The new Loan Estimate Form integrates and replaces the existing RESPA Good Faith Estimate and the initial Truth in Lending forms.

|

|

|

- Alvin Bradley

- 5 years ago

- Views:

Transcription

1

2 The Consumer Financial Protection Bureau s (CFPB) integrated mortgage disclosure rule will be effective August 1, This rule consolidates four existing disclosures required under Truth-in-Lending (TILA) and the Real Estate Settlement Procedures Act (RESPA) for transactions secured by real estate into two forms: The new Loan Estimate Form integrates and replaces the existing RESPA Good Faith Estimate and the initial Truth in Lending forms. The new Closing Disclosure Form integrates and replaces the existing RESPA HUD- 1 and the final Truth in Lending forms. Lender Loan Estimate basic disclosure requirements: Required to provide a Loan Estimate within 3 business days of a loan application. If loan is locked after initial Loan Estimate is provided, a new Loan Estimate must be provided within 3 Business Days. Revised Loan Estimates require a 4 day waiting period. Borrower must receive the new disclosure at least 4 days before closing. Lender Closing Disclosure basic requirements: Must be received by consumer at least 3 business days before closing. Must be given to each consumer who has the right of rescission if a rescindable transaction (such as a refinance transaction). If a revised loan Closing Disclosure is issued, it may trigger a new 3 day waiting period. The instances where this might occur are: o The disclosed APR becomes inaccurate. o There are changes to the loan product. o A prepayment penalty is added or amended. The state contracted exam vendor (PSI) will be incorporating the new material into the broker examinations in August As such, all education providers offering the broker pre-licensing program will need to incorporate the new disclosures into their education content and adjust accordingly with the new forms. Please review the attached document with regards to the new disclosures. If you have any questions, please don t hesitate to contact the Division.

3 Changes to the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA) better known as the Integrated Disclosures rule become mandatory on August 1, These changes have broad impact to the Real Estate and Mortgage practices. This write-up summarizes those changes which impact the Broker Prelicense education program. Schools should also review and update courses such as the 24 hour Broker Administration, Broker Reactivation, 72 hour and 120 hour licensing courses and the 12 hour attorney course. Impact on State approved Pre-license Course Outline As per the State approved pre-license course outlines, we see the greatest impact on section IV on the National side (Real Estate Law and Practice) entitled Real Estate Finance and Settlement sub-sections B. Lender Requirements, C. Settlement/Closing and D. Settlement Documents and on the State side (Closings) paragraph I. Broker s Responsibility Relating to Closing section. Clean blank and filled-out examples of the new forms may be found at: Although there are variations to these disclosures, the pre-license program will be required to address only the base forms as described in this write-up as excerpted from the TILA-RESPA Integrated Disclosure rule Small Entity Compliance Guide. You will find the TILA-RESPA rule on the Bureau s website at Impact on Licensing Exam Questions based on the old rule have already been removed from the current licensing exam. The National and State licensing exams will be updated to reflect the new information on or about August Integrated Disclosure Rule The following information has been excerpted from the attached TILA-RESPA Integrated Disclosure rule Small Entity Compliance Guide with page references for easy access. Page 11-1 Introduction For more than 30 years, Federal law has required lenders to provide two different disclosure forms to consumers applying for a mortgage. The law also generally has required two different forms at or shortly before closing on the loan. Two different Federal agencies developed these forms separately, under two Federal statutes: the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act of 1974 (RESPA). The information on these forms is overlapping and the language is inconsistent. Consumers often find the forms confusing, and lenders and settlement agents find the forms burdensome to provide and explain. First, the Good Faith Estimate (GFE) and the initial Truth-in-Lending disclosure (initial TIL) have been combined into a new form, the Loan Estimate. (Form H-24). Similar to those forms, the new Loan Estimate form is designed to provide disclosures that will be helpful to consumers in understanding the key features, costs, and risks of the mortgage loan for which they are applying, and must be delivered or mailed to consumers no later than the third business day after they submit a loan application. Second, the HUD-1 and final Truth-in-Lending disclosure (final TIL and, together with the initial TIL, the Truth-in- Lending forms) have been combined into another new form, the Closing Disclosure (Form H-25), which is 1

4 designed to provide disclosures that will be helpful to consumers in understanding all of the costs of the transaction. This form must be provided to consumers at least three business days before consummation of the loan. The forms use clear language and design to make it easier for consumers to locate key information, such as interest rate, monthly payments, and costs to close the loan. The forms also provide more information to help consumers decide whether they can afford the loan and to facilitate comparison of the cost of different loan offers, including the cost of the loans over time. The final rule applies to most closed-end consumer mortgages. It does not apply to home equity lines of credit (HELOCs), reverse mortgages, or mortgages secured by a mobile home or by a dwelling that is not attached to real property (i.e., land). The final rule also does not apply to loans made by persons who are not considered creditors, because they make five or fewer mortgages in a year. The TILA-RESPA rule is effective August 1, Detailed Subsections: PAGE What transactions are covered by the TILA-RESPA rule? The TILA-RESPA rule applies to most closed-end consumer credit transactions secured by real property, but does not apply to: HELOCs; Reverse mortgages; or Chattel-dwelling loans, such as loans secured by a mobile home or by a dwelling that is not attached to real property (i.e., land). Consistent with the current rules under TILA, the rule also does not apply to loans made by a person or entity that makes five or fewer mortgages in a calendar year and thus is not a creditor. There is also a partial exemption for certain transactions associated with housing assistance loan programs for low- and moderate-income consumers. However, certain types of loans that are currently subject to TILA but not RESPA are subject to the TILA-RESPA rule s integrated disclosure requirements, including: Construction-only loans Loans secured by vacant land or by 25 or more acres Credit extended to certain trusts for tax or estate planning purposes also are covered by the TILA-RESPA rule. 2

5 Page What information goes on the Loan Estimate form? The following is a brief, page-by-page overview of the Loan Estimate, generally describing the information creditors are required to disclose. For detailed instructions on the individual fields and calculations for the Loan Estimate, see the Bureau s companion guide, TILA-RESPA Guide to Forms. Page Page 1: General information, loan terms, projected payments, and costs at closing 3

6 4

7 Page 1 of the Loan Estimate includes general information, a Loan Terms table with descriptions of applicable information about the loan, a Projected Payments table, a Costs at Closing table, and a link for consumers to obtain more information about loans secured by real property at a website maintained by the Bureau. 5.5 Page 2: Closing cost details 5

