required pursuant to section 10 of RESPA, or other statements required by TILA

32 RECORD RETENTION Creditors must keep such records in an electronic, machine readable format Retain evidence of compliance for three years Retain each completed closing disclosure and all documents related to such disclosures, for five years after settlement.*investors agent contracts keep all title files forever in electronic, machine readable format Machine readable means a format where the individual data elements comprising the record can be transmitted, analyzed, and processed by a computer program, such as a spreadsheet or database program (NOT PDFs)

33 APR REDEFINED Includes almost all up-front costs except charges that are applied after the loan closes, such as late fees or delinquency charges Previously exempted costs like application fees now included

34 THOUGHTS TO PONDER If lender becomes responsible for preparation and delivery of the e final Disclosure Form, what role will settlement agents play? Will settlement agents continue to aggregate information for the Closing Disclosure from other parties outside the realm of the loan l itself i.e. real estate commissions, homeowner s s associations, obtaining payoff of debts, ordering final utility readings, ordering ring surveys, collecting back child support or other government liens and debts? If so, could lender decide to act as the disbursement agent for all loan proceeds, some loan proceeds?

35 THOUGHTS TO PONDER How will the lenders begin to incorporate all of these facets into their daily operations? Consumers look to us to be timely and look to us to handle the transaction an efficient manner, Evans said. If we lose productivity through these new regulations, it will impact production and how we serve our customers. ALTA

36 SPECIFIC ISSUES How often do closing costs change within 3 days of closing? What are the reasons these costs change? What other exemptions to the rule might be warranted to ensure the consumer is not harmed by a delay? What training, increased precalls with lenders, time taken within redisclosures, costs will you have?

37 OTHER CHANGES

38 HIGH COST MORTGAGE PROTECTIONS Effective January 2014 Definition: first mortgage with APR > 6.5 points higher than average prime offer rate mortgage for less than $50,000,for personal property dwelling (ie mobile), and APR > 8.5 points higher than the average second mortgage, and your APR > 8.5 points higher Mortgage for less than $20,000 and the points and fees > the lesser of 8 percent of your loan or $1,000, or loan >$20,000 and the points and fees exceed 5 percent of your loan

39 PROHIBITIONS Fees for paying all or part of early Balloon payments Late fees > 4 percent of payment Most fees for getting a payoff statement Fees for loan modifications Creditors or brokers advising homeowners refinancing into high-cost mortgages not to make their payments on an existing loan

40 SUPERVISION OF PROVIDERS Conduct due diligence to verify service provider understands and is capable of complying with federal consumer financial law Request and review service provider s s policies, procedures, internal controls, and training material to ensure that the service provider conducts appropriate training and oversight of employees or agents that have consumer contact or compliance responsibilities Include contractual provisions about compliance Establish internal on-going monitoring Take action to address problems identified Service providers are defined to include settlement service providers IMPACT-vetting companies ALTA Best Practices

41 It has been said that man is a rational animal. All my life I have been searching for evidence which could support this. -Bertrand Russell

42 "Developing Solutions to Grow Your Bottom Line" Presented by Powered by Investors Title

43 Topic: CFPB and the Changing Landscape of Real Estate Closings What you need to know about CFPB changes Proposed Tolerances Tolerance Existing RESPA Rules Proposed Integration Rules 0 Tolerance May not exceed fees estimated on the GFE Origination Charges Points Transfer Tax Fees paid to the creditorpoints, yield spread premium, processing & underwriting fee Transfer Tax Fees paid to broker Fees paid to an affiliate Fees paid to unaffiliated third party if consumer is not allowed to shop 10% Tolerance Individual fees may increase or decrease, but the sum of the charges at settlement may not be greater than ten percent above the sum of the amounts included on the GFE. Required services selected by lender Title Services and lenders title insurance if selected by lender or off list Owner s title if on list Required services selected by consumer off list Government Recording Charges Fees paid to unaffiliated third party settlement agent if consumer can shop, does not choose one, or chooses one off list provided Recording Fees No Tolerance Fees not subject to any tolerance restriction, can change at settlement and the amount of the change is not limited. Required services selected by consumer Title services and lenders title if selected by consumer and not on list Owners title not on list Initial escrow deposit Daily interest charge Homeowners insurance Prepaid interest Property insurance Escrow Charges paid to third party selected by consumer and not identified by creditor *Provided estimates are consistent with best information available to creditor at time loan estimate is made

44 FICUS BANK 4321 Random Boulevard Somecity, ST Loan Estimate date issued 7/23/2012 Applicants John A. and Mary B. 123 Anywhere Street Anytown, ST Property 456 Somewhere Avenue Anytown, ST sale price $180,000 Save this Loan Estimate to compare with your Closing Disclosure. Loan TERM 30 years Purpose Purchase ce product Fixed Rate Loan Type x Conventional FHA VA LOAN ID # RATE LOCK NO x YES, until 9/21/12 at 5:00 p.m. EDT Before closing, your interest rate, points, and lender credits can change unless you lock the interest rate. All other estimated closing costs expire on 8/6/12 at 5:00 p.m. EDT Loan Terms Can this amount increase after closing? Loan Amount $162,000 NO Interest Rate 3.875% NO Monthly Principal & Interest See Projected Payments Below for Your Total Monthly Payment Prepayment Penalty Balloon Payment $ NO Does the loan have these features? NO NO Projected Payments Payment Calculation Years 1-7 Years 8-30 Principal & Interest $ $ Mortgage Insurance Estimated Escrow Amount Can Increase Over Time Estimated Total Monthly Payment $1,050 $968 Estimated Taxes, Insurance & Assessments Amount Can Increase Over Time $206 a month This estimate includes In escrow? x Property Taxes YES x Homeowner s Insurance YES Other: See Section G on page 2 for escrowed property costs. You must pay for other property costs separately. Cash to Close Estimated Cash to Close $16,054 Includes $8,054 in Closing Costs ( $5,672 in Loan Costs + $2,382 in Other Costs $0 in Lender Credits). See details on page 2. Visit for general information and tools. Loan Estimate page 1 of 3 Loan ID #

