Plaza s VA Renovation

|

|

|

- Mariah Riley

- 5 years ago

- Views:

Transcription

1 Click here to add a longer headline about the slide Plaza s VA Renovation July 2018

2 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial in from your telephone. Click here to download any handouts. If you have any questions, please type them in here. All questions will be addressed, time permitting. 2

3 Legal Disclaimers This information is published and/or provided by Plaza Home Mortgage, Inc. as a courtesy to its clients and is meant for instructional purposes only. It is not intended for consumer use. None of the information provided is intended to be legal advice in any context. Plaza makes every effort to provide accurate information. Plaza does not guarantee, warrant, ensure or promise that it is correct; and any effort to blame Plaza if this information proves to be incorrect will be vigorously defended. All ideas expressed during this event are those of the individuals making them and are not to be imparted to the organizations they represent. Any unauthorized use, dissemination or distribution of these documents or ideas is strictly prohibited. Please visit our website at to view full program guidelines. The information contained in this webinar may not highlight all requirements of these programs and does not reduce or eliminate any requirements set forth in our guidelines. Guidelines are subject to change without notice. Plaza Home Mortgage, Inc. is an Equal Housing Opportunity Lender. This is not a commitment to lend. Information is intended for mortgage professionals only and not intended for public use or distribution. Terms and conditions of programs are subject to change at any time. Refer to Plaza s underwriting and program guidelines for loan specific details and all eligibility requirements Plaza Home Mortgage, Inc. All rights reserved. Company NMLS #

4 Objectives This training session is for Wholesale, Mini-Correspondent and National Correspondent Loan Origination Partners. The webinar is scheduled for 60 minutes. The goal of this webinar is to show you how Plaza s VA Renovation Program can help make the dream of homeownership possible for more veterans. 4

5 Presenter Ragen Cunningham National Renovation Lending Manager 5

6 What is a VA Renovation Loan? The VA Renovation loan, valid for purchases or refinances, allows VA-qualified borrowers to easily fund the cost of a purchase or re-fi and include the costs of renovations, up to $50,000, into a single loan. A more affordable option compared to adding a second mortgage or HELOC. Both Purchases and Refinances allow borrowers to borrow up to 100% of the after improved value. 6

7 Key Advantages of Plaza s VA Renovation Loan Up to $50,000 in additional financing toward renovation costs is included in the VA financing. Allows luxury improvements (pools, outdoor living). Both purchases and refinances allow borrowers to borrow up to 100% of the after improved value. Like typical VA loans, originators will receive compensation when the loan is closed and before construction has begun. Our seasoned Renovation Specialists are experts in the field, and know the in s and out s of renovation loans. 7

8 Opportunity 100 Financing No MI 2.1M Active Veteran Loans 19,349,382 Total US Vets Total Active VA Loans *National Center of Veteran Analysis and Statistics,

9 Click here to add a longer headline about the slide VA Renovation Guidelines

10 Qualification Guidelines 620 Min Credit Score- Conforming 10

11 Borrower Eligibility Active duty service members Reserve and National Guard members Unmarried surviving spouse Honorably discharged Veterans 11

12 Eligible Properties Attached/Detached SFRs and PUDs VA approved Condos interior unit upgrades only 2-4 Units Owner Occupied Only 12

13 Ineligible Properties x Mixed use properties in commercial zoning x Non-VA approved or warrantable condos x Timeshares x Working farms, ranches, orchards x Commercial properties x Cooperatives x Condotels x Properties listed on the National Historic Register x Geothermal homes x Manufactured housing or mobile homes x Homes that have been completely demolished, including the foundation x Homes being moved from one location to another x Refinance transactions for properties listed for sale on or after the date of application 13

14 How to Calculate Loan Amount Loan-to-value is based on: Purchase: is the lessor of the sales price plus repairs OR the as completed NOV appraised value Refinance: 100% of as completed NOV appraised value Base loan amount cannot exceed 100% LTV/CLTV 14

15 Let s look at a Purchase example: LTV 100% Purchase/Renovation Costs Sales Price $220, Labor/Materials 30, Soft Costs (permits, etc.) % Contingency 3, *Inspection fees (max 3 draws) Total $254, As Completed NOV appraised value 280, % of As Completed NOV appraised value 280, $254,964 < 280,000 Maximum Loan Amount $254,

.")

16 Timing and Occupancy Construction must BEGIN within 30 days of closing. All rehabilitation must be completed within 4 months of closing. The borrower cannot be displaced from the property (for more than 15 days). Examples of work that may cause them to be displaced: Properties that will not have running water plumbing repairs that would require the water to be shut off for long periods of time No electricity electrical repairs that would require the electricity to be shut off for long periods of time Missing roof No heat source 16

17 Purchase Contracts Quick Tips: Have accessibility to the property for contractors, inspectors, architects/engineers, and appraisers. Make sure power/water, utilities are on at time of appraisal inspection to avoid increased contingencies. 17

18 Allowable Renovation Costs Actual cost of the renovation based on plans, specifications and accepted contractor s contract stating scope of work, cost of materials and labor, timeframe for start, and completion of work. Contingency Reserve is required equal to 10% to 15% Allowable construction related fees and costs Inspection/Title Update Fees Permits and Other Fees Discount Points on Repair Costs 18

19 Non-Allowable Renovation Costs x HUD Consultant x Architect x Engineer 19

20 Fund Definitions Contingency Fund 10% of the actual repair amount (and 15% maximum) will be held in the repair escrow account. This reserve of funds is for the purpose of covering unplanned repairs that become necessary due to health or safety issues. No portion of this money may be used for building material changes or repairs. This contingency fund is always capped at 15%. If utilities are off at the time of appraisal inspection, a minimum 15% contingency reserve is required. Any unused funds are returned as a principal reduction and do not affect payment. Borrower Funded Contingency Alternatively, the contingency can be funded with the borrower s own funds and not be financed. The funds must be provided at escrow from a documented source (not borrowed or financed). If not required for repairs, the funds would be returned to borrower at completion of the renovation and at final closeout. NOTE: VA Renovation Refinance only - borrower may request the remaining financed contingency reserves returned as part of final close out OR applied to the principal balance of the loan. The option to refund excess financed contingency funds at completion is not allowed in Texas. 20

21 Fund Definitions (cont d) Holdback Fund 10% of the total draw request amount will be deducted and held in the repair escrow account until the entire project is complete. For example, if $1,000 draw is requested, Plaza Home Mortgage will issue a check for $900. The $100 difference will remain in the repair escrow account. All monies held back will be released after all work is complete and Plaza Home Mortgage has confirmed that the property s title is clear of any liens. 21

22 VA Renovation Draw Process No more than 3 draws allowed, 2 interim draws performed by a construction inspector and a final performed by VA appraiser. Funds will be made available via 2-party check payable to borrower and contractor. Plaza should release monies within 5 business days of receipt of a properly executed VA Renovation Draw Request. No draw at closing allowed. 22