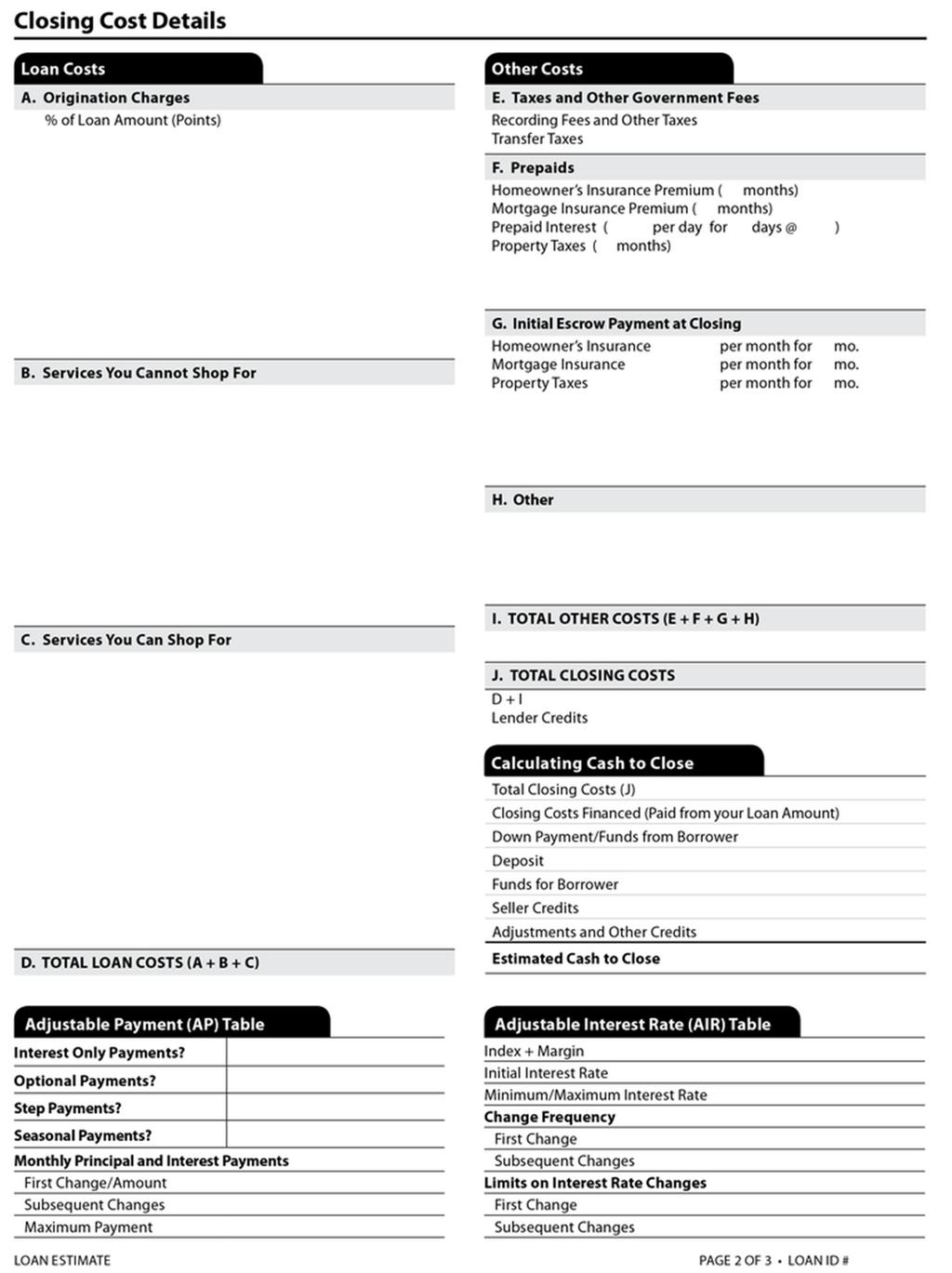

8 6

9 Four main categories of charges are disclosed on page 2 of the Loan Estimate: A good-faith itemization of the Loan Costs and Other Costs associated with the loan. A Calculating Cash to Close table to show the consumer how the amount of cash needed at closing is calculated. For transactions with adjustable monthly payments, an Adjustable Payment (AP) Table with relevant information about how the monthly payments will change. For transactions with adjustable interest rates, an Adjustable Interest Rate (AIR) Table with relevant information about how the interest rate will change. The items associated with the mortgage are broken down into two general types, Loan Costs and Other Costs. Generally, Loan Costs are those costs paid by the consumer to the creditor and third-party providers of services the creditor requires to be obtained by the consumer during the origination of the loan. Other Costs include taxes, governmental recording fees, and certain other payments involved in the real estate closing process. These two tables are further broken down, as discussed below. Items that are a component of title insurance must include the introductory description of Title. If State law requires additional disclosures, those additional disclosures may be made on a document whose pages are separate from, and not presented as part of, the Loan Estimate. 5.6 Page 3: Additional information about the loan Page 3 of the Loan Estimate contains Contact information, a Comparisons table, an Other Considerations table, and, if desired, a Signature Statement for the consumer to sign to acknowledge receipt. 7

10 8

11 Page What are the general timing and delivery requirements for the Loan Estimate disclosure? Generally, the creditor is responsible for ensuring that it delivers or places in the mail the Loan Estimate form no later than the third business day after receiving the consumer s application. The Loan Estimate must also be delivered or placed in the mail no later than the seventh business day before consummation of the transaction. The creditor also is responsible for ensuring that the Loan Estimate and its delivery meet the content, delivery, and timing requirements discussed in sections 5, 6, 7, 8, and 9 of this guide. Page What is considered a business day under the requirements for provision of the Loan Estimate? For purposes of providing the Loan Estimate, a business day is a day on which the creditor s offices are open to the public for carrying out substantially all of its business functions. Note that the term business day is defined differently for other purposes; including counting days to ensure the consumer receives the Closing Disclosure on time. For these other purposes, business day means all calendar days except Sundays and the legal public holidays specified in 5 U.S.C. 6103(a), such as New Year s Day, the Birthday of Martin Luther King, Jr., Washington s Birthday, Memorial Day, Independence Day, Labor Day, Columbus Day, Veterans Day, Thanksgiving Day, and Christmas Day. Page What is the general accuracy requirement for the Loan Estimate disclosures Creditors are responsible for ensuring that the figures stated in the Loan Estimate are made in good faith and consistent with the best information reasonably available to the creditor at the time they are disclosed. Whether or not a Loan Estimate was made in good faith is determined by calculating the difference between the estimated charges originally provided in the Loan Estimate and the actual charges paid by or imposed on the consumer in the Closing Disclosure. Generally, if the charge paid by or imposed on the consumer exceeds the amount originally disclosed on the Loan Estimate it is not in good faith, regardless of whether the creditor later discovers a technical error, miscalculation, or underestimation of a charge. However, a Loan Estimate is considered to be in good faith if the creditor charges the consumer less than the amount disclosed on the Loan Estimate, without regard to any tolerance limitations. Page What charges may change without regard to a tolerance limitation? For certain costs or terms, creditors are permitted to charge consumers more than the amount disclosed on the Loan Estimate without any tolerance limitation. These charges are: Prepaid interest; property insurance premiums; amounts placed into an escrow, impound, reserve or similar account. 9

12 For services required by the creditor if the creditor permits the consumer to shop and the consumer selects a third-party service provider not on the creditor s written list of service providers. Charges paid to third-party service providers for services not required by the creditor (may be paid to affiliates of the creditor). However, creditors may only charge consumers more than the amount disclosed when the original estimated charge, or lack of an estimated charge for a particular service, was based on the best information reasonably available to the creditor at the time the disclosure was provided Page What charges are subject to a 10% cumulative tolerance? Charges for third-party services and recording fees paid by or imposed on the consumer are grouped together and subject to a 10% cumulative tolerance. This means the creditor may charge the consumer more than the amount disclosed on the Loan Estimate for any of these charges so long as the total sum of the charges added together does not exceed the sum of all such charges disclosed on the Loan Estimate by more than 10%. These charges are: Recording fees Charges for third-party services where: The charge is not paid to the creditor or the creditor s affiliate; and The consumer is permitted by the creditor to shop for the third-party service, and the consumer selects a third-party service provider on the creditor s written list of service providers. Page What charges are subject to zero tolerance? For all other charges, creditors are not permitted to charge consumers more than the amount disclosed on the Loan Estimate under any circumstances other than changed circumstances that permit a revised Loan Estimate, as discussed below in section 8.1. These zero tolerance charges are: Fees paid to the creditor, mortgage broker, or an affiliate of either Fees paid to an unaffiliated third party if the creditor did not permit the consumer to shop for a third party service provider for a settlement service; or Transfer taxes. Page What must creditors do when the amounts paid exceed the amounts disclosed on the Loan Estimate beyond the applicable tolerance thresholds? If the amounts paid by the consumer at closing exceed the amounts disclosed on the Loan Estimate beyond the applicable tolerance threshold, the creditor must refund the excess to the consumer no later than 60 calendar days after consummation. For charges subject to zero tolerance, any amount charged beyond the amount disclosed on the Loan Estimate must be refunded to the consumer. 10

13 For charges subject to a 10% cumulative tolerance, to the extent the total sum of the charges added together exceeds the sum of all such charges disclosed on the Loan Estimate by more than 10%, the difference must be refunded to the consumer. Page When are revisions or corrections permitted for Loan Estimates? Creditors generally are bound by the Loan Estimate provided within three business days of the application, and may not issue revisions to Loan Estimates because they later discover technical errors, miscalculations, or underestimations of charges. Creditors are permitted to provide to the consumer revised Loan Estimates (and use them to compare estimated amounts to amounts actually charged for purposes of determining good faith) only in certain specific circumstances: Changed circumstances that occur after the Loan Estimate is provided to the consumer causes estimated settlement charges to increase more than is permitted under the TILA-RESPA rule Changed circumstances that occur after the Loan Estimate is provided to the consumer affect the consumer s eligibility for the terms for which the consumer applied or the value of the security for the loan Revisions to the credit terms or the settlement are requested by the consumer The interest rate was not locked when the Loan Estimate was provided, and locking the rate causes the points or lender credits disclosed on the Loan Estimate to change The consumer indicates an intent to proceed with the transaction more than 10 business days after the Loan Estimate was originally provided or The loan is a new construction loan, and settlement is delayed by more than 60 calendar days, if the original Loan Estimate states clearly and conspicuously that at any time prior to 60 calendar days before consummation, the creditor may issue revised disclosures. Page Are there any restrictions on how many days before consummation a revised Loan Estimate may be provided? Yes. The creditor may not provide a revised Loan Estimate on or after the date it provides the Closing Disclosure. The creditor must ensure that the consumer receives the revised Loan Estimate no later than four business days prior to consummation. If the creditor is mailing the revised Loan Estimate and relying upon the 3 business day mailbox rule, the creditor would need to place in the mail the Loan Estimate no later than seven business days before consummation of the transaction to allow 3 business days for receipt As discussed in section 11.2 below regarding the Closing Disclosure, when a revised Loan Estimate is provided in person, it is considered received by the consumer on the day it is provided. If it is mailed or delivered electronically, the consumer is considered to have received it three business days after it is delivered or placed in the mail. However, if the creditor has evidence that the consumer received the revised Loan Estimate earlier than three business days after it is mailed or delivered, it may rely on that evidence and consider it to be received on that date. 11