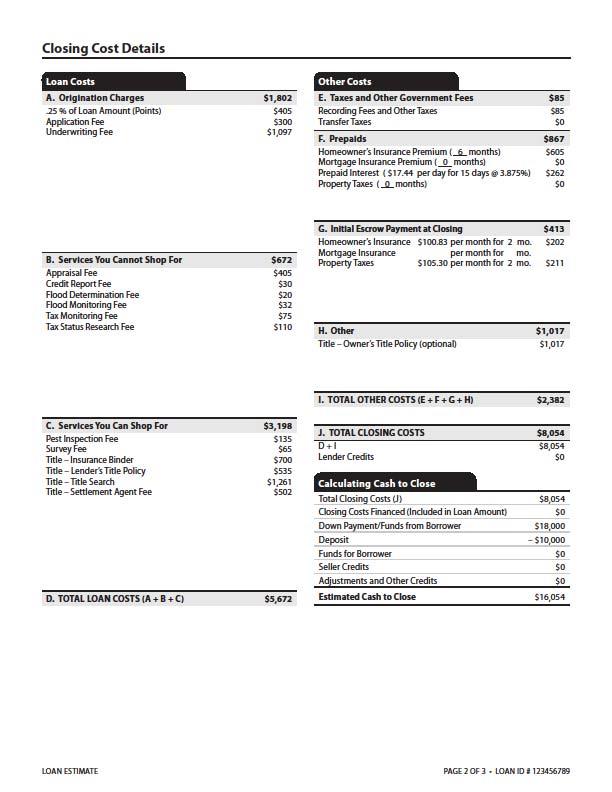

45 Closing Cost Details Loan Costs A. Origination Charges $1, % of Loan Amount (Points) $405 Application Fee $300 Underwriting Fee $1,097 Other Costs E. Taxes and Other Government Fees $85 Recording Fees and Other Taxes $85 Transfer Taxes $0 F. Prepaids $867 Homeowner s Insurance Premium ( 6 months) $605 Mortgage Insurance Premium ( 0 months) $0 Prepaid Interest ( $17.44 per day for %) $262 Property Taxes ( 0 months) $0 B. Services You Cannot Shop For $672 Appraisal Fee $405 Credit Report Fee $30 Flood Determination Fee $20 Flood Monitoring Fee $32 Tax Monitoring Fee $75 Tax Status Research Fee $110 G. Initial Escrow Payment at Closing $413 Homeowner s Insurance $ per month for 23mo. $202 Mortgage Insurance per month for 0 mo. Property Taxes $ per month for 2 mo. $211 H. Other $1,017 Title Owner s Title Policy (optional) $1,017 I. Total Other Costs (E + F + G + H) $2,382 C. Services You Can Shop For $3,198 Pest Inspection Fee $135 Survey Fee $65 Title Insurance Binder $700 Title Lender s Title Policy $535 Title Title Search $1,261 Title Settlement Agent Fee $502 D. Total loan costs (A + B + C) $5,672 J. Total Closing Costs $8,054 D + I $8,054 Lender Credits $0 Calculating Cash to Close Total Closing Costs (J) $8,054 Closing Costs Financed (Included in Loan Amount) $0 Down Payment/Funds from Borrower $18,000 Deposit $10,000 Funds for Borrower $0 Seller Credits $0 Adjustments and Other Credits $0 Estimated Cash to Close $16,054 Loan Estimate page 2 of 3 Loan ID #

46 Additional Information About This Loan LENDER Ficus Bank NMLS/License ID Loan officer Joe Smith NMLS ID PHONE Mortgage broker NMLS/License ID Loan officer NMLS ID PHONE Comparisons In 5 Years Annual Percentage Rate (APR) Total Interest Percentage (TIP) Use these measures to compare this loan with other loans. $56,582 Total you will have paid in principal, interest, mortgage insurance, and loan costs. $15,773 Principal you will have paid off % Your costs over the loan term expressed as a rate. This is not your interest rate % The total amount of interest that you will pay over the loan term as a percentage of your loan amount. Other Considerations Appraisal Assumption Homeowner s Insurance Late Payment Refinance Servicing We may order an appraisal to determine the property s value and charge you for this appraisal. We will promptly give you a copy of any appraisal, even if your loan does not close. You can pay for an additional appraisal for your own use at your own cost. If you sell or transfer this property to another person, we will allow, under certain conditions, this person to assume this loan on the original terms. x will not allow this person to assume this loan on the original terms. This loan requires homeowner s insurance on the property, which you may obtain from a company of your choice that we find acceptable. If your payment is more than 15 days late, we will charge a late fee of 5% of the monthly principal and interest payment. Refinancing this loan will depend on your future financial situation, the property value, and market conditions. You may not be able to refinance this loan. We intend to service your loan. If so, you will make your payments to us. x to transfer servicing of your loan. Confirm Receipt By signing, you are only confirming that you have received this form. You do not have to accept this loan because you have signed or received this form. Applicant Signature Date Co-Applicant Signature Date Loan Estimate page 3 of 3 Loan ID #

47 Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 9/10/2012 Closing Date 9/14/2012 Disbursement Date 9/14/2012 Agent Epsilon Title Co. File # Property 456 Somewhere Ave Anytown, ST Sale Price $180,000 Transaction Information Borrower John A. and Mary B. 123 Anywhere Street Anytown, ST Seller Steve C. and Amy D. 321 Somewhere Drive Anytown, ST Lender Ficus Bank Loan Information Loan Term Purpose Product 30 years Purchase Fixed Rate Loan Type x Conventional FHA VA Loan ID # MIC # Loan Terms Can this amount increase after closing? Loan Amount $162,000 NO Interest Rate 3.875% NO Monthly Principal & Interest See Projected Payments Below for Your Total Monthly Payment Prepayment Penalty Balloon Payment $ NO Does the loan have these features? NO NO Projected Payments Payment Calculation Years 1-7 Years 8-30 Principal & Interest Mortgage Insurance Estimated Escrow Amount Can Increase Over Time $ $ Estimated Total Monthly Payment $1, $ Estimated Taxes, Insurance & Assessments Amount Can Increase Over Time See Details on Page 4 $ a month This estimate includes x Property Taxes x Homeowner s Insurance x Other: Homeowner s Association In escrow? YES YES NO See page 4 for escrowed property costs. You must pay for other property costs separately. Cash to Close Cash to Close $14, Includes $9, in Closing Costs ($4, in Loan Costs + $5, in Other Costs $0 in Lender Credits). See details on page 2. CLOSING DISCLOSURE PAGE 1 OF 5 LOAN ID #