23 Eligible Improvements All alterations and repairs must be permanently affixed to the property (dwelling or land) and be ordinarily found on similar properties of comparable value in the community. Project must be complete with final inspection no later than 120 days from note date. The maximum renovation amount, including fees and contingency, must not exceed $50,000. There is no minimum dollar amount for repairs. 23

24 Eligible Improvements (cont d) Repairs should be non-structural, although minor structural repairs are allowed. Any work that requires structural engineering reports or architectural specs is not allowed. If any structural work is included, building/construction jurisdictional evidence that project does not require engineer reports or architectural specs must be provided, e.g. local code pertaining to type of structural repair, permits and/or other written verification from the jurisdiction (state, city, municipality or county). Minor structural repairs must be those that can reasonably be expected to be completed within the 120-day time frame. If structural repairs are included, the contractor s bid must include a statement addressing the fact that all structural repairs do not require engineering or architecture reports to obtain permits or meet local building codes and that such work will be completed within 120 days. 24

25 Ineligible Improvements Any work that cannot be completed within 120 days of note date. Major structural repairs, rehab or improvements such as load bearing walls, foundation repair or support joists. Improvements or changes that were not approved prior to the start of work. Materials or work performed prior to the first draw disbursement. Any improvement that does not become a permanent part of the subject property. 25

26 Borrower Provided Materials Materials provided by the borrower may be allowed but cannot be financed in the loan amount. All materials provided by the borrower must be new from the manufacturer and be documented with paid invoices, and Source of funds to acquire the materials must be documented Borrower provided materials must be documented on the contractor s bid as borrower provided materials (zero cost) labor must be provided by the contractor. 26

27 Click here to add a longer headline about the slide Underwriting

28 Underwriting Loans must be submitted to DU or LPA. Loans not receiving a DU or LPA approval may be manually underwritten if: Loan meets all published loan program guidelines AND Underwriter s evaluation has determined loan is an investment quality mortgage AND Loan file contains documentation to support underwriting decision. 28

29 Income and Employment All VA loans must be fully documented. Refer to the VA Lenders Handbook for more details. A verbal VOE is required for all borrowers. All transactions require a signed and dated IRS Form 4506-T for all borrowers completed prior to closing. Refer to Plaza s Tax Transcript Guidelines to determine if transcripts are required. 29

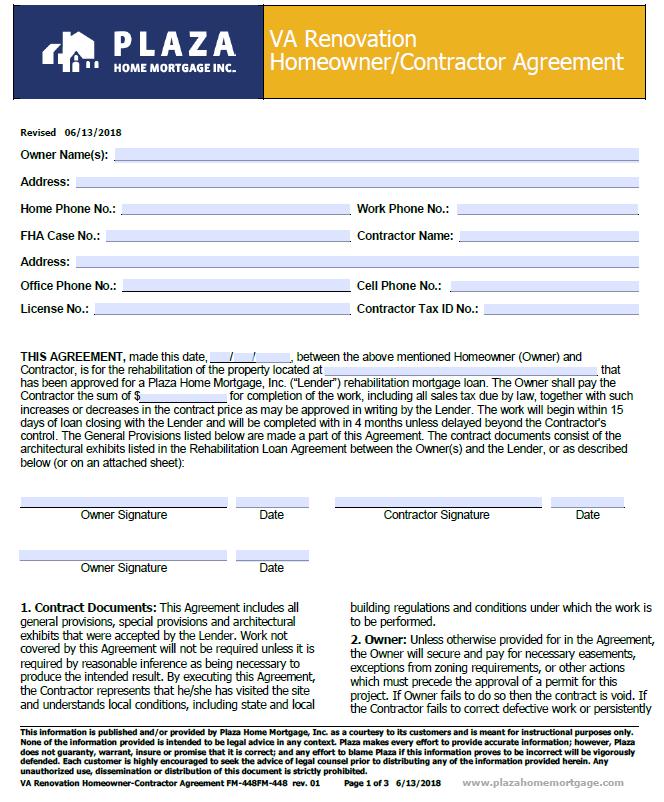

30 TRID Fees 1 x $200 30

31 VA Appraisal Fee Schedules and Timeliness Requirements Click the VA Regional Loan Center link On the US map, click a state to obtain the supporting Regional Loan Center for that state, where you can obtain maximum allowable fees for the appraisal type and number of days allowed for completion. If you hover your mouse over a state without clicking, you will see all of the states supported by that particular Regional Loan Center. VA will set the fees for the appraisal and final inspection 1004D cost. 31

32 VA Renovation: 1, 2, 3 Forms Contractor Approval Bid Approval 32

33 Forms Click here to add a longer headline about the slide

34 VA Renovation Forms Contractor s Fully Executed Bid(s) (see Bid Template) Homeowner/Contractor Agreement Maximum Mortgage Worksheet Borrower s Acknowledgment Per contractor W-9, License, Bond, History Letter, and Insurance Contractor Profile Report Loan Submission Checklist 34

35 Closing and Servicing Forms SERVICING: Lender s Notice of Work Completion Change Order Request Lien Waiver and Release Loan Draw Request CLOSING DOC SET: Rehabilitation Loan Agreement Rehabilitation Loan Rider 35

36 Maximum Mortgage Worksheet 36

37 Contractor s Specifications of Repairs/Bid 37

38 Homeowner/Contractor Agreement Note: Confirm contractor sum matches finalized bid. Must be an actual completion date, not a timeframe 38

39 Lien Waiver and Release 39

40 Rehab Loan Agreement 40

41 Rehab Loan Rider 41

42 Lender s Notice of Work Completion 42

43 Borrower s Acknowledgement 43

44 Loan Submission One-Pack 44

45 Click here to add a longer headline about the slide Contractor Requirements and Bids

46 Contractor Requirements Contractor to provide: License Bond W-9 (must be current year) $1 million in liability insurance Contractor Profile Report VA ID Number 46

47 Licensing Requirements Lead Based Paint and Mold Abatement All repairs of this type require specialty license/certification. List the name of the company to be used for the repairs on the bid. Provide a copy of the verified license or certification. If a General Contractor is not licensed in these specific fields and is using a subcontractor for electrical or plumbing repairs, the subcontractor is required to provide a valid license for their profession. 47

48 Contractor ID Number Contractors need to obtain a VA Builder ID number at /appraiser_cv_builder_info.asp The VA Builder ID Number is not the only step to contractor approval. Up to 3 licensed contractors are allowed per file. Builders are not approved by the VA. They only need to register with VA to obtain a VA Builder ID number. Thus, there is no lengthy processing time and in most cases, an ID number can be issued within a day or two. 48

49 Builder ID Number To obtain a builder ID number, three items need to be submitted to the Construction and Valuation unit of the local VA Regional Loan Center having jurisdiction over the area in which the builder will construct property. These items are: Builder information and certification required form VA Form Equal Employment Opportunity Certification VA Form 8791 VA Affirmative Marketing Certification 49

50 Sample of Incomplete Bid No address for contractor No borrowers name or address/ job location Need explanation of reframe i.e. is it structural? Not signed by all parties ABC Company, Inc. Need breakdown of labor costs and material costs for each item Need specific location each item is taking place Need License # Only licensed plumber can perform plumbing work 50