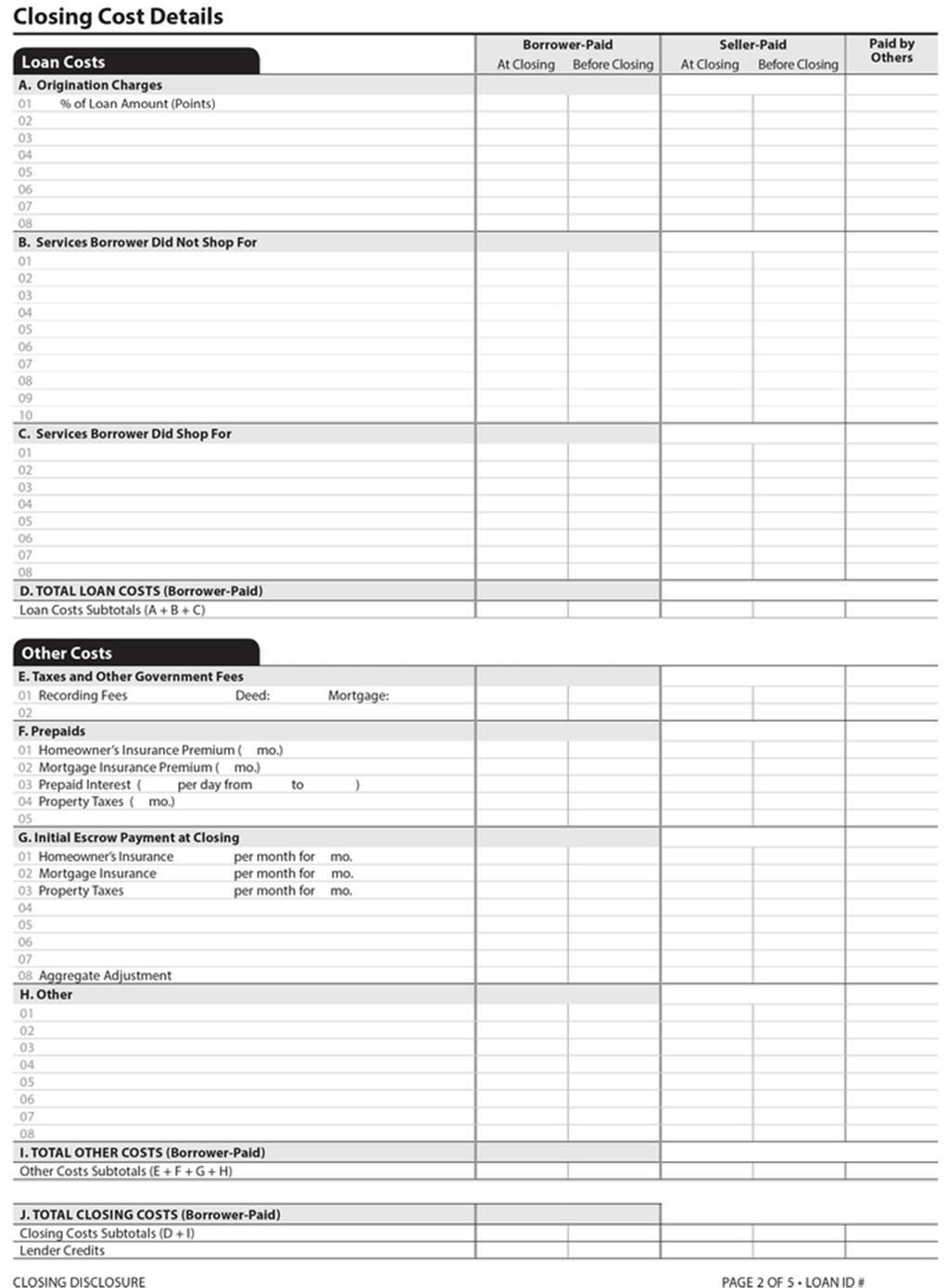

14 9.5 What if a changed circumstance occurs too close to consummation for the creditor to provide a revised Loan Estimate? If there are less than four business days in between the time a the revised Loan Estimate would have been required to be provided to the consumer and consummation, creditors may provide consumers with a Closing Disclosure reflecting any revised charges resulting from the changed circumstance and rely on those figures (rather than the amounts disclosed on the Loan Estimate) for purposes of determining good faith and the applicable tolerance. If the changed circumstance or other triggering event occurs between the fourth and third business days from consummation, the creditor may reflect the revised charges on the Closing Disclosure provided to the consumer three business days before consummation. If the event occurs after the first Closing Disclosure has been provided to the consumer (i.e., within the three-business-day waiting period before consummation), the creditor may use revised charges on the Closing Disclosure provided to the consumer at consummation, and compare those amounts to the amounts charged for purposes of determining good faith and tolerance. Closing Disclosures Page What are the general requirements for the Closing Disclosure? For loans that require a Loan Estimate and that proceed to closing, creditors must provide a new final disclosure reflecting the actual terms of the transaction called the Closing Disclosure. The form integrates and replaces the existing HUD-1 and the final TIL disclosure for these transactions. The creditor is generally required to ensure that the consumer receives the Closing Disclosure no later than three business days before consummation of the loan. The Closing Disclosure generally must contain the actual terms and costs of the transaction.. Creditors may estimate disclosures using the best information reasonably available when the actual term or cost is not reasonably available to the creditor at the time the disclosure is made. However, creditors must act in good faith and use due diligence in obtaining the information. The creditor normally may rely on the representations of other parties in obtaining the information, including, for example, the settlement agent. The creditor is required to provide corrected disclosures containing the actual terms of the transaction at or before consummation The Closing Disclosure must be in writing and contain the information prescribed in The creditor must disclose only the specific information set forth in (a) through (s), as shown in the Bureau s form in appendix H-25. If the actual terms or costs of the transaction change prior to consummation, the creditor must provide a corrected disclosure that contains the actual terms of the transaction and complies with the other requirements of (f), including the timing requirements, and requirements for providing corrected disclosures due to subsequent changes. 12