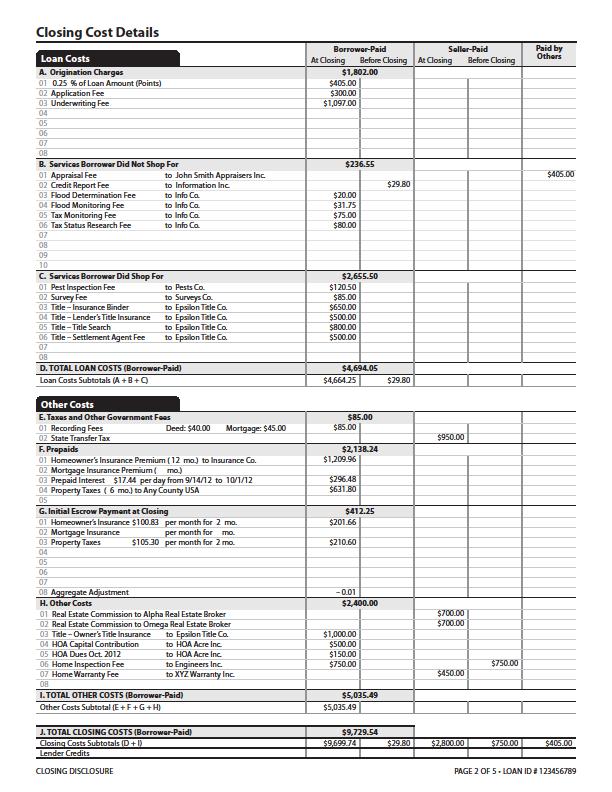

48 Closing Cost Details Loan Costs Borrower-Paid Seller-Paid Paid by Others At Closing Before Closing At Closing Before Closing A. Origination Charges $1, % of Loan Amount (Points) $ Application Fee $ Underwriting Fee $1, B. Services Borrower Did Not Shop For $ Appraisal Fee to John Smith Appraisers Inc. $ Credit Report Fee to Information Inc. $ Flood Determination Fee to Info Co. $ Flood Monitoring Fee to Info Co. $ Tax Monitoring Fee to Info Co. $ Tax Status Research Fee to Info Co. $ C. Services Borrower Did Shop For $2, Pest Inspection Fee to Pests Co. $ Survey Fee to Surveys Co. $ Title Insurance Binder to Epsilon Title Co. $ Title Lender s Title Insurance to Epsilon Title Co. $ Title Title Search to Epsilon Title Co. $ Title Settlement Agent Fee to Epsilon Title Co. $ D. TOTAL LOAN COSTS (Borrower-Paid) $4, Loan Costs Subtotals (A + B + C) $4, $29.80 Other Costs E. Taxes and Other Government Fees $ Recording Fees Deed: $40.00 Mortgage: $45.00 $ State Transfer Tax $ F. Prepaids $2, Homeowner s Insurance Premium ( 12 mo.) to Insurance Co. $1, Mortgage Insurance Premium ( mo.) 03 Prepaid Interest $17.44 per day from 9/14/12 to 10/1/12 $ Property Taxes ( 6 mo.) to Any County USA $ G. Initial Escrow Payment at Closing $ Homeowner s Insurance $ per month for 2 mo. $ Mortgage Insurance per month for mo. 03 Property Taxes $ per month for 2 mo. $ Aggregate Adjustment 0.01 H. Other Costs $2, Real Estate Commission to Alpha Real Estate Broker $ Real Estate Commission to Omega Real Estate Broker $ Title Owner s Title Insurance to Epsilon Title Co. $1, HOA Capital Contribution to HOA Acre Inc. $ HOA Dues Oct to HOA Acre Inc. $ Home Inspection Fee to Engineers Inc. $ $ Home Warranty Fee to XYZ Warranty Inc. $ I. TOTAL OTHER COSTS (Borrower-Paid) $5, Other Costs Subtotal (E + F + G + H) $5, J. TOTAL CLOSING COSTS (Borrower-Paid) $9, Closing Costs Subtotals (D + I) $9, $29.80 $2, $ $ Lender Credits CLOSING DISCLOSURE PAGE 2 OF 5 LOAN ID #

49 Calculating Cash to Close Estimate Final Did this change? Total Closing Costs (J) $8, $9, YES See Total Loan Costs (D) and Total Other Costs (I) Closing Costs Paid Before Closing $0 $29.80 YES You paid these Closing Costs before closing Closing Costs Financed (Included in Loan Amount) $0 $0 NO Down Payment/Funds from Borrower $18, $18, NO Deposit $10, $10, NO Funds for Borrower Seller Credits $0 $2, YES See Seller Credits in Section L Adjustments and Other Credits $0 $ YES See details in Sections K and L Cash to Close $16, $14, Use this table to see what has changed from your Loan Estimate. NO Summaries of Transactions BORROWER S TRANSACTION Use this table to see a summary of your transaction. SELLER S TRANSACTION K. Due from Borrower at Closing $189, Sale Price of Property $180, Sale Price of Any Personal Property Included in Sale 03 Closing Costs Paid at Closing (J) $9, Adjustments Adjustments for Items Paid by Seller in Advance 08 City/Town Taxes to 09 County Taxes to 10 Assessments to 11 HOA Dues 9/14/12 to 9/30/12 $ L. Paid Already by or on Behalf of Borrower at Closing $175, Deposit $10, Borrower s Loan Amount $162, Existing Loan(s) Assumed or Taken Subject to Seller Credit $2, Other Credits 06 Rebate from Epsilon Title Co. $ Adjustments Adjustments for Items Unpaid by Seller 12 City/Town Taxes 7/1/12 to 9/14/12 $ County Taxes to 14 Assessments to CALCULATION Total Due from Borrower at Closing (K) $189, Total Paid Already by or on Behalf of Borrower at Closing (L) $175, Cash to Close x From To Borrower $14, M. Due to Seller at Closing $180, Sale Price of Property $180, Sale Price of Any Personal Property Included in Sale Adjustments for Items Paid by Seller in Advance 09 City/Town Taxes to 10 County Taxes to 11 Assessments to 12 HOA Dues 9/14/12 to 9/30/12 $ N. Due from Seller at Closing $115, Excess Deposit $10, Closing Costs Paid at Closing (J) $2, Existing Loan(s) Assumed or Taken Subject to 04 Payoff of First Mortgage Loan $100, Payoff of Second Mortgage Loan Seller Credit $2, Adjustments for Items Unpaid by Seller 14 City/Town Taxes 7/1/12 to 9/14/12 $ County Taxes to 16 Assessments to CALCULATION Total Due to Seller at Closing (M) $180, Total Due from Seller at Closing (N) $115, Cash From x To Seller $64, CLOSING DISCLOSURE PAGE 3 OF 5 LOAN ID #