51 Sample Complete Bid 51

52")

52 Sample Complete Bid (cont d) 52

53")

53 Sample Complete Bid (cont d) 53

54")

54 Sample Complete Bid (cont d) 54

55 Self Help 55

56 Click here to add a longer headline about the slide After Closing

57 Loan Servicing A Welcome Call is placed to the homeowner(s) by a Construction Service Specialist that will be handling their renovation project. The Construction Service Specialist: Inquires if borrowers would like their Welcome Package ed or sent regular mail, confirm the address where they want their checks sent. Explains how the renovation process works, answer any questions and advise that the Welcome Package includes a toll free number and an address for them to use if they have any questions. 57

58 Renovation Customer Service Hours of Operation: 8 am 5 pm Pacific Time Toll Free: , Option 2 Fax: RenoServicing@PlazaHomeMortgage.com Please note: Loan Servicing Information can only be provided to the borrowers directly. 58

59 Click here to add a longer headline about the slide Process Flow

60 Process Steps Step 1: Borrower Finds a Property Step 2: Review the Purchase Contract Step 3: Find Contractor must have VA license. Step 4: Obtain Contractor Bid, Plans and Specs Step 5: Finalize Forms and Contractor Approval Items Step 6: Disclosing Fees Correctly TRID Step 7: Order Appraisal Step 8: Underwriting Step 9: Closing Step 10: Renovation Begins Step 11: Final Inspection Completion 60

61 Click here to add a longer headline about the slide Resources

62 Renovation Specialist Team Donna Chetner-Blackwell, Mountain and Pacific Jim Pontious, Central Jeri Murdock, Eastern 62

63 New Income Streams Think Outside the Box Providing the opportunity to stand out as a Specialty Originator! Home Remodeler EDUCATION! Create your own presentation for a real estate office Become certified to teach a free CE class hour** Set up displays in a home remodeling or an outdoor living/pool store* Roofer Get a bid, create a color board & develop a one-sheet with monthly payments Become a deal saver business partner. Search for those dirty dog listings * HomeStyle/VA only ** Check with your local issuing authority 63

64 Marketing Materials Log into Click on the Marketing Materials link on the right navigation 64

65 Customizable Materials: Originator to Consumer Quick, easy and customizable Originator to Consumer Marketing Resources. Simply download the materials from and add your contact information using Adobe Reader or Acrobat. You can even add your logo using a photo editing software. Customizable PDF Flyers & HTML s. Variety of photography options available for each product flyer. 65

66 Resources 66

67 Q & A Click here to add a longer headline about the slide

FHA 203(K) PROGRAM. General Description. Overlays. Available Options

PROGRAM. General Description. Overlays. Available Options") General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home. The new first mortgage includes the purchase price or

General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home. The new first mortgage includes the purchase price or

FHA 203(k) () streamline mortgage Program

() streamline mortgage Program") FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Presented by: Mountain West Financial Why FHA 203(k) Through the Federal

FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Presented by: Mountain West Financial Why FHA 203(k) Through the Federal

Low down payment option; qualify with as little as 3.5% down

Not every home is move-in ready. The FHA 203(k) Renovation Loan allows you to broaden your home shopping horizons and create the home you want from the start. The FHA 203(k) Renovation Loan combines the

Not every home is move-in ready. The FHA 203(k) Renovation Loan allows you to broaden your home shopping horizons and create the home you want from the start. The FHA 203(k) Renovation Loan combines the

203(k) Program Full and Streamline

Program Full and Streamline") General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home The new first mortgage includes the purchase price or

General Description Renovation Lending is simply adding the cost of repairs and improvements into the mortgage used to purchase or refinance a home The new first mortgage includes the purchase price or

FHA 203(k) () streamline mortgage Program. make improvements all with a single loan

() streamline mortgage Program. make improvements all with a single loan") FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Why FHA 203(k) Through the Federal Housing Administration (FHA) 203(k)

FHA 203(k) () streamline mortgage Program Help qualified borrowers purchase or refinance and make improvements all with a single loan Why FHA 203(k) Through the Federal Housing Administration (FHA) 203(k)

Products. Loan Amount

Freedom Mortgage FHA 203(k) FRM & ARM Product Guide Loan Program Overview This document is not all encompassing. It is a summary reference tool to be utilized in conjunction with Agency guidelines and

Freedom Mortgage FHA 203(k) FRM & ARM Product Guide Loan Program Overview This document is not all encompassing. It is a summary reference tool to be utilized in conjunction with Agency guidelines and

Benefits to Borrower - Why Renovation?

Whether your borrower is looking to purchase a home that needs renovations or repairs or are refinancing an existing mortgage and looking to make home improvements, the Fannie Mae Homestyle Renovation

Whether your borrower is looking to purchase a home that needs renovations or repairs or are refinancing an existing mortgage and looking to make home improvements, the Fannie Mae Homestyle Renovation

HomeStyle Renovation Product Offering 8/29/14

HomeStyle Renovation Product Offering 8/29/14 Overview of HomeStyle Offering Define the HomeStyle product and features Discuss benefits of the HomeStyle renovation loan Learn how to determine eligibility

HomeStyle Renovation Product Offering 8/29/14 Overview of HomeStyle Offering Define the HomeStyle product and features Discuss benefits of the HomeStyle renovation loan Learn how to determine eligibility

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage General Eligibility Requirements Loans must fully comply with all requirements of this Product Guide, Desktop Underwriter

Fannie Mae HomeStyle Conforming and High Balance Fixed Rate and Adjustable Rate Mortgage General Eligibility Requirements Loans must fully comply with all requirements of this Product Guide, Desktop Underwriter

Revised 04/30/18. FHA Standard 203K

Revised 04/30/18 FHA Standard 203K FHA Standard 203K Disclaimer While every effort has been made to ensure the reliability of the webinar content, PRMG s product profiles and their updates, are the official

Revised 04/30/18 FHA Standard 203K FHA Standard 203K Disclaimer While every effort has been made to ensure the reliability of the webinar content, PRMG s product profiles and their updates, are the official

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

RESIDENTIAL CONSTRUCTION LENDING POLICY

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

Renovation Lending Suite

Renovation Lending Suite M A R C H, 2 0 1 9 4/10/2019 1 Agenda Renovation Loans FHA 203(k): Limited & Standard FNMA HomeStyle Renovation Need to Knows Processing Renovation Loans Reference Materials Why

Renovation Lending Suite M A R C H, 2 0 1 9 4/10/2019 1 Agenda Renovation Loans FHA 203(k): Limited & Standard FNMA HomeStyle Renovation Need to Knows Processing Renovation Loans Reference Materials Why

Revised 4/6/18. FHA 203K Renovation

Revised 4/6/18 FHA 203K Renovation Important Notice While every effort has been made to ensure the reliability of the training content, PRMG s product profiles and their updates, are the official statements

Revised 4/6/18 FHA 203K Renovation Important Notice While every effort has been made to ensure the reliability of the training content, PRMG s product profiles and their updates, are the official statements