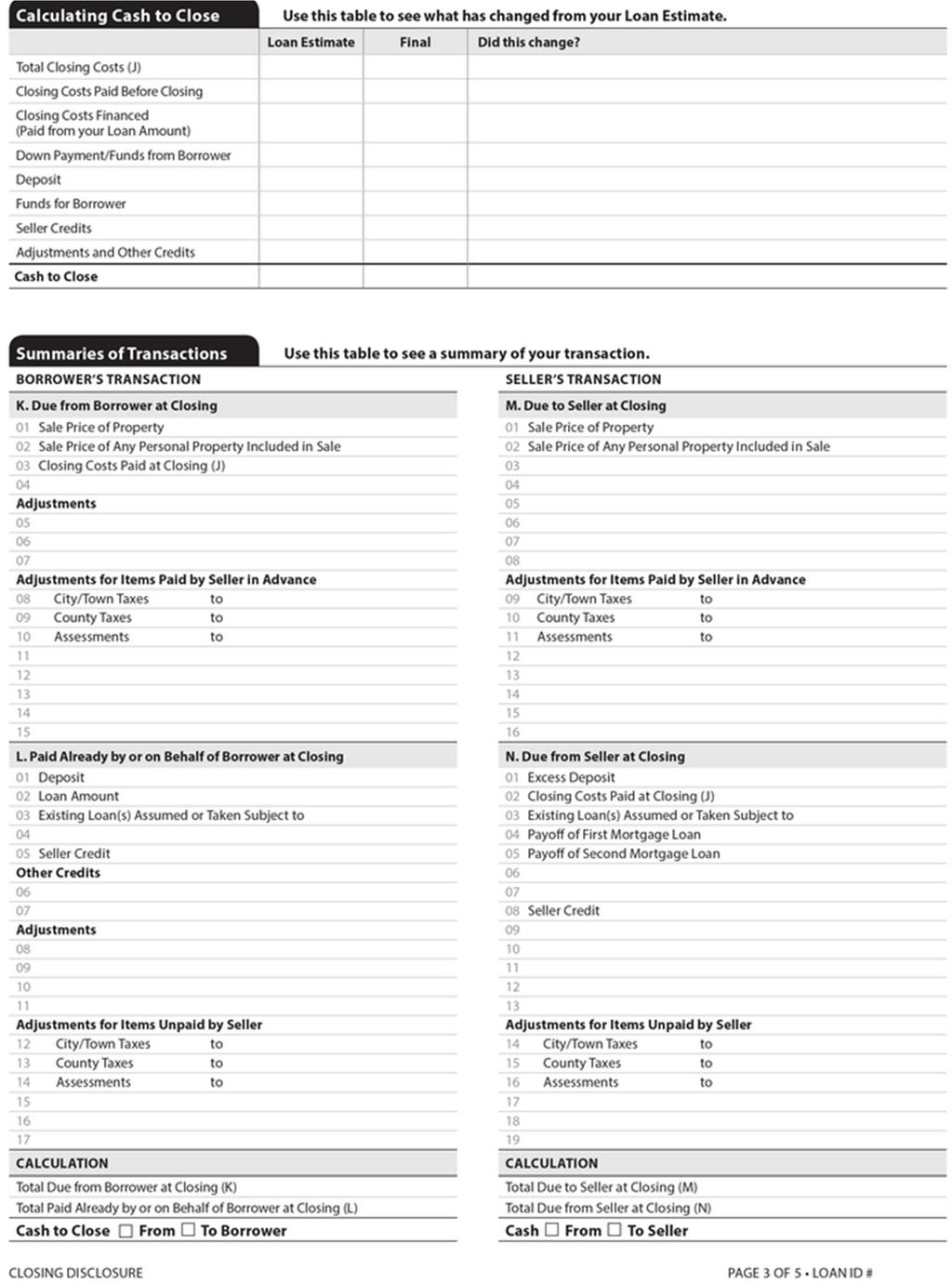

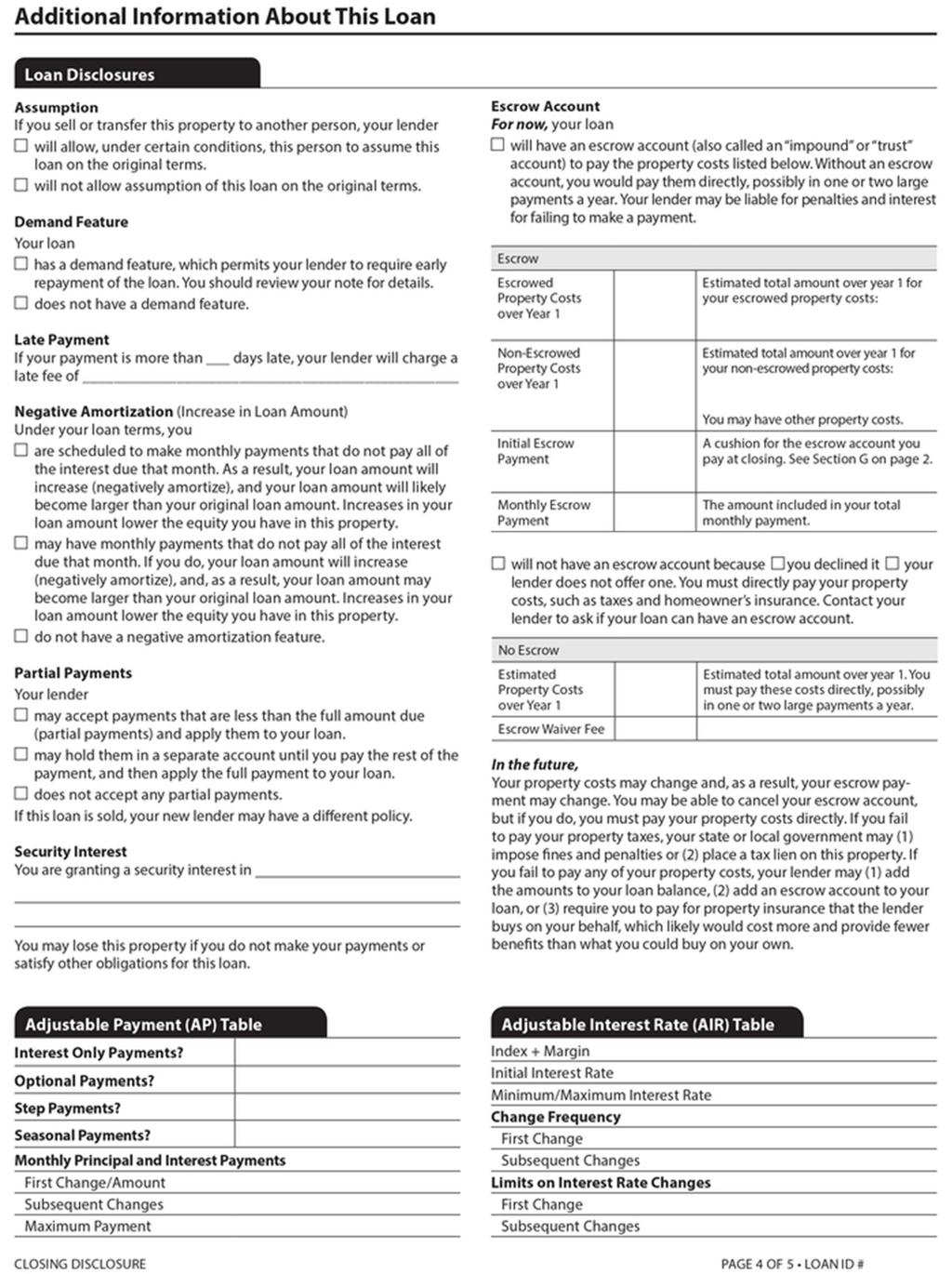

15 New three-day waiting period. If the creditor provides a corrected disclosure, it may also be required to provide the consumer with an additional three-business-day waiting period prior to consummation. Page The rule requires creditors to provide the Closing Disclosure three business days before consummation. Is consummation the same thing as closing or settlement? No, consummation may commonly occur at the same time as closing or settlement, but it is a legally distinct event. Consummation occurs when the consumer becomes contractually obligated to the creditor on the loan, not, for example, when the consumer becomes contractually obligated to a seller on a real estate transaction. The point in time when a consumer becomes contractually obligated to the creditor on the loan depends on applicable State law. Creditors and settlement agents should verify the applicable State laws to determine when consummation will occur, and make sure delivery of the Closing Disclosure occurs at least three business days before this event. Page What information goes on the Closing Disclosure form? The following is a brief, page-by-page overview of the Closing Disclosure form. For detailed instructions on how to determine the contents of each of these fields, see the TILA-RESPA Guide to Forms. 13

16 14

17 15

18 16

19 17

20 18

21 Page What are the general timing and delivery requirements for the Closing Disclosure? Generally, the creditor is responsible for ensuring that the consumer receives the Closing Disclosure form no later than three business days before consummation The creditor also is responsible for ensuring that the Closing Disclosure meets the content, delivery, and timing requirements discussed in sections 10, 11, and 12 of this guide. Page May a consumer waive the three-business-day waiting period? Yes. Like the seven-business-day waiting period after receiving the Loan Estimate (see section 9.6), consumers may waive or modify the three-business-day waiting period when: The extension of credit is needed to meet a bona fide personal financial emergency The consumer has received the Closing Disclosure; and The consumer gives the creditor a dated written statement that describes the emergency, specifically modifies or waives the waiting period, and bears the signature of all consumers who are primarily liable on the legal obligation. The creditor is prohibited from providing the consumer with a pre-printed waiver form. Page Does the three-business-day waiting period apply when corrected Closing Disclosures must be issued to the consumer? Yes, in some circumstances. The three-business-day waiting period requirement applies to a corrected Closing Disclosure that is provided when there are: Changes to the loan s APR; Changes to the loan product; or The addition of a prepayment penalty. If other types of changes occur, creditors must ensure that the consumer receives a corrected Closing Disclosure at or before consummation. Page When must the settlement agent provide the Closing Disclosure to the seller? The settlement agent must provide the seller its copy of the Closing Disclosure no later than the day of consummation. 19

NEW INTEGRATED DISCLOSURES EFFECTIVE AUGUST 1, May 7, 2015

NEW INTEGRATED DISCLOSURES EFFECTIVE AUGUST 1, 2015 from a program presentation made by Nellie Woodward at the Texas Land and Mortgage/TLDA membership meeting held on May 7, 2015 The following BRIEFLY

NEW INTEGRATED DISCLOSURES EFFECTIVE AUGUST 1, 2015 from a program presentation made by Nellie Woodward at the Texas Land and Mortgage/TLDA membership meeting held on May 7, 2015 The following BRIEFLY

What is T.R.I.D TILA-RESPA Integrated Disclosure

T.R.I.D. What is T.R.I.D TILA-RESPA Integrated Disclosure The CFPB has issued a rule that is aimed to simplify and improve disclosure forms for mortgage transactions. The rule replaces the current forms

T.R.I.D. What is T.R.I.D TILA-RESPA Integrated Disclosure The CFPB has issued a rule that is aimed to simplify and improve disclosure forms for mortgage transactions. The rule replaces the current forms

THE CLOSING DISCLOSURE

THE CLOSING DISCLOSURE Coverage: Most Closed-End Consumer Mortgages Not HELOCs, reverse mortgages or mobile home loans not attached to real property Agency/Citation: Consumer Financial Protection Bureau

THE CLOSING DISCLOSURE Coverage: Most Closed-End Consumer Mortgages Not HELOCs, reverse mortgages or mobile home loans not attached to real property Agency/Citation: Consumer Financial Protection Bureau

What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule.

Rule.") What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule Presented by Overview Know Before You Owe (the TILA RESPA Integrated Disclosure (TRID)

What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule Presented by Overview Know Before You Owe (the TILA RESPA Integrated Disclosure (TRID)

Delivered in partnership with your local title agency

Delivered in partnership with your local title agency titlesinsured 1.877.439.4910 About this Manual In an effort to provide a thorough condensed training reference, this manual was created based on the

Delivered in partnership with your local title agency titlesinsured 1.877.439.4910 About this Manual In an effort to provide a thorough condensed training reference, this manual was created based on the

The TILA-RESPA Integrated Disclosures Rule consolidates. Estimate (GFE) into the Loan Estimate and. the Closing Disclosure

into the Loan Estimate and. the Closing Disclosure") Agenda This training consists of three parts explaining the general requirements of the law that consolidated multiple disclosures into two separate forms; the Loan Estimate and the Closing Disclosure:

Agenda This training consists of three parts explaining the general requirements of the law that consolidated multiple disclosures into two separate forms; the Loan Estimate and the Closing Disclosure:

TILA-RESPA Integrated Disclosure rule

This guide has been updated to reflect the 2018 TILA-RESPA Rule. However, it has not been updated to reflect the 2017 TILA-RESPA Rule. The 2017 TILA-RESPA rule includes an optional compliance period. During

This guide has been updated to reflect the 2018 TILA-RESPA Rule. However, it has not been updated to reflect the 2017 TILA-RESPA Rule. The 2017 TILA-RESPA rule includes an optional compliance period. During

TILA-RESPA Integrated Disclosure rule

TILA-RESPA Integrated Disclosure rule Small entity compliance guide This guide is current as of the date set forth on the cover page. It has not been updated to reflect the 2017 TILA-RESPA Rule or the

TILA-RESPA Integrated Disclosure rule Small entity compliance guide This guide is current as of the date set forth on the cover page. It has not been updated to reflect the 2017 TILA-RESPA Rule or the