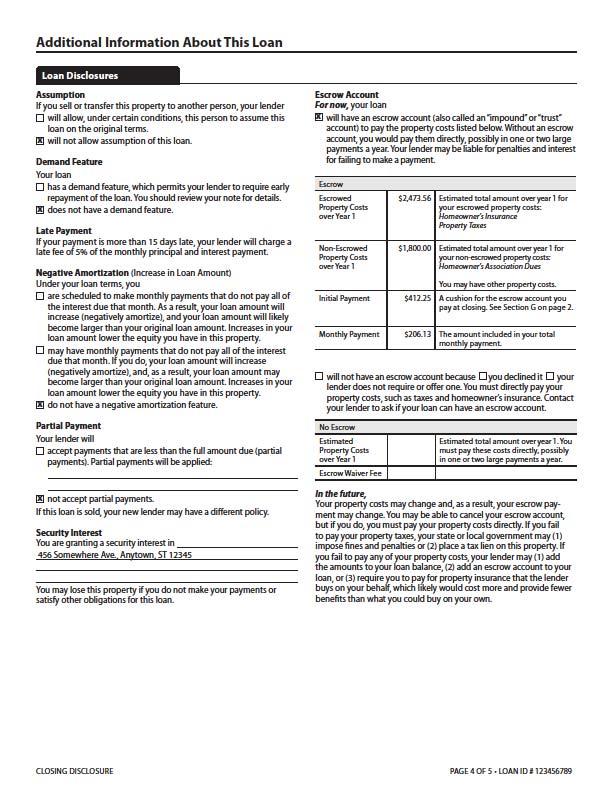

50 Additional Information About This Loan Loan Disclosures Assumption If you sell or transfer this property to another person, your lender will allow, under certain conditions, this person to assume this loan on the original terms. x will not allow assumption of this loan. Demand Feature Your loan has a demand feature, which permits your lender to require early repayment of the loan. You should review your note for details. x does not have a demand feature. Late Payment If your payment is more than 15 days late, your lender will charge a late fee of 5% of the monthly principal and interest payment. Negative Amortization (Increase in Loan Amount) Under your loan terms, you are scheduled to make monthly payments that do not pay all of the interest due that month. As a result, your loan amount will increase (negatively amortize), and your loan amount will likely become larger than your original loan amount. Increases in your loan amount lower the equity you have in this property. may have monthly payments that do not pay all of the interest due that month. If you do, your loan amount will increase (negatively amortize), and, as a result, your loan amount may become larger than your original loan amount. Increases in your loan amount lower the equity you have in this property. x do not have a negative amortization feature. Escrow Account For now, your loan x will have an escrow account (also called an impound or trust account) to pay the property costs listed below. Without an escrow account, you would pay them directly, possibly in one or two large payments a year. Your lender may be liable for penalties and interest for failing to make a payment. Escrow Escrowed Property Costs over Year 1 Non-Escrowed Property Costs over Year 1 $2, Estimated total amount over year 1 for your escrowed property costs: Homeowner s Insurance Property Taxes $1, Estimated total amount over year 1 for your non-escrowed property costs: Homeowner s Association Dues You may have other property costs. Initial Payment $ A cushion for the escrow account you pay at closing. See Section G on page 2. Monthly Payment $ The amount included in your total monthly payment. will not have an escrow account because you declined it your lender does not require or offer one. You must directly pay your property costs, such as taxes and homeowner s insurance. Contact your lender to ask if your loan can have an escrow account. Partial Payment Your lender will accept payments that are less than the full amount due (partial payments). Partial payments will be applied: No Escrow Estimated Property Costs over Year 1 Escrow Waiver Fee Estimated total amount over year 1. You must pay these costs directly, possibly in one or two large payments a year. x not accept partial payments. If this loan is sold, your new lender may have a different policy. Security Interest You are granting a security interest in 456 Somewhere Ave., Anytown, ST You may lose this property if you do not make your payments or satisfy other obligations for this loan. In the future, Your property costs may change and, as a result, your escrow payment may change. You may be able to cancel your escrow account, but if you do, you must pay your property costs directly. If you fail to pay your property taxes, your state or local government may (1) impose fines and penalties or (2) place a tax lien on this property. If you fail to pay any of your property costs, your lender may (1) add the amounts to your loan balance, (2) add an escrow account to your loan, or (3) require you to pay for property insurance that the lender buys on your behalf, which likely would cost more and provide fewer benefits than what you could buy on your own. CLOSING DISCLOSURE PAGE 4 OF 5 LOAN ID #

51 Loan Calculations Total of Payments. Total you will have paid after you make all payments of principal, interest, mortgage insurance, and loan costs, as scheduled. $292, Finance Charge. The dollar amount the loan will cost you. $123, Amount Financed. The loan amount available after paying your upfront finance charge. $156, Annual Percentage Rate (APR). Your costs over the loan term expressed as a rate. This is not your interest rate % Total Interest Percentage (TIP). The total amount of interest that you will pay over the loan term as a percentage of your loan amount % Approximate Cost of Funds (ACF). The approximate cost of the funds used to make this loan. This is not a direct cost to you. 1.63% Other Disclosures Appraisal If the property was appraised for your loan, your lender is required to give you a copy at no additional cost at least 3 days before closing. If you have not yet received it, please contact your lender at the information listed below. Contract Details See your note and security instrument for information about what happens if you fail to make your payments, what is a default on the loan, situations in which your lender can require early repayment of the loan, and the rules for making payments before they are due. Liability after Foreclosure If your lender forecloses on this property and the foreclosure does not cover the amount of unpaid balance on this loan, x state law may protect you from liability for the unpaid balance. If you refinance or take on any additional debt on this property, you may lose this protection and be liable for debt remaining after the foreclosure. You may want to consult a lawyer for more information. state law does not protect you from liability for the unpaid balance.? at Questions? If you have questions about the loan terms and costs on this form, contact your lender. To get more information or make a complaint, contact the Consumer Financial Protection Bureau Refinance Refinancing this loan will depend on your future financial situation, the property value, and market conditions. You may not be able to refinance this loan. Tax Deductions If you borrow more than this property is worth, the interest on the loan amount above this property s fair market value is not deductible from your federal income taxes. You should consult a tax advisor for more information. Contact Information Lender Mortgage Broker Real Estate Broker (B) Real Estate Broker (S) Settlement Agent Name Ficus Bank FRIENDLY MORTGAGE BROKER INC. Address NMLS/ License ID 4321 Random Blvd. Somecity, ST Terrapin Dr. Somecity, MD Omega Real Estate Broker Inc. 789 Local Lane Sometown, ST Alpha Real Estate Broker Co. 987 Suburb Ct. Someplace, ST Z Z61456 Z61616 Epsilon Title Co. Contact Joe S. JIM TAYLOR Samuel G. Joseph C. Sarah A. Contact NMLS/ License ID P16415 P51461 PT1234 joesmith@ ficusbank.com JTAYLOR@ FRNDLYMTGBRKR.COM 123 Commerce Pl. Somecity, ST sam@omegare.biz joe@alphare.biz sarah@ epsilontitle.com Phone Confirm Receipt By signing, you are only confirming that you have received this form. You do not have to accept this loan because you have signed or received this form. Applicant Signature Date Co-Applicant Signature Date CLOSING DISCLOSURE PAGE 5 OF 5 LOAN ID #

Transaction Information. Michael Jones and Mary Stone 123 Anywhere Street. Anytown, ST Steve Cole and Amy Doe 321 Somewhere Drive

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 4/15/2013 Closing Date 4/15/2013 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 4/15/2013 Closing Date 4/15/2013 Disbursement

FICUS BANK 4321 Random Boulevard Somecity, ST 12340

FICUS BANK 4321 Random Boulevard Somecity, ST 12340 Loan Estimate DATE ISSUED 2/15/2013 APPLICANTS Michael Jones and Mary Stone 123 Anywhere Street PROPERTY 456 Somewhere Avenue SALE PRICE $180,000 Save

FICUS BANK 4321 Random Boulevard Somecity, ST 12340 Loan Estimate DATE ISSUED 2/15/2013 APPLICANTS Michael Jones and Mary Stone 123 Anywhere Street PROPERTY 456 Somewhere Avenue SALE PRICE $180,000 Save

The New CFPB Mortgage Disclosures: What You Need to Know. William A. Anderson Vice President, Best Practices and Legislative Affairs

The New CFPB Mortgage Disclosures: What You Need to Know William A. Anderson Vice President, Best Practices and Legislative Affairs Poll Question Tell us about yourself: o This is my first NSA Webinar

The New CFPB Mortgage Disclosures: What You Need to Know William A. Anderson Vice President, Best Practices and Legislative Affairs Poll Question Tell us about yourself: o This is my first NSA Webinar

TILA RESPA Integrated Disclosure

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-25(B) Mortgage Loan Transaction Closing Disclosure Fixed Rate Loan Sample This is a sample of a completed Closing Disclosure for the fixed rate loan

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-25(B) Mortgage Loan Transaction Closing Disclosure Fixed Rate Loan Sample This is a sample of a completed Closing Disclosure for the fixed rate loan

Consumer Financial Protection Bureau Rule

Consumer Financial Protection Bureau Rule Presented by Jerry T. Gorman Attorneys Title Guaranty Fund, Inc. Champaign CFPB Rule Consumer Financial Protection Bureau (CFPB) Came into being July 2011 Created

Consumer Financial Protection Bureau Rule Presented by Jerry T. Gorman Attorneys Title Guaranty Fund, Inc. Champaign CFPB Rule Consumer Financial Protection Bureau (CFPB) Came into being July 2011 Created

February 2016 FEBRUARY Sunday Monday Tuesday Wednesday Thursday Friday Saturday. CD is placed in the mail IF DELIVERED BY OVERNIGHT MAIL...