FNMA Homestyle Steps to Success

FNMA Homestyle Steps to Success Disclosing the Loan estimate for a FNMA Homestyle Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit

FNMA Homestyle Steps to Success Disclosing the Loan estimate for a FNMA Homestyle Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit

Properties listed with the following two logos are eligible: and

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate FNMA only Eligible properties must be owned by Fannie Mae (as a result of foreclosure or other similar action such as deed-in-lieu of foreclosure), sold by

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate FNMA only Eligible properties must be owned by Fannie Mae (as a result of foreclosure or other similar action such as deed-in-lieu of foreclosure), sold by

FHA 203 (h) Program Guidelines

Program Guidelines") FHA 203 (h) Program Guidelines Revised 3/27/2018 Rev. 04 (Click the link to go straight to the section) 1 Program Summary 13 Income and Employment 25 ARM Adjustments 2 Product Codes 14 Qualifying Ratios

FHA 203 (h) Program Guidelines Revised 3/27/2018 Rev. 04 (Click the link to go straight to the section) 1 Program Summary 13 Income and Employment 25 ARM Adjustments 2 Product Codes 14 Qualifying Ratios

Lenders must be approved by PennyMac prior to delivering HomeStyle loans.

PennyMac Correspondent Group Fannie Mae HomeStyle Product Profile 03.19.18 Overlays to Fannie Mae are underlined Lenders must be approved by PennyMac prior to delivering HomeStyle loans. Agency Finance

PennyMac Correspondent Group Fannie Mae HomeStyle Product Profile 03.19.18 Overlays to Fannie Mae are underlined Lenders must be approved by PennyMac prior to delivering HomeStyle loans. Agency Finance

FHA 203(k) Standard Product Guide

Standard Product Guide") FHA 203(k) Standard Product Guide Section 203(k) Financing enables homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single

FHA 203(k) Standard Product Guide Section 203(k) Financing enables homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single

WCDA LOAN PRODUCT MATRIX

The matrix below compares the components of the various first mortgage loan and down payment assistance loan products offered by WCDA. This matrix is designed to provide guidance for these products and

The matrix below compares the components of the various first mortgage loan and down payment assistance loan products offered by WCDA. This matrix is designed to provide guidance for these products and

Limited FHA 203K. Village Mortgage NMLS Intended for Mortgage Professionals Only 1

Limited FHA 203K Before After Village Mortgage NMLS 6331 Intended for Mortgage Professionals Only 1 Program Highlights Up to $35,000 in repairs with no minimum No consultant required Up to 3 Contractors

Limited FHA 203K Before After Village Mortgage NMLS 6331 Intended for Mortgage Professionals Only 1 Program Highlights Up to $35,000 in repairs with no minimum No consultant required Up to 3 Contractors

10, 15, 20, 25 & 30 YR Fixed Rates

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

VA Fixed Rate Program Matrix Purchase Doc Type Occupancy Units FICO LTV/CLTV Full Primary Residence /100

VA Fixed Rate and ARM Program Summary VA Fixed Rate Program Matrix Purchase Doc Type Occupancy Units FICO LTV/CLTV Full Primary Residence 1-4 620 100/100 INTEREST RATE REDUCTION REFINANCE LOAN/IRRRL Streamline

VA Fixed Rate and ARM Program Summary VA Fixed Rate Program Matrix Purchase Doc Type Occupancy Units FICO LTV/CLTV Full Primary Residence 1-4 620 100/100 INTEREST RATE REDUCTION REFINANCE LOAN/IRRRL Streamline

FHA Renovation Loan Program, or 203K

FHA Renovation Loan Program, or 203K The Federal Housing Administration (FHA), which is part of the Department of Housing and Urban Development (HUD), administers various single family mortgage insurance

FHA Renovation Loan Program, or 203K The Federal Housing Administration (FHA), which is part of the Department of Housing and Urban Development (HUD), administers various single family mortgage insurance

Lock dates on or after March1, 2018: WSHFC Home Advantage Government Loan Programs

Lock dates on or after March1, 2018: WSHFC Home Advantage Government Loan Programs Red indicates changes from previous matrix Overlays to Investor guidelines are underlined and in italics Owner Occupied

Lock dates on or after March1, 2018: WSHFC Home Advantage Government Loan Programs Red indicates changes from previous matrix Overlays to Investor guidelines are underlined and in italics Owner Occupied

Renovate your Real Estate Business

Renovate your Real Estate Business Shawn Barsness NMLS ID #67292 Renovation Lending This class is to help real estate agents better serve their clients by understanding how renovation loans work to solve

Renovate your Real Estate Business Shawn Barsness NMLS ID #67292 Renovation Lending This class is to help real estate agents better serve their clients by understanding how renovation loans work to solve

FHA 203(k) Product Offering 8/12/14

Product Offering 8/12/14") FHA 203(k) Product Offering 8/12/14 Overview of 203(k) Offering Define the 203(k) product and features Discuss benefits of the 203(k) products Learn how to determine eligibility Review guideline specifics

FHA 203(k) Product Offering 8/12/14 Overview of 203(k) Offering Define the 203(k) product and features Discuss benefits of the 203(k) products Learn how to determine eligibility Review guideline specifics

One-Close Construction

RESTRICTED USE PROGRAM All loan originators must complete Flagstar s Construction Loan training course prior to originating any loans under this program. Originators will not be able to register construction

RESTRICTED USE PROGRAM All loan originators must complete Flagstar s Construction Loan training course prior to originating any loans under this program. Originators will not be able to register construction

PURCHASE. Max LTV w/o Sec. Fin. Max LTV w/ Sec. Fin. Max TLTV w/ Sec. Fin.

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

chfa firststep program loan operations training

chfa firststep program loan operations training Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training events. The training content provided is intended to help

chfa firststep program loan operations training Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training events. The training content provided is intended to help

Plaza Home Mortgage Inc. Reverse Mortgage Presentation Basics. May 2018

Plaza Home Mortgage Inc. Reverse Mortgage Presentation Basics May 2018 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial in from your

Plaza Home Mortgage Inc. Reverse Mortgage Presentation Basics May 2018 Your GoToWebinar Toolbar Use speakers or a telephone to listen to the audio. Use the information in your toolbar to dial in from your

USDA REPAIR ESCROW COPYRIGHT 2017 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

12/5/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

12/5/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

program compliance loan operations training chfa conventional loan programs for processors and underwriters

program compliance loan operations training chfa conventional loan programs for processors and underwriters Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training

program compliance loan operations training chfa conventional loan programs for processors and underwriters Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training

ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Agency ELIGIBILITY MATRIX & SUMMARY GUIDELINES 10, 15, 20, 25 & 30 YR s 10, 15, 20, 25 & 30 YR s 10, 15, 20, 25 & 30 YR s Products 5/1, 7/1 & 10/1 s 5/1, 7/1 & 10/1 s 5/1, 7/1 & 10/1 s DU Approve/Eligible