The TILA-RESPA Integrated Disclosure (TRID) Rule. Compiled by: 110 Title, LLC

Rule. Compiled by: 110 Title, LLC") The TILA-RESPA Integrated Disclosure (TRID) Rule Compiled by: 110 Title, LLC 1 I. Introductory Note The Dodd-Frank Wall Street Reform Act and Consumer Protection Act of 2010 (Dodd-Frank), ushered in the

The TILA-RESPA Integrated Disclosure (TRID) Rule Compiled by: 110 Title, LLC 1 I. Introductory Note The Dodd-Frank Wall Street Reform Act and Consumer Protection Act of 2010 (Dodd-Frank), ushered in the

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

Our Industry Today TRID AND BEYOND. RDH Education Services. Presented by RDH Education Services

RDH Education Services Our Industry Today TRID AND BEYOND Presented by RDH Education Services RDH Education Services can be contacted at: 4361 Technology Dr, Unit A, Livermore, CA 94551 877-734-4347 info@rdheducation.com

RDH Education Services Our Industry Today TRID AND BEYOND Presented by RDH Education Services RDH Education Services can be contacted at: 4361 Technology Dr, Unit A, Livermore, CA 94551 877-734-4347 info@rdheducation.com

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview Disclaimer Information included is intended for general information purposes only and is current as October 2, 2015. It should not

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview Disclaimer Information included is intended for general information purposes only and is current as October 2, 2015. It should not

TILA / RESPA Integration

The Times, They Are A-Changing (Again)! presented by Jack Konyk Executive Director, Government Affairs OwnOK The Future of Oklahoma Real Estate Feb. 12, 2015 Petroleum Club Oklahoma City, OK 2 Upcoming

The Times, They Are A-Changing (Again)! presented by Jack Konyk Executive Director, Government Affairs OwnOK The Future of Oklahoma Real Estate Feb. 12, 2015 Petroleum Club Oklahoma City, OK 2 Upcoming

Advertising, Consumer protection, Credit, Credit unions, Mortgages, National banks,

12 CFR part 1026 Advertising, Consumer protection, Credit, Credit unions, Mortgages, National banks, Recordkeeping and recordkeeping requirements, Reporting, Savings associations, Truth in lending. Authority

12 CFR part 1026 Advertising, Consumer protection, Credit, Credit unions, Mortgages, National banks, Recordkeeping and recordkeeping requirements, Reporting, Savings associations, Truth in lending. Authority

CFPB: The New Closing Process

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 (CFPB revised date: October 3, 2015) INTRODUCTION

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 (CFPB revised date: October 3, 2015) INTRODUCTION

TRID. Acceptable Broker Submissions Booklet WHSL EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471

TRID Acceptable Broker Submissions Booklet EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471 WHSL-0022-0116 At Fremont Bank, our goal is to make the submission of your loan applications to us as streamlined

TRID Acceptable Broker Submissions Booklet EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471 WHSL-0022-0116 At Fremont Bank, our goal is to make the submission of your loan applications to us as streamlined

TILA-RESPA Integrated Disclosure rule

May 2018 TILA-RESPA Integrated Disclosure rule Small entity compliance guide Guide for creating on-brand reports Version Log The Bureau updates this Guide on a periodic basis to reflect finalized clarifications

May 2018 TILA-RESPA Integrated Disclosure rule Small entity compliance guide Guide for creating on-brand reports Version Log The Bureau updates this Guide on a periodic basis to reflect finalized clarifications

RESPA/TILA Integration

RESPA/TILA Integration 1 Presented by: Richard Hogan, Vice President & Associate General Counsel Tracy Pandolfo, Director Agent Services Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

RESPA/TILA Integration 1 Presented by: Richard Hogan, Vice President & Associate General Counsel Tracy Pandolfo, Director Agent Services Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

TRID October 3, 2015!

TRID October 3, 2015! Purpose This announcement includes the following topics: Consumer Financial Protection Bureau (CFPB), Truth-in-Lending and RESPA Integrated Disclosures (TRID). Policy It is MSI Policy

TRID October 3, 2015! Purpose This announcement includes the following topics: Consumer Financial Protection Bureau (CFPB), Truth-in-Lending and RESPA Integrated Disclosures (TRID). Policy It is MSI Policy

RESPA/TILA INTEGRATION PART II: CLOSING DISCLOSURE AND ACTION PLAN INCLUDES CLOSING DISCLOSURE TABLE. Jonathan Foxx * WHITE PAPER

RESPA/TILA INTEGRATION PART II: CLOSING DISCLOSURE AND ACTION PLAN INCLUDES CLOSING DISCLOSURE TABLE Jonathan Foxx * WHITE PAPER This second White Paper of a four-part series will introduce and treat the

RESPA/TILA INTEGRATION PART II: CLOSING DISCLOSURE AND ACTION PLAN INCLUDES CLOSING DISCLOSURE TABLE Jonathan Foxx * WHITE PAPER This second White Paper of a four-part series will introduce and treat the

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules Covered Transactions Exemptions Title of Instructions for completion of Delivery of Electronic delivery Federally

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules Covered Transactions Exemptions Title of Instructions for completion of Delivery of Electronic delivery Federally

REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY

POLICY") I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

Reasons for Change. Are You Ready for the Regulation Z & RESPA Changes. Past, Present & Future Changes

Are You Ready for the Regulation Z & RESPA Changes Community Bankers Association of Illinois Annual Convention September 26, 2009 Presented by: Young & Associates, Inc. 1 Past, Present & Future Changes

Are You Ready for the Regulation Z & RESPA Changes Community Bankers Association of Illinois Annual Convention September 26, 2009 Presented by: Young & Associates, Inc. 1 Past, Present & Future Changes

HERE S. TRID. ROBERT E. PINDER (904) ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015

ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015") HERE S. TRID ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015 ROBERT E. PINDER rpinder@rtlaw.com (904) 346-5551 HERE S. TRID 2 COUNTDOWN TO TRID TRID Goes into Effect

HERE S. TRID ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015 ROBERT E. PINDER rpinder@rtlaw.com (904) 346-5551 HERE S. TRID 2 COUNTDOWN TO TRID TRID Goes into Effect

Understanding the New Truth in Lending Act Disclosure Rules Effective July 30 th

Understanding the New Truth in Lending Act Disclosure Rules Effective July 30 th July 15, 2009 The home mortgage industry is abuzz with concerns about new disclosure rules under the Truth in Lending Act

Understanding the New Truth in Lending Act Disclosure Rules Effective July 30 th July 15, 2009 The home mortgage industry is abuzz with concerns about new disclosure rules under the Truth in Lending Act

Comment Call (12-14)

") Comment Call (12-14) To: From: All Affiliated Credit Union CEOs Veronica Madsen Director of Regulatory Affairs Date: August 28, 2012 RE: CFPB Combined TILA/RESPA Disclosures Summary The Dodd-Frank Wall

Comment Call (12-14) To: From: All Affiliated Credit Union CEOs Veronica Madsen Director of Regulatory Affairs Date: August 28, 2012 RE: CFPB Combined TILA/RESPA Disclosures Summary The Dodd-Frank Wall

The WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms

The WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Holly Spencer Bunting K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 holly.bunting@klgates.com Phillip

The WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Holly Spencer Bunting K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 holly.bunting@klgates.com Phillip

The New Mortgage Disclosure Forms: Know the Rule

The New Mortgage Disclosure Forms: Know the Rule 10:15 11:15 a.m. Phillip L. Schulman, Esq., Partner, K&L Gates LLP THE WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Phillip

The New Mortgage Disclosure Forms: Know the Rule 10:15 11:15 a.m. Phillip L. Schulman, Esq., Partner, K&L Gates LLP THE WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Phillip

TILA / RESPA Integrated Disclosures. The Game-changing Impacts and Action Items

TILA / RESPA Integrated Disclosures The Game-changing Impacts and Action Items CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited CUNA Mutual Group 2013 Presenters Jon Bundy

TILA / RESPA Integrated Disclosures The Game-changing Impacts and Action Items CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited CUNA Mutual Group 2013 Presenters Jon Bundy

TILA-RESPA Integrated Disclosure (TRID) Rule a.k.a. Know Before You Owe. with New Haven Middlesex Association of REALTORS

Rule a.k.a. Know Before You Owe. with New Haven Middlesex Association of REALTORS") TILA-RESPA Integrated Disclosure (TRID) Rule a.k.a. Know Before You Owe with New Haven Middlesex Association of REALTORS July 16, 2015 Jeremy Potter, General Counsel and Chief Compliance Officer, Norcom

TILA-RESPA Integrated Disclosure (TRID) Rule a.k.a. Know Before You Owe with New Haven Middlesex Association of REALTORS July 16, 2015 Jeremy Potter, General Counsel and Chief Compliance Officer, Norcom

Reference Guide: Loan Estimate (LE) TILA- RESPA Integrated Disclosure (TRID) Rule Requirements

TILA- RESPA Integrated Disclosure (TRID) Rule Requirements") Reference Guide: Loan Estimate (LE) TILA- RESPA Integrated Disclosure (TRID) Rule Requirements The purpose of this document is to provide a reference guide for the Loan Estimate (LE) TILA-RESPA Integrated

Reference Guide: Loan Estimate (LE) TILA- RESPA Integrated Disclosure (TRID) Rule Requirements The purpose of this document is to provide a reference guide for the Loan Estimate (LE) TILA-RESPA Integrated