DELIVERY METHODS & TIMING CHEAT SHEET IF DELIVERED BY MAIL... Closing Disclosure (CD) is sent to borrower in the mail 3 day mailing rule applies for the receipt of the disclosure Then 3 day waiting period

DELIVERY METHODS & TIMING CHEAT SHEET IF DELIVERED BY MAIL... Closing Disclosure (CD) is sent to borrower in the mail 3 day mailing rule applies for the receipt of the disclosure Then 3 day waiting period

Contents. Basics of the Integrated Mortgage Disclosures Rule...3. Closing Disclosure Sample...4. Closing Disclosure Delivery Calendar Examples...

Contents Basics of the Integrated Mortgage Disclosures Rule...3 Closing Disclosure Sample...4 Closing Disclosure Delivery Calendar Examples...9 Basics of the Integrated Mortgage Disclosures Rule What

Contents Basics of the Integrated Mortgage Disclosures Rule...3 Closing Disclosure Sample...4 Closing Disclosure Delivery Calendar Examples...9 Basics of the Integrated Mortgage Disclosures Rule What

The New Loan Estimate & Closing Disclosure Explained. Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. 2015 Chicago Title Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. 2015 Chicago Title Know before you close.

Transaction Information. Michael Jones and Mary Stone 123 Anywhere Street. Anytown, ST Steve Cole and Amy Doe 321 Somewhere Drive

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 4//2016 Closing Date 4/15/2016 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 4//2016 Closing Date 4/15/2016 Disbursement

Closing Disclosure $0 NO. $0 a month. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Information Transaction Information Loan Information. VA Property Loan ID # Lender MIC # Sale Price $

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Transaction Information. 123 Anywhere Street Anytown, ST NO NO. Payment Calculation Years 1-4 Years x Property Taxes.

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 4/15/2013 Closing Date 4/15/2013 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 4/15/2013 Closing Date 4/15/2013 Disbursement

Quick Reference Guide

Integrated Mortgage Closing Disclosure Quick Reference Guide A Compilation of Tools, Tips, Forms & Samples This guide is for informational purposes only and was designed to provide high level particulars

Integrated Mortgage Closing Disclosure Quick Reference Guide A Compilation of Tools, Tips, Forms & Samples This guide is for informational purposes only and was designed to provide high level particulars

Transaction Information. Michael Jones and Mary Stone 123 Anywhere Street. Joe Seller 1234 Main Street Anywhere, TX PPDocs, Inc.

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 8/3/20 Closing Date 8/17/20 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 8/3/20 Closing Date 8/17/20 Disbursement

2015 Freddie Mac and Fannie Mae. All Rights Reserved. MISMO is a registered trademark of the Mortgage Industry Standards Maintenance Organization.

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix F: UCD Sample Use Case Purchase/Fixed Rate Document Version 1.1 February 24, 2015 In support of the Integrated

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix F: UCD Sample Use Case Purchase/Fixed Rate Document Version 1.1 February 24, 2015 In support of the Integrated

Closing Information Transaction Information Loan Information. VA Property Lender Loan ID # MIC #

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

TILA-RESPA INTEGRATED DISCLOSURE AND ETHICAL CONSIDERATIONS

TILA-RESPA INTEGRATED DISCLOSURE AND ETHICAL CONSIDERATIONS Andy Maloney, Esq. President 2818 Bransford Avenue Nashville, TN 37204 615-385-5944 andy@nashvilletitle.com WHAT HAVE WE LEARNED AND WHAT HAS

TILA-RESPA INTEGRATED DISCLOSURE AND ETHICAL CONSIDERATIONS Andy Maloney, Esq. President 2818 Bransford Avenue Nashville, TN 37204 615-385-5944 andy@nashvilletitle.com WHAT HAVE WE LEARNED AND WHAT HAS

Closing Disclosure $ % $ $ $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

document with your Loan Estimate. Transaction Information X Property Taxes NO X Homeowner's Insurance NO Other: details.

Closing Disclosure document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement Agent File # Property Sale Price BLANKTRID Transaction Information Borrower

Closing Disclosure document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement Agent File # Property Sale Price BLANKTRID Transaction Information Borrower

Closing Disclosure $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Joe W. Borrowers and Jane R. Borrower Some Street Ardsley, New York Peter Sellers

Closing Disclosure This form is a statement of final loan terms and closings cost Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closings cost Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Settlement Disclosure

Settlement Disclosure This form is a statement of final loan terms and closing costs. Compare this document to your Loan Estimate. Settlement information Date 1/24/2012 Agent ABC Settlement File # 01234

Settlement Disclosure This form is a statement of final loan terms and closing costs. Compare this document to your Loan Estimate. Settlement information Date 1/24/2012 Agent ABC Settlement File # 01234

Closing Disclosure $ NO

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Transaction Information. Tennessee Housing Development Agency

Tennessee Housing Development Agency Second Mortgage Loan This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Disclosure Closing Information

Tennessee Housing Development Agency Second Mortgage Loan This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Disclosure Closing Information

DRAFT SAMPLE. Closing Information Transaction Information Loan Information

REFINANCE Closing Disclosure DRAFT SAMPLE GREEN = HIGHLIGHTED SECTIONS NEEDED FROM CLSG AGENT RED = LENDER WILL PROVIDE Closing Information Transaction Information Loan Information Date Issued 11/19/2015

REFINANCE Closing Disclosure DRAFT SAMPLE GREEN = HIGHLIGHTED SECTIONS NEEDED FROM CLSG AGENT RED = LENDER WILL PROVIDE Closing Information Transaction Information Loan Information Date Issued 11/19/2015

Closing Disclosure $ NO $1, $ a month. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 8/15/2015 Closing Date 8/31/2015 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 8/15/2015 Closing Date 8/31/2015 Disbursement

Settlement Disclosure Form

Settlement Disclosure Form This form is a statement of final loan terms and actual settlement costs. Settlement information Date 11/9/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd,

Settlement Disclosure Form This form is a statement of final loan terms and actual settlement costs. Settlement information Date 11/9/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd,

Closing Disclosure. This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate.

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Transaction Information. Johnathan James Doe and Jennifer Jane Doe 1234 Riverside Drive Grand Prairie, TX ABC Mortgage Company

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 10/31/2016 Closing Date /30/2016 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 10/31/2016 Closing Date /30/2016 Disbursement

Settlement Disclosure Form

Settlement Disclosure Form This form is a statement of final loan terms and actual settlement costs. SETTLEMENT INFORMATION Date 11/9/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd,

Settlement Disclosure Form This form is a statement of final loan terms and actual settlement costs. SETTLEMENT INFORMATION Date 11/9/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd,

Closing Information Transaction Information Loan Information Vickery Blvd. Dallas, TX Lender CrossCountry Mortgage, Inc.