Agency ELIGIBILITY MATRIX & SUMMARY GUIDELINES 10, 15, 20, 25 & 30 YR s 10, 15, 20, 25 & 30 YR s 10, 15, 20, 25 & 30 YR s Products 5/1, 7/1 & 10/1 s 5/1, 7/1 & 10/1 s 5/1, 7/1 & 10/1 s DU Approve/Eligible

2 TERMS AND CONDITIONS

2 TERMS AND CONDITIONS All House Key loans must be delivered to Lakeview Loan Servicing, LLC Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate

2 TERMS AND CONDITIONS All House Key loans must be delivered to Lakeview Loan Servicing, LLC Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate

Correspondent Lending FHA Fixed Rate & ARM Product Profile

Government Occupancy Correspondent Lending ELIGIBILITY MATRIX & SUMMARY GUIDELINES 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM High Balance 15 & 30 YR Fixed Rates Primary Residence Purchase Property

Government Occupancy Correspondent Lending ELIGIBILITY MATRIX & SUMMARY GUIDELINES 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM High Balance 15 & 30 YR Fixed Rates Primary Residence Purchase Property

Buy a home, plus make improvements, with just one loan

Homebuyer guide to a mortgage with built-in renovation financing Buy a home, plus make improvements, with just one loan Learn how Are you thinking of buying a home that needs work? Well Fargo is here to

Homebuyer guide to a mortgage with built-in renovation financing Buy a home, plus make improvements, with just one loan Learn how Are you thinking of buying a home that needs work? Well Fargo is here to

***UPDATED 9/5/18*** TPO Fannie Mae HomeStyle Renovation Product

***UPDATED 9/5/18*** Updated items have been highlighted in yellow. TPO Fannie Mae HomeStyle Renovation Product Overview HomeStyle is Fannie Mae s renovation loan program. This loan will be locked in,

***UPDATED 9/5/18*** Updated items have been highlighted in yellow. TPO Fannie Mae HomeStyle Renovation Product Overview HomeStyle is Fannie Mae s renovation loan program. This loan will be locked in,

VA IRRRL PROGRAM MATRIX

MAXIMUM LTV **Mortgage Only Report IRRRL PROGRAM 1-4 Unit Properties, Condos, and PUD s (Primary Residence) NO FICO PROGRAM MINIMUM FICO MAX LTV 580 100% 620 125% **No FICO 660 UNLIMITED High Balance 100%

MAXIMUM LTV **Mortgage Only Report IRRRL PROGRAM 1-4 Unit Properties, Condos, and PUD s (Primary Residence) NO FICO PROGRAM MINIMUM FICO MAX LTV 580 100% 620 125% **No FICO 660 UNLIMITED High Balance 100%

Under Construction. Construction and Rehab Loan Programs

Under Construction Construction and Rehab Loan Programs Sources: FNMA FHA Portfolio Lenders Home equity lines of credit for homes already owned FNMA Homestyle Renovation Loan Loan Purpose Purchase Terms

Under Construction Construction and Rehab Loan Programs Sources: FNMA FHA Portfolio Lenders Home equity lines of credit for homes already owned FNMA Homestyle Renovation Loan Loan Purpose Purchase Terms

FHA 203K MATRIX. Second Appraisal Requirements

FHA 203K MATRIX Self Help Allowed NO NO ELIGIBLE PROPERTIES 1-4 Family including HUD REOs 1-4 FAMILY INCLUDING HUD REOs ALLOWS RELATIVES/EMPLOYERS TO COMPLETE WORK NO NO MIXED USE ACCEPTABLE ONLY UNDER

FHA 203K MATRIX Self Help Allowed NO NO ELIGIBLE PROPERTIES 1-4 Family including HUD REOs 1-4 FAMILY INCLUDING HUD REOs ALLOWS RELATIVES/EMPLOYERS TO COMPLETE WORK NO NO MIXED USE ACCEPTABLE ONLY UNDER

2 TERMS AND CONDITIONS

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

203K Steps to Success

203K Steps to Success Disclosing the Loan estimate for a 203K Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit Report (if locked

203K Steps to Success Disclosing the Loan estimate for a 203K Loan Broker to provide the following: 1003 Signed by LO dated within 24 hours Completed Norcom LE Worksheet Copy of Credit Report (if locked

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

HomeStyle Renovation Submission Checklist

HomeStyle Renovation Submission Checklist Borrower Name: Loan #: Homestyle Calculation Worksheet (LoanBuilder) * HomeStyle Renovation Consumer Tips (Form 1204) signed by borrower Appraisal with all improvements

HomeStyle Renovation Submission Checklist Borrower Name: Loan #: Homestyle Calculation Worksheet (LoanBuilder) * HomeStyle Renovation Consumer Tips (Form 1204) signed by borrower Appraisal with all improvements

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile

Agency Finance Type Occupancy Term PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile 05.10.18 Freddie Mac - LPA Accept Purchase and Rate/Term Refinances Owner Occupied

Agency Finance Type Occupancy Term PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile 05.10.18 Freddie Mac - LPA Accept Purchase and Rate/Term Refinances Owner Occupied

Renovating and Rebuilding America - One Home at a Time. FHA 203(K) Renovation Lending Product Information

Renovation Lending Product Information") FHA 203(K) Product Information 1 Program Summary The FHA 203(k) The FHA 203(k) loan allows a borrower to purchase or refinance and repair or renovate a property all in one loan. The borrower closes with

FHA 203(K) Product Information 1 Program Summary The FHA 203(k) The FHA 203(k) loan allows a borrower to purchase or refinance and repair or renovate a property all in one loan. The borrower closes with

Delaware State Housing Authority. Homeownership Loan Programs Lender Training

Delaware State Housing Authority Homeownership Loan Programs Lender Training DSHA is committed to follow all aspects of the Fair Housing Act in our efforts to promote responsible homeownership and obtaining

Delaware State Housing Authority Homeownership Loan Programs Lender Training DSHA is committed to follow all aspects of the Fair Housing Act in our efforts to promote responsible homeownership and obtaining

HomeStyle Renovation & Energy Mortgages. Finance renovation or energy efficient costs into a single-close home purchase or refinance loan

HomeStyle Renovation & Energy Mortgages Finance renovation or energy efficient costs into a single-close home purchase or refinance loan 1 An important note about the seminar content While every effort

HomeStyle Renovation & Energy Mortgages Finance renovation or energy efficient costs into a single-close home purchase or refinance loan 1 An important note about the seminar content While every effort

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Conventional and Government Program Overlays

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

Rehab Financing The FHA Streamline 203(k) Program

Program") The FHA Streamline 203(k) Program A Guide to Financing Your Home Improvement Project The Program: This is a new 1 st mortgage program sponsored by the FHA and designed to provide homeowners with low-cost

The FHA Streamline 203(k) Program A Guide to Financing Your Home Improvement Project The Program: This is a new 1 st mortgage program sponsored by the FHA and designed to provide homeowners with low-cost