TILA RESPA Integrated Disclosures

TILA RESPA Integrated Disclosures Jimmy Vuong Branch Relations Manager jvuong@afncorp.com Rev. 03/22/2017 American Financial Network, Inc. All Rights Reserved. The Beta is Open Please see Encompass Newsflash

TILA RESPA Integrated Disclosures Jimmy Vuong Branch Relations Manager jvuong@afncorp.com Rev. 03/22/2017 American Financial Network, Inc. All Rights Reserved. The Beta is Open Please see Encompass Newsflash

TILA/RESPA Integrated Disclosure Rule

TILA/RESPA Integrated Disclosure Rule Solving the Puzzle July 22, 2015 Presented by: Gary D. Clark, CMB Chief Operating Officer Sierra Pacific Mortgage Webinar All lines will be muted You can type your

TILA/RESPA Integrated Disclosure Rule Solving the Puzzle July 22, 2015 Presented by: Gary D. Clark, CMB Chief Operating Officer Sierra Pacific Mortgage Webinar All lines will be muted You can type your

TRID Quick Reference Guide

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

TRID. Acceptable Broker Submissions Booklet WHSL EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471

TRID Acceptable Broker Submissions Booklet EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471 WHSL-0022-1015 As Fremont Bank transitions to the new Rule, our goal is to make the submission of your loan applications

TRID Acceptable Broker Submissions Booklet EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471 WHSL-0022-1015 As Fremont Bank transitions to the new Rule, our goal is to make the submission of your loan applications

Tips for Implementing the TILA-RESPA Integrated Disclosure rule

Tips for Implementing the TILA-RESPA Integrated Disclosure rule To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on

Tips for Implementing the TILA-RESPA Integrated Disclosure rule To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on

TRID Update: 6 Months In, Areas of Concern and Uncertainty

TRID Update: 6 Months In, Areas of Concern and Uncertainty New Jersey Bankers Association prycompliance@hotmail.com 0 0 of of 6674 Clarifications Coming CFPB announced upcoming Proposed Rule in April 28,

TRID Update: 6 Months In, Areas of Concern and Uncertainty New Jersey Bankers Association prycompliance@hotmail.com 0 0 of of 6674 Clarifications Coming CFPB announced upcoming Proposed Rule in April 28,

TRID (TILA-RESPA Integrated Disclosures) Presented by:

Presented by:") TRID (TILA-RESPA Integrated Disclosures) Presented by: What is TRID? TRID will eliminate the use of the good faith estimate, truth in lending disclosures, and HUD-1 Settlement Statement. They will now

TRID (TILA-RESPA Integrated Disclosures) Presented by: What is TRID? TRID will eliminate the use of the good faith estimate, truth in lending disclosures, and HUD-1 Settlement Statement. They will now

The CFPB s New Mortgage Disclosures

The CFPB s New Mortgage Disclosures Benjamin K. Olson March 10, 2015 Key Changes Effective August 1, 2015: GFE and initial TIL replaced with the Loan Estimate The items constituting an application are

The CFPB s New Mortgage Disclosures Benjamin K. Olson March 10, 2015 Key Changes Effective August 1, 2015: GFE and initial TIL replaced with the Loan Estimate The items constituting an application are

TRID: THE BUCKET CHALLENGE

TRID: THE BUCKET CHALLENGE 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer TriComply Services WHAT YOU WILL LEARN Good faith Changed circumstance The Tolerance Buckets

TRID: THE BUCKET CHALLENGE 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer TriComply Services WHAT YOU WILL LEARN Good faith Changed circumstance The Tolerance Buckets

The CFPB s TILA-RESPA Integrated Disclosure Rule: What You Need to Know for October 3rd. Paul Bugoni, Esq. Stewart Title Guaranty Company New York, NY

The CFPB s TILA-RESPA Integrated Disclosure Rule: What You Need to Know for October 3rd by Paul Bugoni, Esq. Stewart Title Guaranty Company New York, NY 1 2 The CFPB s TILA-RESPA Integrated Disclosure

The CFPB s TILA-RESPA Integrated Disclosure Rule: What You Need to Know for October 3rd by Paul Bugoni, Esq. Stewart Title Guaranty Company New York, NY 1 2 The CFPB s TILA-RESPA Integrated Disclosure

Section 12.1: Regulation Z Mortgage Disclosure Improvement Act (MDIA) Policy

Policy") Section 12.1: Regulation Z Mortgage Disclosure Improvement Act (MDIA) Policy Background SecurityNational Mortgage Company (SNMC) shall comply with the Housing and Economic Recovery Act of 2008 (HERA) which

Section 12.1: Regulation Z Mortgage Disclosure Improvement Act (MDIA) Policy Background SecurityNational Mortgage Company (SNMC) shall comply with the Housing and Economic Recovery Act of 2008 (HERA) which

CFPB PROPOSED REGULATIONS

CFPB PROPOSED REGULATIONS TILA/RESPA DISCLOSURES For more than 30 years, 2 different disclosure forms to consumers applying for a mortgage Developed by 2 different federal agencies under 2 federal statutes:

CFPB PROPOSED REGULATIONS TILA/RESPA DISCLOSURES For more than 30 years, 2 different disclosure forms to consumers applying for a mortgage Developed by 2 different federal agencies under 2 federal statutes:

TRID. Quick Compliance Guide T I L A-RESPA INTEGRAT E D DISCLOSURES Temenos USA. All rights reserved

TRID T I L A-RESPA INTEGRAT E D DISCLOSURES Quick Compliance Guide 09.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636 e: usainfo@temenos.com While the publisher and

TRID T I L A-RESPA INTEGRAT E D DISCLOSURES Quick Compliance Guide 09.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636 e: usainfo@temenos.com While the publisher and

CFPB: The New Closing Process

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 INTRODUCTION (10-12 minute segment) TEACHING OBJECTIVE:

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 INTRODUCTION (10-12 minute segment) TEACHING OBJECTIVE:

TIL/RESPA Final Rules on Integrated Mortgage Disclosures

TIL/RESPA Final Rules on Integrated Mortgage Disclosures CLAconnect.com Disclaimers The information contained herein is general in nature and is not intended, and should not be construed, as legal, accounting,

TIL/RESPA Final Rules on Integrated Mortgage Disclosures CLAconnect.com Disclaimers The information contained herein is general in nature and is not intended, and should not be construed, as legal, accounting,

The New Loan Estimate & a. Closing Disclosure Explained. Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. http://cfpb.fntic.com/ Barry S. Wolfinsohn

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. http://cfpb.fntic.com/ Barry S. Wolfinsohn

The SoftPro Solution

The SoftPro Solution 1 The Final Rule Patrick Hempen SoftPro Corporation SVP Sales & Marketing patrick.hempen@softprocorp.com 2 The Goals of the Final Rule: Improved consumer understanding Risk factors

The SoftPro Solution 1 The Final Rule Patrick Hempen SoftPro Corporation SVP Sales & Marketing patrick.hempen@softprocorp.com 2 The Goals of the Final Rule: Improved consumer understanding Risk factors

FREQUENTLY ASKED QUESTIONS (FAQ) FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID)

FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID)") Best Practices FREQUENTLY ASKED QUESTIONS (FAQ) FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID) SUMMARY With the upcoming implementation of the Truth in Lending (TILA)/Real Estate Settlement

Best Practices FREQUENTLY ASKED QUESTIONS (FAQ) FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID) SUMMARY With the upcoming implementation of the Truth in Lending (TILA)/Real Estate Settlement

TRID TILA RESPA Integrated Disclosures. Presented by David Luna

TRID TILA RESPA Integrated Disclosures Presented by David Luna Thank you I d like to thank the many sources of information: the Attorney s, Creditors, Title, Credit providers and the CFPB for the information

TRID TILA RESPA Integrated Disclosures Presented by David Luna Thank you I d like to thank the many sources of information: the Attorney s, Creditors, Title, Credit providers and the CFPB for the information

CFPB- Getting Ready for NEW Real Estate Closing Procedures. Ruth Dillingham, Special Counsel First American Title Insurance Company April 17, 2014

CFPB- Getting Ready for NEW Real Estate Closing Procedures Ruth Dillingham, Special Counsel First American Title Insurance Company April 17, 2014 1 Supervision of Third Party Vendors CFPB Bulletin April

CFPB- Getting Ready for NEW Real Estate Closing Procedures Ruth Dillingham, Special Counsel First American Title Insurance Company April 17, 2014 1 Supervision of Third Party Vendors CFPB Bulletin April

TILA RESPA Integrated Disclosure ~ Closing Disclosure (CD) ~

~") Click for audio recording of training TILA RESPA Integrated Disclosure ~ Closing Disclosure (CD) ~ Fowler Williams President Crescent Mortgage Company 1 Question and Answers Email fwilliams@crescentmortgage.net

Click for audio recording of training TILA RESPA Integrated Disclosure ~ Closing Disclosure (CD) ~ Fowler Williams President Crescent Mortgage Company 1 Question and Answers Email fwilliams@crescentmortgage.net

Presentation by Janet M. Bonnefin Aldrich & Bonnefin, PLC

Washington Bankers Association 2015 Northwest Compliance Conference TRID We re Down to the Wire! Presentation by Janet M. Bonnefin Aldrich & Bonnefin, PLC Agenda Creditor s duty to give Loan Estimate Restrictions

Washington Bankers Association 2015 Northwest Compliance Conference TRID We re Down to the Wire! Presentation by Janet M. Bonnefin Aldrich & Bonnefin, PLC Agenda Creditor s duty to give Loan Estimate Restrictions