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

TILA RESPA Integrated Disclosure

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

Your home loan toolkit

Your home loan toolkit A step-by-step guide Consumer Financial Protection Bureau Page 1 How can this toolkit help you? Buying a home is exciting and, let s face it, complicated. This booklet is a toolkit

Your home loan toolkit A step-by-step guide Consumer Financial Protection Bureau Page 1 How can this toolkit help you? Buying a home is exciting and, let s face it, complicated. This booklet is a toolkit

Your home loan toolkit

Your home loan toolkit A step-by-step guide Consumer Financial Protection Bureau Page 1 How can this toolkit help you? Buying a home is exciting and, let s face it, complicated. This booklet is a toolkit

Your home loan toolkit A step-by-step guide Consumer Financial Protection Bureau Page 1 How can this toolkit help you? Buying a home is exciting and, let s face it, complicated. This booklet is a toolkit

Closing Disclosure Form

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Closing Information Transaction Information Loan Information KRISTINE GERMOLAI 132 PHILIP STREET HOLBROOK, NY PLAZA HOME MORTGAGE INC NO NO + -

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET. Christopher W. Smart

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET Christopher W. Smart Introduction and Background Residential mortgage lenders have long been required to disclose to their

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET Christopher W. Smart Introduction and Background Residential mortgage lenders have long been required to disclose to their

Loan Estimates. with the following requirements: Estimate SMF SMF SMF

Loan Estimates with the following requirements: Estimate SMF SMF SMF Please follow the directions below when completing the Initial Loan Application and Disclosure processes. e e cc e and Locked LE, including

Loan Estimates with the following requirements: Estimate SMF SMF SMF Please follow the directions below when completing the Initial Loan Application and Disclosure processes. e e cc e and Locked LE, including

2014 Freddie Mac and Fannie Mae. All Rights Reserved. MISMO is a registered trademark of the Mortgage Industry Standards Maintenance Organization.

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Closing Disclosure with Numbers Purchase Transaction Document Version 1.1 July 15, 2014 In support of the Integrated

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Closing Disclosure with Numbers Purchase Transaction Document Version 1.1 July 15, 2014 In support of the Integrated

FINALLY HERE TILA-RESPA INTEGRATED DISCLOSURE FORMS

TRIPLE PLAY CONVENTION FINALLY HERE TILA-RESPA INTEGRATED DISCLOSURE FORMS December 7, 2015 Phillip L. Schulman K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 phil.schulman@klgates.com

TRIPLE PLAY CONVENTION FINALLY HERE TILA-RESPA INTEGRATED DISCLOSURE FORMS December 7, 2015 Phillip L. Schulman K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 phil.schulman@klgates.com

TRID. Quick Compliance Guide T I L A-RESPA INTEGRAT E D DISCLOSURES Temenos USA. All rights reserved

TRID T I L A-RESPA INTEGRAT E D DISCLOSURES Quick Compliance Guide 09.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636 e: usainfo@temenos.com While the publisher and

TRID T I L A-RESPA INTEGRAT E D DISCLOSURES Quick Compliance Guide 09.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636 e: usainfo@temenos.com While the publisher and

Loan Estimate $ NO. Loan Terms. Loan Amount $ NO. Interest Rate 1.75% NO

Pennsylvania Housing Finance Agency 211 N. Front Street Harrisburg, PA 17101 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate DATE ISSUED APPLICANTS PROPERTY PROP. VALUE LOAN

Pennsylvania Housing Finance Agency 211 N. Front Street Harrisburg, PA 17101 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate DATE ISSUED APPLICANTS PROPERTY PROP. VALUE LOAN

Comment Call (12-14)

") Comment Call (12-14) To: From: All Affiliated Credit Union CEOs Veronica Madsen Director of Regulatory Affairs Date: August 28, 2012 RE: CFPB Combined TILA/RESPA Disclosures Summary The Dodd-Frank Wall

Comment Call (12-14) To: From: All Affiliated Credit Union CEOs Veronica Madsen Director of Regulatory Affairs Date: August 28, 2012 RE: CFPB Combined TILA/RESPA Disclosures Summary The Dodd-Frank Wall

2014 Freddie Mac and Fannie Mae. All Rights Reserved. MISMO is a registered trademark of the Mortgage Industry Standards Maintenance Organization.

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Closing Disclosure with Numbers Non-Seller Transaction Document Version 1.1 July 15, 2014 In support of the

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Closing Disclosure with Numbers Non-Seller Transaction Document Version 1.1 July 15, 2014 In support of the

Integrated Disclosure Vocabulary List. Term Definition as of 8/1/2015 Adjustments and Other Credits

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Sample Closing Disclosures with Reference Numbers

Specification Issued by Fannie Mae and Freddie Mac Appendix C: Sample Closing Disclosures with Reference Numbers") Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Sample Closing Disclosures with Numbers Document Version 1.5 June 06, 2017 In support of the Integrated Mortgage

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Sample Closing Disclosures with Numbers Document Version 1.5 June 06, 2017 In support of the Integrated Mortgage

TRID. Acceptable Broker Submissions Booklet WHSL EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471

TRID Acceptable Broker Submissions Booklet EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471 WHSL-0022-1015 As Fremont Bank transitions to the new Rule, our goal is to make the submission of your loan applications

TRID Acceptable Broker Submissions Booklet EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471 WHSL-0022-1015 As Fremont Bank transitions to the new Rule, our goal is to make the submission of your loan applications

THE CLOSING DISCLOSURE

THE CLOSING DISCLOSURE Coverage: Most Closed-End Consumer Mortgages Not HELOCs, reverse mortgages or mobile home loans not attached to real property Agency/Citation: Consumer Financial Protection Bureau

THE CLOSING DISCLOSURE Coverage: Most Closed-End Consumer Mortgages Not HELOCs, reverse mortgages or mobile home loans not attached to real property Agency/Citation: Consumer Financial Protection Bureau

Notice Regarding Updated Regulations and Summary of Recent CFPB Mortgage Rules

April 23, 2012 Notice Regarding Updated Regulations and Summary of Recent CFPB Mortgage Rules The Consumer Financial Protection Bureau ( CFPB or Bureau ) recently issued final rules related to mortgage

April 23, 2012 Notice Regarding Updated Regulations and Summary of Recent CFPB Mortgage Rules The Consumer Financial Protection Bureau ( CFPB or Bureau ) recently issued final rules related to mortgage

TRID October 3, 2015!

TRID October 3, 2015! Purpose This announcement includes the following topics: Consumer Financial Protection Bureau (CFPB), Truth-in-Lending and RESPA Integrated Disclosures (TRID). Policy It is MSI Policy

TRID October 3, 2015! Purpose This announcement includes the following topics: Consumer Financial Protection Bureau (CFPB), Truth-in-Lending and RESPA Integrated Disclosures (TRID). Policy It is MSI Policy

TILA/RESPA Integrated Disclosure Rule

TILA/RESPA Integrated Disclosure Rule Solving the Puzzle July 22, 2015 Presented by: Gary D. Clark, CMB Chief Operating Officer Sierra Pacific Mortgage Webinar All lines will be muted You can type your

TILA/RESPA Integrated Disclosure Rule Solving the Puzzle July 22, 2015 Presented by: Gary D. Clark, CMB Chief Operating Officer Sierra Pacific Mortgage Webinar All lines will be muted You can type your

21 Closings THE CLOSING EVENT

21 Closings The Closing Event Real Estate Settlement Procedures Act Financial Settlement of the Transaction Computing Prorations Taxes Due at Closing Closing Cost Calculations: Case Study TILA/RESPA Integrated

21 Closings The Closing Event Real Estate Settlement Procedures Act Financial Settlement of the Transaction Computing Prorations Taxes Due at Closing Closing Cost Calculations: Case Study TILA/RESPA Integrated

CFPB Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

The TILA-RESPA Integrated Disclosure (TRID) Rule. Compiled by: 110 Title, LLC

Rule. Compiled by: 110 Title, LLC") The TILA-RESPA Integrated Disclosure (TRID) Rule Compiled by: 110 Title, LLC 1 I. Introductory Note The Dodd-Frank Wall Street Reform Act and Consumer Protection Act of 2010 (Dodd-Frank), ushered in the