ONE TIME CLOSE RENOVATION TO PERM OPTION III

ONE TIME CLOSE RENOVATION TO PERM OPTION III REVISION DATE: 5/4/2018 PRODUCT CODES: RP 1x 15 YR Renovation, RP 1x 30 YR Renovation, RP 1x 5/1 LIBOR ARM 275 2/2/5, RP 1x 5/1 TBill ARM 275 2/2/5, RP 1x 7/1

ONE TIME CLOSE RENOVATION TO PERM OPTION III REVISION DATE: 5/4/2018 PRODUCT CODES: RP 1x 15 YR Renovation, RP 1x 30 YR Renovation, RP 1x 5/1 LIBOR ARM 275 2/2/5, RP 1x 5/1 TBill ARM 275 2/2/5, RP 1x 7/1

Fannie & High BalanceGuidelines

Fannie & High BalanceGuidelines Agency Finance Type Occupancy Term High balance and transactions with non-occupant coborrowers are limited to 95% LTV/CLTV. High Balance Cash Out Transactions are limited

Fannie & High BalanceGuidelines Agency Finance Type Occupancy Term High balance and transactions with non-occupant coborrowers are limited to 95% LTV/CLTV. High Balance Cash Out Transactions are limited

USDA Guidelines GUSDA30

USDA Guidelines GUSDA30 BSM Direct guidelines have been created to provide guidance and consistency in determining credit decisions. The guides are not all inclusive of different situations that may arise

USDA Guidelines GUSDA30 BSM Direct guidelines have been created to provide guidance and consistency in determining credit decisions. The guides are not all inclusive of different situations that may arise

One loan to renovate. Your homebuyer guide to renovation

One loan to renovate Your homebuyer guide to renovation Maybe you ve found the perfect location, but the house needs improving. Maybe staying in your current (but outdated) home is what s important. Either

One loan to renovate Your homebuyer guide to renovation Maybe you ve found the perfect location, but the house needs improving. Maybe staying in your current (but outdated) home is what s important. Either

Reasonable closing costs may be included in the Loan amount, but any cash back to the Borrower makes the transaction a Texas Equity Loan.

Texas Equity Loans The information below is specific to refinance transactions for properties located in the State of Texas. Refer to the Fixed Jumbo program guidelines in addition to these guidelines.

Texas Equity Loans The information below is specific to refinance transactions for properties located in the State of Texas. Refer to the Fixed Jumbo program guidelines in addition to these guidelines.

Conventional and Government Program Overlays

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

VA CONFORMING & HIGH BALANCE MATRIX

CONFORMING LIMITS PURCHASE 1 RATE/TERM REFINANCE 2 CASH-OUT REFINANCE Max LTV/CLTV MIN FICO Max LTV/CLTV MIN FICO Max LTV/CLTV MIN FICO 1 unit 100% 580 / NO FICO 2 100%/Unlimited 580 95/95% 640 2-4 units

CONFORMING LIMITS PURCHASE 1 RATE/TERM REFINANCE 2 CASH-OUT REFINANCE Max LTV/CLTV MIN FICO Max LTV/CLTV MIN FICO Max LTV/CLTV MIN FICO 1 unit 100% 580 / NO FICO 2 100%/Unlimited 580 95/95% 640 2-4 units

MAGNOLIA BANK CORRESPONDENT FUNDING RURAL DEVELOPMENT PRODUCT SUMMARY

RURAL DEVELOPMENT FIXED RATE (DELEGATED CLIENTS ONLY) 1. PRODUCT DESCRIPTION USDA Fixed Rate Mortgage 30 year term Fully amortizing 2. PRODUCT CODE 3. INDEX 4. MARGIN 5. ANNUAL/ADJUSTMEN T CAP 6. LIFE

RURAL DEVELOPMENT FIXED RATE (DELEGATED CLIENTS ONLY) 1. PRODUCT DESCRIPTION USDA Fixed Rate Mortgage 30 year term Fully amortizing 2. PRODUCT CODE 3. INDEX 4. MARGIN 5. ANNUAL/ADJUSTMEN T CAP 6. LIFE

YORK HOMEBUYER ASSISTANCE PROGRAM GUIDELINES AND RULES. Funding Source. Program Code. Eligible States Minimum Loan Amount.

Revised 6/8/2015 YORK HOMEBUYER ASSISTANCE PROGRAM GUIDELINES AND RULES Funding Source Program Description - This program is designed to provide down payment & closing cost assistance to low/moderate income

Revised 6/8/2015 YORK HOMEBUYER ASSISTANCE PROGRAM GUIDELINES AND RULES Funding Source Program Description - This program is designed to provide down payment & closing cost assistance to low/moderate income

APMC FHA PROGRAM GUIDE

FHA LTV Matrix Conforming FHA Fixed Purchase Full Primary Residence 1-4 600 96.5/105 Rate & Term Refinance Full/Simple Primary Residence 1-4 620 97.75/97.75 Streamline Primary Residence 1-4 620 97.75/125

FHA LTV Matrix Conforming FHA Fixed Purchase Full Primary Residence 1-4 600 96.5/105 Rate & Term Refinance Full/Simple Primary Residence 1-4 620 97.75/97.75 Streamline Primary Residence 1-4 620 97.75/125

Brown - HECM / Reverse Product Guidelines. Loan Parameter HECM Fixed Variable Rate HECM

Brown - HECM / Reverse Product PRODUCTS & UNDERWRITING GUIDELINES Youngest Borrower Age Eligibility Occupancy Allowed States Allowed 62 years and above Owner Occupied Primary Residence Loans are accepted

Brown - HECM / Reverse Product PRODUCTS & UNDERWRITING GUIDELINES Youngest Borrower Age Eligibility Occupancy Allowed States Allowed 62 years and above Owner Occupied Primary Residence Loans are accepted

Jumbo Non-Conforming Products (Series-49)

") Jumbo Non-Conforming Products (Series-49) This guide provides parameters for standard fixed rate and 5/1, 7/1, and 10/1 adjustable rate, fully amortizing, nonconforming products for primary residence up

Jumbo Non-Conforming Products (Series-49) This guide provides parameters for standard fixed rate and 5/1, 7/1, and 10/1 adjustable rate, fully amortizing, nonconforming products for primary residence up

Du Refi Plus Guidelines

Du Refi Plus Guidelines Units Contiguous States, DC Alaska, Hawaii Max Loan Amount Conforming 1 Unit 2 Unit 3 Unit 4 Unit $417,000 $533,850 $645,300 $801,950 $625,500 $800,775 $967,950 $1,202,925 Units

Du Refi Plus Guidelines Units Contiguous States, DC Alaska, Hawaii Max Loan Amount Conforming 1 Unit 2 Unit 3 Unit 4 Unit $417,000 $533,850 $645,300 $801,950 $625,500 $800,775 $967,950 $1,202,925 Units

Correspondent Lending FHA Fixed Rate

Agency Correspondent Lending FHA Fixed Rate Correspondent Lending FHA Fixed Rate Maximum Loan Amount County Minimum Loan Amount $50,000 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM DU Approve, LP Accept

Agency Correspondent Lending FHA Fixed Rate Correspondent Lending FHA Fixed Rate Maximum Loan Amount County Minimum Loan Amount $50,000 10, 15, 20, 25 & 30 YR Fixed Rates & 5/1 CMT ARM DU Approve, LP Accept