TILA-RESPA Integrated Disclosures (TRID) FAQs

FAQs") TILA-RESPA Integrated Disclosures (TRID) FAQs On July 21, 2015, the Consumer Financial Protection Bureau (CFPB) published the final rule to delay the effective date of the TILA-RESPA Integrated Disclosure

TILA-RESPA Integrated Disclosures (TRID) FAQs On July 21, 2015, the Consumer Financial Protection Bureau (CFPB) published the final rule to delay the effective date of the TILA-RESPA Integrated Disclosure

TRID TOPICS Forms The Closing Disclosure (CD)

") TRID TOPICS VIII June 8, 2015 TRID TOPICS Forms The Closing Disclosure (CD) WHAT IS THE CLOSING DISCLOSURE AND HOW DOES IT DIFFER FROM TODAY: The Closing Disclosure, also referenced as the CD, under the

TRID TOPICS VIII June 8, 2015 TRID TOPICS Forms The Closing Disclosure (CD) WHAT IS THE CLOSING DISCLOSURE AND HOW DOES IT DIFFER FROM TODAY: The Closing Disclosure, also referenced as the CD, under the

Introduction to the TILA-RESPA Integrated Disclosure Rule TRID

Introduction to the TILA-RESPA Integrated Disclosure Rule TRID October 3, 2015 Aaron Mason NMLS 54707 Mortgage Loan Officer 859-230-4628 AaronMason@homeserviceslending.com AaronMason.RectorHaydenMortgage.com

Introduction to the TILA-RESPA Integrated Disclosure Rule TRID October 3, 2015 Aaron Mason NMLS 54707 Mortgage Loan Officer 859-230-4628 AaronMason@homeserviceslending.com AaronMason.RectorHaydenMortgage.com

CFPB Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

TILA-RESPA Integrated Disclosures, Part 2 Various Topics

Outlook Live Webinar- August 26, 2014 TILA-RESPA Integrated Disclosures, Part 2 Various Topics Presented by the Consumer Financial Protection Bureau The content of this webinar is current as of the date

Outlook Live Webinar- August 26, 2014 TILA-RESPA Integrated Disclosures, Part 2 Various Topics Presented by the Consumer Financial Protection Bureau The content of this webinar is current as of the date

Ready. Set. know. Understanding TILA-RESPA Integrated Disclosure (TRID)

") Ready. Set. know. Understanding TILA-RESPA Integrated Disclosure (TRID) How our competition is handling TRID. Relying on 3rd party vendors to provide material Communicating what we need to know through

Ready. Set. know. Understanding TILA-RESPA Integrated Disclosure (TRID) How our competition is handling TRID. Relying on 3rd party vendors to provide material Communicating what we need to know through

TILA / RESPA Integrated Disclosures Roll-Out. CUNA Lending Council November 4th, 2014

TILA / RESPA Integrated Disclosures Roll-Out CUNA Lending Council November 4th, 2014 Presenter Jon Bundy Regulatory Compliance Manager LOANLINER Documents CUNA Mutual Group Agenda Overview of Integrated

TILA / RESPA Integrated Disclosures Roll-Out CUNA Lending Council November 4th, 2014 Presenter Jon Bundy Regulatory Compliance Manager LOANLINER Documents CUNA Mutual Group Agenda Overview of Integrated

TRID. Old vs New Comparison of TILA/RESPA Integrated Disclosure Changes for Real Estate Agents. Copyright 2015 Go2Training Consultants, LLC.

TRID Old vs New Comparison of TILA/RESPA Integrated Changes for Real Estate Agents Old vs New Comparison of the TILA/RESPA Integrated Changes Good Faith Estimate Loan Estimate The GFE and Initial TIL are

TRID Old vs New Comparison of TILA/RESPA Integrated Changes for Real Estate Agents Old vs New Comparison of the TILA/RESPA Integrated Changes Good Faith Estimate Loan Estimate The GFE and Initial TIL are

HUD s New RESPA Rule

1300 Nineteenth Street, NW Fifth Floor Washington, DC 20036 202.628.2000 www.wbsk.com HUD s New RESPA Rule November 24, 2008 On November 17, 2008 the United States Department of Housing and Urban Development

1300 Nineteenth Street, NW Fifth Floor Washington, DC 20036 202.628.2000 www.wbsk.com HUD s New RESPA Rule November 24, 2008 On November 17, 2008 the United States Department of Housing and Urban Development

TITLE TERMS YOU NEED TO KNOW

TITLE TERMS YOU NEED TO KNOW Abstract Plant A geographically arranged abstract plant, currently kept to date, that is adequate for use in insuring titles, so as to provide for the safety and protection

TITLE TERMS YOU NEED TO KNOW Abstract Plant A geographically arranged abstract plant, currently kept to date, that is adequate for use in insuring titles, so as to provide for the safety and protection

21 Closings THE CLOSING EVENT

21 Closings The Closing Event Real Estate Settlement Procedures Act Financial Settlement of the Transaction Computing Prorations Taxes Due at Closing Closing Cost Calculations: Case Study TILA/RESPA Integrated

21 Closings The Closing Event Real Estate Settlement Procedures Act Financial Settlement of the Transaction Computing Prorations Taxes Due at Closing Closing Cost Calculations: Case Study TILA/RESPA Integrated

There will be subsequent presentations over the next several months which will provide:

This is an introductory presentation which will cover the basic information about the new rules including a: Practical description of the new rules and An overview of the changes There will be subsequent

This is an introductory presentation which will cover the basic information about the new rules including a: Practical description of the new rules and An overview of the changes There will be subsequent

Forensic Review Report

Forensic Review Report Prepared by Aequitas Borrower: John Smith Date: 7/9/2009 Copyright 2009 MHI. All Rights Reserved. 2 of 19 TABLE OF CONTENTS Review Letter... 4 Forensic Review Summary... 5 Forensic

Forensic Review Report Prepared by Aequitas Borrower: John Smith Date: 7/9/2009 Copyright 2009 MHI. All Rights Reserved. 2 of 19 TABLE OF CONTENTS Review Letter... 4 Forensic Review Summary... 5 Forensic

Facing Today s Real Estate Regulations

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

TILA-RESPA Integrated Disclosure

This guide is current as of the date set forth on the cover page. It has been updated to reflect the final rule issued on July 7, 2017 and published on August 11, 2017. December 2017 TILA-RESPA Integrated

This guide is current as of the date set forth on the cover page. It has been updated to reflect the final rule issued on July 7, 2017 and published on August 11, 2017. December 2017 TILA-RESPA Integrated

What REALTORS. Should Know About CFPB Changes. Courtesy of:

What REALTORS Should Know About CFPB Changes Courtesy of: CFPB was formed as a result of Dodd-Frank in 2010 CFPB governs all matters consumer finance related CFPB now oversees RESPA CFPB regulates: Credit

What REALTORS Should Know About CFPB Changes Courtesy of: CFPB was formed as a result of Dodd-Frank in 2010 CFPB governs all matters consumer finance related CFPB now oversees RESPA CFPB regulates: Credit

Interagency Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

CFPB Integrated Mortgage Disclosure Final Rule

CFPB Integrated Mortgage Disclosure Final Rule Current Status of the New Rule Mary Schuster Chief Product Officer - RamQuest The Regulatory Reform Ecosystem Meet the CFPB Mission Statement o To make markets

CFPB Integrated Mortgage Disclosure Final Rule Current Status of the New Rule Mary Schuster Chief Product Officer - RamQuest The Regulatory Reform Ecosystem Meet the CFPB Mission Statement o To make markets

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 2 A New Way to Disclose

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 2 A New Way to Disclose 1. Does the intent to proceed have to be received by all Applicants or just an applicant? Answer: The regulation

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 2 A New Way to Disclose 1. Does the intent to proceed have to be received by all Applicants or just an applicant? Answer: The regulation

Integrated Disclosure Vocabulary List. Term Definition as of 8/1/2015 Adjustments and Other Credits

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

WELCOME! Are You Ready for TRID?

1 WELCOME! www.grantsimon.com Are You Ready for TRID? 2 Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE 3 Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1

1 WELCOME! www.grantsimon.com Are You Ready for TRID? 2 Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE 3 Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1

FINALLY HERE TILA-RESPA INTEGRATED DISCLOSURE FORMS

TRIPLE PLAY CONVENTION FINALLY HERE TILA-RESPA INTEGRATED DISCLOSURE FORMS December 7, 2015 Phillip L. Schulman K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 phil.schulman@klgates.com

TRIPLE PLAY CONVENTION FINALLY HERE TILA-RESPA INTEGRATED DISCLOSURE FORMS December 7, 2015 Phillip L. Schulman K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 phil.schulman@klgates.com

WELCOME!