The TILA-RESPA Integrated Disclosure (TRID) Rule Compiled by: 110 Title, LLC 1 I. Introductory Note The Dodd-Frank Wall Street Reform Act and Consumer Protection Act of 2010 (Dodd-Frank), ushered in the

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) General 1) Q: When does the new RESPA Rule take effect? A: The November 2008 RESPA Rule was effective January 16, 2009. Implementation of the provisions are

New RESPA Rule FAQs (New items are in bold) General 1) Q: When does the new RESPA Rule take effect? A: The November 2008 RESPA Rule was effective January 16, 2009. Implementation of the provisions are

The TILA-RESPA Integrated Disclosures Rule consolidates. Estimate (GFE) into the Loan Estimate and. the Closing Disclosure

into the Loan Estimate and. the Closing Disclosure") Agenda This training consists of three parts explaining the general requirements of the law that consolidated multiple disclosures into two separate forms; the Loan Estimate and the Closing Disclosure:

Agenda This training consists of three parts explaining the general requirements of the law that consolidated multiple disclosures into two separate forms; the Loan Estimate and the Closing Disclosure:

Closing Disclosure August 1, CFR

Closing Disclosure August 1, 2015 12 CFR 1026.38 Agent Questions for Lender Clients Who will prepare the Closing Disclosure (CD) Form? How will Agents coordinate with the lender to prepare the Closing

Closing Disclosure August 1, 2015 12 CFR 1026.38 Agent Questions for Lender Clients Who will prepare the Closing Disclosure (CD) Form? How will Agents coordinate with the lender to prepare the Closing

What is T.R.I.D TILA-RESPA Integrated Disclosure

T.R.I.D. What is T.R.I.D TILA-RESPA Integrated Disclosure The CFPB has issued a rule that is aimed to simplify and improve disclosure forms for mortgage transactions. The rule replaces the current forms

T.R.I.D. What is T.R.I.D TILA-RESPA Integrated Disclosure The CFPB has issued a rule that is aimed to simplify and improve disclosure forms for mortgage transactions. The rule replaces the current forms

CFPB: The New Closing Process

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 (CFPB revised date: October 3, 2015) INTRODUCTION

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 (CFPB revised date: October 3, 2015) INTRODUCTION

Interagency Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

RESPA REFORM TRAINING Effective January 1, FOR MORTGAGE PROFESSIONALS ONLY Rev 1, 12/29/09

RESPA REFORM TRAINING Effective January 1, 2010 OVERVIEW In November 2008, HUD published its final rule amending Regulation X of the Real Estate Settlement Procedures Act (RESPA). The final rule includes

RESPA REFORM TRAINING Effective January 1, 2010 OVERVIEW In November 2008, HUD published its final rule amending Regulation X of the Real Estate Settlement Procedures Act (RESPA). The final rule includes

HERE S. TRID. ROBERT E. PINDER (904) ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015

ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015") HERE S. TRID ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015 ROBERT E. PINDER rpinder@rtlaw.com (904) 346-5551 HERE S. TRID 2 COUNTDOWN TO TRID TRID Goes into Effect

HERE S. TRID ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015 ROBERT E. PINDER rpinder@rtlaw.com (904) 346-5551 HERE S. TRID 2 COUNTDOWN TO TRID TRID Goes into Effect

Guidance for Completing the 2010 Good Faith Estimate

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Guidance for Completing the 2010 Good Faith Estimate

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Loan Comparison Report. Sample

Loan Comparison Report Prepared for: Jonny Williams Date: Prepared by: April 14, 2008 Taylor Abegg Phone: 801-225-4120 E-mail: TJAbegg@EverySingleHome.com Dear Jonny Williams Attached is the Loan Comparison

Loan Comparison Report Prepared for: Jonny Williams Date: Prepared by: April 14, 2008 Taylor Abegg Phone: 801-225-4120 E-mail: TJAbegg@EverySingleHome.com Dear Jonny Williams Attached is the Loan Comparison

The new Loan Estimate Form integrates and replaces the existing RESPA Good Faith Estimate and the initial Truth in Lending forms.

The Consumer Financial Protection Bureau s (CFPB) integrated mortgage disclosure rule will be effective August 1, 2015. This rule consolidates four existing disclosures required under Truth-in-Lending

The Consumer Financial Protection Bureau s (CFPB) integrated mortgage disclosure rule will be effective August 1, 2015. This rule consolidates four existing disclosures required under Truth-in-Lending

The WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms

The WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Holly Spencer Bunting K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 holly.bunting@klgates.com Phillip

The WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Holly Spencer Bunting K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 holly.bunting@klgates.com Phillip

TRID Audit 5: Cash-to-Close and Loan Calculations

ABA BRIEFING PARTICIPANT S GUIDE TRID Audit 5: Cash-to-Close and Loan Calculations Tuesday, October 18, 2016 Eastern Time 2:00 p.m. 4:00 p.m. Central Time 1:00 p.m. 3:00 p.m. Mountain Time 12:00 p.m. 2:00p.m.

ABA BRIEFING PARTICIPANT S GUIDE TRID Audit 5: Cash-to-Close and Loan Calculations Tuesday, October 18, 2016 Eastern Time 2:00 p.m. 4:00 p.m. Central Time 1:00 p.m. 3:00 p.m. Mountain Time 12:00 p.m. 2:00p.m.

Understanding CFPB Rules CONSUMER FINANCIAL PROTECTION BUREAU

Understanding CFPB Rules CONSUMER FINANCIAL PROTECTION BUREAU The Consumer Financial Protection Bureau The CFPB is a new federal agency Created by Dodd Frank Wall Street and Consumer Protection Act Dodd

Understanding CFPB Rules CONSUMER FINANCIAL PROTECTION BUREAU The Consumer Financial Protection Bureau The CFPB is a new federal agency Created by Dodd Frank Wall Street and Consumer Protection Act Dodd

RESPA/TILA Integration

RESPA/TILA Integration 1 Presented by: Richard Hogan, Vice President & Associate General Counsel Tracy Pandolfo, Director Agent Services Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

RESPA/TILA Integration 1 Presented by: Richard Hogan, Vice President & Associate General Counsel Tracy Pandolfo, Director Agent Services Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

The New Mortgage Disclosure Forms: Know the Rule

The New Mortgage Disclosure Forms: Know the Rule 10:15 11:15 a.m. Phillip L. Schulman, Esq., Partner, K&L Gates LLP THE WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Phillip

The New Mortgage Disclosure Forms: Know the Rule 10:15 11:15 a.m. Phillip L. Schulman, Esq., Partner, K&L Gates LLP THE WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Phillip

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

Closing Disclosure $ NO $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 1/6/2016 Closing Date 1/19/2016 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 1/6/2016 Closing Date 1/19/2016 Disbursement

Executive Summary of the 2017 TILA- RESPA Rule

1700 G Street NW, Washington, DC 20552 July 7, 2017 Executive Summary of the 2017 TILA- RESPA Rule On July 7, 2017, the Consumer Financial Protection Bureau (Bureau) issued a final rule (2017 TILA-RESPA