DETROIT HOME MORTGAGE RENOVATION EDUCATION

DETROIT HOME MORTGAGE RENOVATION EDUCATION COURSE OUTLINE Ways to Renovate Using Detroit Home Mortgage Things to Consider Before You Begin Renovating Roles and Responsibilities Renovation-Related Documents

DETROIT HOME MORTGAGE RENOVATION EDUCATION COURSE OUTLINE Ways to Renovate Using Detroit Home Mortgage Things to Consider Before You Begin Renovating Roles and Responsibilities Renovation-Related Documents

All-in-One Custom Construction

Wholesale Lending All-in-One Custom Construction This is a true one-time-close loan program designed to finance the construction or major remodel of a primary residence or second home. This loan includes

Wholesale Lending All-in-One Custom Construction This is a true one-time-close loan program designed to finance the construction or major remodel of a primary residence or second home. This loan includes

FHLMC Relief Refinance Open Access

The Federal Housing Finance Agency (FHFA) Home Affordable Refinance Program ( HARP ) is designed to assist borrowers who have demonstrated an acceptable payment history on their existing Freddie Mac mortgage

The Federal Housing Finance Agency (FHFA) Home Affordable Refinance Program ( HARP ) is designed to assist borrowers who have demonstrated an acceptable payment history on their existing Freddie Mac mortgage

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

203k Quick Reference Guide

Table of Contents 203(K) Quick Reference Consumer Renovation Information 203(K) Borrower s Acknowledgement Rehabilitation Loan Agreement Consultant s Identity of Interest Certification Borrower s Identify

Table of Contents 203(K) Quick Reference Consumer Renovation Information 203(K) Borrower s Acknowledgement Rehabilitation Loan Agreement Consultant s Identity of Interest Certification Borrower s Identify

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE CASH-OUT REFINANCE SECOND HOME PURCHASE AND RATE/TERM REFINANCE

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE Property Type Max. Loan mount Max. LTV Max. CLTV/HCLTV Min. FICO 1-Unit, PUD $679,650 85% N/A 760 Warrantable Condo $679,650 80% 90% 680 PRIMARY RESIDENCE

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE Property Type Max. Loan mount Max. LTV Max. CLTV/HCLTV Min. FICO 1-Unit, PUD $679,650 85% N/A 760 Warrantable Condo $679,650 80% 90% 680 PRIMARY RESIDENCE

Fannie Mae Conforming and High Balance

Primary Loan Purpose Minimum FICO Units Max LTV/CLTV/HCLTV Purchase or Rate/Term Cash-Out 2 3-4 2-4 Fixed 97%,2 / ARM 95% Fixed/ARM 85% Fixed/ARM 75% Fixed/ARM 80% Fixed/ARM 75% Second Home Loan Purpose

Primary Loan Purpose Minimum FICO Units Max LTV/CLTV/HCLTV Purchase or Rate/Term Cash-Out 2 3-4 2-4 Fixed 97%,2 / ARM 95% Fixed/ARM 85% Fixed/ARM 75% Fixed/ARM 80% Fixed/ARM 75% Second Home Loan Purpose

Section 2.23 Veterans Administration (VA) Loan Program

Loan Program") Section 2.23 Veterans Administration (VA) Loan Program In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Correspondent Lenders with

Section 2.23 Veterans Administration (VA) Loan Program In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Correspondent Lenders with

Conventional Loan Program - Quick Reference Guide

Loan Program - Quick Reference Guide Eligible Products LTV/(H)CLTV Matrices and Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Fannie Only Products 5/1 and 7/1 ARMS,

Loan Program - Quick Reference Guide Eligible Products LTV/(H)CLTV Matrices and Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Fannie Only Products 5/1 and 7/1 ARMS,

PennyMac Correspondent Group Open Access

PennyMac Correspondent Group Open Access 01.18.18 Overlays to Freddie Mac are underlined The new loan must have an application date on or before December 31, 2018. Mortgage Product Program Eligibility

PennyMac Correspondent Group Open Access 01.18.18 Overlays to Freddie Mac are underlined The new loan must have an application date on or before December 31, 2018. Mortgage Product Program Eligibility

BUILD BUY RENOVATE. Your guide to understanding and financing your new home

BUILD BUY RENOVATE Your guide to understanding and financing your new home TURNERR@FNB-CORP.COM Table of Contents Your Dreams become reality 3 Overview 3 Why Construction / Renovation Permanent 4 Financing

BUILD BUY RENOVATE Your guide to understanding and financing your new home TURNERR@FNB-CORP.COM Table of Contents Your Dreams become reality 3 Overview 3 Why Construction / Renovation Permanent 4 Financing

CONFORMING HB FIXED LENDER PAID MORTGAGE INSURANCE PROGRAM HIGHLIGHTS

Program Summary A Conforming High Balance Conventional loan with increased loan size limits, featuring a 30-year and 15-year fixed interest rate for the term of the loan. Loan Term & Program Category Loan

Program Summary A Conforming High Balance Conventional loan with increased loan size limits, featuring a 30-year and 15-year fixed interest rate for the term of the loan. Loan Term & Program Category Loan

CONFORMING HIGH BALANCE FIXED PROGRAM HIGHLIGHTS

Program Summary A Conforming High Balance Conventional loan with increased loan size limits, featuring a 30-year and 15-year fixed interest rate for the term of the loan. Loan Term & Program Category Loan

Program Summary A Conforming High Balance Conventional loan with increased loan size limits, featuring a 30-year and 15-year fixed interest rate for the term of the loan. Loan Term & Program Category Loan

Conventional and Government Program Overlays. OVERLAYS All Programs

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

CHFA-Approved Lenders Mortgage Program Training. Rev 5/10/18

CHFA-Approved Lenders Mortgage Program Training Rev 5/10/18 Our Mission To alleviate the shortage of housing for low-to-moderate income families and persons in this State and, when appropriate, to promote

CHFA-Approved Lenders Mortgage Program Training Rev 5/10/18 Our Mission To alleviate the shortage of housing for low-to-moderate income families and persons in this State and, when appropriate, to promote

Program Qualifications

This matrix is intended as an aid to assist in determining if a property/loan qualifies for certain USDA offered programs. It is not intended as a replacement for USDA guidelines. Users are expected to

This matrix is intended as an aid to assist in determining if a property/loan qualifies for certain USDA offered programs. It is not intended as a replacement for USDA guidelines. Users are expected to

ONE-TIME CLOSE CONSTRUCTION LOAN INFORMATION PACKET

ONE-TIME CLOSE CONSTRUCTION LOAN INFORMATION PACKET At AmeriFirst we are committed to providing you with all the information you need regarding your construction loan. This guide will walk you through

ONE-TIME CLOSE CONSTRUCTION LOAN INFORMATION PACKET At AmeriFirst we are committed to providing you with all the information you need regarding your construction loan. This guide will walk you through