WELCOME! www.grantsimon.com Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1 & TIL

WELCOME! www.grantsimon.com Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1 & TIL

TILA-RESPA Integrated Disclosures Part 5 Common Questions

TILA-RESPA Integrated Disclosures Part 5 Common Questions Outlook Live Webinar - May 26, 2015 Presented by the Consumer Financial Protection Bureau The content of this webinar is current as of the date

TILA-RESPA Integrated Disclosures Part 5 Common Questions Outlook Live Webinar - May 26, 2015 Presented by the Consumer Financial Protection Bureau The content of this webinar is current as of the date

TILA RESPA Integrated Disclosure (TRID) Doing Business with NewLeaf

Doing Business with NewLeaf") TILA RESPA Integrated Disclosure (TRID) Doing Business with NewLeaf Presented By Marti Tromley EVP, Chief Risk Officer mtromley@newleafwholesale.com The information contained herein is intended as informational

TILA RESPA Integrated Disclosure (TRID) Doing Business with NewLeaf Presented By Marti Tromley EVP, Chief Risk Officer mtromley@newleafwholesale.com The information contained herein is intended as informational

Executive Summary of the 2017 TILA- RESPA Rule

1700 G Street NW, Washington, DC 20552 July 7, 2017 Executive Summary of the 2017 TILA- RESPA Rule On July 7, 2017, the Consumer Financial Protection Bureau (Bureau) issued a final rule (2017 TILA-RESPA

1700 G Street NW, Washington, DC 20552 July 7, 2017 Executive Summary of the 2017 TILA- RESPA Rule On July 7, 2017, the Consumer Financial Protection Bureau (Bureau) issued a final rule (2017 TILA-RESPA

Truth in Lending / RESPA Regulatory Changes

Steve H. Powell & Company Truth in Lending / RESPA Regulatory Changes Truth in Lending and RESPA Update Note: This publication is not offered as legal advice. Readers should seek legal counsel for advice

Steve H. Powell & Company Truth in Lending / RESPA Regulatory Changes Truth in Lending and RESPA Update Note: This publication is not offered as legal advice. Readers should seek legal counsel for advice

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET. Christopher W. Smart

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET Christopher W. Smart Introduction and Background Residential mortgage lenders have long been required to disclose to their

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET Christopher W. Smart Introduction and Background Residential mortgage lenders have long been required to disclose to their

Know Before You Owe Policy Manual Table of Contents [Sample Client] Table of Contents. Sample

![Know Before You Owe Policy Manual Table of Contents [Sample Client] Table of Contents. Sample](/thumbs/96/128500341.jpg "Know Before You Owe Policy Manual Table of Contents [Sample Client] Table of Contents. Sample") TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 4 1.1 GOALS AND OBJECTIVES... 4 1.2 REQUIRED REVIEW... 4 1.3 APPLICABILITY... 4 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 5 2.1 INTERNAL CONTROLS... 5

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 4 1.1 GOALS AND OBJECTIVES... 4 1.2 REQUIRED REVIEW... 4 1.3 APPLICABILITY... 4 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 5 2.1 INTERNAL CONTROLS... 5

TRID RULE UPDATES AND THE BLACK HOLE CONUNDRUM JONATHAN FOXX *

TRID RULE UPDATES AND THE BLACK HOLE CONUNDRUM JONATHAN FOXX * On August 11, 2017, the Consumer Financial Protection Bureau ( Bureau ) issued a Final Rule (2017 TILA-RESPA Rule or 2017 Rule, hereinafter

TRID RULE UPDATES AND THE BLACK HOLE CONUNDRUM JONATHAN FOXX * On August 11, 2017, the Consumer Financial Protection Bureau ( Bureau ) issued a Final Rule (2017 TILA-RESPA Rule or 2017 Rule, hereinafter

The TRID Process for Wholesale Lending

The TRID Process for Wholesale Lending Michelle McLaughlin 2015 CMG Financial, All Rights Reserved. CMG Financial is a registered trade name of CMG Mortgage, Inc., NMLS #1820 in most, but not all states.

The TRID Process for Wholesale Lending Michelle McLaughlin 2015 CMG Financial, All Rights Reserved. CMG Financial is a registered trade name of CMG Mortgage, Inc., NMLS #1820 in most, but not all states.

Understanding CFPB Rules CONSUMER FINANCIAL PROTECTION BUREAU

Understanding CFPB Rules CONSUMER FINANCIAL PROTECTION BUREAU The Consumer Financial Protection Bureau The CFPB is a new federal agency Created by Dodd Frank Wall Street and Consumer Protection Act Dodd

Understanding CFPB Rules CONSUMER FINANCIAL PROTECTION BUREAU The Consumer Financial Protection Bureau The CFPB is a new federal agency Created by Dodd Frank Wall Street and Consumer Protection Act Dodd

CFPB-TRID Frequently Asked Questions June 15, 2015

CFPB-TRID Frequently Asked Questions June 15, 2015 Contents TILA-RESPA Integrated Disclosure Rule... 2 Effective Date(s)... 2 Impacted People, Property & Transaction Types... 2 Financing Type... 4 Seller

CFPB-TRID Frequently Asked Questions June 15, 2015 Contents TILA-RESPA Integrated Disclosure Rule... 2 Effective Date(s)... 2 Impacted People, Property & Transaction Types... 2 Financing Type... 4 Seller

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 9 GFE Interest rate expiration... 9 GFE Expiration... 10 GFE Denial... 10 GFE

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 9 GFE Interest rate expiration... 9 GFE Expiration... 10 GFE Denial... 10 GFE

Mortgage Lending Compliance Issues Session 1. Higher Priced and High-Cost Mortgages

Mortgage Lending Compliance Issues Session 1 Higher Priced and High-Cost Mortgages Today s Topics Learn the definitions of Higher Priced and High Cost Mortgages and how to test to determine if you are

Mortgage Lending Compliance Issues Session 1 Higher Priced and High-Cost Mortgages Today s Topics Learn the definitions of Higher Priced and High Cost Mortgages and how to test to determine if you are

Are You Ready for the TILA-RESPA Integrated Disclosures (TRID)? By Vincent Spoto

? By Vincent Spoto") Are You Ready for the TILA-RESPA Integrated Disclosures (TRID)? By Vincent Spoto 1 Are You Ready for the TILA- RESPA Integrated Disclosures (TRID)? By Vincent Spoto By now, most lenders should be well

Are You Ready for the TILA-RESPA Integrated Disclosures (TRID)? By Vincent Spoto 1 Are You Ready for the TILA- RESPA Integrated Disclosures (TRID)? By Vincent Spoto By now, most lenders should be well

Texas Administrative Code

Texas Administrative Code TITLE 7 BANKING AND SECURITIES PART 8 JOINT FINANCIAL REGULATORY AGENCIES CHAPTER 153 HOME EQUITY LENDING (Includes amendments effective on January 1, 2018) 153.1 Definitions

Texas Administrative Code TITLE 7 BANKING AND SECURITIES PART 8 JOINT FINANCIAL REGULATORY AGENCIES CHAPTER 153 HOME EQUITY LENDING (Includes amendments effective on January 1, 2018) 153.1 Definitions

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

Closing Disclosure August 1, CFR

Closing Disclosure August 1, 2015 12 CFR 1026.38 Agent Questions for Lender Clients Who will prepare the Closing Disclosure (CD) Form? How will Agents coordinate with the lender to prepare the Closing

Closing Disclosure August 1, 2015 12 CFR 1026.38 Agent Questions for Lender Clients Who will prepare the Closing Disclosure (CD) Form? How will Agents coordinate with the lender to prepare the Closing

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

The New Loan Estimate & Closing Disclosure Explained. Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. 2015 Chicago Title Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. 2015 Chicago Title Know before you close.

Legal Bulletin 205 July 24, 2015 Financing Forms Revisions. By Northwest Multiple Listing Service July 6, 2015

Legal Bulletin 205 July 24, 2015 Financing Forms Revisions By Northwest Multiple Listing Service July 6, 2015 1. Introduction This bulletin reviews upcoming revisions to NWMLS financing forms, including

Legal Bulletin 205 July 24, 2015 Financing Forms Revisions By Northwest Multiple Listing Service July 6, 2015 1. Introduction This bulletin reviews upcoming revisions to NWMLS financing forms, including

Display the questions that impact the date through which the interest rate is available with a left click on the control.

New Standardized Good Faith Estimate On November 17, 2008, the Department of Housing and Urban Development published its final rule regarding RESPA Reform. The final rule requires mortgage lenders and

New Standardized Good Faith Estimate On November 17, 2008, the Department of Housing and Urban Development published its final rule regarding RESPA Reform. The final rule requires mortgage lenders and

6/21/2013. Section III. Federal Rules, Regulations and Their Requirements. Federal Regulations. Federal Regulations

Section III Federal Rules, Regulations and Their Requirements Federal Regulations The federal rules, regulations and requirements in this course are complied into 4 categories for analysis: Laws requiring

Section III Federal Rules, Regulations and Their Requirements Federal Regulations The federal rules, regulations and requirements in this course are complied into 4 categories for analysis: Laws requiring

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 10 GFE Interest rate expiration... 10 GFE Expiration... 10 GFE Denial... 11

FAQs About RESPA for Industry

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

Texas Administrative Code. TITLE 7 BANKING AND SECURITIES PART 8 JOINT FINANCIAL REGULATORY AGENCIES CHAPTER 153 HOME EQUITY LENDING (As of 12.

Texas Administrative Code TITLE 7 BANKING AND SECURITIES PART 8 JOINT FINANCIAL REGULATORY AGENCIES CHAPTER 153 HOME EQUITY LENDING (As of 12.2014) Rules 153.1 Definitions 153.2 Voluntary Lien: Section

Texas Administrative Code TITLE 7 BANKING AND SECURITIES PART 8 JOINT FINANCIAL REGULATORY AGENCIES CHAPTER 153 HOME EQUITY LENDING (As of 12.2014) Rules 153.1 Definitions 153.2 Voluntary Lien: Section