1700 G Street NW, Washington, DC 20552 July 7, 2017 Executive Summary of the 2017 TILA- RESPA Rule On July 7, 2017, the Consumer Financial Protection Bureau (Bureau) issued a final rule (2017 TILA-RESPA

TRID TILA RESPA Integrated Disclosures. Presented by David Luna

TRID TILA RESPA Integrated Disclosures Presented by David Luna Thank you I d like to thank the many sources of information: the Attorney s, Creditors, Title, Credit providers and the CFPB for the information

TRID TILA RESPA Integrated Disclosures Presented by David Luna Thank you I d like to thank the many sources of information: the Attorney s, Creditors, Title, Credit providers and the CFPB for the information

TILA-RESPA Integrated Disclosure rule

May 2018 TILA-RESPA Integrated Disclosure rule Small entity compliance guide Guide for creating on-brand reports Version Log The Bureau updates this Guide on a periodic basis to reflect finalized clarifications

May 2018 TILA-RESPA Integrated Disclosure rule Small entity compliance guide Guide for creating on-brand reports Version Log The Bureau updates this Guide on a periodic basis to reflect finalized clarifications

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules Covered Transactions Exemptions Title of Instructions for completion of Delivery of Electronic delivery Federally

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules Covered Transactions Exemptions Title of Instructions for completion of Delivery of Electronic delivery Federally

Advertising, Consumer protection, Credit, Credit unions, Mortgages, National banks,

12 CFR part 1026 Advertising, Consumer protection, Credit, Credit unions, Mortgages, National banks, Recordkeeping and recordkeeping requirements, Reporting, Savings associations, Truth in lending. Authority

12 CFR part 1026 Advertising, Consumer protection, Credit, Credit unions, Mortgages, National banks, Recordkeeping and recordkeeping requirements, Reporting, Savings associations, Truth in lending. Authority

Our Industry Today TRID AND BEYOND. RDH Education Services. Presented by RDH Education Services

RDH Education Services Our Industry Today TRID AND BEYOND Presented by RDH Education Services RDH Education Services can be contacted at: 4361 Technology Dr, Unit A, Livermore, CA 94551 877-734-4347 info@rdheducation.com

RDH Education Services Our Industry Today TRID AND BEYOND Presented by RDH Education Services RDH Education Services can be contacted at: 4361 Technology Dr, Unit A, Livermore, CA 94551 877-734-4347 info@rdheducation.com

Closing Disclosure $ NO $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 1/6/2016 Closing Date 1/19/2016 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 1/6/2016 Closing Date 1/19/2016 Disbursement

What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule.

Rule.") What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule Presented by Overview Know Before You Owe (the TILA RESPA Integrated Disclosure (TRID)

What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule Presented by Overview Know Before You Owe (the TILA RESPA Integrated Disclosure (TRID)

TILA / RESPA Integration

The Times, They Are A-Changing (Again)! presented by Jack Konyk Executive Director, Government Affairs OwnOK The Future of Oklahoma Real Estate Feb. 12, 2015 Petroleum Club Oklahoma City, OK 2 Upcoming

The Times, They Are A-Changing (Again)! presented by Jack Konyk Executive Director, Government Affairs OwnOK The Future of Oklahoma Real Estate Feb. 12, 2015 Petroleum Club Oklahoma City, OK 2 Upcoming

Compliance Update - ACUIA. Presented by:

Compliance Update - ACUIA Presented by: Mike Carter Director of Compliance September 30 th, 2014 Topics Discussion of the CFPB Mortgage Rules TILA/RESPA Rule Flood Insurance CUSO Rule Regulation CC Proposal

Compliance Update - ACUIA Presented by: Mike Carter Director of Compliance September 30 th, 2014 Topics Discussion of the CFPB Mortgage Rules TILA/RESPA Rule Flood Insurance CUSO Rule Regulation CC Proposal

The CFPB s New Mortgage Disclosures

The CFPB s New Mortgage Disclosures Benjamin K. Olson March 10, 2015 Key Changes Effective August 1, 2015: GFE and initial TIL replaced with the Loan Estimate The items constituting an application are

The CFPB s New Mortgage Disclosures Benjamin K. Olson March 10, 2015 Key Changes Effective August 1, 2015: GFE and initial TIL replaced with the Loan Estimate The items constituting an application are

TILA-RESPA Integrated Disclosures (TRID) FAQs

FAQs") TILA-RESPA Integrated Disclosures (TRID) FAQs On July 21, 2015, the Consumer Financial Protection Bureau (CFPB) published the final rule to delay the effective date of the TILA-RESPA Integrated Disclosure

TILA-RESPA Integrated Disclosures (TRID) FAQs On July 21, 2015, the Consumer Financial Protection Bureau (CFPB) published the final rule to delay the effective date of the TILA-RESPA Integrated Disclosure

Good Faith Estimate Training 2/3/14

Good Faith Estimate Training 2/3/14 Objectives At the end of this training you will be able to: Understand RESPA Reform Recognize a complete Loan Application Understand GFE requirements Know requirements

Good Faith Estimate Training 2/3/14 Objectives At the end of this training you will be able to: Understand RESPA Reform Recognize a complete Loan Application Understand GFE requirements Know requirements

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE January 1, 2018 In case of any queries regarding the information available in this guide, please reach us at qmteam@swmc.com. Sun West Mortgage Company, Inc.

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE January 1, 2018 In case of any queries regarding the information available in this guide, please reach us at qmteam@swmc.com. Sun West Mortgage Company, Inc.

Reasons for Change. Are You Ready for the Regulation Z & RESPA Changes. Past, Present & Future Changes

Are You Ready for the Regulation Z & RESPA Changes Community Bankers Association of Illinois Annual Convention September 26, 2009 Presented by: Young & Associates, Inc. 1 Past, Present & Future Changes

Are You Ready for the Regulation Z & RESPA Changes Community Bankers Association of Illinois Annual Convention September 26, 2009 Presented by: Young & Associates, Inc. 1 Past, Present & Future Changes

REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY

POLICY") I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

THIS IS NOT LEGAL ADVICE

I. Ability to Repay (ATR) Qualified Mortgage (QM) Overview In 2008 the Board of Governors of the Federal Reserve System adopted a rule under the Truth in Lending Act prohibiting creditors from making higher-priced

I. Ability to Repay (ATR) Qualified Mortgage (QM) Overview In 2008 the Board of Governors of the Federal Reserve System adopted a rule under the Truth in Lending Act prohibiting creditors from making higher-priced

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview Disclaimer Information included is intended for general information purposes only and is current as October 2, 2015. It should not

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview Disclaimer Information included is intended for general information purposes only and is current as October 2, 2015. It should not

Ability to Repay / Qualified Mortgages Frequently Asked Questions January 15, 2014

Q: Which transactions are covered and excluded? Covered transactions - First liens - Fixed Seconds - Refinances Excluded transactions Home Equity Line of Credit loans (HELOCs) Interest-only (QM) Transactions

Q: Which transactions are covered and excluded? Covered transactions - First liens - Fixed Seconds - Refinances Excluded transactions Home Equity Line of Credit loans (HELOCs) Interest-only (QM) Transactions

2013 Home Ownership and Equity Protection Act (HOEPA) Rule Guide

Rule Guide") March 2016 2013 Home Ownership and Equity Protection Act (HOEPA) Rule Guide Small entity compliance guide Version Log The Bureau updates this guide on a periodic basis to reflect finalized clarifications