AMX / Land Home Financial Services Wholesale Lending Division

1 of 10 Fixed Program Codes: CRR 30-006, CRR25-006, CRR20-006, CRR15-006, SCRR30-006, SCRR15-006 Adjustable Program Codes: Not Available Automated Underwriting: LP Accept/Eligible Conforming Loan Continental

1 of 10 Fixed Program Codes: CRR 30-006, CRR25-006, CRR20-006, CRR15-006, SCRR30-006, SCRR15-006 Adjustable Program Codes: Not Available Automated Underwriting: LP Accept/Eligible Conforming Loan Continental

PORTFOLIO ARM CLOSED END 2 ND TD. Table of Contents

Table of Contents 1. Program Codes...2 2. Product Overview...2 3. Product Summary...2 4. Documentation...2 5. Underwriting...2 6. Qualifying Rate...2 7. Borrower Eligibility...2 8. Appraisal...3 9. Appraised

Table of Contents 1. Program Codes...2 2. Product Overview...2 3. Product Summary...2 4. Documentation...2 5. Underwriting...2 6. Qualifying Rate...2 7. Borrower Eligibility...2 8. Appraisal...3 9. Appraised

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile Overlays to Freddie Mac are underlined

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile 01.01.18 Overlays to Freddie Mac are underlined Agency Finance Type Occupancy Term Freddie Mac - LPA Accept Purchase

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile 01.01.18 Overlays to Freddie Mac are underlined Agency Finance Type Occupancy Term Freddie Mac - LPA Accept Purchase

Wholesale Overlay Matrix

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

CONFORMING FIXED LENDER PAID MORTGAGE INSURANCE PROGRAM HIGHLIGHTS

Program Summary Loan Term & Program Category A conforming conventional loan with a fixed interest rate for the term of the loan. Loan Term Program Category 30-year Conf Fixed 30 15-year Conf Fixed 15 Transaction

Program Summary Loan Term & Program Category A conforming conventional loan with a fixed interest rate for the term of the loan. Loan Term Program Category 30-year Conf Fixed 30 15-year Conf Fixed 15 Transaction

Conventional Loan Program-Quick Reference Guide

Loan Program-Quick Reference Guide Eligible Products Fannie & Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Program Features Fully-Amortized Fixed Rate LP Accept or

Loan Program-Quick Reference Guide Eligible Products Fannie & Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Program Features Fully-Amortized Fixed Rate LP Accept or

ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10-30 year term in annual increments Fully amortizing

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10-30 year term in annual increments Fully amortizing

Conforming limits - Purchase - Rate and Term Refinances (Loans must have been purchase money A quality mortgage at origination)

") DREAM MAKER FIXED RATE LOW INCOME / LOW FICO WHOLESALE PRODUCT GUIDELINES PRODUCT CODES: C30XO C20XO C15XO C10XO Several states and local municipalities have enacted legislation which define High Cost

DREAM MAKER FIXED RATE LOW INCOME / LOW FICO WHOLESALE PRODUCT GUIDELINES PRODUCT CODES: C30XO C20XO C15XO C10XO Several states and local municipalities have enacted legislation which define High Cost

FHLMC Only Conforming and Maximum DTI is the more restrictive of Loan Product Advisor or 50%.

AUS (Automated Underwriting System) GENERAL POLICY OVERLAYS FHA, VA, CONVENTIONAL and USDA FHA, VA & Conventional AUS approval recommendation is required for all FHA, VA, (Purchase and Non-Streamline/Non-IRRRL

AUS (Automated Underwriting System) GENERAL POLICY OVERLAYS FHA, VA, CONVENTIONAL and USDA FHA, VA & Conventional AUS approval recommendation is required for all FHA, VA, (Purchase and Non-Streamline/Non-IRRRL

AFR JUMBO OVERVIEW COPYRIGHT 2017 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

12/20/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

12/20/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

CONSTRUCTION-TO-PERMANENT GUIDELINES BROKER LOANS

AKA USALLIANCE FEDERAL CREDIT UNION CONSTRUCTION-TO-PERMANENT GUIDELINES BROKER LOANS Available Conforming and Jumbo FIXED: 10 Year, 15 Year, 20 Year and *30 Year Programs: ARMS: 5/1, 5/5 and 7/1 (*30

AKA USALLIANCE FEDERAL CREDIT UNION CONSTRUCTION-TO-PERMANENT GUIDELINES BROKER LOANS Available Conforming and Jumbo FIXED: 10 Year, 15 Year, 20 Year and *30 Year Programs: ARMS: 5/1, 5/5 and 7/1 (*30

JUMBO PRIME PROGRAM (FIXED & ARM)

") JUMBO PRIME PROGRAM (FIXED & ARM) PRIMARY RESIDENCE Purchase & Rate/Term Refinance (1),(2) Units Min. FICO LTV/CLTV/ HCLTV Max. DTI Max. Loan Amount 700 80% 43% 1 unit 680 80% 35% 680 70% 43% 740 80% 43%

JUMBO PRIME PROGRAM (FIXED & ARM) PRIMARY RESIDENCE Purchase & Rate/Term Refinance (1),(2) Units Min. FICO LTV/CLTV/ HCLTV Max. DTI Max. Loan Amount 700 80% 43% 1 unit 680 80% 35% 680 70% 43% 740 80% 43%

Wholesale Lending DU Refi Plus 12/27/2013

Program Code Loan Description Program Type Loan_Type Program Code DU30-105 DU REFI 30 YR FIXED LTV 0-105 FIXED CONV DU20-105 DU REFI 20 YR FIXED LTV 0-105 FIXED CONV DU15-105 DU REFI 15 YR FIXED LTV 0-105

Program Code Loan Description Program Type Loan_Type Program Code DU30-105 DU REFI 30 YR FIXED LTV 0-105 FIXED CONV DU20-105 DU REFI 20 YR FIXED LTV 0-105 FIXED CONV DU15-105 DU REFI 15 YR FIXED LTV 0-105

VERY IMPORTANT THE LOAN WILL BE RUN THROUGH DU PRIOR TO START OF CONSTRUCTION AND MUST REFLECT APPROVE ELIGIBLE.

REVISION DATE: PRODUCT CODES: One Time CP 15YR, One Time CP 30 YR. PURPOSE: To construct Borrower s primary or second residence with credit approval prior to start of construction. Correspondent will monitor

REVISION DATE: PRODUCT CODES: One Time CP 15YR, One Time CP 30 YR. PURPOSE: To construct Borrower s primary or second residence with credit approval prior to start of construction. Correspondent will monitor

Section Agency Loan Programs

Section 2.01 - Agency Loan Programs In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Related Bulletins... 4 Loan Terms... 5 Minimum

Section 2.01 - Agency Loan Programs In This Product Description This product description contains the following topics. Overview... 3 Product Summary... 3 Related Bulletins... 4 Loan Terms... 5 Minimum

ditech BUSINESS LENDING VA REFINANCE PRODUCTS

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in annual increments Fully amortizing Servicing retained Qualified Mortgage (QM) Safe

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in annual increments Fully amortizing Servicing retained Qualified Mortgage (QM) Safe